Abstract

In late 2016, Umair Mohsin, marketing director at Telenor Pakistan, a major telecommunication company, had to decide on the brand architecture system. Telenor launched as a rural brand in the competitive telecommunication sector in Pakistan and had reached the second-largest market share. It offered brands targeted towards different segments: a voice-based, mass brand called Telenor Talkshawk, an SMS-based youth brand called Djuice and a post-paid brand called Telenor Persona. Telenor Persona was later changed to Telenor post-paid. Although these Telenor brands were differentiated in their target groups, brand personality and tone of voice, the financial concerns of the heads in Oslo, Norway, forced Umair to think and decide about the present nomenclature. Should he continue with both brands? Should he discontinue Talkshawk as the shareholders suggested? Should he only focus on the mother brand, Telenor? To make this decision, he had to keep the recent award of the 4G spectrum in mind. The 4G spectrum ensured the company could improve customer experience, expand services and serve the unserved market. Umair had to decide whether the 4G launch had to be communicated using the Talkshawk brand, which had a less tech-savvy audience, the Djuice brand, which had a tech-savvy audience, or the mother brand, Telenor. He had to decide in a short time frame of two days. He could listen to the shareholders’ concerns regarding cost reduction and accept their proposal or convince them of a better top line by satisfying the existing customer base.

Discussion Questions

What is the current health of Telenor’s brands?

How do you assess the current architecture and brand portfolio strategy?

What should Umair do to improve the company’s financial situation?

Should he continue with the multiple-brand approach? Why or why not?

Should he merge all other brands under the umbrella of Telenor? Why or why not?

What are the pros and cons of each architecture option?

What solution would you recommend to Umair?

On 2 January 2017, Umair Mohsin, marketing director at Telenor Pakistan, sat in a pensive mood at the Telenor head office in Islamabad. Telenor Pakistan was a mobile and digital service provider owned by the Norwegian Telenor Group. The group company’s shareholding was predominantly equity-based. Telenor Pakistan entered a mass market segment with the Telenor Talkshawk brand and the youth segment with the Djuice brand in 2007 and 2006, respectively.

Telenor was awarded the 850 MHz spectrum and planned to launch its 4G services in Pakistan. However, recent financial reports had raised concerns from heads in Oslo regarding continuing Talkshawk as a separate brand. Umair was asked to present the crucial plan for the year before the board of governors in a meeting that was due in two days. He discussed the matter with his team, who all had mixed responses. While some felt that the brand discontinuation would risk losing customers and hurt the top line, others felt that focusing only on Telenor would be more cost-effective. While making this decision, he also had to keep the 4G spectrum launch in mind. Should he launch the 4G spectrum under the umbrella of the mother brand, Telenor, or launch it under one of the two brands—Talkshawk or Djuice? Multiple questions were running through Umair’s mind. Did the multi-brand approach represent an efficient and effective brand portfolio strategy? Would the culling of the brand alienate the existing target audience? What would be the long-term implications of launching the 4G services under the mother brand umbrella versus the individual brand? While he prepared his presentation that decided the fate of Talkshawk, he knew that he could play it safe and address shareholders’ concerns by removing the brand or convincing the heads of a better top line with existing brands that connected deeply with the Pakistani audience.

Background

Pakistan was located in South Asia and was a semi-industrialized economy with a population of 213.5 million. Its neighbouring countries included India, China, Afghanistan and Iran. It had an Arabian Sea coastline in its South. It had around 205 main cities: Karachi, Lahore, Rawalpindi, Faisalabad and Gujranwala. Its capital was Islamabad. Males comprised 51% of the population, while females comprised 49%, and the median age was 22 years. Pakistan’s rural–urban split was approximately 60–40. The rural population was mainly involved in agriculture. Agriculture contributed approximately 18.5% to the economy (Food and Agriculture Organization of the United Nations, n.d.).

Pakistan saw a GDP growth of approximately 5% by the end of 2016 against a target of 5.7% (Shahbaz, 2017). Politically, the country lacked stability. The growth in the industrial sector was lower than the targeted percentage; however, the services and agricultural sectors witnessed growth (Government of Pakistan, 2017). It was an emerging digital society with approximately 90 million unique mobile subscribers. Internet penetration and mobile broadband subscriptions stood at 17.8% and 10%, respectively (GSMA, 2016) . Increasing Pakistan’s internet penetration to 50% was a part of Pakistan’s government’s Vision 2025, an initiative to transition Pakistan towards a digital society (Government of Pakistan, 2014). After 2014, the telecommunication (telco henceforth) industry witnessed shrinking margins due to the launch of over-the-top (OTT) services such as WhatsApp (Baloch, 2017). This led the government to develop policy frameworks ensuring OTT services’ regulation (Business Recorder, 2016). A report by McKinsey and Company expected messaging, fixed voice and mobile voice services from OTT players to reach to 60%, 50% and 25%, respectively, by 2018 (Mohr & Meffert, 2017). The report highlighted that OTT services had started capturing the profit pools of incumbent telecom companies by offering consumers a comprehensive ecosystem. This shift had compelled incumbents to reassess their core competencies and operational efficiencies as OTT services had become a threat for these telcos.

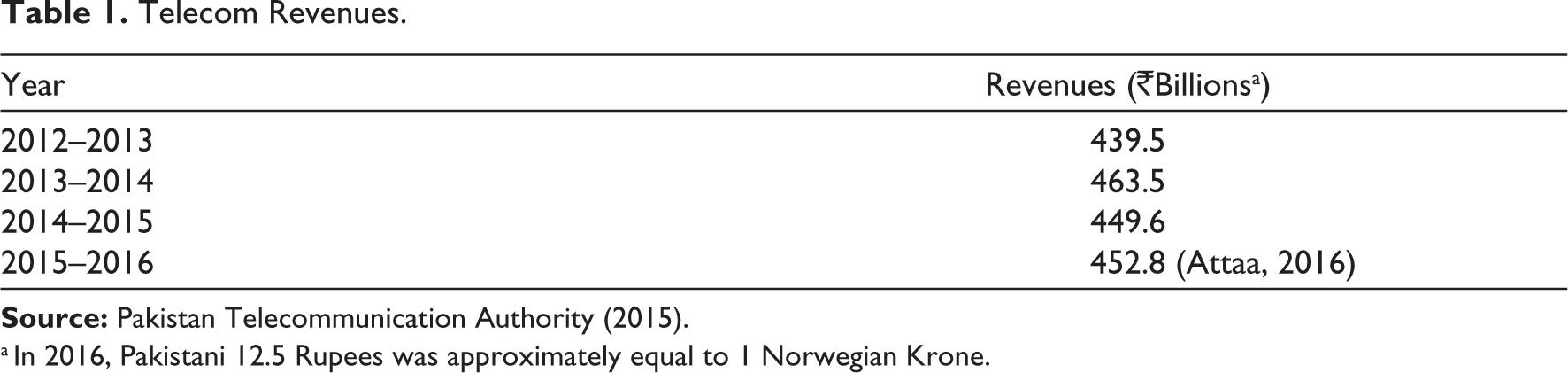

Revenue earned by telcos on the sale of 3G services in 2016 was 98.82 million compared to 77.94 million in 2015 (Siddiqui, 2016). At the beginning of 2015, Pakistan’s telecom operators had to biometrically verify their complete customer base and disconnect all unverified subscriber identity module (SIM) cards. During the verification period, restrictions on new SIM sales through retail channels were enforced. Before the biometric verification, individuals had twenty to thirty SIMs based on different company offers. This verification process resulted in a 5% reduction of the subscription base to 34.6 million at the end of the year (Telenor Group, 2015). The average revenue per user (ARPU) also declined by the end of the fiscal year 2015 (please refer to Table 1) (Pakistan Telecommunication Authority, 2015).

Telecom Revenues.

a In 2016, Pakistani 12.5 Rupees was approximately equal to 1 Norwegian Krone.

Pakistan’s smartphone penetration was 19% (Statista Research Department, 2016) and was further expected to increase (Farooq, 2016). Social media presence also grew, as evidenced by the rise in Facebook subscribers, which reached 30 million in 2016, followed by Instagram, with 3.1 million users. According to the Global System for Mobile Communications Association (GSMA) report, voice-only telecommunication subscribers contributed approximately 18% by the end of 2015 and were expected to decline. Voice tariffs also declined (please refer to Exhibit 1). Conversely, broadband subscribers contributed about 8% in 2015 and were expected to increase by 2020. Consumer loyalty was based on the network of the social circle, quality of service and availability of service. Was the connection proper? Was the recharge easy? Telenor and other big players had an advantage due to greater tower share (please see Exhibit 2). Price also played a huge role in consumer decision-making. People considered the rate for social calling and converted their entire family to another telco brand if better rates were offered. Moreover, people kept primary network and secondary network numbers. A primary network number meant that number was available to most people in their social network, so one had to maintain it to avoid the hassle of resharing a new number. Secondary numbers were obtained if the consumer got a better package from a certain network, such as better call packages, SMS or internet packages. Telcos had an annual churn rate of 15%–20%. The monthly churn rate ranged between 1.2% and 1.6%.

The key telco players of Pakistan, apart from Telenor, included Jazz, Zong, Ufone and Warid. At the end of the year 2016, Jazz (previously called Mobilink) had the highest market share at 29.2%, followed by Telenor (27.5%), Zong (19%) and Ufone (15%)(Pakistan Telecommunication Authority, 2015). By early 2016, most telcos focused on launching 3G/4G services, tower leasing, sharing and attaining operational efficiencies (Our Correspondents, 2016).

Jazz (Previously called Mobilink)

Mobilink entered the Pakistani market in 1994 and became the first mover in the telecom sector. In the year 2009, Mobilink witnessed a decline in its growth rate. By the end of March 2015, Mobilink’s revenue was Rs. 51.3 billion. Mobilink had a prepaid mass brand, Jazz, and a niche post-paid brand, Indigo. The prepaid cards were called Jazz cards, and the recharge was a Jazz recharge. The company also launched Jazz Jazba, which targeted the youth segment but could not succeed. At the end of 2015, Mobilink took a unified brand approach, consolidating its prepaid and post-paid functioning under the single umbrella brand, Mobilink. Customers were disgruntled with this change. They were used to buying their Jazz connection. Based on this negative customer sentiment, the company changed the umbrella brand from Mobilink to Jazz. All sales and service centres were rebranded as Jazz, and a new campaign to depict this was launched with a tagline, ‘Dunya ko bata do’ (tell the world). Jazz was aggressively marketed on broadcast media.

Umair believed, ‘The Pakistani masses connected with Jazz and not Mobilink; the change was the right move by the company’.

Most of the company’s shares were owned by VEON, a digital operator headquartered in the Netherlands with a brand presence in Central Asian countries, Ukraine and Pakistan (VEON, n.d.). In October 2016, it had a forty-one million subscriber base. In the same year, Warid Telecom merged with Jazz, increasing the brand’s overall footprint by fifty million subscribers (Shairani, 2016). Tower shares and customer convenience also increased. At the end of 2016, Jazz’s earnings were Rs. 135.6 billion (Baloch, 2017).

Zong

Zong was launched in 2008 as a single shareholding company of China Mobile. China Mobile was headquartered in Beijing, China. China Mobile was present in Hong Kong and China, apart from Pakistan. Zong introduced its 4G spectrum in December 2014 with an investment of $600 million as license fees. By 2016, Zong had the widest 4G network, with approximately three million 4G subscribers in 200 cities across Pakistan (Arshad, 2017). Umair believed that Zong was a forward-looking company. It knew the future was about digital solutions and had solid support to back its assertion. He believed that China Mobile’s focus on the Pakistani market was not only due to the huge consumer demand but also due to its limited global presence.

At launch, Zong was positioned as an accessible brand for the masses with a tagline ‘sab kehdo’ (say everything). It also extensively engaged in price wars to entice price-sensitive customers. It was later repositioned, focusing on urban consumers, especially the millennials, with a tagline ‘A new dream’. Zong offered prepaid and post-paid services and mobile broadband devices.

Ufone

Ufone, launched in 2001, was a mass brand with 5.2 million subscribers in 2016. It was a subsidiary of UAE-based Etisalat (Ufone 4G, 2024). Due to its burgeoning population, Pakistan was an important market for Etisalat. Ufone was the number 2 telco brand in Pakistan until 2005. Both old and young age groups loved its humorous ads. The brand often took a dig at its rivals cleverly. Ufone communications were considered creative. However, the brand health tracking studies depicted lower customer satisfaction with Ufone’s service quality, leading to its eventual market share and profits decline (Tirmizi, 2019). Ufone had prepaid and post-paid services by the name of Ufone.

Internationally, there were many telcos, such as Airtel, Verizon, Vodafone, Reliance, Orange, AT&T, and so on. These companies operated in different regions across the world. The concept of mobile virtual network operators (MVNOs) was also prevalent. MVNOs were network resellers that did not have telecommunication infrastructure and targeted different customer segments. For instance, Lyca was an MVNO that operated in sixty countries globally. Umair believed that the competition in telecom was intense globally. He recalled the Indian example: ‘In the Indian market, the top four players, Airtel, Vodafone, Idea, and Reliance, occupied approximately sixty percent of the market, and the other small players had the rest of forty percent’.

Telenor

Unlike urban-focused Zong and Mobilink, Telenor entered the Pakistani market as a rural brand in March 2005. It was a subsidiary of Telenor Norway, which had a presence in the Scandinavian region and Asian countries like Pakistan, Bangladesh, Malaysia, Myanmar and Thailand. At launch, Telenor specifically focused on regions with difficult typography, such as the mountainous regions of Hunza and Gilgit. Telenor was the fourth player to enter the Pakistani market with its commercial services. At that time, major cities and towns were already well covered by companies such as Ufone, Jazz/Mobilink and Warid. Telenor, therefore, went to rural areas not covered by the present telecom operators. This proved to be a very successful strategy in acquiring customers.

Umair remembered: ‘At the time of launch, our position was number four, and our assessment of the Pakistani market was very bullish. Overall, the telecom industry was on double-digit growth, and the Pakistani outlook was very positive’.

Telenor’s mission was focused on empowering society, and its positioning revolved around empowering communities. The initial tagline was ‘karo mumkin’ (make it possible). This tagline represented the company’s socially responsible point of view and was intentionally kept broad as a few other brands were also endorsed by Telenor, including Easy Paisa. From a subscriber’s point of view, Telenor was a mass brand with the most rural subscriber base amongst all the four operators in Pakistan. The overall tone of voice of Telenor’s parent brand was rather sophisticated. Telenor spent 5% of the top line on advertising. By 2016, its ARPU reduced to Rs. 205 from Rs. 212 in 2015.

Talkshawk was launched in early 2006 as a mass brand. This brand was the company’s primary breadwinner and contributed 99% to the company’s revenue, delivering good value to the user at an affordable price (refer to Exhibit 3 for logo). A total of 80% of Telenor customers used Talkshawk. The brand positioning was around transparency, primarily due to decreased customers’ understanding of tariffs. A market segmentation study in 2013 revealed five key segments in Pakistan, of which three segments, namely affluent males, bargain hunters and value-seeker youngsters, included males who spent more on mobile technology and quickly adopted the new services provided by telecommunication companies. Additional research also showed that people feared losing their balance (paid amount as credit in phones). Telecom operators were working on a model of auto deductions, that is, there was a daily amount deduction; for instance, at the end of the day, a 50 paisa or 1 rupee deduction happened due to service provision. This had led to trust issues and poor customer perception for other operators. Research also showed that subscribers were aware that Telenor had no hidden charges. This insight led to Telenor’s functional positioning around the platform, ‘your truthful partner’, executed entertainingly rather than in the form of in-your-face, dull communication. Through this platform, the brand became more vocal about its transparency. A new relaunch campaign based in a rural setting focused on the brand’s new platform with a tagline ‘sachi yari sab pay bhari’ (true friendship outweighs everything). The new tagline reflected the brand’s transparency and reliability in providing cellular service. Telenor’s advertising spend was 80% on Talkshawk and 20% on Djuice. The ‘Sachi yari’ campaign was carried out on broadcast media and through on-ground activation. The activations involved street theatre with dramas such as Ali Baba Chalees Chor (Ali Baba and Forty Thieves) and Heer Ranjha (love folklore), which amused the entertainment-starved audience and communicated brand benefits.

Telenor’s brand that targeted the urban youth, 55% of Pakistan’s population, was Djuice. This brand contributed 80% to the company’s revenue. The core audience included tech-savvy males below 22 years of age residing in urban centres. This brand had a rebellious personality. Djuice was a fighter brand that countered competition through its focus on price. Early on, Djuice was promoted independently, but later, Telenor’s endorsement appeared at the end of the communication with a voiceover stating, ‘Djuice, powered by Pakistan’s best 3G network, Telenor’. Djuice’s communication adopted a social platform that emphasized changing the attitudes and behaviour of young consumers. It urged them to raise their voice against the evils of society, such as harassment, bribes, etc. with its slogan ‘khamoshi ka boycott’ (boycott silence). An anthem was also launched for this campaign. This Djuice campaign won two Pakistan Advertisers Society awards in 2012. Telenor spent 20% on the Djuice brand overall. Djuice’s on-ground activities included stand-up comedy at urban universities and cricket activation. Later, Djuice was positioned towards data and 3G. Brand health tracker studies showed high awareness and relevance amongst the core brand audience. The ARPU for the Djuice brand was higher compared to Talkshawk. Furthermore, 15% of Djuice’s customers used the Talkshawk SIM. Telenor used data-driven marketing, advanced segmentation and concepts like social influence for its Djuice brand to get subscribers and to create usage-based packages and campaigns (Malik, 2023).

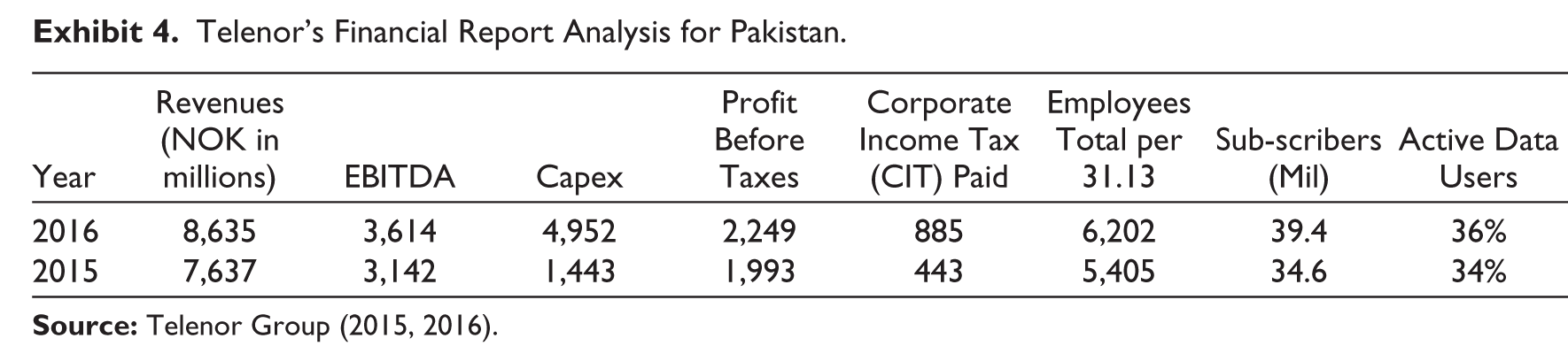

Telenor’s post-paid connections targeted urban business owners and consumer segments. The business segments included small and medium enterprises (SMEs) and the corporate sector. Mobilink had a monopoly in the corporate segment, while Telenor dominated the SME segment. The consumer segment included post-paid connections for urban people. In 2010, Telenor post-paid packages were branded as Telenor Persona, which was later discontinued and branded as Telenor due to the lack of equity-building efforts. Brand health tracking studies showed that overall awareness for Talkshawk and Djuice was not increasing despite advertising spend, and sales were not increasing as per the set targets (please refer to Exhibit 4).

Umair mentioned:

Our brands, Talkshawk and Djuice, had distinct personalities. The mass audience related with the Talkshawk brand. It was a very local and awami (mass) brand with a cultural tone of voice. On the other hand, Djuice focused on a social mission platform that appealed to urban youth. We had intentionally kept the personalities and brand associations distinct through our communications on different platforms.

Value Chain

All Telenor brands used the same network, Telenor. The same network meant no differentiation in the actual product experience, the experience of a call, or the data experience. A Djuice or Talkshawk SIM was purchased, but all recharges were Telenor recharges. Another important aspect was the recharge channel. Telenor-owned channels and franchise walk-in shops also provided recharge and SIM provision services. However, once a customer had bought the Telenor SIM, an SMS was received, for example, ‘Welcome to Talkshawk’. Logos of the three brands were placed outside and inside the shops. Moreover, customer complaint handling and helpline happened under Telenor’s umbrella. Separate outlets for Djuice were experimented with in 2015, but this concept was later discontinued. Survey research indicated that Telenor customers identified using Telenor, even though Talkshawk was approximately 80% of the base and Djuice was 20%. Overall, all Telenor brands varied in terms of pricing and communication. Talkshawk was voice-oriented, whereas Djuice was SMS and late-night calls-oriented because youth could make cheaper phone calls by changing their usage time.

As Umair prepared for the meeting, he considered how phasing out Talkshawk would alienate its core audience and compromise its big scale. He had examples from the telecommunication industry that emphasized a branded house approach, all offers presented under the same brand name, but what would be the repercussions for the number 2 player, challenger, Telenor, if they went for this option? How would the customers react? He knew the shareholder requirement on the return on investment was much higher. He frowned at the fact that the company earned in Pakistan Rupees terms, but the shareholders’ payout was in NOKs (please refer to Exhibit 4). He could convince heads about the increased top line with both brands or accept their suggestion to do away with Talkshawk.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Appendix

Telenor’s Financial Report Analysis for Pakistan.

| Year | Revenues (NOK in millions) |

EBITDA | Capex | Profit Before Taxes | Corporate Income Tax (CIT) Paid | Employees Total per 31.13 | Sub-scribers (Mil) |

Active Data Users |

| 2016 | 8,635 | 3,614 | 4,952 | 2,249 | 885 | 6,202 | 39.4 | 36% |

| 2015 | 7,637 | 3,142 | 1,443 | 1,993 | 443 | 5,405 | 34.6 | 34% |