Abstract

The case examines the dilemma surrounding Zepto’s anticipated 2026 initial public offering. Zepto was founded by Aadit and Kaivalya Vohra, both Stanford University dropouts. It disrupted the quick commerce landscape and leveraged it. Initially, they offered micro-transaction services and 10-minute grocery delivery, which was unrealistic at the time, particularly with COVID-19 looming large; however, they identified the urgent need for faster grocery delivery during the pandemic. With their technology background, they brought a tech-driven model and established ‘dark stores’ to ensure faster delivery. The model boasted a strong logistics system and a fleet of delivery partners, supported by its app, to deliver groceries in under 10 minutes. This led consumers to embrace the option of faster grocery delivery at their convenience, helping Zepto emerge as a strong player by 2023. Zepto was then set on being an entirely Indian company after raising $350 million from Motilal Oswal Private Wealth. The case discusses the convergence of financial strategies and the decision to go public. The case is based on qualitative data and relies solely on secondary sources, including financial performance data published by the company on reputable business reporting sites like Inc42 and Entrackr, press releases and official statements, media interviews with the founders, and industry analysis of the quick commerce industry.

Discussion Questions

Why did Zepto target a 2026 IPO?

How strong were Zepto’s financials for an IPO? Do you think Zepto was prepared?

What risks and opportunities did Zepto’s IPO present?

Based on the case, should Zepto list in 2026, or delay its IPO?

The useful hours in Mumbai were ending, and through the glass of the relentless towers, their shadows fell on the Zepto building. In the conference room, Aadit Palicha surrounded himself with papers covering topics such as financial forecasts, the competitive environment, and several related to the initial public offering (IPO). The quick commerce startup he had started with Kaivalya Vohra had transformed the way millions of Indians shopped. However, one evening, Aadit wrestled with a tough dilemma: should Zepto move forward with its IPO in 2026 to raise growth capital and establish an appropriate market position, or improve its financial situation and increase the likelihood of profitability?

Most entrepreneurs viewed an IPO as the end of the road for a business—a success and confirmation to the world. For Aadit, it was not just a milestone but a strategic decision with financial implications. Customers, suppliers, co-investors, competitors, existing venture capitalists, and internally generated ambitions all placed pressure on the company. In in-house deliberations, management appreciated that Zepto’s IPO timing could not be merely a financial move but a strategic message to investors and the sector, as the company was confident in its business model and growth path. The 2026 IPO would be viewed by markets as a bold move by Zepto to declare its readiness to operate at scale, its level of operational maturity, and its aspirations to become a market leader. The postponement of the initial offering, on the other hand, might be seen as a risk-avoidance strategy, possibly reflecting unresolved profitability issues or a desire to wait until market conditions became more stable.

Several directors noted that sector IPOs, such as Zomato and Paytm, were evaluated not only on financial performance but also on the implicit messages their timing conveyed. Aadit and his team deliberated extensively on whether to capitalize on the existing momentum, which would have excited investors and enabled Zepto to command premium valuations, or to wait until confidence in the long-term viability of the firm improved. The management knew that their decision regarding IPO timing would shape external perception, influence investor sentiment, media narratives, and even competitor responses. Aadit hesitated and reflected that an IPO was not a decision made in cost accounting terms but a strategic, interpretive one. The market was exerting pressure—either the company would give in or would stand its ground. The question was whether they were ready for that.

He was aware that a listing in 2026 would reflect the company’s aspirations and would signal to the sector that it intended to be a leader, but it also would be subject to market scrutiny regarding profitability and growth trajectory. Alternatively, it could be seen as a cautious move by stakeholders, who would interpret it as prioritizing long-term stability over short-term hype.

The board deliberated until late into the night, not only on financial projections and market signals but also on the reputational and strategic messages that the timing of the IPO would send. It became less about raising funds for future growth and more about what Zepto would communicate to the market.

Emergence of a Vision

Zepto was started by Aadit and Kaivalya Vohra, both dropouts from Stanford University, at a time when ‘convenience’ was the word that best captured the entrepreneurial spirit in 2020. It did not begin with the dictum of comfort inherent in its product strategy, but it brought disruption and leveraged the quick commerce landscape. Initially, they offered micro-transaction services and 10-minute grocery delivery, which was considered unrealistic at the time, though it appealed to the general Indian consumer base. They claimed they would deliver groceries in under 10 minutes, recognizing the strong need for faster grocery delivery during the pandemic. They identified the gap: most consumers could not step out to access basic grocery items and failed to take advantage of available options.

With their technology background, they introduced a tech-driven model and established ‘dark stores’ in densely populated areas, strategically located to ensure faster delivery (TICE, 2024). Due to the sharp focus on the delivery model, coupled with strong organizational performance, the company was able to raise significant funding, as investors believed in the founders’ ability to execute the change. The model included a strong logistics system and a fleet of delivery partners, supported by its app, to deliver groceries in under 10 minutes. This led consumers to adopt faster grocery delivery at their convenience, helping Zepto emerge as a strong player by 2023.

Within a relatively short time frame, Zepto performed strongly in business terms. It expanded its operations to over 20 cities and built a large network of dark stores, while continuing to serve a growing customer base. Despite operating with a relatively small workforce and a dispersed base, the company disrupted the market through a focused delivery model and strong operational execution. Founded in 2021, it promised to deliver groceries in less than 10 minutes, tapping into India’s embrace of innovation during the pandemic.

The quick commerce segment was highly competitive. Competitors such as Blinkit and Swiggy Instamart actively competed for market share. Additionally, costs such as fuel, human capital, and technology continued to rise. The journey was not without challenges, including intense competition, operating margin pressures, and the persistent question of profitability in the Indian market.

Still, Swiggy’s Instamart, Blinkit, and Dunzo put pressure on Aadit, and he realized the importance of maintaining a strong financial ‘war chest’ to fend off competitors and keep Zepto ahead. At the last funding round, the company was valued at USD 1.5 billion, but due to its high burn rate, Aadit needed additional capital quickly.

To expand into Tier-2 cities, scale the use of artificial intelligence in logistics, and improve profitability, the company required additional funding. The IPO could have helped them acquire the necessary resources, along with other strategic advantages.

Quick Commerce Market in India

The quick commerce (Q-com) segment focused on grocery delivery services that enabled last-mile delivery solutions by utilizing dark stores with a limited product range but faster delivery times. In these cases, the platform was solely responsible for delivery operations. This also included grocery delivery services that advertised delivery in 3 hours, despite most competitors advertising delivery services in under 30 minutes.

The quick commerce business model was perceived to be destroying Kirana stores. Palicha dismissed such arguments as ‘narratives that did not adduce any data to understand the sector as a job creator and an incubator of entrepreneurship’. ‘The instant 10-minute delivery model had created more than 450,000 jobs with wages above informal sector trends’, he underlined, adding that ‘Zepto aimed to use Indian innovation to deliver groceries like nothing else’. Another effort to respond to the indictments arguing that Zepto engaged in predatory pricing was made by Palicha, who stated that, according to the data, 99.8% of all offerings listed on the platform were offered at a price higher than the cost.

The quick commerce segment market in India was expected to reach $5.5 billion in 2025. This market was projected to grow at a CAGR of 24.33% over the assessment period of 2024–2029 and could have reached approximately $9,951.00 million by 2029. Toward the end of that period, the quick commerce user base in India was expected to rise to 60.6 million. The user penetration rate, which was 1.8% in 2024, was projected to increase to 4% in 2029 (Statista, 2024). The Global Mobile Virtual Network Operators (MVNO) market was forecast to reach $780 billion in 2018, with an average revenue per user (ARPU) of $127.70. At the global level, China was expected to dominate the quick commerce market in terms of revenues, grossing $80,840.00 million in 2024, and it had recorded the highest user penetration rate of 21.4% in 2024. As far as India was concerned, the factors behind the exponential growth of quick commerce included increased smartphone penetration and strong demographics of people under 35 with digital dependency (Mukherjee, 2024). The technological setting was proactively developed to support continual improvements to business operations; this approach increased elasticity and efficiency across the supply chain. Such innovations helped platforms deliver services faster to meet the increasing need to deliver products at the earliest, the report suggested.

In India’s swiftly evolving consumer landscape, quick commerce was reshaping the way convenience shopping was perceived, turning it into a fierce race. A civilization with a history spanning 5,000 years was now expecting essentials to arrive in just 10 minutes—whether sugar or diapers. Services such as Blinkit, Zepto, and Swiggy Instamart were stepping up to meet this demand, placing pressure on traditional retailers and established e-commerce giants. As the appetite for instant satisfaction grew, the number of quick commerce platforms expanded, providing consumers with a plethora of immediate service options. While this abundance was enticing, the consequences of such rapid delivery often went unnoticed.

For industry leaders, these challenges also opened doors to growth. Blinkit, for instance, reported an impressive over 100% increase in year-on-year sales during the September quarter, with average delivery times for groceries and essentials reduced to 8 minutes. It expanded to nearly half the scale of Zomato’s original food delivery service. Swiggy, which started as a food delivery app, broadened its Instamart service to 43 cities, doubled its product offerings to almost 20,000 items, and slashed delivery times from 17 minutes to under 13 (Desk, 2024).

Quick commerce had rocketed in India, growing by more than 280% over the last 2 years, and Gross Merchandise Value (GMV) rose from USD 0.5 billion in FY22 to USD 3.3 billion in FY24, as revealed by Chryseum.

The quick commerce sector was expanding at a 73% annual rate, while traditional e-commerce grew at a much slower 14%. The quick commerce market was valued at USD 3.34 billion in 2024 and was expected to reach USD 9.95 billion in 2029 at a CAGR of >4.5%. However, it remained a modest industry, with a penetration of only 7% of the estimated total addressable market of USD 45 million, suggesting growth potential. Thus, manufacturers partnered with quick commerce platforms, which enabled direct sourcing, refined operations, and consequently reduced expenses to match competitive costs.

The Convergence of Financial Strategies

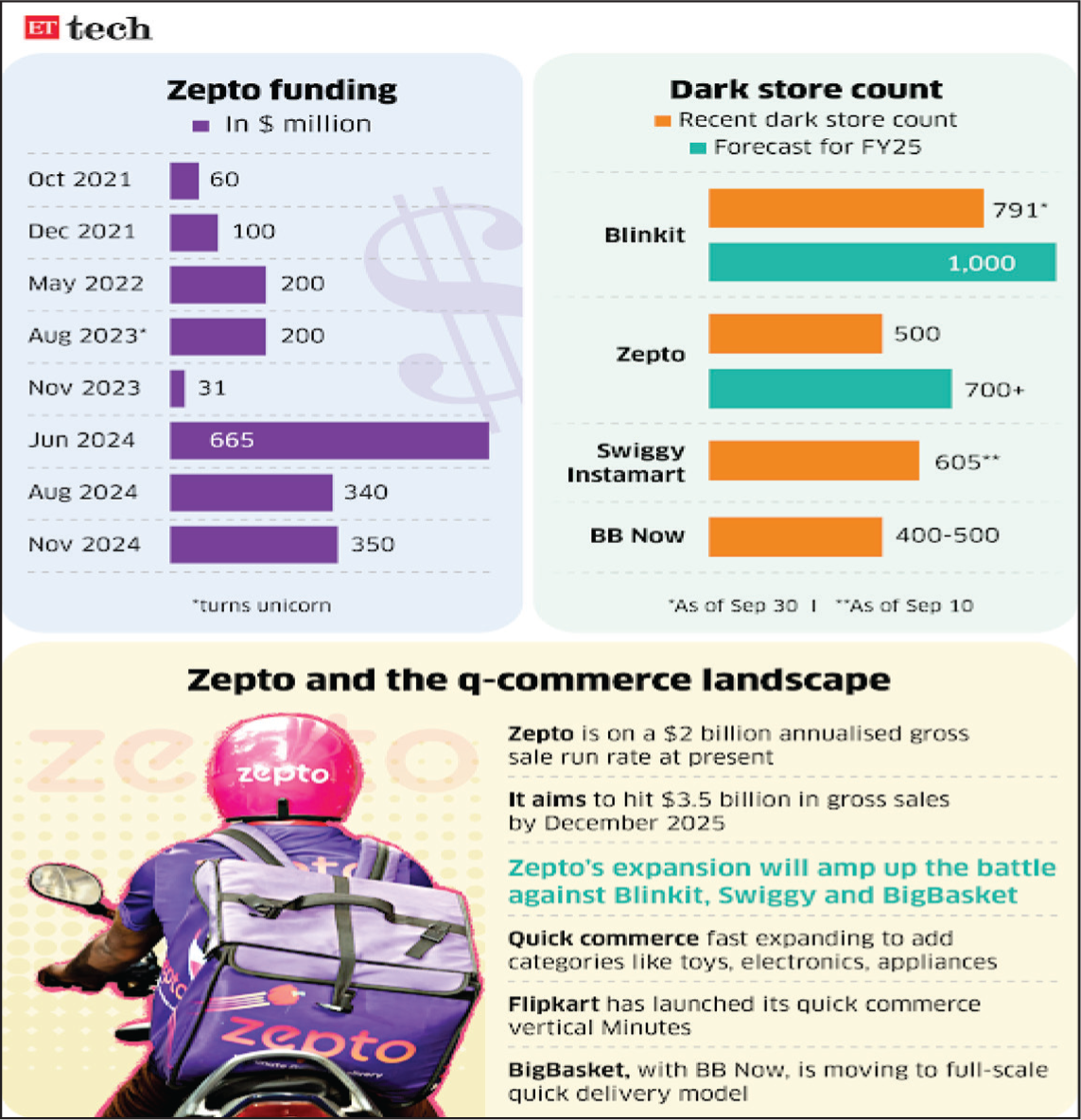

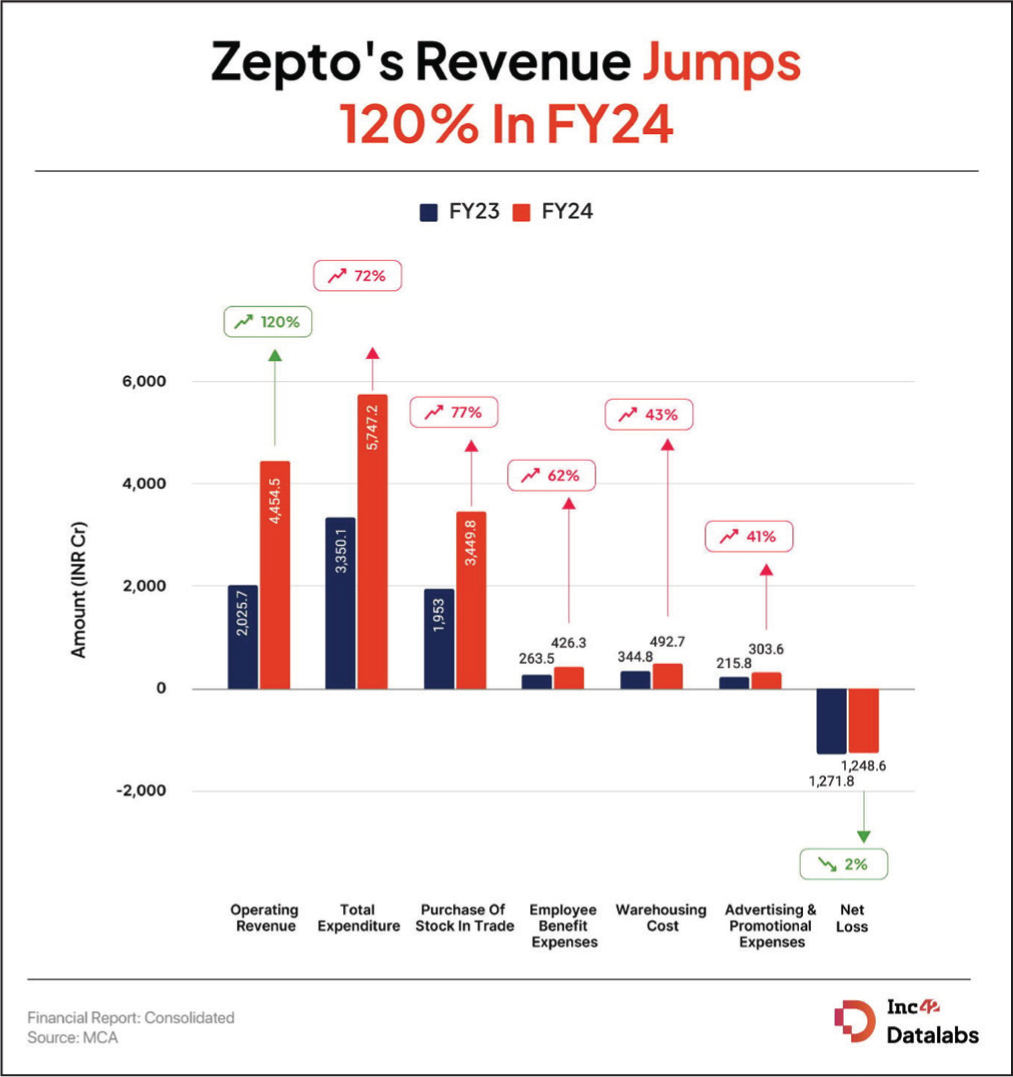

Since the company merged, it grew on the top line by more than fivefold and eyed INR 100 billion revenue in FY24 from INR 20 billion in FY23 (Malhotra, 2024). This 3-year-old startup was able to raise $665 million (around INR 55 billion) from new investors such as NY-based PE firm Avenir Growth Capital, venture capitalist Lightspeed, and Avra Capital from erstwhile Y Combinator Continuity head & partner Anu Hariharan, and billionaire Marc Andreessen’s Andreessen Horowitz. The current round of funding was also invested in equally by earlier investors Glade Brook, Nexus, and StepStone Group. Prior investors Glade Brook, Nexus, and StepStone Group also participated in the funding round equally.

The startup’s target was the delivery of groceries within a 10-minute timeframe by March 2025, with a warehouse count expected to be over 700 within a 2-km radius. This expansion was funded by retained earnings from older stores that were already operating. It was brought out that Zepto captured approximately 29% of the quick commerce business, up from 15% in March 2022. At that time, Blinkit controlled 39% of the market share, and the rest was held by Instamart. Seventy-five percent of Zepto stores had become fully profitable, and this was expected to increase further.

At that time, Zepto was established in 24 cities and expected to open in more than 50 by the current quarter, with gross sales of more than USD 1 billion in May. The company applied the above-mentioned approach to minimize the timeframe required to generate profits and worked to reduce the profitability period of a single store to exactly 8 months. The success shown by the company could only be explained by the framework of the above-described systematic approach. At that time, sustaining PAT positivity for the following financial year was stated to be a strong signal to the market, Palicha said. The coffee business, Zepto Café, which was also projected by Palicha to reach INR 10 billion, enhanced customer market penetration and retention for the company.

In responding to competition from Blinkit and Swiggy Instamart, Palicha encouraged the view that ‘there was enough market share for everyone’. ‘What we did was emphasize more on the process of execution rather than competition. The opportunity here was phenomenal’, he said. Considering the promising development trajectory outlined, combined with Zepto’s positioning itself on a profitable trajectory, it was entering the rapidly growing quick commerce market in India.

Funding Rounds

Zepto’s key investors comprised the following entities:

Motilal Oswal Private Wealth: invested in the third round of fundraising for Zepto in 2024, raising USD 350 million. General Catalyst: invested USD 340 million in August 2023.

Apart from the aforementioned investors, there were other investors as well, such as Dragon Fund, which invested in a round announced in August 2023. Epiq Capital joined as the latest backer of Zepto when the startup raised funds. StepStone also invested and recently increased its investment stake in Zepto (Gupta, 2024) (Refer to Exhibit 1).

Financial Overview Pre-IPO

India raised over ₹1.75 trillion through 103 mainboard IPOs in 2025, but the 2026 pipeline emphasized mature firms in healthcare, green energy, and fintech. SEBI approvals for nearly 200 companies signalled volume, yet experts predicted selectivity with a focus on earnings visibility and realistic valuations (Buch, 2026). Quick commerce players like Zepto navigated this by balancing growth capital needs against profitability proof.

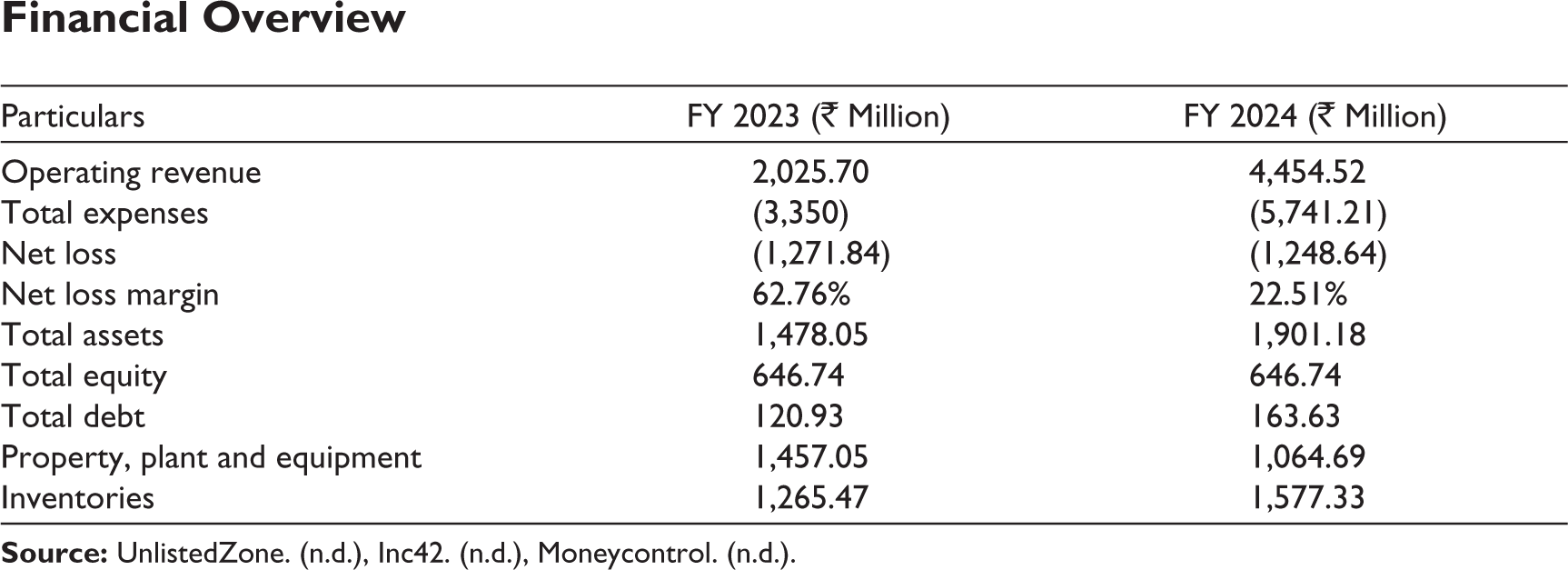

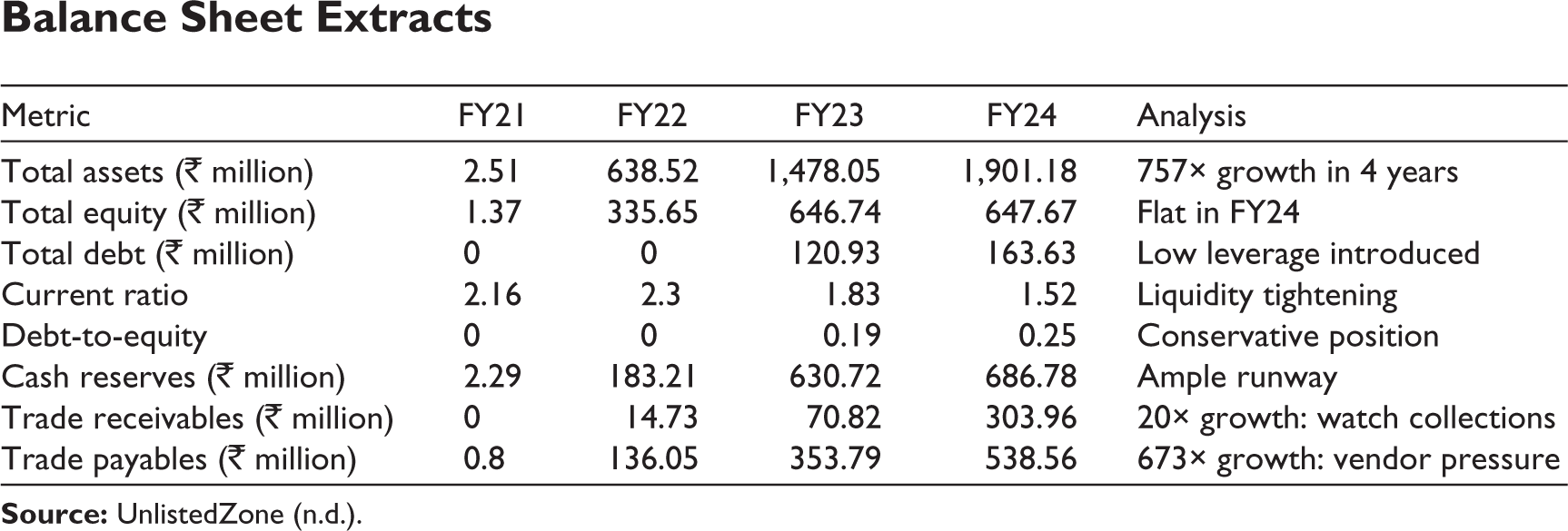

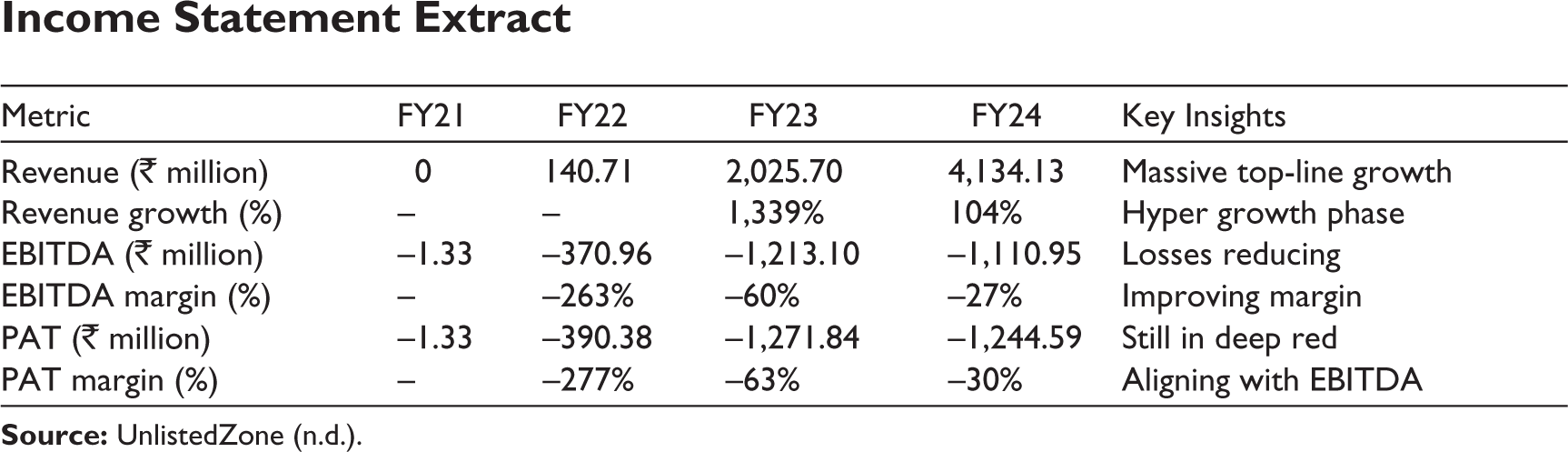

When any company plans for an IPO, its financials came under scrutiny by investors and analysts, and Zepto was no exception. Based on secondary data available in the public domain, the consolidated financials of the company showed a mixed outlook of high revenue growth coupled with sustained losses.

Financial Overview

Balance Sheet Extracts

Income Statement Extract

The Decision to Go Public

Even when attempting to position the IPO in a favourable light, the actualities were inescapable as much as when Aadit presented the facts. Zepto’s valuation was projected on ambitious growth projections:

Revenue forecasts: This particular outcome is designed in a plan to double income at least twice in the next 3 years. Path to profitability: To realize a breakeven point over the next 18 months by creating and delivering cost efficiencies (Refer to Exhibit 2). Valuation multiple: The P/CF is rather higher and ranks the firm in the upper tier, above such nice growth rates among peers. It usually sets this out as a benchmark for market sceptics (CFI Team, 2024; Ramasubramanian, 2024; Shukla, 2024).

Zepto had earlier planned to raise at least $450 million through fundraising; however, this figure may be readjusted before the draft IPO documents are filed (Desk, 2025). But as per the recent development published in the print media, Zepto plans to expand its public offering from $800 million to $1 billion, which will incorporate secondaries. CEO Aadit Palicha met with major mutual funds while discussing the potential stock market listing for Zepto in recent weeks (Mishra, 2025).

The CFO added, ‘Aadit, investors will require some degree of assurance on such figures’. If we are unable to meet these expectations, there is a real possibility that the price of our shares will decline. Here is how one can analyze it: Try to picture the days following Zomato’s IPO—the first several days are joy, but then weeks of doubt strike. But this decision had some issues; not trying for the IPO right away had its issues. They also discovered that while they have adequate capital with ₹3.5 billion, it would only be sufficient to fund the operations for slightly more than a single fiscal year if gross expenditure were to be maintained at current heights for Zepto. Another wave of the private funding round might decrease the founder’s percentage considerably; investors began looking for the prospects for companies’ adaptation to the probability of shifting to net profit (Bhupta, 2023). Aadit, therefore, had two key concerns: The first external threat was attention and gaze, and the second was a threat to Zepto’s innovation. In the last scenario in Hawken’s picture, interested parties pose a question: ‘What if we lose our nimbleness?’ That is why we must pay attention to the fact that having some of the targets set quarterly makes them act in the interest of the short-term goals rather than the long-term goals.

There was serious consideration in the boardroom. ‘Aadit, we have gone through all possibilities’, the CFO put a pile of reports in front of Aadit. What happens is that the IPO is the next stage that should be taken. The market conditions are ideal, and the investors’ interest in enterprises that use technology is still high. Aadit started turning pages through constant focus on landmark numbers to pull from his existing knowledge database. Zepto’s revenue has grown to INR 15 billion, and yet the profitability was more of an abstract concept associated with the quick commerce sector. It was a sign of self-confidence and acknowledgement at the same time which also came in the form of commitments at the $1.5 billion valuation at the end of the last funding round. ‘Shutdown facing markets—Are we ready to face them?’ Aadit said with a concerned tone in his voice.

These new funds will be used to increase the number of dark stores since Zepto aims to have 700 stores by March 2025. There are a few new geographies like Nasik, Chandigarh, Vizag & Ahmedabad where the company has to foray, while on the other hand, the company requires more outlets in the main markets of Mumbai, Delhi & Bengaluru. This strategy of expansion is expected to take advantage of the perception that Tier-2 cities’ operational costs are relatively affordable and that the market will achieve profitability within a shorter duration than in larger cities. In the discussion, Kaivalya added, ‘This is our opportunity to drive growth, enhance the technology portfolio, and leave everyone else in the dust’. One outcome is effective PR, but we have to avoid the problem of being overpriced and hiding our deficiencies.

The Pathway to Becoming a Public Entity

A new round of funding was employed in the growth of the number of dark stores since Zepto aimed to have 700 by March 2025. Emerging outlets such as Nasik, Chandigarh, Vizag, and Ahmedabad required simultaneous development, and the company had to extend its outlets in the main cities, namely Mumbai, Delhi, and Bengaluru. This kind of expansion was likely to take advantage of lower operational expenses in Tier-2 cities, where the market was expected to achieve breakeven sooner than in large cities.

Kaivalya joined the discussion. ‘As it stood, this was an opportunity to power growth, upgrade the tech portfolio, and overrun everyone else. But we had to be sensible in our pricing, honest about it, and mindful of our business challenges’, he said.

By 2024, venture capital and private equity investors had taken over Zepto’s shareholding and invested in the company through several rounds of funding (Exhibit 3), significantly increasing its valuation. In line with standard venture capital investment processes, an IPO was a significant valuation discovery and capital realization tool for late-stage investors. Meanwhile, reliance on private financing made the firm vulnerable to pressure on valuation in the case of delayed profitability milestones (ETtech, 2025). The IPO decision was therefore determined not only by operational readiness but also by investor expectations regarding exit and liquidity.

The board of Zepto had approved plans to issue up to INR 110 billion in the proposed IPO (Entrepreneur Staff, 2025). The issue was to include both a fresh equity issuance and an offer for sale by existing shareholders as part of the listing process; however, the specific mix of fresh issue and offer for sale had not yet been disclosed in publicly available filings (Upadhyay, 2025). Media reports indicated that regulatory filings revealed the company’s expectation to file its draft red herring prospectus under seal, suggesting that the company was planning to raise substantial capital and provide existing investors with a liquidity exit.

The Turning Point and the Decision

Zepto was experiencing rapid expansion and entering the quick commerce market, which investors saw as a strong opportunity for profit. Its fivefold increase in revenues and INR 100 billion FY24 target, together with multimillion-dollar financing from new and returning foreign investment funds, were indications of financial momentum uncommon among young startups. Investors realized that a successful IPO would open a new capital pool needed to further boost growth, especially into Tier-2 cities and new market segments, while also protecting against high operating costs and intensifying competition (Exhibit 4). The store-level profitability history, Zepto’s increasing market share, and strong backing from reputable venture capitalists created expectations that the public offering would provide liquidity and long-term value.

From the investor’s perspective, Zepto’s pursuit of profitability, continued growth, and operational efficiency were positive indicators of business health ahead of a public listing. The fact that the company needed to achieve the shortest possible breakeven time per store and maintain positive operating margins, even after the IPO, reassured investors about its potential stability. Zepto’s strategic focus was seen not only as a means of surviving intense competition from Blinkit and Swiggy Instamart but also as an effort to become a dominant player in a segment that was expected to grow exponentially. With Zepto’s management outlining ambitions for new geographies and scaled technology, investors expected that a timely IPO would place them in a strong position to capture disproportionate returns from the rapidly developing quick commerce market in India, while also positioning Zepto as a leading example of tech-driven retail growth.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.