Abstract

This study examines the mediating effect of investors’ sentiment on the relationship between corporate governance (CG) and herding and risk-averse behaviour in the Shariah-compliant stocks in Malaysia and Gulf Cooperation Council (GCC) countries. Panel data and quantile regressions are adopted, and the research timeframe is 2017 to 2021. The result shows that remuneration. Audit Committee, risk management and internal control and engagement with stakeholders significantly and positively correlate to Malaysia, Kuwait, Oman, Qatar, Saudi and the UAE stock returns. Board responsibility is the only variable significant in Malaysia, Saudi and the UAE. The result implies a full mediation as the CG has caused the changes in investors’ sentiment and subsequently triggered the investors to herd and become risk-averse. The impact of CG is more pronounced in the upper and lower quantiles of the returns of Malaysia, Saudi and the UAE, as well as the median quantile of Bahrain, Kuwait, Oman and Qatar. The result of this study contributes to policymakers, regulators and practitioners in identifying the best CG practices that assist the Shariah-compliant stocks in Malaysia and GCC countries to gain a better stock return, investors’ sentiment and behaviour. The results assist the governments in the impact and benefits of adopting CG in different Islamic countries.

Introduction

Malaysia and Gulf Cooperation Council (GCC) countries are still young at practising corporate governance (CG) reporting to enforce the public listed companies to disclose their compliance with CG practices. In 2017, the Securities Commission revamped the Malaysian Code on Corporate Governance (MCCG) and implemented the corporate governance (CG) reporting to be published separately from the annual report. Similarly, the regulators of GCC countries have emphasised the disclosure of the environmental, social and governance (ESG) in the annual report. These transformative regulations improve the transparency and corporates’ impact on the CG. Nonetheless, what is the impact of complying with the CG best practices? Are investors’ sentiment and behaviour affected by the CG compliance? These answers are worth finding as the cost of achieving CG can be a burden for any publicly listed companies, especially in developing Islamic countries.

Herding is a behaviour where investors mimic the decisions of a bigger group of investors they perceive as well-informed. The existence of herding is widely documented in developed markets such as the United States, United Kingdom, Canada and Hong Kong markets. Nonetheless, previous studies often overlook emerging markets, especially the Middle East. The Middle East regional market consists of the GCC members, namely, Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates (UAE). One of the uniqueness of GCC markets is that they trade Shariah-compliant stocks, which prohibits riba, gharar or doubtful transactions, gambling, etc. Although other markets such as Malaysia, Singapore and Egypt also trade Shariah-compliant stocks, Malaysia and GCC markets have a higher number of Islamic companies due to their Muslim population. Moreover, the Malaysian and GCC markets are more dominated by Muslim investors, who may have different investment motives (Barom, 2019).

Risk-averse behaviour is often shown in many developed markets such as the United States, the UK, Hong Kong, Japan and Canada. Nonetheless, contradictory findings are spotted in explaining the investors’ behaviour in emerging markets. Momin and Masih (2015) show that investors in emerging markets are less likely to be risk-averse in increasing the appearance of their portfolios in emerging markets compared to developed countries. On the contrary, Ali and Asri (2019) argue that investors are risk-averse to prioritising the principal’s safety invested in emerging markets. Nonetheless, limited studies look at the impact of CG on risk-averse behaviour, especially on Shariah-compliant stocks. It is necessary to establish a comparative study examining risk-averse behaviour in a few emerging countries.

Shariah-compliant stocks are the key growth of Malaysia and GCC markets, not only for Muslims but also for socially conscious investors. Nevertheless, herding and risk-averse behaviours show that investors are irrational in following the investment decision of others to make similar decisions. Previous studies (Baharudin, 2019) show that the board effectiveness has improved along with the quality of CG reporting. Nonetheless, GCC countries still lag on CG reporting. Some authors (e.g., Shamsudin et al., 2018) argue that the adoption of CG can cause the listed companies to perform poorly due to higher cost of compliance. In Malaysia and GCC markets, the impact of CG on investors’ sentiment and behaviour has not been delved thoroughly.

The public listed companies are crucial in shaping economic development in a nation. Nonetheless, most public listed companies cannot effectively and efficiently realise the budget without powerful CG practices (Mauro et al., 2021). The lack of CG goals can also lead to a negative impact on the nation’s development in the long term (Boros & Fogarassy, 2019). As developing markets with limited history in regulating CG, Malaysia and GCC countries may not provide uniform normative regulations that would regulate the control of conformity in a broader sense. The government must understand whether implementing governance and CG of public listed companies is sufficient to serve the public, as in developed markets.

Hence, it is necessary to examine the impact of CG on the financial market and company performance of Malaysian public listed companies compared to the GCC countries. It allows this study to identify the gaps in practices of Malaysian public listed companies versus GCC countries to provide practical suggestions and enhance the current practices with empirical evidence. This is because the public listed companies are supposed to be the benchmark of best practices of corporate governance and CGs in a country. Many companies will argue that while it is too good to be true to maintain the best CG practices it can also be too costly to the public listed companies (Martens, 2020).

For practical implications, this study assists policymakers, regulators and practitioners in enhancing and establishing a comparative analysis of CG practices of Malaysia and GCC Shariah-compliant stocks. This study encourages public listed companies to adopt the best practices as it can prove the positive impact of CG on investors’ sentiment and behaviour. The results of this study can assist the governments in enhancing the CG reporting framework by adopting the CG practices that benefit the listed companies and society.

The remaining sections of this paper are structured as follows: The second section examines related literature. The methodology and estimated models are described in Section 3. Section 4 contains the findings and analysis. Section 5 concludes with a summary, implications, limits and suggestions for further research.

Literature Review

Corporate Governance

Studies on the corporate governance of Malaysian and GCC-listed companies are limited and the bipolar view on its contribution to investors’ sentiment and behaviour is controversial. Naeem et al. (2022) examine the impact of corporate governance adoption and argue that firms that comply well with the code significantly contribute to the firm’s capital structure and sentiment. Similar evidence is documented in the studies of Al-Jaifi et al. (2017) and Khatib and Nour (2021). On the contrary, Zabri et al. (2016) investigate the top 100 listed companies in Bursa Malaysia and argue that board responsibilities and composition do not influence investors’ behaviour. This statement is supported by the studies of Wai Kee et al. (2017) and Kamalluarifin (2016) in which they argue that governance in the Audit Committee does not improve audit quality and not all elements of governance can contribute to the financial market and company performances. In regard to the GCC countries, Al-Ahdal et al. (2020) show that good CG practices can lead to higher investors’ sentiment due to improved financial performance. Nonetheless, the impact of CG on investors’ behaviour on GCC countries remains limited in academic study. Therefore, it is necessary to examine the bipolar view in convincing the public listed companies to comply with the best practices of CG.

Previous studies (e.g., Baharudin, 2019) focus on the impact of MCCG 2017 and show that the board effectiveness has improved along with the quality of CG reporting. Most public listed companies have outlined their CG practices and are more than willing to adhere to the guides of Bursa Malaysia. On the contrary, some authors (e.g., Shamsudin et al., 2018) argue that the adoption of CG can cause the Malaysian firms to perform poorly due to higher cost of compliance and no difference in the performance level of public listed and private sector companies. Nevertheless, these studies examine the MCCG 2012 and data before 2015 mare obsolete for the current Malaysian situation. For GCC countries, the practice is still new, and the UAE announced its CG Code in February 2020. Therefore, it is necessary to validate the contradictory results to examine the impact of CG on investors’ sentiment and behaviour.

The impact of CG is widely proven in developed countries. Muhmad and Muhamad (2021) examine the corporate governance practice of Singapore and argue that public listed companies have higher cash flow and valuations compared to private sector companies due to better CG practices. Besides, Sarkodie et al. (2020) compare the CG practices of UK and US firms and show that investors value the companies’ social and environmental behaviour as materials for investment decisions. This is because the investors have long-term considerations to trust the companies to behave morally to reduce their investment risk. Ghouma et al. (2018) argue that Canadian firms with better CG practices seem to reduce the cost of debt financing due to higher protection of investors’ rights to reduce agency problems within firms. These studies show that the CG practices in developed countries can improve the financial market and company performance. Nonetheless, limited studies examine the impact of CG on emerging Islamic markets, such as Malaysia and GCC countries.

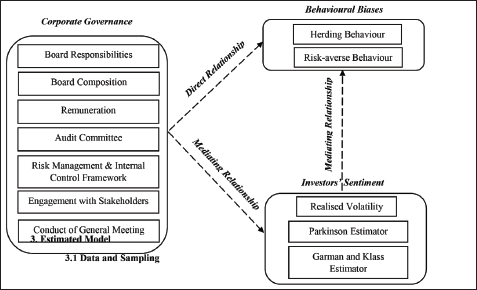

Hence, this study examines the impact of CG compliance on herding and risk-averse behaviour of Malaysia and GCC countries as no study has looked at it from this perspective. The information on the comparative analysis of Islamic countries remains limited. In this context, this study proposes to examine the mediating effect of investors’ sentiment on the relationship between CG and herding and risk-averse behaviours. It allows this study to identify the impact and benefits of CG compliance on investors’ sentiment and behaviour. Based on the above discussion, this study proposes the following hypotheses and research framework:

H1: Investors’ sentiment mediates the relationship between the compliance with CG and herding and risk-averse behaviours in Shariah stocks of Malaysia and GCC markets. H1(a): The compliance with CG is significantly correlated to herding and risk-averse behaviour. H1(b): The compliance with CG is significantly correlated to investors’ sentiment. H1(c): Investors’ sentiment is significantly correlated to herding and risk-averse behaviour. H2: The impact of CG is stronger on in developed markets compared to developing markets.

Research Framework.

Estimated Model

Data and Sampling

A total of 572 public listed companies in Bursa Malaysia were selected. As for the corresponding GCC countries, the following have been selected: Bahrain (42), Kuwait (165), Oman (107), Qatar (55), Saudi Arabia (203) and the UAE–Abu Dhabi Securities Exchange (75). The research timeframe is from 1 January 2017 to 31 December 2021. Only shariah-compliant stocks that remain listing status as of 31 December 2021 are chosen. Shariah-compliant stocks safeguard the interests of stakeholders to prohibit riba, gharar, suspicious transactions and gambling. The other securities such as derivatives, mutual funds, exchange-traded funds and warrants are excluded as the disclosure of CG is not compulsory. S&P Capital I.Q. The database is used to collect information such as CG compliance, stock prices, volatility, investors’ sentiment and behavioural biases.

Corporate Governance

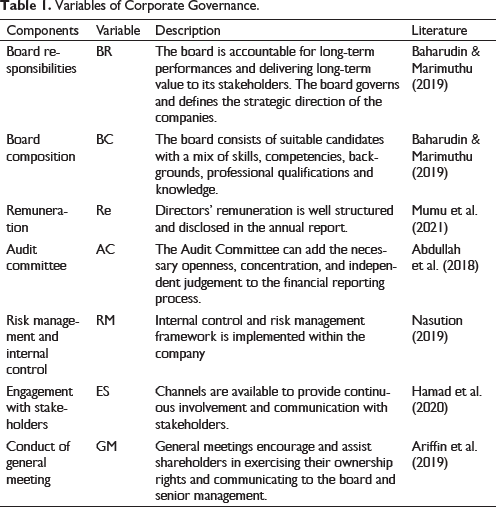

Seven types of CG components are selected, which are board responsibilities, board composition, remuneration, audit committee, risk management and internal control, engagement with stakeholders and conduct of general meeting. All CG variables are proxied by dummy variables with 1 as full compliance to 0 as partial and non-compliance based on the practices as outlined in the MCCG 2017. Table 1 summarises the description and related studies of CG components.

Variables of Corporate Governance.

Investor Sentiment

Investor sentiment reflects the emotions of individual investors, while market sentiment reflects the aggregate decision of all investors in the markets. In this study, investor sentiment is proxied by the volatility of stock returns. Realised volatility (Wen et al., 2019), Parkinson estimator (Parkinson, 1980) and Garman and Klass measures of volatility are used (Garman & Klass, 1980). Realised volatility is used to capture overnight data that is error-free and near to actual volatility. The realised volatility is determined by utilising the variance of discrete returns observed at different periods, and it is expressed as

where Ri,t indicates the return of stock i at time t, which is computed using the closing stock prices from the previous trading day. The realised volatility reflects the overnight-adjusted stock values.

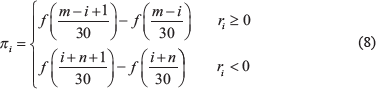

Parkinson’s estimator is another measure of volatility. Parkinson (1980) proposes that volatility may be calculated using the highest and lowest stock prices rather than the starting and closing stock prices. It is a metric that measures severe volatility. Parkinson’s estimator is more useful than starting and closing prices for analysing investors’ extreme behaviour (Blasco et al., 2012). The formula for the Parkinson’s estimator is written as

where

The Garman–Klass estimate is derived from the Parkinson’s estimator to correct the underestimating of the starting leaps caused by the Parkinson estimator’s disregard for the opening stock prices. As markets are more active during opening and closing hours, the Garman–Klass estimator is expanded to incorporate opening and closing stock values. The estimator of Garman–Klass is given as

where

Various volatility metrics may be used to describe the investor mood. The realised volatility captures the stock values from the prior day using overnight data. The Parkinson’s estimator measures the severe volatility of intraday trading. Garman–Klass’ estimator is improved from Parkinson’s estimator by using opening and closing stock prices as a complete metric to proxy volatility.

Herding Behaviour

This research uses the cross-sectional absolute deviation (CSAD) instead of the OLS regression of CSAD, as in Chiang and Zheng (2010), to examine herding in the Malaysia and GCC markets. Panel data regression is used because it is more effective than OLS regression in capturing cross-sectional and time-series analysis (Loang & Ahmad, 2022). OLS regression tends to disregard unobserved factors that affect the dependent variable, which might result in subjective conclusions. Hence, panel data regression is adopted to enhance the explanatory strength of the CSAD regression when detecting the presence of herding. The equation for CSAD is as follows:

where CSAD is the CSAD of stock i at time t, N is the number of stocks, Ri,t is the observed stock return of stock i at time t, Rm,t is the market return at time t (linear), |Rm,t| is the absolute term of the cross-sectional market return at time t, and

Investors’ Risk-averse Behaviour

Tversky and Kahneman (1992) established prospect theory to argue that investors evaluate profits and losses differently. They demonstrate that investors are risk-averse and more emotionally affected by investment loss. Prospect theory explains why investors often depart from the predicted returns of security (Barberis et al., 2021). In this context, risk aversion is assessed by the following value function based on the historical returns of stocks:

where:

is the value function for each stock return, and

with

is referred to as the probability weighting function. In the above equations, RB represents risk-averse behaviour, r represents stock return,

The probability weighting (

Quantile Regression Analysis of Herding and Risk-averse Behaviours

For robustness, quantile regression examines the occurrence of herding and risk-averse behaviours in various

where

The quantile loss function is written as

when

Equation (13) shows that the quantile regression estimators can be measured when the weighted sum of the absolute errors is minimised. The weights are dependent on the quantile values. Therefore, the quantile regression can be expressed as

where

Herding behaviour:

Risk-averse behaviour:

where

Results and Discussion

Estimate Impact of CG on Herding and Risk-averse Behaviour

This study designed two different panel data regression models, namely the herding behaviour model and the risk-averse behaviour model, to examine the effect of CG. These models seek to examine extensive data for assessing CG compliance outcomes. For panel data regression, the Hausman test is used to choose between fixed-effect and random-effect models. The fixed-effect model (p < 0.05) adjusts for the impacts of time-invariant factors, while the random-effect model (p > 0.05) assumes no association between individual traits and the dependent variable (Loang & Ahmad, 2021). As anticipated, the hypothesis Hausman test is as follows:

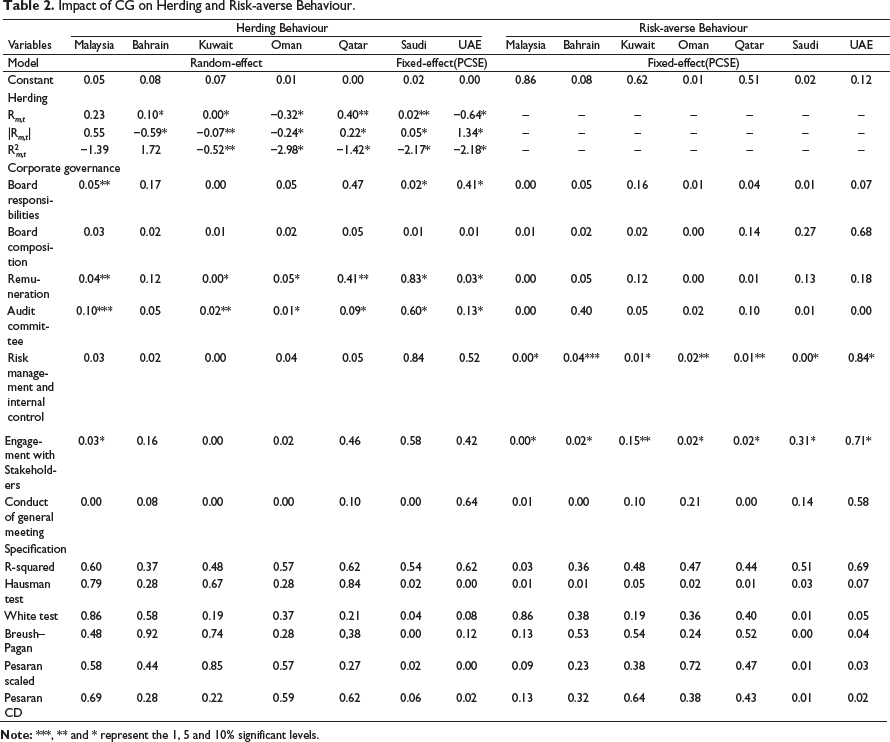

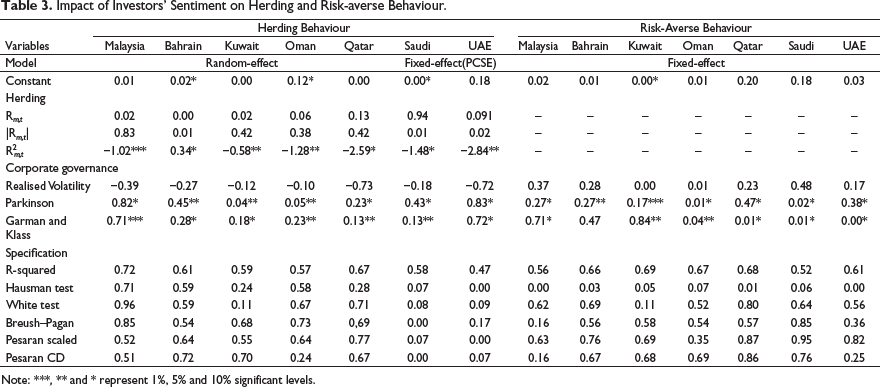

The White test, Breush–Pagan test, Pesaran scaled test and Pesaran CD test are used to identify the presence of heteroscedasticity. These tests determine if the values of the independent variable in the regression influence the variance of the regression errors. When the p-value of heteroscedasticity is less than 0.05, heteroscedasticity is present. This study applies panel-corrected standard error (PCSE) to adjust for heteroscedasticity. Table 2 summarises the impact of CG on herding and risk-averse behaviours. Malaysia, Bahrain, Kuwait, Oman and Qatar use the random-effect model while Saudi and the UAE adopt the fixed-effect (PCSE) model to rectify heteroscedasticity in the herding regression. For the risk-averse behaviour model, Malaysia and GCC countries use the fixed-effect (PCSE) model.

Impact of CG on Herding and Risk-averse Behaviour.

The result presented in Table 2 implies that herding exists with negative values of squared market return (

Apart from that, the risk-averse behaviour model measures investors’ tendency to avoid risk in investment. The result shows that risk management and internal control and engagement with stakeholder are positively and significantly correlated to risk-averse behaviour. It implies that CG can affect the tendency of risk-averse behaviour in the Shariah stocks of Malaysia and GCC. Investors are conservative in trading Shariah-compliant stocks.

The findings are consistent with Almashhadani’s (2021) argument that developing markets have less advanced CG practices than developed markets. Consequently, the effect of CG practices is greater in developed markets. Bahrain is a relatively smaller size market compared to Malaysian and other GCC markets. One possible explanation is the greater market efficiency in developed markets compared to developing markets (Mertzanis et al., 2019). According to the Efficient Market Hypothesis, efficient markets should represent all accessible public and private information. In this context, developing countries, which are assumed to be less efficient, are sluggish to reflect the impact of CG on herding and risk-averse behaviour. Furthermore, the findings show that greater adoption of CG good practices might result in increased stock returns for Shariah-compliant stocks. This argument is supported by the findings of Khaled et al. (2021), who argue that bigger size and more profitable companies tend to have a higher social responsibility and internal controls. One potential reason is that solid CG practices may result in advanced risk management and internal controls that limit enterprise risks, resulting in higher stock prices.

Estimate Mediating Effect of Investors’ Sentiment

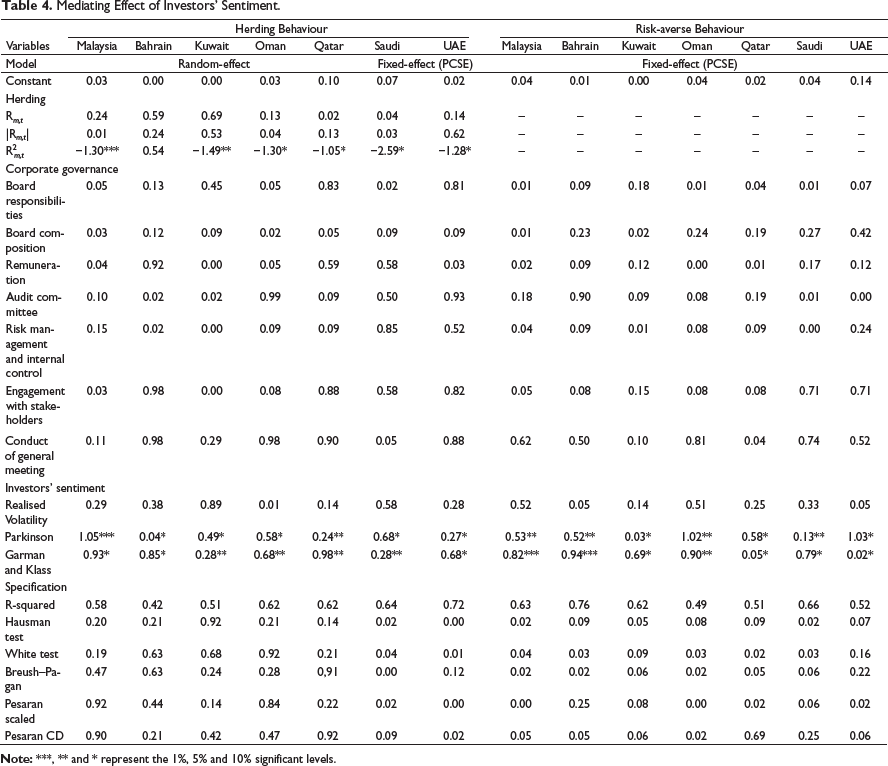

The second objective of this study is to examine the mediating effect of investors’ sentiment on the relationship between CG and herding and risk-averse behaviours. In accordance with Baron and Kenny’s model of statistical mediation (Baron & Kenny, 1986; O’Laughlin et al., 2018), there are three steps to examine the mediation effect in a regression. First, the independent variable (CG) must be correlated to the dependent variable (herding and risk-averse behaviour). It shows that investors herd and risk-averse due to the cause of CG compliance in the market that triggers the investors to react to it. Second, the independent variable must also be proven to impact the mediator variable (investors’ sentiment) significantly. The third step of the Baron and Kenny statistical mediation model is to examine a full mediation effect of the mediator variable. A full mediation process is valid when the independent variable (CG) is no longer affecting the dependent variable (herding and risk-averse behaviour) once the mediator (investor’s sentiment) has controlled the relationship.

Table 3 illustrates the impact of investors’ sentiment on herding and risk-averse behaviour. The result shows that herding exists in the Shariah stocks of Malaysia, Kuwait, Oman, Qatar, Saudi and the UAE with significant and negative coefficient of squared market return. Bahrain is the only market that is found without herding evidence. For the impact of investors’ sentiment, Parkinson and Garman and Klass estimators are significant to herding and risk-averse behaviour in Malaysia and GCC countries. Nonetheless, realised volatility is insignificant. It implies that the investors rely on the previous day’s stock prices as the benchmark to trade. This is because Parkinson and Garman and Klass estimators capture the historical volatility.

Impact of Investors’ Sentiment on Herding and Risk-averse Behaviour.

Table 4 summarises the mediating effect of investors’ sentiment on the relationship between CG and herding and risk-averse behaviours. Herding is persistent in the Malaysia, Kuwait, Oman, Qatar, Saudi and UAE markets. The significant and negative coefficient of squared market return implies that investors trade on the stock herd toward the market return. Surprisingly, the result implies that CG are insignificant by adding the investors’ sentiment to the regression. This is because investors’ sentiment has changed the direction of the relationship between CG and herding and risk-averse behaviour. For investors’ sentiment, Parkinson and Garman and Klass estimators are significant to herding and risk-averse behaviour. It shows that CG has affected the investors’ sentiment, which subsequently influences the existence of herding and risk-averse behaviour. Based on Baron and Kenny’s mediation model, the result implies a full mediation.

Mediating Effect of Investors’ Sentiment.

The result of this study is consistent with Zeidan (2022), in which the author argues that ESG factors affect the sentiment of finance professionals. Most investors have taken CG compliance as part of investment considerations to indicate better corporate governance and social responsibilities. Hence, compliance with CG can lead to a higher tendency of investors’ sentiment that triggers the investors to herd and be risk-averse.

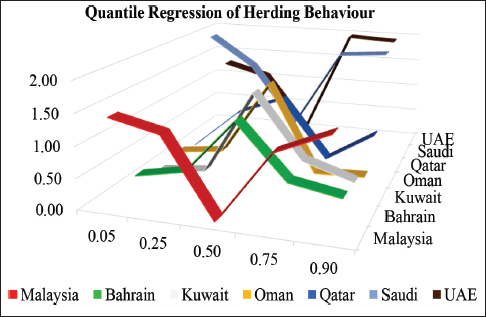

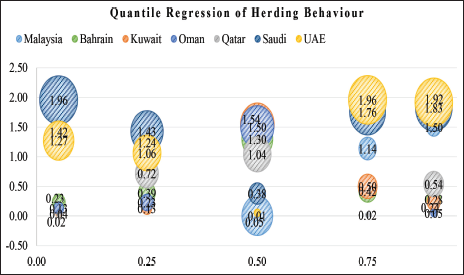

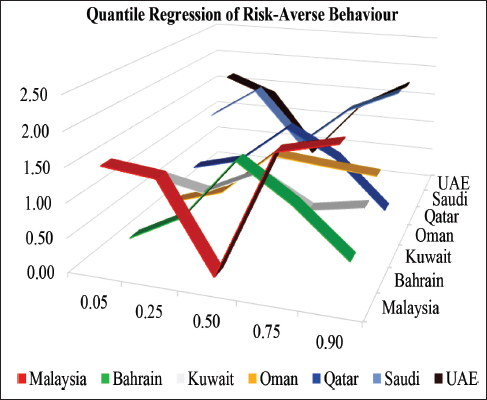

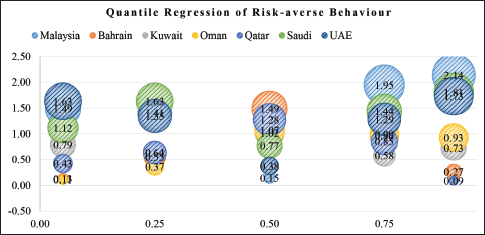

Estimation of Quantile Regression of Herding and Risk-averse Behaviour

For robustness purposes, this study employs quantile regression to examine the impact of CG on herding and risk-averse behaviour in quantiles 0.05, 0.25, 0.50, 0.75 and 0.90. Figure 2 illustrates the impact of CG on the tendency of herding. Figure 3 illustrates the impact of CG on the tendency of risk-averse behaviour. Quantile regression measures the conditional median different from panel data regression to calculate the conditional mean. The result shows that the impact of CG on herding is more pronounced in the lower and upper quantile in Malaysia, Saudi and the UAE at the significant level of 5% and 1%. Bahrain, Kuwait, Oman and Qatar show that herding tends to exist in the median (quantile = 0.5). The herding tendency of Bahrain is lower than in other GCC markets. For risk-averse behaviour, similar evidence is spotted. The impact of CG on investors’ risk-averse behaviour in Malaysia, Saudi and the UAE are stronger in the lower and upper quantile. It implies that investors tend to be risk-averse to the Shariah stocks that comply with the most or least CG practices to safeguard their investment.

Line Chart of Herding Behaviour.

Bubble Chart of Herding Behaviour.

Line Chart of Risk-averse Behaviour.

Bubble Chart of Risk-averse Behaviour.

This finding is consistent with the study of El-Bassiouny and El-Bassiouny (2018), in which they show that the impact of CG is stronger in developed markets than in developing countries, especially under market stress. One potential reason is that CG adoption in developing markets is not as widely accepted as in developed markets. This is because the cost of compliance with CG is numerous for every listed company and the comparison between the incurred costs and benefits of CG adoption cannot be quantified in the financial statement, which is a detriment to shareholders. Hence, the impact of CG on herding and risk-aver behaviours in Bahrain, Kuwait, Oman and Qatar is not as pronounced as in Malaysia, Saudi and the UAE on the distribution’s tails.

Conclusion

This study examines the impact of CG practices on herding and risk-averse behaviour. It also examines the mediating effect of investors’ sentiment on the relationship between herding and risk-averse behaviour. The research timeframe is from 2017 to 2021. The seventeen CG goals are chosen based on the guidelines of the United Nations. For methodology, this study adopts panel data and quantile regressions.

The result shows that herding exists in Malaysia, Kuwait, Oman, Qatar, Saudi Arabia and the UAE. No evidence of herding is detected in Bahrain. Furthermore, remuneration and Audit Committee are significant to stock return. Board responsibility is the only variable of CG that is found to be significant to stock return in Malaysia, Saudi and the UAE. For risk-averse behaviour, risk management and internal control and engagement with stakeholders are positively and significantly correlated. The empirical evidence shows that CG affect the stock return in positive correlations. Compliance with CG can result in higher values in stock return. The result of this study is consistent with Almashhadani (2021) who claims that developed markets have greater compliance with CG practices than less-developed markets. Developed markets also have a higher level of market efficiency to reflect the impact of CG practices in the financial market. Hence, the impact of CG is more pronounced in developed countries.

Based on Baron and Kenny’s mediation model, the result implies a full mediation of investors’ sentiments. By adding the investors’ sentiment in the relationship between CG and herding and risk-averse behaviour, the direction path has changed, and CG is no longer significant to herding and risk-averse behaviour. This is because the CG has caused the changes in investors’ sentiment and subsequently triggered the investors to herd and become risk-averse. Besides, the result shows that Parkinson and Garman and Klass estimators mediate the relationship between CG and herding and risk-averse behaviour. Investors rely on the previous day’s stock price as the trade benchmark. The result of this study is consistent with Zeidan (2022) in which the author shows that ESG affect the sentiment of finance professionals. Most investors have taken CG compliance as part of investment considerations to indicate better corporate governance and social responsibilities.

For robustness, quantile regression is employed, and the result shows that the impact of CG on herding and risk-averse behaviour is more pronounced in the upper (

For theoretical implication, this study contributes to the literature on CG by examining the impact of CG on the tendency of herding and risk-averse behaviours. Investors’ sentiment acts as a mediating variable and provides new insight into investigating the impact of CG on investors’ behaviour. Besides, the findings reveal that the efficient market hypothesis is no longer valid in real life since herding and risk-averse behaviour contradicts the EMH assumptions. EMH believes that investors are rational and that stock prices represent all public and private information. The evidence of herding and risk-averse behaviour in Malaysia and GCC markets shows that investors can be irrational in investment decision-making.

For practical implications, the findings of this research enable policymakers, regulators and practitioners to improve the current CG practices of Shariah-compliant companies. This research highlights the impact of CG in increasing the stock return, herding and risk-averse behaviours. The result encourages the investors to invest in the Shariah-compliant stock due to the prohibition of riba, gharar, suspicious transactions and gambling activities. Besides, Sharish stocks are considered as safer investment choices than conventional stocks. A robust policy should be established to ensure the herding and risk-averse activities are monitored, controlled and regulated to avoid deviation from stock fundamentals. Furthermore, the result of this study can be used as supplemental information for the Corporate Governance Guide to assist the public listed companies in adhering to comprehensive CG practices that can benefit society.

One of the limitations of this study is the lack of data to examine the different behaviours of local and foreign investors in trading the companies with and without the compliance with CG practices. For recommendation, future studies are encouraged to examine the impact of CG in benefiting the financial market and company performances, such as return on assets.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.