Abstract

The Chinese bond market is the world’s second largest, with government bonds accounting for the majority of the market. The Chinese government has been gradually opening up its bond markets to foreign investors since 2015. However, studies on the Chinese bond markets are very few. Based on data of most frequently traded government bonds in 2015 and 2019, statistical tests including Ken-tau tests and variance ratio tests show that while Chinese government bond markets were generally not efficient in 2015, the efficiency has significantly improved in 2019. The change of market efficiency is likely from the increasing foreign investments, thus a more diverse investor base of the Chinese government bonds. Some structural issues remain such as immature derivative market, low marketization of commercial banks, and restrictions to foreign investors. Finally, this study discusses the implications for investors, policymakers and academics.

Introduction

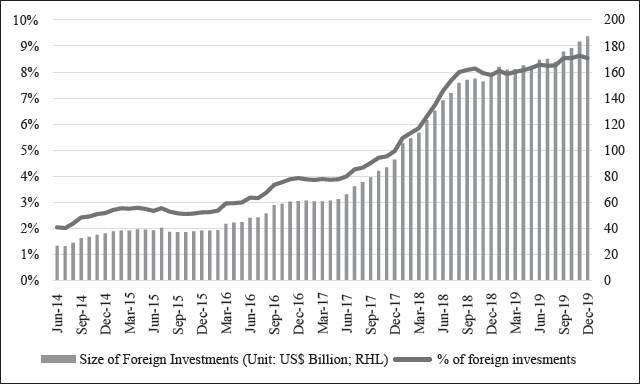

For the development of sophisticated and well-functioning financial markets, the government bond market is critical. Government bonds, for example, often have low credit risk, strong liquidity, a wide range of maturities, and a well-developed market infrastructure, including an active derivative market. Government bonds, rather than private sector securities, may play a larger role in financial markets in this regard. Providing benchmark interest rates for pricing other fixed income instruments, managing financial risk, providing a low-risk, long-term investment vehicle, and functioning as a “safe haven” during periods of financial instability are among the most prevalent roles cited (The Treasury, 2002). As of December 2019, the outstanding notional amount of Chinese bonds has reached RMB 97.1 trillion (equivalent to $13.9 trillion), just second to the United States of America. Among them, Chinese government bonds (excluding local government bonds) represents 17.5%, that is, $2.4 trillion. At the same time, China has further opened up its bond market since 2015. Foreign investors have expanded their investment in China’s government bond markets dramatically from just $26.5 billion in June 2014 to $187.3 billion in December 2019. 1 As argued by Fung et al. (2019), global investors may find additional investment and growth opportunities in China’s bond market.

At the same time, studies on Chinese bond markets including government bond markets are very few, and these studies generally find the Chinese bond markets to be still premature. For example, Porter and Cassola (2011) found that regulation, liquidity, and segmentation all contribute to the inefficiency of Chinese bond yields. Bai et al. (2013) studied the microstructure of Chinese government bond market and concluded that although certain announcements of macroeconomic news have significant effects on yields, the null hypothesis of market efficiency are rejected. Ang et al. (2015) examined China’s local government debt issues, which are separate from the government bond market discussed in this study. Liu (2020a) examined China’s local government bonds, which were transformed from local government debts following the debt-for-bond swap program in 2015, and concluded that the pricing of Chinese local government bonds is still highly regulated. Compared with offshore Renminbi-denominated government bonds, Löchel et al. (2016) found that the market forces play a less important role in determining onshore government bond yield. Luo et al. (2016) also found that as a result of the distorted pricing mechanism, Chinese credit bond market is also immature. By evaluating the risk and return of the Chinese bond markets, Fan et al. (2015) discovered that investors who hold diversified bond portfolios spanning China and the United States are more likely to outperform their peers. This conclusion is not surprising as the Chinese bond markets are traditionally of low correlation with global markets because of its low integration into global markets. Regarding foreign investments, Cerutti and Obstfeld (2018) conducted a cross-country comparative analysis and found that there is substantial room for improving foreign investments in the Chinese bond markets in both size and structure.

This study focuses on the recent developments of the Chinese bond markets especially government bond markets, and the increasing foreign investments, and aims to look at the potential changes which foreign investments have brought. Specifically, the study will conduct standard market efficiency test on the Chinese government bond markets before the substantive increase of foreign investments, that is, in 2015, and after the massive flow of foreign investments, that is, in 2019. If there are any changes regarding market efficiency, they may be attributed to the foreign investments.

The structure of this article is as follows. First, a brief overview on the most recent developments in the Chinese bond markets especially since 2015 including foreign investment are presented. Then, standard market efficiency tests are conducted to see whether there have been substantive changes after the significant flow of foreign investments. Lastly, the conclusions are presented.

Chinese Bond Markets, Government Bond Markets, and Foreign Investment

In China, there are two types of bond markets: over-the-counter interbank bonds and listed exchange-traded bonds. The National Association of Financial Market Institutional Investors and the China Securities Regulatory Commission are in charge of them, respectively. Large institutional investors are the primary participants in the interbank bond market, whereas small and medium-sized institutional investors, as well as individuals, mostly participate in the exchange bond market. However, in terms of contribution to primary issuance and proportion of outstanding bond market value, the interbank bond market is completely dominating (over 90%). 2

As of December 31, 2019, the outstanding notional amount of China’s bond market had reached RMB 97.1 trillion (equivalent to $13.9 trillion), growing 13.4% over the end of 2018. In terms of global comparison, China’s bond market is the world’s second largest, trailing only the United States. Chinese government bonds account for 17.2% of total outstanding notional amount of Chinese bonds. Although Chinese regulatory authorities have been trying to diversify the profiles of bond holders, bond market investments remain highly concentrated with commercial banks. Regarding the government bond market, commercial banks accounted for 65.0% by the end of 2019. The turnover for all Chinese bonds including government bond, local government bond and private bond had reached RMB 213.5 trillion (equivalent to $30.6 trillion) in 2019, growing 36.9% over the end of 2018. In terms of the maturity profiles, 1-year or shorter bond accounts for 25.8% for all Chinese bonds by notional amount as of December 31, 2019. 1–3-year bond, 3–5-year bond, 5–10-year bond and 10-year bond or longer accounts for 28.0%, 19.4%, 21.3%, and 5.5%, respectively. As to government bonds maturity profile, 1-year or shorter bond, 1–3-year bond, 3–5-year bond, 5–10-year bond and 10-year bond or longer accounts for 14.6%, 29.9%, 18.8%, 20.4%, and 16.3% respectively. 3

The Chinese government has implemented a number of policies aimed at progressively opening up the country’s bond market to international investors. The People’s Bank of China (PBC, China’s central bank) issued a notification on July 14, 2015, allowing foreign central banks, monetary authorities, international financial organizations, and sovereign wealth funds to invest in the interbank bond market without approval or quota restrictions (PBC, 2015). On February 24, 2016, commercial banks, insurance companies, securities firms, fund management companies, and other asset management institutions, as well as their investment products, pension funds, charity funds, endowment funds, and other mid-term or long-term institution investors recognized by the PBC, were added to the list of foreign institutions permitted to invest in the interbank bond market (PBC, 2016). The PBC, on the other hand, retains the ability to limit investors whose orientation it deems to be short-term or speculative. The reciprocal bond market access programme between Hong Kong and Mainland China was formed on May 16, 2017 (HKMA, 2017). Through a connection between the Mainland and Hong Kong Financial Infrastructure Institutions, Mainland and offshore investors will be able to trade bonds tradable in the Mainland and Hong Kong bond markets. Northbound Trading will commence first, that is, foreign investors from Hong Kong and other countries and areas would be able to invest in the China Interbank Bond Market through mutual access between Hong Kong and Mainland Financial Infrastructure Institutions in terms of trading, custody, and settlement. Responding to the increasing accessibility to China’s bond market for foreign investors as a result of these further opening-up measures, on March 1, 2017 Bloomberg Barclays Benchmark Fixed Income Index family launched new indices to cover Chinese bonds denominated in RMB (Bloomberg News, 2017). The other two major global bond indices including FTSE Russell World Government Bond Index, and JP Morgan, EM Global Diversified have also included some Chinese onshore bonds (Liu, 2020b). It is part of the Chinese government’s policy of further opening up its domestic markets (Liu, 2020c).

Foreign investors mainly invest in Chinese government bonds, and other types of bond investments are marginal. For example, as of December 2019, foreign investments in Chinese local currency bonds were in total $307.3 billion including $186.7 billion in government bonds, followed by $71.6 billion in policy bank bonds, and $31.1 billion in non-negotiable certificate of deposits. Others including local government bonds are neglectable. Chinese government bond holdings account for 61.0% of all foreign investments in Chinese bond markets, and this fraction has been almost stable since June 2017. Accordingly, this study only considers foreign investment in government bonds. Figure 1 shows foreign investments in the Chinese government bond markets. It indicates that the overall investments from foreign investors in Chinese government bonds have greatly increased from below $40 billion before 2016 to $187.3 billion by December 2019. The shares foreign investors account for have significantly increased from around 2.7% in February 2016 to around 8.5% in December 2019. The main driving factor for this increase is the opening-up measures implemented by the PBC since February 2016. The drop of the share of international investments in the Chinese government bond markets between July 2015 and January 2016 is argued to be because of the RMB depreciation expectation. While the fraction of foreign holdings is still below developed markets such as the US and Europe (30–40%) (Guo, 2019), China is comparable to some Asian economies such as Korea (11.9%, as of Q2, 2019) and the Philippines (4.9% as of Q2, 2019). 4

Efficiency Tests on Chinese Government Bond Markets

An efficient financial market is “one in which prices always fully reflect available information” (Pilbeam, 2005). An efficient financial market means that funds are channeled from ultimate lenders to ultimate borrowers/users in the most socially and economically beneficial way possible. So, the question whether the Chinese government bond markets are efficient matters to both investors (whether prices fully incorporate available information) and Chinese economy (whether funds are used efficiently).

This study will be based on Bai et al.’s (2013) approach by employing Kendall Tau test and the variance ratio test to test the efficiency of Chinese government bond markets. While Bai et al. (2013) is based on a much early period of data between April 1, 2009 and December 31, 2011, this study uses recent data sets between January 1, 2015 and December 31, 2015, and January 1, 2019 and December 31, 2019. Furthermore, this study uses dirty prices, that is, prices that include accrued interest.

Kendall’s Tau is a non-parametric measure (a statistical method wherein the data is not required to fit a normal distribution) of relations between columns of ranked data, where sorting the data into order and substituting each value with its related place in the order determines the ranks. For example, assume the original data set contains the following values: 1.8, 2.5, 2.2, 3.3, 2.7. In sorted order, the values are: 1.8, 2.2, 2.5, 2.7, 3.3. The relative placements of these values take their place: 1 2 3 4 5. The new dataset (column of ranked data) will become 1, 3, 2, 5, 4. Accordingly, another column of ranked data can also be obtained. The Tau correlation coefficient has a range of –1 to 1 as a value, where: –1 is 100% negative association, 0 is no relation, and 1 is 100% positive association (Agresti, 2010).

Campbell et al. (1997) and Bai et al. (2013) concluded that whether the series has independent increments can be assessed by their daily returns {rt} to see if bond prices follow a random walk. The null hypothesis is that the Kendall Tau-b coefficient for rt and rt–1 is equal to zero.

Kendall Tau Test—2015.

The Kendall Tau test findings are shown in Table 1. Within a 5% confidence level, the null hypothesis that the daily return follows a random walk is rejected, but it cannot be rejected within a 10% confidence level for 7-year and 10-year bonds.

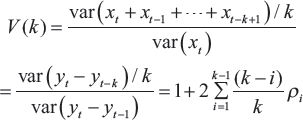

The variance ratio test is frequently used to determine whether a time series or its first difference (or return), xt = yt yt–1, is made up of independent and identically distributed observations or follows a martingale difference sequence. The hypothesis is that the variance of random walk increments must be a linear function of the time interval (Charles & Darné, 2009)

The variance ratio of the k-period return is defined as:

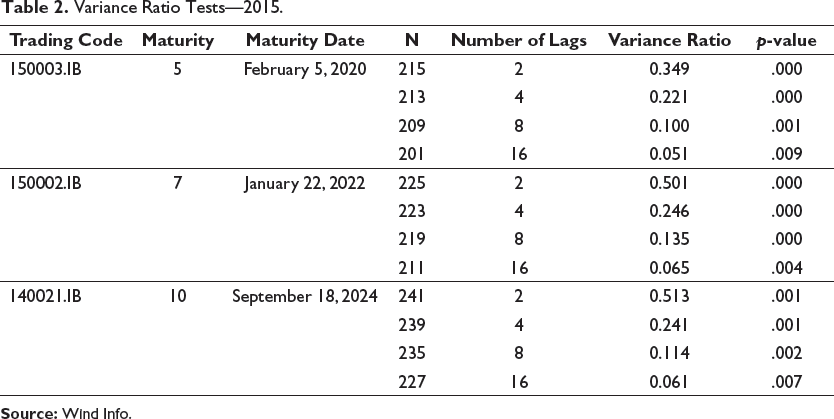

Variance Ratio Tests—2015.

Table 2 indicates that at the 1% confidence level, the null hypothesis is rejected for all bonds with lag orders of 2, 4, 8 and 16, suggesting that the returns exhibit significant serial correlations.

Based on the datasets in 2015, the empirical results from variance ratio tests show that Chinese government bond markets were inefficient in 2015 although Kendall Tau tests show a different result for the 7-year and 10-year bonds.

Kendall Tau Test—2019.

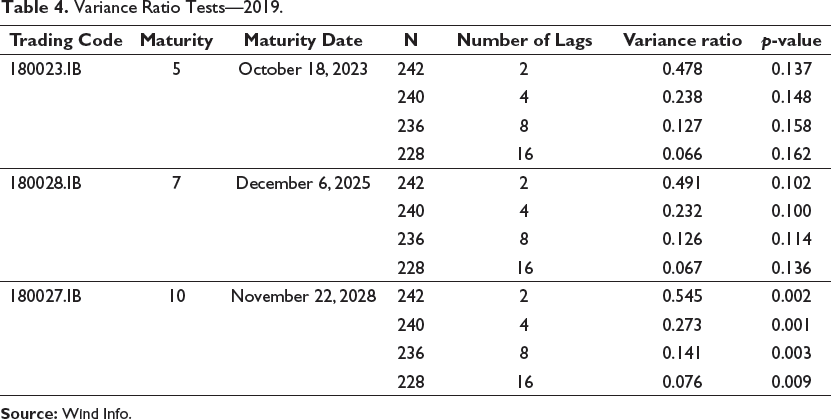

Variance Ratio Tests—2019.

The Kendall Tau test findings are shown in Table 3. For all bonds, the null hypothesis that the daily return follows a random walk cannot be rejected within a 10% confidence level. Table 4 further indicates that for 5-year and 7-year bonds, the null hypothesis cannot be rejected within a 10% confidence level across all lag orders, but not for the 10-year bond.

In short, the Chinese government bond markets in 2019 were almost efficient. This is a sharp contrast to 2015, when the Chinese government bond markets were almost inefficient.

Many factors may have contributed to this change. According to Xu (2020), during the past couple of years, the Chinese government bond market has made some progress in several areas including government bond market-making mechanism, government bond derivative market, government bond yield curve, and opening-up to foreign investors. Regarding government bond market-making mechanism, it has been in existence since 2011. Thus, the policy initiative launched in November 2016 may not be substantial. The major breakthrough in reforming the government bond derivative market is the approval of 2-year government bond futures in 2018 (Xinhua News, 2018). Furthermore, while the first issuance of 3-month and 6-month government bond yield in 2015 (State Council, 2015) is helpful in building a government bond yield curve, it may not be regarded as being significant. In short, as discussed previously, the major game-changing policy initiative is the “opening-up to foreign investors.”

From 2015 to 2019, China’s economic environment has substantially changed. For example, from November 2015, the Chinese government initialized the “supply-side structural reform” (Liu, 2019). Official realization that Keynesian demand-side policies had run their course prompted the reform process. Specifically, Liu (2019) found that China’s overcapacity issues from steel and coal industry had been significantly relieved. Furthermore, its new positioning of “real estate being for living in not for speculation” has curbed the speculation. Even under the pressure from the US–China trade war, according to Liu (2020c), the Chinese government’s policy focus has shifted from traditional demand-side economics (such as the stimulus programs of 2008–2009, 2012 and 2015–2016) to supply-side economics (such as the 2018–2019 stimulus). Simultaneously, while China’s debt issue has drawn widespread attention from investors and China watchers across the world, and prior studies have typically indicated that China’s credit crisis is imminent, the Chinese authorities have been systematically dealing with the issue since 2016. According to Liu (2021), some progress has been made in deleveraging the Chinese economy, particularly in the non-financial corporate sector and the finance corporate sector. The fundamentals of the Chinese economy have improved during 2015–2019.

As a result of improving economic fundamentals together with significantly lifting restrictions on foreign investors, the Chinese government bonds have become more attractive in terms of enhancing return and/or reducing risk. As more and more foreign investors enter the Chinese government bond markets, the increasingly diverse investor base of the Chinese government bonds has become the most important institutional change during 2015–2019. As WB and IMF (2001) argued, a diversified investor base is necessary for market stability and efficiency. Furthermore, a varied investor base reduces the risk of an issuer being held captive by a small number of investors. Specifically, first, foreign investors can help deepen the liquidity and extend maturities of government bond markets. Foreign institutional investors can generate additional liquidity through advanced trading and investment strategies in the form of arbitrage activities and investor portfolio diversification. Foreign institutional investors can also help extend the maturity of government bonds. Responding to requirements from different types of investors, China has gradually increased its issuance of super-long maturity bonds (Xu, 2020). Second, foreign institutional investors can bring extra competitions, promoting innovation and enhancing productivity. Domestic investors may easily absorb and develop the sophisticated trading and investment techniques used by foreign investors. The WB and IMF (2001) cited the emergence of guaranteed return mutual funds as an example of foreign investor innovation in the Spanish government bond market. The WB and IMF (2001) also claimed that a variety of market innovations, ranging from floating-rate and zero-coupon bonds to inflation and foreign-currency-linked products, were produced to fulfil the needs of various types of investors. Porter and Cassola (2011) also argued that the introduction of foreign participants may improve bond market liquidity since these participants are likely to pursue different trading strategies from the current participants.

As discussed before, the fraction of foreign ownership of the Chinese government bonds has significantly increased. This figure has increased from 2% in June 2014 to 8.5% in December 2019 and has become comparable to other Asian economies. Liu (2020b) especially examined the determinants of foreign investments in the Chinese government bond market, and found that foreign investors’ trading strategies have been evolving. For example, initially the main foreign investors were central banks and similar institutions, and they primarily considered strategic factors rather than pure return or risk factors during June 2014 to July 2016. As more institutional investors entered the Chinese bond markets, the considerations of enhancing returns and/or reducing risks became more significant during August 2016 to October 2017. Since November 2017, these new foreign institutional investors began to pursue price change rather than hold the bond investments for yield change. These investment strategies are different from those adopted by Chinese commercial banks and insurance companies, which tend to hold the government bonds to maturity. As a result, Chinese government bond market’s liquidity has deepened, and market efficiency improved. For example, China’s quarterly government bond turnover ratio (defined as the ratio of value of bonds traded over average number of bonds outstanding) in Q1, 2015 is 0.34. This figure has significantly increased to 0.75 in Q3, 2019, the highest during 2015–2019. 5

At the same time, there are also a series of structural issues with Chinese government bond markets. More specifically these are as follows.

First, Chinese commercial banks (followed by insurance companies) are the main participants in the Chinese government bond markets, and the degree of marketization of commercial banks in China is still very low. In October 2015, the interest rate liberalization procedure was completed. However, the interest rate channel is limited (Liu, 2019). So, commercial banks in China still rely mainly on benchmark deposit/lending rates announced by the PBC as the basis for pricing. 6 While the government bond yield curve is supposed to respond to monetary policy signals and transfer monetary interventions to the real economy through changes in the yield curve’s level, slope, and curvature (Dewachter & Lyrio, 2006), the commercial banks in China are less concerned about the change of government bond yield.

Second, while derivative securities can improve market efficiency for the underlying assets, the derivative market for Chinese government bonds is still immature. For example, there are only 2-year, 5-year and 10-year government bond futures. Other government bonds do not have corresponding future products and markets. Furthermore, because foreign investors are not permitted to trade Chinese government bond futures, they are unable to completely manage their investment risk (Guo, 2019). Moreover, the longest term for the interest rate swap is only 5-years. Many market participants can only choose to either hold the assets to maturity, or adjust the holdings in the spot market. The market will take longer to eliminate arbitrage opportunities.

Third, Chinese commercial banks and insurance companies tend to hold the government bonds to maturity, which limits the liquidity. Most developed-economy banks define less than 10% of bond investments as held-to-maturity, whereas Chinese commercial banks classify roughly 60% of bond investments as held-to-maturity (Adrian et al., 2019). Furthermore, their investment styles tend to converge, which negatively affects the price discovery function of the bond yield curve. The government bond yield curve may only reflect a certain fraction of investors’ expectation.

Fourth, as argued by Guo (2019), for foreign investors, there are still a number of restrictions on some types of bond transactions. Foreign institutional investors, for example, have access to bond borrowing and lending, as well as forwards and interest rate swaps. These transactions are only possible if they can demonstrate the presence of underlying risks. Furthermore, while bond repurchase (repo) is a popular bond transaction and money market product, it is restricted to foreign central banks, clearing banks, and overseas participant banks; other institutional investors are not permitted to participate.

Conclusion

China’s government bond markets have grown to become the world’s second largest, and Chinese officials have continued to open up the market since 2015. This article studies market efficiency and gives some stylized facts on the most recent trends in the Chinese government bond market. According to the results of the Kendall Tau-b test and the variance ratio test, the Chinese government bond markets were usually inefficient in 2015, but have become almost efficient in 2019. The key driver of the transition is a growing diversity of investor profiles, as foreign investors have boosted their investments in onshore Chinese government bonds significantly. At the same time, some structural issues with Chinese government bond markets remain including—immature derivative market, low marketization of commercial banks, and foreign investors are subject to a number of restrictions on certain types of bond transactions.

Quantitative analyses of the benefits and costs of foreign participation in bond market development are rare due to a lack of data (Daniel, 2008) especially in emerging markets (Peiris, 2010). To the best of the author’s knowledge, no studies have empirically tested the relation between foreign investments and local bond market efficiency. As a result, this study adopts a qualitative approach (such as WB and IMF, 2001). While it would be ideal to perform an empirical study, this study mainly relies on economic logic. The rationale is as follows: first, the study finds that the efficiency of the Chinese government bond markets has improved during 2015–2019; second, the next reasonable conclusion is that some factors must have played a significant role in this shift; third, this study reviews the developments of the Chinese government bond markets during this period, and finds that the major game-changing policy initiative is the opening-up to foreign investors; fourth, supported by some evidence such as on liquidity and trading strategies, this study finally concludes that foreign participants may have helped the improvement of market efficiency.

From the viewpoint of investors, the improvement of the efficiency of the Chinese government bond markets shows the significant roles foreign investors have played during the past couple of years. At the same time, the Chinese government bond market is still not fully efficient (such as the 10-year government bond). Foreign investors can further potentially exploit this inefficiency to obtain attractive yields. The fierce competition among investors to profit from any new information is the primary reason for the existence of an efficient market. The ability to spot overpriced and underpriced securities is quite useful. As a result, many investors devote a large amount of time and effort to spotting mispriced securities (Clarke et al., 2001). Naturally, as more and more foreign investors enter the Chinese markets, they would go head-to-head to take advantage of overvalued and undervalued assets. As a result, the chances of finding and using such mispriced assets grow increasingly slim. This current (partial) inefficiency, and the further opening up of Chinese government bond markets are a good opportunity for foreign investors.

From the viewpoint of policymakers, Guo (2019) made a number of recommendations to the Chinese authorities, including allowing foreign investors more access to various types of bond transactions and increasing their share of participation; increasing market liquidity and improving risk management tools; and allowing foreign investors more access to different types of bond transactions and increasing their share of participation; putting in place a custodial system that adheres to international standards; further simplifying foreign institutional investors’ account opening procedure; creating a convenient institutional environment in areas such as accounting and auditing, tax, legal issues and rating agencies; and improving management of cross-border capital flows.

From the viewpoint of academics, the Chinese bond markets including government bond markets are a potential gold mine for future research. They are developing very fast, and have increasingly attracted attentions from global investors. At the same time, serious research are few and interesting topics are just too many.

Footnotes

Acknowledgements

The author would like to thank Professor Kevin Davis from the University of Melbourne, and an anonymous referee for very valuable comments on an earlier version of this article. All errors are the author’s sole responsibility.

Declaration of Conflicting Interests

Funding

The author received no financial support for the research, authorship and/or publication of this article.