Abstract

Academic and popular literature suggest that multinational companies are more likely to be attracted to democratic regimes; they are generally seen as more reliable in honoring contracts compared to their undemocratic counterparts. On the flip side, some scholars claim that autocratic governments guarantee lower costs as they can more effectively suppress labor rights and are easier to negotiate with. Despite the existence of evidence for both claims, when all the arguments are considered, it is seen that the most attractive countries for foreign direct investment (FDI) have stable regimes and, hence, are predictable. This article aims to question the proposed relationship between democracy and FDI inflows and argue that the stability of the regime is what matters. Using a sample of developing and least-developed countries from 1970 to 2022, the study demonstrates that a fast-changing political decision-making environment is negatively associated with FDI inflows, while political regime variables do not have any significant impact on developing countries.

Introduction

Since the 1980s, the world has witnessed a remarkable increase in capital mobility, a level unseen since World War I. This period has also seen many countries transition to democratic regimes. As foreign capital inflows and outflows became increasingly crucial for the economic prosperity of developing countries, foreign direct investment (FDI) emerged as a key driver for enhancing production capacities and transferring technological knowledge. Consequently, governments began competing to create more favorable environments for foreign companies. These developments, alongside the growing emphasis in the economic literature on the importance of institutions, spurred researchers to explore the relationship between capital inflows and political regimes. Discussions about which political framework best allows foreign companies to maximize profits extended beyond academic circles and into public debate.

A strand of empirical research has shown that democratic regimes create a more favorable environment and explored the underlying mechanisms behind this effect (Choi & Samy, 2008; Jakobsen & de Soysa, 2006; Jensen, 2003, 2008; Li, 2006, 2009; Sinha et al., 2024). These studies focused on check and balance mechanisms that characterize democratic systems, which make abrupt policy changes difficult. The argument, rooted in North and Weingast’s (1989) work, posits that institutions that limit sovereign power foster credible commitments to agreements. In democratic regimes, the presence of veto players and audience costs that governments face during policy changes contributes to a stable and predictable environment for multinational companies.

Conversely, earlier literature suggested that multinational companies prefer authoritarian regimes because they are more effective at suppressing labor rights (Haggard, 1990; O’Donnell, 1978). More recent studies support that democracies guarantee better conditions for labor class (Robertson & Teitelbaum, 2011; Wang, 2017). They also follow antitrust regulations more frequently (Li & Resnick, 2003). Yet, empirical studies generally show no evidence for an inverse relationship between democracy and FDI. Although Oneal (1994) shows that the returns on investments made in authoritarian countries were higher, he could not show evidence of the relationship between authoritarian regimes and the destination of US-based FDI.

Recent research has explored how authoritarian regimes can also create favorable conditions for foreign companies. While the time horizon of the ruler is an important determinant (Cui & Moon, 2020; Moon, 2015), legislatures (Moon, 2019) or local governments (Zheng, 2011) can all signal the government’s commitment as well. Additionally, international investment agreements have the potential to substitute weak domestic commitment mechanisms (Arias et al., 2018; Bastiaens, 2016; Rosendorff & Shin, 2012). These findings suggest that mechanisms typically assumed to be exclusive to democracies can also develop within authoritarian regimes.

This study argues that the only factor establishing the relationship between the political regime and FDI is predictability. Both democratic regimes and authoritarian regimes can create a favorable environment for the operations of multinational companies as long as the political decision-making environment is stable. This study conceptualizes stability as the stability of the existing political regime. Regardless of the regime type, if there is a persistence in the characteristics that define the political regime, and if rapid changes do not occur, this is defined as stability. I provide evidence for my argument that stability is what really matters using panel data econometrics and a sample of developing and least-developed countries between 1970 and 2022. Empirical results indicate that in developing countries, the nature of the political regime has no significant impact on FDI inflows, regardless of the democracy index used. On the other hand, in least-developed economies, the level of democracy is negatively associated with investment inflows. The democratic political institutions in least-developed countries are not sufficiently developed to create a stable environment. Moreover, a fast-changing political decision-making environment lowers the expected profit of multinational corporation (MNC) operations by adding unforeseen costs, so it reversely affects the FDI inflows.

This study contributes to the literature by critically reassessing the common view that democracy is inherently more favorable for attracting FDI. This study challenges this assumption by demonstrating that the key determinant of FDI inflows is not democracy as such but rather the consistency and predictability of the institutional and political environment. By emphasizing the importance of institutional and policy continuity, this study offers a refined perspective on the political factors influencing FDI and the conditions under which democratic and authoritarian regimes can support a favorable investment climate.

The remainder of the study is structured as follows: The following section traces the literature on the relationship between the political regime and FDI inflows. In the sequel, the next section introduces the econometric methodology and the dataset. The subsequent section reports the estimation results and the discussion of the findings. The study concludes with final remarks.

Literature Review

The assumption that democratic institutions create an attractive environment for foreign investors is based on the idea that countries with such institutions offer stronger protection of property rights. Since political constraints make policy changes more difficult, violations of property rights against foreign investors are observed less frequently (Li, 2009). One contributing factor is the greater number of veto players in democratic countries. A veto player is an individual or collective actor whose approval is required for a policy change (Tsebelis, 1995). Depending on the political system, these actors may include institutional figures such as constitutional courts, senates, presidents, or monarchs, as well as coalition partners. The greater the number of veto players, the harder it becomes to introduce policy changes that could undermine predictability. Additionally, having multiple veto players provides MNCs with more access points to influence policymakers (Kim & Milner, 2020). Another factor making democratic regimes attractive for foreign investment is audience costs, which make policy changes more difficult for democratic governments. This increased policy stability, in turn, enhances the appeal of these countries to foreign investors (Jensen, 2003).

However, the positive impact of veto players on foreign investment is conditional. If the political environment of a country is favorable to foreign investment, the presence of veto players will encourage investment. Otherwise, their presence will not necessarily provide additional security for investors (Roberts, 2018). Moreover, this relationship is not necessarily linear. According to Zheng (2011), in the absence of veto players, frequent policy changes create uncertainty, which deters foreign investment. However, too many veto players can also reduce policy flexibility, preventing governments from adopting investor-friendly policies when needed. Furthermore, in a favorable economic climate, a high number of veto players enhances predictability and attracts foreign investors. In contrast, under unfavorable economic conditions, having too many veto players reduces policy flexibility, slows down necessary policy adjustments, and ultimately creates a less favorable environment for investors.

According to O’Donnell (1978), authoritarian regimes create a more favorable environment for FDI because they can effectively suppress labor rights. A more recent study by Robertson and Teitelbaum (2011) finds that countries with democratic regimes experience more worker strikes than countries with authoritarian regimes. Additionally, Wang (2017) shows that democratic regimes are better at protecting labor rights. Li and Resnick (2003) argue that antitrust regulations are more frequent in democratic countries, and firms that lose market share to foreign firms can more easily influence governments to act in their favor in democracies. So, they claimed that authoritarian countries carry certain advantages. Li and Resnick also showed that when property rights are controlled for, a negative correlation is observed between democracy and FDI inflows. However, Jakobsen and de Soysa (2006) suggest that firms losing their market share might have more influence over authoritarian governments, leading to policies that oppose foreign investment, which is considered beneficial for the majority. They also argue that Li and Resnick’s (2003) findings resulted from sample bias and demonstrated that democracy actually increases FDI inflows. Oneal (1994) found that the regime type does not influence the destination of US-based FDI, but the returns on investments made in authoritarian countries were higher. Li (2006) also showed that there are more incentives for foreign companies in non-democratic countries, but he claimed this is due to the weakness of institutions that secure property rights. Since these institutions do not ensure reliability, governments in these countries need to offer more incentives.

Choi and Samy (2008) argued that neither the empirical strategies used by Li and Resnick (2003), who claimed that foreign firms have the opportunity to become monopolies in authoritarian countries, nor those by Jensen (2003), who argued that democracies are attractive due to veto players and audience costs, could sufficiently prove their theories. This is because the democracy indices used in both studies do not proxy the channels they proposed. Furthermore, audience costs can only arise in the presence of free media, as free media can be a voice of opposition to government policies that are hostile to foreign investment. Choi and Samy’s (2008) findings did not support the audience cost argument or Li and Resnick’s (2003) findings but did show that veto players are important for foreign investment.

Dang (2015) demonstrated that the findings suggesting foreign investments flow more to democratic countries are due to sample bias. According to Dang, firms prefer to invest in countries with legal frameworks similar to the framework in their home countries when deciding where to invest. Since FDI is often conducted by firms from democratic countries, econometric findings are biased to show that democratic regimes attract more capital inflows. After controlling for the bias using a Heckman-type method, Dang concluded that the political regime is not a determining factor. Similarly, Cezar and Escobar (2015) found that the greater the institutional differences between their home country and the host country where they intend to invest, the lower the likelihood of investment and the amount of investment.

While democratic institutions are often seen as key mechanisms for ensuring credible commitments to foreign investors, another line of research shows that authoritarian countries can also establish commitment institutions. Olson (1993) notes that dictators’ time horizons influence their actions—a stationary bandit, who expects to remain in power for a long time, has a greater incentive to protect property rights than a roving bandit, who extracts resources opportunistically. Building on this idea, Moon (2015) finds that authoritarian leaders with long time horizons and a low risk of being overthrown can create strong institutions that safeguard property rights. Institutions within authoritarian regimes can also function as veto players, limiting arbitrary policy changes and increasing investor confidence. Moon (2019) finds that authoritarian countries with legislatures attract more FDI than those without, since legislatures serve as commitment mechanisms. Similarly, Cui and Moon (2020) demonstrate that dictators with long time horizons are more likely to sign bilateral investment treaties (BITs), which signal credible commitments to foreign investors. Zheng (2011) provides further evidence from China, showing that local governments act as constraints on the central government, preventing arbitrary expropriation of foreign assets. Additionally, authoritarian regimes become more attractive to investors when the ruling elite’s interests align with those of foreign businesses (Li, 2006).

Beyond domestic institutions, international agreements can substitute for weak domestic commitment mechanisms in authoritarian countries. Since property rights institutions are often underdeveloped in such regimes, BITs provide foreign investors with a sense of security (Arias et al., 2018). As a result, authoritarian governments are more likely to sign these agreements, and their impact on FDI inflows tends to be stronger than in democratic contexts (Rosendorff & Shin, 2012). The time horizons of authoritarian leaders further shape their likelihood of entering such agreements. Bastiaens (2016) argues that, for authoritarian regimes, BITs serve as an important signal of liberal economic policies. However, the credibility of these commitments is greater in authoritarian states with some degree of public debate culture, as this creates pressure for compliance.

In short, these findings challenge the assumption that only democracies can ensure credible commitments to foreign investors. Authoritarian regimes, particularly those with long-term stability, veto players, and strong international agreements, can also provide investment-friendly environments.

The vast majority of studies in the literature focus on the expropriation of investments as the primary risk faced by foreign firms. However, expropriation is not the only political risk associated with foreign investments. Other risks include the imposition of new taxes on foreign companies and restrictions on profit transfer. As an exception, Graham et al. (2015) consider restrictions on profit transfers as a political risk and find that political constraints do not significantly affect the profit transfer restriction risk. According to the authors, the main difference between transfer restrictions and expropriation is that expropriation is more visible and noticeable. Transfer restrictions are more technical and are often claimed by governments to be temporary. In addition to such policy changes that directly impact foreign investments, there are also macroeconomic policy changes that indirectly affect the profitability of investments, posing another risk. For example, a sudden devaluation of the national currency or, conversely, an excessive appreciation of the currency due to a policy change can impact the profitability of investments in that country. Another example is when a government increases the minimum wage to boost its popularity during an election period; this often leads to higher costs for foreign firms operating in that country. Therefore, the anticipation of election-driven economic policies can also influence these firms’ decisions to invest. In conclusion, uncertainty about the government’s future macroeconomic policies is a deterrent for foreign firms. The relationship between political regimes and foreign investment inflows should also be discussed within the context of these risks.

Both democratic and authoritarian regimes offer unique advantages for foreign investment, primarily through their impact on predictability and stability. A stable regime reduces uncertainty and provides a better investment environment. 1 Ahlquist (2006) demonstrates that countries with more stable political frameworks attract more foreign investments. Resnick (2001) found that both instability and transitions to democracy decrease capital inflows due to higher labor costs and regime change uncertainty in democratic countries. Lacroix et al. (2021) examined the impact of transitioning to democracy in 115 developing countries, concluding that while uncertainty is high immediately after the transition, FDI increases on average after about 10 years. Goldsmith (2021) highlights that the usage of econometric techniques in various studies showed conflicting results, suggesting that case studies of similar countries might provide more reliable results. His analysis of four pairs of similar countries in Africa finds no significant difference in FDI between countries that transitioned to democracy and those that did not.

Elections, like regime changes, can also introduce uncertainty, affecting investment decisions. Julio and Yook (2016) found that US companies reduce investments before elections in host countries due to uncertainty and increase the investment volume afterward. Chen et al. (2019) showed that uncertainty during elections leads to reduced FDI, while a developed democracy hinders this effect. Rooney and DiLorenzo (2021) argued that not only the expectation of government changes but also the formation of new coalitions impact investment behavior, with democratic regimes reducing uncertainty more effectively than non-democratic ones. In summary, the relationship between political regimes and foreign investment is influenced more by stability and predictability than by the regime type per se. Effective governance and predictable policies, regardless of whether a country is democratic or authoritarian, are crucial for minimizing investment uncertainty.

Method and Data

This study utilizes a panel dataset that covers developing and least-developed countries from 1970 to 2022. Countries are classified by development level according to UNCTAD standards.

2

As many country-specific unobservable variables and international economic cycles affect the FDI flows, both country effects and time effects are included in the model. The sample covers a specific group of countries and a specific period; therefore, two-way fixed effect regressions are appropriate. The nature of the study and the Hausmann test require the inclusion of two-way fixed effects. Driscoll–Kray standard errors (Driscoll & Kraay, 1998) were calculated, which are robust to autocorrelation, cross-sectional correlation, and heteroskedasticity. The model to be estimated is given in the following equation:

where FDI is the net inflow of FDI as a share of gross domestic product (GDP), democracy is proxied using different continuous indexes, and instability measurement is explained below. While X represents the vector of control variables,

The dependent variable is FDI inflows. GDP shows the market scale, and as the market scale increases, foreign investment naturally increases (Tsai, 1994), which can be observed in many other economic variables. To eliminate this scale effect, considering net FDI inflow as a share of GDP would be an appropriate approach.

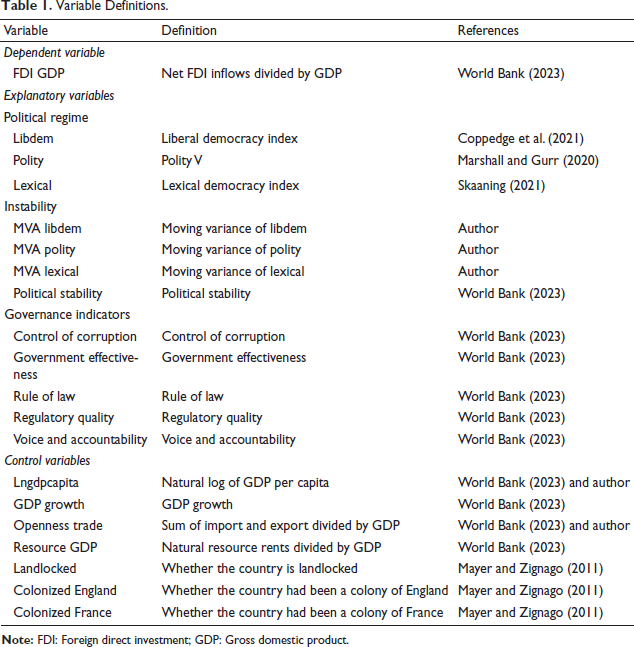

There are different indices to measure the political regime. This study uses the liberal democracy index from the varieties of democracy (V-DEM) project by Coppedge et al. (2021). Polity V (Marshall & Gurr, 2020) and the Lexical index of democracy (Skaaning, 2021) were included as robustness checks. The World Bank Governance Indicators (Kaufmann et al., 2011) were also used as explanatory variables to check the robustness of the findings to show the effect of institutions, although they do not directly indicate the regime score.

Political stability is a complex phenomenon that is challenging to measure directly. Consequently, it requires the use of proxy variables to represent instability. In this article, stability is conceptualized as the stability of the existing political regime. Regardless of the regime type, if there is continuity in the characteristics that define the political regime, and if abrupt changes do not occur, this is defined as stability. Conversely, any change in the quality of the existing regime, whether it is a categorical change or not, implies a change in the political decision-making environment, indicating instability in the political regime.

To measure this instability, the 5-year moving variance of the regime index as a proxy variable was calculated. The moving variances of three different democracy indices have been calculated for this purpose. This method of measuring instability was previously utilized by Resnick (2001) and Ahlquist (2006). It is hypothesized that a fast-changing political decision-making environment increases uncertainty, which in turn leads to a decline in FDI inflows. Consequently, the parameter estimate is expected to be negative. Additionally, to demonstrate the robustness of the findings, the political stability variable from the World Bank’s governance indicators, which covers a shorter time span, has also been employed. The parameter estimate for this variable is expected to be positive. Table 1 shows definitions of variables.

Variable Definitions.

Control Variables

GDP per capita is commonly used as a control variable because it reflects a country’s level of development. A country’s development status can influence the flow of FDI in several ways. Higher levels of foreign investment are expected in more developed countries, where necessary infrastructure investments have already been made and more qualified human capital exists. Additionally, since the level of development also indicates the purchasing power of a country’s citizens, foreign firms targeting the domestic market might prefer more developed countries due to the favorable demand conditions. On the other hand, in more developed countries, higher wages and stricter regulations might create a negative relationship between the level of development and foreign investment, especially if the investment is export-oriented rather than domestic market-oriented. GDP growth, which indicates the dynamism of economic activity in a country, may attract foreign firms seeking new profit opportunities in growing economies.

Another crucial control variable in analyzing FDI is trade openness, which is calculated by dividing the sum of a country’s exports and imports by its GDP. This variable serves as a key de facto indicator of a country’s trade policies. Multinational companies targeting domestic markets may avoid investing in countries with high trade openness, as they can access these markets through trade and face intense competition. However, in the current era of globalization, FDI is increasingly driven by the motivation of global value chain integration rather than solely targeting domestic markets. Therefore, a country’s trade openness signals that investing companies will not face barriers in importing raw materials and intermediate goods, nor in exporting the finished products. Moreover, countries engaged in large-scale trade are likely to be more cautious about violating property rights related to foreign investments, as a high volume of trade serves as a commitment mechanism. International institutions can “punish” governments through trade channels, making such countries more attractive to multinational companies. Trade openness as a variable has been included in many studies examining the impact of political regimes on FDI, often revealing a positive relationship. The role of trade in facilitating FDI has been demonstrated by Büthe and Milner (2014), who found that reciprocal trade agreements create a credible commitment mechanism, leading to increased investments.

The ratio of natural resource rents to GDP is included as a variable to control for the effect of a country’s natural resource wealth on FDI. Generally, a positive relationship is expected, as resource-rich countries are often attractive to investors. However, a negative relationship may also emerge. According to Asiedu and Lien (2011), the natural resource sector can crowd out foreign investment in other sectors. Besides, since extractive industries typically require significant fixed investment only at the beginning and subsequently focus on profit transfers, net capital inflows to resource-rich countries may be lower.

Geographic factors also influence firms’ choice of countries for investment. To control for these effects, dummy variables indicating whether a country is landlocked and its continental location have been included.

At the beginning of the twentieth century, most of the least-developed countries were colonies of European powers, with Britain and France being particularly prominent. Studies focusing on the international economic relations of developing and underdeveloped countries must account for the lasting effects of colonialism. 3 To this end, two dummy variables were used: one indicating whether a country was a former British colony and the other whether it was a former French colony. Colonialism often allowed Western companies to establish monopolistic positions in least-developed countries. Svedberg (1982) demonstrates that British companies earned higher profits in former British colonies, with profit rates declining after independence. In regions like Latin America, where competition among imperial powers was higher, profits were lower. Continued diplomatic relations with former colonies (e.g., the Commonwealth) and the ongoing privileges of Western companies may lead to sustained capital flows from these countries to their former colonies (Glaister et al., 2020). Additionally, the construction of similar institutions and the common language between former colonial powers and their ex-colonies can reduce transaction costs for investments. The validity of these effects will be tested using the colonial dummy variables.

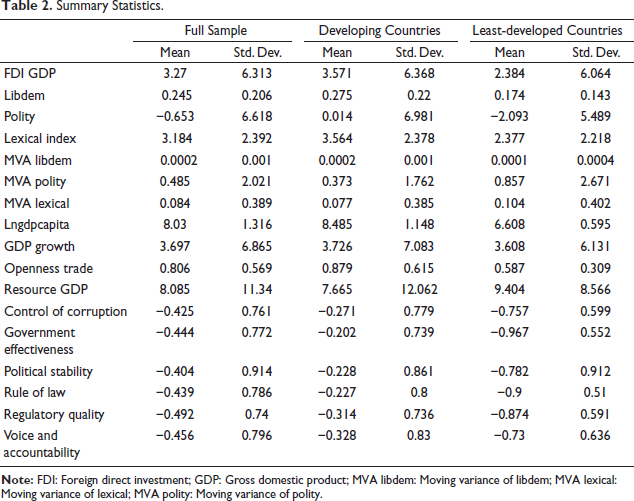

Certainly, other variables influence FDI as well. For instance, the labor cost is a significant determinant. Although various labor market statistics are available for many countries, data are often missing for numerous developing and underdeveloped countries. Including this variable would narrow the sample in this study, but since it is not critical to the main argument, it has been omitted. Additionally, GDP per capita to some extent reflects labor costs. Similarly, a country’s communication infrastructure can impact foreign investment decisions. However, the empirical focus of this research spans the years 1970–2022, making it challenging to use a single communication technology variable that consistently covers the entire period. GDP per capita also partly captures the quality of communication infrastructure, so this variable has not been separately included. Table 2 presents summary statistics of all variables used in the empirical analysis.

Summary Statistics.

Estimation Results

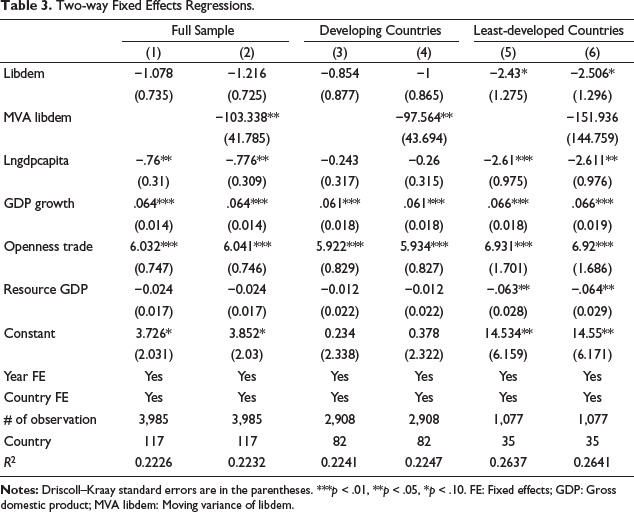

Table 3 presents the impact of democracy, as measured by the V-DEM liberal democracy index, on FDI using a fixed effects model across different samples. When considering the full sample and only developing countries, no statistically significant relationship is observed between democracy (political regime) and FDI inflows. This indicates that there is no significant difference in capital inflows between democratic and authoritarian regimes within the sample of developing countries. However, in the sample of least-developed countries, the democracy index shows a statistically significant negative effect on FDI at the 10% significance level. As the level of democracy increases in least-developed countries, FDI tends to decrease, suggesting that authoritarian regimes are more successful in attracting FDI in these contexts.

Two-way Fixed Effects Regressions.

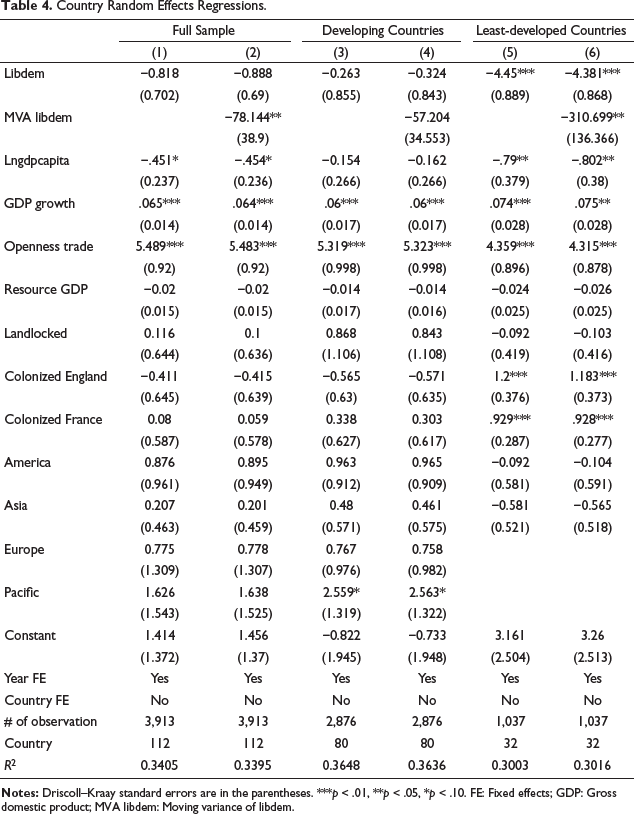

Table 4 shows the results of the random effects model, which includes time-invariant control variables. The findings reaffirm the lack of a significant relationship between democracy and FDI inflows in developing countries. However, in least-developed countries, the negative effect of democracy on FDI becomes more pronounced, with a higher level of statistical significance compared to previous models.

Country Random Effects Regressions.

The results from the fixed effects model indicate that political instability, measured by the moving variance of the democracy index, has a negative and significant impact on FDI for the entire sample and specifically for developing countries. This supports the hypothesis that the instability of a regime adversely affects FDI, as a rapidly changing political decision-making environment creates unforeseen costs for foreign companies, thereby negatively influencing investment decisions. Conversely, the random effects model does not find this effect in developing countries but does observe it in least-developed countries. In addition to the 5-year moving variance to proxy political regime instability, 3-year and 7-year moving variances were calculated for robustness. The results remain consistent and significant when using the 7-year moving variance. However, when using the 3-year moving variance, the estimated effect for developing countries loses statistical significance, likely due to the shorter time horizon failing to capture meaningful shifts in the political environment. Models incorporating both the 3-year and 7-year moving variances are provided in Appendix Table A1 (available as online supplementary material).

Per capita GDP is shown to have a negative and significant effect on FDI in the overall sample and least-developed countries. This suggests that countries with lower GDP per capita attract more FDI due to lower labor and non-labor regulatory costs, making them more appealing to foreign investors. However, this effect is not observed in developing countries. These findings, presented in Tables 3 and 4, align with earlier studies such as Li and Resnick (2003), Jakobsen and de Soysa (2006), and Jensen (2003), which found no significant relationship between development level and FDI inflows, while Dang (2015) identified a positive relationship.

As expected, a positive relationship is observed between GDP growth and FDI inflows, consistent with the broader literature. Additionally, trade openness is positively associated with FDI inflows. As a de facto indicator of a country’s trade policy, trade openness suggests that investing countries will face minimal challenges in import and export and that the government is less likely to violate property rights due to the high potential for international sanctions. The findings indicate that these factors influence investment decisions and are consistent with previous studies.

Regarding natural resource rents, the study finds no statistically significant relationship between natural resource abundance and FDI inflows in developing countries. However, a negative relationship is observed in least-developed countries, consistent with the findings of Asiedu and Lien (2011). They argue that investments in natural resources require significant capital inflows initially, followed by profit transfer, and that the natural resource sector can crowd out other investments, leading to a negative relationship. This finding, derived from the fixed effects model for the sample of least-developed countries, is not replicated in the random effects model.

The random effects model presented in Table 4 incorporates time-invariant dummy control variables. Although it is generally assumed that countries with coastlines would attract more investment due to easier transportation, no significant effect was found. Additionally, the continent where a country is located did not show a significant impact on FDI, with one exception: in developing countries, being in Oceania is associated with higher investment at the 10% significance level compared to other regions.

Dummy variables to control for the colonial history of countries reveal statistically significant positive coefficients in the sample of least-developed countries. Former British colonies, in particular, receive more FDI compared to other countries. This effect is also observed in former French colonies. The ongoing diplomatic relations and institutional similarities between former colonies and their colonizers likely contribute to this effect. Interestingly, the impact of having been a British colony is higher than that of having been a French colony. This finding aligns with the results of Glaister et al. (2020), suggesting that the United Kingdom has maintained stronger ties with its former colonies. It can also be argued that the British established institutions that laid the groundwork for a favorable investment environment in these regions. However, the direction of causality remains blurred. For example, in Africa, the areas colonized by the British were already more densely populated and economically active compared to those colonized by the French (Flint, 1973, cited by Hobsbawm, 1989).

Since none of the time-invariant control variables show significant effects in the full sample or developing countries, and given the nature of this study and the necessary tests, the results from the fixed effects model are considered to be more reliable for the full sample and developing countries. On the other hand, colonial history continues to influence many economic characteristics, including FDI flows, in least-developed countries. Therefore, regression models that do not control for this effect may fail to capture the full picture. As such, the results from the random effects model, which includes these control variables, should be considered when analyzing FDI in least-developed countries.

Revisiting the main hypothesis, the findings indicate that in developing countries, the type of political regime—whether democratic or authoritarian—does not have a statistically significant impact on FDI inflows. However, political instability has a negative influence. As long as a political regime remains stable, the regime per se does not affect FDI. Political instability, on the other hand, means an environment where the rules about governing decision-making processes, which are critical to societal functioning, change abruptly and have a significant impact on FDI. Such volatility in the decision-making environment creates unforeseen costs, thereby reducing the expected profitability of investments and leading to a decline in FDI inflows.

In least-developed countries, this effect is even more pronounced, with democracy exhibiting a negative impact on FDI. As these countries increase their level of democracy, FDI inflows tend to decrease. This suggests that economically underdeveloped countries also struggle to establish stable political institutions. Given the polarized and conflict-prone political environments often present in these countries, it is likely that insufficiently institutionalized democratic systems contribute to greater instability and uncertainty. Such conditions undoubtedly deter foreign investment. Consequently, a negative and statistically significant relationship between democracy and FDI inflows has been observed in least-developed countries.

Robustness

Different Democracy and Stability Measurements

To demonstrate the robustness of the findings across different democracy indices, the results of models estimated with the same specifications are presented in Table 5. Given the nature of the analysis and the results of the Hausman test, the two-way fixed effects model is appropriate. Moreover, due to the lack of significant results for time-invariant country-specific variables in the full sample and developing countries, the robustness checks were conducted using the fixed effects model. However, for least-developed countries, where variables related to colonial history showed significant results, the random effects model is employed in Table 6.

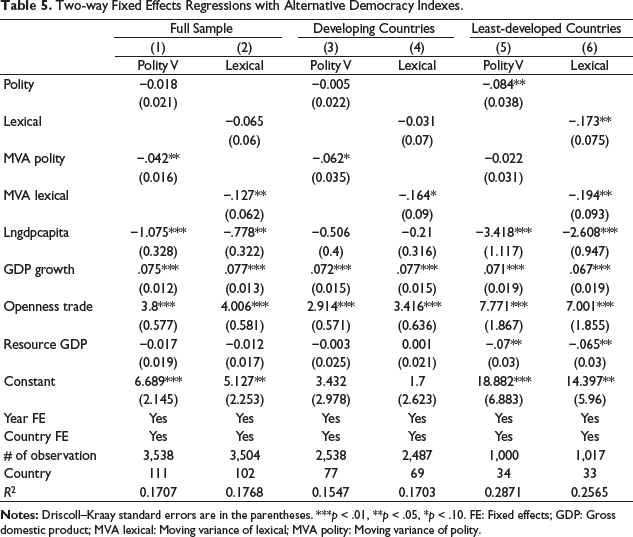

Two-way Fixed Effects Regressions with Alternative Democracy Indexes.

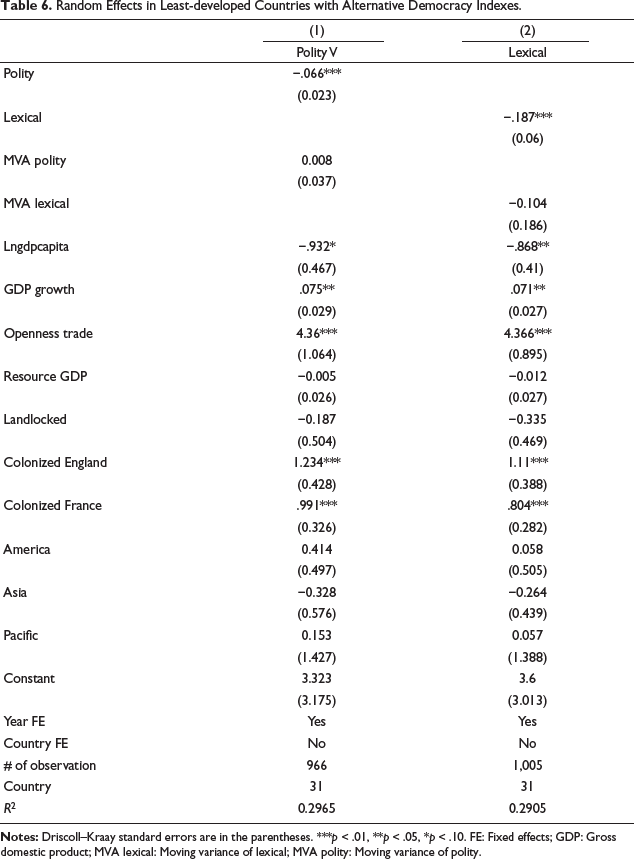

Random Effects in Least-developed Countries with Alternative Democracy Indexes.

Table 5 illustrates that the earlier finding, derived using the V-DEM liberal democracy index, of no significant relationship between democracy and FDI in developing countries holds valid when using the Polity V and lexical democracy indexes. Additionally, in least-developed countries, the observation that increased levels of democracy lead to reduced FDI inflows is shown to be robust across different indices, as demonstrated in both Tables 5 and 6.

While the random effects model (Table 4) using the V-DEM liberal democracy index indicated that regime instability negatively affects FDI in least-developed countries, this finding does not hold when the Polity V and lexical democracy indices are applied, as shown in Table 6. Here, the instability variables do not exhibit statistically significant effects. The signs and significance levels of the parameter estimates for control variables previously calculated are replicated in these robustness checks.

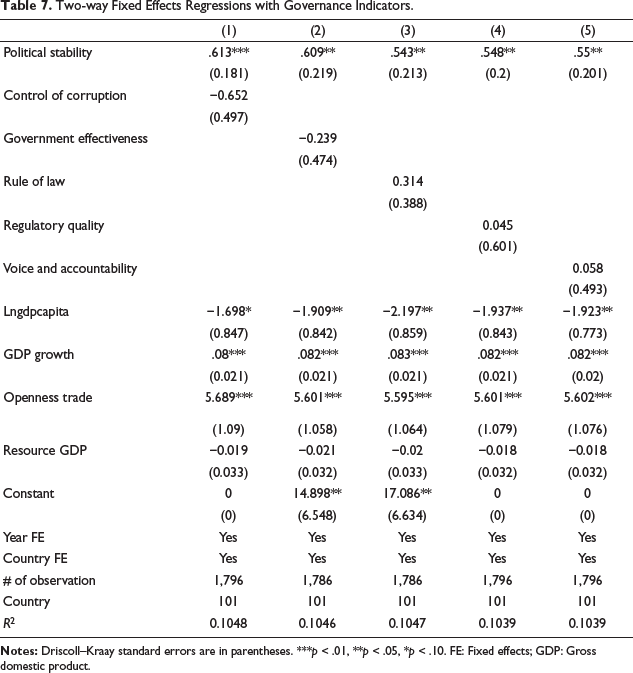

To further test the robustness of the findings, governance indicators were utilized, and models were estimated with data from 1996 to 2022 for the full sample of developing and least-developed countries using a fixed effects model. The results confirm that the main hypothesis—that political stability is the most critical political variable—remains valid even when using different indices over a narrower time period. Due to the correlation among various governance indicators, they were not included in the same model to avoid multicollinearity. Table 7 demonstrates that political stability has a positive and statistically significant impact on FDI, while no other governance indicator shows a statistically significant effect on its own. Specifically, indicators such as control of corruption, government effectiveness, rule of law, regulatory quality, and voice and accountability did not demonstrate statistically significant effects. This highlights that among the governance indicators considered, only political stability has a positive impact on foreign investments.

Two-way Fixed Effects Regressions with Governance Indicators.

Potential Endogeneity Bias

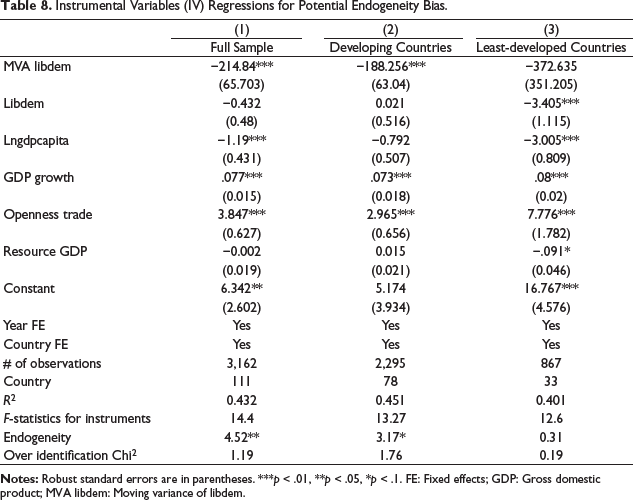

Since political instability can influence FDI inflows, but FDI can also shape the political environment, there is a potential endogeneity issue due to reverse causality. For example, Okara (2023) shows that FDI inflows can contribute to political stability. To address this, an instrumental variables (IV) regression using the lagged values of political instability and the fractionalization index were used as instruments, since political instability is influenced by its past values, and ethnic fractionalization has been argued to impact the political environment (Alesina et al., 2003; Jensen & Skaaning, 2012; Karnane & Quinn, 2019). When employing the liberal democracy index, weak evidence of endogeneity was found. However, the IV regression results, presented in Table 8, remained consistent with our previous findings. In contrast, when using the polity and lexical democracy indexes, there was no indication of endogeneity; thus, these results were omitted for conciseness.

Instrumental Variables (IV) Regressions for Potential Endogeneity Bias.

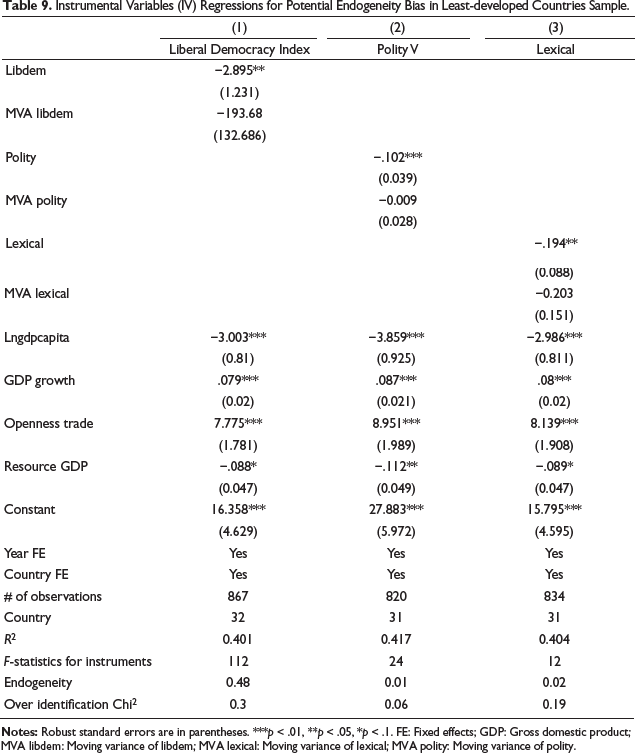

Similarly, previous findings suggest that democracy reduces FDI inflows in least-developed countries. However, democracy itself may be influenced by FDI, raising concerns of endogeneity. To account for this, an additional IV regression was conducted, using lagged political regime indexes and the fractionalization index as instruments. The results, shown in Table 9, indicate no significant endogeneity issue. Importantly, even after addressing potential endogeneity, the negative effect of democracy on FDI persisted, reinforcing the robustness of our initial findings. To sum up, the main findings are not affected by endogeneity bias and remain consistently robust across different estimation methods.

Instrumental Variables (IV) Regressions for Potential Endogeneity Bias in Least-developed Countries Sample.

Conclusion

This study investigates the role of host countries’ political regimes in attracting FDI inflows and questions the proposed positive relationship between democracy and FDI inflows. In the broader context of developing countries, the study finds no statistically significant relationship between political regimes and FDI inflows. This indicates that the type of political regime, per se, does not affect the attractiveness of these countries to foreign investors. Instead, stability and predictability within the political environment are critical. Political instability, characterized by rapid and unpredictable changes in governance, emerges as a significant deterrent for FDI. Such instability increases operational risks and costs, reducing the expected profitability of investments and ultimately leading to a decline in foreign capital inflows.

The situation differs in the least-developed countries, where the level of democracy exhibits a negative impact on FDI inflows. The analysis reveals that as the level of democracy increases in those countries, FDI inflows tend to decrease. This negative relationship suggests that least-developed countries, often characterized by polarized and conflict-prone political environments, struggle to establish stable and effective democratic institutions. Insufficiently institutionalized democratic systems in these contexts contribute to greater political instability and uncertainty, thereby deterring foreign investment.

Economic factors such as GDP growth and trade openness positively influence FDI inflows, consistent with established literature. Higher GDP growth generally indicates a growing market and increased potential for returns on investment, while trade openness reduces barriers to import and export, thereby enhancing the attractiveness of a country to foreign investors. Conversely, natural resource abundance does not significantly attract FDI in developing countries and negatively impacts the least-developed countries. This negative relationship reflects the capital-intensive nature of resource investments and the potential for natural resource sectors to crowd out other investment opportunities. Historical ties also play a significant role, particularly in the least-developed countries. The analysis shows that former British and French colonies attract more FDI, with British colonies exhibiting a stronger effect. This enduring influence of colonial history is likely due to ongoing diplomatic relations and institutional similarities established during the colonial period. These historical connections continue to shape investment flows and suggest that colonial legacies should be considered when analyzing FDI.

Footnotes

Acknowledgments

The author would like to thank Murat Birdal, Betül Pişkin, the participants of the VII International Conference on Economics—EconAnadolu2024 in Eskişehir, and the Turkish–German University Economics Conference in Istanbul, as well as the anonymous referees, for their valuable comments and suggestions.

Data Availability Statement

The datasets analyzed during the current study are available upon request.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Notes

Supplementary Material

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.