Abstract

This study examines how sustainable energy finance and environmental regulatory quality jointly influence two dimensions of Sustainable Development Goal-7 in sub-Saharan Africa: energy cleanability and energy accessibility. Covering 26 countries from 2005 to 2022, the analysis introduces novel composite indices derived using principal component analysis. The relationships were estimated using panel-corrected standard errors and feasible generalized least squares, complemented by the method-of-moments quantile regression and subregional breakdowns. Findings show that environmental regulatory quality exerts a strong and consistent positive effect on energy cleanability. Sustainable energy finance improves energy cleanability to a lesser extent and enhances energy accessibility only in low-performing countries with higher regulatory quality. Subregional analysis reveals that in West Africa, sustainable energy finance alone has little effect on energy access without strong regulation; in East Africa, regulation plays the dominant role; and in Central/Southern Africa, energy finance tends to be weak or even negative unless moderated by regulation. The study contributes to the literature by highlighting finance–regulation complementarities and recommending sequenced, blended finance tied to verifiable regulatory milestones.

Keywords

Introduction

Sub-Saharan Africa (SSA) continues to face dual challenges; not only is energy access far from universal, but the available energy also often falls short in terms of cleanliness and reliability. While national electrification rates have slowly improved, reliance on biomass and low-quality fossil-fuel generation perpetuates health hazards from indoor and ambient pollution, hindering development gains (Haines et al., 2007). Even where grid connections exist, frequent outages and voltage fluctuations erode the utility of electricity for households and productive activities alike (Kwakwa et al., 2021). In this context, energy cleanability (the capacity of an energy system to deliver services with minimal environmental and health externalities) and energy accessibility (the affordability, reliability, and geographic reach of modern energy services) must be disentangled. Although these dimensions are conceptually linked, they often respond differently to policy levers, and, to date, no study in the African context has examined them using separate analytical panels.

A growing consensus holds that sustainable energy finance (SEF) can catalyze improvements in both the cleanliness and reach of energy systems (Onabowale, 2025). For this study, we define SEF as the flows of capital (public, private, bilateral, and multilateral) that are explicitly directed toward accelerating clean-energy outcomes, including (but not limited to) funding for renewable energy production, clean-energy research and development (R&D), concessional project finance for low-carbon infrastructure, and dedicated instruments whose proceeds are earmarked for energy-related environmental objectives (Alabi, 2026). SEF therefore functions as an umbrella concept encompassing market instruments such as green bonds and sustainability-linked loans, dedicated green/climate funds, development finance, and direct public R&D support. Evidently, green bonds, sustainability-linked loans, and blended concessional financing have unlocked billions of dollars for renewable energy and clean-cookstove projects in developing regions (Xiong & Dai, 2023). Yet, in SSA, these flows remain embryonic, often constrained by high perceived risks and weak project bankability (Michaelowa et al., 2021). What has been firmly established is that financial development correlates with increased electricity access and renewable deployment (Li et al., 2024), but the specific role of global funding for clean-energy R&D and renewable generation in the African context remains underexplored. Critically, there is no empirical framework that relates such finance to independently measured indices of energy cleanability and accessibility in SSA.

Similarly, environmental regulatory quality (EnvReg) has been shown to influence clean-energy uptake and environmental outcomes (Ma et al., 2022; Shahzad et al., 2024). Strong regulation can drive firms and utilities to adopt cleaner technologies, yet overly rigid standards without supportive infrastructure or subsidies may exacerbate energy poverty (Ma et al., 2022). In SSA, weak regulatory institutions and fragmentation often blunt the effectiveness of policies (Oteng-Abayie et al., 2022). What remains unclear is how regulatory quality interacts with financial flows to shape energy outcomes across distinct subregions and how these interactions manifest across the separate dimensions of cleanability and accessibility.

This study addresses these gaps by introducing novel composite indices of energy cleanability and accessibility, drawing on the framework of Zhong et al. (2025), and applying them to panel data on SSA countries. Unlike existing work, we treat cleanability and accessibility as distinct outcome variables, enabling us to capture differential effects of finance and regulation. We further disaggregate our analysis by subregion to uncover heterogeneity in the finance–regulation–energy nexus and employ mixed-method quantile regression to explore distributional impacts across the spectrum of country-level energy performance. To our knowledge, this is one of the first studies to integrate global clean-energy R&D funding metrics with measures of EnvReg in the SSA context and the first to apply these innovations in a unified framework of Sustainable Development Goal (SDG)-7 metrics.

Accordingly, the objectives of this study are to:

Quantify the impact of SEF on both energy cleanability and accessibility. Investigate the direct role of EnvReg in energy cleanability and accessibility. Assess how the quality of environmental regulation moderates the relationship between energy finance flows and energy outcomes. Examine regional heterogeneity across West, East, Central, and Southern Africa. Uncover the distributional effects to determine whether energy finance and regulation differentially benefit low- versus high-performing countries.

This study makes several novel contributions to the sustainable energy and development literature by providing timely evidence to inform policymaking on SDG-7 in sub-Saharan Africa. First, it offers one of the earliest multi-country analyses of how SEF and EnvReg jointly shape energy accessibility and cleanability in the region, revealing important heterogeneity in their complementarities. Second, the study advances the literature methodologically by combining static and dynamic estimators to address small-sample bias, persistence, and endogeneity in developing-country panels. Third, the findings highlight regulatory capacity as a key policy lever that strengthens the impact of SEF, with clear implications for governments, donors, and private investors.

Literature Review

The Effect of Sustainable Energy Finance on Energy Cleanability and Accessibility

In recent years, the mobilization of sustainable finance has emerged as a cornerstone in advancing SDG-7 (affordable, reliable, sustainable, and modern energy for all) across Africa. For instance, Onabowale (2025) emphasizes the importance of innovative instruments, such as green bonds, sustainability-linked loans, and carbon pricing, for aligning market incentives with renewable energy goals. Stable regulatory regimes and clear long-term targets are shown to de-risk investments and attract private capital, illustrating how tailored finance can enhance both energy cleanability and access. Li et al. (2024) find that a 1% increase in GDP or financial development raises electricity access by 0.15% and 0.14% in low- and middle-income economies, respectively, with renewable electricity output and clean fuel access exhibiting bidirectional causality with electricity access. This suggests a reinforcing cycle where finance supports clean energy deployment, which in turn stimulates further investment. Xiong and Dai (2023) similarly report that each 1% rise in renewable energy investment increases private sector investment by 1.243%, highlighting green finance’s catalytic role in innovation and renewable scale-up.

At the regional level, sub-Saharan Africa faces distinctive institutional and infrastructural barriers. Chirambo (2018) notes that initiatives such as Power Africa, SE4All, and the China South-South Climate Cooperation Fund have injected capital; however, fragmented governance and a potential “climate finance curse” limit their impact. Strengthening institutional coordination is key to harmonizing funding streams and linking rural electrification with agricultural and irrigation development, as in Vietnam’s energy expansion. Kwakwa et al. (2021) show that income, foreign direct investment (FDI), political regime quality, and employment all boost clean energy access in SSA, while inflation erodes it, underscoring the need for macroeconomic stability and democratic deepening to translate financial growth into tangible access. Innovative, community-focused financing models are gaining traction. Chukwuma-Eke et al. (2024) highlight microfinance, pay-as-you-go systems, crowdfunding, and impact investing—often supported by digital platforms and analytics—as mechanisms to reduce transaction costs and tailor products to low-income households, thereby enhancing both cleanability and accessibility. Michaelowa et al. (2021) find that United Nations Framework Convention on Climate Change (UNFCCC)-backed tools such as the Clean Development Mechanism and Green Climate Fund can mobilize private investment, but only when integrated with national renewable actions and aligned with local market frameworks.

Country-specific studies show varied pathways. In Morocco, Ainou et al. (2023) used the 4-As framework (availability, applicability, acceptability, and affordability), which showed that despite ambitious renewable targets (42% by 2020 and 52% by 2050), energy security declined after 2004 due to rising imports and low efficiency. They stressed the need for green finance to address both technological applicability and social acceptance to sustain the transition. In Ghana, Frimpong et al. (2025) identified policy coherence, sustainable energy indicators, and strategic communication as essential for reducing emissions and advancing SDG-7, highlighting the role of robust policy in mobilizing stakeholders.

Cross-cutting evidence links green finance to both renewable expansion and environmental gains. Chen et al. (2024) documented dynamic spillovers between green bonds, renewable investment, and carbon markets across 30 developing countries, with the banking sector as a key intermediary. They demonstrated that stronger bond frameworks drive more renewable investment, creating positive feedback loops for ecological quality. Hu and Jin (2023) showed that in China’s green bond market, financial, environmental, and regulatory factors influence the mobilization of renewable capital, illustrating the transformative potential of well-designed mechanisms.

The Effect of Environmental Regulatory Quality on Energy Cleanability and Accessibility

Another consequential factor in shaping both the cleanliness and reach of energy systems is the stringency and quality of environmental regulations. Haines et al. (2007) argue that clean energy policies deliver major health and development co-benefits by cutting air pollution and enabling modern services, but warn that without strong regulation and intersectoral coordination, gains may be fragmented and inequitable. At the household level, Ma et al. (2022) found that stricter environmental standards in China can worsen energy poverty among conventional fuel users unless affordable clean alternatives are made available. Households adapt more easily to regulation-driven shifts when modern energy is reliable and affordable.

Governance quality evidently shapes regulatory effectiveness. In OECD countries, stringent environmental rules raise clean-energy use only under strong governance conditions, such as the rule of law and low corruption (Shahzad et al., 2024). Weak governance undermines enforcement, enabling non-compliance and eroding energy-access benefits. In SSA, higher regulatory quality improves environmental sustainability; however, when enforcement falters, resource exploitation still harms green outcomes (Oteng-Abayie et al., 2022). Across 61 developing nations, stronger institutions amplify the positive effect of clean-energy adoption on electricity access, while inequality and unstable remittances hinder progress (Murshed, 2023). In Africa, enhancing regulatory quality and curbing corruption substantially increase the likelihood of exiting low-efficiency energy states, underscoring the role of capable institutions in meeting SDG-7 (Akorli & Adom, 2023).

Environmental regulations can drive technological innovation, improving both cleanability and accessibility. Herman and Xiang (2020) showed that stringent foreign standards spur domestic cleantech innovation, particularly when institutional differences are small, highlighting cross-border spillovers. In the Asia-Pacific, Annamalaisamy and Vepur Jayaraman (2023) posit that regulatory quality and renewable-energy adoption reinforce each other; a 1% increase in their interaction reduces emissions by 0.35%, even though income growth alone tends to raise emissions. This underscores the need for policy stringency to advance alongside renewable capacity expansion for maximum environmental gains.

For G7 countries, Liu et al. (2023) showed that policy stringency and renewable investment reinforce each other, with stronger long-run impacts when combined than when considered separately. These findings suggest that regulations shape both market rules and the flow of finance and R&D toward cleaner, more accessible energy. In low-income contexts, Rahman and Sultana (2024) find that strict rule of law and corruption curb CO2 emissions and improve human development by ensuring renewable policies lead to favorable outcomes. Wang et al. (2022) add that in N-11 economies, environmental regulations reduce ecological footprints, while democracy and renewable use jointly enhance environmental quality. These studies show that governance and regulatory stringency must align to advance both energy cleanliness and accessibility, accelerating SDG-7 progress.

While prior research has richly documented the separate roles of green finance (Onabowale, 2025; Xiong & Dai, 2023) and environmental regulations (Ma et al., 2022; Shahzad et al., 2024) in advancing clean energy, no study to date has woven these two strands together in the specific context of African energy systems. By simultaneously examining how SEF and the quality of environmental regulation interact to shape both energy cleanability and accessibility, this research fills a critical gap. We offer the first integrated framework by moving beyond one-dimensional analyses to capture the dynamic feedback loops between financial flows and regulatory strength, using novel panel data for 46 African countries and drawing on insights from institutional quality studies in SSA (Akorli & Adom, 2023; Oteng-Abayie et al., 2022).

Interactive Effects: Sustainable Energy Finance and Environmental Regulation

This study incorporates both SEF and EnvReg as core explanatory variables, as they represent two structurally distinct but interdependent policy channels underpinning SDG-7 progress. While SEF reflects the availability of capital required for renewable deployment, grid expansion, and clean-fuel adoption, regulatory quality captures the institutional effectiveness that determines whether such financial resources are efficiently allocated, enforced, and translated into operational energy outcomes (Liu et al., 2023; Onabowale, 2025).

From an institutional economics perspective, the effectiveness of SEF is conditional on regulatory capacity (Liu et al., 2023). Strong regulatory frameworks reduce information asymmetry, mitigate moral hazard, and lower project risks, thus improving the efficiency with which financial resources are converted into tangible energy outcomes. In weakly regulated environments, financial inflows may be diverted, delayed, or misallocated, attenuating their developmental impact (Ma et al., 2022; Shahzad et al., 2024). The interaction between SEF and regulation is also consistent with the complementary assets framework, which posits that financial capital alone is insufficient without supporting institutions and enforcement mechanisms. Regulatory quality enhances the marginal productivity of finance by facilitating project approval processes, ensuring compliance with technical standards, and improving coordination among public and private stakeholders (Liu et al., 2023).

Importantly, the strength of this interaction may differ across energy outcomes. For energy accessibility, improvements often involve decentralized or community-level projects (e.g., grid extensions, mini-grids, and off-grid solar systems) that are highly sensitive to regulatory clarity, permitting efficiency, and subsidy targeting (Wang et al., 2022; Xu & Gallagher, 2022). In such contexts, regulation amplifies the effectiveness of SEF by accelerating project execution and reducing transaction costs. In contrast, energy cleanability reflects structural shifts in the energy mix that typically require large-scale capital investments, technological upgrading, and long adjustment periods (Ma et al., 2022; Murshed, 2023; Shahzad et al., 2024). While SEF directly supports clean energy deployment, the marginal role of contemporaneous regulation may be less pronounced, particularly where legacy energy systems, infrastructure lock-in, or political economy constraints dominate.

This theoretical stance suggests a complementary relationship between SEF and regulation for energy access outcomes, while predicting a weaker or delayed interaction effect for energy cleanability. Accordingly, the empirical analysis explicitly tests the interaction between SEF and environmental regulation across multiple energy dimensions.

Methodology

Data Sources and Sample

Our empirical analysis employs an unbalanced panel dataset covering 26 sub-Saharan African countries over the period 2005–2022. This timeframe captures both the rapid acceleration of global clean-energy finance mechanisms and the evolving institutional landscapes across the region. Based on data availability, the study focuses on a country sample that includes Burundi, Burkina Faso, the Central African Republic, Côte d’Ivoire, Cameroon, the Democratic Republic of Congo (DRC), the Republic of Congo (ROC), Cabo Verde, Ethiopia, Ghana, Guinea, Gambia, Kenya, Lesotho, Madagascar, Mali, Mozambique, Mauritania, Niger, Nigeria, Rwanda, Sierra Leone, Chad, Togo, Tanzania, and Uganda. Given the data availability constraint, we selected the largest set of countries for which the core variables were jointly observed.

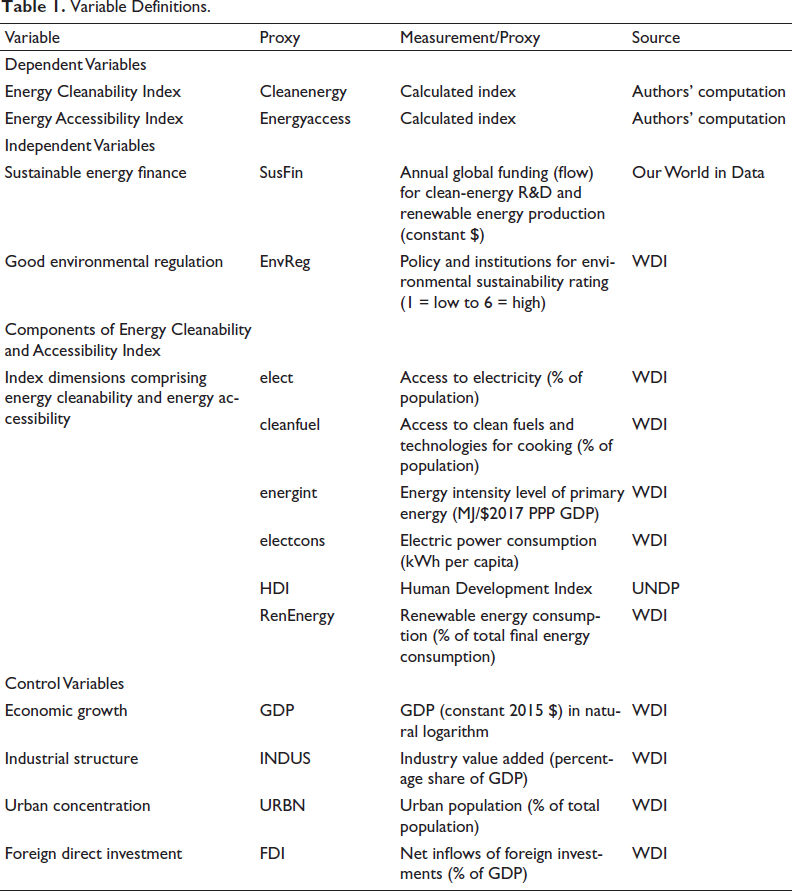

Sustainable energy finance (SusFin) is measured as annual global funding for clean-energy R&D and renewable energy production in developing countries (constant USD) and treated as a flow variable. Owing to skewness, SusFin is log-transformed, while untransformed values (millions USD) are reported in the descriptive statistics. EnvReg, sourced from the World Bank governance indicators, ranges from 1 (weak) to 6 (strong). Control variables include GDP, industrial value added, urbanization, and FDI inflows. Sporadic missing observations are addressed using linear interpolation. Variable definitions are reported in Table 1.

Variable Definitions.

The dependent variables are two composite indices: energy cleanability and energy accessibility (Zhong et al., 2025). The cleanability index combines energy intensity, renewable energy share, the human development index (HDI), and clean cooking access, while the accessibility index aggregates electrification rates, per-capita electricity consumption, and HDI. Both indices are standardized and constructed using principal component analysis (PCA) following Alabi et al. (2025).

As shown in Appendix Table A1 (in supplemental material), the first two PCA components explain 85.5% of the variance in energy cleanability and over 90% of the variance in energy accessibility, exceeding the 70% benchmark. For cleanability, the first component captures clean fuel access, renewables, and HDI, while the second reflects energy efficiency. For accessibility, the first component reflects broad access, and the second captures variation in consumption intensity.

Model Specification

In crafting our empirical models, we express each variable in natural logarithms to ameliorate skewness, stabilize variance, satisfy normality assumptions, and allow coefficients to be interpreted within a proportional-response framework. This transformation is also particularly necessary for flow-based financial variables such as sustainable energy finance, whose absolute magnitudes vary substantially across countries and over time. For bounded ratio variables, the estimated coefficients are interpreted as semi-elasticities rather than strict elasticities.

Model 1 (baseline cleanability specification):

where i indexes country, t indexes year, αi captures time-invariant country fixed effects, and λt captures common time shocks. SusFin is sustainable-energy finance, EnvReg denotes environmental regulatory quality, and Xk denotes our four controls (GDP, INDUS, URBN, FDI).

Model 2 (baseline accessibility specification):

This mirrors Model 1, but with “energyaccess” as the dependent variable.

Model 3 (moderation of cleanability by EnvReg)

The interaction term EnvReg it × SusFin it tests whether the impact of sustainable energy finance on cleanability is conditioned by environmental regulatory strength.

Model 4 (moderation of accessibility by EnvReg)

Estimation Strategy

Before proceeding with model estimation, it is essential to establish the statistical properties of the panel dataset. Pesaran’s (2015) test for cross-sectional dependence evaluates whether residuals across panel units are correlated. The test statistic is based on the average of all pairwise correlation coefficients of residuals:

where

Once the order of integration is confirmed, we tested for long-run equilibrium relationships between the variables using the Westerlund (2007) cointegration test given by:

Here,

Next, we estimated the main models using panel-corrected standard errors (PCSE):

where Σ allows for heteroskedasticity across panels and contemporaneous correlation across units. This technique yields efficient and unbiased standard errors in the presence of CSD.

We re-estimated all baseline and moderation models using feasible generalized least squares (FGLS), which also addresses cross-sectional dependence and panel heteroskedasticity. While PCSE remains our baseline, FGLS serves as a robustness check. Given that policy effects on energy cleanability and accessibility may vary between low- and high-performing countries, we also applied the method of moments quantile regression (MMQR) by Machado and Santos Silva (2019), which estimates conditional quantile effects while preserving location–scale flexibility, enabling detection of distributional heterogeneity. Formally, the MMQR model can be expressed as:

Where

Results and Discussion

Pre-estimations

Preliminary diagnostics in Appendix Table A2 (in supplemental material) show strong cross-sectional dependence for most variables using the Pesaran CD test, indicating that shocks, policy changes, or spillovers in SSA are not country-specific. The only exception is INDUS. This confirms the need for second-generation panel methods that account for common shocks and contemporaneous correlation. Stationarity was assessed with the CADF test, which accommodates such dependence.

Most macro and policy indicators are non-stationary at the level but stationary after first differencing, except FDI, which is stationary at the level. The composite indices for energy cleanability and energy accessibility were standardized after PCA, making unit-root testing less meaningful; their statistical behavior is tied to their components. Westerlund cointegration tests, adjusted for cross-sectional means, confirm long-run equilibrium relationships despite mixed integration orders. This supports estimating models at levels while focusing on long-run coefficients. Given these results, PCSE is used as the baseline estimator, with FGLS for robustness.

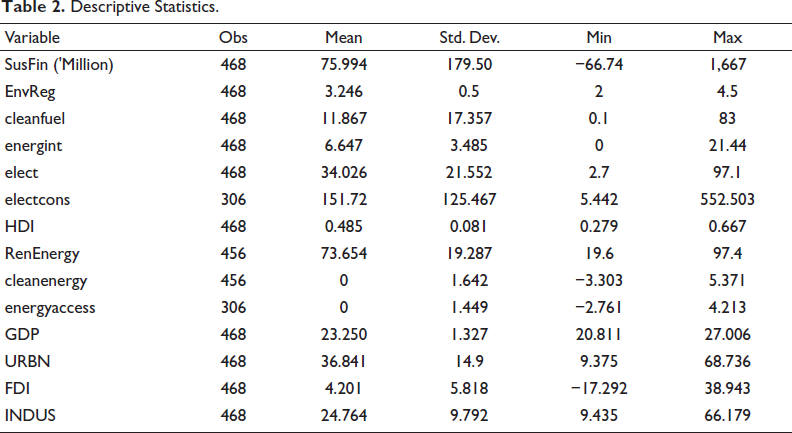

Summary Statistics

Descriptive Statistics.

Energy access and clean energy variables are standardized indices with mean values close to zero, confirming their suitability for panel estimation. Control variables such as GDP, urbanization, industrial activity, and FDI show distributions consistent with existing evidence for developing economies. Appendix Table A3 (in supplemental material) presents the pairwise correlation matrix. The correlations among explanatory variables remain well below conventional thresholds for multicollinearity, suggesting that multicollinearity is unlikely to bias the regression estimates.

Estimations and Discussions

Energy Cleanability

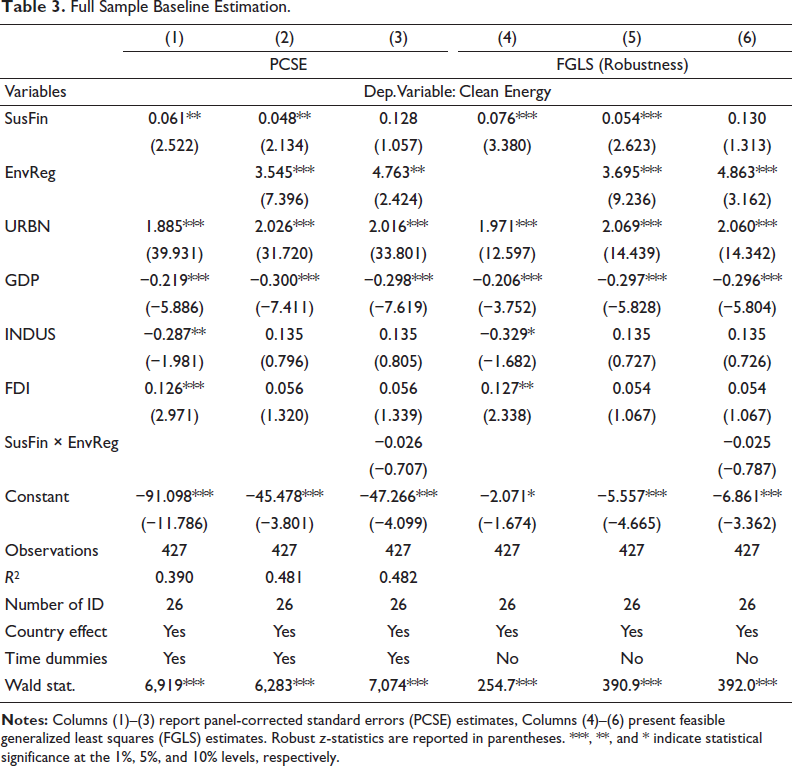

Sustainable energy finance exhibits a positive and statistically significant effect across specifications (Table 3, Columns 1–2 for PCSE and Columns 4–5 for FGLS), with coefficients ranging from 0.048 to 0.061 (Table 3, Columns 1–2) and corroborated by FGLS robustness checks (Table 3, Columns 4–5). Interpreted as elasticities, a 1% increase in sustainable energy finance raises the cleanability index by approximately 0.05%–0.08% (Table 3, Columns 1–2 and 4–5). This supports existing evidence that green finance promotes cleaner energy systems (Onabowale, 2025; Xiong & Dai, 2023), though the relatively small magnitude suggests an incremental effect in sub-Saharan Africa.

Full Sample Baseline Estimation.

EnvReg exhibits large, robust, and highly significant elasticities in both PCSE and FGLS estimates (Table 3, Columns 2 and 5), indicating that improvements in regulatory quality are strongly associated with higher energy cleanability. For example, the EnvReg coefficient is 3.545 (PCSE, Table 3, Column 2) and 3.695 (FGLS, Table 3, Column 5), both statistically significant at the 1% level. The interaction term between sustainable energy finance and EnvReg is negative but statistically insignificant (Table 3, Column 3, where SusFin × EnvReg = −0.026, t = −0.707). This lack of statistical significance is explicitly noted; it is noteworthy that the interaction is insignificant under both PCSE and FGLS (compare Table 3, Columns 3 and 6). Among the control variables, urbanization consistently enhances energy cleanability (URBN: Table 3, Columns 1–6), GDP exerts a negative effect (Table 3, Columns 1–6), and FDI remains small but positive (Table 3, Columns 1 and 4).

Energy Accessibility

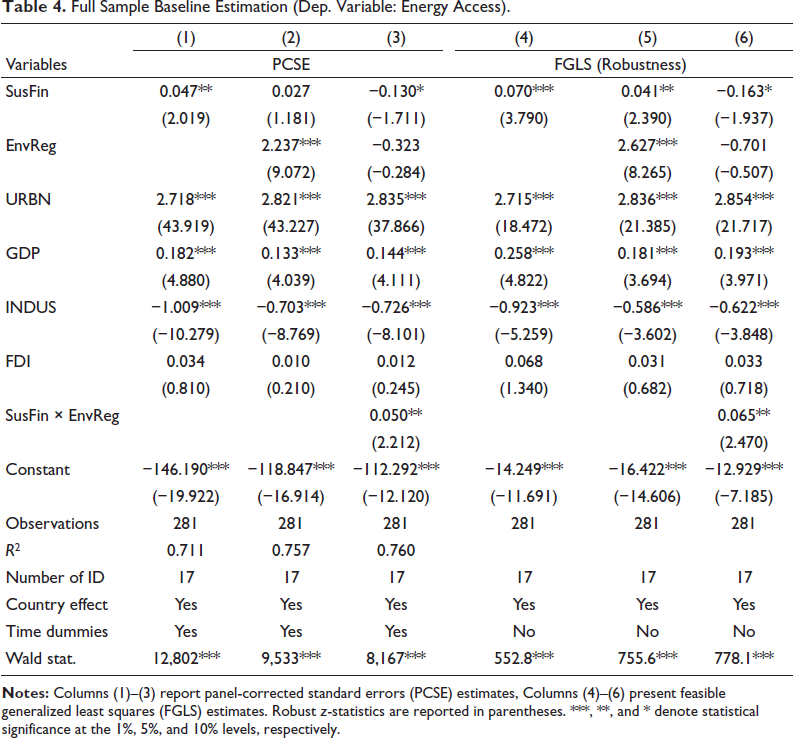

Table 4 indicates that sustainable energy finance and regulatory quality jointly influence energy accessibility, though not additively. In the baseline PCSE models without interactions, sustainable energy finance is positive and significant, with a 1% increase associated with a 0.05% rise in the energy accessibility index, consistent with Li et al. (2024) and Kwakwa et al. (2021). However, once the interaction term is introduced, the main effect of SusFin becomes negative, while the interaction term is positive and significant (Table 4, Column 3: SusFin = −0.130 and SusFin × EnvReg = 0.050; and the FGLS analogue in Table 4, Column 6: SusFin = −0.163, SusFin × EnvReg = 0.065). These exact coefficients and their significance levels are reported in Table 4 (Columns 3 and 6). The positive interaction coefficient implies that stronger environmental regulation enhances the effectiveness of sustainable energy finance in expanding access (Table 4, Columns 3 and 6). This aligns with evidence that institutional quality moderates the transmission of external resources into electricity access by reducing uncertainty and facilitating project deployment (Murshed, 2023; Shahzad et al., 2024).

Full Sample Baseline Estimation (Dep. Variable: Energy Access).

Among controls, urbanization strongly increases energy accessibility (URBN: Table 4, Columns 1–6), and GDP is positive (Table 4, Columns 1–6). Industry share (INDUS) is negative and significant in most specifications. FDI remains small and statistically insignificant, suggesting that foreign inflows during the period were not systematically directed toward expanding household access (Kwakwa et al., 2021).

Interaction Effects

The baseline interaction results reveal a clear asymmetry; the interaction between SusFin and EnvReg is positive and significant for energy accessibility, but insignificant (and slightly negative) for energy cleanability. To formalize this difference, we computed the marginal effect (ME) of SusFin on each outcome, conditional on regulatory quality. Formally, when the model includes an interaction between sustainable finance and regulatory quality, the ME of a 1% change in SusFin on the outcome y (cleanability or access) is:

where

Using PCSE estimates from Tables 3 and 4 (accessibility:

Regional Estimates for Energy Cleanability

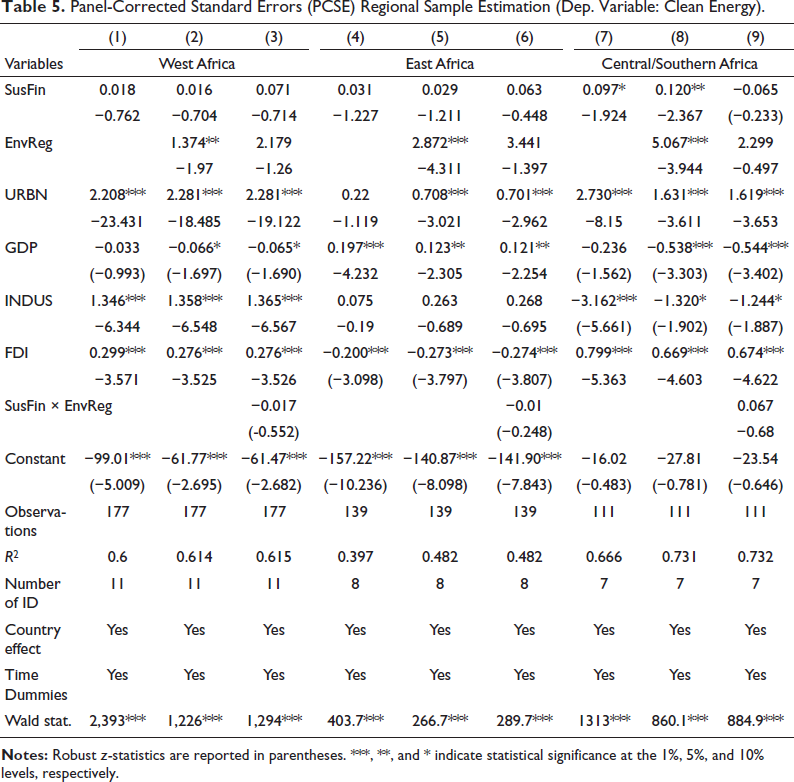

Table 5 reports regional heterogeneity estimates in the determinants of energy cleanability across sub-Saharan Africa, where Columns 1–3 correspond to West Africa, Columns 4–6 to East Africa, and Columns 7–9 to Central/Southern Africa. In West Africa, sustainable energy finance is small and statistically insignificant, while EnvReg is positive and significant, indicating that institutional capacity rather than finance flows drives cleanability improvements. Urbanization and FDI are also positive, and INDUS is strongly positive, suggesting that industrial activity in the subregion may be relatively cleaner or concentrated in urban settings where grid upgrades are feasible (Kwakwa et al., 2021; Li et al., 2024).

Panel-Corrected Standard Errors (PCSE) Regional Sample Estimation (Dep. Variable: Clean Energy).

In Central and Southern Africa, sustainable energy finance is materially larger and statistically significant, implying that finance flows more effectively translate into cleaner energy systems in this subregion. EnvReg is also large and significant, while INDUS is strongly negative, reflecting the dominance of energy-intensive extractive activities. FDI is positive, consistent with greater investment in renewables and infrastructure. The contrast with West Africa highlights the importance of industrial composition in shaping cleanability outcomes (Kwakwa et al., 2021; Li et al., 2024). Overall, FDI effects vary by region, being positive in West and Central/Southern Africa but negative in East Africa, supporting the view that the environmental impact of foreign capital depends on its sectoral allocation (Chirambo, 2018; Michaelowa et al., 2021). FGLS estimates reported in Appendix Table A5 (in supplemental material) closely mirror the PCSE results in Table 5, with similar signs and significance across regions, confirming the robustness of the findings and the continued insignificance of the interaction term.

Regional Estimates for Energy Accessibility

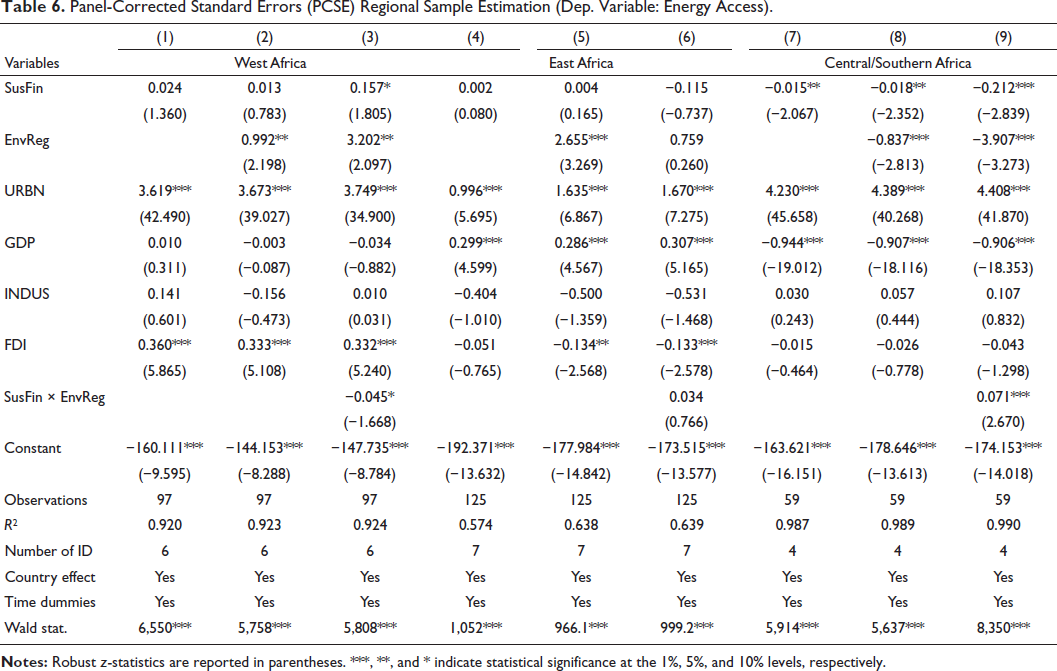

Table 6 shows pronounced regional heterogeneity in the determinants of energy accessibility, with urbanization emerging as the dominant driver across sub-Saharan Africa. In West Africa, both sustainable energy finance and EnvReg are positive and weakly significant, while their interaction is negative and marginally significant, suggesting that simultaneous tightening of finance and regulation may dampen short-run access, consistent with evidence on regulatory frictions and compliance delays (Chirambo, 2018; Ma et al., 2022).

Panel-Corrected Standard Errors (PCSE) Regional Sample Estimation (Dep. Variable: Energy Access).

In East Africa, sustainable energy finance is negligible, whereas EnvReg, urbanization, and GDP are positive and significant, indicating that access gains are primarily growth- and urban-driven. The insignificant interaction term suggests limited financial leverage through regulatory channels, potentially due to an emphasis on long-gestation projects or the composition rather than volume of capital inflows (Michaelowa et al., 2021).

Central and Southern Africa exhibit a contrasting pattern; sustainable energy finance and regulatory quality are individually negative and significant, while their interaction is positive and highly significant. This implies that finance and regulation reduce access when applied in isolation but jointly enhance access when effectively aligned, underscoring the importance of sequencing and conditional policy design (Michaelowa et al., 2021; Xu & Gallagher, 2022).

Among the controls, urbanization is uniformly positive and highly significant across all regions. GDP and FDI display region-specific effects, highlighting differences in growth structures and capital allocation. FGLS estimates reported in Appendix Table A6 (in supplemental material) closely mirror the PCSE results in Table 6, with minor changes in magnitude and significance that do not alter the core conclusions.

Full-sample Distributional Effects

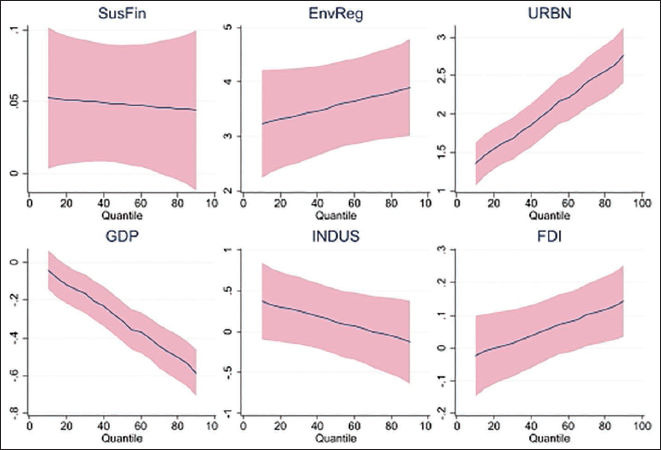

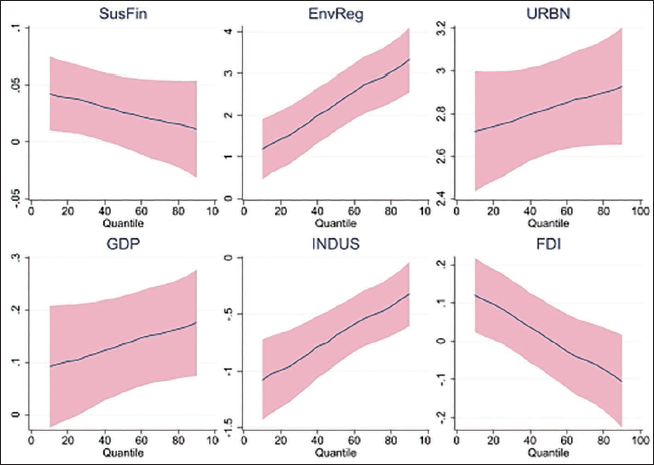

The MMQR estimates in Appendix Table A7 (in supplemental material) confirm substantial distributional heterogeneity in the effects of sustainable energy finance and regulatory quality. EnvReg is a consistently large and positive determinant of both energy cleanability and accessibility across quantiles, with effects strengthening toward the upper quantiles. Sustainable energy finance, by contrast, exerts uniformly positive but modest effects on cleanability across the distribution, whereas its impact on accessibility is concentrated among lower-performing countries and weakens at higher quantiles. Urbanization remains a strong and stable driver of both outcomes.

For energy cleanability, sustainable energy finance shows a stable positive elasticity across quantiles (≈0.045–0.051), indicating broadly similar benefits for low- and high-performing countries, with little effect on dispersion. EnvReg exhibits increasing effects from lower to upper quantiles, implying that regulation accelerates cleanability more strongly where baseline capacity is higher.

For energy accessibility, sustainable energy finance displays its clearest distributional role. Its effect is largest and statistically significant at the lower quantiles and declines steadily, becoming insignificant at the upper quantiles. This indicates that finance is most effective in expanding access in the poorest-performing countries. EnvReg again shows robust and increasing effects across quantiles, suggesting that regulation becomes especially influential once basic access systems are in place. Urbanization strongly and uniformly improves access, GDP effects strengthen toward higher quantiles, industry remains consistently negative, and FDI shifts from positive at low quantiles to negative at the top, reflecting changes in the sectoral destination of foreign capital. Figures 1 and 2 illustrate these heterogeneous marginal effects across quantiles.

Visualization of the Marginal Effects Across Different Quantiles (Panel A: Clean Energy).

Visualization of the Marginal Effects Across Different Quantiles (Panel B: Energy Access).

Additional Robustness Tests

To test the sensitivity of results to the choice of regulatory proxy, we replaced the baseline EnvReg measure with the CPIA business regulatory environment rating (EnvReg2; as in Appendix Table A8 [in supplemental material]), capturing broader institutional capacity for market entry and enforcement. Re-estimating all baseline and interaction models confirms that EnvReg2 is positive and significant for both energy cleanability and accessibility. The SusFin × EnvReg2 interaction remains significant for accessibility but not for cleanability, consistent with the main results, indicating that institutional and regulatory capacity, however measured, conditions the impact of sustainable energy finance on SDG-7 outcomes.

Turning to potential endogeneity, reverse causality, and omitted-variable bias, we applied dynamic panel estimators: two-step system GMM and a bias-corrected dynamic panel estimator, including lagged dependent variables to capture persistence. Instruments were collapsed and lag depth was restricted to prevent proliferation. Results (Appendix Table A9, in supplemental material) show strong persistence in both outcomes, with baseline and interaction effects of SusFin and regulatory quality broadly consistent with PCSE and FGLS estimates. Specifically, for energy accessibility, sustainable finance and its interaction with regulation remain significant; for energy cleanability, the interaction remains insignificant, reaffirming that finance–regulation complementarities mainly influence access rather than system cleanliness in the short to medium term.

Conclusion and Policy Recommendations

This study analyzed the effects of sustainable energy finance and EnvReg on energy cleanability and access across 26 sub-Saharan African countries (2005–2022), using PCSE, FGLS, and MMQR, with full-sample and subregional analyses. Three consistent patterns emerge: regulatory quality is a strong, persistent driver of energy outcomes; sustainable energy finance is most effective when combined with robust governance; and effects differ markedly across regions. For the full sample, finance–regulation synergy was especially critical for energy access, while urbanization consistently supported both outcomes. GDP growth favored access but often at the expense of clean energy shares, reflecting a structural reliance on fossil-based energy. Subregional analysis shows sharper contrasts: in West Africa, finance alone had limited impact unless backed by regulation; in East Africa, regulatory quality dominated; and in Central/Southern Africa, unmoderated finance sometimes showed weak or negative associations with outcomes.

Policy implications follow directly from these findings. First, strengthening regulatory capacity alongside mobilizing finance is essential because it amplifies the impact of financial inflows, particularly for decentralized projects (such as mini-grids and off-grid solar). Second, differentiated strategies are needed for access versus clean energy. Access responds more quickly to finance–regulation interactions, while clean energy transitions require longer-term reforms, including grid modernization, market liberalization, and technology upgrading. We recommend sequenced approaches; short-term access initiatives coupled with medium- to long-term clean energy planning. Third, development partners and climate financiers should integrate regulatory readiness into allocation decisions, directing funds toward countries with minimum institutional capacity and providing technical assistance where needed.

Finally, SDG-7 strategies must be regionally tailored and institutionally sequenced. Regulatory capacity should be strengthened before or alongside scaling finance. In West and Central/Southern Africa, reforms should focus on transparent licensing, grid integration standards for renewables, and long-term power purchase agreements to reduce investment risk. East Africa should consolidate regulatory gains and harmonize frameworks to enable regional power pooling and cross-border renewable investment.

Footnotes

Data Availability Statement

The data are available upon reasonable request.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.