Abstract

Does infrastructure development help African countries boost their currently weak industrial structure to meet with pressing needs of their growing population? Answering this question which is also the ambition of SDG 9 requires taking into account rising global uncertainty which provokes a ‘wait-and-see’ behaviour in production and consumption expenditures. To this end, the new World Uncertainty Index and data on 43 African countries from 2003 to 2018 are used. The two-step system generalised method of moments modelling framework was recruited for regression analysis. Results show that while infrastructure development boost industrialisation in Africa, global economic policy uncertainty and risk of uncertainty undermine these benefits after a given uncertainty threshold. The positive net effects were apparent up to respective global uncertainty and uncertainty volatility thresholds where these effects are nullified. When disaggregated proxies of infrastructure are used, similar results are obtained with transport and electricity. Practical policy implications are discussed.

Introduction

Long-term growth is thought to be sped up by industrialisation (Hausmann, Pritchett and Rodrik 2005; ONUDI 2002), which also lowers poverty (Cadot et al. 2016), boosts human capital development (Young 2012) and drives economic diversity that increases national investment (Duarte and Restuccia 2010; Ketu, Tchouto and Kelly 2022). Thus, in recent years, African countries reaffirmed their commitment to industrialisation as part of a bigger agenda to lower poverty, diversify their economies, increase formal jobs and better withstand shocks (UNCTAD and UNIDO 2011). Around the 1970s, the majority of these nations followed an import-substitution industrialisation strategy that involved manufacturing commodities needed to meet domestic demand locally and shielding domestic businesses from outside competition. The 1980s were designated by the continent as the ‘Decade for the Industrial Development of Africa’ acclaimed by the international community, particularly the United Nations Industrial Development Organization and the African Economic Community.

Sadly enough, the predicted results have not materialised, and the continent continues to lag behind in the global manufacturing trends (Ketu and Ningaye 2024; Totouom 2018). The failure of such enthusiastic aforementioned policies can be explained by many unanticipated factors (including economic and political uncertainty) when they are designed and implemented (Ketu, Ningaye and Tchounga 2024). Africa has not suffered only from global uncertainty but also from local uncertainty that emanated from the devaluation of the Franc Communauté Financière Africaine (CFA), its classification in the highly indebted poor countries initiative, just to name a few. As a result, Africa is classified as the least industrialised region globally. As shown by statistics from the World Bank (2019), the GDP contribution of the industrial sector in Africa fell from 37.96% in 1980 to 26.5% in 2015. Additionally, the manufacturing sector’s contribution to this continent’s GDP fell from 18% in 1975 to 11% in 2014, a relative decline of 38.8%, whereas Asia’s climbed by 8% over the same time period. This rendered the import-substitution strategies questionable. Indeed, if the widely held belief that industrialisation is essential for Africa to achieve its development goals is anything to go by (Landry 2018), then we agree with Nnyanzi et al. (2022) who assert that the implications of low and stagnant levels of industrialisation for economic transformation are a serious policy challenge in need of immediate empirical attention.

Unfavourable trade circumstances, low GDP per capita and economic slumps (Louri and Minoglou 2001), foreign direct investment (FDI) (Paus and Gallagher 2008), government policy (Lall 2004) and ineffective industrial technology coordination (Ciccone 2002) are some setbacks of industrialisation as per the extant literature. Similar to this, numerous studies focused specifically on Africa and have highlighted financial crisis (Shafaeddin 2005), FDI (Nkoa 2016), ratio of imports to exports, underdeveloped human capital (Ben Mim, Hedi and Ben Ali 2022; Totouom 2018) and environmental taxes (Tchapchet Tchouto et al. 2022). Nevertheless, the role of infrastructure development and economic uncertainty is still nascent, added to the divergences in findings, and the insufficiency of these factors in explaining industrialisation, particularly in Africa implies an inconclusive debate on the issue at hand.

The development of infrastructures is crucial for fostering growth and ameliorating the lives of Africans as it contributes significantly to all aspects of human development, poverty abatement and achieving sustainable development goals (Ketu and Wirajing 2024; African Development Bank 2018). Development economists have thus considered physical infrastructures such as telecommunications, roads, electricity and social infrastructure such as water supply, sewage systems, hospitals and school facilities to be a precondition for industrialisation and economic growth (Murphy, Shleifer and Vishny 1989). Erenberg (1993) cautions that if public infrastructures are not extended to them, domestic and multinational businesses will operate less effectively and below their optimal level. This is because they would be forced to incur additional costs to build their own infrastructures, which would result in duplication and waste of limited resources.

Despite Africa being ranked consistently at the bottom of all developing regions in terms of infrastructure performance (Bond 2016; Calderón and Servén 2010; Ketu 2023a), there are still notable improvements in infrastructure development in the region. For instance, the African Infrastructure Development Index (AIDI) highlights that between 2016 and 2018, practically all African nations saw improvements in all of their ratings for energy, ICT, transportation, and water and sanitation. Also, relative to other infrastructure forms, telecommunication infrastructure has not only experienced progress across all income groups in Africa but also doubled total access rates to sanitation (38% of population accessing the services) albeit still low relative to South Asia with 55%, Latin America and the Caribbean and East Asia (above 80%).

On the empirical front, while the economic growth importance of infrastructure development cannot be underestimated (Calderón and Servén 2010), there is still a missing link with regard to the extent to which infrastructure is important for industrialisation in particular. A few studies (Gafer and Saad 2009; Umofia, Orji and Worika 2018) focused only on single-country case studies with mixed findings. However, as Kodongo and Ojah (2016) acknowledge, it would be a worthwhile exercise to ascertain whether some public infrastructure is more important than others, and a new study reflecting this suggestion is needed. Furthermore, past studies ignore other types of infrastructure as well as the multifaceted nature of infrastructure development, in which electricity (Abokyi et al. 2018; Isaksson 2010), transport (Muvawala, Sebukeera and Ssebulime 2021), ICT (Njangang and Nounamo 2020), and water and sanitation are all captured. Exceptions that included different types of infrastructure are Azolibe and Okonkwo (2020), Nnyanzi et al. (2022), Malah Kuete and Asongu (2023) and Nkemgha, Nchofoung and Sundjo (2023).

Yet, none of the above studies addressed the marginal effects of global economic policy uncertainty (EPU) on the infrastructure industrialisation nexus. Our prime objective is, therefore, to fill this gap in the literature. Indeed, since the book ‘The age of uncertainty’ by John Kenneth Galbraith was published in 1977 (Galbraith 1977), a number of significant events have taken place, causing economic and political uncertainty i all over the world (Al-Thaqeb and Algharabali 2019). Keynes (1937), Bernanke (1983) and Bloom (2009) explain that the ‘wait-and-see’ attitude of investors caused by uncertainty could undermine potential positive effects of infrastructure on industrialisation by retarding both national and foreign investment (Avom, Njangang and Nawo 2020; Ketu, Ningaye and Tchounga 2024). To fill the gap, we employ a comprehensive dataset on 43 African countries which allows us to gain greater degrees of freedom. Also, we used a dynamic panel framework, unlike previous studies which mostly relied on static models ignoring the possible dynamic nature of the relationship between infrastructure development and industrialisation. In essence, most investments in infrastructure take time to be completed and also for the effects to be noticeable, adding to the fact that the previous level of industrial production matters for current production as entrepreneurs do base their projections on previous realisations (Keynes 1937). Moreover, we use the generalised method of moments (GMM) to handle endogeneity issues that appear omnipresent in most empirical studies. Results show that while infrastructure development boosts industrialisation in Africa, global EPU and risk of uncertainty undermine these benefits after a given uncertainty threshold.

The other sections of the article are structured as follows: Section 2 gives a review of the literature, Section 3 presents the data and estimation approach, Section 4 contains the findings and discussions, and the last part concludes with policy suggestions.

Infrastructure and Industrialisation: Theoretical Foundations

How Can Infrastructure Development Affect Industrialisation?

The existence of a sufficient and effective infrastructure should theoretically improve both the standard of living of the population and the rate of industrialisation. Infrastructures make significant contributions to advancing humankind, reducing poverty and realising sustainable development objectives (African Development Bank 2018; Ketu 2023a). Development economists have identified infrastructures as the basis for industrialisation and economic prosperity. Therefore, industrialisation and infrastructure go hand in hand in any economy’s pursuit of sustainable development (Ningaye and Ketu 2023; Umofia, Orji and Worika 2018).

A good number of studies on the endogenous growth theory (Barro 1990; Romer 1986) have documented the catalytic role played by infrastructures on the economic growth of nations. Eustace and Fay (2007) contend that strong infrastructure promotes economic growth, which in turn increases demand for infrastructure. For instance, the transportation system makes it easier for people and goods to move around, which encourages trade and production. Similar to how people can move information and money across borders for trade and production, communication systems also enable exchange of information. Energy is required for the production and delivery of goods from the locations of production to the locations of sale.

Trade in the integrated space is amplified by the presence of effective networks for transportation and trade infrastructure. According to the predictions of gravity models, the resulting decrease in transport costs leads to an increase in the market and the volume of transactions (Krugman 1980). Companies will benefit in ways other than price from the ensuing externalities. Centrifugal forces produced by this dynamic result in diffusion effects as a result of advantageous externalities related to the decrease in transportation costs between territories. The growth of Africa’s infrastructure has the potential to influence industrialisation through a variety of mechanisms and channels. The impact of ICT diffusion on industrialisation, for instance, can be felt through a number of different mechanisms. The first is the channel of starting new businesses. According to Njangang and Nounamo (2020), the diffusion of ICT is always associated with the emergence of new businesses, particularly in the manufacturing and service sectors. Start-ups are launched, typically in the production of practical technologies (using computers and the internet). New services can now be provided in the primary sector thanks to the introduction of ICT, which will impact industrialisation by impacting employment. African governments can use digital technologies to improve public administration’s support for industrialisation in addition to initiatives to assist African manufacturers in getting better access to digital inputs.

In order to improve industrial development, digitisation can help increase the productivity and efficiency of services related to manufacturing, such as general logistics and customs administration (Oulton 2002). Particularly in the context of the African Continental Free Trade Area, digitisation of customs administration can aid in enhancing the effectiveness of customs, lowering trade costs and promoting more intra-African trade, all of which would support the expansion of the continent’s industrialisation (Nkemgha, Nchofoung and Sundjo 2023).

Moreover, energy infrastructure is important for industrialisation, particularly the transportation of goods and services and manufacturing of raw materials into both semi-finished and finished products (Malah Kuete and Asongu 2023). Finally, water supply and sanitation not only remains an important input in itself for manufacturing activities but also helps the primary sector to provide quality input for the industry.

The Role of Global Economic Policy Uncertainty

Although uncertainty is very difficult to estimate, it directly affects economic activities (Baker, Bloom and Davis 2016). Global EPU can affect both infrastructure development and industrialisation. It has been shown among others that uncertainty inhibits investment activities (Baker, Bloom and Davis 2016; Gulen and Ion 2016), reduces domestic credit (Hu and Gong 2019) and increases exchange rate volatility (Krol 2014), thus hindering industrialisation and reducing economic growth (Kang, Ratti and Vespignani 2019).

Bernanke’s theory of irreversible choice under uncertainty, established in 1983, provides a theoretical framework for understanding cyclical changes in investment as well as assessing the consequences of uncertainty on investment in general and industrialisation in particular. The detrimental consequences of uncertainty on industrialisation might thus be attributed to investment volatility and investors’ ‘wait-and-see’ mentality. First, according to Keynes (1937), investments are the most erratic component of effective demand because they are more dependent on opinions about future events, and any negative opinions about future events will cause investments to fall, especially if investments are irreversible (Bernanke 1983; Bloom 2009).

However, while most research see EPU as a negative component in economic development, other perspectives have developed. Gabauer and Gupta (2018) found that EPU has a favourable impact on economic production during downturns. According to Leduc and Liu (2016), EPU does not always cause economic volatility but may actually stimulate economic production by encouraging corporate innovation (Brogaard and Detzel 2015) and supporting the manufacturing industry (Kang, Lee and Ratti 2014). Overall, while the effects of infrastructure development and EPU are growing up separately, no known study has considered their joint effects on industrialisation. Our goal is thus to fill this gap for the case of African countries whose low performance in infrastructures coupled with weak industrial structure in an uncertain atmosphere fuels the interest for an empirical investigation.

Methodology and Data

Data

The data used in this article constitute of a panel of N = 43 African countries

ii

covering the period 2003–18 (T = 16). The data is collected from the African Development Bank, Ahir, Bloom and Furceri (2018) at

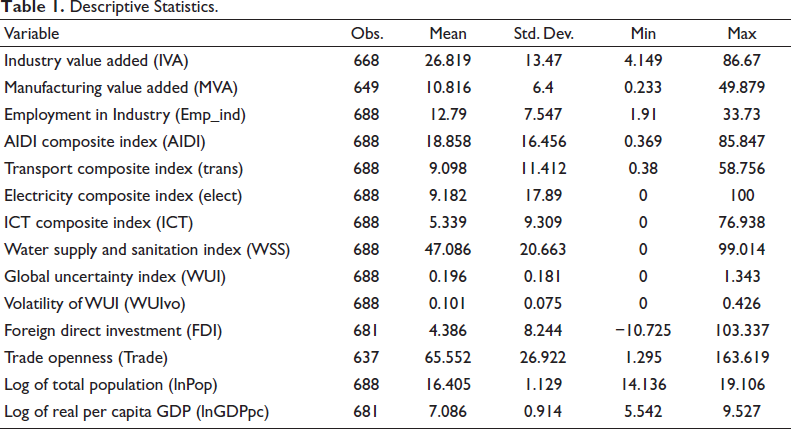

The total number of observations is given by T(16) × N(43) = 688. Missing data is thus reported for variables such as FDI, trade and GDP per capita. Our panel is therefore unbalanced. These data from Table 1 have a low overall degree of heterogeneity, with the majority of the variables clustered around their averages, according to a preliminary assessment. iii This feature can be seen in the proportionality of the first two moments (mean and standard deviation) of the distributions corresponding to these variables.

Descriptive Statistics.

Descriptive Statistics.

Dependent Variable

Based on the World Bank classifications, industrial activities include value added in construction, mining and manufacturing (note that the manufacturing sector at times is also reported as a separate subsector). The net output or value added of a sector is the sum of all the sector’s outputs minus all the inputs used in the production process. It is calculated without taking into account the deterioration of natural resources, the depreciation of manufactured goods or value losses. Data are expressed as a percentage of GDP in current US dollars. For robustness purpose, other proxies such as employment in industry and manufacturing value-added to GDP are used. These variables are extracted from the World Development Indicators database. Several studies investigating the drivers of industrialisation also used these proxies (see Gui-Diby and Renard 2015; Njangang and Nounamo 2020; Nkemgha, Nchofoung and Sundjo 2023).

Variables of Interest

Infrastructure Development

Following the African Development Bank, infrastructure is measured in this work using the AIDI. AIDI is a composite index which captures progress of infrastructures across the African continent. However, we also include four disaggregated major components of AIDI; water and sanitation systems, transport, ICT and energy access. Other studies also used theses proxies including Ketu (2023b), Malah Kuete and Asongu (2023), and Azolibe and Okonkwo (2020).

World Economic Policy Uncertainty

Regarding economic uncertainty, while the Economic Policy Uncertainty (EPU) index of Baker, Bloom and Davis (2016) appears among the most popular indicators, data on this index is only available for a few advanced countries. Meanwhile, the new World Uncertainty Index iv (WUI) by Ahir, Bloom and Furceri (2018) is more advantageous as it covers this shortcoming, available quarterly for 143 countries from 1996 onwards. According to Ahir, Bloom and Furceri (2018)’s analysis, there is a significant correlation between WUI and EPU, suggesting that the former is reliable to capture economic uncertainty. Additionally, the WUI index is based in part on news from widely read newspapers in each country, despite the fact that these newspapers vary from nation to nation. The Economist Intelligence Unit reports, which are defined using the frequency of the word ‘uncertainty’, serve as the foundation for all of the data used to compute the WUI. Therefore, there are two reasons why the WUI could be superior for cross-country comparison. The index, first and foremost, is based on a single source that covers specific topic: political and economic changes. Second, the reports adhere to a uniform procedure and format (Ahir, Bloom and Furceri 2018). Furthermore, recent research show that economic factors depend on both the magnitude and volatility of economic uncertainty (Nguyen, Binh and Duyen 2022). We compute the quarterly data’s annual standard deviation in accordance with these guidelines to represent the volatility of economic uncertainty (WUIvo). Every variable has two key characteristics: level and volatility. Level changes might not necessarily coincide with volatility changes (Engle 2004). According to Brooks and Persand (2003), changes in volatility represent whether fluctuations are up or down in an index, whereas changes in level reflect rise or decline in values. Other studies have also used these indicators as proxy for economic uncertainty (see Avom, Njangang and Nawo 2020; Ekeocha et al. 2023; Ketu, Ningaye and Tchounga 2024; Nguyen, Binh and Duyen 2022).

Figure 1 reveals rising uncertainty over the past three decades which reached unprecedented level in 2020 with the upsurge of the COVID-19 pandemic.

Source: Ahir, Bloom and Furceri (2018).

Foreign Direct Investment

Following the World Bank, FDI is the net inflow of investment to acquire a lasting interest (10% or more of the voting shares) in an enterprise operating in an economy other than that of the investor. As for the relationship between FDI and industrialisation, results are mixed. Nkoa (2016) found that host countries could benefit from FDI through different channels, such as upstream and downstream links and technology transfers. Unlike these authors, Gui-Diby and Renard (2015) found that FDI has no effect on industrialisation and that FDI could rather crowd out domestic investment (Mignamissi and Ngeukeng 2022).

Population

It is measured as the total population. The total population counts all residents regardless of citizenship or legal status. The values displayed are midyear estimates. Aghion and Howitt (1990) argue that a large population creates the demand for technological change and therefore stimulates industrialisation and economic growth. But in the case of African nations, it might instead have a perverse effect. Indeed, due to the low level of population involvement in development, its growth could be detrimental to industrialisation, particularly in Africa (Mignamissi and Ngeukeng 2022). Most African countries have populations that are marked by poverty, inequality and a low human capital—factors that do not support economic dynamism and, consequently, industrialisation.

Trade Openness

Trade openness as used in this study is defined by the sum of imports and exports as a percentage of GDP. The data on this variable is extracted from the World Development Indicators. Following the narrative of the proponents of international trade (such as Smith and Ricardo), immense opportunities await countries that engage in trade (such as opportunities to specialise, expansion of target markets, knowledge diffusion and many more).

Income Per Capita

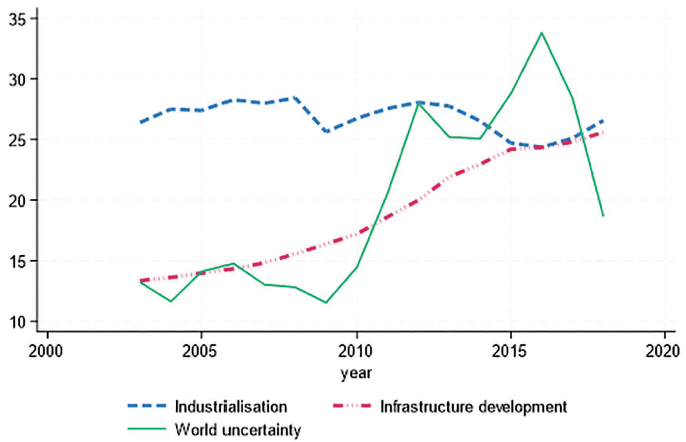

This variable is measured in real values and expressed in per-capita terms. Income per head can also be seen as a proxy for the level of development. Aghion and Howitt (1990) posit that when income per head increases, consumption preferences may also change in favour of manufactured goods. The variables of interest in this study are represented in Figure 2. It can be seen from this figure that while infrastructure development has been steadily increasing, industrialisation has not kept pace and is at best stagnating. At the same time, uncertainty is drastically rising.

Trend of Main Variables.

Trend of Main Variables.

Based on the works of Gui-Diby and Renard (2015), Azolibe and Okonkwo (2020) and Nkemgha, Nchofoung and Sundjo (2023), the following empirical model is adopted.

where

Given that the objective of this article is not limited to the determination of direct effects of infrastructures on industrialisation but also indirect effects through global policy uncertainty and volatility of uncertainty, we therefore reformulate Equation (1) as follows:

In this case,

Given that the estimation technique used is based on interactive regressions, we briefly discuss certain problems to avoid. These include (1) according to Brambor, Clark and Golder (2006), all constitutive phrases must be included in the specifications. (2) Furthermore, to give the estimates economic meaning, the calculated interaction parameters are interpreted as conditional or marginal effects. (3) Furthermore, for the resultant threshold to make economic sense, it must fall within the range indicated by the summary statistics, and both the direct and marginal (conditional) impacts must be statistically significant.

That said, net effects can be computed from the interactive regression by taking the first (partial) derivative of (2) with respect to any of the interaction variables as follows:

where

The solution to Equation (4) is therefore simply the ratio of direct effect coefficient to the indirect coefficient.

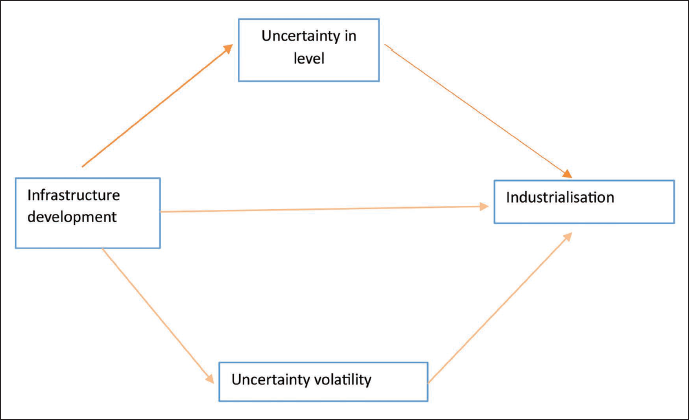

Following the formulation of the econometric model and theoretical underpinnings discussed earlier, the relationship between world uncertainty, its volatility, infrastructure development and industrialisation is summarised in Figure 3.

The Relationship Between Uncertainty, Infrastructure and Industrialisation.

This study makes use of Blundell and Bond’s (1998) two-step GMM estimator. Several considerations affected the decision to use this regression approach. First and foremost, our temporal dimension is less than the cross-sectional dimension. Roodman (2009b) states that a GMM can only be employed in a regression if the cross-sectional dimension is bigger than the temporal dimension, which is the situation with our data. Second, when estimated using OLS approaches, the lagged dependent variable correlates with the fixed effect in the error term, resulting in a dynamic panel bias (Nickell 1981). The GMM estimate approach reduces this bias and effectively manages cross-country dependency across panels (Ningaye and Ketu 2023).

The pitfall of having too many instruments is the main issue that is typically associated with GMM estimation. Although there is not a specific threshold for how many instruments are considered excessive, Roodman (2009a) extended Arellano and Bover’s (1995) forward orthogonal deviation approach to limit the number of instruments below panels and increase sample size. Instead of subtracting earlier observations from the subsequent ones, this method’s computational methodology subtracts the average of all upcoming observations of a variable that are currently available. As a result, the number of lags that could continue to be orthogonal to the error and useful as instruments in the regression is constrained. In order to prevent an instrument proliferation problem, we use the aforementioned forward orthogonal deviation methodology in this study. We used the two-step procedure in place of the one-step procedure to control for heteroscedasticity because the one-step procedure is only consistent with homoscedasticity.

The GMM procedure in level and in difference is summarised in the following equations:

The problems of identification, simultaneity and restrictions are also well handled in the GMM estimation. Accordingly, we treat all of our control variables as endogenous in accordance with recent literature (Nkemgha, Nchofoung and Sundjo 2023; Ningaye and Ketu 2023). In addition, period dummies are employed as instruments in the difference equations. Within this framework, Roodman (2009b) argued that time-invariant variables are unlikely to be endogenous after a first differencing. Lags of the variables are employed as instruments in the differenced equation while the level equation is instrumented with lagged differences of the variables. The absence of second-order serial correlation and validation of Hansen test guarantees the validity of the system GMM.

Preliminary Evidence

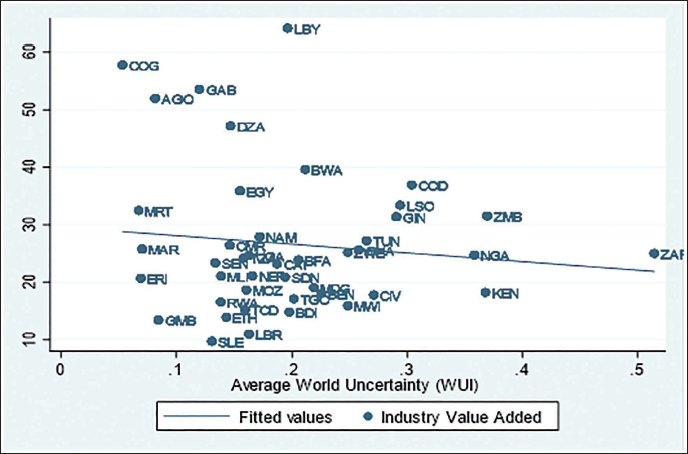

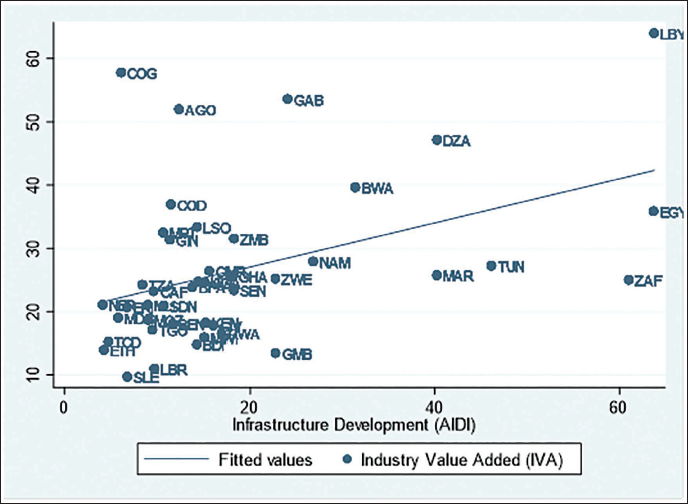

It is common in the scholarly literature to start the presentation of results of an empirical study with a preview and simple representation of variables of interest. Figure 4 thus presents a scatter plot of uncertainty and industrialisation. The figure shows a negative correlation between uncertainty and industrialisation. Meanwhile, a positive relationship is perceived in Figure 5 between the overall index of infrastructure development (AIDI) and industrialisation in the selected sample. From these figures, we could conclude of respectively a positive and negative association between infrastructure development and economic uncertainty with industrialisation. But what about their conditional effects? This question leads us to further analysis notably, through econometric regressions in order to complete the puzzle and robustly assess these correlations given that association does not necessarily imply causation. This further analysis is discussed in the next sub-section.

Scatter Plot Between World Uncertainty and Industrialisation.

Scatter Plot Between World Uncertainty and Industrialisation.

Scatter Plot Between Infrastructure and Industrialisation.

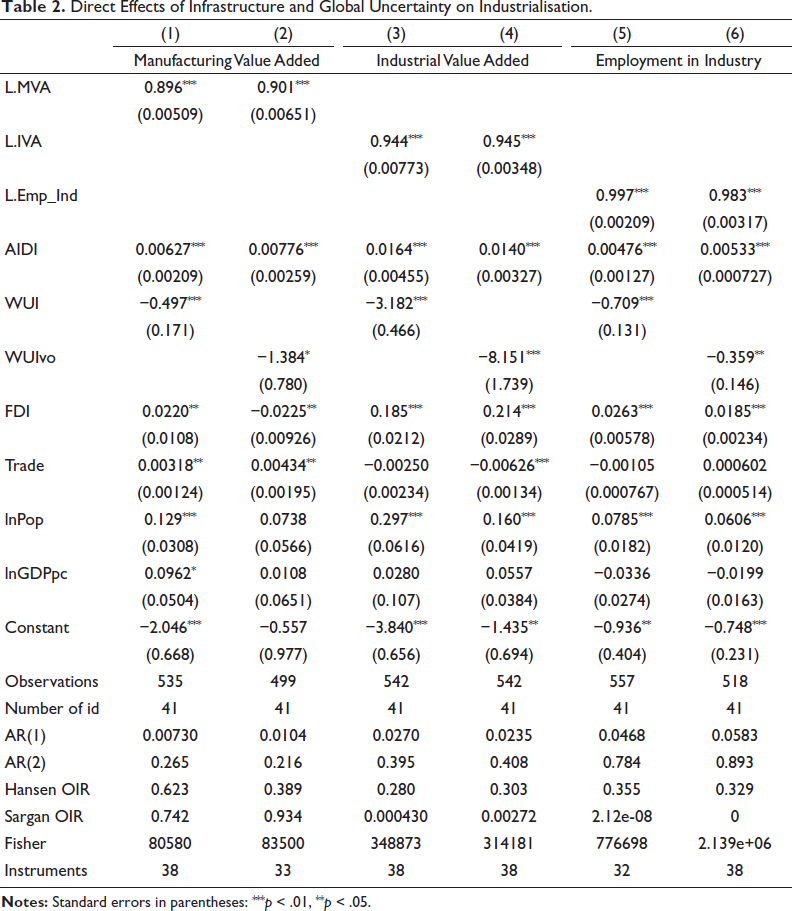

Direct Effects of Infrastructure and Global Uncertainty on Industrialisation

Table 2 presents the direct effects of infrastructure development and economic uncertainty on industrialisation in African countries. The analysis is based on a two-step dynamic system GMM regression of Blundell and Bond (1998). The main dependent variable is industrial value added though we also employed manufacturing value added and employment in industry as alternative explained variables for robustness checks.

Direct Effects of Infrastructure and Global Uncertainty on Industrialisation.

Direct Effects of Infrastructure and Global Uncertainty on Industrialisation.

Following common practice, we begin the interpretation with diagnostics checks. The AR(1) test reveals the presence of first order autocorrelation of residuals. This result is expected by construction of the system GMM. It results from the presence of the lagged dependent variable among the regressors. As seen from the p value of the AR(2), we do not reject the null hypothesis of no second-order serial correlation implying that our estimates do not suffer from second-order serial correlation. Also, associated p values of the Hansen and Sargan tests of over-identifying restrictions (OIR) are reported. In essence, the Hansen OIR test is robust but weakened by many instruments, in contrast to the Sargan OIR test which is not robust but not weakened by instruments. We have based our interpretations on the Hansen test making sure that instruments are smaller than the number of cross-sections in the majority if not all of specifications in order to restrict identification or limit the proliferation of instruments (Roodman 2009a). Lastly, the Fisher statistics of overall significance reassure consistent estimates.

Irrespective of the proxy of industrialisation considered, the lagged dependent variable is positive and significant across all specifications. As these coefficients associated to the lagged dependent variable are greater than 0 but less than 1, it implies that there is conditional convergence among countries of the sample. Thus, African countries with low levels of industrialisation are catching up with their counterparts with high industrialisation. However, the important caveat to note here is that conditional convergence depends largely on the set of controls considered (Asongu 2013).

Regarding the composite infrastructure index (AIDI), it is positive and significant at 1% level. This means that on average, a 10% increase in infrastructure would lead to a 0.06, 0.15 and 0.05 increase in manufacturing value added, industrial value added and employment in industry, respectively. Azolibe and Okonkwo (2020) used a panel of 17 sub-Saharan African countries to arrive at a similar conclusion. Also, Nkemgha, Nchofoung and Sundjo (2023) whose analysis is based on panel data on 33 African countries support these findings.

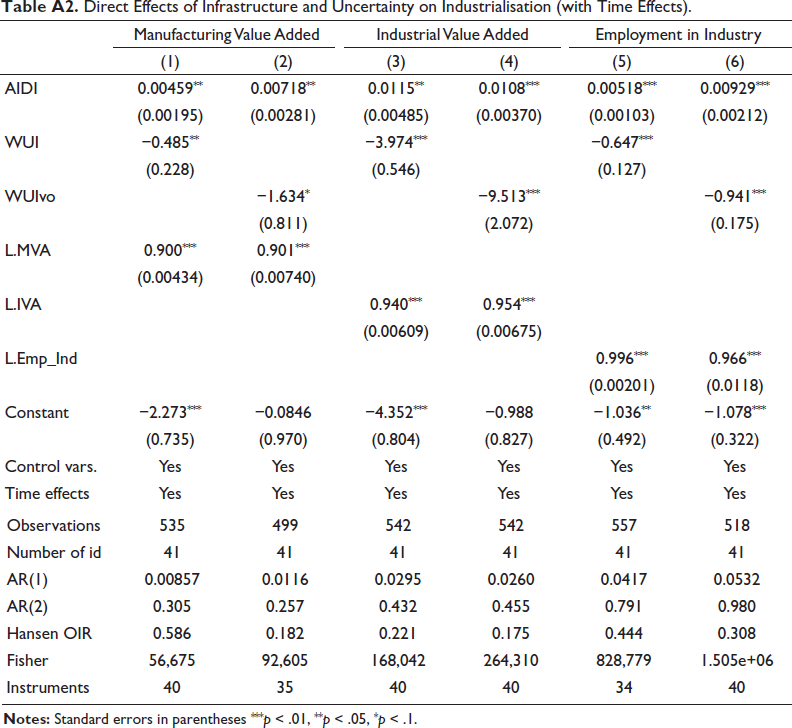

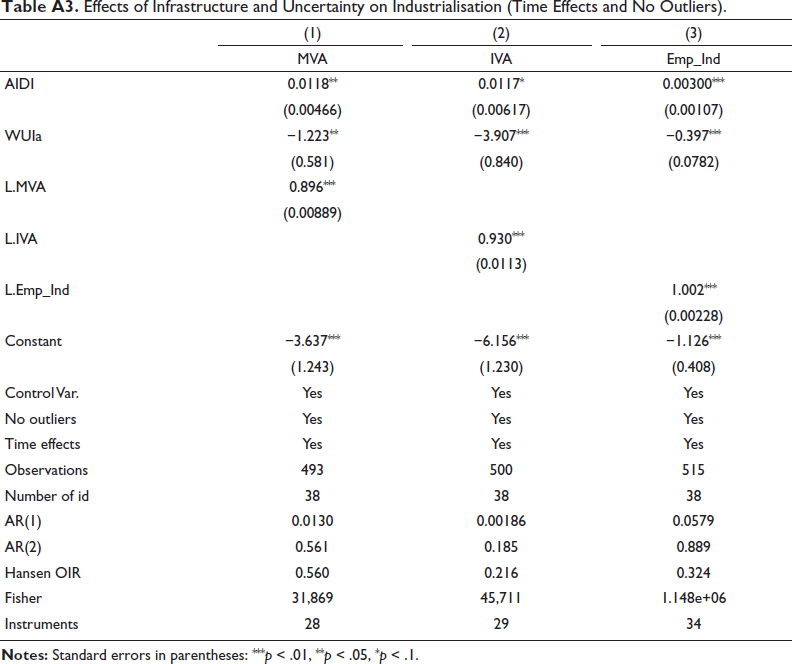

Negative effects of both volatility and level of economic uncertainty are reported. These negative effects appear to be more severe for the risk of uncertainty than uncertainty at level. These results are not surprising given the negative effects’ economic uncertainty on other macroeconomic variables such as inhibiting investment activities (Baker, Bloom and Davis 2016; Gulen and Ion 2016), reducing domestic credit (Hu and Gong 2019), reducing employment (Caggiano, Castelnuovo and Figueres 2017) and increasing exchange rate volatility (Krol 2014). Also, Zhu and Yu (2022) found that higher levels of economic uncertainty negatively affect industrial output of the Chinese economy. These findings come in confirmation of the ‘wait-and-see’ behaviour of investors popularised by Keynes (1937) and Bernanke (1983) which turn to paralyse investment activities, especially if the latter is irreversible including foreign investment (Avom, Njangang and Nawo 2020). These results are similar to those of Ketu, Ningaye and Tchounga (2024) who found that EPU impedes industrialisation in a cross-country framework. Interestingly, when outliers, country and time effects are considered and removed as shown in Tables A2 and A3, results remained consistent, indicating that the leverage due to outliers and individual heterogeneity is of lesser concern in our sample.

Regarding other control variables, trade openness, FDI, population growth and income per head all have enhancing effects on industrialisation though the effect of GDP per capita is weak.

In Table 3, economic uncertainty at level is interacted with infrastructure composite indexes to yield positive net effects. This net effect is given by [0.0248–0.0469 (0.19629) = 0.0156] where 0.0248 is the unconditional effect, −0.0469 is the marginal (conditional) effect and 0.19629 is the mean of economic uncertainty as apparent in the summary statistics table. Thus, infrastructure development will continue to enhance industrialisation in African countries up to a given economic uncertainty threshold where this effect is nullified and becomes negative. Specifically, when uncertainty reaches a threshold of 0.53, the positive effect of overall infrastructure becomes nil. Therefore, industrialisation in Africa will benefit from infrastructure development only if uncertainty is kept below a threshold of 0.53. This result is consistent with the literature and with Zhu and Yu (2022) who argued that uncertainty will stimulate technological progress to enhance positive effects on industrial output. In other studies, Nkemgha, Nchofoung and Sundjo (2023) found a similar result when they interacted human capital and infrastructure on industrialisation, reporting a human capital threshold at which the positive effect of infrastructure is nullified.

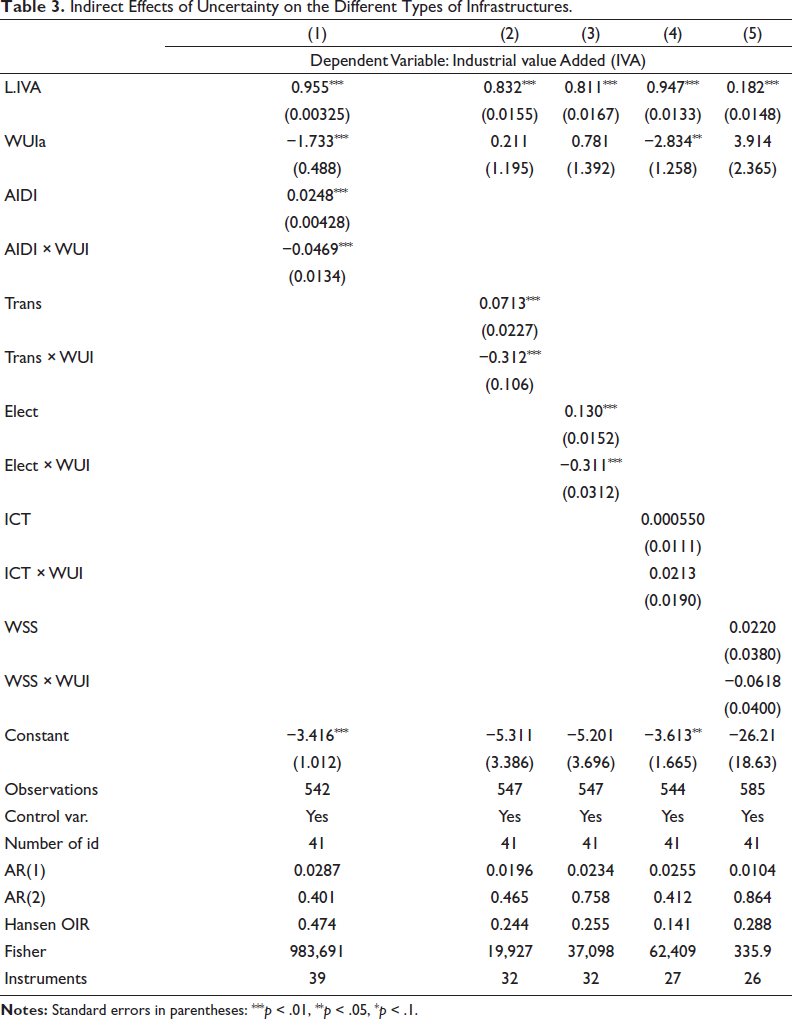

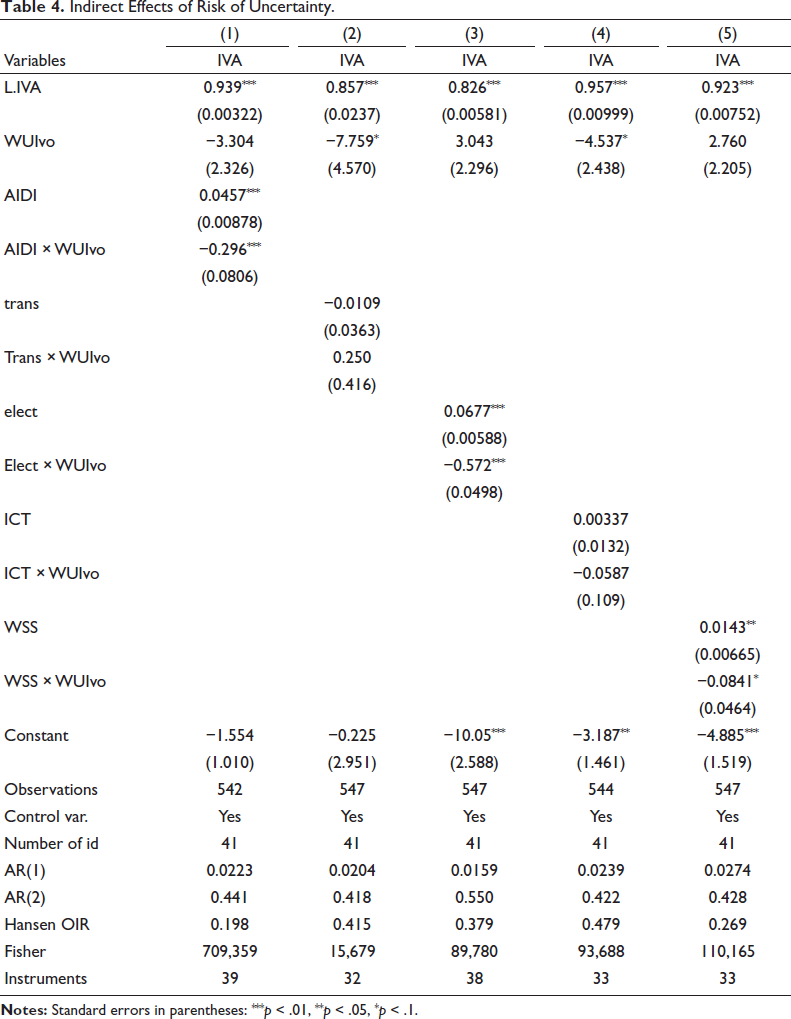

Indirect Effects of Uncertainty on the Different Types of Infrastructures.

Indirect Effects of Uncertainty on the Different Types of Infrastructures.

Looking at sub-components of infrastructure, only transport and electricity interacted with global economic uncertainty to yield positive net effects of 0.01 and 0.06, respectively, while ICT and water supply and sanitation did not give significant results. This result suggests that at low global uncertainty (i.e. below 0.23 for transport and 0.42 for electricity), upgrades are stimulated in the transport and electricity infrastructures which in turn promote industrial value added. However, the ‘wait-and-see’ behaviour of investors sets in to override this effect when uncertainty exceeds the threshold of 0.42. In Table 4, global uncertainty volatility is interacted with infrastructure to also yield total positive effects. This total (net) effect is given by [0.0248 − 0.0469 (0.101) = 0.0157] and the corresponding threshold is 0.0248/0.0469 = 0.15. These results are quite similar to those of global uncertainty at level.

Indirect Effects of Risk of Uncertainty.

Regarding the control variables, the positive effect of FDI is consistent with the work of Nkoa (2016). He concluded that host nations may gain from FDI through a variety of routes, including upstream and downstream connections, as well as technological transfers, which would increase industrialisation. This outcome however contradicts Gui-Diby and Renard (2015) who found that FDI had no significant effect on industrialisation for the case of 49 African countries during the period 1980–2009. The positive effect of population growth follows Aghion and Howitt (1990) argument that a large population creates the demand for technological change and therefore stimulates industrialisation and economic growth by acting as a source of demand and supplying labour. Finally, Mignamissi and Ngeukeng (2022) explained that openness to trade could be beneficial for industrialisation. But the failure of the import-substitution strategies as explained earlier in this article could explain why most African countries still cannot fully benefit from openness to trade. Most of its demand is highly imported spanning from simple manufactured goods like foodstuff and clothing to others like automobiles.

The inability of most African countries to structurally transform their economies through industrialisation, by providing formal jobs and significantly reducing poverty, remains a call for concern. Despite a plethora of studies in this area, only few considered the role of infrastructure development reporting mixed results, failing to discuss transmission mechanisms, and none of them focused on the interactive effects of world EPU, exacerbated today by increasing globalisation. To cover this lacuna, a theoretical discussion on how infrastructure and global EPU may affect industrialisation is first discussed before building a dataset on a panel of 43 African countries from 2003 to 2018 for empirical investigations. Three proxies (industrial value added, manufacturing value added and employment in industry) were mobilised to capture industrialisation, the dependent variable. Infrastructure development was measured using the composite index, AIDI and its four disaggregated components (transport, ICT, electricity and water supply and sanitation) provided by the African Development Bank while global uncertainty was measured both in level and in volatility using the new WUI by Ahir, Bloom and Furceri (2018). The two-step system GMM modelling framework was recruited for regression analysis. The results show that first, infrastructure development enhances industrialisation in African countries while global economic uncertainty as well as the risk of uncertainty negatively affect industrialisation in the region. Second, when economic uncertainty as well as the volatility of uncertainty interact with infrastructure, negative marginal effects emerge. These negative conditional effects are overridden by the direct positive effects to yield total positive effects. The positive net effects were apparent up to respective global uncertainty and uncertainty volatility thresholds of 0.53 and 0.15 where these effects are nullified. When other measures of infrastructure are used, similar results are obtained with transport and electricity while ICT infrastructure had no modulating effect on the infrastructure–industrialisation relationship. The results were robust to the consideration of country and time effects, and the exclusion of outliers. Therefore, policies aiming to improve industrialisation in Africa should not ignore rising uncertainty levels that could undermine potential benefits of infrastructure development.

Some policy implications emerge from these findings. While industrialisation policies will be optimal should proper infrastructures are put in place, caution must be taken by African leaders and policymakers. In essence, attention should be paid to rising uncertainty levels and higher risk of uncertainty. To be specific, when global uncertainty exceeds the threshold of 0.53, other policies should be put in place to encourage industrialisation, such as good governance which could guarantee the ease of doing business and override the ‘wait-and-see’ behaviour, a major setback to industrialisation in periods of rising uncertainty in the region.

As caveats, it would be interesting for future research to also consider the role of domestic policy uncertainty, which is gaining ground in Africa as a result of internal conflicts, coups d’états and terrorism. Country-specific case studies are also welcomed for their strong/specific policy targets.

Appendix

Pairwise Correlations.

Direct Effects of Infrastructure and Uncertainty on Industrialisation (with Time Effects).

Effects of Infrastructure and Uncertainty on Industrialisation (Time Effects and No Outliers).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.