Abstract

The study finds a considerable increase in non-statutory (tied) transfers, particularly evident after the abolition of the Planning Commission. Centrally sponsored schemes (CSS) constitute the largest portion of these non-statutory grants. Although the number of CSS has increased over time, the overall financial allocation has fallen during the last few years. A significant structural shift occurred in 2023–2024: the number of CSS schemes was first raised to 75 and then further to 82, while the previous rationalized categorization of ‘Core of Core’ and ‘Core’ schemes was simultaneously discontinued. The state-wise analysis shows that states such as Kerala, Haryana and Punjab receive the lowest per capita CSS compared to other states. The problem is compounded by implementation issues, as evidenced by the significant gap between the budgeted and actual CSS flows to Kerala.

Keywords

Introduction

Fiscal federal transfers are critical for the development of sub-national governments in federal countries like India. India’s federal system operates within a framework where fiscal powers are shared between union and state governments. However, the design of this fiscal federalism is fraught with long-standing issues and challenges that continually shape inter-governmental relations. Inter-governmental transfers are intended to provide public goods and basic services across different regions, guided by principles of equity and efficiency (Bird & Smart, 2002; Kohli, 2024). The twin problems associated with fiscal federalism are vertical and horizontal fiscal imbalances (Chakraborty, 1998; Chakraborty & Chakraborty, 2018; Kelkar, 2019; Mohan & Ramakumar, 2024; Ramakumar, 2024; Rangarajan & Srivastava, 2008; Rao & Singh, 2004). Like in other federal countries, growing fiscal imbalances in resource sharing pose a major challenge for India as well. In the Indian federal set-up, transfers include general-purpose and specific-purpose transfers. General-purpose transfers are recommended by the Finance Commission (FC), a constitutional body, while specific-purpose transfers are routed through various Union Ministries (Gupta et al., 2025; Rao, 2015).

The grants-in-aid include statutory Finance Commission grants and non-statutory grants. Non-statutory grants, in turn, include centrally sponsored schemes (CSS), central sector schemes and other grants. While statutory grants are generally unconditional, non-statutory grants are largely discretionary in nature (Rao, 2015). These fiscal imbalances raise several concerns regarding the developmental needs of the states, as resource transfer plays a significant role in their revenue mobilization. This is particularly important at a juncture where state-level development is key to meeting the targets of Sustainable Development Goals and other national development indicators. This context has become even more significant following the abolition of the Planning Commission and the subsequent removal of plan grants to the states. Of late, many discussions have centred on the growth of discretionary transfers, issues pertaining to the central design of schemes (often criticized as a ‘one-size-fits-all’ approach), and their impact on state finances (Kumar, 2022; Varghese & Anilkumar, 2023). Given this context, the present study explores the nature and composition of federal transfers in India by examining both general-purpose and specific-purpose transfers to the states. Specifically, the study analyses in detail the structure of discretionary transfers, mainly focusing on CSS and their changing nature in India.

The paper is organized as follows: Section two deals with the review of literature encompassing analytical and empirical studies on the research area. The details of the data sources used in the study is discussed in the third session. Fourth session provides the discussion on the resource transfer to the states by the union government which includes statutory and non-statutory grants, Centrally Sponsored Schemes, CSS and states’ development, gap between actual and budgeted CSS, and its burden on the state governments. The final session concludes the paper.

Review of Studies

The review of literature presented in this study covers both analytical and empirical works on different aspects of the fiscal federalism such as constitutional provisions on resources sharing, vertical and horizontal fiscal imbalances in resource devolution and issues pertain to conditional and unconditional grants.

Analytical Studies

The theory of fiscal federalism is anchored in Richard Musgrave’s three functions of the public sector: allocation, distribution and stabilization. Specifically, the allocation function, which advocates for the decentralized provision of public goods to better match with local preferences and needs, owes a significant intellectual contribution to the work of Wallace Oates. Despite these theoretical underpinnings, the major practical issue confronting fiscal federal transfers is the presence of vertical and horizontal fiscal imbalances. In India, these twin problems are the results of both constitutional assignment of powers and the subsequent execution of federal fiscal arrangements over time. These imbalances have been consistently high and, in fact, have been increasing (Mohan & Ramakumar, 2024). The vertical imbalance arises from the delink between revenue-raising and expenditure requirements between the union and states, which affects fiscal responsibility and management at both levels (Rao & Sen, 1995).

The horizontal imbalance, on the other hand, stems from the difference in fiscal capacities and fiscal needs among sub-national governments, resulting in varying resource gaps across states. The persistent spending pressure, combined with insufficient revenue generation at the state level, has further intensified states’ reliance on inter-governmental transfers. Although several reforms have been adopted, a satisfactory resolution to India’s fiscal imbalances remains elusive today (Darshini & Gayithri, 2024). The Indian Constitution provides the primary mechanism for resource sharing. According to Article 270 (post-80th Constitutional Amendment), the net proceeds of all taxes levied by the union government excluding surcharges and cesses are shareable with the states. However, transparency in the calculation of these net proceeds has been a point of concern (Ramakumar, 2024).

Overall, the transfer of resources to states comprises tax devolution, statutory grants (under Article 275 based on FC recommendations) and discretionary grants. These transfers are further classified into tied (conditional) and untied (flexible) grants. Tied grants come with specific schemes and conditionalities, leaving state governments with no flexibility in spending. An example is CSS. However, untied grants, such as tax devolution and FC-recommended post-devolution revenue deficit grants, have no conditionalities attached, allowing states greater autonomy. While statutory grants (both tax devolution and unconditional grants) are decided by the FC, non-statutory (discretionary) grants are provided by respective Union Ministries (Isaac et al., 2019). The quantum of these discretionary transfers is often influenced by factors such as fiscal performance, economic capacity and political alliances (Nayak & Satpathy, 2021).

The existing literature offers a rich debate on the design and impact of these transfers. Unconditional transfers (e.g., tax devolution) are praised for promoting state autonomy, as they allow states to allocate funds according to their own priorities. In contrast, conditional transfers are earmarked for specific purposes and cannot be diverted. Conditional transfers, particularly the CSS, are frequently criticized because states are often compelled to invest in central schemes to secure funding, even if those schemes do not align with their unique developmental needs or priorities (Das & Mitra, 2013; Saxena et al., 2023; Varghese & Anilkumar, 2023).

Empirical Studies

The state governments in India are heavily dependent on union transfers to meet their growing expenditure requirements, a situation that highlights the severe vertical fiscal imbalance. As quantified by the 15th FC, the union government generates 63% of resources but accounts for only 38% of the expenditure, while the states, generating only 37% of revenue, are burdened with 62% of the expenditure. Addressing this and the associated horizontal and developmental imbalances, Kelkar (2019) argues for a fundamental re-examination of the existing fiscal federal system, including constitutional provisions for sharing GST proceeds with local self-governments. Empirical evidence underscores the severity of this issue: a study on 24 major Indian states (1995–1996 to 2014–2015) revealed that a 1 percentage point decline in vertical fiscal inequality corresponded to an average 15 percentage point decline in the state governments’ primary deficit as a proportion of net state domestic product (NSDP; Koley & Mandal, 2019).

A major factor exacerbating the vertical imbalance is the union government’s increasing reliance on cesses and surcharges, for which no constitutional provision mandates sharing with the states. Though originally intended as temporary measures to mobilize resources for specific schemes, their share has recently surged to between 25% and 30% of the union government’s gross tax revenue. This practice significantly reduces the size of the divisible pool. For instance, a case study on the education cess highlights the strain: while state governments contribute a significant 15%–20% of their total expenditure to education, the union government accounts for less than 10%. Furthermore, nearly half of the Union Ministry’s education expenditure is raised through this cess, which is a substantial one fourth of the total public expenditure on education (union and states combined; Motkuri & Revathi, 2023). This mechanism raises critical questions about how states are expected to raise additional resources to meet their growing educational obligations.

While tax share and grants-in-aid are crucial for state development, the mechanism designed to address horizontal fiscal imbalances is also subject to criticism. The devolution criteria used by the FC, which are meant to ensure the equitable provision of public services at comparable costs, have been criticized for ignoring state-specific factors in favour of common ones such as population, poverty and backwardness (Sarma, 1997). Specifically, the use of old population census data and per capita gross state domestic product for measuring income distance has been largely criticized (Srivastava, 2010). The FC attempts to achieve equity by assigning a higher weight to the income distance criterion, assuming that per capita income positively correlates with fiscal capacity. However, empirical evidence suggests the opposite: that fiscal capacity often declines with rising per capita income, effectively penalizing high-income states through the income distance criterion (Joseph & Kiran, 2025). Even after post-fiscal adjustments, the revenue gap still persists in a majority of states due to growing expenditure needs and poor revenue performance.

Beyond tax devolution, grants-in-aid play a significant role in states finances. However, the most debated issue regarding grants in recent times is the design and implementation of CSS. These grants are intended to bridge vertical fiscal imbalances, yet the major criticism is the union government’s tendency towards a ‘one-size-fits-all’ central design and uniform implementation across all states. This approach is problematic because Indian states have attained different levels of development and possess varied spending priorities. For example, a socially developed state like Kerala has achieved high levels of development in sectors such as education and health. Consequently, basic schemes aimed at primary improvement in these social sectors may not align with its specific, advanced developmental needs. Similarly, all other states have unique requirements and priorities that are often overlooked by centrally designed, discretionary schemes.

Data Sources

The data for this study were drawn from the publications of the Controller and Auditor General (CAG) and state governments. Information on FC grants and non-statutory grants, along with the total expenditure of the union government, was sourced from Budget at a Glance, published annually as part of the Union Budget documents (Government of India, n.d.a). Scheme-wise and total CSS data were collected from the Expenditure Profile section of the Union Budget (Government of India, n.d.b). To analyse state level variations, state wise CSS data were compiled from the finance accounts of the respective state governments published by the Comptroller and Auditor General of India. Additionally, specific budgeted CSS information for Kerala, Karnataka and Tamil Nadu was gathered from their respective state budgetary documents: the Budget in Brief (Government of Kerala, n.d.), Budget Volumes (Government of Karnataka) and Budget Documents (Government of Tamil Nadu). The data on budget outlay of CSS for the period 2024–2025 have been collected from the Annual Plan Proposals 2024–2025, Kerala State Planning Board, Government of Kerala.

Resource Transfers to the States by the Union Government

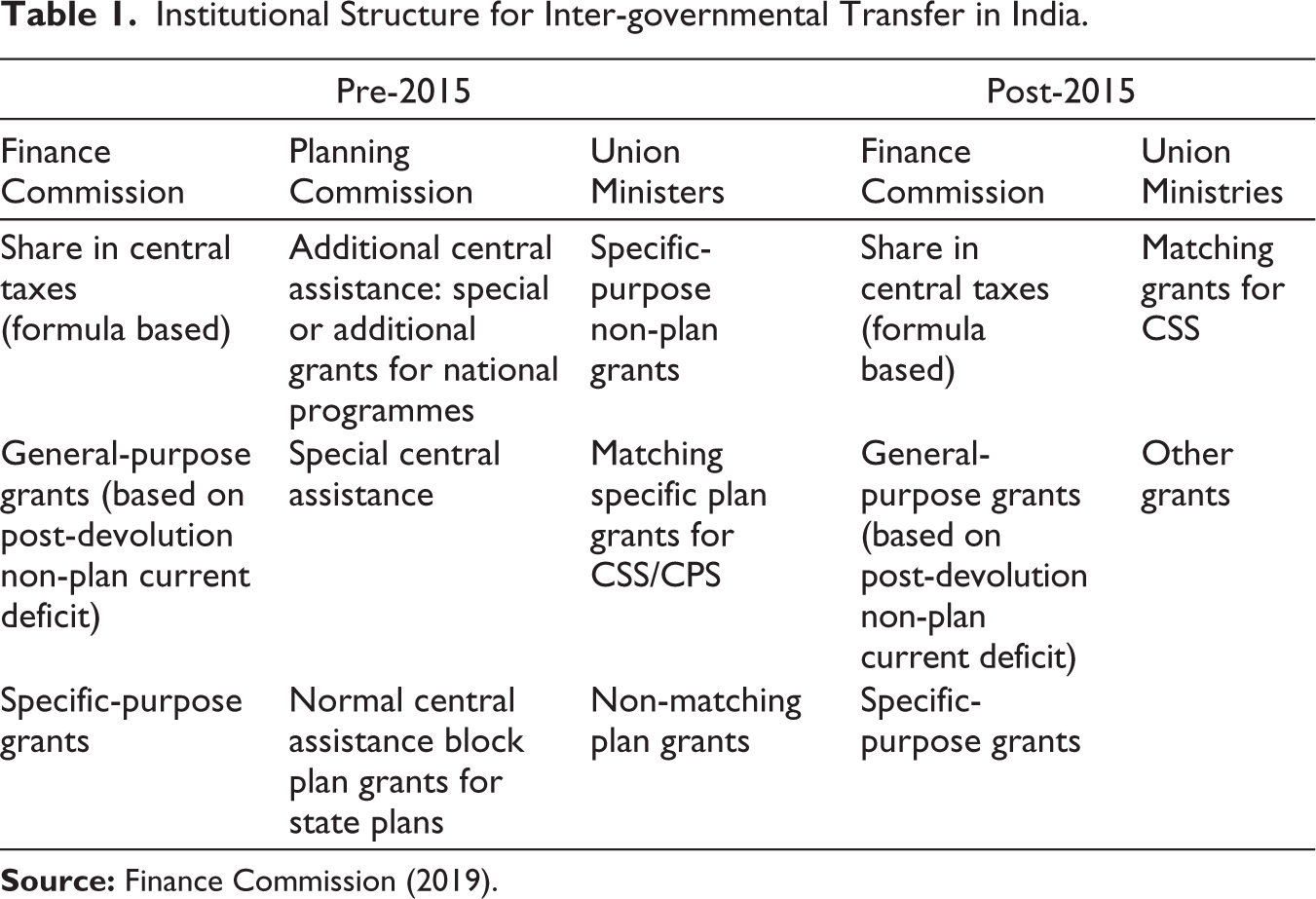

The vertical fiscal gap is high in India compared to other federations in the world, indicating the large mismatch between revenue and expenditure decentralization. Given the growing fiscal gap and high heterogeneity across states, fiscal equalization ensuring horizontal fiscal balance at the sub-national level becomes a major challenge for a country like India. Apart from formula-based transfers (general-purpose transfers), specific-purpose transfers are also devolved to the states by the union government to meet the infrastructure needs of the states, as in the case of other federations. These transfers are mainly attached with certain conditions that have to be fulfilled by the sub-national governments (Finance Commission, 2019). Specific-purpose transfers contribute around 30% of total transfers in India. The drastic changes in India’s transfer architecture took place especially after the abolition of the Planning Commission and subsequent discontinuation of plan grants. While in the pre-2015 years, the transfers mainly included FC transfers, Planning Commission transfers and Union Ministry transfers, in the post-2015 years, there are FC transfers and Union Ministry transfers alone (Table 1).

Institutional Structure for Inter-governmental Transfer in India.

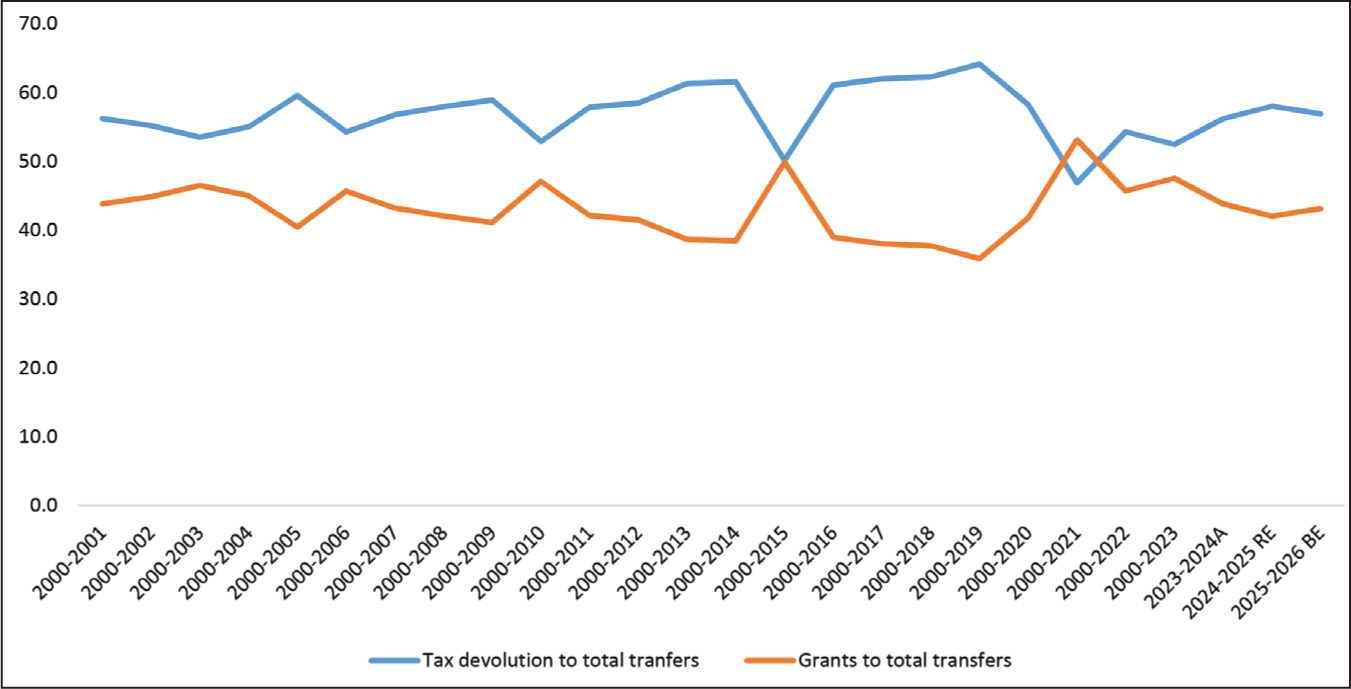

The trends in the composition of tax share and grants-in-aid in total transfers from the union to the states are given in Figure 1. During 2000–2001, tax devolution constituted the larger share at 56% of total transfers, with the remaining 44% being grants-in-aid. While tax devolution generally remains the higher proportion, grants-in-aid temporarily surpassed it in 2020–2021, accounting for 53% of the total transfers compared to 47% for tax devolution. Since then, however, tax devolution has shown an increasing trend, while the share of grants-in-aid has declined.

Statutory and Non-statutory Grants

The grants from the union government to state governments are classified into two types: statutory and non-statutory grants. Statutory grants are recommended by the FC and are referred to as non-plan grants. These include a set of transfers such as post-devolution revenue deficit grants, grants for local bodies (rural and urban), grants for the health sector, grants for the incubation of new cities, grants for shared municipal services and grants-in-aid for disaster relief (SDRF and State Disaster Mitigation Fund), along with schemes under the Provision to Article 275(1) of the Constitution. In contrast, non-statutory grants are tied (conditional) grants and cannot be used for purposes other than those specified. This category encompasses CSS, central sector schemes, assistance to states from the NDRF, externally aided projects, special assistance (as loans for capital expenditure or under the demand transfer to the states) and special central assistance to tribal areas (Government of India, 2025–2026).

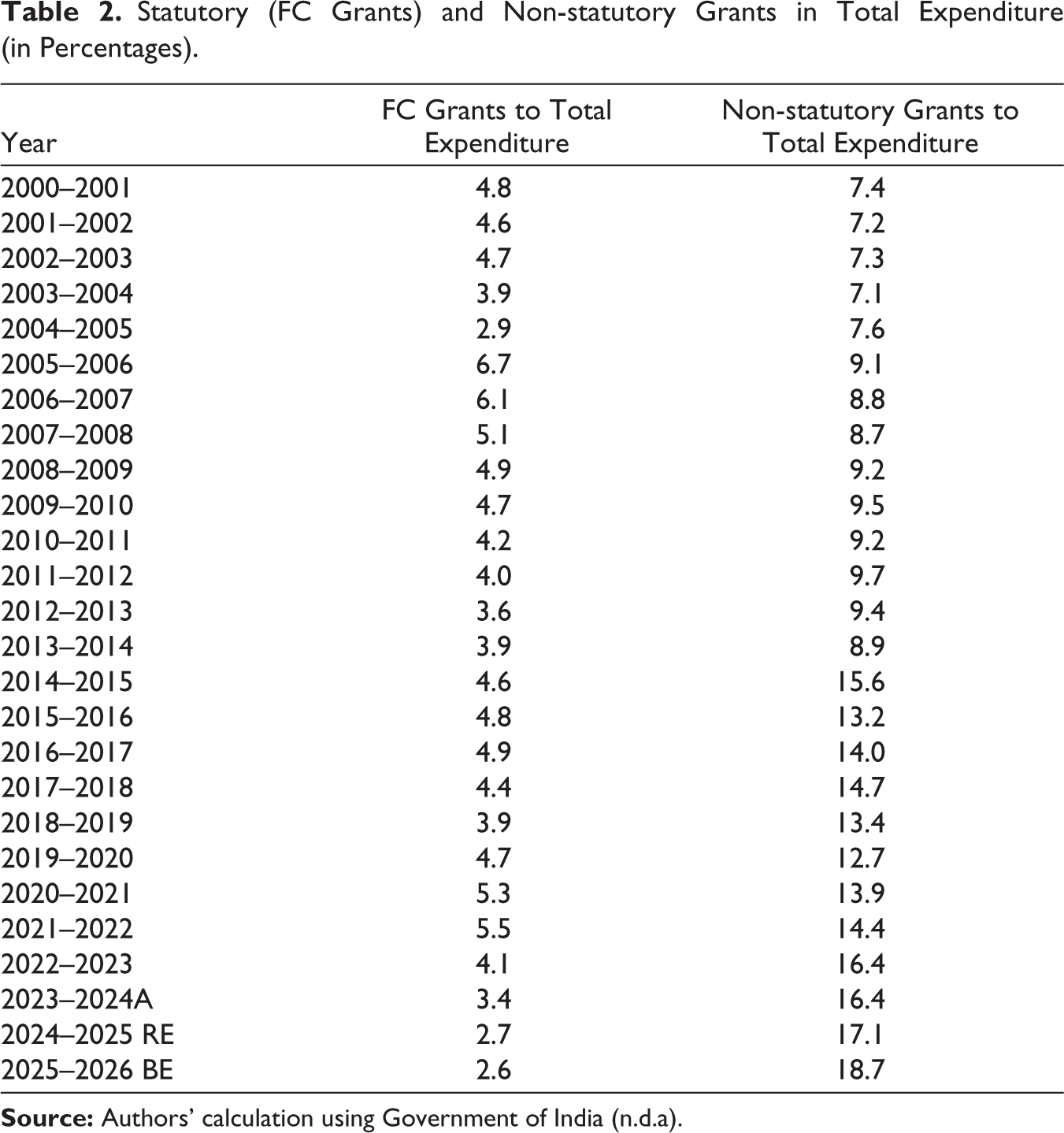

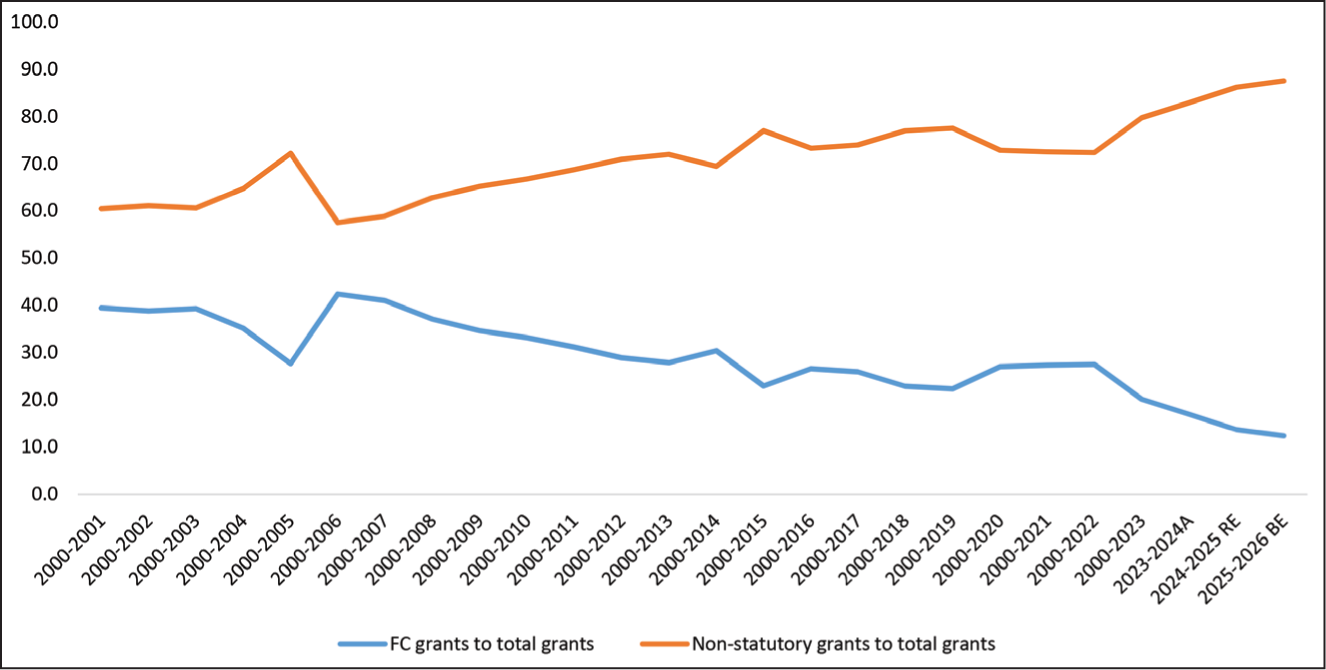

As shown in Table 2, the share of non-statutory grants in the union government’s total expenditure has significantly increased from 7.4% in 2000–2001 to 18.7% in 2025–2026 (budget estimate). Over the same period, the share of statutory FC grants has declined sharply from 4.8% to 2.6%. This trend is starker when considering total grants. In 2023–2024 (and projected for 2025–2026 BE), non-statutory grants constituted a high proportion of 83% (rising to 88% in BE 2025–2026) of total grants from the union to states, while FC grants represent a diminishing share (only 17%, dropping to 12.4% in BE 2025–2026; Figure 2). The substantial and increasing size of these non-flexible, tied grants, particularly the CSS and central sector schemes, suggests an excessive centralization of resource transfers.

Statutory (FC Grants) and Non-statutory Grants in Total Expenditure (in Percentages).

Centrally Sponsored Schemes

The CSS are designed and funded by the union government on subjects that fall under both state and concurrent lists, with implementation being carried out by the state governments. These transfers are typically backed by Article 282 of the Indian Constitution, which provides for discretionary spending by the union (Chakraborty & Gupta, 2025). However, the CSS mechanism has attracted significant criticism. Many schemes are seen as intruding upon the powers of state governments, effectively allowing the union government to exercise a high degree of control over the financial use by states (Kumar, 2022). These schemes should be designed and implemented based on the requirements of the states (Jha et al., 2021) and to achieve the objective of ensuring minimum standards of public services (Rao, 2015).

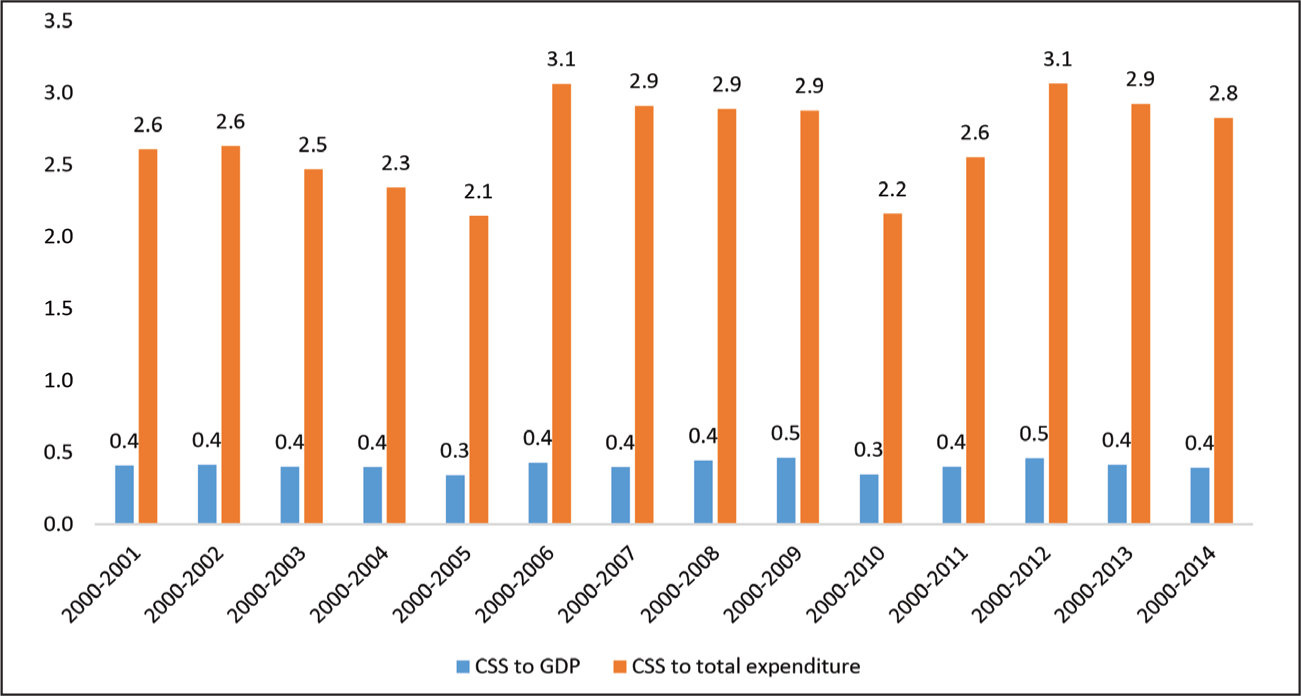

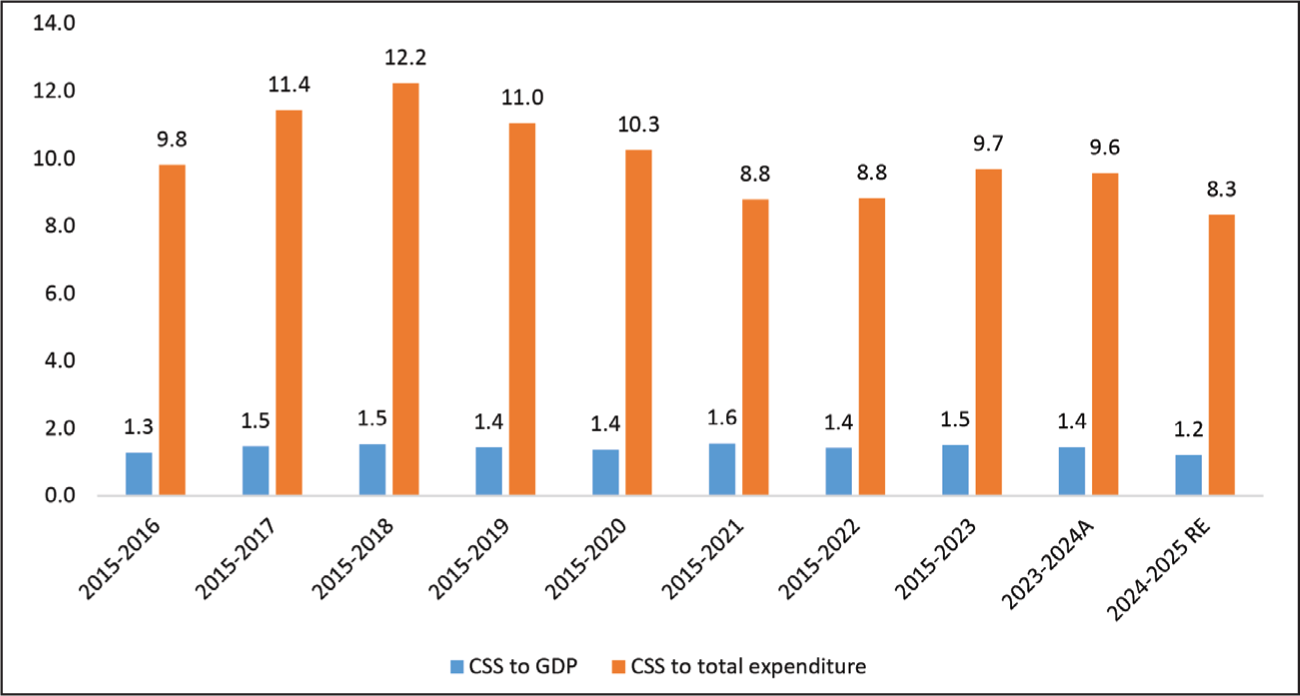

The average share of CSS accounted for 0.41% of GDP and 2.68% of the union’s total expenditure. It is noteworthy that no separate earmarking for CSS was available in 2014–2015 due to transitional changes. Following the abolition of the Planning Commission, the size and prominence of CSS increased substantially. The average ratio of CSS to GDP rose significantly to 1.42%, and the union’s total expenditure climbed to 10%. However, both Figures 3 and 4 indicate that, despite this overall increase, a decline in the ratio of CSS to total expenditure has been observed in the last few years.

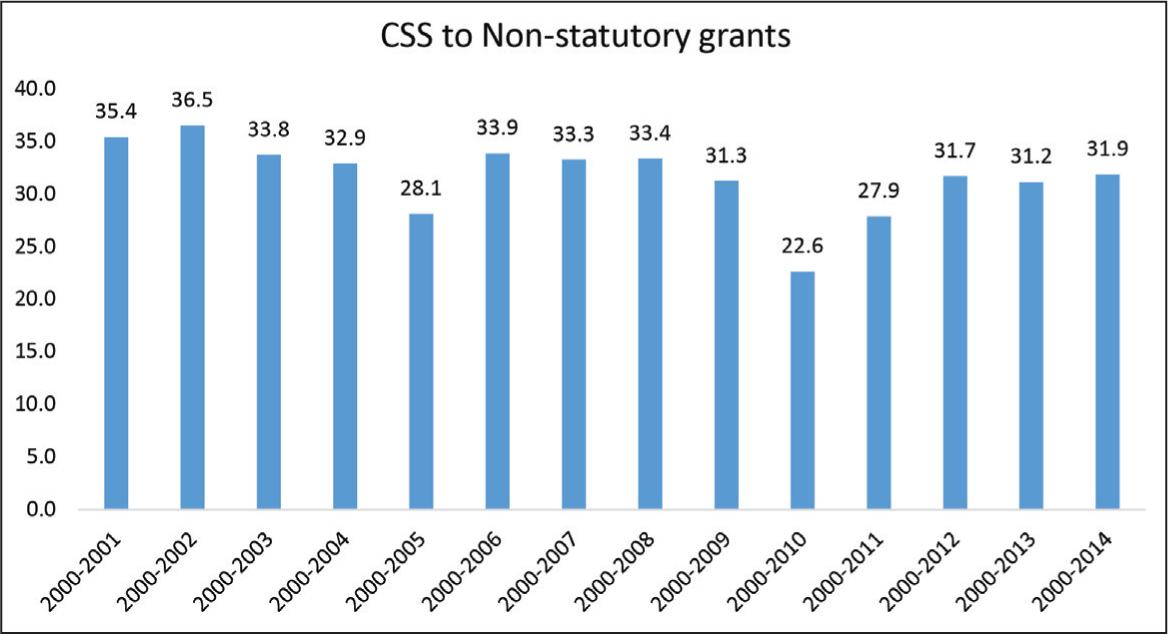

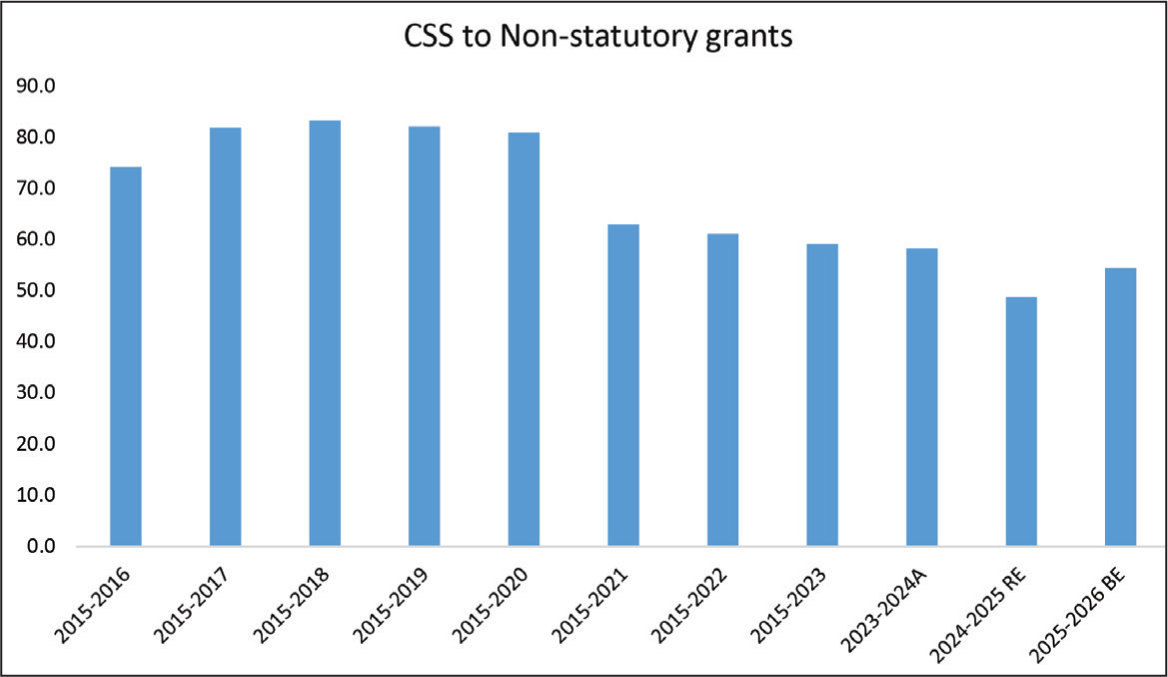

In the pre-Planning Commission period (2000–2001 to 2013–2014), the share of CSS was relatively consistent, ranging between 35.4% and 31.9%, with an average of 31.7%. In sharp contrast, the post-Planning Commission period (2015–2016 to 2025–2026 BE) shows a significant surge, with the share ranging from a high of 74.2% down to 54.4%, maintaining a much higher average of 67.9%. This dramatic increase demonstrates that following the abolition of the Planning Commission, the share of CSS in total non-statutory grants more than doubled, rising from an average of 31.7% to 67.9% (Figures 5 and 6).

Classifications of CSS

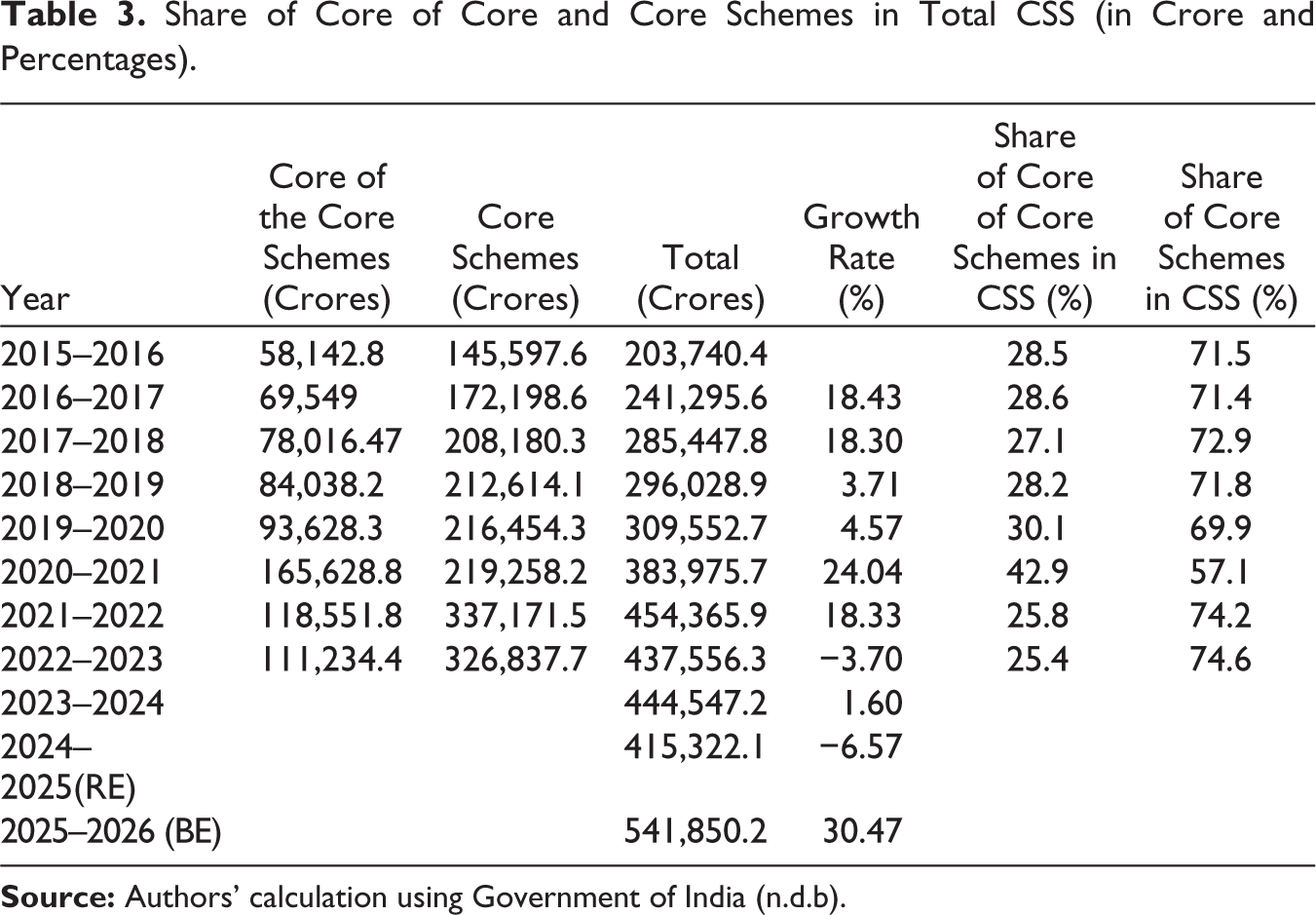

The structure and number of these schemes have undergone substantial rationalization over the past two decades. The number of schemes varied widely, ranging from 188 in 2002–2003 to 147 in 2011–2012. In 2011, a Committee chaired by Shri B. K. Chaturvedi was appointed to restructure the CSS with the aim of enhancing flexibility, scale and efficiency. Following its recommendations, the number of schemes was initially reduced from 147 to 66. Further rationalization occurred in 2016, where a sub-group’s recommendations led to the restructuring of the 66 schemes into just 28 umbrella schemes (Chakraborty & Gupta, 2025; Das & Mitra, 2013; Varghese & Anilkumar, 2023). These 28 schemes are categorized into ‘Core of Core’ schemes, which constitute below 30% of the total CSS amount, and the remaining ‘Core Schemes’. When examining the growth rate, Table 3 shows that the growth rate of the CSS amount peaked at 18% in 2016–2017. Following this, the growth rate has declined, though there was a remarkable increase during the COVID-19 period. However, the post-COVID period has seen a contraction, registering an average growth rate of −2.9% during the period from 2022–2023 to 2024–2025.

Share of Core of Core and Core Schemes in Total CSS (in Crore and Percentages).

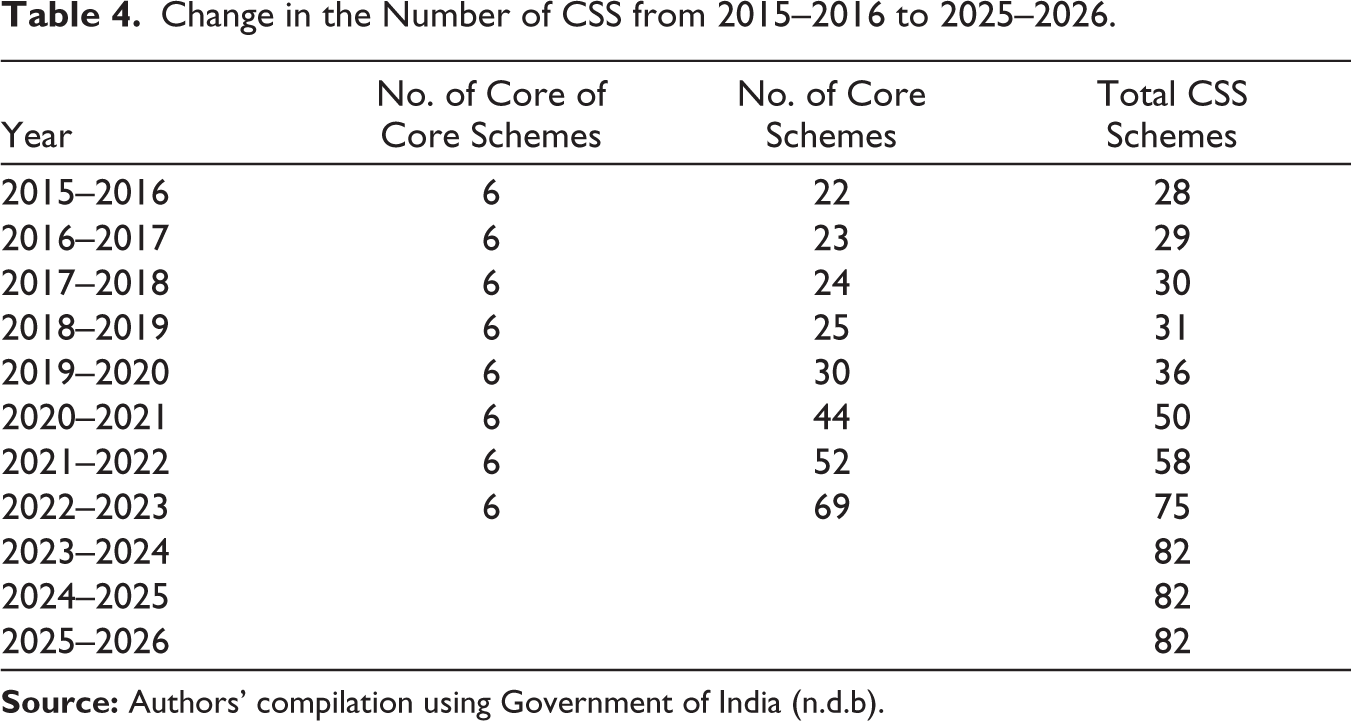

Following the rationalization efforts, the structure of CSS underwent continuous change. Initially, in 2015–2016, the 28 umbrella schemes were categorized into 6 ‘Core of the Core’ schemes and 22 ‘Core Schemes’. This system of classifying schemes as ‘Core of the Core’ and ‘Core’ continued until 2022–2023, during which time the total number of CSS schemes incrementally rose to 75 due to the addition of more schemes under the ‘Core’ category. It is important to highlight that a further significant shift occurred in 2023–2024, where the total number of CSS schemes was further increased to 82, and the ‘Core of the Core’ and ‘Core’ categorization was discontinued. This rapid increase in the number of centrally designed schemes suggests an apparent trend towards increased centralization and intrusion into states’ autonomy. This practice poses a threat to the spirit of co-operative federalism by sidelining the local and specific interests of states (Table 4).

Change in the Number of CSS from 2015–2016 to 2025–2026.

The ‘Core of Core’ schemes, which include key programmes such as the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) and the National Social Assistance Programme, are fully funded by the union government. In contrast, the ‘Core Schemes’ mandate a sharing of funds with the states. For these schemes, the general funding pattern stipulates that the union government contributes 60% of the required funds, with the remaining 40% to be met by the respective state governments (Jha et al., 2021). The Core of Core schemes stood at 30% in 2019–2020, then sharply increased to 43% during the COVID year (2020–2021) and subsequently declined sharply to 26% in 2021–2022. The allocation to key schemes also shows a decline. The budget for MGNREGA has been consistently reduced: the actual allocation of ₹98,468 crore in 2021–2022 fell to ₹89,154 crore in 2022–2023 (RE), and further decreased to ₹86,000 crore in the latest budget estimate (Table 5). It implies that the streamlining of CSS is back to square one, and this is largely against the interests of states.

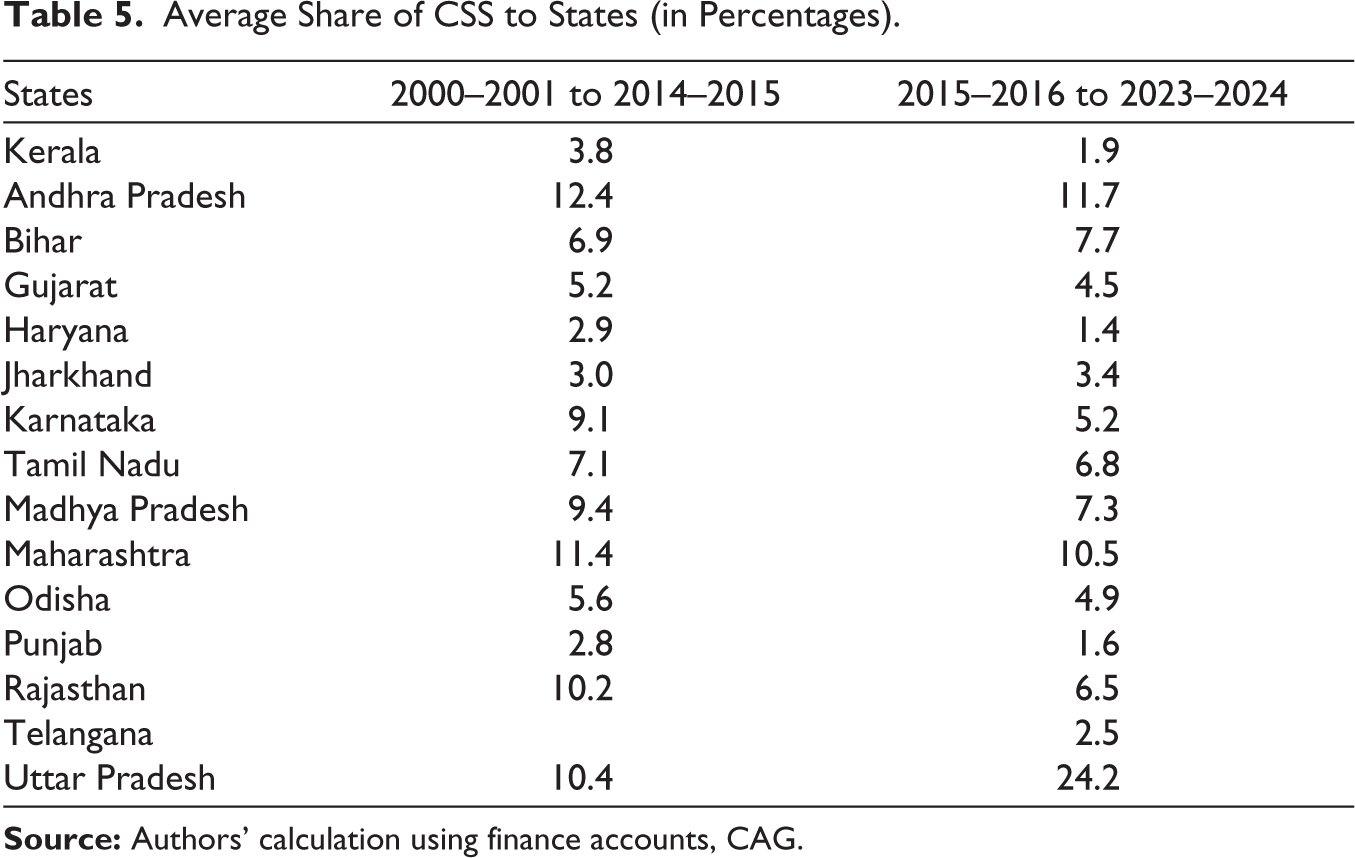

Average Share of CSS to States (in Percentages).

At present, CSS are implemented by various Union Ministries and Departments. In 2023–2024, CSS spending was highly concentrated among a few departments. The Department of Rural Development was the highest spender, utilizing 33.7% of the total CSS amount (an actual expenditure of ₹149,714 crore). The second-highest spender was the Department of Drinking Water and Sanitation, accounting for 17.2% (₹76,538 crore). The Department of School Education and Literacy utilized 9.7% of the CSS (₹43,420.9 crore), the Department of Health and Family Welfare spent 9.7% and the Department of Housing and Urban Affairs spent 9.7% and 8.6%, respectively, occupying third and fifth places. Together, these five departments collectively accounted for a commanding 85% of the total CSS expenditure during the year 2023–2024.

CSS and States’ Development

Apart from the main aim of the CSS to ensure equalization in the provision of public services, it has spillover effects and externalities associated with the provision of merit goods. Through CSS, union and state governments together focus on achieving the national priorities set out in the National Development Agenda. Under CSS, several programmes were introduced by the union government in sectors such as education, health, skill development and labour, which are in the state list mainly with the objective of national priorities (Jha et al., 2021). Unlike the plan grants and FC grants, which were distributed based on Gadgil formula and FC devolution criteria, respectively, provision of CSS is fully discretionary under Article 282. Two main issues raised from the discussions on the rationalization of CSS were that due to high implementation capabilities and matching grants, better-off states benefit more from CSS compared to poor states and the one-size-fits-all approach leads to the non-suitability of schemes for advanced states. States do not have any role in designing schemes as they are only part of its implementation. As advanced states have achieved higher positions in most of national priority sectors, the schemes representing national priorities may not be useful to these states and do not address their current requirements. States requirements and needs are not taken into account while designing and implementing the schemes. This actually handicaps the advanced states in utilizing the discretionary grants of the union government. Also, the matching grants required from the state part creates more trouble for state finances. These mandatory contributions from the states governments for the implementation of the schemes aggravate state finance for the states which are already in deficits.

Table 6 details the state-wise share of CSS across two distinct periods: 2000–2001 to 2014–2015 and 2015–2016 to 2023–2024. The data show that the CSS share has declined for the majority of states, with notable exceptions being Bihar, Jharkhand and Uttar Pradesh, which registered an increase. For instance, Kerala’s share saw a reduction, falling from 3.8% to 1.9% during the specified periods. To facilitate a more accurate comparison of the resource flow across states, the analysis is further refined by considering the per capita CSS received by each state, the details of which are presented in Table 5.

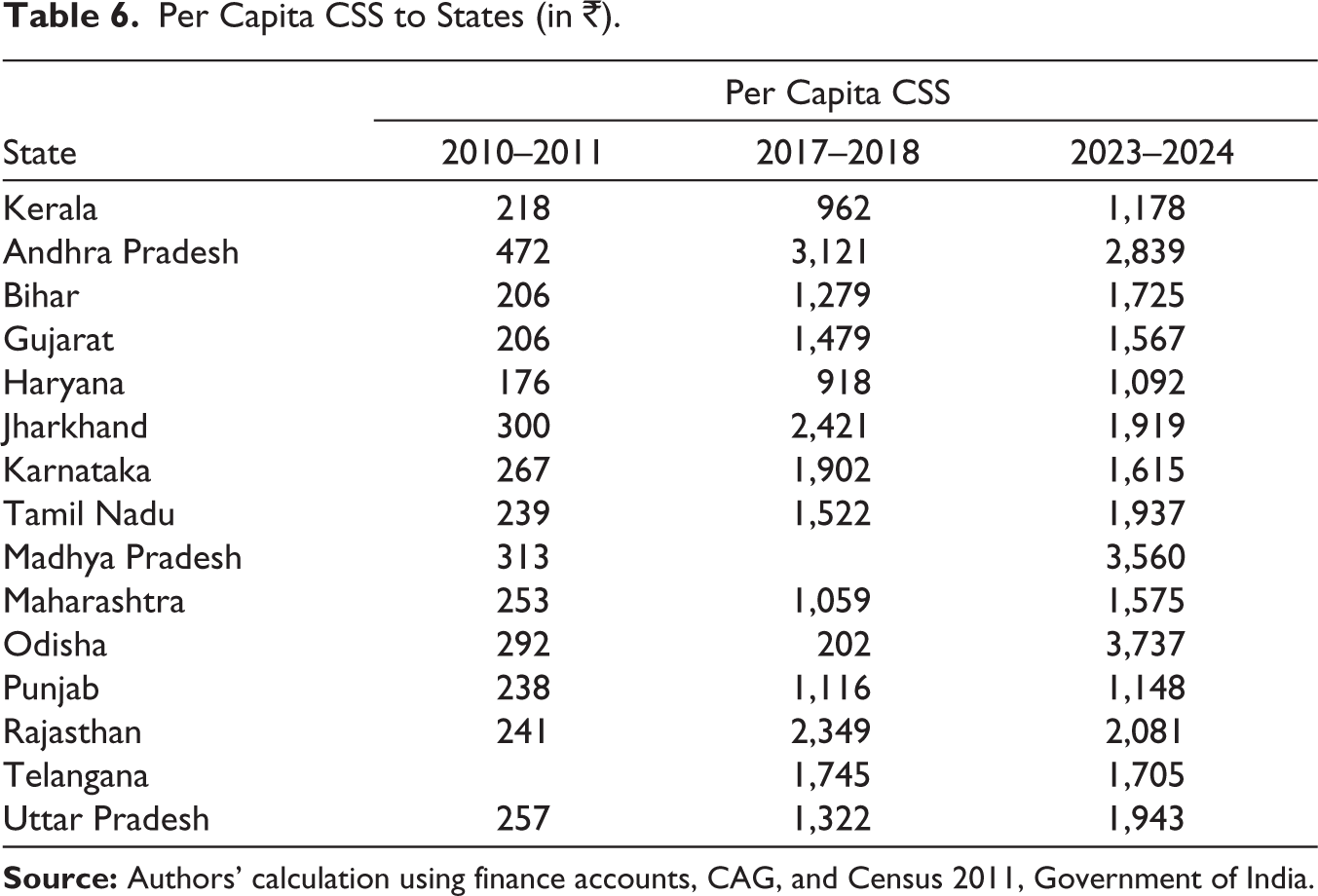

Per Capita CSS to States (in ₹).

As Table 6 indicates, there is a significant variation in the per capita distribution of CSS across states. States such as Kerala (₹1,178), Haryana (₹1,092) and Punjab (₹1,148) received the lowest per capita CSS amounts compared to other states. Although the per capita share for these states has increased over time, it remains among the lowest. Conversely, states such as Odisha, Madhya Pradesh, Rajasthan, Andhra Pradesh, Jharkhand and Tamil Nadu have a higher per capita CSS. Not all states maintained upward momentum, however; Karnataka experienced a decline in per capita CSS, falling from ₹1,902 in 2017–2018 to ₹1,615 in 2023–2024.

The decline in the CSS share for the advanced states may be due to the mismatch in the schemes available for their requirements. Though CSS aims at equalization in the provision of public services, it in a way discriminates those states for which the schemes do not align. As indicated in the above session, there is a high increase in CSS allocation after the abolition of the Planning Commission and discontinuation of plan grants. Replacing the formula-based plan grants (unconditional) with the discretionary matching CSS (conditional) reduces the discretionary expenditure of the states and deteriorates their finances. States are put under trouble due to non-flexibility of the schemes. One of the recommendations of the Arvind Varma Committee in 2005 on restructuring CSS was that ‘a new CSS should be introduced only after full consultation with the states’. This is very relevant and important as many of the advanced states are concerned as they have new generation problems and different requirements. While designing the schemes, state specificities should be taken into account.

Gap Between Actual and Budgeted CSS

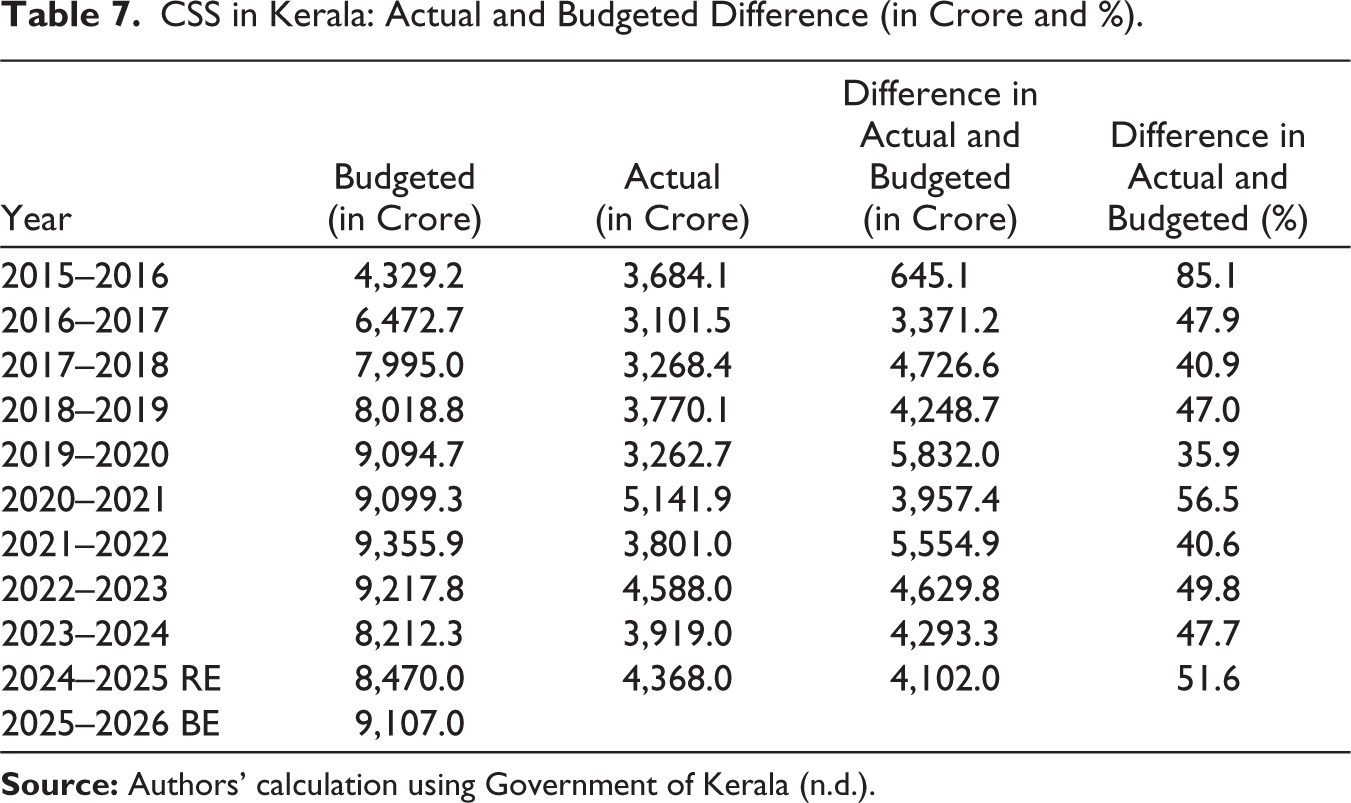

A matter of serious concern in Kerala is the wide gap between the budgeted and the actual receipt of CSS. As shown in Table 7, the states’ estimated budget for CSS was consistently high, yet the actual realization was less than 50% on average from 2016–2017 to 2024–2025. For instance, in 2023–2024, the budget estimate was ₹8,212.3 crore, but the actual amount received was only ₹3,919 crore (47.7%). This low realization rate suggests potential reasons related to the nature of CSS itself. Given Kerala’s advanced achievements in sectors such as health and education, the lack of consideration for state-specific needs means that many basic central schemes may simply not align with the states’ developmental priorities, leading to challenges in implementation or utilization and, thus, low actual fund flow.

CSS in Kerala: Actual and Budgeted Difference (in Crore and %).

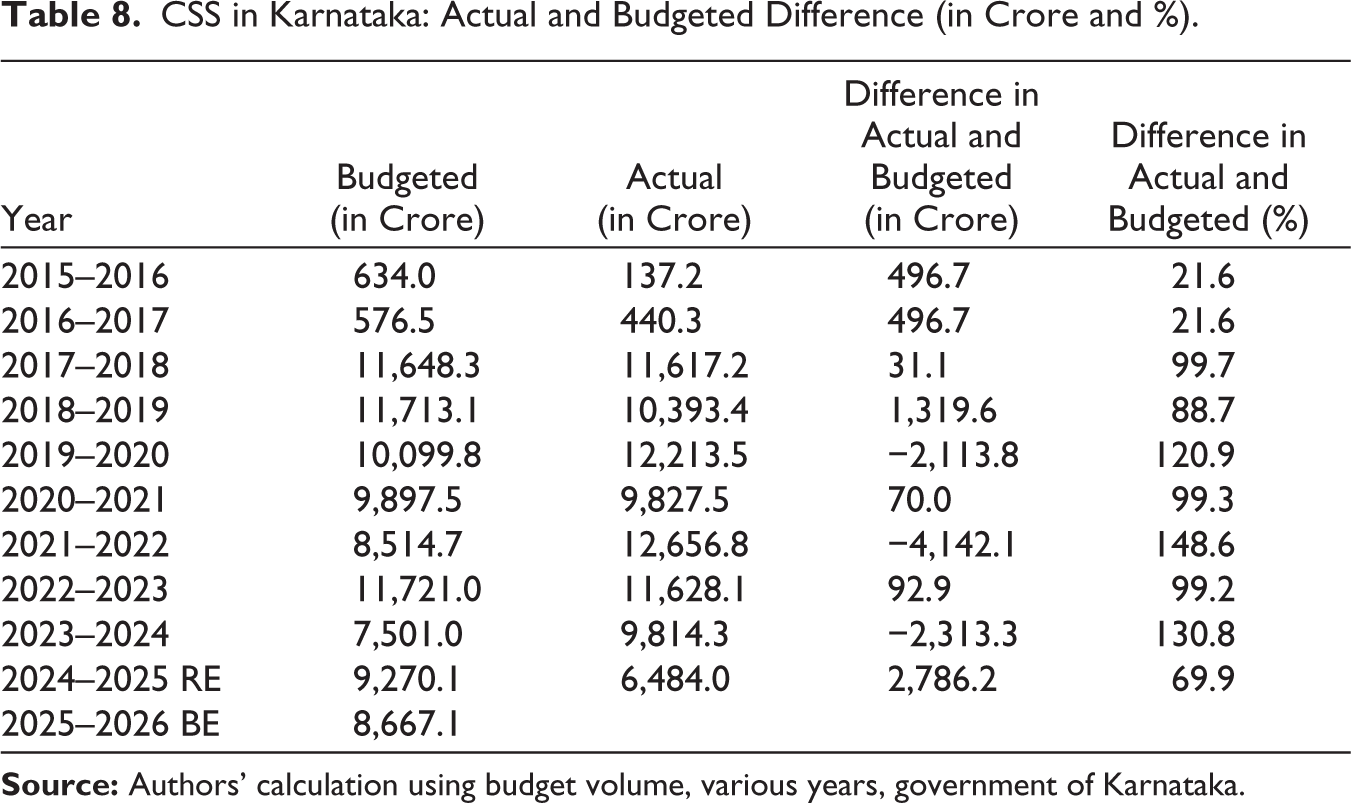

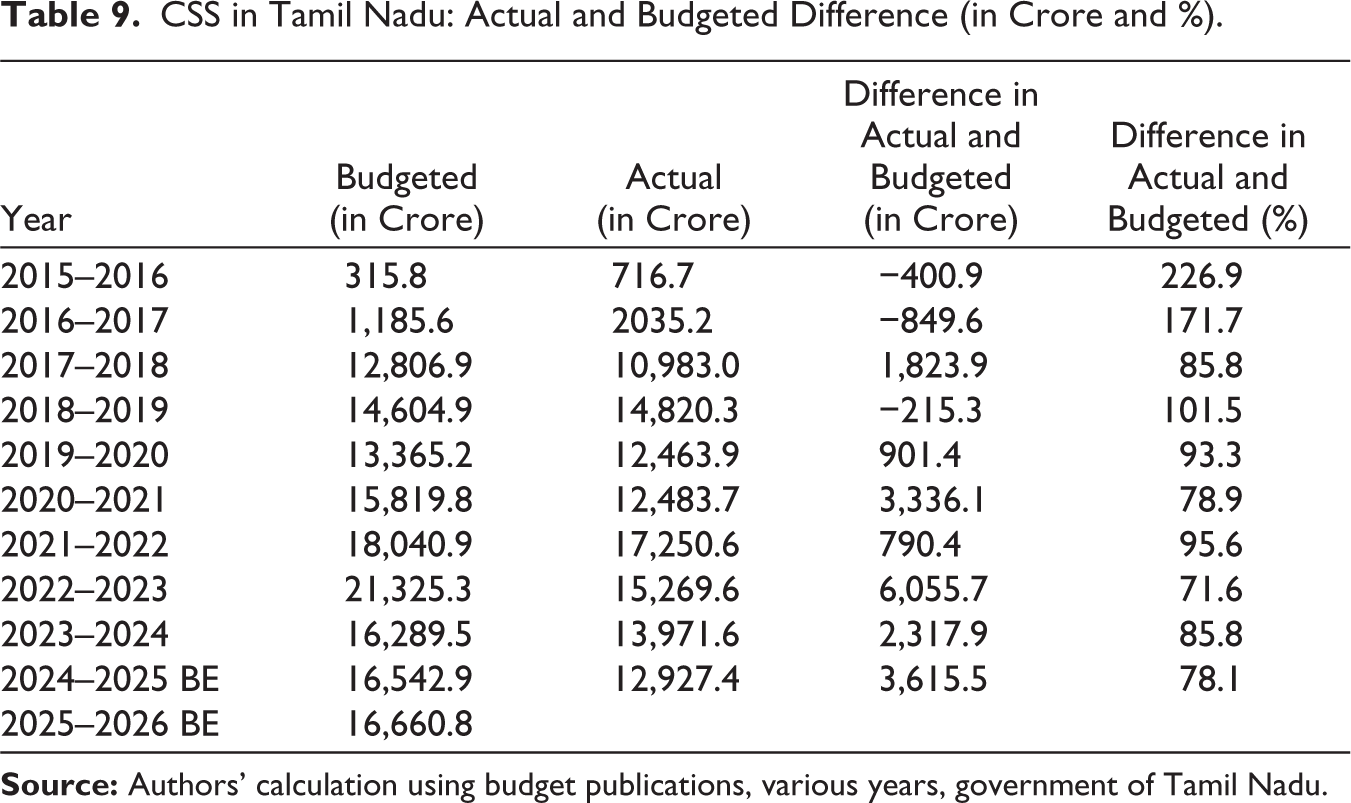

In order to analyse the extent of the difference between budgeted and actual realization of CSS, a comparative analysis was conducted for neighbouring states of Karnataka and Tamil Nadu. In Karnataka, the gap between budgeted and actual CSS has steadily decreased since 2017–2018. On average, the actual realization rate was high, standing at around 90% from 2015–2016 to 2023–2024 (Table 8). In 2023–2024, the state not only met but also exceeded its budget estimate of ₹7,501 crore, with an actual realization of ₹9,814.3 crore. Similarly, Tamil Nadu showed a strong realization rate, with the average actual receipt of CSS from 2017–2018 to 2023–2024 being approximately 87%. For the year 2023–2024, against a budget estimate of ₹16,289.5 crore, the state realized ₹13,971.6 crore, representing an 86% realization rate (Table 9). When compared to its neighbours states of Karnataka and Tamil Nadu, Kerala’s actual realization of CSS is significantly lower. The difference between Kerala’s low utilization (around 50% on average) and the high utilization rates of its neighbours (87%–90% on average) is a matter of serious concern. Therefore, the reasons for Kerala’s persistently low realization rate must be thoroughly explored to develop effective strategies aimed at reducing the gap between budgeted and actual CSS funds.

CSS in Karnataka: Actual and Budgeted Difference (in Crore and %).

CSS in Tamil Nadu: Actual and Budgeted Difference (in Crore and %).

The issues associated with the implementation and utilization of various social welfare schemes including CSS across states have been noticed and reforms were introduced for better transferring and utilization of funds. The Public Finance Management System (PFMS) is one form of reforms adopted by the Government of India in order to monitor the implementation of schemes. In order to have better release and monitoring utilization of funds under CSS, the union government introduced the Single Nodal Agency under PFMS.

Burden on the State Government

Considering the large discrepancy between the budgeted and actual realization of CSS funds, it is crucial to examine the additional financial burden incurred by states due to the revised funding ratios between union and state governments.

Following the abolition of the Planning Commission, particularly starting in 2016–2017, the funding pattern of most CSS was significantly changed. Before this period, the Union government’s funding ratios for various schemes in major states were typically 90%, 80% or 75%. The remaining shares of 10%, 20% or 25%, respectively, were to be financed by the major states. However, from 2016–2017 onwards, the state funding share for most schemes was sharply increased to 40% (Varghese & Anilkumar, 2023). This substantial rise in the states’ mandated share for financing CSS increases the financial burden on state governments.

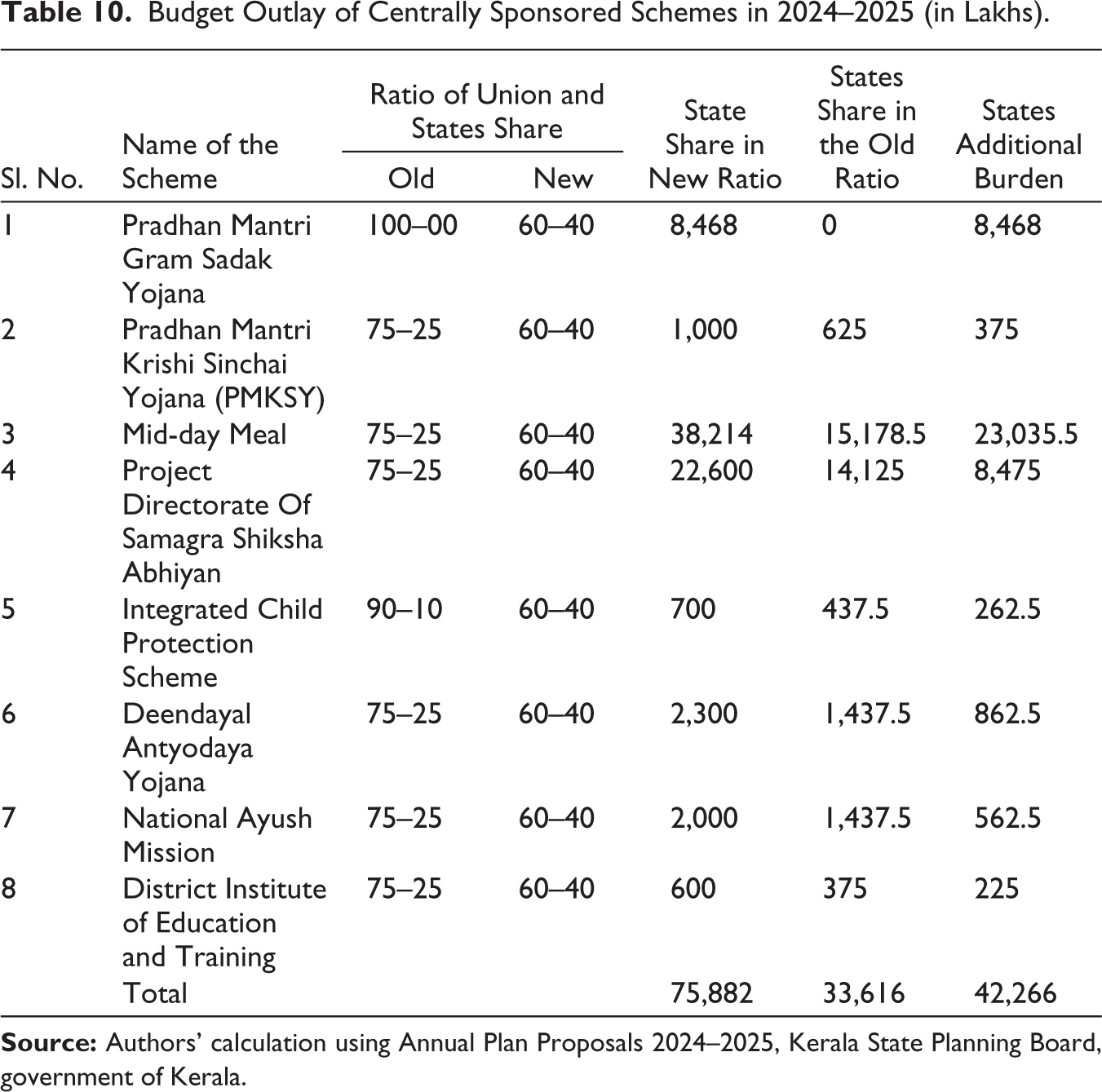

To quantify this increased burden, a case study was conducted using eight selected CSS schemes from Kerala’s list. The additional burden was calculated by comparing the state’s required share under the new funding ratios against what it would have paid under the old ratios. In 2024–2025, the state’s expenditure on these selected schemes under the new ratio was ₹7,588.2 lakhs. Had the old ratio been in place, the expenditure would have been only ₹3,361.6 lakhs. For this specific period, the state had to incur an additional expenditure of ₹4,226.6 lakhs to finance these CSS, demonstrating the direct financial strain caused by the revised funding arrangements (Table 10).

Budget Outlay of Centrally Sponsored Schemes in 2024–2025 (in Lakhs).

Conclusion

The study’s findings reveal a shift in India’s federal transfers, indicating a move towards increased central control through non-statutory (tied) grants following the abolition of the Planning Commission. The share of non-statutory grants in the Union’s total expenditure has significantly increased from 7.4% in 2000–2001 to 18.7% in 2025–2026 (BE). Conversely, the FC grants share declined from 4.8% to 2.6% over the same period. Non-statutory grants now constitute the vast majority of all grants, representing 83% in 2023–2024 (up from 61% in 2000–2001 and projected to be 88% in 2025–2026 BE), while FC grants have shrunk to only 17% (down from 40% in 2000–2001). The average growth rate of FC grants sharply declined from 17.9% (2000–2010) to 3.1% (2020–2025), whereas the non-statutory grants’ growth rate increased from 16.7% to 19.2% in the corresponding periods. The design of CSS sidelines states’ local and specific interests, as the ‘one size fits for all’ approach negatively affects the fiscal health of the states. Most states, including Kerala, have seen a decline in their CSS share between the 2000–2001 to 2014–2015 and 2015–2016 to 2023–2024 periods. Kerala’s share, for example, dropped from 3.8% to 1.9%. States such as Kerala, Haryana and Punjab have the lowest per capita CSS allocations, despite an increasing trend in the absolute amount. Conversely, states such as Odisha, Madhya Pradesh, Rajasthan, Andhra Pradesh, Jharkhand and Tamil Nadu receive higher per capita CSS. There is a consistent gap between budgeted and actual CSS receipts in some states. In Kerala, the actual realization averaged less than 50% of the estimated budget from 2016–2017 to 2024–2025, highlighting a failure to align scheme design with state-specific needs.

The study presents the following suggestions for improving the effectiveness of CSS: (a) ensuring flexibility in the implementation of CSS by considering the needs and requirement of the states, (b) states should get the freedom to utilize CSS funds considering regional disparities and diverse needs; (c) the ‘one size fits all’ approach in CSS implementation has to be avoided; (d) there is a need to increase the size of CSS funds and also provide more funds to Core of Core schemes so as to reduce the burden of states (the Core of Core schemes is fully funded by union government); (e) there is a need to reduce the number of schemes so as to avoid the duplication of schemes and thereby increase the effectiveness of CSS implementation and (f) any deviation from the existing CSS should be done with the consensus and mutual agreement of the states with more flexibility. This will promote co-operative federalism and reduce discretionary nature of fund transfer.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.