Abstract

This article explores the contradictory relation between globalisation and crisis in the Korean capitalism since the 1990s. After formulating the relation between globalisation and crisis from the perspective of Marxian theory of world market crisis, this article overviews the process of globalisation in Korea after the 1990s, focusing on foreign trade, capital export and global value chains. In addition, this article empirically examines the relation between globalisation and crises in the Korean capitalism by analysing the trend of Marxian ratios, including rate of profit. Based on the case study on the Korean capitalism, this article concludes that globalisation is not the cause of but the capitalist responses to the economic crises.

Introduction

Korean capitalism entered the period of structural crisis around 1987, ending about 30-year-long high economic growth. The policy for globalisation of Kim Young-Sam government in the early 1990s, ‘Segyehwa’, literally in Korean, was the response to the onset of the structural crisis. However, it could not prevent the explosion of the 1997 crisis. Globalisation was pursued aggressively after the 1997 crisis, and accelerated again after the global economic crisis of 2008.

This article explores the contradictory relation between globalisation and crisis in the Korean capitalism since the 1990s. Second section formulates the relation between globalisation and crisis by applying Marxian theory of world market crisis. Third section overviews the process of globalisation in Korea after the 1990s, focusing on foreign trade, capital export and global value chains. In fourth section, after examining the relation between globalisation and crisis in the Korean capitalism during the 1997 crisis and the global economic crisis of 2008, it is argued that globalisation cannot be considered as the cause of the crises in Korea. Fifth section concludes and suggests theoretical and political implications.

Dialectics of Globalisation and Crisis: Marxian Theory of World Market Crisis 1

Marx always discussed the crises in the context of world market and globalisation. He regarded world market and globalisation as factors of facilitating capital accumulation by extending its loci on a global scale. Marx never conceived the world market or globalisation as the cause of crises, though he admitted that it prepared an extended arena for crises. On the contrary, Marx situated the expansion of foreign trade, for example, the core of globalisation, as a counteracting force to the tendency of falling rate of profit and crises:

In so far as foreign trade cheapens on the one hand the elements of constant capital and on the other the necessary means of subsistence into which variable capital is converted, it acts to raise the rate of profit by raising the rate of surplus-value and reducing the value of constant capital. It has a general effect in this direction in as much as it permits the scale of production to be expanded. In this way it accelerates accumulation, while it also accelerates the fall in the variable capital as against the constant, and hence the fall in the rate of profit. … Capital invested in foreign trade can yield a higher rate of profit, firstly, because it competes with commodities produced by other countries with less developed production facilities, so that the more advanced country sells its goods above their value, even though still more cheaply than its competitors. In so far as the labour of the more advanced country is valorised here as labour of a higher specific weight, the profit rate rises, since labour that is not paid as qualitatively higher is nevertheless sold as such. … As far as capital invested in the colonies, etc. is concerned, however, the reason why this can yield higher rates of profit is that the profit rate is generally higher there on account of the lower degree of development, and so too is the exploitation of labour, through the use of slaves and coolies, etc. (Marx, 1981, pp. 344–345)

Following Marx, Henryk Grossmann also emphasised the role of foreign trade in counteracting the tendency of falling rate of profit:

(The) injection of surplus value by means of foreign trade would raise the rate of profit and reduce the severity of the breakdown tendency … Foreign trade gains importance in periods of internal saturation, when valorization disappears due to overaccumulation and there is a declining demand for investment goods. … Thus here we have means of partially offsetting a crisis of valorization in the domestic economy. (Grossmann, 1992, pp. 172–173)

Marx also argued that the foreign trade would raise the rate of profit by cheapening the raw materials, for example, key elements of constant capital:

Since the rate of profit is s/C or s/(c + v), it is clear that everything that gives rise to a change in the magnitude of c, and therefore of C, also brings about a change in the profit rate, even if s, v and their reciprocal relationship remain constant. Raw material, however, forms a major component of constant capital. … If the price of raw material falls by a sum we shall call d, then s/Cor s/(c + v) is changed to s/(C − d) ors/{(c − d) + v}, and the rate of profit falls. As long as other circumstances are equal, the rate of profit falls or rises in the opposite direction to the price of the raw material. This shows among other things how important low raw material prices are for industrial countries … It also explains how foreign trade influences the rate of profit, irrespective of any effect that it has on wages by cheapening the necessary means of subsistence. (Marx, 1981, p. 201)

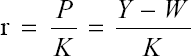

However, it seems to be difficult to identify the effects of cheapening of the elements of constant capital on the rate of profit from the Equation (1), for example, the ratio of profit (P) to fixed constant capital (K), which is widely used to estimate Marxian rate of profit in the existing works (e.g., Kliman, 2012), because it does not include the circulating constant capital, that is, stock of parts and raw materials, in the denominator of the rate of profit.

2

However, if we consider that the value added (Y) is total outputs (Z) minus intermediate inputs (M) and that profit (P) is Y minus wages (W), the Equation (1) can be rewritten as Equation (2), which shows the positive effects of cheapening of M, that is, elements of circulating constant capital, on rate of profit (r).

3

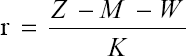

From the perspective of Marxian theory of world market crisis, the relation between globalisation and crisis can be schematised as Figure 1. Post-Keynesian economists or Developmental Statists argued that the globalisation caused the crisis (arrow (5) in Figure 1, Chang, 1998; Crotty & Lee, 2009). They also argued that state responses to the crisis led to deceleration of globalisation and the rise of state capitalism (arrow (6) in Figure 1, Polanyi, 1944). They tended to privilege the ‘double movement’ between market and state on the surface of capitalist mode of production à la Polanyi (1944). On the contrary, Marxian theory of world market crisis emphasises that the state responses to the crises accelerate the process of globalisation. Moreover, globalisation is understood to prepare bigger crisis by extending and deepening the contradictions of capital accumulation on a world scale. Marxian theory of world market crisis duly conceptualises the relation between globalisation and crisis as the dialectical interaction, for example, ‘globalisation ⇆ crisis’, emphasising that the Polanyian ‘double movements’ between market and state, favourite cliché shared by Post-Keynesian economists and Developmental Statists, are nothing other than the result of contradictory dynamics of capital accumulation inherent in the capitalist mode of production.

Globalisation Drive of the Korean Capitalism after the 1997 Crisis

Deepening Dependence on Exports

The rapid increase of the exports has driven the globalisation of the Korean capitalism after the 1997 crisis. As Figure 2 shows, the ratio of exports to GDP increased from 11.4 per cent in 1970 to 34.9 per cent in 1987, but decreased till the 1997 crisis. However, it rose again after the 1997 crisis, reached to 40.4 per cent in 1998, then jumped to 50 per cent in 2008. In 2011, it was 55.7 per cent, higher than the ratio of private consumption in the same year (51%). After 2003, while the ratios of private consumption and investment to GDP were stagnant, the ratio of exports to GDP significantly increased. The increase of exports played the crucial role in the recovery from the 1997 crisis as well as in preventing the Korean capitalism to fall in the global economic crisis of 2008.

The ratio of exports to GDP in Korea in 2014 was more than twice than those in OECD countries in the same year. It was higher than that in Sweden, Germany or Japan, that is, representative export-led high-income economies. It is especially notable that the ratio of exports to GDP in Korea reached the highest level in the world after the global economic crisis of 2008, even surpassing that in Sweden and Germany (World Data Bank, 2016a). On the contrary, the ratio of private consumption to GDP in Korea after the 1997 crisis was lower than that in Sweden or Germany by 5–8 per cent points (World Data Bank, 2016b). In fact, it decreased from 55.5 per cent in 2002 to 48.8 per cent in 2014. Above facts indicate that the Korean economic growth after the 1997 crisis has nothing in common with so-called ‘domestic consumption-led growth’ or ‘wage-led growth’.

The rapid increase of the Korean exports accompanied the diversification of export markets by countries. The ratio of exports to the USA and Japan to the total Korean exports crumbled from 29.8 per cent and 19.4 per cent in 1990 to 12.3 per cent and 5.6 per cent in 2014, respectively, while the ratio of exports to China to the total Korean exports jumped from 0.9 per cent to 25.4 per cent during the same period. 4 Indeed, the export-led growth of the Korean economy after 2000 was crucially indebted to so-called ‘China effect’.

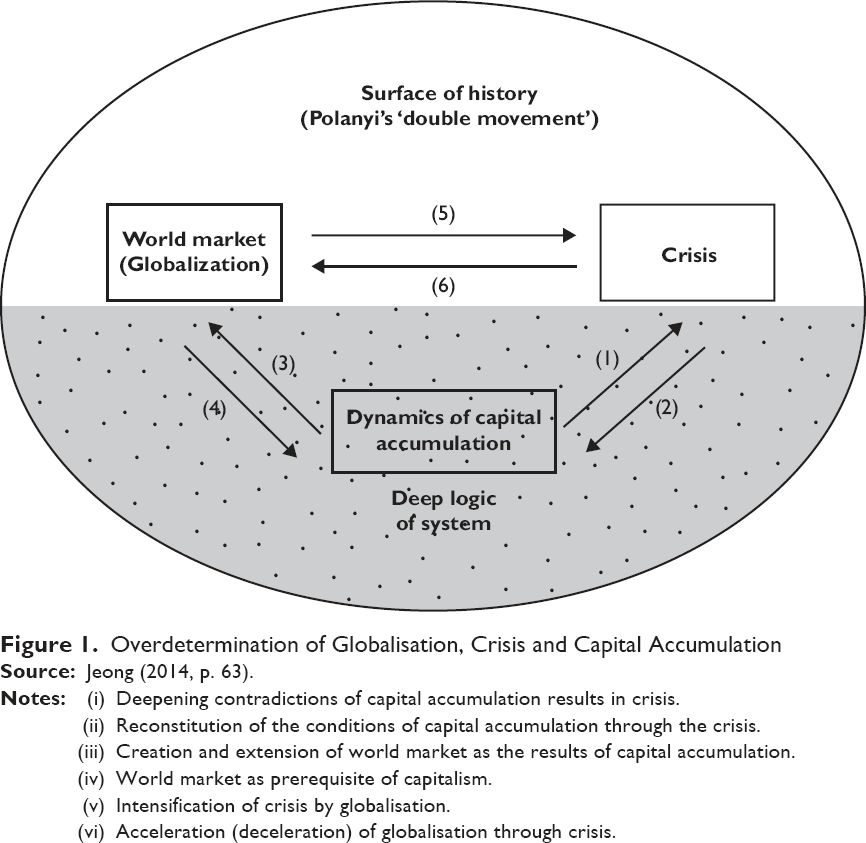

The rapid increase of exports after the 1997 crisis was based on the strengthened competitiveness of Korean capitals enabled by the decrease of unit labour cost. Indeed, as Figure 3 shows, the index of unit labour cost in Korean manufacturing sector in the Korean currency substantially decreased from 107.8 in 1996 to 89.6 in 2000. The same index virtually collapsed from 154.9 to 91.6 for the same period, when it is calculated in the US dollar. While the index in the Korean currency slightly increased for the period of global economic crisis, it dropped from 121.5 in 2007 to 92 in 2009, when it is calculated in the US dollar. Figure 3 reveals that the rapid increase of the exports which drove the recovery of the Korean capitalism after the 1997 crisis and the global economic crisis of 2008 was critically dependent on the substantial decrease of unit labour cost, due to the wage repression as well as the depreciation of the Korean currency. Considering that the decrease of unit labour cost implies the increase of the rate of exploitation of workers, 5 it can be said that the main factor behind the rapid increase of the Korean exports after the 1997 crisis was the intensified exploitation of workers.

Transformation of the Korean Dominant Capitals into Transnational Capitals

The globalisation of the Korean capitalism after the 1997 crisis was not only characterised by the growing domination of the transnational capitals in Korea but also by the transformation of the Korean dominant capitals into the transnational capitals. Indeed, the foreigners’ share in the total value of market capitalisation skyrocketed after the 1997 crisis, from 14.6 per cent in 1997 to 42 per cent in 2004. It slightly decreased after 2004 but still remains at 36.4 per cent in 2017 (Financial Supervisory Service, 2018). The foreign direct investment (FDI) inflow also explosively increased after the 1997 crisis. The FDI inflow jumped from 0.8 billion USD in 1990 to 15.5 billion in 1999, and recorded 19 billion USD in 2014.

Besides the increase of the foreign transnational capital inflow into Korea, Korean capital outflow also increased after the 1997 crisis. Overseas investment of Korean capital increased from 2.38 billion USD in 1990 to 7.14 billion USD in 1996, and 35 billion USD in 2014 (Bank of Korea, 2016a). Korea became a net capital export country after 2006, as the Korean FDI outflow surpassed FDI inflow to Korea. 6 The ratio of the stock of Korean FDI outflow to total stock of global FDI outflow also increased from 0.11 per cent in 1990 to 0.83 per cent in 2013 (UNCTAD, 2014). Globalisation of Korean capitals, as is usually estimated by FDI outflow and inflow, entered qualitatively a new phase after the 1997 crisis. The average annual ratio of FDI outflow to GDP increased from 0.74 per cent for the period of 1987–1997 to 2.12 per cent for the period of 1998–2013, while the annual average ratio of FDI inflow to GDP increased from 0.34 per cent to 1.03 per cent between the same periods. The ratio of FDI inflow to GDP in Korea was about 1 per cent after 2000, lower than average level of those ratios in OECD or East Asian countries, which was 3 to 4 per cent, but higher than that of Japan (World Data Bank, 2016c).

Deepening Incorporation into the Global Value Chains

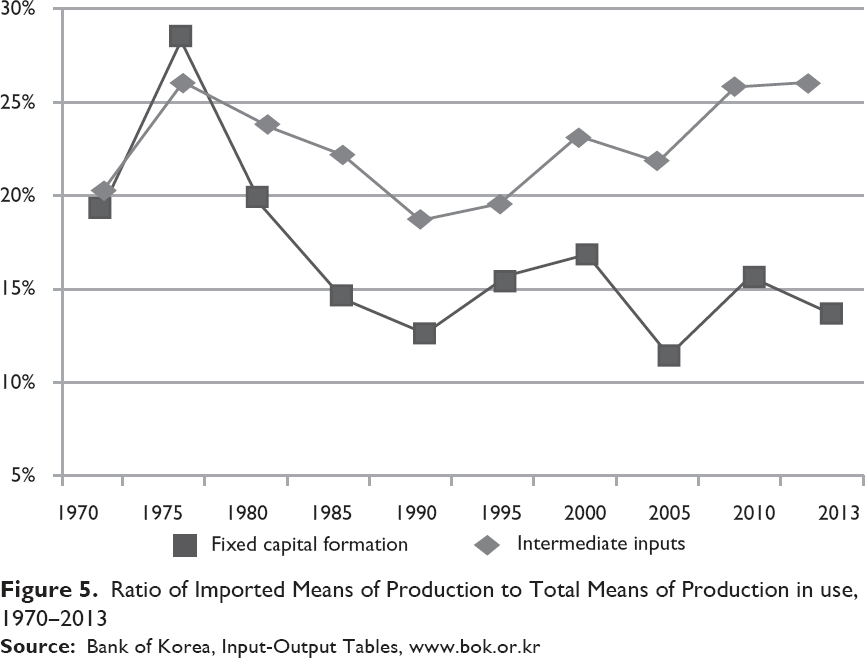

The globalisation of the Korean capitalism after the 1997 crisis accompanied the deepening dependence on the imported means of production. As Figure 5 shows, the ratio of imported means of production to total means of production in use decreased till the middle of 1990s, harbouring an illusion for ‘self-reliant’ economy then. However, it reverted to increase from the late 1990s. Indeed, the ratio of imported intermediate inputs (raw materials and parts) to total intermediate inputs in use decreased from 25.6 per cent in 1975 to 18.8 per cent in 1990, before it increased to 25.6 per cent in 2013. The ratio of imported fixed capital to total fixed capital in use also decreased from 27.7 per cent in 1975 to 12.8 per cent in 1990, but it resumed its increase in the late 1990s, recording 14.6 per cent in 2013.

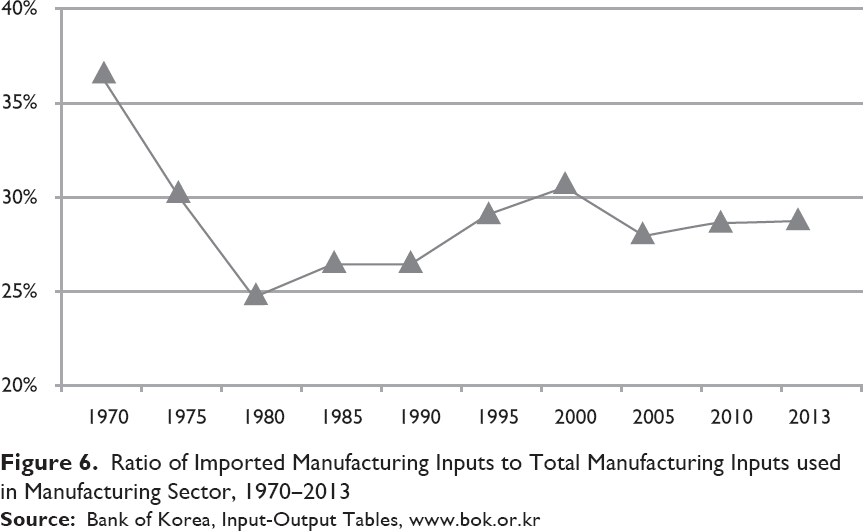

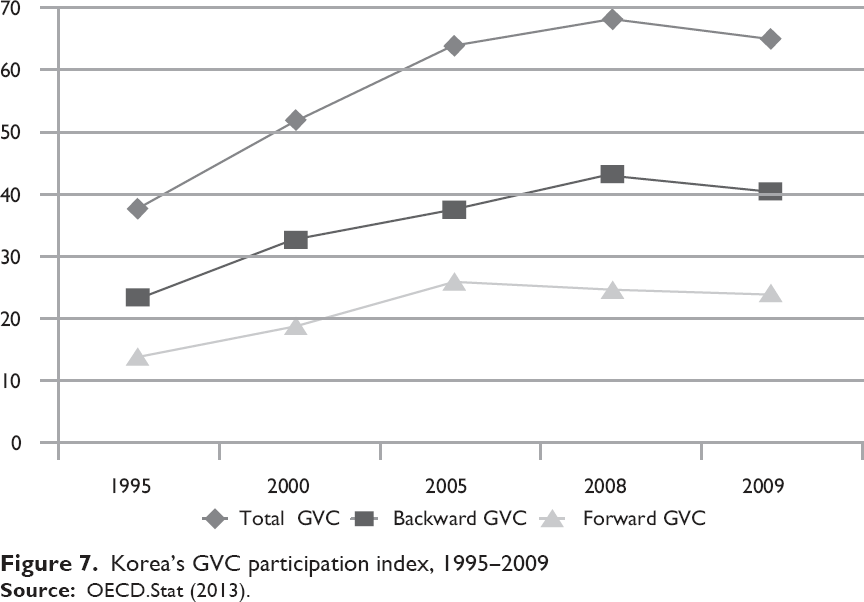

One of the novelties in the globalisation of the Korean capitalism after the 1997 crisis is the deepening incorporation into the global value chains (GVC). 7 As is seen in Figure 5, the ratio of imported intermediate inputs (raw materials and parts) to total intermediate inputs, for example, the basic indicator of GVC, rapidly increased after 1995. Figure 6 shows that the ratio of imported manufacturing inputs to total manufacturing inputs used in manufacturing sector decreased during 1970s before it increased after 1980s, reaching 28.8 per cent in 2013. Indeed, Korean capitalism rapidly incorporated into GVC and the East Asian production networks after the late 1990s. 8 According to OECD, Korea’s ‘total’ GVC participation Index, calculated as the sum of ‘forward’ and ‘backward’ GVC participation Index, rapidly increased from 37.9 in 1995 to 69 in 2009 (Refer Figure 7). It is notable that the ‘backward’ GVC Participation Index was not just higher than ‘forward’ GVC Participation Index. It also increased even in the period of global economic crisis of 2008. The OECD reported that Korea’s ‘total’ GVC Participation Index ranked 6th from the top in 2009 among 57 countries surveyed (OECD.Stat, 2013).

Contradictions and Limitations of Globalisation

The strategy to cope with the 1997 crisis by the forcible drive of globalisation, especially the maximisation of exports, more or less worked till the global economic crisis of 2008. However, it is uncertain that it would be effective in the future, considering that the increase of export critically depends on the low wage and weak Korean currency and that the Korean economy’s dependence on exports as a whole, measured by the ratio of exports to GDP, is already too high to continue to increase any more. Indeed, it already began to decrease from 2013, as is seen in Figure 2. In addition, as ‘China effect’ became weaker, the Korean export-led economy is facing increasingly serious problem. Indeed, Korea’s exports to China decreased consecutively in 2014, 2015 and 2016 by 0.4 per cent, 5.6 per cent and 9.3 per cent, before it recovered by 13.9 per cent in 2017. 9

The weakness of the export-led growth of the Korean economy is also revealed in the fact that the increase of exports induces the increase of imports rather than the increase of production and employment. The acceleration of globalisation after the 1997 crisis resulted in the loosening of domestic inter-industry linkage and the weakening effectiveness of exports as the motor of economic growth. Indeed, value-added inducing coefficient of export decreased from 0.7 in 1995 to 0.524 in 2013, while the import-inducing coefficient of export jumped from 0.3 in 1995 to 0.466 in 2013 (Bank of Korea, 2016b). According to OECD, the ‘import content of export’ of Korea, calculated as the ratio of imported raw materials and parts used for export products to total exports, was 65 per cent in 2009, ranked 6th from the top among 57 countries surveyed, while the ‘domestic value added in gross exports’ of Korea, calculated as the ratio of domestic value-added originated from exports to total exports, was 59.4 per cent, ranked 6th from the bottom (OECD, 2016a, 2016b). As a result, regime of ‘economic growth without employment increase’ consolidated. Indeed, according to Bank of Korea, the number of job creation, directly and indirectly attributable to the increase of exports by 1 billion KRW increased from 22.2 in 1995 to 5.6 in 2013. What Marx said in Capital volume 3 seems to be an exact description of the Korean economy after the 1997 crisis:

The internal contradiction seeks resolution by extending the external field of production. But the more productivity develops, the more it comes into conflict with the narrow basis on which the relations of consumption rests. It is in no way a contradiction, on this contradictory basis, that excess capital coexists with a growing surplus population. (Marx, 1981, p. 353)

Globalisation and Crisis in the Korean Capitalism

The Korean capitalism experienced economic crisis twice after 1970, first, in 1980, and second, in 1998. The annual rate of growth of real GDP was −1.9 per cent in 1980 and −5.7 per cent in 1998. During the period of global economic crisis of 2008, Korean capitalism slowed down, but did not contract. The annual rate of growth of real GDP in 2009 was 0.7 per cent, but not negative. However, it is certain that Korean capitalism entered into long downswing after 1987 and the regime of ‘low growth’ was established after the 1997 crisis. Indeed, the annual average rate of growth of real GDP consistently decreased for all successive government periods after 1987: 8.6 per cent for 1988–1992 (Roh Tae-Woo government); 7.4 per cent for 1993–1997 (Kim Young-Sam government); 5.2 per cent for 1998–2002 (Kim Dae-Jung government); 4.5 per cent for 2003–2007 (Roh Moo-Hyun government); 3.2 per cent for 2008–2012 (Lee Myung-Bak government); and 2.95 per cent for 2013–2016 (Park Geun-Hye government). The gap between Korea and OECD countries in the annual average rate of growth also narrowed down from 5.9 per cent (Korea 9%, OECD 3.1%) for the period of 1970–1997 to 2.13 per cent (Korea 4.05%, OECD 1.92%) for the period of 1998–2016 (World Data Bank, 2018).

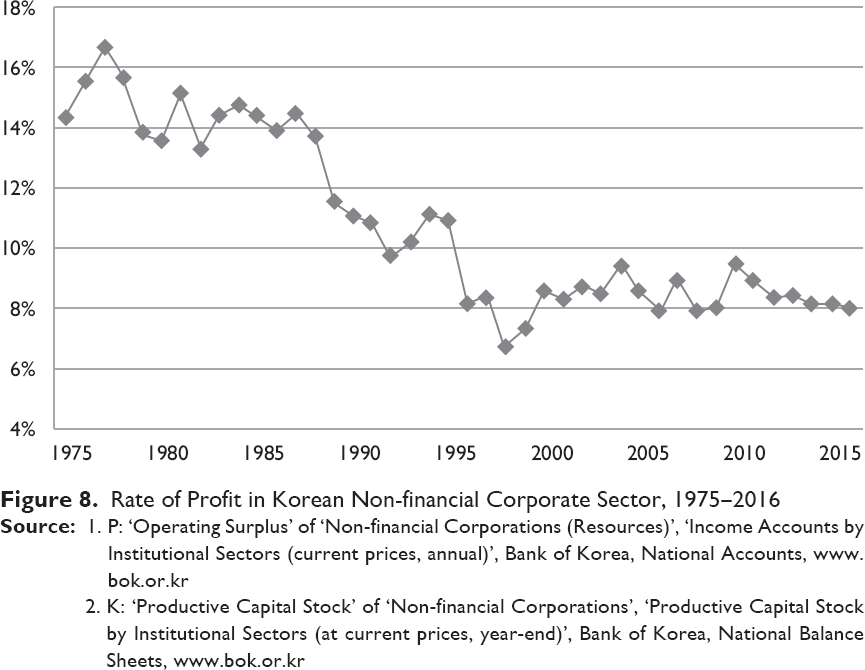

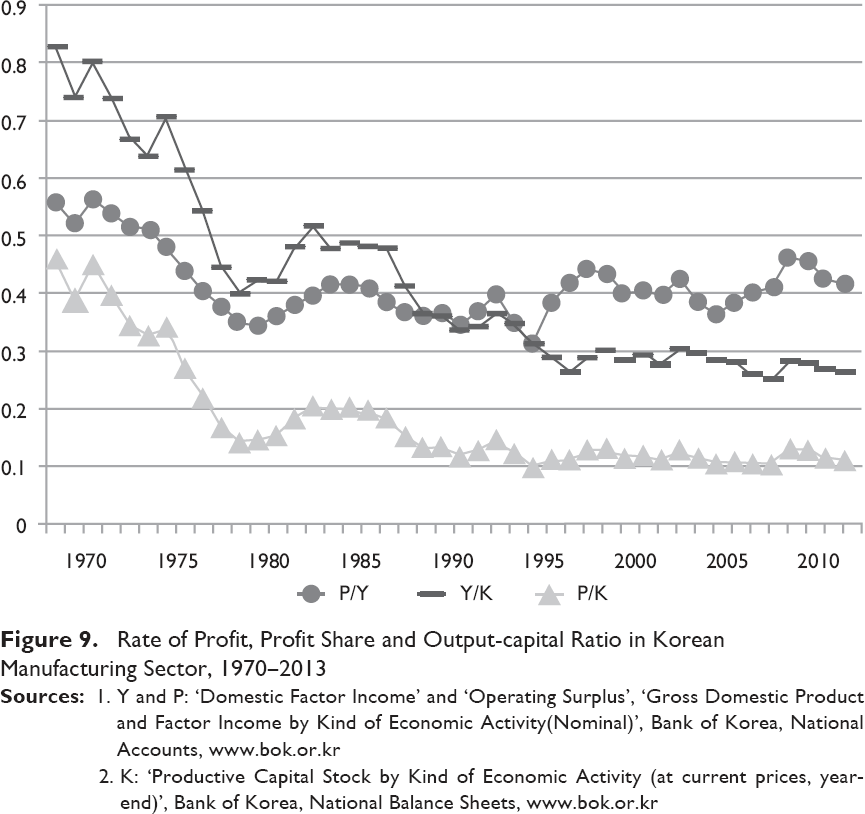

The long downswing or structural crisis in the Korean capitalism from 1987 onwards was closely related with the falling rate of profit. Figure 8 shows the trend of rate of profit in the Korean non-financial corporate sector for the period of 1970–2013. It epitomises the ‘stylised facts’ of the trajectory of the Korean capitalism through the movement of rate of profit. 10 First, the ‘golden age’ or high economic growth of the Korean capitalism ended around 1987 and was followed by structural crisis. Second, 1997 crisis was not just currency crisis or financial crash but the eventual explosion of the contradictions of capital accumulation, underpinned by the falling rate of profit since 1987. Third, despite the recovery from the 1997 crisis and fortunate avoidance of the global economic crisis of 2008, Korean capitalism failed to escape from the 30-year long structural crisis since 1987. As is seen in Figure 8, the rate of profit in the Korean non-financial corporate sector, which sustained as high as about 15 per cent till the late 1980s, rapidly declined after 1987 and hit 6.7 per cent in 1998, the lowest rate for the entire period of 1970–2016. With the drive of neoliberal globalisation and structural adjustment after the 1997 crisis, the rate of profit slightly recovered to 9.5 per cent in 2004. However, it fell again prior to the global economic crisis of 2008, followed by temporary and small recovery, but eventually decreased to 8 per cent in 2016, which was about 60 per cent of the pre-1997 crisis peak, that is, 14.6 per cent in 1987.

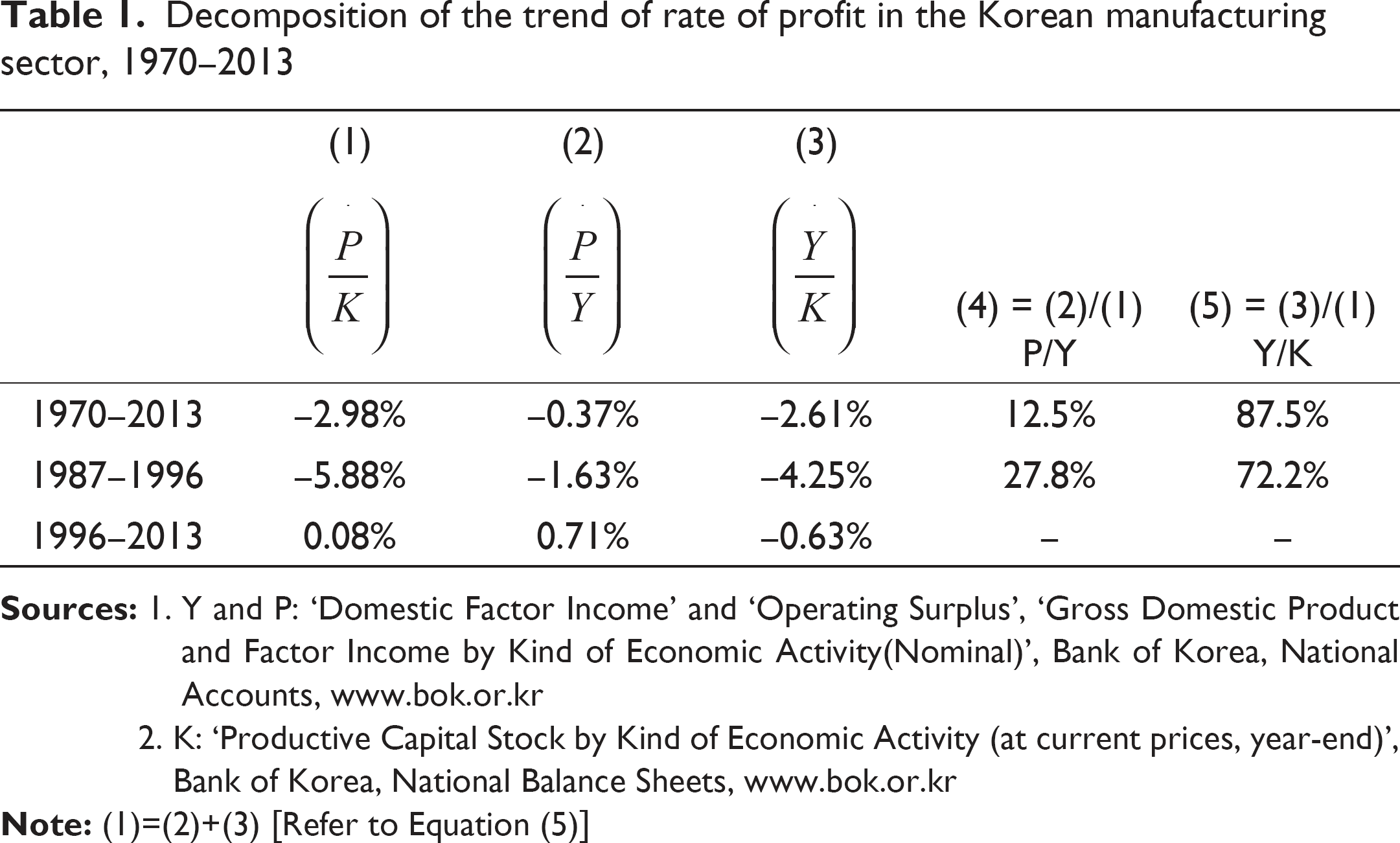

The rate of profit (P/K) can be decomposed into profit share (P/Y) and output-capital ratio (Y/K), as is seen in Equation (4), suggesting that the rate of profit changes in the same direction with profit share and oppositely with output-capital ratio. Marxian law of falling rate of profit due to the rising organic composition of capital can be empirically verified by the relation of falling P/K due to decreasing Y/K in Equation (4), considering that the reverse of Y/K, for example, capital-output ratio (K/Y), is a surrogate for Marxian organic composition of capital. If Thomas Piketty’s ‘first fundamental law of capitalism’, for example, α = r × β, argues that the increase of β(=K/Y, capital-output ratio) leads to the increase of α(=P/Y, profit share), in other words, worsening inequality of income distribution (Piketty, 2014, p. 52), Marxian law of falling rate of profit confirms the causal relation that the increase of β(=K/Y) results in the decrease of r(=P/K) in the equation r = α/β, which is a reformulation of Piketty’s ‘first fundamental law of capitalism’ (α = r × β). Equation (4) can be rewritten as a growth accounting equation, like Equation (5). Table 1 shows the estimated rate of change of the determinants of rate of profit in the Korean manufacturing sector, using Equation (5).

Decomposition of the trend of rate of profit in the Korean manufacturing sector, 1970–2013

2. K: ‘Productive Capital Stock by Kind of Economic Activity (at current prices, year-end)’, Bank of Korea, National Balance Sheets, www.bok.or.kr

Figure 9 and Table 1 show that the long-term trend of falling rate of profit is obvious in the Korean manufacturing sector as well. They also confirm that the falling rate of profit was overwhelmingly caused by the decrease of output-capital ratio, for example, rise of Marxian organic composition of capital. Moreover, they illustrate that falling rate of profit for the period of 1987–1996, leading to the 1997 crisis, was more a result from the decrease of output-capital ratio (Y/K) than from the decrease of profit share (P/Y). Indeed, the decrease of output-capital ratio accounted for 72.2 per cent of the falling rate of profit for the period of 1987–1996, more than twice the decrease of profit share did, 27.8 per cent. Then, the 1997 crisis can be understood as the crisis of capital accumulation underpinned by falling rate of profit due to rising organic composition of capital. While Figure 9 also shows that the rate of profit decline was arrested and remained at a low level after the 1997 crisis, Table 1 demonstrates that the stabilisation of the rate of profit was enabled by the intensified exploitation of working class. Indeed, the profit share, which can be used as a proxy to estimate Marxian rate of exploitation, 11 increased at the annual average rate of increase 0.71 per cent for the period of 1996–2013, which more than counteracted the downward pressure on the rate of profit due to the decrease of output-capital ratio at the annual average rate of 0.63 per cent. Indeed, the profit share jumped from 31.2 per cent in 1996 to 41.7 per cent in 2013, surpassing the pre-1997 crisis peak level, for example, 41.5 per cent in 1985. More specifically, the profit share jumped twice before and after crisis periods: first, for before and after 1997 crisis period, from 31.2 per cent in 1996 to 43.3 per cent in 2000; second, for before and after global economic crisis period, from 36.4 per cent in 2006 to 46.1 per cent in 2010. Indeed, the stabilisation of the capitalist profitability after the 1997 crisis was crucially indebted to the historically unprecedented intensification of exploitation of working people.

Besides intensified exploitation of workers, the globalisation drive after the 1997 crisis substantially counteracted the tendency of rate of profit to fall by facilitating the realisation of surplus value and capital turnover on an extended world market and cheapening the elements of constant capital. Indeed, the prices of imported capital good and intermediate goods fell or largely stabilised after 1997 (Statistics Korea, 2016). According to Hong (2013), FDI inflow and outflow also contributed to the increase of rate of profit of the Korean manufacturing sector during the period of 1999–2009. Then, following argument that the neoliberal globalisation was the main cause of the Korean 1997 crisis is hard to be defended:

The major cause of the crisis was not inherent inefficiencies in the structure of the Korean development model, but rather contingent inefficiencies created by liberalization, especially in the 1990s. … liberalization had brought Korea to the point where a financial crisis was almost inevitable. … Destructive liberalization in the 1990s made the onset of a difficult economic period in Korea inevitable. (Crotty & Lee, 2009, pp. 151, 153, 164. Emphasis by Crotty and Lee)

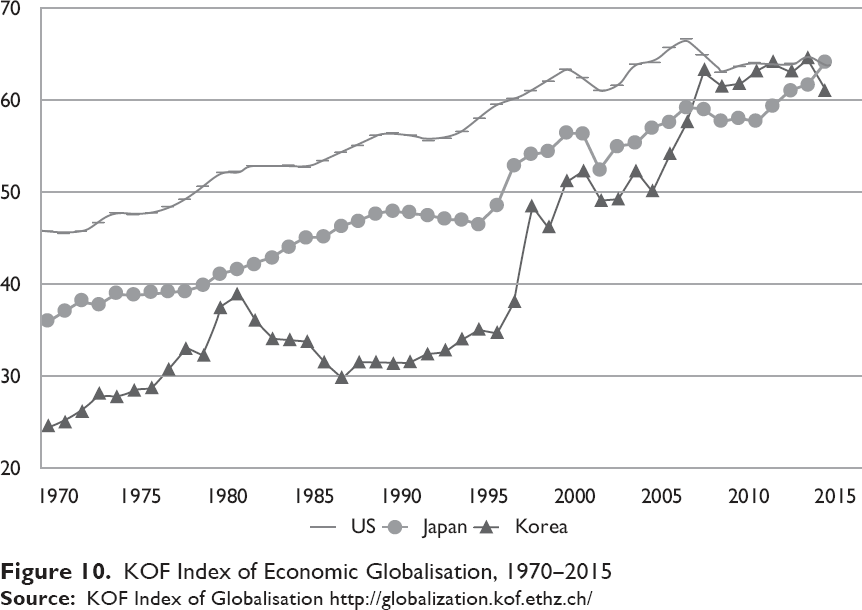

However, alleged advancement of globalisation prior to the 1997 crisis is hard to be evidenced. As seen in Figure 2 and Figure 4, the ratio of exports to GDP or the ratio of FDI inflow to GDP, key indexes of globalisation, do not show any significant trend for the period of 1987–1997. On the contrary, these ratios little increased or even decreased for some years during the period of 1987–1997. The globalisation proceeded rapidly not before but after the 1997 crisis. As Figure 10 shows, the ‘KOF Index of Economic Globalisation’ 12 of Korea jumped twice during the period of 1970–2012: first, for the post-1980 crisis period, from 31.8 in 1979 to 38.6 in 1981; and second, for the post-1997 crisis period, from 37.8 in 1997 to 48.4 in 1998. It increased more rapidly during the 2000s, surpassing the level of Japan, eventually reaching 64.7 in 2012, almost same as that of the USA, one of the most globalised economies in the world. It is also remarkable that the globalisation proceeded uninterruptedly in Korea after the global economic crisis of 2008, when it retreated in many countries. For example, between 2007 and 2009, ‘DHL Global Connectedness Index’ 13 of Korea increased from 59 to 64, while that of Germany, Japan and China all decreased from 77 to 71, from 53 to 49 and from 40 to 39, respectively. The Index of Korea was 68 in 2013, ranked 13th from the top in the world. The post-1997 globalisation of Korea was not just enforced from outside through such as the IMF rescue package by transnational capital. Indeed, Korean capital and state actively pursued the globalisation for themselves as the strategy to resolve the 1997 crisis. Free Trade Agreement (FTA) was one example of this strategy. Starting from FTA with Chile in 2003 and with the USA in 2007, Korea has signed FTA with as many as 50 countries as of 2015.

The post-crisis acceleration of globalisation can also be noticed in the trend of cross-border M&A sales and purchases. The value of cross-border M&A sales for Korea jumped from less than USD 1 billion in early 1990s to USD 3.9 billion in 1998 and USD 10.5 billion in 1999. The value of cross-border M&A purchases for Korea also jumped from about USD 1–2 billion before 2006 to USD 8.4 billion in 2007 and USD 10 billion in 2010. 14 Indeed, the globalisation of Korean capital proceeded rapidly after the 1997 crisis and the global economic crisis of 2008. While the globalisation of Korean capital of the post-1997 crisis period was mostly pursued by foreign transnational capital to purchase Korean companies, Korean capitals are the main actors of globalisation of capital after the global economic crisis of 2008, as they actively purchased foreign companies. Considering that the globalisation of capital retreated in many OECD countries after the global economic crisis of 2008, the aggressive pursuits of globalisation of Korean capitals appear all the more pronounced as well as dangerously discordant with the trend.

Concluding Remarks

Intensification of exploitation of working people and aggressive globalisation are the main characteristics of post-1997 Korean capitalism. The globalisation of the post-1997 Korean capitalism accompanies the transformation of the Korean dominant capitals into transnational capitals, global extension of the loci of valorisation and realisation of Korean capitals and the incorporation into GVC rather than one-sided expansion of domination of the foreign transnational capitals and imperialism in Korea. Globalisation of the Korean capitalism accelerated after and not before the 1997 crisis. Admitted that globalisation preceded the 1997 crisis in Korea, it was the responses of the capitals and state to the structural crisis that already began from 1987. Then, post-Keynesian economists and Developmental Statists assertion that the ‘financial liberalisation without preparation’ caused the 1997 crisis is simply groundless. The pre-1997 globalisation was almost nothing, compared to the post-1997 globalisation, which was characterised by the globalisation of production capital and the incorporation into GVC. In short, the crises in the Korean capitalism were not caused by globalisation. On the contrary, globalisation was consciously and forcibly pursued by Korean capitals and state as a weapon to fight with the on-going crises. Post-Keynesian or Developmental Statist’s position is also hard to be sustained, in the face of the fact that the Korean capitalism was largely exempted from the global economic crisis of 2008 despite the rapid globalisation after the 1997 crisis, and that globalisation became all the more conspicuous after the global economic crisis of 2008. As globalisation is not the cause of crisis but the counteractive forces of capital and state to stem the crisis due to falling rate of profit, the proposed post-Keynesian or Developmental Statist regulation of the globalisation, such as Tobin tax or exit from Eurozone etc., cannot be effective policy to cope with the crisis. On the other hand, the pursuit of globalisation can neither resolve the capitalist crisis, because it will only temporarily postpone the day of reckoning. Indeed, recent cooling down of the export-led growth engine of the Korean economy demonstrates the inherent limitations to the acceleration of globalisation as a way of fighting with crisis. Neither will the incorporation into GVC be the alternative. Indeed, any malfunction, bottleneck or break in any GVC could spread the crisis of value production on a global scale. As GVC is more likely to break in the production chain, than financial or distributive chain, repercussions of the break in GVC will be more direct and serious, compared to the case when the problem is mainly financial, like the global economic crisis of 2008. In short, globalisation can counteract the tendency of the rate of profit to fall and crisis temporarily only to prepare the explosion of bigger crisis in the long run by extending and deepening the contradictions of capital accumulation on a global scale. The capitalist crisis can be ended only by the globalisation of anti-capitalist movements against the capitalist globalisation.

Footnotes

Acknowledgement

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

2.

The difficulty of estimating the stock of the circulating constant capital is frequently quoted to justify its exclusion from the denominator of the rate of profit.

4.

Korea International Trade Association, KITA.net.

5.

Considering that P = Z − M − W from Equation (2) and dividing the equation P = Z − M − W by the quantity of products (Q), ![]() obtains, where P/Q, Z/Q, M/Q, and W/Q mean the unit profit (or profit margin), unit price, unit intermediate input cost, and unit labor cost, respectively:

obtains, where P/Q, Z/Q, M/Q, and W/Q mean the unit profit (or profit margin), unit price, unit intermediate input cost, and unit labor cost, respectively:

![]() shows that the decrease of unit labor cost (W/Q) results in the increase of profit margin (P/Q), if all other things being constant. Considering also that P/Q could be used as an index of rate of exploitation, it is obvious that the decrease of unit labor cost leads to the increase of rate of exploitation.

shows that the decrease of unit labor cost (W/Q) results in the increase of profit margin (P/Q), if all other things being constant. Considering also that P/Q could be used as an index of rate of exploitation, it is obvious that the decrease of unit labor cost leads to the increase of rate of exploitation.

6.

9.

Korea International Trade Association, KITA.net.

10.

For the details of the ‘stylized facts’ of the trajectory of the Korean capitalism, focusing on the trend of ‘Marxian ratios’, including rate of profit, rate of exploitation and organic composition of capital, refer to Jeong (2004) and Jeong (![]() ).

).

11.

12.

‘KOF Index of Economic Globalization’ is calculated by combining following variables with some weights: trade in goods, trade in services, trade partner diversification, foreign direct investment, portfolio investment, international debt, international reserves, international income payments, trade regulations, trade taxes, tariffs, investment restrictions, capital account openness, etc.

13.

‘DHL Global Connectedness Index’ is calculated to measure the depth and breadth of countries’ integration with the rest of the world as manifested by their participation in international flows of products and services (trade), capital, information and people, combining following variables with some weights: exports of goods and services (% of GDP), FDI flows (% of total investment), stock market investment (% Int’l), telephone calls (% Int’l,) tourists (% Int’l), university students (% Int’l), migrants (% of population), etc. DHL, Global Connectedness Index 2016 ![]() .

.

14.

Cross-border M&A sales of Korea are calculated on a net basis as follows: Sales of companies in Korea to foreign transnational companies (TNCs) minus sales of foreign affiliates in Korea. Cross-border M&A purchases are also calculated on a net basis as follows: Purchases of companies abroad by Korea-based TNCs minus sales of foreign affiliates of Korea-based TNCs. UNCTAD, World Investment Report 2015: Annex Tables. ![]() .

.