Abstract

Abstract

The effects of a unilateral cut in emissions (e.g., by Annexure 1 countries in Kyoto) are analysed in a dynamic two-country two-commodity model. If the fossil fuel is priced at marginal cost, then a unilateral cut reduces total emissions (the carbon leakage is less than 100%). But if the fuel is priced above marginal cost, then a ‘green paradox’ appears, that is, the price of the fuel will fall until its use (over time) exhausts the entire stock. Here, a unilateral policy is self-defeating and it is necessary to get binding commitments on fossil fuel use from all the countries. The production and trade implications for the participant and non-participant countries are analysed.

Introduction

The total stock of fossil fuel available in the world, if burnt with existing technologies, would add so much to the stock of carbon in the atmosphere that there would be serious consequences for the quality of human life on this planet. 1

The stock of carbon in the atmosphere will raise the mean temperature and increase weather variability. The world will see a rise in the sea level (due to a melting of polar ice caps) and a melting of glaciers where some of the big rivers of the world originate. The rise in the sea level will cause migration from the areas that would get inundated, while changes in the weather will require a major change of cropping pattern, etc. Parts of the world would see land becoming more arid. Coping with this would require massive redeployment of resources.

In the last hundred years, 63 per cent of the cumulative emissions of greenhouse gases have come from the developed economies. Of that, the United States has accounted for 25 per cent and Western Europe for 21 per cent. China and India, home to 40 per cent of the world’s population, have contributed, respectively, 7 per cent and 2 per cent of the last hundred years of cumulative emissions.

See Eichner and Pethig (2011), Dutta and Radner (2012) and van der Ploeg and Withagen (2012) for discussions on these issues.

The Kyoto Protocol tried to grapple with this twin problem of the heating of the planet and a desire to break out of poverty by the poorer nations by dividing the world into Annexure 1 countries and Annexure 2 countries. The former set had quantitative targets imposed on emissions while the latter did not. In the recently concluded follow-up meeting in Durban, there was a call to include the Annexure 2 countries in the quantitative targets. The meeting also saw Canada (an Annexure 1 country) withdraw from the Kyoto agreement. This article looks at the implications of not including all major economies in restricting global emissions. It focuses on the interaction between the actions of Annexure 2 countries and fossil fuel producers. These are at the heart of including China and India in any future agreement (and possibly, for the withdrawal of Canada).

Thus, we try to answer the question that if a subset of countries become more virtuous (by reducing greenhouse gas emissions), then is it a step in the right direction towards fighting global warming (as was the case in the Kyoto Protocol and the commitment by the European Union to unilaterally cut emissions until 2020)?

Climate negotiations moved away from the Kyoto Protocol to the Paris Agreement wherein each country decides on its contribution (voluntarily) towards a global carbon reduction programme. But with the election of Donald Trump and the withdrawal of the United States from the Paris Agreement, unilateralism is back, except it is the richest country in the world that has removed itself from any binding carbon emission norms! The analysis further goes through with this twist—there are some countries who are not using policies to reduce their emissions. Of course, one has to recognise that the equity principle behind exempting poor countries in the Kyoto Protocol has been replaced by the bullying attitude of the world’s biggest polluter!

International trade and competitiveness issues have been absent from the centre stage of modelling of the climate change economic models, though always lurking in the background of the policy debate (for instance, in Eichner and Pethig, 2011, there is only one final good, so competitiveness issues do not arise). have an intermediate input (oil) and only a single final good). I set up a two-country model—the two countries are identified as Annexure 1 countries (the North) and Annexure 2 countries (the South). North cuts its emissions unilaterally either now or in the future. The model has two goods—called clean or dirty depending on the type of fuel used to produce it. This enables us to analyse terms of trade (or competitiveness) issues that arise from the unilateral policies to mitigate climate change. Finally the model allows for capital accumulation. This is introduced to look at accumulation effects of emission reduction. 4

It also raises the marginal product of complementary inputs—see Dutta and Radner (2012) for a discussion, although capital accumulation in their model is exogenous.

The answer that emerges to the question whether a unilateral emission cut benefits the world is, it seems, both ‘Yes’ and ‘No’. It depends on the supply curve for fossil fuels. The answer is in the affirmative if the fossil fuel is priced at marginal cost, and the increased demand from, for example, Annexure 2 countries is less than the lower use by Annexure 1 countries (carbon leakage is less than 100%). This is the normal reaction in a market, where following the (exogenous) decrease in the supply of a good, a rise in its price will elicit supplies from other producers—in this case the good in question is a dirty good. The empirical evidence based on CGE models (see, e.g., Burniaux & Martins, 2000; IPCC, 2007) estimate carbon leakages to be about 20 per cent, at most.

The pessimistic ‘No’ comes from a concept known as ‘the green paradox’ 5

The concept is due to Hans Werner Sinn (2008). It has spawned a large literature, most of it in a partial equilibrium setting. See for example (in addition to the references in the text) Gerlagh (2011) and Hoel (2010).

The problem of global warming (i.e., the aggregate effects) has two dimensions. The first is the level of emissions. These have to reduce drastically because the initial stock in the atmosphere is very large. The second is the timing: given a level, postponing emissions is better, that is, emission cuts have to be front-loaded. The green paradox may violate both of these. 6

See van der Ploeg and Withagen (2015) for an elaboration of the term green paradox—different authors use different welfare measures. For our purposes, since we are not doing a welfare analysis, the discussion in the text would do.

The green paradox is based on the reaction of producers to the decline in the price of fossil fuel when subsidies to clean fuel or taxes on the fossil fuel are set at arbitrary (as opposed to optimal) levels—see Hoel (2010) for a discussion of the nature of those taxes. One can possibly appeal to (even in the absence of uncertainty) Weitzman’s quantitative restriction argument because the effects of the green paradox occurring would be catastrophic.

There is by now a large literature that deals with these issues. A number of papers have looked at the logical consistency of the green paradox in partial equilibrium settings. The outcome is mixed. In a general equilibrium setting, there are papers by van der Ploeg and Withagen (2010, 2011, 2012), Eichner and Pethig (2011) and Smulders, Tsur, and Zemel (2010). Van der Ploeg and Withagen (2011, 2012) and Smulders et al. (2010) look at a closed economy infinite horizon optimal growth model where two sources of energy—a clean backstop and a fossil fuel are perfect substitutes. 8

In Smulders et al. (2010), there is a sunk cost of using the clean fuel.

This is reminiscent of the convergence literature in growth theory, where, for example, China or India may have a lower output per capita given their lower capital–labour ratios compared to the United States. No trade is allowed. If we open up these economies to trade, within a Heckscher–Ohlin set-up, factor-price equalisation would ensure that there is no convergence—both economies via their Euler equations would have identical growth rates of consumption (see Chen, 1992).

The three major exceptions to the closed economy modelling are di Maria and van der Werf (2008), Eichner and Pethig (2011) and Sen (2016). The former looks at trade and directed technical change, but without the intertemporal element in fossil fuel pricing. They find that there is carbon leakage when a subset of countries embarks on limiting fossil fuel use, and that this is reduced by directed technical change. Eichner and Pethig (2011) set up a two-period model (with one final good produced with fossil fuel being the variable input) to analyse carbon leakages and the green paradox. 10

A three-period model is also discussed as an extension.

There have also been some interesting papers analysing technical change to make growth ‘cleaner’. Some of these take into account the nature of the fuel market, in particular exhaustibility and the endogenous response of resource owners (see, e.g., Chakravorty, Leach, & Moreaux, 2011; Grafton, Kompas, & van Long, 2010; Henriet, 2012, albeit in a partial equilibrium setting). Others like di Maria and van der Werf (2008) and Acemoglu, Aghion, Bursztyn, and Hemous (2012) look at directed technical change but do not discuss this in any detail. 11

In the two papers closest to ours, di Maria and van der Werf (2008) look at carbon leakage but not the dynamic nature of fossil fuel pricing; while Eichner and Pethig (2011) have only one final good and no capital accumulation. Since they also do not allow for borrowing or lending, their intertemporal substitution parameter is redundant. In equilibrium, countries consume the production of their final good output. For an analysis of borrowing and lending and the effect of carbon leakage on the world interest rate, see Sen (2012).

Finally, there is a strand of the literature that emphasises strategic interaction (see, e.g., Barrett, 2003; Chatterji, Ghoshal, Walsh, & Whalley, 2011; Finus, 2001). Dutta and Radner (2012) analyse the strategic interaction with capital accumulation (being treated as exogenous—more like disembodied technical progress). 12

Their conclusion about ‘aid’ from the rich to the poor countries to make the latter participate in cutting back emissions is similar to the policy implications obtained in this article. I focus on different issues, though.

This article should be seen as providing a slightly different perspective on the use of different types of fossil fuels. Van der Ploeg and Withagen (2012) have drawn our attention to the fact that oil (and gas) is less polluting than coal, and hence should be used exclusively initially. My analysis suggests that while this may be true, oil is much more likely to upset the applecart of climate change negotiations because of the presence of Hotelling rents.

What about the distribution of welfare losses (in a more general set-up ‘competitive’ advantage) between the belt-tightening Annexure 1 countries and the ‘free-riding’ Annexure 2 countries. This requires two goods to analyse a terms of trade advantage. As mentioned earlier in Eichner and Pethig (2011), for instance, there is only one final good and thus there is autarky in ‘value-added’.

Before turning to my model, I also note that the analysis further has implications for free trade in goods (import of fossil fuel embodied in goods). As the production of the dirty good moves to those countries that do not cut fossil fuel use, those who do can continue to import these by exporting the clean good. Thus, in the context of the recent climate change negotiations, how much of the increased Chinese emissions should actually be debited to the American account, since they will consume the goods produced? I do not pursue this line of enquiry as it would take us too far afield (see Whalley, 2011, for a discussion on trade and environment negotiations).

Consider a three-period model. Not much happens in the third period in which the fossil fuel input is not available, having either been exhausted or been prohibited by policy or superseded by innovation—this is the equivalent of the ultimate clean steady state of van der Ploeg and Withagen (2011). Two goods—called clean and dirty—are produced and consumed in each country initially. International borrowing or lending is not considered and thus trade is balanced in each period. The first period is one where the capital stock is given by history, the second and the third period capital stocks are optimally chosen. The fossil fuel producers are not considered separately as a third bloc (as do Eichner & Pethig, 2011). If they are, then imagine that only the value-added in each economy is available for consumption and capital accumulation, and that the fossil fuel producers consume the dirty good only. Unlike Copeland and Taylor (2005), there is no trade in pollution permits. Emissions between blocs remain strategic substitutes. No strategic interaction between the bloc of countries is considered (as in Barrett, 2003; Dutta & Radner, 2012; Finus, 2001), nor defection or entry into blocs (unlike Babiker, 2005). It will become clear that free-riding pays, but in the presence of the green paradox this comes at the expense of everyone becoming worse off.

As discussed in the Introduction, the first period is one where the accumulated carbon in the atmosphere is likely to make life in the future difficult. Thus, policy should endeavour to reduce carbon emissions as much as possible. Also, too much emission now could exacerbate the problem. So given the total emissions, postponing these is desirable.

Consumers

The representative individual in each country has a utility function defined over the three periods with a constant discount factor given by β. There are two goods, indexed ‘X’ (the numeraire) and ‘Y’. The instantaneous utility function is quasi-linear. 13

See Bond, Iwasa, and Nishimura (2011) for a discussion of non-homothetic preferences in dynamic trade models.

Quasi-linearity makes the utility derived from dirty goods concave but the utility from the clean good is linear.

For the South, we have identical preferences 15

Preferences are identical but not homothetic.

In the earlier equations, a subscript (t = 1, 2, 3) denotes the time period, and the South’s corresponding variables are denoted by an asterisk. In principle, the rates of time preference could be different but to keep the analysis simple let us assume that they are identical. This will enable us further, given quasi-linearity, to talk of ‘the’ rate of interest in any period.

Note, given the public bad nature of global warming, we do not explicitly mention this as an argument in the utility function. It is easy to incorporate a term in each period to take cognizance of the stock of greenhouse gases, for example, Π1 = Π0 + π1, where Π0 is the stock of emission at the beginning of period 1 and π1 is the emission in period 1 (net of any regenerative capacity of the environment).

The Firms

Let us turn to production decision by firms. A firm solves a static problem in each period. It is assumed to rent the capital from households and choose the allocation of capital between the two ‘sectors’ as well how much of the clean and fossil fuels to be used (the specific factors are, naturally, not mobile between sector and earn rents). The dynamic part of the firms’ problem is delegated elsewhere—the household decide on investment and the fossil fuel suppliers decide on the time path of the price of fuels. First, I present the static decisions of the firm.

The clean good (its supply denoted by X) is produced using capital (KX), clean energy, S, that is supplied (perfectly elastically) at a price s, and some specific factors (ZX). 16

The clean energy could be inelastically supplied, but then it would be indistinguishable from ZX. The main results of the article do not depend on the supply curve for S.

Our analysis imposes quantitative restrictions on fossil fuel use (as do Eichner & Pethig, 2011). Ishikawa and Kiyono (2006) look at non-equivalence of various types of emission-reducing policies. It is possible to include an abatement technology but it does not seem worth the additional complications.

The production functions F(.) and G(.) are increasing and linearly homogeneous in their respective three arguments, with diminishing marginal productivity. Since the Zi’s are fixed, the two production functions are strictly concave in the variable inputs KX, and S, and KY and R, respectively. It is noteworthy that armed with quasi-linearity and the strict concavity of the production functions in their variable inputs, all the signs of the comparative static effects further are determined unambiguously!

The revenue function involves equating the value of marginal product of capital in the two sectors (5a), the marginal product of the clean fuel to its price (5b), and the marginal product of the fossil fuel input equal to its market price (5c).

A similar set of equations describe the production block in the South.

Market-clearing

In the absence of international borrowing and lending, trade is balanced between the two countries. The two goods are traded in the first two periods (in the third, only one good is produced in either country so there is autarky). Market-clearing requires, in any period, Equation (6) to hold—the left-hand side is the total supply of the dirty good and the right-hand side is the total demand:

By Walras’ law, the market for the clean good also clears (shown in Equation (7) to highlight that capital accumulation involves the clean good) (note the subscript 1 here is the constant price of the clean good and not a time subscript):

In the light of the interest rate being constant 18

.Note that it is the product interest rate in terms of the X-good that is constant, and not the consumption interest rate.

Further, we shall see that the South will expand its dirty good production, when the North imposes restrictions on the use of fossil fuel (we will let the North and the South be identical in their endowments and hence there is no reason to trade in the absence of, for example, different attitudes to fossil fuel use). In Eichner and Pethig’s (2011) one final good model, such a restriction makes the North’s (their ‘Abating Countries’) GDP and consumption fall one-for-one. In my model, The North’s consumption of the dirty good need not fall, even when its production does.

Dynamics

There are three sources of dynamics in this model, two of them familiar from optimal growth models, namely the investment and the consequent accumulation of capital, and allocation of consumption across periods via the Euler equation (or the Keynes–Ramsey rule). The third comes from models of natural resources—when we have the Hotelling rule in the pricing of the fossil fuel.

Investment in any period becomes next period’s capital stock (implicitly assuming 100% depreciation). 19

Nothing hinges on this. Assuming zero depreciation makes no difference to the analysis. A rate of depreciation that lies between zero and one would necessitate carrying the parameter of depreciation in calculating the expected marginal product of capital.

In a dynamic context, the linearity of the utility function in good X ties down the real rate of interest (in terms of good X) to be equal to the rate of time preference.

If the discount factors are identical, as is assumed here, then r = r*.

Finally, the demand for fossil fuel across periods must be at most equal to the existing stock. The demand for fossil fuels occurs in the first two periods when the dirty good is produced:

If Equation (10) holds as an equality, the price of fossil fuel must satisfy the Hotelling rule (since fossil fuel reserves can be extracted in either period). 20

We assume a constant marginal cost of extraction, c. If the cost of extraction were variable (e.g., stock-dependent, then the Hotelling rule would hold for one unit—all units with lower cost of extraction would be mined now, all units with a higher cost would be mined in the future. This is clear by setting different c’s in Equation (11).

In Equation (11), the left-hand side is the surplus from extracting one unit of the fuel in the next period (with c being the constant marginal cost of extraction), while the right-hand side represents the surplus today carried over to tomorrow at the interest factor β-1.

This implies

On the other hand, if demand is strictly less than the exogenous stock of the fossil fuel (in Equation (10)), Equation (11) holds trivially with

That is, marginal cost pricing prevails.

Of course, policy and climate change negotiations are precisely in place to ensure that Equation (10) does not hold with an equality—all or some of the terms on the right hand are sought to be reduced. Note, as emphasised by Acemoglu et al. (2012), that an environmental disaster is possible even when the natural resource is not exhaustible. We consider the exhaustible case also because it comes with a sting in its tail (i.e., the ‘green paradox’).

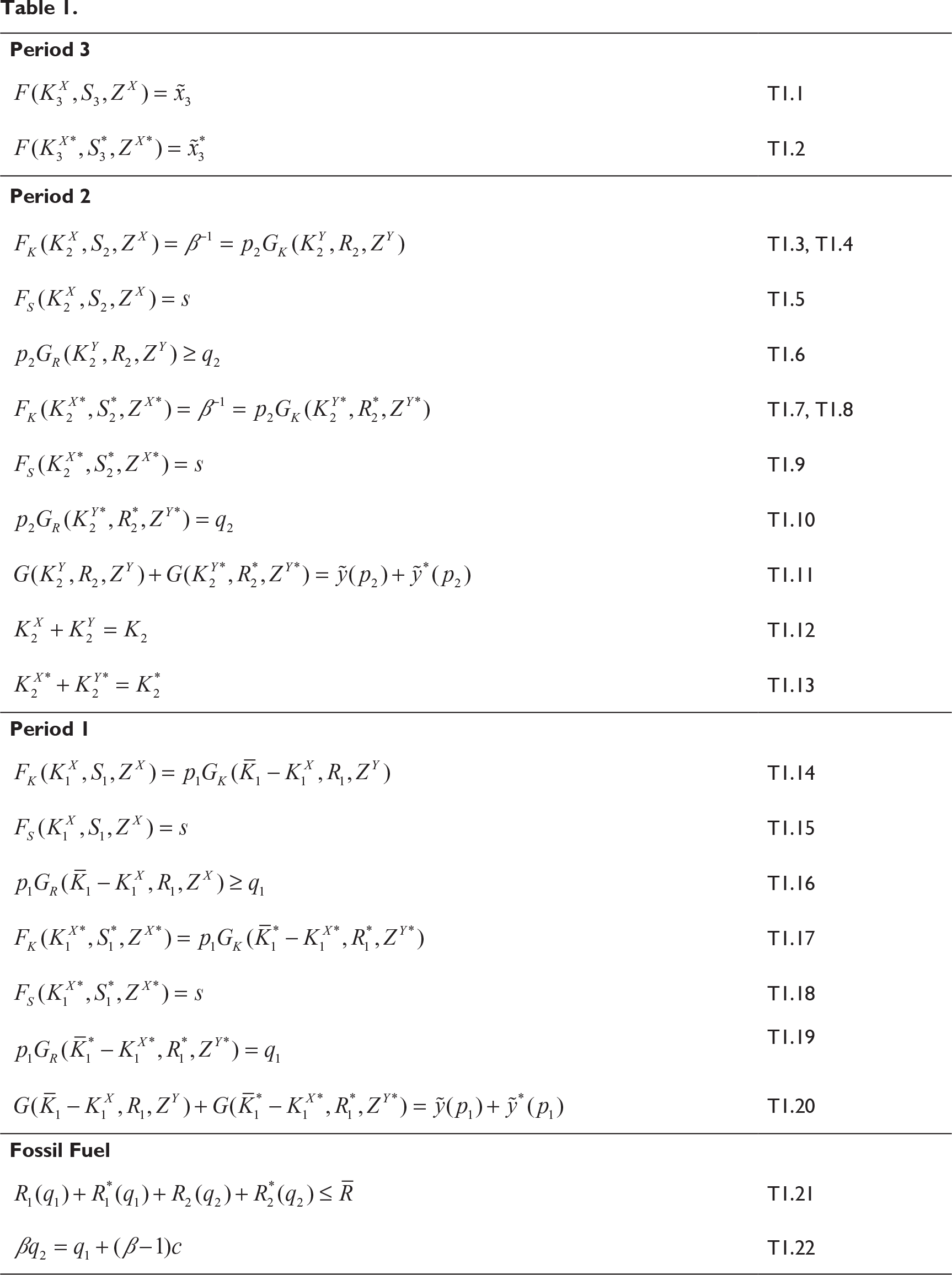

This completes the description of the model. Let us collect the equations describing the model to be used in Table 1, before turning to the analysis of the problem at hand.

Equations T1.1 and T1.2 are the market-clearing equations for the clean good in period 3.

Summary of the Model with Marginal Cost Pricing

A similar interpretation is to be used for period 1 (T1.14 to T1.20) except that now the initial capital stock is historically given and, while there is mobility of capital between sectors to ensure the equality of marginal products, the return to capitals is no longer tied to a given real interest rate.

To anticipate (and avoid repeating) some tedious derivation further, note that for period 2, Equations T1.4, T1.6 (with an equality), T1.8, T1.10 and T1.11 can be solved for

For period 1, Equations T1.14 to T1.20 (when T1.16 holds as an equality) can be solved for

Let us now turn to the effects of a unilateral cut in fossil fuel use by the North. In Section III, fossil fuel is supplied competitively with marginal cost pricing, while in Section IV there is an endogenous mark-up over marginal cost and the Hotelling rule kicks in.

Before turning to the analysis of effects of a restriction on fossil fuel use by the North, let us define a few terms.

Note that this is different from the way some others use this term, for example, Eichner and Pethig (2011). They use this term to imply 100 per cent or more leakage within the same period. It is also different from the definition(s) given by Gerlagh (2011).

We shall see later in this section that carbon leakage by our definition (without the green paradox) turns out to be less than unity (in absolute value). Taken together, these definitions imply that when the green paradox occurs some, leakage necessarily spills over to periods without a cut in fossil fuel use (the carbon leakage in these periods would be infinity).

We start off with the case of marginal cost pricing of the fossil fuel. While this maybe empirically relevant for some fossil fuels, for example coal, it also serves to prepare us for the Hotelling rule case discussed in the next section. 22

Eichner and Pethig (2011) do not discuss marginal cost pricing of the fossil fuel—in their analysis the marginal cost is zero.

We look at two specific situations: Either (a) in period 1 the North will reduce its production of the dirty good or (b) it will do so in period 2—this is anticipated in period 1 23

Complete cessation of production of the dirty good in the North is a simple extension in the framework of this article. It, however is not a ‘small’ change and is imperfectly served by calculus.

Period 1

Suppose now the North restricts the fossil fuel input at some exogenous level

When T1.16 does not hold with an equality, that is,

we solve the six equations (T1.14, T1.15 and T1.17 to T1.20) for

What does this tell us about fossil fuel use in the ‘non-abating’ countries? We would expect some carbon leakage as fossil fuel demand in the abating countries falls. Although its price is tightly tied to the marginal cost of production (and therefore does not change), its demand in the non-abating South increases via an excess demand for the dirty good that manifests itself in a rise in

The answer is that the excess demand for the dirty good is met partly through increased production (using more fossil fuel), and partly through an increase in price of the good. This is what one would expect in a well-behaved market with Walrasian price adjustment. More than 100 per cent increase in the use of fossil fuel (apart from a lacking in good economic intuition) would make an increase in fossil fuel use by the North a policy to (partially) mitigate climate change—this would no doubt be music to the ears of the oil lobbies and climate-change-deniers!

In our set-up we have (again see the appendix for details),

The denominator in Equation (14) is the excess demand for the dirty good and the numerator is only a fraction of that. The fact that the derivative is negative implies that the oil use are strategic substitutes across the two blocs. 24

See the discussion on strategic complimentarity versus strategic substitutability in Copeland and Taylor (2005).

Period 2

Imagine that there is marginal cost pricing, but now a (foreseen in period 1), reduction in fossil fuel use in the North in period 2, such that the marginal product of fossil fuel exceeds its price, that is,

Again the quotas are auctioned and the revenue rebated to the households in a lump-sum fashion.

We can solve the four Equations T1.4, T1.8, T1.10 and T1.11 for

As earlier, we shall first solve for the seven variables in terms of

The interpretation is the same as that for a period 1 reduction, with one major difference: when in period 1 the North reduces its use of fossil fuel, capital is relocated from the Y-sector to the X-sector. Its Y-output falls compared to the laissez-faire level but there is increased production of X. In period 2, on the other hand, the output of the X sector is given by the input use determined solely by Equations T1.3 and T1.5 (and therefore do not change). 26

For the South, similarly, Equations T1.7 and T1.9 uniquely determine input use in the clean sector, and hence the size of that sector.

Imposing control on fossil fuel use in both periods by the North results in the sum of the effects in the individual periods and needs no further elaboration. 27

Quasi-linearity is important here. We do not have to worry about capital accumulation being affected when the restriction on fossil fuel is operative in both periods.

A simple extension gives us Proposition 2:

Period 1 Emission Cut

What happens to worldwide use of the fossil fuel if the North cuts its use of these in the first period, in the presence of positive rents in the price of fossil fuel? The market price of fossil fuel follows the Hotelling rule (Equation 16), with the price in both periods exceeding marginal cost. The scarcity rents arise from limited fuel supply over the two periods being equated to the demand for it (Equation T1.21 holding as an equality).

The exposition of this section is helped enormously if we recognise the analysis of the previous section is the effect of the stricter abatement policy in the North with the price of fossil fuel held constant (of course, in contrast to the previous section, in this section the price is above marginal cost). The only additional bit required in the analysis is to allow the qi’s to adjust so that Equations (16) and (17) hold. To anticipate the detailed results further, we saw that in Section III, compared to the initial situation, there was an excess supply of fossil fuel after the adjustment (with price of fossil fuel constant). Now if its price were allowed to adjust it would decline in that period but not so much that takes its (fossil fuel) demand back to the initial equilibrium. The quantity demanded in the period that the policy is implemented, must be less than initial demand, that is, carbon leakage in that period is not 100 per cent. The reason why this is so, is that if the price of fossil fuel falls today, it must also fall tomorrow (and vice versa) via the Hotelling rule. 28

.In my model, the real product interest rate is pinned down by the rate of time preference. It is possible that in other models, where this is not the case, fossil fuel prices across periods are not so tightly linked. See for example Strand (2010) for a detailed discussion of the interest rate.

.In these years, the reduced emission due to abatement is zero (and this is in the denominator for calculating carbon leakage in any period).

We also know (either from the set of Equations T1.3 to T1.13, or from the set T1.14 to T1.20) that fossil fuel use is negatively related to its price in any period when there is no voluntary restriction, that is,

(This is a statement that the own price effect is always negative.)

In the first case, the North reduces fossil fuel use in period 1. Since in the first period, capital stocks are given by history, as capital in the North is shifted to the clean good, its rate of return will fall. As capital shifts to the Y-sector in the South, its production of clean goods would fall, but the rate of return to capital will rise. The price of fossil fuel falls in both periods, causing production of the dirty good to rise in the South in both periods, as well as in the North in the second period. Since the size of the clean sector in either country remains unchanged in period 2, there will be an investment boom in period 1 worldwide.

Period 2

If the price of the fossil fuel falls, now consider the additional effects (to those in Section III) in period 2. Capital accumulation in period 1 in the North would fall in the dirty sector—so that the marginal product of capital in that sector stays unchanged (fossil fuel is Edgeworth-complimentary with capital—if less of it is used, the marginal product of capital falls). The marginal product of capital schedule in the South will shift out in the Y-sector as the price of fossil fuel falls, while remaining unchanged in the clean sector. In the first period, its capital accumulation will be speeded up. In period 2, the world will produce the same amount of clean goods and a lower amount of the dirty good (because of diminishing marginal productivity the price of the dirty good also rises).

Since the price of oil has to rise at the rate of interest (the Hotelling rule), there will be first period effects also. The price of fossil fuel would be lower in the first period and both North and South will witness an expansion in the dirty sector. Pollution in period 1 definitely rises in this case, while period 2 pollution falls (since the sum total of world fossil fuel is given).

To sum up, dirty goods production is relocated spatially and intertemporally. Period 2 witnesses a slowdown in activity. The clean good output continues to be the same, but the total production of dirty goods falls. In period 1 dirty goods production increases, because fossil fuel is cheaper now and clean goods output falls globally, as capital is relocated to the dirty sector.

If cleaning up one’s act implies reducing fossil fuel use, we are not getting anywhere. The South uses all the fossil fuel that the North does not. This is also inefficient (in a production sense) because of diminishing returns to capital. And dirty goods production is brought forward in time. 30

In Indian English, it is called ‘preponing’, in symmetry with ‘postponing’.

The pattern of trade is quite clear. In the periods that the North reduces its use of the fossil fuel, it would import this good from the South and pay for this by restricting its demand for the clean good below its production levels (note that in period 2, the production of the clean good is unchanged globally after the restriction on the use of fossil fuel).

Now, in passing, consider the case where the North makes binding commitments in both periods. In this case, there may not be any relocation of production across periods, although there is spatial relocation in both periods. Think of a knife-edge case. Due to the reduced demand in the two periods from the North, fossil fuel prices fall and in each period the increased demand for it in the South just matches the reduced demand in the North. Worldwide production efficiency goes down, without any change in either total emission or its distribution over time. Of course, dirty production is relocated to the South.

But this is just a knife-edge case. If the use of the fossil fuel changes across periods then, depending on the details, it is possible that carbon leakage in one period exceeds 100 per cent, matched by an equivalent shortfall in the other period, since the sum total of emissions across the two periods is unchanged.

The upshot of all this is that it is imperative that the South’s demand for fossil fuels be curtailed. A quantitative target for dirty goods production could be imposed. An equivalent tax could be imposed—this would be rising over time, as the South accumulates capital. Or the world could do the ‘mother of all sequestrations’ by making a transfer to the fossil fuel producers to keep their valuable resource underground (geological sequestration).

In a trading world, country-wise production-based emissions make no sense. Emissions have to be consumption-based. Some of China’s recent increase in emissions should be attributed to the US consumption.

I have outlined a model that highlights the reaction of the market economy to a reduction in carbon emissions. The analysis in the literature so far has concentrated on carbon leakages—a movement along a given supply curve for fossil fuels. The problem is compounded by the green paradox, that is, a shift down of the supply curve. Fossil fuel producers have an incentive to reduce their prices, as long as it is above marginal cost, and to bring forward the time profile of extraction. This would benefit those countries which do not have binding emission commitments (e.g., India and China, as has happened in Durban recently). Trade would take some of this dirty production back to the now ‘clean economies’. It is therefore imperative that developing economies with large industrial bases be brought within the ambit of climate change agreements with strict binding constraints. In the presence of the green paradox, it is even more ironical that those economies that did not create the problem (of the stock pollutant) have necessarily to be part of the solution. But the emerging economies may well ask ‘What is it in this for us?’ Thus, serious side payments, technology transfers, etc. have to be considered.

The model needs extensions. The quasi-linear utility fixes the interest rate—this is useful as an expository device but surely lacking in realism. No international borrowing or lending is considered here. The extraction of oil is possible at constant marginal cost. The backstop is available in infinite supply at a given price. All these need modifications. In an open economy context, whether pollution is caused by production or consumption is important—though in a global bad context it is less important (since the world is a closed economy).

Finally, the issue of many fossil fuels, some whose supply is elastic (e.g., coal), and others (e.g., oil) whose known sources involve pricing above marginal cost, needs careful analysis. The latter class involves exploration for new sources, and that is elastic in supply. At any point in time, however, with large sunk and fixed costs, the price of the output of existing oil wells exceed marginal cost. Thus, a serious attempt at combating climate change would involve elements of both Sections III and IV.

Acknowledgements

Some of the material was presented in invited lectures at conferences in Exeter and the Singapore Economic Review Conference, and at seminars in Oxford and Toulouse. I am grateful to Jean-Pierre Amigues, Michael Finus, Peter Lloyd, Michel Moreau, Francois Salanie, Tony Venables and Alan Woodland for helpful comments. Special thanks to Rick van der Ploeg and Roger Guesnerie for extensive discussions. Also to Brian Copeland, who persuaded me to reduce my exposition from an infinite horizon model to a three-period one. Finally, thanks are also due to an anonymous referee of this journal for his/her interesting comments on an earlier version of this article. The usual disclaimer, however, applies.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Appendix

Emission Tightening in Period 1 (Marginal Cost Pricing)

Home Country

Emission control in the North means

We then have the conditions A1 to A6 describing the new equilibrium in the world economy:

North

South

Market-clearing

We can solve

We have, in particular (S1 and

Insert these values from A7a and A7d into A6 to solve for

Since

Note this a sufficient condition—we have not used the demand terms (D’(p1) plays no role here). Then we have

Thus with the fossil fuel priced at marginal cost, there is carbon leakage in period one but the sum of emissions worldwide falls.

Now we have:

Thus, we have the following conditions describing the new equilibrium in the world economy (Equations B1 to B9 and B11):

North

South

From B3

Market-clearing

Substitute Equations B10a to B10d in the market-clearing Equation (B11) to solve for

Thus, for the World Economy

The issue of leakages then asks about the magnitude of

It can be shown by substitution that—a sufficient condition is the concavity of G(.) in K and R:

Thus here, a perfectly foreseen reduction in emissions by the North in the next period does not cause leakages greater in magnitude than the proposed initial decline in emissions by the North.

Now the price of the fossil fuel is endogenous and the market-clearing condition (over the two periods) for it becomes relevant. The equilibrium conditions for the North are still the same as in A1 and A2, while for those for the South are those given in A3 to A5 but now depend on

The equilibrium condition A6 for the Y-good can be written as the excess demand for Y equal to zero, that is,

We can borrow all the results from Section A, except now the price of the fossil fuel is endogenous.

We then calculate

C10 This is obtained by inserting

We now need to consider the second period, where there is no abatement in either country.

Home Country

solves for

In particular:

For the South, it is completely symmetric (if the specific factors are the same, as is being assumed here, then the initial equilibrium yields identical values of inputs in the North and South). Now plug these values into the market-clearing equation for the Y-good, that is,

Market-clearing

We then have after appropriate substitutions:

Note the earlier two expressions are a long-winded derivation of the own-price effect being negative (the calculations are available on request for the non-believers).

Then, we substitute the relationships

Note that while the emission tightening does not reduce aggregate emissions, it does postpone it. This is because p2 falls to ensure higher a fossil fuel use in the second period.

Second period restriction on fossil fuel use in the North

The second period equilibrium conditions are given by

Solve D1, D2 and D3 for

Again we can borrow all the results from Section B, except now the price of the fossil fuel is endogenous.

As for period 1, the equilibrium condition for the Y-good in period 2 can be written as the excess demand for Y equal to zero, that is,

or

We then calculate

Then we have

This is obtained by inserting

In period 1, there is no restriction on fossil fuel use. Thus we have: T1.14 to T1.20 with T1.16 holding with equalities.

Solve Equations D.9 to D.14 for

Again as in Section C, we substitute the relationships

Here, we have aggregate emissions remaining the same but the time profile of fossil fuels is brought forward.