Abstract

This study aims to analyse the financial performance of microfinance institutions (MFIs) in Afghanistan for an extremely unstable period, for the financial years of 2014–2015 to 2023–2024, to address significant political instability and the COVID-19 pandemic. Using panel data from the top larger MFIs in Afghanistan, the study looks at the effects of internal institutional characteristics on the return on assets (ROA), which is an indicator of financial sustainability. Panel regression techniques are employed to analyse the relationships between these factors and institutional performance. The findings indicate that branch expansion enhances ROA; therefore, increasing branches led to greater profitability, even amid political instability and uncertain conditions. While the gross loan portfolio had a negatively significant effect on financial performance, this finding indicates that quality and assessing the associated risk of the loan portfolio may be challenging. Total income and the number of active borrowers were less significant or impactful variables. Overall, the findings indicate that MFIs encountered financial problem and even some of them led to stop their services, moreover, highlighting the need for risk-adapted progress and efficient portfolio control to maintain the financial viability of MFIs working especially in fragile or crisis-affected economies.

Keywords

Introduction

Microfinance Institutions in Afghanistan

The visibility and power of Afghanistan’s microfinance institutions (MFIs) have increased over the past 20 years. In Afghanistan, MFIs have been critical to facilitating poverty reduction and enhancing rural life. With multiple institutions that provide financial services to millions of households, the microfinance sector has greatly expanded over the last 20 years. Microfinance has positive impacts on employment and income, although the impact on women’s empowerment and poverty reduction is less straightforward (Hemat & Rahman, 2024). The microfinance sector was able to move forward a significant step with the establishment of the Microfinance Investment Support Facility for Afghanistan (MISFA) in 2003. The MISFA aims to help provide poverty relief, develop financial autonomy and provide humanitarian assistance to people in Afghanistan by managing and supporting the provinces of Afghanistan’s MFIs. The MISFA is a project that takes a mixture of different types of donor money and brings it into organised funds and flexible assistance; the primary beneficiaries of such funds are Afghanistan’s MFIs (Sultani & Rahman, 2023). The Afghanistan Microfinance Association (2023, June 1) is the country’s national network of Development Finance Institutions (DFIs). It was founded in 2005 by the MISFA, microfinance specialists and other participants, and in 2007, AMA was given approval by Afghanistan’s Ministry of Justice (AMA, 2023). The banking and non-banking financial sectors make up Afghanistan’s financial system. Afghanistan’s financial organisations, such as the Da Afghanistan Bank (DAB), face four major obstacles: a lack of an up-to-date legal and regulatory framework for banking operations; inexperienced executives and technical employees; the absence of any banking operating systems; and weak payments made through communication networks. These limitations severely limit the formal financial sector’s capacity to offer the general public, non-governmental organisations, businesses, cross-border and multilateral organisations, and governmental institutions efficient and dependable financial services, particularly both local and global systems of payment (Şahin & Humta, 2023).

As of December 2019, there are nine MFIs in existence in Afghanistan, which hold a total loan portfolio of 9,607,678,446 AFN. These institutions in total have approximately 423,357 clients, 150,509 of which are active borrowers, which includes around 37% women and 2,670 staff members working from their offices in different provinces (Sultani, 2021). These MFIs provide very useful financial services to marginalised groups with an emphasis on women’s economic self-sustainability and financial access. The COVID-19 pandemic has affected the private education sector and MFIs in Afghanistan, leading to financial losses and discontinuity of educational activities. While these continue to be issues, factors that determine the financial success of MFIs, such as institutional characteristics, interest rate charges, the length of operations in the market, profitability and sustainability, are incorporated as a part of the environment (Ibrahim et al., 2018).

The aim of this study is to investigate the financial performance of MFIs in Afghanistan during the unstable time of political instability and the COVID-19 pandemic.

Selected Microfinance Institutions

This study is limited to five MFIs in Afghanistan. They accounted for a large part of the microfinance sector in Afghanistan, which has financial services mostly in rural and semi-urban areas.

The First Microfinance Bank (FMFB).

Foundation for International Community Assistance (FINCA).

Mutahid Development Finance Institution.

OXUS-Afghanistan.

Aga Khan Development Network.

For the purposes of this study, given the need to evaluate the MFI operations that operate in Afghanistan in each of the dimensions of the microfinance practices, the MFIs were selected based on being a part of the microfinance sector while also offering relevant insights into the performance indicators selected. Some variety in relation to the MFIs with respect to characteristics, distribution area and recent performance is needed to study microfinance in this way.

Literature Review

Challenges Impacting Microfinance Institutions

There are several challenges that affect the way in which MFIs operate and their effectiveness. In Tanzania, some of the problems that hinder group lending models include lack of trust, group dynamics and operational complexities, leading to conflicts and imbalanced participation (Magambo, 2024). Similarly, governance challenges are also encountered in Bangladesh as they attempt to reconcile poverty reduction and ensure that MFIs in the country are on a financially sustainable footing through strategic improvements that would increase MFI performance (Uddin, 2024). MFI sustainability in China is influenced by factors such as operating technology, the external environment and financial conditions that are critical for economic performance but less critical for operational sustainability (Li et al., 2023). Furthermore, macro- and micro-challenges, including legal barriers and high transaction costs, restrict access to microfinance for the rural population in India (Das, 2023). Sultani and Rahman (2023), in their study, aimed to clarify the difficulties faced by MFIs in Afghanistan. Although this issue set was described via a descriptive and principal component analysis approach, research on this topic yielded nine distinct components. Many problems plague microfinance organisations; in addition to the difficulty with technology, inadequate government support, a lack of administrative and skilled staff and the rise of harmful rivalry across various MFIs are the main challenges.

Influence of Exterior Shocks on Microfinance Institutions

External variables such as regulatory concerns had a major effect on loan defaults inside MFIs, outweighing other factors such as financial infection and recessions, which were shown to be statistically minimal in a Cameroonian situation (Fotabong, 2016). MFIs in Uganda demonstrate resistance in the face of major shocks such as conflicts and natural catastrophes, suggesting their importance in economic wellness; however, their financial structure remains crucial for stability (Sekabira, 2013). Furthermore, in Pakistan, tactical failures by borrowers were worsened by insufficient enforcement measures, especially amid correlate shocks such as the 2005 earthquake, underscoring MFIs’ sensitivity to outside influences (Kurosaki & Khan, 2012). In Bolivia, MFIs’ capacity to handle liquidity risk under instability in politics was linked to institutional and subjective benefits, implying that outside factors do not affect all MFIs similarly (Soto, 2007). Research by Assefa et al. (2013) sought to understand how market competition affects the efficiency of microfinance organisations’ operations. This study tested the hypothesis that MFIs’ outreach and loan repayment rates were impacted by the amount of competition among them using a Lerner index. Using data from 362 MFIs in 73 nations, the study ran from 1995 to 2008. Microfinance competition has been on the rise for the past decade, says one report. Results from econometric analysis showed that competition among MFIs has a detrimental effect on outreach and repayment rates.

Performance Indicators for Microfinance

MFIs performance measures include both financial and social components, indicating their twin aims of revenue and social operation. Portfolio value, funding sources, operating expenditures and institution size are important financial variables for analysing fiscal viability and outreach success (Green et al., 2023). The impact of microfinance on income and employment in Afghanistan’s Bamyan province was studied by Sultani (2021). The First Microfinance Bank of Afghanistan (FMFB-A) is an institution that collaborates with the AMA and the MISFA. The study focuses on this particular set of 220 borrowers. Microfinance significantly contributes to income development and job creation, according to a study that meticulously analyses data obtained before and after FMFB-A loans were granted (Şahin & Humta, 2023). They looked into microfinance in the banking sector as part of their study, bringing attention to the importance of this form of financing in filling a big funding gap for businesses in developing nations. The International Finance Corporation (IFC) had previously brought this requirement to visibility. In their analysis of the current microfinance literature, Gupta (2018) claims that they shed light on certain important issues. They highlighted the methods employed by Indian banks and MFIs to deal with the scarcity of capital by means of mechanisms like joint liability groups (JLGs) and self-help groups (SHGs). Among all microfinance programmes, Gupta regarded SHG-BLP as the most crucial one globally. The analysis conducted by Gupta thoroughly examined the growth and effects of MFIs, with a special emphasis on lending portfolios and existing loans, by making extensive use of secondary data from academic journals, NABARD reports and MFIN reports. The main purpose of the research by Ashraf et al. (2014) was to identify the variables that caused MFIs across countries with diverse religious and cultural standards to have significantly varied performance metrics. The research included 754 MFIs from 83 different countries in its cross-sectional data set. It dives into the performance of MFIs by looking at indicators including outreach, loan recovery, profitability and cumulative financial success. Research has shown that MFIs can be financially sustainable over the long run, casting doubt on their reputation as change agents (Chary et al., 2014). In terms of portfolio yields, their study found that SML, BSFL, CMC, GVMFL and GFSPL were among the MFIs that fared better than average. This shows that these institutions were successful financially and socially. The most disadvantaged communities cannot get loans from conventional banks due to their profit-driven policies and stringent lending rules. Poverty, hunger, illiteracy and health issues can all be effectively addressed with microfinance (Manoharan et al., 2011). How is microfinance being utilised in India to assist the economically and socially marginalised? Nasir (2013) sought to answer this question. Focusing on the SHGs-Banks Linkage Programme, issues with loan distribution methods, insufficient product diversification, client overlap and high interest rates were detected. These issues demonstrated the lack of cohesion in the microfinance industry.

Research Gap

The literature that we reviewed reveals that MFIs are indeed useful tools for decreasing poverty and increasing financial inclusion, but they have faced continuing issues such as governance problems, technological issues, lack of government support and negative competition. The optional studies focused on Afghanistan highlight only descriptive issues, such as staff shortages, inadequate operational structures and competition among institutions, and do not analyse empirically and demonstrate how financial outcomes are affected by institutional characteristics. The gap is even more pronounced in Afghanistan, an already fragile context, where COVID-19 and political instability have aggravated existing vulnerabilities within the system. Therefore, we propose the following hypothesis to address this gap.

H1: Internal institutional characteristics do not significantly affect the financial performance of MFIs in Afghanistan.

Data and Methodology

This study provides an empirical analysis of the financial performance of MFIs in Afghanistan amid ongoing sociopolitical and economic instability. The analysis is based on panel data on five of the leading MFIs in Afghanistan, which have maintained continuity of reporting and operational sustainability. The five MFIs were pre-selected for analysis to provide a representative sample, which includes diversity in institutional attributes without compromising the analytical capacity of a reduced sample size. A select number of MFIs provide a limited, yet manageable, list of ‘cases’, as we reduce transactional complexity and measurement bias while still providing variability in institutional characteristics in several dimensions, such as a combination of institutional size, outreach and financial depth.

The data collected from published and audited annual reports and financial declarations available in the sector, besides other publicly available reports from MISFA and AMA. The study period is FY 2014–2015 through 2023–2024—effectively capturing indicators of financial performance during relative stability and periods of heightened unease and uncertainty (specifically as a cumulative effect of COVID-19 and political instability), thus providing a significant temporal lens of financial institutional performance.

Econometric Model

To empirically test the effects of institutional attributes on the financial performance of MFIs in Afghanistan, the present study has adopted a panel data regression framework. The choice of the panel data model follows the structure of the data, which consists of a series of multiple individual observations for each of the institutions over time. The value of the panel data estimators to help control for variation across sections and time series means that our estimates and conclusions are likely to be consistently informative relative to the consequences of a pure cross-section or time series analysis. For this study, we attempt to evaluate the relationship between operational and structural variables—borrower outreach, institution size, loan portfolio size, income and expenses—on financial performance (in this study, financial performance is measured by ROA. The model set up was done to be able to analyse these relationships while facilitating heterogeneity across institutions and time.

The general function of the econometric model is specified below:

where ROA it is the return on assets MFI i in year t.

Active borrowers, no of branches, gross loan portfolio, total income and total expenses, are independent variables for each MFI that changed through time. µi symbolise unobserved individual-specific effects. ɛit is the idiosyncratic error term.

To validate the robustness and selection of model(s), three different regression models were employed:

Pooled OLS regression—serves as a baseline estimate, given that heterogeneity across institutions is not considered.

Fixed effects (FE) model—controls for unobserved characteristics specific to an MFI that do not change over time.

Random effects (RE) model—assumes that unobserved effects are random and not correlated with the explanatory variables.

A Hausman test was conducted to determine which specification was appropriate between FE and RE. The Hausman test statistic (p value = .3392) showed the RE format was the more appropriate specification for this data set. Therefore, the final analysis is based on the RE model with robust standard errors to correct for possible heteroscedasticity and serial correlation to further enhance the credibility of statistical inferences. This model formulation represents an effort to provide empirical evidence of how operational and financial circumstances affect profitability in the Afghan MFIs given the prevailing circumstances of economic instability and institutional constraints, and the COVID-19 period.

Results and Interpretation

Descriptive Statistics

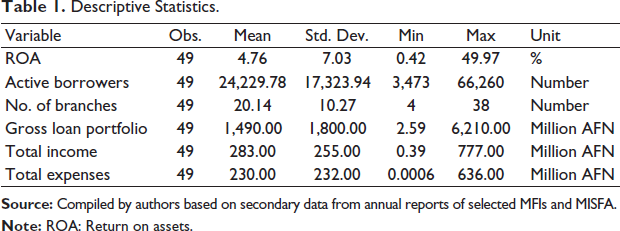

Table 1 provides summary statistics for the variables within the empirical analysis and is based on a balanced panel that consists of 49 firm-year observations of selected MFIs. Among the five selected MFIs, FINCA MFI has stopped their service since 2021. The summary statistics provide the number of observations, mean, standard deviation, and minimum and maximum values for each of the variables.

Descriptive Statistics.

According to Table 1, Afghan MFIs have an average ROA of 4.76% and a standard deviation of 7.03. This implies significant variation in profitability, varying from 0.42% to 49.97%, this indicates that while some MFIs have modest returns, others have exceptionally high numbers in some years, likely due to isolated events or good fortune. The mean number of active borrowers is approximately 24,230, with quite a bit of variation by institution (3,473–66,260) and differences in outreach capacity. The average network size is 20 branches (4–38), which demonstrates differences in institutional strategies, ranging from a relatively limited presence to coverage expansion attempts for greater service of larger populations, often distant and remote.

Regression Results and Model Selection

The panel data regression technique was used as the means for empirical testing of institutional characteristics and financial performance of MFIs in Afghanistan. Three models were employed: the pooled ordinary least squares (OLS) as a pre-estimation baseline model, and FE and RE models to account for unobserved heterogeneity across institutions. The Hausman specification test determined the appropriate estimation technique. This decision made a statistical justification for the adoption of the RE model as an appropriate model. Each model’s outputs are presented in the subsections below, which include a discussion on their tweaks.

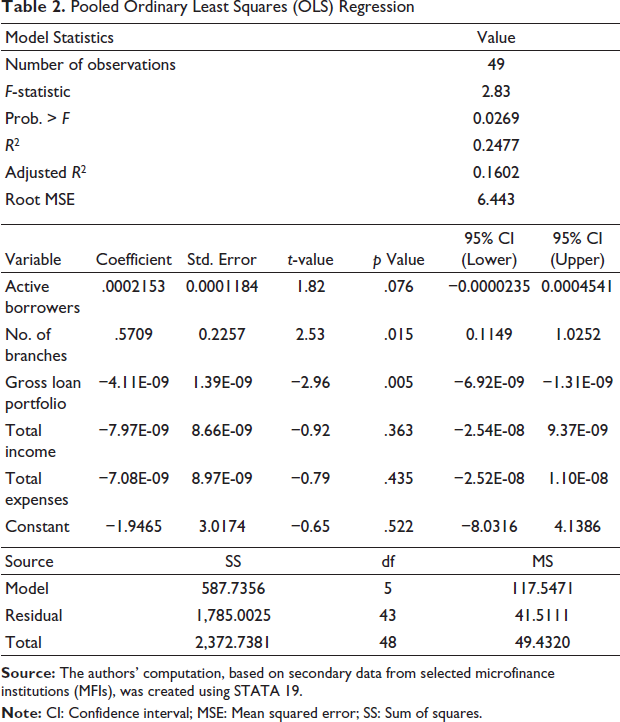

A pooled OLS model was estimated as a starting point for the panel regression analysis, to analyse the direct relationship between selected institutional characteristics and the financial performance (measured by ROA) of Afghan MFIs. The pooled OLS treats each of the cross-sectional units in the sample as homogeneous, which does not account for unobserved effects which might be specific to each entity. While a pooled OLS provides a useful interpretation within the overall context of the variables, it is insufficient because it allows for ambiguity in terms of determining potential endogeneity due to omitted institutional heterogeneity.

The pooled OLS findings in Table 2 indicate that the overall model is statistically significant at 5% (F-statistic = 2.83; p = .0269), which indicates that the predictors combinedly explained the variations in ROA, the R2 (0.2477) suggests that 24.77% of the variation in overall financial performance was explained by independent variables, and the adjusted R2 (0.1602) suggests that improvement declined among independent variables combined. The gross loan portfolio had a significantly negative effect on ROA, suggesting that increasing the volume of loans without enough efficiency would decrease profitability. The number of branches had a positive and significant effect on ROA, which was expected if the distribution channel exploited additional market coverage. The active borrowers had a positive relationship with ROA, but weakly supported. All other financial variables were insignificant to ROA and could be attributed to multicollinearity or model specification issues. Findings support looking at fixed and RE models.

Pooled Ordinary Least Squares (OLS) Regression

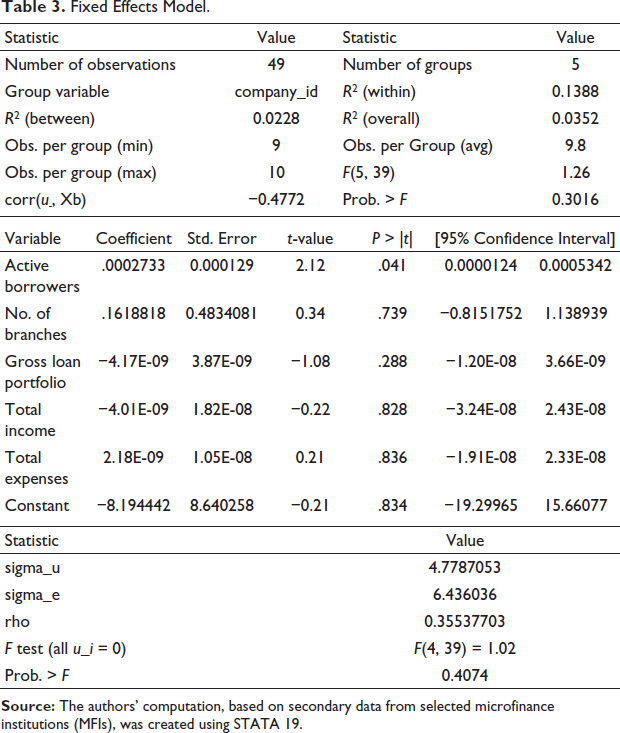

To control for unobserved heterogeneity that may bias the pooled regression estimates, an FE model was estimated. In this specification, each MFI has its own intercept, allowing us to control for time-invariant, firm-specific characteristics. The FE method accounts for omitted variables at the firm level that are constant over time, which prevents bias arising from omitted variables. The FE method reduces efficiency by ignoring the between-groups variation, but when we believe that we suspect heterogeneity, this should improve internal validity. Table 3 presents the estimation results under an FE framework.

Fixed Effects Model.

The overall FE R2 equals 0.0835, suggesting limited explanatory power overall. However, roughly 13.88% of the variation in ROA is accounted for by variation across institutions. The F-statistic is 1.26; the p value, .3016, suggests that the model, as a whole, does not statistically explain institutional differences in profitability. However, observations about individual-level variables may provide some insight. Only active borrowers are statistically significant, as a regressor at the 5% level (coefficient = torch = 0.0002733, p = .041), indicating that scale is an important contributor to profitability. Increases in borrowers contribute to positive profitability, particularly when controlling for FE at the firm level. Based on this model, there were no statistically significant changes in ROA for the other terms—branches, gross loan portfolio, total income, total expenses—implying the within-institution variation for these terms does not have a systematic change in performance. The rho statistic suggests that 35.5% of the variation in ROA is attributable to unobserved, firm-specific characteristics (rho = 0.3554), suggesting even further that you need to account for these types of stochastic heterogeneity. It should be noted that the joint significance of the F-test indicates the regressors collectively are not statistically significant at p = .4074 overall, minimising the significance of the explanatory power of the FE model. Given this, the eliminated need to test the RE model and to conduct the Hausman specification test to determine the most efficient and consistent estimates.

The regression results using the RE specification are shown in Table 4.

Random Effects (RE) Model.

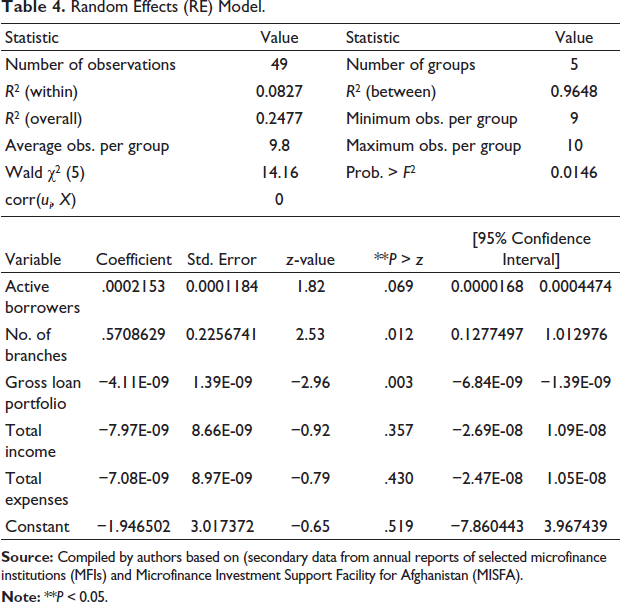

The RE estimates provide a Wald chi-square estimator of 14.16 (p = .0146), indicative of overall significance at the 5% level. The proportionate R2 of 0.2477, consistent with pooled OLS, shows that 24.77% of the variation in ROA is explained by these predictors. The decomposition of variation shows a very high between-entity R2 (0.9648) and a relatively low within-entity R2 (0.0827), thus suggesting that differences across institutions (as opposed to changes within an institution over time) drive the variation in ROA. At the variable level, the gross loan portfolio has a significant negative influence on ROA (coefficient = –4.11e–09, p = .003) and reinforces the conclusion that if a loan portfolio expands rapidly without financial efficiency in operations, profitability declines. In contrast, the number of branches has a significant positive association with ROA (coefficient = .5706, p = .012) and supports the argument that broader outreach correlates with improved ROA. Active borrowers remain marginally significant (p = .069) and suggest scale benefits, but not at conventional significance level criteria. Alternatively, total income and total expenses are deemed to be insignificant; perhaps due to structural overlap, or ‘noise’ in reporting. Overall, the RE model yields more efficient and consistent estimates than the FE specification during the first phase of the analyses, and the Hausman test will aid in confirming the appropriate specification.

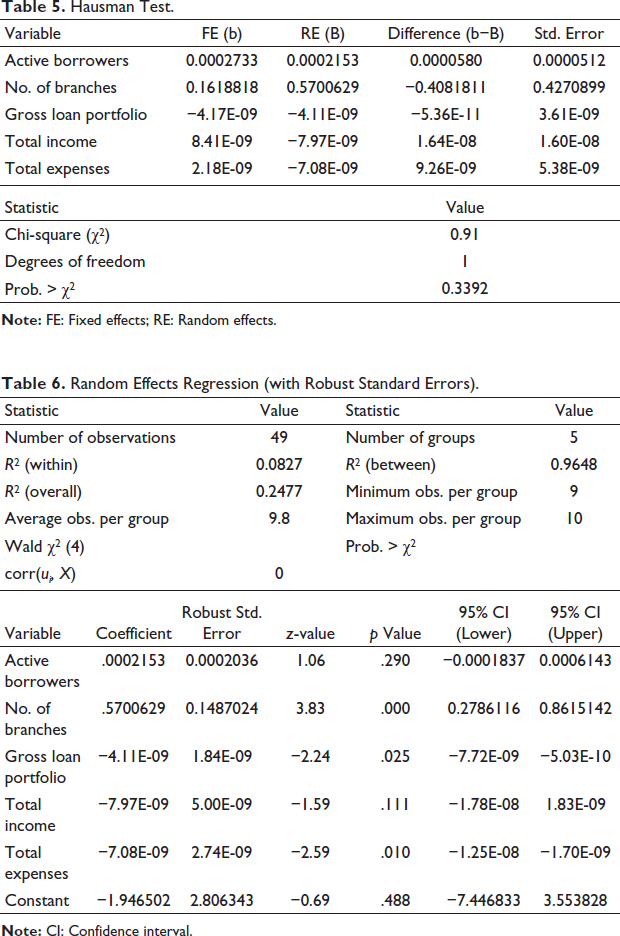

A Hausman test was applied to determine whether FE or RE were suitable for this study. This test analysed if the unique errors (unobserved heterogeneity) are connected with regression factors. The null hypothesis is that we prefer the RE model, while rejection of the null indicates that the preferred model is the FE model, since the coefficient estimates are systematically different. The results of the tests are available in Table 5.

Hausman Test.

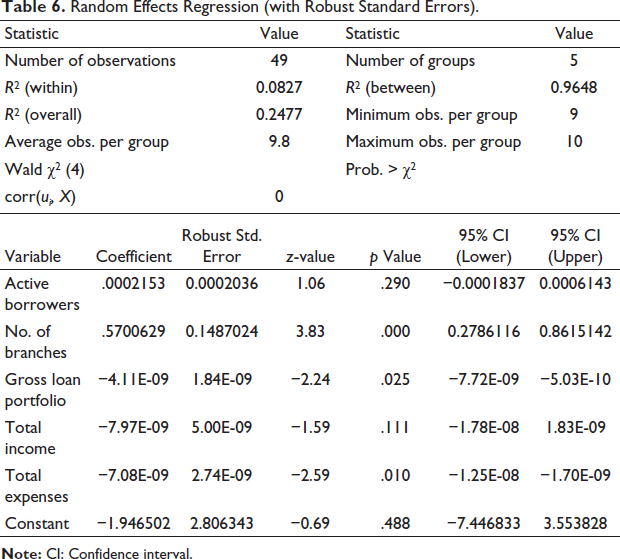

The Hausman specification test shows a chi-square statistic of 0.91 and a p value of .3392 which exceeds traditional significance levels (.01, .05 or .10). Thus, the null hypothesis cannot be rejected, and we can conclude that the RE estimator is consistent and efficient for this purpose. Given the lack of systematic differences in coefficient estimates between the FE and RE models, the assumption that unobserved individual effects are orthogonal to the explanatory variables is upheld. The note, ‘(V_b–V_B is not positive definite)’ also sometimes occurs in small sample sizes and is not a concern when the chi-square is low, and the p value is considerably above significance levels. For this reason, we use the RE model as our preferred specification. Robust standard errors clustered at the firm level were used to control for heteroskedasticity and intra-group correlation. They are reported in Table 6.

Random Effects Regression (with Robust Standard Errors).

The robust RE model preserves the forms of the original RE specification but employs corrected standard errors, thereby increasing the validity of statistical inferences. The total R2 value of 0.2477 indicates that institutional characteristics account for roughly 24.77% of the variation in ROA. An exceptionally high between-group R2 value (0.9648) suggests that institutional differences explain the majority of the variation in profitability, while the within-group R2 value is low (0.0827). At the variable level, the number of branches has a strong and statistically significant positive relationship with ROA (coefficient = .5706, p = .000), emphasising the importance of outreach infrastructure to support higher institutional performance. Meanwhile, the gross loan portfolio has a significant negative effect (coefficient = –4.11e–09, p = .025), again demonstrating concerns that increasing loans at the same pace, without any changes in the operating efficiency, poses a risk to profitability. The number of active borrowers maintains a positive sign despite no longer being statistically significant (p = .290), indicating borrower scale effects will depend on other drivers of performance. Total income and total expense, while fundamental to the operation of institutions, are not statistically significant, suggesting little explanatory power in these specifications of these variables.

Across all of the estimated models (pooled OLS, FE, RE), a few consistent patterns emerge. The strongest predictor is the institution’s outreach, measured by the number of branches, which has a consistent, positive impact on financial sustainability through increased market coverage and improved service provision. In contrast, the consistently negative relationship of gross loan portfolio with ROA likely reflects diminished return, increased risk exposure and greater inefficiencies with portfolios of increasing size. Active borrowers, while normally positive, appear to require institutional complements of repayment capacity assessments and regular monitoring to convert sheer scale to financial return. The non-relationship of income and expense variables may reflect collinearity or omitted variables such as governance, dependency on donors, or loan write-offs. Overall, these results demonstrate the structural and operational aspects of MFIs with regard to the outreach-expansion of microfinance in a vulnerable context like Afghanistan and the importance of responsible lending in sustaining baseline financial performance.

Interpretation of Results

This study’s results are both consistent with and in dispute with earlier studies on the financial success of microfinance groups, especially in emerging conflict-affected areas. The positive and substantial relationship between the number of branches and the desired level of ROA agrees with Mersland and Øystein Strøm (2009) assertion about the importance of reviewing the institutional outreach mechanisms, particularly physical infrastructure, since the authors suggest the following will be able to strengthen performance by way of both market penetration and supervision of clients. Hartarska (2005) came to similar conclusions by pointing out that the structures of governance and delivery contribute considerably to the profitability of MFIs in developing countries. Here in Afghanistan, where digital financial offerings are in their infancy, the remaining branch-level, loan-level interactions could still be prioritised as a form of client engagement and monitoring of loans. On the other hand, the negative link between gross loan portfolio and ROA is different from much of the mainstream literature that notes that larger loan portfolios suggest more efficient institutions through economies of scale (Cull et al., 2006). The ambiguous statistical relationship between active borrowers and ROA stands in contrast to the typical findings in South Asian microfinance studies that have found volume of borrowers to have a significant effect on profitability due to the costs of group lending and efficiencies of large loan portfolios (Armendáriz & Morduch, 2005). However, in Afghanistan, the economic instability of borrower income sources, as well as the lack of institutional tracking and demand from customers to comply with enforcement, may attenuate the benefits of a rapidly expanding client base. Moreover, the small impact of overall income and expense calls into question the traditional microfinance performance framework, which argues that financial self-sufficiency can be used as a proxy for sustainability (Nabizada & Dhanda, 2024). The lack of congruence may be due to donor inflows, unreliable reporting standards, and the hybrid nature of many Afghan MFIs with commercial and development objectives. More broadly, the comparisons presented here demonstrate that context matters in influencing microfinance outcomes. Some of the empirical patterns replicate templates observed globally, while others are reflective of the specific limitations and complexities of the financial landscape, particular to working in a conflict-affected and weakly institutionalised setting. Overall, these contrasts point to the need to amend performance models to local context(s) rather than to standardised benchmarks.

Implications for MFIs, Policy and Theory

The findings have several significant implications. First, for MFI managers and practitioners, the evidence suggests that a strategic expansion of branch infrastructure needs to be prioritised over rapid loan growth. Moreover, decentralised service delivery seems to be more effective than pure scale effects for improving financial returns—especially in a country where physical access to the product, community trust and local knowledge-based performance are still critical drivers. Second, the negative relationship observed between gross loan portfolios and ROA reinforces the need to strengthen credit risk management practices in situations where fast-paced expansion has the potential to disrupt the repayment discipline of borrowers. MFIs should, for example, invest in financial and social sustainability screening tools for borrowers, diversify the geographical aspects of loan portfolios, and develop early-warning systems for financial performance to monitor loan performance. Third, the findings imply that instead of pushing MFIs to accelerate their growth and become mature organisations, policymakers and agencies such as MISFA and DAB should support MFIs through capacity-building programmes as needed in credit analytics, digitalisation and compliance. Regulatory concessioning during periods of crisis should be supplemented by a performance monitoring framework that measures and captures both financial sustainability and client welfare.

Limitations of the Study

Despite this research’s contributions, several limitations remain. The sample size (n = 5 MFIs) is small due to a lack of available data, which limits our generalisability beyond this data set, combined with the fact that all indicators of financial performance (e.g., ROA) are limited and do not include social performance or outreach equality, which are key to the mission of microfinance. Additionally, the data are at the institution level (n = 5) and do not include borrower-level behavioural data or loan default profiles. Subsequent research could include qualitative data, more clearly differentiate performance before and after 2021, expand to a larger community-based or informal MFI category, or develop multilevel panel models to better capture time lags and crisis response models. A final point of potential interest includes comparisons across countries and with other microfinance markets that are conflict-affected as a way to provide useful benchmarks for policy adaptation.

Conclusion

This research presents an empirically rigorous analysis of Afghan MFI financial performance for the FY 2014–2015 to 2023–2024, a framework that has endured systemic institutional fragility and unusual crises, specifically the COVID-19 pandemic and the transition to political cessation. This analysis used a panel data set comprising five prominent MFIs in Afghanistan and employed panel regression analysis, utilising RE with robust standard errors, to learn whether institutional characteristics influence financial sustainability, captured as ROA. The study determined that institutional outreach, as indicated by the number of branches, statistically significantly and positively impacted financial performance (β = 0.5706, p < .01). As a result, physical presence in Afghanistan is a documented determinant and remains a significant predictor of operating efficacy in a trust-dependent and geographically fragmented context. The gross loan portfolio impacted ROA in a statistically significant negative manner (β = –4.11e to 09, p < .05) and potentially highlighted that increased lending could devour profitability, potentially related to increased exposure to credit risk and inefficiencies related to lending. Interestingly, active borrowers were positively correlated with ROA but were statistically insignificant at conventional statistical levels in the robust model, calling for greater participant selection and monitoring strategies for clients. These conclusions have serious implications following recent sociopolitical events. MFIs in Afghanistan managed to adapt despite elevated operational risk, donor flight, uncertainty regarding regulations, interrupted repayment flows during lockdown, and regime instability. The strong panel regression results demonstrate that institutional stability, the systematic management of growth, the diversification of branches and financing sources, and sound operations are important attributes of resilience shown to contribute to the likelihood of financial viability under conditions of fragility. Theoretically, this study emphasises the growing literature on microfinance in unstable contexts by demonstrating that standard proxies of scale and outreach do not equally result in financial return. In relation to the implications for practice and policy, the study reinforces the need for balance in the range of considerations faced by MFIs: easy access to finance while continually monitoring performance and contingency planning. The study has limitations due to its small sample, and although we relied mostly on secondary data, we strive to provide the foundation for future studies that could include social performance data or comparative studies of financial service providers in other fragile economies. The findings were impactful and contextually relevant in providing a better picture of how MFIs can rethink their sustainability strategies or change the narrative for the MFIs that work under uncertainty.

Footnotes

Acknowledgement

The information available in the article is research-based and original.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest regarding the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.