Abstract

To allow for large-scale common EU borrowing of over €1 trillion for NextGenerationEU, SURE, SAFE and assistance to Ukraine, the EU significantly adapted its legal framework since 2020, consolidating national borrowing capacity with centralized EU debt issuance. This article examines the main features of this new era of common EU borrowing, detailing both the legal and financial architecture underpinning this policy. Financially, EU borrowing aims to achieve better market access and enables tax smoothing, making assistance viable only as long as it improves the fiscal position of the Member States. Legally, the EU has created an elaborate system of guarantees and secondary laws to assure creditors that it is legally obliged, able and financially capable of honouring its debt. The article also discusses the financial implications of borrow-to-spend instruments on the budget, and the legal adjustments in the current and future Multiannual Financial Framework designed to meet financing needs for these borrowing costs.

Introduction

In the context of the Covid-19 pandemic in 2020 and the Russian war on Ukraine, the EU has adopted several financial support instruments to assist its Member States as well as Ukraine. EU financial assistance to Member States had been a recurring but sporadic policy since the 1970s. 1 The developments since 2020 have not only dwarfed the financial volume of previous support instruments channelled via the EU, but they also included for the first time borrowing for the purpose of transferring outright non-repayable assistance. Since 2022, the EU also began to provide large-scale concessional loans to Ukraine, a third country, creating new record-high liabilities for the EU via borrowed funds. 2 By 2027 the EU will have accumulated over €1 trillion in debt, linked to loans and grants under NextGenerationEU (NGEU), SURE and several assistance instruments to Ukraine and other third countries, as well as loans under the SAFE instrument for defence. Part of these borrowed funds will be repaid via the EU budget and therefore make the EU for the first time the end-user and direct, rather than intermediate, debtor to the market. These developments underscore two core aspects of EU financial solidarity, first the common borrowing directly via the EU, and second, the use of EU funds to support Member States and third countries.

Recent legal scholarship focused particularly on the legality of large-scale EU borrowing. Regarding common borrowing-for-spending, Dermine and Bobić have assessed the ruling of the German Federal Constitutional Court (GFCC) on the legal aspects of NGEU. They argue that the GFCC emphasized that borrowing for NGEU was only constitutional because it was temporary, of exceptional nature, as well as limited in government liabilities. 3 Grund and Steinbach found that while a replication of an extra-budgetary fund, such as NGEU, to finance EU public goods is legally feasible, a permanent revolving debt-financed budget is not. 4 Regarding the use of EU funds for the support of Member States, scholars highlighted the reinterpretation of Article 125 TFEU by the EU since NGEU in order to allow a deviation from the market logic in favour of fiscal transfers, 5 as well as illustrating under which conditions common borrowing would violate Article 125 TFEU and when it would not. 6

While recent scholarship has analyzed the ‘legal engineering’ of the Covid-19 recovery fund, 7 the literature remains almost firmly on the interpretation of the possibilities provided by the treaties, without discussing in substance the financial sub-construction required to enable the EU to act as large borrowing entity on the market. This article complements this recent debate about common borrowing for EU expenditure by analyzing how the EU has (legally and financially) built and leveraged its fiscal space to engage in tax smoothing for its Member States. 8 By doing so, this article addresses several aspects of the EU's fiscal structure. It highlights first the purpose of common borrowing, which derives entirely from interest rate differences and access to sustainable finances. Second, it underscores the role of guarantees from Nordic EU Member States for credible EU borrowing on the market, without which the needed financial benefits would not be achieved. Last, it addresses the implications for the budget linked to large-scale borrowing via the EU, stressing the costs in the current and future budget and the way these costs were absorbed by budgetary innovation. It therefore contributes to the literature by engaging with the economic factors lying behind the legal construct of the recent EU's common borrowing activities, which so far has received little scholarly mentioning.

The structure of this article is as follows. The next section explains the intrinsic rationale of using EU borrowed funds for financial assistance, as well as the costs and benefits associated with this practice. The third section outlines the legal basis and the EU's relationship with the market, including the role of national guarantees and the diversified funding strategy applied since 2021. The fourth section discusses the impact of current borrowing under NGEU and Ukraine assistance on the budget and future MFFs. The last section concludes.

The Rationale for Common Borrowing

The first aspect to discuss is why common borrowing is a useful tool for EU Member States. For EU governments, it is usual practice to increase expenditure in times of crises to mitigate the immediate impact of economic downturn on the citizens and on the economy as whole. Thus states borrow larger funds to cushion the negative effect from crisis and repay them over a longer period. The Stability and Growth Pact considers this tendency by allowing the national or general escape clauses to trigger in exceptional circumstances or severe general economic downturn. 9 In these moments countries do not need to follow the fiscal constraints of the pact. This counter-cyclical spending with borrowed money is referred to as tax smoothing, and is particularly relevant in times of war or – in case of the recent events in the EU – in moments of severe health and financial crises, when spending largely overruns revenue. 10 Thus a state requires the necessary funding to spend its way out of the crisis, at a time when revenue through taxes and social contributions tend to drop. To be able to do so, EU governments turn to market financing to borrow the additionally needed funds. All EU Member States borrow capital from the market on a more or less regular basis and therefore they all have debt. Without the access to market borrowing in a situation where states need larger funds, governments would either face a sudden stop, 11 which usually would lead to a government default, or face a massive loss of state expenditure, usually causing heavy social costs. Governments tend to try to avoid both.

If market access is not available, either because of a lack of financial depth, or simply because of the (high) risk premium demanded by the market, often in relation to the impact of the crisis, financial assistance can help to replace or facilitate this access to funding. Due to this vicious circle of crisis-impact on public financing and the increased need for financing in these times, financial assistance is explicitly foreseen under several articles of the Treaties, which allow for financial support in different contexts. Article 122(2) TFEU refers to ‘exceptional circumstances outside of the control of the Member State’, Article 136(3) to the purpose ‘[of] safeguard[ing] the stability of the euro area as a whole’, and Article 143 TFEU to cases where a Member State finds itself ‘in difficulties or is seriously threatened with difficulties as regards its balance of payments’. 12 Irrespective of the legal possibility of supporting Member States, assistance via the EU has to follow a specific financial logic to achieving its objective. In the following two subsections this logic is elaborated as first, borrowing for loans, and second, borrowing for grants.

EU Borrowing for Providing Loans

The rationale for common borrowing for loans is entirely linked to the costs of interest rates (or better, the savings on borrowing costs from lower interest rates), which a recipient benefits from when borrowing via the EU instead of itself. The EU borrows and transfers its better conditions to the recipient Member States, which in turn can borrow cheaper, or regains access to funding through a higher debt sustainability linked to the lower funding costs. This fiscal easing impact on governments’ finances is inherent and was illustrated by the savings on SURE loans through EU borrowing. The Commission estimated these savings to be between 28% of the loan costs for Romania to about 10% for Greece, with Hungary, Bulgaria, Italy and Croatia being situated somewhere in-between. 13 In parallel with SURE the European Stability Mechanism (ESM) offered loans to euro area governments, even though these Member States could still finance themselves on the market. This access to the ESM was provided even though the recitals of the ESM treaty state that assistance is only provided if ‘regular access to market financing is impaired or at risk of being impaired’. 14 The emphasis of the ESM's credit offer relied entirely on its ‘very low interest rates’. 15 This underscores that the risk of impaired market access is the key metric for assistance to be released, and emphasizes that default does not have to occur or be imminent, but only that the ‘regular’, i.e., the ex-ante market conditions before the assistance, have to worsen.

For assistance under Article 122 TFEU, no mention of market access is made, and solely serious difficulties and threats are mentioned. Thus, while euro area assistance has an explicit purpose to substitute market access, EU assistance is more flexible and only requires the presence of exceptional occurrences beyond the control of Member States. However, that market access is also the key metric for governments requesting support under Article 122 TFEU is highlighted by the practice of assistance. For SURE, 19 EU Member States with higher interest rates than the EU requested loans, and for SAFE, 18 Member States with higher interest rates have requested loans, including France. 16 All these Member States still (more or less) had access to market financing. Thus the key to determine whether EU borrowing for loans is financially desirable, irrespective of the purpose or reason for assistance, lies entirely in the costs linked to the interest rates of EU debt compared to that of the respective recipient Member State.

EU Borrowing for Grants

The rationale for grants is similar but linked to the advantages of tax smoothing via the EU. In the context of Covid-19, EU governments had different capacities to borrow funds for tax smoothing ex ante. For most governments borrowing costs were rising, having the potential to cause another debt crisis if more debt was to be added to the national balance sheet. To avoid such a crisis, outright grants instead of loans were demanded by EU leaders. 17 However, direct transfers between Member States with high fiscal capacity and countries with low fiscal capacity would have been inconceivable.

First, all states had lower revenue from taxes and social contributions in parallel to massively higher expenditure through healthcare and furlough schemes, and announcing higher net contributions to the EU in this moment was politically unrealistic. While direct transfers would have to be financed by EU governments, tax smoothing via the EU was politically easier to defend, as repayment would be over a long period of time divided between several multiannual budgetary cycles. In the agreement on NGEU, the repayment costs for grants were even blurred to some extent by the political decision to insert ‘new own resources’ in the respective European Council Conclusions, which kept undefined to what extent repayment is made by direct Member States’ contributions to the budget and to what extent by new own resources, such as plastic levies. 18

Second, many countries would have needed to borrow the funds for higher EU expenditure, and particularly Italy, a net contributor to the EU budget, was increasingly under fiscal pressure. Thus, instead of borrowing nationally, EU borrowing for grants was financially desirable for many Member States because EU borrowing allowed them to offload more costly national borrowing to the EU level without increasing their own debt levels, thus keeping their fiscal position more sustainable. Politically, grants through common EU debt also allowed a large increase of direct EU transfers to be avoided, while also stretching and somewhat blurring the costs of repayment. Thus grants were financially desirable because they avoided the path of increased national borrowing for Member States with worsened fiscal positions and, similar to loans, eased the fiscal burden of governments through borrowing that was commonly shouldered via the EU. Again, similar to EU loans, the logic is built on the fact that the EU borrows cheaper than many Member States and thus tax smoothing via the EU is more beneficial to several governments than applied nationally.

In its reasoning on the compatibility of NGEU with Article 125 TFEU, the Council Legal Service noted that ‘NGEU is not a mechanism for assuming the liability of Member States before or in lieu of the markets’ (original emphasis). 19 This is noteworthy, as it argues that, since NGEU does not replace market financing, it is not to be submitted to the logic of the market test derived from the Pringle ruling. 20 Panascì noted that this broadened the scope of financial assistance and the interpretation of Article 125 from a purely market discipline paradigm to also include the mitigation of structural differences. 21

While channelling support via the EU is thus legally possible in different contexts, it is only a financially feasible option if the EU, or in the case of Article 136(3) the ESM, have better market access than the Member States needing or receiving support. If all EU governments had access to market financing at better refinancing rates than the EU, the use of the EU as a borrower for any form of financial assistance would be of no avail. Therefore, the financial rationale of using EU borrowing for assistance is to reduce the costs of financing through cheaper EU borrowing. Due to this rationale, any form of assistance has by default an effect of improving fiscal sustainability and thus can positively impact the access to market financing. This applies, ipso facto, to assistance to third countries by the EU.

The EU's Borrowing Capacity – An Intergovernmental Guarantee-System

To achieve lower rates than Member States, the EU had used its budget as collateral for borrowing in the past. 22 Until 2010, the EU borrowed cheaper than many EU Member States, and passed on the lower interest rates to the final recipient of the loan. 23 The EU did not incur any direct costs from this kind of borrowing operation, as all financial conditions that the EU had to meet (interest rate, maturities, fees and scheduled repayments) were passed on entirely to the beneficiary of the credit. The EU only functioned as guarantor and intermediate borrower. This helped Member States in the past to fill financing gaps, and to bypass more expensive – that is, unsustainable – market rates or gain access to needed funds. The risk lying with the EU was that a Member State would miss a payment, and the EU had to cover it, which also meant that if the beneficiary of a credit honoured their loan, the EU had no direct costs from these operations. Since 1975 there has never been a situation in which the EU had to cover missed reimbursement by a Member State.

With the introduction of SURE and NGEU in the context of Covid-19, the European Union committed to a €844 billion support structure for EU Member States, which included a transfer of non-repayable grants amounting to €338 billion from the EU to all Member States, and two loan instruments, of which €315 billion was committed until 2026. 24 On the one hand, this support structure reproduced the loan-based assistance design of previous instruments by borrowing cheaper via the EU and to on-lend these funds at the same rates to the recipient. On the other hand, this new system went further than previous ad hoc instruments as it included legal revisions to establish a robust borrowing architecture (away from back-to-back and closer to sovereign-style borrowing) 25 and, most importantly, introduced non-repayable assistance, which was not to be repaid by the recipient Member States, but commonly through the budget of the EU. 26 Thus the grant component of NGEU made the EU indebted to the market, without an equivalent public debt towards the EU being generated by the Member State receiving the borrowed funds. The EU became therefore the end-user of its own borrowing, marking a shift to a more sovereign-style use of borrowed funds. These borrowed funds were assigned to the budget as external assigned revenue and thus fell outside the budgetary procedure and legal limitations. 27

The Legal Basis and Capacity for Borrowing Via the EU

While Article 310 and Article 311 TFEU provide the limitations for borrowing and the frame for the resources of the EU (principles of budgetary unity, balance and discipline, as well as the own resources), 28 borrowing via the EU is enabled by a different legal footing. In fact, Article 310(1) does not prevent the EU from borrowing, it only poses some limits to it. Most notably, it prevents the EU from borrowing to an extent which is not commensurable with budgetary balance according to Article 310(4). 29 Thus the costs of borrowing have to be balanced (or neutral), not the amount borrowed. According to Article 47 TEU the EU has its own legal personality and is therefore allowed to enter financial contracts, 30 and it has done so for decades. Further, Article 323 TFEU stipulates that ‘the European Parliament, the Council and the Commission shall ensure that the financial means are made available to allow the Union to fulfil its legal obligations in respect of third parties’. 31 With regard to repayments of debt and service costs of debt, this means that EU ‘liability from borrowing is only permissible if the Union is able to repay the debt including interest’ (original emphasis). 32 Grund and Steinbach argued in that regard that ‘an operational deficit that would undermine the principles of budgetary balance and discipline would be factually impossible under the accepted NGEU logic’. 33

In practice the EU's borrowing capacity is determined ex-ante by the amount of money available for the EU to service debt payments (interest and principal). Article 310(4) TFEU on budgetary discipline provides for the possibility of using the margin between the own resources and the Multiannual Financial Framework (MFF) to meet financial obligations. 34 Thus since 2010, the borrowing capacity has been interpreted in line with this margin between the MFF and the own resources, also referred to as headroom. Further, Article 322(2) TFEU outlines the procedure to meet cash requirements, which has been detailed in Regulation 609/2014/EU. 35 This Regulation clarifies that the EU can use available funds from its own budget through active cash management as well as additional short-term borrowing to repay debt. 36 In case the Commission cannot do so, it can draw additional Member State resources within the limit of the own resources. 37 This cascade system of guarantees ensures that Member States are only transferring additional funds as a last resort. However, this backstop possibility was also the key metric to increase the EU's borrowing capacity, as an increase of the headroom could achieve that more funds could be drawn upon to service payments linked to EU debt, without immediately increasing budgetary transfers.

The headroom thus functioned as guarantee for repayment and the enabler for tax smoothing. For this reason, governments changed the Own Resources Decision (ORD) to include an additional and exceptional ceiling solely for the purpose of honouring debt under NGEU. 38 In addition, Article 9(5) ORD defined the cascade for obligations arising from NGEU. First, Member States are called to transfer on a pro rata basis (proportional to their estimated budget revenue) the needed funds within the limits of the own resources. Second, if a Member State is unable to honour its share, the Commission can collect the funds from the other Member States on a pro rata basis. However, and most importantly, Article 14(3) of Regulation 609/2014 states that in the case of default on EU debt, the Commission can exceptionally draw Member State funds in excess of the own resources ceiling on a pro rata basis, 39 with the same rule applying in case a Member States cannot honour such calls. As in this procedure Member States are expected to be reimbursed by the respective non-paying Member State ex-post, the debt repayment is not joint and several in its finality, 40 but only temporarily, providing a security for market lenders. It is, however, noteworthy that an amount above the own resources ceiling could be temporarily drawn.

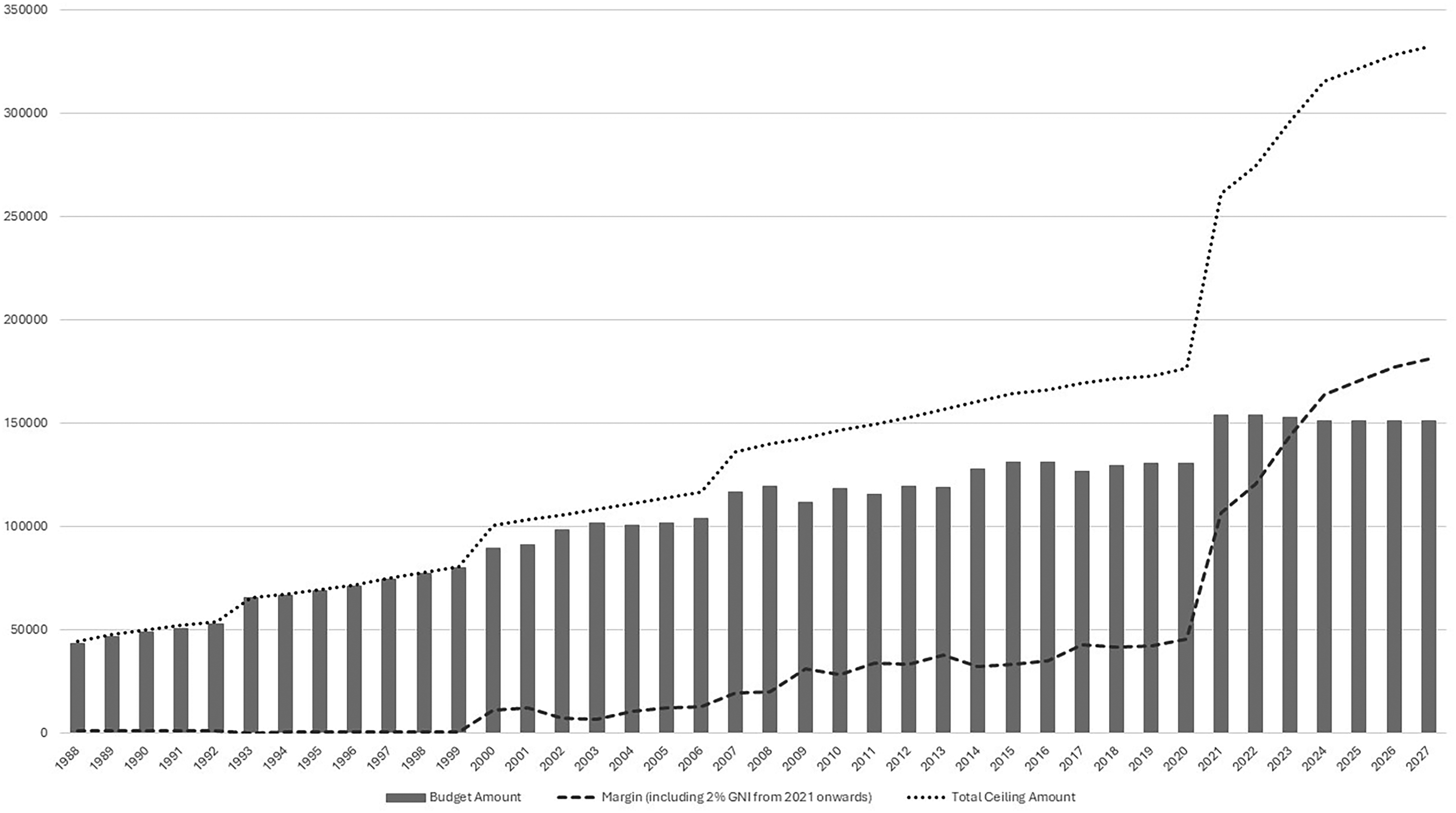

Thus, while the headroom determined the de facto borrowing capacity of the EU, de jure, this limit could be breached in case of default. However, the purpose of the own resources safeguard is to legally and effectively make funds available for honouring EU debt. Thus the headroom became the core metric for credit rating agencies to determine the EU's fiscal capacity. With the introduction of the multiannual financial planning (starting with the Delors package 1 in 1988), 41 the Community introduced a headroom between the planned annual budget and the own resources ceiling. This margin was considered a buffer for unforeseen expenditure and planned at 0.03% of Gross National Product (GNP) between 1988 and 1992, and at 0.01% of GNP between 1993 to 1999. 42 Only with the 2000–2006 MFF, 43 the headroom rose to about 0.14% of Gross National Income (GNI), which was around €10 billion per year, representing a significant buffer. This amount increased to 0.23% of GNI, representing about €27 billion, in 2010. 44

While the headroom could have always been used to cover missing payments, the EU used the margin explicitly in 2010 to determine the capacity of financial assistance under the European Financial Stabilisation Mechanism (EFSM) without determining the lending ceiling of the instrument itself. 45 In comparison, assistance under Regulation 332/2002/EC (balance of payment (BoP) assistance facility) was not explicitly linked to the margin and had a clear lending ceiling of €50 billion. 46 Thus the use of the headroom was a political manoeuvre to make assistance through the EFSM dependent on capital that the EU had available and did not use, avoiding that the EU would prioritize repayment to the detriment of non-compulsory expenditure in the budget. 47 In other words, the potential risk from the EFSM on eating into the budget was limited to the unused margin, while the maximum ceiling of the BoP was fixed. This distinction is noteworthy, as it was the first step to handle the budget and the headroom separately regarding EU borrowing and pathed the way for SURE and later the RRF, as well as SAFE and Ukraine assistance. Thus, with the EFSM, the headroom not only became the buffer for the execution of the budget, but also a potential cash reserve for loan repayments to the market. With SURE, the headroom guarantee was exhausted and did not suffice to cover the full €100 billion loan capacity of the instrument, and thus Member States provided additional pro rata guarantees for the left-over €25 billion. 48

To enable borrowing via the EU under the later-agreed NGEU, EU governments decided to increase the own resources ceiling first from 1.23 to 1.4% of GNI, and by an additional 0.6% of GNI (the extraordinary own resources ceiling), solely linked to increasing the headroom, so as to make borrowing with a headroom guarantee possible. In 2018, 72% of the own resources were GNI-based contributions, 49 with the increase to 2% of this GNI-base within the ORD in 2020, the EU's guarantee for borrowing within the headroom became predominantly intergovernmental. With the increased own resources ceiling by 0.6 percentage points, the headroom amount shot from about €45 billion in 2020 to over €113 billion in 2021, increasing further to over €180 billion in 2024 and even further to a planned €217 billion in 2027 (see Figure 1). The increase of the own resources ceiling was a calculated increase that considered the creditworthiness of EU Member States as the core safeguard to EU borrowing. Thus the EU's borrowing capacity was not derived from centralizing tax authority in parallel with borrowing, but increasing Member States callable guarantees.

Annual amounts in millions of EUR (author's compilation).

In 2010, the governments of the euro area had already engaged in building a supranational funding mechanism with the European Financial Stability Facility (EFSF) and the ESM, which both required a clear commitment from euro area countries to be considered credible. In the case of the EFSF and ESM, euro area governments provided guarantees in the form of callable capital or paid-in capital, which were, if needed, collected from countries and used to reimburse the creditor from which the EFSF or ESM borrowed. As these instruments were established to mitigate a sudden stop and to lend money to Member States in comparatively concessional terms to improve their fiscal space, EFSF and ESM borrowing rates had to be as low as possible, which was entirely dependent on the euro area countries’ own borrowing rates on the market. The evaluation of credit rating agency was crucial as a signpost of credible common borrowing by the euro area. In order to achieve a top rating, the guarantee for each country was increased so that a large share of the potential borrowing via the EFSF was covered solely by countries with top ratings themselves. 50 A similar solution, including paid-in capital, was later applied for the ESM to achieve a top rating. When France, one of the largest top-rated guarantors of the EFSF/ESM, was downgraded in 2012, it caused a subsequent downgrade for both instruments as well, 51 illustrating the dependence of common borrowing instruments on governmental guarantees.

To achieve a top rating for its borrowing in 2020, the EU had to mirror what had been previously done in the sovereign debt crisis by illustrating a credible guarantee through oversubscribing capital from fiscally stronger countries. The EU's increased own resources ceiling served as this callable capital base, which ‘ensures full coverage of debt service by potential additional contributions from “AAA” MS, the main metric relevant for the EU's ratings’. 52 Thus, for the EU to have a top credit rating, and consequentially the lowest possible costs to borrow, the guarantee from the highest rated Member States was fundamental. As of May 2025, only five EU Member States have the highest rating (Germany, the Netherlands, Sweden, Denmark and Luxembourg), with the weighted average of all EU countries being considered of very high creditworthiness. 53 It is therefore implicitly given that the EU borrows with comparably low rates based on a German-Nordic-backed guarantee covering roughly a third of EU GDP, 54 without which these common borrowing operations would be less financially viable. This implicit German-Nordic guarantee also puts the headroom into perspective, as callable claims from other larger Member States such as Italy, Spain or France do not achieve the needed rating. In other words, were Germany and the Netherlands downgraded, the EU is unlikely to uphold its AAA rating and in consequence its borrowing costs would increase, potentially reducing the usefulness of common debt.

Finally, as part of the borrowing capacity, the EU adjusted its procedure to issue bills and bonds. Whereas the EU had until 2019 borrowed solely back-to-back, including currently outstanding €42 billion of EFSM loans to Ireland and Portugal, 55 it introduced the ‘diversified funding approach’ into its financial regulation in 2022. This approach allowed that borrowing for financial assistance could be done through the pooling of funding with different maturities and maturity transformations. 56 This adjustment gave the EU more flexibility in borrowing and allowed it to roll-over its debt. 57 Through this approach, the market presence, including a primary dealer network of 41 financial bodies, and the debt management of the EU were elevated, leading to a more permanent structure for borrowing, which not only covered funding under NGEU, but also previously adopted borrowing instruments such as SURE, as well as assistance to Ukraine and the 2025 adopted €150 billion SAFE instrument for defence expenditure. 58 Through an annual implementing decision, the Commission decides on its yearly borrowing operations, including maximum borrowing ceilings and maximum average maturities. 59 Twice per year the Commission announces its funding plan to manage market expectation, including details about bond-volumes, syndicated transactions and dates of the auctions. 60 This re-organizing of the borrowing structure allowed the Commission to reduce its funding costs, part of the core element of the financial rationale behind common borrowing, and to engage in active and more permanent debt management (as NGEU borrowing is to be repaid until 2058). Thus, while Article 122 TFEU has been triggered ad hoc three times since 2020, the borrowing structure behind assistance via the EU has become permanent. 61

Overall, the EU's capacity to borrow funds from the market has been massively bolstered since 2020 by a financial architecture built on a German-Nordic guarantee through the own resources ceiling. This guarantee is a several, but temporarily joint and several, repayment cascade for debt repayment purposes legislated in secondary law. In addition, the institutional reorganization of EU borrowing gave it a more permanent presence on the market. This has been done with a clear intention of ensuring that creditors and rating agencies classify the EU as top borrower, in order to achieve the low borrowing rates required for improving the fiscal burden of Member States.

The costs of common borrowing in the budget

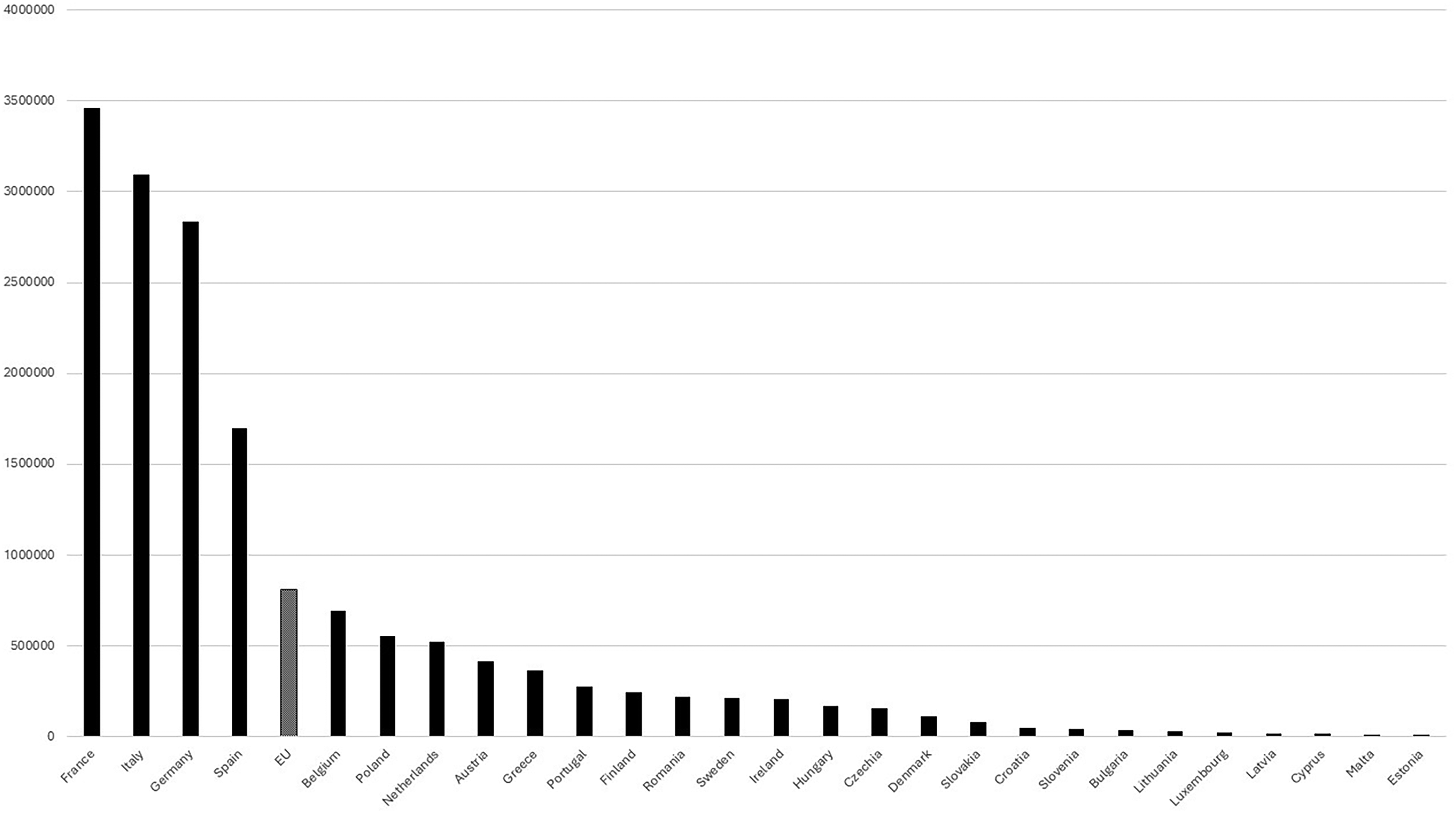

By May 2026, the EU has raised, as intended under the NGEU funding plan and in line with assistance to Ukraine, an amount of outstanding debt of roughly €808 billion (see Figure 2). 62 If including the outstanding EFSM loans to Ireland and Portugal, this amount rises to €847 billion. For the loans under the EFSM, SURE, RRF and potentially SAFE, all costs are covered by the Member States receiving the financial support, thus bypassing the EU budget. For the RRF grants and Ukraine assistance, the borrowing costs are covered by the budget and additional Member State contributions. By May 2026 the EU has paid out €247 billion in RRF grants, €157 billion in RRF loans, €98 billion in SURE loans and €70 billion in loans for Ukraine (MFA + Ukraine Facility). 64 In addition, up to €83 billion are to be borrowed for other funds in the EU budget as part of NGEU. If fully funded by the end of 2027, this amount will increase by €113 billion for RRF grants, €69 billion for RRF loans, as well as about €97 billion for Ukraine assistance, 65 reaching over €1.2 trillion in debt.

Nominal debt by political entity in millions of EUR (author's compilation). 63

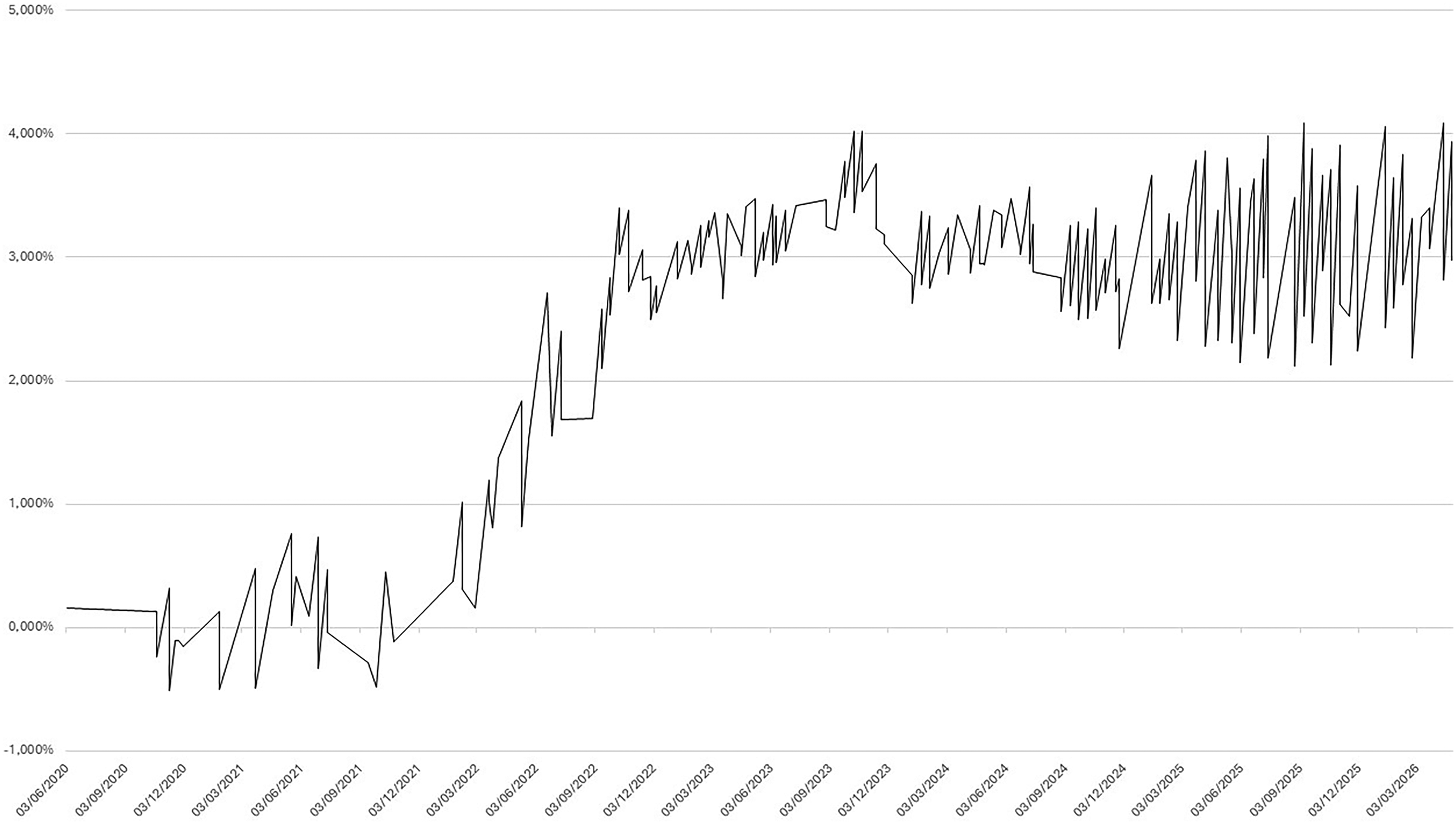

With the introduction of non-repayable assistance in NGEU, the EU budget has to cover all costs related to repayment of these grants. 66 The interest rate costs were initially low and estimated to remain that way, considering the increased ECB asset purchases in the context of Covid-19, which contributed to a low-interest rate environment throughout the euro area. However, with the Russian invasion of Ukraine and the subsequent wave of inflationary tendencies in EU economies, the ECB scaled back its purchases and significantly increased the key interest rates, which made borrowing on the market also more expensive, for governments and the EU. The latter saw its borrowing rates for bonds increase from a negative rate to about 3% (see Figure 3), reaching temporarily higher levels than the French yield, even though France had an AA- (lower) credit rating than the EU. Over the subsequent months, the EU's 10-year bond settled somewhat close to the French yield. Claeys et al. argued that market actors still have higher trust in larger EU sovereigns, which is linked to the EU's lack of fiscal permanency, absence of taxation power and the resulting comparative smaller financial depth. 68 However, the recent announcement that France will use EU loans from SAFE illustrates that even large sovereigns with slightly higher rates utilize the more favourable yield provided by the EU.

Yield of EU Bonds (1 year and longer) at issue date (author’s compilation). (Note: excluding EU bills and non-defined debt certificates.) 67

The costs of interest rates for the borrowed non-repayable assistance rose significantly from the expected range between 0.54–1.15% to a range more than double that, exceeding the amounts earmarked in the budget for costs related to NGEU borrowing. For grants under NGEU, the funding costs are part of the budgetary planning under the heading of ‘European Recovery Instrument’ interest line. 69 Due to the increasing interest rates for EU borrowing, the costs related to coupon payments covered by the EU almost doubled from an estimated €14.9 billion for the period 2021–2027 MFF to over €30 billion, representing about 2.5% of the total MFF. In order to cover this so-called ‘overrun’, the EU has amended the current MFF to be able to mobilize left-over margins from previous years over and above the MFF. The revised MFF introduced the ‘EURI instrument’ to cover the unforeseen borrowing costs for NGEU, a flexibility instrument, 70 as well as the possibility of mobilizing decommitted appropriations from previous budgets. 71 The EURI instrument provides a cascade of funds to be used for costs related to borrowing operations with a final backstop from Member States over and above the MFF. If the higher costs related to borrowing have absorbed all left-over funds from the budget, Member States have to transfer the needed funds to the budget. 72

Next to NGEU grants, assistance to Ukraine also has an impact on the budget. With the Russian invasion of Ukraine in 2022, the EU financial assistance to Ukraine began and is expected to continue until 2027, potentially longer if the Russian war continues. The EU first turned to its Macro-financial Assistance (MFA) framework to help Ukraine using loans covered by a provisioning fund. This fund was supposed to be filled with 9% of the value of each MFA programme, which was paid directly from the EU budget into the fund. For the 2021–2027 MFF, the EU adopted an External Action Guarantee, which dedicated about €1.4 billion for MFA provisioning, making the total loan assistance available for third countries equal to €15 billion. 73 However, considering that lending to a country at war was relatively risky, the provisioning rate was increased from 9% to 70% for loans to Ukraine. 74 The External Action Guarantee was too small for provisioning these Ukraine loans, so the EU decided to use 9% of provisioning from the budget and provide an additional 61% through direct national guarantees. As these loans to Ukraine exhausted the budgetary guarantees, the Council decided to situate the subsequent assistance programmes for Ukraine not in the budget but in the headroom, as it was done for the EFSM, SURE and the RRF. This move avoided the use of provisioning in the budget and relocated the risk with Member States directly.

The entire financial assistance to Ukraine will amount to €91 billion until 2027, of which €17 billion is in the form of grants and €74.1 billion is highly concessional loans. In addition, the EU adopted a further €90 billion concessional loan to Ukraine in April 2026. 75 The maturities of these loans are between 25 and 45 years, with interest subsidies that cover the entire accrued interest over the loan period. The costs of these subsidies and grace periods are borne by the Member States directly, the EU budget and by proceeds from frozen Russian assets. Thus, unlike the RRF or SURE loans to EU Member States, Ukraine will not have to cover all the costs related to the loans.

With the increase in the funding costs for the EU, the interest rate costs for its Ukraine loans also rose in parallel. Similar to the EURI instrument, the costs for Ukraine borrowing were included in the budget. For the exceptional MFAs (€6 billion in loans), 76 the ‘Global Europe’ funds (€19 billion in the 2021–2027 MFF) for the Neighbourhood covered the costs. For the second programme, the MFA + (€18 billion in loans), 77 the interest rate subsidies were covered by Member States directly through externally assigned revenue to the budget of €560 million in 2025, 78 thus shielding the budget from the largest share of the credit costs incurred. In the revision of the budget, this was changed for the third programme, the Ukraine Facility (€50 billion, of which €33 billion in loans). 79 For this instrument, the subsidy for interest rate costs were part of the Ukraine Reserve, 80 a €17 billion fund in the MFF, that covered non-repayable assistance for Ukraine. Part of these grants go directly (up until about €5.27 billion) into servicing the fundings costs of the loan part of the facility. 81 Thus overall funding costs for Ukraine assistance were included in the budget, but separated from the costs linked to funding the NGEU grants, and partially borne by Member States. In the 2025 budget, the loan subsidies were €612 million.

Budgeting Borrowing Costs in the Future

Taking the estimates and the current tendency in the financing costs for NGEU and Ukraine, the EU budget shoulders about €34.4 billion of coupon payments between 2021–2027, as part of its €1,080 billion payment appropriations in the MFF. 82 In total, about 3.2% of the current MFF is dedicated to service EU debt. In comparison, Germany dedicated around 7.3% of its budget to repayment of its debt obligations in 2024, 83 while France dedicated 17.9% of its 2025 budget to debt servicing. 84 Considering Germany as a baseline for high debt sustainability, the interest rate costs for the EU are somewhat low in the current MFF. However, these costs are still guaranteed mostly by GNI contributions of EU Member States, which offload loan payments through the EU, for which they are liable, without increasing debt on their balance sheet.

With the beginning of the redemption period starting in 2028, the expected annual costs for NGEU borrowing ranges between €25 billion and €30 billion. 85 In its proposal on the future MFF, the Commission earmarked a somewhat lower amount of €168 billion for NGEU repayments, representing 8.5% of the total €1,985 billion proposal. 86 Assistance to Ukraine is earmarked with €100 billion, without specifying how much is new loans and how much is funding costs carried by the EU or its Member States. If the current annual costs for the MFA + and Ukraine Facility continue as they stand in 2025, the overall borrowing costs for Ukraine in the new MFF would be €8.3 billion. With the new €90 billion Ukraine Support Loan adopted in 2026, for which the EU could also cover the funding costs, these costs might further increase.

Thus the direct costs for common borrowing are linked to the costs of borrowing of non-repayable assistance under NGEU, as well as the interest subsidies and grants linked to Ukraine assistance. While these costs were relatively low in the current MFF, they will reach over €150 billion between 2028 and 2034, taking a substantial share of the budget. Costs linked to borrowing are exclusively linked to the case that a Member State, or in the future Ukraine, is missing their payments. These liabilities will be over €1 trillion by 2027. Up until May 2026, no EU Member State has ever failed to service its debt to the EU; however, with lending to Ukraine continuously increasing, and the Russian war on Ukraine continuing, it remains to be seen if Ukraine will have the capacity to honour its debt in the future.

Conclusion: Leveraging the budget and ensuring the market

This article illustrates that the main purpose of using EU borrowing for expenditure is to achieve lower borrowing costs. EU loans have the financial rationale to ease the fiscal burden for Member States in order to allow or cover higher expenditure in exceptional circumstances, while EU grants have the purpose of avoiding over-indebtedness and allowing higher tax smoothing than would have been possible through national borrowing.

The EU's fiscal space – that is, its capacity to borrow – is predominantly dependent on a German-Nordic guarantee. These Member States have top credit ratings and can thus borrow on the market at the most favourable conditions. To achieve a similar credit rating and access to market financing for the EU, these top-rated Member States had to provide guarantees for EU borrowing. Thus, while the EU was legally always able to borrow capital, the legal structure to back unprecedent borrowing on the market was built on market-focused secondary law and the ORD, which provided insurance to the market that the EU will legally and can financially honour its debt. The own resources ceiling was exceptionally increased to 2% of GNI, representing a substantial national guarantee for EU borrowing, carried substantially by German-Nordic guarantors. Further, the EU restructured its borrowing operations towards a more permanent market presence with sovereign-style borrowing plans and instruments. Thus the EU leveraged its fiscal space, derived from credible national safeguards in the ORD and legal acts that ensure debt repayment to the market. All of them allowed the EU to lower its costs for its expected total borrowing of over €1 trillion by 2027.

This expansion of EU borrowing has also increased the borrowing costs borne by the budget. While the current MFF used a mix of Member State-assigned revenue, flexibility and special instruments to cover borrowing costs for EU grants and Ukraine assistance, the future MFF already points towards an over five-fold increase of the expenditure linked to the redemption of EU borrowing, reaching close to 10% of the proposed MFF. While previous borrowing operations were purely back-to-back, thus financially neutral for the budget, the borrow-to-spend part of the budget is unprecedented and will continue to represent large shares of subsequent MFFs until 2058. In addition, according to the Commission's proposal, further loans and interest subsidies for Ukraine will be included in the new ‘Global Europe’ envelope, which would increase by 75% to €200 billion. Thus, even though the assistance to Ukraine and the debt issuance under RRF is argued to be temporary, the EU's debt management and budgetary implications are long-term.

Finally, the highly uncertain developments in Ukraine could lead to the EU having to bear the entire costs of loans to Ukraine were the latter to default on its debt to the EU. In that case, the EU will have not only the interest subsidies to cover, but also the principal of the borrowed funds. Considering the increased coupon payments and the potential shortfall in Ukraine's loan repayments, it is probable that the EU budget will be negatively impacted. This could lead to a clash over the financing to cover EU liabilities to the market between those who defend budgetary integrity and EU expenditure and those who are net contributors to the EU budget, over where to mobilize the financing to cover EU liabilities to the market.

Footnotes

Acknowledgements

The author would like to thank the participants of the workshop ‘The future of EU budget in the post-Covid-19 era’ held at Bocconi University Milan on 22–23 May 2025, and in particular Rosalba Famà and Eleanor Spaventa for the organization of the workshop and their valuable feedback on several drafts of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Data Availability

Data is available through the European Commission, Eurostat and the ECB data platform.