Abstract

By embedding pre-funded occupational pensions into the status order of a neo-corporatist system of industrial relations, the Netherlands has developed a second pillar that is second to none in terms of size, inclusiveness and solidarity. But this has also led to a universal financialisation of retirement provision, making the income of the elderly population contingent on the vagaries of financial markets. Two financial crises within less than a decade ended the illusion that such generosity can come at a low price, and thus be reconciled with competitive labour costs. The Dutch government initiated a series of reforms that gave employers a partial exit from shouldering the risks of retirement, reduced generosity and recently also started to undermine the extent of solidaristic redistribution. Hence, occupational pensions are gradually being disembedded from the status order crucial for their comparative good performance in the past with regard to reconciling social and financial sustainability.

The Dutch multi-pillar pension system is often seen as successfully accomplishing the twin goals of social and financial sustainability. It supplements a relatively generous basic pension financed on a pay-as-you-go basis with pre-funded supplements that ensure income replacement after retirement. Through a system of indirect mandating it succeeds in covering most wage-earners, including many workers employed under atypical contracts. It is a system that has infused elements of solidarity and collective governance into what are formally considered to be private agreements.

However, in the aftermath of two financial crises – the 1999 dotcom crisis and the 2008 crash –, the system has come under severe strain, entering a process of change that is fundamentally altering some of the core features that once formed the foundations of its strength. The reforms initiated around the turn of the century have so far left the system’s inclusiveness largely intact, continuing to provide a relatively generous and unconditional basic pension, and a generous second pillar that can boast one of the world’s highest coverage rates. However, the reforms currently being enacted will dramatically change the nature of risk redistribution in Dutch occupational pensions.

This article seeks to explain these changes in terms of the interaction between three interrelated mechanisms: (1) the neo-corporatist sub-system of industrial relations that has resulted in a second pillar that is far more inclusive and plays a significantly larger role in the retirement package of the wage-earning population than in other countries; (2) the reliance on external funding and the financialised nature of the second pillar that has made occupational pensions very dependent upon financial market trends and has facilitated an alignment between labour and capital; (3) the economy’s strong export orientation that has facilitated an identification of workers with the interests of their employers. In the aftermath of the two financial crises, these three mechanisms led to a series of incremental reforms, which on their own only tampered with the system’s parameters, but which in their cumulative effect ended up dramatically changing the nature of the second pillar. They proved however to be insufficient to guarantee financial sustainability under the stricter regulatory regime introduced in the wake of two financial crises, leading the country to embark on a more radical overhaul of the second pillar. This instrumentally invoked arguments of restoring generational justice and adapting occupational pensions to a deregulated flexible labour market, with a view to individualising retirement risks, thereby eroding the system’s solidaristic nature.

The post-war pension compromise

The Dutch pension system is a mix of ‘Beveridgean’ universalism and ‘Bismarckian’ corporatist principles. 1 It combines a flat-rate public pension that provides quite generous benefits to the entire elderly population irrespective of their employment history, with pre-funded earnings-related occupation-based supplements that are negotiated by the social partners as part of collective agreements. The Dutch system of occupational pensions is quite different from what one would expect under a typical ‘Beveridgean’ model, because it is embedded in a ‘state-protected’ or even ‘state-defined’ status order, and as such is reminiscent of the fragmentation of a ‘Bismarckian’ social insurance system. It has infused what according to the OECD are ‘private voluntary’ arrangements, not merely with a state mandate (like in Australia, or more recently in the United Kingdom through auto-enrolment), but also by instituting entitlements based on state-protected status categories. In this context ‘status’ should be understood as ‘a bundle of rights and duties…legally prescribed procedures…privileges, which are attached to virtually every participant in contractual economic transactions and the collective actors representing and governing these participants.’ (Offe, 2003)

This makes Dutch occupational plans rather different from how such plans are established in more traditional ‘Beveridgean’ systems such as the United Kingdom and New Zealand, or in their more generous and more inclusive social democratic variants in Scandinavia. In both variants, occupational plans are negotiated and embedded in a voluntaristic system of industrial relations. As we will argue, this includes the extension of collectively bargained pensions to entire industries and the formal parity-based social partner governance of occupational pensions. The importance of state-sanctioned labour market status is something that Dutch second-tier pensions share with ‘Bismarckian’ countries, an often unacknowledged aspect of the ‘hybrid’ nature of the Dutch pension system.

The occupational pensions in the second pillar aim to supplement the basic pension so that, after 40 years of employment, the sum of benefits from the two pillars replaces 70 per cent of the career average salary. The full integration of the basic pension into the benefit formula of the occupational plans means that the higher the earnings of a person, the more important his or her second pillar pension becomes (both in terms of benefits and contributions). Through a system of ‘quasi mandating’, it is almost impossible for individual firms or wage-earners to defect from the plan negotiated for the industrial sector they are active in. This largely explains the uniquely high coverage of Dutch second pillar pensions: nine out of ten wage-earners are estimated to be enrolled in an occupational pension plan, though if one relates it to all employed persons (i.e. employed and self-employed), this proportion drops to about seven out of ten.

The 70 per cent replacement rate is only considered to be an ‘ambition’ (Tamerus, 2011). Following the move from final to average salary schemes at the beginning of this century, the realisation of this ‘ambition’ has become increasingly uncertain, because the indexation of benefits and accrued pension rights has been made largely contingent upon the investment performance of the pension fund concerned. This is why Dutch second pillar pensions have recently started to be labelled as being based on a ‘defined ambition’ logic, rather than on a pure ‘defined benefit’ approach. It also means that the theoretical replacement rates used in projections by the European Union (European Commission, 2015), the OECD (OECD, 2015), a number of academic studies (e.g. Bannink and de Vroom, 2007), or by financial services industry think tanks (Allianz, 2011; Mercer, 2016), all of which praise the Dutch system for its adequacy, make the system appear far more generous than it actually is (Knoef et al., 2016).

Formally, there is joint representation in the collective bargaining process through which plans are established, and in the governance of the industry-wide schemes. The contribution rates and benefits are set in accordance with the compensation standards of the industry in which the worker is employed. As a consequence, there are significant differences between the 59 industry-wide multi-employer plans. The plans use different values for the basic pension offset (the amount that pensioners are entitled to from the basic pension that is taken into account to arrive at the 70 per cent replacement rate); and use different accrual rates.

There are also significant variations in the distribution of the contribution burden between employers and employees; the level of contribution rates; the formulas used to calculate benefits; the procedures used for requiring additional funding for plans faced with the underfunding of promises made in the past; and the mechanism used for indexing pensions and pension accruals.

Risk redistribution and solidarity in a neo-corporatist variant of pre-funded pensions

In the past, the solidaristic nature of the second pillar has been used with success by Dutch governments to exempt occupational plans from the application of European competition policy. Thus, a 1999 decision of the European Court of Justice

2

accepted the arguments of the Dutch government and of the defendants of the industry-wide pension funds that the solidarity of Dutch pension plans was reflected in the following features: an obligation to accept all employees without a preliminary medical check; the continuation of pension accruals without requiring corresponding premiums to be paid when participants become work-incapacitated; the collective responsibility of the pension fund to take on the burden of overdue contributions in the case of the bankruptcy of one of the affiliated employers; the indexation of benefits to ensure they keep pace with inflation; the use of uniform contribution rates that sever the link between pension accruals and individual risks.

Especially the last feature made compulsory membership a necessity, preventing the possible ‘exit’ of those with ‘low’ risks, which could lead to a downward spiral jeopardising a scheme’s financial sustainability. Employees are required to enrol in their employer’s pension plan, while employers are obliged to participate in the plan negotiated for their industry, unless they can offer a company-based scheme that is ‘actuarially and financially equivalent’ (Harmsen, 2005: 17). 3 The quasi-mandatory nature of the system has not only made the second pillar very inclusive, but has also helped limit problems of selection bias and moral hazard. It has enabled the solidaristic redistribution of longevity risks, albeit only within the confines of the industry or the company one works in.

Fragmented solidarity

Even though the Dutch pension system is often presented as a relatively homogenous model covering the entire wage-earning population under very similar conditions, closer examination reveals quite a different picture. The quite unique combination of occupational fragmentation embedded in an encompassing system of neo-corporatist industrial relations has resulted in what one could see as a ‘Bismarckian’ variant of funded pension provision.

Most employees belong to one of the industry-wide schemes. These schemes cover three out of four wage-earners. But even here, we are still faced with 59 different schemes that differ in terms of the above-mentioned aspects. As in an ideal-typical conservative-corporatist welfare state, the ‘basic universe of solidarity’ thus remains limited to the level of industrial sectors; and, as in a corporatist-conservative welfare state, workers and employers in each sector have to shoulder the costs of their own solidarity (Esping-Andersen, 1987). On the other hand, the embeddedness in a state-induced status order has facilitated convergence and coordination between the different industry-wide schemes, and pension agreements are nowadays much more similar than they were two decades ago.

Because of this fragmentation, conditions for pension rights vary depending upon which industry one works in, or the company one is employed by. Even though the social partner associations negotiating these agreements are organised in national federations that sometimes issue ‘recommendations’, these are not binding. There is no ‘pattern bargaining’, although traditionally some agreements (like those concluded in the metal sector) are considered more important than others (van het Kaar, 2015). Various pension covenants have also contributed to a significant harmonisation of the different schemes and sometimes the government has simply imposed uniform rules through legislation, e.g. the obligation to use a pro-rata pension accrual method so that pension entitlements for part-time workers are not calculated on the basis of the actual wage, but on the basis of the equivalent full-time wage (Anderson, 2012: 221).

Conditional defined benefit or collectively defined contribution?

Pure defined contribution (DC) schemes still only represent a fraction of all arrangements, while most active participants are now enrolled in an average salary scheme with conditional indexation of accruals. While in 1998 more than 66 per cent of all participants were still building up a defined benefit (DB) final salary pension, by 2013 this type of plan was effectively phased out for new accruals. Because indexation of accruals in post-2000 DB plans is almost always conditional upon a fund’s investment performance, nearly all these average salary schemes now resemble schemes for which the pension industry has invented a new label: collective defined contribution (CDC) schemes.

So far, this label has not appeared in the official pension statistics, but the reform of DB schemes in the early 2000s resulted in a hybrid arrangement closely resembling the CDC model. In both cases, the schemes’ sponsors (in the Netherlands predominantly the employers) are no longer willing to fund possible pension plan deficits or pay extra for indexing benefits and accruals. This means that the sponsoring employers have effectively withdrawn from shouldering the demographic and financial market risks of second pillar pensions.

There is nevertheless a major difference between the post-2000 DB schemes and the new CDC model. In the case of the latter, the risks of investment losses are borne solely by employees and pensioners. The scheme’s collective aspect is only that demographic and financial market risks are not carried by individual employees and pensioners but continue to be collectively shared by all plan members. But whereas under the CDC model this is the only option and happens almost automatically, under the reformed DB model there is still the theoretical possibility of the social partners on the board opting for other measures to restore the funding rate (such as increasing the contribution rate).

In contrast to an ideal-typical DB scheme, the Dutch schemes do not grant inalienable pension rights, even if the defined ambition approach does entail what the Dutch call a zekerheidsborging, which one could translate as ‘security safeguards’. Those safeguards are embedded in three institutional provisions (Tamerus, 2011: 273): the collective wage agreements where employers and trade unions ex-ante negotiate the trade-off between the targeted benefit and the acceptable costs of the scheme; the risk management as decided by the pension fund board under the aegis of the supervising authorities; the collective wage bargaining where the social partners monitor ex-post whether the targets were achieved in the best possible way.

Finally, another major difference between individual DC schemes and the conditional DB and CDC schemes prevailing in the Netherlands is that, in the latter, longevity risks are pooled. All members keep their accumulated assets in the scheme and draw a retirement income, circumventing the cost of buying retail annuities, providing profits to insurers and complying with solvency capital requirements.

An ambivalent role for trade unions

Trade unions have traditionally played a role at two levels in the governance of occupational pensions, first negotiating the industry-wide pension schemes with employer associations, and second having a strong formal voice in the governance of the pension funds implementing them.

Negotiating pension schemes

Occupational pensions are a central issue in the nationwide tripartite dialogue between trade unions, employers’ associations and the government. The social partners are also responsible for negotiating pension agreements at industry or enterprise level. Following the conclusion of an agreement, they normally ask the Minister of Social Affairs to make it mandatory for the entire sector. This procedure of mandating (verplichtstelling) is quite similar to the administrative extension procedure used in the system of collective wage bargaining (algemeen verbindend verklaren), and is a core feature distinguishing Dutch occupational pension plans from those found in other Beveridgean systems, i.e. the inclusion of workers in a plan, and the conditions under which this happens, is not solely dependent upon the bargaining power of the individual employee or that of the local union (or in the case of Scandinavian countries of the trade union density rate).

Governing the sectoral multi-employer plans

Most Dutch pension funds are established as an independent foundation (stichting) endowed with the formal ownership rights of the pension fund’s assets and jointly administered by the social partners. Hence, the implementation of occupational pensions was traditionally the exclusive domain of the social partners, with the government only providing the legal framework and supervision through its regulatory agencies. In exchange for this representational monopoly, the social partner delegates on pension fund boards are expected to refrain from pursuing their narrow self-interests. Boards are staffed with an equal number of representatives from employer associations and trade unions.

The very broad coverage of funded occupational pensions has inadvertently laid the foundation for a kind of ‘universal financialisation’ (Belfrage, 2008) in which workers and their trade union representatives ‘have staked their long-term welfare on the ability of their pension funds to reap high returns on investment’ (Engelen et al., 2010: 631). As the domestic capital markets of small and medium-sized states such as the Netherlands are simply not big enough to absorb national pension fund assets, workers unwittingly become part of a coalition driving globalisation and financialisation. With occupational pensions embedded in the neo-corporatist system of industrial relations, the country’s political economy has changed significantly, spreading confusion among workers and their political representatives as to their ‘objective’ interests, unintentionally turning them into stakeholders of global finance, and encouraging them to pursue the same goals as activist investors. Wage-earners and their union representatives have become part of a ‘transparency coalition’ in which workers and owners jointly push for shareholder value (Gourevitch and Shinn, 2005). At the macro level, this identification of workers with their employers’ interests is reinforced by the strong export orientation of the Dutch economy, with unions and the wage-earning population consenting to the gradual retreat of employers from shouldering retirement risks for the sake of keeping non-wage labour costs down and thus not endangering exports. Limiting the financial responsibilities of employers has become part of the Dutch variant of the ‘new general equivalent’ (Bélanger and Thuderoz, 1998), i.e. that jobs have become the currency against which all collective bargaining and social policies are being measured. Trade unions accept the higher-risk investment strategies and increased uncertainty as the only viable way of maintaining adequate pension levels in the future and preserving jobs. Universal financialisation has effectively persuaded Dutch labour to take over the risks and responsibilities of their employers and to adjust their retirement expectations for the sake of company competitiveness (a similar broader point is made by Streeck, 2008).

The impact of two financial crises: from parametric to radical reform

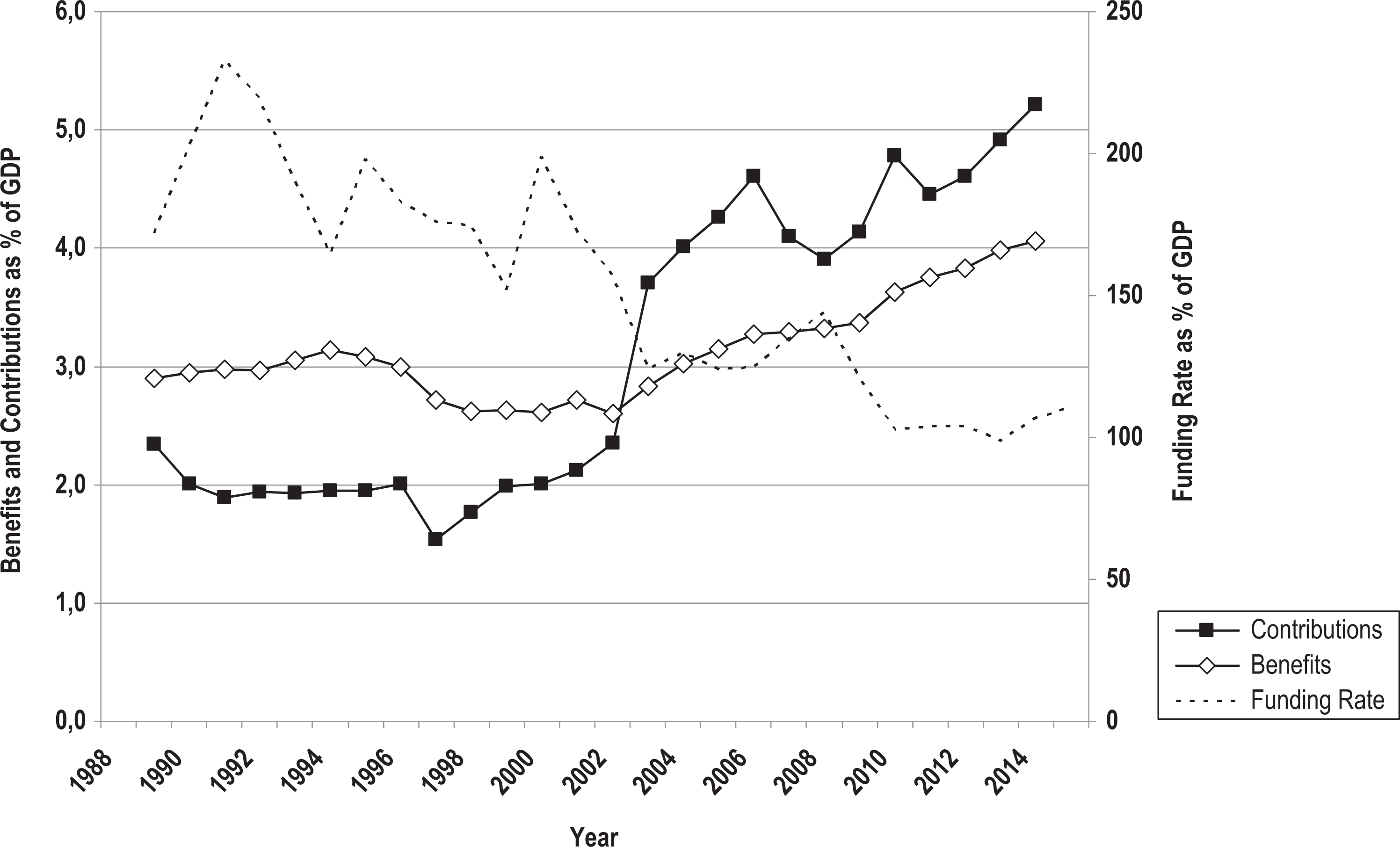

Though the financial crisis of 2008 accelerated the radical transformation of Dutch occupational pensions, the main external shock that triggered the change was the stock market downturn at the turn of the century. The bursting of the dotcom bubble caused Dutch pension funds to lose on average 38 per cent of their assets within three years, with the average funding rate declining from 199 per cent in 1999 to just 124 per cent in 2002. In the subsequent years, most funds had to drastically cut benefits and sharply increase premiums.

Figure 1 demonstrates how the funded nature of the earnings-related part of the Dutch pension system turned from the blessing it appeared to be in the 1990s to a curse in the 2000s. During the earlier period, the total volume of benefits paid out was about one percentage point higher than the total volume of contributions that pension funds needed to stay afloat. After the dotcom bubble burst, things started to change and the situation reversed. During the past decade, the total volume of annual contributions exceeded the total volume of benefits paid out that year on average by one percentage point, in spite of the fact that over this period the average funding rate was almost halved and now often falls below the minimum funding requirement.

The evolution of the funding rate and the total volume of contributions and benefits between 1988 and 2014.

The investment losses and stricter government regulations not only forced pension funds dramatically to increase the contributions, but also led to a temporary suspension of benefit indexation and significantly lower future pension promises.

Parametric reforms

The most important incremental change in the aftermath of the stock market crisis of 1999 was the transition from a final earnings formula to an average earnings formula. As this cut in entitlement only applies to future beneficiaries, its effect does not have a visible impact on current spending levels.

The 1999 crisis is often blamed for the weak financial position Dutch pension funds ended up in during the early 2000s, but the low funding rate was as much a consequence of irresponsible fund management during the period preceding the financial meltdown. On the one hand, it has been argued that most pension funds reduced contribution rates to unsustainably low levels during the stock market boom of the 1990s. The fund for public sector employees, ABP, is indicative of this trend. When it was privatised in 1981, the contribution rate was set at 21 per cent, but in order to reduce labour costs in the public sector, this rate was reduced to little under 9 per cent in 1993. In the private sector, some funds went even further, granting employers so-called ‘contribution holidays’ and sometimes even repaying part of the employer contributions to boost company profitability (Bosch, 2011).

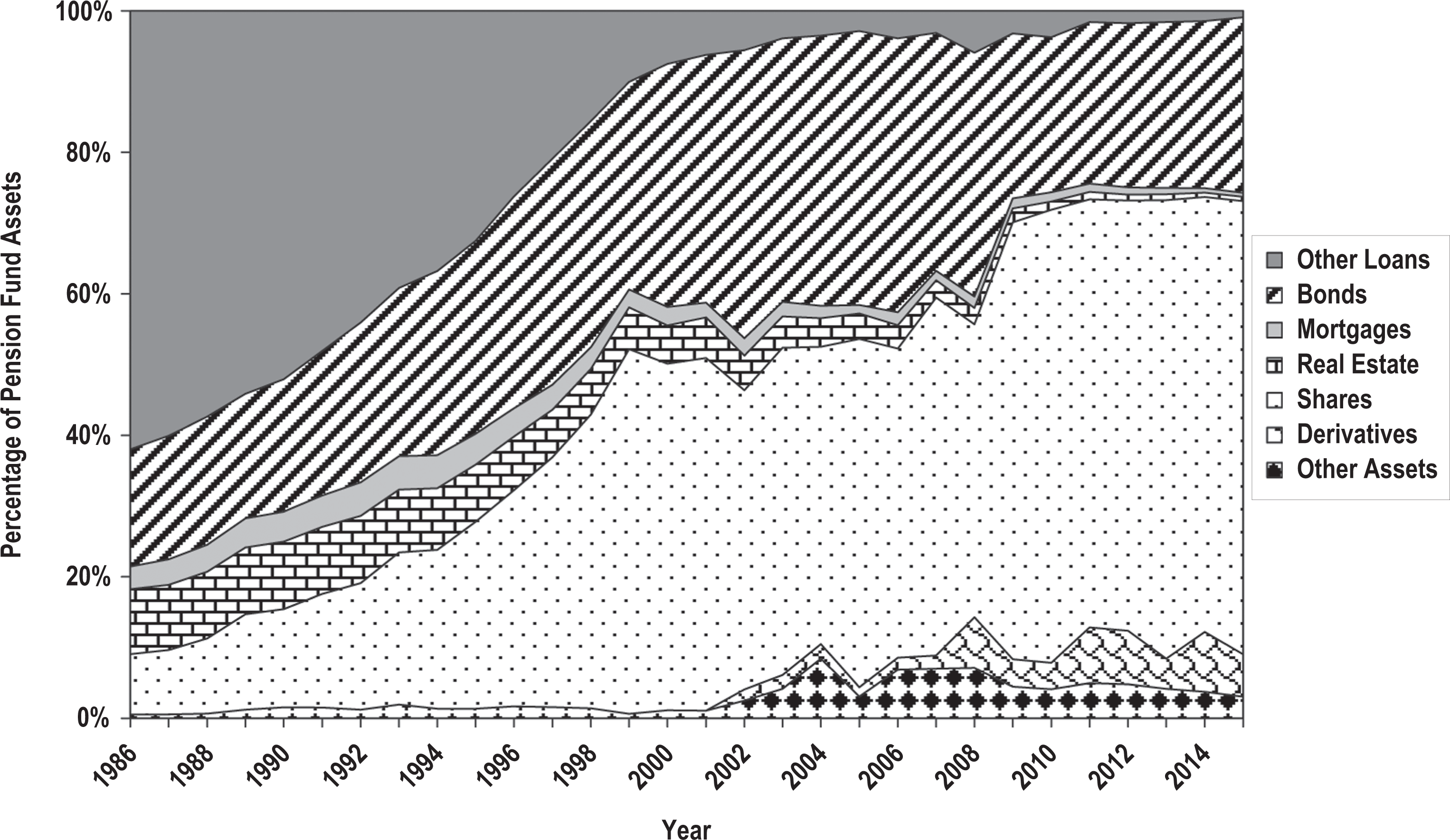

On the other the hand, pension funds were drained to finance large-scale early retirement schemes used to facilitate corporate restructuring. At first the consequences of this chronic underfunding and lavish spending remained invisible because the pension funds managed to achieve spectacular rates of return by massively shifting their portfolios from low-risk lower-performing loans to more volatile and potentially higher-risk shares (see Figure 2). 4

But when the speculative boom came to an end, funds suddenly found themselves underfunded (Figure 1). Almost all pension funds switched from a final-salary plan with de facto unconditional indexation, to an average-wage plan with solvency-contingent indexation of accrued liabilities. This had far-reaching consequences, not only for existing pensioners, but now also for the pension accruals of active workers.

The change in the portfolios of Dutch pension funds 1986–2015.

In the Netherlands, it had always been possible, in the event of disappointing investment returns, for the benefits defined in a pension agreement to be simply re-negotiated, and even cut retroactively (the so-called afstempelen). However, as of 2003, the regulator started imposing constraints on this bargaining process, with negotiations between the social partners on the pension fund board now expected to be guided by a so-called ‘policy ladder’ (beleidsstaffel) formalising the conditionality of the indexation policy and establishing a direct link between the indexation decisions and a fund’s financial position (Westerhout et al., 2004), arguing that the problems were not only the consequence of demographic and financial market developments, but could just as much be attributed to employer practices in the 1980s and 1990s of redirecting pension fund assets towards companies. Even though this diagnosis had already been suggested by a prior report of the regulator (PVK, 2002), it was ignored by the investigatory commissions of 2010. Though secretary of state Jette Klijnsma did order a pilot study on the issue, she later decided not to follow up this inquiry because of the alleged ‘complexity’ and ‘potential costs’ of the study (Klijnsma, 2012; van Baars, 2012). Hence, the alternative narrative never gained much resonance in the pension community.

Instead, the social partners and the government negotiated another pension covenant launching a new kind of pension contract that made the risks more explicit, sought to explain them to pension plan participants and provided a ‘more realistic’ overview of the financial risks (STAR, 2011). Even though the leaders of the union confederations consented to the agreement, it was rejected by a large majority of unions belonging to the largest federation, the FNV, including Abvakabo (the union of public sector and education employees), FNV Bouw (the construction industry) and FNV Bondgenoten (the largest union covering various industries and services). Apart from their opposition to raising the retirement age, these unions were particularly critical of the lack of assurances about benefit levels, and the refusal of the employers to provide extra funds in the case of any disappointing pension fund investment performance.

In the end, the measures proposed in the 2010 covenant were implemented, with a majority within the union movement consenting to the arguments that restoring the funding rate by increasing contribution rates would at any rate not be sufficient, and would endanger employment by raising non-wage labour costs to uncompetitive levels. In the aftermath of the covenant, the government also modified the regulatory framework, introducing a mechanism to adjust automatically the retirement age of both the basic and the supplementary pension when life expectancy increased, and to reduce automatically benefits and accruals in the case of adverse financial shocks or unexpected demographic developments. The combined effects of the new model contracts and the revised regulatory framework have effectively shifted financial market and longevity risks from employers to employees/pensioners (De Deken, 2017).

But even after those incremental reforms, occupational pensions continued to maintain a significant degree of collective risk-sharing among current and future pensioners and between the two groups. As already argued, such risk-sharing is dependent on uniform contribution rates, i.e. that the same conditions mediating the relationship between contributions and benefits apply to all members of a specific fund. These include the rate as a percentage of pensionable income, accrual rates, indexation of accruals and benefits, asset allocation policy (i.e. that the wealth of all participants is kept in a single asset mix), and reductions of accrued benefits in the case of disappointing investment returns or adverse demographic developments. While uniform contribution rates allow a redistribution between younger and older members, male and female participants, it is precisely this kind of ex-ante redistribution that is currently being increasingly questioned.

The discussion of uniform contribution rates was never really part of the discussions surrounding the 2010 pension covenant. It only entered the reform debate during the so-called National Pension Dialogue initiated by the Minister of Social Affairs in 2014. Two interrelated arguments were advanced by the opponents of the existing system of uniform pension contributions. On the one hand, the uniform treatment of participants is questioned in terms of generational justice, with the assertion made that uniform contribution rates lead to a systematic redistribution from younger to older generations. On the other hand, it is considered to be at odds with ‘modern’ flexible labour markets. The underlying argument is that, because the pension accruals of the young have more time to mature, they in principle have a greater impact on the accumulated pension than contributions paid by older workers that have less time to generate an investment yield (Goudswaard, 2013). In a study of the Netherlands Bureau for Economic Policy Analysis this loss for younger generations was estimated to be 2 to 10 per cent of pensionable income for a person aged 30 – dependent on his or her occupation and gender (Bonenkamp and Westerhout, 2010). The proponents of this kind of reasoning state that all this does not need to be a problem, provided that people remain their entire working lives in the same pension plan. However, because of increased labour market mobility, this is increasingly no longer the case. Were all pension plans to apply the same rules, the impact of this problem would be limited. However, uniform rates can pose a real problem for those who start their career as a wage-earner and later decide (or are forced) to enter (quasi) self-employment. It remains to be seen, though, to what extent the increasingly flexible employment histories of Dutch workers indeed involve a career start in a standard employment relationship and a career end in atypical work. The opposite pattern appears more likely, in which it is impossible for younger people to build up sufficient pension rights over the course of their careers due to erratic early employment relationships before finally entering a more standard (and stable) employment relationship (Keune and Payton, 2016: 30). Nevertheless, it is exactly this move from standard employment during the early years of a career towards atypical work in later years that is currently used as the main argument in support of abandoning the uniform treatment of the members of a pension plan.

The initial idea of increasing contribution rates for older workers was abandoned, as it would have increased their cost disadvantage in the labour market and would have undermined the government’s goals of getting people to work longer (De Rijk, 2016). Instead, the government favoured a system of so-called ‘digressive accrual rates’, with the same contribution giving rise to a higher accrual for a younger employee than for an older colleague.

The unions again ended up divided over the issue, with the minority Christian federation CNV being in favour of the government proposal (van Alphen, 2014), while the larger FNV rejected the plans, arguing that maintaining uniform contributions was essential for preventing a ruinous competition over employment conditions. The proposed system would make it impossible for many employees to build up a decent pension, as more and more workers could at best hope to obtain a standard employment relationship in the second half of their careers (FNV, 2016). Women especially would be unable to build up an adequate pension, as they often seek to reconcile work and raising children by working only part-time (De Rijk, 2016). Instead the FNV proposed framing the problem less in generational terms and more in class terms. The ‘perverse’ forms of solidarity allegedly entailed by uniform contribution rates should not be addressed by introducing a system of career-specific accruals or contributions, but rather by redistributing accruals between lower and higher earners. The union proposed increasing the employee share of the contribution rate for higher-earning employees, a system they have labelled ‘dynamic uniform contribution rates’.

So far, the government’s radical reform plans have not materialised, but three of the four parties negotiating to form a government in the summer of 2017 explicitly advocated abolishing uniform contributions. The fourth party did not openly support the idea, even though the research foundation close to that party had already called for digressive accrual rates in 2014, while maintaining the same contribution rates for the young and the old (WI, 2014). Hence, it appears quite likely that a future government will be replacing the system of uniform contribution rates by a less redistributive system (Klopper, 2017).

Conclusion

By embedding pre-funded occupational pensions into the status order of a neo-corporatist system of industrial relations, the Netherlands developed a second pillar that is second-to-none in terms of inclusiveness and magnitude. But this approach to second-tier pensions also led to a form of quasi-universal financialisation of retirement provision, making pensioners’ incomes contingent on the vagaries of financial markets. During the 1990s, this approach contributed to the apparent Dutch miracle allowing generous pension promises and comparatively low non-wage labour costs. Two financial crises made this approach unsustainable. The dotcom crisis of 1999 led to a series of incremental reforms that, taken together, significantly reduced the system’s generosity and guarantees, and allowed employers gradually to retreat from shouldering the retirement risk of their workforce. During the stock market boom of the 1990s it appeared that a generous pension system for which the sponsoring employers were the main risk-takers could be reconciled with competitive labour costs. The two crises destroyed this illusion, and the only course to follow appeared to be to shift the financial risks from employers to employees and pensioners and to trim down the system’s generosity.

However, the reformed system still maintained solidaristic risk redistribution between pension plan members. The extra funding and retrenchment proved to be insufficient to restore financial stability to a system that experienced a second blow following the 2008 banking crisis. Investment losses were aggravated by changes in the valuation method and the ECB’s policy of extremely low interest rates, leading to a call for more radical reforms questioning the system’s ex-ante redistributive elements. So far, these reform proposals have not been implemented, but it is quite likely that Dutch occupational pensions will be significantly less generous, far more insecure, less solidaristic and more expensive in the future than they were two decades ago. In effect, occupational pensions are gradually being disembedded from the status order that was crucial for their comparatively good performance in the past.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.