Abstract

This article compares the responses of the governments and social partners in Italy and Spain to the inflation crisis of 2021–2023. Faced with a common exogenous shock and sharing a comparable institutional setting in the labour market, the two countries’ responses to the inflation crisis differed substantially with regard to the policy mode of crisis response and the types of policy intervention. First, social partners’ involvement was far more significant in Spain, where peak-level agreements were signed setting a three-year trajectory for negotiated wage increases. In contrast, Italian governments proceeded unilaterally, with no attempts at collective bargaining coordination. Secondly, while the Italian government disbursed more fiscal resources through targeted compensatory measures, the Spanish government relied primarily on energy price controls and minimum wage revaluation, with lower overall fiscal expenditure. Finally, the distribution of inflation costs across population groups differed, with inflation in Spain being lower and having less regressive distributional effects than in Italy. We attribute the differing policy responses to the different partisan compositions and ideological orientations of the two governments.

Introduction

Since 2020, European economies have experienced accelerating inflation. Many observers have attributed this to disruption of value chains in the wake of the COVID-19 pandemic and surges in energy and food prices triggered by the war in Ukraine. Given that low inflation was the norm from the late 1990s, this supply-side inflation shock constitutes a major change in the policy environment in which governments and the social partners have to operate. First, inflation erodes workers’ purchasing power, thus weakening private consumption. Secondly, it affects lower income workers and households disproportionately because the latter devote a larger share of their incomes to energy and food (ILO, 2022). But although all EU countries have had to cope with the same exogenous shock they have exhibited considerable variation in both the development of inflation and the adjustment strategies devised by their governments and social partners (see the other contributions to the special issue). Governments have in fact relied on a variety of policy instruments and measures to bring down inflation, including price caps, price subsidies or income maintenance mechanisms, all with different implications for both distributional outcomes and inflation dynamics.

In southern European economies the challenge of inflation management has been particularly acute since the energy crisis. In this article, we compare the adjustment strategies of Italy and Spain to the inflationary shock since 2021. Because of their disproportionate exposure to international tourism (Bürgisser and Di Carlo, 2023) southern European economies were hit particularly hard by the COVID-19 pandemic and the lockdowns that followed (Financial Times, 2021). Furthermore, when the energy crisis began in the wake of Russia’s cutting off of energy supplies to Europe in 2022, European economies were suddenly hit by an inflationary supply-side shock that soon resulted in higher inflation across the economy (De Santis, 2024). Southern Europe was not spared by the energy crisis, and Italy was relatively more exposed than Spain given the former’s greater dependence on Russian gas imports (Redeker, 2022).

Historically, industrial relations and comparative political economy scholars have treated southern European countries as especially vulnerable to the emergence of wage-price spirals because of their lack of neo-corporatist, coordinated industrial relations systems (Hancké, 2013). These countries feature weakly coordinated collective bargaining systems and a pluralistic, fragmented and adversarial system of interest representation (Afonso et al., 2022) When confronted with external challenges (for example, EMU accession), southern European governments had in the past turned to tripartite, peak-level social pacts with trade unions and employers’ associations to achieve wage moderation and compensate for social partners’ limited coordination capacity (Molina and Rhodes, 2007). Compared with the 1990s, however, a period marked by strong social partnership and various successful tripartite agreements, the coordination capacities of southern European economies have been eroded, especially since the 2008 global financial crisis (Molina, 2021; Tassinari and Sacchi, 2021). Under the watch of the European Central Bank and the Commission (Braun et al., 2024), labour market and wage-setting institutions in southern European economies have been weakened by a decade of structural reforms aimed at decentralising wage setting, eroding collective bargaining coverage and disempowering trade union organisations (Marginson, 2015). As a result, Italy and Spain entered the recent inflationary period with ‘blunted tools’, in the sense of a weakened institutional capacity for coordinating a concerted adjustment strategy to tackle the energy crisis. This has been exacerbated by the fact that the balance of class power has tilted further in favour of employers at the expense of unions.

Although they have faced a common exogenous shock and have comparable institutional settings, the policy mode and policy instruments employed by Italy and Spain to adjust to the inflation shock have diverged significantly. First, in terms of policy-making mode and the extent of coordination, the social partners have been more closely involved in Spain, participating in several policy initiatives, including a peak-level agreement to coordinate collective bargaining and set a wage increase trajectory for the following three years. In contrast, no such coordination of incomes policy has been observed in Italy during the inflation crisis, where the government has acted unilaterally. Secondly, regarding fiscal effort and policy responses, Italy has allocated more targeted fiscal resources than Spain, which has focused instead on price controls, with lower fiscal expenditures, mainly for untargeted measures. Finally, the two cases differ in the distribution of inflationary costs across the population. Overall, inflation in Spain has been lower, and more importantly, its distributional impact has been less regressive than in Italy. In Italy, inflation has disproportionately affected the bottom quintile of the income distribution in a context of overall wage stagnation, whereas in Spain, the impact has been distributed more evenly across income groups, and wage stagnation has been less deep. Despite these differences, the two cases demonstrate a common trajectory of overall wage restraint, reflecting the delayed adjustment of collective agreements and the challenges faced by weakened systems of collective bargaining in restoring workers’ purchasing power.

How can one explain the observed variation in the adjustment strategies of two such similar – weak neo-corporatist – countries as Italy and Spain? We compare the cases of these two countries based on the logic of the most similar systems comparative design (Hancké, 2009). Our analysis shows that political variables have the most explanatory power to account for the divergence between two cases. Partisanship and parties’ economic ideology help to explain the different attitudes of the Italian and Spanish governments to management of the inflation crisis, as these influence both the governments’ attitudes towards trade unions, as well as their interpretation of the causes of and necessary responses to the inflation crisis.

This article unfolds as follows. In the next section, we locate the Italian and Spanish cases within the literature on neo-corporatism and inflation management. Subsequently, we elaborate on theoretical expectations of the determinants of cross-country variation in the politics of inflation management and proceed with the empirical analysis of the two cases. In the conclusion we summarise and discuss our findings.

The politics of inflation management: past and present

The study of inflation management was a defining topic in the emergence of comparative political economy scholarship in the 1970s and 1980s (Streeck, 2011; see also the Introduction to this special issue). Neo-corporatist scholarship emerged from the necessity to study governments’ responses to the inflationary pressures resulting from the oil shocks in 1973 and 1979. Neo-corporatist scholars showed that, faced with a similar exogenous shock, countries’ capacity to internalise price shocks and avoid the perpetuation of wage-price spirals hinged largely on industrial relations institutions and systems of interest representation (Tarantelli, 1986). Countries with centralised and hierarchical systems of interest representation were better able to internalise inflation shocks because of the capacity of national/federal unions to adopt and enforce restrictive wage policies.

Since then, the concept of neo-corporatism and its empirical applications in the study of industrial relations have been multi-faceted (Molina and Rhodes, 2002; Streeck and Kenworthy, 2005). While originally understood as a structural concept, neo-corporatism later came to be associated with the process of social partners’ inclusion in public policy-making, namely social concertation. Because of their pluralist and fragmented systems of interest representation (Lijphart, 1999), southern European countries have generally been regarded as lacking the institutional preconditions to engage in structural neo-corporatist policy-making. But precisely because of these institutional deficiencies, during times of economic hardship governments and social partners have often resorted to concerted policy-making. This was the case, most prominently, during the 1990s when southern European countries engaged in a series of social pacts aimed at producing the economic policies and institutional reforms necessary to join the European Economic and Monetary Union in round one in 1999 (Hancké and Rhodes, 2005). In this respect, Spain and Italy developed various social pacts aimed at reforming, among other things, the labour market, the wage-setting regime – to remove or reduce forms of wage indexation – and the pension system. This was done against the background of the restrictive fiscal and monetary policies needed to bring budget deficits and inflation within the parameters of the Stability and Growth Pact (Perez, 2002).

Despite the absence of the institutional preconditions needed for centralised and inclusive public policy-making, social partnership became a common public policy-making mode throughout the 1990s – and in some cases also the 2000s – in the southern European countries where one would have least expected it (Hassel, 2006, 2009). Tripartite incomes policy agreements thus became instrumental as a functional equivalent of wage-setting centralisation to institutionalise wage moderation across the economy.

The institutional and political foundations of incomes policy and collective bargaining coordination in southern Europe have however undergone important changes since the late 1990s. On the one hand, the practice of social concertation appears progressively to have fallen out of favour, as governments have largely excluded the social partners, especially unions, in the formulation of responses to the Great Financial Crisis (Di Carlo and Molina, 2024; Molina and Miguélez, 2014; Tassinari and Sacchi, 2021), or have included them only in ‘cosmetic’ forms of tripartite policy-making (Ebbinghaus and Weishaupt, 2021), with little in the way of substantive outcomes.

On the other hand, various rounds of labour market liberalisation and policies to decentralise collective bargaining – implemented under the aegis of the European Central Bank and the European Commission (Braun et al., 2024) – have further reduced trade unions’ strength and diminished their grip on labour market governance, eroding institutional capacity for the cross-sectoral coordination of collective bargaining (Bulfone and Tassinari, 2021). Institutional reforms after the eurozone crisis have weakened unions’ capacity to engage in collective bargaining and extract meaningful wage increases with an equalising effect across the economy. Rather, various rounds of reforms to decentralise collective bargaining to the firm level have contributed to accentuate cross-sectoral and inter-firm inequalities in wages and working conditions. In a context of weakened sectoral collective bargaining, state-led increases in the minimum wage (often, but not always negotiated with the social partners) have become an important tool in Spain to sustain purchasing power and internal demand and to compensate for the weakness of collective bargaining, especially since 2018 (Bondy et al., 2024). In Italy, a heated debate on the introduction of a national minimum wage has been ongoing, but to no avail because of the hesitancy of the government and social partners alike. The manifest urgency of the wage stagnation crisis in Italy has however decreased unions’ appetite to engage in visible tripartite coordination for the purposes of wage moderation.

Overall, the social partners in Italy and Spain had to face the inflation crisis in a condition of inherited institutional weakness, leaving the possibilities for effective coordination of inflation management on an uncertain footing.

Explaining cross-country divergence in the politics of inflation management

How can one explain cross-country variation in the mode of policy-making and in the type of policy tools adopted for inflation management in most similar cases of weak neo-corporatist countries such as Italy and Spain? Spain’s government opted for an inclusive and coordinated approach to inflation management, involving the social partners in the policy response to the crisis with the purpose of controlling prices and maintaining purchasing power. Italy meanwhile took a different approach, despite being even more exposed than Spain because of its greater dependence on Russian fossil fuel imports (Redeker, 2022) – hence a greater problem load.

The long-established literature on social partnership at the crossroads of industrial relations and political economy provides a well-developed set of theories with which to explain the occurrence of government coordination with the social partners (Avdagic et al., 2011; Ebbinghaus and Weishaupt, 2021). Four sets of – complementary – factors could theoretically contribute to explain cross-country variation in governments’ decisions to engage in social partnership: (i) partisanship and party politics; (ii) trade union power resources; (iii) the government’s strength, and (iv) the problem load (and its nature).

Given their allegedly common goal of de-commodifying workers and providing them with social and institutional protection in the labour market and in the economy more broadly, one could expect an alignment in the material interests of left-wing parties and the trade union movement (Ebbinghaus, 1995; Mattina, 2018). This organisational alignment should in theory be reinforced by the presence of networks and interconnections between left-wing parties and the trade unions (Allern and Bale, 2017). By contrast, because of their opposing ideology and policy preferences, right-wing parties may be opposed to trade union involvement in policy-making and to measures that would further their power in wage setting and in the labour market more widely. Thus, we can expect left-wing parties in government to be more likely to involve the trade unions in processes of social concertation, and to introduce policies aimed at shoring up their wage-setting power and broader institutional power resources.

Another explanation for differences in inflation management concerns trade union power resources. Trade unions not only organise workers with an eye to channelling their interests in the political arena. They can also acquire the de facto role of semi-public policy actors, contributing to the definition and implementation of government policies – what is commonly known as institutional power resources (Ebbinghaus, 2010). Yet powerful trade unions can also act as an impediment to governments’ policy-making ambitions. This occurs when trade union strength is such that they have the capacity to significantly disrupt economic activity or their strike action and demonstrations politically threaten the very legitimacy of the incumbent. In the context of high inflation, unions’ capacity to sustain industrial conflict, advance high wage demands and demand other compensatory measures could thus impact governments’ willingness to negotiate with them in a coordinated fashion. Hence, governments confronted with tough policy decisions in hard times are more likely to involve trade unions in social concertation when the unions are perceived to be strong enough to pose a threat to government survival (Avdagic et al., 2011) or to make high wage demands backed by industrial action. Such incentives could be expected to be much lower when governments face unions that have been significantly weakened and thus pose no threat to government legitimacy (Culpepper and Regan, 2014).

Concomitantly, whether governments decide to share their policy-making prerogatives with trade unions is a function of their executive strength in power. The literature has amply demonstrated that weak governments find it difficult or undesirable to pursue painful reforms or policies unilaterally and are instead more likely to engage in social partnership to obtain the legitimacy they require to remain in power or to run for office near election times (Baccaro and Lim, 2007).

Finally, times of high perceived national emergency have often called for concerted action in the face of a common external threat or, more simply, a high problem load (see Katzenstein’s classic insights on the matter in his 1985 classic Small States in World Markets) (Katzenstein, 1985). In the 1990s, for example, even southern European countries, which lacked the neo-corporatist structures for social concertation, entered into social partnership to address the common challenge of entering the European Monetary Union. Additionally, the nature of the problem load might matter. If the policy challenges at hand are perceived by policy-makers as pertaining to the competence and expertise of social partners, where their knowledge and capabilities are deemed particularly useful for tackling the problem load, it is more likely that they will be invited to participate.

In the case we are considering, the nature of the policy problem is linked to the interpretation of the inflation crisis. The type of policy instruments adopted and whether the social partners’ input is deemed valuable in helping to cope with crisis management depends crucially on governments’ interpretation of the underlying causes of inflation. The causes of contemporary inflation are extremely controversial (Weber and Wasner, 2023; Weber et al., 2022; also Cova, 2023). On the one hand, the supply-side causes of the current inflationary push (Stiglitz and Regmi, 2023) and the contributing role of so-called ‘sellers’ inflation’ (Weber and Wasner, 2023) on top of ‘imported’ inflation are well-documented. This highlights the importance of policy measures to control inflation (such as targeted price controls or taxes on excess profits), which fall outside the traditional logic of wage moderation via coordinated wage setting. This sets the current inflationary crisis apart from the stagflation of the 1970s, whose causes were usually interpreted in terms of an imbalance in the distributive conflict between labour and capital (Hirsch et al., 1978) in which wage-setting dynamics and leapfrogging were central, and thus coordination to attain wage moderation was a fundamental tool of economic stabilisation.

This understanding of the causes of inflation as largely exogenous to the wage-setting system might reduce the incentives to activate coordinated incomes policy agreements or social pacts to achieve wage moderation in favour of other tools, such as price controls. However, governments might still choose to intervene in wage setting, either directly, through minimum wages and public sector wage setting (Di Carlo, 2023; Di Carlo et al., 2024), or indirectly, by supporting collective bargaining as a parallel tool to price controls, with the aim of achieving sustainable wage revaluation to tackle the consequences of inflation on purchasing power and the ensuing cost-of-living crisis, and to contain, control and mitigate its distributive and inequality-exacerbating effects while supporting internal demand.

On the other hand, fears of a so-called wage-price spiral being set off by excessively high wage increases in response to the cost-of-living crisis, although not borne out thus far by the available evidence (Alvarez et al., 2022; The Economist, 2023), have continued to play an important role in the public and policy debates over 2021–2023. This has put the continued necessity of wage moderation on the political agenda (Cova, 2023). If governments fear a wage-price spiral and confront a strong union movement which they believe capable of advancing high wage demands, they might see a need to initiate coordination with the social partners to keep such demands in check and avoid the outbreak or escalation of industrial conflict. If the unions are too weak to make high wage demands, however, the incentive to coordinate with them might be greatly reduced. Governments might instead opt to introduce compensatory measures to sustain purchasing power by bypassing the channels of collective bargaining and avoiding wage revaluation. Factors such as social partners’ real or perceived coordination capacities in wage setting, or their capacity and willingness to orchestrate and sustain, or control and tame, industrial conflict, might thus encourage policy-makers to include them (or not) in crisis management.

We compare Italy and Spain based on the ‘most similar systems’ comparative case study design (Hancké, 2009). Our argument is that political variables are best able to account for the divergence between the two cases. Partisanship and political parties’ economic ideology help to explain the different attitudes that Italian and Spanish governments have adopted to the management of the inflation crisis. These factors influence both government attitudes towards trade unions and their interpretation of the causes of and necessary responses to the inflation crisis. In the next section we explore the three dimensions of comparative analysis for the two countries, namely government responses to the crisis, the role of social dialogue and collective bargaining developments.

Case studies

Italy

Italy’s recent inflation crisis has been managed by two quite different governments: the technocratic Draghi government, in power from 2021 until October 2022, followed by the right-wing Meloni government, which has been in power since October 2022. The most salient feature of this case is therefore the change in government composition and partisan orientation.

Government responses to the inflation crisis

Because of the high share of natural gas in Italy’s energy consumption and its relatively high dependence on Russian gas imports, Italy was particularly vulnerable to the energy crisis. Despite their different political complexions, the two governments’ policy responses have been remarkably similar, in terms of both policy mode and types of measure adopted.

To stem the fall in purchasing power and the pressure on production costs, both governments focused on reactive, mostly targeted compensation measures for households and businesses. Both chose not to intervene with price regulation in the already liberalised energy market, nor to pursue wage revaluation to protect labour income. Already at the beginning of 2022, Mario Draghi’s government introduced tax cuts on energy, subsidies to companies and one-off payments (‘bonuses’) to low-income households. These measures were then variously extended or reshaped, with substantial continuity in the measures introduced by the Draghi and Meloni governments, except for the reduction on excise duties on petrol, gas and fuels, which the Meloni government did not extend.

The compensatory measures introduced from the end of 2021 were aimed directly at compensating households’ real income losses. Resources were mobilised to the amount of €24.6bn, mainly for interventions such as ‘social bonuses’ (€9.9bn in the form of one-off allowances) and ‘energy bonuses’ (€6.2bn) for households and workers with the lowest incomes (Ufficio parlamentare di bilancio [UPB], 2022, cited in Nascia et al., 2023). The energy bonus for low-income households was extended by the Meloni government on several occasions through to 2024. In June 2022, a one-off ‘social bonus’ of €200 was granted by the Draghi government to low- and middle-income workers with a monthly wage of less than €2700 or an annual personal income of less than €35,000 (Nascia et al., 2023). This was then followed in September 2022 by another €150 one-off bonus for employees with annual incomes below €20,000. These one-off bonuses were not replicated by the Meloni government.

A second major policy tool used by the Draghi government was tax reductions on energy (reduction to 5 per cent of VAT on gas for civil and industrial use, and compensation for general system charges for electricity and gas for 2021–2022 and the beginning of 2023). Cuts in excise duties on petrol, diesel and gas were introduced from March to December 2022, as well as a reduction in VAT on petrol. The Meloni government extended several of these measures, except for the cut in excise duties on petrol in 2023, whose suspension provoked social protests and a petrol station strike in January 2023 (Nascia et al., 2023). In March 2023, the government extended tax credits for companies and the reduction of VAT on gas consumption to 5 per cent to the first half of the year; the elimination of general system charges was extended to gas bills but not to electricity bills, resulting in a 20 per cent increase in consumer bills (Nascia et al., 2023).

A third area of – rather timid – intervention focused on the taxation of energy companies’ excess profits. In January 2022, the Draghi government introduced an additional 10 per cent tax rate on companies that benefited from higher energy prices (that is, companies dealing in gas, electricity and petroleum products). The tax rate was subsequently increased from 10 to 25 per cent and extended until April 2022. As of November 2022, however, revenues from the taxation of energy companies were well below previous estimates (over €10bn). Companies opposed the tax, launching legal action and delaying payments (Nascia et al., 2023). The Meloni government proposed to introduce a new ‘solidarity contribution’ for energy companies for 2023, with the prospect of collecting €2.5bn, a much lower amount, and in late 2023 forewent the collection of the last instalment of the tax on excess profits.

Some of the resources generated by the windfall tax on excess energy profits (around €5.5bn) were earmarked from early 2022 to provide a 20 per cent tax credit (credito d’imposta) for all energy-intensive companies experiencing a 30 per cent price increase on 2019. In March 2023, Meloni’s government extended the tax credit for firms until July 2023, then prolonged it (although with some modifications) first until the end of 2023, and then for 2024.

Direct interventions on the wage front were extremely limited. In January 2022, social security contributions for employees with a monthly taxable income below approximately €2700 were reduced by 0.8 percentage points. This reduction was subsequently increased to 2 percentage points and extended to the whole of 2022, and further extended in 2023 by the Meloni government (up to 3 per cent for workers earning up to €25,000 a year). This measure helped to increase workers’ net earnings by reducing the contributory burden on firms – thus relieving the pressure on negotiated wage increases in collective bargaining – but shifted the costs of economic adjustment onto the public budget. A reduction in the taxation on productivity premiums (premi di risultato) from 10 to 5 per cent, up to a maximum of €3000 per year, has also been implemented indirectly to stimulate wage growth. Finally, the 2 per cent cost-of-living adjustment for pensions planned for 2023 was brought forward to the last quarter of 2022 at a cost of €1bn.

The role of social dialogue

The Italian government’s response was characterised by the exclusion of social partners from the design and implementation of adjustment policies. None of the measures discussed above were the result of explicit negotiations or agreements with unions. In line with the approach adopted by the previous technocratic government under Mario Monti during the Great Financial Crisis, Draghi’s technocratic government explicitly avoided interaction with the unions on most significant policy issues, including the negotiation of the National Recovery and Resilience Plan. The government’s goal was to maintain technocratic control of key dossiers, as well as to cultivate strong relationships of support with employers, especially from the northern manufacturing-industrial sector, the backbone of Draghi’s support coalition. Meloni’s government, with a markedly right-wing/far-right ideological orientation, has maintained cold, arms-length relations with the unions, with the occasional official meetings but no substantive negotiations. The unions have, for their part, also been cautiously suspicious of the new government, although without pursuing a strategy of open conflict in its initial period in power. This is partly explained by their usual internal divisions, which undermine their capacity for joint action. The more moderate CISL are more keen on dialogue, while CGIL and UIL are more critical and prone to conflict. The unions thus limited themselves to threatening general strikes (which materialised only in late 2023), organising some national demonstrations (though without particularly strong mass appeal) and repeatedly urging the government to open up proper negotiations (with little to show for it to date).

The Meloni government also adopted an explicitly conflictual approach to the unions, for example, passing a controversial labour reform package on 1 May 2023 (International Workers Day) that deregulated temporary work, tightened the provisions of and rebranded the Citizens’ income (Reddito di Cittadinanza – a form of conditional minimum income) and introduced a further cut in social security contributions for workers earning less than €35,000 per year (see above).

Collective bargaining and wage developments

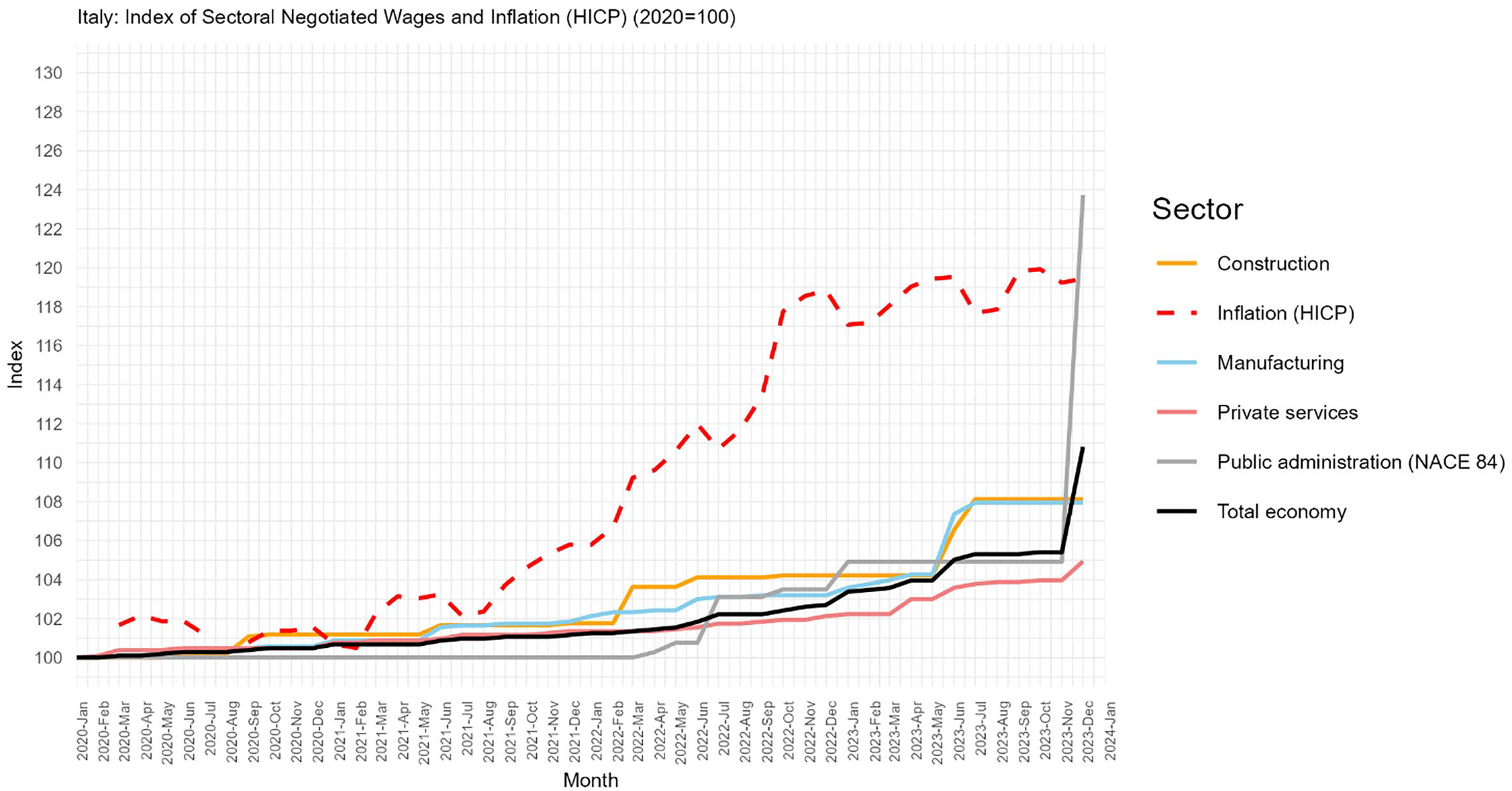

In Italy, collective bargaining has been characterised by an overall paralysis over the 2021–2023 inflationary period, as reflected in a general dynamic of wage stagnation (see Figure 1). In 2022, against a Harmonised Index of Consumer Prices (HICP) of 8.7 per cent, collectively negotiated wages rose by an average of 1.1 per cent (ISTAT, 2023). The gap between contractual wage rises and inflation thus reached 7.6 per cent, the highest since 2001 (Maccarrone, 2023a). The reasons for this prolonged wage stagnation are manifold.

Index of collectively agreed wages, sectoral and monthly (January 2020 = 100) and HICP.

First, despite the supposed institutional resilience of the Italian collective bargaining system (Regalia and Regini, 2018) in recent years the Italian social partners have found it increasingly difficult to renew collective agreements. This is true especially, but not only, for the private services sector and points to growing signs of unions’ organisational weakness and difficulties coordinating with the employer side. Despite the higher number of renewals recorded in 2022 compared with previous years, the Italian Statistics Agency ISTAT estimates that the agreements covering about half of all employees (49.6 per cent) expired by the middle of 2023 (ISTAT, 2023, cited in Maccarrone, 2023b). The national public administration agreements signed in 2022 came into force when their terms had already expired, as they referred largely to the three-year period 2019–2021 (Maccarrone, 2023b). The wage increases recorded by these agreements therefore do not relate to inflationary dynamics, but rather the recovery of lost wage increases which followed the multi-year wage freeze after the eurozone crisis (Di Carlo, 2023).

A further factor accounting for the slow wage dynamic was the inflation index used since 2009 to set the rate of wage increases – this is the so-called HICP net of the costs of imported energy, which is estimated annually by the Italian Statistical Agency (ISTAT) – and the mechanisms providing for wage adaptation to deviations from the index (see Maccarrone, 2023b for a detailed discussion). In the deflationary years following the eurozone crisis, the inflation forecasts were often higher than actual inflation, thus – marginally – favouring labour. In 2021–2022, however, the HICP ‘net of imported energy’ estimates proved to be completely inadequate in the face of the inflation crisis, as the forecasted inflation for 2022 was only 1.0 per cent and 3.4 per cent for 2022–2024. The HICP estimates were valid until June 2022 and thus the agreements renewed up until then included relatively modest wage increases. As the collective bargaining framework in force when the inflation crisis hit did not foresee uniform mechanisms for ex-post verification across sectors to align negotiated wages with actual inflation rates, ‘the gap between contractual wages and inflation exploded’ (Maccarrone, 2023b: 103).

The estimates were revised after June 2022, to 4.7 per cent for 2022 and a total of 9 per cent for 2022–2024. This was closer to the actual value of inflation, but still fell short (in 2022 alone HPCI inflation in Italy amounted to 8.7 per cent). Maccarrone (2023a) further shows that only seven agreements (predominantly in industrial sectors, but also in insurance) were renewed after June 2022, covering only around 10 per cent of dependent employees. Most of the dependent workforce therefore continued to be covered by collective agreements that had either expired or included annual wage increases well below actual inflation. This amounts to a fall in real wages. In this context, labour conflict in Italy has remained low, if not altogether absent, thus further reducing the government’s incentives to enter into negotiations with the unions.

Spain

In December 2019, a left-wing coalition came to power in Spain formed by the centre-left Socialist Party PSOE (Partido Socialista Obrero Español) and left-wing Unidas Podemos. It was supported by some of the nationalist parties for specific pieces of legislation. The coalition government had an ambitious social agenda and a strong commitment to social dialogue. In July 2023, new elections led to an uncertain outcome, resulting in a new coalition government between the PSOE and a new political party SUMAR (partly arising from Podemos), which also gained the support of Catalan and Basque nationalist parties.

Government responses to the inflation crisis

Government policies to cope with rising energy prices focused primarily on containing inflation. The first policies were already implemented in the first half of 2021 and consisted of a VAT cut for small consumers and an increase in the social bonus for vulnerable consumers, together with some incentives for non-CO2 emitting power plants to reduce customer bills. But the government made clear from the very beginning the need to stop the increase in energy prices (and thus inflation) and put all its efforts into achieving this through several (mostly untargeted) measures. These include the so-called ‘Iberian exception’, a set of price controls that decoupled electricity prices from gas prices and reduced electricity bills for families by 15–20 per cent in a context in which inflation was disproportionally affecting low-wage groups and threatened to increase poverty among a large portion of the population. The fight against the negative impact of inflation thus became the main issue on the government’s policy agenda in 2022. Several policy packages were launched to that end (Uxó, 2022).

A first package of measures was adopted in March 2022 as part of the National Plan of Responses to mitigate the social and economic impact of the war in Ukraine. The Plan aimed to mobilise €16bn of public resources, €6bn in direct aid and tax reductions, and €10bn through a new line of guarantees managed through the Official Credit Institute (ICO). The package included a reduction in the VAT on electricity, a 15 per cent increase in the minimum subsistence (‘vital’) income, a bonus of 20 cents per litre of fuel until 30 June 2022 and measures to cap housing rental increases.

The largest policy package came in the second half of 2022 and consisted mostly of untargeted measures, including tax rebates to aid businesses and households, for example, on motor fuel. The decline in electricity prices was accompanied in the second half of 2022 with a reduction in VAT on gas from 21 to 5 per cent until December 2022. The combined impact of these untargeted measures and the ‘Iberian exception’ brought inflation down substantially, from 10.7 to 5.6 per cent by December 2022. This took some fiscal pressure off the government, which shifted to a more targeted approach in its support measures, such as the above-mentioned rebate of 20 cents per litre on motor fuel, which was focused on fuel-intensive companies, or new subsidies for heating and electricity bills for low-income households. Other measures were targeted at energy-intensive firms. The government also introduced a 30 per cent reduction in the price of monthly passes and multi-trip land public transport tickets, an extraordinary tax on large electricity companies with the aim of capturing so-called windfall profits and a temporary tax on large financial institutions.

A third package was passed in December 2022 that extended some existing measures and introduced new ones, such as a reduction in VAT on some basic foods, a direct payment of €200 for families with annual incomes below €27,000 and an 8.5 per cent increase in old-age pensions.

Repeated increases in the statutory national minimum wage have been another important government intervention aimed at combating the effects of inflation. The government has implemented these increases in agreement with the unions and despite the employers’ open opposition (Bondy et al., 2024). After the inflation crisis got under way, the minimum wage was increased first by 1.55 per cent (from €950 to €965 per month) in January 2022. 1 In January 2023, it was increased by another 8 per cent to €1080 per month; 2 and in 2024, it was increased by a further 5 per cent to €1134 per month. 3 In this way, the Spanish statutory minimum wage was increased, even in a context of high inflation, from 51.4 per cent of the median wage in 2020 to 52.2 per cent of the median wage in 2023. 4

Social dialogue

One of the defining traits of the Spanish coalition government elected in 2019 has been its reliance on social dialogue and the involvement of social partners in the negotiation of key policy measures. This was particularly intense during the pandemic years (Molina, 2021). The tripartite agreement on labour market reform stands out in this context.

From the early stages of the inflation crisis, the government made clear its intention to negotiate an incomes policy agreement with the social partners to mitigate the negative inflationary impact on workers and restore workers’ purchasing power. From the beginning of 2022, negotiations failed repeatedly despite a number of tripartite attempts. The main reasons for failure included differences between the most representative trade unions and the employers’ organisations on wage indexation to protect purchasing power. Evidence provided by the Social and Economic Council (CES, 2023) indicates that corporate profits and not wages were responsible for secondary inflationary effects, a finding confirmed by the OECD and the Bank of Spain. This led trade unions to seek mechanisms to ensure a recovery of real wages. Aware of the differences in sectoral dynamics, the unions were open to various forms of flexible indexation, including ‘objective’ indicators for wage indexation in different sectors, hoping that this would make it easier to reach agreement with the employers. However, employers’ organisations have firmly opposed any ex-ante or ex-post form of wage indexation. The employers heavily criticised the government’s inclusion of corporate tax rises for large companies in its anti-inflation packages, together with an increase in the taxes on bank and energy company windfall profits, and tripartite negotiations collapsed.

The Spanish centre-left government, particularly Labour Minister Yolanda Diaz, has made dialogue with the unions a key characteristic of its policy-making approach, in contrast with the rift that had opened between the last centre-left government of Zapatero and the union movement during the global financial crisis (Molina and Godino, 2013). This pragmatic alliance with the union movement serves various political purposes, chief among which is consolidating and broadening the base of support for the weak coalition government and circumventing the opposition of the employers, which have aimed consistently to stymy the government’s re-regulatory and wage-boosting policy initiatives since the left took power (Bondy et al., 2024). Dialogue with the unions has thus acquired both an ideological-symbolic value for the PS-Podemos government, and for Diaz in particular, as well as a pragmatic function of shoring up electoral support (although the centre-left’s local elections debacle in May 2023 called into question the effectiveness of this strategy). This form of labour involvement from above has little to do with the objective strength of the labour movement – union density was 12.5 per cent in 2020 – and has more to do with the strategic-electoral aims of the governing parties. Nonetheless it has restored an important role in policy-making for organised labour, which had previously been eroded.

Collective bargaining and wage developments

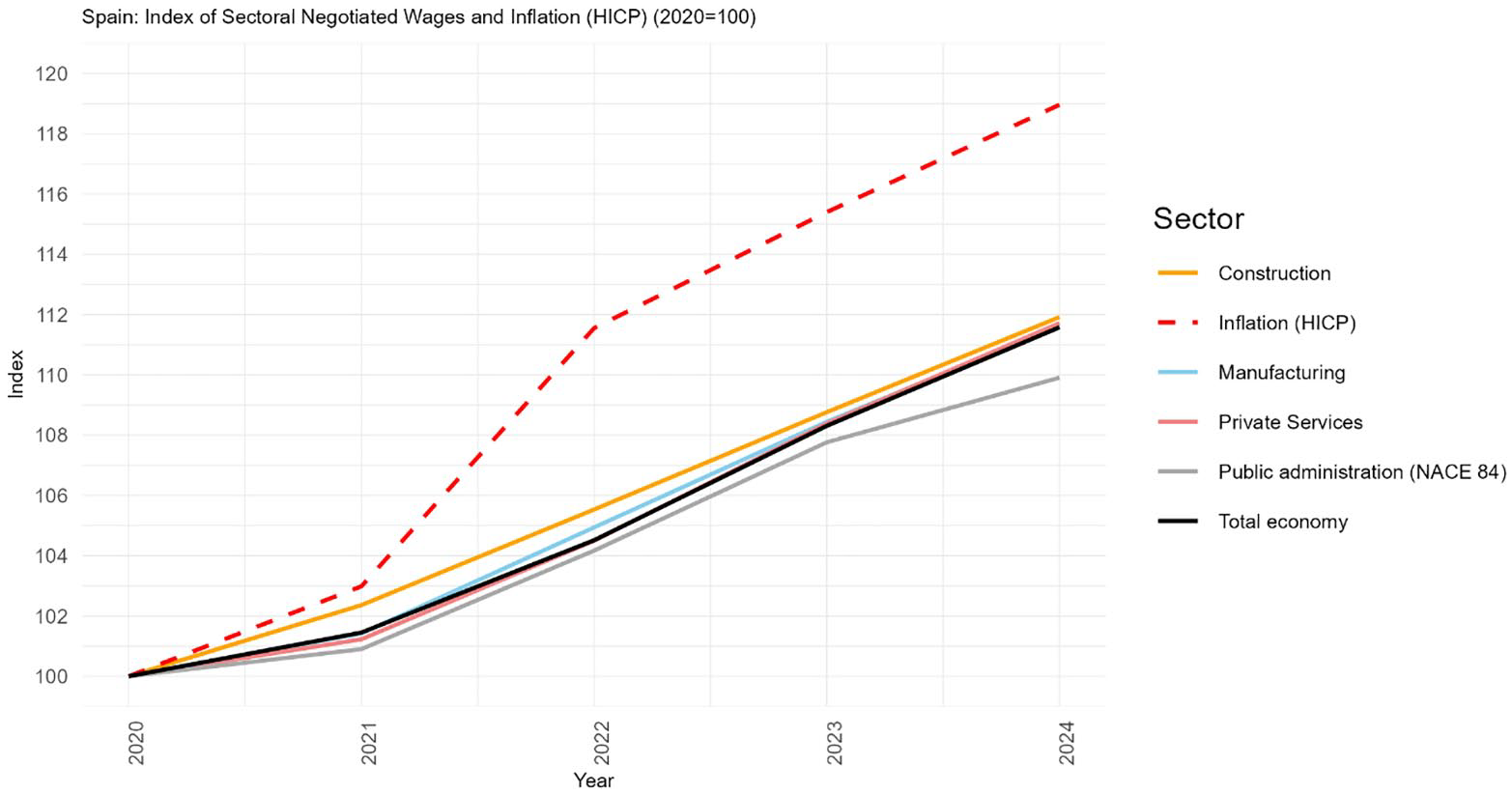

The adjustment of wage increases to inflation in collective agreements became the key issue in collective bargaining in 2022 and 2023. This process has been characterised by a limited capacity to sustain wage purchasing power. During the period 2021–2024, negotiated wages have remained below increases in inflation and a sizeable gap between the two has emerged (Figure 2). This is due to several factors. First, since the late 1990s there has been a decline in ex-post indexation in collective agreements. The proportion of workers whose collective agreement included a wage guarantee clause allowing negotiated wages to adjust to rising inflation was only 21 per cent in 2021. This increased steadily during 2022 and 2023, however, and according to the Bank of Spain, around 45 per cent of workers with a collective agreement signed for 2023 have wage review clauses that allow for wage increases in case real inflation rises above forecast inflation (Izquierdo and Herrera, 2022; Izquierdo and Soler, 2022). Secondly, the number of new or renewed collective agreements fell in 2022 when many employers opposed higher wage settlements or the introduction of wage guarantee clauses. Thirdly, failure to renew the peak bipartite cross-sectoral agreement to coordinate collective bargaining added tensions to this process. Unions and employers signed the so-called fifth peak cross-sectoral agreement for collective bargaining and employment (V Acuerdo para el Empleo y la Negociación Colectiva) only in May 2023. 5 This established a path for wage increases over the next three years, consisting of a 4 per cent increase in 2023, 3 per cent in 2024 and 3 per cent in 2025. If actual inflation exceeds 4 per cent in 2023 and 3 per cent in 2024 and 2025, an extra 1 per cent increase will be provided.

Index of collectively agreed wages, sectoral and annual, and HICP (2020 = 100).

In the case of the public sector, two of the three most representative trade unions and the government signed an important agreement in June 2022. The agreement, which had the support of CC.OO and UGT, provided that the Budget Law for 2023 would include a 2.5 per cent increase in wages of public sector employees. In addition, this rise may be increased by up to 1 additional percentage point, depending on variables linked to the CPI and nominal GDP. Specifically, if the sum of the harmonised CPI for 2022 and the harmonised CPI for September 2023 exceeded 6 per cent, public wages would rise by an additional 0.5 per cent. The second variable contemplates a rise of 0.5 additional percentage points if nominal GDP equals or exceeds the estimate included in the Budget law. The fixed salary increase for public sector employees in 2022–2024 is thus a fixed percentage of 8 per cent, which can be increased to a maximum of 9.5 per cent, depending on certain variables provided for in the review clauses. In real terms, the wage revaluation could reach 9.8 per cent.

Comparative analysis of policy dynamics and outcomes

Comparison of the two cases highlights divergence between Italy and Spain along key policy dimensions. First, involvement of the social partners in policy-making has been considerably more significant in Spain, with participation in several policy initiatives, compared to Italy, where involvement was very limited. We contend that the differences can be attributed largely to the different partisan ideological orientations of the governments in the two countries (centre-left in Spain, technocratic and then right-wing in Italy). Indeed, considering the alternative explanations, no significant difference existed ex ante between the cases, whether regarding the organisational strength of the union movement (severely weakened in both countries, especially in Spain) or governmental weakness (both countries were run by coalition governments). The intensity of the problem load was also more acute in Italy than in Spain, a factor which should have encouraged the Italian government to engage in closer dialogue with the unions. Partisan ideological differences therefore seem to play an important explanatory role. In particular, Spain’s centre-left government displayed both an ideological inclination and an electoral-strategic interest in fostering close relations with the unions.

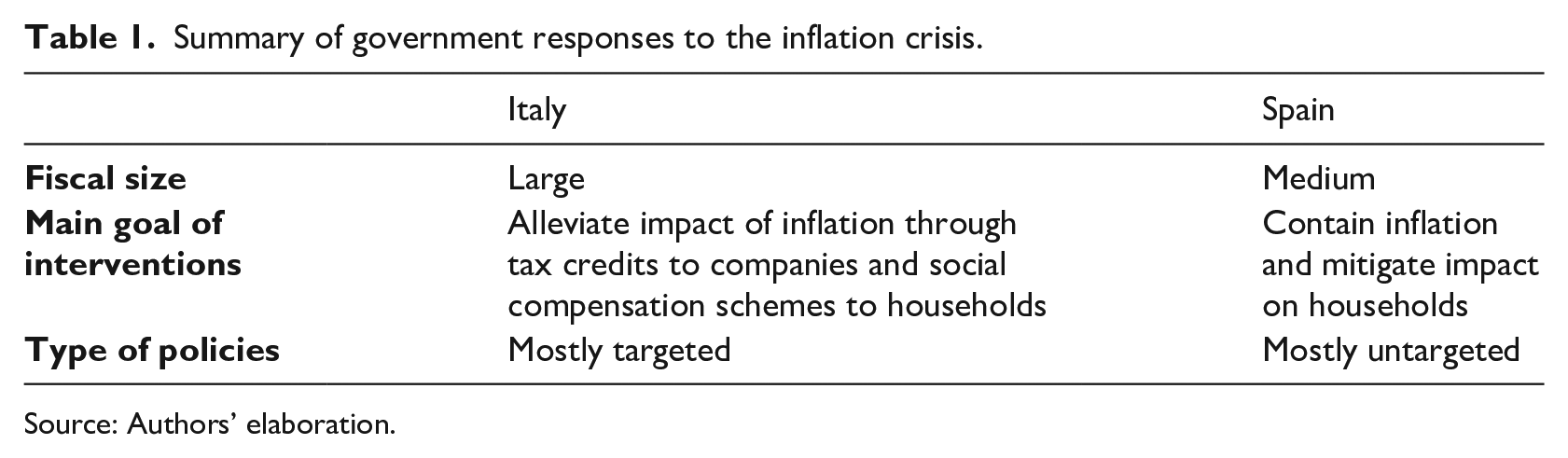

Secondly, differences in partisan-ideological orientation also help to explain the policy mix adopted in the two countries (Table 1). The Spanish government has put stronger emphasis on setting price caps, taxing windfall profits and supporting vulnerable households, while also intervening directly in maintaining wage increases. In Italy, tax credits to companies have played a particularly important role, while taxation of windfall profits has remained more limited and interventions to support wages almost completely absent.

Summary of government responses to the inflation crisis.

Source: Authors’ elaboration.

What sets the two cases most clearly apart is policy-makers’ different interpretations of the causes of and necessary solutions to tackle the inflation crisis. In keeping with its left-wing orientation, the Spanish government has implemented a labour-friendly policy agenda, focused on tackling the distributive conflicts at the root of the inflation crisis and on fostering wage growth even against the employers’ opposition (for example, with regard to the minimum wage). As the Spanish government has explicitly recognised the (excess) profit-driven nature of current inflation, strengthening households’ purchasing power and domestic demand has been a central policy goal, as reflected in its (failed) attempts to coax the social partners into reaching a tripartite agreement on incomes policy for wage revaluation. Despite the limited effectiveness of the Spanish state in its attempts to persuade the social partners to reach a tripartite agreement, the conclusion of several inter-confederal agreements on wage-setting guidelines do indicate that state support for collective bargaining coordination still makes a difference in facilitating bipartite cooperation.

Conversely, the two Italian governments – partly for different reasons – have steered well clear of adopting an explicitly ‘class-based’ reading of the causes of the inflation crisis and its consequences. Instead, they have paid considerable attention to supporting firms and employers and have sought to keep their support, avoiding intervention in collective bargaining. In contrast to Spain, the spectre of a wage-price spiral has repeatedly been evoked in the Italian public debate (Bankitalia, 2022) to support the necessity of caution in wage setting. In the common policy discourse wage increases are to be made conditional on productivity increases rather than considering the possibility of there being an inverse causal relationship. Accordingly, the Italian governments have preferred to resort to alternative tools to strengthen household purchasing power and tackle the cost-of-living crisis, such as tax credits, cuts in social security contributions and cash bonuses. They have eschewed any kind of direct intervention in wage revaluation or collective bargaining. Their concern to maintain positive relations with employers also accounts for the timidity of the measures introduced to tax excess profits, and for the complete absence of regulatory interventions in energy markets. The government’s general lack of concern about widespread wage stagnation also accounts for its failure to intervene in collective bargaining to encourage the social partners to overcome the current impasse and enter serious dialogue on incomes policy and wage revaluation.

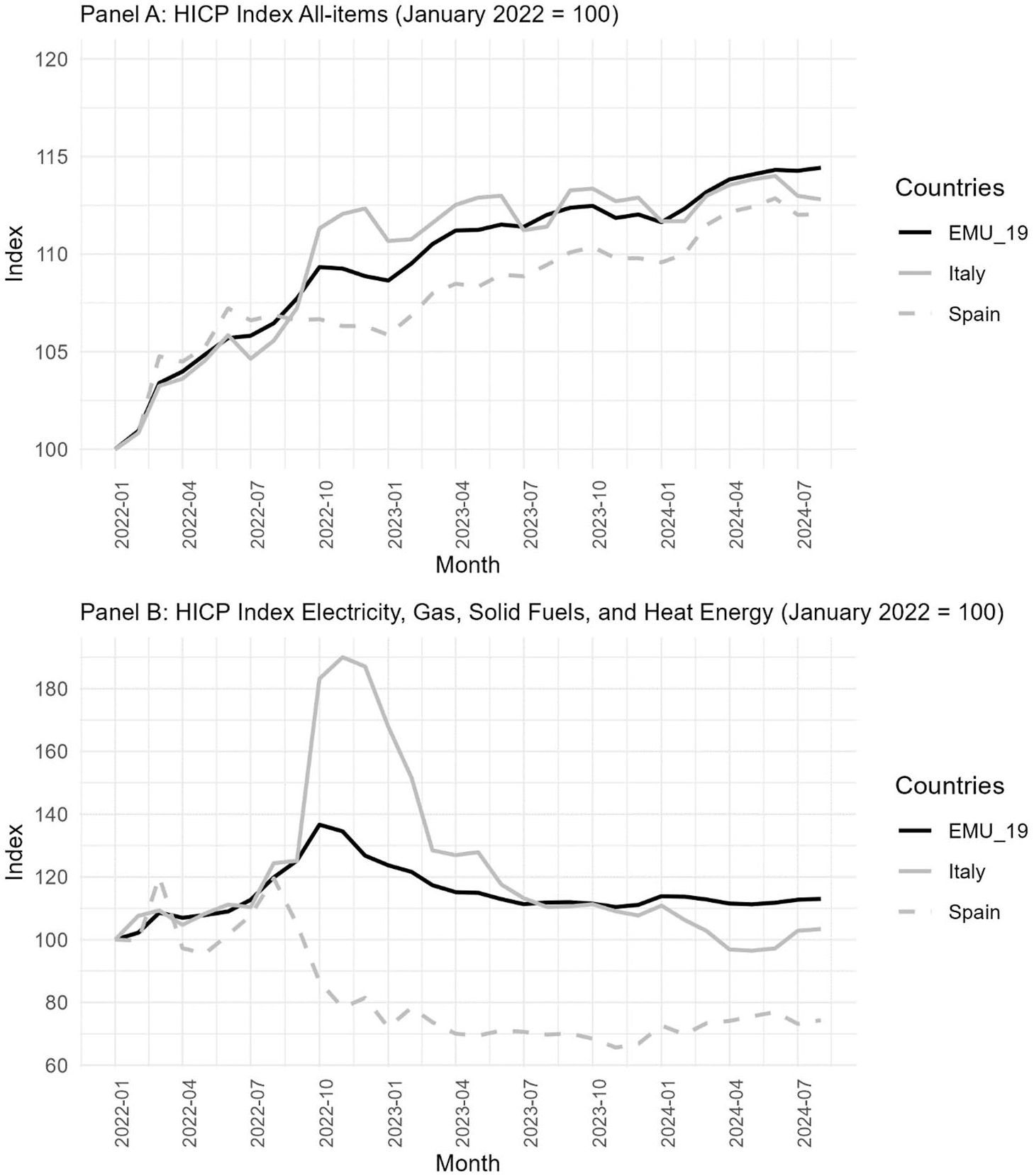

The two countries’ different adjustment strategies have given rise to correspondingly different policy developments. First, while of course both countries have had to cope with the energy shock, inflation was significantly higher in Italy during 2022–2023, while Spain managed to keep price inflation in check (Figure 3, Panel A). Two factors may explain this difference. On the one hand, Italy was more dependent on gas imports from Russia (Redeker, 2022), while on the other hand, in June 2022, the European Commission gave the Spanish government permission to regulate energy prices to decouple the price of gas from that of electricity for 12 months (European Commission, 2022). This was the so-called ‘Iberian mechanism’ or ‘Iberian exception’. According to Spanish government estimates, 6 this decision helped to reduce electricity bills by around 15 to 20 per cent, as reflected in the decline in energy price inflation in summer 2022 (Figure 3, Panel B).

Price inflation (Harmonised Index of Consumer Prices, HICP) and energy price inflation, monthly data (index, January 2022 = 100).

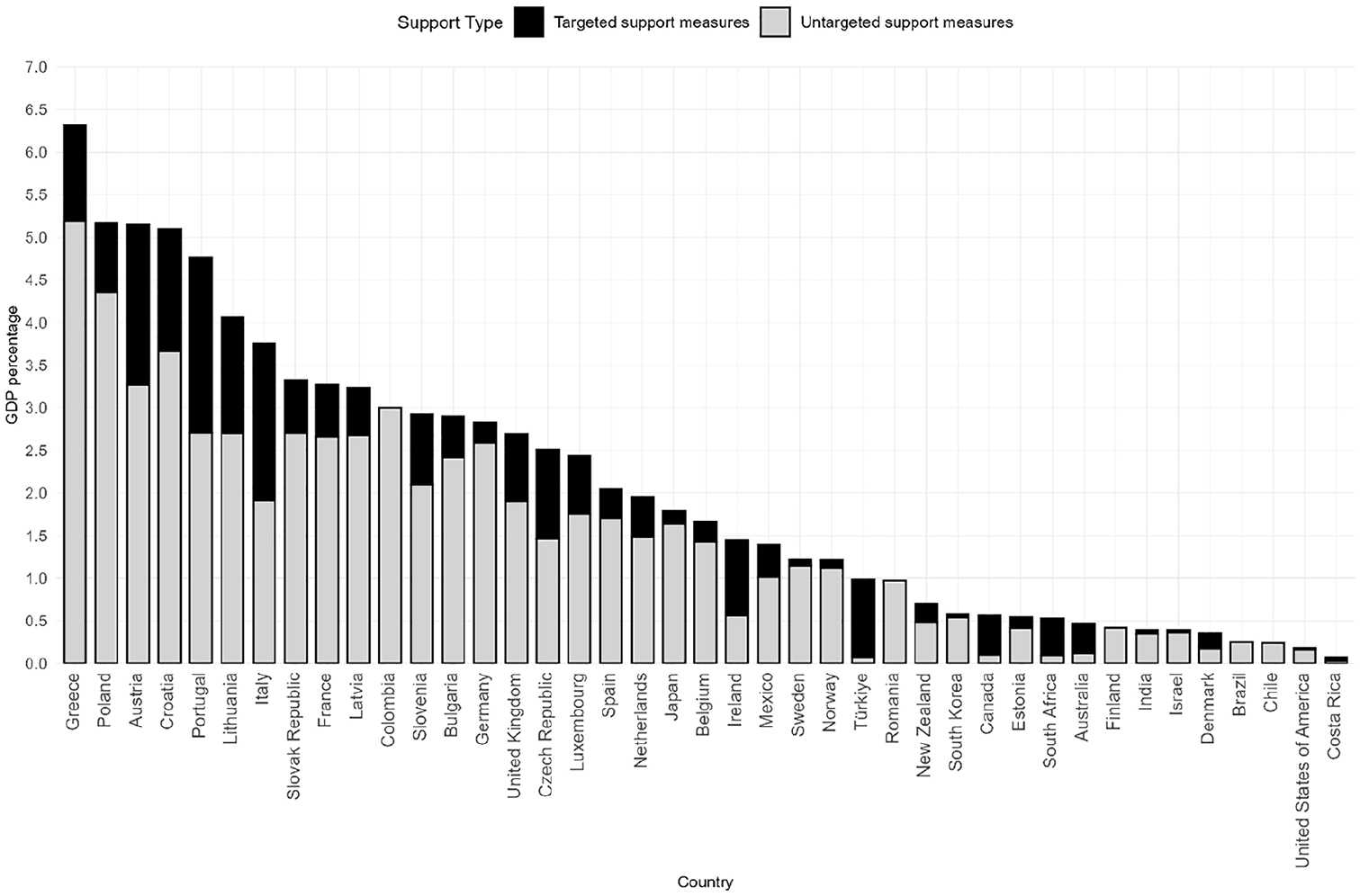

Secondly, Italy and Spain have diverged in the size and targeted nature of their policy measures. Regarding the size of intervention, the fiscal effort was greater in Italy than in Spain, which relied more on regulation of the price mechanism in energy markets. At the same time, the need to compensate for higher inflation led the Italian government to implement more targeted measures to compensate lower income households. These targeted measures can, however, often be more regressive in a distributional sense (Figure 4).

Fiscal size of government support measures by type of policy response.

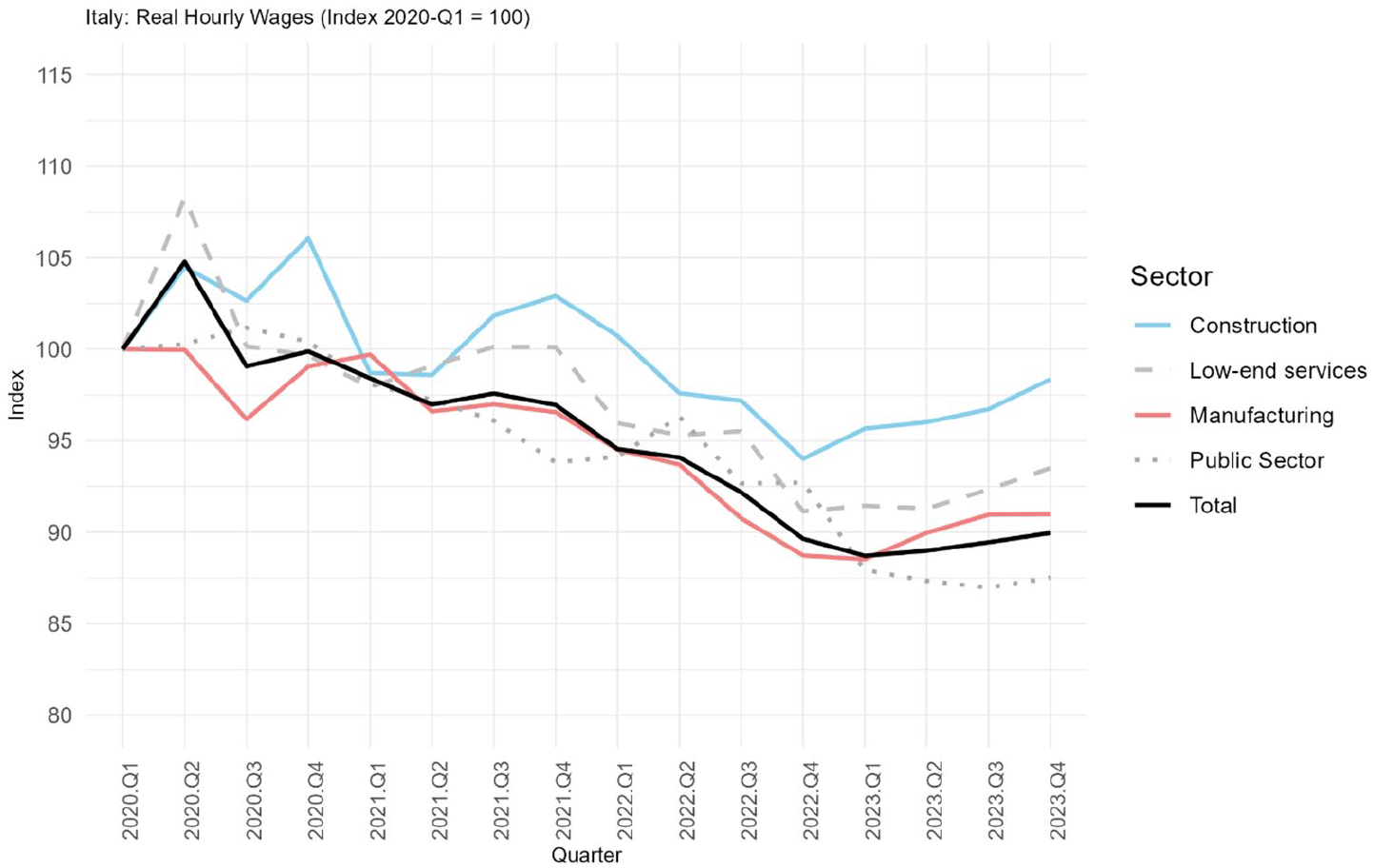

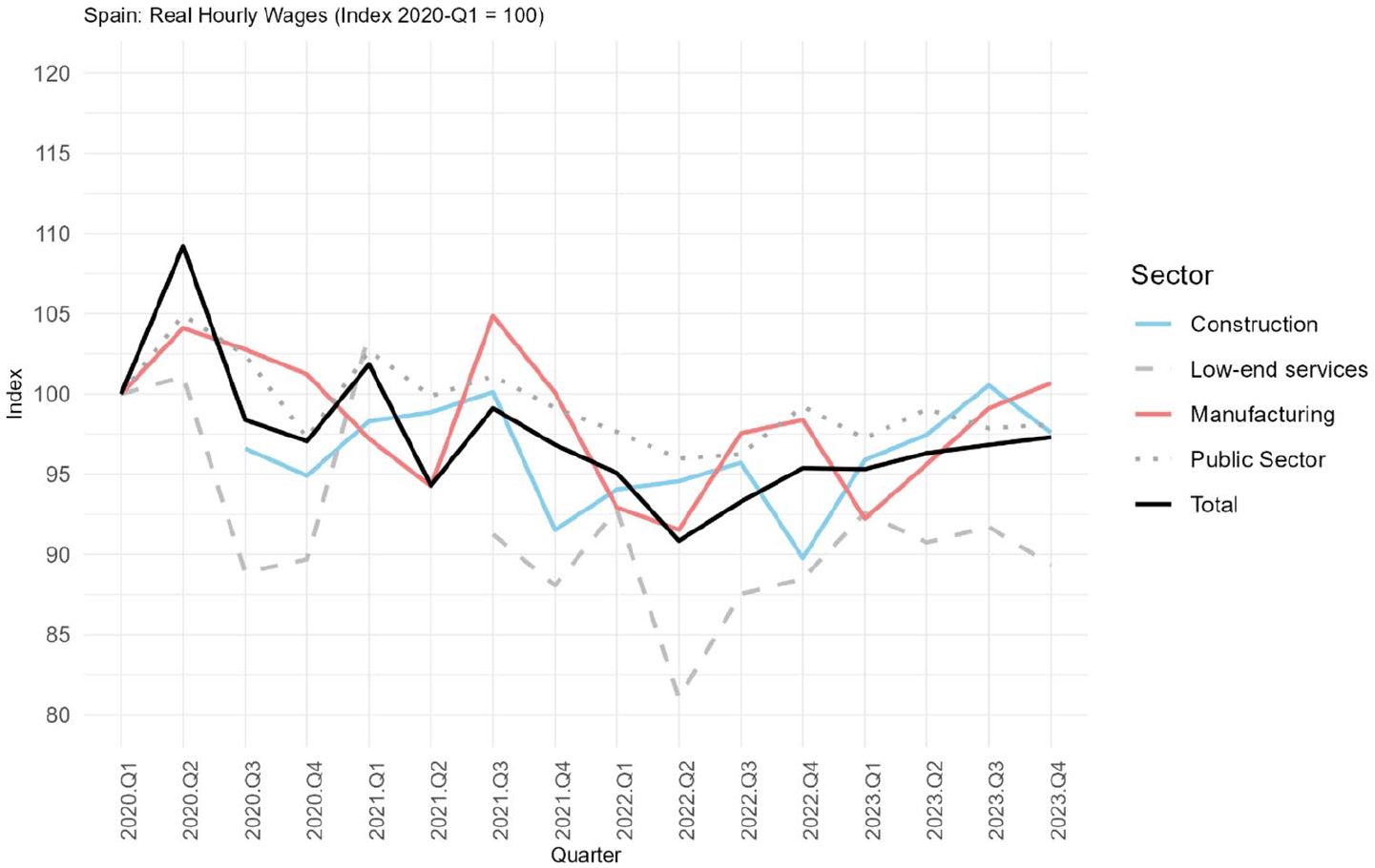

Thirdly, differences have emerged in relation to the two countries’ real wage trajectories. Real wages have fallen much more in Italy since the start of the inflation crisis (Figure 5) than in Spain (Figure 6), although wage-earners’ purchasing power has fallen in both countries. In Spain, however, it appears that the combination of public sector wage agreements and robust increases in the statutory minimum wage implemented by the left-wing government has managed to sustain real wages more effectively than in the Italian case, despite difficulties with collective bargaining in both countries.

Italy, index of real hourly wages (2020 = 100).

Spain, index of real hourly wages (2020 = 100).

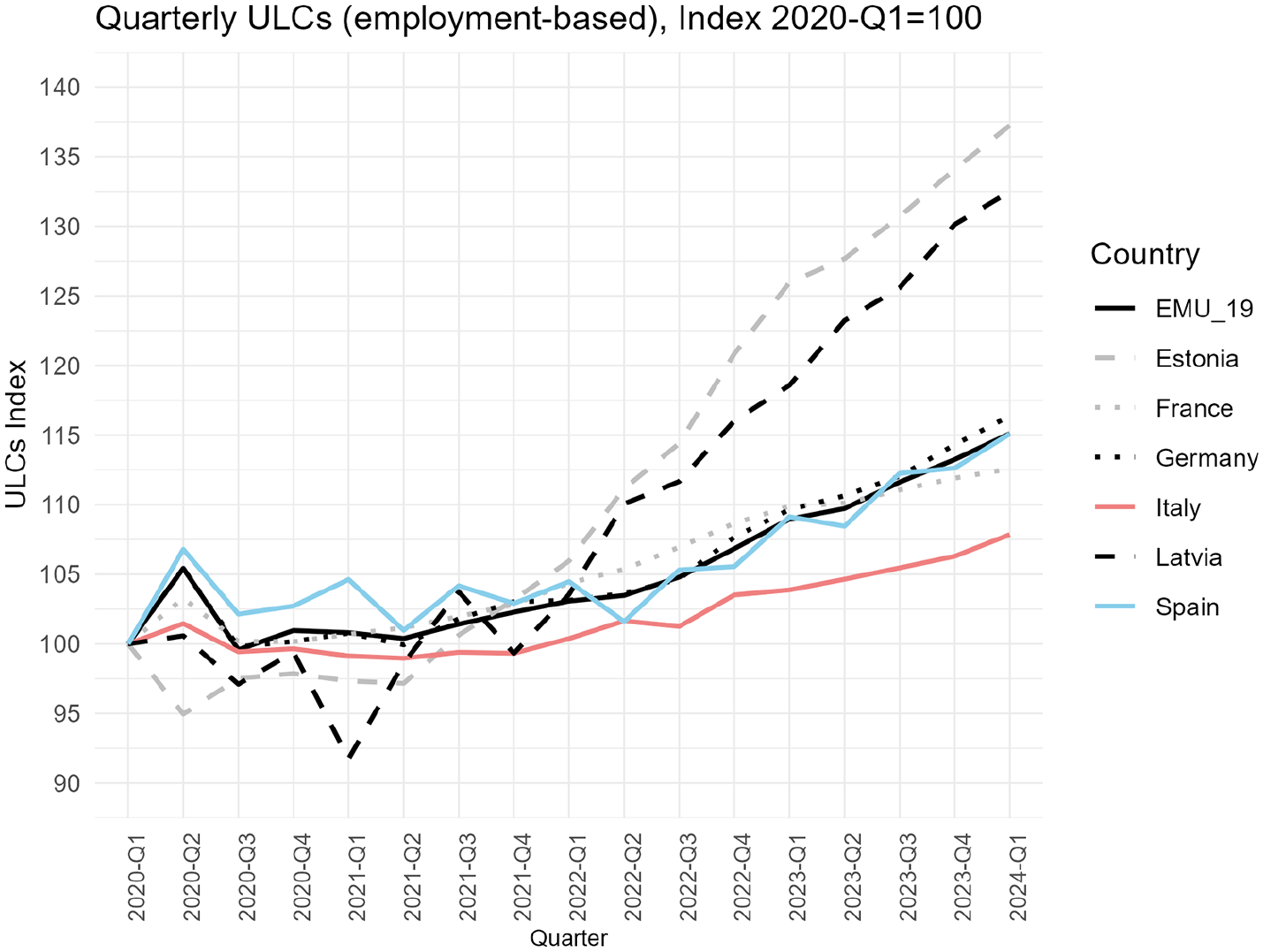

Fourthly, unit labour costs in the two countries have undergone different developments (Figure 7). Whilst in Spain unit labour costs developed in alignment with the eurozone average, in Italy they lagged behind, causing the country to experience internal devaluation.

Index of quarterly unit labour costs (ULCs) (employment-based), Italy, Spain and selected EU countries (2020 = 100).

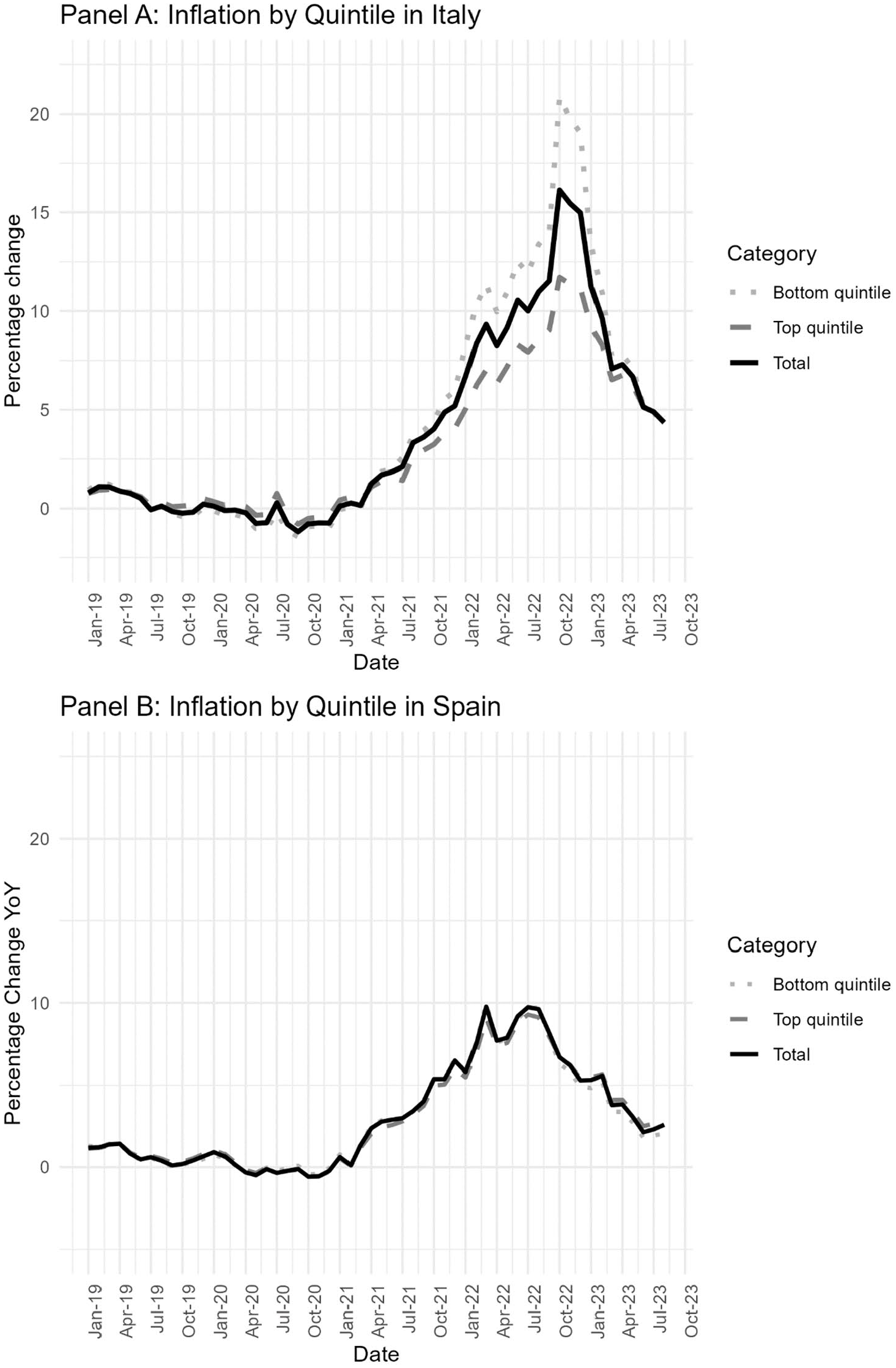

Finally, turning to the inequality dimension of inflation (Figure 8), the disparity between the inflation rates experienced by households in the top and bottom quintiles of the income distribution has been significantly higher in Italy. Inflation inequality is analysed in terms of how inflation affects different income groups asymmetrically, depending on their consumption baskets. According to Bruegel’s dataset on inflation inequality in the European Union (Claeys et al., 2022), both Italy and Spain show similar trends in the contribution of various consumption categories to inflation. Electricity is a crucial exception, however, which explains much of the difference in the distributional impact of inflation between the two countries. In Spain, government interventions to control electricity prices have been essential in mitigating the regressive effects of inflation. Conversely, in Italy, where electricity prices have risen more sharply and without significant government intervention, the lower-income quintiles have borne a much heavier inflationary burden.

Inflation in Italy and Spain, by quintile.

The medium-term effects of these measures on income distribution remain uncertain. According to Eurostat, both Spain and Italy registered the same Gini index for equivalised disposable income in 2023, at 31.5, compared with the euro area average of 29.8. Historically, both countries have displayed higher levels of inequality, with Spain showing a marked increase following the financial crisis and subsequent austerity policies. Since then, income inequality in Spain has declined steadily, interrupted only by the COVID-19 pandemic. In contrast, Italy’s income distribution was more egalitarian in 2014 but saw a modest rise in inequality in the years leading up to the pandemic. The recent inflation crisis and related policy measures appear likely to reinforce these existing trends, with Spain’s Gini index potentially continuing to fall, while Italy’s inequality level may remain relatively stable.

Concluding remarks

Three decades after the run-up to Economic and Monetary Union, which led to a major institutional reshuffling in the collective bargaining systems of southern European countries in order to avoid inflationary wage setting, governments and social partners in Italy and Spain faced a new inflationary context. This article has analysed the policies implemented to fight the cost-of-living crisis and has explored some of its consequences along three dimensions: the involvement of the social partners in policy responses, the policy mix and the relationship with collective bargaining. Significant differences emerged between Italy and Spain in these three dimensions. Among the explanations offered for these differences, government partisanship and ideological orientation play a key role. This concerns policy responses to the inflation crisis and governance styles (labour friendly and union inclusive or not). This calls for a much closer investigation of the political dimension of the inflation crisis and its interaction with wage-setting dynamics.

In both countries, governments faced trade unions that had been institutionally weakened and thus lacked the capacity to pose a credible and sustained threat through industrial and political conflict. In Spain, however, the weak, left-wing coalition government of Prime Minister Sanchez (coalition of PSOE and Unidas Podemos) chose nonetheless to involve unions in crisis management as this was deemed expedient both for consensus-seeking and to achieve the government’s longstanding policy objectives of sustaining purchasing power through wage revaluation and restoration of union power resources in collective bargaining (Bondy et al., 2024). Given their left-wing partisan orientation, the Spanish government was also more inclined to adopt a supply-side and ‘profit-led’ interpretation of the causes of the inflation crisis, which led them to prioritise policy instruments such as price controls, direct intervention in market mechanisms and taxes on excess profits, as well as revaluation of the minimum wage through statutory intervention, even when this meant entering into conflict with organised business.

In contrast, successive governments in Italy had no political incentive to strike deals with the unions because they commanded comfortable parliamentary majorities and had no ideological or electoral affinity with labour and the unions and their support bases. Thus they did not initiate coordinated policy-making that could have shored up unions’ institutional power resources and influence on public policy and in the wage-setting system by attempting to overcome the paralysis of the collective bargaining system. Instead, they opted mainly for the unilateral introduction of various social and energy bonuses that went directly to households, bypassing collective bargaining. This approach did little to overcome the longstanding wage stagnation. The Italian government also interpreted the inflation crisis as unleashing the potential risk of a wage-price spiral, and attached corresponding importance to wage moderation. Accordingly, price control measures and direct interventions in market mechanisms also remained absent from the arsenal of policy instruments adopted by Italian governments, also because of their desire to maintain a close and amicable relationship with business. Interventions in the energy market (such as windfall profit taxes on energy companies) also remained more timid in Italy than in Spain.

The analysis has also revealed the difficulties faced by collective bargaining systems in both countries in recovering purchasing power after three decades of reforms aimed at decentralising and introducing flexibility in wage setting. Indeed, one could explain the lack of tripartite incomes policy agreements in the two countries as a consequence of their collective bargaining systems being oriented towards (excessive) wage restraint. This in itself makes wage-led inflation unlikely. Excessive wage restraint, however, clearly has undesirable implications for workers’ purchasing power and aggregate domestic demand. It may thus make sense to boost the role of the state in coordinating and supporting collective bargaining and wage increases, especially in demand-led growth regimes, as the Spanish case has shown.

Overall, there are lessons here for understanding the political economy of inflation management and wage setting in southern Europe. As Italy and Spain lack some of the requisite neo-corporatist preconditions for wage-setting coordination, the state has played a key role in crisis junctures such as the early 1990s or the global financial crisis. In the first case, it facilitated negotiated incomes policy agreements, while in the second it unilaterally reformed collective bargaining to enforce wage moderation. As a result of these reforms there was further erosion of the institutional preconditions for coordinating wage setting. A weakened capacity to govern collective bargaining could in principle provide governments with more incentives to reach centralised incomes policy agreements with the social partners, or alternatively to intervene unilaterally, bypassing negotiations with social actors. The cases of Italy and Spain demonstrate that such decisions tend to be mediated by partisan politics, by diverse configurations of class power and by the fiscal space governments have available to reduce the negative distributional impacts of inflation.

This article shows that inclusive public policy-making through coordination with the social partners, as observed in Spain, may make it easier for governments to protect workers’ purchasing power. In a context of weakened collective bargaining institutions, government action appears necessary to mitigate the adverse impacts of inflation on earnings and inequality to achieve a more ‘worker-friendly’ response to inflation crises.

Footnotes

Funding

This work was supported by the European Commission, DG Employment, Social Affairs and Inclusion, under the Social Prerogatives and Specific Competencies Lines (SOCPL) Programme, through the MAINSOC (Managing Inflation Through Social Dialogue) project [grant number 101126451].

4

Stats.OECD, Minimum relative to median wages of full-time workers. (accessed 15 September 2024).