Abstract

Global commodity chain, global value chain and global production network scholars have established the importance of studying lead firms and their business strategies to understand how new competitive pressures impact the organization of supply chains. In this analysis of the tobacco commodity chain, the author examines internal strategic planning documents for major cigarette manufacturers from 1960 to 2010 and identifies moments in which the lead firms shift competitive strategies. The article argues that these changes in inter-firm competition are linked, in part, to the changing demands, successes, and failures of the tobacco control movement. During each period, the movement shaped the particular opportunities and constraints facing Big Tobacco, which in turn changed the competitive dynamics amongst these firms, with important implications for other supply chain actors. This historical case of inter-firm competition among cigarette manufacturers reveals the importance of including powerful and enduring pressure groups in the study of global value chain governance – particularly global health movements and environmental movements that may have direct and indirect effects on global value chains above and beyond specific targeted campaigns.

Keywords

Introduction

Research on global value chains (GVCs) has contributed to understanding the contemporary dynamics of globalization. One of the strengths of this literature is its focus on lead firms and their ability to coordinate activities of actors around the globe. The early phase of research on global commodity chains (GCCs) focused on theorizing forms of governance that characterize specific value chains and industries. These studies explained how lead firms exercise their power to restructure global production (Bair, 2005). However, the strategies of lead firms have at times been ‘black-boxed’ in that there has been less effort to explain the impetus behind shifting strategies and governance structures. In other words, we still have much to learn about why different forms of inter-firm competition develop at distinct moments in specific commodity chains – as well as the role played by non-firm actors in influencing these strategies.

In the last decade, commodity studies has gone ‘beyond firm-centrism’ and begun to include other actors previously excluded from analysis. One goal of this literature is to incorporate a better understanding of the role of collective and institutional power in chain governance (Coe et al., 2008; Coe and Hess, 2013; Henderson et al., 2002). Scholars such as Barrientos (2008, 2013), Selwyn (2007, 2012, 2013) and Schurman and Munro (2009) have looked at civil society organizations that are pressuring transnational corporations (TNCs) to engage in more socially responsible behaviour. They have focused on collective agents directly targeting a particular firm or group of firms and the extent to which their campaigns have succeeded.

While this is an exciting new area of study, there is a need to consider the multifaceted impacts of pressure groups beyond their success or failure in specific campaigns. For example, health and environmental movements may have significant direct and indirect influences on corporations’ competitive strategies, which then reverberate to other participants in the supply chain. These transnational movements have been active for decades and their power is considerable. They have experimented with many different strategies, including pressuring governments and international agencies to enact regulations, taking legal action against corporations, sparking public outrage and attempting to change global values and norms. As such, it is worth exploring the relationship between these kinds of actors and TNCs using a commodity chain governance framework.

This article seeks to address these gaps by examining the case of tobacco. The global tobacco value chain is characterized by a significant power imbalance between lead firms (cigarette manufacturers) and their global suppliers, but the chain’s governance has also been shaped by a lengthy and powerful attack on the industry. Although the tobacco control movement is considered a social movement by some, given the involvement of state agencies and actors, it is better characterized as a pressure group. Notably, the tobacco control movement is widely considered one of the most successful of such groups in recent history.

The Legacy Tobacco Documents library is an extraordinary resource for scholars studying this industry, because it is a searchable, online archive of 14 million internal tobacco company documents collected during litigation between the US States and the seven major cigarette manufacturers. As such, it provides access to historical data that is virtually impossible to come by in other industries, thus allowing researchers to delve into the ‘guts’ of a powerful value chain. It is a particularly good source for studying lead firms as researchers are able to download the internal strategic planning documents of transnational cigarette manufacturers, and learn directly from the firms about when and why their competitive strategies changed at particular moments in time.

The aims of this article are threefold: first, to identify key moments in which lead firm strategies have changed over the last half century; second, to examine the changing nature of inter-firm competition within these historical periods; third, to explore the role of the tobacco control movement in shaping these changes in the competitive landscape. To answer these questions, the author analyzes strategic planning reports and other internal company documents of the largest cigarette manufacturers from 1960 to 2010.

Based on this analysis, the article makes two arguments. First, inter-firm competition among cigarette manufacturers underwent two major shifts during this time period. The first occurred in 1980, when manufacturers began to aggressively compete based on price, rather than competing through branding and strategic tweaking of existing products. Then, in the late 1990s, ‘Big Tobacco’ switched course again and began to compete intensely on the basis of new quality criteria. Second, the article argues that these changes in competition are linked to the strategic actions of the tobacco control movement. During each period, the movement shaped the opportunities and constraints facing Big Tobacco, which in turn changed the competitive dynamics among firms.

Literature review

In an attempt to understand globalization, there has been a proliferation of research focused on value chains over the last 25 years (Bair, 2009). World systems theorists Hopkins and Wallerstein (1986) coined the term ‘commodity chain’, which they defined as a ‘network of labour and production processes whose end result is a finished commodity’ (159). In other words, a commodity chain is the connected path along which a good travels on its way to market. The chain imagery helps scholars analyze the ongoing division of labour between firms linked together in the global production of a single commodity. Scholars speak of commodity chains as being comprised of ‘boxes’ or ‘nodes’, each of which captures a set of activities around a particular production process. As Collins (2003: 20) observes, ‘construing a set of activities as a “node” in the chain reduces concrete geographical and historical instances to their role in a single global production process’.

According to Gereffi and Korzeniewicz (1994: 7), a GCC has three features: ‘an input/output structure (a set of products and services linked in a sequence of value-adding economic activities); a territoriality (spatial dispersion or concentration of enterprises in production and distribution networks) and a governance structure (authority and power relationships)’. Scholars typically map the commodity chain by these three features, although the majority of the analyses tend to focus on the chain’s governance structure.

A governance structure points to who ‘drives’, controls or coordinates a chain and helps us understand how control is exercised. ‘Lead firms’ refer to the ‘powerful firms that orchestrate complex global production networks (GPN) in their respective industries, which span different territories and regions’ (Yeung, 2014: 83). GCCs are driven by different types of lead firms. Gereffi and Korzeniewicz (1994) initially hypothesized that there are two types of chains: producer-driven and buyer-driven chains. Subsequent research has identified a more complex variety of possibilities.

A parallel literature on GVC emerged around this time from the Institute of Development Studies in Sussex; these research efforts also focused on governance structures (Coe and Hess, 2013). Although in practice GVC is often considered interchangeable with GCC analysis, Bair (2009: 1) highlighted its different theoretical origins, which draw heavily on transaction cost economics rather than comparative development studies. Sturgeon (2009) argued that GVCs’ conceptualization of chain governance is less useful in assessing power relations along the entire commodity chain, but best used for studying a specific link in the chain.

Despite their differences, neither approach gives much attention to the role of the state and non-firm actors in governance and chain restructuring. In 1995, Gereffi introduced the concept of the ‘institutional framework’ as a fourth dimension of GCCs. The institutional framework ‘identifies how local, national, and international conditions and policies shape the globalization process at each stage in the chain’ (Gereffi, 1995: 113). In other words, it acknowledges that actors not directly engaged in the chain may nonetheless have a strong influence on how lead firms act and GCCs are structured.

The most recent variant of commodity chain analysis is GPN analysis, which was influenced by actor-network theory (ANT) and aims to do a better job of incorporating labour and all relevant non-firm actors into its framework (Coe et al., 2008; Coe and Hess, 2013; Henderson et al., 2002). As Selwyn (2013: 77) explained, ‘GPNs are conceived of as being “embedded” within broader, multi-scalar structures and institutions of the global economy’. As such, the approach puts more emphasis on the social and institutional context that shapes global production (Barrientos, 2013). In practice, however, it is unclear whether this framework has resulted in research that is qualitatively different from GCC/GVC research (Selwyn, 2013).

Scholars working in all three traditions have seldom asked when and why lead firms change their competitive strategies – nor have they investigated the full range of actors and forces that shape inter-firm competition. There are some important exceptions. There is a small body of literature that examines how chains are articulated within the broader institutional framework, exploring regulatory factors, such as trade policy or international commodity agreements, and examining how these factors affect lead firms and the organization of GCCs (Gereffi et al., 2005; Gibbon, 2002; Haakonnsson, 2009; Ponte, 2002; Talbot, 1997). Additionally, scholars such as Palpacuer (2008) and Gibbon and Ponte (2005) have studied external economic forces, such as the rise of the shareholder value doctrine and financial market pressures, and how these have shaped sourcing decisions of lead firms.

An emerging scholarship is beginning to investigate the role of collective agents (primarily labour and consumer movements) in GVC analysis. In a recent article, Schurman and Munro (2009) drew on GCC analysis to explain the different outcomes of anti-GMO movements in Britain and the United States. They analyzed how the structure and geography of commodity chains creates specific opportunities and constraints for social movements, with implications for success. Selwyn (2007, 2012, 2013) researched horticultural production in impoverished northeast Brazil and brought together GCC studies and class analysis to make the case for how rural trade unions can use knowledge of their strategic position in the global supply chain to extract concessions from capital and promote regional development. Barrientos (2008, 2013) examined the extent to which civil society organizations can use knowledge of GPNs to campaign for worker’s rights, investigating why some firms have been more responsive than others, what difference tactics make, and how a better understanding of lead firm competitive pressures can illuminate some of the unanticipated failures of campaigns. While all of these studies seek to incorporate social movements into GCC/GVC/GPN analysis, they focus primarily on successes and failures of campaigns rather than the multiple and indirect ways that movements may shape industry strategy. The next section looks at the global tobacco commodity chain.

The Global Tobacco Commodity Chain

Structure of the tobacco commodity chain

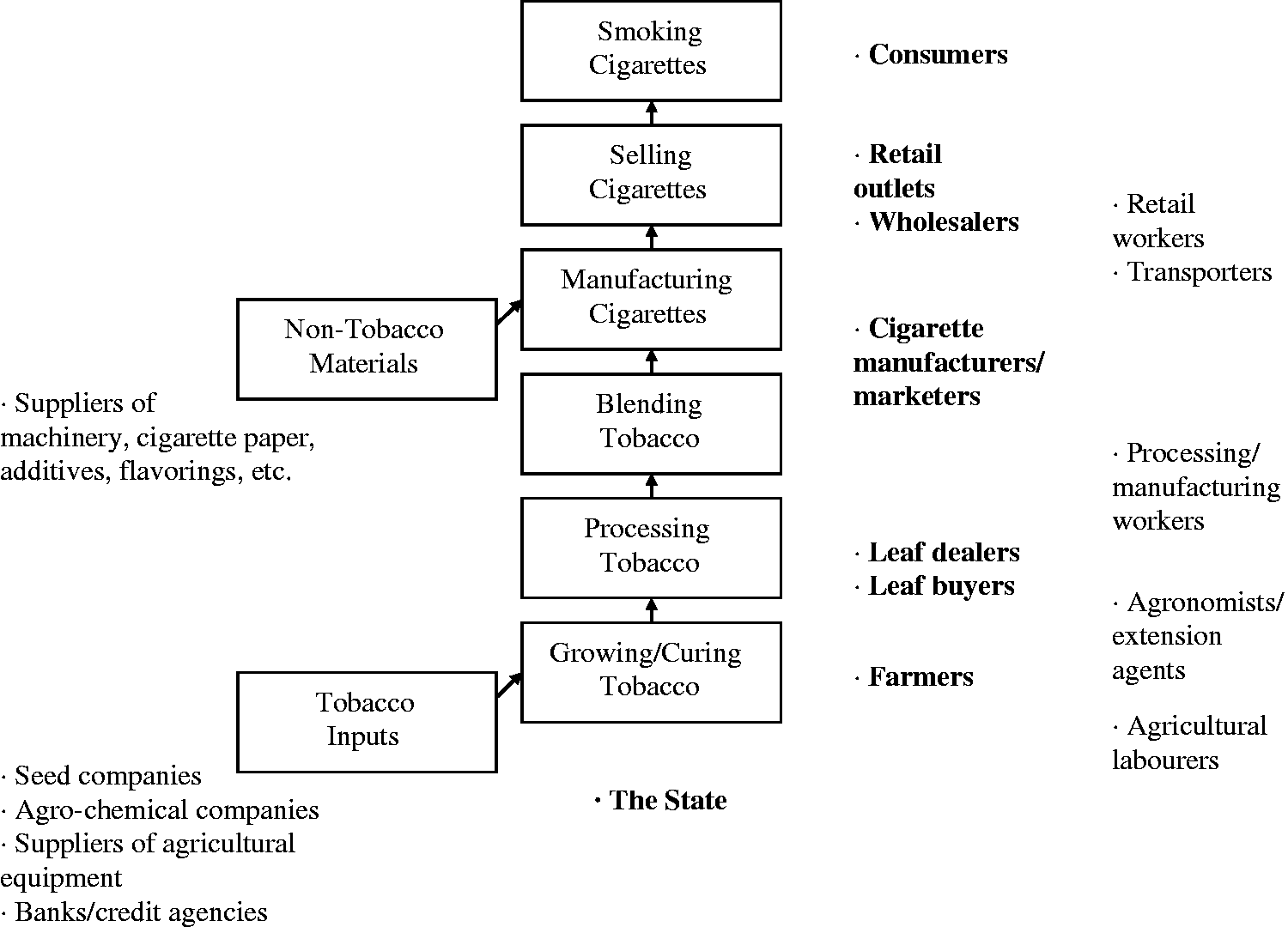

The tobacco commodity chain is simple in comparison with most manufacturing chains. As can be seen in Figure 1, it has relatively few nodes. The main actors are farmers, leaf buyers and dealers, cigarette manufacturers, distributors and retailers, consumers, and the state. Cigarette manufacturers occupy the most important position in the chain. As the lead firms, they have the power to influence the behaviour of leaf merchants, processors, buyers and growers. These governing agents also have influence over retailers, governments and consumers. Using Gereffi’s terminology, the chain is ‘driven’ by this segment of the chain.

The tobacco commodity chain.

Worldwide, the cigarette-manufacturing sector is comprised of large multi-national corporations, state-owned monopolies, and smaller, independent manufacturers. The industry is highly consolidated and there are only four major private players: Altria/Philip Morris (PM), British American Tobacco (BAT), Japan Tobacco (JT) and Imperial Tobacco (in order of profits). There are also 16 state-owned companies, including the China Tobacco Monopoly. Because most of the state-owned monopolies focus on their domestic markets, this analysis is restricted to an investigation of the private sector, with a focus on the internal planning documents of Phillip Morris and British American Tobacco.

The modern tobacco control movement

The tobacco control movement is best characterized as a pressure group. Wolfson (2001) argues that the movement for tobacco control does share a number of characteristics with other social movements, specifically: (a) efforts are aimed at social and political change above and beyond persuading individuals to alter their behaviour; (b) proponents consider themselves part of a movement and (c) advocacy organizations are crucial players. However, it is a unique movement in that it has particularly strong ties to both the state and health organizations and professionals. Thus, it is arguably most accurate to label it as a pressure group.

The tobacco control movement is made up of a diversity of actors and institutions, including local public health agencies, federal agencies, professional health organizations, non-profits, litigation lawyers and state attorneys general. The stated goal of the movement, as expressed in the Institute of Medicine report (2007: 1), is to ‘end the tobacco problem; in other words, to reduce smoking so substantially that it is no longer a significant public health problem for our nation’. The modern tobacco control movement began during the 1950s, but took many years to build the economic, political and moral capital that defines it today.

Inter-firm competition and the tobacco control movement

This section of the article describes the three periods of inter-firm competition (1960–1979, 1980–1994 and 1995 to present), highlighting the role of the tobacco control movement in influencing lead firm strategies.

Period 1: 1960 to 1979

From 1960 to 1979, the tobacco control movement had little impact on inter-firm competition. This first wave of movement activities focused on disseminating emerging scientific evidence about the dangers of smoking (Jones, 1997). Smoking was a mainstream cultural practice, and the movement sought to inform smokers about the deleterious health effects. They also pressed government to regulate the industry.

The state responded to these early demands in industry friendly ways. In 1964, the Surgeon General issued a report based on three epidemiological studies that revealed a connection between smoking and lung cancer, heart disease and emphysema. Although the public was alarmed, the policy response was minimal. Congress passed the Cigarette Labeling and Advertising Act of 1965, which required health warnings on cigarette boxes. In 1967, the FCC required free airtime for anti-smoking announcements commensurate to cigarette advertising. Four years later, Congress banned cigarette advertising on radio and television, which also ended the anti-smoking announcements. Excise taxes increased modestly, which did not introduce major shocks to the industry.

Despite the movement’s success in warning consumers, prospects for growth in the US-based cigarette sector remained favourable. According to industry documents, early efforts of the tobacco control movement, including the regulatory actions of the US government, posed little threat to overall sales (PM USA, 1971). Although the percentage of Americans who smoked began a downward slide after the release of the US Surgeon General’s report, per capita consumption continued to climb. Population trends also worked to the industry’s favour as the key 21–54 age range group grew (PM USA, 1971). Total US cigarette consumption thus increased from 484 billion cigarettes in 1960 to a high of 635 billion in 1980 (‘Cigarette’, n.d.).

During this period, competition among manufacturers was not based on price. As many have noted, the cigarette industry … has long been one of America’s most profitable, in part because for many years there was no significant price competition among the rival firms … List prices for cigarettes increased in lock-step twice a year, for a number of years, irrespective of the rate of inflation, changes in the cost of production, or shifts in consumer demand. (Brooke Group, Ltd. v. Brown & Williamson Tobacco Corp., 509 U.S. 209, 213 (1993) as quoted in the Federal Trade Commission (FTC, 1997: iii-iv) staff report to Congress)

Consistent pricing was a hallmark of industry strategy during this time period. In planning documents, PM USA (1971) observed that government intervention actually supported their strategy of high prices: ‘Even the tax increases have their bright side in that they are continually re-demonstrating to the companies' managements that the public will pay more for cigarettes if they are required to do so’. Thus when raw material prices increased (as they did during this period), manufacturers could make up for it by increasing prices. This reduced pressure to drive down costs of production, although firms did try to minimize costs through technologies such as increased leaf utilization (PM USA, 1971).

In this environment, cigarette manufacturers grew market share through branding and subtle improvements to existing products. Cigarettes were differentiated into market segments based on characteristics such as full-flavour, menthol or low-tar. Through market research, manufacturers developed an understanding of the preferred product characteristics of target groups of consumers and tweaked product lines accordingly. To differentiate products from their competitors, the industry relied on branding. Firms sought to create a unique image associated with each brand and increased brand exposure through advertising campaigns, event sponsorship and product placement. Because, according to PM USA (1971), the cigarette industry had ‘the highest degree of brand loyalty in the whole consumer goods field’, branding became the key to company growth.

Finally, during this period, cigarette manufacturers tacitly agreed not to compete on the basis of the ‘safety’ or ‘health’ attributes of their products. In the previous decades, firms had experimented with this kind of competition. In the 1940s and 1950s, some companies tried to compete based on ‘fear advertising’ and radical product innovations aimed to reduce harm. This early search for a ‘safer cigarette’ resulted in the introduction of filter-tip cigarettes in 1953–1955 and the ‘tar derby’ of the late 1950s, leading to a 40% drop in nicotine and ‘tar’ levels between 1957 and 1959.

Calfee (1986), former staff economist at the FTC, describes the development of ‘fear advertising’ that accompanied these new products, noting ‘companies sought to gain business by scaring smokers about competitors’ brands’ (39). However, these activities damaged the entire industry; cigarette sales dropped with the constant reference to the dangers of smoking. The major industry players reacted by forging a tacit agreement to avoid competing based on health claims – an understanding that became more important as the industry faced mounting legal challenges. More subtle mentions of tar and nicotine or claims of ‘safer’ filters were then completely shut down in 1959 when the FTC negotiated a voluntary, industry-wide ban on claims without epidemiological evidence.

Thus, during the 1960 to 1980 period, product development focused on relatively minor improvements to existing technologies rather than more radical innovations to alleviate consumer fears. Advertising campaigns were ‘upbeat’, focusing on pleasure, taste and flavour. Rival firms competed by trying to attract consumers with unique brands and industry profits grew for all the major players in the context of expanding markets and steady price increases.

Period 2: 1980 to 1994

By the early 1980s, the tide had turned and the tobacco control movement was having a large and unanticipated effect on cigarette sales. What made the difference was the re-framing of the public debate. Instead of focusing on how dangerous cigarettes were for smokers, the movement pointed to the dangers of second-hand smoke for children and non-smokers. A Roper (1978) report prepared for the Tobacco Institute (the lobbying and public relations arm of the industry) noted that the non-smokers’ rights movement ‘is the most dangerous development to the viability of the tobacco industry that has yet occurred’. Private businesses began to restrict smoking in the workplace, Congress banned smoking in certain locations, federal excise taxes increased sharply, and states and local governments began to regulate and tax tobacco products. Additionally, lawsuits continued to challenge the industry, although manufacturers leveraged their substantial reserves to ‘cast doubt about the health charge’ and continued to win these cases, avoiding all damages throughout this period.

As a result of these changes and the decreasing social acceptability of smoking, sales declined faster than expected. Cigarette manufacturers faced a more challenging environment in which to secure profits, and their concern was reflected in company documents. Hamerton (1984) described the current ‘environment’ that BAT faced: Public pressure will continue to force a decline in total market unless concerns related to passive smoking, fire safety, and the smoker’s own convictions about his/her smoking are alleviated. Furthermore, additional taxation at state/local level will continue to erode the market.

The issue that each firm faced was how to secure profits in a mature and declining market (driven, in no small part, by rising consumer condemnation of smoking). BAT executives mapped two possible directions (‘assumptions’) for how growth might proceed in this challenging environment. First assumption: Major industry leaders offer no products that meet concerns mentioned in item #1 (Environment – quoted above). In that case, we will have a steadily declining, cost-driven market. Those that can produce the lowest-priced, acceptable product will win. Alternative assumption: Major industry leaders offer products that meet public/consumer concerns (see I. Environment). This scenario could lead to both cigarette and chewing products that return social acceptability for tobacco products. (Hamerton, 1984)

Thus, tobacco companies hoped to extend the life of the industry through a technological fix that would address the social and health concerns of consumers. On Philip Morris’ product development agenda, and backed by ‘considerable commitments’ were: ‘lowered biological activity’ cigarettes, ‘reduced nitrosamine cigarettes’ and cigarettes that ‘lowered the visibility or aroma of sidestream smoke’ (see PM USA, 1987, 1991a). However, efforts at creating an alternative smoking device faced significant challenges.

One of the main problems was the existence of a gentleman’s agreement not to compete on the basis of the safety of products. Through the 1990s, the main legal defence of the tobacco industry was their denial of the link between smoking and disease. The industry faced a ‘Catch 22’: if they threw their weight behind the search for a ‘safer cigarette’, they would be implying that the rest of their products were not safe, thus exposing themselves to increased liability. As Sheehy, the former chief executive of BAT, wrote in 1986, In attempting to develop a ‘safe’ cigarette you are, by implication, in danger of being interpreted as accepting the current product is unsafe, and this is not a position that I think we should take. (as quoted in Parker-Pope, 2001)

Lacking substantial innovation, the competitive market of the 1980s and 1990s was refashioned into a ‘cost-driven’ market that relied heavily on the discount sectors. The threat of volume reductions led firms to aggressively seek market share. Responding to the rise in real cigarette prices, Liggetts introduced a generic, discount product to draw consumers away from competitors, thus setting off the industry’s first wave of price competition. RJ Reynolds followed suit with a branded discount cigarette. Liggetts then introduced another category of discounted cigarettes, the deep-discount brands (FTC, 1997). According to PM USA (1991a): These competitive moves radically changed industry pricing and related profitability, creating a permanent discount cigarette segment with lower margins known as price/value that threatens to turn cigarettes into a commodity with little real or perceived differentiation.

The new price-driven market put pressure on firms to drive down costs and increase productivity. Cost-efficiency was the word of the day. Consider this excerpt from PM USA’s (1992) five-year operations plan: Although PM USA’s total production volume has been increasing, the growth in the lower margin price/value and generic segments domestically is creating increasing pressure on both earnings and cash flow … To counter this, we must continue to aggressively develop ways to lower the costs of production in order to meet PM USA’s income and cash flow growth targets.

Pursuing a low-cost, high-value product strategy was a substantial challenge, but globalization and economic liberalization of the 1980s and 90s brought new opportunities to do so – by opening doors to expand into foreign markets with high growth rates. The major tobacco companies worked to establish a presence in Europe and Asia through exports and building manufacturing capacity abroad. With trade liberalization and reduced barriers to foreign investment, tobacco companies gained flexibility in determining where to concentrate production and which consumer markets to target.

Period 3: 1995 to Present

By the mid-1990s, the tobacco control movement gained influence, as cigarette manufacturers lost credibility and the state radically reshaped the rules of competition and growth. All branches and levels of the US government stepped up involvement in the ‘tobacco issue’ through increased taxation, regulation and litigation. The Federal Drug Administration (FDA) attempted to assert jurisdiction over cigarettes, the state Attorneys General brought suits that led to the Master Settlement Agreement, and smoking restrictions and cigarette excise taxes rose exponentially. Also starting in 1995 was a ‘third wave of litigation’. Courts began to rule against the industry, resulting in substantial liability threats, payouts and new restrictions on corporate activity. These interrelated events resulted in cigarette manufacturers paying tremendous legal expenses and settlement costs, admitting that smoking was dangerous, and contending with negative public opinion, advertising restrictions, and further declines in cigarette consumption. The changes of this period culminated with FDA regulation of tobacco products in 2009.

Arguably, the turning point was the appointment of Kessler in the early 1990s as FDA Commissioner. The FDA is charged with protecting consumer health by assuring the safety of drugs, cosmetics, medical products and the food supply. While the FDA had oversight over quit-smoking aids such as nicotine gum, cigarettes were excluded from their jurisdiction because they were not considered a drug. Hoping to change this, Kessler proposed regulating tobacco products as ‘nicotine delivery devices’ in 1994. FDA scientists and lawyers then embarked upon a massive investigative campaign, reviewing corporate documents, scientific reports and transcripts of government debates.

Through their investigation, the team discovered scientific evidence of the addictive properties of nicotine. Their report also revealed the extent to which tobacco companies understood this and manipulated nicotine content to their advantage. Finally, the team found that cigarette manufacturers consciously targeted youth under the age of 18 to boost sales and ‘hook’ a new generation of consumers.

Up to this point, no tobacco company had admitted that tobacco was addictive or that it caused cancer. They also explicitly denied marketing to youth. Industry representatives followed a carefully worded script crafted by the most prestigious law firms in the country. But as the FDA released statements of industry insiders and secret litigation documents were leaked to the media, it became increasingly difficult for the industry to suppress information, and public sentiment turned against Big Tobacco. Polls conducted by PM in 2000 found that only 32% of the US population responded ‘strongly’ or ‘somewhat’ favourably to the industry (PM USA, 2000).

On top of this, activists and public health officials were waging war against tobacco at the local level, where industry influence was weaker. Smoking bans increased exponentially. In 1985, 90 US communities had ordinances restricting smoking in public places. By 2008, 2216 communities had them. States and municipalities also began to balance their budgets by increasing excise taxes (National Conference of State Legislatures, 2010). In addition, the federal government raised excise taxes from 24 cents a pack to 34 cents in 2000 and to $1 a pack in 2010.

This time period also marked a shift in the litigation environment for tobacco companies. Frustrated by limited legislative intervention, crusaders turned to the courts. Before 1994, the industry had never paid out damages. They were committed to fighting every battle to the bitter end – no matter what the cost, which discouraged individuals and groups from bringing suit. When a challenge did make it to court, the industry relied on a two-pronged argument: first, that there was not sufficient evidence that smoking causes cancer; and second, that individual were responsible for their own consumption choices (Luik, 2006). But the potency of this argument changed in the 1990s, as new evidence was uncovered and popular disapproval mounted. The courts began to rule against the industry and manufacturers faced new lawsuits and enormous fines.

One of the most important cases heard as part of this ‘third wave’ of legislation was brought against the industry by the state itself (see van Liemt, 2002: 19; Ciresi et al., 1999). In 1994, the Attorney General of Mississippi brought a lawsuit against the major tobacco companies to recoup health care costs. They argued the government was entitled to compensation for public funds spent on persons who got sick from smoking. They pointed to the joint federal-state Medicaid program that cost the state approximately $1 billion in 1993 (Derthick, 2005). Encouraged by lawyers and crusaders and a growing sense that the case could be won, other states followed suit.

In 1998, the Attorneys General of 46 states and 5 territories reached the largest civil settlement in US history with the four largest tobacco manufacturers. Under the Master Settlement Agreement (MSA), the companies agreed to pay an estimated $206 billion over 25 years (Derthick, 2005). As part of the agreement, the industry was stripped of its trade organizations, including the arms responsible for pro-tobacco research, public relations, media promotion and lobbying. They publicly admitted that cigarettes are addictive and cause cancer. In this difficult environment, cigarette manufacturers faced a ‘fragile’ outlook for sustainable profit growth (BAT, 1999).

From 1995 to the present, a new competitive dynamic defined the industry: product competition based on the search for a ‘safer’ cigarette or substitute. When the tobacco companies were forced to admit that smoking was deadly, their existing gentleman’s agreement not to bring attention to the health hazards of cigarettes no longer held force. The companies were now condemned for not having devoted enough resources to producing a ‘safer’ or completely ‘safe’ cigarette product. The incentives structure changed and encouraged real product competition.

For companies looking to survive in a declining global market, product competition was the way to go. Firms ramped up investments in research and product development in the race to create a ‘safer’ tobacco product. In the words of BAT (1999), ‘There is a real need to accelerate BAT’s efforts to develop radically new products, both as a competitive response and to develop competitive advantage’. The websites of top global cigarette manufacturers all recognized that ‘there is no such thing as a “safe” cigarette’, and yet they are doing ‘everything they can’ to develop products that may be less harmful. In 2006, Szymanczyk, CEO of PM USA, addressed the Prudential Consumer Conference and explained that, An important area of focus for PM USA has been developing products that have the potential to reduce smokers’ exposure to harmful compounds and, ultimately, to reduce the harm caused by smoking…The fact that we are in a declining industry and have limits on our ability to grow cigarette revenue means that, as we look to the future, we need to find new ways to grow by expanding beyond our core business to other tobacco and tobacco-related adjacent categories. (as quoted in ‘PM USA focusing on reducing risk’, 2006: 5)

Despite the increase in research and new commitments, one obstacle still stood in the way, which was that there were no standards for a ‘safer’ product, nor mechanisms in place to assess product innovations and specify how firms could communicate product attributes. There was still no agency responsible for regulating tobacco products (while the FDA attempted to assert jurisdiction back in 1994, these efforts failed). As tobacco analyst Gay (2007: 38) explained, At the moment, you get the feeling that O’Reilly and his fellow scientists at BAT – and presumably scientists at other cigarette manufacturers – are like darts players who have been given a board to aim at, but a board without numbers on it.

With the support of PM and certain sectors of the public health community, various bills were introduced, but it was not until 2009 that the industry came under the regulatory authority of the FDA. The Family Smoking Prevention and Tobacco Control Act was signed on 22 June 2009. This law imposes strict controls on the making and marketing of tobacco products. It gives the FDA power to reduce nicotine yields, regulate other components of cigarettes, mandate design changes on tobacco products and set guidelines for appropriate communication with smokers (Wilson, 2009). The FDA is now the first regulatory body in the world responsible for overseeing the development of potentially reduced exposure products. The development makes it easier for manufacturers to market reduced-harm tobacco products and communicate a clear health message.

Cigarette manufacturers currently face a global tobacco control movement that has contributed significantly to the decline of the market in addition to creating a web of unexpected challenges and risks. To grow and survive in such an environment, tobacco companies continue to drive down costs and capture market share by adding value to their current line-up of branded products. Companies seek to avoid price-competition and focus instead on consistent price increases and growing new markets (particularly in the third world), a strategy that has been only partially successful in the context of intense competition. However, the real future of the industry depends on the development of a consumer-acceptable, ‘safer’ product, which has introduced a crucial new competitive dynamic into the market.

Conclusion

This article builds on insights from the GCC/GVC/GPN literature, describing how the bases for competition among lead firms in the cigarette manufacturing industry shifted over the last half century. There were three distinct periods of competitive activity. From 1960 to 1979, industry profit margins depended primarily on expanding cigarette sales in the first world through careful branding, marketing and tweaking of products in different industry categories. Consistent pricing was absolutely critical for profits at this time; there was little competition based on price or radical product innovation. During the 1980–1995 period, however, cigarette manufacturers faced a rapidly declining market and price-competition broke out, resulting in falling profits. During 1995 to the present period, the rules of the game changed yet again. Product competition based on the principle of ‘harm reduction’ became a central defining feature of corporate strategy during this period.

This article also analyzes the impacts of the tobacco control movement, an important component of the institutional context around this GVC, and it argues that the strategies and successes of this pressure group played a critical role in spurring the development of new corporate strategies and reshaping the terrain of inter-firm competition in each of these periods. In other words, the tobacco control movement created external openings and closures that triggered changes in industry strategy. That said, the specific way the social movement impinged upon the market and elicited such responses varied across the time periods.

In the early 1980s, the anti-smoking movement influenced the market directly by changing consumption patterns and demands. They did this by re-framing the public debate around the dangers of ‘secondhand smoke’. This argument was more compelling to the general public as well as to regulators, which resulted in a proliferation of smoking restrictions, excise tax hikes, and a newfound stigma associated with smoking. As a result, cigarette consumption plummeted. In a mature and declining market, competition increased. Manufacturers preferred to seek a technological fix to the problem and develop a new product that would assuage consumer fears. However, competing based on health or safety attributes would have opened the industry up to increased liability. Spurred on by the tobacco control movement, Big Tobacco faced hundreds of lawsuits and their defence rested on casting doubt on the scientific evidence linking smoking to cancer. Marketing ‘safer’ products was effectively admitting that smoking was dangerous. Consequently, given no other choice, the market was refashioned into a cost-driven market as manufacturers began to compete based on price.

Then, in the mid-1990s, the tobacco control movement influenced the market indirectly by forcing major industry concessions that ultimately required Big Tobacco to admit they were at best being economical with the truth, thus eliminating a major obstacle for quality-based competition. First, it was the FDA that launched a major investigative campaign into the industry and amassed a large amount of evidence showing that the tobacco companies knew that smoking was dangerous and nicotine was addictive, and that they actively misled the public. As the media publicized these and other reports of wrongdoing, public opinion hit an all-time low. At the same time, the industry began to lose in court and faced billions in damage awards. Smoking bans mushroomed and excise taxes continued to shock the industry. Cornered from all sides, the industry was eventually forced to admit their misconduct. Recovering from this hostile environment was very difficult, but it did create a new opening. Now that Big Tobacco had admitted that cigarettes were dangerous, they were free to address consumer concerns and compete based on radical product innovations. Thus began the race for a reduced-risk product in a new era of competitive activity.

Although it is beyond the scope of this article to discuss all the supply chain implications of these historical shifts in inter-firm competition, it is nonetheless instructive to consider a few of the most noteworthy consequences (more detail can be found in Breazeale, 2010). For example, in the 1980s and early 1990s, when the market was refashioned into a cost-driven market and cigarette manufacturers began to compete based on price, this led to industry-wide obsession with cost reductions. As stated in corporate documents, the relatively high price of tobacco leaf in many subsidized first world markets began to be of serious concern for the first time, propelling firms to build production capacity and the quality of leaf in both new and old supplier regions in the third world, resulting in a shift in global production from the developed to the developing world and a rise in contract farming arrangements.

Similarly, the shift in competitive dynamic during this last period has profound implications for supply chain actors. The newfound commitment to ‘harm reduction’ and a ‘safer smoke’ means that firms are seeking to control a wide array of new ‘quality’ concerns throughout the entire supply chain. For example, as emerging studies showed a possible link between tobacco-specific nitrosamines (TSNAs) and lung cancer, firms tried to reduce the level of TSNAs in the tobacco. Companies required tobacco producers to retrofit their curing barns and to use new low-converter seed varieties. These new seed varieties produce a lighter, more delicate tobacco that is easily damaged by poor weather, increasing the risks of crop loss. In this competitive environment, manufacturers impose private, company-specific ‘quality’ standards down their supply chains, forcing suppliers to adjust, as each aspect of the production process becomes a variable to control. Thus, in the current era, firms are not just seeking cheap, high quality raw materials (in the traditional sense of tobacco ‘quality’, that is) – but rather they manage a complex web of additional process and product characteristics essential to marketing the new ‘safer’ tobacco products. The result is greater vertical integration of the supply chain and rigid new private quality standards.

The historical case of competition among cigarette manufacturers reveals the importance of including pressure groups in the study of chain governance – particularly global health movements and environmental movements that may have direct and indirect effects on GVCs beyond specific targeted campaigns. While this article emphasizes how the tobacco control movement shaped the competitive dynamic among lead firms, it is important to note that the process is interactive. As cigarette manufacturers responded to the changing social and institutional context brought on by the tobacco control movement, their strategies in turn altered the framework within which the movement operated. For example, once the tobacco corporations had publicly admitted the dangers of smoking, Phillip Morris split from the pack and joined the movement in lobbying for FDA regulation. Activists disagreed on whether or not they should join forces with their ‘enemy’ and worried that regulations would be watered down under the influence of this corporate giant.

Considering the lessons for the tobacco control movement, this article argues that a historical analysis of GVC governance can provide important insights to guide future activities. Most important is the recognition that collective action can affect more than just public health. The tobacco control movement is often heralded as one of the most successful movements of our time, having ‘beat’ Big Tobacco at their game. Although cigarette manufacturers have adjusted their competitive strategies in response, given their dominant position in the GVC, they have been able to reorganize their supply chains and offload much of the burden and risk to actors down the line, creating new struggles for tobacco farming communities around the globe (Benson, 2011; Kingsolver, 2011; Otañez and Graen, 2014). It is for this reason that we find poor farmers in Argentina trying to choose between using their valuable household labour to grow a garden or walk through their tobacco field yet again to hand apply additional rounds of expensive, ineffective pesticide that leave little detectable chemical residue on these new, vulnerable varieties of burley tobacco. Big Tobacco would not be able to produce the new products that health standards demand without these farmers and the other supply chain actors they control and coordinate. Thus, social movements need to consider the global public health question in tandem with the economic development question; the links between these issues are made clear through GCC analysis. Tobacco control activists could align forces with farmer organizations that represent these growers (not to mention trade unions that represent those who work the line in leaf processing and cigarette manufacturing) to help them transition out of tobacco or, at the very least, to strengthen their relative position in the chain.

Footnotes

Acknowledgements

The author wishes to thank Jane Collins, Amy Quark, Doug Clayton-Smith and Phillip Johnson for their assistance and support.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the World Affairs and the Global Economy (WAGE) Fellowship at the University of Wisconsin-Madison.