Abstract

In the period following the Great Recession of 2007–2009 the financialization of the US economy reached a watershed characterized by stagnant financial profits, falling proportions of financial sector and mortgage debt, and rising proportion of public debt. The main macroeconomic indicators of financialization in the USA show structural breaks that can be dated around the period of the Great Recession. The reliance of households on the formal financial system appears to have weakened for the first time since the early 1980s. The financial sector has lacked the dynamism of the previous three decades, becoming more reliant on government. The state has increased its own indebtedness and supported large financial institutions via unconventional monetary policy measures. At the same time, state intervention has tightened the regulatory framework for big banks. The future path of financialization in the USA will depend heavily on government policy with regard to state debt and financial regulation, although the scope for boosting financialization is narrow.

Introduction

The financial sector in the USA has tended to expand in the post-war era, despite numerous economic crises. The march of finance seemed relentless during the last four decades, giving rise to the concept of financialization. The implications of this development for the economy and for wage workers have been pronounced in terms of value extraction, indebtedness and the unprecedented penetration of finance into personal and household life.

However, the period following the Great Recession of 2007–2009 has been distinctly different in the USA. For one thing, economic growth has been weak. For another, the financial sector has recovered from the shock of the crisis but its performance in terms of trading, lending and profits has also been weak compared to other periods of recovery in the last four decades. Furthermore, the exposure of households to formal finance has not advanced with nearly similar vigour.

Three aspects of the economic performance of the USA stand out in this regard. First, financial profits, as shown by several indicators, have not resumed their upward trend since the crisis. US banks have operated in an environment of sustained pressures on profitability during the last decade. Second, the volume of mortgage debt relative to disposable personal income has declined substantially for the first time since the 1980s, a development with potentially significant implications for the financial system. Third, the US government has provided support to financial institutions by lowering nominal interest rates in the vicinity of zero and implementing unconventional policy measures, while supplying abundant liquidity to banks. The outcome has been a substantial expansion of state indebtedness which has roughly cancelled out the decline in household indebtedness. At the same time, the US state has constrained the activities of financial institutions through new regulations.

Taken together, these developments point to a halt in the march of financialization in the USA. On the evidence available so far, financialization has reached a watershed and its future path will depend on government policies. It is conceivable that, if financial deregulation received a new boost, a fresh acceleration of financialization could occur, in view especially of the expansion of state debt since 2007–2009. However, a very different possibility is also open. The US economy is likely to remain financialized, and the ability of the financial system to generate bubbles and financial crises will continue to mark its performance, but the high point of financialization might be behind us.

The rest of this paper comprises four sections. The next section reviews relevant bodies of work that emphasize different aspects of financialized capitalism. Then, the watershed in the financialization of the US economy after the great crisis of 2007–2009 is considered at the macroeconomic level by presenting data on the evolution of financial profits, indebtedness and the composition of aggregate debt. We corroborate the presence of statistically significant structural changes around the period of the Great Recession in the main indicators and discuss the results obtained. In light of this evidence, some relevant theoretical issues are explored with regard to the relationship between households and finance; followed by conclusions.

Main approaches to financialization

Financialization in the USA emerged in a fairly modest way at the end of the 1970s as the financial sector began to grow relative to the rest of the economy. Since the early 1980s the balance between the financial sector and the rest of the economy has shifted strongly in favour of the former, and did so with considerable vigour in the 1990s and 2000s. This is the context in which the concept of financialization has emerged in social sciences.

The literature on financialization is large and continually expanding. Using van der Zwan’s (2014) literature survey it is possible to identify three bodies of work that emphasize, respectively, the emergence of a new period of accumulation, the ascendancy of shareholder value and the financialization of everyday life. Although informed by different theories of capitalism, these approaches share a common concern for financialization as a structural transformation of contemporary capitalism.

The accumulation approach has been developed by a broad group of scholars – French Regulationists, Marxist and Post-Keynesian economists, economic sociologists and critical international political economists – who have emphasized the systemic aspects of financialization as a distinct historical phase in the development of capitalism. Krippner (2005: 174) pointed out that financialization represents ‘a pattern of accumulation in which profits accrue primarily through financial channels rather than through trade and commodity production’. The study of financial profits has also played a fundamental role in the Marxist approach developed by Lapavitsas (2009, 2011, 2013), who argued that the extraction of profits in financial markets but also from households includes a ‘direct’ component in contrast to the ‘indirect’ extraction of surplus value in production. This feature of profit extraction has been termed ‘financial expropriation’ and is explained in more detail at the end of this section. 1

Important in this respect is the ‘dual movement’ of non-financial corporations that have increasingly derived profits from financial activities while at the same time augmenting their payments to the financial sector as interest, dividends and share-buy-outs (Crotty, 2005). This ‘dual movement’ has created a constraint for non-financial corporations by limiting capital available for productive investment despite the increase in profits from financial activities. Financialization has thus contributed to a slowdown of accumulation since investment in tangible assets has suffered. It is important to note, however, that empirical evidence at the firm-level suggests that there have been variations according to firm size (Orhangazi, 2008). The interplay between ‘real’ and ‘financial’ processes with regard to investment is, thus, complex and contradictory (Lapavitsas, 2013; Orhangazi, 2011).

In this regard, some scholars have emphasized the role of ‘the rentier’ at the centre of an inherently unstable financial system (Epstein and Jayadev, 2005). The rising profits of the owners of loanable capital and of financial institutions have been the counterpart to weak investment, stagnant real wages and increased indebtedness by households. The presence of the rentier combined with high debt levels and low economic growth has increased the instability of the economy. 2

The literature on financialization as a period of accumulation has also emphasized the importance of government policies toward finance. Thus, Krippner (2012) and Lapavitsas (2013) argue that the US state has buttressed the ascendancy of finance through a sustained policy of financial deregulation, the first intimations of which could be observed already in the second half of the 1960s. The US state has also been pivotal to confronting the successive crises that have emerged in the course of financialization, above all, the great crisis of 2007–2009. The ability of the state to intervene in the sphere of finance has critically depended on its monopoly control over the final means of payment.

Further light on financialization has been cast by the literature on the rise of shareholder value as a characteristic feature of the modern corporation, especially in the USA. Shareholder value has become, first, a norm that provides justification for practices favouring shareholders over other constituents of the enterprise and, second, an ideological construct that legitimates a far-reaching redistribution of wealth and power among shareholders, managers and workers, at the expense of workers.

The seminal paper by Lazonick and O’Sullivan (2000) pointed out that financialization has fostered widespread belief in the economic benefits of maximizing shareholder value as the principle of corporate governance. The implications for the internal structure of corporations have been dramatic, as discussed by recent economic sociology. Thus, Thompson (2003, 2013) has emphasized that financialization has worsened the condition of labour at work as employers have not kept their side of the employment bargain. The ideology of shareholder value was stressed by Clark (2009) in explaining the further destabilization of labour relations through exposure to capital markets. Daguerre (2014) has noted that financialization has weakened labour by making employment more insecure, implying that the end of the full-employment compact is a consequence of the rise of financialization. More recently, Cushen and Thompson (2016) have returned to the ideology of shareholder value and have explicitly considered the intensification of value extraction from labour as corporations have become financialized.

Finally, the literature on the financialization of the everyday life has emphasized the diverse ways in which finance has spread across society through a range of projects and schemes aimed at incorporating low-income and middle-class households in financial markets – the ‘popular finance’ described by Aitken (2007). This process has several complex aspects, including increased household participation in pension plans (Waine, 2006), the spread of consumer credit (Montgomerie, 2006) and the rise of home mortgages (Aalbers, 2008, 2015; Fernandez and Aalbers, 2016; Langley, 2008). By participating in financial markets households and wage-earners have been encouraged to internalize new norms of risk-taking, increasingly turning toward financial markets for the provision of basic needs.

The analysis in this paper draws on the Marxist approach developed by Lapavitsas (2013), which treats financialization as a distinctive period in the development of capitalism lasting broadly four decades and characterized by the following three tendencies. First, large non-financial (productive) enterprises have less need to borrow from financial intermediaries since they command substantial amounts of liquid money capital, which they often deploy in financial transactions. This means that financialization has been marked by the relative detachment of industrial capitalists from banks. Second, financial intermediaries are less engaged in supporting investment by non-financial enterprises, instead trading in financial markets and transacting directly with households. Thus, financialization is also marked by the turn of banks toward profiting from transactions in financial markets rather than lending to productive enterprises. Finally, households and individual workers have been drawn heavily into the formal financial system both to borrow and to place available saving. The increasing implication of wage-workers and other social strata in the operations of the financial system providing further opportunities for profit extraction is another defining feature of financialization.

The trajectory of financialization in the USA since the outbreak of the Great Recession is examined in this paper by focusing on specific economic magnitudes. First, and of paramount importance is financial profit, since its extraction and accumulation effectively sum up the conduct of capitalists (industrial and finance-focused) that drive financialization. The tremendous growth of financial profit has marked the ascendancy of financialization. By this token, the broad direction of financialization in the USA since the Great Recession can be usefully surmised from the trajectory of financial profit.

Equally important are the fluctuations of aggregate debt in its various forms. Financialization amounts to the expansion of the financial sector relative to the productive sector, typically resulting in greater debt creation. Financialization has been undoubtedly marked by the growth of aggregate debt as well as by a shifting balance in its composition. On these grounds, insight into the direction of development of financialization in the USA since the Great Recession could be gained by considering the overall trajectory and the changing composition of aggregate debt.

Finally, financialization as a historical period has occurred within a social and political framework of laws, rules and policies by the state, and therefore its content can be expected to vary from country to country. In examining its trajectory in the USA it is vital to take the social and political framework into account, while being aware that there could be little generalization in this respect. The main purpose is to outline the broad confines of state policy toward finance, thus casting further light on the development of financialization in the USA since the Great Recession.

Financialization in the USA since the Great Recession

The crisis of 2007–2009 can be considered as the culmination of tendencies characteristic of the period of financialization. The crisis originally broke out in the US financial system following a huge real-estate bubble in the 2000s; the immediate trigger was the inability of the poorest layers of the US working class to meet mortgage debt obligations accumulated during the bubble; it spread to other financial systems as the international money market froze for lack of liquidity and became a global recession as trade and investment were affected by the collapse of credit. The crisis was subsequently dealt with through large-scale intervention by the US state, mainly by providing liquidity to banks through the Federal Reserve that has monopoly control over the final means of payment, but also through the injection of capital in banks out of tax income.

To assess the evolution of financialization in the USA since the crisis we present indicators from two fields. These are, first, the profits (or income share) of the financial sector and its main determinants; and, second, the accumulated debt of households, the financial sector and the non-financial corporate sector. 3 The empirical analysis tests for the presence of structural changes in the main indicators that can be dated approximately around the period of the Great Recession. To that effect we deployed the algorithm for simultaneous estimation of multiple breakpoints occurring at unknown dates developed by Bai and Perron (1998, 2003) and calculated the corresponding confidence intervals associated with the breakpoints following Zeileis and Kleiber (2005).

The procedures were implemented using a univariate regression model for each series, including a constant (a0) and a linear deterministic trend (t): yt = a0 + a1(t) + ut, where yt is the series under consideration, a1 is the coefficient on the linear trend, and ut is the error term. 4 In all cases, we tested for structural breaks both in the mean and trend of the series and accounted for potential serial correlation via non-parametric adjustments. 5 We also allowed up to five breaks, used a trimming percentage of 15% and made provision for error distribution heterogeneity across breaks.

The main results are presented in Table 1. All the selected indicators of financialization present structural breaks around 2007–2009 when the confidence intervals at the 95% confidence level are considered, the only exception being the two series that depict non-interest income (both shown in Figure 3). We interpret the presence of structural breaks estimated around the period of the Great Recession in the mean and trend of the series as evidence of a relative halt of financialization: the period before the Great Recession was characterized mainly by rising financial profits, rising debt of the financial sector and rising household and mortgage debt; in contrast, the period since the Great Recession has been characterized by stagnant financial profits, falling debt of the financial sector and falling household and mortgage debt. 6

Endogenous structural break tests.

GDP: Gross Domestic Product.

aBai and Perron’s (1998, 2003) algorithm, which estimates the optimal number of breakpoints by minimizing the residual sum of squares (RSS) of a regression model. The number of breakpoints were selected according to the Schwarz information criterion (BIC).

bThe last date of each regime.

cA description of the distribution function used to estimate the confidence intervals for the breakpoints can be found in Zeileis and Kleiber (2005).

dRegression model employed: yt = a0 + a1(t) + ut, where yt is the time-series under consideration, a0 is the intercept, t is a linear deterministic trend, a1 is the coefficient on the latter, and ut is the error term.

eRegression model employed: yt = a0 + a1(t) + a2(t2) + ut, where yt is the time-series under consideration, a0 is the intercept, t is a linear deterministic trend, a1 is the coefficient on the latter, t2 is a quadratic trend, a2 is the coefficient on the latter, and ut is the error term.

fIt was not possible to estimate these confidence intervals using the Zeileis and Kleiber (2005)’s procedure.

Stagnant financial profits

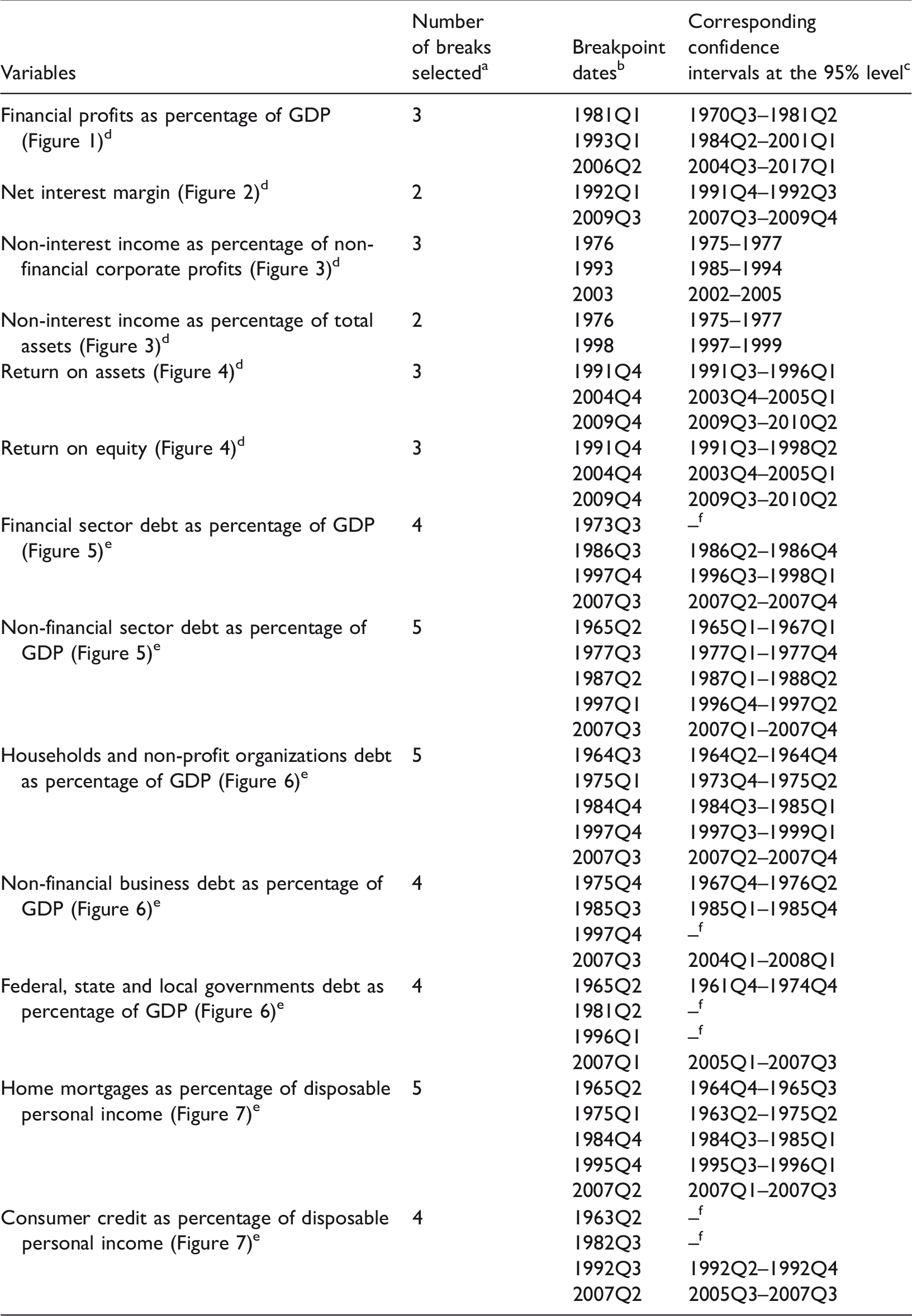

Figure 1 presents the trajectory of financial profits, that is, the profits of financial institutions relative to gross domestic product (GDP), for the entire period after the Second World War. 7

USA, 1948Q1–2017Q2 (quarterly data). Financial profits as percentage of GDP.

Financial profits in the US economy declined in the late 1970s and early 1980s, the time of the ‘Volcker Shock’, which led to turmoil in the financial system; but rose during the ensuing two decades. 8 After 2006, financial profits declined sharply and collapsed in the course of the crisis of 2007–2009. In 2009 financial profits bounced back but have not since attained the rising trend characteristic of the two decades following the Volcker Shock. As shown in Table 1, there is a statistically significant structural break in the financial profits series around 2004Q3–2017Q1. 9

To explain the historic trajectory of financial profits, two fundamental variables have been identified on the basis of previous work by Lapavitsas and Mendieta-Muñoz (2017). The first is the net interest margin (NIM), i.e. the difference between interest received and interest paid out by banks relative to their total interest-earning assets. The second is Non-Interest Income (NII), i.e. income deriving mostly from fees, commissions and proprietary trading. The empirical analysis shows that the former is the most important explanatory factor with regard to aggregate financial profits.

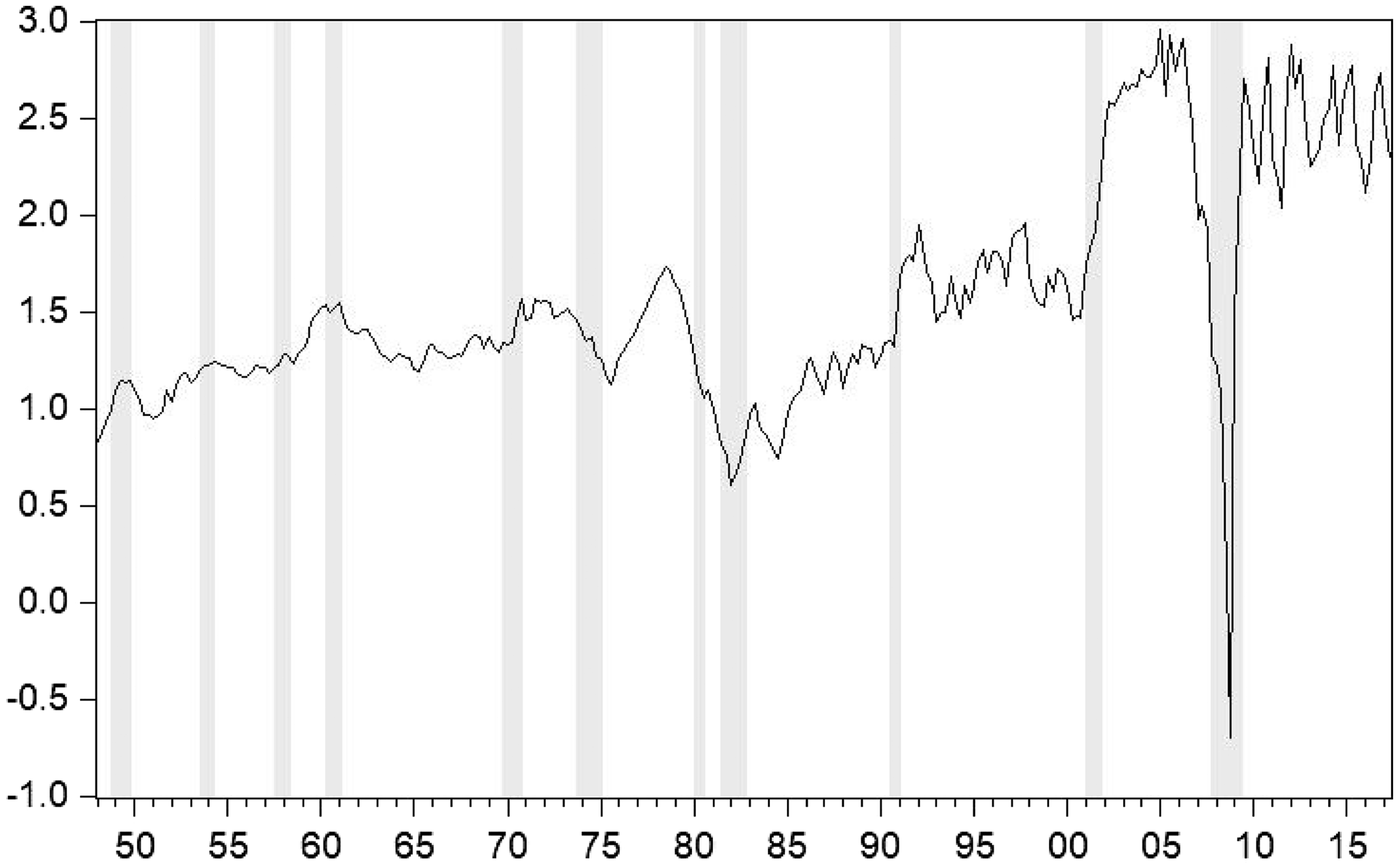

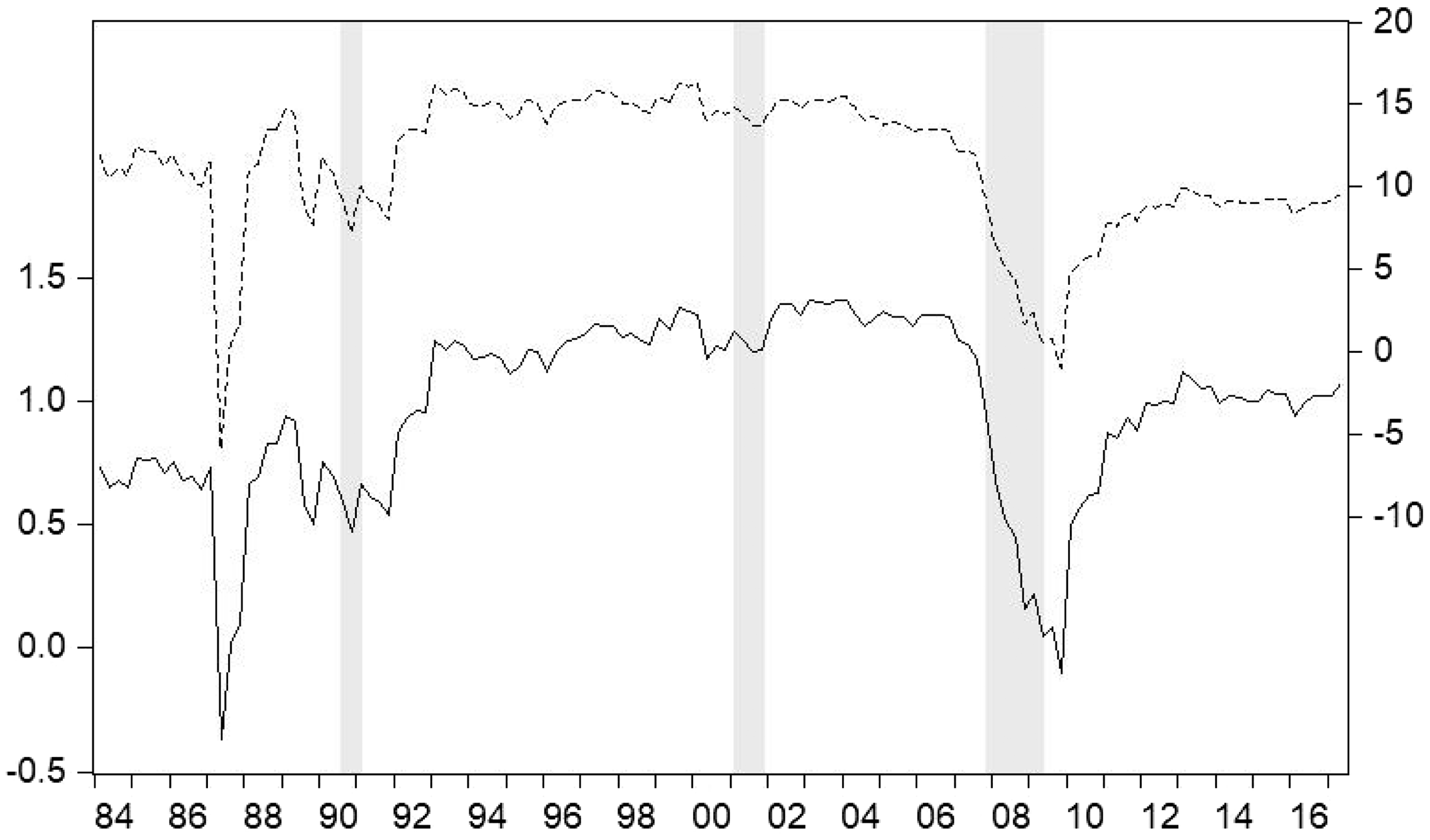

Figure 2 shows the NIM for all US banks. It is notable that the NIM has been in steady decline since the early 1990s, reaching very low levels as the crisis of 2007–2009 broke out. It bounced back strongly toward the end of the crisis as the borrowing rates of US banks were sharply reduced following government intervention, but has subsequently resumed its steady decline. As shown in Table 1, the NIM series presents a structural break around 2007Q3–2009Q4. In an environment of extremely low interest rates that has lasted for several years after the crisis, US banks appear to have faced difficulties in increasing the interest rate differential on their assets and liabilities to boost their profitability. The fall in NIM has negatively affected bank profitability.

USA, 1984Q1–2017Q2 (quarterly data). Net interest margin for all banks, in percentage.

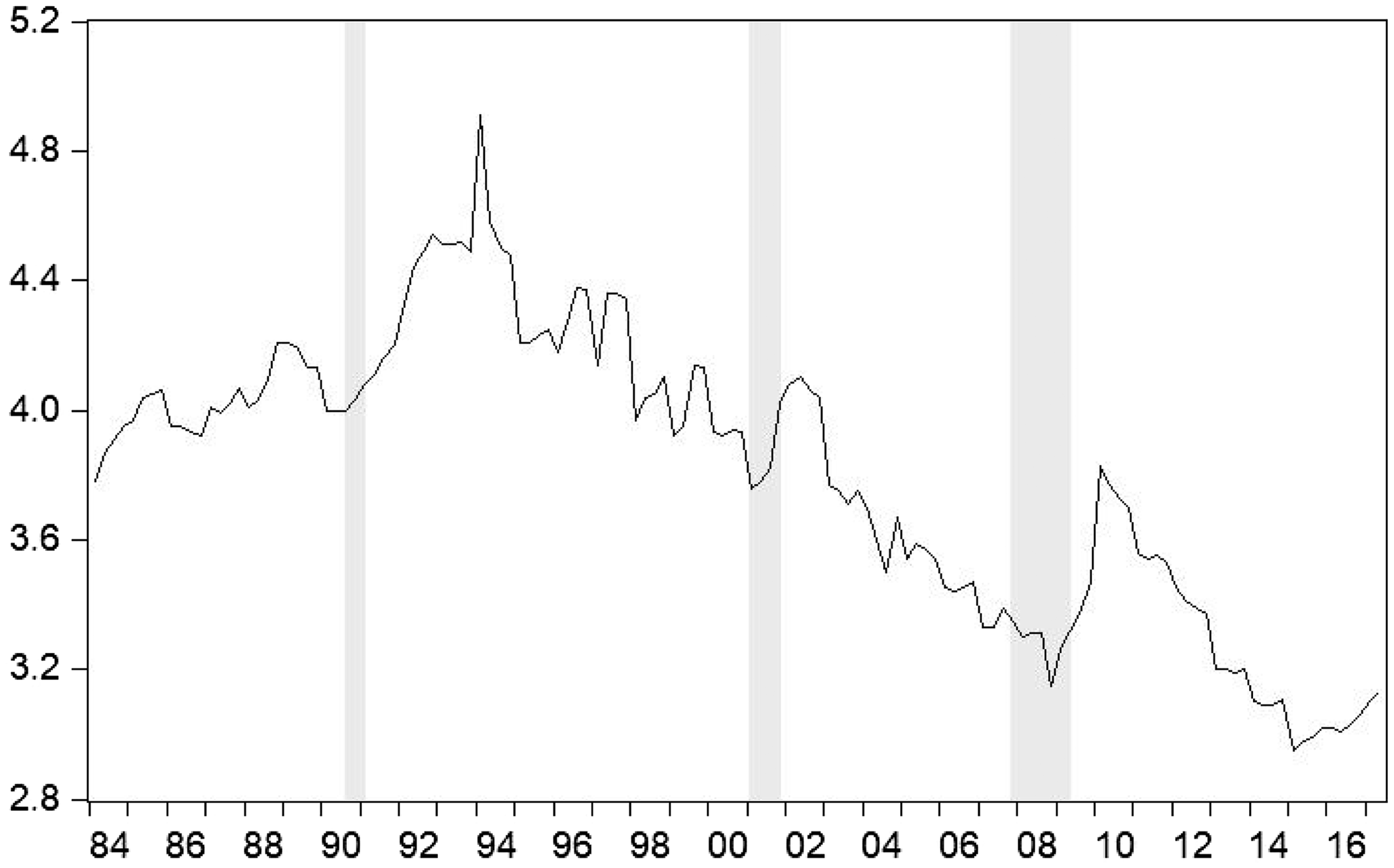

US banks have also faced difficulties in generating profits from NII since the Great Recession. These forms of bank income have been important to financialization, reflecting the deep transformation of banks during the last four decades. Note that the NIM has been declining since 1994; but financial profits were very high until 2007. This reflects the importance of NII during the period. However, as shown in Figure 3, in the conditions that have emerged since the Great Recession, the NII of US commercial banks has declined both as a percentage of total bank assets and as percentage of non-financial corporate profits. 10

USA, 1948–2016 (annual data). Non-interest income for all commercial banks as percentage of non-financial corporate profits (straight line, left axis) and as percentage of total assets for all commercial banks (dotted line, right axis).

The downward turn of the mortgage market in 2006-2007 also seems to have signalled the end of a period of sustained increases in NII for US banks. To be more precise, in the years preceding the Great Recession the ability of banks to extract non-interest profits was closely linked to the real-estate bubble and to securitizing and trading mortgage debt. In the aftermath of the Great Recession US banks have found it difficult to restore NII to a rising path. The structural break tests for the NII series shown in Table 1, however, detect the breakpoints before 2007, indicating that the downward trend of the NII component started before the Great Recession.

The difficulties that US financial institutions have faced with regard to profits since the Great Recession are also apparent in two alternative measures of financial profitability, i.e. the return on assets (ROA) and the return on equity (ROE), both presented in Figure 4. Data availability does not allow for accurate calculation prior to the 1980s; nonetheless it is clear that from the early 1990s to the mid-2000s the profitability of financial institutions was exceptionally high. The crisis brought a collapse of profitability, which bounced back in the early 2010s but has never attained the previous levels. The era of exceptional financial profits characteristic of the 1990s and 2000s came to an end after the Great Recession, as corroborated by the statistically significant breakpoints presented in Table 1 detected for both the ROA and ROE around 2009Q3–2010Q2.

USA, 1984Q1–2017Q2 (quarterly data). Return on average assets (straight line, left axis) and return on average equity (dotted line, right axis) for all banks, in percentage.

In sum, the rising trajectory of financial profits in the US economy appears to have come to a halt after the Great Recession. During the four decades prior to the crisis of 2007–2009 financial profits escalated as banks took advantage of the margin between interest received and interest paid, while also drawing fees, commissions and proprietary profits from transacting in financial markets and from dealing with households. The inability of financial profits to resume a rising trend since the Great Recession of 2007–2009 is a strong sign that financialization has reached a watershed in the US economy.

Aggregate debt and its changing composition

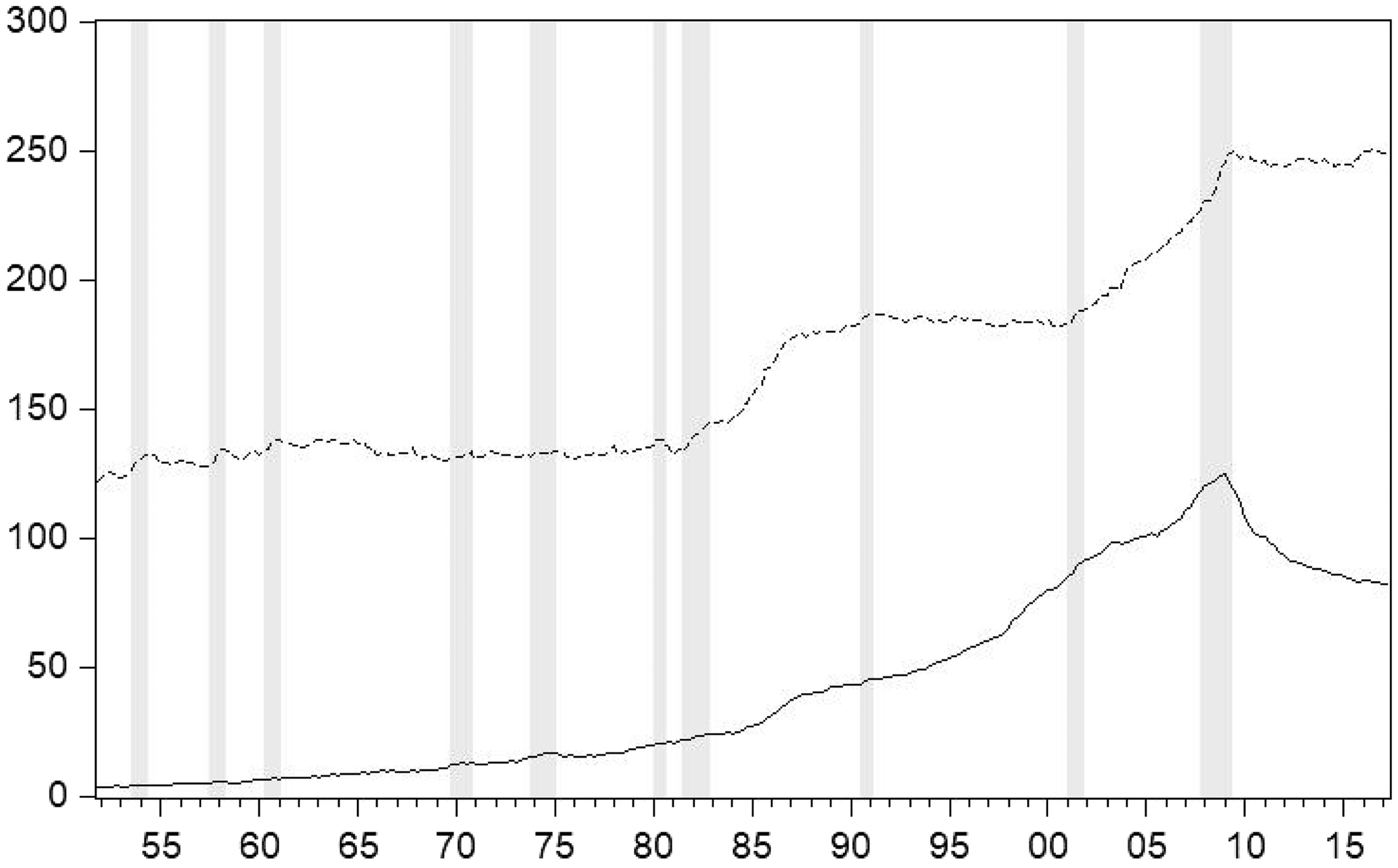

Turning to indebtedness, Figure 5 shows the proportion of debt relative to GDP for the non-financial and the financial sectors of the US economy since 1955. The period of financialization has witnessed rapid growth of all debt but particularly that of the financial sector, i.e. debt created by financial institutions as they transact with each other and as they borrow and lend to the non-financial sector. It is clear that financial debt has declined substantially post-2009, while the debt of the non-financial sector has remained broadly stable. Indeed, as shown in Table 1, it is possible to detect breakpoints in both series around 2007Q1–2007Q4. The contraction of aggregate financial debt is consistent with banks having fewer opportunities to generate non-interest profits out of financial transactions. In part, it is also probably related to the regulatory measures taken after the crisis to restrict the ability of large banks to engage in proprietary trading of financial assets (briefly discussed below). It is prima facie evidence of a relative halt of financialization in the USA.

USA, 1951Q4–2017Q2 (quarterly data). Financial sector debt as percentage of GDP (straight line) and non-financial sector debt as percentage of GDP (dotted line).

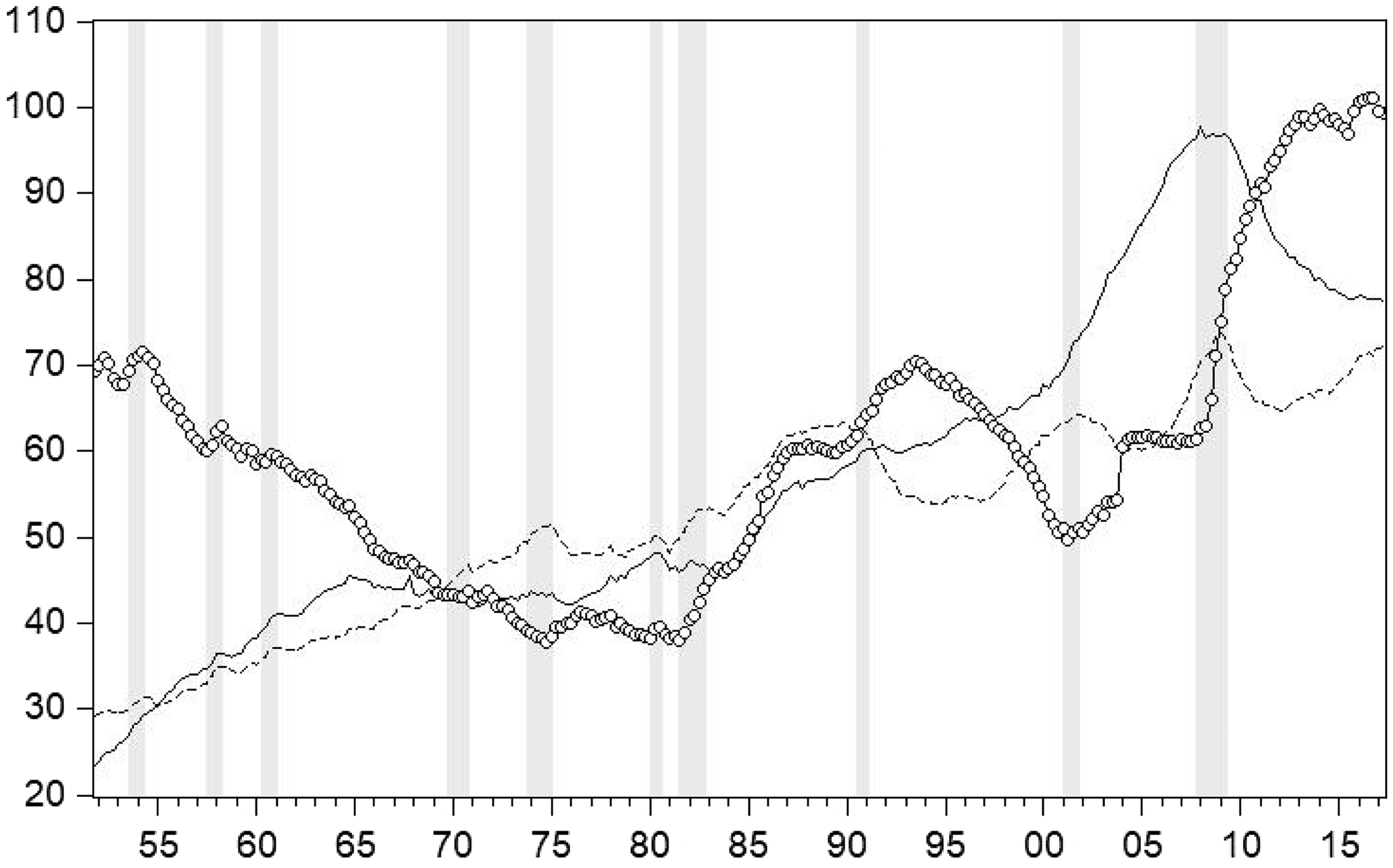

Even more important, however, is the dramatic change in the composition of non-financial debt. Figure 6 splits non-financial debt into its main components: household, non-financial business and government debt.

USA, 1951Q4–2017Q2 (quarterly data). Non-financial sector debt: Households and non-profit organizations debt as percentage of GDP (straight line), non-financial business debt as percentage of GDP (dotted line), and federal, state and local governments debt as percentage of GDP (line with circles).

It is immediately apparent that household debt has declined significantly as a proportion of GDP for the first time since the early 1980s. 11 Rising household debt has been an important source of financial profits in the decades of the ascendancy of financialization. Its decline for the first time – associated almost exclusively with a fall in mortgage debt – indicates that the penetration of finance into household life in the USA has been attenuated after the Great Recession. As shown in Table 1, the presence of a structural break around 2007Q2–2007Q4 for the household debt series can be corroborated statistically.

At the same time, the debt of the US non-financial business sector, i.e. of the core agents of capitalist accumulation, fell after the crisis and, although it has recovered in the ensuing period, it has not registered a significant increase. Its trajectory indicates that productive US enterprises continue to be relatively detached from the financial system since the Great Recession, even if they draw on the supply of credit. Again, the presence of a breakpoint in this series can be detected statistically around 2004Q1–2008Q1 using the endogenous structural break tests presented in Table 1.

During the same period, government debt has risen substantially, thus entirely counterbalancing the fall in household debt. From Table 1, it is possible to observe that a statistically significant structural break occurred in the government debt series around 2005Q1–2007Q3. Rising US government debt since 2007 is inextricably linked to state intervention to deal with the crisis and its aftermath. One of the most important aspects of government policy was to lower public interest rates. The federal funds rate of the Federal Reserve was driven close to zero, meaning that in real terms (i.e. subtracting the rate of inflation) the federal funds rate has actually been negative for the entire period since 2009. The increase in US government debt is thus the counterpart of near-zero interest rates.

The indispensable role of public debt in sustaining the US economy after the crisis has been stressed by Hager (2016). His work emphasizes that the global financial system was rescued from the brink of collapse by the explosive rise in public indebtedness and that the actions taken by the US government provided vital support to financialization. Consequently, domestic ownership of public debt has become increasingly concentrated in the hands of wealthy households and large corporations during the last 35 years, especially in the period since the crisis. Growing concentration of the ownership of US public debt has also reinforced unequal power relations in society.

Additionally, confronted with the zero lower bound for nominal interest rates and having exhausted the traditional tools of monetary policy, the Federal Reserve resorted to unconventional policy measures. It purchased large amounts of securities in what became known as ‘quantitative easing’ or ‘large scale asset purchase program’ in order to lower yields on longer-term assets in the hope of accelerating economic recovery. However, as Montecino and Epstein (2015) mention, another plausible reason for the implementation of such monetary policies could be that the Fed attempted to help its main constituency, the large banks, faced with the fall-out from the financial crisis. Their results show that banks which sold mortgage-backed securities to the Fed experienced economically and statistically significant increases in profitability (measured by the ROA). Moreover, they also find evidence of indirect spillover effects on bank profits: ‘exposure’ banks (banks with large holdings of mortgage-backed securities relative to total assets prior to the Great Recession) experienced significant increases in profitability relative to ‘non-exposure’ banks. This means that banks able to sell mortgage-backed securities in the course of quantitative easing obtained further economic benefits in addition to the benefits experienced by the financial sector as a whole.

At the same time, however, the US state has changed the regulatory environment through the Dodd-Frank Act, making it harder for large deposit-taking banks to engage in financial trading. 12 Without dramatically altering the regulatory framework of financialization, the Dodd-Frank Act passed into law in 2010 has aimed at reducing speculative risk-taking by large banks. It has also aimed at creating a framework that would allow large banks to fail without presumably endangering the financial system, and thus requiring rescue from public funds. In addition, the so-called ‘Volcker Rule’, included in the Act and operational since 2013, has constrained banks from engaging in proprietary trading, while severely limiting bank ownership of hedge funds or private equity funds. To strengthen the prudential aspect of the Act, furthermore, the US central bank has been given greater supervisory powers over capital, liquidity and leverage of large banks. The Dodd-Frank legislation has affected the ability of banks to extract NII by engaging in market transactions.

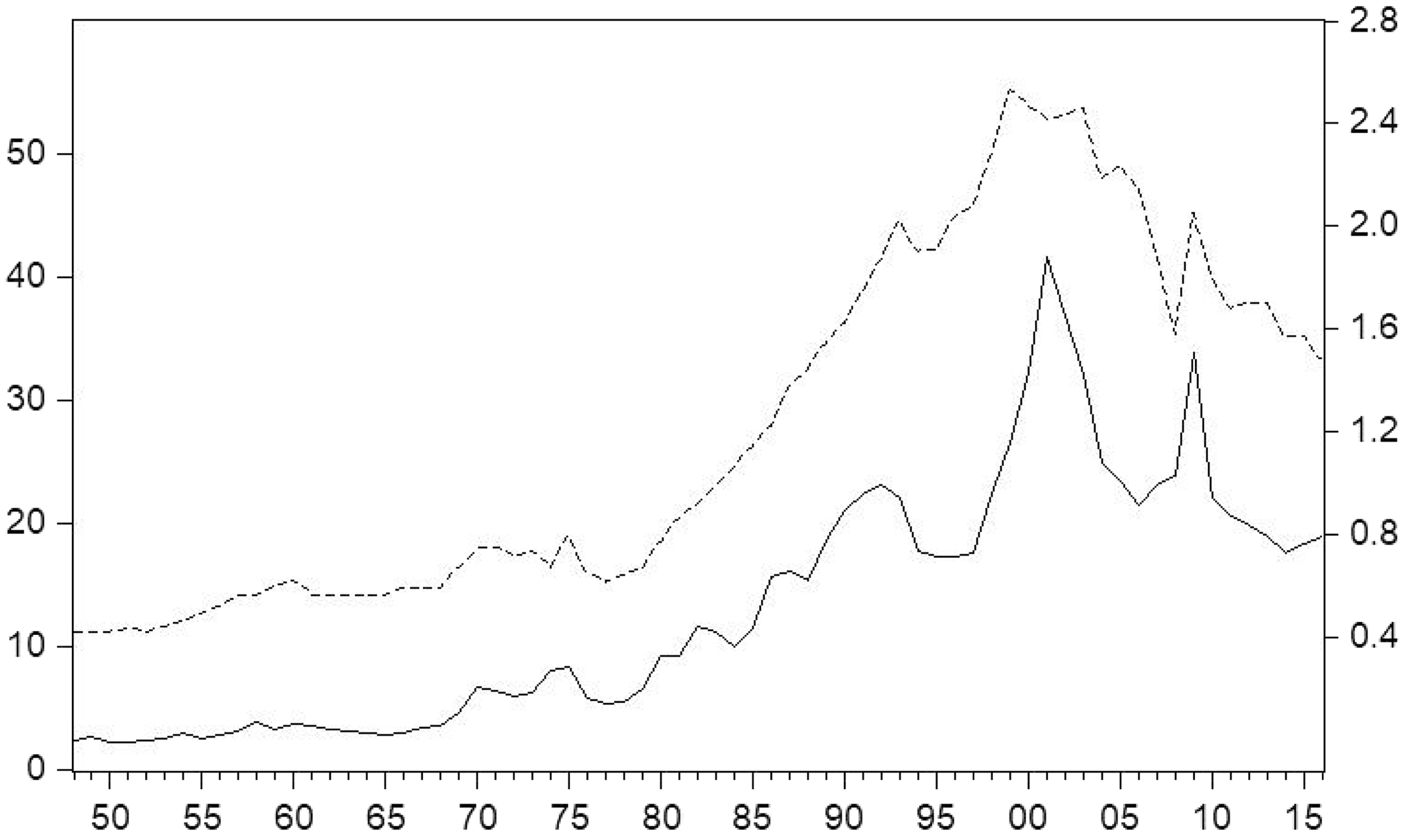

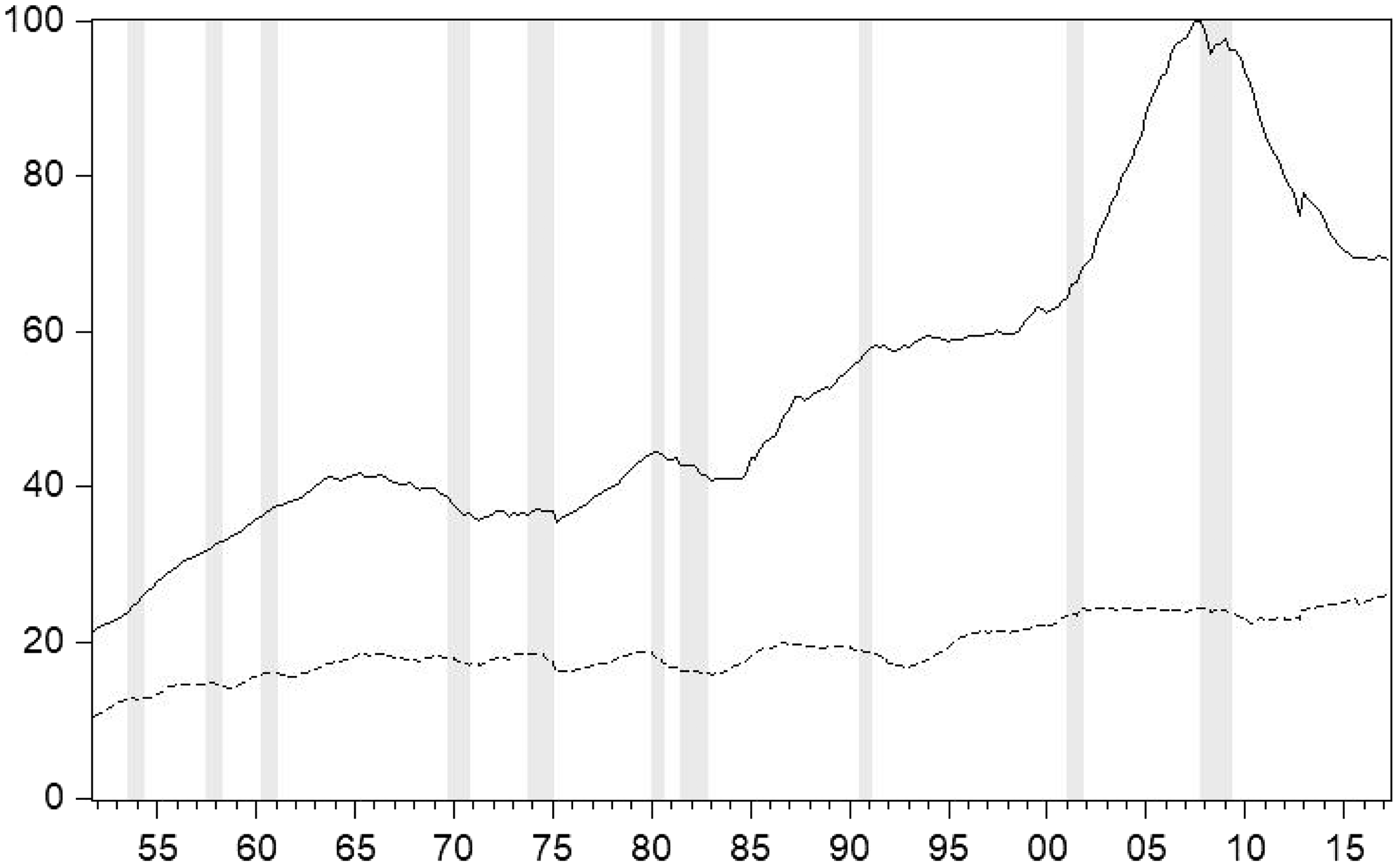

The final piece of evidence relates to the composition of declining US household debt. Figure 7 tracks the composition of this debt in terms of mortgage and consumer debt relative to disposable personal income. It shows a significant relative decline in mortgage debt since the crisis. At the same time, consumer debt registered a dip relative to disposable income at the time of the crisis, and has returned to a mildly upward trend since then. The structural breaks for each series are detected around 2007Q1–2007Q3 and 2005Q3–2007Q3, respectively. Note that mortgage debt is by far the decisive component of household debt. On these grounds, household and worker income has lost some of its importance as a source of potential profit – in terms of both interest and NII – for US financial institutions since 2007.

USA, 1951Q4–2017Q2 (quarterly data). Households and non-profit organizations sector debt: Home mortgages as percentage of disposable personal income (straight line) and consumer credit as percentage of disposable personal income (dotted line).

The deleveraging of US households has been well documented by recent work. Jian and Sánchez (2016) show that the deleveraging may have been caused by the declining willingness of households to borrow (operating on the side of credit demand) instead of a tightening of borrowing constraints (operating on the side of credit supply). Garriga et al. (2017) stress the substantial changes in debt composition that have taken place. Prior to the Great Recession, there were large run-ups in the average debt per borrower for both student debt and mortgage debt; after the crisis mortgage debt has decreased but student debt has continued to grow. Focusing on the decline in mortgage debt, Bhutta (2012) found that the drop in mortgage debt has more to do with shrinking inflows (which come from borrowers who increase their mortgage debt during a given two-year window) than with expanding outflows (which come from borrowers who decrease their mortgage debt during that window), including defaults. 13

Further aspects of households, housing and finance in the USA since the Great Recession

Crises can be turning points in capitalist development. Evidence on key macroeconomic indicators for the USA point to a watershed for, or even a relative halt of, financialization during the period following the Great Recession of 2007–2009. On the one hand, the debt of non-financial enterprises indicates a continuing relative detachment from banks supported by access to own funds. On the other, US households have substantially lowered their exposure to the formal financial system, which is reflected mainly by the decline in mortgage debt. The formal financial system, meanwhile, has reduced debt created among financial enterprises. These developments have had a substantial impact on banks, contributing to a relative decline in financial profit.

The policies of the US government during this period have had additional and complex effects on financialization. The dramatic reduction in the Fed funds interest rate, the quantitative easing policy and the abundant provision of liquidity by the state allowed banks to deal with the shock of the crisis of 2007–2009. However, liquidity provision over several years has raised state indebtedness to levels that are extraordinary for the post-war period. Moreover, regulatory intervention by the US government has lessened the scope for purely speculative bank activity, thus further constraining the profits of banks. Thus, financialization in the USA since the Great Recession has carried the strong and complex imprint of the state, both supporting and inhibiting its development.

The reduced exposure of US households to mortgage debt in relative terms is perhaps the most striking change in the components of aggregate private debt during the last decade. Housing and mortgage credit have been of paramount importance during the period of financialization in the USA and elsewhere, not least by providing new sources of financial profit. 14 Assessing the significance of the decline in mortgage debt in the USA ought to depart from the peculiar character of household debt.

Bank lending involves the advance of value in the money form against a promise of repayment with interest. Borrower and lender engage in complex relations that rest on the borrower’s ability to generate funds to make repayments, and on the lender’s ability to impose conditions ensuring repayments. The relationship between banks and non-financial enterprises as, respectively, lenders and borrowers is driven by the innate logic of capital accumulation and profit making for both parties. Thus, the decisions to borrow, lend and engage in financial transactions would be based on the search for profits; and their relationship as lenders and borrowers would be shaped by comparable expertise, information and motivation in extracting monetary profits.

The relationship between financial institutions and households and wage workers is qualitatively different. Households and wage workers are driven by the logic of obtaining the means of subsistence – or fulfilling consumption needs, while for financial institutions the logic remains that of profit making. Their mutual relationship represents a clash of qualitatively different principles, and an unequal balance of information and power. Debt could allow households to fulfil consumption needs in excess of the value of current earnings and possible savings. At the same time, debt could also place households and wage workers in a systematically disadvantageous position due to the unequal relationship with lenders. Repayments on household debt are generally made out of future income earnings, and represent an appropriation of value, thus providing a foundation for financial expropriation of households and wage workers.

The decision by households to increase or decrease their debt cannot be explained by relying exclusively on economic criteria that refer to the maximization of returns. The development of consumption needs, norms, habits and expectations takes place also through complex non-economic processes. Consequently, financial decisions by households can also be modified by the interaction between social norms, cultural trends and institutional changes. Both the volume of household debt and the flow of service payments on such debt will also depend on the concrete evolution of non-economic factors.

In this light, it would be misleading to assume that US households from the early 1980s to the late 2000s became heavily indebted simply because wages, salaries and other forms of income were ‘insufficient’ for the purposes of obtaining the means of subsistence. Goldstein (2013) has provided evidence that the patterns of the ratio of debt to income in the USA for the period 1988–2007 are less consistent with an income squeeze and more consistent with the spread of a culture of reliance on finance. The growth of debt to income was concentrated disproportionately among college-educated, upper-middle income households, rather than the lower-middle class households which felt the effects of the income squeeze most acutely. As discussed earlier in this article, finance has come to pervade the lives of US households in complex ways, which have to do with the balance between the public and private provision of key goods and services as well as changes in the norms of consumption.

In accounting for the composition of household debt, therefore, reference ought to be made to the different systems of housing provision that reflect historical, institutional and even cultural aspects of housing expenditure. 15 The paper by Fernandez and Aalbers (2016) is of relevance in this respect, referring, on the one hand, to the rise of housing finance as an integral part of macroeconomic policy and, on the other, to the role of financial globalization in the rise of housing finance. According to the authors, under financialized capitalism, there is a ‘wall of money’ – given the growing imbalance between the growth rate of the stock of capital and GDP – looking for profitable investment. This wall of money fuels a variety of traditional and ‘innovative’ financial instruments that could be characterized as a ‘financial fix’: an emergent financial landscape in a permanent state of stable instability that enables a continuous circulation of capital outside the sphere of production.

In this light, the structural break in mortgage debt in the USA is a development of considerable importance for it indicates that a vital element of financialization with regard to labour and households has been weakened by the Great Recession. What is beyond dispute is that the large decline of household debt relative to GDP and of mortgage debt relative to disposable personal income is unprecedented since the early 1980s. From a longer-term perspective, it would appear that the tremendous growth of mortgage finance in the 2000s was an exception in the post-war years propelling financialization forward but coming to an end after the crisis.

Equally complex factors have contributed to the rise of consumer debt among US households. The exposure of labour to financialization is far more complex than the simple syllogism ‘insufficient wages lead to higher debt’. The trajectory of consumer debt reflects the existence of secure employment (or lack thereof), the degree of unionization and, more particularly, the type of access to consumer credit, i.e. personal loans, credit cards and so on. The literature on consumer debt indicates that changes in the level of personal or household indebtedness are related to the easy availability of credit and to the broader social dimensions of consumer behaviour, which can influence the preferences of individuals through the media and otherwise. Barba and Pivetti (2009) and Cynamon and Fazzari (2008, 2013), for example, emphasize, first, the growth of indebtedness as a result of people’s desire to improve their individual material well-being – which includes imitation of the upper classes; and, second, how social institutions create preferences and expectations over time, encouraging households and labour to learn and repeat consumption patterns from their social reference groups – which could be constituted by neighbours, family and friends, but they could also be virtual, arising from behavioural models portrayed by the media.

The structural breaks in consumer debt and mortgage indebtedness by US households at the time of the Great Recession are, therefore, developments of significance. The reliance of US labour on credit for consumption purposes seems to have resumed a rising trend after the crisis in view of stagnating wages and salaries, but also given the prevalent norms of borrowing for consumption. In sharp contrast, the links of US labour to the formal financial system have significantly weakened with regard to mortgages, i.e. the most important element of household credit. Judging by this differential performance it is possible that the norms and practices of housing in the USA have changed since the Great Recession, perhaps in view of the costs that the collapse of the housing bubble entailed for US households. Be that as it may, there is no doubt that at the aggregate level a historic retrenchment has taken place with regard to mortgage debt, constituting a new development for the USA in the post-war years. 16

Concluding remarks

The path of the main indicators of financialization in the USA at the aggregate level since the Great Recession bring to mind Crotty’s (2008: 182) comment on the eve of the Great Recession: I find it hard to believe that financial markets can continue to grow forever at the rapid pace of the current era, or that giant firms piling up unprecedented if hidden risk will never suffer the consequences. No one knows what dangers are hidden off their balance sheets, or in obscure footnotes in incomprehensible financial reports, or in the massive leverage they have created. The current Golden Age of finance may end with a whimper, or … it could go out with a bang. But at some point not knowable today, it will end.

This is not to imply, however, that the US financial system is no longer prone to bubbles and instability. The US economy remains complexly financialized and easy access to liquidity provided by the state has boosted financial asset prices, as a mere glance at the Stock Market in 2017–2018 would indicate. However, the stagnation of financial profits, the decline in mortgage debt and the drop in financial debt, which have been counterbalanced by the rise in public debt, indicate a relative weakening of financialization in the years since the Great Recession.

The future path of financialization in the USA is likely to depend critically on government policies. It is conceivable that the US government will once again loosen the constraints on financial activity, thus giving a fresh boost to financialization. Yet, the US government remains constrained by the enormous burden of public debt accumulated as a result of the crisis of 2007–2009. Moreover, it is not in the state’s gift rapidly to increase mortgage debt, and it would be utterly reckless to seek to intensify once again the reliance of labour on the formal financial system with regard to mortgages. Furthermore, the Federal Reserve has recently started to raise interest rates in a sustained fashion, even if the risks are manifest in view of rising consumer debt and the tremendous increase in government debt. In sum, although the future trajectory of financialization is likely to depend on government policies, the scope for boosting financialization is narrow. A financialized economy characterized by stagnant financial profits that continues to drift in the long run is also a latent possibility.

Footnotes

Acknowledgements

We are grateful to the editors of the journal and two anonymous referees for comments on previous versions of this paper. All remaining errors are the authors’ responsibility.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.