Abstract

An ongoing dispute in comparative corporate governance studies concerns the extent to which cross-country convergence towards, essentially, the shareholder primacy view is occurring. While some scholars, especially legal scholars and economists, have predicted (and sometimes advocated) a convergence of corporate governance practices towards the Anglo-American model of (seemingly) shareholder primacy, others sharply disagree and point to the persistence of stakeholder-oriented governance in many countries. Banking, from the point of view of corporate governance convergence, is an interesting industry, for at least two reasons: (i) banks are peculiar types of business organizations, entailing specific governance rules in most systems; (ii) banks are (monetary) financial intermediaries more and more active on capital markets, and thus more and more exposed to the isomorphic pressures generated on corporate governance by those markets. Thus, predictions on the convergence or divergence of banks’ corporate governance are not easy to make. The present paper aims to contribute to the scholarly dispute by analysing the Italian case, which has seen, over the past 30 years or so, an apparently unfettered process of transformation of banks’ governance and ownership towards the shareholder primacy model – a process epitomized by the recent reforms of the country’s cooperative banking sector. ‘Apparently’, because a closer look at the legal and regulatory bases of banks’ corporate governance actually shows many sources of divergence from the shareholder primacy model.

Thus, the contribution proposed by the present study is twofold: first, it extends the ‘convergence’ discussion to the banking industry, where specific dynamics may help us better ‘test’ the hypotheses developed in the ‘convergence’ debate; second, it emphasizes alternative divergent patterns to those normally identified in the literature, where divergent ‘practice’ is often opposed to converging laws. Here, the sources of resistance to convergence are found in law itself.

Introduction

Seventeen years have passed since the provocative essay by Hansmann and Kraakman (Hansmann and Kraakman, 2001), and the history of corporate law has not ended yet. In the meantime, corporate law scholars’ attention has shifted from a static to a dynamic version of the Hansmann and Kraakman’s thesis: instead of predicting the sudden end of history, some have been observing a gradual convergence of corporate governance systems (and laws – see, for a good discussion of the issues, Rasheed and Yoshikawa, 2012b; and also Gordon and Roe, 2004). The ‘convergence’ corporate governance scholars seem to have in mind is the convergence towards some form of the model that has been often portrayed (perhaps mistakenly) as the Anglo-American model: the shareholder-oriented governance model – that is, a model geared to secure shareholders’ claims over the corporation.

Whereas the Hansmann and Kraakman’s end-of-history argument was predicated upon a functionalist view, assuming shareholder-oriented governance as the most efficient governance mode, the convergence thesis, instead, relies on political-economic hypotheses regarding the diffusion of ‘best practice’ (i.e. English and North-American) corporate governance. Such purported convergence is tightly linked to globalization processes, which entail the diffusion of norms across economic systems (Guillén, 2000; Khanna et al., 2006). Several factors have been invoked to explain such diffusion, such as competition on product and capital markets (Coffee, 1998; Gilson, 2001), the increasing role of institutional and foreign investors (Rebérioux and Roudaut, 2018), ideological isomorphism.

The empirical evidence, however, is mixed (Collier and Zaman, 2005; Lane, 2003). Several studies, especially in the last decade, have found that rather than converging to the Anglo-Saxon model, corporate governance arrangements across countries have become more hybrid (Ahmadjian, 2012; Kim and Lee, 2012; Rasheed and Yoshikawa, 2012a). In some cases, company law has evolved towards a less rigid form of shareholder orientation, such as in the case of the ‘enlightened shareholder value’ approach embedded in UK company law (Keay, 2007, 2011). This non-convergence can be explained in various ways: first, as some political scientists do, by pointing to the forces of resistance in the political-economic fabric of governance systems (Culpepper, 2007; Gourevitch and Shinn, 2005; Höpner, 2007; Roe, 2003). But this is resistance to legal convergence of corporate governance systems. Another explanation has been provided by corporate governance scholars, who seem to agree on the importance of distinguishing between de jure and de facto convergence: while, indeed, the diffusion of corporate governance norms and practices has made legal arrangements more alike (see, for instance, Collier and Zaman, 2005), corporate governance practices may remain rooted in more idiosyncratic institutional and political arrangements that are less prone to change or converge to one single model (Bebchuk and Roe, 1999).

The distinction made between formal and substantial governance may hold less easily in the case of banking. Indeed, banking, in addition to the specificity of its core business, differs from other industries in terms of the pervasiveness of government regulation applied to it. According to one extreme view (Fama, 1980), banking is different (only) because of government regulation. A much less extreme view holds that ‘there are no fully “private” banking systems’; and that ‘modern banking is best thought of as a partnership between the government and a group of bankers’ (Calomiris and Haber, 2014: 13). Also, banking is a strategic industry where government ownership used to be pervasive (La Porta et al., 2002); and where, as a consequence, governments may have higher incentives to resist a generalized shift away from public and semi-public ownership.

On the other hand, banking is much more tightly linked to capital markets, which are a driving force behind corporate governance convergence. The world banking industry, moreover, has been exposed to a sweeping wave of regulatory reforms since the late 1980s – reforms targeting, inter alia, the corporate governance of banks. Banks’ ownership patterns, shareholders rights and boards’ responsibilities have been fundamentally altered in many countries over the past three decades. Nowhere perhaps is such change visible as Italy, where early 1990s privatization and liberalizing reforms in the ensuing decades have radically changed Italian banks’ de jure corporate governance.

The Italian case is all the more interesting as it is identified with a corporate governance model that is opposite to the Anglo-American model: a model of ‘relational capitalism’ where corporate ownership is concentrated, where there are personal ties between owners and top managers, where shareholder rights are not adequately protected and where state intervention is widespread (Barca, 1994). This was, at least, the portrait that was drawn of Italian capitalism at the outset of the 1990s. Such a model was associated with poor economic performance, and in particular limitations to the growth of Italian firms; insufficiently mobile equity; the lack of foreign investment; chronic under-capitalization of Italian firms (Barca, 1994; Barca et al., 1994). Hence, as economists would have it, the liberalizing reforms of the 1990s, which, together with a sweeping wave of privatization, dramatically altered the patterns of ownership and control in banking as well as in other industries.

The present paper, therefore, aims at addressing the issue of corporate governance convergence from the point of view of the banking industry; and it does so on the basis of an analysis of the Italian case, which, on the face of it, represents a clear case of corporate governance convergence. However, we argue here that the apparent legal convergence of Italian banks’ corporate governance hide profound contradictions; contradictions, we suggest, that may have less to do with ‘decoupling’ than with the specific legal embeddedness of banking in Italy – and perhaps other countries.

The paper is structured as follows: The next section briefly reviews the literature on corporate governance convergence and applies its main hypotheses to the banking industry; Then the stylized facts about changes in Italian banks’ corporate governance since the early 1990s are presented, along with a brief discussion of the factors of convergence and divergence. The‘Legal and regulatory limits to convergence’ section delves into a more detailed analysis of Italian banking regulation to show the limits of convergence. The final section concludes.

Corporate governance convergence: Specificities of the banking industry

Convergence in corporate governance: Trends and debates

As reminded by Rasheed and Yoshikawa (2012a), Hansmann and Kraaksman’s ‘end-of-history’ argument was both positive and normative (Hansmann and Kraakman, 2001). In positive terms, while, as mentioned in the ‘Introduction’ section, the history of corporate law has clearly not ended yet, there is some evidence of cross-country convergence in corporate governance. Convergence may be defined here as ‘increasing isomorphism in the governance practices of public corporations from different countries’ (Rasheed and Yoshikawa, 2012b: 2). While, theoretically, corporate governance systems may converge on any model, convergence is usually, in the literature, equated with alignment on what is often presented as the ‘Anglo-American’ model of corporate governance, i.e. a model predicated on shareholder control of the firm – regardless of the variation in key corporate governance elements, such as ‘shareholder power’, among the countries associated with that model (Bruner, 2013).

This is where the positive side of the Hansmann and Kraakman argument meets the normative side of the argument – i.e. the notion that shareholder-oriented governance is synonymous with more efficient corporations. Thus, convergence is evidence of market selection: corporations (and, by extension, entire economies) increasingly opt for shareholder-oriented corporate governance because it guarantees superior performance. This hypothesis is also consistent with a narrow view of corporate governance formulated within mainstream economic theories of the firm – the view that corporate governance is a set of mechanisms that help align managerial interests with shareholders’ interests (Jensen and Meckling, 1976). Shareholders are, in this perspective, treated as the owners of the firm – that is, the principals, with managers being their agents (Jensen, 1986). In this framework, costly agency conflicts may arise out of the tendency of agents to seek to maximize their own utility, which may diverge from that of shareholders/principals. Since it is deemed more efficient, the shareholder value model of corporate governance should wipe out alternatives in a context of increasing global competition.

One may call this hypothesis the ‘market selection’ hypothesis for corporate governance convergence. Its functionalism is highly problematic, both because it assumes that shareholder-oriented governance is the most efficient type of corporate governance across countries, and because it assumes that organizations will always tend to choose the most efficient structure. Both assumptions are highly questionable. However, the ‘market selection’ hypothesis does point to one of the key drivers of corporate convergence: the global integration of product markets. Indeed, global product market competition either leads corporations to adopt Anglo-American governance in an effort to be more competitive, treating governance as, effectively, a strategic resource (Kogut et al., 2002); or encourage governments to adopt Anglo-American governance so as to ensure the competitiveness of their economy as a whole (Witt, 2004). 1

In their already mentioned study summarizing the literature on corporate governance convergence, Rasheed and Yoshikawa (2012b) cite two other main drivers of corporate governance convergence: the global integration of capital markets, on the one hand, and the diffusion of codes of good governance and the harmonization of accounting rules and standards, on the other hand. The global integration of capital markets generates convergence through at least three channels: foreign listings and cross-listings lead companies to comply with listing requirements and governance practices in systems other than their own (Khanna and Palepu, 2004); cross-border mergers push target firms to import their acquirer’s corporate governance arrangements (Bris and Cabolis, 2002); the growing presence of foreign investors in the equity of listed companies increases pressures for higher shareholder power and control (Rebérioux and Roudaut, 2018). A third driver of corporate governance convergence is the global diffusion of codes of corporate governance (Aguilera and Cuervo-Cazzura, 2004) and the harmonization of accounting rules (Coffee, 1998).

Given the strength of each of these forces, is corporate governance convergence actually happening? The empirical evidence is mixed (see Rasheed and Yoshikawa, 2012b, for a review). The adoption of governance codes (Aguilera and Cuervo-Cazzura, 2004) and of homogenous takeover regulation (Goergen et al., 2005) seems to point to convergence. On the other hand, a large cross-country study by Guillén (2000) found very little evidence of convergence on a large range of corporate governance indicators.

While there is no univocal evidence in favour of the convergence hypothesis, this does not mean that convergence is not happening at all. In the past decade, the comparative literature on corporate governance has tried to move beyond the convergence/divergence dichotomy (Rasheed and Yoshikawa, 2012a). Rather than outright convergence or divergence in corporate governance, more recent empirical studies show evidence of hybridization: this seems to be the case of Japan (Ahmadjian, 2012) and Korea (Kim and Lee, 2012). Similarly, in a study of European corporate governance codes, Collier and Zaman found both evidence of convergence and divergence (Collier and Zaman, 2005). Further, there may be convergence in form but not in function (Gilson, 2001); for instance, codes of good governance may be adopted everywhere but non-implementation is not sanctioned (Khanna et al., 2006). Thus, there may be decoupling between de jure and de facto convergence. Decoupling occurs ‘when an actor claims conformity or adoption, yet implements a new practice differently or does not actually implement it’ (Rasheed and Yoshikawa, 2012b: 3). There might be convergence in corporate governance law, which might be due to the factors discussed above; and divergence in corporate governance practice. As a consequence, both corporate governance law and practice may diverge or resist homologation.

Given the mixed evidence the corporate governance literature has soon turned its sights on the potentially multiple obstacles to corporate governance convergence (Rasheed and Yoshikawa, 2012b). In particular, corporate governance systems may be path dependent (Bebchuk and Roe, 1999); there may be strong institutional complementarities that prevent changes in one part of the system (Khanna et al., 2006); there may be differences in property rights regimes that make it highly unlikely, in some countries, to adopt shareholder-oriented governance. These factors one may call ‘institutional’, as they mostly originate in the institutional context where corporate governance operates. A second type of obstacles originates, instead, from the interaction between the interests and ideologies of powerful actors: this we call ‘political’ factors of divergence. As Mark Roe has argued, corporate governance is strongly influenced (or, in Roe’s terms, ‘determined’) by political factors – among which, in particular, stakeholder pressure (Roe, 2003). There may be, in particular, ‘normative’ opposition to the Anglo-American governance model (Rasheed and Yoshikawa, 2012b); and direct political opposition from actors who do not have interest in importing or implementing shareholder-oriented governance. The latter figure prominently in the political explanation of non-divergence, according to which ‘[t]he difference between countries with and without blockholding is largely a product of politics.’ (Culpepper, 2011: 14) Similarly, Gourevitch and Shinn (2005) argued that corporate governance varies across countries because political institutions vary.

Thus, in a comparative study of corporate control in Europe and Japan, Culpepper argues that the decisive factor (in determining whether countries create markets for corporate control or not) is the ‘political preferences of managerial organizations’ (Culpepper, 2011). The same author, drawing on an empirical case study of Italy between 1996 and 2005, where concentrated share ownership was surprisingly stable, concluded that despite significant legal changes, a policy-driven effort at changing the country’s prevalent model of corporate governance failed, due to the effective resistance of incumbents (managers and large shareholders) (Culpepper, 2007: 799).

Interestingly, none of these obstacles stem from the (potential) a priori incompatibility with shareholder-oriented governance with some systems, industries or types of firms. In addition, to our knowledge no investigation has been conducted on corporate governance convergence in banking. But why would banking be different from other industries, with regard to corporate governance?

Are banks different?

Banks 2 are certainly, on average, different from other corporations. ‘On average’, because it is hard, if not outright impossible, to identify a completely invariant model of business enterprise that is a bank – banks change over time, like all organizations, and this change can be so radical as to threaten, precisely, the uniqueness of the banking model. This is especially true of the past few decades, both prior and subsequent to the 2007–2008 global financial (and especially banking) crisis. Some authors have began speaking of market-based banking (see Hardie and Howarth, 2013) to capture the radical transformations many (large) banks have undergone – transformations that break with the traditional banking model we continue to refer to.

Thus, what we identify as the features that differentiate banks from other corporations are the core features of the traditional business model of banks, which continues to define most banks in many countries. In this view, banks are specialized financial institutions that generate money claims on the economy (Hockett and Omarova, 2017; Wray, 2013). This core characteristic has two consequences: first, the money claims generated by banks are a public good that is (mostly) implicitly treated as such by monetary authorities (Hockett and Omarova, 2017; Ricks, 2012). Second, banks’ capacity to operate is as much predicated upon the existence of equity capital (provided by shareholders) as it is dependent upon access to illiquid resources (current account deposits) and reliant on high levels of trust from regulatory authorities and society at large (Butzbach, 2016).

These two consequences explain the following specific features of banking in most countries/periods: (i) higher leverage and exposure to capital markets (than non-banking firms); (ii) multiplicity of agency relationships or potential agency conflicts; (iii) higher levels of regulation; (iv) historical importance of alternative organizational forms (to the joint-stock company form). Each of these features has significant effects on the corporate governance of banks, on the one hand; and on the likelihood of governance convergence in the banking industry, on the other hand.

Banks are highly levered firms, and their balance sheets are more highly exposed to capital markets than average non-banking firms. High leverage can reach unsound levels, such as in the case of many banks prior to the 2007–2008 crisis. But leverage is implied by banks’ business model. Banks are also, on average, more exposed than non-banking firms to capital markets – both for raising funds and to manage their assets. These two characteristics help explain the second key feature of banking mentioned above, i.e. the multiplicity of agency relationships in banking. Indeed, banks have many principals beyond shareholders, among whom depositors, bondholders and regulators. This has an immediate consequence in corporate governance terms: banks are by nature multi-stakeholder firms; and, therefore, convergence to shareholder-oriented governance may be less likely in banking. In other words, the stakeholder approach to corporate governance (see, for instance, Donaldson and Preston, 1995) might be more appropriate to describe banks’ governance. On the other hand, as mentioned above, capital markets exposure is seen in the corporate governance literature as a key driver of corporate governance convergence. Thus, banks’ higher capital markets’ exposure makes convergence more likely in banking.

Another key feature of banking is the higher levels of regulation banks are exposed to. As mentioned in the ‘Introduction’ section, banking cannot be conceived as a purely private industry – given its role in the provision of such an important public good as money. Higher levels of regulation may have various effects on banks’ governance: on the one hand, it may shield banks from the pressures to adopt shareholder-oriented governance and, more generally interfere with the factors of convergence mentioned above. There are interaction effects between regulation and ownership patterns, as shown by Laeven and Levine in a 2009 paper, where they found that regulations influence banks’ risk-taking behaviour differently according to their ownership structure. On the other hand, the higher involvement of state regulation in banking increases the likelihood of formal corporate governance convergence. This is especially the case in the post-2007/2008 crisis context, where regulators around the world have been keen on imposing more stringent rules on banks that buffered the role of equity capital – given that in banking, the socially efficient capital level may exceed the privately efficient capital level (Thakor, 2014).

A final key feature of banking is the historical importance of diverse business models and governance arrangements. In particular, as La Porta and colleagues showed in a seminal 2002 paper, government ownership is pervasive in banking (La Porta et al., 2002). Public sector banks tend to have very different governance arrangements from private sector banks (Gup, 2007: 20). Cooperative and savings banks are also widespread in many banking systems, sometimes competing very effectively with for-profit, joint-stock banks (see Butzbach and Von Mettenheim, 2014).

This diversity of ownership patterns and business models generates vested interests in the maintenance of non-shareholder-oriented governance; in other words, it may buffer forces of resistance to corporate governance convergence identified among the ‘political’ factors of divergence mentioned above.

Overall, the specificity of banking, while it may explain governance features that may significantly differ from the Anglo-American non-banking firm (see Hagendorff, 2014; and John et al., 2016), does not allow us to make clear predictions on corporate governance convergence in that industry. In particular, given the pervasiveness of regulation in banking, the potential resistance to convergence is not likely to take the ‘practice against norms’ form, weakening the case for decoupling in banking. On the other hand, banking as an industry has been fundamentally transformed, in most advanced economies, by three decades of privatization and liberalization. Thus, the actual degrees of convergence, divergence or hybridization are not clear. The next two sections present the empirical evidence on the Italian case, emphasizing the tensions within Italian banking law and regulations.

Legal changes in Italian banks’ corporate ownership, 1990–2018

Privatization, corporatization and the rise of Italian banks’ private shareholders

Italian capitalism in the twentieth century revolved, essentially, around the dual capacity of the Italian state to (i) ensure sufficient funding levels to small and large firms and (ii) direct the strategic actions of entire industrial sectors. For most of the century, state-owned enterprises and public law entities were the dual means to such mission (Barca, 1994). The publicness of Italian capitalism was associated with a traditionally low protection of shareholders’rights (Barca and Trento, 1997). The Italian banking industry reflected or magnified such patterns, given the key strategic importance of banking for the country’s economic development (in the absence of well-developed capital markets). Thus for most of the twentieth century the Italian banking industry was dominated with non-private entities with absent shareholders.

Pre-1990 banking ownership patterns

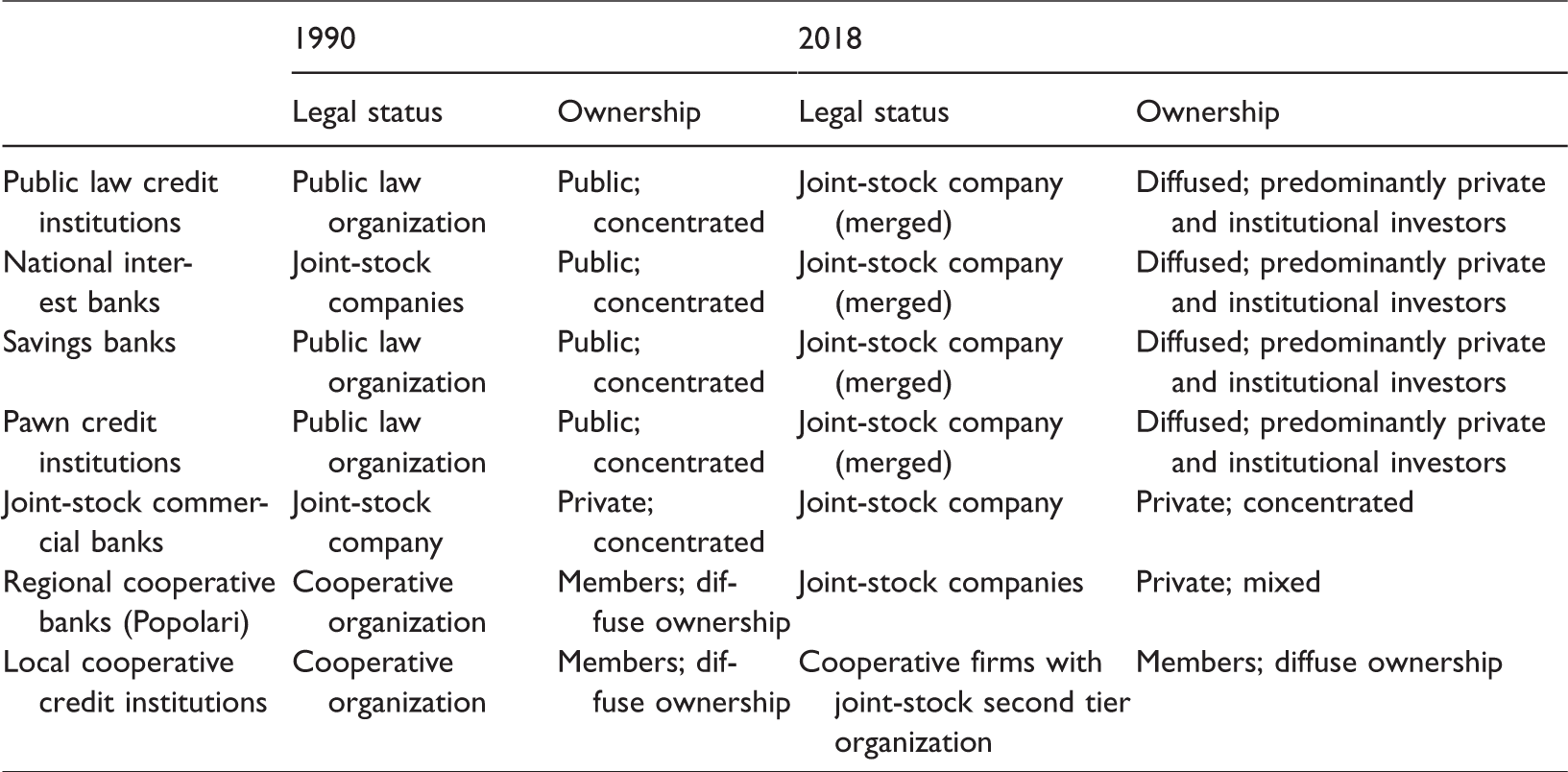

Until the early 1990s, Italian banks were regulated under a framework dating from the 1930s – the so-called ‘banking law’ of 1936–1938, consisting of several related legal and regulatory instruments. 3 In particular, the 1936–1938 banking law recognized different legal types of credit institutions, attributing to each type certain rights and duties related to specialization in certain segments of the credit markets. These bank types or categories were: (i) Public law credit institutions; (ii) ‘national interest banks’; (iii) savings banks; (iv) pawn credit institutions; (v) joint-stock commercial banks; (vi) regional cooperative banks (‘Banche popolari’); (vii) local, rural cooperative credit institutions (Banche di Credito Cooperativo; henceforth BCC).

All these credit institutions, except of course, for-profit banks, were considered ‘public banks’ by Italian regulation; all ‘public banks’ except ‘national interest banks’ were public law institutions: that is, ownership rights over these banks’ equity were entirely held by public entities, which in turn were considered ‘the owners of themselves’ as one Italian legal scholar put it (Mottura, 2011). However, these public ‘owners’ did not control either the board or the bank itself: board members were appointed by the Italian State or by local or regional governments, which were responsible for supervising the adequacy of public banks’ activities with regard to their official (legal) status.

The ‘national interest banks’ mentioned above (there were only three: Banca Commerciale Italiana, Banco di Roma, Credito Italiano), although considered public banks as well, were, unlike other public banks, joint-stock companies, with, as a majority shareholder, a state-owned holding company – IRI. 4 Popolari and local cooperative credit institutions had yet a difference governance system based on the cooperative model of one member, one vote. 5

Another specificity of the 1936–1938 banking law was that while joint-stock commercial banks were prohibited from holding equity in public banks, the reverse was not true. Thus, the ownership patterns of joint-stock commercial banks fell in two categories (Trivieri, 2005: 52): (a) banks with concentrated ownership and a majority shareholder (usually a public bank); (b) banks with diffused ownership.

The 1990 reform and its aftermath

Law n.218 of 30 July 1990 6 (called ‘Amato Law’ after the name of its principal proponent) signalled the end of the regulatory regime created by the 1936–1938 banking law. The Amato law was Italy’s first large-scale attempt at restructuring the country’s public banking sector. It was based on two premises: first, that Italian public banks were struggling to operate efficiently, given the increasing political control they had been subject to over time – in particular, Italian public banks were increasingly seen as undersized and undercapitalized; Second, that the new competitive environment of the 1990s (especially with the planned completion of the European single market) threatened to wipe out non-competitive banks. The ultimate aim of the government was, then, to start the process of banking privatization; however, public banks, given their special legal statuses and governance systems, could not be privatized as they were. Thus, the Amato Law enabled two fundamental changes in public banks’ status and governance: first, it corporatized those banks, doing away with the public law status (for most of them) and turning them into joint-stock companies 7 ; second, the 1990 law created the so-called ‘banking foundations’ – ex nihilo owners, which were endowed all voting rights in the newly structured banking entities. Banking Foundations were thus set up with an explicit mandate: that of facilitating an orderly restructuring of Italian banking through the gradual divestment of the shares they held in banks, favouring mergers and acquisitions and the shift from public to private ownership.

In the subsequent period, the trend towards the corporatization and privatization of Italian public banks consolidated. Another milestone in the history of Italian capitalism (and of Italian banks’ governance) was reached in 1993 when, following a referendum held in June that year, the government dissolved the Ministry of state shareholdings and adopted a measure (legislative decree n.389 of September 1993) that removed the remaining legal obstacles to the divestment of state shareholdings (Barca and Trento, 1997). Shortly afterwards, IRI sold its stake in Credit Italiano and Banca Commerciale Italiana (two of the three ‘national interest banks’).

By 1994, all savings banks, the pawn credit institutions and the public credit institutions (save one) had been transformed in joint-stock companies. But banking Foundations were slow in divesting shares (see below) – in part because of certain measures contained in the Amato Law that prevented an abrupt decline in public ownership, such as article 19, which made it mandatory for ‘public banks’ to have a public entity (such as banking Foundations) as a majority shareholder. Thus, in 1994, the government abolished that requirement. 8 Next the Ministry of the Treasury issued a regulation (the so-called ‘Dini directive’) that mandated banking foundations to diversify their assets, with the explicit aim of having their shareholdings in banks decrease to below half of their total assets within 5 years. Almost 5 years later, a law (the so-called ‘Ciampi Law’) further prohibited banking foundations to hold majority equity stakes in banks. 9 The Ciampi law also, importantly, transformed banking foundations themselves into private entities. However, the law did not achieve banks’ full autonomy from their (previously) majority shareholder, since it did not prohibit foundations to de facto control banks through their power of appointing board members as a powerful minority shareholder. Also, with a change in government in 2001, a new law brought Foundations back to the public orbit. 10 But two years later, a new reversal ensued from a decision by the Constitutional Court, Italy’s supreme legal body, which struck as ‘inconstitutional’ those parts of the Tremonti law that made foundations public again. 11

Accelerating convergence in banks’ownership: From the late 2000s to the present

The twists and turns associated with the slow legal autonomization of Italian banks from their foundation owners show the recurrent struggles between successive Italian governments, on the one hand, and banking foundations, on the other hand, around the issue of the extent of foundations’ control over the banks they held equity into. In other words, this non-linear process shows the many obstacles lying on the path to the shift from public to private ownership in Italian banking up until the early 2000s. In fact, the godfather of the 1990 law, Giugliano Amato, famously called Foundations ‘monsters’. Foundations, were, in particular, criticized for their politicization and their political influence over banks’ strategy (Boeri, 2013; Boeri and Guiso, 2012; Messori and Zazzaro, 2003). This view is consistent with the broader thesis of political scientists studying cross-country changes (or non-changes) in corporate governance and patterns of corporate control, briefly cited in the previous section: in his 2007 study, mentioned above, Culpepper emphasized the stability of traditional (relational) patterns of corporate ownership in Italy, thus concluding that there was no corporate governance convergence in the Italian case. Other studies written in the mid-2000s shared this view (see Gourevitch and Shinn, 2005; Messori and Zazzaro, 2003).

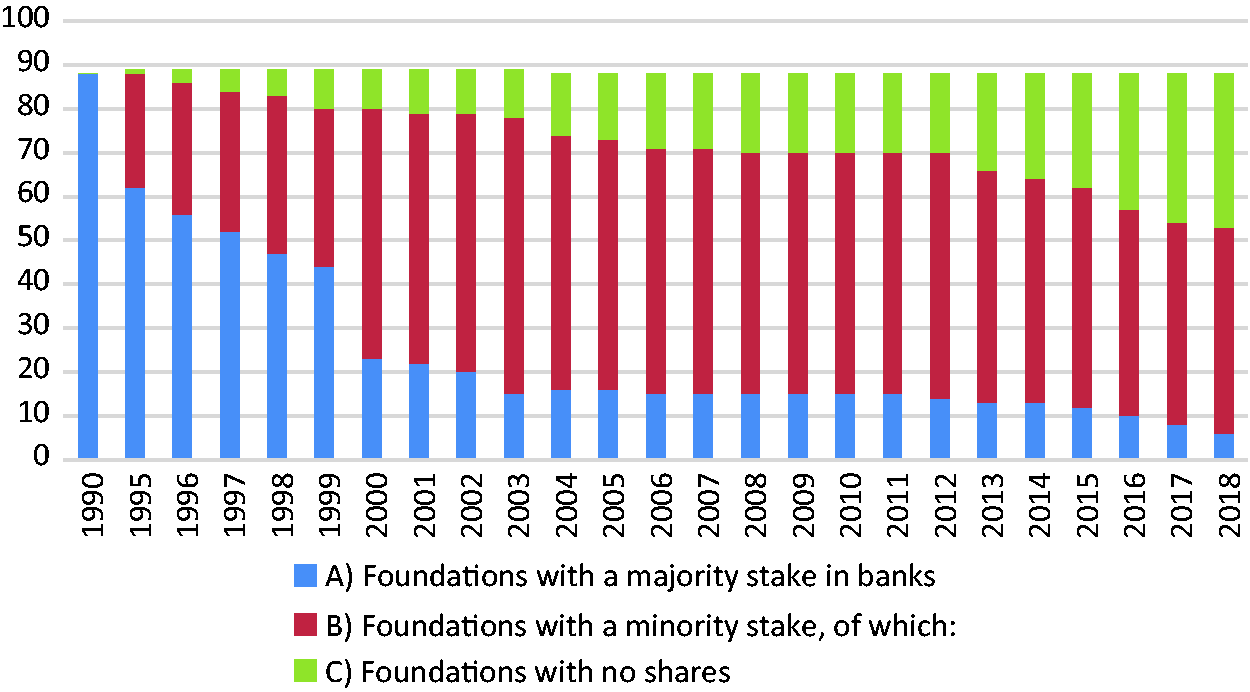

Yet, by then, and despite the twists and turns in the legislation on Foundations mentioned above, change was under way: data shows the unequivocal decrease in foundations’ bank shareholdings starting in the mid-1990s, as can be seen in Figure 1. In other words, while this shift in ownership patterns in Italian banking did take a while to materialize, prompting observers to emphasize path dependency (along the lines of Bebchuk and Roe, 1999) and the resistance to change of significant segments of the Italian political economy, it did happen.

Italian banking foundations’ equity shares in banks, 1990–2018.

The shifts in ownership spurred by the 1990 Amato law and subsequent regulatory reforms were instrumental in helping to achieve the desired large-scale restructuring of the Italian banking sector: of the more than 1000 banks and credit institutions present on the Italian soil in the early 1980s, only 331 exist today; Former public banks have aggregated and merged to become large banking groups, such as IntesaSanPaolo and Unicredit – Italy’s largest banks and among the largest European banks, in total assets.

In addition to this shift from public to private ownership, corporate ownership patterns in Italian banking show an unequivocal trend towards the ‘public company’ model for the largest banking groups, with diffused ownership and a few minority shareholders – mostly private institutional investors. This is certainly the case with IntesaSanPaolo: As of September 2018, more than 80% of Intesa’s shares belonged to the public; slightly over 19% of shares were held by four minority investors, of which two banking foundations (Compagnia di San Paolo and Fondazione Cariplo), with approximately 6.8% and 4.4% of shares, respectively; and two global, US-based institutional investors (Blackrock and JP Morgan Chase). Unicredit, on the other hand, had a similar ownership structure with the prevalence of minority shares held by foreign-based institutional investors (primarily investment funds), and a small stake held by two banking foundations.

The latest events confirming this decades-long change in ownership patterns were the two laws reforming Italian cooperative banks: a 2015 law reforming the Banche Popolari 12 and a 2016 law reforming local credit cooperatives. 13 The 2015 reform forces Popolari – regional cooperative banks, whose existence, in some cases, dates back to the second half of the nineteenth century – to convert into joint-stock companies if their turnover exceeds a threshold of euro 8 billion. As a consequence, 8 of the 10 largest Popolari (those targeted by the law) decided to convert to joint-stock company status.

The 2016 reform of local credit cooperatives, by contrast, does not attempt to change the legal status of cooperatives, but forces them to regroup in bank holding groups headed by a joint-stock company. The law sets an opt-out option for the largest credit cooperatives – i.e. those above 200 million euro of equity – but the latter will have to convert into joint-stock companies. Like in the case of the 2015 reform of the Popolari, then, the reform of local credit cooperatives indicates a clear preference of law-makers towards the joint-stock company form and private equity ownership.

Table 1 summarizes this shift in corporate ownership and legal statuses.

Italian banks’ legal status and ownership patterns, 1990 and 2018.

But the ‘normalization’ of banks’ shareholdings does not exhaust the pattern of corporate governance convergence in Italian banking. In particular, the corporate governance of banking entities listed on the stock exchange has been greatly affected by a series of legal changes brought in the late 1990s – early 2000s. The first important legal change was caused by the so-called ‘Draghi law’ in 1998. 14 Conceived as a legal re-ordering of financial regulation (hence, it is being named ‘Single financial regulatory text’), the Draghi law contained important corporate governance measures incorporating European law into the Italian system. In particular, the law aimed at reducing interlocking directorates and improving the protection of minority shareholders’ rights. Right after the Draghi law was passed, the Italian stock market came up with its own code of good governance, the so-called ‘Preda’ code, for listed firms. According to recent evidence, by 2016 the Preda code was adopted by 94% of Italia listed firms (Cucinelli and Mascia, 2017). More recently, a 2011 legislative decree (the so-called ‘Save Italy’ decree) prohibited cross-shareholdings for listed companies.

As a consequence of these legal changes, the 2000s have marked a limited but continuous erosion of relationship capitalism in Italy – an erosion characterized, in part, by the decline in interlocking directorates and cross-shareholdings. In a series of recent studies focused on listed firms, Drago et al. have observed a slight decline in interlocking directorates – both during the period 1998–2007 (Drago et al., 2015); and in the aftermath of the 2011 reform (Drago et al., 2016). This decline is not, however, observed across the board; in particular, Drago et al. note that core companies within Italian capitalism continue to exhibit cross-shareholdings (Drago et al., 2016). Moreover, most listed firms continue to have a controlling shareholder – usually, members of the family that founded the firm.

But, importantly, this does not concern the largest banking groups evoked above. In its latest annual report, the Italian securities market authority, the Consob, noted that the financial industry is the industry with the least presence of controlling shareholders (Consob, 2017). If there is decoupling, it does not concern banks as much as non-financial companies. Finally, some authors have observed an increase in institutional investor activism across all industries (Belcredi and Enriques, 2015).

The main drivers of convergence

The main drivers in the long process of privatization and de-personalization of ownership and control patterns in Italian banking are those identified in the corporate governance literature cited above. In particular, one may single out five key factors: (i) the radical transformation of Italian banks’ competitive environment since the late 1980s; (ii) long-lasting changes in the macroeconomic policy environment faced by successive Italian governments since the early 1990s; (iii) shifts in the political-economic foundations of Italian banking in the 1990s and 2000s; (iv) the active role played by banks’ top management; (v) the 2007–2008 global banking crisis and its aftermath.

The first factor – radical transformation of Italian banks’ competitive environment – is directly linked to the implementation of the European Single Market in the late 1980s and early 1990s (De Bandt and Davis, 2000; Underhill, 1997). In particular, one should emphasize the importance of the European-wide harmonization of rules and standards since the 1980s, starting with the First EC Banking Directive in 1977.

A second major factor behind the changes in ownership patterns and other related corporate changes discussed above lies in the shifts in the political economy of Italian capitalism – in particular, changes in the socio-economic basis of Italian ruling coalitions, together with significant shifts in their resource environment. It is precisely the eroding power of the coalitions still ruling the corporate world in the early 2000s, identified by Culpepper (2007), that paved the way for the late 2000s converging trends noted above.

Capital markets pressure, together with regulatory reform in the wake of the 2007–2008 global banking crisis, has also played a role in the convergence of ownership patterns. Indeed, the 2016 reform of the local credit cooperatives was explicitly motivated by policy-makers by the perceived need to help cooperative banks re-capitalize and thus improve these banks’ access to capital markets. According to some observers, however, such objectives were instrumental to ‘normalize’ banking cooperative entities and turn them into joint-stock companies (Capriglione, 2016).

As a conclusion, then, two trends appear clearly in the Italian case: first, a decades-long shift in ownership patterns; second, a gradual and somewhat limited convergence of Italian banks’ governance towards some key features of the shareholder-oriented governance model. Importantly, among the key drivers of late 2000s corporate governance convergence is the weakening of the obstacles found in the earlier period – in particular, the resistance of powerful groups around banking Foundations. But there is another series of obstacles to full-fledged convergence that arises out of banking law itself; they are discussed below.

Legal and regulatory limits to convergence

Obstacles to a full alignment of cooperative banks on the joint-stock model

There is no consensus, among Italian legal scholars, as to whether the recent reform of cooperative credit institutions implies a complete alignment of the cooperative governance model on the joint-stock model (see Cardarelli, 2017, for a presentation of the legal debates). And it may be too early to assess the degree of such alignment. However, there are two series of obstacles to full alignment: first, certain measures contained in the recent reforms (especially the 2016 law) entrench the mutual nature of credit cooperatives – in a sense, these measures reveal the limits to law-makers’ infatuation with the joint-stock company model. Second, the main building blocks of the reforms have been exposed to vocal opposition by several groups.

The first series of obstacles consist in the presence of several measures contained in the 2016 reform that have been presented as guarantees that cooperative banks will not see a complete transformation of their control mechanisms. In particular, one may cite (i) the fact that local credit cooperatives hold shares in the newly formed groups, and not the other way round; (ii) the possibility for newly created groups to constitute ‘sub-holdings’, explicitly prohibited for other banks (and non-banking firms), according to the Italian regulations on cross-shareholdings (mentioned above); (iii) the ‘cohesion contract’ that ties the hands of the holding company – by explicitly (contractually) aligning the mandate of the holding company on the objectives of member cooperative banks. Thus, the formal governance of the local credit cooperatives should be maintained. Additional measures, not related to governance, should help preserve, according to the regulatory agency, the mutual nature of credit cooperatives – for instance, the BCC remain dedicated to ‘prevalently’ serving their members (articles 2511–2514 of Civil code). Finally, the newly formed cooperative banking groups have the obligation to channel 3% of net earnings to a mutualistic fund for all group members.

A second series of hurdles to the full alignment of cooperative banks’ governance to the joint-stock company model are mostly legal technicalities, such as the ‘right to withdraw’ negated to cooperative bank members by art. 2 of the 2016 Law. According to the Italian Civil code, any member of an entity whose scope is significantly altered has the ‘right to withdraw’, that is, the right to obtain the full amount of his or her shares in that entity. The law suspends that right for cooperative banks deciding to join a cooperative group – which does correspond to a significant alteration of local credit cooperatives’ scope. This measure, according to many legal scholars, is anti-constitutional and is poised to be cancelled by the Constitutional Court (Capriglione, 2016). A similar criticism was voiced against the 2015 reform (Urbani, 2015). In fact, the issue of the right to withdraw is at the heart of ongoing legal battles around the two reforms. A significant legal victory for supporters of the 2015 law was won in March 2018 when the Constitutional Court decided that the measure suspending the right to withdraw, in the case of the Popolari, was legitimate. However, the reform was frozen in September 2016 when the Consiglio di Stato, Italy’s highest administrative court, suspended its main measures – i.e. the conversion of Popolari in joint-stock companies. Yet this may seem as a rearguard legal battle, given that, as mentioned in the previous section, only 2 of the 10 Popolari targeted by the reform have not converted yet.

Regarding the reform of local credit cooperative banks, on the other hand, while the ongoing legal battle focuses on the ‘right to withdraw’, other aspects of the reform are still being opposed by cooperative banks themselves. Indeed, while most of the largest credit cooperatives accepted the reform, embracing the need for constituting large groups to strengthen their competitive edge on credit markets, most of them were not ready or willing to leave the mutual sector altogether. Yet the reform sets a switch from the Italian regulator to the European one (the European Central Bank), given the higher size of the newly formed banking groups. This switch is being resisted by many credit cooperatives as it is perceived as a further push to embrace the joint-stock model. Hence, the temporary suspension of the reform decided by Italian law-makers in July 2018. 15

Resistance against the main building blocks of the 2016 reform follow the patterns identified in the literature on corporate governance divergence discussed in the ‘Corporate governance convergence: Specificities of the banking industry’ section: it aggregates social groups that have interest in the maintenance of the traditional cooperative model. The latter are legal scholars, cooperative bank ordinary members and top management in the smaller banks.

Legal and regulatory obstacles to shareholder primacy in joint-stock banks

The most consistent obstacles to corporate governance convergence in Italian banking, however, do not originate in the (limited) persistence of mutuality among Italian cooperative banks, but, rather, come from legal and regulatory measures regulating shareholders’ rights and powers in joint-stock banks. Given the growing interpenetration of European and national banking law in European Union member states, these measures both express a European tendency and a specific Italian pattern. These obstacles may be grouped in three categories: (a) limitations to the acquisition/sale of equity ownership; (b) limitations to the exercise of voting rights by shareholders; (c) specific constraints on the role and function of banks’ governing bodies.

Limitations to the acquisition and sale of equity ownership in banks

European banking regulations, in particular European Directive n. 2007/44/CE, 16 define procedures and criteria for the prudential assessment national regulatory authorities have to follow in the processes of acquisition of equity in banks. These criteria derive from an overarching objective – that of ensuring the ‘sound and prudent management’ of banking entities. The latter principle originated in 1980s European legislation – specifically, the Second Banking Co-ordination Directive adopted by the European Commission in December 1989. While, however, in European law the principle mostly applies to the screening of bank shareholdings, in the Italian context, where the ‘sound and prudent’ principle was adopted in 1992, the same principle has been broadened into a general supervisory objective (art. 5 of the Italian Single Banking Law, or Testo Unico Bancario, henceforth TUB). 17 In particular, the principle helps to sustain Italian regulation’s commitment to the operational (and managerial) autonomy of banking entities (Brescia Morra, 2000). This is, obviously, autonomy from shareholders; in general, contemporary Italian banking regulation is predicated upon the need to protect banks against the potentially damaging behaviour of shareholders (Rotondo, 2009); a need that, at the European level, became even more cogent in the wake of the 2007–2008 global banking crisis.

Italian securities laws 18 contemplate further restrictions applied to equity shareholdings in listed firms. These restrictions vary according to industries and regulatory situations, but they are the tightest in banks (articles 19–24 of TUB). In particular, any acquisition of shares that gives rise to ‘significant influence’ (influenza notevole) over the banking firm has to be authorized by the Bank of Italy – the Italian authority responsible for banking supervision (art. 19 TUB). The ultimate goal of such restriction is to avoid that subjects that are ‘external’ to the banking industry (that is, have no prior experience in banking or finance) may end up exerting excessive influence of the banks’ management (Costi, 2007). Importantly, such ‘significant influence’ is deemed to arise either directly, through shareholdings above 10% of voting rights; or indirectly, through the acquisition of a stake below 10% but giving de facto the minority shareholder the ability to influence the bank’s management (for instance, in the case of banks with diffused ownership). A further limitation to access to bank shareholdings stems from the ‘honorability’ requisite (art. 25 TUB) applied to banks’ shareholders.

These limitations are compounded by extra information and communication duties required of banks – in excess of those normally required for non-banking firms (Costi, 2007). These duties are aimed at ensuring the maximum transparency regarding banks’ shareholdings, obligating shareholders to communicate ‘relevant shareholdings’ – to the benefit of both banks’ management and supervisory authorities. Such obligations also concern shareholders’ agreements (‘Patti parasociali’), that is, all agreements between shareholders that produce effects on the exercise of voting rights. The obligation (articles 20 and 21 of TUB) is, again, motivated by the need to avoid conflicts of interest and excessive infringements, on the part of shareholders, on a bank’s operational autonomy.

Limitations to the exercise of voting rights

Italian banking regulation contains a series of measures that punish delinquent shareholders. In particular, the supervisory authority may suspend or ‘freeze’ shareholders’ voting rights in case of non-compliance with communication duties (art. 24 TUB) or whenever shareholdings have not yet received authorization (Brescia Morra, 2000). Whenever, despite this suspension, shareholders do exert their voting rights at the general assembly of shareholders, the outcome of the vote may be legally challenged on this basis (Costi, 2007); and, a specificity of banking regulation (with respect to the regulation of non-bank firms), the challenge may be raised by the supervisory authority itself. The suspension of voting rights becomes definitive when, absent the authorization of which above, or in the event of the withdrawal of such authorization, the supervisory authority forces shareholders to sell their stake into the bank.

Specific constraints on the role and function of banks’ governing bodies

Both the European and Italian legislation contain specific constraints on the role and function of banks’ governing bodies. Such constraints have been considerably tightened in the wake of the 2007–2008 global banking crisis; the latter, indeed, revealed boards’ and internal control mechanisms’ incapacity to deal with, or significantly reduce risk. Again, the notion of ‘sound and prudent management’ is a key driver of banking regulation (Basel Committee on Banking Supervision, 2015; Capriglione and Masera, 2016; Cera, 2015). These constraints have been spelled out in 2011 guidelines published by the European Banking Authority (Capriglione, 2016), which were made into European law with European Directive 2013/36/UE (the so-called ‘CRD IV’ Directive). In Italy, these measures are combined with those contained in Bank of Italy’s 2013 and 2014 guidelines. 19

Such legal and regulatory limitations on shareholders’ rights and power of control are directly motivated or inspired by the view that banks are not ordinary firms; this is acknowledged by the Italian legislator when, in article 10 of the TUB, banking is defined as a combination of ‘monetary intermediation and the functional linking of collecting savings and lending money.’ Such business model has a social utility and its protection belongs, therefore, to the general interest. Hence, the public law influence is pervasive in Italian banking regulation, noted by Italian legal scholars (see Capriglione, 2016; Cera, 2015; Costi, 2007; Vella, 2011).

Conclusions

This paper has shown that, as already observed by various studies in several other countries or sectors, there is no full-fledged corporate governance convergence in Italian banking; rather, we may observe hybridization – or, in other words, the simultaneous combination of strong converging trends (reflected in the prevalence of private shareholders and institutional investors in banks’ ownership, in the decline of blockholding, in cross-shareholdings and interlocking directorates) and divergent trends (notably the resistance of mutual forms of banking organizations and legal obstacles to shareholders’ claims to control the banking firm).

In particular, the 2007–2008 global banking crisis had two contradictory effects on the corporate governance of Italian (and, more broadly, European) banks: on the one hand, it buffered the position of banks’ shareholders by (i) emphasizing the importance of equity in banks’ balance sheet; and (ii) pushing regulatory authorities to streamline banks’ legal statuses in favour of the joint-stock company. On the other hand, it led to the erection of yet more barriers to shareholders’ control of the banking entity.

This is not the decoupling several authors point to when observing conflicting tendencies between law and practice; rather, there are conflicting tendencies or tensions within law itself. Thus, corporate governance divergence – or, more adequately, the resistance of Italian banking regulation to shareholder control – cannot be attributed to the political economy elements traditionally brought forward in the political science literature. The latter may have explained resistance to legal change in the 1990s and 2000s (as shown above); but not the persistent dis-alignment of Italian banks’ corporate governance with respect to the Anglo-American model today.

Rather, it is the legal construction of banking – of banks’ uniqueness as economic institutions – that offers such resistance. Here banks offer an interesting alternative to the usual criticism of shareholder value from the points of view of multiple stakeholders’ interests. The latter has historically laid the ground for alternative approaches to corporate governance, such as the ‘enlightened shareholder value’ approach (see Keay, 2007, 2011) or the stakeholder approach (see Donaldson and Preston, 1995). 20 Both approaches, indeed, focus on the interests that should be considered within the reach of directors’ fiduciary duty. 21 Yet Italian banking regulation is not predicated on the need to protect concurrent claims to banks’ capital; it seems, rather, that when Italian banking law does explicitly consider the interests of diverse stakeholders (such as, beyond shareholders, creditors and the wider public), it does so as a consequence of the construction of the banking firm as an autonomous entity with an institutional function – rather than the other way around. It maybe that the end result of such approach to the governance of banks does buffer the sustainability of banks as businesses – in line, thus with the aims of the enlightened shareholder value or the stakeholder models (see Armour et al., 2003; Klettner et al., 2014); but the premises are, we argue, very different – and therefore have different implications for our understanding of corporate governance convergence and divergence.

However, our findings and interpretation raise new problems, for the observer and the policy-maker alike. One such problem is the conceptualization of corporate governance. One could argue that the current debates around corporate governance convergence imply a dichotomous view of corporate governance: on the one hand, corporate governance is viewed as the set of mechanisms ensuring the alignment of managerial interests on shareholders’ (owners’) interests. This is what we may call a ‘minority view’ nested in financial economics and some parts of corporate law, consistent with the Hansmann and Kraakman thesis (Hansmann and Kraakman, 2001). On the other hand, corporate governance may be seen as the set of mechanisms devised to minimize agency costs and to ensure an efficient government of corporations. This is what we may call a ‘majority view’ – a much more neutral (axiologically speaking) view shared, it seems, by a majority of corporate governance scholars who do not believe shareholders’ claims are superior (by right) to other stakeholders’. One may propose a third view of corporate governance, which is more historically situated – i.e. that corresponds to the context of the rise of the ‘shareholder value maximization’ model – and consists in seeing corporate governance as a set of mechanisms devised to either govern the firm in the absence of owners (for equity shareholders are not the owners of the firm) 22 or to limit shareholders’ claim to control the firm (see AUTHORS).

A second problem has to do with the adequate time-frame within which one may assess convergence or divergence (or hybridization); The ‘traditional model of banking’ enshrined in Italian banking law and regulation may offer resistance to convergence pressures for some time; But banks change, too. As a consequence, the very basis for the specificity of banks (and of legal and regulatory treatment of banks), which, in our view, provided the foundation for the ‘legal resistance’ to convergence, may be eroded. Such erosion is likely to have governance consequences – but by that time, the current, powerful forces towards corporate governance convergence may have subsided.

Finally, a major limitation of the present study is that it does not offer a complete, systematic study of the causal factors behind the regulatory hurdles against corporate governance convergence in Italian banking. 23 As a matter of fact, the causality we (implicitly) had in mind when analysing the latter was more of an ontological rather than an agentic sort, as is usually the case, for instance, in political-economy accounts of corporate governance divergence (such as in Culpepper, 2011; and Gourevitch and Shinn, 2005). In other words, we identify a resistance (to corporate governance convergence) in law based on the legal construction of the banking identity, and not on the action of some groups (such as regulators and law professors) having a particular interest in such identity. This assumption, however, is certainly open to further questioning and further research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.