Abstract

Repeated crises have proven credit rating agency (CRA) models/methods erroneous and “business-as-usual” unsustainable. Nevertheless, considerable dubious “default risk” management and technoscientific capitalist expertise remain unchanged. Unpacking sovereign ratings, we appreciate how “debt sustainability analysis” (DSA) distortions underpin expertocratic CRA (default) anomaly. Their neoliberal “politics of limits” performance helps market (shareholder) imperatives trump those of democratic (stakeholder) politics. Given surging inflation and debt (distress) to remedy Covid-19-induced shocks, ratings aid constitute and (re)validate the subjectivities/affinities and organizational conditions advancing a “self-equilibrating,” “self-generative” agencement political economy of creditworthiness (PEC). Antagonizing sustainable budgetary government’s programmatic/expertocratic and operational/democratic asymmetry, econophysics ratings diminish fiscal sovereignty. Universal PEC management through hybrid credit risk/uncertainty qualculation mitigates negative externality contestation shielding CRAs from serious reform. Ratings procyclicality and contagion reinforce this precarious sociotechnical agencement PEC as the status quo.

Introduction

Recurrent crises have proven neoliberal finance and democratic politics to be contested, uncertain, yet resilient. Neither did Anglo-American capitalism’s gravest existential threat since the Great Depression—2008 Great Recession/Global Financial Crisis (GFC)—signal its demise. Nor has its fallout, as it morphed into a sovereign debt crisis, whose austerity plagued the OECD to incite authoritarian populism (e.g., US Trump; UK Brexit), destroyed democratic chains of authority. Whether a “contested failure” (Best, 2014) or a “status-quo crisis” (Helleiner, 2014), given Covid-19 pandemic surging debt (distress)—OECD (2021) $19 trillion—PEC sustainability and systemic financial/credit risk face looming crises (IMF, 2022; IOSCO, 2020). Rising stagflation, income inequality, stagnant welfare, and dismal productivity aggravate “political risks,” plus zero-sum “deglobalization” (Birch and Muniesa, 2020; Svetlova, 2018). Should sharp long-term rates increases suddenly normalize, servicing record (total) global $296 trillion debt (355% debt-to-GDP—2021) (IMF, 2022) stresses fragile recoveries and national, democratic self-determination. “Business-as-usual” is unsustainable.

Unfortunately, I contend how a discredited “referentialist metaphysics” and predictive positivism of the natural/physical sciences (Maurer, 2002), or econophysics, blamed for precipitating and deepening severe corrections (e.g., 1997–98 “Asian Crisis”; GFC/Great Recession) (Krippner, 2011), exacerbates PEC instability and unsustainability. Taken for granted and promoted across financial enterprise, especially core operations like credit ratings, technoscientific “default risk/uncertainty” management expertise amplifies systemic (liquidity and valuation) dangers (Beckert, 2016). Despite reoccurring failures, which bankrupt other firms, Moody’s and S&P—who account for 81% of outstanding US ratings (PRI, 2022) (EU-73%)—emerge relatively unscathed, without substantial revision to methods or business. Targets for overdue reform (IMF, 2010), this comprehensive analysis reveals, CRA (default) anomaly and PEC “inertia” jeopardize democratic integrity and pandemic recovery.

Through the re-encodement of singular, socioeconomic uncertainties as aggregable, probabilistic measures, DSAs objectify the sovereign debt problem for portfolio securitization (Carruthers, 2013). Consequently, (disinflationary) neoliberal financial and democratic imperatives conflict. Suspect quantitative (quant) forecasting, notably (nonlinear) “environmental, social and governance” (ESG) datafication (IOSCO, 2020), compromises rebalancing the growing asymmetry between market (shareholder) “epistocracy/expertocracy”—knowledge-based expert rule—and national (stakeholder) democratic self-determination (Paudyn, 2014). Repeatedly, ratings threaten market and political failures. Yet, what accounts for CRA’s own expertocratic exemption from ruin and impedes amending ratings distortions? How does rating “default risk” bolster CRA reprieve from substantial reform? Ultimately, what are the repercussions of “business-as-usual” for sustainable fiscal sovereignty and financial stability?

Contributing to the “social studies of finance” (Lépinay, 2011; Mikes, 2009; Preda, 2009), through the “analytics of government” deconstructive/reconstructive tools (Best, 2014; de Goede, 2005; Langley, 2014), this paper problematizes rating constitution of the hegemonic (neoliberal) agencement PEC through hybrid “default risk/uncertainty” modality expertocracy (Callon, 2016). Combining assemblage and agency, agencements render PEC subjectivities meaningful and actions permissible (Deville, 2016). Sociotechnical devices of control and governmentality, ratings commanding capacity and utility intertwine with their “legitimate” production and circulation of the authoritative knowledge underpinning a seemingly “self-generative” agencement PEC (Lépinay, 2011). Divorcing technoscientific expertise from its politico-economic contexts, (micro-level) ratings align CRAs/investors with (macro-level) “transcendental,” “self-systemic/self-regulating” (Anglo-American) capitalism, particularly its preemptive temporal logics (Svetlova, 2018). Mutual franchise reinforcement results through the universal ratings scale (“AAA”-“D”), as uncertain PEC futures are captured, calculated, and then classified. Indexical authority facilitates ratings normative (neoliberal) referential/data infrastructure’s “distributed framing,” as creditworthiness “sociomaterial facticity” (Carruthers, 2013). Methods make markets and repeated valuations become social facts to leverage speculatively (MacKenzie, 2006). Rating “techniques of truth production” help reproduce an (artificial) “self-generative” PEC with (CRA) insulating effects.

Credit risk managerial modality econometric framing of DSA macroeconomic indicators (e.g., GDP/capita) monopolizes the sovereign debt problem’s definition (Moody’s, 2008/2019). Uncertainty eludes quantitative capture, however, demanding subjective estimations and contingent (claims) information about “satisfying ‘intertemporal budget constraints’ without defaulting,” or no “Ponzi new issuance financing long-term debt repayment,” DBRS’ analyst clarifies these “transversality conditions” (Best, 2014). Through hybrid (inductive/deductive) DSA qualculation, I indicate how quantitative (risk) calculations render qualitative (uncertainty) judgments about sovereign “debt-carrying capacity” equivalence, and vice versa (Cochoy, 2008). Increasingly, as “big data” and algorithmic trading compound time and cost constraints, this expertocratic agencement PEC prizes defensible, utilitarian risk calculus/geometrics (Gapen et al., 2008; Pasquale, 2015). Its universal modality across (multiple) expert domains assists enable and entangle mutual qualculative cognitive agencies in PEC materialization (Callon, 2016). Rating induces adequate cognitive interdependence, orienting the normative, analytical, and organizational expert convergence between CRAs, investors, and officials (Beunza and Stark, 2012). Synergies bolstered by their preemptive leverage reinforce this “conformity bias” sustaining agencement PEC status quo (Dittrich, 2007). Yet, a (false) confidence about market transparency, expectations, and asset class safety/liquidity (Dorn, 2012), especially among yield-starved, “passive” (index-tracking) asset managers, breeds due to diligence complacency and “herding” (Krippner, 2011).

While validating a neoliberal “politics of limits”—parameters defining fiscal sovereignty—I illuminate how ratings econophysics PEC depoliticization invalidates and marginalizes alternatives (Paudyn, 2014); or counter-agencement (MacKenzie, 2011). Counter-performative ESG datafication misfires amplify systemic financial and climate-related dangers, plus debt/democratic distress (Graeber, 2011). My in-depth study traces how sociotechnical rating constitution of PEC subjectivities, organizational affinities, and qualculative conditions (evidential spaces and cultures) masks contingent liabilities enough to shift/absolve responsibility (Mikes, 2009). Arguably, this expertocratic agencement exempts CRAs from serious contestation and reform.

Compounding corporate “myopia,” regulators like the European Securities and Markets Authority (ESMA) or US Securities and Exchange Commission (SEC) require/sanction technoscientific (sovereign) DSA risk validation (Paudyn, 2015). Inherent (reflexive) DSA/financial self-referentiality aggravates PEC intractable valuations, limiting effective governance (Preda, 2009). My better understanding of this black box paradox shows how the OECD’s democratic legitimacy crisis inciting populism is also self-inflicted: a negative externality of (quant) risk measurement overdependence to enhance transparency and preempt/correct capitalist excess (Dorn, 2012). Eager to rectify, but avoid political interference in rating analytics, ESMA/SEC seeks scientific objectivity and overemphasizes risk validation (Paudyn, 2015). Inadvertently complicit in depoliticizing the “politics of limits,” regulatory passivity suggests superficial CRA contestation.

Deconstruction problematizes how DSA qualculation skews “default risk/uncertainty” synthesis to render sovereign creditworthiness intelligible: “legitimate” authoritative knowledge implicating CRAs in sociotechnical agencement PEC performance. I clarify how Moody’s “dynamic cohorts” and S&P’s “static pools” “through-the-cycle” (TTC), plus newer “through-a-crisis” (TAC), platforms mediate PEC potentiality and materialization. Reconstruction reveals the obscured relationship between credit risk/uncertainty instrumentality, its counter-performative intensification of financial vulnerability, and the repercussions for national self-determination. Re-embedding this technoscientific agencement in its debt politics exposes how it naturalizes a crisis-prone (neoliberal) “self-generative” PEC threatening populist backlash. Cyclical rebalancing, consequently, may intensify elite expertocracy to “redress” populist follies (e.g., Brexit).

Subsequently, the article examines deficient, conventional (CRA) market failure accounts, plus ratings referential/data infrastructure. Second, PEC performance principal dimensions are analyzed: rating methods and outcomes. Three credit risk/uncertainty management elements facilitate PEC plasticity: conditionality, reactivity, and interactivity. Finally, how “contagion” and “procyclicality” amplify PEC “self-generation” triggering systemic crises concludes the study. Despite repeated failures, as demonstrated, rating performation induces sufficient qualculative (financial/fiscal) cognitions and reflexive agencies that keep ratings/CRAs relevant and a neoliberal agencement PEC resilient.

Methodology

The study of primary-source documentation and semi-structured interviews advance my contention. Analyzing PEC “inertia” normalization through CRA/rating intervention—leveraged through investment synergies—the scrutiny of updated methodologies, “outlooks/watches,” defaults reports, plus portfolio composition and security prospectuses provided initial comparative themes (e.g., CRA/investor DSA modeling/validation). Supplementing documents, CRA staff insights reveal a richer explanation of scoring. Several meetings with David Levey (MDL), Managing Director (Retired) of Sovereign Ratings (Moody’s), James McCormack (FJM), Fitch’s Managing Director and Global Head of Sovereigns, and a Dominion Bond Rating Service (DBRS) fixed-income analyst clarify analytics, deployment; including official and industry relations. The subscription to “robust risk measures” helps define CRA expert mentalities/mechanics, and the broader asset management correspondence underpinning agencement PEC financialization.

Concurrently (March 2012–December 2018), 25 (hourly) open-ended interviews with London and Toronto portfolio, bank, and fixed-income managers underscore analytical and empirical (CRA/rating) parallels. Assets under management (AUM) size, returns on investment (ROI), and diversity determined selection. Worldwide the quickest-expanding and Europe’s largest fund manager ($8.4 trillion AUM), Vanguard’s Head of Credit Research-Europe, Michael Pollitt (VG1), explains DSA modeling/methods, indexing/benchmarks, plus portfolio construction. Several sessions elaborate rating impact on bond market trends, including agencement PEC organizational dynamics. For a “holistic account” of fund strategies, Nick Eisinger (VG2), Vanguard’s Co-Head of Active Fixed Income Group, clarifies hybrid risk/uncertainty qualculative techniques, rating deployment, and ESG securitization.

Complementary (three) meetings regarding (default) modeling/metrics, especially ESG/“political risks,” involve a Country Insights for Roubini Global Economics/Continuum Economics (former) Managing Director (RGEM) and credit risk analyst (RGE1). DSA parameterization, validation, and strategic asset allocation disclosures by CI Financial’s asset manager and trader (CIF1/CIF2) confirm (CRA) commonalities. Further comparative conclusions derive from investment explanations by (three) national bank brokers (BB1/BB2/BB3)—off-premises. Upon request, anonymity is preserved. Preparation involved examining firm outlooks, technical/quarterly reports, plus prospectuses.

Unless declined, interviews were recorded and (dataset) transcribed using thematic analysis. Initial textually formulated themes were revised, as necessary, to reflect illuminated rating expertise, assessments, and investment practices. Empirical and analytical synthesis influenced chosen themes. Since this interdisciplinary study surpasses simple (auto)coding, manual codes include passive/active management; sovereign debt sustainability; quant financial expertise; and ratings referential/data infrastructure. Extensive (interview) notes and follow-up sessions verified statement details. Similar rating analytics/mechanics facilitated organizational cross-examinations and categorizing evaluations. Their operational affinities foster harmonization effects shaping PEC-defining investments and materiality.

Market failure

Given the pandemic’s “unprecedented shock,” global FDI (2020) plunged by 35% ($500 billion)—rebounded in 2021 (IMF, 2022). Again, central banks drove risk appetites through historically low-interest rates: like 2008–16, the US Federal Reserve funds rate decreased to 0–0.25% (March 2020). Negative rates/yields may cause more problems (e.g., moral hazard; “everything rallies”) than solve. Profits are privatized, but costs are socialized through $15 trillion “quantitative easing” (QE) (IMF, 2022)—Fed’s $8.77 trillion (January 2022) balance sheet enlargement. Surging debts, including Europe’s €3.6 trillion (2020) issuance, yet uneven recoveries compromise sustainable creditworthiness. Cheap credit chasing alpha—risk-adjusted active/excess return—fuels “rich” valuations, inflationary pressures, and financial vulnerabilities, which (crisis-prone) ratings exacerbate (IOSCO, 2020).

Three market failure accounts preoccupy conventional CRA/rating critiques: large macroeconomic externalities; agency and ideological problems, including poor judgment; or improper methods/models (Eijffinger, 2012; Reinhart and Rogoff, 2010; Stiglitz and Heymann, 2014). None completely or adequately explains their authoritative capacity and longevity. First, CRAs cannot fully account for how their actions designed to mitigate (credit) risk often amplify systemic dangers (Reinhart and Rogoff, 2010). Complete prescience in complex financial systems is impossible. Neither does rating produce tangible (negative) externalities directly attributable to S&P or Moody’s. Nor is precisely forecasting authoritative market knowledge circulation, regeneration, and sedimentation feasible. DBRS and FJM echo MDL that “ratings are informed opinions – not statements of fact.” Yet, “to grant the entire process material, statistical significance,” Fitch’s (2014: 6) Sovereign Rating Model (SRM) “uses empirical data, [and] does not allow for judgmental analyst input.” Incorporated discretion, nevertheless, defines the (bylaw-enforced) creditworthiness sociomaterial facticity actualizing (neoliberal capitalist) referential/data infrastructure prescriptions. Their repercussions threaten fiscal sovereignty and democratic legitimacy (Svetlova, 2018).

Second, excessive preoccupation with CRA institutional agency or capitalist “inertia” renders the problematic path dependent on official endorsement (Coffee, 2006). Vilified agents of “finance” (Sinclair, 2005), CRAs' ideological and judgmental errors’ (indirect) negative externalities subjugate populations. Ontological questions about intentions, causality, or incentivizing “correct” conduct burden us, but lack resolutions. No true creditworthiness essence exists to unearth or evoke as the “gatekeepers” “regulatory license” threshold (Partnoy, 2006). Instead of assuming ontological coherence or regulation, I trace how a ubiquitous, shared DSA mentality/mechanics expertocratic conditioning privileges (austere) agencement PEC social facticity financialization. Across temporal investment portfolios, ratings facilitate the convergence of debt normality/rectitude expectations and organizational conduct engendering PEC materialization.

Conflicts of interest linked to “issuer-pays model” incentive structures mainly ensue when CRAs blindly adopt Wall Street’s “collateralized debt obligations” (CDO) risk models, which precipitated the GFC (Gaillard, 2012). Despite ambitions “strengthening analytical independence from issuer influence”, S&P (2021b: 2) “does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.” I reveal how rating monopolization with technoscientific (certainty equivalence) verification/validation jeopardizes efforts. Compromising autonomy, risk-leveraged ratings distributed cognitive interdependence induces sufficient normative, analytical, and organizational expert convergence pressures institutionalizing a “self-generative” (disinflationary) sociotechnical agencement PEC (Beunza and Stark, 2012). Forthcoming sections demonstrate how commercialized hybrid DSA techniques constitute and validate corresponding reflexive ontologies/organizational affinities through common risk calculus (Deville, 2016). Referential congruity effects compensate for deviation (Dittrich, 2007). Initially, PEC uncertainty-induced (ratings) adherence provokes mimetic responses, reducing poor judgment costs. Rating risk legitimized standardization, moreover, exerts (neoliberal) normative pressures. Particularly pertinent with elevated inflation (e.g., US 8.5%—Q1 2022) (IMF, 2022), broad compliance (temporarily) mitigates major consequences and insulates financial expertocrats, including CRAs (Paudyn, 2014).

Third, as an application problem involving tangible phenomena calculations (Löffler, 2013), ratings are considered neutral instruments measuring a pregiven, ontological (creditworthiness) reality (Afonso et al., 2014). Apolitical DSA econometrics employ fallacious dichotomies, economistic (power) conceptions, abstract agency, and (static) causality notions. Risk and uncertainty are juxtaposed as synthesizable or displaceable concrete matter (Eijffinger, 2012). Hybrid DSA qualculation “transforms” (idiosyncratic) uncertainty into a measurable risk propensity. Treating ratings as brute facts or opinions, like CRAs, mainstream accounts divorce technoscientific expertise from its politico-economic contexts (see Lowe, 2002; Stiglitz and Heymann, 2014).

This “instrumentalist rationality” shares affinities with (corporate) utilitarian risk calculus/geometrics fixation, especially its “referentialist metaphysics” and predictive positivism, on maximizing (credit) risk’s financial disintermediation, securitization, and trade (Langley, 2014). Reinforcing this sociotechnical agencement, similarly, S&P’s (2017) Rating Analysis Methodology Profile (RAMP) relies heavily on parametric statistics to backtest “institutional” factors, including elusive “sovereign debt repayment cultures” and (ESG) “legitimacy discourse.” “Following initial calibration,” FJM reports, (Fitch’s) “SRM econometrics ‘legitimate’ linear regression analysis leads the process,” whose “neutral verification contributes to material, statistical significance and detached commentary.” Granted independent observer status through DSA expertocracy, CRAs/investors assume a privileged position relative to the scrutinized objects: nation-states.

Acknowledging transparency’s significance in performance (risk) measurements (Mikes, 2009), yet a problem replicating financial model results (Svetlova, 2018), sovereign ratings resemble “fugitive social facts” or “black boxes” (MacKenzie, 2006; Pasquale, 2015). Overly secretive and technical internal structures make them opaque to outsiders. Rather than bankrupt CRAs, however, Partnoy (2006: 61) considers ratings an “unusual paradox” since: rating changes are important, yet…possess little informational value…ratings do not help parties manage risk, yet parties increasingly rely on ratings…are not widely respected among sophisticated market participants, yet their franchise is increasingly valuable.

Unpacking ratings anomaly through deconstructive/reconstructive tools, my better account of this enigma explains CRA survivability of repeated crises via rating facilitation of agencement PEC plasticity. Sovereign creditworthiness objectification and commercialization through risk/uncertainty expertocratic modalities bolster ratings/CRA authoritative utility and organizational affinities. Constitution of principal PEC players and conditions validates their neoliberal “politics of limits,” thereby compensating for failures (Best, 2014).

Referential data infrastructure

Similar to Preda’s (2009) study of the stock ticker precipitating new arbitrage calculations, or Lépinay’s (2011) research into derivatives trading reliance on geometric Brownian motion, I reveal how ratings scales “[construct] data that, owing to their format, [produce] specific effects of cognition and action,” which “distribute their calculative activities” (Callon and Muniesa, 2005: 1237). “Illocutionary” performatives, especially “junk” downgrades (below “BBB−”), ratings are easily distinguishable utterances/scores, whose indexical authority communicates creditworthiness judgments (MacKenzie, 2011). “Significant ‘indices constructors’,” VG1 observes, “CRA investment-grades define indices design…against which funds are benchmarked.” Their distributed referentiality facilitates “generating income streams from bond’s present (fair) valuation of discounted future cash flows and face/par values,” VG1 clarifies, through heterogenous PECs’ synchronic connection, comparison, securitization, and trade. Notwithstanding failures, hegemonic risk management/discourse (re)empowers ratings indexical illocution with an aggregating “sovereign” character (re)legitimizing their actionable capacity to influence PEC conduct, by assigning it meaning (Callon, 2016). Action and authority combine to “govern-at-a-distance” (De Goede, 2005), as these sociotechnical vehicles drive agencement PEC distribution and performance: “perception is reality.”

Leveraged through their (ordinal) scale, as expected value variance from “AAA,” ratings naturalize the development of budgetary deviance and debt normality/rectitude causal knowledge (Sinclair, 2005). Re-encoding fiscal relations according to “transcendental” (Anglo-American) capitalist logics, econophysics DSAs (re)align them with its automatic, “self-systemic/self-equilibrating” dynamics promoting “self-generative” PEC performance (Maurer, 2002). Framing the sovereign debt problem, this expertocratic agencement PEC elevates “supply-side” economics above “demand-side” management to curb deficits, stabilize prices, protect asset values, and suppress interest rates (Beckert, 2016). Ratings referential infrastructure constitution reinforces ratings/CRA authoritative (financial) utility and durability, fostering mutual correspondence across corporate enterprise, from accounting (Mikes, 2009) to trading (Binici et al., 2020).

Hybrid DSA qualculation conditions this expertocratic (CRA/investor) cognitive agency of debt investment, along with budgetary policies (Deville, 2016), as “normal and taken-for-granted business practice” (Carruthers, 2013: 17). Successfully rendering (idiosyncratic) fiscal contingencies amenable to (universal) predatory risk investment, without tangible liability, ratings referential/data infrastructure dissemination induces (varied) investor and official cognitive interdependence and conduct convergence (Beunza and Stark, 2012; Helleiner, 2014). BB1 acknowledges: Basel II [credit risk] Standardized Approach business modeling compatibility helps scores shape the overarching referential framework defining expectations and trade triggers, boosting index-tracking ROI…thereby, despite fueling “rich” valuations…enhancing expected portfolio value maximization.

Widely internalized as creditworthiness (sociomaterial) facticity constituted and legitimized via technoscientific expertocracy, plus bylaws/statutes, rating indexicality intensifies this agencement PEC normative, analytical, and organizational expert congruence (Callon and Muniesa, 2005). Potentially reducing the scope for poor judgment, namely speculating against market trends, nevertheless, this cognitive interdependence heightens herding and “cliff effects” (Lowe, 2002).

“Self-generative” performance

Convention claims that effective credit risk analysis should:

1. Identify existing balance sheet mismatches.

2. Incorporate uncertainty…since uncertain changes in future asset value…ultimately drive default risk.

3. Translate uncertainty into quantifiable risk indicators [to] measure risk exposures (Gapen et al., 2008).

Communicated via ratings identifiable scale, the uncertainty of (idiosyncratic) fiscal failure is qualculatively re-encoded as “default risk.” Hybrid risk/uncertainty DSAs help CRAs (and funds) blur and map (inductive) “bottom-up” (fundamentals) reduced-form/intensity (Duffie and Singleton, 2003; Jarrow and Turnbull, 1995) with (deductive) “top-down” structural credit risk models (Black-Scholes, 1973; Merton, 1973). Modality manipulation “transforms”/misrepresents uncertainty into/as risk, thereby masking contingent liabilities and expert accountability (Carruthers, 2013). Forthcoming sections document how quant DSA mechanics “(re)legitimize” this (discredited) discretionary epistocracy crucial to accommodating/incorporating heterogenous fiscal relations: government through uncertainty (Best, 2014). By constructing the preemptive (artificial) budgetary uniformity and debt normality facilitating sovereign creditworthiness securitization, technoscientific ratings render normative social facts to leverage speculatively.

Market outperforming “sustainable investments,” including $269.5 billion “green bonds” (2020), increasingly concern regulators, (democratic) stakeholders, and investors (e.g., BlackRock) (Moody’s, 2020b). Accordingly, qualculative ESG contingencies adjustments prove paramount to financial prosperity, decarbonization for net-zero emissions, without inciting (PEC) instability. The UN Principles for Responsible Investment (PRI, 2022) network’s ESG in Credit Risk and Ratings Initiative involves 180 investors, $40 trillion in AUM, and 27 CRAs. Qualculation facilitates “Vanguard’s Capital Markets Model (VCMM)/Sovereign Dashboard’s (VSD) rating replication of broad ESG factors relevant for determining bond market valuations and alpha generation,” reckons VG2. I contend how similar hybrid DSA methods and (contagion-/procyclically reinforced) rating outcomes, produce positive, synchronizing feedback loops/reflexivity entangling CRAs in ostensibly “self-generative” PEC (status quo) performation (Callon, 2016).

DSA qualculation blends quantitative/qualitative analyses to (re)engage CRAs in self-referential verification processes, which implicate them as agencement PEC subjects/experts. Ambitious to replicate predictive positivism—fundamental to prescriptive authority—defensible econometric modeling is routinely privileged over discretion in “physical default probability” calculation (Fitch, 2021). MDL clarifies that “‘physical’ means ‘real world’ default probabilities…without risk aversion premiums,” namely displaceable or synthesizable (exogenous) brute facts. PEC surveillance, increasingly, deploys complicated quant models, strategies, and instruments (Krippner, 2011). Highly educated physicists/quants are imported into corporate enterprise (Pasquale, 2015). Previously “completing three CERN Geneva ‘Large Hadron Collider’ postdocs in quantum mechanics,” BB2 “recognized the [Heisenberg] uncertainty principle in portfolio valuations”; or predicting exact simultaneous (position and momentum) geometrics. “Regulatory demands and investor appetites for quant [defensible] ‘equivalence’ validation and technical proficiency reinforce risk’s mutual [speculative] utility,” RGE1 reports. Divorcing technoscientific expertocracy from their own/targets’ operational, politico-economic contexts, CRAs assume independent, objective observer status, however invalid and unsustainable said exemption.

Purporting scientific objectivity, Moody’s Steps or S&P’s RAMP hybrid risk/uncertainty DSA conditionality, reactivity, and interactivity serve to generate “credible” PEC self-referential cognitions, which foster organizational interdependence (Garland, 2003). Subsequent sections problematize how DSA methods enable and entangle CRAs (and investors) in mutually reinforcing reflexive effects, thereby implication in neoliberal agencement PEC governmentality relations. CRA PEC oligopoly helps common sociotechnical DSAs induce sufficient analytical, organizational expert convergence (Dittrich, 2007). Consequently, parallel rating feedback intensifies expert agency and “self-generative” PEC performance (Paudyn, 2014). Contagion and procyclicality advance ratings programmatic translation into material fiscal reality, embedding (neoliberal) capitalist rectitude and debt normality dominance, as austere “politics of limits” (Deville, 2016).

Risk/uncertainty conditionality, reactivity, and interactivity

Hotly contested, “default risk’s” definition highlights hybrid DSA qualculation’s three dimensions: conditionality, reactivity, and interactivity (Garland, 2003). Rare sovereign failures preclude a clear understanding or unequivocal econometrics reliance (Eijffinger, 2012). Acknowledging variances, I show how proprietary DSAs align creative entrepreneurial freedom through uncertainty modes, with quant risk calculus/geometrics. Together this expertocracy conditions CRA subjectivity and forges financial agencement PEC affinities, plus liability/default “exemption.” DSA uncertainty management facilitates organizational CRA qualculative cultures and self-understanding impulses (Mikes, 2009). Simultaneously, universal risk calculus/discourse parameterizes discretion enough to normalize DSA/PEC congruity.

First, conditional risk/uncertainty modality DSAs fulfill context-specific objectives predicated on predefined parameters. Despite denying “predictions,” Moody’s Steps, S&P’s RAMP, and Fitch’s SRM target (physical) frequencies of fiscal failure via (lognormal distribution) Brownian geometrics. Adopted from particle physics, Brownian motion entails the random movement of tiny particles from collisions with surrounding molecules (MacKenzie, 2006). Although FJM underscores econometrics, as forthcoming sections dissect, discretionary DSA “selective shocks or policies conditional occurrence as stress events influence [TTC/TAC] model indicators,” MDL explains. Given such reflexive/self-referential estimations, interviewed investors acknowledge how repeated stress-/backtest manipulation validates plausible model coefficient accuracy—evidenced by T-statistics or analogous measures (Pasquale, 2015). With “client pressures to hit targets, and [SEC/ESMA’s] rigorousness, transparency, and consistency demands,” CIF1 “expects data technicals to produce high-density pictures.” Never explicitly parameterized, qualculative model recalibration disguises incorporated discretion instilling the impression of neutral-tool verification (Gaillard, 2012). This conditional expertocracy bolsters rating synergies, adoption, and exemption.

Second, risk/uncertainty mode DSAs are reactive because preceding, changing circumstances, plus rating committee/analyst subjective interpretations, affect analyses. Indicative of financial forecasts (Preda, 2009), CRA “extrapolations from past experiences are always inferences from a limited dataset using premises (about cause and effect, factors involved, ceteris paribus)” (Garland, 2003: 53). Dynamic (ESG) conditions challenge DSA econophysics “ergodicity”—political economy fails to repeat itself at regular intervals. “Geopolitical” (e.g., Russia–Ukraine conflict) or “domestic political” (e.g., terrorism) dangers evade simple codification as probability distributions and confidence intervals (Moody’s, 2008/2019). Limited datasets mean interpreting contestable (ESG) figures about sovereign payment ability and willingness. Sociotechnical agencement PEC alignment, however, naturalizes qualculative rating revisions which reflexively implicate their authors (Cochoy, 2008). Prone to institutionalizing dubious heuristics, (CRA) cognitive biases (e.g., confirmation) and systematic errors result.

Finally, risk/uncertainty rating interactivity conditions DSA adjustments and PEC commercialization. ESG flux demands due diligence to reassess CRA weighted factors/sub-factors. Only “approximations of their importance for rating decisions,” their “actual importance may vary substantially” (Moody’s, 2019a: 50). Critical analysis is necessary when adopting the externally sourced average percentile rank of main World Bank Worldwide Governance Indicators (WGI): Voice and Accountability; Political Stability and Absence of Violence/Terrorism; Government Effectiveness; Regulatory Quality; Rule of Law; and Control of Corruption. Yet, FJM and MDL report incorporating WGIs, notwithstanding their “opacity,” “construct validity,” “margins of error,” or various data sourced estimates. Just as inexpensive forms of out-sourced due diligence, external ratings appeal to “passive” investors, so does IMF-/World Bank-performed homework entice CRAs. Reinforcing cognitive interdependence, consequently, it amplifies inconsistencies and failures.

Next, once issued/commercialized, ratings programmatic compliance is reflected by sovereign and bond market convergence, which CRAs monitor. Corresponding fiscal consolidation facilitates its disinflationary PEC materialization (Graeber, 2011). By lowering/elevating borrowing costs, bond market feedback validates their prescriptions. Analyzing EU yield spreads (1995–2010), Afonso et al. (2014) demonstrate their bi-directional causality with rating announcements. Even post-GFC, despite some “discounting,” Binici et al. (2020) observe statistical significance between announcements and (55 states) credit default swap (CDS)—derivative contract—spreads. Risk premiums often jump with “arbitrary” downgrade contagion and procyclical self-fulfilling prophecy processes enacting rating judgments (Gärtner et al., 2011; Merton, 1973). Beyond mechanistic prophecy, this study indicates how ratings foster PEC cognitive interdependence. Qualculative expertocracy helps engender enough analytical/organizational accordance between CRAs, treasuries, and investors to reinforce ratings PEC performance. Normative agencement PEC convergence further constitutes its material “self-generation” (Callon and Muniesa, 2005).

Qualculative expertise

Next, I trace how said three dimensions of risk/uncertainty modality DSA assist induce CRA self-referential cognitive agency, with (regulation-reinforcing) self-validating expert effects (de Goede, 2005). Whereas S&P’s RAMP (2017) privileges default probability with payment willingness, MDL confirms that Moody’s Steps (2008/2019) evaluates expected loss and payment ability, while FJM integrates them. Deconstruction of Steps “dynamic cohorts” and RAMP “static pools” TTC/TAC platforms reveals the CRA reflexive feedback loops mediated through these methods. Transforming (future) debt contingency into ergodic risk for (present) discounted valuations, as Best’s (2014) “technocratic exceptionalism” account, TTC/TAC expertocracy manipulates creditworthiness temporality. Particularly appraising long-term ESG uncertainties through shorter-term DSA metrics (PRI, 2022), CRAs deploy stochastic processes in continuous-/discrete-time hazard modeling (Löffler, 2013). Indicative of (math/natural sciences) technoscientific model validation techniques, this geometric averaging of fair-value CDS spreads (FVS-CDS) provides forward-looking estimations whose “legitimacy” portfolio managers recognize and employ (Svetlova, 2018).

Broader quant/technoscientific finance boosts expertocratic agencement PEC/CRA performance. Akin to Lépinay (2011), MacKenzie (2006) contends how fair option pricing is determined by the Black-Scholes-Merton framework’s geometric dependence. Similarly, as market-based estimates of physical default probability, Moody’s Analytics (2010) Expected Default Frequency (EDF) incorporates Brownian motion. Insufficient data, however, hampers parameterizing sovereign ESG “default risk” as geometrics/physics or corporates. Thus, CRAs and investors disclose qualculatively blurring and mapping (statistical) reduced-form/intensity modeling (Duffie and Singleton, 2003; Jarrow and Turnbull, 1995), with (option-theoretic) structural approaches (Black-Scholes, 1973; Merton, 1973).

Precision, pricing, and hedging may be “bottom-up” (exogenous) reduced-form/intensity modeling advantages (Gapen et al., 2008). Contingency, however, including future cash flows, constrains formulistic fundamentals analyses. Yet, no obvious referential (sovereign) asset value hinders “top-down” (endogenous) structural methods. Inadequate data or inconsistent reaggregation notwithstanding, hybrid DSA qualculation’s inductive/deductive blending compensates. Comparability may trump accuracy, which defines ratings discriminatory power, especially with excluded or random key qualitative factors (Lowe, 2002). Obscuring contingent liabilities, geometric validation helps shape reflexive (expert) CRA cognitive agency (Paudyn, 2014). “Lacking serious public scrutiny into rating analytics, which are a sham…yet increasing pressures for quant metrics,” MDL notes, cursory official oversight, arguably, sanctions DSA contrived creditworthiness “equivalence.” Institutionalizing technoscientific validation, the article argues, this underpins “self-generative” agencement PEC/CRA performance, with insulating effects.

Moody’s Steps

In 2002, Moody’s acquired (quant) credit risk heavy-weight KMV (Kealhofer, McQuown, and Vasicek). Derived from Merton’s (1973) structural diffusion model, “KMV’s ‘point-in-time’ (PIT) ratings expertise… including its renowned cardinal [numeric] KMV EDF9 measure…considerably bolstered Moody’s market position,” RGEM affirms. Vis-à-vis traditional structural models, MDL recounts, KMV’s: vast resource combined 30 years of default data for 60,000 public and 2.8 million private companies…KMV’s superior [predictive] performance [has] helped Moody’s pioneer integrated solutions to enhance most elements of credit processes, from prospecting, underwriting to pricing, syndication, and securitization.

Its usage by 40 of the world’s 50 largest financial firms further fosters the analytical/organizational synergies reinforcing Moody’s/CRA epistocratic (liability) exemption.

Through Moody’s Steps “scorecard” (Figure 1) application, qualculative EDF conditionaity, reactivity, and interactivity enable expertocratic CRA/investor organizational cognitive agency. Moody’s summational reference “scorecard.”

Extending KMV’s/Black-Scholes-Merton’s corporate framework, Moody’s CDS-implied EDFs (CDS-I-EDF) are PIT measures conditionally adjusted for “loss given default” (LGD) and risk’s market price (MPR) (“market Sharpe” ratio) (Moody’s Analytics, 2010). Sovereign expected loss rates are functions of default probability multiplied by loss severity, or recovery rate. Rare, convoluted sovereign failures, however, impair EDF realized recovery data (Gapen et al., 2008). Investors like Ashmore who retained Lebanese bonds before Beirut defaulted (09 March 2020) on $1.2 billion found seized markets offering 28 cents on the dollar. Therefore, (sovereign) conditional LGD is 75% and MPR reflects US investment-/speculative-grade corporates (Moody’s Analytics, 2010). “Preferred model specifications,” MDL indicates, “determine the appropriate loss or risk function like forecasting or hypothesis testing.” Expanded to nonequity issuers, LGD assumptions help invertible DSAs derive FVS-CDSs from (selective) EDFs. Model-implied and risk-neutral, default probabilistic conditionality grants sovereign ratings precision optics more available with greater corporate failures (Paudyn, 2015). Objectivity effects reinforce PEC/CRA performance.

Bond default forecasts estimate expected realized maturities from historical data. Moody’s (2020a: 37) “highly stylized” DSA “idealized default and LGD rates” are (nonrandom) “common fixed benchmark parameters” imposed on EDF future dynamics. Cumulative EDF qualculation assumes transitional matrix “stationarity” (perfect markets) when capturing ESG/PEC input interdependencies. Albeit “sensitivity scenarios” claim to “measure” assumption relevance, questionable EDF continuous, frictionless (sovereign) asset tradability conditions plague (corporate-inspired) DSAs. Conditional “idealized rates,” arguably, precipitate arbitrary (hybrid) EDF “case-by-case…stylized” qualculation (Moody’s, 2019a). Notional model inputs/assumptions may “bring a degree of stability, consistency, and transparency to something that may in practice be uncertain” (Moody’s, 2020a: 35). Unfortunately, tensions with “rating committee judgments…not intended to be applied consistently and systematically” downgrade practical applicability (Moody’s, 2020a: 36). “Troublesome with unique sovereigns,” MDL explains, “inadvertently…this promotes an over-reliance on model-centric analyses difficult to relinquish when ubiquitous”. Generalized model-driven scoring compromises (PIT) accuracy (Maurer, 2002).

Imperfect knowledge, delayed disclosures, or public accounts misreporting frustrates stochastic asset dynamics (structural) modeling (Duffie and Singleton, 2003). Governments, as Greece demonstrated, may manipulate financial statements. First, to satisfy 2001 EMU convergence criteria, “creative accounting” inflated Greece’s 2001-03 social security surplus by €2.8 billion. Next, the European Commission (2021) denounced Athens for “deliberately misreporting figures” after its original 3.7% (April 2009) fiscal deficit’s revision to 12.5% (October 2009). Combining specific sovereign knowledges with (interactive) financial (FVS-CDS) price movements, EDF qualculation misrepresents uncertainty as risk to incorporate bold assumptions and neglected factors (Svetlova, 2018). Expertocratic reflexive/self-referential effects ensue.

Contestable incentives falsifying figures, political willingness to honor obligations (e.g., Ecuador 2008), or geopolitical strife (e.g., Russia–Ukraine war) thwarts econophysics DSA. Thus, my study deciphers how ad-hoc reduced-form/intensity modeling mediation with (diffusion process) structural assessments “validates” technoscientific DSAs/EDFs. Continuous-duration estimation TTC EDFs mechanistically assign (market) unobserved (structural) sovereign debt valuation elements Brownian motion dynamics (MacKenzie, 2006). Total debt postulates temporally homogenous DSA predictive positivism. Default risk materialization is geometrically calculated through Black-Scholes (1973): perpetual put-options on sovereign asset values. Moody’s TTC EDFs are “distance-to-default/-distress” (DD) functions—the trend plus cyclical components, or the standard deviations whereby assets exceed liabilities (Duffie and Singleton, 2003). Multi-year, annual calculations track identical DD-profiled sovereign group defaults/exits. Whereas S&P’s “static pools” fail to adjust for mid-year rating withdrawals, Moody’s “dynamic cohorts” update regularly.

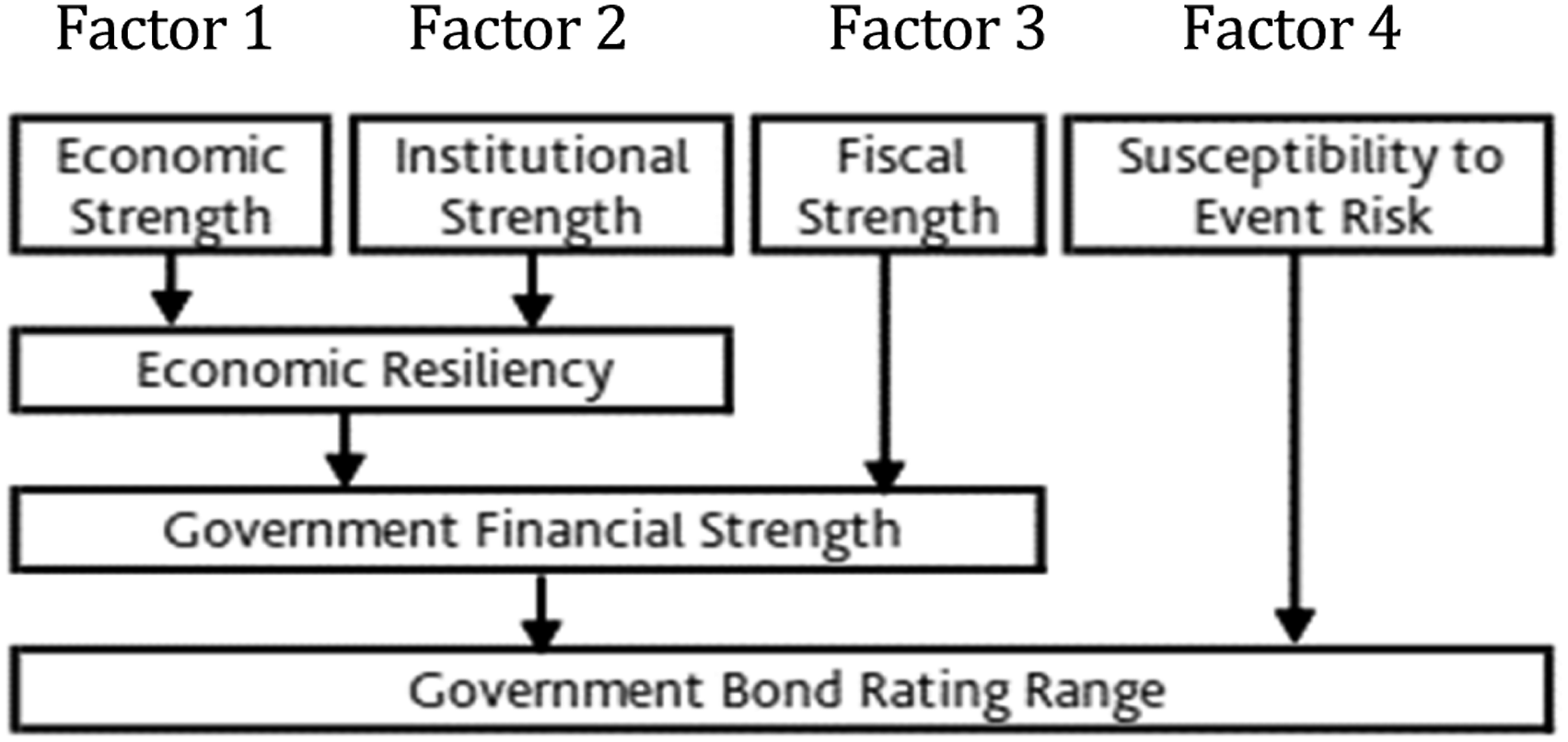

Incomplete mid-term defaults/withdrawals and survival bias information entails conditional, reactive, and interactive EDF effective cohort size estimations determine realized benchmark input parameters, especially Factor 4 “politics” that trigger 36% of defaults (Moody’s, 2020b). Intuitive, reflexive reactions to (ESG) “sudden, extreme events that severely strain public finances” (Moody’s, 2019a: 32), including random censoring (survival) premises, constitute Moody’s expert judgment/self-referentiality.

Mutual modality manipulation enables CRA self-verification through qualculative techniques, which entangle in wider expertocratic agencement PEC validation. Contrasting “real” (objective) risk against “false” (subjective) uncertainty, DSAs/EDFs initially establish, and next collapse, the (quantitative) risk versus (qualitative) uncertainty distinction. Allegedly, physical EDF’s “big advantage…isolates entities’ ‘true’ default risk from market ‘noise’” (Moody’s Analytics, 2010: 1), or arbitrary uncertainty management. Inconsistencies, including unavailable representative data samples necessary for backtesting, transitional matrices, or withdrawals, demand individual, incremental default (mid-year) modifications through (reflexive) uncertainty modalities. Masking contingent liabilities, EDF Brownian geometrics average issuer cohort experiences at monthly frequencies (Moody’s, 2020b). Qualculatively assigning conditional or reactive (ESG) adjustments (econophysics) dynamics, although randomly (p-value below 5%) censored data, aids “evidence” issued ratings and actual defaults correspondence. Reinforcing “expectations that ratings, on average, relate to subsequent default frequency,” MDL clarifies, future loss curves are anticipated from backtesting and payment ability. Sufficient prediction facilitates agencement PEC “self-generation.”

“Rare,” extreme shocks or “abnormal” market conditions (e.g., pandemic), however, elude Brownian motion-based asset process capture/verification. Managing fiscal idiosyncrasies via ergodic risk calculus, VG2 acknowledges “often portfolio optimization or stress testing model validation…against standard forecasting criteria…is unrelated to their use.” Qualculative DSA discrete-/continuous-time hazard model synthesis “reconciles” conflicts. EDF “equally weighted historical and forecast data” facilitates verifying geometric averages, compressing volatility, and smoothing out ratings (Moody’s, 2019a: 3). Desired DSA (ceteris paribus) parameterizing usually produces expected results. But given limited sovereign defaults/datasets, rather than proving causality, Moody’s mapping devises “default risk” correlations. Corporate CDS-I-EDF proxies help verify sovereign DD “robust” relationships. Together providing (conditional) EDFs automatic, “self-equilibrating” dynamics, feedback effects intensify “self-generative” agencement PEC/CRA performance.

Fixed-income investors interviewed prize TTC EDF “R-squared”—coefficient of determination—calibration. Its reproducible predictive positivism and more prudent rating migrations minimize costs/fees. Parallel geometric modeling “replicates the experience of a portfolio of both seasoned and new-issue bonds purchased in any given month” (Moody’s, 2019). Comparable statistical correlations allow funds and banks like Barclays to map CRA TTC ratings to internal PIT measures through Agency Read-Across Matrix scales. VG1 clarifies similar “VCMM/VSD cyclical smoothing techniques…plus market ‘closet indexing’ boost ratings” (interactive) analytical and organizational expert congruence effects. Proprietary modeling or ad-hoc mapping, however, fails to replicate enough matching scores to normalize unequivocal PEC performance.

Artificial conditionalities compound how interactive and reactive adjustments exacerbate the ill-defined/-operationalized speculative-grade range and downgrade arbitrariness—“what is left unexplained by observed previous procedures,” or econometrics (Gärtner et al., 2011: 3). Ratings distributed PEC cognitive interdependence helps procyclically feed market spreads and volatility. PEC stability suffers because arbitrary “junk” downgrades are also more susceptible to reversals. Between 1987 and 2011, 38 rating reversals occurred within 12 months of being issued—S&P accounted for 24. Most disturbing were the 20 default downgrades revised up (Gaillard, 2012). Budgetary havoc and frequent portfolio adjustments, which erase cost advantages like lower tax rates and fees, amplify—not dampen—market volatility “noise.”

While “building models is a costly exercise”—FJM reports that 40 analysts design Fitch’s SRM—Moody (2020a) recommends “multiple approaches” for “comparing baseline projections with stressed outcomes.” But because “there is no single formula for combining scores…to to arrive at a ratings decision” (S&P, 2021b: 93), sovereign “assessments [require] a combination of quantitative and qualitative factors whose interaction is difficult to predict” (Moody’s, 2008/2019: 1). Especially uncertain, FJM remarks, when: Brexit threatens to intensify zero-sum populism at the UK’s expense…growing acrimony over unavailable plans or costs (e.g., £350 million/week bus claim)…convinced Fitch to abandon any specific base case because no individual scenario has a high success probability.

Lacking OECD treasury transparency, and often accountability, laments FJM, key “frontier market” officials are “even more inaccessible and/or unreliable” than Brexiteers; or CRAs. Greater uncertainty mode DSA becomes vital to scoring “debt-carrying capacity”, which enhances (CRA) reflexivity/self-referentiality.

To mitigate arbitrary rating, Fitch’s (2021: 6) multiple regression SRM privileges “statistically significant (at 90% confidence)…empirical data/factors” and only “allows for very limited judgemental analyst input.” “Political factors are not incorporated into the SRM, but applied as qualitative overlay afterwards,” FJM remarks, as if (ESG) politics is binary arithmetic. Unfortunately, secretive proprietary modeling never reveals reactive or (IMF/WB) interactive DSA adjustments. Overemphasis on the (linear) “ordinary least squares” (OLS) calculation of 18 economic/financial variables also makes discretionary model outliers like “frontier” debt rare and disproportionately influential. Estimating unknown regression parameters, OLS minimizes the sum of square errors/residuals (deviation) between model predictions and observations to generate EDF-similar results (Duffie and Singleton, 2003). Constraining the informal DSA conditionality imposed on case-based cyclical components, or uncertainty management, qualculative OLS regression analysis diminishes proprietary standard/model deviation: expertocratic agencement.

Parallel technoscientific methods (outcomes) repeatedly feed back as CRA/investor self-validating expert effects (Paudyn, 2014). Post-GFC, MDL (and FJM) acknowledge that “expert judgment receives a greater audience”; just not much greater. Self-equilibrating econophysics verification of displaceable or synthesizable, exogenous facts distorts risk’s/uncertainty’s dialectical relationship and constant state of virtuality (Best, 2014). Upon occurring, once a static figure is available, it is a crisis—no longer its probability. Moreover, testing empirical veracity conditions an onerous search for ontological equivalence nonexistent in fiscal relations (de Goede, 2005). Moody’s (2008/2019: 1) concedes that a: mechanistic approach based on quantitative factors alone is unable to capture the complexity of the interaction between political, economic, financial and social factors [defining] the degree of sovereign credit danger.

Increased factor score granularity and sub-factor quantification, however, attest to “continuous efforts to make the analysis more quantitative” (Moody’s, 2008/2019: 6). Negating or skewing EDF (reflexive) adjustments black boxes how CRA risk/uncertainty mode expertocracy constitutes a (neoliberal) “self-generative” PEC referential/data infrastructure and sociomaterial facticity. Ratings expertocratic cognitive interdependence triggers bond yield and CDS spread movements, plus fiscal policies, shaping agencement PEC materiality.

S&P’s RAMP

S&P’s (2021b: 93) DSA considers “default likelihood—encompassing both capacity and willingness to pay—as the single most important factor.” Homogenizing sovereign alterity through dilution in “static pools,” akin to Moody’s or Fitch, S&P’s (2021b) RAMP emphasizes “common default behavior, measurement, and approaches to risk analysis.” For “debt-carrying capacity” comparison, S&P’s (2021a: 67): metrics treat all issuers equally and are not adjusted for size or influence. Therefore…a default by Argentina counts the same as a default by Mali, even though the latter has a much smaller economy.

Suffering another recession and liquidity crisis, Argentina’s ninth default (May 2020) rendered attempts to “reprofile”/restructure $65 billion of debt—almost four times Mali’s GDP—nearly collapsed. Upon canceling a record IMF $57 billion bailout, its (dispersed) $44 billion repayment stalled. Such panic of a potential full-blown economic/banking crisis severely straining solvency and regional stability, Mali could not trigger.

Repeated RAMP stress tests binomially distribute defaults annually conditional on identical cohort/independent sovereign probabilities (S&P, 2017). Cognate with Moody’s EDF, fixed (unobservable) parameters’ structural modeling may standardize absolute “likelihood” qualculation. Unfortunately, RAMP’s endogenous inaccessibility undermines Brownian geometrics risk neutrality. Unable to model spillover effects rigorously and consistently, S&P provides disembodied accounts of globally/regionally integrated and interdependent, but unique, political economies (Langley, 2014). Argentina’s November 2001 54-month (dollar-denominated) default triggered contagious regional shocks (Binici et al., 2020). Disregarding globalization’s (dis)integrating forces offers incomplete versions of neighboring defaults by Paraguay (February 2003), Uruguay (May 2003), Grenada (December 2004), and Venezuela (January 2005). Thailand’s 1997 woes infected Asian economies (Sinclair, 2005), while Greece’s default engulfed Europe’s ‘periphery’ (Gärtner et al., 2011). When Mali (2012) defaulted, few blinked.

Essentially (constant membership) “buy-and-hold portfolios,” by aggregating “marginal weighted-average default rates conditional on survival (nondefaulters),” S&P (2021a: 70–71) “static pools” TTC/TAC DSAs differentiate individual from cumulative (annual) default probabilities. Retroactively assigning default to all the issuer’s cohorts, RAMP’s universal 1975 start date mitigates temporal continuity problems. Multi-period comparisons produce 1-year transition matrices numbering 47 by January 2022. Arguably, S&P (2017) devises the historical frequency database enabling comparative (forward-looking) default distributions and confidence intervals. Notwithstanding “the small sample size results in less accurate readings” (S&P, 2021a: 46), especially since few sovereign rating records exceed a decade, said conditions facilitate stricter correlation claims: lower grades denote higher defaults. For econometric-based material significance, DSA qualculation accommodates limited data and disguises conditional, reactive adjustments defining reflexive CRA performance to “(re)legitimize” expertocratic exemption (Paudyn, 2014).

DSA survival conditions vary according to CRA surveillance through uncertainty. Moody’s Steps qualculation accommodates rating withdrawals, and S&P and Fitch ignore them. Constant RAMP identical pool probabilities oversimplify and homogenize idiosyncratic sovereigns, whose defaults’ strict binomial distribution lacks factual evidence (Duffie and Singleton, 2003). Standardized conditionality may enhance rating stability, and mask (reactive) hybrid risk/uncertainty management, but accuracy suffers. Unique sovereign willingness evades capture through simplistic, uniform DSAs.

“Comparative statistics are affected by the small number of rated sovereign defaults,” S&P (2021a: 11) echoes Moody’s, but given the “same rating definitions,” these should “converge with corporate ratios over time.” DSA reduced-form/intensity and structural modeling temporal manipulation helps mimic rating corporates. Higher (observed) company failures facilitate “static pools” econometric parameterization. Substantiating RAMP uncertainty modalities, thereby S&P’s expert self-referentiality, DSA qualculation overlap advances the market mentality about sovereign creditworthiness malleability. Transforming contingency into risk, technoscientific expertise heightens PEC command (Stiglitz and Heymann, 2014). Implication in “self-generative” agencement PEC performation and expertocratic validation, as sociomaterial facticity, intensifies ratings analytical, organizational affinities, extending CRA anomaly (MacKenzie, 2011).

To integrate sovereign heterogeneity, and calibrate credit risk granularity, RAMPs synthesize conditional, reactive, and interactive stressors. Hypothetical scenario endurance defines ratings “AAA” through “B” as benchmarks. For example, the (Great Depression) “extreme” conditions imposed for “AAA” witness GDP fall by 26%, possible 25% unemployment, and equities plunging 85% (S&P, 2021b). Next, “AA” stress tests must withstand a “severe” 15% GDP contraction, 20% unemployment, and stock indexes losing 70% (S&P, 2021b). Moderating with each lower grade, selective scenarios influence fundamentals and presuppose a referentialist econophysics (Maurer, 2002), whereby debt normality/rectitude is represented and assessed. Empirics inform TTC DD continuous-duration estimates. But RAMP reactive (cyclical) premises and interactive figures (e.g., WGI) erect artificial investment-/speculative-grade thresholds. Neither substantial nor unequivocal, but liable to error, revision, and/or suspension, (reflexive) DSA qualculation appraises fiscal contingencies and compensates for incomplete ‘static pools’ datasets to justify one notch upgrades/downgrades. Inducing expert, self-referential cognitive agency aligned with broader sociotechnical agencement PEC financialization, technoscientific RAMPs validate S&P’s expertise.

Cohorts/pools “peer comparison” methods expand PEC referential/data infrastructure distribution helping embed expertocratic cognitive interdependence (Birch and Muniesa, 2020). Attractive to investors and regulators, TTC RAMP smoothing produces (replicable) prudent rating migrations. Complementary TTC DD methodology, VG2 explains, aids VCMM/VSD: denote what is significant to understanding individual issuer differences and nuances…while maintaining consistency across sovereign scores…which ensures infrequent rating changes and reduces trading costs/fees.

Whatever Vanguard’s “aversion to positioning issuers in a rigid grid based on 25 metrics,” VG2 continues, CRA-similar DSA “technicals” (one-third of VCMM) like “monetary” and “economic” cycles, plus “fundamentals” (e.g., debt/GDP) (one-third) generate vast “data lakes.” Commonalities facilitate: replicating broad risk trends for enhanced Monte Carlo [random sampled inputs/variables] simulated return distributions…contributing to strategic asset allocation and ROI.

Collectively fostering interactive agencement PEC epistocracy, as inexpensive forms of out-sourced due diligence, “static pools” TTC ratings stability boosts (passive) investor internalization (Preda, 2009). Given a “notable patient-capital appreciation for their ‘buy-and-hold’ character,” BB2 reports ratings “close correlation with market-based indicators and macroeconomic developments.” “Self-generative” agencement PEC synergies constitute CRA expert subjectivity, mitigating major liability.

Long-term default horizons enhance rating stability primarily within selective TTC parameters. Absent independent verification, opaque (hybrid) risk/uncertainty qualculation preserves internal DSA/model consistency, assigning random (ESG) components Brownian geometrics (Löffler, 2013). However reactively necessary, TTC RAMPs/EDFs poorly capture permanent sovereign credit quality transitions (Afonso et al., 2014); especially ESG credit risk translation. Upon breaching that benchmark scenario, subsequent sections demonstrate, adjustment lags threaten procyclical herding and “cliff effects” (Kiff and Kisser, 2020). Arbitrary downgrades/upgrades and “outlooks/watches” amplify boom-bust cycles heightening systemic hazards: contractions or bubbles materialize (Lowe, 2002).

Since ESG political economy flux complicates sovereign assets’ fair valuation, option-theoretic structural approaches render DSA continuous-duration estimations. Black-Scholes-Merton risk-neutral valuation advantage bolsters technoscientific DSA synthesis of conditional, reactive, and interactive TTC econometrics with uncertainty simplifications and approximations. Qualculation implicates CRAs in self-referential effects: as “detached” “expert observers”. Opaque structural modeling’s greater analytical and computational complexity, however, helps institutionalize heuristics that produce cognitive biases, systematic errors, and crises (IMF, 2010). Neoliberal capitalist orthodoxy adherence also privileges self-perpetuating, exogenous debt metaphysics (see Reinhart and Rogoff, 2010)—unmediated by their discursive relations. Although entangled, I argue how econophysics removes CRAs from PEC qualculability spaces (Mikes, 2009). Independent observer status serves to shield CRAs from serious reform, as contestation is superficial.

Unlike the Black-Scholes-Merton framework, unfortunately, this fails to secure sovereign assets risk-neutral valuation—being unable to reveal “how much risk exposures could change as the health of the sovereign improves or declines on the margin” (Gapen et al., 2008: 121). To forecast/monitor this degree of budgetary politics/ESG contingency, hypothetical (reflexive) RAMP “static pools” distort fiscal uncertainties as probabilistic risks (Paudyn, 2014). Like MDL, FJM acknowledges DSA “forward-looking categories are more amenable to repeated, regression stress testing under strict [conditional] parameters,” which “remain relatively constant over time.” Financial “big data” and digitalization accelerate temporal compression (Svetlova, 2018), frequenter (reactive) DSA qualculation, further implicating Moody’s/S&P in agencement constitutive governmentality relations.

Evident with the GFC/Great Recession or pandemic, newer TAC methods extend hybrid DSA qualculation beyond RAMP TTC/cyclical components. TAC ratings deploy greater conditional and reactive uncertainty modalities to construct increasingly stringent (ex-ante) “hypothetical [‘what-if’] stress scenario benchmarks for calibrating criteria” (S&P, 2021b: 94)—selective ESG shocks impair “fundamentals.” Doubtful of market efficiency or risk premia/yields perfectly pricing debt dangers, similar successively severe (investor) DSAs “incorporate statistical uncertainty into VCMM/VSD Monte Carlo projection outcome distributions,” VG2 clarifies. TAC “responsiveness targets ‘extreme’ ‘event risks’…especially ESG and financial system contingent liabilities.” PEC plasticity, I contend, reflects this constant stability/fluidity dynamic interplay actualized through its dialectical credit risk/uncertainty management (Beckert, 2016). Instead of exercising in-depth country-specific knowledge, however, experts on models often make DSA projections (Beunza and Stark, 2012). Yet, as EU (2021) Sustainable Finance Disclosure Regulations (SFDR) standardize evidence, Covid-19 or war “stress tests” TAC rating and (ESG) investment success. Thus, (reactive) DSA qualculation determines $650 billion (2021) “sustainable bond” market prosperity (PRI, 2022).

Despite admissions that establishing fixed DSA numerical thresholds or assessing/monitoring ESG contingency “would not be possible using a quantitative, automated…model-driven approach” (S&P, 2021b), econometrics dominate TAC DSAs (Kiff and Kisser, 2020). Unfortunately, econophysics disguises subjective TAC judgment diminishing advantage over ergodic TTC platforms. Although permitting CRA, market, and regulatory DSA divergence, TAC risk/uncertainty displacement or synthesis, as verifiable tangibles, preoccupies enough to preclude vast variation (Paudyn, 2015). Notwithstanding (GFC-exposed) model-centric ratings defects, without sustained pressure from either corporate clients or regulators (ESMA/SEC), business remains as usual.

Rating contagion and procyclicality

Technoscientific ratings shape and naturalize (expertocratic) agencement PEC cognitive interdependence. Its distribution actualizes a (disinflationary) debt normality (Deville, 2016). Material PEC transformations in budgetary conduct and market portfolios/conditions reflect referential infrastructure prescriptions (Callon, 2016). Institutionalizing transcendental (“self-generative”) neoliberal capitalist logics (Graeber, 2011), convergent PEC adjustments feedback (re)validates CRA expertocratic leverage (and anomaly). Two everyday economics promote transnational convergence through adoption and compliance rendering ratings austere programmatic real: contagion and procyclicality.

Institutionalized CRA or fund qualculative cultures may disturb automatic model-centric performation (Mikes, 2009), as MacKenzie’s (2006) Black-Scholes-Merton analysis (arguably) suggests. Ubiquitous DSA econophysics sufficiently homogenizes rating analytics, however. Skewing social facticity as natural ontology for speculative (curve) comparison, this mitigates major discretionary valuations or outcome deviations (Carruthers, 2013). “Without credible, profitable alternatives…ratings lower volatility, information, and trading costs enhance yield targets, index rebalancing…[plus] ROI,” BB3 admits. Adoption/deployment (endogenously) reinforces cognitive interdependence through interactive risk/uncertainty management (Beunza and Stark, 2012). Contagion and procyclicality (exogenously) strengthen variable (CRA, treasury, and investor) organizational congruence pressures (Dittrich, 2007).

First, as Argentina and Greece remind, downgrade contagion may forebode adverse, systemic consequences implicating neighbors, and financial markets (IMF, 2010). In reaction to (unanticipated) downgrades, bond prices plummet, yields rise, which elevates financing costs, plus impacts securities like equities. Studies document bivariate Granger causality between ratings cuts and bond yield (and CDS) spreads. Between January 1995 and October 2011, Afonso et al. (2014) observed statistically significant equity and bond volatility asymmetric effects, notably with downgrades, evident with a conditional coefficients estimation model. Similarly, Gärtner et al.’s (2011) 26 OECD countries (1999–2010) test concluded credit spreads react to ratings systematic and arbitrary (uncertainty modality) elements. Speculative “downgrades trigger panic, [Fed/ECB] collateral statute clauses, CDS contracts, bank and investment bylaws…prompting large bond sell-offs,” RGEM reports—being “market movers.”

Caution should be exercised, however, given negative externalities. Conventional Granger vector autoregression cannot accommodate complex PEC interactions. Highly entangled political economies and sophisticated financial systems thwart contagion’s (transmission/amplification) systematic, continuous-time diffusion modeling. Nonlinear pandemics and “tail/event risks” (e.g., GFC; war) further frustrate (lognormal distribution) Brownian geometrics structural forecasts (Maurer, 2002). Contagion’s systemic shocks qualculation may compensate but eludes IOSCO or ESMA simple DSA disclosure.

More unequivocal are ratings prohibitive effects constraining fiscal sovereignty. While $15 trillion of corporate welfare/bailouts erased toxic (GFC) liabilities, market-imposed austerity curtailed public investment (Helleiner, 2014). By 2015, contractions in government spending exceeded 10% in 16 EU states (European Commission 2021). Rather than enhance export competitiveness, GDP, or employment, however, the fiscal policy and economic health negative feedback loop produced stunted growth, high unemployment, plus populist sentiments. EU debt ballooned from 58.7% of GDP (2007) to 95% (2020)—EMU reached 102% (European Commission 2021). Covid-19 and war exacerbate recovery, particularly “periphery” EU/EMU macroeconomic imbalances. Surging debt, protracted growth, yet fixed exchange rates, demand internal devaluation (i.e., wage cuts) to recover competitiveness. Politically destabilizing, like Italy, persistent imbalances with the Germanic core jeopardize EU/EMU cohesiveness and integrity (Eijffinger, 2012).

Since EMU increases cross-border (sovereign) securities holdings, ratings contagion can adversely affect neighboring banks/finances to intensify downward pressures (Coffee, 2006). Similar Greek, Italian, Spanish, and Portuguese “periphery” credit profiles, specifically weak government balance sheets, heighten vulnerability to comparable shocks: ESG hazards (e.g., wildfires) or banking “event risks” like nonperforming loans and lackluster profitability (European Commission 2021). “Common, chronic [structural] headwinds, including poor, ‘super-aged’ demographics and sluggish productivity growth…compound knock-on effects,” remarks CIF2 (and CRAs). Rating-prompted arbitrage magnifies EMU susceptibility to downgrade contagion, extending ratings/CRA scope and leverage.

Expertocratic agencement cognitive interdependence amplifies ratings transmission resembling “self-generative” PEC performance. On 5 July 2011, negative spillover effects from Greece’s imminent (structured) default compelled Moody’s to cut Portuguese debt to “junk”—“Ba2”/negative outlook from “Baa1.” Additional bailout anxieties, including private sector “haircut,” drove its 10-year bond yield above 13%—euro-era record against Bunds. On 13 January 2012, S&P followed suit declaring Portugal “junk”—“BB”/negative outlook from “BBB−.” Said benchmark bond yield jumped by 2.04% to 17.26%. Prompting internal/external imbalances adjustments, subsequently, yields paralleled Portugal’s 5-year cumulative EDF decline—convergence confirms DSA qualculation. Temporary, given the coalition government’s near collapse, its (July 12/2013-high) EDF 4.89% spike validated CRA prescriptions that politics is a mitigatable liability (Moody’s Analytics, 2013). During ESG/PEC flux, technoscientific DSAs retain command, as post-crisis.

Like “Brexit,” EMU “Grexit” fears deteriorated market sentiment, and Spanish banks exceeded credit losses expectations, which amplified Portugal’s downgrade. CRA-stoked alarm of its (5-year) 70% “default risk” drove Portuguese CDSs to record highs. Counter-agencement mounting protests and “social upheaval” helped abort subsequent “fiscal devaluation,” including a 7% “tax-swap” (Eijffinger, 2012). While Bunds flight-to-safety positively benefited Austrian, Finnish, or Dutch spreads, Greek downgrade contagion negatively impacted Portuguese, Italian, Spanish, Belgium, and French debt (Afonso et al., 2014).

Even before Covid-19, compounding contagion effects proved precarious for the “elephant in the room”: Italy (Moody’s, 2012; 2018b). With €2 trillion in gross debt (140% of GDP), Rome was scheduled to refinance €415 billion (25% of GDP) in 2012-13. Elevated financing costs originating from neighbors/abroad strained affordable credit accessibility. Denied inexpensive channels, Italian emergency European Security Mechanism (ESM) intervention would severely tax EMU’s new firewall. On 13 July 2012, citing “Italy’s increased susceptibility to event and liquidity risks,” particularly “an eroding nondomestic investor base,” Moody’s (2012) axed its “A3” grade to “Baa2.” Global capital attraction is vital for national programs, whilst controlling profligacy through neoliberal agencement PEC convergence. Although €5.25 billion of medium-/long-term notes sold, domestic banks bought most not foreign investors. Facilitating the cross-border cognitive interdependence informing asset allocation, ratings referential/data infrastructure dissemination expands contagion. Yet, MDL notes how “negative spillover effects can jeopardize the necessary sociopolitical stability sustaining the “democratic advantage” that agencies prize.” Hindering national self-determination, imposed austerity’s counter-agencement intensifies “political risks”: rising inequality, protectionist populism, and zero-sum deglobalization (Birch and Muniesa, 2020).

Ratings indexical authority helps distribute PEC cognitive agency widely. Bordering “junk,” Italy’s populist La Lega-Five Star Movement (M5S) government’s (May 2018) “fiscal shock” stimulus pledge breaching (Stability and Growth Pact) budgetary rules only deterred foreign investment. Threatening “particularly serious non-compliance” provocation of the “excessive deficit procedure” (EDP), it instigated a Brussels crackdown. Moody’s (19 October 2018) “Baa3” downgrade further eroded market confidence, which precipitated its government’s implosion. “Fueling fears and drama concerning overly conservative mispriced political risk,” RGE1 reports, “bond vigilante short bets arbitrarily priced “redenomination risk” into Italian yields.” Without prior evidence of EMU contagion (Q3 2018), he estimates the “rating action contributed to about half the 10-year benchmark’s spike to four-year highs [3.71%]”. Arbitrage advantage from exploiting “junk’s” (artificial) investment-grade threshold also threatened “Spain’s higher credit quality and non-resident investors’ robust demand,” plus “Portugal’s increasingly diversified funding sources” (Moody’s, 2018b). Yet, June 2019 budgetary adjustments curtailed EU/EDP censure, investor anxiety diminished, while Italy’s 10-year yield declined below 2%. Corresponding Spanish and Portuguese borrowing costs fell to new lows.

Fragile PECs, after annual-record (2020) defaults (seven) from (Covid-19) downgrades—S&P (2021a) slashed 26 sovereigns (Fitch 24), including Italy to “BBB/BBB3”—threaten intensifying contagion. Financial volatility endangers broader fiscal sovereignty underpinning recovery sustainability. Gross financing needs (GFN) have doubled: EU 23% GFN-to-GDP (2021). ECB €1.85tn QE intervention—annual €760 billion public debt purchases—reduced financing pressures. Approaching 157% debt-to-GDP (2021), however, Italy’s 27% GFN-to-GDP imposes “severe limits to cushion future shocks” (European Commission, 2021). Breaching IMF 15–20% sustainability guidelines, it heightens Rome’s susceptibility to arbitrary “junk” qualculation. Significant short-term debt issuance—25% of OECD (2021) total debt matured in 2021—means looming larger rollover ratios, refinancing risk, and downgrade contagion volatility. Russian coupon payment “redenomination” default looms large. Turmoil abroad, as China’s GDP (2020) (double-digit) plunge to −6%, “magnifies stressors jeopardizing better recovery and transition to a post-QE environment” (S&P, 2021a), EMU, and rallies populists, or counter-agencement.

Spillover effects promote ratings sociomaterial facticity cross-border distribution and analytical, organizational congruity translation into PEC reality (Lépinay, 2011). Unfortunately, neither Steps nor RAMP DSAs account for CRA-triggered contagion risk (Gaillard, 2012). Quant DSA dominance constrains interactive CRA self-reflexivity enough to muddle their (performance) role as “market movers.” Instead, econophysics qualculation “(re)legitimizes” (risk-neutral) financial expertocratic exemption (Best, 2014). Even if priced into market expectations, rating event transmissions or precisely assigning one CRA blame are difficult to determine, given bank collateral statutes, investment bylaws, etc. (Coffee, 2006). CRA self-analysis/-referentiality may also entrap in causal circularity, which technoscientific rating precludes.

Second, ratings’ procyclical bias bolsters CRA self-validating effects, yet with systemic repercussions. Downgrades and negative “outlooks/watches” help deteriorate conditions precipitating further cuts (Binici et al., 2020). “Procyclicality-induced feedback effects” intensify “excessive deleveraging in falling asset markets,” collapsing credit channels, “cliff effects,” with “serious financial stability and real economy consequences” (IMF, 2010: 69). Financial ad-hoc (external) TTC EDF mapping to (internal) PIT scores exacerbates procyclical fluctuations. Inconsistent rating and migration matrix methods miscalculate portfolio risks (Kiff and Kisser, 2020). Relative to CRAs, BB3 recalls: greater risk aversion among investors, which [pre-downgrade] growing yield spreads and CDS-implied ratings demonstrated…meant mispricings accelerated 1997 or GFC panicked selling and herding.

Referential agencement PEC interdependence amplifies the alarm of breaching “junk.” Evidenced in Asian and European bond movements, within 2 days of “junk” downgrades, growing risk aversion and distress widened spreads—unobserved in bond trends between days -60/-30 and -1 (Gaillard, 2012). Corresponding market interactivity (re)endorses ratings utility merits—expertocratic feedback prolongs CRA longevity.

TTC long-term bias lags help render PEC performance procyclical (Löffler, 2013). Smoothed over extended default horizons, TTC ratings “wait to detect whether [creditworthiness] degradation is more permanent than temporary…exceeding one notch” (IMF, 2010: xiii). Slow (reactive) adjustments to credit quality changes (e.g., Asian and Greek crises) mean “Moody’s EDF stability produces ‘stickier’ ratings than S&P’s or Fitch’s more market-correlated grades,” acknowledges MDL. Thus, Moody’s delayed (December 2009) Greek “A2” downgrade from “A1”—already cut thrice by S&P (“junk”) and Fitch (“BBB−”). Again, Greek 10-year bond spreads surged from 0.5% over Bunds, surpassing 3% (January 2010) (IMF, 2010). Interactive debt investment enables agencement PEC convergence, reaffirming expertocratic CRA (self-referential) performance.