Abstract

This paper examines the rise of tokenization platforms as strategic instruments through which incumbent banks reassert power within the post-crisis financial system. Challenging dominant accounts of platform capitalism that emphasize disruption, data extraction, and/or ecosystem expansion, it argues that bank-led tokenization platforms, developed by institutions such as UBS, JPMorgan, HSBC, and Citi, constitute a distinct modality of platform power. Rather than dis-intermediating finance, these platforms operate through infrastructural embedding and regulatory compliance, offering other institutions more efficient, lower-friction ways to operate in critical financial segments. This enables banks to reorganize balance sheet operations and reclaim strategic centrality in private credit, repo markets, and asset management, responding to regulatory pressures and competition from non-bank financial actors. In doing so, this paper advances a political economy account of tokenization platforms that move beyond existing theories of platform power, highlighting infrastructural efficiency and reconfiguration as central mechanisms of contemporary financial authority.

Introduction

“We believe the next step going forward will be the tokenization of financial assets, and that means every stock, every bond (…) will be on one general ledger” (Larry Fink, the CEO of BlackRock, January 2024)

In recent years, some of the most powerful and traditionally conservative actors in global finance, notably large banks and asset managers, have become vocal advocates of financial asset tokenization. This is puzzling. Tokenization is typically linked to decentralization and disintermediation, yet it is incumbent institutions that are now investing most heavily in building and scaling tokenization platforms. Why are they embracing a technology initially framed as a threat to their authority (e.g., Goghie, 2024), and what kinds of power relations does this actually generate in contemporary finance?

This puzzle is often treated as a question of technological innovation. Yet, incumbents are not simply adopting new tools. These actors are constructing tokenization platforms embedded in financial infrastructures that shape asset circulation, organize participation, and ultimately structure control. Explaining why they are leading this push requires moving beyond narratives of innovation or efficiency and situating tokenization platforms within broader debates on platform power (e.g., Culpepper and Thelen, 2019; Cutolo and Kenney, 2021; Plantin et al., 2018).

For theoretical clarity, this power is understood as the capacity of platforms to structure access, interaction, and value creation by controlling the technical, organizational, and/or institutional conditions under which economic activity takes place (Cioffi et al., 2022; Cutolo and Kenney, 2021). Early accounts emphasized platforms’ infrastructural role, arguing that their expansion has rendered them indispensable to contemporary societies (Plantin et al., 2018; Van Dijck et al., 2018; Rahman and Thelen, 2019). Building on this view, one strand of the literature conceptualizes platform power as stemming from platforms’ distinctive institutional form, in which layered architectures generate durable (power) asymmetries between platform owners and participants (Cioffi et al., 2022). However, important disagreements remain about the underlying sources of this power. For instance, Culpepper and Thelen (2019) suggest that platform power stems from user allegiance and the political costs of regulating infrastructures embedded in everyday life. Other strands of the literature conceptualize platform power as operating through technical design and contractual governance (Cutolo and Kenney, 2021). In this view, platform code and contracts function as private regulatory systems that shape markets and redistribute power (Kenney et al., 2021; Rahman and Thelen, 2019). Some critical political economy accounts situate platform power in broader structural dynamics, highlighting how weak regulatory oversight and privatized digital markets have allowed platforms to scale, expand across sectors, and consolidate power through network effects and ecosystems (Cioffi et al., 2022; Kenney and Zysman, 2020; Langley and Leyshon, 2017). In this view, platform power is closely linked to data-driven accumulation, where value is extracted via data capture, user dependence, and monopoly rents (Birch, 2023; Roitman et al., 2025).

Yet, despite its complexity, the literature on platform power has developed largely through the study of consumer-facing and data-intensive digital platforms. As a result, its core analytical categories, such as user allegiance, data capture, ecosystem expansion, network effects, and/or monopolistic market domination, are often implicitly generalized as the defining sources of platform power across sectors (Culpepper and Thelen, 2019; Kenney and Zysman, 2020; Langley and Leyshon, 2017). This generalization becomes problematic when applied to financial platforms, and particularly to the emerging class of tokenization platforms introduced by incumbent banks.

Unlike platforms that organize consumer markets or monetize user data, tokenization platforms function within the institutional architecture of finance, operating through regulated balance sheets (BIS, 2023) and serving systemically important institutions rather than politically mobilizable users. Conventional accounts of platform power thus only partially capture their dynamics. This paper argues that tokenization platforms constitute a distinct form of platform power, rooted not in user mediation or ecosystem expansion, but in their ability to provide other financial institutions with faster, more liquid, and lower-friction ways to issue, transfer, and collateralize assets within existing regulatory frameworks (Rahman and Thelen, 2019). By embedding compliance into operations, these platforms reduce regulatory and operational complexity, making adoption the most efficient route for market participation and allowing banks to reclaim strategic control over flows that had shifted to non-bank actors after post-crisis of 2007–2009 regulatory tightening.

From a political economy perspective, this distinction matters because it challenges the assumption, implicit in much of the platform power literature, that platformization necessarily entails the displacement of incumbent institutions or the erosion of public regulatory authority (Kenney et al., 2021; Piletić, 2024). In the case of tokenization, platform power unfolds through incumbency rather than disruption (e.g. Goghie, 2024). Banks deploy these platforms not to bypass regulation, but to reorganize compliance and restore control over financial flows by offering a more efficient path for operating in key financial domains.

Empirically, this form of platform power materializes most clearly in three financial domains that are central to contemporary finance. In private credit markets, where tokenization platforms enable banks to reassert influence over credit intermediation by improving asset mobility, transparency, and collateral usability, countering the growing dominance of large asset managers and private credit funds. In repurchase agreements (repo) markets, where tokenization enhances collateral circulation and settlement efficiency, reinforcing banks’ infrastructural role in short-term funding and liquidity provision. In asset management, where tokenized funds and securities allow banks to embed themselves more deeply in portfolio construction, custody, and settlement processes, reasserting control over value chains increasingly shaped by large institutional investors such as BlackRock, Vanguard, and State Street.

As such, the central contribution of this paper is twofold. Theoretically, it extends the platform power literature by identifying a distinct form of power exercised through regulatory compliance and financial infrastructure rather than through users or data. This highlights how incumbent banks can leverage platform embedding to restore control over financial flows that had shifted toward non-bank financial actors following post-2007–09 regulatory tightening. Empirically, the paper examines how this power is exerted through the deployment of tokenization platforms by UBS, JPMorgan, HSBC, and Citi. By providing more efficient, lower-friction ways to issue, mobilize, and settle assets, these platforms allow banks to strategically reclaim influence across private credit, repo markets, and asset management, financial domains where regulatory pressures and competitive dynamics had previously constrained their activity. By linking platform power to concrete financial practices, this paper shows how incumbents maintain and/or regain market centrality by strategically embedding control in specific financial domains through tokenization platforms.

To build this argument, this paper employs a qualitative, document-based methodology. It draws on primary and secondary sources including policy reports, working papers, and institutional publications from the Federal Reserve, the Bank for International Settlements (BIS), the International Monetary Fund (IMF), the Global Financial Markets Association (GFMA), McKinsey & Company, Deloitte, and the Asian Development Bank Institute (AIB), alongside peer-reviewed research and news coverage. These materials were systematically analyzed to identify how incumbent banks deploy tokenization across private credit, repo, and asset management. Charts were constructed using data primarily from the BIS and Deloitte.

This paper is organized into five sections. The first traces the emergence of blockchain technology and its evolution toward tokenization (platforms). The second examines the specific characteristics of platform power and its intellectual origins. The third shows how tokenization platforms diverge from existing understandings of platform power in the literature. The fourth analyzes how tokenization platforms are being deployed in financial segments deemed critical by incumbent banks, highlighting how they use these platforms to counter their post-GFC loss of influence. The final section concludes.

Blockchain technology and the path towards tokenization platforms

The crypto ecosystem emerged with the advent of Bitcoin in 2009, introducing a decentralized, peer-to-peer system for transferring assets via a shared public ledger. Built on distributed ledger technology (DLT), this system reduced reliance on traditional intermediaries (BIS, 2023). As the technology diffused, its functionality expanded beyond payment systems. Swan (2015) conceptualizes this evolution in three phases: the emergence of cryptocurrencies, the development of smart contracts, and the application of blockchain technology in broader public and institutional domains. This paper focuses on the second phase, which underpins the tokenization of financial assets.

Smart contracts, software protocols that automatically execute predefined contractual conditions, gained prominence with Ethereum, which enabled programmable asset ownership rather than simple value transfer (Banerjee et al., 2024; Khan et al., 2021). This development facilitated the emergence of decentralized finance (DeFi), where financial functions traditionally performed by intermediaries are replaced by rule-based systems embedded in smart contracts (Born and Vendrell Simon, 2022; Schär, 2021). DeFi operates through decentralized applications (DApps) and decentralized exchanges (DEXs), which function as marketplaces for activities such as collateralized lending, trading, and risk management using crypto-assets and stablecoins (Aramonte et al., 2021; Bank for International Settlements, 2023).

Two design principles underpin these systems, namely, programmability and composability. Programmability refers to the capacity to build applications directly on blockchain infrastructures, while composability denotes the ability to interconnect protocols to generate new financial arrangements, a feature often described as “money legos” (Bank for International Settlements, 2023; Lalav, 2023). Together, these properties enable modular and scalable financial market architectures.

Against this background, the tokenization of real-world assets (RWAs) represents a critical extension of DeFi into traditional finance (Chainlink, 2024). Stricto sensu, tokenization refers to the process of generating a digital representation of a real-world asset on a programmable ledger, thereby enabling traditional financial instruments, such as bonds, equities, or funds, to be issued, transferred, and settled through smart contracts (Aldasoro et al., 2023; Gundiuc, 2022). Unlike earlier forms of digitization, which primarily involved electronic record-keeping within centralized databases, tokenization embeds assets directly into programmable infrastructures, allowing ownership, transfer, and servicing functions to be automated and interoperable by design.

As a result, token holders obtain legally enforceable claims on the underlying reference asset, linking blockchain-based infrastructures to existing legal and institutional frameworks (Carapella et al., 2023). This linkage increases the interconnectedness between traditional finance and crypto markets, introducing new sources of funding, leverage, and competition for banks and other financial institutions (Bank for International Settlements, 2023). Tokenization offers several operational advantages, including automation of settlement and servicing functions, reduced operational costs, fractional ownership and enhanced auditability through immutable ledgers, among others (Aldasoro et al., 2023; Banerjee et al., 2024; Sexton, 2023).

These benefits have translated into strong institutional expectations regarding the scale of tokenization. BlackRock’s CEO Larry Fink argued in 2024 that tokenization represents the next stage of financial market infrastructure, envisioning stocks and bonds issued and settled on a unified ledger (Banerjee et al., 2024). This view is echoed across major financial institutions and consultancies. A survey by BNY Mellon reports that over 97% of institutional investors expect tokenization to have a transformative impact on asset management, anticipating a broad migration toward digital assets (Reinertsen and Butler, 2022). Market projections further confirm the magnitude of these expectations. Estimates for tokenized market capitalization by the end of the decade range from approximately $4 trillion (McKinsey) to nearly $5 trillion (Citi), with more expansive projections reaching $16 trillion (BCG/IMF) and up to $24 trillion as early as 2027 (HSBC), depending on asset coverage and institutional uptake (Agur et al., 2025; Banerjee et al., 2024; Citi GPS, 2023; Tummala et al., 2020). Ultimately, these projections frame tokenization as a prospective reconfiguration of financial market infrastructure at scale.

While tokenization denotes a process, it is enacted and stabilized through tokenization platforms. Tokenization platforms are digital systems that allow financial assets (such as bonds, loans, or other claims) to be represented and managed in digital form (BIS-CPMI, 2024). They provide the technical environment in which these assets can be issued, transferred, and settled using standardized digital rules rather than paper-based or manual processes. Technically, they integrate distributed ledger technology, smart contracts, and application-layer interfaces with legal, regulatory, and custodial arrangements that anchor tokenized assets within existing institutional frameworks (Aldasoro et al., 2023). At the base layer, DLT provides a shared and tamper resistant ledger that records asset ownership and transaction histories, while consensus mechanisms determine validation authority and settlement finality (Yaga et al., 2018). On top of this ledger, smart contracts encode asset-specific rules governing issuance, transfer, servicing, and redemption, effectively embedding core financial functions directly into programmable architectures (Aldasoro et al., 2023; Schär, 2021).

Where the platform power comes from?

Despite the existence of multiple definitions (e.g., Parker et al., 2016), for greater theoretical clarity, this paper defines platforms in line with Roitman et al. (2025) as heterogeneous socio-technical arrangements that combine computational components, organizational models, and institutional actors to structure and govern interactions among multiple participants. Rather than constituting a uniform organizational form, platforms take multiple, layered configurations, rendering platformization, or “(…) the penetration of the infrastructures, economic processes, and governmental frameworks of platforms in different economic sectors and spheres of life” (Poell et al., 2019: 5-6), a dispersed and sometimes internally contradictory process.

It is precisely these multiple, layered configurations that generate power asymmetries both across markets and among platforms, giving rise to what has been described as platform power (e.g., Cioffi et al., 2022; Cutolo and Kenney, 2021). This power, it is argued, has emerged because over the past two decades, platforms have expanded to such an extent that they are increasingly regarded as essential infrastructures (Calvo et al., 2025; Plantin et al., 2018; Van Dijck et al., 2018), owing to their capacity to shape technological innovation as well as the conduct and content of social and political discourse (Cioffi et al., 2022; Kenney and Zysman, 2016; Srnicek, 2016).

Of course, power can take multiple forms. As discussed above, platforms are increasingly understood as essential infrastructures. Building on this view, some authors have gone further (explicitly or implicitly) by suggesting that platforms exercise a form of infrastructural power, insofar as they provide services that have become indispensable to the functioning of contemporary societies (e.g., Rahman and Thelen, 2019; Klinge e al., 2023). Culpepper and Thelen (2019), however, adopt a contrasting view, arguing that platform power stems not from infrastructural indispensability but from platforms’ ability to define access for consumers. This power, rooted in user allegiance, cannot be classified as purely instrumental or structural. Unlike banks, platforms cannot counter regulation by disinvesting; instead, their influence relies on the anticipated political costs regulators face when intervening in infrastructures deeply embedded in everyday life.

Moving forward, platform power is also commonly understood to take two forms: artifactual and contractual (Cutolo and Kenney, 2021; Kenney et al., 2021). Artifactual power refers to the affordances built into a platform’s technical architecture, which enable certain activities while constraining others. Even minor code changes can impose new modes of participation, allowing platforms to shape participant behavior across market interfaces and function as critical points of control over access and liquidity (Rahman and Thelen, 2019). Contractual power, by contrast, operates through the terms and conditions users must accept to participate. These arrangements govern access, enable data extraction and facilitate the creation of white-label products and new functionalities, functioning as private regulatory systems through which platforms exercise power (Kenney et al., 2021).

Beyond these two dimensions, Cioffi et al. (2022) emphasizes that power also derives from broader structural characteristics, including the historically passive stance of governments toward regulatory oversight. Left largely to private ordering, the most successful platforms expanded rapidly in scale and influence through both technological design and the relatively unconstrained legal structuring of their contractual relations (Cioffi et al., 2022; Kenney et al., 2021). In the absence of effective regulatory constraints, these economic and legal advantages enabled patterns of rapid concentration and monopolistic growth (Cioffi et al., 2022). Importantly, this dynamic highlights the deep power asymmetries. Not all platforms, and not all sectors, allow firms to shape user choice to the same extent. Platform power is therefore unevenly distributed and context-dependent, rather than a universal feature of digital markets (Schmidt and Engelen, 2020).

But not only that, these power asymmetries can also be traced to the generative capacity of platforms. By attracting and aggregating large volumes of data, users, and complementary product and service providers, platforms give rise to a platform ecosystem (Kenney and Zysman, 2020) that enables the modification and creation of new structures and patterns of behavior (Zittran, 2008). In this sense, platform value (or power) no longer derives primarily from radical scientific or technological innovation per se, but from the construction of digital ecosystems that enable institutional empowerment through collaborative and pro-common forms of exchange, particularly when supported by appropriate governance mechanisms (Torrent-Sellens, 2023).

Another perspective on platform power emphasizes platforms’ ability to generate digitized value by transforming economic activity into data-driven and programmable forms, leveraging their advantages in collecting, analyzing, and commodifying data, either internally or for third-party sale (Cioffi et al., 2022; Langley and Leyshon, 2017; Van Dijck, 2013). This is closely linked to the extraction of monopoly rents, as platforms can capitalize on user dependencies (Birch, 2023; Langley and Leyshon, 2017; Roitman et al., 2025). This power extends to controlling individuals: personal data are often collected without meaningful consent, and repeated exposure to pop-ups generates “consent fatigue” (Graef and Bostoen, 2025). Platform power is also evident in the gig economy, where workers on platforms such as Uber are (or were) legally classified as self-employed despite substantive dependence on the platform, excluding them from key labor law protections (Daskalova, 2019).

This logic has been central to explanations of how network effects underpin the rise of platforms and how these effects allow platforms to leverage user data to deepen and expand the range of services they offer within specific industries, with direct implications for platform generativity and the capacity to extend market share (Kenney and Zysman, 2020; Parker et al., 2016). In short, empirical studies consistently show that the data accumulated by platforms are crucial for the creation of commercial value and, ultimately, their power (Thatcher et al., 2016).

Of course, other strands of the literature have shown that value is not always generated through data capture or enclosure, but also through interoperability. In this vein, scholars point to the use of APIs in the US healthcare sector, where platforms do not perform a monopolistic function but instead contribute to the development of interoperable data infrastructures aimed at overcoming closed data systems and generating both public and private goods (Huber, 2025; Roitman et al., 2025). These arrangements similarly rely on connectivity, but their extended role lies in mediating across data infrastructures rather than siloing systems for rent extraction (Roitman et al., 2025). Building on this logic of intermediation and connectivity, it has also been argued that another driver behind platform development is their capacity, as “non-human mediators” (Calvo et al., 2025: 15), to resolve coordination problems by extending the distance-shrinking networking capacities of the internet. This capacity enables platforms to facilitate two-sided or multi-sided markets, in which economic actors must be brought together in order to transact (Langley and Leyshon, 2017).

Along similar lines, it has been argued that platforms possess the capacity to create new infrastructures through which buyers and sellers can be coordinated, allowing them to outperform firms that rely primarily on internal resource ownership (Kenney et al., 2021; Parker et al., 2016). As platforms increasingly become constitutive infrastructures of social and economic life, they also display pronounced monopolistic tendencies (Cioffi et al., 2022; Kenney et al., 2020; Plantin and Punathambekar, 2019). It is therefore unsurprising that scholarship on platforms has questioned whether they represent a new regime of accumulation, implying an endogenous transformation of financialized capitalism, or rather a more intensive variant of an already financialized accumulation regime (Montalban et al., 2019; Piletić, 2024). The prevailing conclusion suggests that platforms have given rise to a hybridization of existing accumulation regimes, entailing transformation within already-established institutional forms rather than a wholesale break from them (Piletić, 2024).

For example, this form of hybridization can also be observed in some financial platforms. In the aftermath of the 2007–08 financial crisis, widespread bank failures contributed to the emergence of “alternative” forms of lending and borrowing, most notably peer-to-peer platforms operating in consumer and firm lending (Clarke, 2019; Clarke and Tooker, 2018). These developments reflect continuity in accumulation practices, insofar as value creation continues to rely on activities associated with financial production and exchange (Piletić, 2024; Roberts, 2013).

Yet, can existing conceptions of platform power be applied to tokenization platforms deployed by incumbent banks? In this context, power does not arise from imposing unilateral terms and conditions (Kenney et al., 2021), unconstrained contractual design typical of digital platforms (Cioffi et al., 2022), or data capture and monopoly rents (Birch, 2023; Roitman et al., 2025). Instead, it emerges from the platforms’ ability to provide other financial institutions with faster, more liquid, and lower-friction ways to operate within regulatory frameworks. By embedding compliance directly into their operations, these platforms reduce operational complexity, incentivize adoption, and allow banks to reclaim strategic control over flows that had shifted to non-bank actors. This form of power, exercised through infrastructural and market design rather than contractual leverage, constitutes the focus of the following section.

Why tokenization platforms are different?

Tokenization platforms provide standardized digital interfaces that let issuers, investors, custodians, and market venues interact in a shared environment, enabling traditional market infrastructure functions, like settlement, asset servicing, or collateral operations, to be executed programmably and interoperably, resembling the logic of traditional digital platforms (Tohme, 2025). Indeed, the platform literature has long emphasized that platform power resides in the capacity to coordinate dispersed participants and structure the conditions under which complementary activities unfold (Kenney et al., 2021).

There is also a superficial similarity in the role attributed to users. In both cases, platforms depend on participation by a wide set of actors, and in the digital platform literature this dependence is often framed as a source of political and economic leverage (Cioffi et al., 2022). Alliances with users are understood as particularly salient in regulatory conflicts, where consumer autonomy can be mobilized against public intervention (Culpepper and Thelen, 2019). Yet, this parallel becomes increasingly fragile once tokenization platforms are examined more closely.

Unlike consumer-facing digital platforms, tokenization platforms do not derive power from user allegiance or from the political salience of user autonomy. Their users are not consumers whose everyday practices can be mobilized in regulatory struggles, but regulated financial institutions embedded in dense legal, prudential, and supervisory frameworks. Regulation therefore does not threaten the value proposition of tokenization platforms in the same way. On the contrary, these platforms are often adopted precisely because they provide technical means to operate within regulatory constraints while mitigating their frictions. Rather than resisting regulation or exploiting legal ambiguity, tokenization platforms are designed to function through compliance.

This difference signals a shift from intermediation to infrastructural embedding. Whereas digital platforms primarily act as intermediaries that position themselves between users in order to mediate exchange and scale network effects (Langley and Leyshon, 2017), tokenization platforms are embedded more deeply within the financial system itself. They become part of the infrastructure through which financial claims are issued, transferred, and settled.

This infrastructural orientation also explains why tokenization platforms do not rely on large-scale data capture to generate value. In the case of digital platforms, data extraction is central to accumulation: user data is continuously collected and redeployed to expand services, refine segmentation, and shape behavior, reinforcing platform dominance (Kenney and Zysman, 2020; Parker et al., 2016; Thatcher et al., 2016). Tokenization platforms follow a different logic. Their value does not stem from knowing users better or steering their behavior, but from reshaping how assets and obligations are represented on balance sheets and how they circulate across institutional boundaries. In more detail, they enable financial claims to be mobilized more efficiently, directly shaping balance-sheet dynamics and the management of constraints faced by financial institutions. Power, in this context, derives not from informational asymmetries but from the capacity to reconfigure the infrastructural conditions under which financial accumulation takes place.

Crucially, this also means that tokenization platforms do not seek to reshape social behavior or generate new patterns of everyday practice, as is often the case with digital platforms (Zittran, 2008). Their influence is more contained and more technical, yet also more structurally consequential. It operates through the redesign of financial processes rather than through the governance of users. These characteristics help explain why tokenization platforms are not oriented toward ecosystem expansion in the conventional platform sense. Whereas digital platforms typically grow outward by attracting complementors and scaling network effects (Kenney and Zysman, 2020), tokenization platforms evolve inward through deeper infrastructural integration across adjacent financial segments. A technological core developed internally for one function can thus be redeployed in others, enabling incumbent banks to extend the same tokenization logic into domains where regulatory constraints had previously limited their activity.

Accordingly, the power of tokenization platforms does not lie in the creation of open or collaborative ecosystems (cf. Torrent-Sellens, 2023), but in the controlled evolution of their operational boundaries. As new segments become targets for deployment, these platforms can be selectively extended, for example, from repo markets to the tokenization of foreign exchange swaps (FX swaps) (e.g., Lipsky, 2024). This inward expansion is primarily technological, allowing the reuse of the same infrastructural architecture across multiple regulatory contexts.

This perspective also clarifies their relationship to regulation. Unlike consumer-facing digital platforms that exploited regulatory ambiguity to bypass established legal protections, as in the case of Uber (Graef and Bostoen, 2025), tokenization platforms are adopted precisely because they offer compliant regulatory alternatives. By embedding new technological affordances into financial infrastructure, tokenization platforms enhance efficiency while reallocating strategic centrality back to incumbent banks (Rahman and Thelen, 2019). These dynamics point toward a form of selective re-centralization rather than platform monopolization. Whereas digital platforms often concentrate power by dominating markets and excluding competitors (e.g., Calvo et al., 2025), tokenization platforms reassert centrality within existing financial hierarchies. They do not seek to displace incumbent institutions but to reinforce their position by embedding new technological capabilities into market infrastructure. In this way, banks can selectively regain control over financial flows that had migrated to non-bank actors, without dismantling the broader institutional ecology of financial intermediation.

These observations also bear directly on broader debates about regimes of accumulation. As scholarship on digital platforms has noted, platforms do not constitute a wholesale break with financialized capitalism but rather contribute to a hybridization of existing accumulation regimes, entailing transformation within established institutional forms rather than their replacement (Montalban et al., 2019; Piletić, 2024). A similar conclusion applies to tokenization platforms, though through different mechanisms. They do not create new objects of accumulation or monetize user activity. Instead, they intensify financialized accumulation by increasing the liquidity and circulation of existing claims through infrastructural redesign. Their novelty lies less in displacing institutions than in technically recomposing the infrastructures through which accumulation is organized. By embedding new technological affordances into balance sheets and market architecture, they reinforce the centrality of incumbent banks while maintaining continuity in the underlying logics of financial accumulation.

In sum, tokenization platforms diverge from conventional digital platforms, as their power lies less in intermediation, data extraction, or ecosystem dominance than in reorganizing financial architecture. Through technological embedding, they enable incumbent banks to reclaim strategic centrality while remaining within regulatory frameworks. Focused primarily on private credit, repo, and asset management, these bank-led platforms enhance the liquidity and coordination of existing markets. The next section examines UBS Tokenize, JPMorgan Kinexys, HSBC Orion, and Citi Token Service, showing how tokenization platforms recentralize control via balance sheets and regulatory navigation rather than user bases or data capture.

Tokenization platforms and their role in reshaping power dynamics (of incumbent banks)

This section analyzes how tokenization platforms equip incumbent banks to reassert control over critical areas of the financial system. Following the post-GFC migration of activity toward non-bank institutions, banks deploy these platforms to rebuild market presence and shape the issuance, movement, and ultimately settlement of assets. By embedding compliance and operational efficiency directly into market infrastructure, tokenization platforms enable banks to recover strategic centrality and steer the organization of financial intermediation.

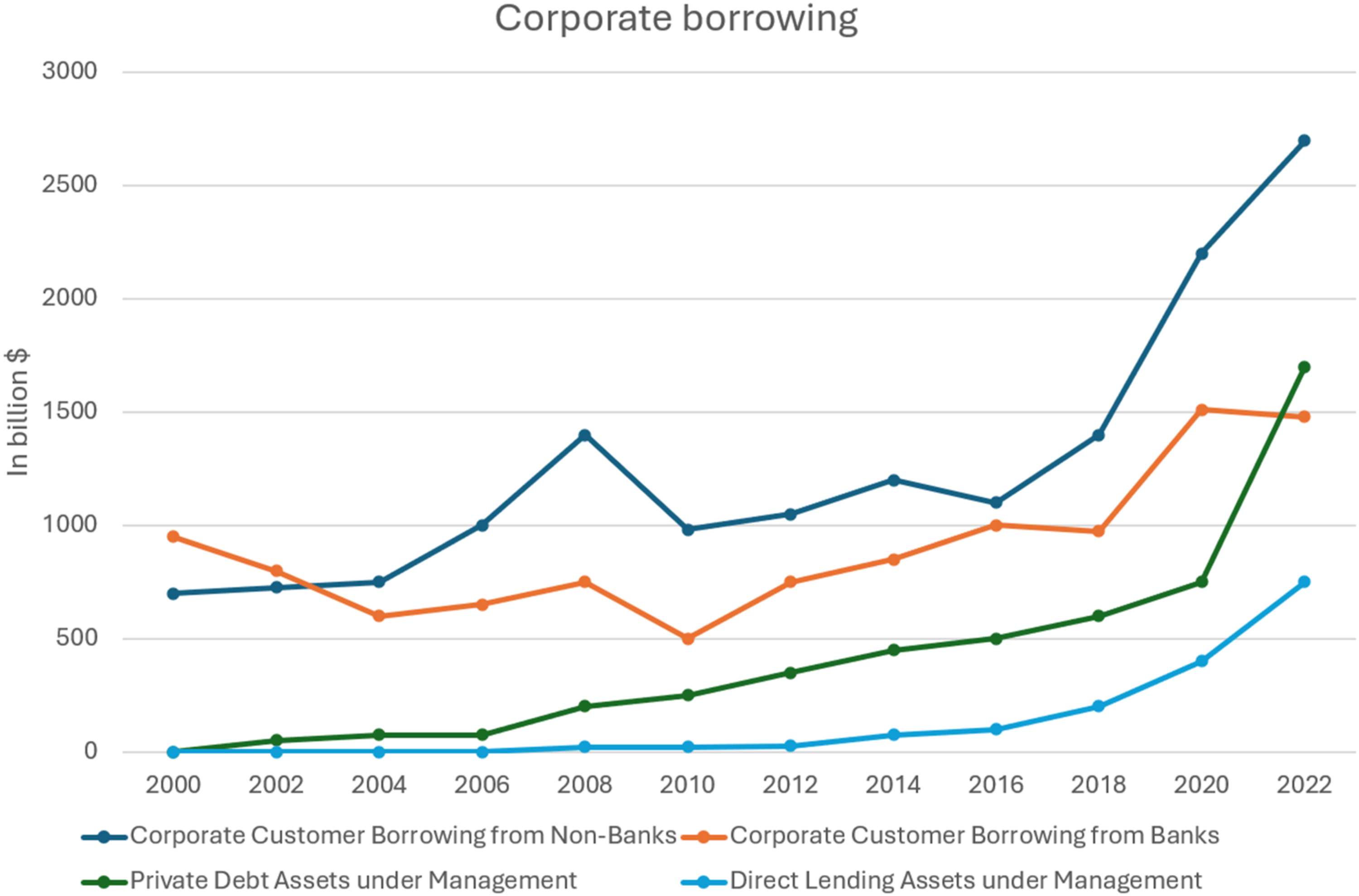

This is important because, over the past decade, competition from non-bank actors, such as hedge funds, private equity firms, and credit funds, has intensified, largely due to their ability to deliver higher returns in the absence of banking-style regulatory constraints. One clear example is the rise of private credit sourced from passive investors, with direct lending increasing 17-fold since 2009 (Degerli and Monin, 2024; Egilsson, 2024). The long-term shift is evident: between 2000 and 2022, corporate borrowing from non-banks has outpaced that from banks, with the latter’s share falling from 44% to 35% (Rosenthal et al., 2024), as can be seen in Figure 1. Source: Author’s Representation based on Rosenthal et al. (2024).

Thus, the role of tokenization platforms as market devices becomes especially clear when we examine the specific segments in which they are currently most active, namely, (1) private credit, (2) repos, and (3) asset management, as previously discussed.

For greater theoretical clarity, private credit refers to non-bank lending by specialized investment vehicles or funds to non-financial corporations of all sizes. These loans are privately negotiated and typically held to maturity on the originator’s balance sheet (Avalos et al., 2025). A key type of vehicle is the Business Development Company (BDC), which may be open to retail investors as in the US, where shares can be listed, or operate as closed-end funds that lock in capital for 5 to 8 years (Avalos et al., 2025). The latter structure dominates private markets and is usually accessible only to large institutional investors (Aramonte and Avalos, 2021).

Moreover, private markets rely on two main sources of leverage. First, target firms take on significant debt to finance acquisitions and amplify returns. For instance, BDCs can leverage up to 2x their net assets versus a 50% cap for US mutual funds. Second, private credit funds are now absorbing former bank clients while simultaneously depending on bank financing to generate leveraged returns, primarily via subscription credit facilities (SCLs) and asset-based lending (ABL). SCLs provide funds with rapid access to capital (faster than traditional capital calls), allowing for swift execution of time-sensitive deals, more predictable capital call schedules, and smoother investment operations (Bowen and Bundrant, 2017). ABL, meanwhile, expands the range of eligible collateral to include receivables, real estate, brand names, and intellectual property, unlocking critical liquidity (BofA, 2025). As such, by 2024, banks’ global exposure to private credit funds exceeded $500bn (IMF, 2025). Moreover, these funds also rely on revolving credit lines from banks, which are then extended to BDC borrowers (Gunter et al., 2024; IMF, 2025).

At this point, the role of the banking system has shifted from being direct lenders to corporates to the main financiers of the private credit ecosystem. As corporate clients migrated to alternative lenders, banks increasingly funded these entities. For example, over 14 years, banks’ loans and commitments to NBFIs grew from 6% to 16%, attaining this level in 2024. Banks also supply around 50% of hedge funds’ dollar funding (IMF, 2025).

This shift accelerated during the 2023 banking turmoil, exemplified by the collapse of Silicon Valley Bank, when private credit managers expanded their role (Rosenthal et al., 2024). That year saw major asset managers like Oak Hill Advisors, Fidelity, and Churchill launches their own BDCs. Yet, this transformation predates 2023: private credit assets under management (AUM) hit $1.4tn that year, up from $134bn in 2020, and reached $2.5tn by 2025, an enormous leap from $0.2bn in the early 2000s (Mouchbahani et al., 2024).

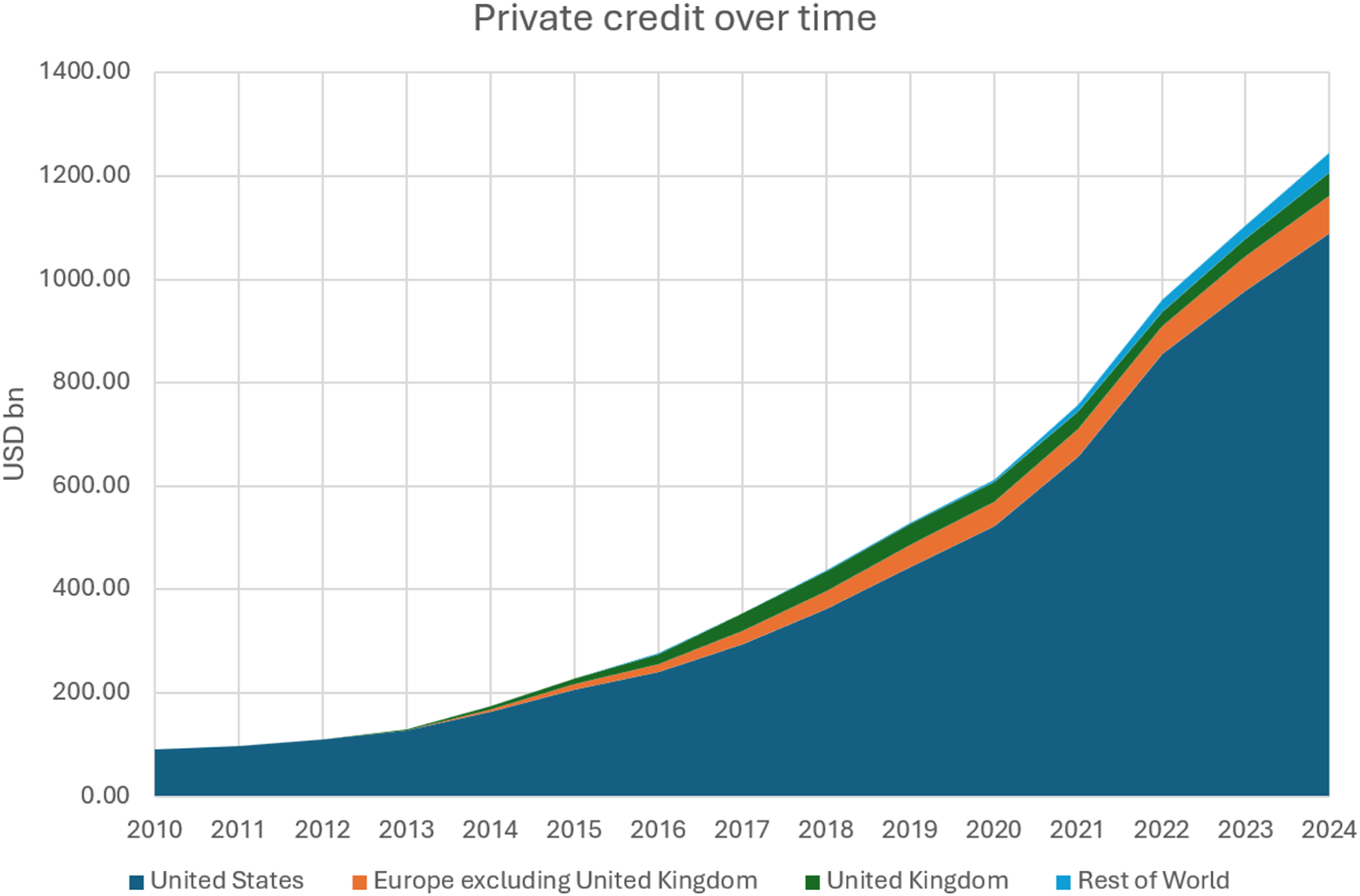

Multiple forces underpin this growth. Chief among them are persistently low interest rates and post-crisis banking regulations. The cost-of-capital spread between listed BDCs and banks narrowed by 200 basis points between the GFC and 2019 (Avalos et al., 2025). Regulations constrained banks’ ability to lend to high-risk or large-scale borrowers, creating space for BDCs, which could leverage more easily, access wholesale funding, and issue floating-rate loans, an attractive feature in low-rate environments (Avalos et al., 2025). Loan margins also contribute to the model’s appeal. Private credit loans tend to be larger than bank loans, averaging over $80mn (Cai and Haque, 2024; Rosenthal et al., 2024), and cater to highly leveraged firms that need flexible terms and lack tangible collateral (Avalos et al., 2025; Block et al., 2024). Macro-prudential rules have increasingly restricted banks’ capacity to meet such demands. This helps explain the steep rise of private credit since 2010, as shown in Figure 2, particularly in the United States. Source: Author’s Representation based on Bank of International Settlement data.

As banks lose direct access to corporate clients, they become increasingly exposed to the credit risks of BDCs and private credit funds, meaning any stress in these vehicles can spill over onto bank balance sheets. In response, tokenization platforms are emerging as tools for banks to win back clients, mitigate systemic risks, and reassert themselves at the center of the financial system. These platforms can also address structural barriers to broader participation in private credit markets, serving as market devices that help banks restructure the infrastructural balance of power in their favor.

For instance, investor concerns about liquidity, transparency, and efficiency remain significant structural barriers to broader participation in private credit markets (Gunter et al., 2024). According to Coalition Greenwich, many asset managers would have increased allocations to private credit if not for liquidity risks and high fees (Gunter et al., 2024), a view echoed by JPMorgan (Lobban et al., 2023). As such, despite its growth, private credit remains largely limited to institutional investors due to fragmented infrastructure and a lack of standardization (Lobban et al., 2023). Tokenization platforms could resolve this by automating and streamlining investment processes, enabling wealthier retail clients to access corporate funding markets. This segment is already viewed as a $400bn opportunity for tokenization providers (Lobban et al., 2023). For banks, this shift offers a chance to attract new retail and institutional clients, many of whom might otherwise gravitate toward the expanding alternative asset management sector.

It is also true that banks have made notable efforts to partner with private funds, but these collaborations have not addressed the core structural weaknesses of private credit. For example, in 2023, Wells Fargo teamed up with Centerbridge Partners to issue loans to mid-sized firms, while JP Morgan pledged $50bn to expand into private lending (PYMNTS, 2025). Though these moves signaled more direct competition by banks in the space, they left the systemic inefficiencies of private credit untouched.

To gain market share while addressing these barriers, US banks are developing and integrating tokenization platforms into their services. A leading example is Citi’s Token Service, which in 2024 completed a proof of concept (PoC) for tokenizing private funds alongside Wellington Management and WisdomTree (Citi Group, 2024). The PoC, conducted on Avalanche Spruce (an institutional test subnet), demonstrated how smart contracts can enhance operational efficiency and provide functionalities absent in traditional asset structures. These innovations could allow both buy- and sell-side institutions to interact with distributed ledger systems in a low-risk, regulatatory-compliant manner (Citi Group, 2024). While still early-stage, such initiatives mark a turning point. Banks, which previously served mainly as lenders to private credit funds, now see tokenization as a way to increase their role in this market. This perspective is supported by a survey from State Street, a leading asset management firm, which found that 64% of 300 surveyed financial institutions believe private equity is the most likely asset class to be tokenized, while 50% pointed to private credit (Redgrave, 2024). Moreover, even today, a large share of tokenized assets consists of private credit. In Q1 2025, private credit accounted for over 60% of all tokenized on-chain assets, specifically $12.5bn out of a total $19.7bn (Tran, 2025). By October 2025, the tokenized value of private credit alone had reached approximately $18 billion, out of about $29 billion in total tokenized assets across private credit, institutional alternative funds, and US Treasuries. This makes private credit by far the largest share of RWAs, with its value effectively doubling from the end of 2024, when it stood at $9.86 billion (PwC, 2025).

But it is not only private credit that is attracting attention; repo markets have also become increasingly salient in discussions on tokenization. Repos, short-term secured funding transactions in which securities are sold with an agreement to repurchase them at a predetermined price, have acquired renewed systemic importance in the post-GFC regulatory environment (e.g., Murau et al., 2025). This shift is largely attributable to the Basel III framework, which fundamentally altered the balance sheet economics of secured intermediation.

A central source of friction is the Supplementary Leverage Ratio (SLR), a non-risk-based capital constraint introduced to limit excessive leverage across bank holding companies (BHC). Despite its simplicity, the SLR has generated significant distortions in repo markets by penalizing balance-sheet-intensive activities, including the intermediation of low-risk assets such as US Treasuries. Under the SLR, all on-balance-sheet exposures are assigned a uniform 100% exposure measure, regardless of maturity or credit risk (D’Avernas et al., 2024), in contrast to risk-weighted capital rules.

In addition, the SLR allows only limited netting of repo and reverse repo positions, even when these transactions are economically offsetting and short-term. Repo intermediation therefore becomes disproportionately capital-intensive for large, systemically important banks operating near their leverage constraints. Importantly, these effects extend beyond the consolidated balance sheet: even when broker-dealers affiliated with BHC are themselves below the SLR threshold, group-level constraints remain binding. Empirical evidence suggests that the mere announcement and implementation of the SLR prompted many (BHC)-affiliated dealers to reduce their reliance on triparty repo funding, particularly in Treasury-backed segments of the market (Allahrakha et al., 2016).

More broadly, Basel III’s leverage-based backstop, while intended to enhance financial stability, has reshaped repo markets by discouraging dealer intermediation in precisely those markets central to monetary policy transmission and collateral circulation. The result has been thinner dealer balance sheets and greater sensitivity of repo rates to stress, as the SLR has raised the cost of balance sheet usage and reduced dealers’ willingness to act as shock absorbers in secured funding markets (Duffie, 2017; D’Avernas et al., 2024).

As such, the integration of tokenization platforms into repo transactions offers banks a strategic opportunity not only to remain active participants, but to become providers of the very infrastructure underpinning these markets. A clear leader in this space is JPMorgan. Since 2020, JPMorgan has developed a permissioned blockchain based on the Ethereum Virtual Machine (EVM), designed to apply tokenization to traditional financial flows. This initiative led to the launch of Kinexys Digital Assets. JPMorgan’s motivation was clear: the tokenization market is expected to grow exponentially, with projections placing it in the multi-trillion-dollar range (JPMorgan, 2024: 6). This can be seen, for example, at Broadridge, a US-based fintech firm, which has facilitated over $1tn in tokenized repo transactions per month via its Distributed Ledger Repo (DLR) platform since 2023 (McKinsey, 2023).

JPMorgan’s approach is multifunctional, with an initial focus on collateral transformation. Through Kinexys (formerly Onyx), it launched the Tokenized Collateral Network (TCN), which enables financial institutions to convert traditional assets into tokenized collateral without relocating the underlying securities (Futures Industry Association FIA, 2025). This unlocks previously ineligible assets for use as collateral (JPMorgan, 2022). The benefits are substantial: improved transparency over collateral ownership, reduced settlement times, enhanced collateral mobility, and/or the elimination of manual processing (JPMorgan, 2024). For JPMorgan, this creates capital efficiencies by broadening the pool of eligible collateral and enabling near-instant settlement of tokenized assets. For third-party clients, TCN offers cost-effective liquidity solutions through repo transactions, serving as an alternative to traditional credit lines. This is possible because third-parties have their own node, as part of the JPMorgan’s blockchain network, where they can settle trades (Futures Industry Association FIA, 2025).

This efficiency made intraday repo the first major use case for Kinexys. Between 2020 and 2024, JPMorgan processed over $1.5tn in intraday repo transactions. While small relative to the $15tn global collateral market, the volume is expected to grow (JPMorgan, 2022). JPMorgan also facilitated the first intraday reverse repo with an external counterparty, OCBC. Using Kinexys, OCBC lent funds to JPMorgan in exchange for tokenized assets; the transaction, settled with interest in under 4 hours, improved OCBC’s liquidity management resilience (Ledger Insights, 2024). Following this, BNP Paribas became the first European bank to execute a repo transaction on JPMorgan’s blockchain, further signaling global adoption (BNP Paribas, 2022). In 2025, Kinexys supported its first intraday non-dollar repo where JPMorgan acted on only one side. Two transactions, $50mn and €50mn, were settled with Santander as the seller and JPMorgan as buyer (Ledger Insights, 2025).

Another prominent example is HSBC Orion, which facilitated the first cross-border repo transaction involving a natively issued digital bond executed and settled on a public blockchain (UBS Media, 2024a). This was not a standard repo because it spanned three jurisdictions: Switzerland, Singapore, and Japan. This transaction involved borrowing tokenized Japanese Yen (JPY) against a JPY-denominated digital bond, with the borrowed JPY used to finance the bond’s purchase. The full cycle, including redemption, principal, and interest payments, occurred entirely on a public blockchain (UBS Media, 2024a).

As such, tokenization platforms help banks in repo markets by easing regulatory constraints in three main ways. First, near-instant settlement and intraday repo shorten how long transactions remain on balance sheet, reducing average exposures under leverage and SLR constraints without altering formal rules. Second, tokenization increases collateral mobility by allowing assets to be pledged in tokenized form while remaining with existing custodians, lowering frictions around collateral transfer and reducing the need for large buffers. Third, real-time tracking and auditability of tokenized repos align better with stress-testing and intraday liquidity requirements (RLAP/RLEN), enabling banks to operate with lower precautionary reserves while meeting supervisory expectations.

Another domain where banks have lost ground is asset management, where dominance has shifted to institutional investors such as BlackRock, Vanguard, and State Street. Asset managers offer collective investment vehicles to both retail and institutional clients, generating revenue primarily through fees (Braun and Christophers, 2024; Goghie, 2023). As this sector expanded, many argue that power has shifted from banks to large pools of institutional capital (Braun, 2022). The scale of this transformation is notable. Between 1980 and 2007, asset management revenue, spanning mutual funds, money market funds, and Exchange-Traded Funds (ETFs), rose fivefold, from around 0.2% to nearly 1% of GDP (Braun, 2021). The GFC accelerated this trend, eroding trust in banks and driving capital toward asset managers. One emblematic outcome was BlackRock’s 2009 acquisition of Barclays Global Investors, including iShares, the world’s top ETF brand at the time (Braun, 2021). In response, banks have turned to tokenization platforms as strategic instruments to reclaim influence across asset management services.

Let’s consider UBS Tokenize, which is a blockchain-agnostic platform. What does this mean? UBS Tokenize is not dependent on a single Blockchain framework; rather, this platform was developed as an open architecture that can be integrated with multiple DLT networks (UBS, 2024). This broadens the use of these services. Moreover, UBS Tokenize functions as a full-service platform. It manages the entire tokenization lifecycle, from origination (i.e., legal documentation and structuring) to the distribution of tokenized assets to investors. Its distribution network supports asset fractionalization and leverages UBS’s existing client base to boost demand, liquidity, and placement. UBS developed Tokenize in response to rising client demand. As Thomas Kaegi, co-head of UBS Asset Management for Asia-Pacific, noted: “We have seen growing investor appetite for tokenized financial assets across asset classes” (UBS, 2024).

Shortly after this strategic positioning, a pivotal development unfolded in the tokenization of RWAs. On November 1, 2024, UBS Asset Management launched its first tokenized money market fund (MMF), namely, the UBS USD Money Market Investment Fund Token (uMINT) (UBS Media, 2024b). MMFs are mutual funds that invest in short-term debt instruments and cash equivalents. uMINT, structured under Singapore’s Variable Capital Company (VCC) framework, is an actively managed, USD-denominated MMF investing in high-quality, diversified money market instruments (ReadiFi, 2024). Access is restricted to accredited investors, and the fund operates as a permissioned system, meaning transfers are limited to verified token holders. In this direction, UBS partnered with DigiFT, a licensed Capital Markets Services provider and Recognized Market Operator in Singapore, ensuring compliance with regulatory standards (ReadiFi, 2024). This reflects UBS Tokenize’s broader strategy: merging blockchain functionality with institutional-grade oversight.

Another important case involves Fidelity International, which joined JPMorgan’s TCN to pilot the tokenization of its MMF via Kinexys. The goal was to enhance margin efficiency, cut operational risk, and reduce transaction costs through real-time tokenization between JPMorgan’s transfer agency business and the TCN (Allison, 2024). A central innovation here was the use of tokenized MMF shares as collateral, in line with JPMorgan’s emphasis on tokenizing assets that traditionally fall outside accepted collateral frameworks.

A further milestone came with the three-way collaboration between JPMorgan, Barclays, and BlackRock, demonstrating how banks can leverage tokenization platforms to re-enter the asset management domain. This initiative also used the TCN to tokenize MMF shares and use them as collateral in an over-the-counter (OTC) derivative transaction, a first involving three regulated entities. BlackRock tokenized MMF shares using TCN, aiming to increase mobility without moving the underlying asset (Watkins, 2023). Barclays then accepted these tokenized shares as collateral in the derivative deal. The transaction was praised as a breakthrough in post-trade settlement, improving transfer speed, reducing margin costs, and lowering operational friction during periods of market stress (Watkins, 2023). Collectively, these initiatives suggest that tokenization not only unlocks new use-cases for traditionally static assets but also provides banks with a strategic entry point into asset management flows, countering the dominance of large institutional investors.

In a sense, in the context of asset management, banks’ tokenization platforms are also a defensive strategy, a way to limit the growing influence of fund tokenization led by asset managers. In recent years, firms like BlackRock and Franklin Templeton have aggressively expanded into the tokenized MMF space as well. Notable examples include the Franklin OnChain US Government Money Fund (FOBXX) launched in 2021, and the BlackRock USD Institutional Digital Liquidity Fund (BUIDL) launched in 2024, which surpassed $2.5bn in AUM by May 2025 (Chan et al., 2024; PANews, 2025). Thus, it has become a race against time for banks to prevent asset managers from further centralizing their role in offering tokenized services such as MMFs.

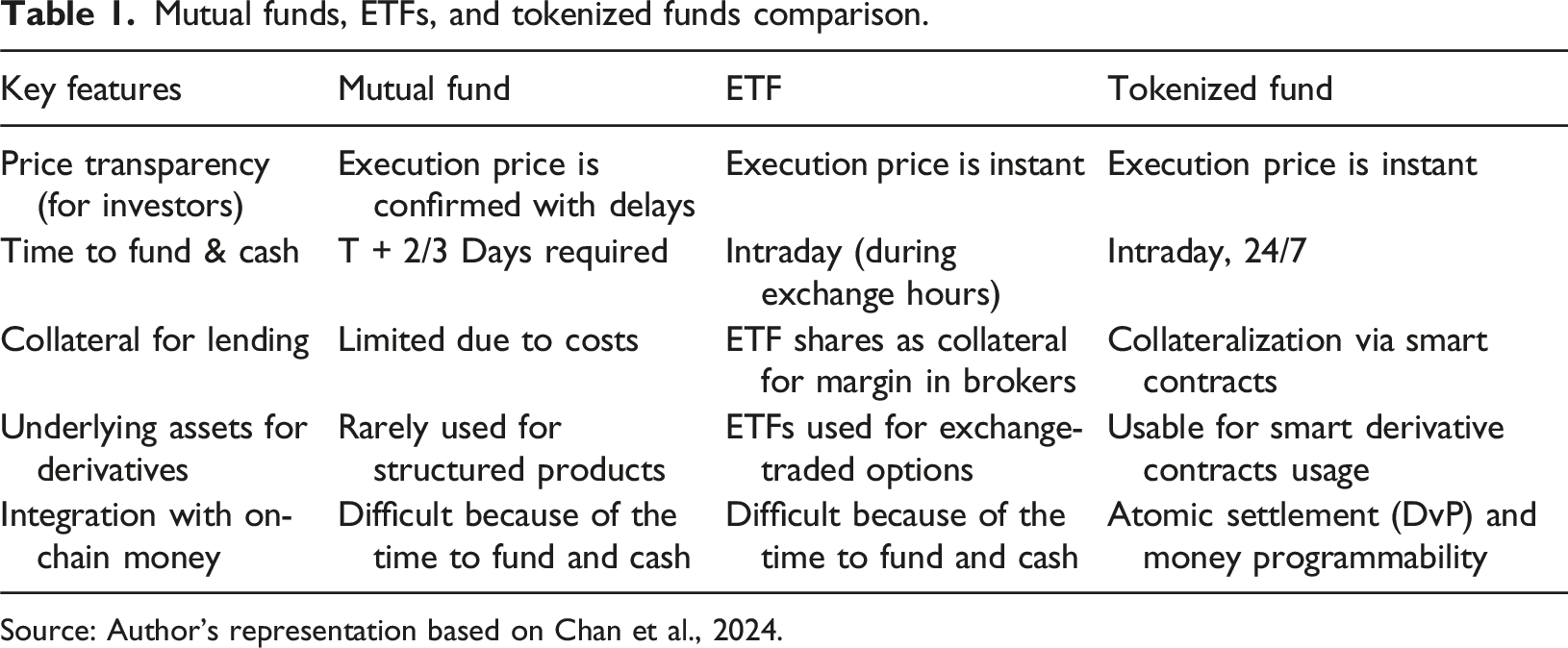

Mutual funds, ETFs, and tokenized funds comparison.

Source: Author’s representation based on Chan et al., 2024.

Thus, tokenization funds solve certain fundamental problems of mutual funds, such as instant settlement, which leads to increased productivity of trapped capital, potentially adding about US$50bn annually to investor portfolios (Chan et al., 2024). Moreover, efficiency gains through smart contracts help simplify collateralization, without mentioning that the simplicity of intraday transactions of tokenized mutual funds will attract even more institutional investors capable and willing to generate returns from Net Asset Value (NAV) fluctuations (Chan et al., 2024). Likewise, since bookkeeping is inherently tied to smart contracts, this streamlines workflow mutualization and process automation, which helps increase liquidity and can make illiquid investments more cash-convertible for individuals. This supports the argument that tokenization in the fund and private credit industries represents a $400bn opportunity (Lobban et al., 2023).

Concluding remarks

This paper has examined tokenization platforms as a distinct form of platform power, through which incumbent banks reassert strategic control in the post-crisis financial system. Unlike paradigmatic digital platforms studied in the platform power literature, where influence is often derived from user mediation, data extraction, or ecosystem expansion, bank-led tokenization platforms operate through infrastructural embedding and regulatory alignment. By offering faster, more liquid, and lower-friction mechanisms to issue, mobilize, and settle assets, these platforms make themselves the most efficient route for participation in critical financial markets. Compliance is encoded directly into operations, reducing regulatory risk and operational complexity, effectively nudging activity through the bank’s infrastructure and restoring centrality over flows that had migrated to non-bank actors following post-GFC regulatory tightening.

In doing so, tokenization platforms extend the concept of platform power beyond consumer-facing and data-intensive digital platforms. Existing literature, emphasizing artifactual and contractual power, network effects, and data-driven accumulation, among others, only partially explains how influence operates in highly regulated financial markets. Tokenization platforms demonstrate that power can be exercised through infrastructural efficiency and embedded compliance, shaping participation and capital allocation without monopoly rents and/or intermediation of dispersed users. This represents a novel modality of platform power, where technological architectures are leveraged to reorganize market dynamics and reassert the dominance of incumbent institutions.

Empirically, the paper shows how UBS Tokenize, JPMorgan Kinexys, HSBC Orion, and Citi Token Service embody this form of power. By embedding efficiency and regulatory alignment into financial infrastructure, banks strategically steer capital and reclaim influence across private credit, repo, and asset management. This challenges the prevailing assumption in the platform power literature that platformization necessarily displaces incumbents or undermines public authority. Instead, tokenization platform represents a strategic use of digital technology by incumbents to entrench their infrastructural and strategic centrality within highly regulated markets.

Ethical consideration

The author confirms that all the research meets the ethical guidelines, including adherence to the legal requirements of the study country.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.