Abstract

The European Union’s strategy for technological sovereignty relies on private capital to fund key sectors like artificial intelligence (AI). However, the structure and composition of this capital ecosystem remain unclear. Using a novel dataset of 110 European AI startups and their 826 funders, this paper maps meso-level investment patterns and identifies the key financial actors underpinning European AI development. Beyond a descriptive mapping, I argue that the EU’s market-based industrial policy empowers a select group of aligned financiers including ‘patriotic billionaires’ as crucial intermediaries in the pursuit of technological sovereignty. This dynamic grants these actors structural potential to shape policy, altering the traditional state-finance relationship. The research suggests a distinctive European model of techno-financing, and analyzes its implications for state power and economic governance in a period of intense geopolitical transformation.

Keywords

Introduction

In an era of intensifying geopolitical competition, the European Union (EU) is pursuing strategic autonomy in key economic sectors (Draghi, 2024a). Artificial intelligence (AI) has been identified as a particularly crucial driver of untapped economic potential. The promise of powerful statistical techniques, such as neural networks, to analyze and generate data is widely seen by investors, policymakers, and the popular press as a solution to reignite productivity growth, safeguard technological sovereignty, and ensure Europe’s relevance in the geopolitical landscape. However, the EU is currently perceived to be lagging in the putative race to develop AI. This has led to growing calls for a more streamlined regulatory environment and targeted capital deployment to bolster the EU’s domestic AI ecosystem.

This should be understood as a part of a shift towards a “catalytic” form of state capitalism, where states occupy a more active role in shaping economic processes (Alami and Dixon, 2024). In the EU, significant institutional, political, and structural constraints on fiscal policy limit the capacity for direct public investment as a tool of industrial transformation (Braun et al., 2018; Lepont and Thiemann, 2024). Consequently, the EU traditionally relies on private, market-based finance, augmented by strategically deployed public capital, to finance key strategic initiatives. This approach, driven by fiscal constraints and an enduring institutional preference for market-led solutions, assigns private financial actors a structurally pivotal role in Europe’s pursuit of strategic goals.

Yet, the structure and interests of the ecosystem of private capital expected to underwrite the EU’s ambitions remain largely unknown. Who are the concrete funders who are supposed to finance the European industrial policy and what are their inter-relations? This ambiguity represents a critical gap in our understanding of the European political economy, especially in the case of early-stage startups. Unlike public markets, which can be treated in aggregate and abstract terms (Braun, 2020; Braun and Koddenbrock, 2022), venture capital (VC) ecosystems are thick social environments. They are characterized by a limited number of embedded actors with established hierarchies, reputations, and geographical and sectoral foci, creating an entrenched structure that conditions the development pathways for the European tech development.

From the perspective of industrial policy, understanding this ecosystem is critical, as it mediates between industrial policy aspirations and outcomes. This is especially salient, due to the inherent mismatch between objectives and the traditional dynamics of venture capital: while the EU’s strategic goals require patient, programmatic capital dedicated to building industrial capacity and strategic externalities (European Innovation Council, 2024; Frolund, 2023), this clashes with the dominant VC logic, which favors hyper-scalable, capital-light startups with a clear preference for rapid, high-return exits, often in the deep capital markets of the United States (Bracy, 2025; Cooiman, 2024; Lerner and Nanda, 2020). Given the EU’s limited capacity to impose policy discipline on capital markets (Liu, 2024), enrolling rooted financiers who are volitionally aligned with Europe’s strategic objectives becomes a central imperative. This tension orients two central questions for this paper. First, what is the actual structure and composition of the capital ecosystem underpinning European AI development? This empirical question, who is actually funding the EU AI companies must be answered before its political implications can be assessed. Second, how does this specific market-based industrial policy, which relies on this ecosystem, empower and interact with specific financial actors?

In this paper, I argue a distinct European model of techno-financing is emerging, different from both the state-corporate dominated model in China and the Big Tech-dominated ecosystem in the US. The European AI finance landscape is characterized by a heterogeneous set of actors, including select national development banks, well-positioned venture capital funds, and high-net-worth individuals I call “patriotic billionaires” who supply patient and strategic capital for European AI companies. Notably, I suggest this signals an inversion of conditionality in European industrial policy. Instead of the state attaching conditions to its capital, strategically aligned private financiers may attach conditions for their cooperation. Their willingness to provide patient capital is a scarce resource, and the possibility of withholding it grants them significant leverage, “voice” to shape policy from within. This process fuses a select group of financiers to the apex of political power and creates an engine for institutional change in the EU, with potential political repercussions.

To substantiate this claim, I empirically explore the capital ecosystem behind private AI companies in the EU and analyze how European market-based industrial policy leverages and empowers these specific financial actors. Using a novel dataset on the funding of 110 private AI startups as of January 2024, I conduct a network analysis to unveil the structure of AI funding. This analysis identifies an apex group of capital circulation, comprising interconnected networks of individual billionaires, national development banks (NDBs), European and third-country private equity companies, and corporate venture investors. This network analysis, complemented by primary documents and inductive case studies as part of a nested research strategy (Lieberman, 2005), reveals distinct regional sub-clusters with varying levels of state involvement and closely-knit networks engaged in both cooperative and conflictual interactions. These findings shed light on how technological transformations and consequent political reactions reorganize social relations, empowering particular actor groups and spurring transformations in the state-finance nexus.

The paper proceeds as follows. First, I will discuss artificial intelligence (AI) as a contemporary theme in political economy. I then discuss what is theoretically at stake. In the empirical section, I uncover and discuss the capital ecosystem underpinning European AI startups. These results are then discussed. The final section concludes.

State of strategic digital autonomy in the European Union

While AI is a longstanding phenomenon, the current wave of generative artificial intelligence emerged into public consciousness with the launch of OpenAI’s ChatGPT in November 2022. The scale of realized productivity gains from AI is still debated (Acemoglu, 2024; cf. Eloundou et al., 2023). Regardless of the outcome, the promise alone has spawned societal conflicts and institutional transformations that are now objects of study in international political economy (Crawford, 2021; Dauvergne, 2022; Ding, 2024; Lehdonvirta et al., 2025; Mügge, 2024; Rikap, 2024).

The development of large-scale AI in the 2010s has been dominated by a few American “hyper-scalers” and their partners (Kak et al., 2023; Rikap, 2024; van der Vlist et al., 2024). In addition to centralizing the R&D that advanced the contemporary AI paradigm (Ahmed et al., 2023), these companies influence innovation trajectories by using their control over key inputs computation, data, and talent and ubiquitous distribution networks to entice fledgling AI startups into their innovation ecosystems (Federal Trade Commission, 2025). A 2024 UK Competition and Markets Authority (CMA) study identified over 90 partnerships between leading AI labs and hyper-scalers between 2019 and 2024 (CMA, 2024: 30–34). In 2023, investments from Big Tech companies accounted for $27 billion, or two-thirds of the total private capital invested in AI startups globally (Hammond, 2023).

In recent years, this economic concentration has taken on a geopolitical dimension. The imaginary of an “AI race,” a hegemonic competition harking back to Cold War arms-race rhetoric (Schmid et al., 2025), has spurred calls for industrial policies to develop domestic AI capacities (Kak and West, 2024). In the US, AI development by large tech companies has been securitized as a matter of national interest; in early 2025 U.S. Vice President J.D. Vance proclaimed the US as the leader in AI, with intentions to “keep it that way” (Vance, 2025). In the People's Republic of China (PRC), state- and corporate-facilitated investment in AI production has accelerated, in line with a coordinated industrial policy to make China the “world’s primary AI innovation center” by 2030 (Chan et al., 2025; State Council of the People’s Republic of China, 2017).

The geo-politicization of AI has transformed the state’s role in AI governance away from the regulatory state (see Ferrari, 2024). While the EU has been proactive in developing regulatory frameworks, it has struggled to cultivate domestic AI champions. Although a facilitatory state role was part of the 2018 EU AI strategy (European Commission, 2018), this has gained more prominence in the “geodirigiste turn” (Seidl and Schmitz, 2023) in reaction to geopolitical frictions, embedded in considerations of achieving “strategic autonomy” in critical sectors. While the precise content of such autonomy remains contested (Falkner et al., 2024) it has gained prominence amid threats of weaponized interdependencies (Farrell and Newman, 2019), spurring calls to develop European capacities to stay in the “AI race.” The focus on artificial intelligence companies is but a part of sweeping efforts to negotiate and derisk the Europe’s dependencies in the global networks of production, finance and digital infrastructures (Schindler et al., 2024) that have translated to efforts to develop an alternative digital “stack” in the European Union (Falkner et al., 2024, e.g. Eurostack 2025).

Salience of perceived failure to act on AI was highlighted in a landmark report by former ECB chief Mario Draghi (Draghi, 2024a). The report outlined Europe’s weaknesses, and a dedicated section argued that the failure to grasp previous technological transformations was a key factor in the growth gap between the EU and the US. Grasping the AI transformation is seen as a window to restore European productivity and manufacturing potential (Draghi, 2024a: 6). While a strong research base in AI is a key strength, the failure to commercialize this potential is lamented. The data shows substantial gap: only 6% of AI funding goes to the EU, in contrast to 61% to the United States (Draghi, 2024b: 79).

In addition to regulatory obstacles, a key challenge for European AI is the lack of risk-willing, patient capital (Draghi, 2024a; Fratto et al., 2024). Developing internationally competitive AI companies is capital-intensive, given notable infastructure costs and the expensive talent required. While early-stage capital is available, mobilizing growth-phase capital for scaling has proven a potent policy challenge (Draghi, 2024b: 79–83). A key response has been the activation of the European Investment Bank Group (Cooiman, 2021; European Innovation Council, 2023; Mocanu and Thiemann, 2024), bringing the previously “hidden” investment state (Mertens and Thiemann, 2019) into the open.

Crucially, these initiatives attempt to not only raise but also direct private finance towards policy objectives. In contrast to technologically shallow, short term, hyperscalable companies (Cooiman, 2023), EU initiatives are directed at “deeptech” rooted in cutting-edge science and engineering (European Commission, 2024), with the objective to scale best-in-class companies while managing strategic dependencies. The focus is on building foundational infrastructural technologies, like large AI models, that can create spillovers to the broader European ecosystem.

This objective has implications on the capitalization table of the start-ups. Threat of acquisition by foreign investors is referred to as a particular threat to European aspirations for strategic autonomy. Moreover, the focus on deep tech necessitates distinctive capital sources. As noted by a member of the EIC Fund board, such objectives require “strategic, programmatic and patient capital,” in the form of a “total shift” in the way venture capital currently works in Europe (Frolund, 2023). This identified gap between the EU’s policy aspirations (patient, strategic capital) and the reality of its financial ecosystem (a VC model geared toward rapid exits) creates a central puzzle. It is unclear who is expected to provide this patient capital, what the structure of this emerging finance ecosystem looks like, and how the state is attempting to mobilize these specific actors. The literature has identified the need for this shift but has not yet empirically investigated the financial actors and networks being marshalled to execute it.

Theoretical framework of the investor state

The industrial policy push towards AI is part of a broader transformation of state capitalism, driven by the desire for states to take a more proactive role in pursuit of strategic autonomy and to respond to changing geoeconomic and geopolitical conditions (Alami and Dixon, 2024; Babic, 2023). The evolution of state capitalism is not homogenous. In the political economy of the post-2010s EU, a distinctive form of European state capitalism has been the tendency to “govern through financial markets” (Braun et al., 2018), that is, enrolling the tools and private actors of financial markets to pursue policy goals that exceed the direct institutional and fiscal capacities of the EU. This “off-balance sheet” policymaking is often explained as a result of institutional constraints, such as constraining macroeconomic frameworks (Baccaro et al., 2022; Johnston and Matthijs, 2022), a dearth of common EU-level fiscal capacities, and enduring market-liberal commitments.

In recent literature, this European mode has been conceptualized as the “European investor state” (Lepont and Thiemann, 2024), where the state simultaneously seeks to imitate and enroll private finance, assuming a novel investor role in contrast to the classical “administrative” (Hall, 1989) or “regulatory” (Majone, 1997) roles. This shift leads to new political constellations where successful policy implementation is conditional on private finance cooperation (Lepont and Thiemann, 2024: 384). The dynamics of this transformation are an active research field.

European Union has been especially active in leveraging private finance in the venture capital market, aimed at breeding “European unicorns” (Alayrac and Thyrard, 2024; Cooiman, 2021; Mocanu and Thiemann, 2024). The European Investment Bank Group has become one of the leading sources of capital for European VC, both through direct stakes (EIC Fund) and especially through indirect fund-of-fund investments (EIF) (European Innovation Council, 2023; European Investment Fund, 2024). The objective is to leverage limited public funds to patch the investment gap by mobilizing private investors, manipulating risk-return profiles by providing risk-absorbing public capital to solve market failures in long-term capital allocation (Gabor, 2021). There is a vibrant academic debate on the political-economic consequences of consigning venture capital to public policy objectives (Alami, 2025; Alami et al., 2024; Cooiman, 2023, 2024; Klingler-Vidra and Pardo, 2025; Mocanu and Thiemann, 2024). For political economists, a crucial question is how this structure of financial intermediation shapes the relationship between state power and private finance. Notably, Cooiman (2023) argues that this entanglement subjects policymakers to the logics of market-based finance, structurally constraining their options. In contrast, Mocanu and Thiemann (2024: 447) reserve more agency for European institutions to co-produce these new environments, calling attention to the goals and motivations of public actors.

However, these debates stop short of exploring the variation inside the field of market-based finance. Fiscal interventions do not reach productive resources directly; they are intermediated by a set of actors in the investment chain. Hence, a crucial direction for research is to open the black box of private finance to uncover its “social thickness” in empirical detail. While public financial markets are often usefully treated in infrastructural terms marked by investor substitutability and public information (Braun and Koddenbrock, 2022) private venture capital ecosystems consist of identifiable, sector-specific investors that compete and cooperate in thick social environments (Hochberg et al., 2007; Lerner and Nanda, 2020; Sorenson and Stuart, 2001), in which situated actors operate in a complex, contextual environment, where motives and actions are conditioned by interpersonal networks and relative social positions, in contrast to “thin” environments where conduct is a result of reactions to external forces.

These ecosystems exhibit pronounced hierarchical organization reinforced by the Mertonian Matthew effect where previous successes help top investors attract high-potential startups and valuable networks creating reputational and informational advantages. Research indicates that in the US, the top 2% of VC funds capture 95% of market profits (Rao, 2023). Importantly, these leading investors do not merely “pick” winners but actively “create” them (Cooiman, 2023). As such, the specific structure of investment ecosystem mediates economic statecraft. Mapping this social embeddedness requires a granular examination of the market’s relational structure in contextual detail. Different sectors have idiosyncratic financing patterns. As VC’s value proposition includes sector-specific support, investors specialize, and these patterns develop inertia as networks and reputations create entrenchment. Most promising startups self-select towards prominent investors, creating high barriers to entry for alternative funders. As summarized by an old VC adage: “it isn’t getting the money, it’s who the money comes from” (Sorenson and Stuart, 2001: 1554).

This underscores the underappreciated political salience of the composition of private capital formations as intervening variable in the economic statecraft. In market-based polities, state capacity to steer economic activity towards strategic objectives relies on the cooperation of private capital. These providers differ not only in their structural position within the hierarchy of capital ecosystem or in the sheer amount of investable capital but also in their allocative agency. One source of this variation is driven by the structural constraints governing different investor types. For instance, institutionalized financial actors, such as pension funds, are bound by legal obligations and fiduciary duties that limit their capacity to proactively align with discretionary policy objectives. Conversely, private actors with greater allocative agency such as private corporations, family offices, or even individual billionaires (Hägel, 2020, 11), have more flexibility to deploy capital based on a non-pecuniary political or philanthropic set of interests, such as private economic patriotism.

I investigate the composition of European capital ecosystem using a nested research strategy (Lieberman, 2005), combining computational network analysis with qualitative case studies. First, to answer the research question I conduct a social network analysis (SNA) of the 110 startups and their 826 funders. This analysis maps the ecosystem to identify central actors (using measures of degree and betweenness centrality). This quantitative map of “who is connected to whom” moves beyond an aggregate treatment of finance to reveal the specific, relational structure of the market. Second, to investigate how this policy empowers specific actors the network map is used to guide qualitative case selection. Key central actors and representative clusters identified in the SNA are then explored through inductive case studies and primary document analysis. This layered, mixed-methods orientation helps to mitigate data availability challenges and follows recent calls in computational social science to use computational methods to identify contingent patterns, which are then explained through conjunctural, qualitative inquiry (Törnberg and Uitermark, 2021).

Data and findings

Venture capital industry, business press, and research organizations routinely produce listings on funders in the EU AI and tech ecosystem (Accel, 2024; Shizune, 2024; Atomico, 2024; Ene, 2025; Kaltheuner et al., 2024). The relational structure of this ecosystem, however, remains elusive. Teasing this out requires solving a few challenges. First, it is not obvious how to define the set of prominent European AI companies, given classification problems and selection biases in existing lists. Second, selecting the “most prominent” companies is subjective, as the value of private start-ups is not legible from market capitalization and depends largely on intangible factors (Gornall and Strebulaev, 2017). Third, the venture capital market is “maddeningly private” (Lerner and Leamon, 2023), meaning data on valuations and funding are often not public. Data gathering thus requires triangulation and a tempered expectations on the evidentiary basis. The limitations of the data and search parameters are discussed in more detail in Annex 1.

Dataset development

To address these shortcomings, I constructed a sample of the European AI ecosystem through iterative data collection. The starting dataset consists of all private startups in the European Free Trade Area (EFTA) in the field of artificial intelligence software at the start of 2024, with a reported post-money valuation over $10 million (56 companies from Factset). I enriched this set with non-duplicate companies that have raised a funding round over $100 millionn but have not disclosed their valuation. This resulting set was cross validated against public benchmark reports and listings in the business press.

After qualitative filtering to ensure AI was central to the business, the set was validated against the judgment of industry professionals. For these filtered companies, I extracted funding round information from FactSet research (as of September 2024), resulting in a sample of 110 companies (displayed in Annex 1) and 826 investors. To address data limitations, I focus on unweighted ties (co-investments) between investors. Robustness testing suggests that adding or removing salient cases at the selection boundary does not change the general patterns. However, due to the limitations of the data at hand, the study should be understood as an exploratory foray (Swedberg, 2020) shedding light on the currently murky world of VC finance, a disciplining factual basis to identify the social patterns present in the European AI ecosystem.

The shape of the European AI ecosystem

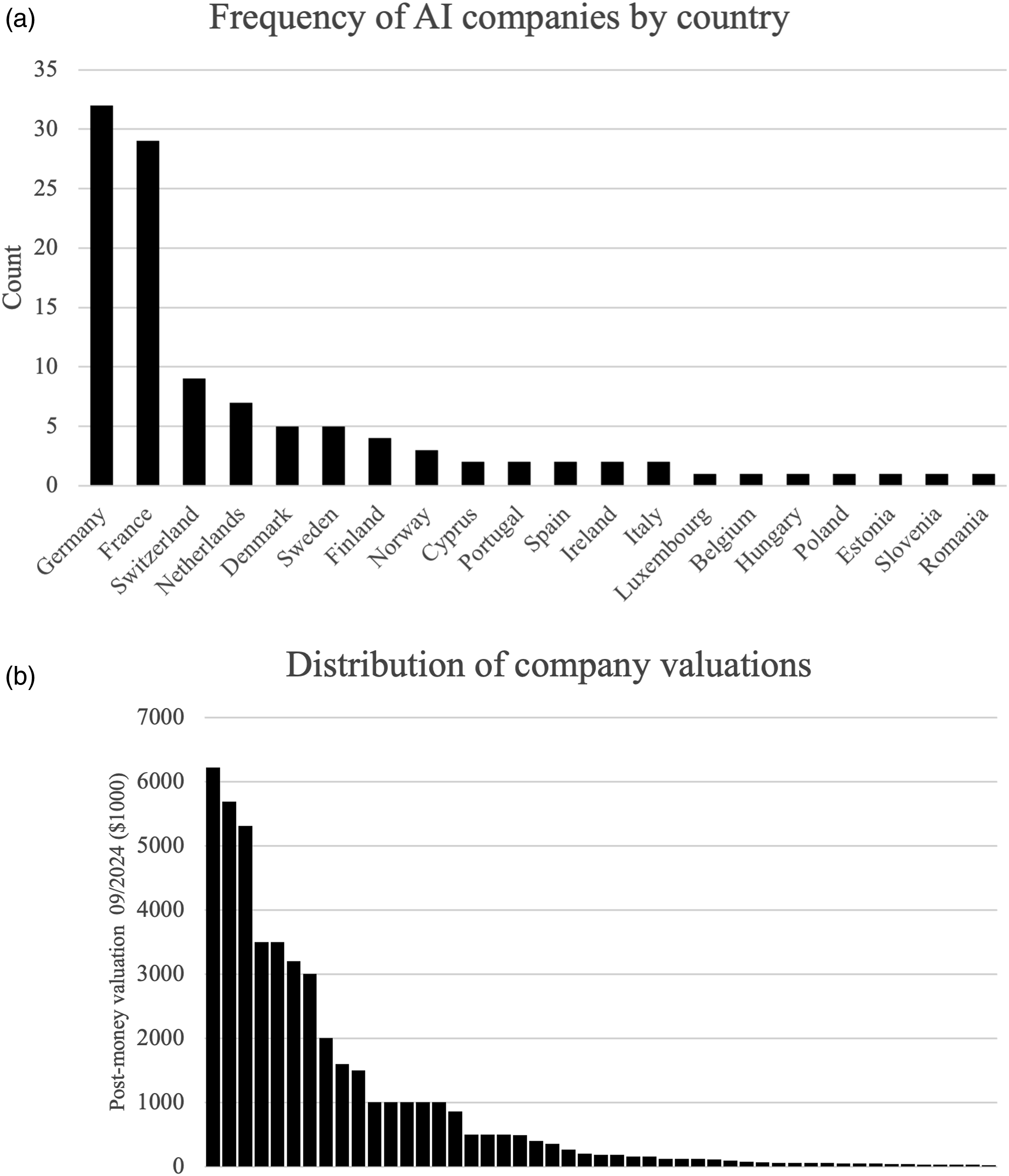

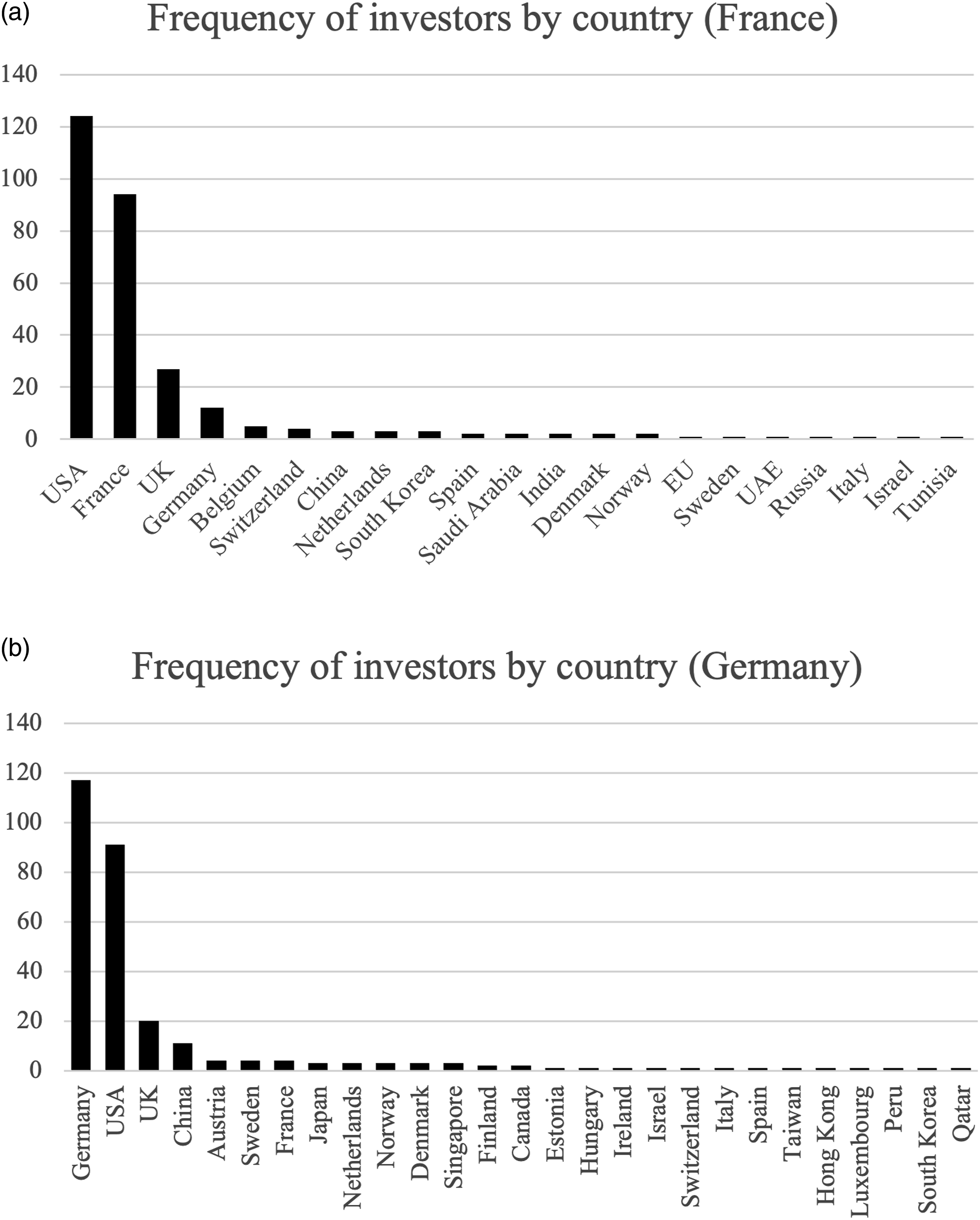

The dataset first reveals substantial variation among the companies. Geographically, AI startups are heavily concentrated in the largest member states, with Germany (28%) and France (26%) collectively accounting for 55% of the sample. Following them are Switzerland (8.1%), the Netherlands (6.3%), and the Nordics. Southern and Eastern European member states are notably underrepresented (Figure 1(a)). The ecosystem exhibits a heavy-tailed distribution in valuations (Figure 1(b)): of the 110 companies, only 20 are “unicorns” (valued over $1 billion), with outliers like the French Mistral AI ($6.2 billion), Finnish Relex Solutions ($5.4 billion), and German Helsing ($5.3 billion). The types of AI range from providers of foundational large-scale AI models (e.g., Mistral, Poolside SAS, DeepL, and Aleph Alpha) and customer service chatbots (e.g., Cognigy and Parloa), to cryptography, cybersecurity, and data protection solutions (e.g., Veriff Oü and Acronis AG), as well as robotics and drone companies (e.g., IX Technologies and Blue Ocean Robotics). (a) Frequency of companies by country. (b) Distribution of valuation of companies in the sample.

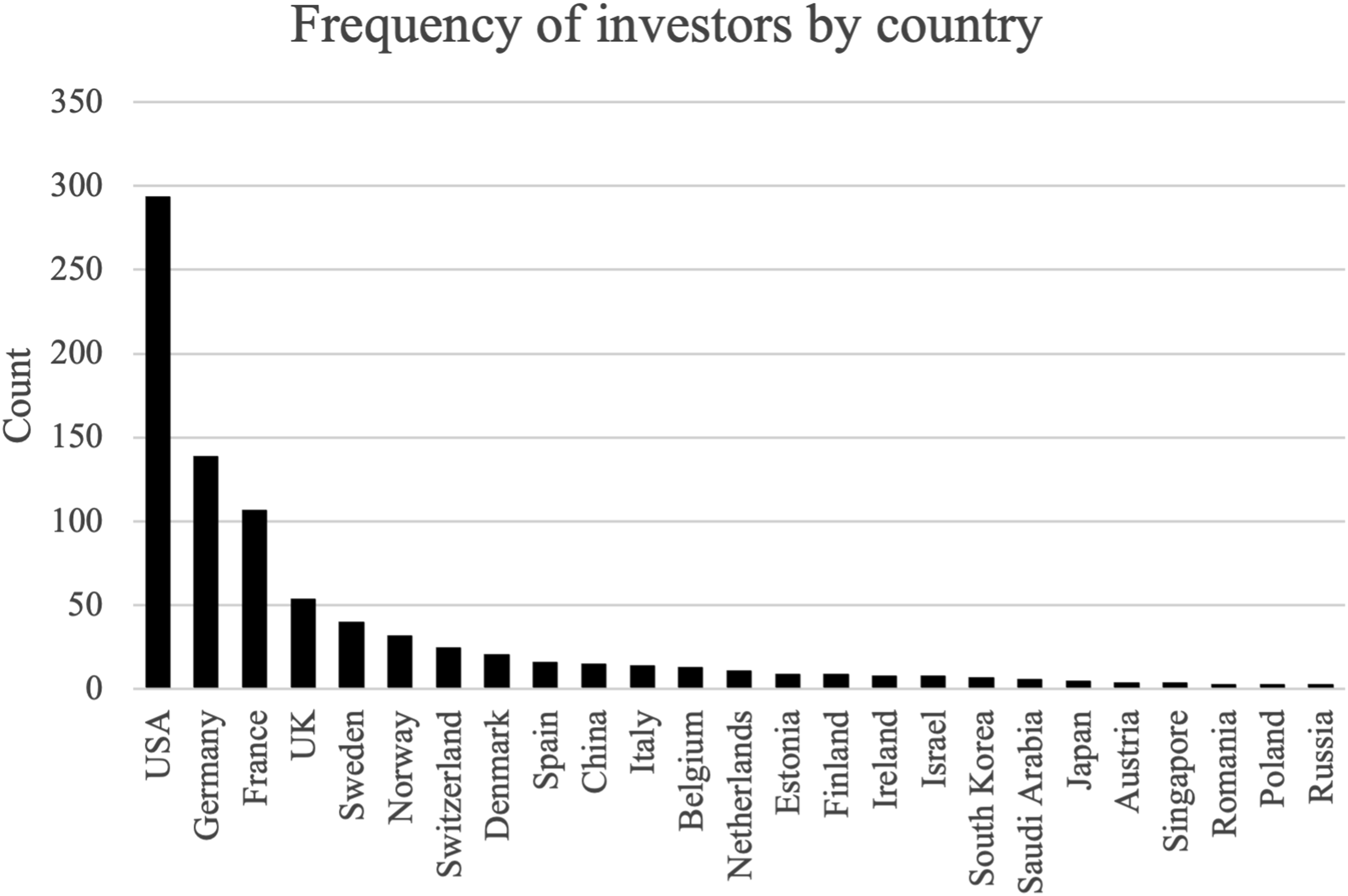

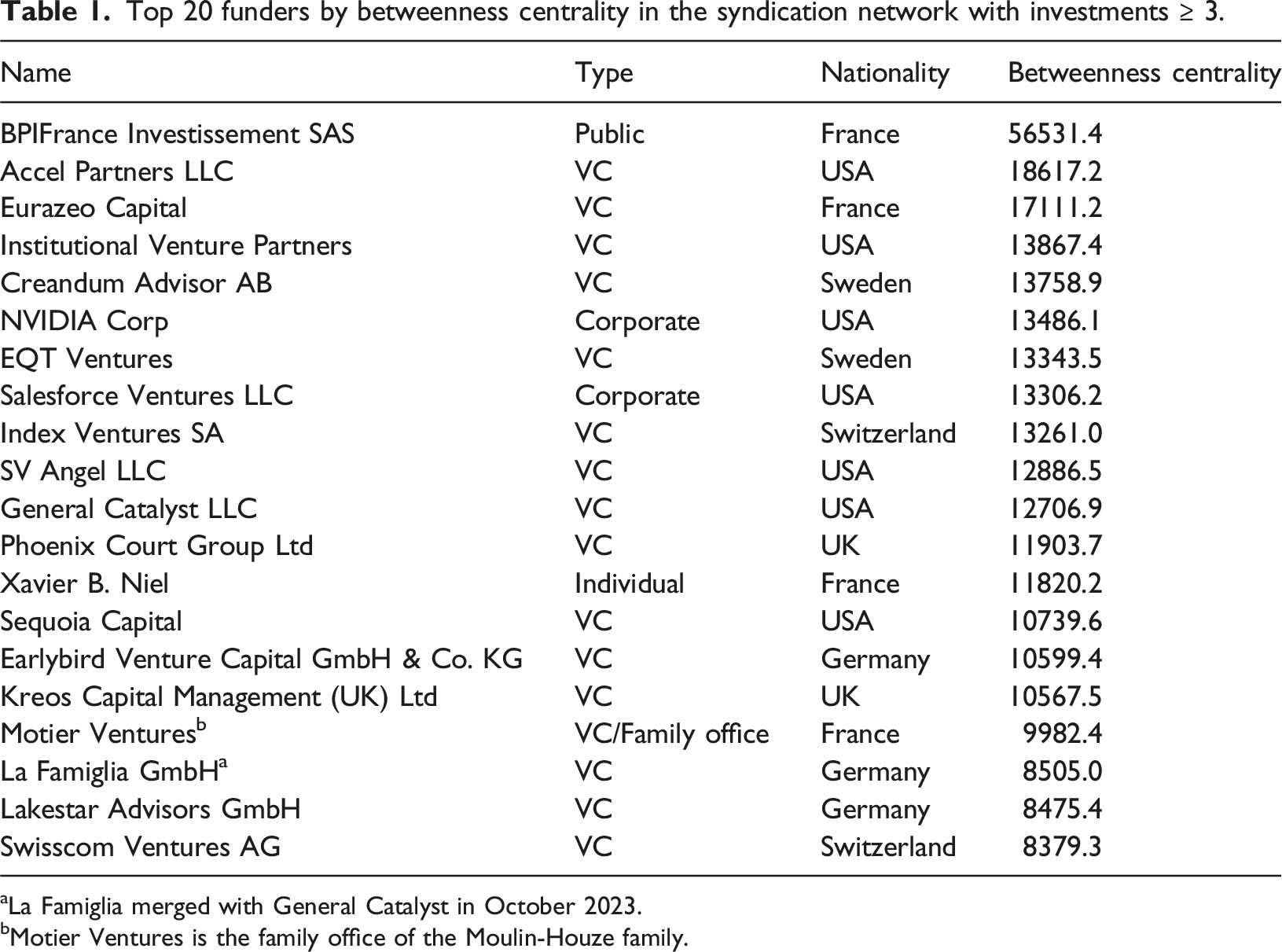

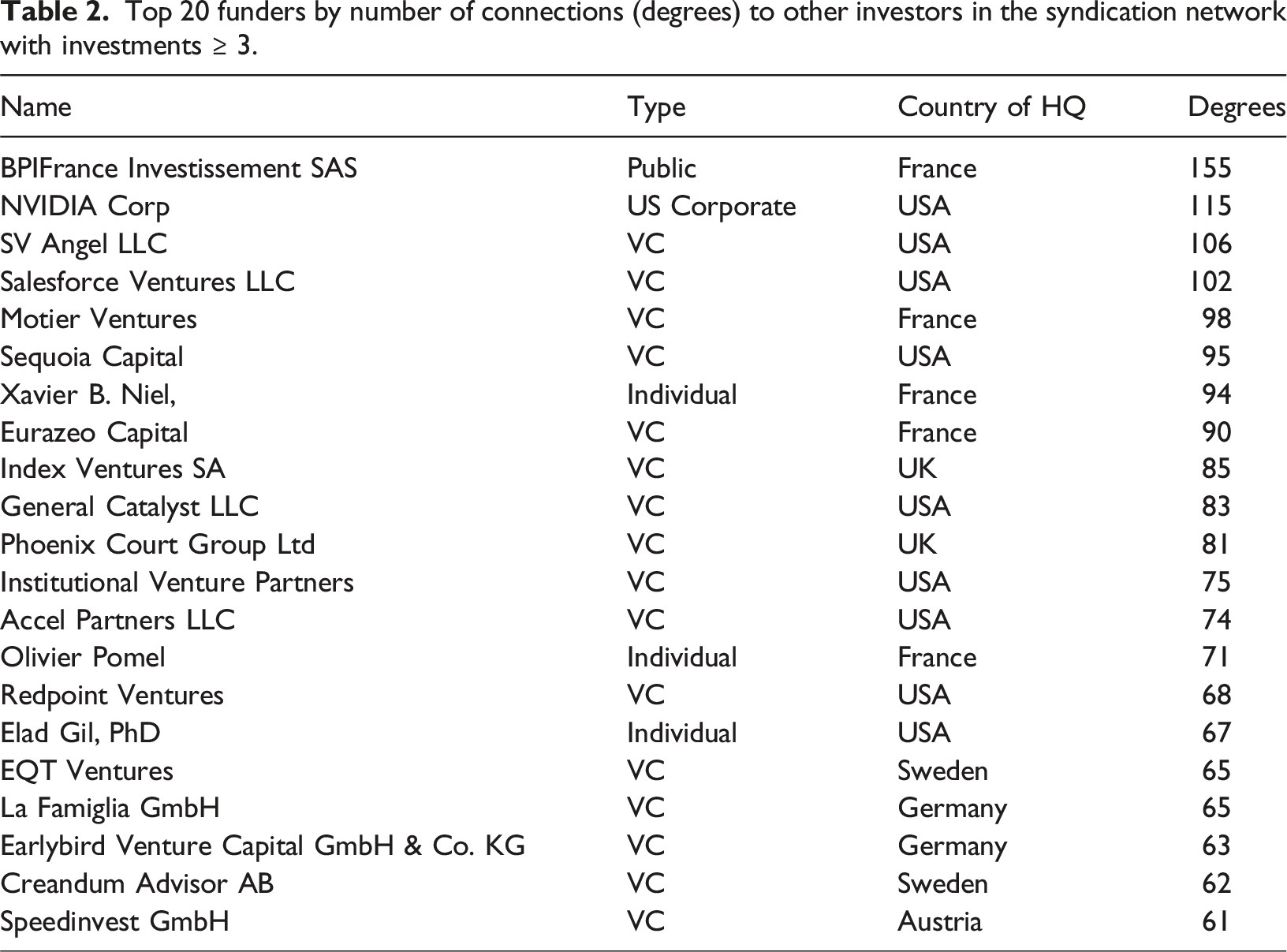

The investor ecosystem presents a more complex picture. The network analysis reveals three key structural features: First, non-EU/EFTA investors account for (52.2 %) of all connections in the network. Third of the connections are from companies headquartered in the United States (33.3%), followed by Germany (15.8%) and France (12.1%), as shown in Figure 2. Second, the network is regionalized rather than pan-European. The network density (the ratio of observed links to all possible links) for the French sub-network (0.083) and the German sub-network (0.049) is significantly higher than for the European network as a whole (0.021). Third, there is a distinct core-periphery dynamic. While 85% of the nodes in the investment network are connected, a core group of 50 out of 826 investors have each funded three or more companies, signifying their central role in the circulation of capital. These investors are selected for further analysis below with two measures: degrees and betweenness centrality. While degree count identifies the most well-connected investors, betweenness centrality helps to uncover “gatekeepers” or “bridges” that connect disparate investment communities. Frequency of investors by country.

Top 20 funders by betweenness centrality in the syndication network with investments ≥ 3.

aLa Famiglia merged with General Catalyst in October 2023.

bMotier Ventures is the family office of the Moulin-Houze family.

Top 20 funders by number of connections (degrees) to other investors in the syndication network with investments ≥ 3.

Comparing French and German ecosystems

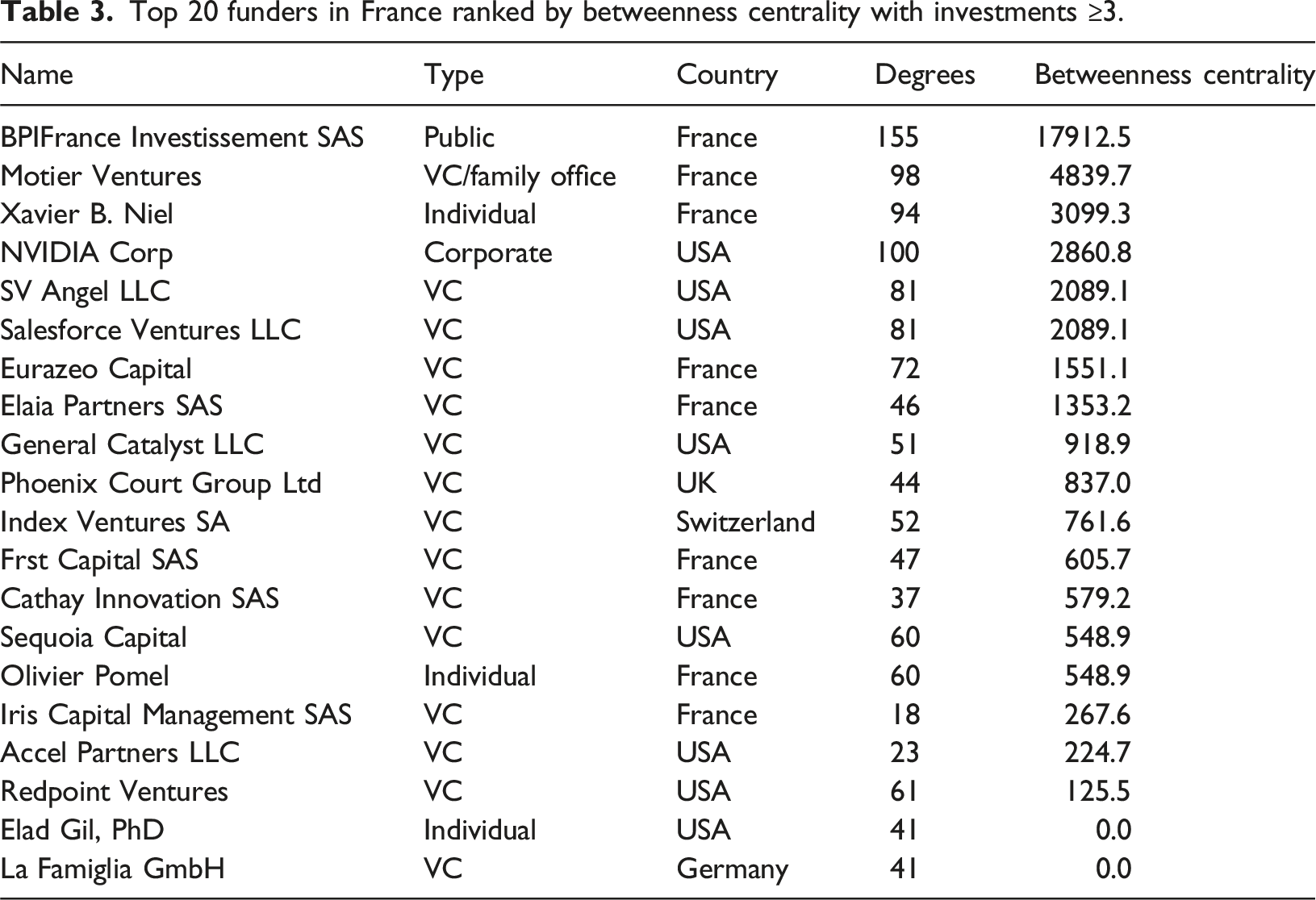

Top 20 funders in France ranked by betweenness centrality with investments ≥3.

. (a) Frequency of investors by country (France). (b) Frequency of investors by country (Germany).

Patriotic billionaires

State actors like Bpifrance are not Caesars in Rome. They operate within a complex and dynamic ecosystem of local VC funds (Eurazeo; Elaia Partners SAS), and high-net-worth individuals who provide patient, strategic capital with allocative agency. In France, a core character with such agency is the tech magnate Xavier Niel. Through investing in prime French AI startups in personal capacity and through affiliated venture funds (Kima; NewWave Ventures), providing computing infrastructure to the AI companies through his cloud company Scaleway, founding a successful start-up incubator Station F, as well as co-investing with other billionaires he has gained a structural position as a key node in the technological life of France (Berthelot, 2023; Laurent, 2025; Meaker, 2024; Prakash, 2024). Publicly, he has downplayed the profit motive, rather focusing on the development of French tech sovereignty, while urging French companies in public statements to stay in Europe instead of positioning for acquisition for the US hyperscalers (Abboud and Klasa, 2024; Olson, 2018). A supporting network of family offices of the French economic elite, such as the Moulin-Houze family (Motier Ventures) of Galeries Lafayétte and the Saadé family in the helm of logistics giant CMA-CGM loom in the background, with some reporting highlighting commitment to “support the ecosystem” to develop European projects instead of “following the English or US companies” (Johnson, 2023).

This emergent phenomenon I call “patriotic billionairism,” a mode of investment by high-net-worth individuals with allocative agency whose capital provision is at least rhetorically guided by extra-economic motivations, such as national technological sovereignty or ecosystem development, can be observed in other European countries as well. Dieter Schwarz, the second-richest individual in Germany and owner of the retail chain Lidl, has been a crucial funder in development of AI in the Baden-Württemberg area, with special focus on his hometown, city of Heilbronn (IPAI, 2025). The key company has been the German AI company Aleph Alpha, once hailed as the European response to OpenAI (Meaker 2023). As noted by one of the early investors, the promise of strategic and patient capital not concerned with immediate profits was crucial for the decision for Aleph Alpha to stay in Germany (Retterath, 2023). As noted by the representative of Schwarz, the investment has been “to certain extent charitable funds” as “there is no expectation of high returns, as is usually the case with venture capitalists (…)” (Bruening, 2024). He also co-funds the largest European AI adoption network with the richest woman in Germany, BMW heiress Susanne Klatten, focused on the adoption of trustworthy AI in German industry (European Commission, 2022). Lastly, Schwarz too, as Niel in France, has also his cloud computing subsidiary STACKIT, aiming to provide cloud computing infrastructure to create “conditions for independence, growth and future viability in Europe.”

In a smaller scale, similar evidence can be gleaned from the Nordics, in the case of the Finnish SiloAI, sold to AMD in July 2024. According to the CEO, due to the support of wealthy Finnish families the company was able to focus on the development of their capital-intensive technology without the involvement of external venture or private equity investors, that enabled the company to focus on “developing sustainable business models, instead of focusing on valuations” (Lappalainen, 2024). After selling the company to the US hardware manufacturer Advanced Micro Devices for $665 million, the CEO of the company returned capital towards the development of European strategic autonomy in tech “aligned with the imperative to improve Europe’s competitiveness and digital sovereignty” (OpenEuroLLM, 2025; Sawers, 2025). In Sweden, local tech billionaires such as the founder of Spotify, Daniel Ek (Bradshaw and Levingston, 2025) and the Wallenberg family are emerging as the key intermediaries of the ecosystem (Billing, 2019).

Whether the “patriotism” of these actors is a genuine expression of conviction or a rhetorical strategy to pursue partial interests in the contemporary juncture is a question that is difficult to ascertain. Individual financiers have likely an idiosyncratic mix of pecuniary and elevated interests. Moreover, it is not obvious whether these patriotic billionaires can be seen as systematic, necessary, and/or sufficient features of strategic industrial efforts, or merely a curious social pattern that has emerged in this juncture. However, for the purposes of this article, it suffices to highlight the politico-economic importance of this nascent pattern of nominal private economic patriotism, departing from the state-centric treatments of the concept (cf. Clift and Woll, 2012). These private actors are embedded public-private exercise of economic statecraft by filling the void of strategic and patient capital (cf. Deeg and Hardie, 2016) in the European Union and deploying it in alignment with the policy objectives of the European Union, with novel implications for business-state relations.

The interlocking class of financiers that operate in the European financing ecosystem is not limited to Europeans. Former Alphabet CEO Eric Schmidt is also prominent in the data, with stakes in the French artificial intelligence companies such as H Company and Mistral. Another prominent foreign individual investing in European companies is Elad Gil, an influential tech thought-leader (Gil, 2018) and serial entrepreneur named the “biggest solo venture capitalist” of Silicon Valley (Jin, 2021), who has made substantial investments to Mistral, Veriff Oü, and Helsing. The international and local billionaire networks also entangle. For instance, on 17th of November 2023 a French open-source initiative Kyutai, led by ex-star AI scientists of Google DeepMind received €300 million from Niel, Saadé, and Schmidt, with public announcements of their friendship and shared philanthropic motivation to “keep European AI talent in Europe” (Scaleway, 2024).

One of the identified policy challenges in the European Union is the lack of European capital specifically in the growth phase. The data qualifies and specifies this thesis. First, there is only a small number of European companies that have reached multihundred-million-euro growth rounds where the influence of United States venture capital presence is more pronounced. The few examples in the data are Mistral’s Series B and C rounds, which included Andreessen Horowitz, General Catalyst and Lightspeed Ventures, Helsing’s Series C funding (Accel, Lightspeed and General Catalyst), and DeepL Series C (Institutional Venture Partners). In concrete terms, then, the effort of the European policymakers to prevent sell-out to abroad seems to be specifically targeted at substituting these American investors for European alternatives, with the hoped warrant that the few sufficiently large European headquartered venture capital would be more inclined to align with the strategic objectives of the EU and hence contribute in the European pursuit of strategic autonomy.

While alluring to simplify the situation as short-term oriented US venture capital companies hijacking the European start-ups to US against patriotic and long-term European capital, the situation is more complicated. First, the commitment of the European VC funds to creating strategic externalities by virtue of geography might be overshadowed by more traditional profitability considerations. As noted explicitly by the Swedish founder of the UK based VC fund Atomico, instead of building own deep technologies, Europe could well settle developing applications that are built on top of AI platforms by US-based companies (Bradshaw, 2025). Second, the VC financing is evolving from the traditional hyperscale model to new forms.

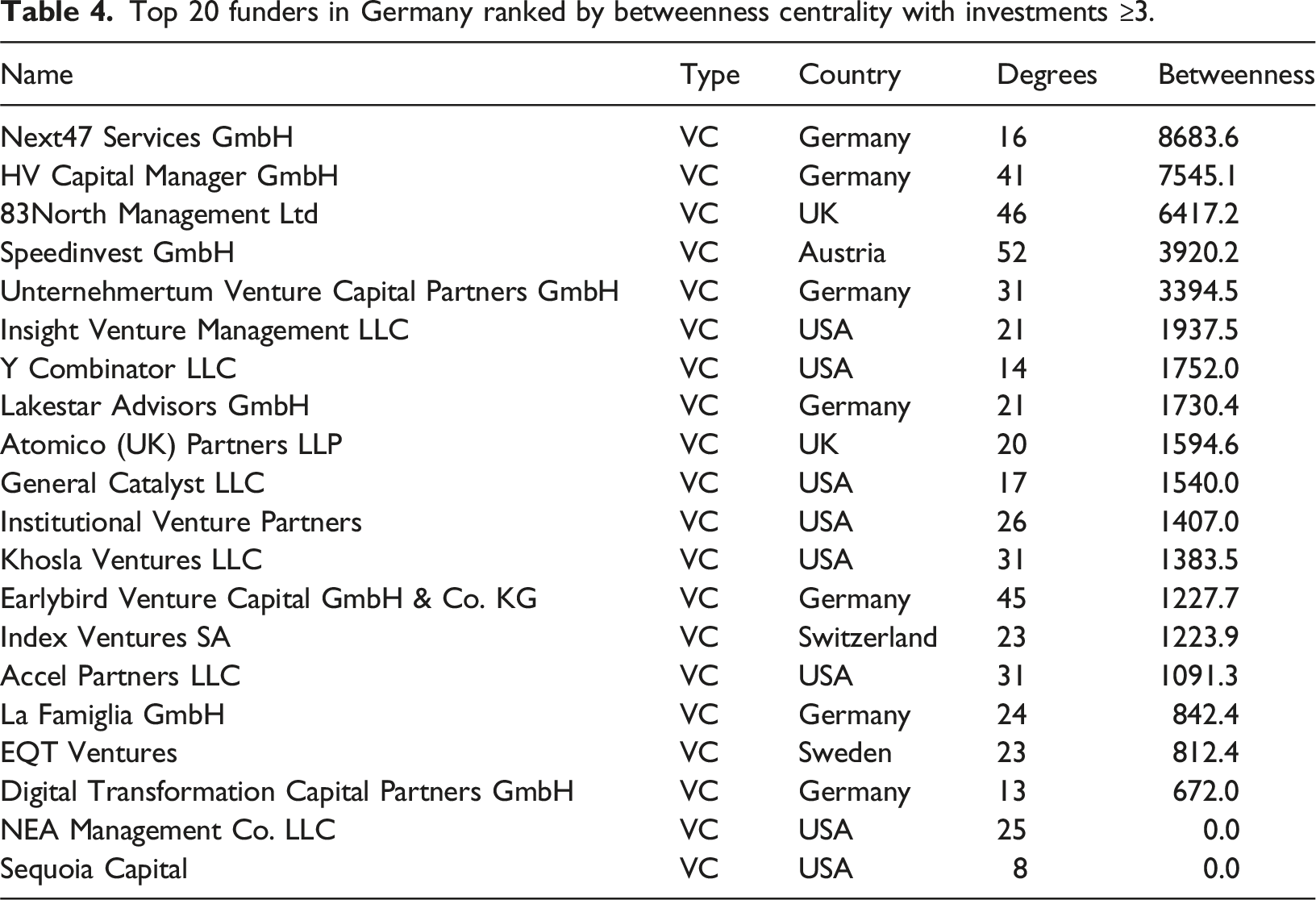

Top 20 funders in Germany ranked by betweenness centrality with investments ≥3.

General Catalyst has explicitly taken a prolific coordinating role in the European tech ecosystem. On 11th of February of 2025, General Catalyst coordinated a strategic “EU AI Champions Initiative” with leading European industrial giants and the leading European AI representing $3 trillion public market cap “committed to establishing Europe as a global leader in AI development and application” (zu Fürstenberg, 2025). The initiative itself reported investment pledges of €150 billion to fund artificial intelligence companies in the European Union. The European Commission added €50 billion to this sum, with the final sum totaling at €200 billion composing the InvestAI initiative, making it at the time the world’s largest private-public initiative in developing artificial intelligence (von Der Leyen, 2025). The initiative includes Dieter Schwarz and Wallenberg family, Saade´s CMA-CGM, L’Oreal, and the established industrial primes of European ecosystem, from ASML to Volkswagen Same day, a new “strategic cooperation” between Mistral and Helsing was announced, facilitated by the co-ownership by General Catalyst (Helsing, 2025).

The findings provide rich insights to the nature of the European AI ecosystems. The European AI activity is geographically clustered in the largest member states, with few prominent companies and variegated use cases. Capital ecosystems show expected entrenchment and polarization, with small group of entrenched and interconnected private and public funders that drive the European AI funding and presence in the best funding opportunities. There is also clear geographic differentiation with especially the French public development bank emerging from the data as the key node in the notionally private venture capital market in France. Social types such as billionaires and strategically oriented venture capital coordinating economic activity emerge as key observations. European aspiration to leverage private capital seems to be like pulling a tangled web, with entrenched and powerful actors occupying key positions in the capital ecosystems.

Discussion: The inversion of conditionality and the new state-finance nexus

These observations suggest diffusion of institutional forms of state intervention in the economy. French example, with a prominent role of BPIFrance in facilitating capital circulation is a salient development. It has become popular amongst European VC community (Invest Europe, 2024), with interest groups urging the European Commission and other member states to adopt the French model of state providing direct and indirect financing for tech investments (e.g. Atomico, 2024). In September 2024, even traditionally fiscally conservative Germany announced a plan to imitate the French example and invest €12 billion through KfW’s Wachstumsfonds Deutschland to German ecosystem intermediated by the leading German VC funds (Martinez, 2024).

This expands our understanding of the rising prominence of the national development banks in the contemporary capitalism. Existing studies tend to focus of NDBs as forms of regional industrial policy or infrastructural buildout for structural transformation in the context of green transition (Griffith-Jones and Ocampo, 2025). In the case at hand, however, the NDBs engage with idiosyncratic features of AI production networks, with implications for “governance domains” of industrial policy (Breznitz and Gingrich, 2025: 332-333). First, instead of mass-employment providing manufacturing companies as part of the Fordist package, the state-business relations in AI are marked with a relationship to an exclusive coalition of elite engineers, founders, and venture capital funds, in hopes to facilitate ecosystem learning and mitigating geopolitical dependencies. These nodal actors are largely clustered in capital areas, which allocates resources to those regions with trade-offs from other regions. Second, the capacity to discipline this private sector coalition is limited by the light local footprint and the embeddedness in international production networks make them highly mobile and prone to exit. National differences in soft and hard policy tools dictate the extent to which these options can be influenced by the state. Third, the promissory nature of the AI technology means that the NDB’s will be exposed to exceptional uncertainty and a risk of failure with potential backlash. In France, some criticism has already been raised against using the public funds to backstop speculative tech investments, with critics pointing to the lack of explicit benefits to the taxpayer (Lestavel, 2023).

Entanglement of public industrial policy with private venture capital suggests shifting structural relations that generate second-order policy demands to European policymakers. Governing through financial markets is not a sporadic choice but a systemic commitment; enlisting private capital to foster European strategic autonomy in AI must be pursued comprehensively or it risks being counterproductive. Without a complete policy package that supports the entire venture capital lifecycle especially in the final exit phase, the EU may find itself merely subsidizing the growth of innovative firms that are ultimately acquired by foreign entities, often at higher valuations. This dynamic, where initial public support spills into external private gain, creates a powerful impetus for further reform in the European polity.

Consequently, the interests of the private market-based financiers are fused to the operation of the European AI strategy. This suggests policy changes that align with the venture capital business model, typically focusing on three areas. First, concerning the supply of capital, industry actors are calling for a deepening of the Capital Markets Union, policies to unlock investment from insurance and pension funds, and lower taxes on cross-border transactions. Second, to ensure returns for their investors, VC funds require viable exit opportunities through acquisitions or IPOs. The difficulty of achieving such exits is cited by nearly half of European VCs as the most critical challenge they face (Invest Europe, 2024), leading to demands for more integrated financial markets and increased M&A activity from large European corporations. Finally, VCs consistently lobby for a more favorable and harmonized regulatory and tax environment, including for employee stock options, and a more “business-friendly” culture to boost European competitiveness. In this way, the initial push for technological sovereignty becomes a potent endogenous engine for broader, market-driven structural reforms of the European Union’s economic governance.

Lastly, the need for volitionally aligned capital sources elevates particular financiers in the European polity to structurally important positions that can be leveraged for policy demands. Currently, the European AI ecosystem is deeply embedded in global networks of finance, with over half of the investors coming from outside the EU. However, this is not a determining structural fact, but a catalyst for adaptation that reformats social relations, elevating particular capital sources to novel positions of political influence. The threat of exit towards more profitable investment opportunities and relaxing on the allocative agency in line with strategic objectives is a nuanced and novel source of structural power that can be used to exercise voice and to put forward policy demands. Some evidence of this is emerging. For example, the release of the European AI Champions Initiative at the Paris AI Summit in 2025 was complemented with a report outlining wide range of policy recommendations to shape the European AI environment by inter alia regulatory simplification, financial market reforms linked to AI investment, using public sector as a strategic customer and developing infrastructure for AI developments (General Catalyst, 2025). After the launch of the initiative, the CEOs participating in the initiative discussed with the president of the European Commission and heads of state of the majority of European member states how to develop “drastically simplified regulatory framework” for AI in Europe. This was followed by open letter from the members calling for postponement and simplification of the EU’s Artificial Intelligence Act (Moens and Bradshaw, 2025). This potential translation of structural potential to instrumental policy influence suggests shifting of the boundaries between the state and the market in the evolving political economy of AI in the European Union.

Conclusion

In this work I have explored the capital ecosystem of artificial intelligence in the European Union. By wedging open the black box of market-based finance, I have argued that the EU’s catch-up push towards strategic autonomy in technology depends on the cooperation of an entrenched capital ecosystem in the European Union. In this process the external structural competitive pressures spill into endogenous adaptations that reformats the state-capital relations. Specifically, the structural importance of strategic, patient and programmatic capital creates differentiated leverage. By having the exit-option, they are well placed to exercise their voice towards policymakers. This changes the relationships of power between state and finance in this historical juncture. Thus, emerging European model, a “patriotic-financial nexus” of national banks, billionaires, and resilience VCs, suggests a distinct variety of techno-capitalism, differing from both the state-dominated model in China and the tech giant-dominated ecosystem in the US. These findings suggest a sovereignty trade-off: in the geopolitical race for technological leadership, the EU’s pursuit of external sovereignty is subsidized by a reduction in autonomy of domestic political sphere, as the state becomes entangled to the logics of the private actors it enlists to secure its geopolitical objectives.

This has been only the start for an empirical exploration of the thick sociality of the European AI ecosystem. Further research is needed to deepen these findings. The concept of patriotic billionairism warrants further exploration, to ascertain whether the deviations from pure profit motivations are linked to legacy building, reputation-washing, long-term viability, or merely more patient investment horizons, as well as investigate the importance of such patriotism across different contexts and conjunctures. More focused analysis on the emergent patterns of investment tribes in the French AI ecosystem centered around BPIFrance would deepen our understanding of the complex sociology of capital around the tech companies and funders scattered around Boulevard Haussman. Further work could also focus on the role of startup incubators such as UnternehmerTUM by Klatten (Partington, 2024) and by Station F by Niel (Ghosh, 2017) and festivals such as the Vivatech and AI-Pulse in structuring and reproducing the networks in the European AI scene provide fruitful sites for empirical research.

Findings of this research have limitations. While best efforts have been made to construct representative sample of the AI investments in the EU, some unavoidable discretionary elements in sample selection remain. Triangulation of these findings in the macro-level financial flows and micro-level studies of companies and investors is necessary to complement and further elaborate on these findings. Additional data sources, such as the network of board memberships, would provide natural linkages to the literature on interlocking directorates and further strengthen the understanding on the networks of influence underpinning the development of contemporary artificial intelligence. Such data is currently unavailable. Moreover, crucially, limiting of the analysis to the unweighted degrees obscures the relative size of the investments by different actors. The analysis has also focused only on capital in the application and model layer of the stack; investments to other layers of the stack such as data layers, chips, and AI computing infrastructure require distinctive kinds of capital, with large PE funds such as Blackstone, EQT, Brookfield, and KKR as well as sovereign wealth funds having a prominent role (Connery, 2024).

Lastly, the investment landscape in AI evolves rapidly which makes particular snapshot analysis outdated. However, the largest investment rounds closed in 2025 show patterns in line with these findings. A new Swedish health AI startup Neko Health raised €260 million by Lightspeed, General Catalyst, Atomico, Lakestar and the co-founder of the company Daniel Ek. At the time of finalizing this article, on 17th of June 2025, Helsing announced a new funding round of €600 million making it the most valuable European AI startup, with post-money valuation of €12 billion (Bradshaw and Levingston, 2025) The financing round was led by Ek’s VC fund Prima Materia, with General Catalyst, Lightspeed Ventures, Accel and Plural, and the Swedish military industry prime SAAB participating in the round. At the time of finalizing this article, Mistral AI finalized €1.7-billion funding round, anchored by €1.3 billion strategic investment from the Dutch chip giant ASML (Mistral AI, 2025).

Whether the new state-financial nexus delivers on the elusive European tech sovereignty in the face of international production and finance networks (Schindler et al., 2024) remains to be seen. The barriers are formidable. Specifically, in the case of artificial intelligence the path to profitability has historically gone through the big tech (Kak et al., 2023; van der Vlist et al., 2024). By controlling access to computational infrastructure, data, and distribution channels, the consumer-facing big tech companies have spawned kill zones around their fiefdoms—areas of economic activity where the competitors cannot compete with the resources of the hyper-scalers. Regardless of whether the effort to develop European AI independent of big tech will succeed, the pursuit of such dream changes the relationships between states and finance in the European Union and points our attention to which actors might “prevail in this society, and in this period” (Wright Mills, 1978, 3).

Supplemental material

Supplemental Material - Capital ecosystem of European AI: Patriotic billionaires, development banks, and the evolution of state-finance nexus

Supplemental Material for Capital ecosystem of European AI: Patriotic billionaires, development banks, and the evolution of state-finance nexus by Leevi Saari in Competition & Change.

Footnotes

Acknowledgments

I am grateful for the comments and encouragements from Daniel Mügge, Milan Babic, Lisa Fenner, Orla Hennessy, Sina Hoch, Frederike Kaltheuner, Nora von-Ingersleben Seip, Jens van’t Klooster, Zuzanna Warso, and the participants of International Studies Association Conference in Chicago in March 2025 and the “AI Value Chains and Infrastructure” workshop at King’s College, London, in May 2025, as well as two anonymous reviewers whose comments improved the paper substantially. All remaining mistakes and errors are mine, despite the tireless efforts of those mentioned above.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: the research was financed through a Vici grant of the Dutch Research Council (NWO; grant VI.C.211.032 “RegulAIte”).

Declaration of conflicting interests

The author is not aware of any affiliations, memberships, funding, or financial holdings that might be perceived as affecting the objectivity of this article. The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Supplemental material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.