Abstract

Numerous regulatory measures aimed at reducing the size and power of European global banks emerged after the Great Financial Crisis (GFC), yet banks remain as large as in 2008. Despite their scale, they repeatedly experience (near) crises and underperform relative to their US competitors. IPE accounts explain the persistence of ‘Too Big To Fail’ (TBTF) banks through their structural power, while CPE approaches emphasise regulatory politics and institutional variation. We argue that both perspectives underestimate the role of geopolitical ambitions and financial hierarchies within global markets in shaping European banking outcomes. Connecting the persistence of TBTF banks to Europe’s geopolitical turn, we analyse European banks’ capacity to deliver on ambitions of strategic autonomy and financial sovereignty. We develop the concept of (S)tra(te)gic banking to capture this trajectory: a state–bank nexus that seeks to project power in global markets while maintaining traditional domestic functions. However, given the structure of global finance, this dual ambition produces contradictory outcomes. European banks are neither globally competitive on par with US banks nor reliably able to support domestic economic functions. We show that their position within dollar-centred financial hierarchies renders Europe’s geo-financial strategy inherently contradictory.

Introduction

Since the Great Financial Crisis (GFC), it has become obvious even to mainstream commentators that there is something deeply wrong in finance. We live in a condition of near-perpetual financial instability, contained by large-scale interventions of the US Federal Reserve, sometimes in tandem with other central banks such as the European Central Bank (ECB). A key problem is the continuous existence of too-big-to-fail (TBTF) banks that many policymakers claimed they would reduce in size after the GFC. Their persistence is often taken as evidence either of regulatory failure or ignorance (Behn et al., 2022; Gabor 2016; Ioannou et al., 2019), or of the enduring structural power of finance that policymakers cannot effectively curb (Culpepper and Reinke, 2014; Massoc, 2020). Both explanations, however, underestimate the geopolitical priorities and financial constraints shaping the relationship between European states, banks, and global financial markets.

In this paper, we argue that the persistence and performance of European TBTF banks cannot be understood without taking seriously both global financial hierarchies and Europe’s geopolitical ambitions. We characterise these ambitions as (S)tra(te)gic banking. The concept has a deliberately double meaning. On the one hand, regulatory and political support for TBTF banks despite their risks, inefficiencies, and dangers reflects a form of strategic banking: European state agents and banks have sought to preserve or enhance the position of large banks in global markets in the name of financial sovereignty, strategic autonomy, and geopolitical power. This dynamic has been present since the 2008 GFC but has intensified with Europe’s more explicit ‘geopolitical turn’ (McNamara 2024). On the other hand, this strategy is also tragic. European banks have not been able to compete on par with US banks within global markets structured by USD hegemony, while their business models have simultaneously moved away from traditional credit provision at home. Europe’s attempt to secure financial autonomy and sovereignty (cf. Lavery 2024) has therefore rested on a contradictory understanding of how US-led financialisation works and of the hierarchies embedded within global finance.

The European case is particularly revealing. European financial and regulatory elites have been among the most vocal critics of US-style finance, European banks were deeply damaged by the crisis, and regulators have repeatedly claimed to be building a more distinct post-crisis banking landscape, partly in an effort to decouple from the US (Beck, 2025; Epstein, 2017; Howarth and James, 2020, 2022; Howarth and Quaglia, 2016; Massoc, 2022). Yet existing explanations still struggle to capture Europe’s specific position within global financial hierarchies. Comparative Political Economy (CPE) scholarship tends to emphasise variation in regulatory politics and outcomes (Bell and Hindmoor 2015; Ganderson 2020; Hardie and Macartney 2019; Howarth and James 2022; Quaglia and Spendzharova 2017; Spendzharova 2016) but often neglects the common entanglement of European banks with USD-centred markets. International Political Economy (IPE) scholarship, by contrast, has done much to show the persistence of US-led financialisation (Crouch 2011; Gabor 2021; Guter-Sandu and Murau 2022; Muegge 2014), but it has paid less attention to the specific dilemmas facing European banks within that order.

Our contribution is threefold. First, we connect the persistence of TBTF banks to Europe’s geopolitical turn and show that banking regulation and market-making have increasingly been shaped by geopolitical ambitions. Second, we show that these ambitions are contradictory: European regulators and policymakers support large banks as instruments of autonomy and sovereignty, yet this support entrenches rather than overcomes dependence on US-centred financial structures. Third, we contribute to efforts to bridge CPE and IPE (Nölke, 2023; Pape and Petry, 2024) by showing how domestic institutional variation and global financial hierarchy interact in shaping the evolution of European banking. In this sense, we also speak to debates on financialisation by showing that even banks occupying near-top positions in global finance remain constrained by the architecture of US-led markets, and that their business models do not deliver the economic functions often invoked to justify political support for them (Dafe et al., 2022; Dafe and Rethel, 2022; Van der Zwan, 2014).

We draw on a mixed set of materials, including public and private documentation, interview material, 1 expert financial journals, and official quantitative data. Our argument proceeds in four steps. First, we show that approaches separating global and domestic dynamics, or state and bank interests, miss the contradictions produced by emulating US finance for both geopolitics and domestic credit creation. Second, we document the persistence of European TBTF banks and show that Europe’s geopolitical turn in banking has largely translated into strategic support for bigger and more consolidated banks. Third, we examine the contradictions of this strategy in a context where European banks remain heavily dependent on dollar funding and unable to compete with US banks on equal terms. We show that size has neither secured global competitiveness nor restored traditional credit provision to domestic firms. The conclusion draws out the dual evolution of European (S)tra(te)gic banking: neither globally competitive nor domestically useful.

Global versus national varieties of TBTF banks

The GFC has spurred a vast literature on the role of global finance and TBTF banks in generating instability and crisis within national economies. Recent contributions have called for bridging Comparative Political Economy (CPE) and International Political Economy (IPE) perspectives in the study of finance (Clift 2021; Nölke 2023; Pape and Petry 2024). While CPE scholarship still struggles to account for how global dynamics shape domestic continuity and change (Germann 2023), IPE approaches have been criticised for insufficient attention to institutional specificities that embed private financial actors (Pape and Petry 2024).

Work focussing on banking institutions has therefore examined the politics of regulatory reform to explain the evolution of financial systems (Howarth and James 2022; Macartney et al., 2020). This literature highlights the interplay of regulatory politics and agency in shaping outcomes, challenging accounts that emphasise the structural dominance of finance (Bell and Hindmoor 2015; Culpepper and Reinke 2014). It shows how domestic political institutions shape government preferences and determine the (in)capacity of reform-oriented coalitions – often located within the state – to resist industry lobbying and impose stricter regulation (Ganderson, 2020; Howarth and James, 2020; Macartney et al., 2020; Massoc, 2020, 2021, 2022).

While this literature provides important insights into variation across national political economies, it tends to overstate domestic differences and underestimate common global constraints. Despite claims that post-crisis reforms have stabilised finance, European banking continues to be characterised by recurring instability, state support, and the expansion of shadow banking (Culpepper and Tesche 2021; James and Quaglia 2024; Thiemann 2018). At the same time, European G-SIBs display similar difficulties in managing global market pressures and in supporting domestic industrial strategies. These common patterns suggest that global financial structures impose constraints that cannot be fully captured through national-level analyses alone.

The growth models (GM) literature offers a promising attempt to bridge domestic and global perspectives (Baccaro et al., 2022; Baccaro and Pontusson 2016). By moving beyond the nation-centred focus of Varieties of Capitalism (Hall and Soskice 2001), GM highlights the role of international interdependencies and positions finance as a key link between domestic institutions and global markets (Baccaro et al., 2022; Bohle and Regan 2021; Helgadóttir and Ban 2021). In particular, it shows how financialisation has reoriented investment towards higher-yielding financial assets, often located in global markets, and how global banks and financial intermediaries facilitate the recycling of surpluses across different growth regimes – for instance, by channelling capital from export-led economies into demand-led, debt-financed ones. Incorporating financialisation has yielded interesting research that focuses on alternative institutions of domestic credit creations (Baccaro and Höpner 2022) or adjustment mechanisms (Spielberger and Voss 2022). As a result, European banks have left their previous role as guardians of firms but, in this view, this does not mean they stop supporting production or being useful for their respective GM. Germany’s export-led model with its twin account and trade surplus relies on demand from abroad and opportunities to invest its surplus money. Hence, German banks do not provide the capital to German industry but instead to US customers to buy German products. 2 The complementarity of these two most prominent ideal types therefore depends on global banks (and other financial institutions) to fulfil their role as international investors. 3 In this sense, finance is conceptualised as a crucial mechanism sustaining the coherence of growth models under conditions of global integration.

However, GM scholarship still tends to assume that financial systems ultimately operate in a functionally complementary manner with national growth models. Even when acknowledging financialisation and global interdependence, finance is often treated as a mechanism that stabilises or reproduces domestic economic configurations. This perspective underestimates the extent to which global financial logics – particularly those associated with US-led financialisation – can undermine domestic objectives and generate tensions within banking systems themselves.

As recent work has shown, financialisation has produced increasingly contradictory outcomes, including rising corporate profits alongside declining productive investment (Helgadóttir and Ban 2021). Building on these insights, we argue that European banks’ dual position – embedded in domestic political economies while operating within global financial markets – generates structural tensions that cannot be reduced to national institutional configurations. Rather than acting in a complementary manner, banks’ global business models may conflict with their domestic roles, particularly in the context of US-led financialisation.

While existing research highlights variation across European banking systems, including important differences in Eastern Central Europe (Bohle, 2018; Ioannou et al., 2019), our analysis points to a shared structural position. European banks occupy a peripheral position within the core of the global financial system. Despite differences in domestic embeddedness, they have converged towards similar patterns of global integration, particularly in their reliance on USD funding. This trajectory reflects a longer process of extroverted financialisation (Beck, 2022), which has tied European banks’ business models to US-centred financial markets.

This structural position is key to understanding the geopolitical turn in European banking. As we show in the next section, geopolitical ambitions have translated into sustained political and regulatory support for large global banks. However, these strategies are based on a misreading of how financial power operates in global markets. The result is a form of (S)tra(te)gic banking: European banks are supported as strategic assets, yet their global business models simultaneously constrain the very objectives they are meant to achieve.

The geopolitical turn and strategic banking: Bigger, faster, larger, stronger!

In the immediate aftermath of the global financial crisis, most politicians and policymakers claimed to be on the same page as then Bundesbank President Axel Weber, who declared in 2009 that ‘in the future banking industry, balance sheets will be smaller’. 4 However, more than 15 years later, the size and business models of Europe’s biggest banks have largely remained unchallenged. In this section, we argue that the persistent outsized volume of balance sheets of European banks is integrally linked to the European geopolitical turn. This has mean that European banks’ purpose has slightly shifted in European elites financial strategies. Since the GFC, we have seen a turn in finance towards ‘strategic banking’ which is concerned – implicitly and explicitly – with European autonomy and financial sovereignty in global markets through balance sheet size, banking consolidation, and, more broadly, increased capacity for the European bloc to entertain large global banks.

Strategic banking is one side of the dual process that has characterised European banking since the GFC. As such, this section documents empirically the extend of TBTF banks and how geopolitics in finance saw a development towards bigger, faster, larger, stronger banks to build European autonomy. This, however, as we will show in the third section, can equally be characterised as tragic banking as it rests on a misconception of how global finance works.

Business models of TBTF

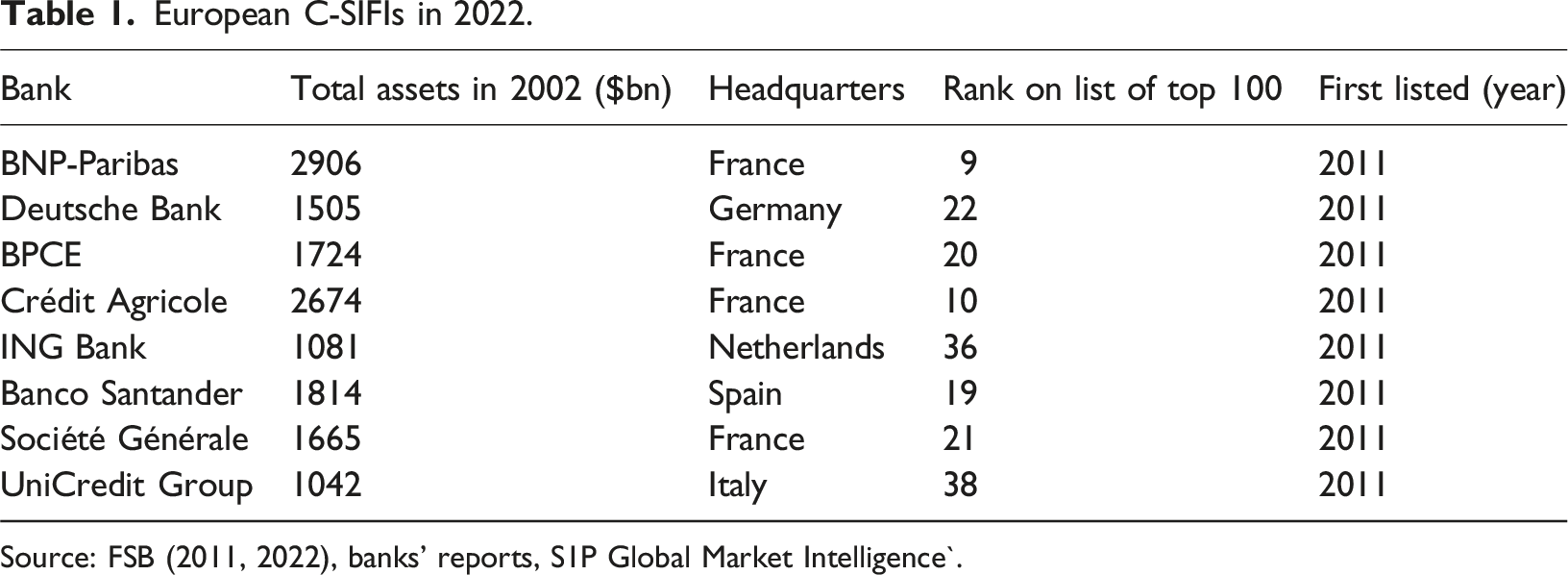

European C-SIFIs in 2022.

The composition of this group has remained remarkably stable over time. Most banks on the 2022 list were already present in earlier iterations, indicating a high degree of continuity in the structure of European global banking. While some institutions dropped out following severe crisis-related losses, this reflects individual failures rather than a broader shift towards more traditional banking models.

More broadly, the size and complexity of European TBTF banks have remained largely intact since the crisis. As Bell and Hindmoor (2018: 16) show, asset sizes of G-SIBs increased substantially in the decade preceding the crisis and did not meaningfully contract thereafter. Similarly, Ioannou et al. (2019: 356) find that changes in the size of the largest global banks since 2008 have been ‘negligible’.

Post-crisis regulatory reforms have focused primarily on increasing capital requirements, strengthening supervision, and developing resolution mechanisms. While these measures have imposed important constraints – requiring banks to raise capital, expand compliance capacities, and adapt internal processes – they have not fundamentally altered core business models (Howarth and James 2022; Ioannou et al., 2019). Resolution frameworks, in particular, remain complex and largely untested in the EU, with limited evidence that they can effectively eliminate reliance on public support (Culpepper and Tesche 2021).

Taken together, these developments point to a persistent pattern: despite extensive regulatory activity and political commitments to reform, European TBTF banks remain large, complex, and deeply embedded in global financial markets. Rather than transforming banking structures, post-crisis reforms have largely stabilised and reproduced them.

From Hausbank to firewall

We suggest that there is an underappreciated imperative underpinning the persistence of TBTF banks, closely linked to Europe’s geopolitical turn. It has been shown that this European ‘geopolitical turn’ (McNamara 2024) has permeated the realm of money creation and financial regulation (Massoc, 2022; Quaglia and Verdun 2023; James and Quaglia 2025). We distinguish three phases in the geopolitical reorientation of European banking, highlighting how geopolitical considerations progressively gained prominence relative to macroprudential concerns.

2008–mid-2010s: Post-crisis sovereignty concerns under macroprudential dominance

In the immediate aftermath of the Global Financial Crisis (GFC), policymakers became acutely aware of the need for European finance to rely on its own globally competitive banks. However, this period was still largely dominated by macroprudential concerns about systemic risk and bank size, particularly within central banking circles (Pierret and Howarth 2023). The idea of financial sovereignty nevertheless emerged at the national level shortly after the crisis. European states sought to ensure that their national banks would remain part of a ‘happy few’ global institutions, seen as necessary to project power and maintain sovereignty (Massoc, 2022).

French banks, in particular, benefited from consistent political support. The French Minister of the Economy and Finance, Pierre Moscovici, made this geopolitical framing explicit, arguing that banking was ‘not only a question of financing the economy, but also of sovereignty’. 5 A vocabulary of economic warfare – especially in relation to US competitors – was developed. As one top banker explained: ‘we’ve been naive in Europe (…). US banks are pushing Europeans out. They fight us and take the leadership. It’s an economic warfare. They (European policymakers) have started to become aware of this’ 6 .

German policymakers expressed similar views. Federal authorities consistently supported favourable regulation for TBTF banks and facilitated their access to deposits by relaxing competition constraints vis-à-vis cooperative and public banks. As one German Treasury official noted, ‘it is normal for a powerful nation like Germany to have a global bank’ (Massoc, 2022: 610). The attempted merger between Deutsche Bank and Commerzbank – strongly promoted by the federal state – reflected this ambition to maintain a strong domestic banking actor in global markets 7 (Beck, 2025), a concern that also shapes current reluctance to allow foreign takeovers.

2015–2020: Institutional consolidation and gradual alignment around size

A more explicit shift began in the mid-2010s with the creation of the Single Supervisory Mechanism (SSM). During this period, national and European policymakers increasingly converged on the view that large banks were necessary not only for financial stability but also for European sovereignty. While macroprudential concerns did not disappear, they were increasingly balanced against competitiveness considerations.

For reasons beyond the scope of this paper, European central bankers progressively aligned with this perspective, combining macroprudential oversight with support for consolidation. This shift is clearly illustrated by statements from Christine Lagarde, who endorsed cross-border mergers: “Cross-border mergers that result in larger institutions […] that can actually compete at a scale, at a depth, and at a range with other institutions around the world—including the American banks and the Chinese banks—are, in my opinion, desirable.”

This marks an important transition: from a defensive posture vis-à-vis US competitors to a more explicit articulation of strategic autonomy, in which bank size becomes a policy objective.

At the same time, state managers used banking structural reform to support balance sheet expansion and financialised business models. French and German authorities rejected ring-fencing proposals that would have separated speculative trading from commercial banking (Ganderson, 2020; Howarth and James, 2020; Massoc, 2020, 2022). This was not intended to revive traditional lending, but rather to enable European banks to compete in global financial markets. As Hardie and Macartney (2019: 517) note, ‘this was a defence of a particularly European universal banking model that was focused not on a “one-stop shop” for NFC clients, but rather on competing with the trading operations of the large US investment banks’.

Similarly, national authorities supported global strategies for ‘their’ banks, even when this came at the expense of domestic credit provision to SMEs. Strikingly, these preferences were relatively homogeneous across different European growth models (Bulfone and Moschella 2025; Massoc, 2022).

2020 onwards: Consolidation and intensification of the geopolitical logic

From 2020 onwards, the geopolitical dimension became more explicit and increasingly dominant. This shift predates – but is significantly amplified by – the Russian invasion of Ukraine, subsequent sanctions regimes, the war in the Middle East, and growing demands for defence financing.

The European Commission’s 2020 Capital Markets Union action plan explicitly linked financial integration to strategic financial and monetary autonomy (Lavery and Schmid 2021). While the rise of industrial policy in the EU has promoted strong financial intermediaries, we observe a broader revival of geopolitical ambitions shaping financial regulation – sometimes even in tension with industrial objectives. 8

European elites increasingly frame large banks as instruments of sovereignty in a context of intensifying geopolitical competition. This evolution reflects a broader reconceptualisation of global finance as a terrain of economic warfare, made particularly visible through the use of financial sanctions.

The role of banks has accordingly shifted from the traditional European Hausbank – supporting domestic industry – towards instruments of geopolitical competition. As James and Quaglia (2025, in this issue) argue, large EU banks are increasingly framed as a ‘firewall’ against US and Chinese actors, particularly in the context of digital sovereignty debates.

This framing is also evident among financial actors themselves. Andrea Orcel, for instance, explicitly linked cross-border consolidation to Europe’s geopolitical ambitions. In a December 2024 op-ed in the Financial Times, he argued: “We may ultimately lose the freedoms and ideals we hold dear. We now have the chance—and I believe, the duty—to scale up Europe’s banking sector and with it our bloc’s ambitions.9”

Geopolitical considerations are likely to become more salient in regulatory thinking, as defence financing and strategic competition gain urgency. 10

As Europe navigates geopolitical pressures in a changing global order (Lavery, 2024; Lavery and Schmid, 2021), European state officials aim to get their global banks in shape to compete against US (and increasingly Asian) banks. Examining the reasons behind the geopolitical turn in Europe is beyond the scope of this paper but this turn has meant a stubborn approach of creating bigger, faster, larger, stronger banks which helps to explain the persistence of TBTF, despite all critique against it and disadvantages involved. Size is strategically promoted by certain regulators to be globally competitive and to finance European’s geopolitical and industrial challenges. While there are nationally specific institutions, this business model is promoted across European states and across political economies.

Tragically, however, while regulators and politicians stressed the need to compete with US banks, the implication that this would play out in a US-dominated financial system was rarely acknowledged, and the dangers of deepening US financial logics go largely unnoticed. This presents us with another puzzle: European state managers were deeply critical of US-style finance when the GFC made it clear that the ‘strategic alignment’ with the US has not translated into improved European financing capacities (Lavery and Schmid 2021). Nonetheless, strategic banking continues to align global banks with US financial models. As we will show in the next section, the translation of the geopolitical and industrial concerns into support for large TBTF banks results from a misconception of how global financial markets work. The question of size has trumped the question of the structural dependence of European banking to US financial logics. This was a fatal error if financial sovereignty and support for GMs were the chief aim. The European version of strategic banking envisioned by state managers does not work within US-led financial markets. The EU geopolitical financial turn has therefore largely been contradictory.

The tragedy of TBTF

Carolyn Sissoko (2025) shows that TBTF emerged in the wake of the collapse of Bretton Woods, when the US ensured that its internationally active banks would not fail. This provided ongoing funding support and contributed to the deepening and liquidity of financial markets. For large European banks, however, balance sheet size does not ensure funding support, global dominance, or financial success. A simple comparison shows that euro area G-SIBs have persistently remained less profitable than their US peers over the past decade, with an average return-on-equity gap of around five percentage points (Di Vito et al., 2023). Since the GFC, opportunities to restore profitability have been limited, while constraints on high-risk activities and securitisation have curtailed alternative revenue sources (Bell and Hindmoor 2018). Attempts to refocus on traditional banking have not generated corresponding income gains. By contrast, US banks have consistently outperformed European banks and dominate not only in US markets but increasingly in Europe.

Why this persistent secondary position? The ECB study (Di Vito et al., 2023) points to differences in business strategies, notably the importance of investment banking income, a stronghold of US banks. More fundamentally, however, this reflects differences in financial environments. Beck (2025) shows how financial globalisation has been characterised by extroverted financialisation (EF), in which European banks’ transformation towards global business models has been shaped by US financial logics and geared towards US money markets. European banks were compelled to compete with US banks on global markets and within the US itself, but lacked comparable access to funding infrastructures. US banks’ ability to mobilise USD funding through domestic money markets gave them a unique advantage (Knafo, 2022). To compete, European banks sought to leverage similar volumes of USD, which required access to US markets and securities – and, in turn, the adoption of US financial logics.

This process has generated global financial markets deeply embedded in US finance, producing the ‘home turf’ advantage identified by the ECB. US banks operate within financial ecosystems that sustain contemporary practices such as securitisation, shadow banking, and CLO markets. European banks, by contrast, face a structural tension within their business models: on the one hand, they adopt US-oriented trading logics tied to dollar funding and global markets; on the other, they remain embedded in domestic systems shaped by long-term relationships and political constraints. As a result, despite attempts to catch up – and periods of profitability – European banks have entrenched a peripheral position and a structural dependency on USD within their own logics of banking (Beck, 2022, 2025).

Even in this position, European banks remain TBTF. At the same time, the hierarchical structure of global finance – centred on the USD – generates broader asymmetries. The US’ ‘exorbitant privilege’ reflects advantages concentrated in the minority world, while the same system imposes constraints on state capacity and development elsewhere (Alami 2018; Gabor 2021; Koddenbrock 2019; Ocampo 2017; Palazzo and Rethel 2008; Pistor 2021; Schwartz 2019). European countries continue to benefit from considerable currency space, and their banks remain among the dominant global players.

Why, then, do we call this ‘tragic’ banking? We do not aim to evoke sympathy for institutions that retain considerable structural power and continue to generate systemic risks, but to capture the contradiction at the heart of their evolution. Larger balance sheets do not necessarily produce dominant banks capable of generating autonomous room for manoeuvre in a hostile financial environment. While it is theoretically possible for European banks to innovate or exploit niches, they have yet to find a sustainable strategy to compete on par with US banks. As a result, geopolitical ambitions overlook the structural dynamics of global finance and ultimately entrench – rather than overcome – US financial dependency. Scholarship focused on domestic variation similarly risks underestimating global financial power relations that generate instability and contradiction across European political economies. The next two subsections show how the post-GFC turn towards ‘misalignment’ with the US has failed to produce financial independence, global competitiveness, or renewed domestic credit provision.

Financial practices and USD funding

USD has been a primary funding currency of global banks’ international activities (Shin 2012), an outcome in part of the process of extroverted financialisation (Beck, 2025) that continues to trouble European banks and policymakers. Offshore dollar banking amounts to around 50% of the US total (McCauley 2020: 423, relying on BIS studies) and European banks continue to be tethered to USD markets (Bassens and Lindo, 2025), a relation and challenge the ECB now also admits (Moschella and Polyak, 2026). If non-US agents can produce so much offshore USD, can we really talk about tragic banking and USD dependency? Yes, we can. The impact of USD hegemony on Europe and its financial autonomy has been a persistent problem, including for the development of its social model (Cafruny and Ryner, 2007; Germain and Schwartz, 2014; Grahl and Lysandrou, 2020). While the precise quantitative volume is difficult to establish, a BIS study finds that USD represents around 50% of international funding, far outpacing any other currency (Davies and Kent 2020). According to the European Banking Authority (EBA, 2025), around 20% of EU bank funding (of that what we know) is denominated in USD. More importantly, nearly a quarter of European banks have insufficient USD funding. Because the EU is exposed to any withdrawal of US dollars, policymakers increasingly recognise that continued access to Federal Reserve swap lines may not be guaranteed.

EF has generated a financial system in which US banks can exploit their USD funding privileges. This helps explain the seemingly puzzling fact that regulation has been more stringent in the market-based USA since the GFC than in continental Europe (Howarth and James 2022), yet this has not undermined the privileged position of US banks. An ECB study shows that US G-SIBs rely more heavily on deposit funding (around 60% on average), a relatively cheap source of funding, compared to 47.6% for euro area banks (Di Vito et al., 2023, p.13). By contrast, European banks rely more on wholesale funding – particularly short-term funding (53% compared to 29% for US banks) – to compensate for limited access to USD deposits (Davies and Kent 2020). For traditional deposit–loan business, European net interest margins are lower, while non-performing loans remain higher, reflecting the legacy of the GFC and sovereign debt crisis (Di Vito et al., 2023).

These differences are consequential. While European banks have deleveraged since the crisis, their reliance on wholesale funding reflects their structural need for USD. Post-crisis lobbying has often framed tighter regulation as a constraint on profitability and lending capacity. Yet US banks are both more tightly regulated and more profitable (cf. Bell and Hindmoor forthcoming). While all banks in global USD markets face liquidity constraints and competitive pressures, US banks operate more successfully within these markets and continue to master what Sgambati (2019) calls ‘the art of leverage’, not least because their home markets provide the financial infrastructures most suited to these practices. US banks have also expanded their presence within Europe and dominate key segments such as investment banking and derivatives markets (Danielsson 2019; Goodhart and Schoenmaker 2016), accounting, for example, for 28% of the derivatives market (EBA, 2025).

The EBA has warned that these dynamics may have adverse implications for the EU’s ‘economic independence and strategic autonomy’ (cited in Arnold 2024). This marks a shift from earlier assumptions of transatlantic alignment. While the Federal Reserve can exercise full control over foreign banks’ US operations (Goodhart and Schoenmaker 2016), European authorities are only gradually recognising their own USD dependency (Paloma and Moschella, forthcoming). As Deutsche Bank chairman Joseph Achleitner noted already in 2018, divergences in transatlantic interests may become increasingly pronounced (Arnold 2024). USD funding is thus not only a challenge for profitability but also a geopolitical constraint.

Understanding how European banks interact with USD markets is therefore crucial. Repo and eurodollar markets have historically provided key channels through which European banks access USD (Beck, 2025). In recent years, European banks – particularly French banks – have become major intermediaries in these markets, reflecting their success in building global business models. Yet this success remains fragile. As one assessment notes, rising funding costs and potential credit rating downgrades could undermine financial intermediation and reduce counterparties’ willingness to engage with European banks, with possible spillovers across the euro area (Man 2024).

This dynamic is also visible in the strategic oscillations of major institutions such as Deutsche Bank, which has repeatedly shifted between attempts to refocus on traditional retail banking and renewed expansion into US-centred investment banking activities (Beck, 2022; Massoc, 2022; Schenk, 2020). Recent moves – including renewed hiring in investment banking and acquisitions such as the UK broker Numis – illustrate continued efforts to compete in US-dominated segments, albeit with more modest ambitions than in earlier phases (Walker and Storbeck 2024). Santander is the latest example (at the time of writing) that has yet another go to integrate more fully into US markets by making a USD 12.2bn bid at Webster Financial.

As TBTF institutions, European banks retain considerable structural power. Yet despite sustained regulatory and political support, they cannot mobilise USD funding to the same extent as US banks. While institutions such as BNP Paribas or Deutsche Bank remain prominent players in global finance, they lag significantly behind US competitors in profitability and market dominance. In practice, European banks often occupy more secondary positions within US-led financial networks, including in financing European firms operating in the United States. Ironically, this reproduces earlier dynamics that European policymakers had sought to overcome.

Firm finance and European financial integration into US finance

Geopolitical concerns have given the Capital Markets Union (CMU) renewed momentum, now reframed as the Savings and Investment Union (SIU). While the CMU has been associated with multiple objectives, its core aim remains the deepening and diversification of European financial markets. Initially, it was discursively framed as a shift towards US-style market-based finance to address an overreliance on bank lending. In practice, however, it was geared towards expanding securities markets that align with the business models of large European banks (Engelen and Glasmacher 2018), particularly as these have adapted their asset structures in the process of extroverted financialisation (Beck, 2025).

More recently, the CMU/SIU has been explicitly linked to the geopolitical turn, with ambitions to create more autonomous and sovereign European financial markets capable of financing industry and SMEs. This ambition reflects the relatively underdeveloped nature of European securitisation markets compared to the US – European issuance, for instance, amounts to only a fraction of US volumes. Yet, as we argue, this project also risks becoming a tragic endeavour. While it may support the trading activities of large European banks, US investment banks continue to act as ‘gatekeepers’ of these markets (Goodhart and Schoenmaker 2016).

Tragic banking here refers to the restructuring of European financial infrastructures in ways intended to strengthen European actors, but which ultimately reproduce US financial logics. It remains unclear why European banks would suddenly succeed in capturing securitisation markets where they have historically struggled to compete with US institutions. Moreover, the expansion of securitisation is likely to reinforce USD dependency, even if this link is difficult to quantify precisely. Such markets rely on complex networks of shadow banking entities – closely connected to, and often backstopped by, banks – that operate predominantly in USD-dominated offshore spaces (Davies and Kent 2020; Sissoko 2025). In this sense, European strategies appear to deepen integration into US-centred financial structures rather than enabling autonomy.

If market-based finance does not provide a clear pathway to financial sovereignty, what about traditional bank lending? European banks remain embedded in domestic political economies (cf. Mertens, 2017), where they are often expected to support industrial policy, including increasingly in the context of defence and strategic sectors (Beck, 2022; Massoc, 2022a, 2022b). Following the GFC, there were strong political commitments to return to more ‘boring’ banking centred on lending to firms (Hardie and Howarth 2013; Howarth and James 2022). Yet, as Bell and Hindmoor (2015) show, regulatory constraints on speculative activities have not resulted in a sustained revival of traditional banking.

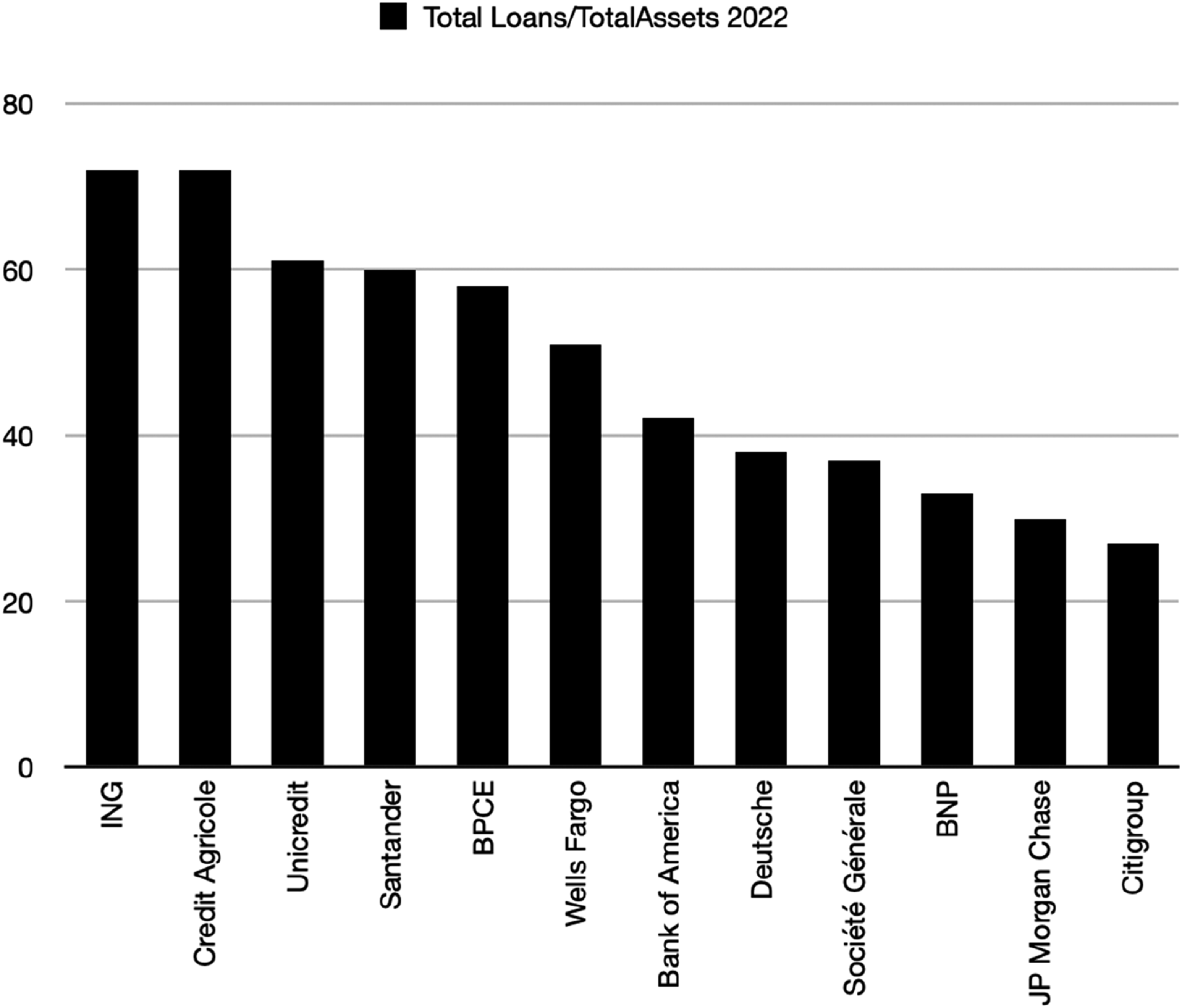

Instead, European banks’ continued orientation towards global financial practices has contributed to a relative decline in corporate lending. As illustrated by Figure 1, loans account for less than 50% of total assets for most large European banks and exceed 70% in only a few cases. This shift is mirrored in national contexts. German banks have increasingly internationalised their portfolios, often through offshore vehicles, at the expense of domestic credit provision (Baccaro and Höpner 2022). At the same time, German firms have diversified their sources of finance, relying more on capital markets, self-financing, and public institutions (Braun and Deeg 2020; Mertens 2021). Total loans/total assets of major banks in 2022.

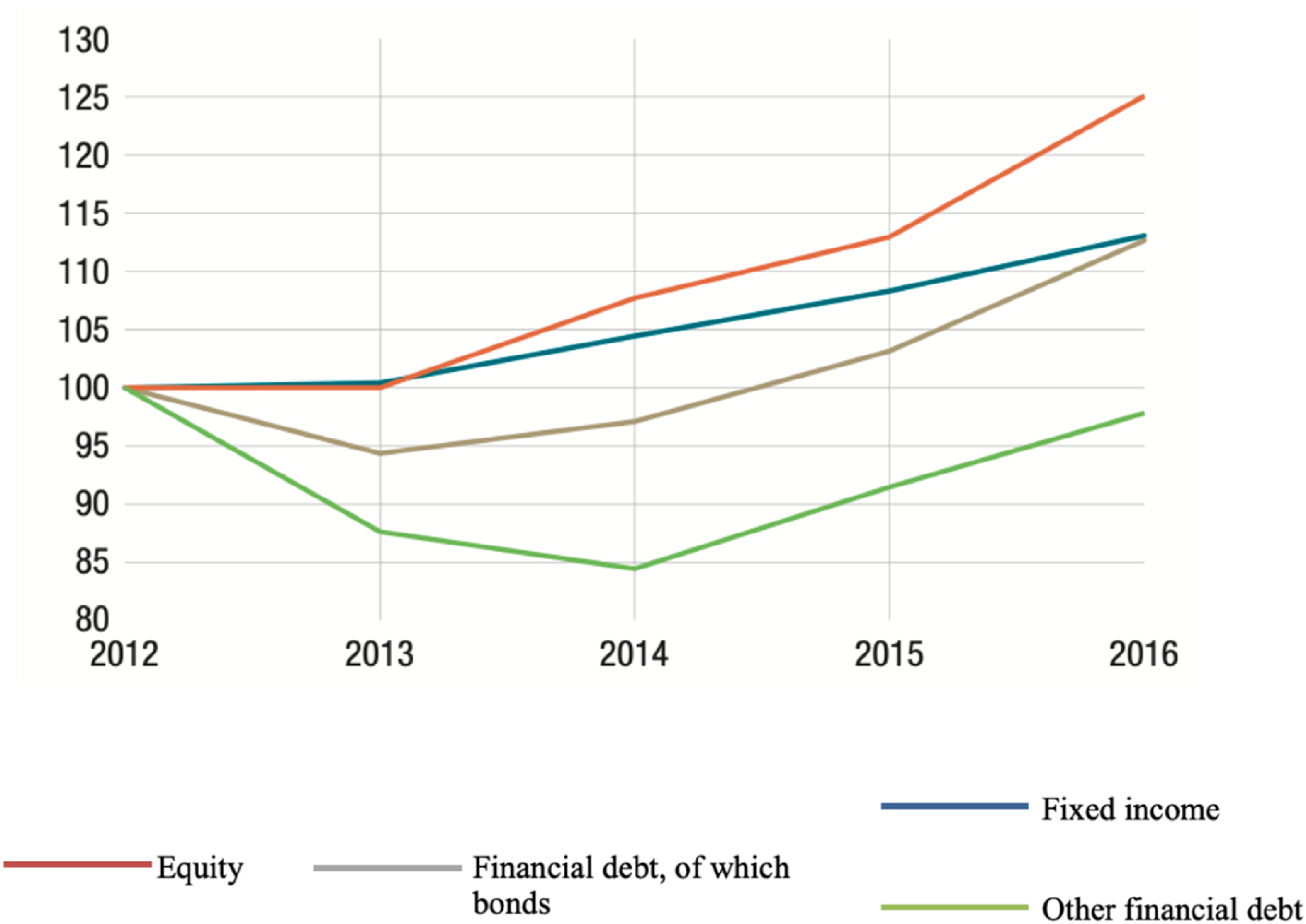

A similar trend can be observed in France. Large firms have increasingly moved away from traditional bank financing towards a mix of market-based instruments and public funding (Keller 2021; Lepont 2024; Villers 2022). As shown in Figure 2, bond debt has become the dominant source of financing for major French companies, rising significantly between 2012 and 2017 (Banque De France 2017). While French banks remain important providers of credit to SMEs – particularly during crises such as COVID-19 – this role is often supported by public guarantees and policy interventions (Beck, Mareike). Progression of the share of financing sources for the French largest 80 companies between 2012 and 2017.

More broadly, SME lending remains structurally unattractive within current banking business models. As one French banker explains, low margins and high risks make such lending difficult to sustain without public support, reinforcing the gap between policy ambitions and financial practices. 11

In sum, the geopolitical ambitions underpinning support for TBTF banks fail to materialise at both the asset and liability sides of banking. The geopolitical support for European global banks has helped them to remain huge, and they are dominant players on global financial markets. However, the banks’ global strategies since the GFC and European financial initiatives have yet to find a way out of two problems commonly raised: USD dependency and generating ‘European’ financial relations that enable both financial sovereignty and SME or corporate finance. As a result, European banking has evolved into a form of (S)tra(te)gic banking: politically supported and globally oriented, yet structurally constrained and domestically limited. European banks not only continue to be non-competitive at the global level, they are also somewhat useless at home – although this reflects structural disadvantage rather than institutional failure.

Conclusion: (S)tra(te)gic banking is neither globally competitive nor domestically useful

A key question of Europe’s geopolitical turn is how to secure ‘a degree of relative autonomy within a rapidly changing global political economy’ (Lavery and Schmid, 2021). Financial markets have been ‘weaponised’ in this regard (Farrell and Newman, 2019). Taking into consideration the local-global links of banking forged during a process of extroverted financialisation, we have argued in this paper that Europe’s geopolitical ambitions vis-à-vis its banks rest on a misconception of how global finance works and are thus doomed to fail. (S)tra(te)gic banking highlights that the ample strategic regulatory and political support that ensures the existence of TBTF banks has turned large European banks into tragic versions of themselves: they are neither globally competitive on par with US banks nor domestically useful in maintaining their traditional functions for European and national industrial development.

For McNamara (2024), the geopolitical turn signifies that current EU state intervention and market-making are qualitatively new, emerging in response to novel geopolitical challenges. We find that, in the case of global banking, it is perhaps not state involvement per se that is new, but rather the explicitly geo-strategic orientation of European financial market-making. Conceptualising banks as geopolitical agents and foregrounding their business models in a USD-centred financial system, we have shown that renewed and evolving geopolitical pressures since the GFC have rendered any potentially well-intentioned goals of reducing balance sheet sizes effectively obsolete.

While we maintain emphasis on the constraints imposed by a US-dominated financial system, we also acknowledge shifts in the broader geopolitical landscape. Tragically for European banks, they do not appear to be at the forefront of shaping these transformations. Emerging research suggests that the centre of financial gravity may be shifting away from Europe and London towards Southeast Asia, at least to some extent. While European banks have scaled back foreign USD-denominated assets, Japanese banks have stepped in to fill the gap (McCauley et al., 2019). Pape and Petry (2024: 233) document a striking shift in global banking: ‘whereas European banks accounted for 62.7% of assets held by the largest 50 banks globally in 2008, their share had decreased to 35.2% by 2020. In contrast, Asian banks increased their share from 17.0% to 43.8% over the same period’. They go as far as to suggest a ‘new normal’ in global finance, in which Europe’s centrality is replaced by East Asian financial flows, at least temporarily. While we remain cautious about this conclusion, it nonetheless points to an important dynamic: European banks struggle to maintain a leading position despite their size and systemic importance. It remains to be seen how their business models can adapt to shifting USD flows.

These findings also highlight the contradictions inherent in attempts to reconfigure Europe’s position within a dollar-centric system structured by US monetary and financial power. While projects such as euro internationalisation, alternative payment infrastructures, and the digital euro are often presented as instruments of strategic autonomy, their development within existing market-based financial architectures raises doubts as to whether they can escape the dynamics of dependency and the reproduction of US-centred financial dominance.

Conceptually, we have shown the significance of global financial power relations in shaping geopolitical capacities and in producing both continuity and change. This perspective helps bridge the gap between IPE and CPE by foregrounding global financial relations as a source of endogenous transformation, and by examining how national institutions adapt to, utilise, and attempt to reshape them. While finance plays a crucial role in CPE, it is often relegated to supporting institutional complementarities. Germany’s growth model, for instance, is not only fragile because it depends on external demand that state managers may struggle to sustain (Baccaro and Höpner 2022: 265); its banking system also underperforms not simply because it is ‘suppressed’, but because global business model aspirations pull banks away from domestic functions. While regional and public institutions continue to support credit relations, global ambitions for national banking champions are failing to deliver. The French model, by contrast, persists through a combination of financial substitutes and the continued political commitment of banks to public missions.

Contradictions and incoherence in European growth models under US-led financialisation are thus more pervasive than commonly assumed. We suggest that the concept of (S)tra(te)gic banking can help future research better capture the interplay between domestic and global political economies by foregrounding the contradictions that emerge when European banks and policymakers attempt to navigate – and master – global financial markets.

Footnotes

Acknowledgement

The authors would like to thank all the participants of the workshop held at the University of Saint Gallen in October 2023 ‘The Transformations of Banking’ for their helpful feedback.

Author contributions

The paper is the result of equal collaboration, and the authors are thus listed in alphabetical order.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.