Abstract

Critical accounting history literature has been scant on the role played by accounting in government coinage policy and its implications for governmental discourse. For this reason, we have examined the implementation of the Spanish Ordinances of the Mints enacted in 1730 and its accounting implications. This analysis allows us to observe the influence of accounting procedures over the government’s monetary policy. We aim to contribute to the literature a new perspective on the role of accounting in governmental and state policies, far beyond the improvement of state income, and concerned more with ensuring the value of the coins and thereby improving commercial activity and the economy in general.

Introduction

Accounting literature has shown broadly how accounting can serve the aims of the state regarding the political economy (Broadbent and Guthrie, 1992, 2008; Goddard, 2010). Part of this research has been devoted to widening the interpretative and critical literature (Goddard, 2010). As a result of this function, accounting has become a pervasive, familiar part of social and economic life (Hopwood et al., 1994; see also Miller, 1994). Archival accounting history can elucidate the relationships of accounting and the state, given its ability to show not only the implementation of the solutions on the population, but also their consequences. Reciprocally, the study of state accounting policies has improved accounting history in general.

To analyse the implementation of state policies, accounting literature has resorted to the governmentality frame developed by Foucault (Carmona et al., 2002; Ezzamel, 2005; Loft, 1986; Miller, 1990; Miller and O’Leary, 1987; Romero, 2005; Sargiacomo, 2008, 2009; Yayla, 2011). Public sector accounting appears a well-established setting to prove the relationships of government discourses and the role of accounting. Thus, according to Foucault (1991: 102), governmentality is the:

ensemble formed by the institutions, procedures, analyses and reflections, the calculations and tactics that allow the exercise of this very specific albeit complex form of power, which has as its target population, as its principal form of knowledge political economy, and as its essential technical means apparatuses of security.

This new way of governing was based on the raison d’etat; that is, “what now appears important is the knowledge and development of a state’s forces” (Foucault, 2007: 365). Interestingly, “[i]n the period of mercantilism and cameralism, the population-wealth couple was the privileged object of the new governmental reason” (Foucault, 2007: 365).

In most of the cases analysed, researchers have focused on the use of accounting to: improve state income (see, for example, Carmona and Gómez, 2002; Carmona et al., 1997, 2002; Sargiacomo, 2008); develop new and more sophisticated paths to control individual behaviour within public institutions (Carmona et al., 1997; Donoso, 2002: Hoskin and Macve, 1988, 2000); fix accurate prices (Carmona and Gutiérrez, 2005); and improve the quality of final products, particularly in public manufactures where high product value increases state incomes (Álvarez et al., 2002; Gutiérrez and Romero, 2007, 2010). The literature has also addressed how accounting practices have been a focus of government attention and/or have spread throughout countries (Gutiérrez et al., 2005; Loft, 1986; Miller, 1994; Miller and O’Leary, 1987).

However, there are few references on the role played by government accounting in the implementation of a coinage policy to improve commerce. Yet, in economic history, the study of coinage policies has been a main branch of research (Gomes et al., 2008; Oldroyd, 1995; Sugden, 1993, for accounting history, and Day, 1999; Grierson, 1967; Mathias, 2009; Nightingale, 1985, for economic history). In the eighteenth century, for example, many of the European countries followed mercantilist policies aimed at wealth accrual by the state, especially through the accumulation of precious metals, and this involved the effective use of coinage policies to stabilize commerce (Gomes et al., 2008; see also Day, 1999).

Such policies went further than merely governing exchanges of commodities within a country. As Ezzamel and Hoskin (2002: 356–357) pointed out, “Coinage represents the writing of a standard value onto metal which is itself deemed to have value”. Such coinage, as they remarked, following Foucault (1974), assumed the standardization of exchange ratios, transforming commerce towards money units instead of physical units (Ezzamel and Hoskin, 2002). Thus, the production of perfect coins, as a representation of their values, should impel those economies implicated to the improvement of their exchanges with other countries. Therefore, governments’ attempts to stabilize their national coins aimed at better conditions to improve their wealth (Day, 1999).

This article aims to analyse the role played by accounting in the process of producing gold and silver coins at the Spanish mints in the first third of the eighteenth century, and the influence that the quality of these coins exercised over Spanish national and international commerce. We do this by studying the implementation of the Spanish Ordinances of the Mints 1 of 1730. We chose this setting because, in spite of the weight of the Spanish economy in Europe in those days, it was declining (Lynch, 1988). A key issue was the bad quality of Spanish coins, which were not welcomed, not only internationally, but also in the Spanish colonial and national markets. Spanish merchants oriented their trades in order to get foreign coins, thus generating a leakage of Spanish gold and silver, and devaluating Spanish money and downgrading Spanish commodities, not only in Spain, but also in its colonies. Also, the centralization imposed by the new Bourbon dynasty mandated the removal of coins that had been used at the Spanish courts of Castile and Aragon in previous centuries (Pulido, 1998). The Ordinances developed a coinage policy based, in general, on controlling the production of gold and silver coins that could not be defaced, so stabilizing the value of the coin versus other European coins and avoiding the cutting, counterfeiting, or eroding practices that had been usual with the previous coins (Day, 1999; Ezzamel and Hoskin, 2002; Lynch, 1988, see also Foucault, 1974).

We aim to add a new perspective to the literature on the role of accounting in governmental and state policies, beyond the mere improvement of state income, and aimed more at improving commercial activity, the economy and, in the final analysis, the general wealth of the population, through a coinage policy that represented governmental knowledge as the main way to develop solutions (Foucault, 2007; Sarrailh, 1992). Interestingly, most of the accounting procedures of these Ordinances were focused on improving the security of the production process and the quality of the coins manufactured, and not simply on getting a higher level of the incomes or reducing state expenses (Carmona et al., 1997; Gutiérrez and Romero, 2007, 2010; Miller, 1994; Sargiacomo, 2008). Governmentality, therefore, proves to be an interesting toolkit for analysing the role of accounting in governmental and state discourses, not being restricted to specific settings and conditions. This conclusion has led us to reconsider Armstrong’s (1994) scepticism on the relationships of discourse and practice in the Foucauldian frame of governmentality, given that the accounting tools used at the mints closely resembled the knowledge, and so the discourse, that engaged them.

We also aim to contribute to the literature by describing the multifarious accounting techniques and controls developed at the Spanish mints after the implementation of the 1730 Ordinances, with 13 books, most of them managed via single entry bookkeeping, as well as books managed via double entry bookkeeping. This mix was the result of the specific activity developed at the coin factories. In strong contrast to other settings of the same period (Carmona and Gómez, 2002; Carmona et al., 1997; Larrinaga and Prieto, 2001), the value of the raw material used in, and the complexity of, the production process required these types of control.

Finally, we also aim to add a new dimension to the relationship of accounting and quality. Studies linking accounting and quality are not new. Álvarez et al. (2002) and Gutiérrez and Romero (2007, 2010) have studied the quality of the tobacco products made in the Royal Tobacco Factory of Seville during the second half of the eighteenth century. However, those studies focused on the quality of final products, tobacco products for direct consumption, whereas we study the quality of the coins that were used throughout Spanish commercial transactions, with interesting implications for balancing trade and the Spanish economy in general terms. Quality, in this case, implies a strategic target for the Spanish coinage policy, given that it was a key element in standardizing the value of the coins (Ezzamel and Hoskin, 2002).

For this article we have drawn on primary sources from the Archivo General de Indias (AGI – General Archive of the Indies) and the Archivo Histórico Nacional (AHN – National Historic Archive), where the accounting statements, the Ordinances, and the correspondence of the mints are kept. We have used secondary sources to complete and verify the information supplied by these primary sources.

The rest of the article proceeds as follows. In the next section we describe the preliminaries of the enactment of the Ordinances of 1730: the arrival in Spain of the Bourbon dynasty and its economic reforms. The third section describes the enactment and implementation of the 1730 Ordinances at the Spanish mints. The fourth section explains the process of producing the coins. The fifth section focuses on accounting control of production and quality. The article ends with analysis and conclusions.

The arrival of a new dynasty and its economic reforms

The end of the War of Succession in 1715 meant the beginning of a process of centralization in Spain 2 by the Bourbon King Philip V (Anes, 1978). However, it also brought permission from the Spanish Crown for England, France, and Holland to conduct transactions with the Spanish colonies in America, with resulting suffering in the Spanish economy. A larger problem to be solved after the war was the restoration of commerce, manufactures, and the Spanish economy in general (Sarrailh, 1992). Spanish commerce was anchored in past practices, not aligned with the most powerful countries, and was locally oriented, and poorly organized. Spain’s production was low and far below that of its main powerful contemporaries (above all, England, France, and Holland), which produced surpluses ready to be exported to any country. As Anes (1978: 235) remarked, “French, English and Dutch agents organised the commerce with America … The luxury products were always imported”.

Commerce with America and other countries after the War of Succession was also greatly influenced by the reliance on Spanish coins. When Philip V acceded to the kingship of Spain, he found a system based on coins produced in gold, silver and copper (Pérez, 2006), with different coins in Cataluña from the rest of Spain, and a desperate drive by Spanish traders to acquire foreign coins, which implied an outflow of Spanish gold and silver coins. 3 Moreover, during the war, Archduke Charles of Austria, Philip V’s opponent, started to produce his own coins in Cataluña. Therefore, the first steps in establishing a definitive system were to prohibit the use of the Archduke’s coins from Cataluña (1709) and the importation of foreign coins (1710). This left three kinds of coins: the escudo de oro (gold escudo); the real nacional (national real) and the real provincial (provincial real), both in silver; and the real de vellón (copper real). But these reforms did not work. Many coins were still sold by their price in silver in international markets.

Thus, in 1726, the government of Philip V decided to improve the value of the silver national and provincial reales in relation to the gold escudo (Pérez, 2006). This proposal, which could be understood as an attempt to stop the outflow of silver coins from Spain, had, however, three negative consequences: first, it implied high inflation, because of the high value of the coins; second, it provoked great confusion about the value of the coins, discrediting the Spanish coins internationally; and third, as a result, the value of the silver coin went down with respect to the gold escudo. The intrinsic values of the coins were not commensurate with their extrinsic values – a key problem to be solved (Pérez, 2006).

Other problems related to the coins were described in 1724 by Gerónimo de Uztáriz, the most important Spanish economist of his time. Uztáriz was a member of the Department of the Royal Treasury and had a huge knowledge of international economics. In Theorica y Practica de Comercio y de Marina (Theory and Practice of Commerce and Navigation), Uztáriz described the best practices developed in the most powerful countries of Europe, 4 comparing them with those in Spain in order to develop means to improve the economy.

Uztáriz (1724) argued that the silver coins should meet a fixed quality specification. Also, the copper real should be abandoned, given the costs of using it for large payments. The introduction of bogus money had to be stopped, and:

all the pieces of gold and silver, old and modern, should be changed to a unique picture, with a circular design … [and] for a greater caution, at the edge, there should be placed an inscription … in the same way as in France, England or other places, in order to prevent clipping, and if it [clipping] is done, it could be found and [the coins] should not be accepted at all. (Uztáriz, 1724: 374)

These dispositions on the form and design of the coin were intended to prevent counterfeiting. Evidently, many of the problems regarding the valuation of the coin were part of the external and presumed value of it that merchants could attribute to its real value. In order to solve these problems, in 1718 the government of Philip V decreed that the mints should be in the hands of the Royal Treasury, thereby avoiding having private businessmen involved. However, the expected benefits were not achieved. The new coins still were of poor quality, with many defects, and were easy to counterfeit (Pérez, 2006).

Other European countries experienced similar problems. England had suffered the same problem some years before. In 1696, R Ford wrote, “I shall not waste any Time in an unprofitable Inquiry into the several Means and Degrees whereby our Coin hath been reduced to its present ill Condition”, and he enumerated the “Evil Consequences that will attend the low valuation of Silver” (Ford, 1696: 4, 5). France, perceiving that its coin system lacked a stable relationship with other coins in the periods 1689–1715 and 1718–1720, established a standard bimetallic relationship in 1726 (Day, 1999). Portugal focused on England as the centre of the destination of their finances and so the Portuguese coin was fixed to the valuation of the English one. Thus, as Day recognized, “[t]he common thread that runs through the tangled history of monetary standards in pre-industrial Europe is the chronic instability of the metallic money supply” (1999: 108).

In 1728, Spain’s Minister of the Royal Treasury, José Patiño, called a meeting of experts on monetary matters in order to solve all these problems. On 9 June, Spain enacted a two-part Ordinance of the Mint. 5 The first part, with 20 articles, described the production process, the metals that should be used and their quality, as well as the tests that should be done to certify the quality of the coins. The second part, with 18 articles, described the staff of the mint and prescribed the tasks, wages, authority, and responsibility of each person (Pérez, 2006). However, this reform did not work. False coins were still in the market, coins were still sold to international markets for their value in gold or silver, and they were also clipped. Only six months later, the minister enacted three decrees to recover false coins, to identify persons who were cutting and splintering coins, and to reject such coins at the customs. Nevertheless, the problems still remained unsolved (Pérez, 2006; Pulido, 1998).

The enactment and implementation of the 1730 Ordinances

In 1730, José Patiño again summoned the experts to meetings in order to set definitive and detailed regulations on the production of coins. These meetings gave rise to the enactment on 16 July of the Ordinances of the Mints of 1730. 6 The Introduction of the Ordinances stated that this was to be a definitive regulation: “this rule will be a permanently binding fulfilment” (Introduction, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375). The main aim of the mints was “to get the best excellence in the production of the new coins” (Introduction, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375).

The main differences between the rules of 1728 and this new set were: (1) The 1730 Ordinances gave exclusive rights to produce coins to the state mints of Seville and Madrid; (2) the 1730 Ordinances increased the number of employees, establishing, for example, two testers for testing the metal instead of one; and (3) the most important difference can be found in the enactment with the Ordinances of the Junta de Moneda y Comercio (Committee on Coins and Commerce), chaired by the Minister of the Royal Treasury.

This committee was chaired in those days by José Patiño (Pérez, 2006), who would also serve as the general superintendent of the mints; all employees were to be subordinate to him (Pulido, 1998), and all top employees were appointed directly by him (Pérez, 2006). Thus, the mints were to be subordinate to the Committee on Coins and Commerce. Most of the members of the committee belonged to the Board of the Royal Treasury or to the Tribunal de la Contaduría Mayor (Tribunal of the Accounting Office), which audited all public institutions (Carmona et al., 1997). Gerónimo de Uztáriz and his son were also members of the committee, because of their knowledge of commerce and coinage (Pérez, 2006).

The Ordinances, as for those of 1728, had two parts: the first, with 16 articles, was devoted to general concerns and technical issues regarding the production process, and the second, with another 16 articles, explained in detail the work, responsibility, authority, and wage of every employee at the mint.

The general issues section of the Ordinances gave the mints exclusive jurisdiction; 7 no entity other than the general superintendent had jurisdiction over any frauds, abuses, or crimes committed at the mints in the course of their activity (Article XVI, Ordinances). In turn, the mints were restricted to state activity: “no coins would be coined for individuals, but for the Royal Treasury” (Article IV, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375). All the gold and silver to be coined was bought or extracted by the Royal Treasury, and the mints were to have a monopoly on making coins.

If an individual wanted to sell his or her gold or silver to the Royal Treasury, two tests were required to verify the purity of the metal. These tests were to be paid for by the seller, who would receive a certificate from the mint. The price of a piece of gold or silver was stipulated, and if the purity of the metal was below standard the price would be proportional.

Article V set the standard of quality of gold and silver for the coins in accordance with practice in other European countries (Pérez, 2006; see also Day, 1999). Article VI prescribed that all the coins should be of a circular form and with an inscription at the edge. Articles VII and VIII set the value proportions between gold and silver coins, and Article VIII also mandated that the measures used to weigh the metal across the production process should be checked every six months in order to keep them exact.

Article IX was devoted to establishing tolerances for the weight of the coins. Thus, for example, the eight-escudo gold coin was to have a tolerance of two grains of gold; the silver eight-real coin, a tolerance of four grains. The Ordinances also mandated “that those officials take care that the coins not exceed the established weight” (Article IX, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375). These tolerances were not always the same, and as the mint employees gained experience, between 1730 and 1756, they were diminished on 10 occasions (Pérez Sindreu, 1992). In order to reduce fraud, only two mints were authorized to produce coins in Spain - one in Madrid and the other in Seville (Article II, Ordinances).

The production process

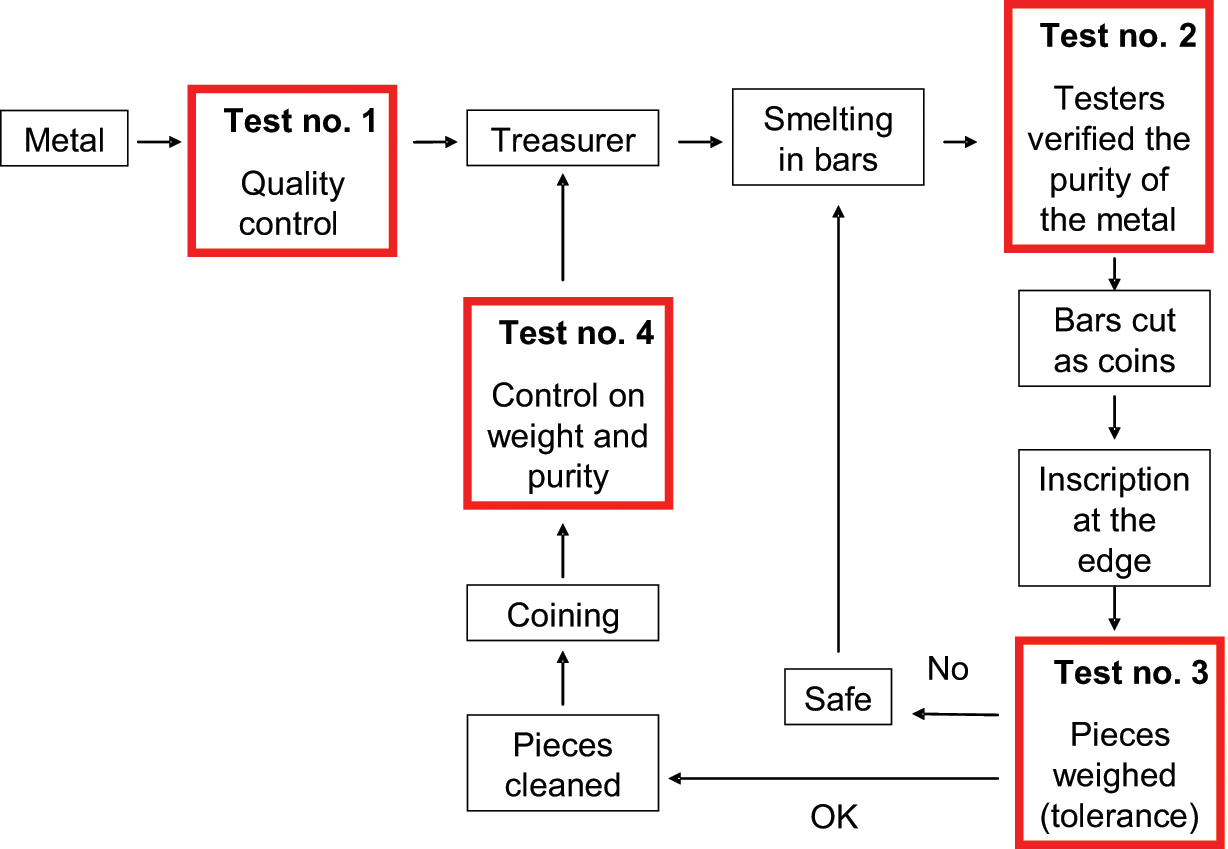

Articles X to XVI defined the production process and the flows of information inside the mints (see Figure 1). The process was as follows: the Royal Treasury bought or extracted the precious metal, usually from Latin America. Once the quality of the metal was classified, the treasurer was made responsible for it (Article X, Ordinances). The metal was then sent for smelting and reduced to regular bars (Article XI, Ordinances). Next, testers verified the purity and quality of the metal before going on with the process (Article XII, Ordinances).

Production process and tests and weights during the process

In the next phase (see Figure 1), the bars were cut into exact discs as coins. Then the edge inscription was added and the coins were cleaned. The remains of the metal after the cutting and stamping went back as raw material “until [such remains] were finished” (Article XVI, Ordinances). After pieces were weighed and found to satisfy the tolerance rates specified in Article IX, they were sent to the next phase, stamping (Article XIII, Ordinances). If they were not within the tolerances, they were to be kept in a safe until they were sent back to the smelter. Finally, the coins were tested again for weight and purity of metal, and then sent to the treasurer (Article XIV, Ordinances).

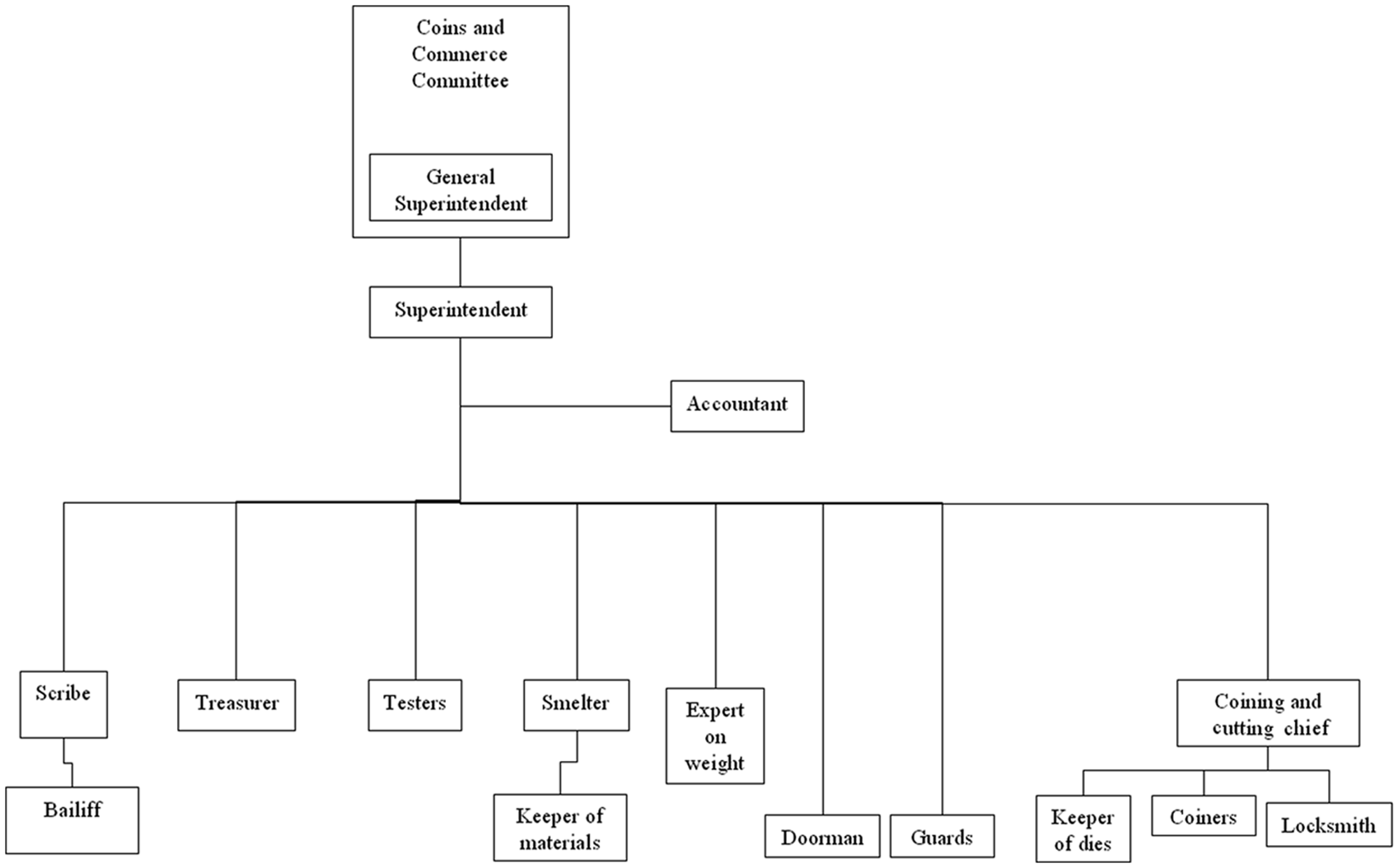

The organizational structure

Articles XVI to XXXII described the posts, tasks, authority, and responsibility of the officials at the mint: superintendent; scribe, bailiff, accountant, treasurer, testers, smelter, keeper of materials, expert on weight, doorman, coining and cutting chief, keeper of dies, coiners, locksmith, guards, clerks and servant. According to the Ordinances, all employees previously working at the mints were to be classified in one of these posts or fired.

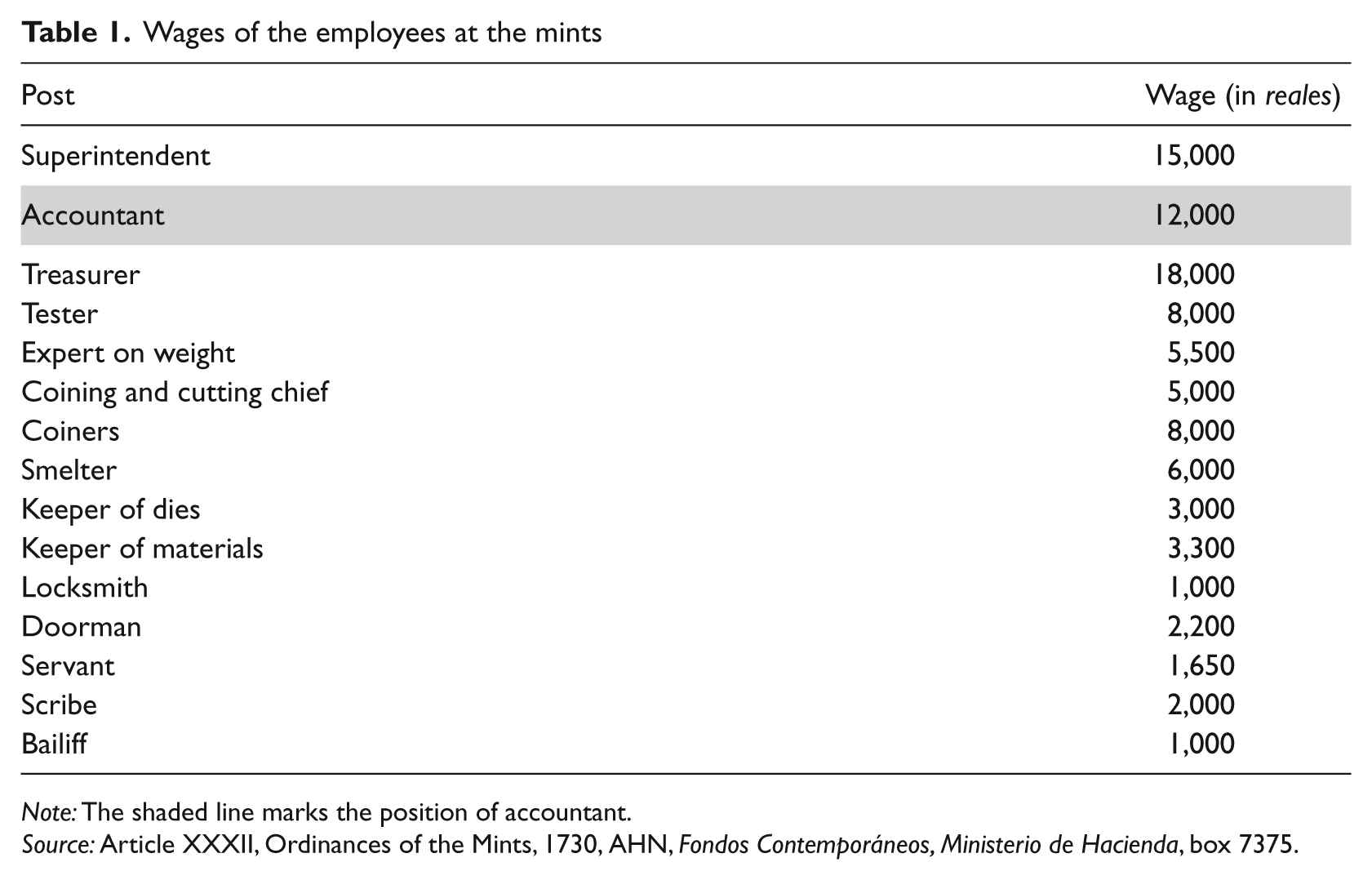

From these articles it is possible to extract an organizational chart for each mint. As Figure 2 shows, the superintendent was the head of the mint, with authority to nominate other officials to the general superintendent in Madrid. The accountant, second in the hierarchy, was responsible for all the official information received at, and sent from, the mint, and for the flow of information inside the mint. The treasurer was responsible for the coins produced and the metal received at the mint. The scribe was a lawyer who certified all facts requiring certification and was responsible for the juridical affairs of the mint. The rest of the posts were related to the technical process of producing the coins. According to their wages, their responsibility and authority can be inferred (see Table 1). The highest wage was that of the superintendent, who received 15,000 reales per year; the lowest was that of the bailiff and locksmith, who received 1,000 reales per year (Article XXXII, Ordinances).

Organizational chart of the mints (according to the Ordinances of the Mint, 1730)

Wages of the employees at the mints

Note: The shaded line marks the position of accountant.

Source: Article XXXII, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375.

One of the posts most relevant to quality was that of the tester. In order to be appointed a tester, the candidate had to pass an exhaustive exam in Madrid with the Great Tester of the Kingdom as examiner (Article XX, Ordinances). Each mint had at least two testers, one of whom had to live in the mint – in a flat inside the factory buildings. They worked in separate offices and made their tests in the presence of a clerk who registered the results. The testers each received 8,000 reales per year (see Table 1).

Another post relevant to quality was that of the expert on weight. Weights were measured several times along the production process: at the intake of the metal, after the smelting, at each phase of the production process and just before the coins were finished. The coin checks were made at random and in the presence of the treasurer, tester, clerk, and a guard. The condition of the weights used by the tester was checked daily. This expert received 5,500 reales per year (see Table 1).

The importance of quality

One of the main issues at the mint was to produce coins with highly accurate proportions, weight, and quality, as the Ordinances recognized: “in the purity of the metal there must not be any tolerance” (Article XII, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375). For this reason, the production process included four tests (see Figure 1).

At the intake of the silver and gold, the testers independently analysed the purity of the metals (Test 1). If the two analyses had different results, the testers were to discuss their results in order to reach consensus. After the smelting of the metals into bars, these bars were kept in a safe, and, again, the testers analysed the purity of the bars (Test 2), once more following a process to achieve consensus.

After the cutting and the inscription on the edge of the coins, they were to be weighed by the expert on weight (Test 3). This weight should be within the tolerance allowed. Coins with a higher weight were to be reduced to the correct value; those with a lower weight were to be recut, with the cost of this process to be paid by the coining and cutting chief.

After the stamping, all coins correctly stamped were retested for purity of metal (Test 4), again by two testers who were to reach a consensus on the quality of the metal. Finally, the coins were weighed again. Underweight coins were to be kept in a safe for future recasting. All these tests were recorded in a book managed by the tester.

Other articles forbade working at night in order to ensure that all operations were performed correctly and to avoid the risk of fire. To ensure the most accurate weight, the Ordinances established that every six months the instruments used to measure the different weights of coins should be verified by comparing those ordinarily used with a set of instruments used only for this verification process (Article VIII, Ordinances).

Another control was established by the Committee on Coin and Commerce. In 1738, an order was issued under which, from every delivery of good coins, the mint should send the committee a sample, to be examined there for quality and purity (Pérez Sindreu, 1992). This practice was maintained for the rest of the century and extended to other mints established in the Western colonies, as Figure 3 shows.

Tests of the purity of the metal of different coins

Accounting books and quality

The accounting books

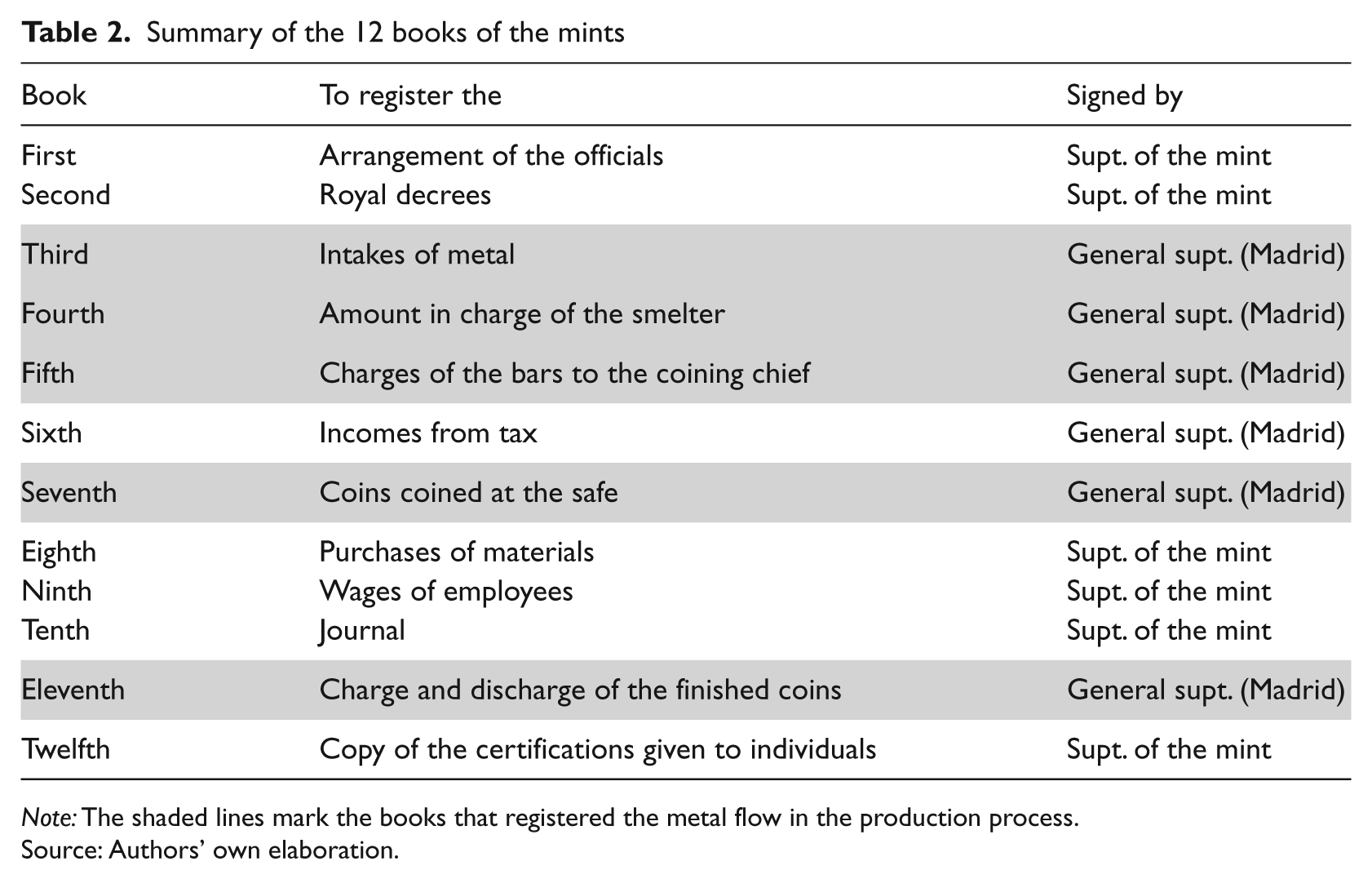

Accounting records were a key issue for the management of the mints. The accountant was to be responsible for twelve books, which covered the main issues under control (Ordinances, Article XVIII). Table 2 lists these books.

Summary of the 12 books of the mints

Note: The shaded lines mark the books that registered the metal flow in the production process.

Source: Authors’ own elaboration.

The first book was to register all the arrangements made at the meetings of the main officials of the mint. 8 The second was to record royal decrees, orders, and the official appointments of the members of the mint. The third was to record all the intakes of metals, giving date, amount and type of metal, and whether it came from an individual or from the Royal Treasury. These intakes were to be registered as a charge against the treasurer. The accountant had to assist at these exchanges on the premises of the mint.

The fourth book was to record the charge for the metal to the smelter, and, concurrently, the discharge to the treasurer. The accountant had to be present at these deliveries. The fifth book was to record the charges to the coining and cutting chief for the bars of metal delivered to his department and the discharges of these bars to the smelter. Again, the accountant had to be present at these deliveries.

The sixth book was to show the income for the Royal Treasury from a tax collected on the production of coins. 9 The seventh was to record, for each delivery, those coins whose weight was under the tolerances once they were stamped. Such coins, together with a copy of this book, were to be kept in a safe. The eighth book was to account for all purchases of materials for mint activities.

The ninth book was to schedule all employee wages, “registering to each one his particular account on credit and debit” (Article XVIII, Ordinances of the Mints, 1730, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375). The tenth was to be a journal, where all the matters considered at the previous book should be written down every day. The eleventh was to register charges and discharges from the safe where the finished coins were kept. Finally, the twelfth book was to register and copy the certifications and reports given to individuals.

Quality and the accounting books

With regard to the quality of the coins, six books were particularly important: the third (concerning the warehouse); the fourth (on the smelting process); the fifth (on the cutting and coining of the bars of metal); the seventh (on deliveries of coins to the safe); the eleventh (on the finished products); and the tenth (which registered the daily control of the coins’ movement inside the mint). Interestingly, the third, fourth, fifth, sixth, seventh, and eleventh were, before their use at the mint, signed by the general superintendent in Madrid. The rest were to be signed by the superintendent of the mint. Evidently, the books signed by the general superintendent in Madrid were considered more relevant for the Committee on Coin and Commerce, and so for the government, than the rest.

All the books were to be closed every three years. At the end of that period, the treasurer was to prepare a statement listing all the intakes of coins and the payments made with those coins. This statement was verified by the Tribunal of the Accounting Office, and, once it was finished, a report was sent to the Committee on Coin and Commerce. In addition, every year, the accountant was to meet with the treasurer to compare their books on the charges and discharges of the safe holding the good coins and the counting of coins in this safe (Article XIX, Ordinances).

For the control of expenses and payments, the Ordinances required that the accountant “must make up the payment letters of all the expenses, wages and purchases, buildings, and the rest needed of my mints” (Article XVIII, Ordinances of the Mints, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375). Further, “the Treasurer [without such payment letters] could or must not make any payment” (Article XVIII, Ordinances of the Mints, AHN, Fondos Contemporáneos, Ministerio de Hacienda, box 7375).

Sometimes the Committee on Coin and Commerce sent an auditor to inspect all activities and books at the mints in a process called a Visita (Visit). This procedure, which was common in public institutions (Álvarez-Dardet et al., 2002; Carmona et al., 1997), was performed without notice to those responsible for the institution (Pérez Sindreu, 1992). In the case of the mints, if any employee at the mint was not working properly, the official or officials responsible were disqualified for some years, and in some cases dismissed (Pérez Sindreu, 1992). For example, the mint of Seville, 500 kilometres distant from Madrid, received only two visits during the eighteenth century, one in 1702 and the other in 1792 (Pérez Sindreu, 1992). Consequently, we consider that activity at the mints can be classified as normal, without any perturbing circumstances.

In spite of the control over money that they assumed, the Ordinances included no directions to save on the expenses of the mints, nor was any mandate postdating the Ordinances directed toward such an idea 10 (Pérez Sindreu, 1992). Curiously, the mint of Seville ceased activity twice due to a lack of money to pay wages, once in 1756 and again in 1765 (Pérez Sindreu, 1992).

Analysis and conclusions

Accounting history has emerged as an interesting way to understand the relationships of accounting and the state. Such relationships have been studied for ancient Egypt (Ezzamel and Hoskin, 2002) as well as more recent contexts that have uncovered how accounting is engaged in the development of various economic policies (Miller, 1994). Foucault’s concept of governmentality has provided an interesting frame for these analyses, as it does for our study of the enactment and implementation of the Ordinances of the Mints of 1730. We have explained why Spain’s new Bourbon dynasty felt a need to reform Spanish coinage, how the state enlisted the aid of economic experts in designing reforms, and how these reforms made use of accounting to control quality at the mints.

The main concept in the governmentality frame is that governments use knowledge to increase state power (Foucault, 2007) through the concept of raison d’état. The government of Philip V resorted to experts to understand Spain’s commercial problems, one of which involved the coin system. Uztáriz’s 1724 report on the coin problem provided a key element of expert knowledge and therefore of policy solutions. Interestingly, the mercantilist ideas that pervaded Europe in those days supported coinage reform (Gomes et al., 2008), not only in Spain but also in other countries such as England, France and Portugal (Day, 1999).

To solve the problem of the Spanish coinage, José Patiño convened a committee of experts (Foucault, 2007) including both Uztáriz and the Great Tester of the Kingdom. While Uztáriz understood the international and national consequences of a bad coin system, the Great Tester understood the technical process of producing coins. Thus, knowledge both uncovered the problem and planned the solution. These experts created a programme for a more accurate coinage system to support trade inside and among countries (Foucault, 2007). From a Foucauldian point of view, this programme solved the problem of the coinage system through raison d’état based on expert knowledge (Miller, 1994). The programme comprised both the Ordinances of the Mints of 1730 and the simultaneous creation of the Committee on Coin and Commerce.

Half of the articles of the Ordinances described the work, authority, responsibility, and wages of mint employees; the other half were focused on the production process, stipulating the quality of the raw materials, the design of the coin, the amount of metal for each coin, and the tolerance rates for the weights of coins, in order to obtain the perfect coins that commerce demanded (Pérez, 2006) and that could be correctly valued and standardized (Ezzamel and Hoskin, 2002; Foucault, 1974). The various controls established by the Ordinances all focused on the excellence of the coins.

Accounting played a key role at the mints. In fact, the accountant was the second-in-command; the Ordinances giving him all the authority of the superintendent in the latter’s absence. The fact that the accountant had to manage 12 books to control the mint offers us an idea of the complexity of the process. The books covered three main issues: production control, the management of expenses, and the registration of official documentation. Books 3, 4, 5, and 7, and in part books 10 and 11, registered all the gold and silver at every stage of the production process. Books 3, 6, 8, and 9, and, in part, books 10 and 11, were devoted to expenses and the collection of taxes. Books 1, 2, and 12 were used to register miscellaneous information.

As we observed above, the Ordinances gave priority to controlling the purity and perfection of the coins, control of expenses being considered a secondary issue. Books 3, 4, 5, and 7 all recorded information on the flow of the production process, but above all on the production of “a correct coin”. In this sense, accounting was helping the government to make visible not only things and people (Carmona et al., 1997, 2002; Miller, 1994), but also the ideal of a coin, an ideal generated by experts to solve a problem. Accounting thus was implicated in the development of an economic policy, broadly understood (Miller, 1994). As Miller pointed out, “policies are articulated and made operable through particular calculative practices” (1994: 13).

As Figure 1 shows, at least two controls were imposed on the quality of the raw material, while two other controls addressed the weight of the coins. Moreover, both the faulty coins and the acceptable ones were registered and controlled in safes. Similarly, the tests made by the tester were registered in a book that he kept. But in contrast to processes studied in the previous literature (Álvarez et al., 2002; Gutiérrez and Romero 2007, 2010), the target of these controls was not a final product, but a medium of exchange in international markets. The new coins, in general, imposed “a standard value onto metal [that was] itself deemed to have value” (Ezzamel and Hoskin, 2002: 357). This concern was not exclusive to Spain, as France, Portugal (Day, 1999), and England (Ford, 1696) also were focused on this idea.

However, the government not only controlled the mint through the Ordinances, it also created the Committee on Coin and Commerce. This Committee, as an agency of the government, was in charge of the development of economic policy, broadly understood, which underlay the coinage programme of the Ordinances (Foucault, 2007). In fact, many of the members of the Committee had also been members of the group that wrote the Ordinances (Pérez Sindreu, 1992), so the knowledge and the discourse that had enabled the construction of the problem and the solution were maintained in the implementation of the programme (Foucault, 1991). The Committee also used accounting to control and manage the mints in various ways, including periodic processes of accountability to the treasurer, control over the quality of the coins attached to the reports on production, and visits to the mints. Thus, accounting was used by an agency of the government to support the development of the economic policy engaged by that agency and directed by that government (Miller, 1994; Miller and Rose, 1990).

Interestingly, incomes and control over state expenses were secondary matters. The expenses of the mint were recorded in books 8 and 9, but neither the 1730 Ordinances of the Mints nor the Committee on Coin and Commerce specified anything regarding this control of expenses (Pérez Sindreu, 1992). We can thus conclude that, in this case, the main target of coinage reform, as an economic policy informed by an accounting system, was to improve commerce instead of state incomes (Miller, 1994).

The programme seems to have worked. The production of silver in Latin America grew after the inception of the Ordinances of the Mints (Vicens Vives, 1965), by nearly 25 per cent for the period 1741–1760, more than 50 per cent for 1761–1780, and more than 100 per cent for 1781–1800. We can assume that this increase in production was driven, at least partly, by the need for more silver at the mints as their activity increased. Similarly, trade with France increased by 27 per cent from 1725 to 1745 (Vicens Vives, 1965). Presumably, there were similar progresses in the exchanges of Spanish traders with other countries.

In the case we have studied, accounting was used and moulded to develop a tight control over the production process of one of the most important features of the government’s monetary policy: the supply of coins. In this case, accounting was adapted to watch over quality control (Hopwood et al., 1994; Miller, 1994). Control over the flow of metals was exercised by the accounting system and by a proper organizational structure. This system helped achieve the objective of getting a high quality product – a key point for Spanish economic policy in the first third of the eighteenth century, just before the appearance of bank notes and bank networks (Annisette and Macías, 2002). Thus, accounting controls at a micro level had great influence on commerce and on society at large (Hopwood, 1987).

An extension of this article could consider the impact of the same problem on the coinage policy in other European countries. As has been explained, England, Portugal and France also had similar problems with the value of their coins, before the Spanish case (Day, 1999). Consequently, a comparison of the French, Spanish, Portuguese, and/or English cases will probably enhance our knowledge of how a similar problem was solved in a different manner, with diverse solutions and implications for accounting (Carnegie and Napier, 2002).

Footnotes

Acknowledgements

The authors are grateful for comments received from the participants at the sixth Accounting History International Conference held in Wellington, the comments and suggestions from the referees and Professor Lee D Parker and Dr Philip Colquhoun, the support of Nancy Mann for the editing, and the financial support of the Spanish Ministry of Education (ECO 2008 - 06052 / ECON) and Regional Government (Junta de Andalucía) (SEJ-4129).