Abstract

This article questions whether the separation of financial and cost accounting in France is an irreversible trend. We begin by showing that the integration of financial and cost accounting was quite “natural” up until the 1940s. We then show that after that date, State-imposed standardization of financial accounting led to separation of the two types of accounting. Last, we study the efforts of one individual, Jean-Pierre Lagrange, to promote a return to an integrated accounting system in the 1980s by means of his method named the système croisé. His efforts were in vain. In our opinion, this failure was not due to technical reasons, but can be attributed to the interaction of the interests of the main actors. Among these actors, the State played a dominant role in France by standardizing financial accounting. In addition, Lagrange was unable to obtain the backing of a network of allies to spread his accounting system.

Introduction

When observing the accounting systems used by most industrial firms before the mid-twentieth century, the integration 1 of cost and financial accounting 2 was common practice. It appeared in the majority of texts on accounting theory and was widely and increasingly taught by the 1870s. Today, the separation of cost and financial accounting is taken for granted. Thus, what in the nineteenth and the first half of the twentieth centuries was possible – even ‘natural’ – apparently ceased to be thinkable in France when financial accounting was standardized in 1947. This standardization became a decisive factor in the separation of cost and financial accounting 3 in the majority of firms. 4

A distinction between cost and financial accounting is now made in most countries. However, to the best of our knowledge, no comparative study on the subject is available. We can only presume that no pure model (complete separation or complete integration) exists, and that the definition of the boundary between the two differs from country to country. The current French system diverges from the Anglo-American accounting tradition. The main difference lies in the fact that, while in the latter, standards are established by bodies that are independent of the State, the French accounting system forms part of a legal framework in which the process of accounting standardization is supervised by the State (Elad, 2000; Hoarau, 1995; Nioche and Pesqueux, 1997; Nobes and Parker, 2004). With the exception of the Fourth European Directive, incorporated in the 1982 Plan Comptable Général (PCG, the French chart of accounts) (Nobes, 1995), the influence of international harmonization in France was, until the 2000s, limited to consolidated financial statements. Since 1947, the PCG has been the central standard-setting tool for individual companies, providing principles, terminology, measurement rules, and a list of accounts and model financial statements for financial accounting. The constraining nature of this tool is further aggravated by the fact that even when alternatives are proposed, these are incompatible with tax and corporate regulations. The traditional French income statement has a macro-economic and external orientation (Elad, 2000). Thus, for macro-economic purposes, the PCG requires that costs be grouped according to their nature (e.g. depreciation, raw materials, wages and salaries, etc.). As a result, cost accounting has, effectively, been separated from financial accounting, which is regulated by the PCG. Individual French company accounts have, since the enactment of the 1947 PCG, followed a dualist approach in which cost accounting is decoupled from financial accounting. Although Anglo-American accounts appear 5 more integrated, some scholars call for greater convergence in this system as well (Hemmer and Labro, 2008; Ikaheimo and Taipaleenmaki, 2009).

Since the nineteenth century, the separation of accounting systems has been the subject of much debate in France and elsewhere. Cost and financial accounting activities, techniques and concepts are continuously evolving, being redefined and becoming increasingly intertwined. In Garner’s work Evolution of Cost Accounting to 1925 (1954), an entire chapter, entitled “Evolution of the integration of the cost and financial records”, is devoted to the situation in Great Britain and the USA. The ensuing debate and subsequent changes have been studied by a number of scholars, including Boyns and Edwards (2007) and, more recently, by Ikaheimo and Taipaleenmaki (2009). In France, the issue has been debated since cost accounting appeared at the beginning of the nineteenth century, even when the integration of the two accounting systems seemed a natural way forward. 6 The debate continued in spite of the separation of the two systems in 1947 7 (Bouquin, 2008). The subject still generates heated debate, although some feel that information technology has rendered it obsolete (Bouquin, 2008: 183). It is therefore essential that both academics and practitioners understand the reasons behind this enduring French particularity of an institutionalized separation of the two accounting systems.

The purpose of this article is not to offer a general or comparative theory on the evolution of the integration or separation of these accounting systems. 8 Such a study, while useful, would require an enormous amount of research which is beyond our scope. Our aim is simply to show how the two types of accounting became separated in France through state intervention, and remain so, as illustrated by failed attempts to return to integrated accounting in the 1990s – notably the persistent efforts of one practitioner (Jean-Pierre Lagrange) and his method, the système croisé. Lastly, we will try to offer some explanations for this failure. Our observations may facilitate the understanding of the separation and integration of cost and financial accounting in France. They will also allow us to offer an opinion on the future situation in France, as well as highlighting the lessons to be learned for the Anglo-American accounting models and international accounting standardization. This article builds upon earlier, although scarce, work on the role of the state in accounting’s past in France (see, for example, Lemarchand, 2002; Nikitin, 2001).

We refer to two types of sources. To consider the evolution of the relationship between cost and financial accounting in France and the underlying reasons, we first looked at the research in accounting history conducted over the past 20 years in France, including our own, mainly drawing on the financial archives of French construction and materials multinational, St Gobain, and the Les Forges d’Oberbrück company in Alsace. 9 We also analysed the writings of the principal nineteenth-century French authors on accounting, such as Reymondin and Degrange. To do so, we used the resources of the Ernest Stevelinck Foundation at Nantes University library, which holds France’s largest collection of works on accounting techniques and history. This research provided insight into accounting practices in France in the period since the Renaissance. For the history of the système croisé, we conducted four long interviews with its principal inventor, Jean-Pierre Lagrange. We also interviewed Michèle Saint Ferdinand, co-author of Lagrange’s thesis on the system, and other academics and consultants either directly or indirectly involved in the système croisé project. We examined the debate between Jean-Pierre Lagrange and Jean-Claude Dormagen, and were given access to Lagrange’s archives and the documents of the Conseil National de la Comptabilité (CNC). 10

The article is organized as follows. In the next section we consider the evolution of the relationship between cost and financial accounting in France against the framework of financial accounting standardization led largely by the French authorities, recognizing accounting as a social rather than purely technical phenomenon (Burchell et al., 1985). An episode in this history is then explored: the story of the système croisé – an attempt to integrate the two systems by Jean-Pierre Lagrange, the chief executive of the L’Oréal group in the mid-1970s. We seek to understand what he set out to achieve in the context of the social and cultural background of the time. In the following section, we investigate the reasons for the failure of this integration system, which, at least on paper, appeared to offer some real advantages in terms of the reliability and relevance of the information it could generate. Finally, we attempt to draw some conclusions concerning the implications for theory and practice, and the lessons that can be learned from the historical perspective.

The separation of cost and financial accounting in France

An examination of the accounts of manufacturing companies for the period prior to the standardization of financial accounting shows a “natural” integration of the two accounting systems. Their separation became noticeable in the 1940s and gradually became the norm from that time. One of the most visible signs of this is the diminishing proportion of cost accounting in successive versions of the PCG. In the most recent version, issued in 1999, all references to cost accounting have completely disappeared.

Integrated accounting systems: a “natural” situation before 1940

Before the Industrial Revolution, double entry bookkeeping was largely practised by merchants and traders whose businesses did not require complex cost calculations; the information provided by the market was sufficient for everyday management decisions. Of the few large manufacturing firms of this era, most did not use double entry bookkeeping, and the very few who did calculate costs, did so by methods that were not associated with their accounts, 11 and were therefore highly approximate. The issue of the integration and/or separation of cost and financial accounting was therefore, with a few exceptions, not generally relevant during this period.

With the Industrial Revolution, manufacturing firms adopted new, double-entry bookkeeping systems which facilitated the calculation of reliable costs (Boyns et al., 1997). Despite appearing quite early, as in the case of Christophe Plantin, such systems had remained rare (Edler, 1937). Although devised independently on the basis of current practice, they should be considered “natural” since they appeared simultaneously with very similar characteristics. Edmond Degrange (1801) was one of the first to design what, for over a century, would be considered the most appropriate accounting system for manufacturing firms. The term “industrial accounting” appeared later, and could be interpreted as either the accounting system used by manufacturing firms, 12 or the part of a firm’s accounts dedicated to establishing cost prices. The term “cost accounting” did not appear in France until after World War II, when production was no longer the only focus of interest in cost calculation, given the rising importance of administrative and sales costs. Regardless of the interpretation of the term, it is certain that all the accounts of a firm were interconnected by means of double-entry bookkeeping, whether accounts payable and receivable, capital accounts, or accounts used for recording internal operations and costing.

When St Gobain published the list of accounts to be opened for each of its 16 factories in 1872, there was no question of distinguishing between two types of accounting. The way these accounts were used is described and presented in alphabetical order of their titles. For every amount debited from an account, the account to be credited is indicated, and vice versa.

An uninformed observer might have had the impression that the organization of the accounting function in some manufacturing firms was divided into two separate parts (financial and industrial accounting) since:

For the sake of convenience, accounts were not always kept in the same place.

They followed the rules for efficient division of duties among accountants with different competencies.

They met different information needs and were not always intended for the same users.

They were, nevertheless, totally integrated in the sense that they were organically connected in a single set of accounts through double entry bookkeeping.

By the end of the period in question (the 1930s), there were signs of a move to separate the two accounting systems at St Gobain. In 1938, the St Gobain group had 56 subsidiaries located in eight countries and had engaged management consultant Charles Héranger to update its information system. The group needed to be able to produce accurate, reliable financial accounts, and have rapid access to costing data, however approximate.

In a document dated 12 September 1941, 13 Héranger recommended that “central” and “manufacturing” accounting should be separated in view of their different purposes: for the latter, intended for decision making, speed was important and approximate figures were acceptable, while the former, intended as proof, had to report exact figures down to the nearest centime, even if this took longer to accomplish.

These proposals were not well received by certain accountants, who saw them as a challenge to their authority. Consequently, the application of the “Héranger method” was short-lived; it was due to come into effect in 1944, but was severely criticized in documents from 1945 onwards – criticisms which appear to have been shared by many of the people working at St Gobain. 14 One anonymous source 15 states that “the costing system thus adopted has become an end in itself and is no longer a simple means of general accounting, from which it is moreover completely separate”. The same document (p.4) lists the drawbacks of the method and reiterates the need to integrate the two accounting systems. To reconcile the desire for rapid production of relevant data with the desire to retain a single accounting system, St Gobain’s management decided to investigate the latest data-processing equipment, the efficiency of which they had observed during a study trip to the USA in July 1946. 16

It is evident that the separation of accounting systems was ultimately seen as a problem at St Gobain, and probably elsewhere. 17 Technical reasons alone do not seem to provide sufficient arguments for separation; but as we shall see, the separation would follow as a result of the on-going standardization efforts at the time.

After 1940, the move towards standardization and the separation of accounting systems

The idea of standardizing accounting systems had begun to spread before World War II (Mattessich, 2008). A series of laws brought in between 1914 and 1917 introduced different forms of income taxes, and gradually developed a set of rules which can be seen as the first steps towards a standardized accounting language (Degos, 2010; Lemarchand, 2010; Touchelay, 2005a). Subsequently, a government decree of 29 July 1939 18 defined and imposed uniform accounting rules on the insurance sector, and, in November 1939, the Finance Minister ordered a commission for economic and fiscal studies 19 to draw up a chart of accounts for use by all firms. It was published in the Ministry’s official gazette Bulletin du syndicat national des contributions directes of February 1940, and was part of the basis for the 1942 PCG (Touchelay, 2005a, 2008a, 2008b).

To introduce a taxation policy that served its purpose, the State favoured a move towards standardized accounting. A parallel movement towards the standardization of costing emerged during the 1930s, as a means of reducing the devastating effects of the depression. Costing had become essential to the “standardization of private business accounting, designed not to calculate exact costs, but to regulate competition within the trade” (Bouquin, 1995: 123). This standardization of costing, driven by business owners both in France (Lemarchand, 1994, 1997; Lemarchand and Leroy, 2000) and abroad (Ahmed and Scapens, 2000; Loft, 1986), did not have the same goals (or instigators) as the standardization of financial accounting undertaken by the French state.

Published in 1943, the 1942 PCG 20 was the product of an inter-ministerial commission set up in 1941. The stated aim of the PCG was to provide companies with an instrument for establishing cost prices, while at the same time standardizing financial statements (the balance sheet and the profit and loss statement). Its real aim was to obtain statistics for the controlled economy at a time when France was occupied by a foreign nation. Preference was given to a chart of accounts in which cost and financial accounting was completely integrated, since the use of a single costing method (full cost) would allow control of margins and thus of prices. One novel feature of the 1942 PCG was the compulsory integration of one costing method: that of the sections homogènes, 21 by which the cost of goods sold was calculated by means of a perpetual inventory. According to Jean Fourastié: 22 “One of the notable innovations offered by modern charts of accounts is that they clearly mark the supremacy of industrial accounting over financial accounting” (Fourastié, 1944: 25). The 1942 PCG, meanwhile, asserted the need to standardize industrial accounting: “to be accurate, the cost of goods sold must include all expenditures that were actually involved in producing the product. In the end, the underlying accounting method must be designed in the same way for everybody” (1942 PCG, 1943: 23). Nevertheless, the 1942 PCG offered two alternatives: integrated accounting for firms that kept accounts based on cost price, and a simplified “separated” version for small and medium-sized businesses. The latter provided the foundation for the 1947 PCG. For several reasons, the 1942 PCG was never officially published or made compulsory, and was never widely adopted. First, there were reservations on the part of employers about “business confidentiality”; second, businesses were reluctant to adopt a PCG that was perceived as the plan of the foreign occupying nation. In addition, there were concerns about the considerable involvement of the tax department (Touchelay, 2005b). Overall, the 1942 PCG was considered too similar to the 1937 German chart of accounts, too closely associated with the Vichy regime, too complex, and much too detailed. It was abandoned in 1946.

This attempt to standardize accounting, and integrate financial accounting and what would become known as cost accounting, thus resulted from the combined efforts of taxation department officials seeking to combat accounting and tax fraud, professional accountants seeking to protect their domain, supporters of accounting standardization, and proponents of costing for improving productivity and a controlled economy, namely Coutrot, Detoeuf and the members of X-crise 23 (Margairaz, 1991; Touchelay 2008a).

After the war, the debate over a new PCG was rekindled. A proposal advocated the separation of accounting systems and culminated in a “rational chart of accounts for the organization of accounting systems” which were separate: “cost-price accounting must remain secondary to commercial accounting without ever interfering with it nor altering it in any way … to avoid extreme complications … and a serious delay in the monthly or annual completion of the accounting work” (Garnier, 1947: 22). This PCG nevertheless allowed the creation of fictitious, temporary accounts for the purpose of providing a link between the two accounting systems.

It was important to abandon the regulatory framework instituted by the Vichy regime, and not to impose cost accounting on all firms: “to ensure the complete standardization in all firms, irrespective of whether they keep management (cost) accounts” (PCG, 1947: 22). Most importantly, the business community was apprehensive of the new government (which included communist party members), taxation, and the on-going price controls. Most business leaders were campaigning to separate cost accounting from financial accounting in order to protect business confidentiality (Richard, 1984). A commission for accounting standardization, set up in 1945, proposed a “dualist” PCG with two autonomous parts. One part concerned financial accounting and had pseudo economic overtones. This part was to become compulsory, while the other part, relating to cost accounting, was to become optional: “an autonomous system of accounting which, based on financial accounting data, serves to calculate cost prices, maintain a perpetual inventory in the accounts, and determine the ‘analytical operating results’”

24

(PCG, 1947: 62). The integration of the two accounting systems featured in the 1942 PCG was replaced by standardization:

It follows that if industrial accounting is fully integrated into financial accounting, the accounts will be presented differently according to whether or not companies keep cost accounts. Faced with the risk of sacrificing part of the accounting standardization it had been instructed to bring about, the commission was unable to opt for such a process. (PCG, 1947: 23)

The successive revisions of the PCG (1957, 1982 and 1999) did not question this separation. On the contrary, the part devoted to the (optional) cost accounting was gradually toned down, and was completely absent from the 1999 PCG.

In conclusion, it should first be noted that although the idea of standardizing cost accounting persisted (perhaps out of habit), it was initially associated with specific circumstances, such as the severe economic recession in the interwar period and the introduction of centralized planning and a national accounting system after World War II. However, it was not popular with firms or the leaders of the accounting profession. The move towards standardization was so strong that the separation of accounting systems became inevitable. Nevertheless, there was a further attempt to unite the two accounting systems in a single système croisé.

The système croisé: The invention of a man swimming against the tide

The système croisé was essentially designed and promoted by Jean-Pierre Lagrange. Before describing his system in detail, a brief outline of his career will be presented.

Jean-Pierre Lagrange’s career

Jean-Pierre Lagrange was born in 1934. While a student at the Ecole Libre des Sciences Politiques 25 in Paris in the mid-1950s, he also studied economics. He was influenced by the economists of the time, several of whom were the founders of the French national accounting system 26 (Alfred Sauvy, Claude Gruson and François Perroux). Their system impressed Lagrange and inspired him to develop his système croisé; it was in fact only through national accounting that he became interested in company accounting. For Lagrange, financial accounting was merely a by-product of national accounting. He graduated from the Ecole Nationale d’Administration 27 in 1963 and started working in the commercial affairs section of the Ministry of Finance. He was appointed rapporteur for the French Plan 28 for the advertising sector, then headed the development of the Rungis Marché d’intérêt National. 29 His career as a senior civil servant in the Ministry of Finance ended in 1965, when he decided to move to the private sector.

Lagrange was headhunted for a position in the La Redoute mail order firm, where he became chief administrative officer. In this position, he found that although it was the financial accounting results which counted at the end of the year, the margins supplied by cost accounting were closely monitored throughout the year. At year-end, these and the results in the financial accounts invariably revealed some major differences that were difficult to explain. He was therefore asked to find the causes of these differences. He quickly discovered that the two systems did not use the same information: it was neither prepared by the same people, nor based on the same methods or time periods. Since comparing these figures a posteriori was a mammoth task, Lagrange came up with the idea of an a priori convergence. He proposed to combine the two systems and make them consistent in order to avoid the inevitable annual divergence.

In 1967 Lagrange went to the USA with the idea that “the Americans have a system for analysing cost accounts”. He visited the ITT Corporation, where the system used recorded accumulated costs with virtually no financial accounting of the type embodied in the PCG. Expenses were recorded according to function and responsibility. Lagrange returned from the USA convinced that this was the answer to La Redoute’s problems: financial accounting must be merged with cost accounting. Lagrange was asked to introduce such a system, assuming the added responsibilities of chief financial officer. Together with the chief accountant, he tried to set up a system of accounts measuring changes in balance sheet amounts, with a first attempt at a “two-way table” in 1969. It was at this point that the idea of the système croisé came about: to combine the Anglo-American system with the French national accounting model. However, before the project was completed, Lagrange left La Redoute early in 1970 to become Chief Finance Officer and Legal Officer at L’Oréal.

At L’Oréal, he encountered problems similar to those encountered at La Redoute: An archaic financial accounting system which provided little useful data. François Dalle, CEO of L’Oréal met regularly with division heads (for each product line), each of whom presented figures produced by their own division. The results were therefore always good, but were regularly contradicted by the financial accounts. Since this constituted a serious management problem, a three-man project team was formed to create L’Oréal’s future accounting system. Several working groups were set up (for turnover, stock, etc.) and, although some members thought computers were the answer to everything, Lagrange was less optimistic and suggested “creating financial accounts whose function would be to monitor internal changes”, with postings made automatically by computer. This resulted in a system that was unified and integrated or “croisé” (literally “crossed”). The système croisé thus came into being, although at the time it was known as Syncofi (SYstème d’iNformation COmptable et FInancier). Cost accounting entries by function came first, followed by financial accounting entries by nature. The person in possession of the information would initiate the entry, requiring a stringent organization.

An initial test was launched in 1973 in the Di Parco subsidiary (manufacturer of Bien être Eau de Cologne). As one of the members of the team was a trained accountant with computing skills, he was sent to the subsidiary to set up the système croisé. Initially, the system was only applied in two subsidiaries, as there was still some reluctance to using it: not only did the implementation require specially trained accountants, but some operational staff was afraid of losing power, since they could not apply “local” rules to the accounts presented to the CEO. There were also reservations on the part of the accountants, who considered that “costing was not accounting”. In response to a demand for a third-party opinion, the Arthur Andersen audit firm was called in at the end of 1973. The auditors concluded that they were not in favour of the système croisé, and presented their report to Dalle, but he did not pass it on to Lagrange. In early 1975, Dalle announced that the implementation of the système croisé was to be suspended. By this time, it had only been tested in seven or eight small subsidiaries. The group’s IT department was against the system, and the plans to install it in Belgium and Italy were never realized.

Lagrange left L’Oréal in 1976 to become CFO at Pricel, a textiles group that was losing money and needed reorganizing. Pricel was later bought out by the Chargeurs group. During his time with the Chargeurs group, Lagrange discussed the système croisé with Jérôme Seydoux, the group’s chief executive, and was asked to introduce the système croisé in La Lainière de Picardie, a group subsidiary that had financial problems and was threatened with closure. The company recovered within three years and Lagrange ascribed part of its recovery to the implementation of the système croisé. When Lagrange left Chargeurs in 1993, the système croisé had not been extended beyond La Lainière de Picardie. According to Lagrange, this was again due to the hostility to the system displayed by two auditors at Coopers & Lybrands; he believed that they had informed Jérôme Seydoux about their misgivings without ever mentioning them to Lagrange himself. Lagrange was convinced that the standardized balance sheet in the French PCG was illusory, since it combined objective items 30 (the by nature costs of financial accounting: purchasing, wages, sales, etc.) with items that follow generally accepted accounting conventions, such as depreciation and provisions. This, in his opinion, made the PCG unsuitable for providing objective financial data.

The système croisé: A micro-economic system integrating both cost and financial accounting systems

How the système croisé works 31

Jean-Pierre Lagrange started by observing the dichotomy between cost accounting and financial accounting in France. Cost accounting followed the successive incorporation of costs and made it possible to know the value of the resulting inventory level at any time. This type of change was not reflected in financial accounting, which did not continuously record changes for internal use and the incorporation of costs, and could only determine the value of goods entering inventory levels from exogenous data. The periodic inventory system in financial accounting has no equivalent in cost accounting, which provides a continually updated record of inventory levels.

The système croisé proposes a reorganization of accounting and financial data in the form of an integrated recording and measuring system. It takes a dual (crossed) approach that is both global, mainly describing the firm’s relations with other players in the economy, and analytical,

32

concerning the internal consequences of these relations and events occurring within the firm:

It is a système croisé because it matches the two accounting approaches by displaying them in a cross-reference table (double-entry) showing:

in the rows, the accounts or items of the analytical approach

in the columns, the accounts or items of the global approach. (Lagrange, 1992a: 34)

The système croisé is based on the philosophy of conventional double entry accounting, but instead of using two accounts, each entry is recorded in four accounts, organized in pairs: An analytical (by-function) account and a global account on the debit side, and an analytical account and a global account on the credit side. Each economic event is recorded in one double entry, simultaneously and in its entirety, in both its “analytical” and its global sense. As a result, these accounts provide the information needed to establish the balance sheet and transactions 33 account directly and simultaneously, including a cash flow statement and an “analytical” profit and loss statement.

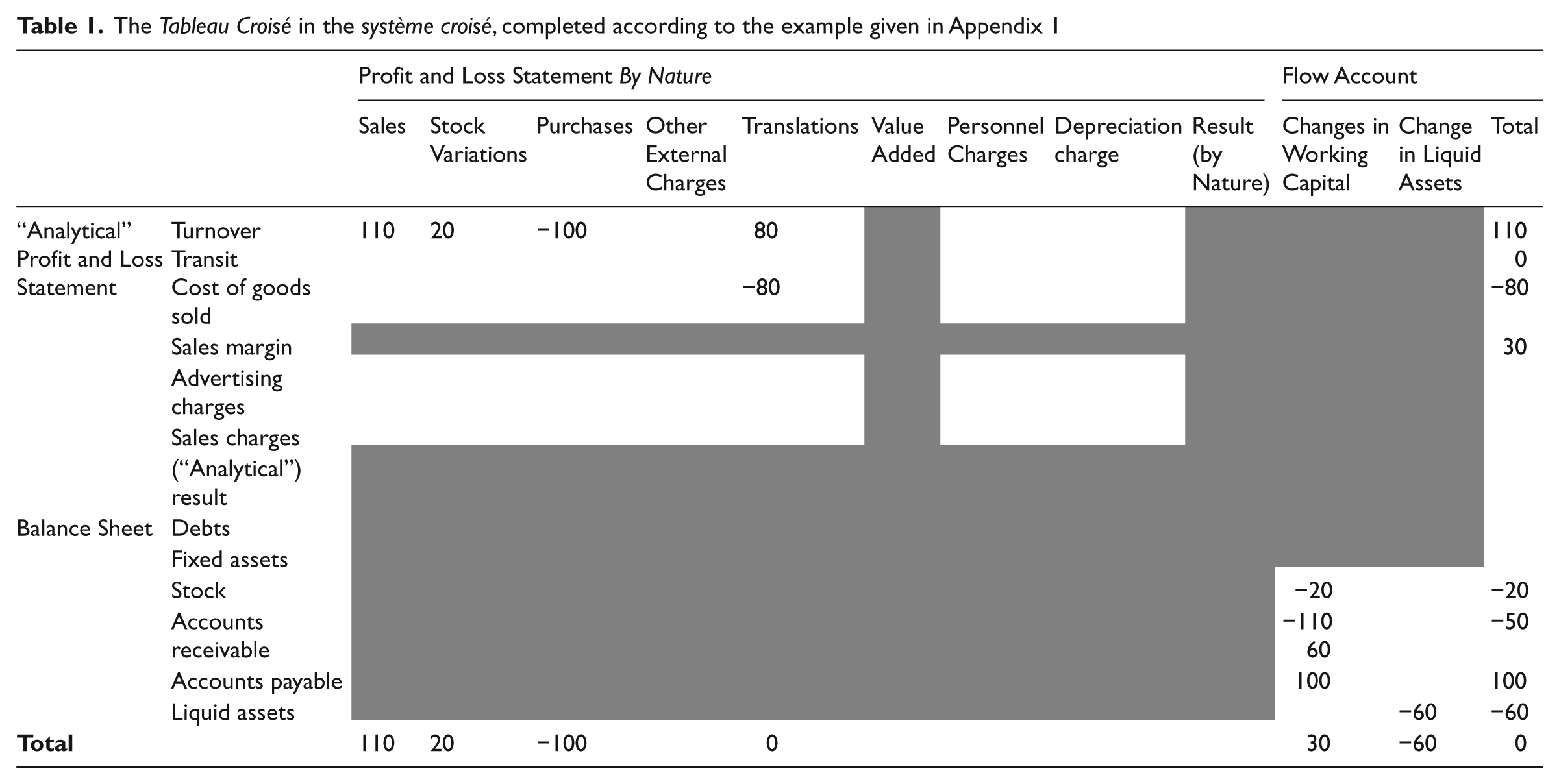

These are two approaches to the same economic reality. The système croisé organizes the simultaneous entry of every economic event in a micro-economic and macro-economic perspective, while providing the means for continuous arithmetical control, the double entrée unique or “two-in-one double entry”. It is presented in a two-way table (Table 1), 34 with the cost accounting (or “analytical”) approach in the rows and the “global” approach in the columns.

The Tableau Croisé in the système croisé, completed according to the example given in Appendix 1

The structure of the tableau croisé (cross-referenced table) is as follows:

two zones at the top and on the left containing the titles of the accounts;

two zones for the entries, one cross-referencing the profit and loss statements, the other cross-referencing the balance sheet and the cash flow account. The entries are recorded in the top left and the bottom right sectors of the table;

two blank sectors where no entries will be recorded. These reflect the logic of the system. For each entry, we activate four accounts paired consistently, that is, a balance sheet account cannot be paired with a cash flow account;

a totalling sector comprising the right-hand column and the bottom line, with balances of the four summary statements: “analytical” profit and loss statement, global result, cash flow statement, and balance sheet;

the last box on the bottom right shows the balance of the accounts, both “analytical” and global, which, by definition, is 0.

The structure of this table can be extended in both directions to add additional accounts when needed.

The système croisé and national accounting

French financial accounting’s concentration on issuing a profit and loss statement and a balance sheet is not consistent with French national accounting or the statistical needs of the INSEE.

35

To restore consistency and produce national accounts, the financial accounts must be restated to extract the production accounts and the necessary financial transactions required for national accounting. The système croisé has the advantage of facilitating the link with national accounting, which was one of Lagrange’s aims (1993b):

36

with the système croisé, it is possible to envisage a system of national accounts that can be established, if not in real time, at least fairly soon after the end of a period, and equipped with sufficient analytical possibilities to become an essential tool in business-cycle policy … Thus, allowing a controlled management of the national economy. (Lagrange, 1991: 101)

Lagrange proposes a more detailed view of the système croisé that provides an economic presentation, with the micro-economic/“analytical” perspective in the rows (“analytical” profit and loss statement and balance sheet) and the macro-economic/“global” perspective in the columns. This presentation offers a complete overview of the activity of each actor, generating four results of which two are based exclusively on that which can be objectively measured. It is possible to not only monitor the composition of value added, but also to describe the resulting cash flows (payment of dividends, investments, changes in working capital), and the way in which value added is allocated to stakeholders. Rather than focusing on results from internal or external conventions, such as the balance sheet and profit and loss statement, the information provided concerns transactions and cash flows.

These advantages were, nevertheless, not enough to win widespread support from accounting practitioners. We will now examine why, despite all its qualities, this system met with such a lukewarm response.

Lack of progress, followed by oblivion: the unsuccessful attempts to expand the use of the système croisé

The système croisé must be considered in the context of the thinking on accounting since the 1950s. The invention of the système croisé was particularly influenced by two phenomena: National accounting from the 1950s onwards, and research in the 1970s and 1980s into the impact of technology on accounting techniques.

After World War II, the progress made in statistical analysis and the increasingly interventionist approach of governments to medium-term control or orientation in a centrally planned economy, created favourable grounds for the development of national accounting and the exploration of its links with financial accounting (De Beelde 2009; Vanoli, 2005). One of the goals of the designers of the 1947 and 1957 PCGs was to integrate financial accounting into the country’s economic information system. These goals were, however, only partly attained as national accounting and financial accounting did not develop at the same rate. Development began in the 1940s for the PCG, but only in the 1950s for France’s national accounting (Fortin, 1986: 349). The authors of the successive PCGs were therefore unable to incorporate the needs of national accounting (Benedetti and Malinvaud, 1977). Moreover, financial accounts were for a long time based solely on the very general figures derived from company tax returns in the possession of the French tax authorities (Direction Générale des Impôts). It was not until 1965 that company tax declaration forms incorporated the language of the 1957 PCG and these forms became available for direct use by the INSEE (Fourquet, 1980; Vanoli, 2005; Volle, 1982). At the end of the 1960s, when the need for greater convergence between national accounting and the PCG once again became an issue, there were some attempts to reconcile the two (Benedetti and Brunhes, 1971; Boutan, 1967; Boutan and Delsol, 1969; Delsol, 1967). French economic policy planners needed micro-simulation models based on data from company financial accounts. The then European Economic Community also needed similar data to set parities for the future single currency, to establish membership criteria for future member states, and for various administrative purposes. This meant that individual databases were to provide more information on households and companies which, in turn, required extensive use of financial accounting data. Lagrange, a former senior civil servant in the Ministry of Finance which supervises the INSEE, and trained in national accounting, could not have been insensitive to these concerns. 37

In the 1980s, some very productive research was conducted on the opportunities offered by computers for the development of accounting systems. Colasse 38 (1993: 130) was even able to state that accounting “had entered a period of change and rebirth as important as that which saw the advent of double entry accounting, i.e. the Italian renaissance”. These reflections mainly concerned the idea of “multiple-entry” accounting and its integration in databases. In France, meanwhile, there were attempts to bring financial accounting and national accounting closer together. This could only encourage Lagrange to believe that his system might be a success. Consequently, he did everything possible to highlight the benefits of his method: he produced publications presenting the method (a book, articles in professional and even academic journals) and a thesis that would afford some “scientific” or at least academic legitimacy. A CNC commission was also set up to examine his system and the feasibility of its implementation. This can be seen as an attempt to institutionalize the système croisé.

However, the originality of the système croisé was contested because of its similarities to the extensive research of the same period on multi-dimensional accounting (Degos, 1991). The growing number of accounting information users, both internal and external, led to a differentiation of information needs, and users were frustrated by the limitations of the double-entry accounting model. This resulted in a proliferation of parallel sub-systems which, although difficult to coordinate, were intended to enhance the “traditional basic entries” multi-dimensionally (Dourneau, 1989): instead of being restricted to a double-entry type classification of assets, it was suggested that accounts could include as many classifications as necessary thanks to progress in information technology. Practitioners had undertaken productive applied research in this field, mainly associated with systems analysis, multi-dimensional databases, and the concept of relational data. This research was continued by supporters of event-based accounting as a result of the collaboration of information systems specialists and accounting theorists. French research on event-based accounting came later than that of Anglo-American authors (Ijiri, 1986; McCarthy, 1982; Sorter, 1969), who proposed entering raw data to avoid any distortion of information due to aggregation and valuation by accountants. These ideas spread in France in the 1980s and gave rise to a French school of event-based theory (Meylon, 1988). Some authors even advocated a complete break with double-entry accounting (Gense, 1983), although Anglo-American researchers considered this a secondary concern. In France, the analysis was built on the increasing use of computers (Akoka, 1981; Augustin, 1986; Samara, 2004; Stepniewski, 1987; Veret 1989). Computers had become extremely powerful, leading to the illusion that, since everything was technically possible, nothing was impossible. All that was needed was to develop a more “powerful” accounting technique to bring accounting into line with the new possibilities offered by computers. Reflections on the social dimension of accounting only came later, and the illusion of technological omnipotence still had a hold on many researchers at the time. Meanwhile, research in accounting had undergone a parallel change of paradigm (Jeanjean and Ramirez, 2008): The normative research which had developed during the 1950s had been replaced by empirical research more concerned with history and sociology. The aim was no longer to invent accounting systems, but rather to understand why the systems in use had taken precedence over others. Normative research (identifying best solutions) was rapidly being overtaken by the standard-setters (national and international).

The 1980s saw an effusion of highly attractive technical proposals 39 which failed to raise the interest of the “market” of users. The system devised by Jean-Pierre Lagrange was one of these proposals, and we will now examine his efforts to promote the système croisé.

In cooperation with Michèle Saint Ferdinand, 40 Lagrange wrote and defended a dissertation in 1987 (Lagrange and Saint-Ferdinand, 1987) at the University of Paris Dauphine. It was entitled “Contributions à la mise en œuvre de systèmes d’information d’entreprises efficaces. Le système croisé et l’enregistrement simultané, base de réorganisation” (Contributions to the implementation of efficient corporate information systems. The système croisé and simultaneous recording, a basis for reorganization). Seeking a renowned PhD supervisor, he met with university dean André Cibert 41 in 1980, and despite Cibert’s initial scepticism, he eventually convinced him that his subject was worth attention. After a few meetings, Cibert became interested and agreed to supervise Lagrange’s work.

Between 1975 and the late 1990s, Lagrange wrote several articles in professional and academic journals (Lagrange, 1975, 1991, 1992a, 1992b, 1993a, 1996), as well as a book entitled: Le système croisé. L’économie traduite en comptabilité (The système croisé: Economics Translated into Accounting) which was published twice (Lagrange and Saint-Ferdinand, 1990, 2000). He also gave a paper entitled: “Economie d’entreprise, économie nationale et comptabilité: le Système Croisé, innovation conceptuelle et économique” (Business economics, national economics and accounting: The système croisé, a conceptual and economic innovation), at the 14th Congress of the Association Francophone de Comptabilité (French-speaking Accounting Association) in Toulouse in May of 1993 (Lagrange, 1993b).

Lagrange was personally acquainted with Jean Dupont, the then president of the CNC. He had met Dupont at CNC discussion groups on consolidation, during which they discussed the shortcomings of cost accounting in France and his project: “Voilà ce que j’ai fait là où j’ai pu le faire … Que peut-on en faire?” (This is what I have done where it was possible … What can we do with it?). In the early 1980s, this led to a CNC project for a système croisé commission which included Edmond Marquès, Professor at HEC Paris and one of the founders of the European Accounting Association and the Association Francophone de Comptabilité.

Meeting regularly for four years, the primary aim was to dispel any objections to the use of the système croisé. A report was finally completed and printed in 1989. Using the system, it had become possible to issue a compte de transactions (transactions account) and a compte de flux monétaire (cash flow statement). Their work on the système croisé was presented during a meeting of the CNC on 30 November 1990 in the presence of Laurent Fabius, the then Minister of the Economy. Unfortunately, Jean Dupont, the system’s only supporter, had suffered a minor heart attack some time before the meeting. He returned to work too soon and died in 1991. He was not replaced until a year and a half after his death, 42 and then by a legal specialist, Yves Cotte. Cotte wanted to unify the recommendations of the CNC and above all make the CNC’s opinions binding, thus preparing the way for the CRC, 43 and a new type of standardization. In a way, the système croisé therefore emerged when the members of the CNC were otherwise preoccupied. In 1996, Jean Arthuis, the then Minister of Finance, worked on the renewal of the CNC 44 and the creation of the CRC with the aim of strengthening the regulatory powers of the CNC and reducing its membership to increase efficiency. The cuts in CNC 45 membership included Lagrange. Dupont’s death and Arthuis’ measures thus deprived Lagrange of his main public platform and his only official support.

It is difficult to reach a firm conclusion on the inherent qualities of the système croisé. In the 1990s, it was the subject of much theoretical debate; neither researchers nor practitioners (apart from Lagrange) were able to observe real-life cases of its application since the system had only been adopted confidentially by a few pilot companies. In keeping with the general opinion on the subject, and as academics and former practitioners, we nevertheless feel that the système croisé could have reconciled the different approaches to financial accounting (by nature), cost accounting (by function) and cash flow monitoring (by activity). More than simply a question of sorting and reclassifying data using computer technology, accounting integration is a means of ensuring accounting coherence and quality through functions that link accounting entries and manipulations. Information technology alone cannot solve the basic issue of how data is entered and allocated, but the système croisé might have done so. Despite its relative complexity, computer technology would have made this system perfectly operable.

It should also be noted that the système croisé faced competition in the 1990s from Jean-Claude Dormagen, a former colleague of Lagrange. The two men had worked together at L’Oréal, where Dormagen was chief accounting officer in the 1970s and 1980s. He held a lower position than Lagrange, but joined L’Oréal before Lagrange, and stayed there after he left. Dormagen developed a system called the système triadique (Dormagen, 1993), which uses a triple-entry approach, thus adding an extra dimension to each entry: The nature of the transaction, that is, its purpose, is recorded in addition to the debit and credit. The système triadique derived its name from the third dimension (Cohen-Scali, 1990). It allowed costs to be classified by nature and by intended use, as well as an analysis of cash flows. The system contained two innovations:

A single entry amount is allocated in three dimensions: Origin/Use/Purpose, such that the preparation of a balance sheet, a profit and loss statement and a cash flow statement is simple, using both cost and financial accounting data.

Inventory changes are recorded as part of the financial accounting. The profit and loss statement is thus created automatically as entries are posted.

A software programme for this method named Lumière was developed with the help of Roland Deboux, director of the Servant Soft software company (Deboux et al., 1995). An initial article published by Dormagen in 1979 (Dormagen, 1979) was followed by others during the 1990s (1990a, 1991, 1993). He also published a book entitled La comptabilité intégrée (Integrated Accounting, 1990b). Despite the conflict between Dormagen and Lagrange over the similarity of their methods and therefore their intellectual origins, the système triadique may be considered as the second generation of the système croisé (Cohen-Scali, 1990). 46 The occasionally tense rivalry between Dormagen and Lagrange obviously had a negative influence on the dissemination of their innovations.

The système croisé was the subject of numerous papers and articles in professional and academic journals during the 1990s. It was also mentioned in the principal university textbooks on financial and management accounting in France (and abroad, see Elad, 2000) during the same period. Yet, like the système triadique, to the best of our knowledge it has never been implemented in any firms other than those in which it was tested by its inventor. After attracting some praise from specialists, both fell into oblivion (see below). Lagrange was unsuccessful in rallying significant opinion leaders – practitioners or academics – to his cause.

Discussion and conclusion

Our article shows how the système croisé failed to become established in a significant number of firms after it was invented in the early 1970s – despite its unquestionable advantages:

undeniable intrinsic soundness;

the opportunities its designer had to demonstrate its feasibility and usefulness in practice;

the connections and influence of its designer among the people in charge of accounting policy in France.

In conclusion, alongside historical understanding, the history of the système croisé provides two important implications for theory and practice. First, it confirms the teachings of the Actor-Network Theory (ANT) stream of sociology of science, concerning the success and spread of innovations. The technical characteristics of an innovation are not sufficient to explain its success, or lack of success, in achieving widespread adoption. Jean-Pierre Lagrange’s belief that his project was deliberately sabotaged by Anglo-American accounting firms is unlikely to be the true cause of the failure of the système croisé. Lagrange believes the auditors (Arthur Andersen and Coopers & Lybrands) were in favour of cost accounting under US and future international standards, and denigrated the French system of recording costs by nature because it did not provide an efficient management tool. Lagrange maintains that the système croisé would have made the Anglo-American audit less significant, since its integrated recording system allows accounts to be balanced and provides a verification of accounting validity. However, we have no evidence to support this claim. Unfortunately, we were unable to obtain copies of the auditors’ reports to L’Oréal and Chargeurs. We can only add that it is highly improbable that either auditing firm was aware of the work by the other firm when issuing a critical opinion of the system: these were two independent firms working with two different companies, almost 20 years apart.

We should also consider the typical experience of inventors of accounting systems. The système croisé was the result of a purely intellectual process, rather than the result of an analysis of firms’ actual practices. To the best of our knowledge, no accounting innovation resulting from the theoretical thinking of a single, clearly-identified inventor has ever achieved widespread use. 47 The système croisé thus joined the long list of “inventions” that have come to nothing; other examples from different periods include:

The system devised by ET Jones (1796) enjoyed only short-lived success, and, along with its author, has been severely criticized by many accounting historians (Edwards, 1989; Yamey, 1956; Stevelinck, 1970).

At the end of the nineteenth century, “marginalist” economists (Walras, Jevons and Menger) demonstrated that marginal cost was minimal when it was equal to the mean cost. This “discovery” was never put to use by firms, as shown by the surveys conducted by Hall and Hitch (1939). 48

The full cost method invented by Georges Perrin in 1940, and later transformed by an engineer, the “UVA method”, 49 failed to gain any ground in 70 years of existence, and was only used by some 30 small and medium-sized businesses in France and a similar number in Brazil.

RS Kaplan (1984) showed that between 1950 and 1980, most of the cost accounting “discoveries” by academics were never put into practice. With regard to transfer prices, he also remarks that micro-economics has shown that the internal supplier’s opportunity cost was the optimal transfer price for a firm – and immediately adds that the number of firms applying this rule are few and far between.

The techniques that have become widespread have almost all been introduced gradually, such that no particular inventor of these techniques may be singled out. Success is often driven by a network of actors who promote existing practices after reformulating them, even when the method is attributed to one of the most influential of these actors. The best-known example of this is double-entry bookkeeping, used in Genoa as early as 1340, that is, 150 years before Pacioli wrote his Summa. Industrial accounting, the precursor to cost accounting, which appeared in England and in France during the late eighteenth century (Boyns et al., 1997), also emerged in a gradual process. The ABC method can also be considered to have emerged progressively, as shown by Dugdale and Jones (2002).

The second contribution of this article is the observation that the over-explicit link between standardized cost and financial accounting in France seems to have allowed the State to interfere in cost accounting practices. A separation of accounting systems was thus inevitable. French firms are naturally averse to the risk of interference by standard-setters in their accounting practices. They were bound to reject the possibility of cost accounting becoming standardized and thus open to scrutiny by the tax and competition authorities, since it was supposed to assess their competitive advantages. We are therefore inclined to see the separation of cost and financial accounting as inevitable, at least in the medium term and in a general manner. A quasi consensus ratifying this separation can be observed among firms, resulting in a standardized financial accounting system and a cost accounting system organized at the firm’s own discretion. Firms may, independently and confidentially, choose to integrate the two accounting systems, but this will not affect the general separation of the two for external relations. For the time being, the need to provide data to the various stakeholders has not overcome the tendency to keep the sources of this information separate.

It should nevertheless be borne in mind that the integration of the two accounting systems seems to be considered necessary, even in France: “Not to accord any autonomy to cost accounting would appear simplistic. But it would be even more dangerous to encourage laxity as a result of autonomy. Cost accounting must remain reliable and therefore verifiable” (Bouquin, 2008: 184).

It should certainly also be noted that the French environment is changing. Globalization, the shrinking role of governments in the economy, changes in information technologies such as enterprise resource planning (ERP) systems (Granlund and Malmi, 2002; Granlund Mouritsen, 2003; Granlund and Taipaleenmaki, 2005), the substitution of supra-national standard-setting bodies for national governments, and pressure from institutional investors seeking to influence internal processes, all exercise the drive for greater accounting integration. For example, the recent integration trend observed in Anglo-American accounting through IFRS, which has led to a shift from historical-cost based to fair value-based financial accounting and adoption of IFRS 8, 50 might call French-style separation of accounting systems into question. The need for corporate cost and financial accounting information systems to be integrated is due to the fact that cost accounting information is expected to be used not only for internal, but also for external reporting. The same phenomenon has been observed in the Anglo-American environment (Ikaheimo and Taipaleenmaki, 2009). The lessons to be learned from the history of the relationship between cost and financial accounting in France may provide food for thought about the reluctance of firms in any location to accept obligations to divulge their cost accounts, whether those obligations derive from State intervention or private requirements, as illustrated in a recent study of the adoption of IFRS 8 in France (Berland et al., 2011).

The relationship between cost and financial accounting and the history of that relationship is an important research topic, because it is central to the concerns of both private and public businesses, financial analysts and standard-setters. It also concerns the relationship between the finance and management control functions. There is a clear need for further research comparing relevant historical and political experiences in other Latin countries using charts of accounts with systems used in the Anglo-American context. The findings of such research would make a significant contribution to the thinking on the standardization of accounting systems, which is now taking place at the global rather than the local level.

Footnotes

Appendix 1: Entry and summary operations according to the système croisé :

A company purchases €100 worth of goods on credit:

It sells four-fifths of these goods and puts the rest in stock:

A sale takes place for €110:

The customers pay €60 cash:

Goods kept in stock:

Depreciation of €30:

At the year end, the balance of the transit and translation accounts will be zero. The grand total of the balance may then be made. In the end, the last section at the bottom right of the table will be zero. Once the balance has been calculated, the four financial statements produced by the système croisé can be issued.

Acknowledgements

The authors would like to thank the editors and the constructive and helpful comments of the two anonymous referees. The article has also benefited from helpful contributions from participants at the sixth Accounting History International Conference (Wellington, 2010). This work was supported by the Association Francophone de Comptabilité.