Abstract

Accountants in South Africa established professional organizations to protect and promote the profession in the rapidly growing business environment after the discovery of diamonds and gold in the last quarter of the nineteenth century. This article investigates the development of the statutory regulatory environment of the accounting profession, which gradually emerged alongside the profession’s own structures. The growth of the South African economy created a rising demand for professional accountants, and large numbers of accountants from Britain emigrated to South Africa (or to the former colonies under British control, which later formed the Union of South Africa in 1910). Professional regulation remained a professional concern until the 1951 Act which established the Public Accountants and Auditors Board. The article extends the existing literature on the state–profession nexus by explaining the circumstances leading to proactive intervention of the state and the intersection of the state’s public interest responsibility and the closure attempts of the profession.

Introduction

Accountants in the Union of South Africa in 1910 shared a long history of heterogeneity and organizational fissure with accountants in Britain. Prior to the emergence of “an imperial accountancy arena” (Chua and Poullaos, 2002: 410; Poullaos, 2010: 10) intra-accountancy contestation unfolded in South Africa. Intra-professional competition developed and a state–profession nexus took shape. An act of Parliament in 1951 introduced statutory compulsory registration for all public accountants in the entire Union in 1951. This development afforded the state direct regulation of professional accounting practising rights. Johnson and Caygill (1971: 172) observed from earlier developments in Australia, India, South Africa and New Zealand that a more intimate relationship had developed between Government and the accountancy profession in those states, and that Government displayed a greater readiness to get involved in control over the field of accountancy practice. Poullaos (2009: 259) also acknowledged “a far more extensive” dynamic in the state–profession nexus in Commonwealth countries than in Britain. Endless attempts in Britain from the late 1930s and the Public Accountants’ Bill of 1945/1946 until the failed integration attempts of the 1960s and 1970s (Walker and Shackleton, 1995, 1998) have come to nothing, and so professional closure remains elusive in Britain. Although, as will be shown below, the South African Act of 1951 came after a long period during which the state was reluctant to become the ally of any of the contesting accounting societies and associations, it nevertheless brought about a form of national “adequate professional closure” for South Africa that has never been achieved in Britain or Australia. The question to be asked is how the passing of the 1951 Act is to be explained, given the South African state’s long-standing status as a reluctant ally? How has the profession–state nexus developed in South Africa and why is this relationship so different from similar relationships with the state in other Commonwealth countries?

The empirical focus of this article is the exploration of the profession–state nexus since the mid-1930s in the professionalization strategies of the accountancy profession in South Africa. The professionalization strategies of the accountancy profession in South Africa developed into attempts to secure state sanctioning of the status of a self-regulated profession. This was the profession’s closure strategy. The accountancy profession in South Africa desired self-regulation, but at the same time statutory incorporation similar to the status acquired in 1904 in the Transvaal Colony under British rule. The simultaneous pursuit of self-regulation and statutory incorporation enhanced the risk of state intervention in the affairs of the profession, and that could jeopardize professional self-regulation. The preferred strategy was therefore to obtain statutory sanctioning for a private bill brought to Parliament by the accountancy profession.

The contribution of this study is the systematic exploration of hitherto unexplored primary archival material from the National Archives of South Africa to explain the unfolding of the profession–state nexus. The archives of the Department of Treasury were used together with the original documents and minutes of the Societies of Chartered Accountants in South Africa and the Public Accountants and Auditors Board. These documents revealed a cautious but carefully directed strategy by the accountancy profession to secure professional standing, by privately initiated acts of the legislature.

The contribution of this article is two-fold. Firstly, it offers a systematic historical analysis of the relationship between the accountancy profession and the state in South Africa using primary archival material hitherto unexplored. Secondly, the article extends existing knowledge on the state–profession nexus in the process of the professionalization of the accountancy profession by explaining the conditions under which the state had decided to take a more proactive role. While it is acknowledged that the state can be either hostile to or supportive of accountancy professional projects, a detailed and systematic study of the specific historical context of that development offers an explanation of why and under what circumstances the state engaged in such an engagement with the profession. Noyce (1954) and Van Rensburg (1990) wrote anecdotal chronologies of the development of the profession in South Africa, but did not seek to explain the course of events or reflect on the wider literature on the profession–state nexus. This article benefits from the theoretical literature on professionalization and seeks to explain the unfolding of the profession–state nexus in South Africa by means of the 1951 Act. It explains the circumstances in South Africa as a member of the British Commonwealth, which afforded a more proactive role for the state in this relationship. The result was the nationwide statutory regulation of the accountancy profession through the Public Accountants’ and Auditors’ Act, No. 51 of 1951 (PAA Act). In effect the state facilitated “adequate professional closure” of practising rights.

This article first briefly explores the theoretical and historical context of professional closure and the state–profession nexus to set the context for the empirical analysis of the historical unfolding of the professional closure strategy in South Africa. A brief overview of the period before 1940 presents the background for the systematic analysis of the circumstances leading up to the promulgation of the Public Accountants and Auditors’ Act of 1951. This is a case study of South African developments.

Professionalization, closure and the state–profession nexus

By 1910 the South African economy was a primary economy, dependent on agricultural and mining production for foreign exchange revenue. Economic progress based on the rationality of a single market constituted a powerful motive for the constitutional union. In promoting economic co-operation, markets were liberalized to allow the free movement of capital, labour and goods. The mining sector created demand for small industrial enterprises and financial institutions. After the discovery of diamonds and gold in the last quarter of the nineteenth century, international interest in the South African economy exploded. Together with foreign mining entrepreneurs, exploration and digging activities gave rise to urban centres where business activities increased rapidly (Schumann, 1938: 233; Schumann, 1951: 240–256). The new economic environment introduced business professionals to provide expert advice and services. After the arrival of fortune-seekers, diggers, farmers and manual labourers, professional accountants followed to participate in new business opportunities (De Kiewiet, 1968; De Kock, 1924; Johnson and Caygill, 1971: 157). Numerous financial deals, amalgamations, floatations on the Johannesburg Stock Exchange and in London, and the formation of limited liability companies, coupled with the need for the protection of the public, made the services of accountants and auditors indispensable. The mining companies in particular soon developed a need for the professional services of accountants and auditors (Noyce, 1954: 4). Accountants who immigrated to the South African Republic (SAR) organized themselves into professional organizations to protect their “profession” and to ensure adherence to standards they complied with in their countries of origin. Those accountants described their professional role in the following way: Whereas the profession of Public Accountants in the South African Republic is of a very extensive nature and their functions are of great and increasing importance in respect of their employment in the capacity of Liquidators acting in the winding-up of Companies, and of receivers under decrees, and of Trustees in Bankruptcies or arrangements with creditors, and in various positions of Trust under Courts of Justice, as also in the auditing of accounts of public Companies, and of partnerships and otherwise. (TVR, 1898)

Professional accountants presented themselves as the promoters and protectors of a sound business environment to serve the emerging SAR economy.

Why professional organizations?

The formation of professional organizations has typically been understood as a response to specific historical circumstances, circumstances which helped to create the market for particular kinds of accounting labour. The purpose of the following section is to explain the literature on the profession–state nexus in Commonwealth countries; to explore where the South African case study fits into this context, given the lack of such research on the development of the accountancy profession in South Africa. In some instances developments diverged from the Commonwealth experience and in other instances similarities can be observed. As privately owned companies expanded, so did technology in the design of work, as well as social relations of production. The social origin of institutions such as the market and the modern state had a profound impact on the emergence of professional organizations – in this case, accounting organizations. Willmott explains the logic and autonomy of the state, market, civil community and the accountancy profession as the latter reinforcing and subverting three sources of authority: that of the market, the state and the community. This symbiosis Willmott summarized as follows: professional organisations are appropriately viewed as private interest governments that emerge in response to tension within and between civil society and the state. In the context of capitalist society they reinforce and subvert its three main sources of authority: the market, the state and the community. (Willmott, 1986: 564)

On the first level, the profession “constrains and distorts” the market, but also preserves the institutions of the market. The profession distorts the market by limiting access to that market through requirements of training, examinations and standards of practice (Willmott, 1986: 563). On the second level, the profession engages with community interests by presenting itself as the promoter of those values and interests. This engagement results in the utilization of the community “ideology” to promote the profession’s self-interest and self-esteem. On the third level, the profession reinforces the authority of the state by seeking state sanctioning. The needs of the modern state to regulate and integrate economic activity in the capitalist economy cement its reliance on professions to provide expertise, training and labour. Professions depend on the state for recognition and legitimacy, thus providing the professions with “legal monopolies”.

The formation of professional societies constituted a strategy to mobilize collectively to achieve goals (in this instance, legal goals) towards securing a more stable social and economic environment in which they could operate. The outcome would contribute to the building of group identity and putting arguments in relevant forums, both public and private (Poullaos, 2009: 250). The significance of the process of professionalization was that it mobilized members in the society and stressed the importance of the links they had developed with other professionals in society in order to achieve recognition and acknowledgement of their social status and specific interests. Professional societies of accountants in the four British colonies organized themselves 1 so as to promote professional standards. The statutory incorporation of the professional societies in the Transvaal and Natal excluded non-member accountants from practising in those colonies, thus marginalizing accountants who had practised as public accountants elsewhere from public practice unless they joined the respective incorporated Societies. In the professionalization of the accountancy profession, strategies of professional closure were utilized to protect the “profession” (Chua and Clegg, 1990; Collins, 1990a, 1990b; Kedslie, 1990; Macdonald, 1985; Poullaos, 2007), which led to the exclusion of other persons who also called themselves “accountants” from the mainstream accountants’ organizations in Britain (Johnson and Caygill, 1971: 155, 157; Stacey, 1954: 21–34) – a similar outcome to developments in South Africa. Poullaos noted: “Also involved was a more general desire to dominate lucrative markets. The interplay of economic class and social status, collective mobility and market control, and social closure and professional closure, is all evident” (Poullaos, 2009: 250). Writers of generic literature on the sociology of professions (Collins, 1990a; Johnson, 1982; Macdonald, 1995; Murphy, 1986) were cautioned by Burchell, Clubb, Hopwood, Hughes and Nahapiet (1980) to consider the specific historical context of the development of the accountancy profession because “Accounting is coming to be seen as a social rather than a purely technical phenomenon”.

A wide range of studies has been undertaken on professionalization of the accountancy profession in Britain, Canada, Australia, “South Africa and the Imperial accountancy arena”, the United States of America and various “Post-colonial” professionalization histories (Poullaos, 2009). An important reason for this study is the lacunae in original research on professionalization in South Africa. 2 The strategies of professionalization include professional self-regulation by means of membership criteria, and educational requirements and practical qualifications with designated professionals. Professional control over this professionalization process was highly contested as a result of the proliferation of accountants’ societies and organizations (Johnson and Caygill, 1971).

How to achieve “closure”

Achieving professional control, uncontested autonomy or professional closure seemed an elusive goal in many of the case studies of professionalization of the accountancy profession in the British Empire. One strategy for professional closure was the profession’s claim to professional self-regulation. The organization of “professional organizations” served to “define occupational territory” (Kronus, 1976: 3; Robson et al., 1994: 527–528), develop “high-grade skills”, lay down “rules that govern conduct of members and thus influence the deployment of human capital”, and establish “monopolies” or “privileges for members”, thus limiting the availability of substitutes for their professional services (Sees, 1966: 2–3). In the early twentieth century Max Weber developed the notion of “social closure”, which refers to the process of subordination whereby one group monopolizes advantages by closing off opportunities to another group of outsiders beneath it that is defined as inferior and ineligible. This form of closure is the product of social and not statutory forces. Parkin (1979: 58–59) placed more emphasis on credentialism and legal means to effect closure. He argued that: the professions … generally seek to establish a legal monopoly over the provision of services through licensure by the state … Their conflict, concealed beneath the rhetoric of professional ethics was, if anything, with the lay public. It was a struggle to establish a monopoly of certain forms of knowledge and practice and with legal protection from lay interference. (emphasis added)

In Britain the professional endeavours to secure a Royal Charter succeeded in 1880. This gave the Institute of Chartered Accountants of England and Wales (Stacey, 1954: 25), the holders of the charter, a mechanism, which was subsequently implicated in some forms of statutory closure. The social forces of professionalization secured a charter, which was, as described by Willmott, “authorisation of their monopoly” (1986: 564). The ultimate form of professional recognition was statutory recognition which specified that professional services of a specific nature may only be performed by registered accountants (Macdonald, 1985: 343). A lack of success in acquiring the desired form of professional closure often led to a search for alternative strategies. Chua and Clegg (1990) noted that the choice of closure strategies was dynamic and changing: as one seemed “dead” another would be implemented. Professional organizations sought official registration as formal recognition of their status. Closure strategies are thus changing, given success or failure and context. Accountants’ activities in society soon provided further justification for state recognition, because it afforded the state indirect regulation of industry and commerce. Treasury involvement followed from public accountants’ public engagement with “public accounts” and “public” interest in sound financial reporting. The nature of the clientele of accountants justified statutory regulation.

After the Second World War the British socio-political fabric changed and led to initiatives by the accountancy profession to achieve closer co-ordination through registration by the licensing of “public accountants”. The 1957 merger of the ICAEW and the Society of Accountants and Auditors (SIAA) “was unable to achieve registration via licensing bodies akin to private interest governments” (Walker and Shackleton, 1995: 486). Yet another attempt at professional “closure” in Britain failed in 1970, because of a change in the nature of the state and “the complexities of actualising closure objectives” (Walker and Shackleton, 1998: 67). In Chua and Poullaos (1993, 1998) and Poullaos (1993, 1994) the authors explored the Australian accountancy profession’s different attempts to secure professional closure in Australia. 3 These closure strategies offered the accountancy profession in Britain, Australia and Canada a Weberian status advantage over accountants who engaged in public practice without the “chartered” designation. Accountants operating under the Royal Charter did not possess a legal monopoly or exclusive licence to engage in public practice, as was also the case after the South African Designation Act of 1927. Sanctioning of public practice by means of a Royal Charter was nevertheless a strategy to enhance market control and collective social mobility. It did not provide legal exclusivity, in Parkin’s sense.

Chua and Poullaos (1993) developed four methodological premises which had a profound influence on the discourse on professionalization. The first described professions as occupational groups that have one general aim, that is to translate one order of scarce resources (knowledge and skills) into another (social and economic rewards) (Larson, 1977). The second premise is that routes to closure are neither presumed to be equal in efficacy nor linear in movement. The third premise is that professions are emergent as a condition of state formation and state formation is a major condition of professional autonomy. Finally, serious attention is given to temporal sequences by “asking questions of social structure and processes when they are understood to be situated concretely in time and space” (Chua and Poullaos, 1993: 694–695; Johnson, 1982). This methodology contributed to an understanding of the failure of the first charter attempt of the accountants of Victoria, Australia, because of the decision by the Colonial Office not to support the application.

The profession–state nexus in the context of the Empire has been the focus of studies by Annisette (1999), Carnegie and Parker (1999), Johnson (1982), Johnson and Cayhill (1971) and Parker (1989). This literature investigates the specific configuration of the state–profession nexus which presented a precondition to understanding the professionalization of accounting. This analysis was extended to explore the impact of the “interactive periphery on the imperial centre” (Chua and Poullaos, 2002). While it is accepted that the British notion of professionalism was exported and adopted in most of the Empire as well as in South Africa and that the British development and operation of the accountancy profession influenced the Empire profoundly (Johnson 1982; Johnson and Cayhill, 1971), in the latter case the agency of the South African state also influenced the professionalization process. This article shows the role of the state in the development of professional regulation in South Africa – first non-interference, then pro-active agency. It shows that accountants’ claim to self-regulation as a defining characteristic of what it means to be professional was challenged by the South African state. The state demanded professional consolidation as a prerequisite to compulsory registration of accountants and auditors. The Colonial Office in Britain, on the other hand, refused to get involved with the ICAEW in its attempts to oppose professional exclusion from some Commonwealth markets (Poullaos, 2010). There were thus clear differences across countries and in time in the unfolding of the profession–state nexus in the British Empire.

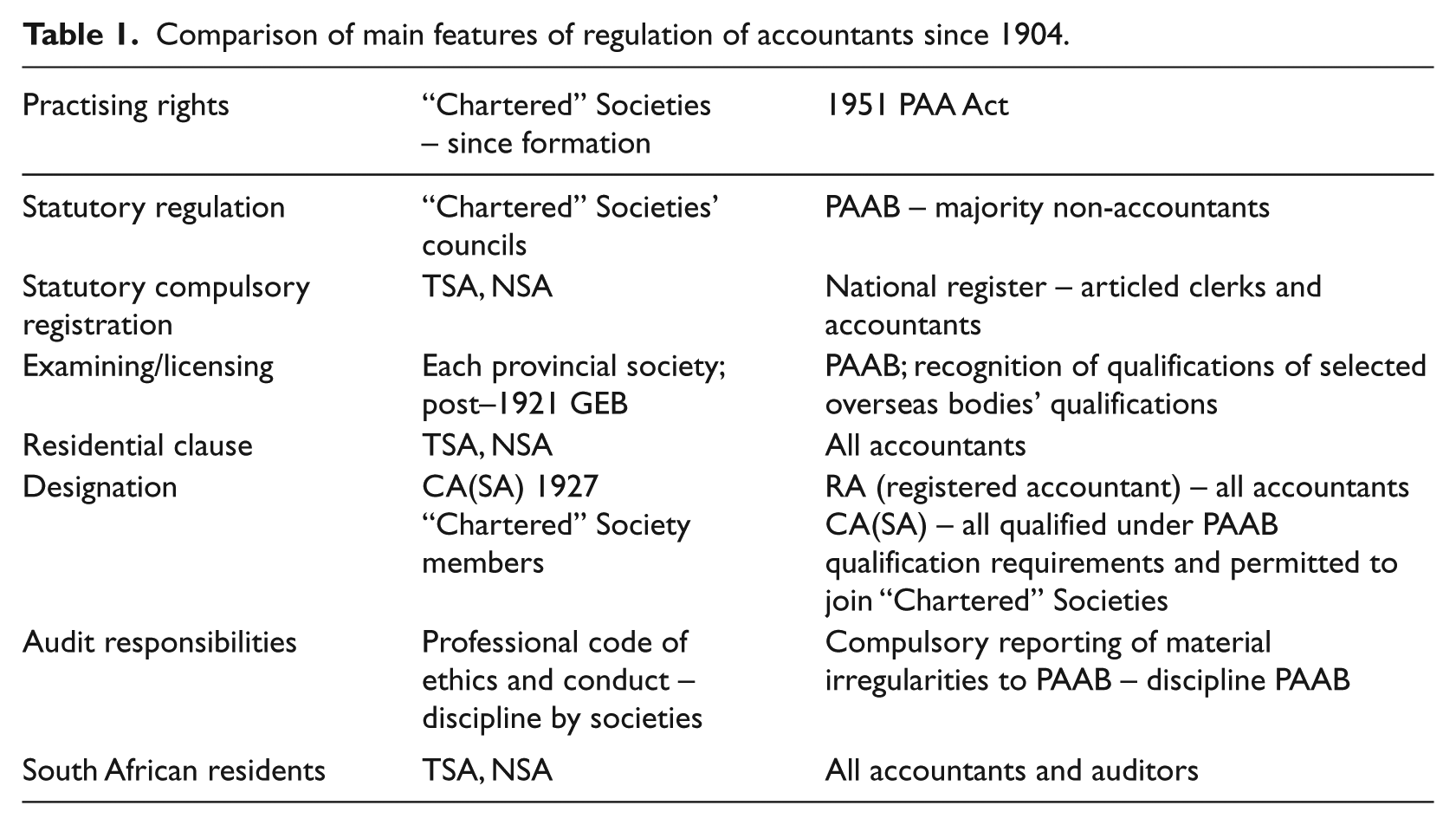

The above contextualizes the formation of professional societies in South Africa. It links the professionalization process to the general trend in the literature and shows how the accountancy profession from the outset attempted to extend professional closure in the way that Weber explained the closing off of opportunities, to more specific professional closure as explained by Parkin, that is, by means of legislation that would exclude, through registration requirements, non-qualifying accountants from public practice. This article investigates the specific South African profession–state nexus in the professionalization process, which displays differences in some instances to that of other Commonwealth countries. While in Britain and Australia (Victoria) accountants sought sanctioning of their status by means of a Royal Charter, in South Africa and Canada accountants used statutory sanctioning of the title of “Chartered Accountant” to secure preferential practising rights to members of professional societies. The accountancy profession, thus entrenched on the exclusionary base of designation, then sought further statutory protection in the Parkin sense of professional closure by means of a private act of Parliament, but was unsuccessful because of a lack of professional unity. The prolonged attempts to acquire statutory sanctioning of professional closure ended in 1951 with the promulgation of the PAA Act. This Act gave the South African state a direct statutory role in professional closure. Why has the state become so directly involved?

The context of professional closure: Contestation and market control, 1904–1940

Early closure attempts

In the rapidly developing SAR under an anti-British Boer republican Government, accountants of British descent and affiliated to the SIAA in England sought official recognition of their status and protection of their practising rights. After the disruption of the South African War the British Government granted such official recognition on condition that the representatives of the Institute of Accountants and Auditors in the South African Republic (IAASAR – all members of the SIAA in England) and the Institute of Chartered Accountants in South Africa (established in 1904 by British chartered accountants in the Transvaal Colony) agreed on a Private Ordinance to incorporate the accountancy profession in the colony. Ordinance No. 3 (Private) of 1904 secured exclusive practising rights to members on the Transvaal Society of Accountants (TSA) in the colony, thus effectively monopolizing the accountancy arena for resident members of the SIAA, who held joint membership with the TSA (Chua and Poullaos, 2002: 417, 425–427; Johnson and Caygill, 1971: 161; SC, 1904). Ordinance No. 3 excluded all non-resident accountants (and therefore also non-resident British chartered accountants) from practising in the Transvaal. Similar accountants’ organizations were formed in the Cape Colony in 1908, in the Orange River Colony in 1907 and in the Natal Colony in 1909. The Natal Society of Accountants (NSA) was also incorporated by means of the Accountants’ Act, No. 35 of 1909, which extended reciprocity of practising rights to members of the TSA, but also excluded foreign non-resident accountants, as in the Transvaal. The TSA reversed this reciprocity in 1909. Prior to unification, the accountancy profession thus acquired strategic state support through statutory recognition in two colonies, for the profession’s private initiatives towards professional closure.

The formation of the Union of South Africa sparked discussions on the extension of the TSA/NSA model to the entire Union (TSA Year Book, 1911: 44). Consensus by the four societies on the harmonization of conditions of practice and registration on a national basis in January 1911, (Noyce, 1954: 7; TSA Year Book, 1911: 44; Van Rensburg, 1990: 22) resulted in the Draft Union Accountant’s Registration Bill (1912). The bill provided for the consolidation of accountants’ Societies in the Union under a single national register for all accountants in South Africa who qualified to be members of the local Societies. It also included recognized resident accountants qualified under the by-laws of the SIAA, ICAEW, the Scottish Chartered Societies and accountants’ societies in Australia, Canada and New Zealand, who were members of the four societies (TES, 2256/F9/42). The draft private bill was considered by a Select Committee of Parliament, but objections against the preamble to the bill, as well as the principles of “Compulsory Registration” stalled this initiative (TES, 2256/F9/42). This first attempt by the profession to obtain state sanctioning for professional self-regulation failed. The First World War disrupted further attempts to pass legislation to establish a national register of accountants (Van Rensburg, 1990: 28).

Since it seemed that the consolidation and registration “closure strategy” had met with unforeseen opposition, the Societies decided in November 1920 on a different course of action. The Societies temporarily suspended their attempts to get statutory sanctioned compulsory registration, to bring about “as far as possible a common standard of qualification if not by Ordinance then by agreement amongst the Societies themselves” (TSA Minutes of Meeting 2/11/20). The result was the establishment of The South African Accounting Societies’ General Examining Board (GEB) in 1921 by the four provincial societies and the Rhodesian Society of Accountants. The GEB agreed to provide uniform conditions of admission, examinations and regulations for service under articles of clerkship. The meeting also recognized qualifications acquired outside the Union (the various Scottish Chartered Societies and the ICAEW) for purposes of public practice in the Union – provided that the accountant was a resident of the Union. Delegates of the SIAA South African branch were present and were granted reciprocity in terms of examinations passed abroad (TSA Year Book, 1922: 7).

The professional accountants’ societies maintained the initiative – the GEB idea was a professional strategy without state involvement. In 1924 the Societies tabled another private bill with the same aims as the 1912 bill: to restrict access to the right of public practice to accountants in public practice, on their own account – not in the full-time employment of another person or firm, and not in government employment – and to accountants qualified according to the Societies’ by-laws (TES, 2256/9/42). These exclusionary criteria also constituted the core of the contestation in Britain in the attempts by the profession to achieve statutory recognition and registration (Parker, 1989; Stacey, 1954; Walker and Shackleton, 1995, 1998). The 1924 private bill also failed because of protests from accountants outside the four Societies against the exclusionary nature of the proposed measure. But in 1927 the accountants’ professionalization strategy took yet another turn. The Chartered Accountants’ Designation (Private) Act, No. 13 of 1927 was successfully passed in Parliament. Only accountants who had acquired their professional qualifications by succeeding in the examinations prescribed by the Societies and who had completed the required years of articled clerkship were permitted by this law to designate themselves as “chartered accountants” (CAs) (Noyce, 1954: 7; TES, 2256/F9/42). This Act granted statutory recognition to the four provincial Societies, sanctioning the use of the designation “Chartered Accountant (South Africa)” – or CA(SA). This act designated the title “chartered” – as bestowed in Britain on the ICAEW members and in Scotland on the Scottish societies, but withheld from SIAA members in England – to accountants in South Africa who were members of the four provincial Societies. Poullaos (2010: 17–34) dealt extensively with the impact of the Designation Act on the accountancy community and the imperial accountancy arena (also see Parker, 2005).

For the purposes of this article it is important to note that the state was only involved in this professional closure attempt because any private act had to be tabled in the legislative assembly, which is Parliament, but the executive arm of the state took no initiative, as it would do in 1946. Members of Parliament representing different political parties of course had strong opinions on the matter, but these were in no sense representative of the executive arm of the state and neither did they necessarily coincide with the views represented by the Treasury. Members of Parliament, as the legislative apparatus of the “state”, were convinced of the justification of the bill and passed the act. Mr Charles Pearce, a solicitor acting on behalf of disgruntled accountants who would be excluded by the Designation Act from using the CA(SA) title, threatened to oppose the bill in Parliament. The four Societies arrived at an out-of-Parliament agreement with Pearce to the effect that accountants who were not members of the four Societies could submit their qualifications to the CSA for accreditation. If their professional qualifications were deemed of a high standard and they had been in public practice, a one-off admission to membership of the Cape Society of Accountants was granted (TES, 2258/9/42). The Designation Act was again an initiative of the profession, but it was known that the Minister of Finance, Mr NC Havenga, supported the measure. When the Institute of Accountants wrote to Havenga in August 1929 requesting permission for its members to register as CA(SA)s on the grounds of their recognition in England, his Secretary, Farrar wrote in a handwritten advisory to him: “I advise you to have nothing to do with these people. They are a group of disgruntled men who were unable to gain admission to the Cape Society” (TES, 2258/F9/349: 6/8/29). The accountancy profession was gradually nurturing the sympathetic support of the Minister of Finance and the Treasury in its professional self-regulation and closure attempts. The success of the GEB and the Designation Act pointed to the state looking favourably on private professional initiatives. The state did not take any proactive steps or prohibitive measures to block these attempts.

Reluctant ally engages

During the 1930s two factors were to create increasing doubt in the state about the accountancy profession’s claim to professional self-regulation. The first was voluntary membership of the CSA and SAAOFS, 4 which allowed arbitrary discretion to those Societies’ Councils on membership. The other matter was the ever-growing opposition and protest by excluded non-chartered accounting associations operating in South Africa, against the privileged position afforded to the four Societies by the Designation Act in 1927. The solution to this dilemma, Havenga wrote, might be to have a single act to bring under one regulatory system all practising accountants in South Africa. Havenga alluded to the British developments where a Commission to the British Board of Trade (Report CMD 3645) advised that it was not advisable to restrict accountancy practice to only those whose names appeared on a “register established by law”, but that the logical route for South Africa might be to extend the practices in the Transvaal and Natal to the entire Union (TES, 2258/F9/349). Between 1934 and 1940 a three-way interaction between the “Chartered” Societies, the non-designated associations and the state evolved.

The “Chartered” Societies’ private initiatives to secure an uncontested professional domain in South Africa were met by equally assertive representatives of non-chartered accounting associations, among them the Institute of Incorporated Accountants, the London Association of Certified Accountants, the Association of International Accountants and the Association of Public Accountants (TES, 2258/F9/349; TES, 2258/536/1/F33/263/4; TES, 2258/539). These associations were smaller in numbers than the four Societies, but aggressively called on the Minister of Finance for equal privileges with those Societies. The South African state had achieved the much sought-after statutory recognition of its sovereign status through the Statute of Westminster in 1931 (which ended the automatic superiority of the Westminster Parliament over all Dominion Parliaments), followed by the Status and Seals Acts in South Africa in 1934 (Davenport and Saunders, 2000: 291–293, 322, 334–337; Howard and Louis, 1998: 296–297). Appeals to the South African government could reinforce the recognition of its sovereign status. Furthermore, the failure of previous accountancy bills opened the door to challenging the position of the “Chartered” Societies.

A private member’s bill, on behalf of the Institute of Accountants of South Africa, was tabled in Parliament in 1934 by Dr Hjalmar Reitz, proposing the registration of all accountants in the Union. This bill did not proceed to the second reading (Hansard, 1934; TES, 2257/526/1/F33/263/4), especially as a result of the strong opposition of the TSA (TES, 2257/526/1/F33/263/4; PAAB, 2001: 6). The bill was referred to the government appointed Accountancy Profession Commission to investigate the qualifications and registration of professional accountants in South Africa and whether it would be “advisable to place the profession of accountancy and auditing in the Union on a qualified basis by the incorporation of a representative body having control over the whole profession and keeping a register in which should be inscribed the names of all qualified members of the profession” (TES, 2257/526/1/F33/263/4).

The Report of the Commission (April 1936) advised that a single register for accountants was necessary and practical (para 26) and that the four “Chartered” Societies maintain an internationally comparable professional status, which should not be undermined (para 37), but that the senior members of the profession should seek ways to admit certain practising accountants “under suitable terms” to chartered rank (para 29). As professional solidarity remained elusive in Canada and Australia (Carnegie, 2009: 282–289; Richardson, 1987), professional division emerged as a bone of contention between the “Chartered” Societies and the state.

Dr Hjalmar Reitz again introduced a Private Members’ Bill on behalf of the Institute of Accountants of South Africa in 1936, but it was unsuccessful again. The state noted the lack of professional unity, but stated categorically that it would not intervene – the profession could bring private member bills to Parliament (TES, 2257/526/1/F33/263/4). Another private members’ bill, the Accountancy Bill, No. 26 of 1938, was brought by Mr Pocock on behalf of the Chartered Societies in the Cape and the Orange Free State, to secure the right of registration of accountants in those provinces. The bill was referred to a Select Committee in August 1938 (SC, 12/38: 1). Allegations were made of unfair exclusion of the Institute of Accountants of South Africa’s members, from practicing rights in Transvaal and Natal, while the Cape and Free State Societies had admitted as members “accountants who had never passed an examination in accountancy” (SC, 12/38: 4–10; TES, 2257/526/1/F33/263/4). The 1938 bill lapsed because the session of Parliament ended. The bill was reintroduced in 1939, with yet another Select Committee appointed to consider further evidence (SC, 8/39). This time the most contentious issue was the use of the designation “Chartered Accountant”. In evidence before the Commission, the “Chartered” Societies were unmoved in insisting on the standard of their qualification as the basis for access to the designation (SC, 8/939: v). The bill was again discussed in the House of Assembly on 23 February 1940, but was terminated by the outbreak of the Second World War (Hansard, 1940).

The section above shows why the state became more proactive, in contrast to its former approach. Between 1910 and 1940 the accountancy profession attempted various strategies to secure professional closure. These were professional strategies to secure self-regulation and were intended to arrive at that goal without state intervention. Because of professional disunity, the 1912 and 1924 private members’ bills failed to proceed beyond the second reading in Parliament. The state did not intervene, but allowed subsequent strategic initiatives of the profession to entrench practising rights, through the establishment of the GEB and the passing of the Designation Act, to proceed. It was only by 1931 that the Minister of Finance started contemplating the possible wisdom of extending the TSA/NSA membership model to the rest of the Union. The state did not want to intervene. The state attempted to facilitate the intra-professional discourse by means of the commissions of inquiry to assist communication between the “Chartered” Societies and the increasingly assertive non-chartered accountancy associations. The state remained “a reluctant ally” of the accountancy profession, but by the end of the war, sentiments were changing. The state could no longer ignore the seemingly blatant discrimination against accountants in the non-chartered associations, so vividly exposed to the 1938 Select Committee, which constituted a refusal of practising rights in the Cape and the Free State to such accountants, where no statutory incorporation of the profession existed. The “Chartered” Societies closed ranks through the GEB and the Designation Act, but had to admit to the inconsistencies in earlier membership admissions in the Cape and the Free State.

Accountability and national interest: The contest for control, 1940-1951

Interdepartmental Committee on regulation of the profession

The war years were not idle years in the contest for professional positioning in South Africa. A steady stream of communication inundated the mailbox of the Minister of Finance at the Department of the Treasury. What distinguished the developments in the post-1940 period was that the state emerged as a proactive facilitator of statutory recognition of the accountancy profession. The state now emerged to intervene since professional contestation and disagreement compromised the “public interest”. In February 1945 the Minister of Finance wrote to the Secretary of the Treasury observing that while the accountancy societies were left to solve their own disagreements, they had failed to do so. He noted that the Auditor-General protected the interests of tax payers, the Registrar of Insurance and the Registrar of Banks protected the respective stakeholders’ interests and the auditor of a company protected the interests of the shareholders of a company. He stated: Many auditors are of the “tick-and-turn-over” variety and are dependent on Directors for re-appointment. This weakens their independence. Should not the Treasury be empowered to intervene in the interest of dissatisfied shareholders? Must the Treasury continue to remain aloof towards the registration of accountants? Please discuss the matter with Arndt and Beak

5

and let me have your prompt views on these two matters. (TES, 2258/9/349/2)

The Registrar of Banks, Arndt, suggested an interdepartmental conference to explore a proposed accountancy bill (TES, 2258/9/349/2). Arndt expected strong opposition but did not intend to hand down an authoritarian verdict. Instead, his aim was to facilitate a development in the interests of the entire country that had to deal with the difficulties arising from the transition from a war-time to a peace-time economy (TES, 2258/9/349/2). An interdepartmental conference in September 1946 considered whether the government should introduce legislation for the registration, qualification, designation and control of accountants and auditors. If so, should it follow on from the Pocock bill? Furthermore, should the Companies’ Act simultaneously be amended in respect of certain related matters? (TES, 2258/9/349). The conference was attended by representatives of the Treasury (Dr EHD Arndt 6 as Registrar of Banks and Building Societies and Mr H Beak as Registrar of Insurance); the Department of Justice (Mr CE Morris as Registrar of Companies); the Department of Commerce and Industries (Dr A Norval as Chairman of the Board of Trade and Industries); and the Department of Inland Revenue (Mr AM Slade as Commissioner of Inland Revenue). This high level public servants’ meeting agreed that “an undesirable state of affairs exists in the accountancy profession”, because of the Cape and Free State admission practices, which allowed incompetent persons to practice as accountants. In disciplinary matters it was feared the profession would be torn between the “desire to protect the public and a desire to protect its members”. Government departments were in their administration of various laws “compelled to accept certificates furnished by auditors and experience shows that some instances these certificates are unreliable”. Concern was expressed by the Minister whether the accountancy profession was in a position to discharge the important functions which ought, under modern conditions, to be entrusted to it. The committee felt that the Pocock bill should be the point of departure, but that the technical nature of the bill, the need to enlist suitable experience in the drafting process and a need for consensus in the profession, cautioned against overdue haste. The bureaucrats advised the Minister to seek suggestions from the profession on the contents of such a bill, rather than to force a Government solution (TES, 2258/F9/349/2).

The message was clear: the profession must pull together to agree on the content of the proposed new bill, but Government would take responsibility for submitting it to Parliament. This would be a public bill and not a private or hybrid bill. Failure to arrive at agreement among the accountants’ organizations would result in Government drawing its own bill (TES, 2258/F9/349/2). Taking the Pocock bill as point of departure, the Interdepartmental Committee wanted clarity on the following matters: the future of five separate and independent bodies responsible for the administration of discipline; whether negligence constituted adequate ground for disciplinary action; the exact definition of the duties of auditors; and the right of an unregistered accountant to practise occasionally or as a side-line. An interesting coincidence occurred in the course of the conference: notice was received that Societies in England had prepared a “Public Accountants Bill” (TES, 2258/9/349/2).

The change in the state’s approach to the self-regulatory statutory aspirations of the accountancy profession was illustrated by the Minister’s enquiry to the Clerk of the Assembly, Mr Ralph Kilpin, on the preferred source of such legislation. The Minister had embarked on a new course of action and needed confirmation that it was the correct one. He wanted to know whether the proposed bill should be a public or a private bill? Kilpin responded: Personally I have come to feel that it is one which ought to be tackled by the Government from the point of view of the public interest. … there is a good deal of ground for the contention that the proposed legislation should be regarded as more important from the point of view of the protection of the public interest than from that of the interest of the profession. (TES, 2258/9/345/2)

This opinion was fully endorsed by the interdepartmental conference. “Public interest” became the rationale for proactive state reversal of its former “hands-off” approach to direct involvement in the statutory regulation of the accountancy profession. On 27 November 1946 the Treasury publicly announced its intention to introduce a bill in Parliament providing for the registration, qualification, designation and control of accountants and auditors in South Africa. This was the first public admission of a change in state policy towards professional regulation and unity. The different societies and associations of accountants and auditors were invited to collaborate in preparing the draft legislation (Hansard, 1951: 4100; JC Minutes 2/12/46). The Joint Council (JC) had been informed of the press announcement in advance and immediately expressed its full support for such a public bill (TES, 2258/9/345/2).

Professional contestation and repositioning

In the next few months the “Chartered” Societies engaged actively among its own members and with other accountancy stakeholders to arrive at the most inclusive consensus position from which to submit a profession-wide endorsed draft bill to Treasury. Prior to the Treasury press release the four Societies of Chartered Accountants formed the Joint Council of the Chartered Accountants of South Africa in 1945 (hereafter “Joint Council”/JC) (JC, Memorandum of Understanding, 30/8/45). The JC informed the Minister of Finance of this development to show progress towards co-ordinated, unitary professional practice in the Union and a readiness to collaborate with the Government. The JC received the Treasury announcement with a sense of optimism. The chairman, Mr Frances Dix, said: “Now is the time for the South African Chartered Accountants’ Societies to pull together and present a united front” (JC, Minutes 2/12/46). The JC was prepared to depart from where earlier initiatives had stalled by considering the demands of the Institute of Accountants of South Africa and of the Association of Certified and Corporate Accountants for equal CA status with members of the Societies. The JC’s preferred point of departure was the 1934 bill, despite opposition against that bill and subsequent bills on accounting registration (JC, Minutes 2/12/46). The reason for this stance by the JC was that the 1934 bill provided for the registration of all accountants on a single Union Register of Accountants as RAs or “Registered Accountants”, while the Pocock Bill, favoured by the bureaucrats, opened the door to access to the CA designation to all the accountants who belonged to professional societies or associations that were party to the agreement on the bill. The Pocock Bill would therefore allow a “one-off” entry into the CA designation to accountants whom the Chartered Societies preferred not to gain access to such a designation. The scenario was now – could agreement on a negotiated one-time only concession be reached before the state enforced its threat of acting unilaterally under conditions of perpetuated professional disagreement?

Collaboration with non-chartered societies was not going to be easy. The “Chartered” Societies, named in the Designation Act of 1927, perceived themselves to be the gatekeepers to the profession of chartered accountants in South Africa. Mr Galbraith, representing the Cape Society, opposed the admission of the Institute of Accountants of South Africa to chartered rank “as this would put them on an equal footing and in view of their requirements would prove a waste of time” (JC, Minutes 2/12/46). The Natal representative, Mr Lance Horne, acknowledged correspondence between ACCA and the NSA, stating that the ACCA did not want the CA(SA) title, but only admission as a body of accountants to “a Union register and to be permitted to practise under their own designation … [and that] … any insistence that admission to a Union Register should be considered on an individual basis only would arouse strong opposition” (JC, Minutes 2/12/46). If agreement with the ACCA on admission to a Union Register as a body, rather than for its members as individuals, could be reached, it could strengthen the Societies of Chartered Accountants’ efforts to collaborate with other associations of accountants without compromising the CA(SA) designation. This route would give the chartered societies the opportunity to assess the professional ability of individuals as a condition for admission, rather than having to accept any person just because of their membership of an association. Admission of individuals would be a cumbersome process requiring accreditation of each individual’s qualifications and personal claims to a professional standard. Such a process would strengthen claims to the CA(SA) designation.

The debate in England on the Public Accountants proposed bill of June 1946 was also lingering in the minds of the JC. It was anticipated that “the provisions of the English Bill [would be] far-reaching and that the Union Government might use the English Bill extensively for any departmentally prepared draft … therefore we should placate the Association [the ACCA]” (JC, Minutes 2/12/46). The English legislation signalled attempts to bring different interests in the practising accountancy profession together under a single register of accountants licensed to carry on the practice of public accountants (Walker and Shackleton, 1995: 481). The potential warning light to the “Chartered” Societies was that a similar strategy could provide access to accountants who did not qualify for Society membership, to register and become licensed. The members of the Natal Society were keen on the 1934 draft bill, since “by adhering to the provisions of the draft Bill, outside bodies will, in time, die out” (JC, Minutes 2/12/46). The strategy of the “Chartered” Societies was to be in control of the unfolding process of statutory recognition.

If the “Chartered” Societies wanted to entrench their privileged position to the exclusion of other contending accountancy associations, they risked the support of the Government. The proposed extended inclusivity in the English draft bill might echo in the South African environment if the process leading up to the new legislation called for by the Treasury was not inclusive. The JC therefore agreed to consultation with the other “bodies of accountants” if the Societies wanted to dispel the idea that the other bodies “were fighting for the rights of South Africans against foreigners” (JC, Minutes 2/12/46). The notion of “South African” or national interests, as opposed to foreign interests, emerged as an important consideration for the sustained recognition of the Societies’ professional leadership and designation. The possibility of securing access to the South African CA designation by foreigners who had passed examinations in Britain, or to “any other outside bodies”, was of grave concern to the Select Committee in 1938 and 1939 (SC, 12/38: 32; SC, 8/39: IV). This is the “there” and “here” notion that Chua and Poullaos (2002: 431) observed in the emergence of an imperial professional milieu during the first decade of the twentieth century. The JC called, for the first time, for statistics on “South African-born members and clerks”.

To maintain the initiative the JC then called a conference in Bloemfontein in April 1947 of the following bodies “which we are aware have been approached by the Union Government”: The Joint Council of the Societies of Chartered Accountants of South Africa (2,062 members); the South African branches of The Society of Incorporated Accountants & Auditors (520 members), the Association of Certified and Corporate Accountants (104 members), the Institute of Accountants of SA (106 members), the Association of Practising Accountants of SA (54 members) and the Institute of Administration and Commerce of South Africa (JC, Minutes 2/12/46; TES, 2258/F9/349/2/: Letter 5/8/47, Letter 24/2/47). The JC position on the draft bill of 1934 as the point of departure was reaffirmed. The 1934 bill had provided for statutory registration of all accountants, designated “Registered Accountant and Auditor”. In addition to such registration, an accountant would use the designation of his own Society or representative body. None of the existing organizational bodies would cease to exist, with each maintaining its own by-laws and administration of its members. Generic registration of all accountants as “RAs” did not compromise the CA(SA) designation and preserved the Chartered Societies’ “gate-keeper” status. The Association of Practising Accountants of SA (APA) objected to the 1934 draft bill, because they insisted on admission to the Chartered Societies. They refused to reconsider their view and left the Conference (TES, 2260/9/42/3). Mr M Edward, Secretary of the JC, noted that the APA’s continued presence might just have affected the “Spirit of harmony which otherwise prevailed throughout” (TES, 2260/9/42/3: Letter JC – APA, 23/4/47). When the consensus proposals of the joint conference of accountants in Bloemfontein were communicated to the Minister, Beak reaffirmed the Treasury’s non-interventionist stance (TES, 2260/9/42/3).

The accountants understood that state intervention would indeed emerge should the profession fail to act in unison. The new dimension to the discourse on statutory regulation of the accountancy profession in South Africa was this reluctant, though reservedly controlling, position occupied by the state. A slow but thorough process of careful consideration of the Bloemfontein bill followed until the Treasury informed the JC in February 1948 that the draft submitted “was not in the public interest … [since] as a Public Bill, it makes insufficient provision for the protection of the public interest” (JC, Minutes 5/8/48; TES, 2260/9/42/3). The Treasury expressed its concern that the profession had not adequately provided for the fact that their draft bill was no longer a “private” bill but a “public” bill. Two serious shortcomings threatened the “public interest”: unqualified persons in public practice, as well as unlimited powers to unqualified persons to sign audit certificates when large sums of private or public money were involved (TES, 2257/9/42). The “public interest” was to be addressed through the thorough definition of an auditor, his qualifications, powers, duties and responsibilities. These proposed amendments would be discussed with the “framers of the original draft” (JC, Minutes 4+5/8/48).

The deliberations in the Interdepartmental Committee offer an understanding of the concerns and objectives of the state. First it was the issue of profession-wide support for the bill – “ … and the object is to frame provisions which will allow the largest measure of acceptance by the Accountancy Profession, compatible with the public interest” (TES, 2260/9/42/3). The extensive correspondence with the Minister, dating back to 1946, from accountancy organizations excluded from the mainstream Societies claiming legitimate standing, were noted. These included the Institute for Administration and Commerce, the Institute of Certified Bookkeepers of South Africa, the South African Branch of the Certified and Corporate Accountants (ACCA), the Institute of Cost and Works Accountants, the Society of Incorporated Cost Accountants, the Practising Accountants Guild Limited, the Association of Practising Accountants of South Africa and the Association of International Accountants Limited (TES, 2260, 1947–1949). These claims were based on long-term public experience, recognition in other countries, reputable examinations passed, de facto public practice and recognition, and the good character of members. In considering these submissions carefully, Arndt reiterated that the Government was not “throwing the doors wide open to all and sundry” nor succumbing to the pressure of “less reputable societies”, but that the proposed bill “seemed more designed for the purpose of consolidating the privileged position of the Accountancy profession”. Since the proposed legislation was to be a public bill, “it should provide primarily for the public interest” (TES, 2260/9/42/3). There was concern about the strong privileged position of the “Chartered” Societies and their right to sanction and register articled clerks and administer discipline, as well as the perpetuation of “unqualified” accountants and an exact definition of the powers and duties of auditors. The reference to “poor audits” in the first Interdepartmental meeting pointed to a concern about the ability of the “Chartered” Societies to act independently and discipline members in cases of negligence or misconduct.

The state as protector of “the public interest”

An intense period of drafting and re-drafting followed in which the state considered submissions by a wide representation of accounting associations and stakeholders. The first Treasury re-drafted bill was available in November 1949 for submission to “the framers of the original draft, for discussion”. The main features of the amendments were the definition of an auditor’s rights and duties (protection from unfair dismissal and action for defamation) and the establishment of a central controlling authority – the Accountancy Board. This Board would be in the hands of the profession itself, but subject to safeguards of the public interest by means of representation of “at least” four senior public servants. This bill was seen to “constitute new conceptions in legislative control of this nature, both here and overseas, and it would be advantageous to obtain the largest possible measure of support for these provisions from the organized profession before submitting the Bill to Parliament” (TES, 2260/9/42/3). The “public interest” from the perspective of the state was addressed by the specific attention to the auditor and the introduction of public sector representatives to oversee the regulation of the profession in collaboration with the accountants.

When the JC received the “Auditors’ Act, 1950” in November 1949 and the Interdepartmental Committee resumed their activities in September 1950, the South African political landscape had changed. The National Party of Dr DF Malan was in power. However, the political changes were hardly felt in the Interdepartmental Committee: Mr Wells was the Commissioner of Inland Revenue, Dr Arndt still the Registrar of Banks and Building Societies, Mr Beak still the Registrar of Insurance, Mr Morris still the Registrar of Companies, while Prof Steenkamp attended as the Chairman of the Board of Trade and Industries, Mr Horrocks represented the Office of Co-operative Societies and the Treasury had a new Secretary in Mr J van Wyk (TES, 2260/9/42/3). A high degree of continuity in representation of public servants was instrumental in facilitating progress in this matter.

The JC was grossly dissatisfied with the new bill, the “Auditors Act, 1950”. Professor Galbraith, Chairman of the GEB, criticized it for insufficient control of the “whole profession of accounting … there should be regulation of all professional duties” (TES, 2260/9/42/3). The focus of the draft reflected the preoccupation with efficient and qualified auditors in the country at the first meeting of the Interdepartmental Committee in 1947. There were talks of reverting to a private bill again. The Secretary of the JC called the new bill “fundamentally different” from the professions’ submission, “fundamentally unsound and wrong in its conception of the practice of accountancy and auditing” (JC, Minutes 2/2/50).

The Joint Council concerns were:

The new proposals by Treasury suggested statutory control of auditors only, while the accountancy profession covered a variety of work and services to the public which extended well beyond only auditing. “In the mind of the public the word ‘Accountant’ is associated with a person well qualified in accounting matters and a person who, because of such qualifications, has attained a prestige higher than that of a bookkeeper. It is not in the public interest that the title ‘Accountant’ should be used by unqualified persons and the Bill should provide a measure of protection” (JC, Minutes 2/2/50). This opinion was reiterated by the Accountancy Profession Commission of 1934 and the JC intended to take a firm stand to sustain it.

The JC insisted on recognition of the four Societies of Chartered Accountants and the Designation Act (1927), but that the opportunity should be granted to members of the other associations in the Union to qualify as Chartered Accountants.

The JC was also dissatisfied with the proposed composition of the Public Accountants’ and Auditors’ Board. A majority of members would be government officials and persons not actively engaged in the profession. Edmund, Secretary of the JC, stated: “My council knows of no other profession controlled by a combination of government officials and other persons not actively engaged in the profession. It should be stressed that no rights conferred on a minority are equivalent to control” (JC, Minutes 2/2/50). The independence of the accountancy profession was at stake. The JC called upon the experience of the regulatory operations in the United Kingdom to reject the proposed government bureaucratic control.

The JC took an unequivocal stance on admission into the profession. The Treasury proposals hinted at the acknowledgement of practical experience of “long standing”. The JC insisted that the principle of admission after completion of service under articles of clerkship, and passing of examinations, including a final qualifying examination set by the Accountancy Board, was non-negotiable.

Finally, the JC insisted that the existing rights and duties of accountants and auditors be honoured. These included the preservation of the existing confidentiality relationship between client and accountant. It rejected statutory compulsory reporting of information about irregularities identified in the accounts of clients. Such disclosure was a contravention of the confidentiality rule.

Whereas a relationship of mutual respect and collaboration had characterized the collaboration among members of the accountancy profession since the initiatives commenced to introduce a public bill on the recognition, regulation and control of the profession, suddenly this seemed in jeopardy. A deputation of the JC met with Arndt, Beak, Morris and Van Wyk on 9 January 1950 to request serious consideration of the objections raised, as well as that the CA(SA) designation should not be replaced by a generic “Registered Accountant and Auditor” title. These submissions were received in a “spirit of candour” (TES, 2260/9/42/3: 9/1/50). Widespread consultation followed. The Treasury consulted with members of the Interdepartmental Committee as well as Attorneys-General in various locations, and particularly on the matter of disclosure of irregularities by auditors. On the last matter widespread support was expressed for the proposed obligation of auditors to report such conduct (TES, 2260/9/42/3: 17/2/50). The JC called conferences in March 1950 to meet with representatives of the Society of Incorporated Accountants and Auditors, the Institute of Accountants of South Africa Ltd, the ACCA (SA Branch) and the Institute of Administration and Commerce of SA (JC, Minutes 15/3/50; 17/3/50). A subsequent meeting took place with the Minister of Finance later in March 1950 (Ministerial Conference, 1950). Consultative meetings in Cape Town on 23 and 24 November 1950 finalized details of the draft bill and on 12 February 1951 the Public Accountants’ and Auditors’ Bill, No. 51 of 1951, was introduced in Parliament (TES, 2260/9/42/3: 24/11/50; Hansard, 1951: 12/2/51). Promoters of the legislation, that is the Interdepartmental Committee, repeatedly expressed satisfaction on the inclusivity and comprehensive nature of the process. When introducing the Bill in Parliament the Minister noted that it was not the intention to create a monopoly of any class whatsoever but to open the profession to all persons complying with conditions set out in the bill (Hansard, 1951: 12/2/51: 4101).

The state’s concern about the potential risks from the public practice of unqualified accountants and auditors, as well as the growing public expression of dissatisfaction among accountants excluded from privileges reserved for members of the four “Chartered” Societies, gradually resulted in a policy shift at the Treasury. The almost passive acceptance of the principle of professional self-regulation of the accounting profession by the state until the mid-1930s was replaced by a proactive state involvement in the professional closure strategy of the profession. The state noted potential threats to the public interest, here referred to as the interests of private shareholders in public companies audited by unqualified accountants and auditors. It also referred to the protection of the public against possible risks that may arise from the conduct of unqualified accountants and auditors that may impact on public expenditure and taxation. Since the state felt that the interest of the public was protected by the work of the Registrar of Banks, or of Insurance, or the Commissioner of Inland revenue or the Registrar of Companies, the state had the responsibility to introduce similar regulation of accountants and auditors to safeguard private and public money.

The 1951 Act

The urgency on the side of the state was illustrated by the fact that the PAA Bill was introduced in Parliament in the House of Assembly on 12 February 1951, where it was read for the first time. Then the unique intervention occurred: the bill was expedited by referring it directly to the Senate, because the Senate had time to consider the bill as a matter of urgency. Amendments were made during the committee stage and read for the third time on 11 June 1951 (Hansard, 1951: various months: 482, 2350, 4099, 9376). This was the only way the bill could pass a third reading before the end of the parliamentary session in June 1951.

The 1951 PAA Act gave statutory regulatory capacity to non-accountants – a first in the imperial accountancy arena. This was an important concession the “Chartered” Societies had to make in order to secure some form of professional closure. The Public Accountants’ and Auditors’ Board (PAAB) was a statutory body entrusted with the registration of accountants and auditors in South Africa, based on compliance with requirements for examinations and articles of clerkship of trainee professionals (Sec 3). Section 3(1) explains the composition of the PAAB. Four representatives of government were appointed by the Minister of Finance. The four members were selected from the following government offices: the Commission of Inland Revenue, the Chairman of the Board of Trade and Industries, the Registrar of Co-operative Societies, the Registrar of Companies, the Registrar of Insurance and the Registrar of Building Societies. The Minister could appoint the four representatives of Government from the designated positions, or individuals “in any other capacities in the full time service of the state where in the opinion of the Minister they are in the performance of their duties concerned to a considerable extent with certificates furnished by accountants or auditors” (Sec 3(1) (a)). Furthermore, two professors or lecturers in accounting or accountancy matters at any university in the Union would serve on the Board (Sec 3(1) (b)). The first six members of the PAAB represented the state and were seen to represent the interests in society, but outside the profession, that were most directly affected by the conduct of the profession. A majority of 11 members on the PAAB represented the professional organizations of accountants. Section 3(1) (c) authorized each “Chartered” Society to nominate one member, and an additional member if the Society’s membership exceeded 250. The Society of Incorporated Accountants and Auditors could also nominate one person to represent all the members in the branches of that organization in South Africa (Sec 3(1) (d)). To be inclusive the following organizations could nominate one representative to the PAAB: South African branches of the Association of Certified and Corporate Accountants of South Africa, the Institute of Accountants of South Africa Ltd and the Association of Practising Accountants of South Africa. Although the legislative process at the time of the PAA Bill going to Parliament had been inclusive as never before, there was still vigorous debate in the House of Assembly about the explicit exclusion of the members of the Society of Commercial Accountants (South African Branch) from the Accountants’ Register (Hansard, 1951: 4112, 4125, 9333–9334). The members of that society were looked upon with little appreciation or recognition. One member remarked that it had been said that the Society of Commercial Accountants had admitted members without requiring the successful completion of examinations, and that they “sold” titles! (Hansard, 1951: 9334).

The PAA Act incorporated the fundamental professional requirements as developed, enforced and administered by the “Chartered” Societies for registration and qualification as accountants in South Africa. The PAA Act introduced a two-tier process of registration. First an Accountants’ Registration Advisory Committee (Section 13) was appointed to consider all applications for registration of accountants and auditors in South Africa on a single national register. Within 18 months of the promulgation of the Act, all accountants and auditors in South Africa had to register accordingly. The Advisory Committee considered all applications, including “contentious” ones, that is applications of accountants who were not members, or eligible for membership, of the four “Chartered” Societies. The window of application closed after 18 months. The second tier of the registration process was to establish a separate register for articles of clerkship (Sec 24). The regulation of articles of clerkship and determination and administration of fees for the registration of articles of clerkship and accountants and auditors were paramount functions (Sec 21(1) (a) (b) (c)). In the past serious contention existed on the right of non-chartered accountants to contract clerks as well as the duration of such contracts.

The first national Register of articled clerks and of qualified accountants and auditors included persons who qualified in terms of Section 23, that is, all accountants practising in South Africa who were 21 years of age or older, who were ordinarily resident in the Union of South Africa, had served under articles of clerkship for a period of five years (university graduates were granted two years’ exemption), and had passed the prescribed examinations (Sec 23(1) (a) (b)). The act also provided reciprocity to accountants and auditors formerly registered with reputable professional societies. Explicit reference was made to former “members of good standing” or those who had qualified to become a member of one of the recognized professional accountants’ societies. This was clearly a concession extended to accountants in South Africa who practiced outside the “Chartered” Societies’ privileged domain. This provision thus recognized foreign-trained (e.g. British-trained) accountants’ qualifications if these qualifications were obtained from “reputable professional societies”, but it did not waive the residency requirement or the requirement that such trained accountants had to comply with the training in practice requirement (completion of a prescribed period of articles of clerkship under a CA(SA) principal) and the requirement that such an accountant pass an examination on South African law.

Full responsibility for the examination of qualifying accountants shifted to the PAAB. The entrenched GEB control of education and qualification standards was terminated and transferred to the statutory body. The PAAB was given sole responsibility for arranging examinations for articled clerks (Sec 21(1) (e)) and for prescribing degrees, diplomas and other qualifications which would entitle persons to register as accountants and auditors (Sec 21(1) (d)). Section 25 of the PAA Act authorized the Board to prescribe the qualifying examinations. The GEB was instructed to deliver all documents pertaining to examinations to the PAAB. The PAAB could arrange examinations to be concluded on its behalf by any “one or more universities or institutions approved by the Minister” (Sec 25(2) (3)). The PAAB could also grant exemptions to persons qualified overseas, provided a paper on South African law was passed (Sec 25). These exemptions illustrated the broad intention of Government to acknowledge de facto practising accountants and auditors beyond the original limited professional chartered societies recognized in the 1934 Accountants’ Bill. Persons who qualified as accountants were by this Act “entitled upon application to be admitted to membership of that society” (Section 29(1)). Statutory oversight of examinations represented a fundamental break with the Societies’ conception of their right to examine, credential and license. The only consolation for the “Chartered” Societies was representation on the PAAB. In fact the Chartered Societies had only seven representatives on a Board of 17 members. Depending on the nature of the relationship with the representatives from universities, chartered accountants might be able to count on the principled support of universities, but not necessarily from the four government officials. University professors were in principle expected to be ad idem with the chartered societies’ on training requirements and accounting standards, since the GEB collaborated with universities in administering professional examinations. The chartered societies had also paid subventions to universities since 1912 to ensure good teaching of accountancy and related material to students. Government officials were not necessarily professional accountants, since non-accountants were appointed to the office of “Registrar of Companies” or “Registrar of Building Societies”, etc. The chartered societies’ closer allies were the representatives of the branches of foreign accounting organizations in South Africa, who finally gained some official recognition.

The most contentious provision in the PAA Act was Section 26, which set out the powers and duties of auditors, emphasizing the conditions for issuing an unqualified audit certificate. Standard principles of auditing applied, but the thorny issue was Section 26(3), which required an auditor detecting “material irregularity” to report such conduct to the person in charge of the audit, who was obliged to report the matter to the PAAB. Strong criticism in Parliament (Hansard, 1951: 4127, 4137, 4140) was finally defeated in a majority vote. The opposition argued that such a measure infringed upon the professional conduct and confidentiality between the auditor and the client. The professional responsibility of accountants and auditors to report inappropriate practices or misrepresentation in financial statements was conceded, but not the procedure to report on such matters to the PAAB. By not issuing an unqualified audit certificate, it was argued, the accountant had publicly declared the existence of inappropriate conduct. A further report to the PAAB exceeded professional responsibility and could place the audit firm at risk of losing the contract (Hansard, 1951: 4405–4420). The representatives of Government argued that it was in the interests of shareholders and the public to be notified of irregularities. To issue a qualified audit certificate was deemed insufficient (Hansard, 1951: 4424). The concerns expressed at the first meeting of the Interdepartmental Committee on the quality of audits hinted at strong state intervention on this matter.

The PAA Act forbade the transfer of professional fee income or profit sharing with persons registered as accountants or auditors, or practising as accountants or auditors outside the Union. Accountants and auditors were not permitted to practise under the name of a firm which included the name of a person “who is not or was not during his lifetime ordinarily resident in the Union” (Section 30). Foreign accountants were given three years to either take up residence in South Africa or terminate their relationship with the profession there. In Parliament the Minister stated that he was not unmindful of the contribution made by “overseas firms to the economic life of the Union”, but that “certain overseas firms with branches in the Union have been using undue influence to obtain work for their South African branches” (TES, 2257/9/42/1). The Act was intended to “place [accountants and auditors] on a sound basis, comparable with the best in overseas countries. South African accountants will, I believe, have a status that will be universally recognised. We will not be dependent on the recognition enjoyed by overseas firms as we will be able to stand on our own feet” (TES, 2257/9/42/1). The state stepped in to protect national interest, whereby the local accountants’ professional closure strategy benefitted.