Abstract

This study provides a systematic overview of financial statements appearing on nineteenth-century temple stelae (alternatively called steles or stone tablets) culled from ten local collections of stele inscriptions from South China and Taiwan. Furthermore, it presents an analysis of the significance of these stele inscriptions for the study of Chinese accounting history in general, and particularly in respect to the influence of Chinese religion on accounting. Confirming “accounting stagnation” in the late Qing period, the temple stelae provide evidence of the increasing importance of wealth, against the alleged oppositions between trust and written contracts, and religion and money, in late Imperial China. As the impact of Chinese religion on the history of accounting is largely understudied, the final section contains proposals for further research.

Keywords

Introduction

During the last couple of decades, the epistemology of accounting has changed from a technical to a “social and institutional practice, one that is intrinsic to, and constitutive of social relations” (Miller, 1994: 1). As a result, many studies have attempted to point out specific cultural concepts underlying fundamental differences in accounting systems between societies. Studying “accounting cultures” rather than “accounting practices”, these studies set out to “identify a set of specific societal values or cultural factors which are likely to be directly associated with accounting practices” (Askary, 2006: 6; citing Perera, 1989: 43). Within this framework, the cultural models conceived by Gray (1988), Hofstede (2001) and Perera (1989) have proved highly popular. 1

Aiken and Lu (2004: 48) have pointed out that numerals were “among the earliest Chinese characters to have been invented”. According to these authors, counting played an early and significant role in the evolution of Chinese writing systems. Unsurprisingly, China’s accounting culture is among the oldest in the world, dating back to the Zhou dynasty (1100–771 BCE). During its history, which is extensively described in the literature (Aiken and Lu, 1993, 1998; Guo, 1988; Lin, 1992; Zhao, 1992), Chinese accounting evolved from the single-entry bookkeeping methods of the Zhou, maturing to double entry accounting in the eighteenth century. Aiken and Lu (1998) have pointed out that this evolution was a result of cultural, economic and technological influences. Within this framework, China has been portrayed as “a splendid case for the explanation of the ties between culture and accounting as China has a long history and a unique culture” (Gao and Handley-Schachler, 2003: 42). 2

In contrast to the eighteenth century, and in spite of the advent of superior bookkeeping methods 3 from the West around 1840, an “accounting stagnation” (Auyeung, 2002; Auyeung and Ivory, 2003) persisted during the second half of the nineteenth century in China. This stands in stark contrast to Japan which, under similar circumstances, quickly adopted Western accounting practices. In China, commercial law and government accounting were only formalized during the reforms of the early twentieth century, and Auyeung and Ivory (2003: 20) have therefore taken the Weberian stance that “Chinese enterprises operated in a political, economic and socio-cultural context where, in the name of ‘harmony’, capitalism was systematically repressed”. Identifying Confucianism, “Feng Shui”, and Buddhism as major constituents within this cultural framework, Gao and Handley-Schachler (2003) have shown how these socio-religious elements have influenced all aspects of traditional Chinese accounting practices, namely accounting information, accounting regulations, the accounting profession and accountants, government accounting, and private accounting. Bloom and Solotko (2003) have similarly noted the Confucian cultural foundations of Chinese and Japanese accounting.

The current study concerns the nineteenth century, specifically the late Qing period, which is commonly recognized as the transitional period from pre-modern to modern China. During the pre-modern period, the social structure of China gradually changed because of increasing commercialization and industrialization, and its political and social foundations were shaken by the rebellions that raged throughout the century, culminating in the Taiping rebellions of the 1850s and 1860s. China’s last dynasty received another major blow when the Opium Wars (1839–1842 and 1856–1860) were lost and the nation had to open its ports to foreigners. Furthermore, Qing China was forced to formally cede Hong Kong to the British in 1842, Macau to the Portuguese in 1887, 4 and Taiwan to the Japanese in 1895. The second part of the nineteenth century saw not only an intensified commercialization, but also mechanization, and the inflow of weaponry and Western ideas into China. However, it was not until the outbreak of anti-foreign riots in 1900 that the Chinese government implemented a rigid reform policy, including the abolition of the examination system, which for centuries had been the only generally available, legitimate access to elite status, and the introduction of Western-style schools and chambers of commerce (Esherick and Rankin, 1990: 14).

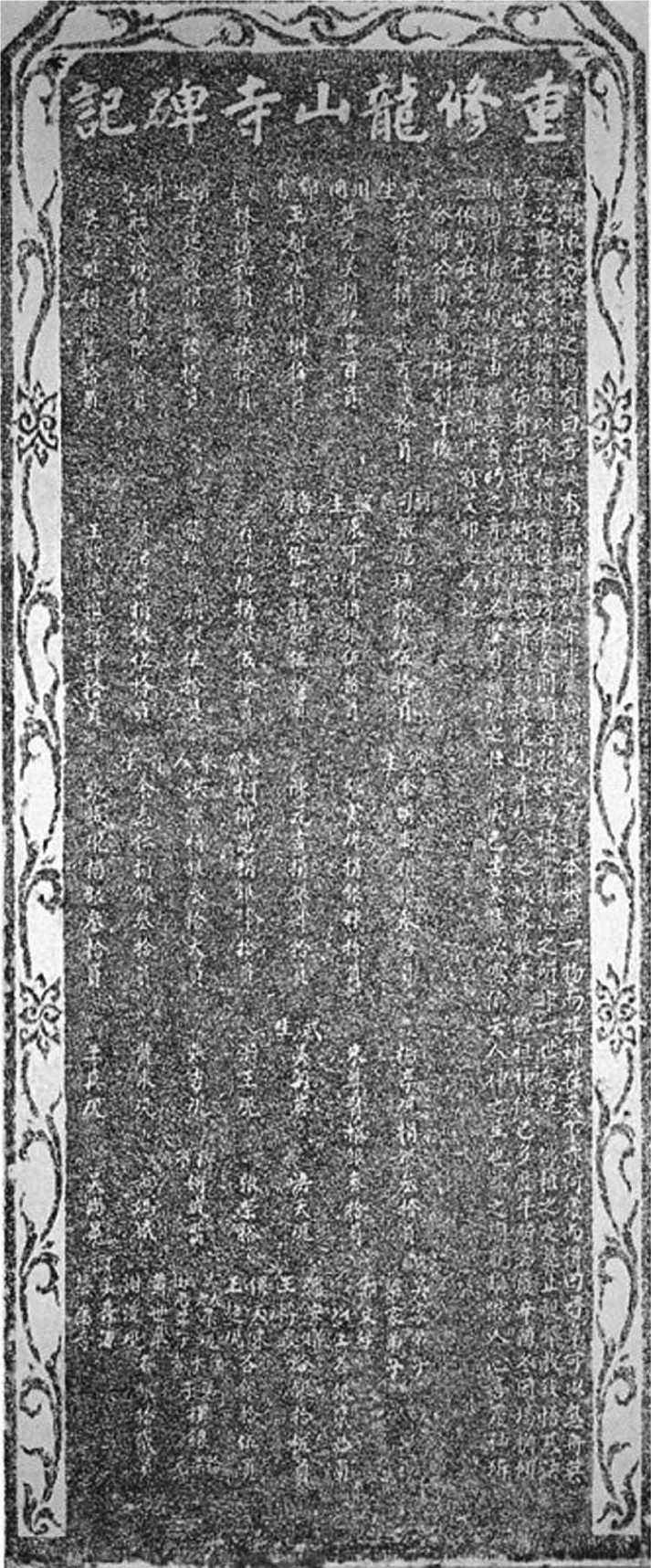

In his comparative studies of the accounting cultures in nineteenth-century China and Japan, Auyeung (2002: 3) states that “little is known about the relationship between socio-cultural change and the development of accounting in China and Japan”. The research reported in the current article provides further evidence of the relationship of socio-cultural change and accounting development in the form of financial statements published on temple stelae. As a “quintessential Chinese monument” (Wong, 2004: 44), the stele has long been recognized as an invaluable historical source. On public display at practically all temples, these stone slabs containing carved inscriptions and images served both as mediums to express pious devotion and as legal documents (Goossaert, 2000: 28). The wide array of literary genres that was published on stelae embraced text genres as different as Confucian, Taoist and Buddhist canonical texts, official documents, contracts, biographies, poems, commemorative texts, lists of names and calligraphy, as well as maps and diagrams (Katz, 1999: 95f.). Among these types of texts, the intertwined economic and religious dimensions of accounting are particularly obvious on the so-called “commemorative stele”. As Katz (1999: 100) has pointed out, the major function of these stelae consisted of describing “major events marking the history of this temple, especially various construction and reconstruction projects”. In so doing, they also conventionally included exhaustive lists of donors. The basic structure of these stelae can be seen on the Taiwanese stele depicted in Figure 1. 5 Surrounded by an ornamental flower design, the inscription contains a sizable title, a short account of the history of the temple and the renovation measures (right-hand side), and a list of donors and donations (larger line spacing), which takes up the largest part of the space.

“Stele inscription of the renovation of the Longshan Temple” (schematic), Mount Fengshan/Southwest Taiwan, 1807. The temple is dedicated to the bodhisattva Avalokitesśvara, although, as usual in Chinese religion, various gods are worshipped there. (Source: TJ)

The nineteenth-century convention of inscribing financial statements on stelae allows for an analysis of popular accounting methods during this period in China. By analyzing a sample of financial statements from South Chinese stele inscriptions, this study firstly presents new evidence of management and accounting practices that were at work in the realization of public tasks during the late Qing period. Secondly, it puts into perspective previous statements about the cultural framework of traditional Chinese accounting practices. As a result, the inscriptions also contain evidence that, by the nineteenth century, major Confucian elements had loosened their grip on the accounting culture in China. Furthermore, the aversion toward accounting within Chinese religion proves questionable. These findings suggest that the cultural framework of traditional Chinese accounting was much less static than has been portrayed in previous studies.

In the next section, the role of the temple and the commemorative stele in shaping accounting practices within Chinese religion are introduced. In order to understand the socio-economic framework of financial statements on nineteenth-century stelae, the third section discusses the social groups that erected those stelae, as well as their involvement in public tasks during the late Imperial period. The fourth section contains a corpus analysis of 80 financial statements on stele inscriptions from four South Chinese regions. In the fifth section, the implications of these accounts are examined in light of previous studies on traditional Chinese accounting and management practices.

The cultural framework: The temples of Chinese religion and the commemorative stele

Auyeung (2002: 2) has defined the “cultural framework” of accounting as follows: “The term ‘cultural framework’, when applied to accounting, designates the particular set of institutions in a society which, while remaining an integral part of the larger culture, represents those aspects of general social life which are most influential in shaping the course of accounting activity”. While socio-religious institutions such as temples and commemorative stelae cannot be said to be “most influential” for Chinese accounting culture in general, they nevertheless played a decisive role within the more narrowly defined accounting culture of Chinese religion.

Based on the foundation of the “three teachings” (sanjiao), that is, Buddhism, Daoism and Confucianism, Chinese religion is much more inclusive than the Western concept of religion suggests. 6 Although each of these teachings had its distinct set of clergy, canon, liturgy and centers, according to Vincent Goossaert (2007: 7) their role was “to transmit their tradition of practice and make it available to all, either as individual spiritual techniques or as a liturgical service for families or whole communities”. As such, Chinese religious communities chose independently from among “the shared repertoire of beliefs and practices and the services offered by the Three Teachings and their clerics” (Goossaert, 2007: 7).

There were, and still are, two categories of Chinese temples. First, a small, yet at times very influential number of monasteries were run by the clergy of institutionalized Buddhism or Daoism. The second much broader category was made up of temples to national or regional saints and gods. While some of the latter temples were also managed by clerics, most were under the purview of lay communities of lineages, territorial, professional and congregational groups (Goossaert, 2006: 28). These were the cult venues of the social groups that constituted the building blocks of late Imperial society and, as Faure (2007: 232) has noted, “The fault lines of late imperial China’s social structure were drawn, not between the scholar, farmer, artisan, and merchant, as the occupational orientations of the imperial subject might instruct the historian, but across territorial groups, defined by settlement rights, lineage and territorial affiliations, incumbents, and outsiders”.

Another characteristic feature of Chinese religion is the dispensability of clerics within its temples. Indeed, as Goossaert (2006: 29) has argued, only a minority of temples were inhabited by clerics. Instead, temples were owned by “the family, or community, or institution that was responsible for the last (re)building”. In this context, lay communities resorted to temple stelae not only as a symbol of their religious devotion but also to mark, and defend if necessary, their ownership rights.

Stele inscriptions conferred symbolic capital and played a decisive role in the “cultural nexus of power”, that is, “the symbols and norms embedded in networks and organizations” that legitimized leadership (Katz, 1999: 97). This fact has been illustrated by Walsh (2010: 115f.) in his description of the erection of a stele recording a land donation to a Buddhist monastery: Erecting a stele was an expensive and lengthy process involving many people … When a stele was erected people knew what it was even if many could not read it … People within the surrounding social arena knew something important had occurred … Someone was hired to write the inscription; stone cutters were needed; calligraphers were involved; the abbot made the decision; and the satisfaction of the donor had to be verified. Most important, in due course, others in the same sociopolitical field, in the same social arena as the donor, would learn of such a donation.

The stele referred to in the above quote involved a commemorative inscription marking the historical event of an endowment of land. For all parties involved, as Susan Naquin (2000: 60) has noted, such a stele “allowed for long-lived expressions of status, piety, and influence”. For that reason, the inclusion of individual names, which often make up the largest part of the inscription, has a long history.

In China, the publication of individual donations on commemorative stelae is a centuries-old tradition reflecting the socio-economic conditions during successive dynasties. This is visible in early instances of the pictures of donors on commemorative stelae from the Northern Wei (386–534). As Wong (2004: 43) has shown, as a result of political and economic consolidation, as well as government patronage of Buddhism, lay Buddhist societies were the first to set up “monuments commemorating the collective groups’ religious, social, and territorial identity”. It is important to note that these societies, as well as the stelae they erected, were “Buddhist adaptations” (Wong, 2004: 44) of socio-religious practices that were already well entrenched at the time. As such, the internal structure of these societies “mirrored the social organization and bureaucracies of local communities” (Wong, 2004: 69). By using commemorative stelae to record individual merit, 7 Buddhist societies established a tradition that lasted throughout the Imperial period. Notably, the representation of donors, initially by means of pictures, later increasingly via personal names, as well as the inclusion of quantified donations, in money or in kind, had become integral features of the commemorative stele (Wong, 2004: 69f.).

These traditions still thrived during the late Imperial period (1368–1911), as can be seen in Naquin’s (2000: 712ff.) study of a collection from the Beijing area. Naquin collected detailed information on donations from around 1420, the year when the city became the capital of the Ming Empire, until the dynastic decline in 1911. Within her collection, changing patterns of donors and donations can be discerned between the late Ming (mid-sixteenth century to 1644) and the Qing (1644–1911). While up until the middle of the eighteenth century the large majority of donors were connected to the Imperial court, including members of the Imperial household, eunuchs or officials, donations after that time came predominantly from individuals and “religious associations”. 8 Furthermore, as Naquin (2000: 63) points out, in the seventeenth century donations were made both in silver and in land, whereas in the ensuing century they were generally made in silver and copper currency. It is also worth noting that throughout the Qing, “lodges and businesses [in their function as donors] were more likely to list the amounts of the donations than were other associations” (Naquin, 2000: 60, n. 11).

As such, temple constructions and renovations were excellent opportunities to stake ownership claims. From the late eighteenth century onwards, commemorative stelae were put up by groups of persons that mostly called themselves “managers” (dongshi) or “gentry managers” (shendong). These stelae were erected by the management of the different types of lay communities, that is, lineages, territorial, professional and congregational groups. The persons that set up these stelae were the managers of the respective investment project. The costs for its production and carving were usually included in the list of disbursements, indicating that the setting up of a stele was an integral part of the project. As these persons put their signatures, and of course also their titles (if they possessed them) at the end of these inscriptions, ideas concerning the make-up of boards of managers in nineteenth-century China are revealed. Such an analysis presupposes some knowledge of the local elite in Qing China. Traditionally, these elites were headed by the “gentry”, which comprised those that aspired to or had already passed the examination system that qualified them for official appointment. Following Chang (1967), the gentry can be meaningfully divided into upper and lower gentry, where the upper gentry had successfully passed examinations for office and the lower gentry had either passed preliminary examinations or purchased official titles. As a result of the limited availability of government posts, the upper gentry numbered only some 125,000 people as opposed to the 860,000 members of the lower gentry. Together, they accounted for about 1.3 percent of the total population (Esherick and Rankin, 1990: 4). Holders of honorary titles such as “village elder” (qilao) or “guest of honor at the village banquet ceremonies” (xiangyinbin) had a more ambivalent status. Although these titles, mostly bestowed on men above 60 years of age, did not confer gentry status, their holders were nevertheless legally “distinguished from the large mass of commoners” and held a special place at official ceremonies (Chang, 1967: 15ff.).

These boards of managers were indicative of socio-economic changes that became visible in the early years of the dynasty, maturating during the eighteenth century. They resulted in the transformation of local elites, notably in the growing visibility and influence of merchants. This transformation, as well as the significance of the public tasks of these elites, is outlined in the next section.

Merchant involvement in public tasks in late Imperial China

In his study of the “organizational forms” that were conceived to maintain the waterways that were of vital importance to the Jiangnan economy, Elvin (1977) observed an organizational change that took place in Shanghai during the final years of the eighteenth century. After a period of experimentations with different official and non-official management practices, “the gentry emerged as the accepted directors of all hydraulic projects not so large as to demand special organization by the government” (Elvin, 1977: 463). Tellingly, the official recognition of the boards of managers in Shanghai in 1775 almost coincides with the earliest financial statements within our sample.

From the Tang Dynasty (618–907) through to the Qing, China experienced a massive population increase which was not matched by a similar expansion of bureaucracy. Only by relying on a very limited number of local officials could an agrarian state impose and collect taxes, while keeping its local representatives in check. As a result, the government of local affairs in late Imperial China was forced to rest on two foundations, namely “a formal governmental structure (the magistrate’s office) and non-bureaucratic ‘liturgies’ (mostly under the control of the gentry and other local elites, such as big landlords, and wealthy merchants)” (Chow, 1994: 71f.). The Imperial court’s dependence on the “liturgies” and “local elites”, pointed out by Max Weber in his 1922 publication Economy and Society (Weber and Whimster, 2008), has since been a focus for many scholars of Chinese history. 9 In the late Imperial context, the performance of “liturgies” has been aptly described as “an established tradition of local elites shouldering responsibility for the provision and maintenance of the physical infrastructure and services necessary for social order and stability” (Peterson, 2005: 92). These “local elites” comprised, thereby, not exclusively those who had won or purchased official degrees, since many of them never took any office. 10 These “local elites” were headed by those who had obtained or purchased official degrees, regardless of whether or not they actually took office. 11 Their ranks were furthermore joined by influential men without degrees, such as “gentry, wealthy peasants and landlords, well-off shopkeepers and laborers, and merchants” (Katz, 1999: 226, n. 19).

In late Imperial China, philanthropy 12 had a long tradition, comprising “a mixture of official, religious and private institutions” (Peterson, 2005: 89). By the late Ming period, the so-called “benevolent societies” brought about substantial changes in the philanthropic field. Originating in the Jiangnan area, the center of Chinese scholarship immediately south of the lower Yangtze reaches, these organizations were the first that made philanthropy their primary purpose. 13 This contrasted with the charitable efforts of emperors, Buddhist monasteries, and lineages that served as means to other primary ends (Handlin Smith, 2009: 4). Benevolent societies were also innovative because they resulted from the joint efforts of officials and local elites, which increasingly included merchants: “During the Qing dynasty, the funding and organization of much philanthropy shifted from the scholarly elite to merchants. By the mid-nineteenth century, urban centers boasted huge benevolent societies, foundling homes, and widow homes” (Handlin Smith, 1998b: 420).

In her study on elite writings about philanthropy, Handlin Smith (1998b) has shown how the visibility and role of merchants within philanthropic institutions changed significantly between the late Ming and the early Qing periods (1644 to the late eighteenth century). Those Confucian scholars that wrote about philanthropy during the earlier period never openly associated themselves with merchants, and in case they were involved in trade themselves hastened to “obscure their merchant origins” (Handlin Smith, 1998b: 423). Merchants that patronized these efforts not only failed to leave behind traces, but were also discredited by those who wrote about philanthropy. Steeped in an idealized Confucian view of society, they “considered occupations in trade and handicrafts to be inferior – or ‘secondary’ (mo) – to agriculture, and idealized a social hierarchy where they, the scholars, stood at the top and their immediate competitors, the merchants, near the bottom (below farmers/peasants and followed only by butchers and prostitutes)” (Handlin Smith, 1998b: 421). The scholars of this period underpinned their supremacy by means of the Confucian “gong-si dichotomy” (Peterson, 2005: 89) that viewed trading activities as the pursuit of selfish interests (si) which were diametrically opposed to public concerns as pursued by a Confucian officialdom (gong) (Peterson, 2005; Rankin, 1990).

In contrast, in scholarly writings from the early Qing merchants were recorded side by side with other benefactors. The idealized society mentioned above was openly rejected in scholarly writings (Handlin Smith, 1998b: 426). These sources are indicative of “the increasing importance of wealth as a source and arbiter of social status” (Peterson, 2005: 90), which inevitably brought about a blurring of social distinctions and an increase in social mobility (Peterson, 2005: 91). In this competition for social status, merchants increasingly gained the upper hand. In the eighteenth century, merchants even came to epitomize elite status (Peterson, 2005: 91).

Peterson (2005: 90) observed that “rapid commercialization meant that money was becoming an increasingly important aspect of social relationships in late Imperial China”. This is particularly apparent within the benevolent societies whose accounting systems have been described by Fuma (2005). In contrast to official or religious institutions, the administration of these societies usually rotated on a yearly basis among the members of a management board. As their activities spanned several counties, involving many people and large funds, an accounting system was conceived that ensured some measure of transparency (Fuma, 2005: 709): When [in late Imperial China] a group of people formed a benevolent society and collected funds, they were inevitably concerned about the correct application of these funds, the organization’s achievements over the years and whether they had gathered merit by their investments. Furthermore, at the end of each year those members that were charged with the management of the society on the one hand hoped to prove that the donations had been used entirely for the designated purposes while on the other hand they wanted to give a report of the achievements of the previous year. For these reasons they published accounting reports, so-called “trust-proving records” (zhengxinlu), for general distribution. By means of these reports donors and associates exerted control over the society.

Trust, one of the five cardinal Confucian virtues governing human relationships (Chow, 1994: 38; Gao and Handley-Schachler, 2003: 44), was a key term of the intellectual discourse of the Qing Dynasty (Fuma, 2005: 710). While the term “trust-proving records” became widespread in late-seventeenth-century Jiangnan only, it is highly probable that the practice of distributing annual reports dates back to the late Ming period, when the benevolent societies emerged. Although the functions of the accounting reports varied according to the internal regulations of these societies, Fuma (2005: 714f.) has pointed out that these reports served three main purposes:

Distribution among the donors to relieve the management board.

Storage in the archives of the local government office to serve as legal documents.

Ritual burning in front of the city god to symbolize accountability toward the gods.

Similarly to the benevolent societies, temple investment projects were also administered by management boards. Although little is known about either management practices within these boards or the biographical backgrounds of board members, the term “trust-proving” occasionally appears on commemorative stele (see the “Trust-proving sketch of the reconstruction of the theatrical stage at the City God Temple in Shanghai County” in the Appendix). This probably indicates two things: First, the board members of benevolent societies and those of temple investment projects were of a similar social background. Second, the paper documents that were copied on the stelae served similar functions as the accounting reports of benevolent societies.

A systematic analysis of these stelae presupposes a relevant corpus of inscriptions. For that reason, the author has collected 80 relevant inscriptions from nineteenth-century South China. The next section contains a presentation and an analytical study of this corpus.

Financial statements on commemorative stelae: Basic features and presentation of the corpus

While referred to in Chinese studies of the social history of China (Peng, 2005; Wang and Che, 2007), financial statements on commemorative stelae have, to date, gone unnoticed in the West. Originating during the last quarter of the eighteenth century, these stelae represent another step in the evolution of the commemorative stele. During the eighteenth century, as evidenced in Naquin’s sample, donations were predominantly registered in cash. These lists provided the basis for the publication of the Chinese forms of ledgers and accounting reports on temple stelae, where the donations took the place of the receipts of a commercial undertaking. 14 Still, on the majority of these inscriptions, the financial statements have prefaces outlining the “major events marking the history of this temple” (Katz, 1999: 100). As such, the inclusion of financial statements did not constitute a significant deviation from the commemorative stele in its traditional form.

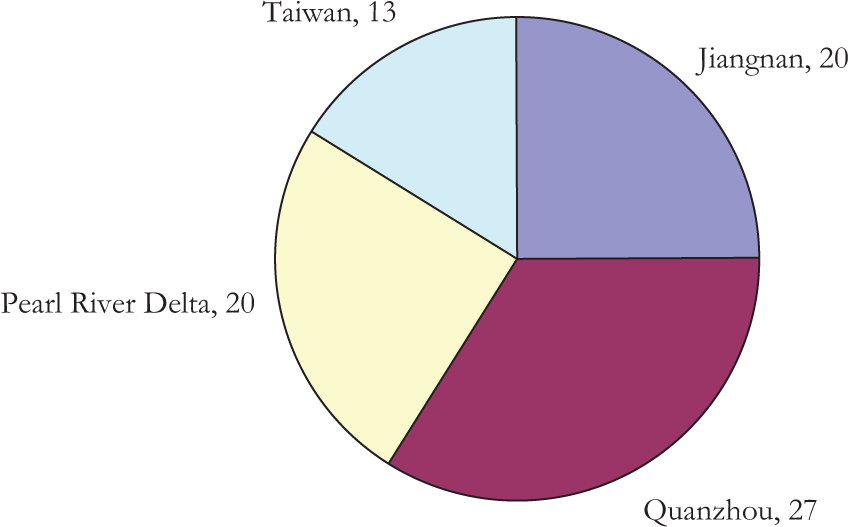

In order to trace the evolution and contents of financial statements on stelae, the author has searched through comprehensive collections of stele inscriptions. From the late eighteenth century onwards, many of these inscriptions, mainly from urban areas, contain evidence of accounting practices. Notably, the collections from South China (commonly defined as the area south of the Yangtze River) lend themselves to a systematic overview of such inscriptions. 15 Relevant inscriptions have been found in 10 collections from the following regions: Jiangnan (JMQBZX, MQSSSBJ, SBZX, SFBWJ), Quanzhou Prefecture in Fujian (FZBH, XMBH), the Pearl River Delta (GDBJ, GZBJ, JMAS, XBH), and Taiwan (TJ). The corpus of 80 stele inscriptions (see Figures 2 and 3) includes a significant number of inscriptions that were put up when the respective town or region was under colonial rule, although these areas had been points of contact with foreign nations long before official recognition. 16 By taking these inscriptions into account, it is possible to arrive at a more general picture of accounting on stelae at temples of Chinese religion.

Regional distribution of the corpus.

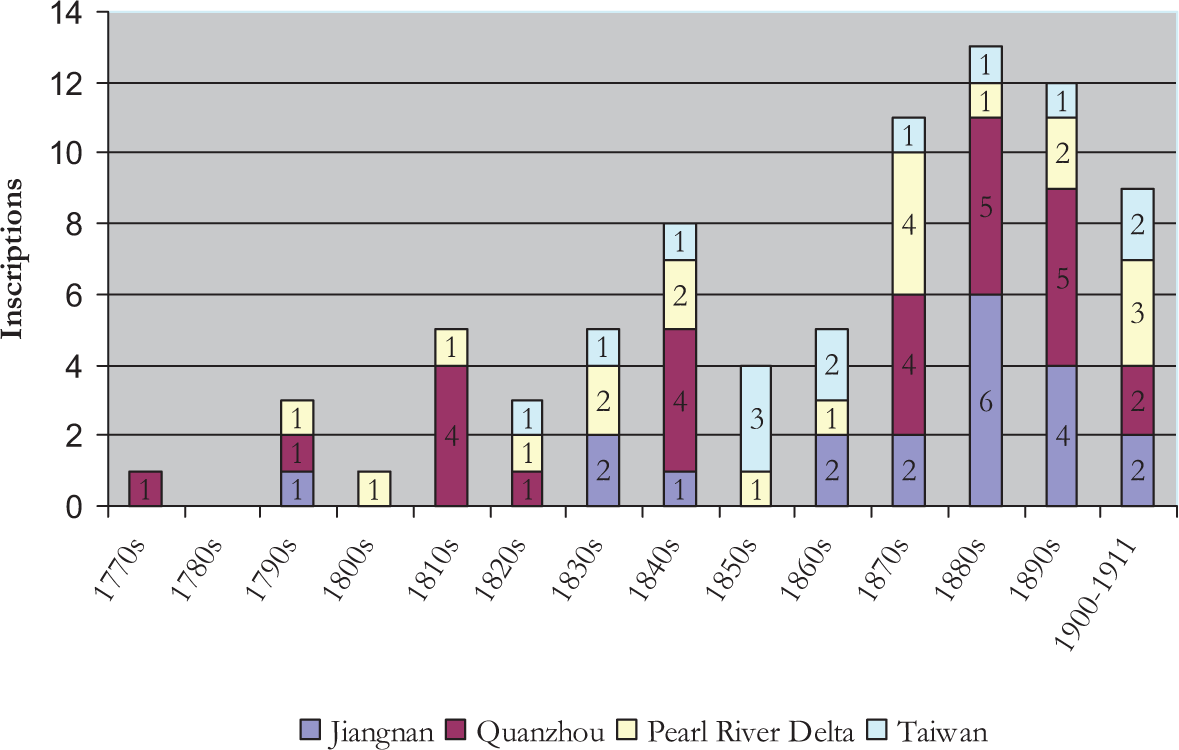

Temporal distribution of the corpus across regions.

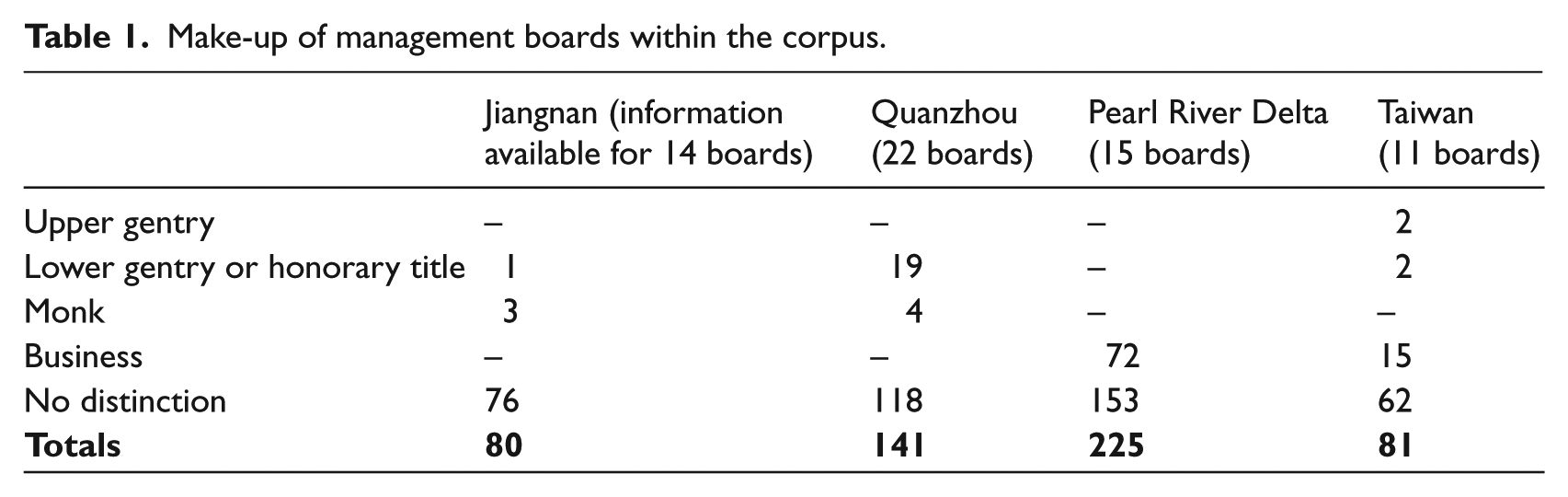

As can be seen in Table 1, there is no sign of upper gentry involvement, except for two individual cases in Taiwan. Lower gentry and holders of honorary titles managed only a few projects in Jiangnan, Quanzhou and Taiwan. The same holds true for individual monks that were involved in some projects in Jiangnan and Quanzhou. Another significant feature is the management of projects in the name of businesses or trade names. This practice was particularly widespread in the highly commercialized region of the Pearl River Delta, where businesses held one third of the management posts in the sample. The most striking fact within the table, however, is the large-scale involvement of managers without any title, which pervades the areas and the period; overall these managers constitute approximately 70 percent of all managers in the sample from the Pearl River Delta, around 80 percent in Quanzhou and Taiwan, and over 90 percent in the Jiangnan sample.

Make-up of management boards within the corpus.

On the stele inscriptions, three different yet related types of financial statements can be discerned (see Appendix for examples):

Zongqingbu: The Chinese counterpart of the ledger was used “to classify and summarize business activities and transactions for a specific period” (Aiken and Lu, 1998: 227). In the framework of the single-entry bookkeeping methods of the late Imperial period, this ledger formed the basis for profit and loss statements. The zongqingbu was a cash-flow statement that, as in other accounts within Chinese single-entry bookkeeping, recorded receipts on the top half and disbursements on the lower half of the sheet. Finally, the figures on the top and lower halves were added up to yield totals for incomes and disbursement, respectively (Aiken and Lu, 1998: 232f.). Although the zongqingbu originated in a single-entry framework, it was integrated and elaborated in the double-entry bookkeeping systems that emerged during the seventeenth and eighteenth centuries (Aiken and Lu, 1998: 229ff.).

Caixiang jiece: This profit and loss statement was one of the accounting reports within the double-entry “Four Feet” or “Heaven and Earth Matching” bookkeeping system that emerged during the mid-eighteenth century. As with the zongqingbu, incomes and disbursements were recorded on the top and on the lower half of the sheet, respectively. After calculations of the subtotals, the disbursements were subtracted from the receipts to arrive at the profit or loss for the relevant project (Aiken and Lu, 1998: 235).

Cunchu jiece: The second accounting report within the Four Feet method was the Chinese form of the balance sheet. Receipts and liabilities, as well as potential profits, appeared on the top half, while disbursements, debits and losses were recorded on the lower part. This resulted in equal subtotals and the matching of the upper part (“Heaven”) and the lower part (“Earth”) (Aiken and Lu, 1998: 235).

The publication of profit and loss statements (caixiang jiece) and balance sheets (cunchu jiece), the two accounting reports within Four Foot bookkeeping, is evidenced in the widespread use of this method throughout nineteenth-century South China. It has to be pointed out, however, that the difference between these accounts is smaller than such a categorization might suggest. It is not surprising that these financial statements have many commonalities, given that they exclusively concerned the realization of construction or renovation projects that were generally financed by fundraising. As such, they rarely include any prior liabilities or debits. 17 Still, the above classification is useful in order to distinguish between accounts that merely list and add up receipts and disbursements (zongqingbu), those that calculate the profit or loss after completion (caixiang jiece), and those that emphasize the balance between incomes and disbursements (cunchu jiece).

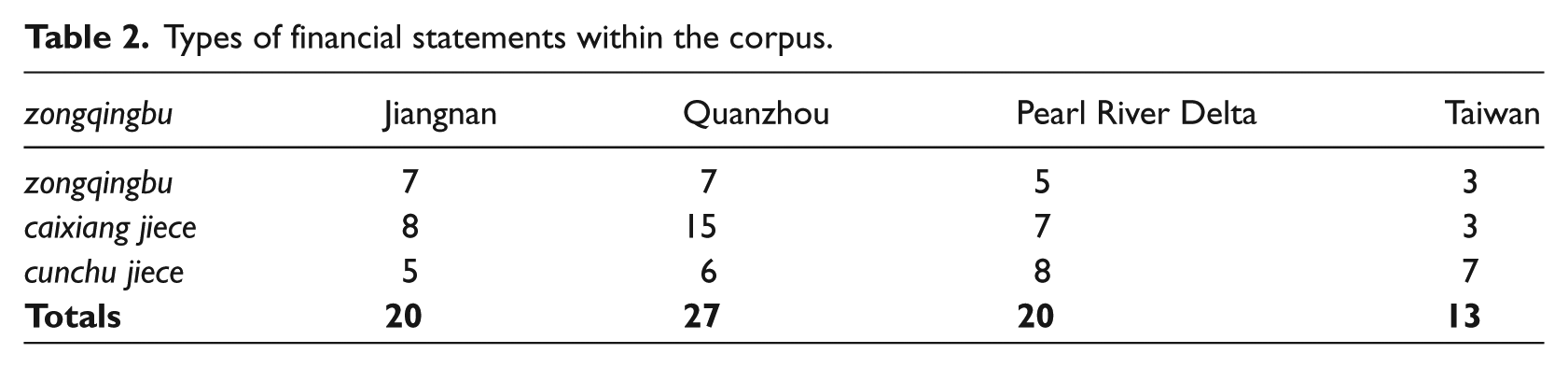

With regard to the regional distribution of these financial statements and their evolution over time, only vague patterns evolved and emerged. In the Jiangnan area, where late Imperial accounting methods were most advanced (Aiken and Lu, 1998: 235), the majority of financial statements on stelae took the form of caixiang jiece (see Table 2). However, profit and loss statements were also a predominant form in Quanzhou Prefecture, while in the Pearl River Delta the caixiang jiece and cunchu jiece statements are almost equally well represented. The sample from Taiwan is markedly different, as there the cunchu jiece seemed much more popular than the other financial statements. Overall, it seems safe to assume that the zongqingbu ledger was the least popular form of financial statements throughout the four regions.

Types of financial statements within the corpus.

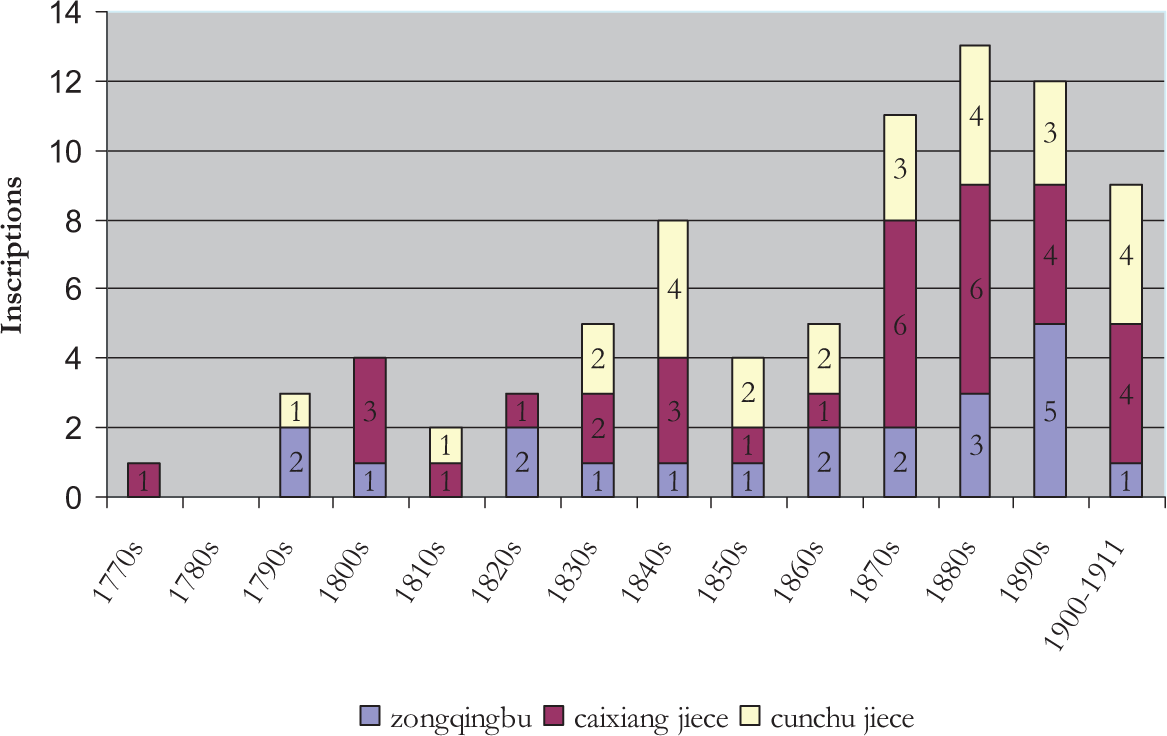

As the inscriptions in the sample date from 1777 until the cut-off year of 1911, some sort of evolution might be expected. However, as can be seen in Figure 4, all three forms of accounts pervaded throughout the period under investigation. Although the use of the zongqingbu ledger increased during the latter half of the century, it can be observed that overall their significance decreased vis-à-vis the profit and loss statements. Arguably, the publication of profit and loss statements instead of ledgers during the late century can be read as a sign of increased economic awareness within the management boards and/or the adepts. If so, then this awareness is symptomatic of the mercantile mindset within regions of increased contact with the global market.

Temporal distributions of forms of financial statements within the corpus.

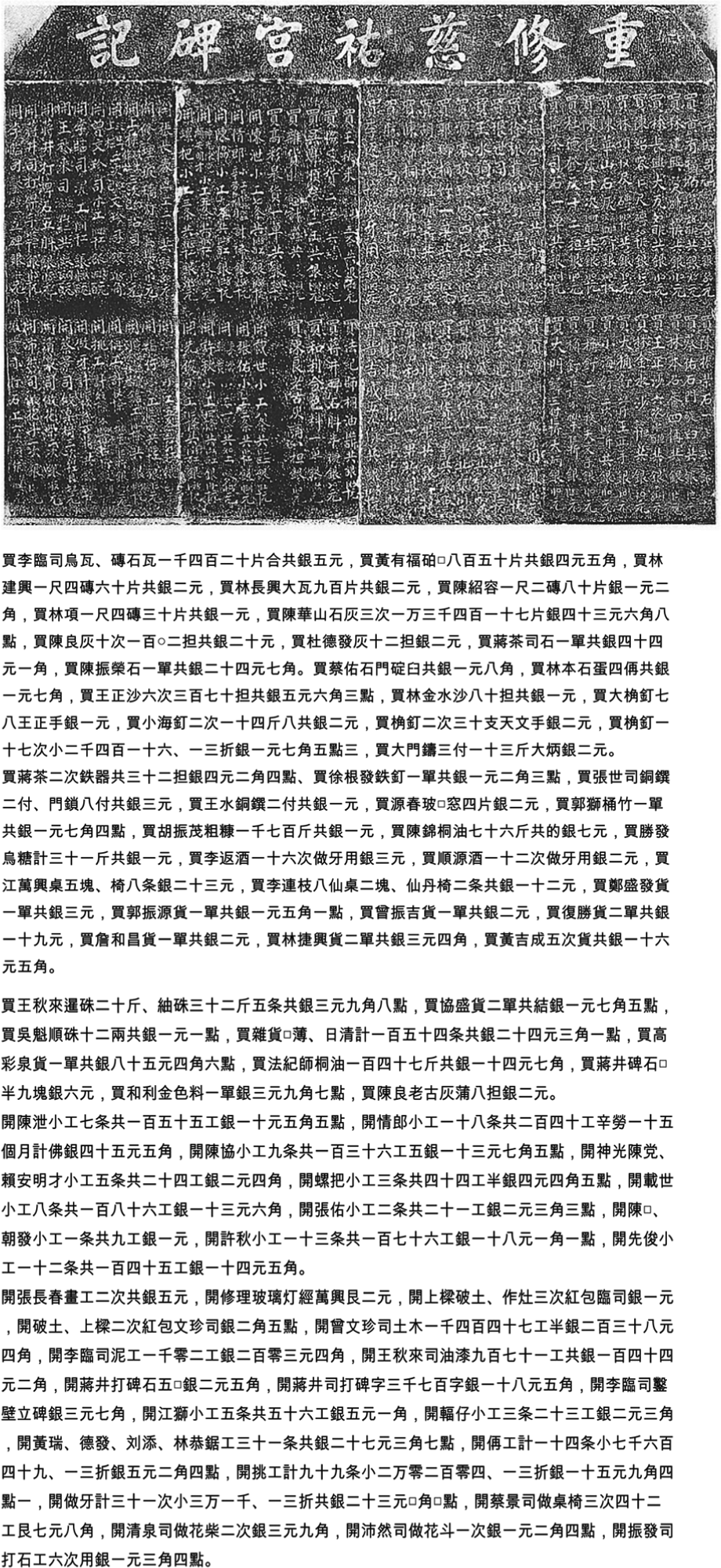

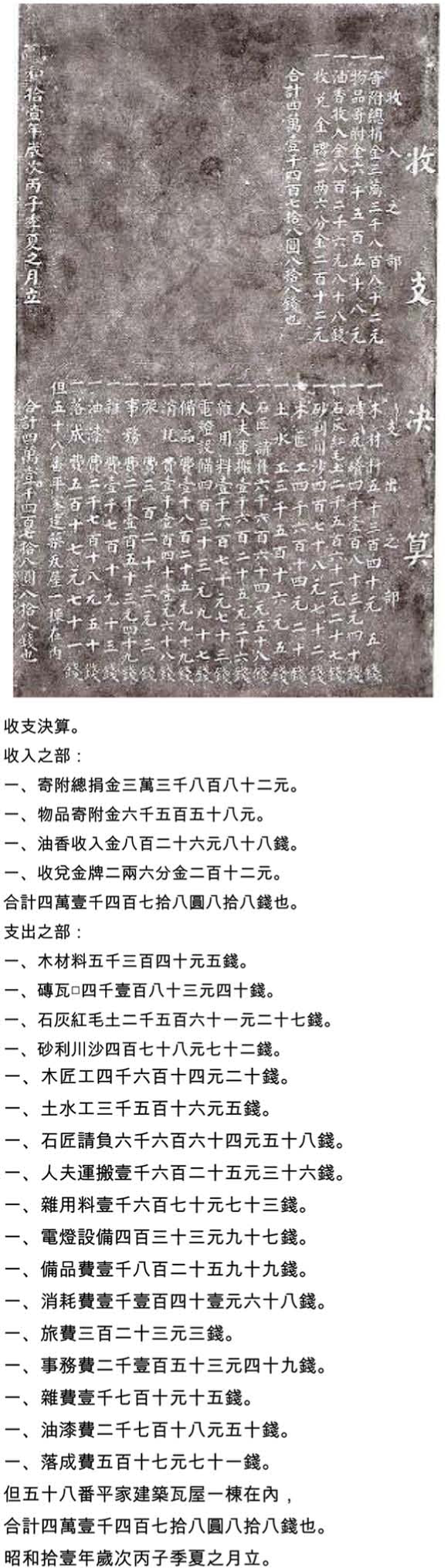

A second significant evolution can be observed in Taiwan during the latter half of the century. There the expenditures are often described in great detail, including numbers of items and workdays, and names of contractors, often spreading over several stelae (see Figure 5). In a third step, in the early twentieth century the most sophisticated form of financial statements on stelae emerged in Japanese-occupied Taiwan. These stelae show a refined graphical representation and are often entitled “final account of incomes and expenditures (shouzhi juesuan)”. As can be seen in Figure 6, these stelae are highly structured, as the upper and lower halves are exclusively reserved for receipts and disbursements, respectively. The two halves are labeled “receipts section” (shouru zhi bu) and “disbursements section” (zhichu zhi bu). These two observations imply that on Taiwan the elite were much less secretive about their merchant origins than was the case on the mainland.

“Stele inscription of the renovation of the Ciyou Palace (No. 4)” and transcription. The inscription is spread over five stelae. As a part of this account, the depicted stele is entirely inscribed with detailed descriptions of expenditures. Xinzhuang District/Taibei, 1873. (Source: TJ; TDXBT: 24.)

“Stele record of the renovation of the Taishanyan [Temple] (No. 5)” and transcription. The inscription, which is spread over five stelae, contains the depicted account entitled “final account of incomes and expenditures”. Taibei, 1935. (Source: TJ; TDXBT: 121.)

As to the ratio between the sample inscriptions and the total number of temple investment projects, or, in other words, were the boards of managers expected to publish a financial statement or were these cases very rare and therefore all the more noticeable, the answers to these questions would necessitate a (near-) complete overview, firstly of stele inscriptions and secondly of the set of temples, as well as the dates of their construction or renovation within a given area. Unfortunately, due to a lack of source material, neither of these conditions can be adequately met. On the basis of the financial statements on stelae from Quanzhou Prefecture and the Pearl River Delta, and data culled from previous studies, some rough estimates can nonetheless be made.

In his study on “temple-building activities” in Imperial China, Eberhard (1964) collected basic historical data for more than 10,000 temples. This data was culled from 43 local gazetteers, those records “published every few generations to preserve local lore and commemorate worthy residents” (Handlin Smith, 2009: 5). For his “test area”, spanning 43 counties (including some prefectures) in seven provinces, 18 he predominantly collected data from nineteenth-century gazetteers. In the cases of Fujian and Guangdong provinces, information on temples has been culled from 18 and 15 county gazetteers, respectively. The number of temples per county ranged between 45 and 592 in Fujian and between 30 and 374 in Guangdong, while the median number of temples is 133 in Fujian and 86 in Guangdong (Eberhard, 1964: 275f.). It should be noted, however, as Eberhard acknowledged, that the information on temples in local gazetteers is far from complete. Rather, these sources listed only those temples that received official funding or were considered important local institutions. For that reason, these data have to be read as absolute minimal estimates.

Eberhard (1964) also included data about the construction and renovation of temples, which he used to perform comparisons between 50-year cycles. For our purposes, however, these numbers are far too low to provide a realistic picture. Rather, we resort to Brook’s (1993: 162f.) estimate of the “half-life” of temples that has been confirmed by Naquin (2000: 77). Although both authors point out that the intervals between temple investment projects varied greatly, both authors consider a 100-year period between projects as a realistic approximation. Going back to Eberhard’s data, we would therefore expect about 133 major investments per county in nineteenth-century Fujian. In Guangdong this figure would amount to 86 renovations. By contrast, the sample contains only 27 inscriptions for Quanzhou Prefecture and 20 for the Pearl River Delta. As a result, even without a near-complete set of inscriptions or a good overview of temple investment projects, these figures indicate that the publication of financial statements on stelae was a highly uncommon and extraordinary phenomenon. For that reason, for the boards of managers these rare stelae were a powerful source of symbolic capital.

Financial statements on commemorative stelae: Implications for accounting history

As can be seen in Table 1, the personal information on the board members that can be culled from stele inscriptions is confined to official or honorary titles, if applicable. The rise of merchants to elite status that has been observed otherwise, and perhaps more strongly the inclusion of financial statements, suggests that merchants played a major part within these projects. Furthermore, the sample inscriptions allow for some general observations about the accounting culture of late Qing China.

Accounting stagnation in nineteenth-century China: Auyeung (2002) and Auyeung and Ivory (2003) have pointed out that when superior bookkeeping methods were introduced from the West after 1840, Chinese firms only rarely used them prior to the twentieth century. This is supported within our sample from different areas where, between the late eighteenth and the early twentieth centuries, no significant evolution can be discerned. Moreover, until the early twentieth century, some of these inscriptions still contained zongqingbu ledgers that had originated in late Imperial single-entry bookkeeping.

The Confucian foundations of society: Aeuyung and Ivory (2003), Bloom and Solotko (2003) and Gao and Handley-Schachler (2003) have unanimously stressed that Confucian philosophy played a decisive role in the development of Chinese accounting. The overall Confucian influence is thereby portrayed as playing “a negative part in the development of Chinese private accounting” (Gao and Handley-Schachler, 2003: 60). This is partly due to the conservative stance of the Confucian doctrine that treasuring the existing social order and established practices (Bloom and Solotko, 2003: 31) led to the accounting stagnation mentioned above. Also, the disdain of “profit” (li), an integral part of the Confucian value system, had resulted in a centuries-long discrimination of the merchant class (Gao and Handley-Schachler, 2003: 56f.). As a result, during the late Qing “the merchants … joined the gentry by buying land and cultivating literary life-styles, rather than remaining a distinct class” (Esherick and Rankin, 1990: 9). The sample inscriptions contain evidence of merchants concealing their origins: firstly, the boards of managers within the sample resorted to the stele, which was a powerful traditional form of symbolic capital. Secondly, they were often joined by gentry or honorary members of their locality (see Table 1). As a result, “the Chinese merchant class of the nineteenth century was unable to articulate an independent ideological stance” (Aeuyung and Ivory, 2003: 19).

However, the commemorative stelae in general, and those that included financial statements in particular, are also evidence of a tidal change within the Chinese elite in the nineteenth century. Detailed records of monetary donations and inscriptions in the form of financial statements were part of an evolution within which “commercial wealth” was “added … to the resources available to elites, changed elite strategies for mobility and status maintenance, and opened arenas of activity outside the state-sanctioned paths of degree acquisition, office holding, and Confucian scholarship” (Esherick and Rankin, 1990: 9). These inscriptions bear witness to the fact that money had become an “arbiter of social status” (Peterson, 2005: 90), which, however, did not yet overthrow the Confucian foundations of society.

Reliance on trust instead of written contracts: Another Confucian moral principle has been identified by Gao and Handley-Schachler (2003: 49): “Chinese believe that the basic nature of human beings is good, so to write everything down in black and white is considered as a demonstration of distrust and against the nature of human beings … Thus, trust and contracts are opposed to each other in Chinese culture”. The importance of trust, one of the five cardinal Confucian virtues governing human relationships (Chow, 1994: 38; Gao and Handley-Schachler, 2003: 44) within Chinese society, is evidenced in the corpus where individual inscriptions are designated “trust-proving stele”. This title indicates that the stelae in question were used by the boards of managers to gain trust within their localities. The denomination “trust-proving stele” directly referred to a quote from the Confucian classic The Doctrine of the Mean: 19 “Without proof there won’t be any trust” (wuzheng buxin) (Fuma, 2005: 710).

The exploitation of inscriptions as a form of written documents, however, contradicts the alleged reliance on personal trust instead of contracts. Of course, as can be seen above, these stelae were not put up in significant numbers and most boards of managers might have relied entirely on personal relationships. However, the reliance on written contracts and handbooks is corroborated by recent scholarship in the field of Chinese economic history. According to Zelin et al. (2004: 2), contracts played a “critical role … in the everyday structuring of all manner of relationships and transactions in China”. Moreover, “the use of contracts in the conduct of business was pervasive, belying the much-touted reliance of Chinese merchants on face-to-face relations and trust” (Zelin et al., 2004: 6). Such contracts, attested since the Song Dynasty (960–1279), were very common in the late Imperial period (Zelin et al., 2004: 2). In light of these findings, the financial statements on stele inscriptions confirm that during the late Qing the alleged opposition between trust and contracts is, at least, questionable.

Accounting practice and socio-religious balance: Aiken and Lu (1998: 238) hold that “the basic principle of Chinese double-entry bookkeeping is that cash inflows should be equal to cash (silver) outflows”. In a similar vein, Gao and Handley-Schachler (2003: 54) have pointed out that under the influence of the yin and yang concept “Chinese accounting was developed without a clear-cut distinction between accounts, but the balance was strongly emphasized”. This is particularly obvious in the case of the Four Feet Method or “Heaven and Earth Matching Method”. This was because in the cunchu jiece balance sheets, the incomes (the upper half, heaven, yang) had to match the disbursements (the lower half, earth, yin) (Gao and Handley-Schachler, 2003: 54). Within the cunchu jiece, the visibility of this balancing function is further enhanced in two ways. First, the totals of incomes and expenditures are matched down to the smallest monetary unit (see the “Stele record of the renovation of the Old Wudi Temple” in the appendix). Second, the balance was sometimes explicitly emphasized by statements such as “incomes and disbursements are balanced (shouzhi liangqing)”.

The importance of balanced accounts is part of a larger “regulatory role of accounting practice in relation to concepts of socio-religious balance” that has been observed in diverse accounting cultures (Kuasirikun and Constable, 2010: 606). With the exception of Quanzhou, the publication of balance sheets of the cunchu jiece type is a pervasive phenomenon, particularly prominent in Taiwan. By means of these financial statements, the managers implicitly “matched Heaven and Earth”, contributing to a cosmological harmony that went beyond the respective undertaking and temple.

Accounting and Chinese religion: Gao and Handley-Schachler (2003: 48) have made the following sweeping statements about the influence of Chinese religion on accounting: “In China, the religious arena was traditionally considered as a ‘sacred place’ where commercial activities and monetary transactions were forbidden. … Although China has many splendid temples and innumerable religious classics, it is difficult to find valuable commercial and accounting materials”. As such, they view the influence of Chinese religion in sharp contrast to the West where “the religious arena … was a significant site of economic activities” (Gao and Handley-Schachler, 2003: 50). Based on the renouncement of personal desires within the Buddhist doctrine, this view does not do justice to the actual practice of Chinese religion as described in recent scholarship. For example, Walsh (2010: 5f.) observed: “One of the great ironies of monastic Buddhism was that renouncing materiality and the self through a series of metaphysical and bodily strategies resulted in the accumulation of material wealth in abundance and a communal identity forged through discipline and practice”. Focusing on the necessity of substantial financial capital for the long-term survival of religious institutions, Walsh (2010: 8, 13) rejects dichotomies such as material/spiritual or sacred/secular as misleading. For Chinese religion in general, Walsh (2010: 13) holds that “to the extent that we speak about Chinese religiosity, we are always talking about, and hopefully thinking through, material relations of exchange and power relations, taking place within a meaningfully prescribed space that we may refer to as participatory rather than simply ‘sacred’ or ‘secular’ space”. As such, the influence of Chinese religion on accounting has much in common with the influence of Thai Buddhism as described by Kuasirikun and Constable (2010: 614): “Accounting in general was perceived as part of a sacred practice of gifting and exchange in pursuit of a wider Buddhist order in which material well-being and socio-moral development were perceived to be intricately intertwined”. By means of liturgies, the local elites of late Imperial China shouldered much of the responsibility and were held accountable for the maintenance of this higher-order “material well-being and socio-moral development”. As such, temples were as much a part of these liturgical duties as were “schools, academies, city walls … orphanages” and other projects and institutions (Brook, 1990: 46).

As regards the history of temple investments in China, the available evidence suggests that the Buddhist doctrine, rather than Daoist or Confucian value systems, was the single most important stimulus. In his path-breaking study of the impact of Buddhism on Chinese socioeconomic history, Gernet (1995: 17) has pointed out the “building passion” of early Chinese Buddhism. Focusing on manuscripts unearthed at Dunhuang, Gernet (1995: 233) identified the fifth century as “the period in which the true development of Chinese Buddhism took place, where an organized monastic community made its appearance and the number of sanctuaries multiplied”. This activism had an enormous impact on the commodity circuits of wood, bricks, tiles, copper, gold and silver (Gernet 1995: 17). Although Gernet (1995: 14) acknowledged the standard argument of Confucian scholar-officials, that financing large monasteries at times had devastating effects on the agrarian society, he is more inclined to stress the positive effects of Buddhism on the general economy: “The needs of the Buddhist communities and laity favored certain businesses – especially those related to construction, the timber trade, dyeing products, and others – and gave rise to or developed certain trades: builders, architects, sculptors, painters, goldsmiths, and copyists”. Besides this socioeconomic boost, according to Gernet (1995: 228), Buddhist monasteries also accumulated capital like modern corporations in order to engage in business, and for that reason introduced “a form of modern capitalism” into China. As a result, Gernet (1995: 219) pointed out a fundamental difference between early Chinese Mahāyāna Buddhism in China and Indian Theravada Buddhism: The share of goods required for the upkeep of the communities, which formed the main part of all offerings under the Lesser Vehicle [i.e. Theravada], became minute in the economy of Chinese Mahāyāna where the biggest expenditures went into the construction of sanctuaries, the casting of bells and statues, and, finally, charitable activities.

For the late Imperial period, Brook (1993: 3) has described the late Ming as “a period of revival for institutionalized religion”. During that era, commercialism and general wealth increasingly threatened the status of the elites. This was because “a greater degree of wealth seems to have opened the examination treadmill to more people in the Ming, engaging the aspirations of almost every family that could afford to put up a son as a candidate” (Brook, 1993: 324f.). As the number of candidates for the already limited official posts increased rapidly, a growing body of degree-holders had to find other means to exert influence and power. Many turned to patronizing Buddhist monasteries, not only to make their status and influence felt, but also to distinguish themselves from the merchant class. In doing so, they “publicized themselves as a unified, refined elite whose power derived not from the state but from their own conduct” (Brook, 1993: 320). In fact, while Gernet’s study revealed the economic relevance of Buddhism during its formative period, Brook’s study of Chinese society, set a millennium later, showed that Buddhist institutions still vested Chinese elites with social capital.

Monasteries were not the only types of temples that flourished in the highly commercialized setting of late Imperial China. Among the few studies of the impact of commercialization on the cults of Chinese religion, von Glahn’s (2004: 222ff.) historical sketch of the Wutong cult in the Jiangnan area contains valuable insights. During that late Ming period, money gained “cultural meaning” (von Glahn, 2004: 222) and pervaded the field of religion. Diverse religious practices came to be symbolized by the “language of the marketplace” (von Glahn, 2004: 222) and mercantile practices: the Daoist notion of the “covert loan” (von Glahn, 2004: 233), for instance, implied that the amount of wealth that an individual can acquire during their lifetime is predetermined and that therefore excessive riches would necessarily imply depletion of that loan. However, among monetary metaphors it was a Confucian rather than a Daoist or Buddhist literary genre that instigated widespread social activism: the “ledgers of merit and demerit” attributed tangible future rewards – “examination success, an abundance of sons, and more diffused benefits enjoyed by society as a whole” – to concrete virtuous deeds (von Glahn, 2004: 233). It has to be pointed out, however, that during the late Ming and early Qing periods, Chinese religion did not raise proto-capitalist hopes but rather advocated meritorious deeds by instilling fear: “caught in the throes of the money economy” the adepts of Chinese religion “lived in a state of perpetual indebtedness” (von Glahn, 2004: 234).

All of this changed during the eighteenth century when the Wutong cult underwent a fundamental transformation, which, according to von Glahn, reflected its changed socioeconomic context: the Chinese market economy of the eighteenth century was much more stable than during the previous century. While the exploitation of the Yunnan copper mines allowed the court to establish the copper coin as standard currency, urban networks stabilized the markets (von Glahn, 2004: 252f.). At the time “the god of wealth became a euhemeristic embodiment of domestic and public virtues” (von Glahn, 2004: 253). By the nineteenth century, this domesticated Wutong reaffirmed rather than threatened the existing socioeconomic order. It “emphasized typical business virtues: hard work, modesty, thrift, and integrity – in short, making money by using one’s own wits and talents rather than depending on a diabolic bargain with a malevolent spirit” (von Glahn, 2004: 249).

Arguably, the transformation of the Wutong god during the eighteenth century from a “malicious and notoriously unreliable” (von Glahn, 2004: 251) spirit to a tutelary god of wealth is symptomatic of the increasing involvement of the merchant class in elite circles. In urban South China, where many temples were “situated near major markets or along commercial routes” (Brook, 1993: 220), they became focal points for the social activism of the new elites.

The sample stelae financial statements prove that, as a corrective to the remark in Gao and Handley-Schachler (2003), “commercial and accounting materials” are indeed available for temples during the late Qing period. Furthermore, these statements contradict the alleged opposition between Chinese religion and monetary transactions. On the contrary, within these financial statements the careful husbanding of donated funds by the managers was as much an expression of piety and devotion as the donations themselves. The statements implied, as it were, that the managers forwarded the donated funds directly to the gods. This point has been made by Wang and Che (2007: 39): Because of their reverence towards the gods, the managers and community heads usually did not dare or even wish to embezzle common funds. As the money belonged to the gods, any bribery would inevitably incur their judgment. Rumors about persons who had been stricken by disasters as a result of embezzling money from the gods were circulating in many regions.

As a result, financial statements on stelae expressed the devotion of those engaged in “commercial activities and monetary transactions”. Chinese religion, therefore, played an important role in the development of Chinese accounting culture.

Conclusion

When during the late Qing Dynasty the lay communities of lineages, territorial, professional and congregational groups invested in their temples, the managers of these projects occasionally published financial statements on commemorative stelae. In order to establish their good reputation, not only within the lay communities but also in local arenas, these managers resorted to a medium of accounting that was “a powerful form of cultural capital” (Walsh, 2010: 116). Playing an important role within the cultural framework of accounting, the commemorative stele was a well-established medium encompassing all three “languages” of accounting – “numbers, words and visual images” (Davison and Warren, 2009: 846). While visual accounting was important in its early, predominantly Buddhist stage, by the late Imperial period narrative and numerical accounts on stelae were omnipresent. The large majority of the numerical accounts concerned the donations of those that wished to make a point of their devotion, participation and influence. Furthermore, as has been shown in this article, by the late Qing, commemorative stelae also included three popular forms of financial statements, namely ledgers (zongqingbu), profit and loss statements (caixiang jiece) and balance sheets (cunchu jiece).

Although these inscriptions contain little or no information about, or biographies of, the boards of managers, the financial statements imply the growing importance of money within a quickly commercializing society, as well as the emancipation of the merchant class. Moreover, these accounts are further evidence for the universal, yet often contested presence of contractual arrangements during that period.

Due to an unfortunate tendency to “marginalize the contribution of religion” (Kuasirikun and Constable, 2010: 599) in the field of Chinese accounting history, much evidence has been overlooked. On the one hand, Chinese religion strongly influenced accounting as the general population viewed “accounting primarily from the spiritual point of view” (Gao and Handley-Schachler, 2003: 48). During the late Ming period this influence was most apparent in “ledgers of merit and demerit”, a popular form of morality books used to keep an account of one’s good and bad deeds (Brokaw, 1991). According to Chow (1994: 26), these accounts conveyed to a person “a sense of control over his or her fate through the accumulation of merits”. On the other hand, as “fund-raising [for an array of merit-making purposes] was actually a fundamental and well-established role for clerics” (Goossaert, 2007: 127), Chinese religion also played a decisive role in the accounting culture of the real world. Another noteworthy phenomenon pervaded Chinese history since the first century of the Christian era: tomb acquisition contracts were inscribed on stone or other materials and buried together with the deceased in order to prove the rightful purchase of the burial sites (Hansen, 1995: 149). In those cases where the purchase price for the site was cited in the currencies of this world and the underworld, these contracts were “designed for use in two court systems, one in this world and one in the afterlife” (Hansen, 1995: 169). Tomb contracts provide further evidence for interdependent religious and economic/legal functions of accounting within Chinese culture. As such, research on the influence of Chinese religion on accounting is only just beginning.

Footnotes

Appendix: Examples of financial statements on stele inscriptions

Acknowledgements

The suggestions and comments of three anonymous referees are gratefully acknowledged.

Funding

This work was supported by the Research Foundation Flanders (FWO) [grant number G.0032.07N].