Abstract

It is generally accepted by historians that in the early twentieth century clubs in Australian Football’s Victorian Football League (VFL) made payments to “amateur” players prior to the legalization of professionalism and that such payments were not disclosed in club financial reports. Previously, financial reports have not been used to support or refute such claims. This article presents findings from a detailed examination of the financial reports and other records of six of the 10 VFL clubs for the years surrounding the legalization of professional football in 1911 (1909–1912). Prior to 1911, most clubs engaged in fraudulent financial reporting practices by misrepresenting player payments as other forms of permitted expenditures, thus concealing prohibited remunerative payments to players within their financial reports. Using isomorphic influences to explain the reasons for this misrepresentation, we conclude that the financial reports were used to legitimate the majority of clubs as amateur organizations. Competing isomorphic pressures, particularly conflicting coercive factors related to the VFL’s prohibition on player payments and normative pressures associated with increasing professionalism amongst players, contributed to clubs engaging in fraudulent financial reporting.

Introduction

It is generally accepted by historians of the code of Australian Football 1 that prior to the legalization of professionalism in the early twentieth century Victorian Football League (VFL) clubs effectively paid “amateur” players and that such payments were not disclosed in club financial reports. This occurred against a backdrop in the late nineteenth and early twentieth centuries in which sport was changing from a predominantly amateur or unremunerated leisure activity, to a commercialized, professional one (see for example Lewis, 1997; Sheard, 1997; Crotty, 1998; Toohey et al., 2012). Across multiple sporting competitions, leagues and countries, this transformation was fraught with angst, dismay and vitriol (Lewis, 1997). Indeed, payments to players, regardless of their type, have been, and continue to be, surrounded by controversy. 2 Australian Football is no different.

As Australian Football spread from Victoria to other colonies, the rules prohibiting remuneration of players were replicated, reinforcing the amateur nature of the sport. However, as with football codes in Britain it was widely held that some players in “amateur” competitions were being directly remunerated (Lewis, 1997; Taylor, 2001).

3

For the VFL, established in 1897 by a breakaway faction of the Victorian Football Association (VFA),

4

the prohibition on payments was captured in Rule 29: Any player receiving payment, directly or indirectly, for his services as a footballer, shall be disqualified for any period the League may decide, and any club paying a player, either directly or indirectly, for his services as a footballer, shall be dealt with as the League may think fit. (Argus, 12 May 1900: 15)

Despite this prohibition, the commercialization of sport encouraged club management to compete to attract the best players by offering payments. In Britain, rising working-class incomes, increased leisure time, and the willingness of spectators to pay to watch high-quality games provided the finance for the growth of professionalism (Vamplew, 1979). Before professionalism was legalized by the British Football Association in 1885, no serious attempts had been made to punish clubs that paid players more than genuine expenses. Vamplew (1988: 191) suggests that some clubs “prepared a fresh set of books for inspection”. It would have been counterproductive for clubs to make information about payments to players available to the public, due to the risk of Football Association (FA) sanctions and the likelihood that rival clubs would seek to lure players once they knew the details of their contracts (Taylor, 2001).

British clubs used three methods to circumvent player payment regulations (Lewis, 1997). Existing histories and newspaper reports reveal that such methods were also used by Australian Football clubs for the same purpose. First, club officials and local supporters who ran businesses may have found jobs for players who had not learnt a trade or profession outside of football. Seven of the 18 members of Carlton’s (VFL) 1909 grand final team had their occupation listed in the press as a “tea grader”, while another worked as an “assistant curator” (Argus, 25 September 1909: 19). These may have been legitimate jobs, or ones that existed in name only, where a club supporter put a player on the payroll but expected them to do little or no work. At least one of Carlton’s “tea graders”, who was a professional gambler, was in the latter category (Frost, 1998: 49). Second, secret payments were made “under the table”, either from cash donations received by clubs from “wealthy patrons”, which were not included in official receipts, or as unofficial bonuses paid directly to players by supporters (Sandercock and Turner, 1981: 59). Such payments would not form part of the club’s accounts or financial reports. Third, direct payments could be made by the club from recorded sources of funds. Because the actual nature of the remuneration could not be acknowledged before 1911, such payments had to be “disguised” in the club’s accounts and financial reports by overstating other expenditure items (Sandercock and Turner, 1981: 59). This method was also used by English rugby league clubs to avoid sanctions for exceeding permitted limits on “broken-time” payments, which were intended to compensate players for time taken off work to train and play. British clubs understated such payments in their accounts until open professionalism was allowed in 1904 (Collins, 2006). Such strategies were also well established in other sporting leagues in the United Kingdom (Lewis, 1997).

The direct payment of players from club funds is acknowledged in many histories of Australian Football, but the nature and extent of such practices have not been examined systematically. Halabi et al. (2012) examined the claim that clubs were directly remunerating players out of club funds prior to 1911, through a case study of Carlton’s accounting reports. Following the rescission of Rule 29, Carlton legitimately remunerated its players, and in the Financial Report of that year, the expenditure classification “Player payments” was recorded for the first time. Prior year payments to Carlton players had hitherto been reported within a series of player-related expenditures such as travelling expenses, training, refreshments, insurance and allowance to injured players, and entertainments. The existence of such items implies that despite the prohibition on “indirect” payments in Rule 29, payments to players were acceptable so long as they did not represent remuneration for services. Carlton professed to be an amateur club that complied with VFL rules, while making payments to players out of club funds in a manner that amounted to de facto professionalism. While this research verifies the existence and details the nature of one club’s disclosure of “illegal” player payments, it does not reveal whether such practices were widespread, as claimed in football histories. 5

The current article builds on and extends existing football histories and prior research through an examination of the disclosure practices of six of the 10 VFL clubs from 1909 to 1912. Full financial information for the remaining four clubs is not available. The article utilizes the concept of institutional isomorphism – coercive, mimetic and normative – to analyse financial reports and ascertain the extent of fraudulent financial reporting as it relates to the payments of players prior to 1911. The study provides a comprehensive basis to explore the use of financial reporting within the context of the rising professionalism, in a league for which little historically based financial research exists. This study therefore increases our understanding of club financial disclosure practices during this important period of Australian Football history.

The remainder of this article is structured as follows. The next section considers the development and evolution of professionalism in Australian Football. This is followed by an overview of legitimacy theory and institutional theory as a lens to examine the research question. The research method is then described. The analysis and discussion sections examine the accounting reports of six VFL football clubs in 1909–1912, the seasons surrounding the historical decision in 1911 to allow player payments to be legally made. Conclusions are drawn as to whether so-called amateur clubs used their financial reports as a legitimation tool, and the extent to which their disclosures indicate that such an image was warranted.

The evolution of professionalism in Australian Football

Australian Football began when members of the Melbourne Cricket Club (MCC) formed the Melbourne Football Club in 1858 (Blainey, 2003). As in Britain, the first football clubs were amateur organizations, established to allow members to take exercise and enjoy the company of others. When the first controlling body of the game – the VFA – was formed, amateurism was strictly adhered to by the middle-class enthusiasts who saw the game as a “noble pastime” with a status above “that of a trade” (Crotty, 1998; Sheard, 1997; Pennings, 2012). Membership fees represented the first source of income to a football club. From these payments members gained the right to elect committees and office bearers, as well as entry to watch matches. Once the VFA was formed, allowing regular schedules of matches, club finances became more important. A growing enthusiasm for football drove increases in membership and increasing numbers of people who revealed a willingness to pay to watch matches. For example, an Argus reporter wrote of a game in 1890 that: [the] game drew together the largest assemblage that has ever been present at a football match in any part of the world. It was expected there would be an enormous attendance, and special measures were taken by the M.C.C. official to thoroughly check the numbers – 25,549 paid for admission, while 32,595 were actually present. In the old country the best attendance was at Glasgow in April of last year, in the match England against Scotland, when 28,000 paid for admission, and 30,000 in all were calculated to be present. (Argus, 25 April 1891: 12)

The importance of the general public to the early financial affairs of Australian Football clubs is evidenced by membership subscriptions and gate money accounting for over 90 per cent of most VFL club revenues from the period 1897–1909 (as represented in the financial reports of the clubs under scrutiny). Attaining higher membership and increasing gate takings required clubs to generate utility for spectators through winning matches. However, it was soon evident that VFA, and later VFL clubs faced a dilemma. Winning required clubs to compete with one another to attract the best players, and the growing popularity of the sport meant that the larger clubs could afford to make increasingly lucrative offers to potential players. Commentators feared that: … the accumulation of surplus resources will assist in developing various evils, chief among them a race of professional players who will reduce the game from its present high position as a fair, manly game to a mere bidding for gate money, with all its attendant curses of bookmaking, betting and scheming. (Cited by Sandercock and Turner, 1981: 41)

The early history of Australian Football was dominated by debates on professionalism and the issue of payments to football players. While deliberations within the League and its clubs are not visible to researchers due to a lack of primary evidence, much debate took place in contemporary newspapers, which were a primary form of disclosure and public communication about all matters of public life, including football. During the football season, newspapers provided regular reports on schedules, results and issues of controversy. Articles also appeared regularly outside of the season itself as matters arose in relation to players, individual clubs or the League. Newspapers also contained editorials and letters to the editor, which painted a picture of how football was perceived by the general public.

Questioning of the amateur nature of football continued through the first decade of the twentieth century, with widespread acknowledgement that the game was characterized by “veiled professionalism” (Argus, 11 May 1904: 5). A split between those who viewed professionalism as a pragmatic consequence of the evolution of the sport and those who saw it as destroying the game persisted. The Argus noted in 1908 that “The practice is to get the best men that can be obtained ‘for love or money’. If love be a sufficient inducement, so much the better; if it is not, the money will be forthcoming from some source” (30 March 1908: 4). Representing those supporting the ideals of amateurism, the Argus wrote “Most of the league clubs were tired of professionalism and desired its elimination, because professional men were spoiling the pastime” (13 August 1909: 4).

It had long been an acceptable practice for amateur clubs to cover players’ out-of-pocket expenses or lost wages through injury (Sloane, 1971; Dabscheck, 1975; Vamplew, 1982). While the VFL’s Rule 29 prohibited “Any player receiving payment, directly or indirectly, for his services as a footballer” (emphasis added), this did not include reimbursement of legitimate player-related expenses, such as travel costs. Broken-time payment and compensation for lost wages through injury was also accepted. Nevertheless, some club members and newspaper reporters scrutinized the annual reports of the individual clubs and were questioning the nature and extent of the rising player-related expenses shown in some financial statements. In particular, there was a concern that “rather devious tricks in bookkeeping have been adopted to cover up the fact” that players were paid by disclosing such payments under legitimate expenditure items (Argus, 30 March 1908: 4).

The potential misreporting of expenditures in club financial reports was further exposed when the strictly amateur Melbourne University Football Club (University) was admitted to the League in 1908. Comparison of the University annual reports with those of other supposedly amateur clubs was deemed by “Albert-Park”, in a letter to the editor: “an eye opener to the public, and has caused a considerable flutter amongst the Victorian Football League who loudly proclaim that there is no professionalism in league football” (Argus, 23 March 1909: 4). Not only were the total expenditures of University significantly less than those of other clubs, the nature of the items listed in its financial reports was also different. Further, the 1909 University accounting reports generated “remarkable” comparisons with Carlton and South Melbourne: “there are no charges [in University’s accounts] for such ‘items as ‘refreshments’, ‘medical and hot baths’, ‘insurance and allowances to injured players’, ‘loss of time’ and ‘accommodation’” (Argus, 15 March 1910: 6).

By the time the clubs provided their 1910 financial reports in early 1911, public debate regarding professionalism and the related disclosure of player payments had reached its zenith, with some of the clubs themselves acknowledging their misleading reporting practices and the need to change. At the 1910 Carlton annual general meeting (AGM), “keen interest was taken in the statement of the president as to the practice adopted by the club in preparing its balance sheets”, particularly in the non-reporting of £964 for payments to players. 6 “The reason the club’s balance sheet was prepared this way was due to the fact that the Carlton football club was one of the ten football clubs which were under the control, management, and rules of the Victorian Football League” (Argus, 17 March 1911: 9) and they were thus required to prepare accounts that indicated compliance with Rule 29. It was moved that “in the future the club prepare a true balance sheet showing the actual amount paid to players” (Argus, 17 March 1911: 9). On the same night as Carlton’s AGM, a “reform group” of dissatisfied Fitzroy club members met at a local hall to discuss the issue of player payments and their non-disclosure in the accounting reports. One of the main objectives of the group “was that all payments to players should be made, openly, and disclosed in the balance sheet”, because “the balance sheet of the club made it appear more amateur than it was” and these statements “were not worth reading”. It was explained at the meeting “that one player had received £50 for eleven matches, but this was not shown” (Argus, 17 March 1911: 9). As a result of the combined pressure from clubs, their members and the general public, in May 1911 the VFL voted to repeal Rule 29 and thus allow clubs to both directly pay players and to disclose such payments in their financial reports.

While historians have made reference to claims that clubs were misreporting player payments or excluding them from their financial reports (Sandercock and Turner, 1981; Sutherland et al., 1983; Pascoe, 1995; Frost, 1998; Hess, 1998; Hess et al., 2008), none have examined primary archival evidence of club disclosures in a systematic way. Thus, there is no evidence of the nature and extent of the disclosure of player-related expenditures, and no comparison of the actual disclosures of the individual clubs prior to 1911. If clubs were “hiding” player payments within their legitimate expenditure categories, the maintenance of an appearance of amateurism within the League would have required all clubs to present their expenditures in a similar manner. If they did not, comparisons between the clubs (in the manner undertaken by journalists when University joined the League) prior to 1911 would surely have exposed amateurism as a farce.

This article therefore examines the annual reports and financial statements of six clubs from 1909 to 1912 to address the following research question: To what extent did the financial reports of VFL clubs demonstrate attempts at legitimizing their behaviour regarding the amateur status of players?

Institutional legitimacy and isomorphism

Legitimacy theories, including institutional theory, deal with how organizational structures as a whole (for example capitalism or government) have gained acceptance from society at large (Tilling, 2004). Legitimacy is a process by which an organization gains approval or avoids sanction from groups in society (Kaplan and Ruland, 1991). Organizations operate in society by means of a social contract and satisfy stakeholders by behaving in a socially desirable manner (Brown and Deegan, 1998). Suchman (1995: 573–574) presents an encompassing definition of legitimacy as “the generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate” within a social system. Organizations seek to manage legitimacy because it helps to ensure the continued inflow of capital, labour and customers necessary for viability and pre-empts disruptive action (Neu et al., 1998; Tilling, 2004). O’Brien and Slack (2004: 15) note that “this drive for resources and legitimacy creates pressure for decision makers to make their organizations similar to those … in their institutional environment”.

Legitimacy theory has an important link with accounting-based research, as accounting practice involves a disclosure of information that in turn forms a source of legitimation. Irvine (2002: 3) states that “any organization that does not conform to societal expectations about how accounting ought to be performed and about accountability … risks losing legitimacy and ultimately funding”. Much of the prior accounting-based research which has used legitimacy theory has focused on environmental and social responsibility reporting and disclosures involving companies and organizations that added disclosure information to existing accounting reports (see for example, Patten, 1992; Deegan and Gordon, 1996; Adams et al., 1998; Wilmshurst and Frost, 2000; O’Dwyer, 2002). Such organizations use their annual reports to portray an image of being environmentally responsible, so that they will be perceived as such by society (Ahmad and Sulaiman, 2004). Legitimacy theory also suggests that companies may use voluntary disclosure to reduce their exposure to social and political costs by projecting an image of environmental awareness (Patten, 1992). While legitimacy theory proposes that organizations disclose positive information, Cho and Patten (2013) also noted that this incentive applies in particular to companies with poor records of environmental performance. In sum, corporate disclosure policies represent a method for management to influence external perceptions about their organization’s activities (Kent and Zunker, 2013). The disclosures improve perceptions of legitimacy.

The application of legitimacy theory in accounting research has to a large extent focused on examining the annual reports of large corporations (see for example, Deegan and Gordon, 1996; Adams et al., 1998; O’Dwyer, 2002). However, legitimacy theory has also been applied to not-for-profit organizations in a historical context. Irvine (2002) finds that the financial statements of the Salvation Army played a powerful legitimizing role, demonstrating that in the Army’s early years (1865–1892), “the organization used its financial statements to enhance and legitimise an image of financial reliability as a church and welfare service provider” (Irvine, 2002: 2). Churches that depended on the public for funds could not afford to ignore the societal requirements for accountability as demonstrated by the provision of audited financial statements, underpinned by a sound system of internal controls. “The presentation of audited financial statements was a valuable aid to assuring the public of the Army’s financial credentials and thereby securing a legitimate claim to the funds it required to continue its mission” (Irvine, 2002: 31).

Similarly, Normand and Wootton (2010) argue that the Chicago-based Northwestern Sanitary Commission, which existed between 1861 and 1865, used accounting reports to “legitimize actions, create an image of financial reliability as a welfare provider and fend off accusations of malfeasance” (Normand and Wootton, 2010: 113) as it came under scrutiny for its stewardship of donations received. Such means of legitimation were especially important for newly created organizations, which could not rely on a history of sound practice to convince donors of their reliability. Daniels et al. (2010) examine the accounting and financial reporting of the Charleston Orphan House from 1790 to 1795 and conclude that accounting and external reporting may have been legitimizing factors to overcome the liability of newness by promoting a sense of transparency among benefactors.

Research exploring historical legitimacy in not-for-profit organizations has largely focused on those that are newly created. Little research has concentrated on the use of financial reports to manage legitimacy within more established bodies. The connection between legitimacy theory and sporting clubs has been rarely considered in accounting research. This is a significant omission, as both amateur and professional sporting clubs are often highly visible organizations that rely heavily on the provision of resources from the community in terms of facilities, membership fees, athletes, donations, etc., and thus are expected to be accountable to the community from which they were derived (Morrow, 1999; Slack and Shrives, 2008). This is particularly so for a sport such as Australian Football, whose teams have historically comprised an integral component of their local communities (Frost et al., 2013).

Legitimacy is a core concept in institutional theory. Institutional theory considers how institutions and social structures, such as the VFL and individual clubs, contribute to legitimacy. DiMaggio and Powell (1983) outline the concept of isomorphism, a central and multifaceted concept of institutional theory. Isomorphism takes three forms: mimetic, coercive and normative. At the organizational level, isomorphism indicates the extent to which organizations are similar, that is mimetic, to certain attributes of other organizations in the same field, and is manifested empirically as increased conformity, such as in the presentation of financial reports (Han, 1994; Westphal et al., 1997; Deephouse and Carter, 2005). A fundamental proposition of institutional theory is that organizations compete for resources (such as playing talent), potential power and legitimacy (DiMaggio and Powell, 1983; Deephouse and Carter, 2005). Organizations conforming to commonly used strategies and practices appear rational and prudent to the social system. As a result, they are generally considered acceptable or legitimate and are thus able to attract necessary resources (Tolbert and Zucker, 1983). DiMaggio and Powell (1983) also identify the existence of coercive isomorphism, brought about by legislation or binding rules which compel specific behaviours, and normative isomorphism, in which common behaviours are compelled by mutual desire and usually the result of professionalism. These forms of isomorphism are used to explore the legitimation behaviours of the VFL clubs through their financial information.

Research method

This article explores the extent to which player payments were incorporated into club financial reports and the nature of such disclosure (or non-disclosure) prior to the rescission of Rule 29. Accordingly, efforts were made to obtain all VFL club annual reports for the two seasons before and after the legalization of professionalism (see Appendix 1 for a summary of the annual reports and financial information obtained for each club). This four-year period was chosen to ascertain the characteristics and significance of any change in reporting of payments to players before and after the abolition of Rule 29.

Financial statements contained in annual reports traditionally represent a vehicle by which an organization’s accountability is demonstrated to its stakeholders (Unerman, 2000), and have a high degree of credibility (Tilt, 1994). Financial reports have been historically noted as legitimizing the activities of organizations (Irvine, 2002; Daniels et al., 2010; Normand and Wootton, 2010). Napier (2002) also notes that it is fundamental that financial statements do indeed stand in some relationship to real transactions and events. Specifically for football clubs, Morrow (2006) reports that annual reports are a mass communication device capable of providing information to a wide range of groups and discharging accountability.

Financial reports (within the annual report) were distributed to members of VFL clubs at AGMs held around March each year. 7 The annual reports included narratives on matters relating to the on-field performance of the club, major issues pertaining to the management of the club, and the club’s financial position. In addition to a narrative commentary on club finances, the reports also contained a statement of the bank balance and receipts and expenditure items (usually called the “balance sheet”) and, occasionally, a statement of other assets and liabilities of the club. The financial accounts were audited, and the auditors’ names and addresses were listed.

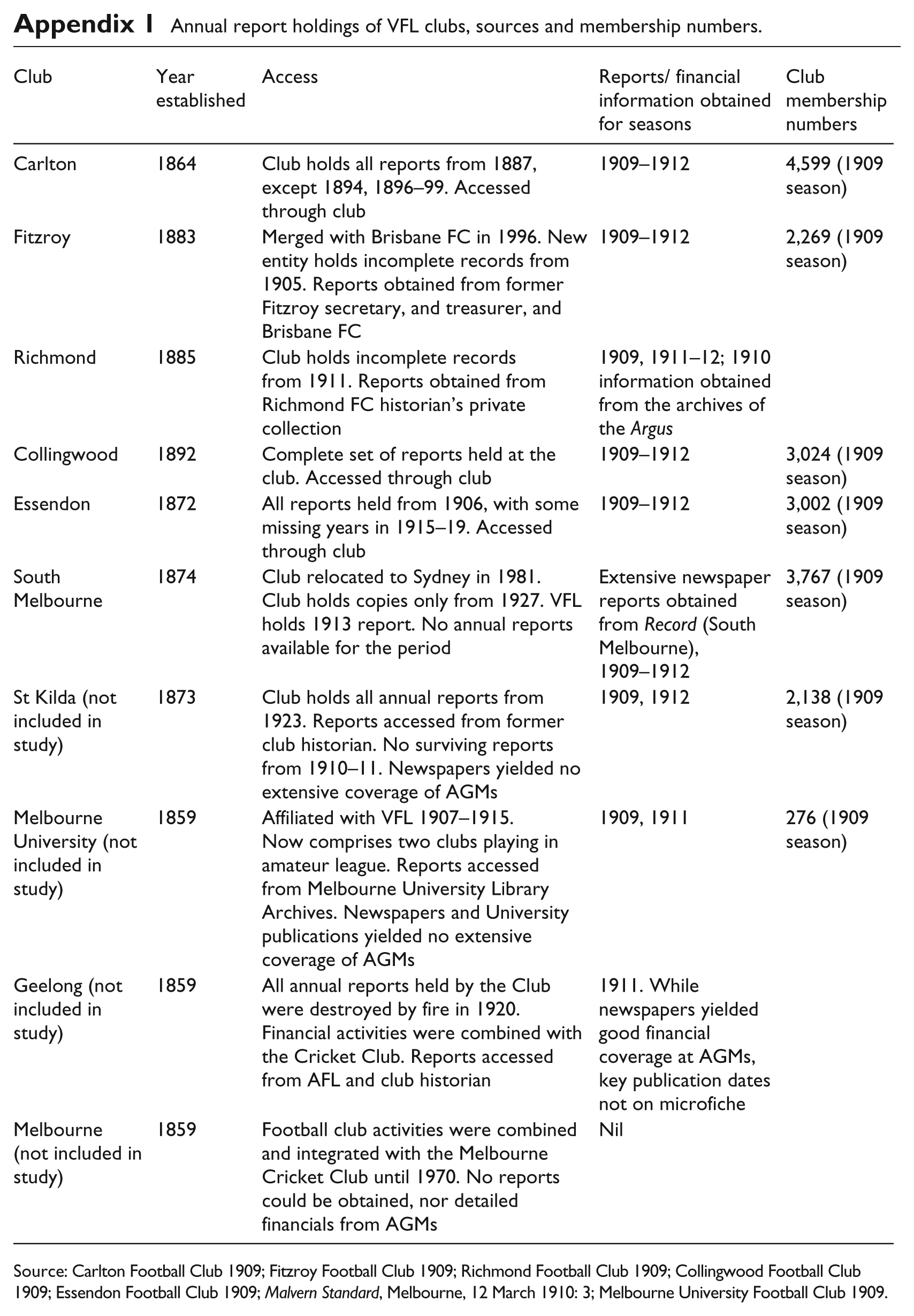

A critical element of the research for this article has been the collection of the individual clubs’ annual reports. Obtaining reports for most of the clubs required significant fieldwork, because no central archive of football records exists. Despite having rich histories, Australian Football clubs rarely maintain complete collections of their annual reports. Surviving reports are scattered in a piecemeal fashion in club archives, the personal holdings of historians and former club treasurers and secretaries, and public libraries. The VFL and the now Australian Football League (AFL) themselves hold only scant copies for the sample period. There has thus been a lengthy process of research and negotiation required to locate and obtain access to each of the documents utilized in this study.

Initially, each club was contacted by the researchers to ascertain the extent of their holdings and to negotiate permission to view any reports held. The majority of clubs did not hold relevant reports, in which case club officials and historians were asked to suggest the names of other persons or institutions that might have copies of the materials of interest. In turn, these additional people were contacted and an extensive process was engaged in to identify and access materials held. If the identified contacts did not have copies, they in turn were asked to suggest further persons of interest and the process was repeated with all newly proposed sources. The researchers also conducted a search (electronically and in person) of a number of archival sources, including the AFL archives, the State Libraries of Victoria and South Australia, the extensive collection of sporting books and documents at the Melbourne Cricket Club library, and a number of university and regional libraries.

Once all avenues for the collection of annual reports were exhausted, searches were then made of newspaper coverage of football clubs’ AGMs. In the period studied, it was common practice for local newspapers to contain detailed reports of the content of football clubs’ annual reports and the items discussed at the annual general meetings. Newspapers have been previously used to note financial information via these meetings (Maltby, 2004). To this end, the National Library of Australia’s Newspaper Digitisation Program (Trove) was utilized. Keyword searches focused on “annual general meetings”, “balance sheets” or “profits” with the names of the individual clubs where full annual reports were missing for the years required. While word searches resulted in many annual meetings being found, often the details of financial information were too brief, and thus not used. The quality of some digitization often lacked clarity – particularly for financial information. Where this was the case, searches were made on microfilm. Microfilm was also used for newspapers not digitized through Trove, but while this allowed a greater number of newspapers to be retrieved, again not all the financial information sought was included. Notwithstanding the above, some newspaper articles were located which adequately supplemented the annual reports.

Clubs were only included in this study if financial information could be obtained for each year of the sample period. Six clubs met this criterion (Carlton, Fitzroy, Richmond, Collingwood, Essendon and South Melbourne). St. Kilda, Melbourne, Geelong and Melbourne University were excluded from the analysis as a complete set of club reports could not be located (see Appendix 1 for a description of the available reports). In 1890, the heavy debts of the Melbourne Football Club were discharged by the MCC, with the latter subsequently administering the football club’s assets and expenditure until 1980 (Batchelder, 2005: 264). An MCC sub-committee that controlled football expenditure and team selection refused to play “working men” (Leader, 2 March 1907: 4). Geelong had strong links with local public schools and during the sample period many of its players were middle-class professionals who worked in Geelong. After Melbourne and Geelong finished last and second last respectively in 1906, an Argus writer concluded that this was because “by contrast with their rivals, they have accepted the amateur definition somewhat too literally, and they suffer accordingly” (Argus, 17 September 1906: 5). University, admitted to the League in 1908, abhorred professionalism and pledged to select only University graduates, current students or schoolboys (Cordner et al., 2007). Due to their amateur status, the exclusion of Melbourne, Geelong and University is not likely to affect the analysis of clubs’ reporting of player payments.

In order to maintain legitimacy as “amateur” clubs, it would be expected that all clubs paying players may use similar strategies to hide payments, explained by mimetics (DiMaggio and Powell, 1983; Han, 1994; Deephouse and Carter, 2005). Football histories suggest that hiding player payments within “other expense” categories was common (Sandercock and Turner, 1981; Sutherland et al., 1983). Therefore, the player-related expenditure of clubs (such as players’ insurance, travelling, teas and refreshments, uniforms, laundry, materials and medical) was examined in the two years prior to 1911 to show (1) what clubs were disclosing in relation to player expenditures when direct player payments were prohibited, and (2) whether there was any sudden change in such expenditures once player payments were permitted in 1911. An examination of the 1912 reports was undertaken to indicate whether such changes, if any, were ongoing. A significant increase in total player-related expenditures between 1910 and 1911 may indicate that player payments were not previously included in the financial statements. The absence of such an increase, accompanied by an item for player payments in 1911, may suggest that player payments were being included in prior years, but not explicitly disclosed. The narratives from both the annual reports and the newspapers were used to support the financial information obtained. The research method applied was similar to that adopted by Halabi et al. (2012) and allows comparisons and conclusion to be reached regarding the majority of VFL clubs at the time. Information on total expenditures and revenues was also used to obtain a detailed analysis of the total financial position of the clubs.

Results

Total player related expenditure, total expenditure and revenues for individual clubs are presented and discussed below.

Carlton

Carlton is the oldest of the sample clubs (formed in 1864). It drew on a substantial local supporter base and the capacity of its home ground was the largest of the sample clubs. Carlton was very successful in the early 1900s, winning premierships in 1906, 1907 and 1908. Increasing crowds generated more revenue for the Club, but this led to discontent among many of the players over their share of the success (Frost, 1998). Between 1905 and 1908, total revenue increased by 51 per cent, while payments to players increased by only 16 per cent (Frost, 1998). By the start of the 1909 season, negotiations between several players and the committee had broken down over the issue of match payments, with some players refusing to train or play in the opening round. It is thus anticipated that Carton would have had some element of player payments within their expenditures.

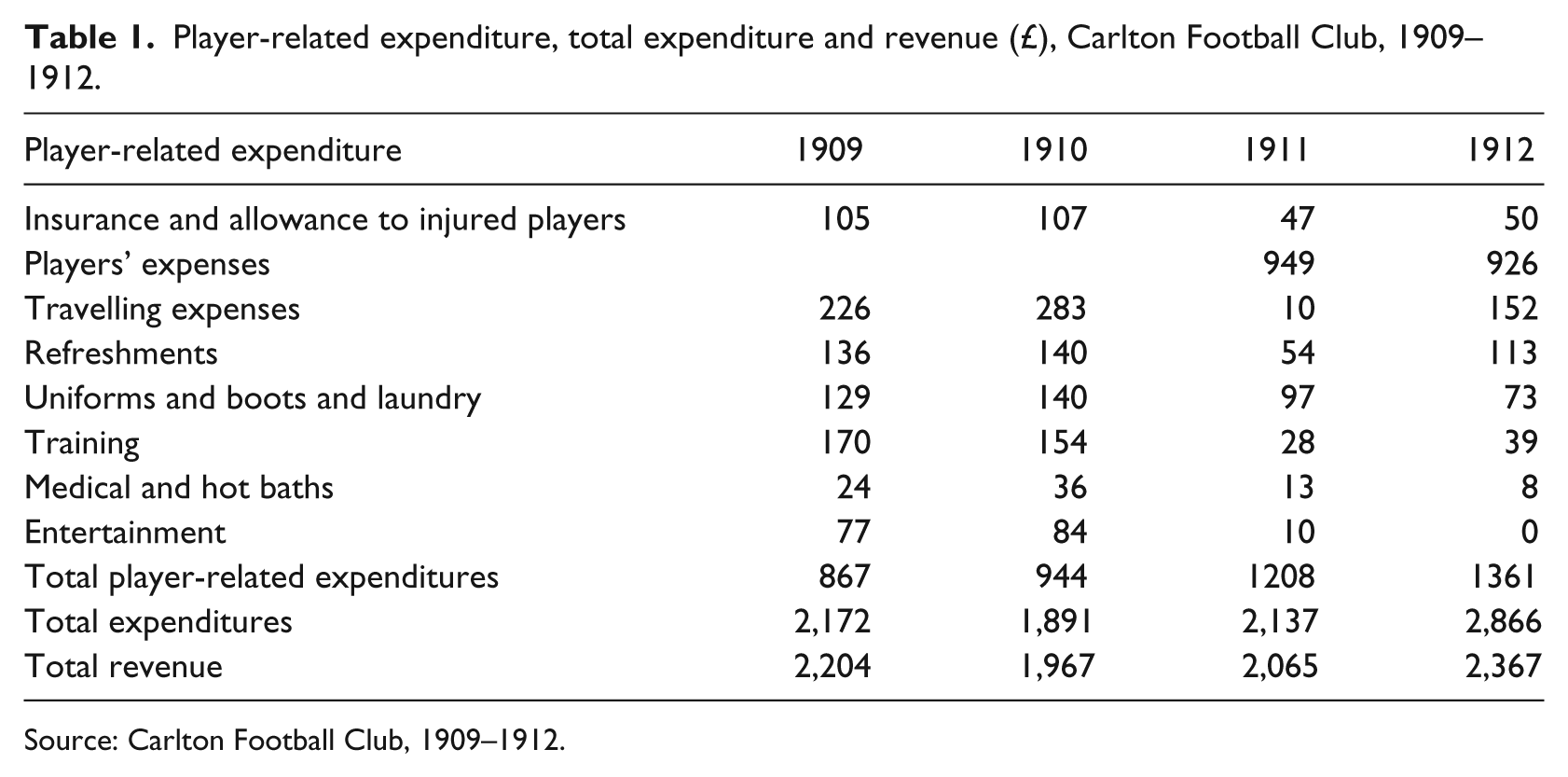

Table 1 shows detailed accounts for Carlton for the sample period. The expenditures show an absence of an expenditure line specifying payments to players (“Player expenses”) until 1911 (£949). While “Player expenses” increased in 1911, a significantly lesser increase in total player related expenditures was made between 1910 and 1911 (£264), and total expenditures (£246).

Player-related expenditure, total expenditure and revenue (£), Carlton Football Club, 1909–1912.

Source: Carlton Football Club, 1909–1912.

Table 1 shows that before 1911 player payments were hidden in four other expense categories: training, travelling, refreshments, and uniforms and boots and laundry. The total reduction in these expenses between 1910 and 1911 (£545) accounted for 57 per cent of a new expense category called “Player expenses”. Revenue increased by £98 in 1911, and the Club financed the remainder of its player payments by running down its 1910 surplus and recording a deficit in 1911. Therefore, prior to 1911 Carlton used its financial reports to legitimize itself as an amateur football club that was a generous supporter of players (via indirect and acceptable player-related expense categories) rather than revealing itself as one in breach of the prohibition on player payments. From 1911, Carlton legitimized itself as a payer of players via the direct “Player expenses” category. Carlton’s total player payments in the first season of professionalism were 49 per cent higher than the average of the five other sample clubs.

Fitzroy

In terms of premierships, Fitzroy was the most successful VFL club from 1897 to 1908, winning four grand finals. However, the club was weak financially relative to other clubs. Though an Age reporter noted in 1902 that Fitzroy’s administration “conducts its affairs in a scrupulous manner … and in consequence there is no institution connected with the game occupying a more prosperous or enviable position” (Age, 19 May 1902: 7), the low capacity of the Club’s home ground limited the growth of revenue.

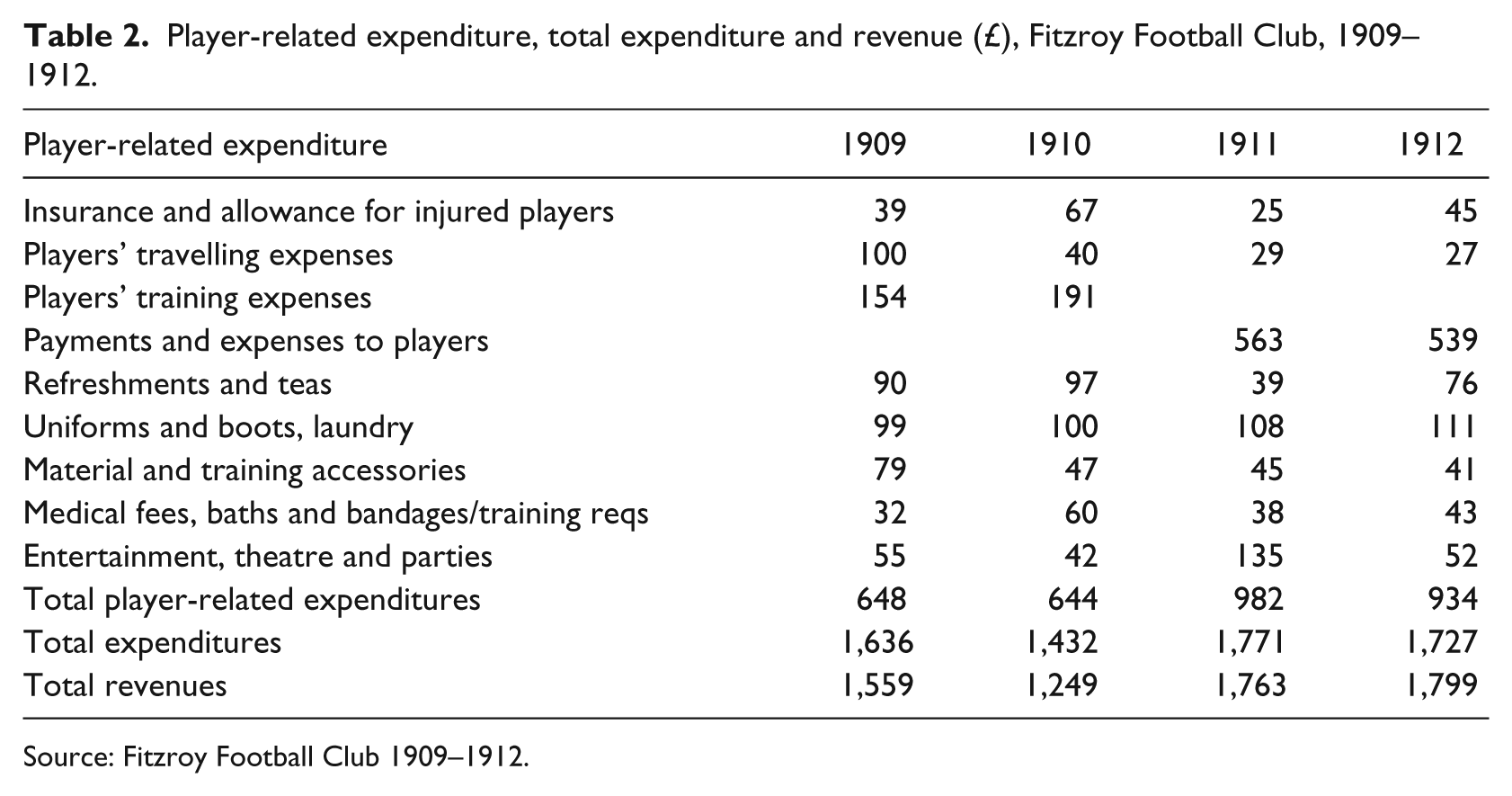

Table 2 shows the introduction of an account titled “Payments and expenses to players” of £563 in 1911. Total player-related expenses increased by 48.3 per cent between 1910 and 1911 (from £644 to £982), while total expenditures increased by 23.7 per cent (from £1,432 to £1,771). Like Carlton, Fitzroy provides an example of mimetic isomorphism, in that the classification and presentation of payments made to players were substantially similar. While some new expenditure for player expenses appears in 1911, much of the total was already being included in the accounts under similar headings as at Carlton. However, Fitzroy’s 1910 expenditure for training expenses, travelling expenses, refreshments and insurance and allowances for injured players was only 58 per cent of that of Carlton’s for the same categories. 8 This suggests that Fitzroy was less likely to be using these expenditure items to conceal player payments than Carlton. Reductions in these items accounted for 53.6 per cent of Fitzroy’s new payments category. An increase in total revenue of £514 between 1910 and 1911 was almost sufficient to finance Fitzroy’s player payments.

Player-related expenditure, total expenditure and revenue (£), Fitzroy Football Club, 1909–1912.

Source: Fitzroy Football Club 1909–1912.

Evidence of “hidden” player payments in Fitzroy’s 1910 accounts is supported by a newspaper article which summed up the 1911 season, where it was reported that: At the last annual general meeting a large majority of the members of the [Fitzroy] club who desired that certain items of expenditure, more particularly in reference to the players, should be more clearly stated on the balance sheet elected a new committee to carry out a reform in that direction. (Argus, 11 March 1912: 5)

While not included in the player-related expenditures listed in Table 2, a large expenditure item was the “club trip”. 9 This cost £379 in 1909, and £305 in 1910 (no trip was made in 1911 or 1912). If the cost of the trip is added into normal player-related expenditures, there was no rise between 1910 and 1911 in the amount shown in the financial reports as being spent on “players”. The amount paid to players and the yearly trip offset each other and in 1911, once direct player payments were introduced, trips were discontinued. It is thus possible that player payments were also being hidden within the expenditures recorded for club trips prior to 1911, or that club trips were eliminated in order to fund player payments. As Carlton did not have any trips recorded in its financial reports for the 1909–1911 period, a comparison of accounting treatment is not possible.

Richmond

Formed in 1885, Richmond was admitted into the VFL in 1908 on the back of “a long and honorable history and a splendid record” in the VFA (Argus, 19 October 1907: 19). Richmond’s premiership success in 1902 and 1905 made it the VFA’s strongest club in terms of support and finances. By 1905, Richmond matches accounted for one third of the VFA’s total gate receipts (Ruddell, 2007).

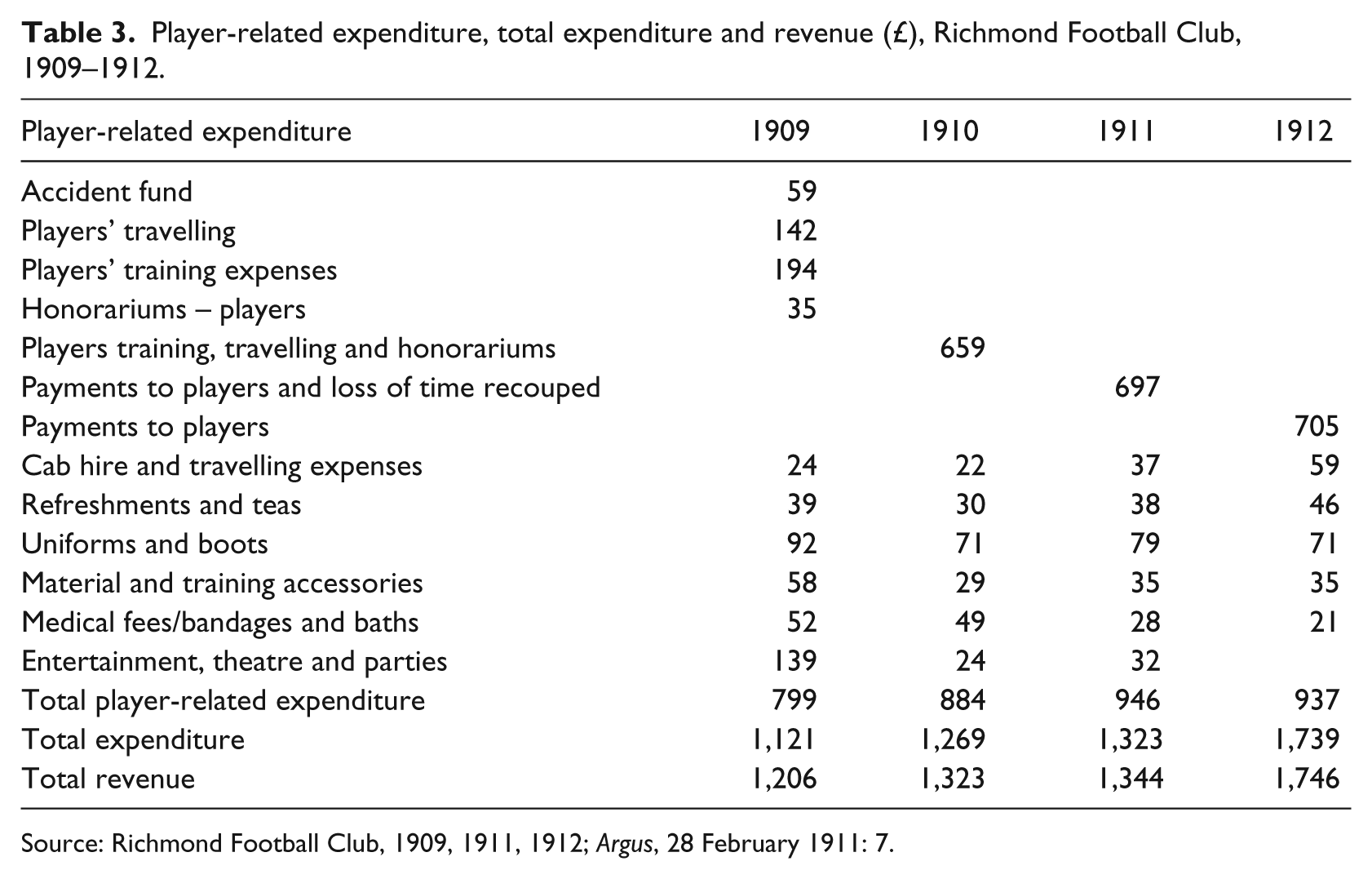

Table 3 shows only a slight increase in Richmond’s total player-related expenses over the period studied. Itemized amounts for “Players’ travelling”, “Players’ training expenses”, and “Honorariums – players” from 1909 are not shown in 1910; rather this is consolidated into a one line item for “Players’ training, travelling and honorariums” of £659 10 (in 1909 these amounts individually came to £371). In 1911, “Payments to players and loss of time recouped” appeared, while “Players’ training, travelling and honorariums” disappeared. While this was in accordance with Rule 29, the similarity of amounts suggests that Richmond’s player payments were hidden in this 1910 “Players’ training, travelling and honorariums” account.

Player-related expenditure, total expenditure and revenue (£), Richmond Football Club, 1909–1912.

Source: Richmond Football Club, 1909, 1911, 1912; Argus, 28 February 1911: 7.

Of the other expenses changing between 1910 and 1911 only medical fees (£49 to £28) decreased, while “entertainments” were £139 in 1909 and £32 in 1911. There was little overall change in Richmond’s total expenditures and revenues after player payments were legalized. The introduction of a club trip (cost of £272), funded by a bazaar (£374), accounted for 65 per cent of the increase in total expenditure in 1912.

Prior to 1911, Richmond incorporated payments under headings such as training, travelling, honorariums, in a similar manner to Carlton and Fitzroy. A strong mimetic tendency amongst these clubs is evident, in terms of both the classifications of reporting expenses and the methods by which payments for services were being hidden. However, Richmond had a large increase in these items in 1910, so it seems to have brought much of its player payments into the financial report in 1910, or significantly increased payments to players in that year. It also appears to have introduced greater clarity in its reports earlier than Carlton, by identifying in 1910 the extent of its payments being made directly to players (if portrayed as “reimbursements” rather than payment for services), rather than possibly “hiding” the expenditures across all of its indirect player-related expense items as it appeared to have done in 1909. There is evidence of the challenges faced by the club in preparing its financial reports in the Richmond 1911 Annual Report: Your committee have had some difficulty prior to this season in producing a balance-sheet and in consequence a few unscrupulous and cowardly persons have been mean enough to make scurrilous statements regarding the same; but thanks for the VFL league resolution re open payment to players, your Executive are in a position to bring before you a balance-sheet audited by a certified auditor. (Richmond Football Club, 1911: 7)

Collingwood

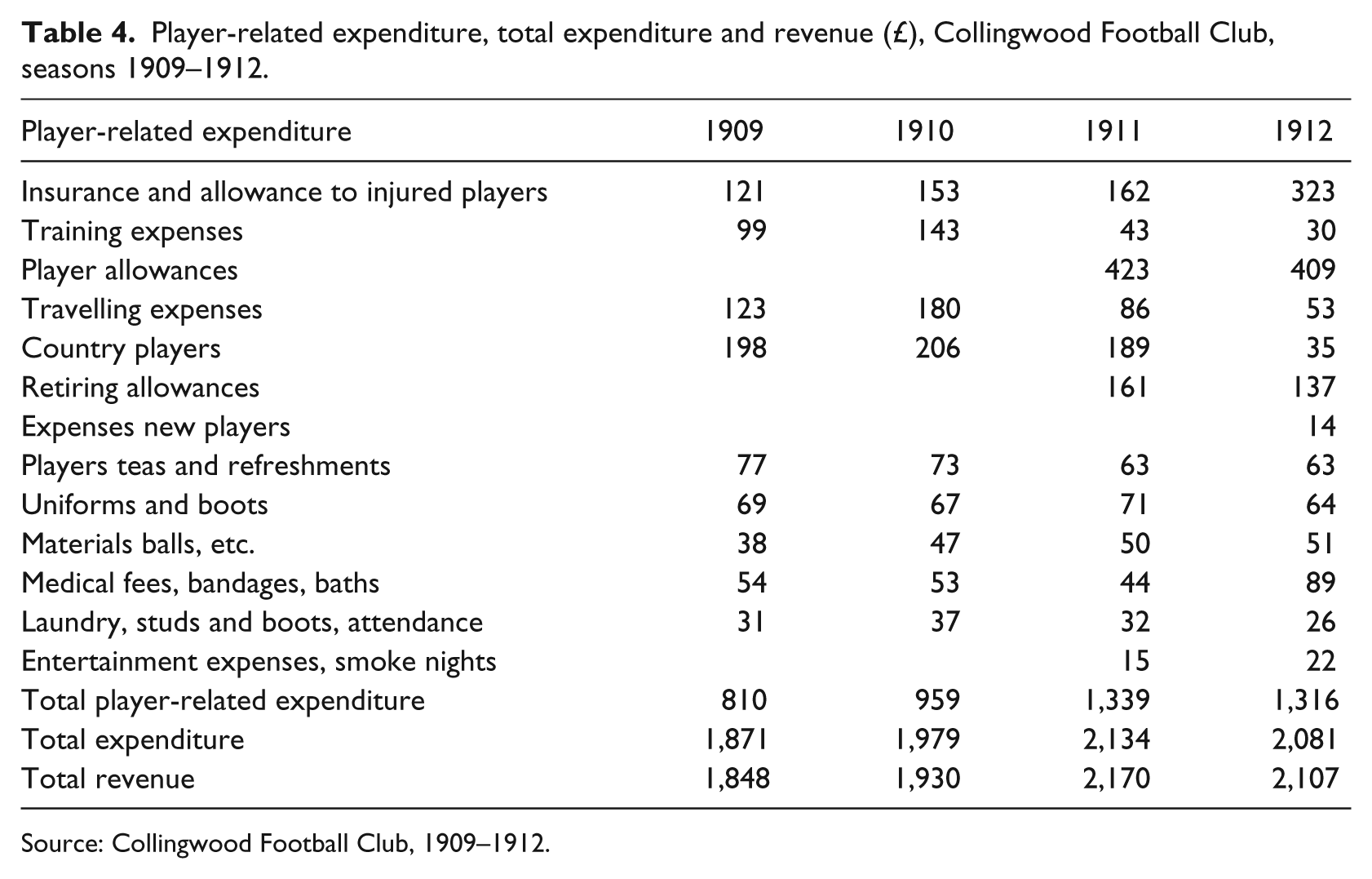

Formed in 1892, the Collingwood Football Club is the youngest of the sample, yet quickly became successful both on and off the field, winning VFL premierships in 1902 and 1903, and again in 1910. Located in one of Melbourne’s poorest suburbs, the club prided itself on the strength of its links with the local community. Collingwood maintained a publically stated philosophy of amateurism, declaring that “it will not play any man who is not regularly engaged in some other occupation than football” (Argus, 20 May 1910: 7). Since 1898, the Club pursued a policy of reimbursing players equally for travelling and other expenses to ensure solidarity and avoid factionalism amongst its teams (Stremski, 1986).

Table 4 shows a significant increase of £380 in player-related expenditures between 1910 and 1911 (from £959 to £1,339). There was also a clear change in the presentation of the accounts, with the introduction of “player allowances” and “retiring allowances” (totalling £584) in 1911. The only substantial change to other player-related expenditure from 1910 to 1911 was a reduction in “training expenses” and “travelling expenses” totalling £294. This accounted for only 33 per cent of player payment items. Growth of total revenue (£240) and reduced expenditure of club trips (£234) 11 were equivalent to 81 per cent of Collingwood’s player payments in 1911.

Player-related expenditure, total expenditure and revenue (£), Collingwood Football Club, seasons 1909–1912.

Source: Collingwood Football Club, 1909–1912.

While Collingwood introduced a far greater proportionate increase in player expenditures into the 1911 accounts than other clubs, the re-allocation of expenditures from categories such as “training” and “travelling” to player allowances reflects the same disclosure practices as exhibited by Carlton, Fitzroy and Richmond. However, Collingwood had a history of open disclosure regarding the nature of player-related payments, with such payments primarily for indirect activities relating to football, such as travelling reimbursements, rather than direct payment for the services of players. On average, the reduction in these payments from 1910 to 1911 at Collingwood and Fitzroy was 52 per cent of that of the other sample clubs, which suggests that the former two clubs were less likely to be concealing player payments in these categories before professionalism was legalized. Collingwood was the only club in the sample to openly discuss its new wages scheme introduced in 1911. This maintained the philosophy that all players were valued equally as members of a team. All senior players signed contracts with a standard match fee (Stremski, 1986). It was noted in the Collingwood 1911 Annual Report that: [T]he discontent which spread like an epidemic amongst League players at the beginning of the season showed signs of breaking forth at Victoria Park. However the counsels of the older players prevailed, and the Committee being approached in the proper spirit, a conference of players and Committee ensued at which the details of a scheme of remuneration to players proposed by your Hon. Secretary (Mr Copeland), were carefully explained. The players unanimously adopted the scheme, which was later confirmed by your committee and a happy season followed. (Collingwood Football Club, 1911: 9)

Essendon

Formed in 1872, Essendon Football Club became a powerful VFA club. Essendon’s profits increased from £16 in 1884 to £343 in 1890 and the Club was first accused of making payments to players and potential recruits in 1886. These claims were repeated as the club won premierships in 1891, 1892, 1893 and 1894 (Frost, 2005). After winning the inaugural VFL premiership in 1897, and another in 1902, the club went through a series of lean seasons. In 1907 the club responded with aggressive player recruiting, offering competitive match payments to players from surrounding clubs (Maplestone, 1994). Essendon was again the premier team in 1911 and 1912.

Table 5 shows almost no change in Essendon’s total player-related expenditure from 1910 to 1911. The primary change in the financial report was the introduction in 1911 of a new item for “Player expenses” of £627 and the removal of the previous year’s expenditure categories of “Expenses of players” and “Expenses of country players”, which reduced expenditure by £590. While Essendon’s total expenditures increased from £1,719 in 1910 to £1,938 in 1911, this was largely due to the net expenditure of a “holiday tour” in a premiership year. Revenues for the club changed only slightly from year to year, suggesting that there was little extra money available to pay players and the additional expenditure in 1911 was funded by running down the debit bank balance of £80 to a credit of £151 at the end of 1911.

Player-related expenditure, total expenditure and revenue (£), Essendon Football Club, 1909–1912.

Source: Essendon Football Club, 1909–1912.

Essendon reported a significantly larger increase in total player-related expenses from 1909 to 1910 than other clubs (with a corresponding increase in the item “Expenses of players” from £201 in 1909 to £491 in 1910), suggesting, consistent with the reports of their player recruitment drive over this period, that they may have introduced or increased player payments at this time. Furthermore, the narratives in the 1911 annual report make no mention of “new” payments of players. In relation to the 1910 season, the Argus noted that the Essendon president: said that the committee … had decided to notify incoming delegates that they were in favour of paying players a limited sum of money. … Everybody knew that the club was paying certain players £1 per week. Other players were paid according to their worth (Laughter). (Argus, 23 March 1911: 5)

This observation supports the conclusion regarding the financial reports for the 1910 season, that a substantial proportion of such player payments were already being included in the Essendon accounts prior to 1911. A further point of difference between the financial report provided by Essendon and those of other clubs is in the nomenclature used prior to 1911. In common with the other clubs, Essendon introduced a new expenditure category for player payments (“Player expenses”) in 1911. However, in previous years, they did not attempt to portray player-related expenditures as pertaining to a specific indirect activity such as “training” or “travelling” but rather used the very general description of “Expenses of players”, which was quite similar to their new expenditure category post-Rule 29.

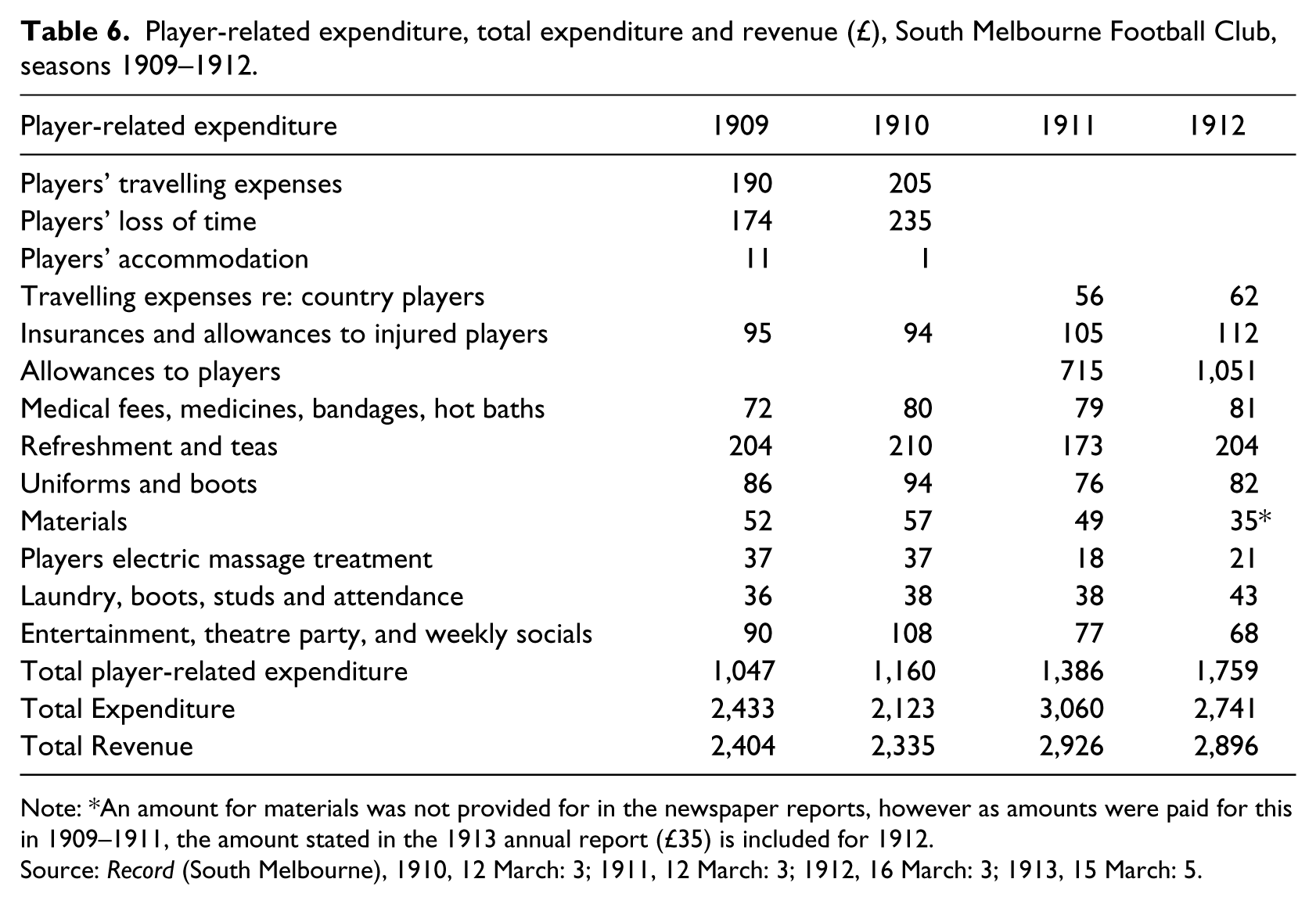

South Melbourne

The South Melbourne Football Club was a founding member of the VFA and one of its most powerful clubs, winning five premierships by 1890. Though it represented Melbourne’s most populous municipality, it had to wait until 1909 to become a premier in the VFL. South Melbourne drew on a large supporter base, which was evidenced when, after having won its first VFL premiership in 1909, the Club had to hold its 1909 annual general meeting in the open air, with “about 7000 persons” present (Argus, 9 March 1909: 8).

Table 6 shows the introduction of an account titled “Allowance to players” of £715 in 1911. Total player-related expenses increased by £226 between 1910 and 1911, while total expenditure soared by £937. 12 South Melbourne’s expenditure was significantly higher than that of other clubs, and was described by the Argus (7 March 1910: 6) as “extraordinary” during their premiership year, with the comment that “If an amateur premiership costs £2433, what would be the outlay with professional players?” In 1912, when South Melbourne finished second, its wages bill was 36 per cent higher than that of the premier team, Essendon, and 94 per cent higher than the average of Collingwood and Fitzroy.

Player-related expenditure, total expenditure and revenue (£), South Melbourne Football Club, seasons 1909–1912.

Note: *An amount for materials was not provided for in the newspaper reports, however as amounts were paid for this in 1909–1911, the amount stated in the 1913 annual report (£35) is included for 1912.

Most of South’s player payments prior to 1911 were hidden in other expense items. Expenses that were no longer reported in 1911, such as “Players’ travelling expenses”, “Players’ loss of time” and “Players’ accommodation” reduced expenditure by £440, equivalent to 61.5 per cent of the growth in expenditure on “players allowances”. The remaining player-related expenditures remained constant throughout the period. Thus, South Melbourne’s “players allowance” introduced in 1911 was being included in previous years’ accounts in a manner consistent with practices at Carlton, Fitzroy and Richmond, legitimizing their status as amateur while providing generous payments to players.

Suggestions that player payments were “hidden” in the 1909 and 1910 accounts is supported by the Club Chairman in a newspaper report of the 1911 AGM: As would no doubt have been noticed there has been an alteration in the presentation of expenditure. For obvious reasons the portion of the annual statement has been submitted in different form in past seasons. Last year there was considerable agitation amongst football supporters who contended that those who played the game should receive better recognition at the hands of the clubs. It was further urged that the clubs should not cover up that expenditure under false headings. This year, therefore, the local committee decided to place clearly before members the exact amount spent in this particular direction. (Record (South Melbourne), 16 March 1912: 3)

Discussion

Examination of the financial reporting of player payments reveals that the majority of individual clubs attempted to legitimate an image of amateurism prior to 1911 by reporting large expenditures on the indirect support of players, particularly for “training expenses” and “travelling expenses”, in their financial reports. Once Rule 29 was deleted in 1911, all of the sample clubs showed an item for “Payments to players” or “Player expenses” in their annual financial reports, indicating that they were now directly paying players. For many clubs, the introduction of the new expense item for “Player expenses” was not the only major change to club expenditures reported. Rather, expenditures previously attributed to “Training” and “Travelling”, as well as some other expense categories, were significantly reduced in 1911, with the result that the overall increase (or lack of increase) in total player-related expenditures following the demise of Rule 29 was significantly less than the “player expense” accounts would otherwise indicate. Only Collingwood, and possibly Fitzroy, appear to have practised the amateurism that their 1909 and 1910 accounts reported. The relative increase in their total player-related expenditure from 1910 to 1911, which averaged 44.8 per cent compared to 13.4 per cent for the other sample clubs, suggests that earlier spending on players was less likely to be happening, although disguised in other categories, as occurred at other clubs. Collingwood and Fitzroy report spending less on training, travelling and similar expenditure items than other clubs prior to 1911. The other four clubs appear to have deliberately concealed illegal player payments within other legitimate expenditure categories in their annual financial reports. Furthermore, they used their financial reports to signal that there had been a change in the nature of their player payment practices in 1911. In this manner, the financial reports were used to legitimate an appearance that the clubs had moved from amateur to professional status.

Organized sport brought with it an inevitable element of community rivalry (Sheard, 1997) and it is this that brings into focus the institutional factors which explain the actions of the VFL clubs examined here. The article has validated that the presentation of the annual financial reports of VFL clubs demonstrated a mimetic tendency – that is, the classification of payments to players were largely standardized amongst the majority. It is also demonstrated that following the repeal of Rule 29 in 1911, substantial changes occurred to the classification for most of the clubs. It is thus evident that clubs were coerced into presenting an image of amateurism that conformed to both League rules and the expectation of society that they were community sporting organizations rather than businesses (Westphal et al., 1997; Deephouse and Carter, 2005).

However, whilst mimetic tendencies may explain the development of roughly uniform presentation of the financial reports of clubs – the like classification of various player-related expenses – it is insufficient to provide a broader explanation of the forces working to make professionalism in the VFL as inevitable as in other sports around the world at the time, and the controversy and actions brought in by organizing bodies to combat this tide.

Institutional theory provides other isomorphisms which gives a theoretical framework in which to understand the forces at play. Normative isomorphism is associated with professionalism – the creation and imposition of normative behaviours. As clubs garnered increasing community support and community identity was increasingly based on sporting club success, the players became subject to increasing control over their sport-related activity, including training requirements. In response to such normative pressures, and in increasing recognition of their importance to clubs and communities, players brought pressure to bear for additional payment (Sheard, 1997). With the VFL fixtures taking place on Saturdays, a normal working day for most manual labourers, the sacrifice of income, in their eyes, warranted compensation.

Coercive isomorphism was also at work. Rule 29 prohibited the payment of players as professionals. The promotion of amateurism was consistent with the prevailing sporting institutions in Australia and around the world. Coercive pressure to conform, and appear to conform, to the amateur ideal required that clubs be creative and/or secretive in meeting increasing demands for player payments. Suchman (1995: 579) notes that “organizations often put forth cynically self-serving claims of moral propriety and buttress these claims with hollow symbolic gestures”. In the case of the VFL clubs explored in this article, this gesture was fraudulent financial reports, designed to show the generosity of clubs in supporting their players whilst hiding the true nature of the payments – that is, remuneration for professional services as football players. That such behaviours were an open secret provided legitimation for the production of the fraudulent report (Lewis, 1997).

While this article has provided a unique exploration of the player payment disclosure practices of the major VFL clubs in the early twentieth century, it has been subject to several limitations. While annual reports and financial information could only be located for six of the 10 VFL clubs, this does not represent a significant constraint on the findings, as three of the remaining clubs were relatively small and operated on a genuinely amateur basis and thus would not have exhibited comparable disclosure practices. Further, while this article has provided a clear description of how clubs were disclosing player payments within their financial reports, a lack of available data means it has been unable to provide a deep exploration of the processes by which the clubs decided to make such disclosures (or non-disclosures). Although minutes and other supporting documentation were sought for all clubs, none was available. Minutes for the relevant period were obtained from the VFL, but contained no detail of any discussions pertaining to Rule 29. Offsetting this deficiency of data was the tendency of local newspapers to provide detailed reports of meetings of club members and to publish letters to the editor and opinion pieces regarding player payments. While such data meant some understanding could be gained of the reasons underpinning the actual disclosures made, the contents of the newspapers are subject to limitations as the reports are likely to be incomplete and biased by the interests of the reporter.

Conclusion

This article has provided unique insights into the nature and extent of the reporting of player payments in the VFL both before and after the formal introduction of professionalism in 1911. General football histories often acknowledge the rumours that the practice of making payments to so-called amateur players was widespread, yet histories of Australian Football clubs have not presented detailed financial evidence to support such claims, nor have they systematically compared the disclosure of player payments amongst clubs. The location and analysis of the financial reports of individual VFL clubs for 1909–1912 demonstrates that clubs were both paying players prior to 1911 out of club funds and were fraudulently disclosing such payments as legitimate expenses. A consideration of the isomorphic institutional pressures experienced by the clubs at the time shows that the clubs adopted common disclosure practices to enable them to use their financial reports to legitimate themselves as amateur sporting organizations prior to the legalization of player payments and as having introduced such payments once professionalism was permitted. With payments to players remaining a controversial issue around the world, examining the practices of sporting competitions in the period where professionalization occurred provides valuable insight into the dubious disclosure practices and fraudulent reporting which were used to hide payments. This lends evidence in suggesting such methods of hiding payments may still be used today.

Footnotes

Appendix

Annual report holdings of VFL clubs, sources and membership numbers.

| Club | Year established | Access | Reports/ financial information obtained for seasons | Club membership numbers |

|---|---|---|---|---|

| Carlton | 1864 | Club holds all reports from 1887, except 1894, 1896–99. Accessed through club | 1909–1912 | 4,599 (1909 season) |

| Fitzroy | 1883 | Merged with Brisbane FC in 1996. New entity holds incomplete records from 1905. Reports obtained from former Fitzroy secretary, and treasurer, and Brisbane FC | 1909–1912 | 2,269 (1909 season) |

| Richmond | 1885 | Club holds incomplete records from 1911. Reports obtained from Richmond FC historian’s private collection | 1909, 1911–12; 1910 information obtained from the archives of the Argus | |

| Collingwood | 1892 | Complete set of reports held at the club. Accessed through club | 1909–1912 | 3,024 (1909 season) |

| Essendon | 1872 | All reports held from 1906, with some missing years in 1915–19. Accessed through club | 1909–1912 | 3,002 (1909 season) |

| South Melbourne | 1874 | Club relocated to Sydney in 1981. Club holds copies only from 1927. VFL holds 1913 report. No annual reports available for the period | Extensive newspaper reports obtained from Record (South Melbourne), 1909–1912 | 3,767 (1909 season) |

| St Kilda (not included in study) | 1873 | Club holds all annual reports from 1923. Reports accessed from former club historian. No surviving reports from 1910–11. Newspapers yielded no extensive coverage of AGMs | 1909, 1912 | 2,138 (1909 season) |

| Melbourne University (not included in study) | 1859 | Affiliated with VFL 1907–1915. Now comprises two clubs playing in amateur league. Reports accessed from Melbourne University Library Archives. Newspapers and University publications yielded no extensive coverage of AGMs | 1909, 1911 | 276 (1909 season) |

| Geelong (not included in study) | 1859 | All annual reports held by the Club were destroyed by fire in 1920. Financial activities were combined with the Cricket Club. Reports accessed from AFL and club historian | 1911. While newspapers yielded good financial coverage at AGMs, key publication dates not on microfiche | |

| Melbourne (not included in study) | 1859 | Football club activities were combined and integrated with the Melbourne Cricket Club until 1970. No reports could be obtained, nor detailed financials from AGMs | Nil |

Acknowledgements

The authors acknowledge the helpful comments of the three anonymous reviewers and the support and encouragement provided by joint guest editor Brad Potter, who managed the refereeing process in respect to this submission. The authors also acknowledge the co-operative support from AFL historians Col Hutchinson and Cameron Sinclair, and Melbourne Cricket Club historian Trevor Ruddell.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.