Abstract

The aim of this article is to describe the role played by accounting in an industrial company in which elements of utopian socialism and capitalism co-existed. The case is the Royal Silk Factory founded by King Ferdinand IV at San Leucio, near Caserta in 1778. The article covers the years 1802–1826. In this hybrid institution, double-entry bookkeeping (DEB) was adopted to calculate the minimum profit rate owed to the capitalist shareholders, while ‘labour accounting’ measured the workers’ performance. The surplus value was shared between the enterprise and the workers. This article makes a number of contributions to the accounting history literature: First, it adds archival evidence of accounting practices in Italian industrial companies; second, it supports the close connection between DEB and capitalism; third, it shows that the accounting system is set up to reflect the different social organisation of a manufacturing company; and finally, it illustrates how the accounting system makes the wealth-generating and wealth-distributing processes accountable.

Introduction

The international accounting history literature focusing on industrial companies which do not meet all capitalistic requirements is limited when compared with that which deals with capitalistic firms. The reason for this is that over the last three centuries, these kinds of experiences have been relatively rare in countries around the world. In the international accounting history literature, some contributions emerge (Davie, 2007; Funnell, 2004; Walsh and Stewart, 1993). However, so far, none can be found from Italy. To fill this gap, the aim of this article is to examine the role played by accounting in a hybrid context, the Royal Silk Factory of San Leucio (hereinafter, RSFSL), between the late eighteenth century and the early nineteenth century, from an institutional, social and economic position.

There are several reasons for focusing on the RSFSL. First, it is the earliest ‘socialist experiment’ in the Western world, as it occurred a few years before those better known to the international historical literature, such as New Lanark and Orbiston. Second, the RSFSL experience also precedes the theme of utopian socialist theories. It starts in the late eighteenth century, while the first works on utopian socialism by Saint-Simon, Owen and Fourier date back to the early nineteenth century. Last, the RSFSL is also a case in which public and private investors became shareholders of a large Italian manufacturing company, one of the first of its kind in Italy. The findings show, on one hand, the role played by double-entry bookkeeping (DEB) in measuring the capital, the profit and the rate of return, and on the other hand, the role played by labour accounting in measuring workers’ performance.

This article makes a number of contributions to the accounting history literature. It describes the accounting system of a factory that is closely interconnected with a social community of reference, which is unprecedented if we look at the earlier accounting history of private or public companies. This article also shows how accounting reflects the hybrid character, capitalistic and non-capitalistic, of the economic and social organisation to which it is applied. Finally, we show how the accounting system was used to make a number of processes visible and accountable in a way that cannot be found in organisations in that form at that time.

The article is structured as follows. The next section is devoted to the research method, reviewing the literature, focusing on the theoretical framework and showing the sources of the article. The political and social context in which the community of San Leucio grew, was shaped and established, and gives prominence to the productive and organisational traits of the RSFSL is then described. The section ‘Findings on the accounting system of RSFSL’ shows the different roles played by accounting and its effects on the organisation and the communal institution, respectively, in terms of financial accounting and labour accounting. A discussion of the RSFSL case follows. Finally, the conclusions are drawn, with a summary of the results achieved, the limitations of the article and any potential developments for future research.

Research method

Literature review

The international accounting history literature dealing with industrial companies in capitalist contexts is extremely wide. It supports the close bond that exists between DEB and capitalism, showing the role played by financial accounting in supporting decision making by external parties (Edwards, 1989; Littleton, 1933; Pollard, 1963). Critical studies have emphasised the importance of accounting in capitalist enterprises after the Industrial Revolution, through different theoretical approaches. These include the socio-institutional (Chapman et al., 2009; Hopwood, 1983, 1987; Hopwood and Miller, 1994), the Foucauldian (Hoskin and Macve, 1986; Miller and O’Leary, 1987; Stewart, 1992) and the labour process to the Marxist (Bryer, 1999, 2005; Hopper and Armstrong, 1991; Tinker, 2005; Toms, 2002, 2005, 2010). Only in recent years, have accounting historians devoted their research efforts to industrial companies operating in contexts and settings that could be defined as ‘non-capitalistic’. Such literature is heterogeneous referring to different places, periods and institutional rules.

The first category of ‘non-capitalist’ industrial companies reviewed by the literature includes state-owned enterprises in market economies. The Seville-based Royal Tobacco Factory is one of the most frequently investigated examples (Carmona et al., 1997, 2002; Carmona and Macìas, 2001; Macìas, 2002). Alongside it, there are the Royal Textile Mill of Guadalajara (Carmona and Gómez, 2002) and the other Spanish and Portuguese experiences of the nineteenth and twentieth centuries (Carvalho et al., 2007; Nùnez, 2002; Sánchez-Matamòros et al., 2005). These were royally owned large-scale factories in which accounting played a key role in keeping labour under control and pursuing efficiency, even without any real profit-oriented drive. Accounting history research focusing on state-owned enterprises in developing countries illustrate the different roles played by accounting in supporting the birth of enterprises and measuring their performance (Foreman and Tyson, 1998; Hooper and Kearins, 2004; Rahaman and Lawrence, 2001). Finally, a large number of accounting history papers have been concerned with the accounting practices of state-owned enterprises in advanced industrialised countries, such as the United Kingdom (McInnes, 2002), France (Touron and Daly, 2013), the United States (Preston and Vesey, 2008) and Japan (Noguchi and Boyns, 2012; Sasaki, 2001).

The second category of non-capitalist industrial companies includes the so-called ‘experiments of utopian socialism’ scattered all over the world after the nineteenth century. ‘Utopias’ have been largely studies by economic history and sociology scholars who have shed light on the two cornerstones of such social and productive models: the factory and the community. On one hand, this line of research concerns the productive (Donnachie and Hewitt, 1993; Robertson, 1971) and organisational areas of the factory (Hatcher, 2013). On the other hand, it is about the community, focusing on its educational (Lambert, 2011), cultural (Davidson, 2010; Kesten, 1996) and social areas (Donnachie, 2006; Lallement, 2012; Royle, 1998; Sutton, 2004). Papers by Walsh and Stewart (1993), Funnell (2004) and Davie (2007) focus on social experiments reproducing the communal and productive models of nineteenth-century utopian socialists in real life, and investigate the role played by accounting, in measuring value in use based on worked hours, not exchange value based on market prices.

The third category consists of industrial companies in a communist context (Barbu et al., 2012; Djatej and Sarikas, 2009; Ji and Lu, 2013; Lin, 2003; Tudor and Mutiu, 2007; Xu et al., 2014; Zelenka and Zelenková, 2013). Such papers show that accounting is to support the control of performance and behaviour, and it is not, of course, aimed at measuring profits.

Some research effort has focused on ‘hybrid’ forms of organisations, where capitalistic and non-capitalistic features are combined. The hybrid nature of the organisation may concern either its economic relations or its social dynamics. Economic relations usually include property rights, governance, relations with labour and profit. The social dynamic covers other less visible, but no less important, dimensions of the organisation. According to Miller et al. (2008), the process of hybridisation is continuing and dynamic even if its rate varies over time. Whether it is a matter of the emergence of new organisational forms, processes, practices or expertise, typically the newly formed hybrid stabilises for a while and may even become institutionalised (Miller et al., 2008: 944).

Other studies emphasise the features of hybrid organisations that, from being non-capitalistic, tend to take on the typical traits of a capitalistic business (Joldersma and Winter, 2002; Nee, 1992; Thomasson, 2009) or, conversely, of private organisations that take on non-capitalistic traits (Battilana and Dorado, 2010; Boyd et al., 2009; Cooney, 2006; Doherty et al., 2014). Alongside, these can be found in the hybrid character of the not-for-profit organisations, which, by their very nature, are born with a mix of private and philanthropic traits (Billis, 2010; Evers, 2005).

The RSFSL is a hybrid form of capitalism and utopian socialism. The hybrid nature of the RSFSL derives from a mutual contamination of the ‘pure’ traits of the two models of social organisation of production. The first (capitalism), already widely prevailing in the early nineteenth century and the second (utopian socialism), mainly theorised and tested in certain limited circumstances.

The qualifying factors of the concept of capitalism have been widely discussed in the literature. The main theoretical and historical elements relevant to this article are detailed as follows. First, the capital and, therefore, the means of production, belong to private investors (Blanc, 1859; Sombart, 1919). Second, the capitalist’s goal is the distribution of dividends proportionate to the profit, measured by accounting, based on a rational calculation that tends to maximise the rate of return (Sombart, 1919; Weber, 1922). Third, the labour class works under the management’s supervision. Its interest is in contrast to those of the company, and the workers are generally undereducated and underpaid. In other words, exploited (Marx, 1906)! Fourth, the city is the place where the population working in the factories lives and which gives its residents an individualistic and egoistic drive (Sombart, 1919; Weber, 1922). Finally, the development of capitalism is boosted by stable and well-ordered social structures, in which an important role is played by religion, sexual ethics, and the State (Braudel, 1993; Marx, 1933; Weber, 1958).

The distinctive traits of the concept of communitarian/utopian socialism have also been widely debated in the historical literature. Utopian socialism acts in reaction, and in opposition, to capitalism by means of social reforms rather than through revolution. In contrast to utopian socialism, scientific socialism (Marx and Engels, 1848) comprises the following theoretical and historical elements. The means of production must not be owned by single individuals but collectively owned (Proudhon, 1849) or, if still privately owned (according to most utopian socialists), they must be managed wisely and in the interest of the community (Engels, 1999). The capital only receives a fair remuneration, so the rate of return cannot exceed a maximum limit considered acceptable. Any profit above this limit will be spent for the workers or, more generally, in philanthropic works (Owen, 1817). The workers’ wages are adequate to their needs (Blanc, 1859). Workers do not compete with each other. Working hours are shorter, children do not work but study, at least up to a certain age (Owen, 1816). The local communities, linked to the factories, should be where equalitarian, supportive social groups can find space to meet (Fourier, 1849; Owen, 1840). Such local communities implement forms of participatory democracy and less rigid, more libertarian social rules than those of the bourgeois society which gave rise to capitalism (Fourier, 1851; Plekhanov, 2003; Taylor, 2013).

As a hybrid form of capitalism and utopian socialism, the history of the RSFSL cannot be univocally read. Each one of the most widespread approaches seems to be unable, on its own, to fully explain this case. Either it does not meet the requirements or it mixes them up, thus making it difficult for historical analysis to be effective as an explanatory tool (Napier, 2006: 467).

From a socio-institutional perspective, the research agenda is open and includes a study of the interconnections between accounting, institutional and social practices (Hopwood, 1983). Research that depicts accounting as a social and institutional practice typically seeks to explore accounting from a broad perspective, probing the applications of accounting practices in the social and organisational contexts in which they occur (Potter, 2005: 267; see also Carnegie and Napier, 1996, 2012; Miller and O’Leary, 1994). Studies in this field attribute the application of accounting practices within particular organisational contexts, with implications regarding the behaviour of individuals and the functioning of organisations and societies (Miller, 1994). The common denominator of such studies is, therefore, an analysis of the social issues and agents involving the connections with the other aspects of social life, and the consequences of such interactions (Burchell et al., 1980: 23; Miller et al., 1991). Accounting is actually considered to be a tool for setting economic norms or standards of efficiency and seeking to define the ways in which economic surplus is to be calculated, adapting to and shaping the context (Miller and Napier, 1993: 645).

Theoretical framework

The main purpose of this article is to analyse the role played by accounting in a hybrid and complex context, the RSFSL. The case of the RSFSL is explored from a very broad perspective, covering the social, institutional, organisational and accounting aspects, both together and in their mutual interplays.

The role generally played by accounting in a hybrid structure such as the factory/community of San Leucio may be understood as instrumental to the multiple relations, which, according to the main theoretical frameworks, connect accounting with the productive and social context in which it is embedded. Accounting is used to measure surplus and yearly profits, according to the analysis by Karl Marx. Accounting, therefore, is a control tool, in that it allows the results of work to be visible, and permits the control of work from a distance through comparison with a standard. Finally, accounting, along with other tools, acts as a sort of ‘social glue’ within a specific human group (King, capitalists, workers, community members). Through the (assumed) objectivity of the information, accounting produces, builds and consolidates values, consensus and a collective identity, while earning and producing at the same time, trust. Marx provides a wide analytical overview of capitalism (Marx, 1906, 1909, 1933). Many of the conceptual categories that Marx uses in his complex theoretical construction actually come from accounting and, above all, from the observation of the accounting practices of the British and German companies of his time, observations that he shares with Engels (Chiapello, 2007).

The people who run capitalist firms, thus, use accounting to make decisions. They adapt their decisions to the goals pursued by capitalists, that is, to maximise profits, or better, surplus value, deriving from the non-remunerated portion of work (Marx, 1909: 428, 870). So, in order to take well-informed decisions, capitalists – or the managers whom capitalists have their companies run by – need information about processes such as the transformation of money into capital, the production of relative surplus value, wages (Marx, 1906), the conversion of surplus value into profit, and the rate of surplus value into the rate of profit, and the division of profit into interest and profit of enterprise (Marx, 1909).

Marx’s pattern of analysis led accounting historians to emphasise accounting’s overall measure of a business entity’s performance, the extent to which it carries out its social duty, that is, the rate of return on capital (Tinker, 1999). Furthermore, in Marx’s analysis, the object underlying accounting profit is surplus value (Bryer, 1999). Surplus is produced entirely by workers while capitalists appropriate such surplus because their aim is to maximise the return on capital (Bryer, 2006; Chiapello, 2007). Thus, DEB has a crucial role in measuring, at a company level, the capital, the profit and the rate calculated dividing the latter by the former (Toms, 2010). In addition, accounting could reveal the components and the accumulation of such surplus (Bryer, 2005).

Foucault described the history of many institutions (prisons, asylums, clinics) as they emerged after the Enlightenment as forms of social control over the population (Foucault, 1967, 2003). Accounting historians who support Foucault’s pattern of analysis, emphasise the importance of remote control and surveillance as means of controlling labour in capitalist and non-capitalist contexts (Fleischman and Macve, 2002; Hopper and Armstrong, 1991; Miller and O’Leary, 1987; Stewart, 1992).

Foucault’s many studies into the use of control focus on the disciplinary functions of the institutions, which, with their own rationality and practices, impose and then progressively educate individuals (Foucault, 1980). Following the metaphor of the Panopticon (Foucault, 1977), they consist of hidden, all-invading forms of control over people’s behaviour which are unseen and, therefore, difficult to avoid. They exist in organised, complex forms such as control from a distance, as in the case of governmentality (Foucault, 1991). Lastly, they are sublimated in the technologies of the self. Individuals no longer need a hetero-direction, as they absorb and make their own all of the environmental expectations and pressures, without the need for any external intervention (Foucault, 1988).

It was with the introduction of mechanisation that the factory system and its discipline became more pronounced. The separation of the workers from the ownership of the means of production increased capital’s control over labour. As a consequence, accounting played a role in controlling individuals – and workers as a category – a role that it had never played on such a large scale previously (Armstrong, 1994; McKinlay and Starkey, 1998; O’Neill, 1986).

On a micro-scale, that is, within an individual organisation, accounting consists of ‘instruments that render visible, record, differentiate and compare’ (Foucault, 1977: 208), tools that allow ‘the construction of an individual person as a more manageable and efficient entity’ (Miller and O’Leary, 1987: 235).

Porter (1992) emphasises the social role of accounting as a result and as a process. If the process whereby accounting information is processed is perceived by a group of individuals as objective, the result of such a process, that is, the figures presented, become credible, in other words, worthy of trust. Having acquired the connotation of the impartial and objective, Porter (1992) argues, numbers became the preferred conduit for information in increasingly open and democratic political systems where authority is regularly contested. Thus, the shift towards quantifying information is a result of the specific social features of bureaucracies and political struggles over knowledge produced by scientific and technical experts, not a simple result of refined techniques (Porter, 1992, 1994).

Numbers that have no credibility as truthful claims are less effective at projecting power and coordinating activity. Numbers alone never provide enough information to make detailed decisions about the operation of a company. Their highest purpose is to instil a sense of ethic. They provide legitimacy for administrative actions, in large part because they provide standards against which people judge themselves (Porter, 1995: 45).

Method and sources of the article

After an in-depth survey of secondary sources, it has been possible to reconstruct the first version of the history of the community and the factory. In particular, from the .pdf Table of Contents of the State Archives of Naples, 1 we deduced that the main clusters of documents kept in the archives should include regulations, documents, account books (journals, ledgers, and labour books), accounts, reports and financial statements. The primary sources were then thoroughly surveyed based on the hardcopy Table of Contents. Based on the Table of Contents, we selected the available account records, which have been kept in the archives since 1802. An accounting document was also found in the Archives of the Royal Palace of Caserta. After a photographic reproduction of the account books and other records, the contents were examined on screen, photograph by photograph. The description of the main documents is provided in the section dedicated to the RSFSL’s accounting system. Because of the incompleteness of the archives – mainly the lack of a full set of financial statements, journals and ledgers, accounting records for 1789 to 1802 – the accounting system could not be traced back to the origins of the San Leucio experience. Summing up, we were able to examine the journals kept for the period 1802 to 1807, the ledgers referred to the periods 1806 to 1807 and 1821 to 1824, the financial statements for the years 1806–1807 and 1821–1823, many documents and notes related to production, labour and workers (1816–1819), the list of buildings and lands (1825) and a production account book (1825).

The Royal Factory of Silk and the community of San Leucio: a hybrid form of enterprise

The factory was set in a communal context that was governed according to socialist–utopian principles of political and social cohabitation (laid down in 1789). In its turn, the community of San Leucio was closely bound to the factory which was founded and funded by King Ferdinand IV. Therefore, they were two distinct but strictly related institutions.

The community of San Leucio

The establishment of the community 2 of San Leucio officially dates back to 1789, when King Ferdinand IV 3 issued the ‘Regulations’ (Ferdinando IV, 1789). The idea of an ideal community – based on a few cornerstones, such as the geometrical design of the interior spaces, the separation of the factory areas from other public areas or from the areas of the workers’ homes, work as a factor for personal improvement and social discipline – and the very prototype of the city-factory were already known in many European countries (Verdile, 2009). The idea was born as much from the ideals of enlightenment regarding a rationalisation of government rule as from a conception from an architectural point of view. In this sense, Ferdinand IV was probably influenced as much by the rationalistic ideals brought about by the reformist philosophy of the Age of Enlightenment as by the works of Abbot Antonio Planelli (1779), who, in a treatise on the education of the Prince, explained how culture, education and training were the basis of human improvement.

In the community, all residents were equal, received proper social assistance and health care and adequate education, regardless of their gender. In the development of such a community, work would have been the key factor for the improvement, qualification and elevation of the residents’ social status (Battaglini, 1983a, 1983b). At the same time, the community would have helped control and govern the residents along with providing compulsory education which – still missing in the Kingdom, as well as elsewhere in Europe – would have been open to women too (Cirillo, 2012: 31–32; Lazzarich and Borrelli, 2012).

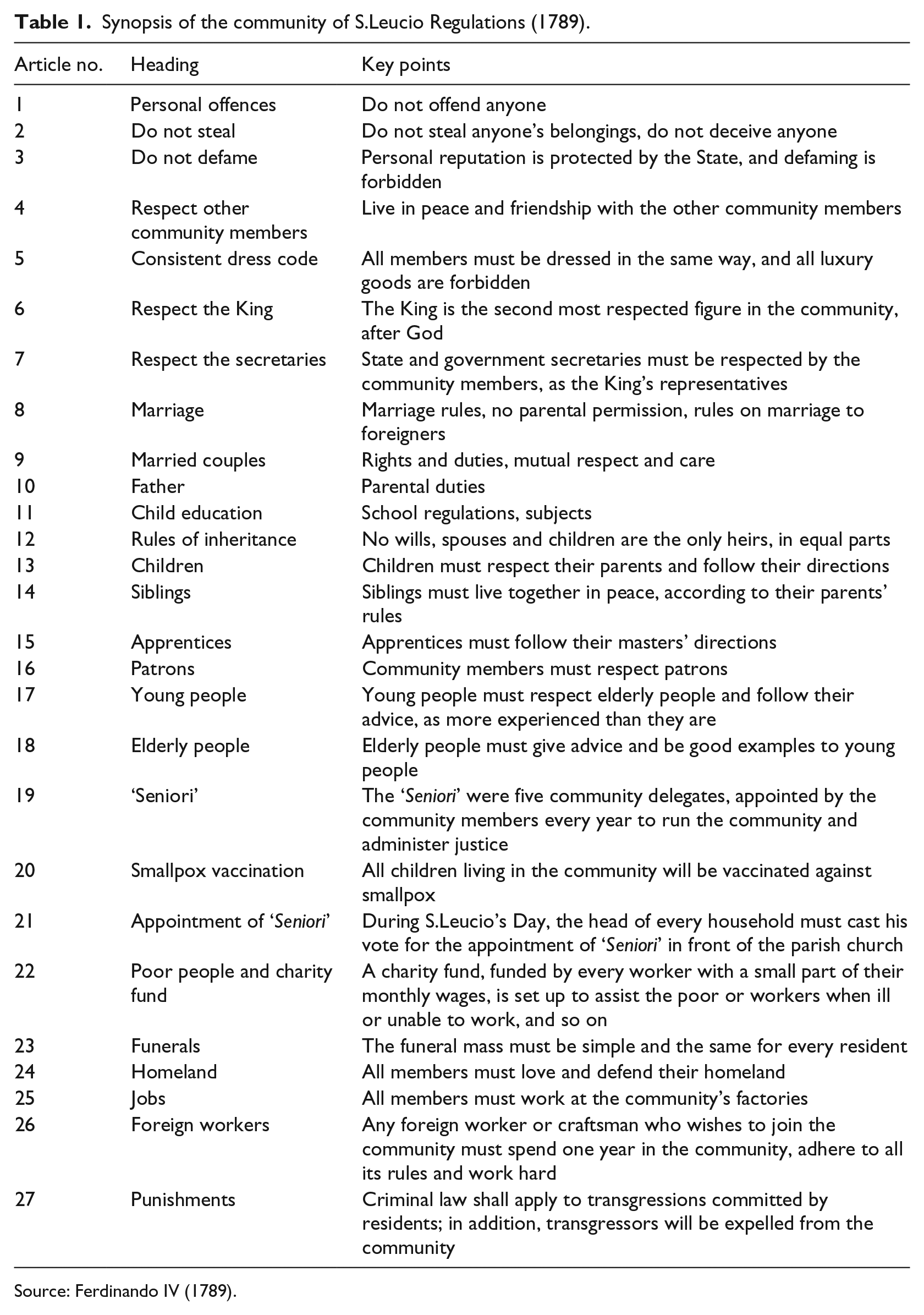

The 1789 Regulations consisted of 27 articles and 3 sections: the so-called ‘negative duties or bans’, ‘positive duties, or rights and obligations’ and ‘work rules’ (Ferdinando IV, 1789; Table 1). The ‘negative duties’ set forth by the regulations punished conduct that could be detrimental to other people and their assets (Ferdinando IV, 1789: XVIII–XX). On the other hand, the ‘positive duties’ were rules that were essential for the optimum operation of the community and also covered employment. A general introduction about the need for equality and mutual respect among the residents was followed by more specific provisions, that distinguished residents based on their talents and professional achievements. Despite censoring luxury (among the residents) and prescribing a consistent dress code and strict personal and home hygiene, the regulations gave pride of place to work as a way to differentiate people from each other (Ferdinando IV, 1789: XXIII–XXV).

Synopsis of the community of S.Leucio Regulations (1789).

Source: Ferdinando IV (1789).

Such legislation was designed to control social relations, thus proving that the experiment was first and foremost a communitarian rather than a productive one. To achieve such a goal, the Regulations laid down, for example, the rules for the institution of marriage, both within the community and with non-residents, meaning the community was bound to a number of rules (Ferdinando IV, 1789: XXXV–XXXVII; San Leucio, 1789).

Capitalist wealth was redistributed to the community in the form of free and compulsory education, health care, social security and housing. In addition, living in the community also meant having access to meals when working at the factory and, generally, to the distribution of victuals during the year or on special occasions (Pezone, 1972).

Work too was entirely different, since living in the community meant working in the silk factory. The employment market within the community was regulated, which meant having no competition on the supply side, such as free bargaining and the option to ask for higher wages. In addition, the residents were skilled workers as a direct result of the factory’s investments in education and apprenticeships. Finally, child labour was almost non-existent in San Leucio, the only form being apprenticeship, but only after attending compulsory education (Ferdinando IV, 1789: XXXV–XXXVII).

Health care was regulated in a way similar to the other health care programmes that were part of the new legislation in the Kingdom. The articles actually took inspiration from the most advanced health care criteria of the eighteenth century, which would not touch the rest of Italy until the early nineteenth century (Ferdinando IV, 1789: XXI; Garbellotti, 2013).

The charity fund – run by the parish priest, the directors of the RSFSL and the ‘Seniori’, that is, the most senior craftsmen living in the community – was an institute that took care of the workers’ sustenance. A portion of San Leucio’s workers’ monthly wages were withheld and paid into a fund that was created. The charity fund was also supported by other assets and transactions (Ferdinando IV, 1789: L–LIII).

The RSFSL

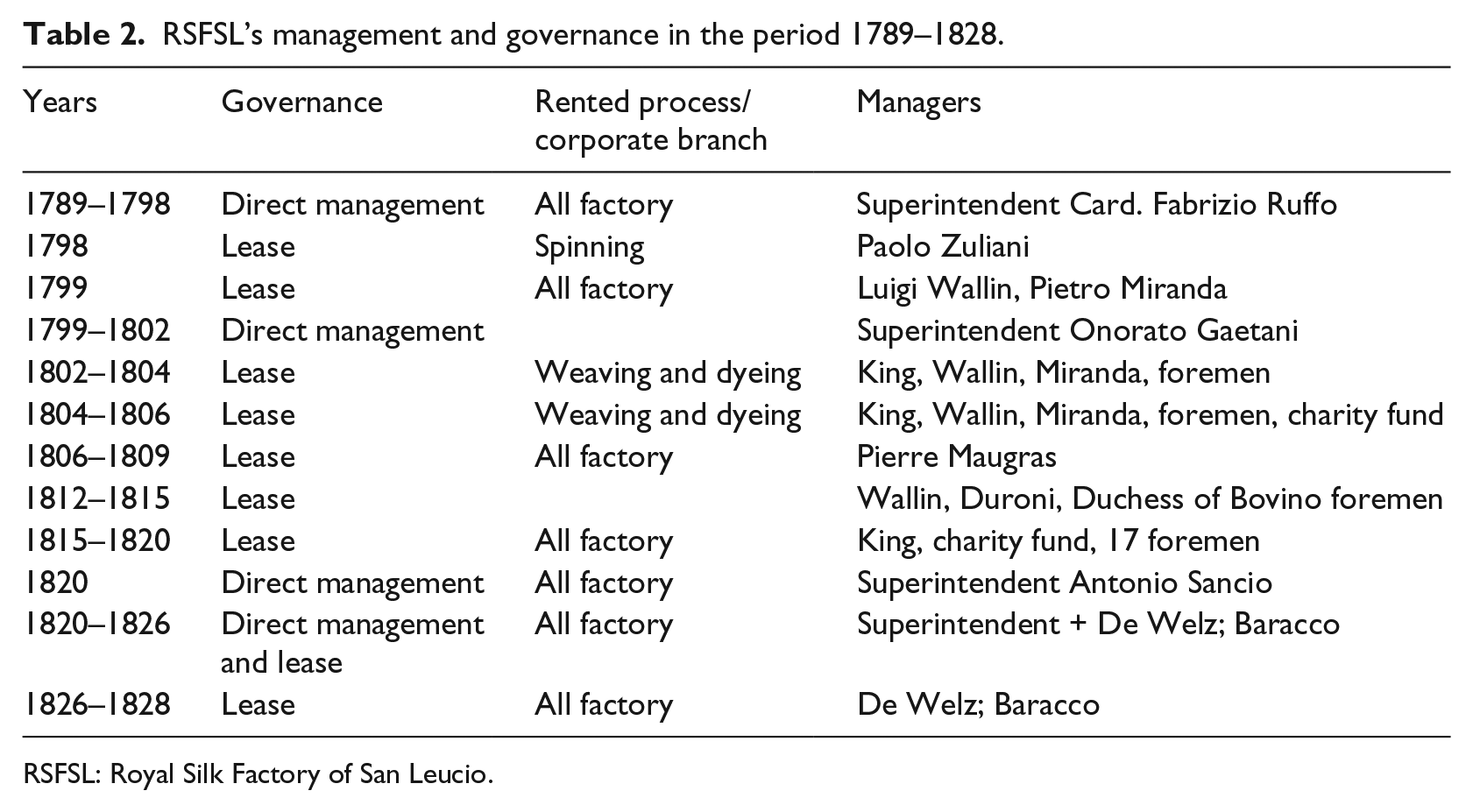

The RSFSL was a large-scale factory at the centre of the system. The works for the equipment and the conversion of the existing buildings cost the King over 200,000 ducats (ARCE, 1825; Patturelli, 1826). Between 1790 and 1799, the RSFSL acquired cutting-edge twisting and weaving equipment. In addition, some French craftsmen were hired to improve the production process and promote the transfer of more modern expertise to the local technicians (Archivio di Stato di Napoli [ASN], 1790, 1791, 1799, 1800; Converti, 2012).

In 1799, the French invasion put a stop to Ferdinand IV’s communitarian project, but not to his entrepreneurial one, as the RSFSL was rented out to two Piedmont-born businessmen, Luigi Wallin and Pietro Miranda (ARCE, 1825). In 1802, after the Restoration of King Ferdinand IV, the new superintendent of RSFSL proposed to revoke the previous lease of the factory and separate the mill’s operations. The RSFSL would run the spinning process, while the weaving and the other high added-value processes were rented out to a company co-owned by the King, the previous renters and some of the community’s supervisors. This change partially broke with the communitarian ideal of the factory and was a safe adaptation to a capitalistic concept of business, even though San Leucio’s community members continued to be the basis of RSFSL’s manpower and continued to receive benefits (e.g. health care, education; Tescione, 1933).

In 1804, the ownership of the RSFSL changed hands again. There were more shareholders, including the charity fund (which invested 1500 ducats). The stock increased to 9600 ducats and the King being more involved in the factory, which took care of the spinning process only (ASN, 1804a).

In 1806, a new French invasion ordered by Napoleon, again put a stop to RSFSL management and to the communitarian approach of the community of San Leucio. Although the French partially gave up the idea of a community, they did build a new, larger silk mill and then complete a few buildings that had been started by Ferdinand IV to house the winders (drying), the weaving and dyeing operations (ARCE, 1825).

The new management of RSFSL was the result of a transformation of the original communitarian project with the surfacing of capitalist specificity of manufacture. The factory became more important than the community that existed simply as a supplier of skilled manpower for weaving. The new Napoleonic government, bearer of bourgeois interests, was more careful regarding RSFSL’s profit production. The forces of capital and the bourgeois model of society quickly overtook the idea of a utopian community, kept together by work and equality as a way to create a perfect society free from social contradiction.

In this period, the community of San Leucio survived with its health care and education system and charity fund still active. Nonetheless, the community members were not the only workers employed in the different branches of RSFSL, with the introduction of non-communitarian skilled salaried and pieceworkers.

In 1806, the superintendent entered into a new agreement for the management of the spinning and weaving operations. Wallin and Miranda entered into partnership with the government of Naples. In January 1809, the partnership was wound up, and the mill was rented out to a French businessman living in Naples, Pierre Maugras. In 1812, because of the low profits produced by the mill and at the insistence of Caroline Bonaparte (sister of Napoleon), wife of King Joachim Murat, the RSFSL was rented for 12 years to a partnership, composed of Wallin, Duroni and a few experienced skilled foremen (ASN, 1816c).

At the Restoration in 1815, under a deed dated 29 August of the same year, a new partnership was formed with 13 new shareholders. They leased the silk spinning and weaving operations, still conducted by community members and some non-communitarians. The production of scarves and stockings was outsourced to pieceworkers, who received the raw material from the RSFSL. By the end of 1816, part of the capital stock was acquired by the charity fund (5000 ducats, which were in fact already part of the previous arrangements), and by the King (12,000 ducats). In addition, 17 foremen of the factory subscribed an overall stock capital of 8500 ducats (Bianchini, 1839).

In October 1825, the new superintendent of the RSFSL proposed to King Francis I 4 that the mill be let out to the company set up by Giuseppe De Welz and Giuseppe Baracco (Cicala, 2003; San Leucio, 1826). The agreement with De Welz and Baracco was wound up at the King’s request 2 years later. Owing to the failure of this attempt to ‘privatise’ the management of the RSFSL, the factory fell back under the close responsibility of the Crown through the superintendent, and the direct involvement of the King in the share capital (Tescione, 1961).

A synoptic picture of the different managing bodies of the RSFSL is in Table 2.

RSFSL’s management and governance in the period 1789–1828.

RSFSL: Royal Silk Factory of San Leucio.

Findings on the accounting system of RSFSL

Financial accounting

The RSFSL adopted DEB. Keeping accounts records and preparing financial statements in RSFSL were duties shared by three people, that is, the ‘accountant’, the ‘journal-keeper’ and the ‘clerk’. The ‘accountant’ supervised the office and kept the cashbook. He was responsible for keeping the book of guilds, the book of silk delivered to traders, the book of certificates and the book of agents. The ‘journal-keeper’ was responsible for keeping the ledgers and journals. The ‘clerk’ kept a summary book, in which he reconciled all the balances coming from the RSFSL accounts books (ASN, 1813).

In the journal, transactions were recorded daily, in paragraph form, with many details and cross-referenced entries (ASN, 1802a, 1802b, 1803, 1804a, 1804b, 1805, 1806a). Ledgers were also extremely detailed. The accounting system required many accounts, approximately 260 per year on average, which thoroughly covered all the manufacturing processes, as well as all transactions (ASN, 1806a, 1806b, 1807b, 1821b). Finally, in the book kept by the clerk, each account was ranked by type and reduced to 30, where the total debits and total credits had to balance the total amounts posted to the ledger accounts and the trial balance drawn up by the journal-keeper (ASN, 1813).

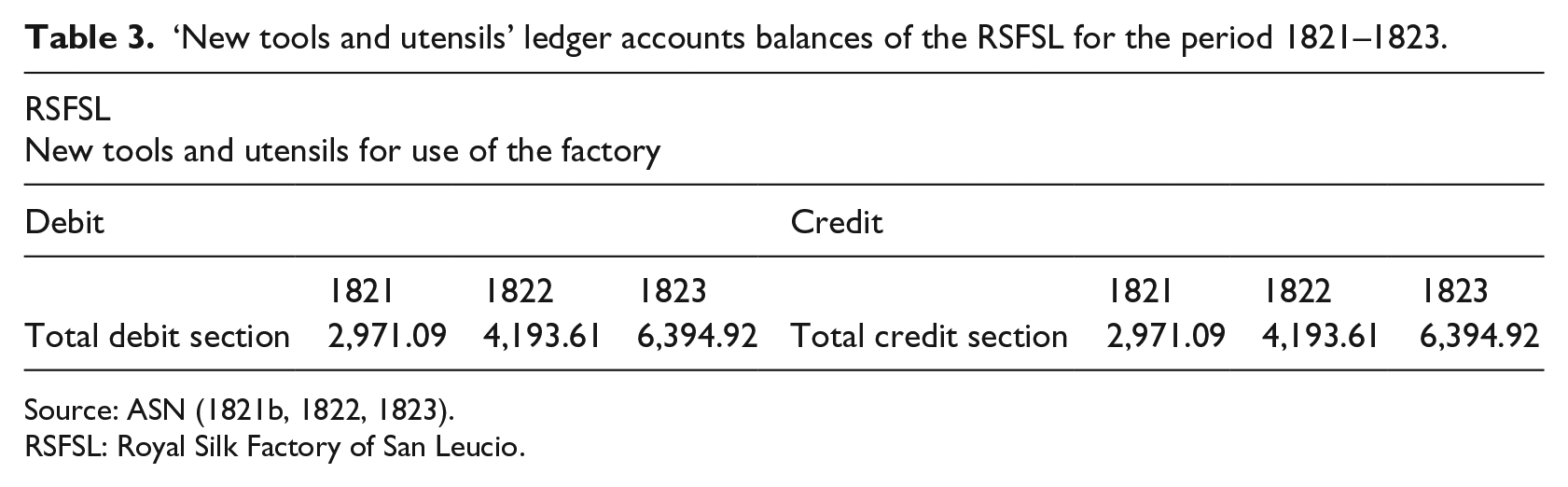

A crucial feature of recording transactions in RSFSL was accounting for fixed assets. Purchases and depreciation of looms or buildings were entered neither in the journal nor in the ledger. In fact, buildings were purchased by the King, and remained in the King’s hands. The title to them was not transferred to the factory (Ferdinando IV, 1789: XXVI). Neither were the looms owned by the RSFSL, as the King gave one loom to every resident family, for free (ASN, 1816; Ferdinando IV, 1789: XXVI–XXXI).

Such circumstances are one of the distinctive traits of the communitarian experiment, where no asset belongs to anyone, but all of them may be freely used by the entire community. Therefore, the accounting system recorded just the purchasing of the equipment and tools involved in the spinning and hemming processes (Table 3).

‘New tools and utensils’ ledger accounts balances of the RSFSL for the period 1821–1823.

Source: ASN (1821b, 1822, 1823).

RSFSL: Royal Silk Factory of San Leucio.

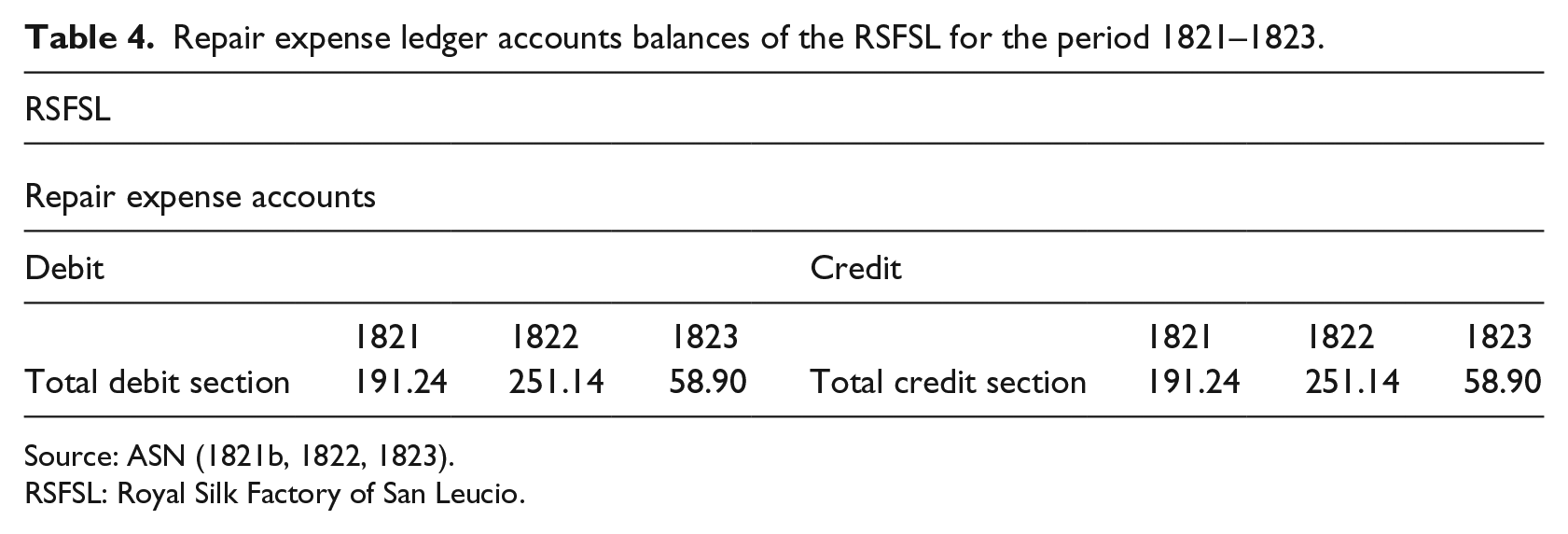

While expenses for buying main fixed assets were not incurred, current expenses for using them were. Table 4 shows the ‘Repair expense’ balance accounts for the years 1821, 1822 and 1823.

Repair expense ledger accounts balances of the RSFSL for the period 1821–1823.

Source: ASN (1821b, 1822, 1823).

RSFSL: Royal Silk Factory of San Leucio.

Maintenance was intended to keep the equipment lent to workers in working order. Generally, repair expense was added to the other costs for the purchase of raw materials. When direct management was replaced by the rental of the factory or its departments, repair expense in the costing of silk had the same purpose as depreciation charges, namely, to record the reduced value of fixed assets, due to use and ageing, on a regular basis.

The problem of recording capital and income was crucial for the RSFSL. The financial year started on 1 May and ended on 30 April (ASN, 1802a, 1821b). The financial statements consisted of the balance sheet and the income statement. They were built on an accrual basis. For example, in the 1802 journal, the adjustment of ending accounts balances and the closing procedure took four pages including entries regarding pre-paid and deferred interests and rents, wages payable and inventory valuation (ASN, 1802c). Similar entries emerge from the other journals (ASN, 1803, 1804a, 1804b, 1805, 1806a, 1807a).

The balance sheets we could consult cover the years 1806–1807 (ASN, 1806b, 1807b) and 1821–1823 (ASN, 1821a, 1821b, 1822, 1823). Formally, the balance sheet consisted of two-sided accounts. The debit section of the balance sheet recorded the RSFSL’s assets, that is, merchandise inventory, accounts receivable, cash and fixed assets (tools and equipment). In turn, the merchandise inventory summarises a number of accounts balances related to raw materials and finished goods held by the warehousemen. The credit section of the balance sheet shows the liabilities and the owners’ equity. A review of liabilities shows that just a small part of the profit was distributed to the owners, while most of it was paid into a fund, for the RSFSL’s retained profits (Table 5).

Balance sheet of the RSFSL at 30 April 1821.

Source: ASN (1821a).

RSFSL: Royal Silk Factory of San Leucio.

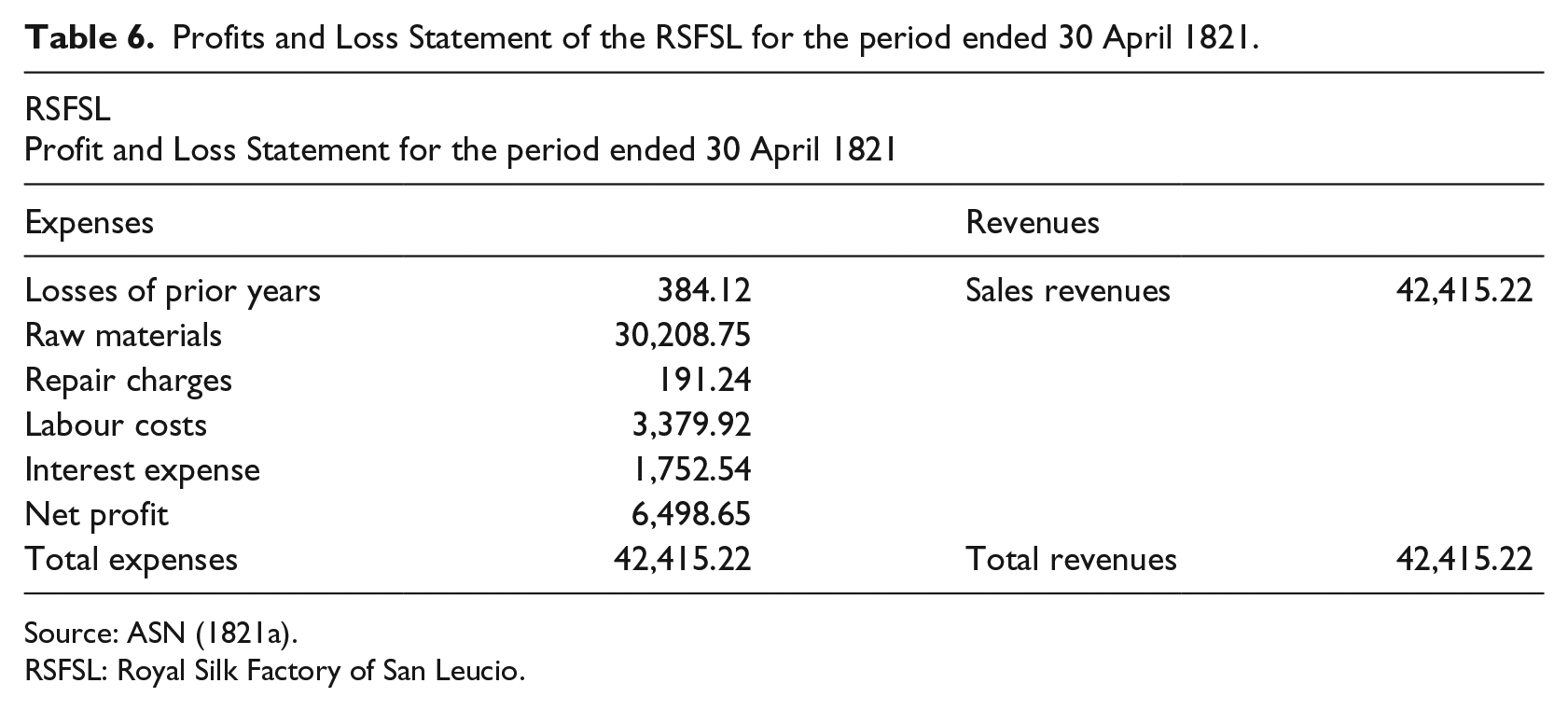

The Profit and Loss Statement was split into side-by-side sections, according to a T-account form. The debit section of the Profit and Loss Statement shows the expenses and the net profit as a balance. This section details losses from previous financial years, supply of raw materials, labour costs, repair charges and interest expense. The credit section of the Profit and Loss Statement shows revenues, summarised in only one account referred to sales revenues (Table 6).

Profits and Loss Statement of the RSFSL for the period ended 30 April 1821.

Source: ASN (1821a).

RSFSL: Royal Silk Factory of San Leucio.

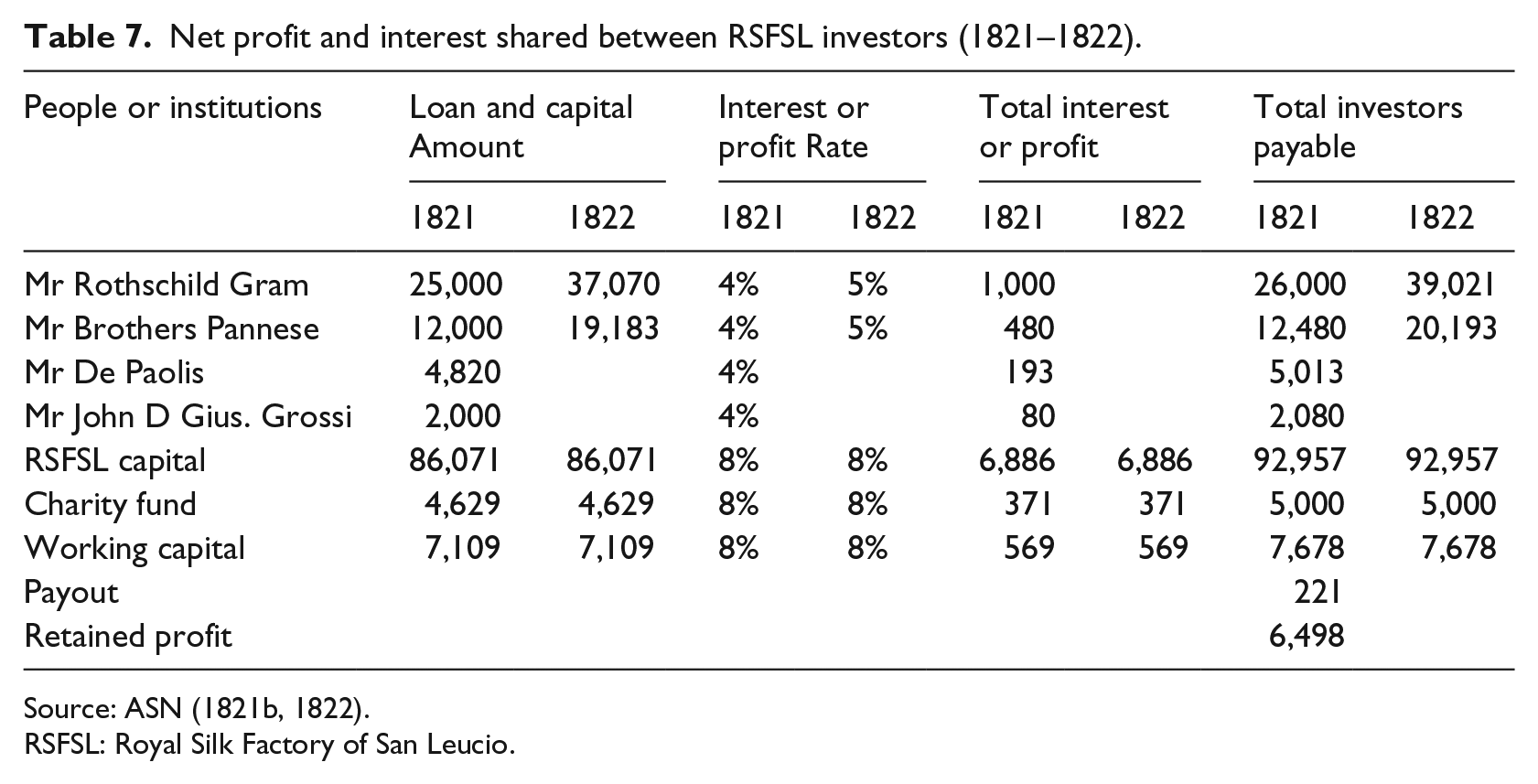

Another crucial feature in order to understand the economic life of RSFSL is undoubtedly the way profits were retained, shared and distributed or, in a different sense, the rate of return for investors. With this in mind, we have drawn up a table for the years 1821–1822 showing ledger accounts records related to profit and interest expense (Table 7).

Net profit and interest shared between RSFSL investors (1821–1822).

Source: ASN (1821b, 1822).

RSFSL: Royal Silk Factory of San Leucio.

Table 7 summarises the investors’ names and the interest or profit rates. Above all, the names of the people who lent money to the company are listed at the top. The interest rate on such loans was 4% for the year 1821. One year later, there were just two external investors, other than the shareholders, and the interest rate increased to about 5%. The central section of the table lists the amounts paid in as equity. At 8%, the rate of return is higher than the interest rate.

Part of RSFSL profits were returned to the community through the charity fund (ASN, 1821a). The charity fund also provided financial support to the neediest members. Nevertheless, like any other shareholder, the charity fund received an 8% profit rate.

The dividend was particularly low, and most of the profits were retained within the factory. In the period at hand, the General Superintendent was responsible for supervising all operations on the King’s behalf. The General Superintendent acted as an agent for the King. Under the 1789 Regulations, the General Superintendent had to supervise the members of the community/colony in their private life as well as their professional conduct. In addition, the General Superintendent made sure laws were abided by, and everyone within the RSFSL fulfilled their duties (San Leucio, 1789: 21).

By acting on the King’s behalf and directly supervising and authorising all the operations that took place at the RSFSL, the Superintendent had more information than the King. In 1820, the King decided to appoint one Superintendent, Antonio Sancio, to protect his interests on all his properties in Caserta, especially the RSFSL. The financial statements were, thus, an essential tool in helping to reduce this information asymmetry so that the Superintendent could report to the King and to any other investor, and document the impact of the new management on the accounts (Battaglini, 1983a).

Labour accounting

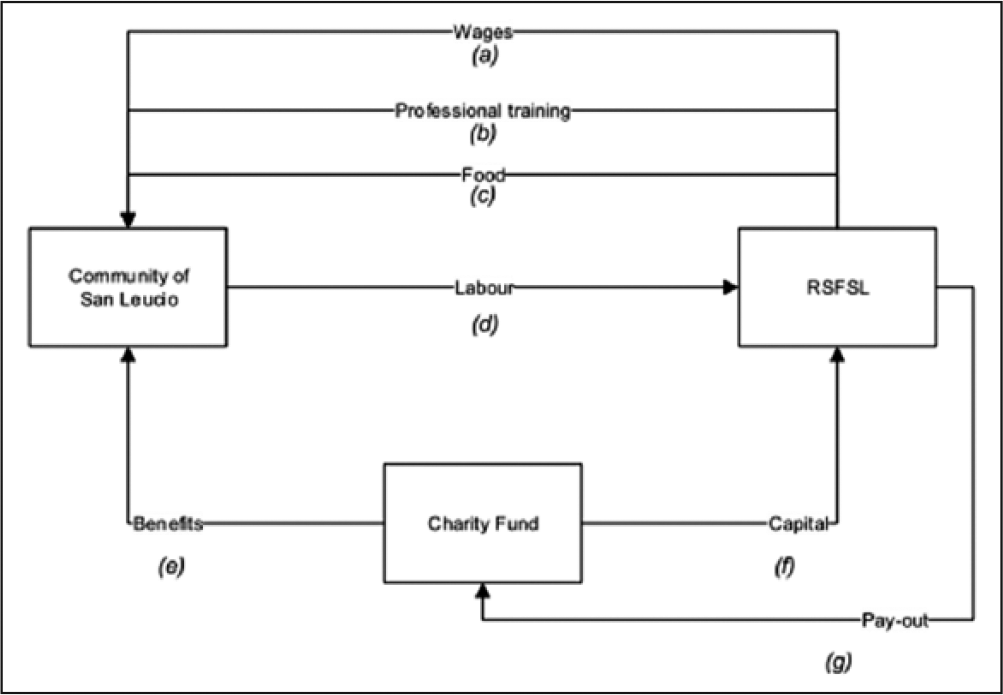

The relations between the workers, the community, the charity fund and the RSFSL were the most distinctive feature of the hybrid nature of the San Leucio social experiment. They are summed up in Figure 1.

Financial flows between the community of S.Leucio and the RSFSL.

Wages

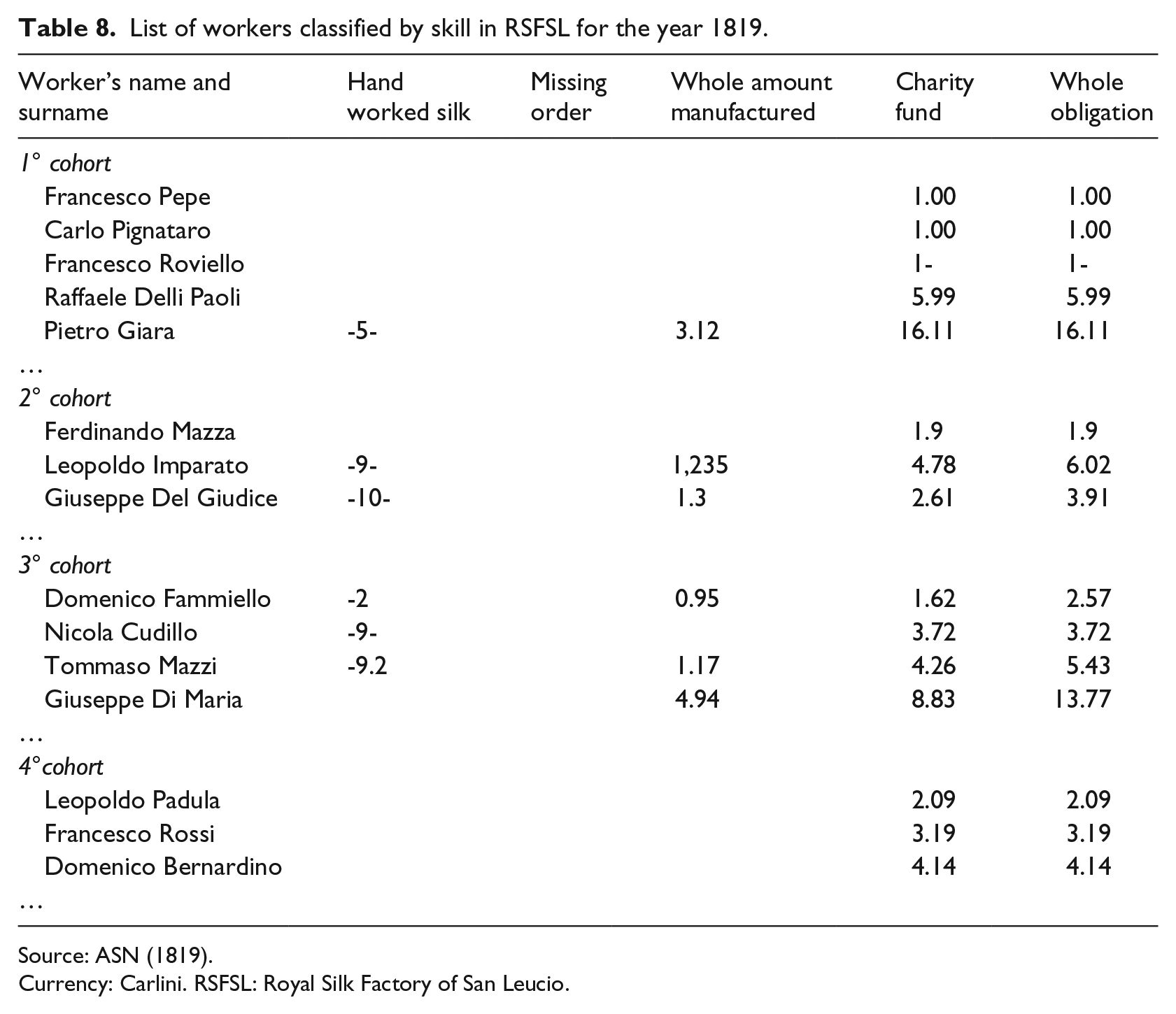

Men and women who worked in the silk factory enjoyed equal rights and their salaries were set ‘according to merit’. The only difference was based on individual skills. The highest salary was paid to the best artists of the Kingdom of Naples and Europe (ASN, 1802a, 1813, 1815; Ferdinando IV, 1789: XXIII–XXIV; Table 8).

List of workers classified by skill in RSFSL for the year 1819.

Source: ASN (1819).

Currency: Carlini. RSFSL: Royal Silk Factory of San Leucio.

The first column in Table 8 shows the artists’ name and surname. They were divided in four cohorts by skills. Each workers’ cohort developed one stage of the silk processing. The first cohort was allocated to the reeling process, the second to the silk throwing, the third to the dyeing and the fourth to the silk weaving (ASN, 1802b). Column 2 shows the amount of hand worked silk required by RSFSL from each artist within that period. In column 3 are summarised the orders carried out from RSFSL and not fulfilled by workers. It was necessary to deduct from the amount in column 2 missing orders to obtain the whole manufacturing amount (column 4).

Column 5 showed the amount due for the charity fund. Each worker had to pay an amount from his wage to the charity fund. This amount, which was proportional to salary, was retained, directly, from the overall wage (ASN, 1821b, 1822). The RSFSL took charge of this amount. The amount due to the charity fund is added to the cost of manufacturing.

The last column summarised the whole obligation. It represented the total amount of money due to the workers. It is the sum of columns 4 and 5, respectively, the part due to the workers for silk manufacturing plus the amount due to the charity fund by the workers.

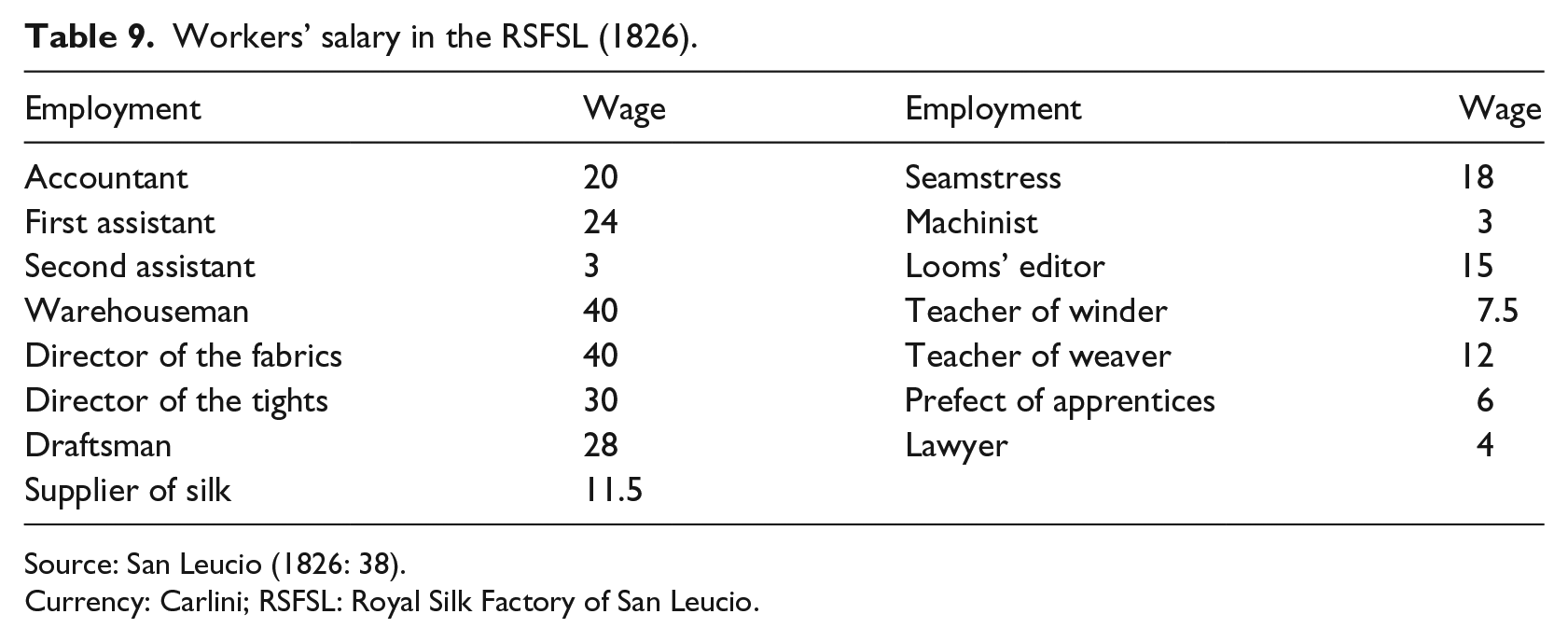

Workers classification in the RSFSL was based on the role played and the tasks performed. As Table 9 shows, a different wage was paid to each worker according to the work performed.

Workers’ salary in the RSFSL (1826).

Source: San Leucio (1826: 38).

Currency: Carlini; RSFSL: Royal Silk Factory of San Leucio.

Professional training

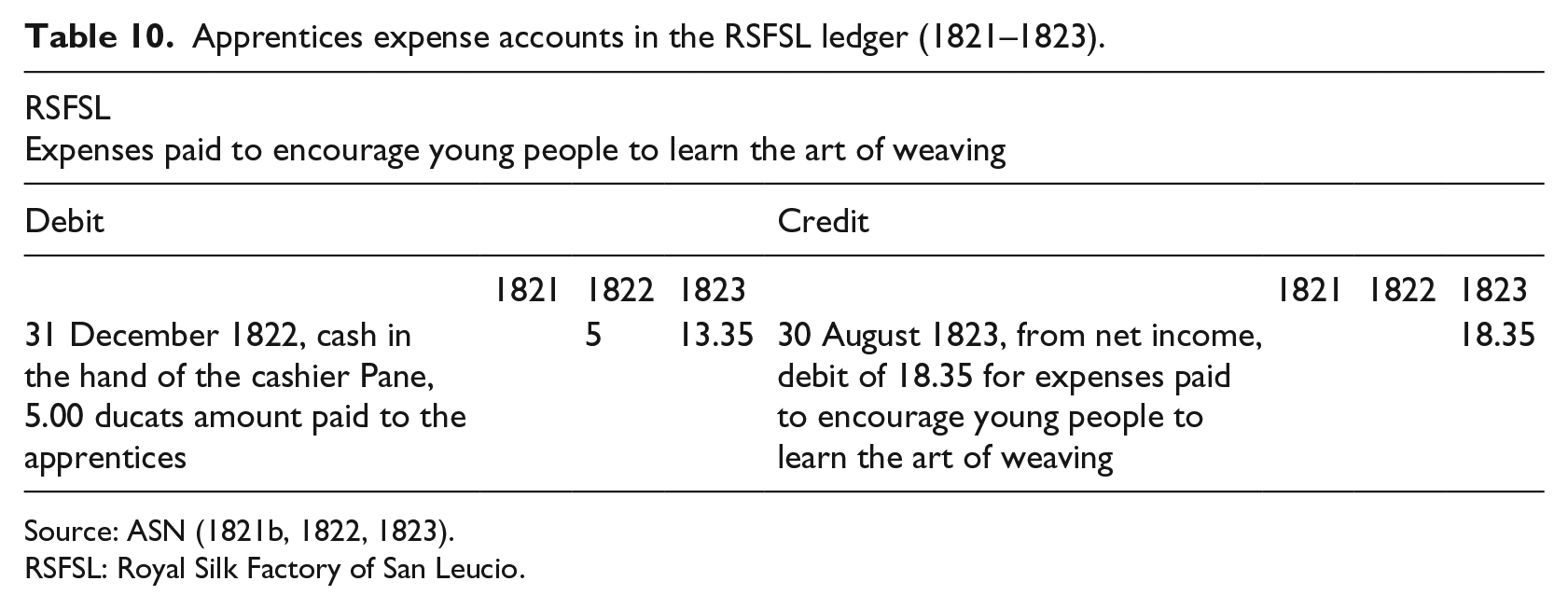

Schooling was compulsory, starting at 6 years of age. Children then went on to learn a trade according to their personal talents and wishes (ASN, 1816; Ferdinando IV, 1789: XXXV–XXXVI; San Leucio, 1789). The mill took care of all the costs for the training of these young residents until they could actively work (ASN, 1816). Officially established in 1797, the articles of apprenticeship stated that, after a 3 months probation period, these young people would officially qualify as apprentices and could, therefore, work for 3 years under a master (Ascione et al., 2012: 397). These young apprentices were also responsible for the upkeep of the mill’s machines. Apprentices too, like any other worker, could use a rent-free loom provided by the King (ASN, 1819). The cost incurred by the RSFSL for the apprenticeship is shown in the accounts records associated with such charges (Table 10).

Apprentices expense accounts in the RSFSL ledger (1821–1823).

Source: ASN (1821b, 1822, 1823).

RSFSL: Royal Silk Factory of San Leucio.

Food

Under the general regulations, basic victuals had to be bought by the RSFSL in the years in which the mill’s wages were too low for the colony to live respectably. In the purchase book for grain, fodder, beans, in 1821, 5225 ducats were spent for the RSFSL, while 971 and 364 ducats were spent in 1822 and 1823, respectively (ASN, 1821b, 1822, 1823).

Labour

A workday consisted of 11 hours. At the RSFSL, there were three classes of workers:

Workers directly reporting to the RSFSL, that is, spinners and warpers.

Salaried workers, most of them directors and administrative staff.

Pieceworkers for all processing steps, except spinners and warpers.

Workers and salaried workers were monitored by special production reports, which measured the number and quality of the pieces they manufactured. Average wages were higher than those of the other companies of the Kingdom of Naples (Tescione, 1933: 182).

Pieceworkers were monitored based on performance, measured ex post (ASN, 1816). If they met the quality standards, then they were entered in a special ranking, which was used when the factory was leased out. The lessee had to hire the people who were at the top of the rank. The pieceworkers’ wages were instead negotiated at market prices when the mill was leased out (Tescione, 1933: 184).

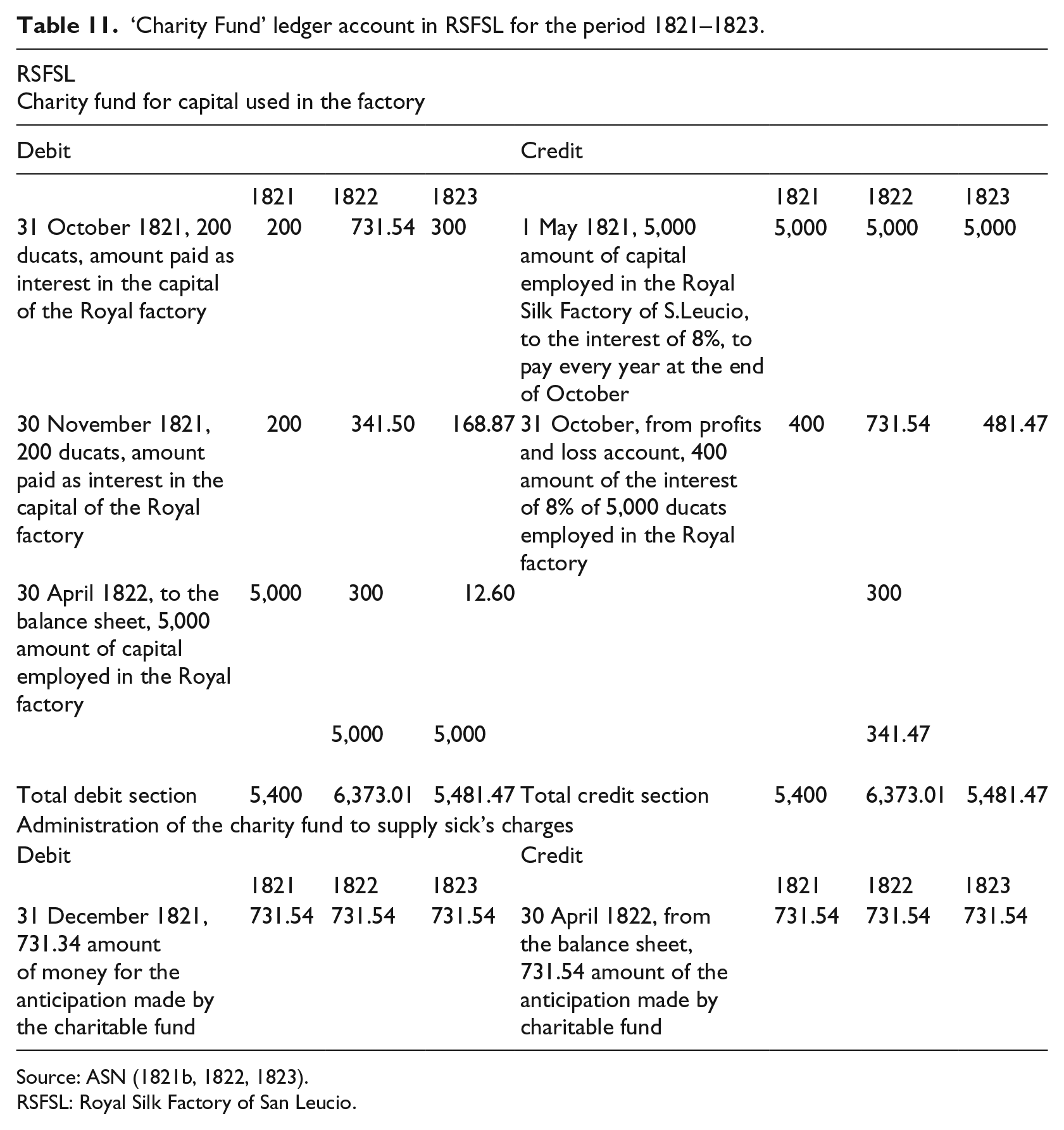

Benefit

The charity fund lent interest-free money to the community members in need and paid the workers’ pensions. It was supported by the members themselves, who paid a small amount of their wages into this fund. The amount withheld from their wages was 1 ‘tari’ a month if the worker earned over 2 ‘carlini’ a day or 15 ‘grani’ if they earned less than this threshold 5 (ASN, 1821b, 1822, 1823).

The charity fund was run by the parish priest of the colony and by the Directors of the arts. Ferdinand IV wanted some urban and rural assets to be added to the fund, so these rents could support health care, lighting and more reasonable pensions.

Capital

Every time the mill’s ownership changed, the charity fund acquired some capital shares (usually 5000 ducats; ASN, 1806b, 1807b, 1821b, 1822, 1823).

Payout

Like any other shareholder, the charity fund received a yearly dividend, set at least at 8% (ASN, 1806b, 1807b, 1821b, 1822, 1823). In this respect, Table 11 shows the ledger account records related to the charity fund for the period 1821 to 1823.

‘Charity Fund’ ledger account in RSFSL for the period 1821–1823.

Source: ASN (1821b, 1822, 1823).

RSFSL: Royal Silk Factory of San Leucio.

The records show the credited and charged amounts of shares bought and dividends and expenses incurred by the charity fund. In addition, the RSFSL’s accounting system recorded the costs of donations made by the parish priest to the poor.

Discussion

An analysis of the accounting system used has shown how capital and work were intertwined in the RSFSL, which can be considered a hybrid form of capitalism and socialism. The complex economic and social construction that links the community, the factory, the King, the capitalists and the workers external to the community is the framework in which the accounting system is set, serving as much the capitalist component as the utopian socialist component of this structure. The roles played by accounting at the RSFSL in the service of each of the two components can each, in their turn, be interpreted in the light of Marx’s, Foucault’s and Porter’s theories.

Two distinctively capitalistic traits are revealed by the accounting system of RSFSL. First, capital played a key role, without which investments in fixed assets (buildings, looms, trenches, water engines, tools, etc.) and working capital (stocks of yarns, raw silk, fabrics, stockings, etc.) would never have happened. Moreover, the capital was not invested for free but provided a return because there were investors who asked for an interest rate, such as the Rothschild family.

From a Marxian viewpoint, the role of accounting in measuring a business entity’s performance (Bryer, 2006; Marx, 1909; Tinker, 1999) is widely confirmed by the evidence since in the RSFSL, DEB had a crucial role in measuring the capital, the profit and the rate of return, formally calculated and ex post verified.

Second, employment was always hierarchical and workers coming from outside the community were paid a fixed wage. Non-resident workers received a salary and their performance was directly supervised and monitored. Again, the Marxian point of view on the role of workers and the surplus value, deriving from the non-remunerated portion of work, is confirmed, even if only partially, because such a viewpoint sheds light only on ‘external’ workers (Marx, 1909: 428, 870). Workers from the community were paid a higher salary, depending on their experience and skills, while supervision was more complex. The factory’s workers and craftsmen were independent, each one responsible for one loom, and involved in a complex relationship of exchange with the institution.

In this respect, RSFSL had a threefold form of control on labour. First, there was a form of ex ante social control based on their being community members, the training received and the threat of symbolic or real punishments for breaching any community or factory rules. Second, the performance of workers and apprentices who were not members of the community was closely monitored in terms of surveillance, aiming to control factory work. Third, there was a form of ex post control, comparing results and objectives in terms of quality standards and production volumes.

If, on a micro-scale, accounting consists of ‘instruments that render visible, record, differentiate and compare’ (Foucault, 1977: 208), tools that allow ‘the construction of an individual person as a more manageable and efficient entity’ (Miller and O’Leary, 1987: 235), labour accounting in the RSFSL enabled the General Superintendent to monitor each individual performance. At the same time, the strong identity as a member of the social system of San Leucio included many beliefs and self-convincing attitudes to duty, efficiency and commitment to the community, which led each ‘internal’ worker of the factory to work as well as possible (Foucault, 1977, 1988; Hopper and Armstrong, 1991; Miller and O’Leary, 1987). On the other hand, the non-capitalist traits of the social experiment of San Leucio, as revealed by its accounting system, are basically three.

In the first place, there was a fixed rate of return on capital. The shareholders (first the King, then the charity fund as well) were not entitled to the entire surplus value (Bryer, 2000, 2005, 2006). Anything in excess of the 8% yearly rate of return was withheld and directly or residually allocated to the workers’ community or invested in the assets of the factory. If the capital only received a fair remuneration, the rate of return could not exceed a maximum limit and any profit above this limit was spent for the community, all such traits fit the ‘ideal’ design proposed by Owen (1817). The surplus value generated by the workers, as defined in Marx’s analysis (Marx, 1906), was not entirely appropriated by the capitalists but, conversely, was partly given back to the workers themselves through a number of benefits, as consistently shown by the accounts. The overall amount of the surplus value paid back to the workers consisted of food, training, health care, subsidies for the poor, goods and services provided free, as well as any undistributed excess from the aforesaid profits. At the same time, the general living and working standards of the community’s workers were comparatively better than those experienced in other capitalist contexts in those years, such as in the Industrial Revolution in the United Kingdom, in terms of wages, working hours, cleanliness, green areas and low levels of child labour. In this respect, workers’ wages, working hours and health and educational services are consistent with the utopian socialist reformistic viewpoint of this matter (Blanc, 1859; Owen, 1816).

Second, the worker-residents owned one loom each, so as the owners of (some) processing equipment were somehow capitalists too. As such looms were not owned by the RSFSL, they were not included in its nominal accounts. Such an exception is perfectly consistent with private property as a part of the means of production managed also in the interest of the community (Engels, 1999).

Third, there was no such thing as a true capitalistic spirit or even an ambition to maximise profits. The ethical and social foundations of the community and most owners’ adherence to such foundations weakened that spirit and that tension. As prominent utopian socialist scholars have argued, the local community, linked to the factory, was egalitarian and implemented some form of participatory democracy, even in the context of the despotic monarchy of the Bourbons (Fourier, 1851; Plekhanov, 2003; Taylor, 2013).

As well as exposing the operating systems of the factory–community system, the accounting system played a key role in supporting and legitimising an organisation that had a mix of innovative institutional rules. On one hand, the accounting system actually played a role specific to any capitalistic context: It measured the capital and the profits, and made the net profit and payout transparent to the shareholders (especially non-resident owners) as Marx and his followers widely stated (Bryer, 1999; Chiapello, 2007; Marx, 1909; Toms, 2010).

On the other hand, the accounting system played a specific role in allowing the ‘non-capitalistic portion’ of the institution to work. It focused on measuring the transfer of resources from the factory to the community and carried out in the interest of the community. The stakeholders, the managers, the resident-workers and the parish priest could control such transfers. The accountability and tracking of such financial and material flows, made possible by the accounting system, provided sound grounds for the moral and social legitimisation of the community–factory system, which supported each other and can, therefore, be regarded as two sides of the same coin (Davie, 2007; Funnell, 2001, 2004; Walsh and Stewart, 1993).

Accounting played a fundamental role in demonstrating the organisation’s performance to the main stakeholders (King, capitalists and community members). Therefore, such stakeholders could trust the numbers thanks to the reliability (if not objectivity) of recording transactions. The small group that ruled the community, along with the parish priest, had to understand the meaning of the records of exchanges between the community and the factory. It was essential for everyone to trust the economic and social order that governed the community, regarding this order as fair and efficient. The accounting with its objectivity could be considered one of the factors that built trust around such order (Porter, 1992, 1994, 1995).

Finally, measuring the workers’ performance and recording the transactions between the community and the factory, enforced the commitment, belief system, attitudes and loyalty of the ‘internal’ labourers and artisans. It helped to sublimate the technologies of the self, in which the community members need a weaker hetero-direction, since they absorb and make their own all the community expectations and pressures, with no need for any other external intervention (Foucault, 1977, 1988, 2007, 2008).

Conclusion

This article deals with one of the first and most important experiments of utopian socialism ante litteram undertaken in Italy between the late eighteenth century and the first few decades of the nineteenth century, that is, the community of San Leucio and its silk factory. The accounting system played a key role in making the complex economic and social body work. It measured total revenues and costs and calculated profits, a fixed part of which was allocated to the capitalists (the King and any other private investor), while the rest was allocated to the workers’ community. It also monitored the wealth distributed to the community and made it accountable to the general manager and, thus, indirectly to the King.

This article provides some contributions to accounting history literature. First, it adds archival evidence to the evidence of modern and contemporary Italian industrial companies that has already been reviewed by Italian scholars, including the Venetian Arsenal in the sixteenth century (Zambon and Zan, 2007; Zan, 2004), the Magona d’Italia, Manifattura Ginori, Ansaldo, Brioni (Antonelli et al., 2002, 2006, 2008; Sargiacomo, 2008) and food factories (D’Amico et al., 2016). Second, it supports the close bond existing between DEB and capitalism. The capitalistic dimension of the RSFSL required an accurate measurement of profits and rates of return, as claimed by Bryer (2000, 2005), Chiapello (2007) and Toms (2010). Third, it shows that the accounting system is shaped to reflect the different social organisation of a manufacturing company, and that such an accounting system is essential for the creation of non-capitalist production relations (Hopwood, 1983; Miller, 1994). Finally, the accounting system gave accountability to the wealth-producing and distribution processes that were grafted into control over the community, which was in turn made accountable by specific reports. Such a mechanism was enforced by trust in the accounting numbers (Porter, 1995). Thus, accounting strengthens the social mechanisms of belonging to the community and increases the feeling of justice and identification with the factory, together with some technologies of the self (Foucault, 1988), playing a significant role in enforcing the factory’s ethic and the social structure where it was embedded (Burchell et al., 1980; Funnell, 2001, 2004; Hopwood, 1983).

The limits of this article are mainly due to archival evidence. There are no account books at all for the years 1778 to 1802. In addition, also due to a lack of archival evidence, the balance sheets of the first period of business of the RSFSL could not be reviewed, so the yearly distribution of profits could not be analysed. Finally, since the documentation is not exhaustive, we could not fully understand whether the communal accounting system measured the wealth received from the factory and the way it was distributed among the community members according to their needs.

Our research paves the way for some other developments. It would be extremely interesting to compare the case of San Leucio with that of other manufacturing enterprises which, in other countries, have experienced similar social experiments, even if slightly later in time, such as New Lanark Mill, Orbiston, New Harmony and Earlton, all inspired by Owen and Fourier’s utopian socialism, or, in an agrarian context, the experiments of Mir in pre-revolutionary Russia and the kibbutz in Israel after World War I. Furthermore, our understanding of the accounting practices of Italian industrial companies in non-capitalist contexts could be enriched by research into state-owned enterprises, the cooperative systems based on Catholic or Communist beliefs and the communes or the Focolare Movement’s enterprises, after the 1970s.

Footnotes

Acknowledgements

Thanks are due to the participants of the eighth Accounting History International Conference, 2015, held at Ballarat in August 2015, for their comments on an earlier version of this paper. Special thanks go to Lee D. Parker and Carolyn Fowler for their helpful comments. We wish to express our appreciation to the anonymous referees for their constructive comments.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.