Abstract

This article responds to a scarcity of literature on pre-nineteenth-century accounting education and addresses calls for more research into what gave rise to how we teach accounting today. The sixteenth century was when double entry began to extend beyond its Italian roots and the first printed bookkeeping manuals began to appear alongside Pacioli’s of 1494. Yet, it is the least covered period in our literature. We address this lacuna using hermeneutic analysis to critically analyse Dominico Manzoni’s seldom studied manual of 1540 to discover what he hoped to achieve, what he did, and identify what impact his manual had on how accounting education and accounting practice developed thereafter. We find Manzoni’s objective was to replace school and apprenticeship with the printed book; and that his experience as an accountant and teacher of bookkeeping resulted in his adopting a highly innovative pedagogy that led, taught, and engaged students through the written word. Finally, we identify Manzoni’s manual as the foundation of a dominant genre of bookkeeping manuals that adopted an approach to accounting education which led to the widespread adoption of Pacioli’s definition of double entry and the double entry system in accounting practice that has lasted to the present day.

Introduction 1

The art of reading and understanding occurs through entering the universe of the author and discovering the core ideas of the author’s thought. (Koskinen and Lindström, 2013: 759)

It is widely acknowledged that a historical lens can provide insights into accounting practice: ‘accounting history . . . puts accounting today into perspective, and may well allow us to draw on the data bank of the past to provide solutions to the problems of present’ (Carnegie and Napier, 1996: 13). In particular, as accountancy is a progressive science (Haskins, 1904), its development is related to time, and ‘to know our past, then, is the better to understand our present and to forecast or control our future’ (Haskins, 1904: 141). Part of that development comes through accounting education.

Modern accounting practice is acknowledged as beginning with the standardisation of the double entry method defined by Luca Pacioli in his publication of the first printed bookkeeping manual, De Computis et Scripturis, in 1494 (Antinori and Hernàndez-Esteve, 1994). But while the roots of modern accounting lie in this first printed textbook, accounting education is considered to be simply a subordinate branch of accounting (Anderson-Gough, 2009; Evans and Paisey, 2018), with a relatively small footprint in the accounting literature, and little possibility of impacting accounting practice. It was not always the case. With few exceptions, when Pacioli’s manual was published, double entry was used only by Italians and Catalans (Davids, 2004; Day, 1987; De Roover, 1963). For centuries, as it spread across the rest of Europe, it was primarily through accounting education led initially by published manuals, not teachers of accounting, that the number of bookkeepers with knowledge of double entry grew. Yet, we know little of the detail of how accounting education developed after Pacioli and, in doing so, became increasingly influential upon accounting practice. Compounding this situation, Pacioli’s manual has been described as being unfit for purpose (Yamey, 2010: 145–146). Yet, it is accepted in the literature that we use Pacioli’s method and that our accounting systems have, at their core, the two account books central to Pacioli’s method: the journal and the ledger. Nowhere in the literature is there an explanation for how Pacioli’s manual, assessed by Yamey as incapable of teaching anyone double entry, became so influential that we still adhere to its main principles today.

This article seeks to address this lacuna by focusing on the sixteenth century and the approach to accounting education presented by the first author to adopt an alternative to Pacioli’s pedagogy, by using rules and exemplar books of account to assist learning. That author was Dominico Manzoni. His manual was first published in 1540: Quaderno doppio col suo giornale novamente composto et dilegentissimamente ordinato secondo il costume di Venetia (trans. The double entry ledger with its journal newly prepared and diligently organised following the Venetian custom).

Very little attention has been paid to it, or any of the other manuals published before 1600. Those few who have considered it have failed to focus on the detail behind the shift away from Pacioli’s pedagogy that it presents. Analysis of the text has been superficial and the way in which Manzoni taught the subject has not been considered. For example, Saporetti (1898) dismissed it as a copy of Pacioli’s manual, which it is not; and while Yamey (1980, 2010) briefly discussed Manzoni’s use of an alphabetic index and his use of exemplars and rules, he failed to assess the underlying pedagogy. The only view he expressed about the pedagogy was that it contained rules and that it was a far more useful text than Pacioli’s because of the exemplar account books it contained.

The first to mention the pedagogy was Sangster (2018a), who noted that it unified the approach of the bookkeeping tutors (Sangster, 2015, 2018b) with Pacioli’s, forming ‘the basis for virtually all the bookkeeping manuals published until the mid-seventeenth century’ (Sangster, 2018a: 323). This article evaluates that assessment by addressing the research question, ‘What was the contribution of Manzoni’s manual to the historiography of accounting education?’.

Research method

In historical studies, context is central to understanding, no less so than when individuals and/or their work are the subject (Lee, 2002). Thus, this study adopts an interpretive historical approach (Carnegie and Napier, 1996; Previts et al., 1990), applying hermeneutics in a critical analysis of Manzoni’s manual. This involved positioning the manual within the educational, commercial, economic, financial, and social contexts of the period, while engaging in a circular process of reading and re-reading the text to generate deep levels of understanding. 2 This process facilitates detailed consideration, in context, of what Manzoni did in his manual that may have impacted accounting education; and of why he adopted the approach identified.

As we shall demonstrate, this study confirms Sangster’s appraisal and reveals that Manzoni’s dual background, as both accountant and teacher, enabled him to identify an approach that would facilitate learning from a book, rather than from a tutor or a bookkeeping master. His experience also enabled him to understand the indivisibility of rules and examples in accounting education; and led him to structure his manual in a new way that changed how printed manuals of bookkeeping and their pedagogy were structured from that point on. Its influence on the later manuals facilitated learning of the subject and the spread of double entry bookkeeping across Europe in the sixteenth, seventeenth and eighteenth centuries. Even today, some of the pedagogical devices within it, intended for self-instruction, would be as relevant in the classroom as in a teaching text.

The next section considers the literature on the history of accounting education. This is followed by consideration of how mercantile education developed between the eleventh and fifteenth centuries, and the part bookkeeping played in that education. The next three sections present the structure of Manzoni’s Quaderno Doppio and his exposition of the method of double entry bookkeeping, highlighting his contribution to the evolution of a pedagogy inherent to the teaching of accounting to the present day. The final section presents some concluding comments.

The history of accounting education

As a ‘branch of a branch’ of enquiry, the history of accounting education has a noticeably small presence in the accounting literature. With respect to accounting historians, it is ‘not yet the subject of significant study’ (Edwards, 2011a: 37). It is even less evident in the accounting education literature: a series of reviews of publications in the leading accounting education journals (Apostolou et al., 2010, 2013, 2015, 2016, 2017) found that among the numerous themes appearing in those publications, a historical perspective on accounting education is marginal, not present in all the journals, and it is almost non-existent if the focus is on the period before the nineteenth century. Our knowledge of how accounting education, and thus, accounting practice evolved is therefore ‘far from comprehensive’ (Evans and Paisey, 2018: 3). One of the first to highlight this lacuna and call for it to be addressed was Anderson-Gough (2009: 298):

[It is recognised that] modern accounting and its education did not simply appear when professional organization commenced during the 1850s . . . [These formative traces in wider educational practices] need to be explored in order to understand the shaping of accounting education.

It is largely outside the accounting education literature that we find the few authors who have gone further back into the past of accounting education – in mainstream accounting journals, economic history journals, accounting history journals, and books.

These include Coronella’s (2014) biographic study of Italian authors and their bookkeeping and accounting texts from the fifteenth to the twentieth century; 12 chapters on the history of Italian accounting education in The Origins of Accounting Culture (Sargiacomo et al., 2018); a special issue of Accounting History on ‘Histories of Accounting Education’ (2018); and the subsequent creation by the editors of that journal of a virtual online issue 3 of selected articles on this topic. Most noticeable among the rest of this literature are the works of Sangster (fifteenth century), Edwards (seventeenth–nineteenth century), Jeannin (sixteenth–eighteenth century), and Yamey (fifteenth–eighteenth century).

Sangster’s work has two foci: (1) accounting education before Pacioli published his double entry bookkeeping manual in 1494 (Sangster, 2015, 2018b; Sangster and Rossi, 2018); and, (2) the innovative approach Pacioli adopted in his teaching of accounting (Sangster, 2010, 2018a, 2018c; Sangster et al., 2014, 2007, 2008, 2011).

Edwards has published extensively on the history of accounting education in England after the sixteenth century, with a focus on English and Scottish manuals, and some of the teachers (Edwards, 2009, 2011a, 2011b, 2015; Edwards et al., 2009).

From a European perspective, in 1991 Pierre Jeannin presented a brief, 17-page overview of the historiography of 782 editions of manuals of bookkeeping and accounting published between 1501 and 1800. It included discussion of where they were published, the authors, their profession, and the success of their manuals in the marketplace, but relatively little about their content. Yamey (1967, 1980, 2004, 2011) also did so, but on a much smaller scale, while reflecting on whether or not instruction contained in the manuals led to the subject of double entry being learned and applied. On this point, Jeannin had no doubt: ‘the [number of editions] speaks clearly about the interest in knowledge of the art of accounts’ (1991: 256).

As is evident above, the sixteenth century remains relatively unexplored as a field of study on the history of accounting education and its impact on accounting practice. Yet, it is the period when other printed manuals began to appear alongside Pacioli’s, when use of double entry by non-Italians began to spread, and when the method and the account books in use standardised. This was not the result of the users of double entry, the Italian and Catalan merchants, revealing their bookkeeping secrets and teaching others how to do double entry, unless they were all Venetian – even a cursory glance at surviving account books from the fifteenth century reveals that the approach adopted across Europe in the sixteenth, seventeenth, and eighteenth centuries was unique to Venice. It was, therefore, the manuals of the sixteenth century that paved the way in how accounting was taught and in how accounting was done in practice. Thus, when it began to be taught in schools at the end of the sixteenth century, as can be seen from the manuals of the seventeenth and eighteenth century, it did so in a relatively standardised and uniform way.

As today, each new manual had variations of its own, some that enhanced and improved accounting education practice, others that did not. One noticeable feature of these manuals is that, while they adopted Pacioli’s description of the Venetian method with its journal and ledger at the core, they all failed to adopt his principles-based pedagogy (Sangster, 2018c). Studying the manuals of this period should offer some new perspectives on the history and development of accounting education, including revealing why the manuals published after the sixteenth century did not use Pacioli’s approach to accounting education.

The earliest signs of formal accounting education: from the abaco schools to Pacioli’s Summa

After the early Middle Ages, the population of Europe slowly began to shift away from the country into existing towns. This trend continued and new ones began to develop in the ninth century. From the eleventh century, much earlier than anywhere else, the Italian economic panorama began to change dramatically. Land registries were created and ordered, and there was a need for technicians who could calculate land surfaces. Trade and exchange flourished and new professions began to appear, including banking, which emerged in the twelfth century. In the same period, major international fairs were established in Flanders and then Champagne; and Italian merchants established themselves as major international traders. Double entry bookkeeping emerged in Italy in the thirteenth century and was used almost exclusively by Italian merchants and Italian international merchant bankers until the sixteenth century. It was a period when, across Europe, cash was in short supply, and what cash there was circulated in multiple currencies of variable and varying value. Anyone wanting to buy or sell goods, or borrow or lend, faced problems in changing currencies and in calculating units of measurement, costs, and prices (Braudel, 2002; Cipolla, 1956; Gamba and Montebelli, 1987; Lopez, 1976; North and Thomas, 1973; Verlinden, 1963).

Knowledge of the practical mathematics needed to serve these demands became increasingly essential, not just for everyone involved in trade and banking, but also for governments, stewards managing feudal estates, craftsmen, masons, and other artisans. With increasing urbanisation, traditional instruction in these skills through apprenticeships was inadequate – there were insufficient masters to educate the swelling numbers moving into new roles. As a result, a pressing need developed for somewhere that all these practical mathematical skills could be taught outside the workplace. The two existing groups of Italian schools were not the answer: the Church schools did not provide this type of education; and neither did the scholastic grammar schools, with their focus on Latin and the classics of ancient Greece and Rome (Grendler, 1991).

This led to the emergence of schools teaching practical mathematics for business and trade in Northern Italy during the thirteenth century. The earliest known was established in Pisa in 1241. Its teacher, Leonardo Bigolli or Bigollo, also known as Leonardo Pisano – Fibonacci – was the author of Liber Abaci, the book written in 1202 upon which this form of education was built (Bonaini, 1857: 241). The aim of these schools defined their structure and how they operated (Girella and Cordazzo, 2018), in both the subjects taught and in how they were taught.

Their teaching adopted a practical orientation and case-by-case approach. It was prescriptive, not explicative; mnemonic-analogic and operative, and inductive rather than deductive. Overall, it was symptomatic of a combined orientation towards the practicalities of everyday commerce and the manual trades, crafts, and arts. This was reflected in its use of the spoken language, rather than the Latin of the grammar schools; and a curriculum which ‘defined . . . a practical culture relating to the technicians’ activity’ (Colli Franzone, 2012: 281): arithmetic, algebra, geometry, trigonometry, and commercial matters (Black, 2007; Giusti, 2011; Maraghini, 2011; Sapori, 1997; Ulivi, 2002; Van Egmond, 1981).

Before attending an abaco school, pupils first attended schools of reading and writing. While a few started attending abaco schools as early as 6, most were between 11 and 14 (Cherubini, 1996: 237), which was viewed as an age that was ‘pedagogically fertile and particularly suitable for acquiring preparations for a profession’ (Becchi, 2013: 183). Though the schedule of lessons and the length of the course differed from school to school, an abaco education typically lasted about two years. This was not, however, the only education these pupils received: when not at school, they continued their training in workshops and in the real-world mercantile environment: the workplace (Becchi, 2013; Goldthwaite, 1972; Grendler, 1991; Ulivi, 2002).

It was in the workplace that they learned bookkeeping, not in the abaco schools:

None of [the abaco manuals] reveals anything specific about the teaching of accounting practice. . . . Many of [the abaco] problems fall into the category of business – money, prices, exchange, mensuration, barter, partnership, interest, discount – but none explains how to keep accounts of monetary transactions. (Goldthwaite, 2015: 620)

The form of instruction in these schools and the absence of bookkeeping from their curriculum reached a turning point with the publication, in 1494, of Pacioli’s Summa de arithmetica, geometria, proportioni et proportionalità. A compendium of all the practical mathematics of the abaco schools, it also contained his manual on double entry. Pacioli’s book transformed the teaching of algebra and, hence, most of abaco mathematics, towards teaching by principles rather than by examples. This was also the approach he adopted in how he presented double entry bookkeeping (Sangster, 2018c).

In several studies, Sangster (2007, 2010, 2018a, 2018c; Sangster et al., 2014, 2007; Sangster and Scataglinibelghitar, 2010) has investigated Pacioli’s pedagogical approach and the place of his manual in the development of accounting education. In particular, he identified Pacioli’s style of teaching as a cognitive apprenticeship (Sangster and Scataglinibelghitar, 2010) and recognised several pedagogical devices in the manual (Sangster, 2010; Sangster et al., 2007, 2014), such as the presence of a summary announcing what is going to be covered and why; the use of backward and forward linking to other parts of the manual (and to other parts of the book); frequent contextualization; and the use of examples embedded in his theoretical material to aid understanding. From an accounting perspective, Pacioli introduced a mathematical explanation of the double entry method (Geijsbeek, 1914; Sangster, 2018c), so defining a ‘universal . . . model that could be used to understand all [such] phenomena characterized by duality’ (Colli Franzone, 2012: 284). He also defined a syllabus to be followed in teaching the method.

The result was ‘a framework for independent learning of the subject –how to organise the books, make entries, and a syllabus’ (Sangster, 2018c: 303), which detached the initial learning of the double entry method and system from the workplace, and also from the bookkeeping tutors and their schools. His approach is very theoretical and focuses on principles, not rules. Consequently, although he offers examples of various entries in relation to the topics he introduces, and does so in context, he does not provide an overall context to which each item taught can be related. There is no simulation of a business that brings the theory to life in the way, for example, we may do today by using a case study. The example entries he presents are mainly generic, and most are without numbers and dates, which further reduces the contextualisation of what he was teaching to the real commercial world.

The size of Summa Arithmetica – more than 600 pages, of which only 27 pages were on bookkeeping – and its selling price of 119 soldi when popular books sold for 2 soldi (Sangster, 2007: 132) may have restricted access to only the more wealthy merchants and men of other trades, crafts, and arts. Nevertheless, many did buy copies and were able to read the bookkeeping manual: an average of as many as 70 copies were sold each year between its first printing in 1494 and its reprinting in 1523 (Sangster, 2007). Furthermore, in 1543, it was used as the basis for the first double entry manuals published in English, French, and Dutch. It was also used by Manzoni (Yamey, 2011: 287). However, as a manual written for beginners, the lack of ‘an illustrative set of accounting books in which the appropriate entries were entered’ (Yamey, 2004: 144) may have limited its impact, leaving others to add that feature in books of their own. The first to do so was Dominico Manzoni.

Dominico Manzoni and his manual

Manzoni was born around the beginning of the sixteenth century in Oderzo, a town 50 kilometres north of Venice. He was a computista (accountant) for the merchant, Alvise Vallaresso (Bariola, 1897), with whom he had grown-up and attended school in Venice (Geijsbeek, 1914: 9), and to whom he dedicated his book. He was one of the first practicing accountants known to have written a manual on double entry, something that many others did after him (Jeannin, 1991). In the dedication of a book of abaco mathematics published in 1553, he wrote that he was a magister abaci, and that he taught double entry to many people: ‘teaching both the theory and practice of arithmetic, geometry and double entry bookkeeping and also composing some works relating to this profession’ 4 (Mari and Picciaia, 2018). His work for the merchant provided the experience and resources to write his bookkeeping manual; and he drew on his employer’s accounts for the worked examples. His experience in both roles is reflected in many ways in the manual, including his advice on how accounts should be classified – in Chapter 13 of Part 1, he suggests that live things (i.e. personal accounts) go on the right in the alphabetic list of ledger accounts and dead things (i.e. real and nominal accounts) go on the left, 5 an approach that some later authors adopted (Yamey, 1980). He also introduced the practice of numbering all the example transactions at the end of his text and used those numbers to label each of the entries relating to them in the journal and the ledger, which makes considerable sense, pedagogically, but was not generally adopted by later authors. We explain why he did this later in this article (see Table 4).

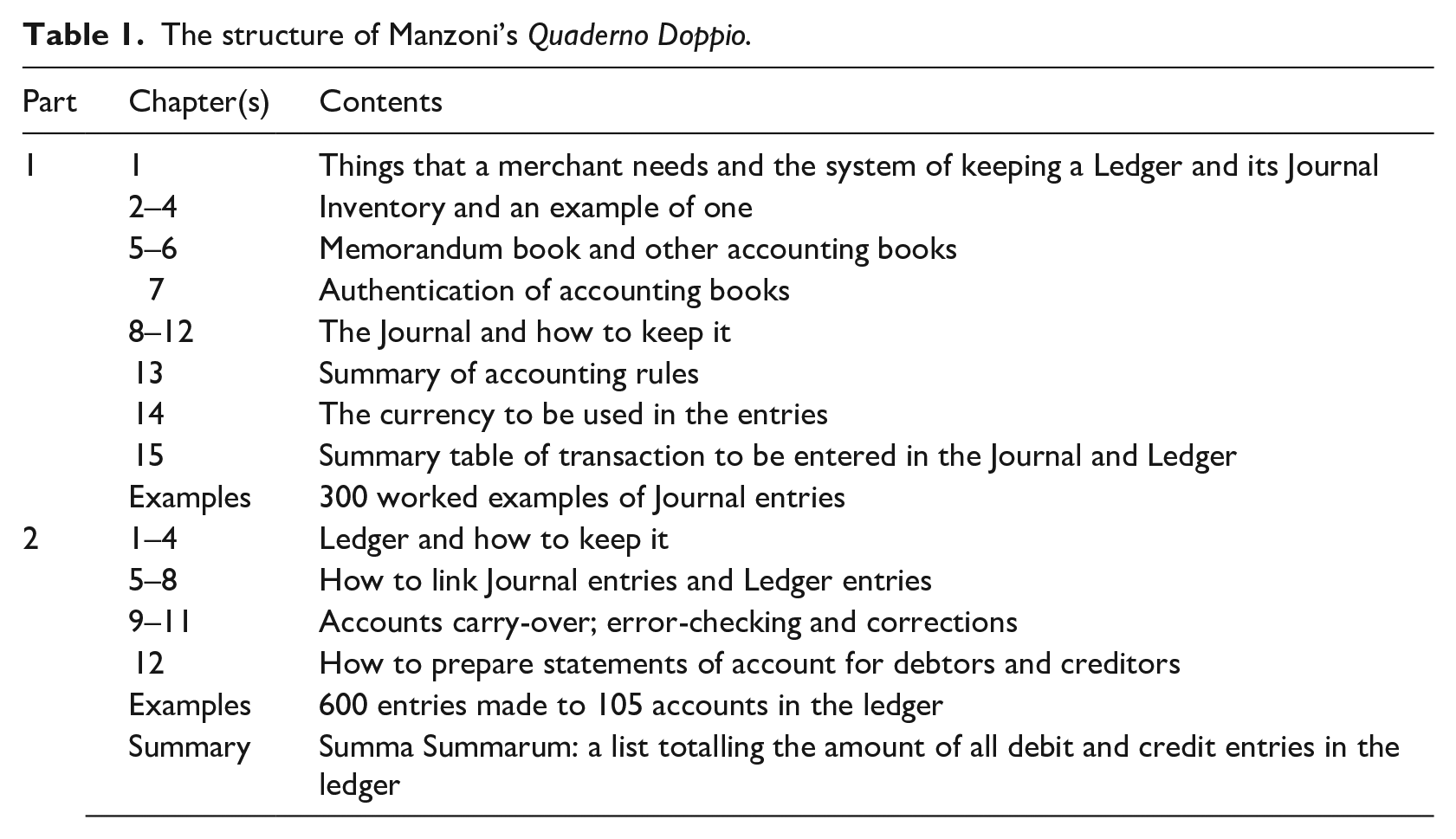

Manzoni’s Quaderno Doppio was published in 1540, followed by four other editions, in 1554, 1564, 1565 and 1573. It was also the basis for a manual published in German by Schweicher of Nuremberg in 1549 (Masi, 1997). The last three editions had a different title but the contents changed very little, apart from a few corrections and changes to terminology and dates (Alfieri, 1891), though an exemplar Alphabetic Index of the ledger accounts was added to the third edition in 1564 where previously it had only been mentioned briefly.

As shown in Table 1, Manzoni’s manual is divided into two parts, the first contains 15 chapters on the Giornale (trans. Journal), the second, 12 chapters on the Quaderno (Ledger). The first part also deals with topics of a more general nature, such as the authentication of books, the currency to be used in the entries, and the choice of Roman or Arabic numerals to avoid falsification (Mari and Picciaia, 2018).

The structure of Manzoni’s Quaderno Doppio.

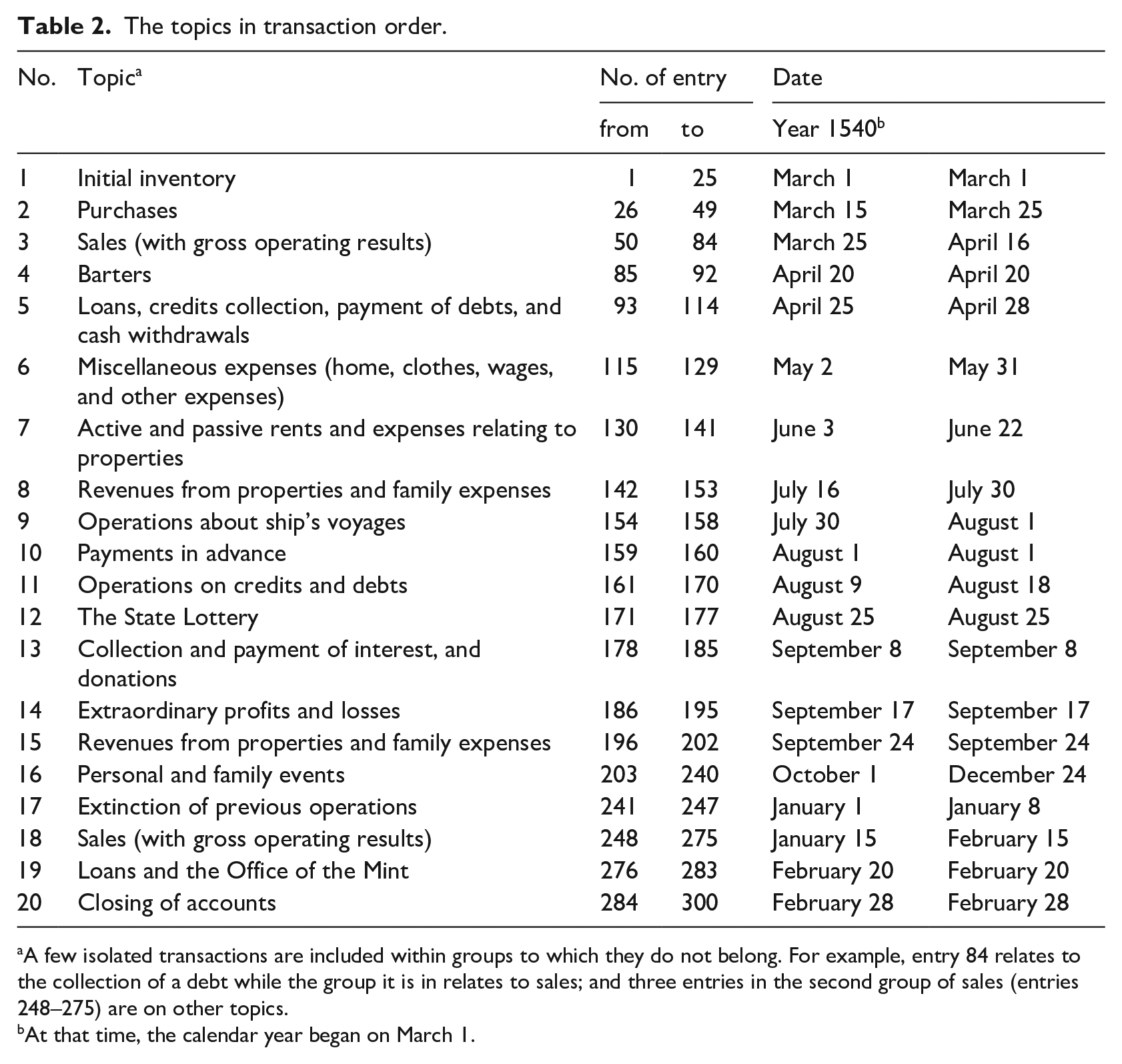

Manzoni used his accounting experience to contextualise all the transactions to mercantile life. But as is true of virtually all accounting textbooks, in using them he prioritised pedagogy over reality. Thus, the sequence in which they appear in the exemplar journal, presented at the end of Part 1, is clearly artificial and designed to ensure that learning of any of these topics can take place in isolation from the rest of the transactions. As shown in Table 2, the sequence focused upon the context of the transaction.

The topics in transaction order.

A few isolated transactions are included within groups to which they do not belong. For example, entry 84 relates to the collection of a debt while the group it is in relates to sales; and three entries in the second group of sales (entries 248–275) are on other topics.

At that time, the calendar year began on March 1.

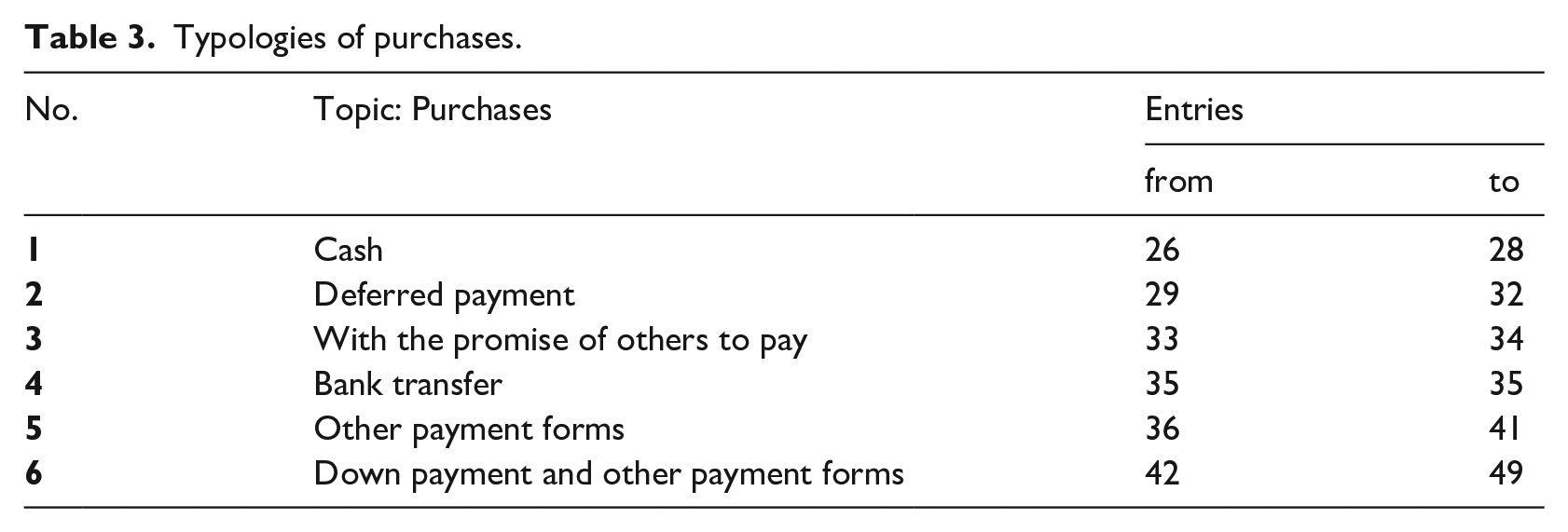

This list covers the typical activities merchants engaged in and recorded at that time. Within each topic (e.g. purchases, sales, etc.), Manzoni begins with the simplest operations, progressively increasing the complexity until the final entry. For example, as shown in Table 3, in the case of purchases Manzoni begins with cash transactions and gradually arrives at entries for down-payments and purchases with different forms of settlement (cash, barter, transfer of State loan, bank transfer).

Typologies of purchases.

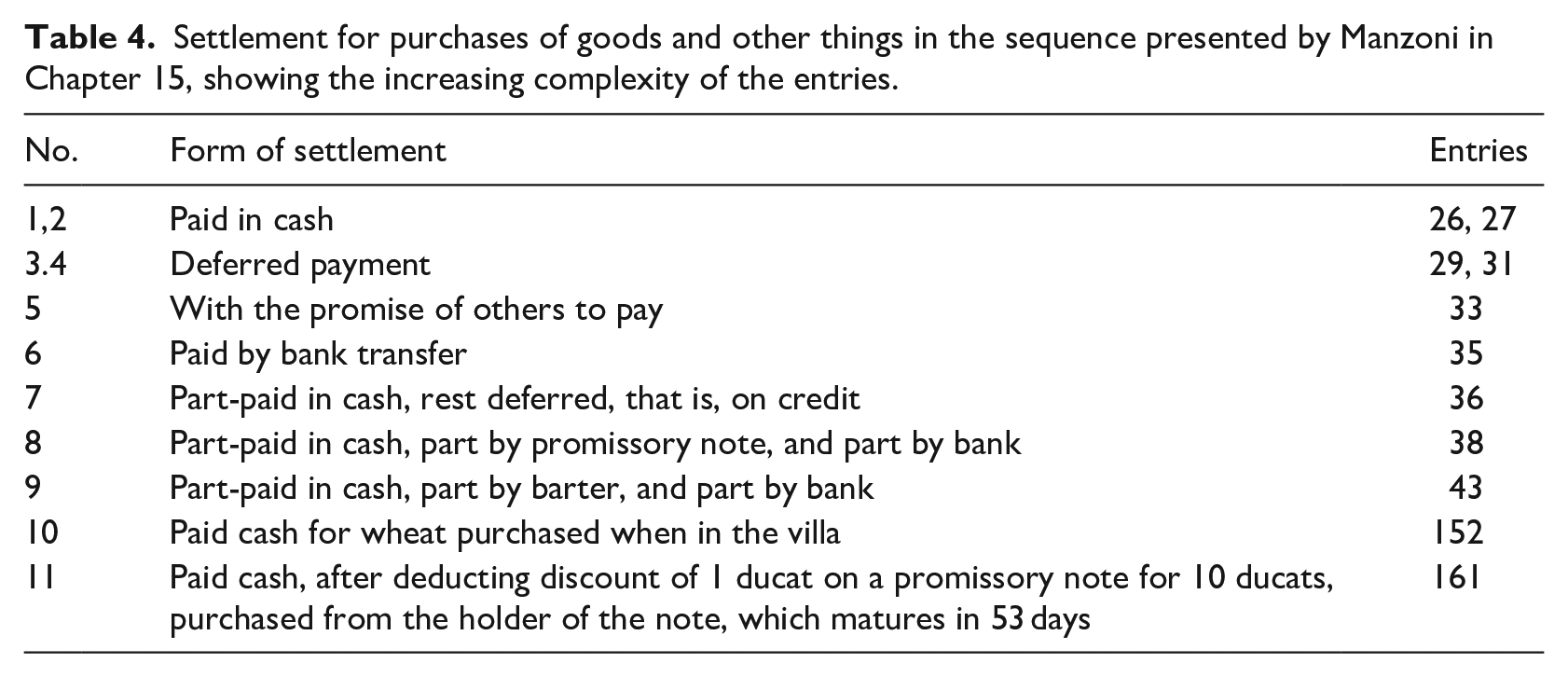

In Chapter 15 of Part 1, Manzoni also presented an alternative sequence in which to work through the entries, grouping the transactions under 40 ‘important’ themes. Table 4 shows Manzoni’s group of transactions relating to settlements of purchases, including two transactions that were not allocated to purchases in his numerically ordered list, and excluding many that were. This approach of tackling topics in multiple ways not only reinforced learning, it helped address the problem of matching the style of instruction to the differing learning needs and abilities of his readers.

Settlement for purchases of goods and other things in the sequence presented by Manzoni in Chapter 15, showing the increasing complexity of the entries.

The last two items in Table 4 illustrate how Manzoni reinforced the learning of topics by locating some relevant transactions outside their main group in Table 2. They present additional complexity to what was covered in that group. Item 10, the purchase of wheat when in his villa, would have challenged some of his students who were accustomed to all such activity occurring in the marketplace; and item 11 is considerably more complex than any of the other transactions, both in this group and in the 24 purchase transactions listed in Table 2.

Thus, by working through the manual from transaction 1 to 300, the reader would study purchases, for example, between transactions 26 and 49; and sales between transactions 50 and 84. Alternatively, he could choose to learn how to record any of 40 different types of transaction – the reader had a choice and could use the one he preferred or, if he really wanted to learn, both. The numbering of the transactions was obviously required if readers were to use this 40-category list. Those later authors who did not use this approach had no need to number the transactions unless they wanted to direct the reader directly to one in their theoretical text.

Despite the obvious educational benefits of adopting this dual approach, the pedagogical device of an alternative grouping of transactions is not used in many later manuals. It is not hard to understand why – doing so made the writing of a manual considerably more difficult – but that was not the only reason why few authors included one. As we will explain in the next section, Manzoni wanted to free learners from the need to be apprenticed and from the need to attend a bookkeeping school. In contrast, many of the later authors wanted the learner to both buy the manual and attend their school (Jeannin, 1991). Nevertheless there is, perhaps, a lesson here for a present-day author on how to strengthen the pedagogy in a textbook; and for others, who do not currently do so, to consider adopting in the classroom.

An analysis of Manzoni’s objective and his pedagogical approach in Quaderno Doppio

Manzoni’s objective is articulated in his one-page Preface, which is politely addressed to the ‘benign reader’. What he writes resonates with Pacioli’s declared intention in his manual to provide merchants with the tools they need, but Manzoni is more specific. He wants to make his knowledge of double entry available to all, particularly those who are unable to become expert in the art, ‘some because they do not have the means to attend a [bookkeeping] school, some because they have no masters and some, perhaps, because they are embarrassed to be under the discipline of others’ 6 (Manzoni, 1540: iv 7 ). That is, Manzoni believed that his manual would replace training in the workplace and school-based training from bookkeeping tutors, something Pacioli never came close to claiming.

Later in the Preface, he again follows Pacioli, declaring the Venetian method to be the best and highlighting that those who have the patience to read his manual will learn the concepts and techniques necessary to keep accounting records in an orderly fashion. In the Introductory chapter that follows (Manzoni, 1540: vi), Manzoni explains the structure of the text as a learning process in progressive steps, beginning with the opening inventory (essential for recording everything that is owned and to be used in carrying out the mercantile activity and maintaining his household) and passing from there to the two main account books (the Journal and the Ledger). When he later presents these topics in the manual, he also describes, step-by-step, the accounting method and, as we will discuss in detail later, uses signposting to indicate where related material can be found elsewhere in the manual.

Pacioli also did this. However, our analysis of Manzoni’s manual highlighted several innovative features that are absent from Pacioli’s. The first is Manzoni’s inclusion of 300 transactions and the resulting entries in the journal and ledger that many others have highlighted (e.g. Besta, 1922; Chatfield, 2014; Coronella, 2014; Sangster, 2018a). This is the most strikingly obvious of the innovations in Manzoni’s text – 10 times as many examples of transactions in the appendices as Pacioli included in his entire manual, and Manzoni matched Pacioli’s in his theoretical text. However, it is more than the existence of the exemplars that represents Manzoni’s outstanding and enduring contribution to accounting education. As shown in the section ‘The earliest signs of formal accounting education’, the sequence of transactions is structured to enhance learning by beginning each topic with simple examples and then gradually increasing the complexity. In itself, this was not ‘new’ – it was part of the bookkeeping tutor tradition, though done by them on a case-by-case basis rather than at the level of the transaction (Sangster, 2015, 2018b) – and it is something we still follow today in our textbooks and in our university accounting courses. However, what really stands out as innovative is the engagement-stimulating, story-telling nature that is present throughout the combined narrative of the exemplars.

In doing so, Manzoni evokes interest and invites engagement while fully contextualising the instruction through his 300 exemplar transactions, intended to represent the range of things that might be recorded in a real merchant’s accounts over 12 months. At times, they bring the manual to life, making the reading of the 300 example transactions more akin to reading a novel than reading a textbook – the day-to-day of business, happiness, sadness, success, failure, fortune, and disaster, all go hand-in-hand.

For example, after the business and family affairs have progressed ‘normally’ since business began on March 1, in August and September the manual is suddenly replete with a series of ‘everyday events’, such as investing in the lottery; winning the lottery; the loss of a bottle of wine confiscated because it was contraband; having someone return money the merchant had lost; paying for a friend to be released from the debtors’ prison; finding money in the street; and receiving from a priest the value of some silver stolen from the merchant by a thief (he had been given the money by the thief in exchange for absolution).

At times, it must have seemed more like reading the script of a satirical comedy than a serious textbook. But all the time the double entries are being learned and the understanding deepened. Perhaps, there is a lesson here too in how to engage students that many of today’s teachers of accounting could embrace.

Rules and exemplars

Principles, such as those adopted by Pacioli, can be applied to any situation. But where too narrow a contextual focus is presented, the lack of reassurance that the principles have been learnt can be problematic, such as when someone trained outside the workplace using principles is suddenly confronted with the variety and complexity of the real world. This gives rise to support for rules, such as we have today with the FASB’s approach to accounting standards as opposed to the principles-based approach of the IASB. Manzoni’s inclusion of 300 exemplar transactions may appear to have been the principal innovation he brought to accounting education but, it was only made possible by what is, arguably, his greatest contribution: rules. Today, virtually everyone teaches using rules, but few do so using a complete set of account books.

In doing so, he completely changed the previous approaches to teaching double entry. When he presents his rules for making double entries in Chapter 11 of Part 1, he implicitly rejects Pacioli’s use of principles to guide the learner in making double entries, relating all his rules to purchases and sales, and making no attempt at generalisation. He also rejected the approach adopted in the abaco schools and by the bookkeeping tutors, whereby learning was by induction from multiple examples. The examples, so dominant in the approach of the bookkeeping tutors (Sangster, 2015, 2018b), were transformed from the primary instructional device into a device that supported, reinforced, and encouraged learning. They were no longer the focus of the instruction, but the support that made it work, made possible by the inclusion of rules to guide learners through the theoretical text that preceded them.

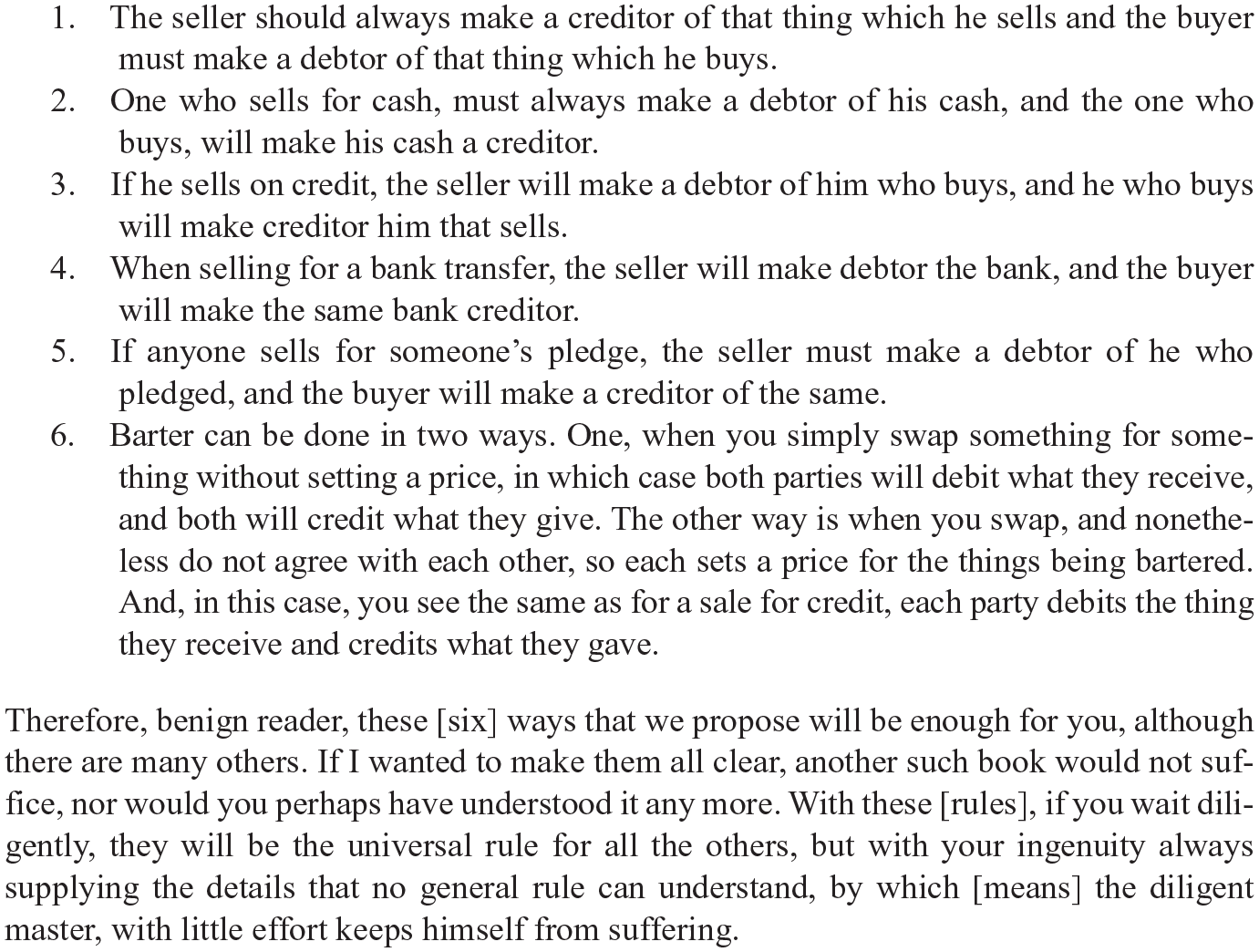

When discussing Manzoni’s rules in the literature, Geijsbeek’s (1914: 85) interpretation is used, but comparison with it to what is shown in Figure 1 demonstrates that his interpretation was incorrect. In contrast to what has been written about these rules, they were simple to understand and it is likely that they would have guided readers through the rest of the theoretical text.

Manzoni’s rules for double entry, Part 1, Chapter 11.

Overall, the introduction of rules supported by exemplar transactions and entries in the journal and ledger represents a major evolution of Pacioli’s links between theoretical explanation and the relatively small number of example entries scattered across his main text. Sangster and Scataglinibelghitar (2010) identified Pacioli’s instructional approach as a cognitive apprenticeship: with explicit links between theory and related worked examples. But Manzoni did this on a far greater scale and with a new emphasis on building upon what has been learnt, something Pacioli avoided because he wanted the learner to develop his use of the method himself. Thus, Manzoni took the responsibility for learning away from the reader and replaced it with directed learning that pulled the learner to a higher level of expertise than is possible in Pacioli’s manual.

As with the inclusion of exemplar transactions and their entries in the journal and the ledger, and the use of stepped learning by increasing complexity as learners progressed through each topic, rules were adopted by virtually all the later authors of manuals on double entry, where none had done so before. These three innovations, one a reworking of an existing approach, one an existing approach that had been avoided by Pacioli, and one completely new, are Manzoni’s enduring contributions to accounting education: ‘After Manzoni, authors did not conceive of a manual without including exemplars’ (Jeannin, 1991: 247).

Devices to assist learning, understanding, and application

The overall philosophy of the manual is clear: making complex topics simple and comprehensible by using a mixture of a linear approach and a context-specific, less-linear style; along with clear language, explaining what will be treated, and showing how to follow a clearly defined order that facilitates the progressive learning of topics. All these characteristics pervade the entire manual. The result is a well-organised and highly focused pedagogic text. For example, Manzoni explains very simply the logic behind the double entry method, stating in Chapter 11 of Part 1 that entries in the journal will always include, ‘one who gives, the other who receives, and that thing that is given or received, and also the reason’.

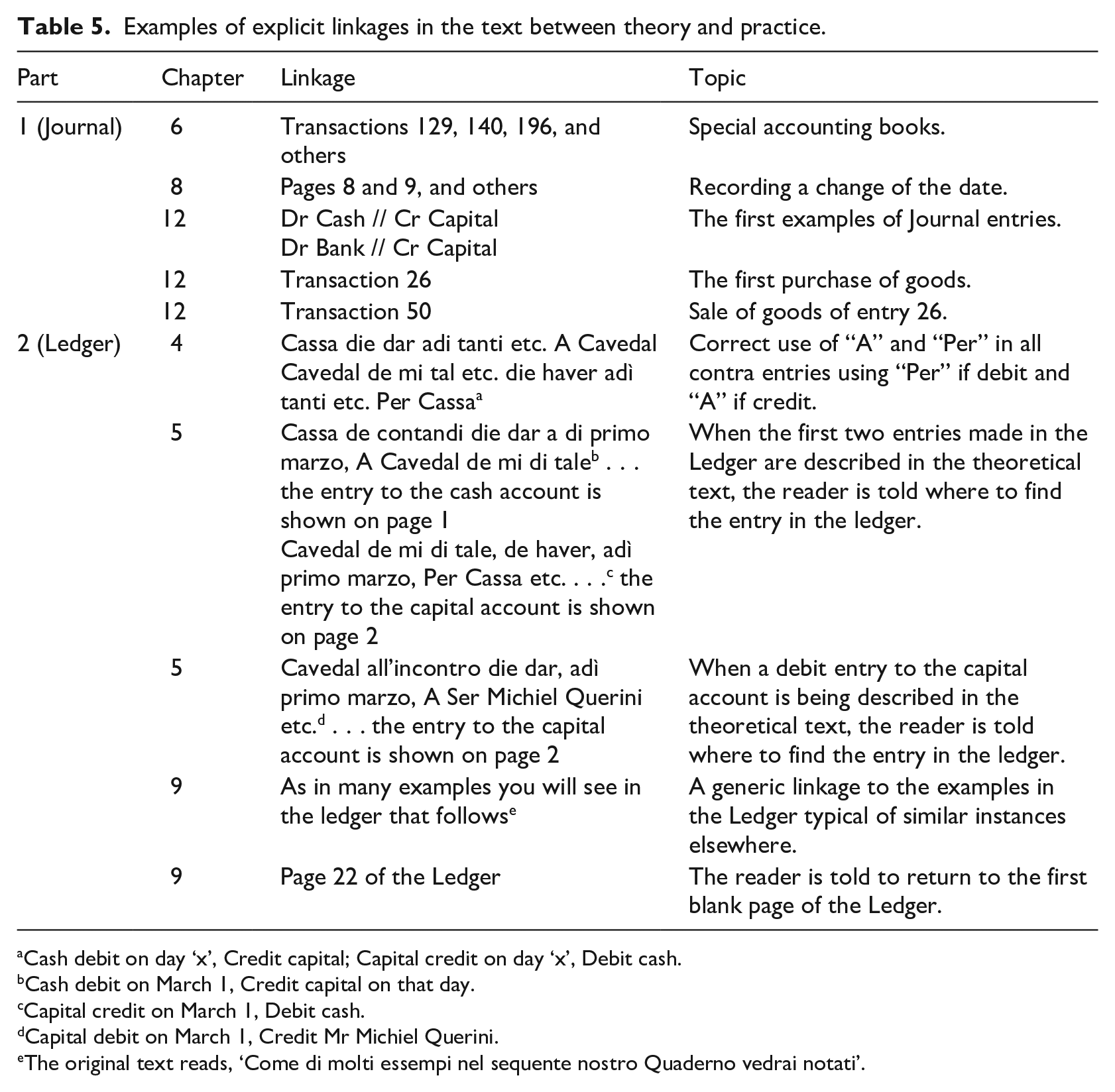

Manzoni clearly believed that by including his 300 exemplar transactions, it was possible to better understand, learn, and apply what is presented in the theoretical part of the manual, which could otherwise be seen as overly verbose and boring. To this end, as shown in Table 5, he makes several explicit connections between theory and practice. For example, in Chapter 6 of Part 1, when he describes specialist account books used for narrowly defined purposes [Libro Spese menute – trans. Book of incidental expenditures; Libro de Villa – Book of the villa; and Libro dei Salariadi – Book of the employees], he indicates the entries (129, 140, and 196) in which these books are used.

Examples of explicit linkages in the text between theory and practice.

Cash debit on day ‘x’, Credit capital; Capital credit on day ‘x’, Debit cash.

Cash debit on March 1, Credit capital on that day.

Capital credit on March 1, Debit cash.

Capital debit on March 1, Credit Mr Michiel Querini.

The original text reads, ‘Come di molti essempi nel sequente nostro Quaderno vedrai notati’.

As shown in Table 5, in some cases Manzoni indicates the page where the worked example that illustrates an explanation is to be found. When he believes topics are forbiddingly complicated but fundamental to learning the bookkeeping method, he advises the reader to take care and emphasises that examples are essential to understanding. He does so, for example, when he describes the aim of the Ledger in Part 1, Chapter 11:

It is necessary that the reader be careful, because this topic is very difficult, so this part will not be fully understood by every person. Nonetheless, as far as we can, with examples and [our] approaches, we will try to make it clear.

Practice and repetition are emphasised as being good for learning in many places, sometimes very soon after he had just mentioned it. For example, in Chapter 14 of Part 1, he writes,

If you were the best mathematician in the world, [without practice] you would remain sterile and inflexible, because it is practice that always [as they say] ‘gets your hand dirty’, and makes you see the real job. For this reason, the wise say that strength comes from doing.

Then, in Chapter 15, he asks his reader to be patient:

Sometimes, as much in this table as elsewhere, there are many duplications, repetitions of the same thing. Don’t be offended. What I write is mainly for those who do not know, to whom nothing can ever be too long, and brevity always brings with it some obscurity. And, I do not believe that this repetition will be without purpose, because things repeated are better remembered.

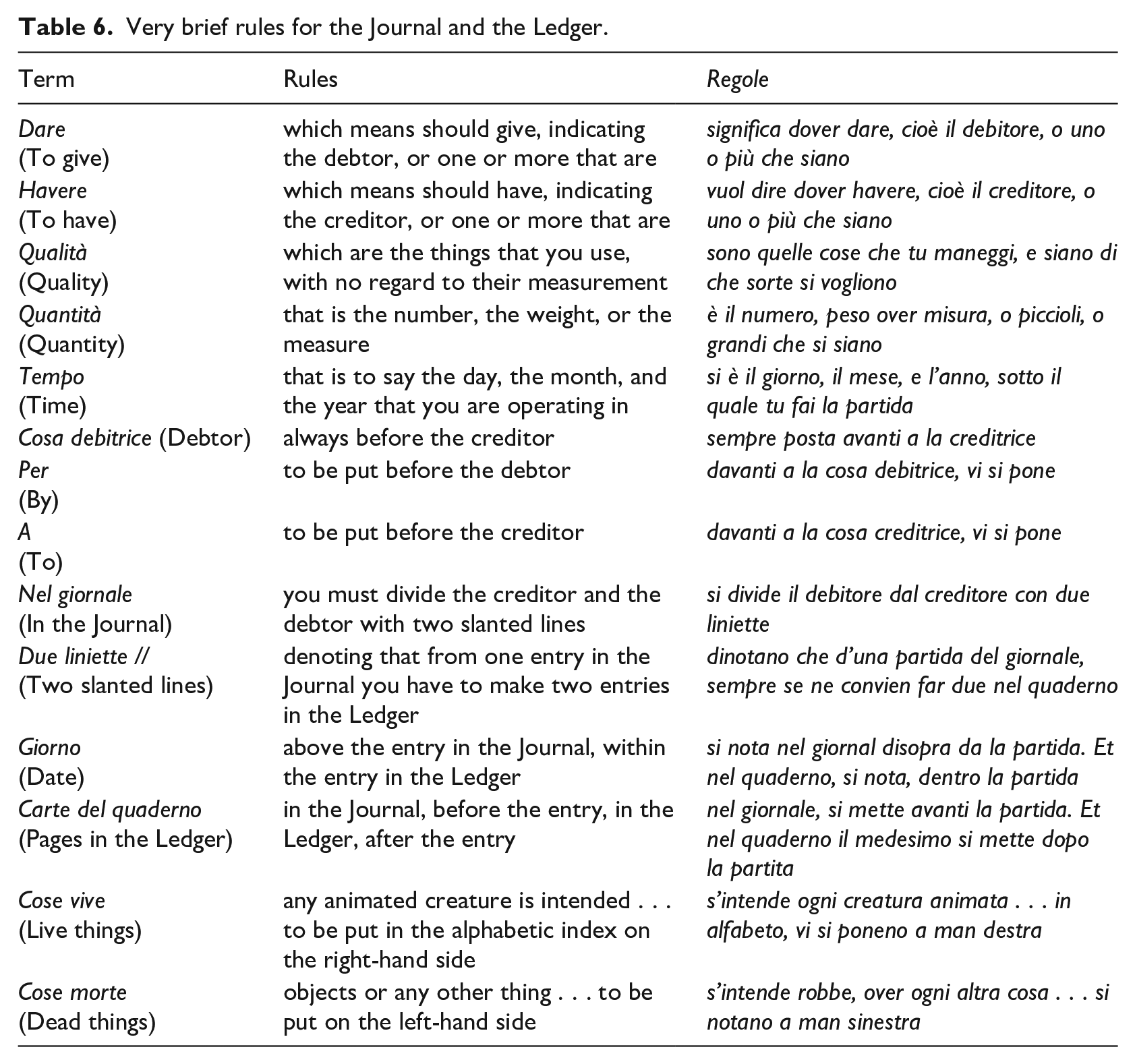

The explanations provided in Manzoni’s manual are sometimes very long, particularly when the topics covered are difficult and potentially confusing. He addresses this potential problem by providing schema to summarise several concepts. For instance, Table 6 presents an example from Chapter 13 of Part 1, Regole brevissime del giornale e quaderno (trans. Very brief rules for the Journal and the Ledger).

Very brief rules for the Journal and the Ledger.

The other schemas all serve a similar function: to help the reader to remember what is explained in a section of the text; and to provide an easy to find source of advice for those who need it.

Examples of entries in the Journal

Some examples from the manual are presented below. The way in which they are prepared follows the guidance presented in Table 6.

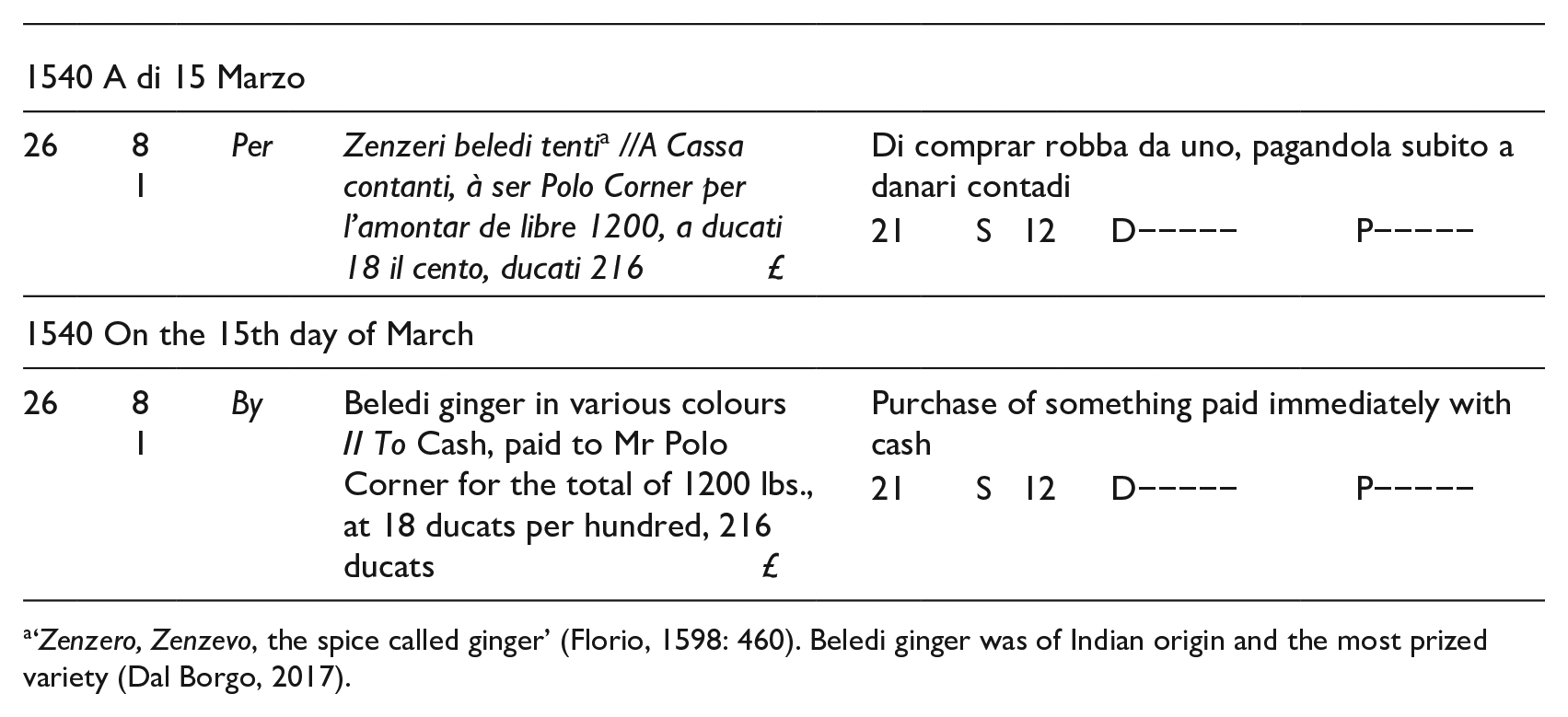

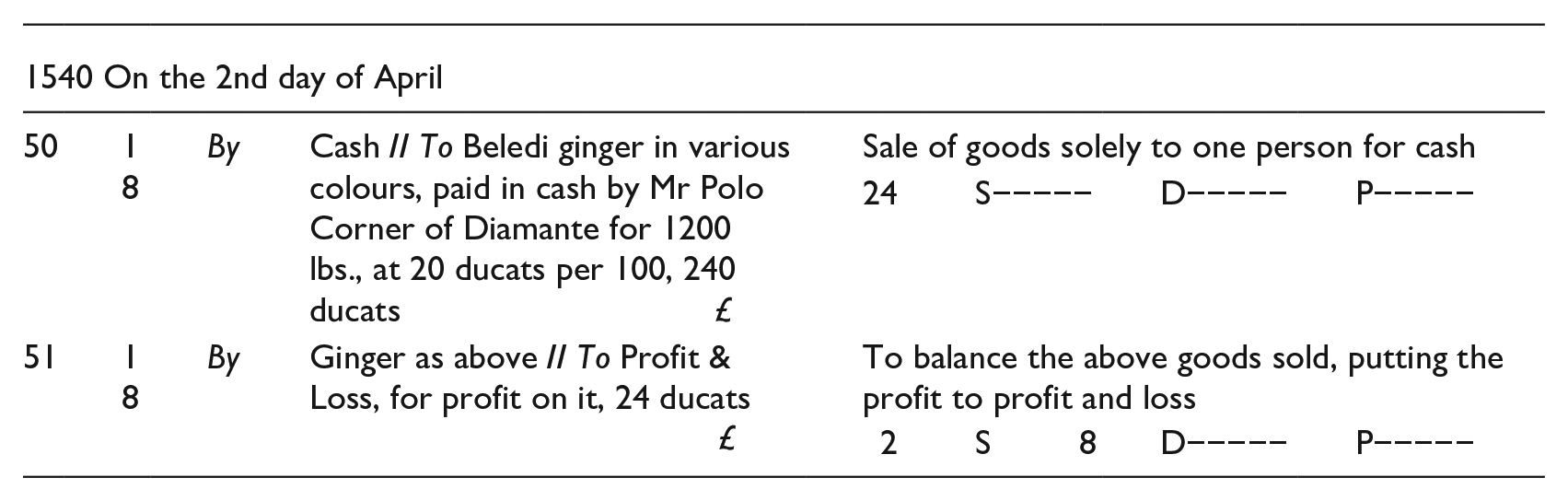

After making the entries relating to his Opening Inventory on March 1, the next entry in the journal is for a purchase of ginger on March 15, which was paid immediately with cash. As this is the first entry on that date, the date is entered above it. The number of the entry is then entered in the first column. In the second column is entered the number of the page in the ledger where the account to be debited (dare) is in the ledger; and, below it, the number of the page containing the account to be credited (habere). In the next column, ‘Per’ is written. The name of the account to be debited is then entered, then two slanted lines ( ‘//’), followed by ‘A’, then the name of the account to be credited, followed by the reason for the entry. At the end of that description, the symbol for lire (£) is placed next to the first monetary column. The entry is completed by entering the amount in the four monetary columns. 8 This entry is shown below.

‘Zenzero, Zenzevo, the spice called ginger’ (Florio, 1598: 460). Beledi ginger was of Indian origin and the most prized variety (Dal Borgo, 2017).

After the purchases have all been entered, sales are recorded for the period from April 2 to April 16. The first entry is for the sale of the ginger purchased above. The next entry is for the profit on the sale of 24 ducats, or 2 lire and 8 soldi.

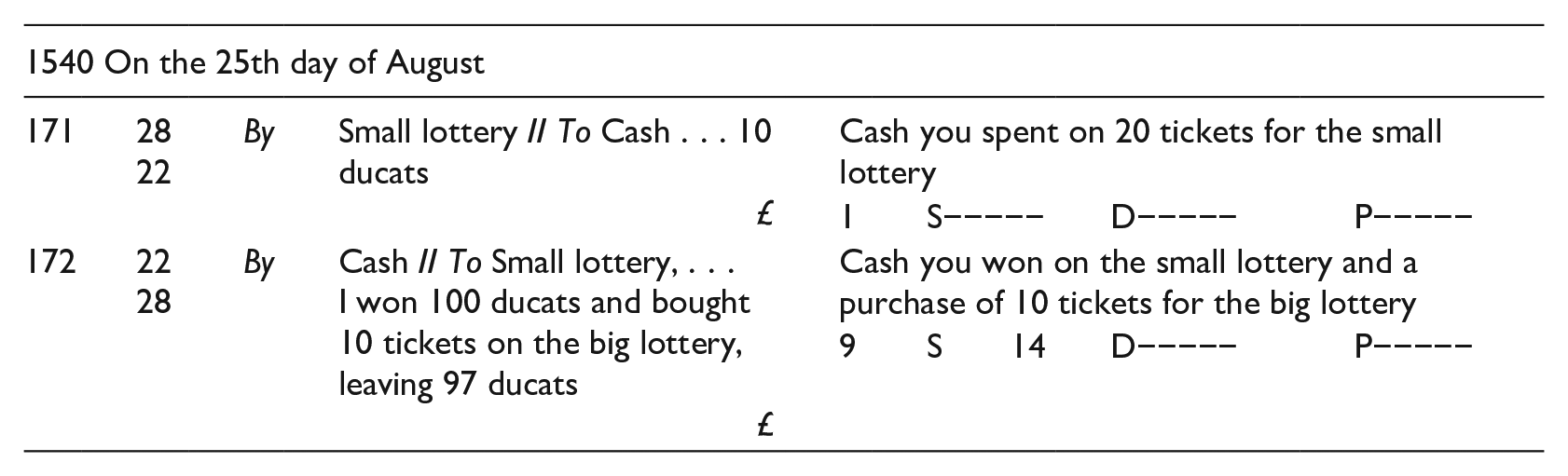

At that time, merchants did not distinguish between their personal life and their business. Personal transactions were, therefore, also recorded. The next example is for the purchase of lottery tickets. Two lotteries feature in the manual, the ‘big lottery’ (lotto grande) and the ‘small lottery’ (lotto piccolo).

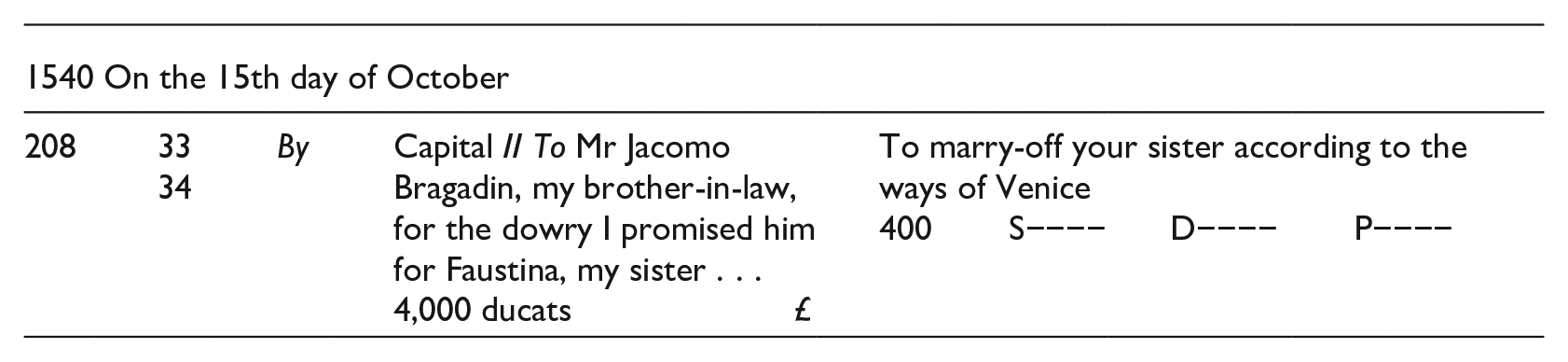

Another example of the intertwined links between business and the merchant’s personal life is a transaction involving the wedding of the merchant’s sister and his obligation to provide a dowry to his future brother-in-law. To do so, the promise to pay the dowry is recorded as a reduction of capital.

Concluding remarks

Manzoni’s Quaderno Doppio was the first manual to follow Pacioli’s syllabus and his pioneering inclusion of instruction in both the journal and the ledger in a single text. While much of Manzoni’s instructional text is firmly founded upon Pacioli’s, this study has confirmed claims in the literature that his approach represents an evolution of Pacioli’s use of cognitive scaffolding to support learning (Sangster and Scataglinibelghitar, 2010): Manzoni was the first to include rules to guide the learner in how to do double entry, and the first to place an emphasis on presenting both theory through instruction and exemplar entries – the pedagogy of the bookkeeping tutors (Sangster, 2015) – that Pacioli’s lacked. In doing so, he created a manual on bookkeeping that bridged the gap between theory and practice which Pacioli never sought to cross.

The way Manzoni presents his material owes much to his experience as both a computista working as an accountant in business, and as a magister abaci teaching classes in business mathematics and classes in bookkeeping to future merchants. This experience enabled him to present his teaching of double entry bookkeeping with deeply embedded innovative pedagogy. In doing so, he engaged his readers with realistic examples that resonated with the commercial and family world of a sixteenth-century Venetian merchant.

Our analysis of the manual identified several innovative features absent in earlier manuals. The first is well-known, though not so much for its pedagogical merits as for its utility as a source to use when struggling to record a transaction in the workplace: Manzoni’s use of 300 example transactions and the entries made from them in an exemplar journal and ledger. Basil Yamey (2010: 147) suggested that this was by far the best feature of Manzoni’s manual. However, these exemplars have never previously been analysed from a pedagogical perspective, either within the context of the rest of the manual, or in the context of the process of learning how to do bookkeeping from a text. The literature simply regards these as examples arranged chronologically by topic that could be referred to when required, and nothing else.

While it is certainly the case that this set of exemplars are sequenced chronologically from 1 to 300 and ordered by form of transaction or event in 20 unlabelled groups (Table 2), our study also found several pedagogical innovations relating to these exemplars not previously identified:

In each of these 20 groups, the level of difficulty or complexity increases as you move from one example to the next, so reinforcing the learning;

The exemplar entries are often referred to in the theoretical text by telling the reader the page on which an entry of the type being described would be found, or where a specific entry being discussed was located (Table 5). This tells us that the exemplars were intended to be used to illustrate the theoretical text, as well as to be studied later in isolation from that text, which is their purpose according to the literature;

Learning was reinforced by organising the same items in a second list, unrecognised in the literature, this time under 40 ‘important’ themes. Providing this alternative approach gave learners who struggled to learn from the 20-category list a more focused way to learn. For those who used both lists, this dual approach not only provided different contexts in which to study a particular transaction, but also served to broaden the learner’s knowledge of when and how a particular entry was made.

Manzoni’s numbering of each transaction made it extremely easy for a reader to find the entries in this second list, so assisting the process of learning by removing the problem of searching for a single entry among 300. (It also made it easier for anyone looking for how to make a particular entry to find what they needed.)

This alternative list also made explicit how learning was reinforced as readers worked through the entries, by returning to one of the 20 main topics when they encountered examples that extended what had been learnt about it earlier in the text (Table 4).

In addition, Manzoni’s inclusion of detailed examples to clarify the theoretical text is prescient of what research has shown to be a benefit of using worked examples in teaching the methods of accounting: an example can substitute for, or integrate more detailed written or verbal instructions. It can also represent a potential substitute for understanding rules, so reducing the cognitive effort required of students (Bonner and Walker, 1994; Halabi et al., 2005; Wynder and Luckett, 1999).

Other innovations introduced by Manzoni include his use of rules (Figure 1) that supported the learner through the rest of the theoretical text and, in particular, through his discussion of the ledger. The rules enabled readers to understand why items were debited and credited and, most importantly, guided them to select the appropriate account to use for those entries, a problem well-documented in the accounting education literature and highlighted by others, including the author of the next manual to be printed in Italian, Alvise Casanova (1558). Yamey (2010: 147) believed that Manzoni’s rules were of limited use, but our analysis refutes this conclusion. We found that the rules underpinned the theoretical material, so leaving the exemplars to reinforce the learning, mainly once the theoretical text had been completed. This prepared the way for the exemplars to support and reinforce learning at a level that the occasional illustration in the text or reference to an entry in the exemplars could not achieve.

Our analysis of the pedagogy in the manual also identified another pedagogical device in how the examples are organised, one designed to relieve boredom resulting from the complexity of business by shifting into the world of the family, while all the time reinforcing the learning of double entry through changes in context deeply emerged in the real world. In this context, we also identified how Manzoni endeavours to retain the attention of his reader through frequent emphasis on the importance of practice, no matter how repetitive and boring it may be. Neither of these features are evident in previous manuals of the bookkeeping tutors. More surprisingly given its purpose, they are also absent from Pacioli’s. Yet, they are particularly relevant to self-study, which was Manzoni’s aim in writing his manual: to replace the need to attend classes or serve an apprenticeship under a bookkeeping master in business.

This article set out to address the research question: what was the contribution of Manzoni’s manual to the historiography of accounting education? In sum, it set the foundations of all that followed, including many novel pedagogical features that to a greater or lesser extent were embraced by later authors. It was the first manual to combine theory with practice – the first to explain how to do double entry and offer an opportunity for the learner to practice how to perform it. It does so by, for the first time, providing a large number of example transactions along with the ‘solutions’ in the form of an exemplar journal and ledger constructed from those example transactions.

Virtually all the double entry manuals published after Manzoni’s, emulated his emphasis on practice through the inclusion of exemplar entries (Jeannin, 1991: 247), typically periodised into one economic cycle. Manzoni’s inclusion of rules, to guide the learner in making double entries, also became standard practice, and their number was increasingly extended, reaching a peak of 74 rules at the end of the seventeenth century in Edward Hatton’s Merchant Manual (Raven, 2014: 187).

The result of Manzoni’s efforts was a bookkeeping manual that embraced a novel and sophisticated set of pedagogical devices to teach double entry. It covered all the basic needs of anyone interested in learning how to do it from a text. As such, in the development of accounting education during this early period, Manzoni overcame the often-mentioned perceived shortcomings of Pacioli’s contribution and developed and extended Pacioli’s pedagogy in a new direction. Pacioli has the undoubted merit of representing a pivotal moment in the entire history of accounting, not only for making the first attempt to schematize and print instruction in accounting procedures, but also for his articulation of a theoretical approach to accounting education. But Manzoni took accounting education to a new level and presented an approach that his successors embraced. His manual was the foundation of how accounting is presented in textbooks today, and how it is taught in the classroom. Pacioli presented us with the method we still use today. Manzoni showed us how it could be taught.

Contribution

The history of accounting education is dominated by consideration of the work of one man, Luca Pacioli. No other medieval or early modern authors of accounting manuals or their works have been viewed as worthy of consideration beyond the occasional stand-alone study of their content, rarely their pedagogy. Despite some, such as Yamey (e.g. 2010: 145–146), denying the fitness for purpose of Pacioli’s manual; and despite there being no alternative to a manual for anyone wishing to learn double entry bookkeeping until the late sixteenth century unless they had an apprenticeship with a merchant skilled in the method, the literature does not question how Pacioli’s method and system of double entry is the one we use today.

This article has identified the link between Pacioli and the development of accounting education and practice in the sixteenth, seventeenth, and eighteenth centuries. In doing so, it has demonstrated the importance of filling-in the gaps in our knowledge if we are to truly understand how we reached the point we are at today. And it has shown that one way of doing so is by studying less known figures, their activities, and their works. This article has shown that accounting practice and accounting education owe as much to Dominico Manzoni, if not more, than they owe to Luca Pacioli. Without Manzoni, the influence of Pacioli’s manual may have been lost and we may all have a very different view of how to do double entry, of the books of account we should use, and of how to teach the method.