Abstract

The purpose of this article is to trace the emergence of bills of exchange in the late medieval and early modern periods in Europe and to discuss the primary reasons for the increased use of bills of exchange, which include: the need for cashless settlements; credit lending by merchant bankers; negotiability through agency; and avoiding charges of usury. Double-entry bookkeeping played a key role in facilitating each of these activities. The contribution of this article is to develop a better understanding of the emergence of bills of exchange and the origins of double entry bookkeeping in Northern Italy in the thirteenth century.

Introduction

The link between double-entry bookkeeping and the emergence of bills of exchange is representative of the relationship between financial innovation and commercial development. While seemingly distinct, double-entry bookkeeping and bills of exchange have a deep-rooted connection that underlines the evolution of commercial activity and the development of banking and finance in that both fashioned the landscape of modern accounting and commerce, thereby shaping the way economic transactions are managed, analysed and understood.

While prior research has examined separately the historical development of double-entry bookkeeping (Sangster, 2016, 2024) as well as the historical development of bills of exchange (Bolton and Guidi-Bruscoli, 2021; Santarosa, 2015), there is a need for research that contextualises their joint emergence within the broader history of finance and economics. In particular, while there is a general recognition of a connection between the emergence of double-entry bookkeeping and the use of bills of exchange (Matringe, 2022; Rosenberg, 1992), the precise causal mechanisms underlying this relationship remain underexplored. For example, how did the adoption of double-entry bookkeeping influence the use of bills of exchange as a multilateral financial instrument, and vice versa? (Matringe, 2020, 2022) Did double-entry bookkeeping facilitate the use of bills of exchange by providing a more accurate means of recording transactions, or did the emergence of bills of exchange lead to a need for double-entry bookkeeping (Matringe, 2022)?

Employing both the ‘inquiries’ (Garraghan and Delanglez, 1946) and the ‘source criticism’ methods (Buckley, 2016; Howell and Prevenier, 2001; Jones, 1999; Kipping et al., 2014; Langlois and Seignobos, 1898), it is argued that the adoption of double-entry bookkeeping was not merely a technical improvement in accounting practices but a transformative development that facilitated the expanded use of bills of exchange in the thirteenth century. This research shows that bills of exchange contributed to the development of a new era of economic development and growth by laying the groundwork for modern financial systems. Thus, this article explores how double-entry bookkeeping facilitated the growth of bills of exchange through four interrelated aspects: (1) enabling more precise financial management, (2) supporting new forms of banking and credit, (3) enhancing the negotiability of financial instruments and (4) avoiding usury laws. These four aspects are important because they address the fundamental challenges and opportunities of medieval trade and finance. Double-entry bookkeeping provided the precision, trust, and standardisation needed for complex financial transactions, supported the development of new credit mechanisms, and enhanced negotiability and liquidity of financial instruments. Together, they created an environment where bills of exchange could flourish, driving economic growth and expanding trade networks during the medieval period. The following section concentrates on the theoretical background of this research. The third section reviews prior research related to this topic. The fourth section presents the methodology and the methods, followed by the historical evidence regarding the origins of double-entry bookkeeping. The sixth section analyses the historical evidence regarding the origins of bills of exchange and the final section discusses and concludes this article.

Theoretical background

The synergy between double-entry bookkeeping and bills of exchange is observable in their complementary roles within the broader framework of banking and finance. Double-entry bookkeeping provided the foundation for recording and analysing financial transactions, while bills of exchange offered a practical means of executing transactions (Chaunu, 1995: 51; Lopez and Raymond, 1955; Pounds, 2013). As such, the relationship between double-entry bookkeeping and bills of exchange contributed to the growth of financial markets and the expansion of global trade networks (Miller et al., 1987). As merchants embraced these innovations (Mauro, 1990; Prestwich, 1979), they gained greater confidence in conducting financial transactions across borders, leading to economic growth. Over time, bills of exchange and double-entry bookkeeping evolved and adapted to meet the changing needs of finance (Ferguson, 1960; Greif, 2006).

At its core, double-entry bookkeeping is a method of recording financial transactions that relies on the principle of duality: every debit has a corresponding credit. This system, which originated in medieval Italy in the thirteenth century and was recorded by Luca Pacioli in the fifteenth century, revolutionised the way businesses managed their activities (Sangster, 2016, 2024; Winjum, 1971; Yamey, 1964). By recording both the inflow and outflow of assets, double-entry bookkeeping provided a comprehensive and systematic approach to financial management, enabling merchants to track their financial position, assess their profitability and detect errors or discrepancies (Lee, 2013). The emergence of double-entry bookkeeping coincided with increasing trade and commerce in Italy during the late Middle Ages (Goldthwaite, 2015). As business transactions grew in complexity and volume, merchant bankers located in Northern Italy, sought more efficient methods to conduct trade and manage their affairs (Tenenti, 1988). Because transporting coins and bullions across long distances was impractical, the bill of exchange emerged as a solution, enabling cashless transactions that were safer and more efficient (Leyshon and Thrift, 1997: 47; Miller et al., 1987). The bill of exchange not only facilitated more efficient transactions, but also reduced the risk of theft or loss during transit (Bolton and Guidi-Bruscoli, 2021).

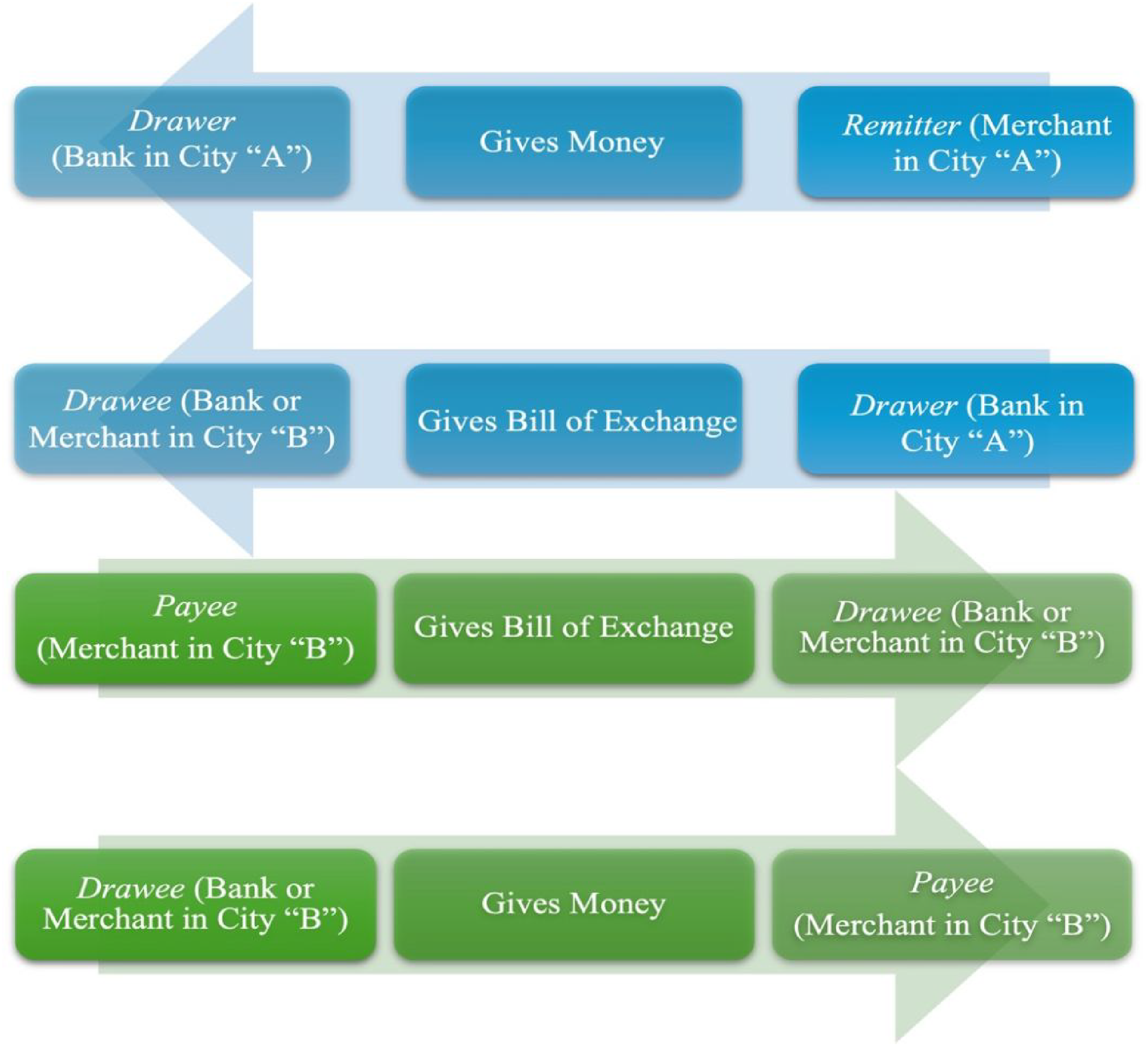

In simple terms, a bill of exchange is a written document given by one person to a second person instructing that person to pay money to a third person. A bill of exchange typically requires three parties, as indicated in Figure 1.

Structure of a bill of exchange.

The first person is the drawer, typically a bank that receives money from a remitter (such as a merchant who wants to make a payment to a person in another city). The second person is the drawee (meaning a merchant in another city, who is ordered to pay the bill). The drawee signs the bill indicating acceptance. The third person is the beneficiary of the bill (or the payee), who presents the bill to the drawee for payment.

Merchants purchased bills of exchange, which could be endorsed, negotiated and settled like modern-day cheques (Börner and Hatfield, 2017; Geva and Scott, 2011). Double-entry bookkeeping played a key role in facilitating transactions by allowing merchants to record transactions in a systematic manner (Irson, 2016). Each transaction involving a bill of exchange could be entered as a credit under the receiver's account and a debit under the payer's account. This tracking method ensured that cash flows could be managed without the actual transfer of physical coins or currency. The ability to account for financial transactions accurately increased the trust and reliability needed for cashless settlements.

As trade routes expanded in Europe, the need for agents who could act on behalf of merchants became important (Vercauteren, 1967). Bills of exchange were designed to facilitate this agency because they could be transferred to different parties (Velinov, 2017). Double-entry bookkeeping supported this transferability by providing a framework whereby such transfers could be accurately recorded, tracking the movement of bills from one holder to another. Each endorsement or transfer of a bill was recorded, ensuring transparency and accountability. This recording was important at a time when communication was slow, and merchants often had to rely on distant partners to conduct business on their behalf.

During the thirteenth century, religious and legal frameworks in many parts of Europe prohibited usury - the charging of interest on loans (Aho, 2005; Le Goff, 1988). Bills of exchange provided a way to avoid these restrictions. By drawing bills in different currencies, or from different cities where exchange rates could vary, merchants and bankers incorporated interest in the exchange rate differences (Leone, 1983). Double-entry bookkeeping supported this practice by allowing for detailed records that could reflect differences as gains in the accounting records. This practice allowed for the growth of credit while adhering to the letter, if not the spirit, of usury laws (Adamo et al., 2017; Galassi, 1992).

Review of prior research

Research on the links between double-entry bookkeeping and the bill of exchange provides insights into the theory of money and monetary exchanges by emphasising connections between financial instruments and economic practices in facilitating economic growth (Bernholz and Vaubel, 2014; Naismith, 2023). The connection between double-entry bookkeeping and the bill of exchange facilitates accurate recording of financial transactions. The widespread use of bills of exchange stimulated demand for bookkeeping methods to record the use of these financial instruments. Studying the historical evolution and interconnectedness of double-entry bookkeeping and bills of exchange sheds light on broader questions related to the nature and functions of money, which highlight the role of financial innovations and institutional arrangements in facilitating economic exchange (Cipolla, 1993).

According to Classical economists such as Smith (1776), money emerged naturally out of the inefficiencies of barter systems, providing a more efficient means of trading goods and services (Sultanum, 2024). Historians have used the term ‘commercial revolution’ (De Roover, 1942) popularised by Lopez (1976), to characterise the period in Europe beginning in the twelfth century and lasting until the beginning of the Industrial Revolution in the eighteenth century. Historians such as Laiou (1997), Spufford (1988) and Goldthwaite (2011) have argued that the Commercial Revolution began in Northern Italy. Polanyi (2001: 69) argued that: ‘politically, the centralised state was a new creation called forth by the commercial revolution.’ Likewise, in The Commercial Revolution of the Middle Ages, Lopez (1976: 63) maintained that: The key contribution of the late medieval period to European history was the creation of a commercial economy between the 12th and the 14th centuries, which was centered at first in the Italo-Byzantine Eastern Mediterranean, but eventually extended to the Italian city-states and thereafter to the rest of Europe.

Consequently, from a historical and theoretical standpoint, the focus of this article is on the late medieval and early modern periods in Northern Italy, when the commercial revolution began.

After the collapse of the Western Roman Empire, coins and bullion became scarce in Europe, causing a contraction in commerce and trade. Because trade was dangerous and expensive, there were few traders. The bill of exchange emerged as a way to engage in trade without the need to settle transactions in coin or bullion (Bell et al., 2017; Kohn, 1999). Accominatti's (2019: 6–7) delineation of the historical evolution of trade and banking in Western Europe before the nineteenth century showed that prior to that century international trade relied on localised, idiosyncratic lending practices within a caravan trade. This involved ad hoc partnerships, known as commendas, formed among fellow merchants for financing individual trading missions. As commercial hubs like the Champagne fairs lacked a clear legal structure for the development of multilateral financial flows, in the thirteenth century a change occurred with the emergence of sedentary trade (Gras, 1939), marked by merchants creating stable networks of correspondents, particularly led by Italian (especially Tuscan) companies (Epstein, 2008; Reinert and Fredona, 2017). This development, while not pervasive across Europe, facilitated multilateral trade flows within correspondent networks. Financial operations in these networks were still conducted by groups of related parties, albeit on a larger scale, with funding sourced internally from these groups.

The bill of exchange originated in this context as a non-standardised certificate, serving as evidence of a private credit contract between local agents within a closed business network. The creation of bills of exchange and similar credit instruments enabled Northern Italians to pay debts without having to transport cash, thereby transforming the Western economy through this refinement in banking and financial practice (Day, 1987; Goldthwaite, 2011; Lopez, 1979; Melis, 1984).

In the early modern era, the introduction of negotiability transformed the nature of the bill of exchange. This legal innovation extended juridical protection to the bearer of the bill, turning it into an exchange-traded financial instrument. This evolution had profound implications for the trade finance sector, contributing to the decline of medieval network companies and enabling direct lending between importing and exporting firms through the purchase of each other's bills (Accominotti and Ugolini, 2019: 6–7).

De Roover (1955: 115) has indicated that double-entry bookkeeping emerged during the commercial revolution in order to facilitate the functioning of bills of exchange, including cashless settlements, credit lending, negotiability through agency, and avoiding charges of usury. In essence, bills of exchange served as financial instruments facilitating transactions between distant parties. As merchants engaged in cross-border trade and sought more efficient means of settling transactions, bills of exchange emerged as a tool that allowed for credit lending.

In the accounting ledgers of medieval merchants, the use of bills of exchange was an important development (Savary, 1675: 181–215). Entries related to bills of exchange documented the issuance or receipt of bills, recording details such as the names of the parties involved, the amounts specified, the agreed-upon terms and the maturity date. These entries not only recorded financial transactions but also provided a transparent overview of the business's financial health (Orlandi, 2011, 2021; Sangster, 2016).

In addition, the bookkeeping entries related to bills of exchange reflected the evolving nature of financial instruments. Initially, these bills were idiosyncratic and tailored to specific transactions within localised networks. As trade networks expanded and became more international, bills of exchange evolved into standardised, negotiable instruments. This transformation is apparent in the details recorded in the accounting records. As noted by Orlandi (2021: 544): ‘as commerce intensified and merchant companies expanded, questions of efficient bookkeeping became tantamount, forcing accountants to build a pragmatic model that was not the result of abstract rules.’

The reflection of bills of exchange in bookkeeping records also highlighted the significance of legal and institutional frameworks in medieval finance. The ledger entries not only recorded the financial aspects of transactions but also documented the adherence to legal norms and regulations governing the use of bills of exchange. The inclusion of legal requirements in the bookkeeping entries demonstrated the integral role played by legal frameworks in shaping and legitimising financial practices during the medieval period (Sangster, 2016).

Research methodology

The methodology employed in this article encompassed two steps involving first, the analysis of the prior historical literature focusing on the commercial revolution in Europe and second, the emergence of double-entry bookkeeping in Northern Italy, during the late medieval and early modern periods. The value of this research methodology lies in its synthesis of prior research which offers a comprehensive perspective on the topic. As a result, the article provides a cohesive narrative. In studying the commercial revolution as well as the emergence of double-entry bookkeeping, this research seeks to increase its own validity and reliability as well as contribute to a better understanding of this important period in economic history. As such, this study draws upon reputable sources, cross-referencing multiple accounts, and identifying patterns and consensus among historians (Elbl et al., 2007). For this initial step, methods of collecting and evaluating primary and secondary data (Bloch, 1954; Mason et al., 1997) have been used.

The second step of this methodology focused on analysing and structuring a coherent narrative about double-entry bookkeeping and the bill of exchange.

For this purpose, this qualitative investigation includes methods of inquiry (Garraghan and Delanglez, 1946) and sources (Buckley, 2016; Howell and Prevenier, 2001; Jones, 1999; Kipping et al., 2014; Langlois and Seignobos, 1898; Smith, 1998, 2006) to (1) validate sources, establishing their credibility and ensuring verifiability, (2) apply the principles of triangulation inherent to case study research, utilising multiple sources (Floquet and Laroche, 2014: 119) and (3) apply hermeneutics (contextualisation) as explained by Westerberg (2024: 3).

The significance of this article lies in its ability to integrate prior research from various authoritative sources (Hunt and Murray, 1999), presenting a well-rounded understanding of the topic. This research could have started from the Medici's archives in Florence since they were important merchants in the Tuscany region. However, this would not be the optimal choice, as evidenced by the research of economic historians like Raymond de Roover.

Orlandi leans towards the rich contents of the Datini archives, in Prato, Tuscany region (Brun, 1930; Cecchi, 2004: 190; Melis, 1962). A vast array of documents is also located in the Venetian State archives under the Procuratori, and the Salviati archives in Pisa are a further potentially valuable repository. Existing scholarship already draws extensively from these archives, and the choice of this study was to build upon these prior sources rather than conducting new primary research for this specific inquiry.

This article adds scholarly value by encouraging a reflexive engagement with the historical evidence, thereby offering a re-evaluation of the existing historiography. As such, it is argued that this article presents a compelling and significant case despite its focus on the usage of prior literature, which it is argued, is important in this context because it contributes to the ongoing historiographical conversation, challenging conventional interpretations and offering alternative viewpoints, especially given the recent work of Sangster (2024).

Accordingly, this analysis centres on the works of well-known authors, among the various scholars who have studied the records and other materials related to the commercial revolution and double-entry bookkeeping including, but not limited to: Goldschmidt (1868), Usher (1914), De Roover (1955), Lopez (1976), Spufford (1988), Laiou (1997), Kohn (1999), Denzel (2006), Bolton and Guidi-Bruscoli (2008, 2021), Orlandi (2011, 2021) and Sangster (2016, 2024). These authors concur that the commercial revolution began in the twelfth century in Northern Italy and that the emergence of the bill of exchange and of double-entry bookkeeping were both important factors in this revolution. These authors have relied on historical documents to support their arguments, especially Goldschmidt (1868), De Roover (1956), Spufford (1988), and Laiou (1997). In particular, Goldschmidt (1868), who was a German historian of business law and the doctoral supervisor of Max Weber, studied merchant banking in Italy during the late medieval and early modern periods. De Roover (1944, 1948: 1953) studied the archives of the Medici Bank in the thirteenth and fourteenth centuries as well as the archives of the Datini trading and banking enterprises of the fourteenth century. Spufford (1988) created a detailed database of currency exchange rates for financial instruments, including bills of exchange in the thirteenth and fourteenth centuries.

Historical evidence on the emergence of double-entry bookkeeping

The accounting history literature recognises the use of double-entry bookkeeping as early as 1296 (De Roover, 1963b). However, Sangster (2016, 2024) argues that the thirteenth-century international trade and banking makes that date too late to mark the emergence of double-entry bookkeeping. Although few complete accounting records exist, Sangster (2024) indicates that four pages have survived from an account book belonging to Florentine bankers who were present at the international trade fair in Bologna in May 1211. This form of banking required the merchant banker to accurately record financial transactions (Aho, 1985; Carruthers and Espeland, 1991). The medieval Italian word for a business firm and the word for its account books were similar: ragione, from the Latin ratio (an accounting, a calculation, a reckoning). In its account books and articles of association, the company attained a concrete existence. Although the limited-liability joint stock company was a much later innovation, merchant banking companies emerged in the second half of the thirteenth century in Tuscany, where there are the earliest references to bookkeeping procedures involving double-entry bookkeeping (De Roover, 1974; Sangster, 2016, 2024). Tuscan bookkeeping records were eventually written in the bilateral format, showing debits verso and credits recto, which did not gain widespread European acceptance until the seventeenth century (De Roover, 1974; Orlandi, 2021; Yamey, 1964). According to Kuter et al. (2024), Datini was using double-entry bookkeeping by 1393 in his widely dispersed business empire. In addition, the Datini archives contain hundreds of copies of bills of exchange. Datini used double-entry bookkeeping to keep track of bills of exchange.

The use of bills of exchange in accounting facilitated trade transactions by providing a mechanism for deferred payment. In essence, a seller drew up a bill of exchange, which directed the buyer to pay a specified sum of money at a future date. This allowed for flexibility in payment terms and was employed in international trade where varying currencies were common. In the bookkeeping records, the issuance and acceptance of bills of exchange were reflected as amounts to be received and amounts to be paid. The bookkeeping entry recognised the bill as an asset or liability, depending on whether the drawer or drawee was doing the accounting. As the bill progressed through its lifecycle, entries were made to reflect any discounts, interest, or changes in the payment timeline, ensuring accurate financial reporting and compliance with legal requirements. The use of bills of exchange added a layer of complexity to bookkeeping records to reflect the nature of financial transactions associated with these instruments, which was both advantageous and challenging for companies; their recording in bookkeeping records required attention to detail. For example, the varying maturity dates, differing currencies and travel times between cities (usance) associated with bills of exchange required accurate recording.

The historical evidence surrounding the emergence of double-entry bookkeeping is characterised by a relationship between archival records, treatises, and practical applications. One of the challenges of accounting history researchers has been the scarcity of early accounting records, making it difficult to trace the precise origins and evolution of double-entry practices (Hernández-Esteve, 1994). The reliance on historical documents is further complicated by issues of interpretation because bookkeeping methods varied across regions and time periods. Additionally, the lack of standardised terminologies in historical archives presents a challenge to establishing a universally accepted timeline of the development of double-entry bookkeeping. While scholars have made efforts to present a consistent narrative, the inherent limitations of historical archives demand a constant reassessment of the provisional nature of conclusions regarding the emergence of double-entry bookkeeping (Sangster and Santini, 2022).

Historical evidence on the emergence of bills of exchange

The emergence of the bill of exchange represents an important chapter in economic history. This financial instrument, with roots reaching back to Rome and before, facilitated international trade transcending geographical barriers and adapting to the evolving needs of commerce. Several factors converged to foster the emergence and bills of exchange.

One of the primary stimuli for the development of bills of exchange was the decentralised nature of medieval trade. In the early medieval period, trade was localised, relying on barter or personal credit arrangements. As trade networks expanded, especially the limitations of the traditional mechanisms became evident (De Roover and Braudel, 1953). The bill of exchange, with its flexibility and negotiability, offered a solution by enabling merchants to overcome the constraints of localised transactions (Gras, 1939). In addition, the expansion of trade routes and the emergence of commercial centres like the French Champagne fairs in the twelfth and thirteenth centuries attracted merchants from various regions, creating a need for a standardised instrument that could facilitate transactions beyond the immediate location (Bautier, 1970; De Roover, 1963a). The bill of exchange, with its portability and negotiability, addressed this need, allowing merchants to conduct trade more efficiently across different markets.

As such, the development of the bill of exchange was closely tied to the evolution of merchant networks (Munro, 1994). The shift from ‘caravan trade’ to ‘sedentary trade’ during the thirteenth century, played an important role in this transformation (Gras, 1939). As stable networks of correspondents were established, the need for a reliable and standardised financial instrument became apparent. The bill of exchange evolved from a certificate of private credit to a negotiable financial instrument (Orlandi, 2021: 148–149; Rabinowitz, 1956).

Legal and institutional factors also played an important role in the development of the bill of exchange. The emergence of a juridical framework was essential for the growth of international financial flows. In this context, the legal recognition of the bill of exchange, either by making it legal tender or promising convertibility into gold, provided the necessary support for its widespread use.

The bill of exchange proved to be a transformative financial tool, but also faced challenges and limitations during its evolution. As mentioned earlier, Medieval bills of exchange were initially idiosyncratic instruments. The transformation into a standardised and exchange-traded financial instrument occurred with the introduction of negotiability, marking a significant shift in its nature and functionality. The following discussion indicates that the threads of cashless settlements, credit lending, negotiability and ethical finance were intertwined with double-entry bookkeeping. Through its systematic approach to recording financial transactions, double-entry bookkeeping not only facilitated the rise of bills of exchange but also laid the groundwork for modern accounting practices that continue to shape global commerce today.

The need for cashless settlements

In a world where gold and silver coins were not readily available, the need for cashless settlements became paramount (Mueller and Lane, 2020; Munro, 1979). Merchants engaged in long-distance trade faced the challenge of transporting coinage, risking theft and other logistical challenges. Hence, the bill of exchange was a paper-based promise to pay a certain sum at a future date. Double-entry bookkeeping facilitated this transition by accurately recording the transaction without the need for an immediate physical exchange of currency.

Goldberg's (2023) exploration of credit bills establishes a theoretical framework for understanding the concept of money. His study commences by addressing the necessity of money as a medium of exchange, distinguishing it from barter as a means of payment. Goldberg (2023) investigates how the need for money can be satisfied and how legal frameworks can smooth monetary circulation, by designating a legal tender or ensuring convertibility into gold. In instances where the demand for money is unmet, resulting in a monetary shortage, innovative solutions are required. This may involve new forms of money, sometimes necessitating circumvention of existing regulations. The capacity to invent and implement new forms of money is often associated with technological innovation.

Historically, there have been challenges for individuals who travel away from home, including the required need for funds during travel or residence abroad. In the medieval period, the Templar Knights protected pilgrims traveling from Europe to the Middle East and offered them the opportunity to deposit money or jewellery with Templar branches in Europe and to receive funds when they arrived in the Middle East: the Templars issued a letter of credit (an early type of bill of exchange) to departing pilgrims which they could cash when they arrived in the Middle East (Barber, 1994; Martin, 2004).

Another form of cashless money transfer in the medieval period was a promissory note, which specified payment of money at a distant location, on a specified date. There were usually two parties to the promissory note: the debtor and the creditor, and both were required to be present at the agreed upon location or to send an agent to complete the transaction. These promissory notes were made payable to the order of the person named, or to the bearer. What made the documents valid as a form of money transfer was that they were notarised and therefore legally valid (Barber, 1994). The relationship between the parties in a promissory note is similar to the relationship in a bill of exchange, but there are important differences. First, there was the requirement for the use of a legal notary to validate the document. Second, promissory notes were not used in mercantile trade; their purpose was primarily to transfer money. Promissory notes were primarily used by religious pilgrims and for the movement of church funds (such as tithes), as well as transfers of money to meet the expenses of students studying in distant places1,2 (Geva, 2016; Sangster, 2024; Usher, 1914).

A merchant traveling to a trade fair could make purchases at the fair using the bill of exchange. The lending merchant did not need to travel to the trade fair; instead, he could send a representative who could use the bill of exchange to make the cashless payment (Denzel, 2006). With the emergence of bills of exchange to make cashless payments, there was a safe way to transfer money. However, it was not legally possible to transfer a bill of exchange. This was because a bill of exchange had to be notarised and therefore the bill was restricted to the person specified in the written document; it was not possible to transfer a bill of exchange to a person who was not involved in the original transaction (Face, 1958).

The problem of transferability, or negotiability, was resolved at international trade fairs when the merchants gathered at aspecific place and at specific time of the year, thereby allowing for the settlement of bills (Munro, 2001). At the Champagne fairs, and later at the Geneva and the Lyon fairs, bills of exchange were settled during the fair through the balancing of merchant accounts. If the creditor in a bill of exchange was also a debtor in another bill, the accounts could be settled in a circle or giro. Unsettled account balances could be transferred to the next trade fair using a new bill (Face, 1958). Double-entry bookkeeping was used to record and keep track of these debtor and creditor transactions (De Roover, 1955; Sangster, 2024).

This manner of settling bills of exchange reached a peak in the Lyon fairs. The settlement of accounts was done by fair bankers who kept the merchants’ accounts using double-entry bookkeeping (De Roover, 1955). Because the fair bankers had accounts balances among themselves, cashless payments could be made by crediting and debiting the respective accounts. The Lyon fairs provided for a special money-of-account, 3 the écu 4 de marc, to which all other currencies were adjusted, thus, simplifying the settlement process (Denzel, 2006; Face, 1958). During the reign of French King Louis XI (1461–83), four annual fairs were held in Lyon, which drew merchants from all over Europe. Following the authorisation by Francis I regarding weaving privileges, which had been an Italian monopoly, Lyon became a major centre for the spice trade as well as the silk trade. Thereafter, Florentine immigrants established Lyon as a financial centre for banking and insurance (Face, 1958).

Cashless payments were further refined at the Genoese fairs, which were created specifically for trading bills of exchange, without any trade in goods (De Roover, 1969; Epstein, 1996, 2008). The development of a system of international settlement of bills of exchange several times a year led to a focus on cashless payments at these fairs, and they became the most important finance markets in Europe in the early modern period (Kindleberger, 1996).

The historical evidence surrounding the origins of the bill of exchange raises questions about the necessity for cash settlements and their impact on the development of this financial instrument. While some scholars argue that the bill of exchange emerged as a pragmatic solution to the challenges of long-distance trade, others emphasise the limitations of cash transactions in facilitating commerce across regions (Matringe, 2020). The need for cash settlements in medieval and early modern trade, marked by the scarcity of precious metals and the logistical challenges of transporting large sums of money, undoubtedly played an important role. However, a critical examination of historical evidence suggests that the bill of exchange did not only emerge as a response to these practical constraints. It is essential to consider the broader economic, social and political contexts that influenced the evolution of financial instruments.

Credit lending by merchant bankers

As trade networks expanded, the demand for credit increased. Merchant bankers recognised the profit potential in extending credit to other merchants (De Roover, 1948). Bills of exchange became the method of credit banking, enabling merchants to defer payment for goods or services received. Double-entry bookkeeping played an important role by providing a systematic method to track credit transactions.

There were two types of commercial practices in which bills of exchange were used. The first was merchandise trading, where the bills of exchange were used to pay for the purchase of goods. The second was a credit transaction in which there was no purchase of goods (Munro, 2008). In the twelfth to fourteenth centuries, various merchant banking partnerships emerged in Northern Italy which engaged in both merchandise trade and credit transactions (Weber, 2003).

In a hypothetical example of a bill of exchange, a seller of goods in city ‘A’ might send goods to a purchaser in city ‘B’ and draw a bill of exchange on the purchaser. This meant that the seller instructed the purchaser to pay the amount owed to a payee in city ‘B’ within a certain period and in a specified currency. In order to receive the money from the sale as soon as possible, the seller of the goods in city ‘A’ could sell the bill of exchange to a merchant banker for cash in city ‘A’. In that way, the seller could obtain cash immediately, and did not have to wait for the payment from the purchaser of the goods in city ‘B’. The seller of the goods also guaranteed that the payee in city ‘B’ would receive the amount of money specified in the bill. Consequently, the seller was responsible to the payee in city ‘B’ for the face amount of the bill when it was presented in city ‘B’. At the inception of the transaction, the buyer of the bill of exchange in city ‘A’ would send the bill and several copies along with an accompanying letter (advice letter) to the payee in city ‘B’. The payee in city ‘B’ would then present the bill of exchange to the purchaser of the merchandise in city ‘B’ for him to accept. The purchaser of the merchandise would then accept the obligation to pay the bill by writing the word accettata, his signature and the date on the back of the bill. As acceptor, he had to pay the face amount of the bill in the local currency on the due date to the payee in city ‘B’ (Denzel, 2006).

In short, among the credit lending purposes of the bills of exchange were: (a) the merchant-seller could avoid a lack of liquidity; (b) the purchaser could buy goods on credit; (c) the participants in the transaction were paid in their local currencies; and (d) the payments were made without costly and dangerous transportation of coins and bullions (Denzel, 2006; Face, 1958).

In addition to the above-described reasons for the increased use of bills of exchange in credit lending transactions, Sangster (2024) quotes Schaube (1906) who argued that the general diffusion of double-entry bookkeeping among merchants in the thirteenth century facilitated credit lending. Schaube (1906) refers to the fragments of the Florentine account book of 1211, which show a double-entry bookkeeping system fully developed. Schaube (1906: 109) goes on to argue that credit lending was intended to address the scarcity and inadequacy of coins, and that credit lending was facilitated by double-entry bookkeeping.

The historical evidence surrounding the origins of the bill of exchange prompts a critical examination of the role played by credit lending by merchant bankers. The bill of exchange emerged as a response to the need for credit in long-distance trade, but credit transactions existed independently of the bill. Merchant bankers, who were often involved in international trade, extended credit to facilitate transactions, and the bill served as a negotiable instrument enabling the transfer of debt. This should not overshadow the role of the broader economic and financial context, including the rise of market economies, the growth of international trade networks and the evolving legal frameworks that influenced the development of financial instruments.

Negotiability through agency

The negotiability of bills of exchange was important to medieval commerce (Munro, 2003). Negotiability meant that bills of exchange could be transferred between parties, serving as a flexible means of payment and settlement. Double-entry bookkeeping facilitated this transferability by recording the transfer of ownership associated with bills of exchange. Through double-entry bookkeeping, merchants could track a bill from issuer to payee.

If a merchant decided to remain at his home location rather than to travel to an international trade fair, he could instruct an agent to look after his interests at the trade fair. As a result, the merchant could send a letter of advice as an order of payment. This letter of advice evolved into the bill of exchange. This development was facilitated by a network of merchant bankers who had agents in various trading cities and who knew each other personally (such as the branches of the Medici Bank). A network of agents and correspondents in the inter-related merchant banking networks made notarial certification unnecessary. Each branch had double-entry bookkeeping records showing the transfer of funds between branches: A network of international commercial correspondents extended to cover the entire economic and geographical area dominated by the Italian merchant bankers, and it was this that gave them the unrivalled possibilities for remitting or drawing from any place to any other. (Leone, 1983: 620)

The growth of banking families and merchant banking trading companies led to the establishment of permanent agents in the principal cities in which merchant banks were engaged in trade and lending (Blomquist, 1979). The effect of this development upon bills of exchange was important. The merchant banks were closely interrelated, and, once permanent branches were established, the merchant bankers could arrange money transfers with great facility. A letter issued by one branch of the merchant banking partnership was sufficient to create an obligation by the other branches of the firm. The unlimited liability of the merchant banking partnerships furnished security. As a result, bills of exchange began to play an important role in the international credit and lending system; the simplicity of this system was based on its informality. The freedom from legal forms allowed merchant bankers to develop their own methods of engaging in financial transactions. These types of transactions were recorded by double-entry bookkeeping entries, including: a book entry that recorded the sum of money received by the branch of the firm that issued the bill of exchange; a signed document given to the depositor/creditor acknowledging the obligation to pay to the depositor/creditor or his designated payee the specified amount and the place where the obligation would be discharged; and a letter called the avisa sent from the branch drawing the letter of credit to the branch which was instructed to pay the money (Usher, 1914: 572).

The development of an endorsement process was an important innovation that facilitated the negotiability of bills of exchange. The endorsement was written on the reverse side (in dosso or in dorso) of a bill of exchange. This endorsement allowed a person who was not part of the initial transaction to present the bill. Consequently, the bill of exchange became a negotiable instrument, like modern paper money. Bills of exchange were not only more negotiable; the bearer had greater financial security than the previous bearer, who remained jointly responsible for payment without being a surety in the legal sense (van der Wee, 1977: 329). Endorsements gradually gained greater economic importance in bourses such as Bruges and Antwerp, where merchant bankers traded bills of exchange in organised capital markets (Denzel, 2006).

The concept of negotiability through agency stands as an important aspect in understanding the historical origins, development and dissemination and of the bill of exchange. Yet, the historical evidence surrounding this concept requires scrutiny as the evolving nature of commerce, international trade networks and legal frameworks also played significant roles. Moreover, as said earlier, the historical record reflects diverse practices, with some regions relying more heavily on the agency-based negotiability of bills than others.

Avoiding charges of usury

In an era where religious pronouncements and laws condemned usury (Lane, 1964, 1966), the use of bills of exchange was a way to avoid charges of usury. Instead of expressly indicating an interest charge, merchants could benefit from the difference in currency exchange rates. Double-entry bookkeeping provided a framework to measure financial gains without exposing the merchant bank to a charge of usury (Adamo et al., 2018; Galassi, 1992; Le Goff, 1988).

There were two key elements that allowed bills of exchange to avoid usury. First, the permutatio pecuniae absentis cum praesenti (exchange of the lack of money with money), and second, the distantia or differentia loci (distance or difference of places). If one of these two features did not exist, the merchants could be charged with usury, which was a serious violation of law in many countries. It was only after various theologians made a distinction between ‘return on investment’ and ‘usury’ that the bill of exchange came to be a permitted (Denzel, 2006).

After the Tractatus de usuris written by the Franciscan priest Alexander Lombardus (ca. 1307), a type of bill of exchange called a cambium was not considered to be usury. Subsequent theologians accepted this argument, that if there was a difference in place and a difference of currency, there was no usury. However, in the fourteenth and fifteenth centuries, the Catholic Church continued to prevent the cambuim reale or cambium verum from being used in local exchanges, because there was no difference of places.

Thomas Aquinas (1225–1274) argued that there was a difference between a return on investment and usury. In other words, if an investment involved risk, it was acceptable to receive a return, whereas usury existed when a lender was certain to have his money returned without incurring any risks. This meant that interest on secured loans constituted usury, while interest on unsecured loans did not. By the mid-fifteenth century, many scholars in the Catholic Church accepted Aquinas's definition of usury, which allowed an expansion of the use of bills exchange (De Roover, 1967).

The problems associated with accusations of usury remained significant into the early fifteenth century. Francisco di Marco Datini (1335–1410), a wealthy merchant from Prato (a small city near Florence) offered bills of exchange to other merchants through a bank that he established in Florence in 1399. The Datini archives in Prato contain hundreds of examples of bills of exchange (Bensa, 1928; Goldthwaite, 2011; Marshall, 1999; Origo, 2020).

Most of Datini's commercial partnerships involved trading between various commercial cities in Europe. The types of bills Datini used were primarily related to international merchandise trade. However, some of Datini's partners engaged in bills of exchange which had features that could be considered to be usurious (Nigro, 2010). As a result, at the end of his life, Datini gave all of his fortune to establish a foundation for the poor of the city of Prato (Origo, 2020, 384).

The key point is that, since a merchant could be prosecuted and prevented from receiving Christian sacraments, the interest component of lending transactions was concealed. This was done through several techniques. The first was to increase the length of the usance 5 specified in the bill. This would add an interest component to the bill, as long as the actual amount of time necessary to travel between two cities was less than the agreed amount of the usance. Another method of concealment was for a merchant to resell goods to the merchant from whom the goods were originally purchased at a higher price than the initial sale. Finally, since the bill of exchange was written to specify an exchange rate between currencies in two different locations, the exchange rates could be manipulated to conceal the interest component (De Roover, 1955).

Discussion and conclusion

In the late medieval and early modern periods, Italian city-states often surpassed other European cities with respect to levels of literacy and knowledge of commercial law and accounting practices. This was based in part on the adoption of Roman law precedents and the creation of new Italian commercial laws regarding partnerships and monetary exchange (Schaube, 1906). The simultaneous appearance of double-entry bookkeeping in Venice and Tuscany also placed Italian cities well ahead of other European cities in terms of economic development (Mueller, 1997; Tognetti, 2015). It is therefore important to recognise the significance of the emergence of the bill of exchange and double-entry bookkeeping in facilitating subsequent economic development in Northern Italy and other commercial cities in Europe such as Bruges and Barcelona. Double-entry bookkeeping and the emergence of the bill of exchange can therefore be viewed as essential elements in the development of the modern economy (Moshenskyi, 2008: 81).

A primary reason for the emergence of bills of exchange revolved around a desire for lower transportation costs in long-distance trade (Munro, 2001). Cashless settlements had existed at international trade fairs, using lettres de foire, but the bill of exchange was an innovation because the issuer could order a third party to pay his debt in another currency, which allowed the bills to function both as a transfer of funds and an instrument of credit. Because bills of exchange initially had to be notarised in order to become valid, they were not freely negotiable. This problem of negotiability was partially solved through the development of networks of inter-related merchant banking partnerships like the Medici's. However, because charging interest on credit transactions was prohibited, the interest component had to be concealed in the exchange rate.

Bills of exchange also had an impact on other trading practices (Cavaciocchi, 2008). By the early fourteenth century, Florentine merchants residing in England were able to purchase raw English wool for export to Tuscany for manufacturing rather than using continental intermediaries (Lloyd, 1977: 60–140). As a result, Florentine merchant bankers came to dominate international finance and the transfer taxes to the Vatican in Rome. Several of the largest Italian merchant banking partnerships made loans to the English Crown secured by English papal taxes. Using bills of exchange, the Italian merchants could purchase English wool in England and instruct their partners in Italy to deliver the papal taxes to the Vatican using profits from other trading activities conducted in Italy and elsewhere. The extension of credit using bills of exchange facilitated international trade among merchants, who no longer travelled to trade fairs to meet in person.

This article has emphasised how double-entry bookkeeping facilitated the growth of bills of exchange in the medieval era through some interrelated aspects. First, double-entry bookkeeping introduced a systematic and accurate method of recording financial transactions, providing a picture of an entity's financial health allowing for merchants and bankers in the medieval period to track transactions accurately, and ensuring that all financial movements were captured comprehensively. Second, accurate financial records helped merchants and bankers make informed decisions about extending or receiving credit, investing in trade ventures and managing risks. Precise financial management was fundamental in the issuance and acceptance of bills of exchange, as it built the confidence needed for these instruments to be widely used and trusted.

Double-entry bookkeeping provided a framework that supported the evolution of banking and credit systems in several ways. First, accurate financial records maintained through double-entry bookkeeping helped establish the creditworthiness of merchants and banking institutions, a trust that was important for the issuance of bills of exchange, which were essentially credit instruments. Second, banks and merchants could engage in more complex financial transactions, backed by reliable accounting practices. Third, banks could intermediate between depositors and borrowers more efficiently, using double-entry bookkeeping to track deposits, loans and repayments accurately. This facilitated the growth of bills of exchange as a means of fostering credit across distances.

Medieval usury laws restricted the charging of interest on loans, posing a challenge for financial transactions. Double-entry bookkeeping played a role in circumventing these laws. Through meticulous record-keeping, interest could be disguised as fees or other charges within the accounts. Moreover, bills of exchange often involved the transfer of funds through trade transactions rather than direct loans. Double-entry bookkeeping allowed merchants to structure these transactions in a way that complied with legal restrictions, while providing credit. Finally, the accurate tracking of transactions allowed for the use of deferred payments, which could function similarly to interest without explicitly violating usury laws.

The limitations of this article are those of historical studies that rely on prior historical research. The attempts to overcome this limitation include focusing on the primary reasons for the increased use of bills of exchange in the late medieval and early modern periods. In addition, specific examples of bills of exchange and their uses are provided in specific circumstances. The value of this research lies in increasing our understanding of an important financial instrument that has been widely utilised since the early modern period to facilitate international trade. Future research might focus more on the issues of endorsement and negotiability, which were the key improvements that caused the bill of exchange to become a permanent feature of international trade and finance.