Abstract

This article analyses Côte d’Ivoire's evolving accounting architecture. Drawing on archival documents, oral histories, and interviews with regulatory and professional actors, it examines how successive interactions between local institutions and external forces shaped accounting standards. The lenses of accounting infrastructure and polycentricity are used to explore how local, regional, and international actors negotiated authority over standard-setting processes. The findings highlight both the endurance of externally shaped frameworks and the development of locally adapted alternatives responsive to economic, legal, and institutional realities. This layered structure – visible in Côte d’Ivoire's selective adoption, modification, and resistance – reflects a pragmatic calibration rather than outright compliance or rejection. The study advances African accounting historiography by offering a rare Francophone case study and demonstrating how standard setting is embedded within complex governance arenas. It invites future comparative research on how diverse African states respond to regional integration and global harmonisation pressures in constructing their accounting regimes.

Introduction

Historical accounts of accounting diffusion, particularly those by Western colonisers about their former colonies, are abundant. The spread of trade, capital, administrative practices, and broader institutional forms – such as accounting – was part of the colonial project (Poullaos and Sian, 2010; Poullaos and Uche, 2012; Sian, 2011). Although such diffusion is well documented, the historical and contextual nuances that determined how imported systems were adopted, adapted, or resisted remain underexplored. While colonial systems were met with adaptation or even enthusiastic acceptance in some regions, their implementation was partial, resisted, or entirely unsuccessful in others (Wallace, 1992).

With regard to accounting, these dynamics have played out differently across former British, French, Spanish, and Portuguese colonies. Factors such as the pre-existing administrative capacity, structure of local economies, and nature of colonial engagement considerably influenced whether accounting systems took root and how they evolved (Elad, 1992). While some colonies had sufficiently developed internal practices and professions to resist or hybridise imported models (Gray, 1998; Nobes, 1998), others, including many in West Africa, had no prior formal accounting infrastructure before their colonisation. Consequently, although imported systems formed their first accounting institutions, they were not always aligned with local needs or capacities.

In Côte d’Ivoire, formal accounting practice did not exist prior to French colonisation in 1893. Côte d’Ivoire became an independent republic on 7 August 1960, with the Democratic Party of Côte d’Ivoire dominating its political system for 30 years (Its first president from 1960 until his death in 1993 was Félix Houphouët-Boigny.). According to the UNESCO Institute for Statistics, gross higher education enrolment rates were 9 and 11 per cent for females and males, respectively, in 2020. The World Bank classifies Côte d’Ivoire as a lower-middle-income nation with a 38.4 per cent poverty rate in 2021 and 38 per cent human capital index in 2020 – lower than the Sub-Saharan Africa average (40%) and other lower-middle-income countries (48%). The World Bank's 2024 statistics indicate that Côte d’Ivoire has 32 million inhabitants with an annual gross domestic product (GDP) of $2709 per capita.

Côte d’Ivoire's professional, legal, and institutional accounting development was based on the French system. However, the process of introducing French accounting practices was far from linear or universally embraced. The country's economy at independence was dominated by agriculture, an informal sector, but it had few public institutions and banks. Most local enterprises lacked the complexity or size to apply the detailed, structured requirements of the French Plan Comptable Général (PCG) – Generally Accepted Accounting Principles. Consequently, the early decades of accounting standard setting were marked not by the displacement of indigenous systems, but by the challenges of aligning sophisticated imported standards with a relatively undeveloped domestic economic structure.

The concept of dependency in the literature explains how African accounting systems developed in close alignment with international agencies and former colonial powers (Jackson and Aycan, 2006; Uche, 2002, 2007; Zori, 2015). Although this framing details a structural alignment, it often downplays the role of local agency – specifically, how actors in postcolonial states negotiated, contested, or redirected imported architectures. This article aims to trace such historical processes in Côte d’Ivoire, focusing on the institutional, political, and professional dynamics that shaped the diffusion, adaptation, and partial indigenisation of accounting standards. We examine how Côte d’Ivoire engaged in layered standard-setting processes through the transfer of French PCG, regional accounting integration, and selective engagement with global standards such as International Financial Reporting Standards (IFRS) as developed by the International Accounting Standards Board (IASB). Using archival records and oral histories based on interviews, this article reconstructs how accounting infrastructure emerged in a space where no indigenous model existed, necessitating significant institutional, economic, and cultural translation to introduce external standards.

Theoretically, the article draws on the concept of accounting architecture (Iyoha and Oyerinde, 2010; Lee, 1987) and accounting polycentricity (Seny Kan et al., 2021), thereby capturing the overlapping arenas of regulation – international, regional, and national – through which accounting systems were constructed and contested. This approach responds to calls for a greater interdisciplinary engagement in accounting history (Gomes et al., 2011). By tracing the Ivorian case, a counterpoint is offered to narratives that assume either straightforward adoption or radical resistance. Instead, it reveals a layered, iterative process shaped by economic structure, professional formation, regional coordination, and global pressures. The article distinguishes two key phases in the development of Côte d’Ivoire's accounting architecture: first, the period up to 1990s, during which French PCG served as the dominant reference model and, second, the period from 2000 onwards, characterised by a dual standard-setting structure involving both Système Comptable Ouest-Africain (SYSCOA) and tion pour l'Harmonisation en Afrique du Droit des Affaires (OHADA) (SYSCOA-OHADA) 1 and increased engagement with the IASB and its IFRS, largely driven by international tions like the World Bank and the International Monetary Fund (IMF) (Botzem, 2008; Camfferman and Zeff, 2007). To examine these historically rooted yet multi-layered dynamics, we explore how the evolution of accounting systems in Côte d'Ivoire reflects complex interactions between institutional realities at local, regional, and global levels.

This study highlights how international accounting standards were not merely received or rejected but reconfigured through negotiations involving professional associations, public institutions, and regional frameworks. Rather than viewing Côte d’Ivoire's accounting evolution through the lens of resistance or emancipation, we uncover the process of strategic institutional calibration. In line with Degos et al. (2019), our article contributes to African accounting history by introducing a Francophone case that has been underrepresented in a field dominated by Anglophone studies, responding to recent calls for comparative, context-rich, and historically grounded analyses of standard setting on the continent (Carnegie, 2014; Verhoef, 2013, 2014). This article has two objectives: first, to strengthen African accounting history literature by bringing insights from historical accounts of accounting development in Francophone Africa to a wider audience within an English-language journal. Second, we seek to develop an understanding of the distinctiveness of African actors’ agency in navigating external influences while shaping accounting systems in French-speaking African countries.

The remainder of the article is structured as follows: The next section presents the institutional context of Côte d’Ivoire. The following section provides a literature review and introduces the theoretical framework. After that, the fourth section discusses the sources and research methods. The findings through a historical reconstruction of key episodes of accounting development are presented and then discussed. The last section concludes with implications for accounting scholarship in postcolonial and development contexts.

Study setting

We seek to provide a comprehensive understanding of Côte d’Ivoire by tracing historical patterns of not only economic variables of accounting development but also social factors such as the development of the accountancy profession, which significantly impacts accounting standard setting and the implementation of accounting standards in the local context.

Brief socio-economic history of Côte d’Ivoire

Côte d’Ivoire emerged from French colonialism, gaining independence in 1960 following its declaration of an autonomous community status in December 1958 (Klaas, 2008). From the 1960s onwards, it became an economical and political rising star in Francophone West Africa, among countries such as Benin, Burkina Faso, Niger, Senegal, etc. Under the leadership of Félix Houphouët-Boigny – who advocated collective development, believing that shared regional goals were essential for progress – Côte d’Ivoire played a central role in fostering regional integration among former French colonies. Before independence, this vision had materialised in the creation of the Council of the Entente, a regional economic and political cooperation body aimed at promoting African solidarity and discouraging foreign interference in internal affairs. This spirit of regionalism deeply influenced the structure of the Ivorian accounting system.

Between 1960 and 1999, Côte d’Ivoire experienced remarkable political stability. From 1960 to 1978, it was one of the world's fastest growing economies (Glewwe and de Tray, 1988). According to the World Bank (2014), two main factors powered this growth: agricultural exports and government spending. Cocoa, coffee, and cotton constituted the core of Ivorian agriculture, with cocoa playing a dominant role, as Côte d’Ivoire soon overtook Ghana to become the world's largest cocoa producer, accounting for nearly 40 per cent of the global supply. However, a sharp decline in cocoa prices in the late 1970s exposed the vulnerability of its mono-crop dependence. Within 2 years, the economy contracted, public debt rose rapidly, and resource mismanagement intensified. Although its domestic stock market, the Bourse des Valeurs d’Abidjan (BVA), established in 1976, was originally intended to allow Ivorians to invest in national firms, it eventually played a pivotal role in the broader regional economic landscape.

By 1980, Côte d’Ivoire's challenges, coupled with large public investment programs, had driven the budget deficit to 11.9 per cent of the GDP, nearly exhausting the country's foreign reserves (Klaas, 2008). Faced with mounting fiscal pressures, the government turned to the IMF and the World Bank for assistance. Houphouët-Boigny's administration negotiated a bailout agreement that led to the introduction of the Structural Adjustment Programme (SAP) in 1981. This called for sweeping reforms, including deep cuts in public expenditure, major reductions in social services, and privatisation of state-owned enterprises (SOEs), particularly in the cocoa sector. The government identified 66 large SOEs for privatisation by 1991 (Lavelle, 1999). In practice, the privatisation process extended ownership to foreign capital, primarily from French investors, through the BVA.

In response, cocoa production initially rose, with export revenues increasing from $3 billion in 1980 to $5 billion by 1995. However, public debt simultaneously ballooned from $7.4 to $17.7 billion. By 1994, Côte d’Ivoire's external debt stood at 231 per cent of its gross national product (Glewwe and de Tray, 1988). In 1994, the government entered a second agreement with the IMF and the World Bank under the enhanced SAP. Over the following 3 years, Côte d’Ivoire borrowed $384 million to implement further reforms. Despite this, economic recovery remained elusive. The International Labour Rights Fund argued that the government's SAP had attempted to reform the cocoa sector without adequately addressing its centrality to the economy, thereby undermining the foundations of economic stability and contributing to increased poverty and social dislocation.

In 1998, the BVA became the Bourse Régionale des Valeurs Mobilières (BRVM), the first regional stock exchange in Francophone West Africa. Headquartered in Abidjan, it now serves multiple countries in the West African Economic and Monetary Union (WAEMU), with Côte d’Ivoire having the largest number of listed firms. This transformation reflects not only economic liberalisation but also a shift toward regional financial integration, aligning closely with the collaborative vision established decades earlier under Houphouët-Boigny.

Côte d’Ivoire's economic and political history is essential to understanding the evolution of its accounting architecture. The rise and fall of the cocoa-based economy, the influence of international financial institutions, and the development of a regional financial market shaped the design and implementation of accounting standards. The heavy involvement of external institutions and the drive for harmonisation across Francophone West Africa created a regulatory environment, causing national systems like Côte d’Ivoire's to simultaneously navigate global, regional, and domestic pressures.

French accounting system and its transfer into its colonies

To the best of our knowledge, no studies of accounting practices in Côte d’Ivoire prior to their colonisation by the French in the 1800s have been conducted. Nonetheless, the existence of any form of accounting prior to colonisation can be assumed to have been rudimentary, largely incapable of developing further during the colonial era. France continued to introduce its accounting systems to many of its colonies long after colonial rule ceased in the 1960s (Degos and Ouvrard, 2008; Lavelle, 2001). Notably, the French themselves relied heavily on the Germans to construct their chart of accounts in the manner suggested by Schmalenbach (Nobes and Parker, 2020).

After the Second World War, French accounting charts of accounts (i.e. standards’ structure) underwent significant changes across four phases. According to Colasse and Standish (2012), the first phase of modern French accounting came into effect between 1946 and 1957, coinciding with the post-war period when the French state began reconstructing its economy by introducing the PCG in 1947, mainly constituting macroeconomic aims with little or no input from the accountancy profession (Nobes and Parker, 2020). Between 1958 and 1973, France experienced significant economic growth while simultaneously strengthening the link between taxation and the overall economy. The PCG's application supported the development of the legal and taxation systems rather than that of the economy as a whole (Richard, 2013). However, the third phase of modern accounting development drew accounting, law, and taxation much closer. Between 1974 and 1983, economic instability and accounting standardisation increased following the integration of the European company law directive into the French accounting system. In the last phase of modernisation from 1984 onwards, professional accountants assumed a more prominent, central position in the delivery of accounting services than before (Evraert and des Robert, 2007).

Although these transformations continued in France, few accounting practices were apparent in former French colonies until the 1970s, when France began to impose its charts of accounts on its overseas territories (Evraert and des Robert, 2007). However, the effect was minimal and restricted to state institutions, as a large majority of French colonies remained agrarian, dominated by the production of natural resources with a sizeable proportion of the population being uneducated. Introducing formal accounting systems to French overseas territories became successful only following the integration of legal systems and the creation of business law in the economic communities of French West Africa. When Côte d’Ivoire gained independence from France in 1960, its basic system of accounting remained unchanged for the following 10 years until the tion commune African, Malgache et Mauricienne (OCAM) 2 was introduced in the 16 member countries of French West Africa.

A historical review of Côte d’Ivoire's accounting system is irrelevant without reference to other French overseas territories, particularly in West and Central Africa. These countries are regionally integrated in several ways, resulting in the diffusion of formal institutions from France to its colonies (Causse, 1999). Indeed, formal institutions such as the legal system, education, medicine, economics, central banking, and finance often adopted a regional tional perspective. Accounting, like these other systems, was organised on a regional basis. In the next section, we present an overview of relevant literature on accounting development in Africa, drafting the theoretical framework underpinning our historical account of Côte d’Ivoire's accounting architecture, inextricably linked to colonial ‘Western Francophone Africa’ – a regional grouping.

Literature review and theoretical framework

We begin by reviewing literature relevant to Africa's accounting development, delineating three strands of research, similar to the literature on the development of accounting systems in developing countries. The three strands are (i) accounting in former colonies, (ii) postcolonial and neo-colonial perspectives, and (iii) diffusion of global accounting standards in non-Western contexts. These strands are then woven through the concepts of accounting architecture and polycentricity to derive our theoretical research framework.

Accounting development in Africa: An overview of relevant literature

The literature on the development of accounting suggests that extant African accounting systems are intrinsically linked to the colonial history of African countries – as in other developing countries (Briston, 1978; Tawiah et al., 2022). Globalisation also impacts these systems (Hopper et al., 2017), with literature revealing that African countries with similar colonial influences use similar accounting systems and standards. Based on Nobes's (1983) pioneering classification of accounting systems, a series of studies demonstrates that African accounting systems fall either into Anglo-American judgemental or Franco-German uniform accounting systems (Elad, 2015; Elad et al., 2023). Tawiah et al. (2022: 6) reveal that during the colonial era (circa 1881 until 1981), an African country's accounting system was mainly determined by three key driving forces: (i) political governance, (ii) economic policies and (iii) social policies. The colonial political governance entailed a direct rule (based on coercion) or an indirect rule (based on co-optation). Trade (i.e. open or closed) and tax (i.e. punitive or incentive) policies were two core components of colonial economic policy. Social policies involved the education system, language, and religion. In the postcolonial era, foreign aid, foreign trade liberalisation, membership in international associations, and prevalence of foreign ownership were four key driving forces of accounting systems in Africa (Tawiah et al., 2022).

Another common feature of African accounting systems is their construction, revealing tensions stemming from former colonisers’ willingness to maintain their influence, the diffusion of international accounting standards associated with the globalisation of African economies, and African countries’ desire for autonomous accounting systems that reflect their independence and best suit their needs. Studies focused on African accounting professions (Ghattas et al., 2021; Musundwa and Hammond, 2024; Uche, 2010; Verhoef, 2011, 2013, 2025; Wallace, 1992) and the diffusion of international accounting standards in Africa (Botzem et al., 2017; Owolabi and Iyoha, 2012; Tawiah, 2019; Tawiah and Boolaky, 2020) have enhanced our understanding of the development of accounting systems in Africa, just as in other developing countries (Yapa, 2022). However, overall, just like general African accounting literature (Ndemewah and Hiebl, 2021; Waweru et al., 2023), the literature on the development of accounting systems in Africa is essentially driven by studies from English-speaking African countries (Degos et al., 2019; Randriamiarana, 2015). Considering that French-speaking countries constitute 57.41 per cent of the African continent, totalling 31 out of 54 nations (Degos et al., 2019), it follows that the understanding of accounting systems in Africa is likely incomplete, as it is largely derived from research conducted in a limited number of predominantly English-speaking African countries.

Indeed, some variations do exist in African accounting systems (Tawiah et al., 2022). For instance, while British colonisers used co-optation as political governance, French colonisers preferred coercion to construct accounting systems in their colonies. For economic policy, British colonisers tended to allow an open trading policy with their former colonies, gearing them towards principles-based accounting. On the contrary, non-British colonisers like France used a closed trade policy, resulting in rule-based accounting systems in former colonies. Although both the Anglo-American and Franco-German accounting schools of thought centred on tax-driven accounting, British colonisers placed emphasis on tax incentives, whereas French colonisers implemented punitive tax strategies. Other studies reveal that the diffusion of international accounting standards, like IFRS, and the increase in the number of international accounting tions utilising IFRS, occur more rapidly in English-speaking than in French-speaking African countries (Boolaky, 2004; Degos et al., 2019; Randriamiarana, 2015).

The few rare studies on the construction of accounting systems in Francophone Africa provide some answers to our questions (Causse, 1999; Degos et al., 2019; El Omari and Khlif, 2014; Lassou and Hopper, 2016, Ngantchou, 2011). Causse (1999: 213) points out that, in the colonial period, the French accounting model was ‘a good instrument of civilising influence and control of the economy’ in the colonies, while it remains ‘a tool of economic conquest of remarkable power’ and ‘a weapon in global economic competition’ in the postcolonial period. Noting the influence of international accounting standards in Francophone Africa, she emphasises the need to maintain ‘French specificities’ in accounting systems in French-speaking African countries (Causse, 1999: 220). This implies the coexistence of at least three power relations in the construction of accounting systems in Francophone Africa: former coloniser–former colony, former colony–international accounting standard-setters, and former coloniser–international accounting standard-setters. For French-speaking African countries, the logic of constructing regional accounting systems constituted a means of navigating these power relations (Causse, 1999; Degos et al., 2019; Ngantchou, 2011). This represents a specific framing of the development of accounting systems in Francophone Africa, alongside the dearth of associated accounting research, which prompted Degos et al. (2019) to advocate for the need to enhance the understanding of the construction dynamics of accounting systems in French-speaking African countries. This article addresses that call, focusing on the role of local African agency in the development of accounting systems in Francophone Africa.

Theoretical framework

This article aims to understand how accounting practices and regulatory systems develop within the context of colonial and postcolonial Africa, particularly in Francophone West Africa, focusing on Côte d’Ivoire. To achieve this, we draw on two interconnected theoretical concepts: accounting infrastructure and accounting polycentricity.

Accounting infrastructure refers broadly to the fundamental elements required for effective accounting systems and practices. It includes professional accountancy bodies, accounting standard-setting institutions, legal frameworks supporting accounting practices, and regulatory oversight mechanisms (Iyoha and Oyerinde, 2010; Lee, 1987). Strong accounting infrastructure supports reliable financial reporting, transparency, and economic development, as evidenced in diverse contexts such as Taiwan and Nigeria (Iyoha and Oyerinde, 2010; Lee, 1987). Robust infrastructure is essential for implementing and effectively adopting global accounting standards (Botzem et al., 2017).

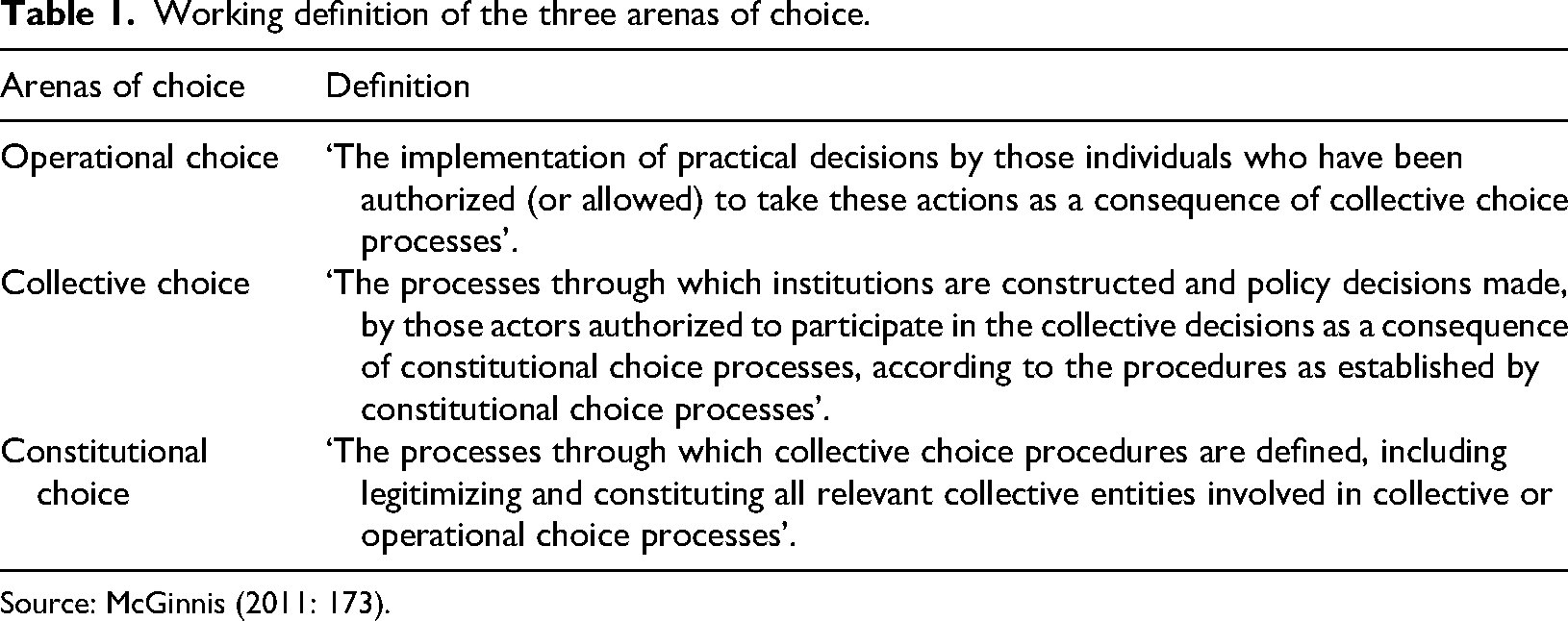

However, in the African context, accounting infrastructure is often influenced or controlled by former colonial powers, reflecting the continent's historical dependency and ongoing global integration (Causse, 1999; Degos et al., 2019; Elad, 2015; El Omari and Khlif, 2014; Lassou et al., 2019, 2021). This legacy creates complexities where international actors, such as the World Bank, IMF, and foreign governments, intersect, and even conflict with local regulatory practices (Neu et al., 2010). To better capture these complex interactions, we employ the concept of accounting polycentricity (Seny Kan et al., 2021), which describes how multiple, independent centres of decision making and authority coexist within a governance system. Within accounting regulation, this involves actors operating at various hierarchical levels – local (operational), regional (collective), and international (constitutional) – each shaping accounting practices through distinct, yet overlapping, influences, and interactions. Our polycentric perspective leverages the Institutional Analysis and Development framework drafted by Ostrom (2010) and McGinnis (2011), which analyses how institutions operate and evolve across three interconnected arenas of choice (Table 1).

Working definition of the three arenas of choice.

Source: McGinnis (2011: 173).

We utilise this framework because it explicitly acknowledges that institutional changes and accounting practices result from dynamic interactions across multiple governance levels, rather than from top-down imposition alone. It enables us to examine precisely how global institutions (e.g. World Bank, IMF), regional bodies (e.g. OHADA), and local actors (e.g. Ivorian accounting professionals) interact within the complex colonial and postcolonial regulatory environment. Although alternative frameworks, such as postcolonial theory, emphasise the cultural resistance and legacy effects of colonialism, our chosen framework of polycentricity provides an analytical advantage. Specifically, it facilitates a detailed exploration of current interactions and regulatory dynamics that combine external global pressures with local institutional responses, thus offering deeper insights into contemporary accounting development and regulatory change in Côte d’Ivoire and similar settings.

To reinforce the applicability of our chosen theoretical lens, our empirical findings (presented in the following sections) explicitly illustrate how different regulatory actors at each institutional-level respond to external pressures and opportunities. Interviews and archival evidence reveal how local actors exercise agency within constraints imposed by global and regional institutions, clearly demonstrating the strength of polycentricity as an analytic tool to understand historical accounting developments within colonial territories.

Method

Our empirical investigation traces the origins of regional accounting standard-setting initiatives and determines their subsequent influences on Côte d’Ivoire's accounting landscape. Accordingly, our research method revolves around explaining history through micro-histories (Ferri et al., 2018) of Côte d’Ivoire's accounting architecture within the broader context of West African regulatory development, presenting a historical account of how Côte d’Ivoire navigated tensions between externally introduced accounting systems and domestic institutional conditions shaped by colonial institutions, professional actors, and regulatory structures. The study traces the historical timeline of accounting standards in Francophone West Africa, focusing on Côte d’Ivoire, covering a 72-year period (1947–2019) and examining how accounting architecture was formed amid postcolonial regional integrations and institutional legacies.

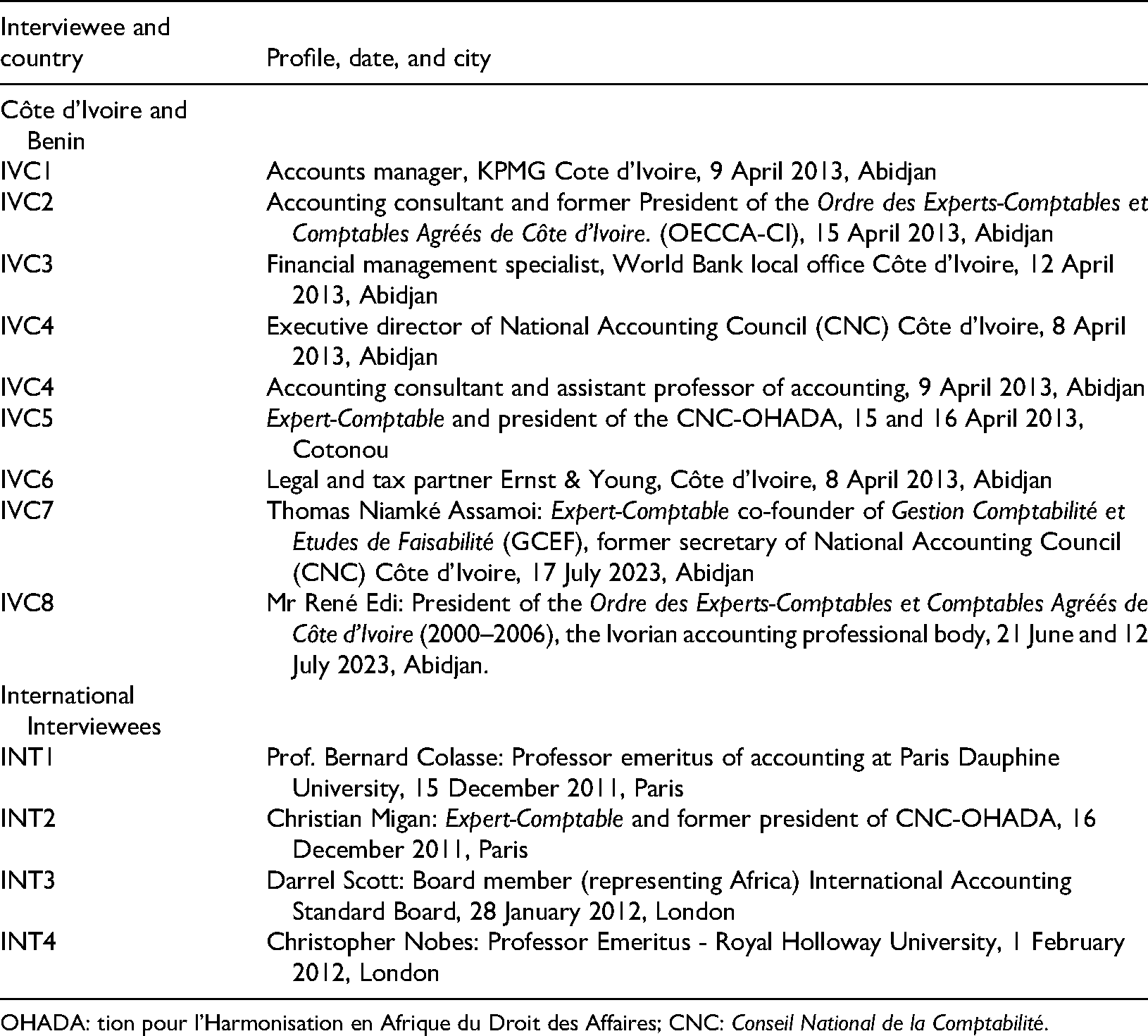

Data were collected in two rounds. The first round began in January 2011 as part of doctoral research, involving 41 semi-structured interviews and an extensive documentary collection from standard-setters, central bank officials, and accounting professionals. Interviews were conducted in accordance with oral history methodology (Hammond and Sikka, 1996; Stevenson et al., 2018), enabling participants to reflect on and recount critical institutional developments. Of the 41 interviews, 13 were analysed in detail based on the respondents’ direct involvement in key accounting standard-setting initiatives in Côte d’Ivoire and the Francophone region. Qualitative aspects of oral histories rely on ‘individual experiences, interpretations, reactions and aspirations’ (Hammond and Sikka, 1996: 79), providing a human agency-centric understanding of accounting development in Côte d’Ivoire.

In addition to Ivorian stakeholders, interviews were conducted with regulators, members of professional bodies, representatives from the World Bank, and scholars engaged in standard setting in France and across Africa. Notably, Professor Bernard Colasse (Paris Dauphine University), who contributed significantly to Francophone accounting education, provided valuable insights into the pedagogical and regulatory evolution of the French model in Africa.

The second round of data collection, conducted in 2023, focused on a key Ivorian professional – Mr René EDI, 3 one of the first Experts-Comptables diplômés d’Etat Français (French State-qualified Chartered Accountants) in Côte d’Ivoire (OEC-CI, 2023). His personal archive provided historical documents on the development of accounting regulation in Côte d’Ivoire, offering unique primary data. Profiles of interviewees and sources are listed in Appendix 1 and Archive sources (Appendix 2), respectively. Although interviews were also conducted with IASB representatives, their contributions were used primarily for contextual framing and were not central to the country-specific historical analysis presented here.

To enrich and verify oral histories, we triangulated interview data with archival material, including official policy documents, meeting minutes, and internal memos, particularly those related to SYSCOA and OHADA standard setting. Relevant literature on Francophone West African accounting history (Degos et al., 2019; Elad, 2007) was also incorporated.

The first author's embedded position within the West African accounting research network provided privileged access to respondents and data. Although this insider perspective informed analytical depth, findings were balanced through cross-validation, documentary triangulation, and collaborative interpretation among the co-authors. This combined approach of archival, oral, and documentary evidence aligns with established standards in accounting history research (Stevenson et al., 2018). For methodological rigour, we obtained permission from all key interviewees to incorporate their statements and oral accounts into our narrative.

Colonial legacies in accounting regulation: Initial developments, 1947–1982

Brown's (2004) account draws attention to France's attempts to introduce accounting practices in its former colonies. Before the second wave of accounting modernisation in 1957, the first version of the 1947 PCG had already been exported to overseas territories (Nobes, 2011). Although it aimed to institutionalise French accounting models abroad, it yielded limited success owing to several structural and contextual challenges.

First, significant heterogeneity existed in the capacity of local elites to comprehend and implement the new system, which a senior Ivorian accountant (IVC8) described as a ‘climat d’anarchie’ (‘climate of anarchy’) in his final year dissertation for accounting studies. Second, economic disparities across member countries resulted in varying utilities of accounting systems. While Cameroon had a relatively well-developed economic and administrative apparatus, other states such as Mali, Niger, and Chad were still attempting to organise basic formal business practices (Elad, 1992, 2015). Consequently, the diffusion of the 1947 PCG remained largely symbolic and uneven across Francophone West Africa.

In response, the 17 member states of the Union Douanière et Économique de l’Afrique Centrale (UDEAC) initiated discussions in 1967 to develop a regionally relevant accounting system, leading to a landmark meeting in January 1968 in Niamey (Niger), where the idea of an integrated accounting framework tailored to the region's diverse institutional contexts gained momentum. A working body was established to develop the accounting plan, culminating in the 1969 draft of the OCAM accounting plan, led by the distinguished French consultant and academic, Professor Claude Pérochon (Corre et al., 1971; Edi and Corre, 1998). His involvement was pivotal in shaping the plan's technical content and legitimising it among local elites and international observers.

The draft plan received robust support from national statistical agencies, private sector actors, and regulators. In October 1969, a technical meeting in Yaoundé, Cameroon, assessed the implications of the OCAM plan for national income accounting (Corre et al., 1971; Edi and Corre, 1998; Elad, 1992), followed by a formal summit of OCAM heads of state in January 1970, where the plan was officially adopted (Edi, 1980). Despite this significant milestone in regional accounting harmonisation, the path to implementation remained contested. Côte d’Ivoire did not ratify the OCAM plan in its original form. According to Mr Edi, Ivorian authorities – under Pérochon's technical leadership – instead adapted the OCAM model to national legal and administrative requirements, leading to the promulgation of the Plan Comptable Ivoirien (PCI) on 29 January 1973, asserting Côte d’Ivoire's institutional autonomy while maintaining technical continuity with the OCAM framework (Degos, 2013; Edi, 1980, 1986).

The OCAM plan was a modified version of the French PCG 1957 and is often referred to as an overseas adaptation (Causse, 1999; Elad, 1992). Despite its ambition, its implementation greatly varied. Much like the diffusion of the 1947 PCG, national responses to the OCAM plan reflected differences in institutional capability, legal orientation, and economic complexity. In Côte d’Ivoire, the alignment of accounting practices with legal frameworks meant that the chart of accounts was interpreted primarily as a compliance instrument, not as a managerial or statistical tool. This early phase (1947–1982) of accounting development in Côte d’Ivoire reveals four key insights:

Colonial asymmetries: The initial dissemination of accounting practices occurred under conditions of colonial rule, where technical expertise and financial decision making were monopolised by metropolitan powers, perpetuating asymmetries in institutional capacity and autonomy (Hopper et al., 2009). Contextual mismatch and adaptation: The sustainability of imported standards depended on not only technical know-how but also contextual ‘know-why’. The limited success of the 1947 PCG and the partial uptake of OCAM highlight the importance of local adaptation. During the interview, Mr Edi indicated that the OCAM initiative was viewed as a response to the impracticality of applying PCG without contextual tailoring. Professional formation: Accounting education in the region remained highly centralised. Early professionals, including Mr Edi and Mr Thomas Niamké Assamoi, were trained in France. The creation of the French Institut National des Techniques Économiques et Comptables in Abidjan in 1977, also under the guidance of Professor Pérochon, extended this model locally while preserving its Francophone epistemological orientation (Degos, 2013), generating a cohort of professionals adept at navigating both regional and imported accounting standards. Emergence of polycentricity in accounting: The PCI's development illustrates the emergence of a polycentric accounting system. Although OCAM embodied a regional collective initiative, individual countries customised their engagement. Côte d’Ivoire's tailored approach reveals how a multi-level – local, regional, and international – approach to accounting coexisted in a layered, negotiated regulatory space.

Ultimately, the failure to achieve uniform OCAM implementation reflects the limits of top-down harmonisation in settings marked by institutional asymmetry. The PCI case demonstrates how local actors harness external expertise, regional dialogue, and domestic priorities to shape accounting regulation, laying the foundation for later developments in SYSCOA, OHADA, and the contested introduction of IFRS. Although the PCI represented a domestically tailored accounting system grounded in the Ivorian legal and economic context, regional harmonisation pressures re-emerged with the launch of SYSCOA under WAEMU in the late 1990s. This marked a shift from nationally adapted plans towards collective regional systems, setting the stage for OHADA's continent-wide influence on accounting reform. The transition from PCI to SYSCOA-OHADA reflects a significant move at the constitutional level of accounting development, from postcolonial experimentation to regional convergence, albeit under continued institutional frictions.

Consolidating standards: The shift toward harmonised accounting in Francophone West Africa (1982–1991)

OCAM's introduction marked an early attempt at regional accounting harmonisation across Francophone Africa. Designed to limit divergent adaptations of the French PCG, it sought to bring coherence to financial reporting across member states. However, it was only partially successful. In practice, many countries continued to use earlier versions of the French PCG, often bypassing OCAM's framework entirely.

This was partly because of legal and institutional constraints. Although states belonged to regional harmonisation bodies, domestic legal systems were often not equipped to adopt or enforce supranational accounting directives. In some jurisdictions, no formal accounting standards existed prior to OCAM, allowing local practitioners to adopt whichever system they deemed most appropriate – usually French-derived models. By 1982, dissatisfaction with the OCAM framework led several member states to abandon it in favour of adopting the newly revised 1982 French PCG (Moussa, 2010).

Concurrently, business law, taxation, and business governance remained fragmented across the region. This patchwork of legal frameworks and reporting practices generated administrative complexity and reduced the comparability of financial data. These concerns gradually escalated until April 1991, when the finance ministers of 16 member states convened in Ouagadougou (Burkina Faso) to explore a coordinated regional solution, culminating in the creation of the OHADA. Officially established through a treaty signed in Port Louis, Mauritius, in October 1993, OHADA became a landmark regional effort to harmonise business law and establish common institutions, including arbitration mechanisms and training centres (Bourque, 2002; Muna, 2001).

Accounting was soon integrated into the OHADA framework as a core component (Ngantchou, 2011). Interviews reveal that even before OHADA's formation, WAEMU policymakers had begun discussing the need for a new accounting system reflecting the economic realities of its member states while moving beyond the limitations of OCAM. As WAEMU pursued deeper financial integration – banking reform, capital markets development, and macroeconomic convergence – it sought a unified accounting framework to support these ambitions.

Therefore, WAEMU re-engaged Pérochon, who had played a formative role in disseminating French accounting practices in West and Central Africa (Colasse and Durand, 1994; Degos, 2013). His influence extended well beyond West Africa: in Morocco, he helped establish the national accounting standards in 1986; in French overseas territories, such as Réunion and Madagascar, he was similarly involved in designing accounting standards and curricula for professional education.

In Côte d’Ivoire, Pérochon's role was especially significant. After years of statistical analysis, the Ivorian government concluded that the OCAM plan was inadequate for national income accounting and broader economic planning. The Central Bank of WAEMU sought a more robust, technically sophisticated framework, calling upon Pérochon to not only advise on accounting standards but also shape the education and certification of a new generation of accounting professionals. His contributions during this period laid the groundwork for a broader transformation of accounting governance in Côte d’Ivoire and across Francophone Africa. By the early 1990s, momentum had built for comprehensive reform, and efforts to replace the OCAM accounting plan were underway (Degos, 2013).

This second step highlights the disjunction between formal commitments at the constitutional and collective levels (e.g. membership in regional harmonisation bodies) and the uneven implementation at the operational level. Côte d’Ivoire, which had already developed its own PCI in 1973, moved forward with national reforms while other countries reverted to updated versions of the French PCG, underscoring the limits of regional coordination, absent institutional alignment, and local capacity – a theme that would recur in later phases of accounting standard setting under SYSCOA and OHADA.

The coexistence of regional and international accounting models in West Africa (1991–2000)

The evolution of Côte d’Ivoire's accounting infrastructure can be understood through Ostrom's lens of polycentric governance (Ostrom, 2010). The interaction between local actors such as the Conseil National de la Comptabilité (National Board of Accountancy; hereafter CNC), regional bodies such as the Conseil Comptable Ouest Africain (West African Accounting Council; hereafter CCOA), and international institutions (e.g. World Bank, International Federation of Accountants [IFAC]) illustrates overlapping jurisdictions and negotiation arenas, each with its own decision-making logic (CNC-Côte d’Ivoire, 2009a, 2009b; Migan, 2012).

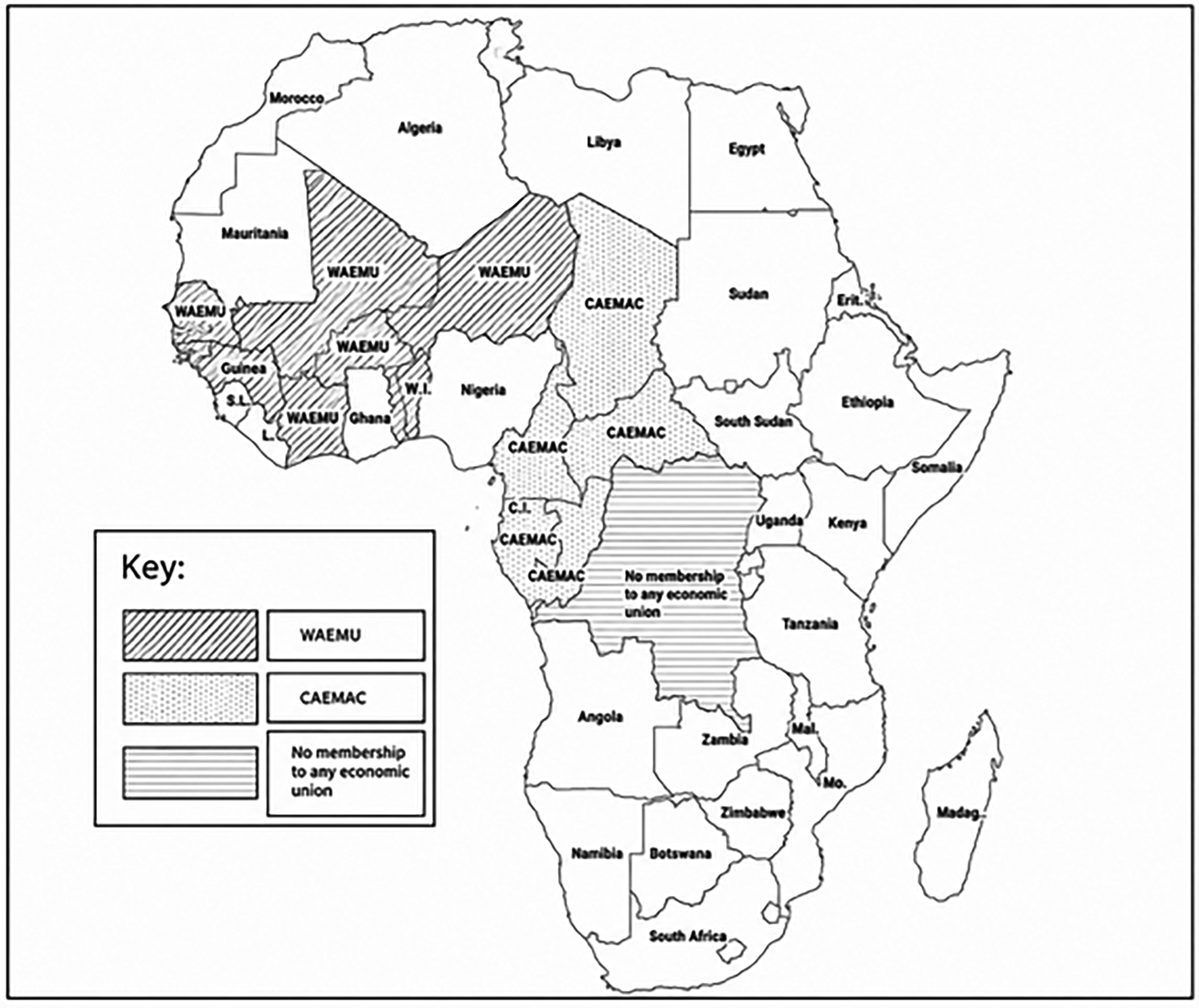

France's colonial legacy in West, Central, and North Africa was entrenched in public institutions, embedding French traditions in administration, education, law, banking, medicine, engineering and many other professions. Even after independence, many of these sectors retained their Napoleonic legal and bureaucratic structures, despite subsequent reforms in metropolitan France. This institutional continuity shaped postcolonial policy development, including the field of accounting. The 1960s witnessed a wave of regional integration efforts across former French colonies. Economic unions such as the Central African Economic and Monetary Union (CAEMAC) and the WAEMU were established not only to enhance cooperation, trade, and macroeconomic stability but also to serve as conduits for the diffusion of French administrative and legal models, reinforcing shared institutional features across national boundaries (see Figure 1). Figure 1 depicts the divide in economically integrated communities in French West Africa. Despite remaining separate on the level of macroeconomic and central banking, together, they form the OHADA.

Economic integration as a driver of diffusing accounting standards.

In Central Africa, CAEMAC developed a shared monetary and financial governance structure through the Bank of Central African States and adopted the Colonies Françaises d’Afrique Franc as a common currency. In parallel, WAEMU established the Central Bank of West African States (BCEAO), replacing national central banks with branch offices and creating the BRVM, a unified regional stock exchange to replace fragmented domestic capital markets. Differing regional trajectories led to inconsistencies in the implementation of the OCAM accounting plan. As economic unions developed independently, the once-unified OCAM framework began to fracture under divergent regulatory agendas and institutional needs. Therefore, both CAEMAC and WAEMU launched parallel accounting reform programmes.

In 1993, CAEMAC began revising its accounting standards as part of broader legal harmonisation initiatives. WAEMU followed closely, initiating the SYSCOA in 1995 under the leadership of BCEAO. SYSCOA aimed to modernise financial reporting and align accounting practices with evolving regional economic structures. Remarkably, both unions turned to Pérochon, whose prior involvement in OCAM and national reforms made him a trusted figure in Francophone Africa. His dual engagement across CAEMAC and WAEMU created a rare intersection of influence, despite also generating tensions over jurisdictional authority and intellectual ownership. Pérochon played a central role in drafting the technical content and designing the pedagogical approach of both accounting systems, further reinforcing the continuity of French accounting doctrines in the region (Degos, 2013).

This period reflected both institutional divergence and the increasing complexity of regulatory coordination in a polycentric accounting environment where regional entities became increasingly independent despite shared legal and historical foundations. By the mid-1990s, both CAEMAC and WAEMU had initiated accounting reform programmes aimed at aligning financial reporting with their evolving regional economic structures. Drawing on established technical expertise from earlier standardisation efforts, both blocs advanced their projects with institutional backing, including support from the French Ministry of Finance.

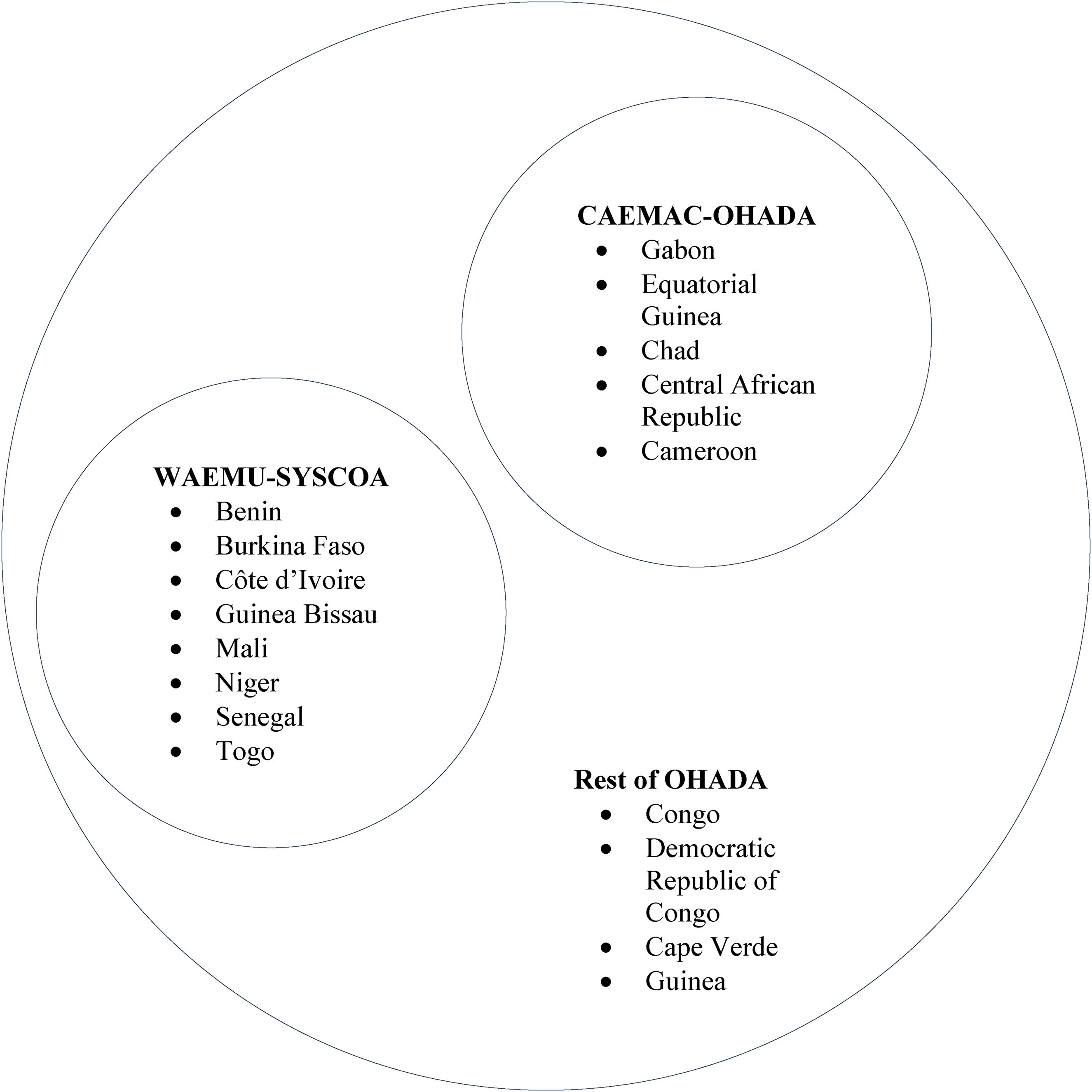

Although work on the OHADA accounting system began in 1996, it progressed slowly owing to the extensive legal harmonisation required across all member states. In contrast, the WAEMU-led SYSCOA project, launched in 1995 under the leadership of the BCEAO, followed a more streamlined administrative process. Thus, the SYSCOA framework was finalised by 1998, while the OHADA accounting plan was completed only in 2000 (Degos, 2013). This illustrates different institutional demands of economic versus legal harmonisation within regional standard setting. On 24 March 2000, discussions commenced between CAEMAC and WAEMU to converge their respective accounting standards. These consultations gained formal traction when a harmonisation committee was established, with the endorsement of all 17 OHADA member states. The outcome was the creation of the SYSCOA-OHADA accounting framework – a unified standard made mandatory across all OHADA jurisdictions, creating an inter-regional grouping as illustrated in Figure 2.

Inter-regional arrangements on accounting standards setting in SYSCOA-OHADA. SYSCOA: Système Comptable Ouest-Africain; OHADA: tion pour l'Harmonisation en Afrique du Droit des Affaires.

Structurally and conceptually, SYSCOA and OHADA shared substantial similarities: both systems were developed under the influence of a shared intellectual foundation rooted in French accounting doctrines. Their alignment reflects both a common legal heritage and the continuity of technical authorship guiding their formulation.

Contested convergence: Regional autonomy and the globalisation of accounting standards (2000–2019)

By early 2011, Côte d’Ivoire had firmly embraced the SYSCOA-OHADA standards and revealed no immediate intention to depart from this regional framework. This position was confirmed by multiple interviewees: Many accounting professionals expressed their view of maintaining the status quo. Why change something if it is not broken? (Interviewee IVC 1) Institutional change can be necessitated by chaos, anarchy, or total failure in the current system. When the status quo proves to be stable, it is difficult to institute change and to convince individuals of the need for such a change. Since SYSCOA-OHADA was introduced in the year 2000, accountants in the member states of OHADA have maintained consistency in implementing the standards. (Interviewee IVC 5) Unlike the case of the OCAM accounting plan that had varying degrees of application in member states, SYSCOA-OHADA has proved to unify accounting practices across the region. (Interviewee IVC 9)

In Côte d’Ivoire, the role of accounting standards in attracting foreign direct investment (FDI) has remained secondary, largely owing to the country's economic structure. Martor et al. (2004) reveal that FDI inflows typically occur through small-scale investments in the agricultural sector rather than via capital market participation. In the absence of a robust stock exchange or significant equity market activity on the BRVM, corporate governance and financial transparency mechanisms play a limited role in economic strategy, as underscored by an interviewee: Investors’ entry into the Ivorian economy has been through the informal sector, which currently accounts for more than 50 per cent of the country's GDP. (Interviewee IVC 5)

This structural reality has led stakeholders to question the relevance of IFRS in Côte d’Ivoire. With only 46 listed companies, its widespread application appears misaligned with the country's corporate profile. Despite its advantages in terms of global comparability and transparency, its usability remains contested. Most domestic firms are micro or small-to-medium enterprises, for which IFRS is deemed overly complex and costly to implement. In contrast, SYSCOA-OHADA was specifically tailored to the socio-economic and legal realities of the region, as an interviewee puts it: IFRS does not give us more information than we already have in SYSCOA-OHADA, and we are not motivated to adopt IFRS. More than 80 per cent of the companies are small and medium-sized entities and microenterprises. The question is who will pay for the adoption of IFRS by these smaller companies? The other problem is that IFRS is too complex. (Interviewee IVC 5)

Institutional arrangements in Côte d’Ivoire present distinct challenges that diminish the real value of adopting international accounting standards. One such challenge is the close link between financial reporting, taxation, and business law. This link between taxation and macroeconomics is inherited from the French accounting system. Tax law in Côte d’Ivoire requires companies to pay taxes based on the taxable profit accounted for using SYSCOA-OHADA accounting standards. Consequently, foreign companies that operate in the country are confronted with a dual reporting system of IFRS and SYSCOA-OHADA. A typical case of an IFRS reporter in the region is the French oil giant Total S.A. (now called TotalEnergies), which has maintained a dual reporting system to meet the obligation of tax payment based on SYSCOA-OHADA.

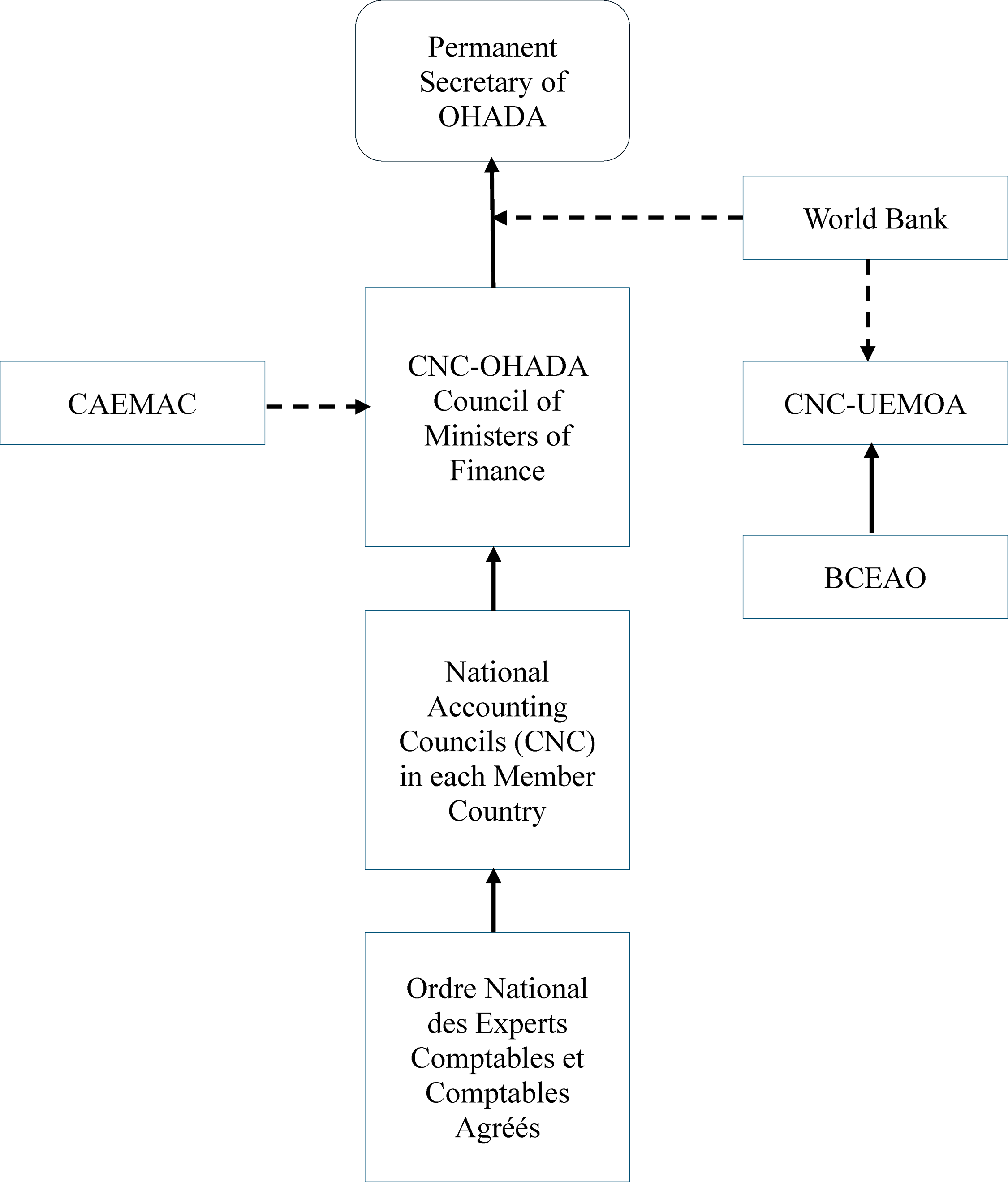

Côte d’Ivoire's accounting standards are organised around the accounting standardisation initiatives of the OHADA secretariat. Although each country's standardising body may monitor the application of accounting standards, they rely on regional accounting standard-setters to pronounce accounting standards. In December 2008, the Council of Ministers created a regional accounting standard-setting body to establish new accounting standards among member countries. Consequently, the Commission de Normalisation Comptable OHADA (Accounting Standardisation Commission CNC-OHADA) was established to collate the views of all the local accounting standard-setting bodies in member countries and propose new accounting standards to the Council of Ministers. Apart from the CNC-OHADA as a regional accounting standard-setter for the 17 member states, Côte d’Ivoire also belongs to a sub-regional accounting standard-setting body within the WAEMU, which is duty-bound to assist with the implementation of the SYSCOA accounting standards. In this process, the CCOA and the Conseil Permanent de la Profession Comptable (Permanent Council of the Accounting Profession) were established to complement accounting standard setting in the eight member states of the WAEMU.

These institutional arrangements for setting Cote d’Ivoire's accounting standards aided the adoption of international accounting standards, enabling diffusion from a central point to all OHADA's member states. However, they also blocked the adoption of IFRS by individual member states. Interviewees expressed this concern in Côte d’Ivoire in 2013: Côte d’Ivoire is not alone in this space of the WAEMU. We cannot adopt IFRS without consulting the others and the Permanent Secretary. The West African Accounting Council must decide. (Interviewee IVC 4) You must know that here in Côte d’Ivoire, the decision to adopt IFRS or not does not come from the country but from the WAEMU commission, which is in Ouagadougou. (Interviewee IVC 2) The West African Accounting Council is the highest accounting standardising body, which must agree on accounting principles before they are adopted by member countries. This structure slows down the decision-making process. (Interviewee IVC 3)

In 2003, the CNC-Côte d’Ivoire was established under the Ministry of Economy and Finance. It is responsible for national accounting standardisation issues and represents the country at the regional level of the West African Accounting Council (See Figure 3). This phase marked a significant development in solidifying Francophone African Accounting institutions, culminating in the SYSCOA-OHADA framework. The Diplôme d‘Expertise Comptable et Financière, WAEMU's accounting diploma created in 2000, further enhanced the region's accounting landscape (WAEMU, 2020). However, external pressures arose from financial incentives at institutional-level funding and technical-assistance mechanisms provided primarily by multilateral development institutions, most notably the World Bank through its International Development Association grants and related trust funds rather than through direct monetary incentives to firms and local government agencies. These mechanisms included project-based financing to strengthen OHADA institutions, national accounting councils, and professional bodies; support for the revision and implementation of SYSCOA-OHADA accounting standards; and capacity-building initiatives to improve financial reporting, auditing, and regulatory enforcement. The incentives were explicitly linked to investment climate reforms and the production of reliable financial information, as documented in World Bank country reports and OHADA-focused project appraisals and grant documents (World Bank, 2009b, 2010).

Accounting standard-setting structure in OHADA. OHADA: tion pour l'Harmonisation en Afrique du Droit des Affaires.

Although they promoted IFRS adoption – a replacement of the SYSCOA-OHADA framework –at their inception, these incentives were met with fierce resistance from stakeholders with strong views on why IFRS were not useful in the context of Ivorian accounting architecture. We show in the next section, the discourse on these contestations and resistance towards adopting IFRS in Cote d’Ivoire.

Negotiating global demands and local realities: Accounting developments in Côte d’Ivoire

International financial institutions, most notably the World Bank, IMF, and the United Nations Conference on Trade and Development (UNCTAD) made several attempts to encourage the Ivorian government to replace the SYSCOA-OHADA framework with IFRS (OEC-CI, 2023; World Bank, 2010), mirroring broader international campaigns to diffuse IASB standards across the African continent. While such initiatives were relatively successful in Anglophone Africa, particularly in jurisdictions with more liberalised capital markets, their impact in Francophone contexts like Côte d’Ivoire has remained limited.

Since independence, Côte d’Ivoire has maintained close ties with global financial institutions. It was among the earliest African partners of the World Bank, the IMF, and the UNCTAD, and is the headquarters of the African Development Bank. Since the 1960s, these institutions have shaped the country's economic trajectory. Côte d’Ivoire was the first country in West Africa to implement SAPs and has long ranked among the region's largest recipients of multilateral lending (Klaas, 2008; Lavelle, 1999, 2001). Despite their leverage in macroeconomic policy, these institutions have had limited success in reshaping accounting governance in Côte d’Ivoire. Repeated attempts to push for IFRS adoption have encountered resistance, particularly from national and regional accounting standard-setters. As noted by interviewees (IVC3 and IVC5), this resistance is rooted in regulatory concerns as well as deep-seated cultural and institutional logics governing the purpose of financial reporting in the region, notably a legalistic, state-centred orientation in which accounting is designed to support statutory compliance, taxation, and economic administration, rather than capital market communication. Within this framework, accounting standards are expected to align closely with business law and public oversight objectives, a logic embedded in SYSCOA-OHADA and reinforced through regional institutions, which explains the persistent scepticism toward the investor-oriented reporting model of IFRS.

Although the World Bank and IMF have traditionally promoted neoliberal economic strategies including private sector-led capital allocation and global integration (Graham and Annisette, 2012) Côte d’Ivoire has historically emphasised public sector leadership in economic development. From this standpoint, calls to modernise accounting systems based on global templates such as IFRS are often perceived by practitioners as misaligned with local institutional priorities and socio-economic realities (CNC-OHADA Decision, 2009; OHADA Accounting Law).

In 2009, the World Bank and IMF jointly produced a Report on the Observance of Standards and Codes (ROSC) in Côte d’Ivoire. Their findings echoed critiques made in other developing countries (Andrews, 2013), concluding that the SYSCOA-OHADA framework, which had not been substantively revised since its inception in 2000, was outdated. The report cited its limited evolution as a factor contributing to the low quality of financial reporting in the country (Klaas, 2008; Lavelle, 2001). In response, the institutions proposed accounting reforms not just in Côte d’Ivoire but across all OHADA member states. However, their implementation has remained slow and contested, reflecting the polycentric and historically embedded nature of accounting governance in the region.

By 2011, the World Bank mounted pressure on the country's OHADA secretariat reassuring accounting standard-setters of its willingness to finance accounting reforms in the region. High ranking officials noted: Six months ago (prior to the date of the interview held in December 2011), I was in Washington and they asked me how we were doing on IFRS adoption. Last week I was again in Washington, and they asked me about it. I tried to explain and then they told me we have to decide now if we want to adopt IFRS or not. … One of my students who now works for the Bank was asked to come and convince us to adopt IFRS; again I tried to explain our position. (Interviewees IVC5 and INT 2)

4

The objective of this subcomponent is to assist the OHADA Secretariat in adopting and implementing a new accounting uniform act that will comply with international standards and best practices. More specifically, the project will aim at (a) adopting the International Financial Reporting Standards issued by the International Accounting Standards Board for Public Interest Entities (listed companies, banks, insurance companies, and state-owned enterprises) and disseminating the new accounting standards, (b) reviewing and updating the OHADA Accounting System for small and medium enterprises, and (c) strengthening the human and technical capacity of CNC OHADA. Successful implementation of this subcomponent will achieve convergence with IFAC's SMO 7 (International Financial Reporting Standards). (World Bank, 2009: 23)

A subcomponent of the project on improving corporate reporting in the OHADA region included the improvement of accounting standards, with the more specific objective of: assisting the OHADA Secretariat in adopting and implementing a new Accounting Uniform Act that will comply with international standards and best practices. More specifically, the project will aim at (a) adopting the International Financial Reporting Standards issued by the International Accounting Standards Board for Public Interest Entities (listed companies, banks, insurance companies, and state-owned enterprises) and disseminating the new accounting standards, (b) reviewing and updating the OHADA Accounting System for small and medium enterprises, and (c) strengthening the human and technical capacity of CNC-OHADA. (World Bank, 2012: 17)

In view of this objective, the project allocated US$ 2.5 million to finance the adoption of IFRS and to the review the current SYSCOA-OHADA accounting standards. Although the World Bank successfully pushed for accounting reforms in Anglophone African countries, professionals and regulators in French West Africa have voiced concerns that these reform initiatives will only yield modest results. As one interviewee stated: The problem is the World Bank. You know the World Bank does not go on the ground before initiating projects. The World Bank does not know exactly what they need. They have money; as a result, they are asking us to adopt IFRS. When I discussed the issue of who would finance the cost of implementation with them, they said they do not know. However, adopt IFRS; afterwards, we see the next steps. (Interviewee IVC 5)

In 2012, the World Bank and the CCOA conducted preliminary IFRS training for professional accountants in the WAEMU region to familiarise them with the work of the IASB. Their aim was to get the accounting standard-setters to adopt IFRS, at least for listed companies on the BRVM (Interviewee IVC 3). At the time of first round of the field research in Cote d’Ivoire, although the CCOA had decided tentatively to adopt IFRS for the 38 companies listed on the stock market, this decision remained pending the approval of the Permanent Secretariat of the CNC-OHADA and the Council of Ministers who have to approve or disapprove decisions by the CCOA. As an interviewee stated: What is happening here is that there is a little misunderstanding between OHADA and WAEMU; regarding the discussion we have been having, we have not yet decided fully which accounting system we would like to apply; the man he just spoke to from Benin thinks OHADA is good. When we met in Ouagadougou, we decided to look into both IFRS and OHADA and see how best we can harmonise the two because obviously they would have some disadvantages. Those of us in WAEMU decided that our 38 companies would continue to use IFRS even though we were pushed by the World Bank to use this system, while those in OHADA said that, since their companies do not interact as much in the world capital market, there was no need for them to use IFRS. (Interviewee IVC 4)

In Côte d’Ivoire, Interviewee IVC 2 indicated that in the event of the CNC-OHADA and the Council of Ministers ratifying the decision to allow listed companies to adopt IFRS, these standards would only be voluntary and without legal basis. When compared with the overall proportion of financial reporting entities, listed companies on the BRVM account for only a small fraction of GDP, constituting less than 10 per cent of companies in Côte d’Ivoire. The majority of companies will continue to apply SYSCOA-OHADA.

The United Nations Conference on Trade's Intergovernmental Working Group of Experts on International Standards on Accounting and Reporting (UNCTAD-ISAR) is another major participant that has urged the Ivorian government to adopt IFRS. In July 2012, UNCTAD-ISAR conducted a pilot study in Cote d’Ivoire to identify gaps in its accounting standards and the inherent challenges of adopting international accounting standards. It found that IFRSs were not in demand and were neither authorised nor recognised for preparing financial statements. In response, the UNCTAD-ISAR recommended the adoption of IFRS to the CNC-Côte d’Ivoire, arguing that IFRS could boost economic growth (CNC- Côte d’Ivoire, 2009a).

Although international tions were exerting pressure on accounting standard-setters in Côte d’Ivoire to adopt international accounting standards, they failed to recognise the institutional settings that did not support the adoption of these standards at the time. Côte d’Ivoire much like other French West African countries has a unique accounting ecosystem (Gray, 1998; Radebaugh et al., 2006) and a strong regional institutional framework that supports the integration of accounting standards into macroeconomic structures. This setting combines law, economics, and taxation to develop unique, multifaceted accounting standards. In contrast, standalone Anglophone accounting standards had thrived little and were not connected with other sectors of the economy. Consequently, the accounting system of SYSCOA-OHADA, developed to meet tax purposes of member countries, has proven to be successful.

Côte d’Ivoire has openly voiced concerns that the recommendations of the World Bank and the accompanying financial assistance to adopt IFRS may not achieve the intended results. An account from an expert in the standard-setting field reflects repeated contentious encounters with the World Bank on the sign value of IFRS adoption: The World Bank asked us to sign on to IFRS adoption … then we said no. We told them exactly what we wanted. We knew we were happy with the OHADA system for everyday tax purposes; this system will serve us well and not IFRS. We told them that IFRS were not a cultural fit. For us to adopt them, we want to know how this can benefit us before implementing them. They said ‘go ahead, go for IFRS, it is better for you’. We said ‘no, you gave us money to develop the OHADA, legal system, the same system for 17 countries. Why do you want us to abandon OHADA and use IFRS’? I said to the World Bank representative, ‘it is not possible for one member country to adopt IFRS. It is not possible for me to decide this for all 17 member states to adopt IFRS’. (Interviewees IVC5 and INT 2)

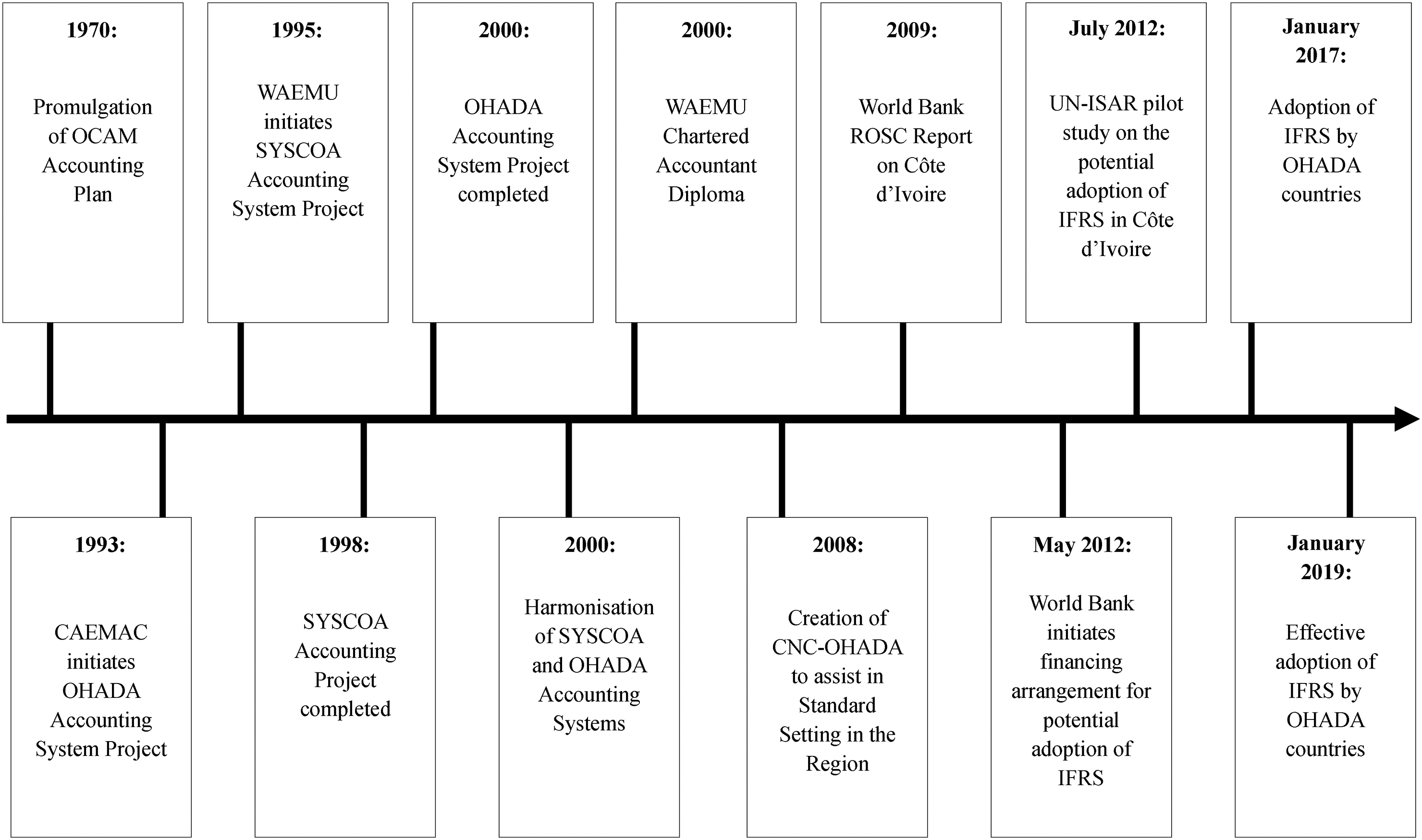

These views on the adoption of IFRS reveal tensions in accounting standard setting and reflect the myriad concerns pertaining to in the decision to adopt IFRS in Côte d’Ivoire. However, the conjecture that our interviewee made about the possible scenario if IFRS were introduced in OAHDA was verified. Indeed, ‘the uniform act relating to accounting law and financial reporting adopted in January 2017 by the member countries of OHADA, paved the way for the introduction of IAS/IFRS into the accounting system of its countries members’ with effective adoption on 1 January 2019, for all listed companies and companies ‘making a public call for capital’(Bationo and Barry, 2020: 69). Figure 4 exhibits a timeline of key dates in the development of Ivoirian accounting architecture.

Timeline of key dates in building the accounting architecture in Cote d'Ivoire.

The implementation of IFRS in OHADA faced resistance, resulting in an adoption process requiring listed companies and multinational subsidiaries to make selective adaptations within the limits set by national and regional local accounting regulations.

Discussion: A polycentric approach to the accounting infrastructure: The Ivorian case

Our findings illustrate the complex, recursive dynamics shaping accounting standard setting in Côte d’Ivoire from 1947 to 2019. To interpret these dynamics, we draw upon the twin theoretical lenses of accounting infrastructure and accounting polycentricity for a rich conceptual framework to understand both the structure and agency underlying standard-setting processes in postcolonial African states. This helps capture three essential features of historical account of these dynamics: accounting infrastructure and layered dependencies, actions arenas and regulatory contestations, and interdependence and independence.

Accounting infrastructure and layered dependencies

The concept of accounting infrastructure, developed by Iyoha and Oyerinde (2010) and Lee (1987), encompasses professional institutions, legal frameworks, regulatory mechanisms, and the broader architecture that sustains accounting practices. Côte d’Ivoire's initial infrastructure was deeply embedded in colonial systems. Rooted in the diffusion of the French PCG, it persisted well into the post-independence era, revealing a path dependency characteristic of systems with limited capacity for endogenous innovation.

However, accounting infrastructure in Côte d’Ivoire was never static. The shift from the OCAM plan to the Ivorian PCI and later to SYSCOA-OHADA demonstrates a progressive, albeit constrained, form of infrastructure adaptation. What emerges is an iterative process in which imported standards are selectively contextualised or modified based on domestic institutional capacity, political will, and macroeconomic priorities. The coexistence of IFRS and SYSCOA-OHADA in recent years further reflects this infrastructural layering, where global templates coexist with entrenched regional systems.

Our findings affirm that a strong accounting infrastructure is necessary but not sufficient for harmonised implementation. In the case of SYSCOA-OHADA, infrastructure supported formal compliance, but the question of fitness for purpose – particularly in microeconomic settings – remains unresolved. The limited equity market and high share of informal sector activity in Côte d’Ivoire present structural barriers to IFRS adoption. Thus, accounting infrastructure must be interpreted in terms of not only institutional robustness but also contextual relevance. This means that accounting technologies premised on investor-oriented disclosure, extensive fair value measurement, and advanced enforcement capacity – such as IFRS – offer limited functional advantages in settings where accounting primarily serves legal compliance, taxation, and enterprise formalisation, roles more directly accommodated by SYSCOA-OHADA.

Action arenas and regulatory contestations

To explore how decisions are made within this multi-level setting, we turn to the concept of polycentricity (Seny Kan et al., 2021; Ostrom, 2010), which describes governance systems where multiple centres of authority coexist and interact. The narrative on standard setting in Cote d’Ivoire precisely captures such a configuration, with decision-making arenas operating at international (e.g. World Bank, IMF, IASB), regional (e.g. OHADA, WAEMU, CNC-OHADA), and national (e.g. CNC-Côte d’Ivoire, local ministries) levels. Our findings reveal two prominent arenas of choice: collective-choice arenas – where professional bodies, ministries, and national regulators debate and influence standard-setting directions – and constitutional-choice arenas – where overarching treaties, legal mandates, and donor conditionalities dictate the rules of the game.

This polycentric structure creates both opportunities and frictions. For instance, while WAEMU and OHADA provide platforms for regional coordination, they also slow IFRS adoption because of the need for collective consensus. Interviewees noted how this arrangement limited unilateral decision making by Côte d’Ivoire and imposed procedural rigidity while also insulating local systems from global pressures, reinforcing regulatory stability. Importantly, the presence of overlapping governance centres does not always lead to fragmentation. In Côte d’Ivoire's case, regional coordination under SYSCOA-OHADA helped consolidate accounting practices, especially compared to the earlier OCAM experience. However, the system remained vulnerable to external pressures, as seen in the persistent lobbying by the World Bank to adopt IFRS. These interactions reflect what Ostrom (2010) described as ‘nested’ governance, where actors across multiple arenas engage in ongoing negotiation, adaptation, and contestation.

Interdependence, not independence

A key insight from applying the polycentric lens is that local accounting evolution in Côte d’Ivoire is neither fully autonomous nor imposed. Instead, it reflects interdependence, a condition characteristic of international commercial and regulatory engagement more broadly, but one that assumes specific forms depending on institutional context. In the Ivorian case, this interdependence is expressed through ways in which local actors respond strategically to external incentives, constraints, and opportunities, rather than through automatic convergence or harmonisation. Professor Pérochon's technical expertise, which was mobilised by both SYSCOA and OHADA illustrates how expertise circulates across institutional arenas to shape regulatory outcomes, while also consolidating particular epistemic traditions (in this case, French accounting doctrine). His role demonstrates how interdependence operates through concrete mechanisms of mediation and translation, linking national and regional initiatives without dissolving contextual specificity. Similarly, interactions between WAEMU, OHADA, and IFRS underscore the simultaneous push for convergence and the assertion of contextual relevance. The interviewees repeatedly stressed the limitations of IFRS in the Ivorian context, highlighting not only technical complexity and cost, but also the mismatch between IFRS's market-oriented logic and the state-oriented economic model prevailing in Côte d’Ivoire. Thus, although interdependence creates pressures toward alignment, the outcomes depend on how agency is exercised within legal, economic, and institutional constraints.

By interpreting our findings through the lenses of accounting infrastructure and polycentric accounting, we underscore that accounting change in Côte d’Ivoire is best understood as a recursive negotiation among multiple stakeholders operating across numerous institutional levels. While infrastructure offers the foundation, polycentricity explains the evolving strategies and compromises that define how standards are introduced, adapted, or resisted. Together, they help demystify the complex politics of accounting development in postcolonial African settings, without presuming interdependence to imply uniform applicability or inevitable harmonisation.

Concluding comments

The diffusion of accounting systems through colonial channels is well documented in accounting history. Yet, a critical question remains: How can a postcolonial state, embedded in global structures of economic and epistemic dependency, exercise agency over the construction of its accounting system? This study explored the interplay of external influences and local contestation in the evolution of accounting regulation in Côte d’Ivoire – a Francophone West African country with a particularly layered regulatory environment.

We addressed the question of how Ivorian accounting professionals and institutions navigated multiple waves of external influence – colonial, international, and regional – while striving to construct and maintain an accounting architecture with local relevance. Our analysis focused on both historical and contemporary efforts, including the crafting of the PCI, resistance to full adoption of the OCAM plan, and the cautious response to the imposition of IFRS. The Ivorian experience exemplifies the tensions involved in reconciling imported standards with domestic legal, institutional, and economic realities.

Employing a methodology that triangulates archival sources, oral histories, and elite interviews, we reconstructed the recursive processes that shape accounting standard setting (Botzem et al., 2017). The findings illustrate how local, regional, and international actors pursue competing agendas, leveraging institutional arrangements such as OHADA and SYSCOA to advance or resist particular models of accounting practice. The case reveals a complex choreography of negotiation, adaptation, and selective appropriation.

Two conceptual insights emerge. First, the introduction of exogenous accounting techniques may provoke a layered response that includes both accommodation and resistance. In the Ivorian case, the early adoption of French PCG standards was eventually challenged through regional collective efforts (e.g. OCAM) and later adapted through national initiatives (e.g. PCI). Second, although international pressures – exerted through IFAC or the World Bank – can penetrate regional structures like OHADA, their success depends on local receptivity, institutional capacity, and political commitment. The belated, partial acceptance of IFRS across OHADA countries reflects not merely resistance, but a rational negotiation of institutional fit.

These insights enrich African accounting historiography (Annisette, 2006; Botes, 2018; Hammond et al., 2007; Mihret and Bobe, 2014; Samkin, 2010; Verhoef, 2013, 2014) and reveal promising avenues for future research. A comparative study of how National Accounting Councils influence OHADA's standard-setting process would reveal the internal dynamics of regional governance. Similarly, a focused inquiry into the professional formation and epistemic preferences of Francophone African accountants could explain the limited traction of indigenous standard setting. Côte d’Ivoire's decision to develop the PCI, rather than adopt OCAM, highlights how individual agency can disrupt collective scripts.