Abstract

How small-business owners assess uncertainty and risk in the macroeconomic environment to report optimism toward their business activity is an important research question for policymakers and academics alike. Drawing on a monthly optimism index and a variety of uncertainty and volatility (risk) trackers from January 1986 to June 2017, in line with the expectation that business owners dislike uncertainty in economic policy, economic policy uncertainty may lower optimism. Business investment and sentiment volatility, however, contributed positively to optimism. The findings provide preliminary implications for policymakers in targeting indicators salient to the optimism index of small-business owners.

The drivers of the economic sentiment of small-business owners are of keen interest to policymakers (Dunkelberg & Wade, 2009; Phillips, 2002). The longest-running small business optimism index in the United States is the National Federation of Independent Businesses (NFIB) Small Business Optimism Index (Dunkelberg & Wade, 2009; Storey, 2011). Released monthly, the optimism index has a score of 100 as the baseline, with scores above 100 indicating a positive mood and scores lower than 90 signaling a recession. The NFIB optimism index remains among the most reliable proxies of the pulse of small businesses in the United States.

The NFIB optimism index represents the shared optimism or shared positive beliefs and expectations of a group of individuals (Santero & Westerlund, 1996). The collective sentiment is studied widely in assessing consumer, executive, supply chain manager sentiments, among others (Christiansen et al., 2014; Santero & Westerlund, 1996). Though individual optimism is partly driven by psychological (Cooper et al., 1988), genetic (Conrad, 2001), or environmental factors (Yuh et al., 2010), collective optimism of the business owners primes economic activity and informs policymakers on the needs of small-business owners.

For this research note, our contribution is primarily not theoretical, but we take a policy perspective by asking which of the available macroeconomic uncertainty and risk indicators influence the small-business owner optimism index in the United States. We focus on the role of two widely assessed elements in entrepreneurship—uncertainty and risk—in driving the collective optimism of small-business owners (Rakow, 2010). The assumption about the nature of uncertainty for our work requires discussion.

Based on Knight (1921), uncertainty is an “unknown, unknown” and risk is a “known, unknown”; as such, uncertainty may be empirically unmeasurable. Knight proposed three types of uncertainty: known distributions and unknown draws, unknown distributions and unknown draws, and nonexistent distributions with unclassifiable instances or true uncertainty. Our conceptualization of uncertainty is based on the first two and not the third type, as it can only be resolved by human action (Buchanan & Vanberg, 2002). As such, we do not focus on pure uncertainty, but based on Knight’s (1921) the uncertainty in the event spaces—set of all possible configurations of expected events—as a driver of decision-making under uncertainty.

Uncertainty- and risk-related macroeconomic factors that drive collective optimism have significant estimation challenges. Uncertainty- and risk-related factors could be correlated, and multiple indicators can aggregate in an unobservable fashion. Which types of uncertainty and risk indices do small-business owners take into consideration in forming optimism are not straightforward. Small-business owners may perceive the absence of reliable probability distribution that can be estimated from current data sources to predict future outcomes. 1 Aggregate small-business owner optimism index is an individual-level aggregation of a variety of firm-specific and environmental factors that are combined in an unobserved fashion, making it notoriously difficult to assess and attribute weights to understanding inclusion, combinations, and aggregations. Furthermore, due to a multitude of uncertainty and risk indicators, the traditional vector autoregressions (VAR) or time-series econometrics-based approaches may be of limited use. The VAR approach has limitations, as it may not be suitable for collapsing or compressing high-dimensional data (Stock & Watson, 2012), and others use graph-theoretic approaches and VARs in specifying risk and uncertainty (e.g., Balli et al., 2019). An additional limitation is that decision-makers cannot fully explain their evaluation process.

One approach to addressing this challenge is to use the stochastic multi-attribute acceptability analysis (SMAA), where the small-business owner is not able to fully report the parameters necessary for devising the optimism index (Doumpos et al., 2016, 2017). In this research note, based on SMAA, we use a Bayesian least absolute selection and shrinkage operator (LASSO) regression model built on the “

We use the monthly optimism index from NFIB from January 1986 to June 2017 and combine these data with monthly economic policy uncertainty and volatility (risk) indicators. We use both the aggregate and individual dimensions of uncertainty and volatility as we ex-ante do not know how the uncertainty and risk indicators could combine in explaining aggregate optimism index. The LASSO component of the proposed Bayesian LASSO regression model in this paper accommodates these multicollinearities between aggregates and individual indicators.

Overall, our goal with this research note is twofold—focus on an important index relevant to small-business owners in the United States and apply a method that helps overcome several estimation challenges in identifying the key uncertainty and risk-related drivers of such an index. We aim to make the following contributions. First, our results show that economic policy uncertainty contributes negatively and business investment and sentiment volatility contribute positively to optimism. The traditional theoretical frameworks in entrepreneurship have focused on positive and negative aspects of risk and uncertainty; however, we jointly consider these two theoretically studied factors to assess how small-business owners consider these indicators in reporting optimism. However, we also caution that several untested assumptions about functional forms and the interactions of risk and uncertainty entering as linearly separable terms in perceptions of small-business owners are required to simultaneously account for risk and uncertainty. Ours is a preliminary step aimed at untangling the risk and uncertainty perceptions in influencing small-business owners’ expectations. Despite the associated negative elements of risk that carry a loss proposition, inconsistent with the assumption of risk aversion among small-business owners (Fairlie & Holleran, 2012), the most consistent effect is the negative effect of economic policy uncertainty. More surprisingly, we find a positive effect of the business investment and sentiment Equity Market Volatility (EMV) tracker. 3 Considering the two findings, business owners, as expected, may not positively perceive uncertainty in economic policy; however, they may perceive volatility in investment and sentiment more positively. 4

Second, equally interesting are the findings on the limited role of widely espoused indicators discussed in the popular press. We find that uncertainty in monetary or fiscal policy, health care policy, or regulatory uncertainty has a negligible impact on optimism. 5 Though monetary and fiscal policy uncertainty can impact access to capital or health care and are also popular when discussing challenges for small-business owners (Kitching, 2019; Snowe, 2006), these factors do not seem to be too critical in influencing optimism. Though regulation is considered an important consideration for small-business owners in the United States, regulatory uncertainty is not a driver of lower optimism. As such, for policymakers considering a gamut of factors that small-business owners are exposed to, our study is an early study that may help parse the key drivers of small-business owners’ optimism. Our primary contribution is empirical. We identify an important consideration for policymakers—in forming business optimism, business owners react negatively to economic policy uncertainty and positively to the business investment and sentiment EMV tracker (Åstebro et al., 2014; Greco et al., 2008).

In the following sections, we start by providing a brief theoretical background followed by the empirical specification and results. We close after discussing the implications for policymakers and academics.

Theoretical Background

Since the 1940s, economists have focused on measuring collective sentiment with the underlying premise that the opinions, feelings, and beliefs of the collectives in societal segments could help predict broader changes in the economy. The measure of economic sentiment is not only informative for the policymakers but is also, at times, a leading indicator of the economic cycle. Timely sentiment indices inform policymakers to act toward devising business-friendly policies.

Among the sentiment indices, NFIB’s optimism index represents the longest-running publicly available sentiment index of small-business owners in the United States. Though idiosyncratic measures are valuable for individual business owners, the sentiment index aims at improving population-averaged assessment. Therefore, moving from individual business owner optimism assessments studied widely in entrepreneurship literature, we zoom out and focus on the optimism of small-business owners’ assessment of expected future business conditions. A variety of studies have shown that consumer and investor sentiments affect market returns and despite their limitations as aggregate self-reported data, sentiment indices remain critical to macroeconomic decision-making (Christiansen et al., 2014).

Small-business owners and entrepreneurs are generally optimistic (Crane & Crane, 2007). We rely on Scheier and Carver’s (1985) definition of optimism as the extent to which the positive expected events of the future outweigh the negative expected events. The optimism index based on the outlook and planned hiring and investments, in the face of uncertainties and risks, explains the strategic and tactical actions of small-business owners. The sentiment index focuses on the time-varying assessments of the underlying sentiment based on changing macroeconomic conditions. Just as investors or consumers reporting sentiments are driven by a variety of personal and social factors, on the aggregate the goal is to assess the responsiveness of investors and customers to changing economic conditions. Similarly, the NFIB optimism index is based on the changing optimism of small-business owners with the changing macroeconomic environment. Collective optimism, defined as shared positive expectations that outweigh shared negative expectations, is previously studied at the team, organizational, community, or national level (Bennett, 2011). Our theoretical assumption, consistent with sentiment indices, is that of an aggregative index (Woehr et al., 2015). In classical microeconomics, aggregation, by summing the indicators of optimism, is problematic as the summated index may not inherit the key attributes of small-business owners’ preferences, and it may also not inherit transitivity among individuals whose optimism levels are summed.

Optimism, Risk, and Uncertainty

Risk and uncertainty are central to entrepreneurial endeavors (Knight, 1921). Knight (1921) proposed that risk refers to unknown outcomes from known distribution, whereas uncertainties refer to unknown outcomes from unknown distributions. In other words, risk refers to variations in possible outcomes that are known or previously experienced. Related to uncertainty, even though events are experienced they may be uncertain when no relevant information is available or when few individuals model “black swan” outcomes in their probabilistic reasoning (Taleb, 2010). Based on bounded rationality (Simon, 1997), though entrepreneurial decision-making is not random and irrational, studies have shown that entrepreneurs engage in deliberative decision-making by seeking information and support and by drawing on a variety of tools, including effectuation (Sarasvathy, 2009), search and satisficing (Berg, 2014), navigating environments by building coalitions (Dew et al., 2008), among others. Knight (1921, p. 237) highlighted that it is correct “to treat all instances of economic uncertainty as cases of choice between a smaller reward more confidently and a larger one less confidently anticipated.” The intuitive approach is faster and requires less effort, but it is subject to errors. The logical approach is cognitively effortful, is rule-based, and driven by conscious attention.

Based on the risk and uncertainty signals in the broader macroeconomy and considering the underlying challenges in processing such signals, a calculus of how multiple signals are interpreted, processed, and aggregated is difficult to ascertain. Therefore, we hypothesize small-business owners to be Bayesian learners who update their expectations in the context of their business and evolving macroeconomic signals. A Bayesian approach may be central to developing an understanding of how small-business owners interpret uncertainty and risk-based signals to devise optimism sentiment.

Small-business owners may not be able to accurately report combinations of uncertainty and risk information used to derive weights for reporting the optimism index. For example, small-business owners in the retail industry may consider an aggregate risk index but may also consider a consumer sentiment risk index. The consumer sentiment risk index is a part of the aggregate risk index; however, this empirically less desirable attention to aggregate and its components can be expected in practice and the traditional regression models may not suffice. The optimism index may not be based on additive parameter weights, though not irrational (Berg & Hoffrage, 2008), which are generally a result of intuitive and less linear thought processes that require accommodation of such errors and also variations in attention to aggregate and components of signals. To accommodate such varying combinations, we develop a model based on LASSO with Bayesian priors.

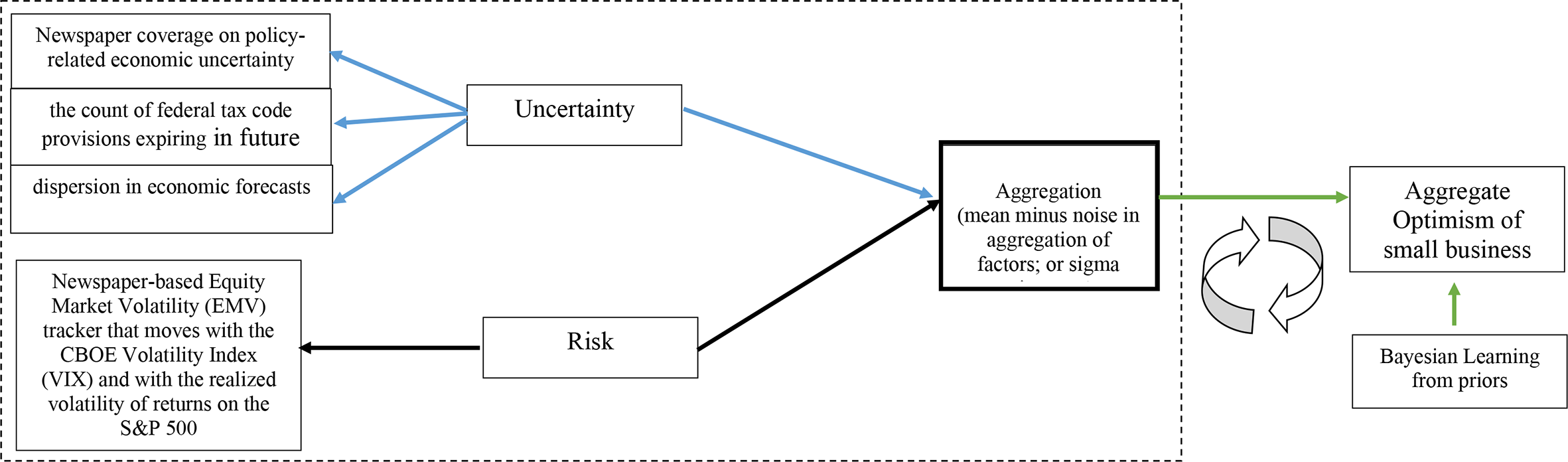

The methodology we offer is not a panacea for addressing the problem of aggregation and reporting of optimism sentiment in the presence of indicators of uncertainty and risk. Due to the lack of theoretical background, we do not propose a formal hypothesis; however, our research question is how do small-business owners interpret (positively or negatively) uncertainty and risk-based signals from the macroeconomy? Though the theoretical framework around this framework could gestate in the future, our primary goal is to empirically test the proposed research question. Based on the above discussion, we present our conceptual model in Figure 1, and below we provide a formal model of our methodology.

A conceptual overview. “Uncertainty must be taken in a sense radically distinct from the familiar notion of Risk, from which it has never been properly separated.... The essential fact is that ‘risk’ means in some cases a quantity susceptible of measurement, while at other times it is something distinctly not of this character; and there are far-reaching and crucial differences in the bearings of the phenomena depending on which of the two is really present and operating.... It will appear that a measurable uncertainty, or ‘risk’ proper, as we shall use the term, is so far different from an unmeasurable one that it is not in effect an uncertainty at all.” “Knightian uncertainty is a lack of any quantifiable knowledge about some possible occurrence, as opposed to the presence of quantifiable risk [uncertainty] acknowledges some fundamental degree of ignorance, a limit to knowledge, and an essential unpredictability of future events.”

Empirical Specification

Suppose we have a vector of explanatory variables

A dynamic factor model is as follows.

where

In many instances, we want to infer the effect of explanatory variables on outcomes via a composite indicator such as

where

where

where

Greco et al. (2019a) introduce a methodology for constructing composite indicators known as

The

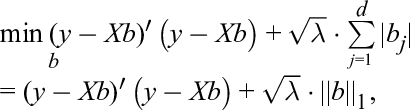

Model

Our model consists of Equation (5) plus the following.

where

where

This is defined as

that is, the weighted variance of the different components in the composite indicator. Normally, we would expect

Notice that

As our explanatory variables are economic policy variables and our outcomes are entrepreneurship-related variables, we modify Equation (5) as follows.

where

Equation (6) provides a way to summarize the effect of policy variables

We denote all observed data by

The major assumption in Equation (7) is that policy-related inefficiency is dynamic or persistent and also depends on the policy variables

When the number

To our knowledge, this is the first instance in which a LASSO prior is placed on a dynamic latent variable model including both the latent dynamic modified composite indicator (

Denote collectively all regression-like parameters by

where

Here,

for

Data and Methods

We use three datasets: (a) the Small Business Optimism Index from NFIB; (b) the categorical policy uncertainty data (a proxy for uncertainty); and (c) categorical volatility index data (a proxy for risk). All data are monthly data from January 1986 to June 2017.

The NFIB index is comprised of responses from small-business owners on prevailing economic conditions. The index comprises 10 components and the seasonally adjusted optimism is derived from subtracting negative responses from positive responses on seasonally adjusted business expectations. Additional details on the NFIB index are provided in Online Appendix B.

The categorical policy uncertainty data are from Baker et al. (2016) and based on a range of subindices based on results from the Access World News database of over 2000 U.S. newspapers. Each subindex is based on terms related to economy, uncertainty, and policy. The time-series are normalized to have a mean of zero and an SD of one. We provide a list of all the categories in Online Appendix C. The index is used in a variety of recent studies (e.g., Acemoglu et al., 2016; Arellano et al., 2019; Bloom et al., 2018).

The components for volatility (risk) index are the newspaper-based EMV tracker that moves with the Chicago Board Options Exchange Volatility Index (VIX) and with the realized volatility of returns on the S&P 500. The policy-related economic EMV tracker is created for 30 categories every month. The details on the 30 categories are listed in Online Appendix D.I, and additional details on the calculation of the measure are available at https://www.policyuncertainty.com/EMV_monthly.html.

Results

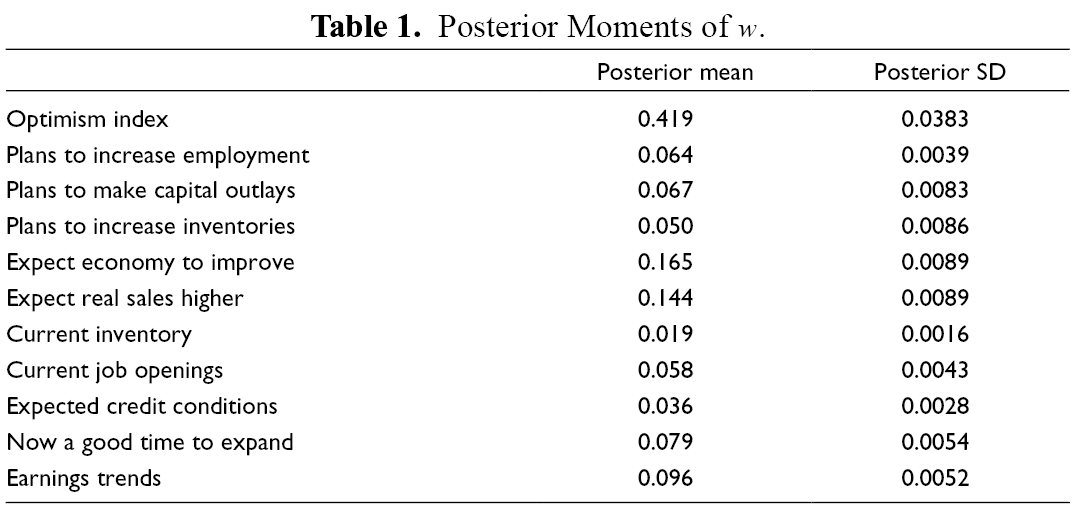

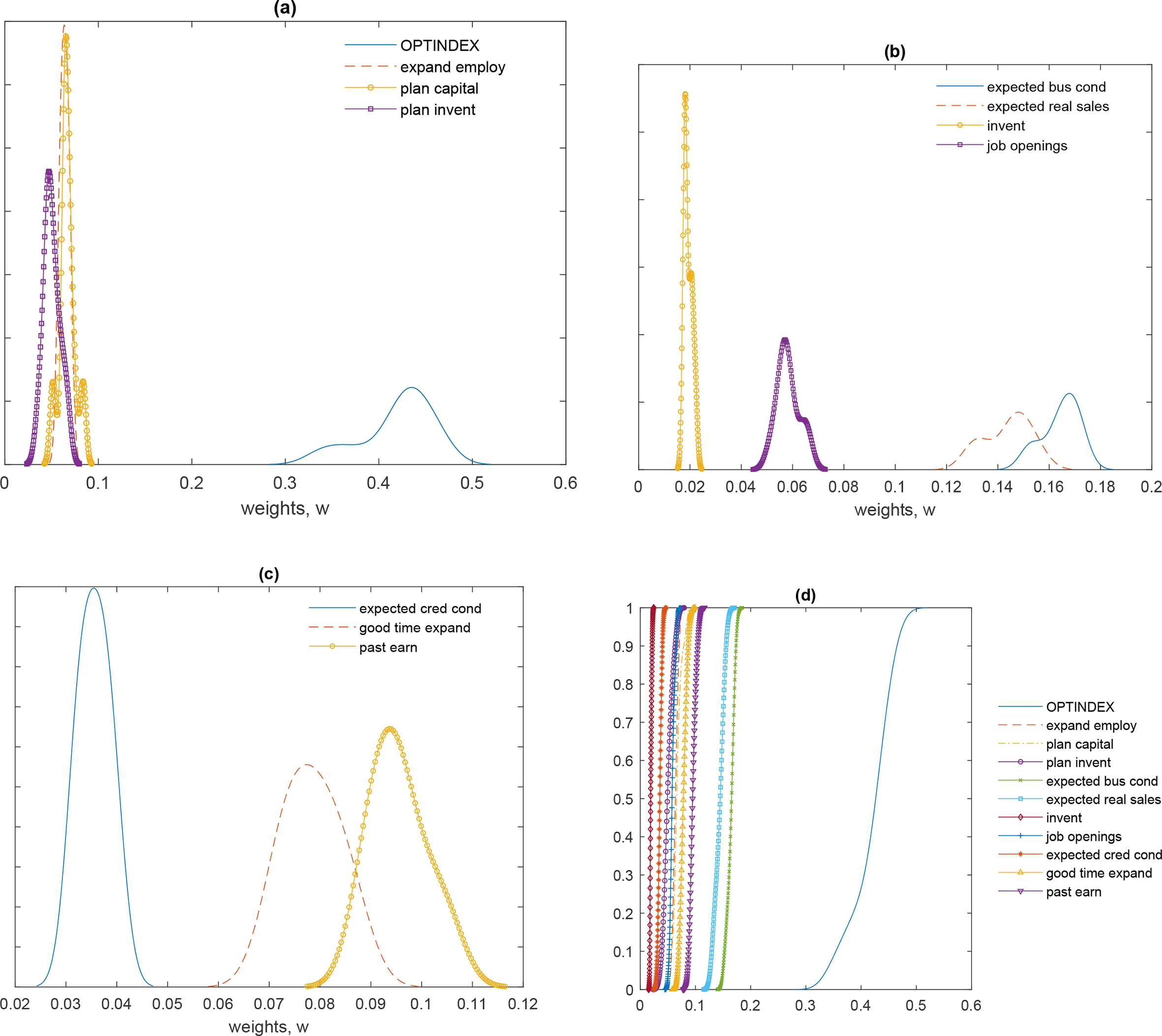

Posterior means and SDs of select parameters are reported in Table 1 and Figure 2. In Figure 2(a)–(c), we report marginal posterior densities of weights that are used in the construction of the new composite indicator. Each of the parts in Figure 2(a)–(c) shows marginal posterior densities for a different set of weights. For the most part, these densities are nonnormal showing the dangers of asymptotic theory applied in our instance. The most important subcomponent is the OPTINDEX (optimism index) in Figure 2(a). An interesting question is whether the weights for the subcomponents can be rankedAltmann et al. (2014). This is taken up in Figure 2(d) where we report marginal posterior cumulative densities. From this evidence, it is easy to see that OPTINDEX stochastically dominates all others, followed by expected business conditions, expected real sales, past earnings, good time expansion, among others. The lion’s share is due to OPTINDEX whose weight ranges from 0.3 to over 0.5 (Figure 2(a)) followed by expected business conditions and expected real sales (Figure 2(b)) whose posterior mean weights are 0.16 and 0.14, respectively.

Posterior Moments of

Marginal posterior densities of

Before proceeding with our main analysis, we present the distribution based on violin plots of all the explanatory variables, descriptive statistics of all the explanatory variables, and time-series distribution of all the indicators (Online Appendix D). An additional concern is that structural breaks may bias the results. The original authors of the uncertainty and the risk measure adjusted for this possibility; however, we also provide tests for structural breaks in Online Appendix D. We used the difference between each indicator and used the estat sbcusum routine in Stata 16. The test assesses whether the coefficients of a time-series regression are stable over time by constructing a cumulative sum of recursive residuals. In Online Appendix D, we present structural breaks plots for the main uncertainty and risk variables, and then we present the plots for all the remaining explanatory variables. Note, if the line is within the confidence interval, the null hypothesis of “no structural break” is not rejected. In the figures, all the explanatory variables are within the confidence interval.

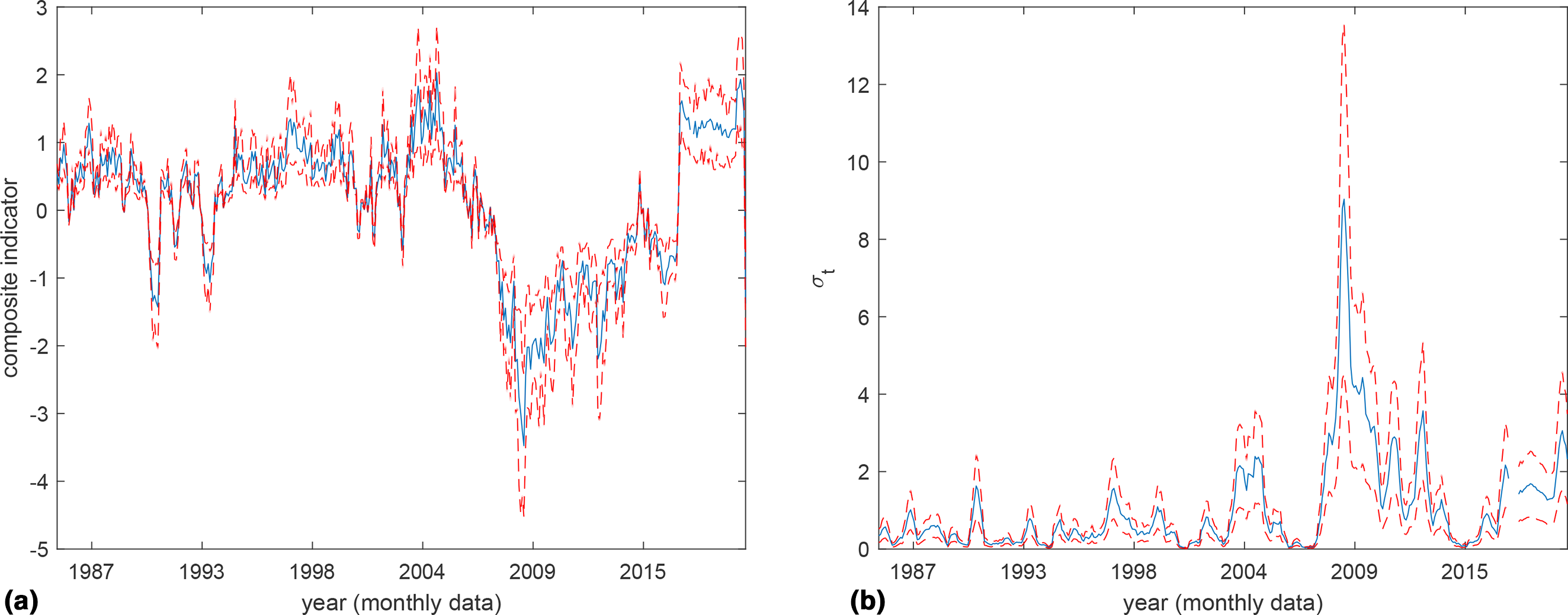

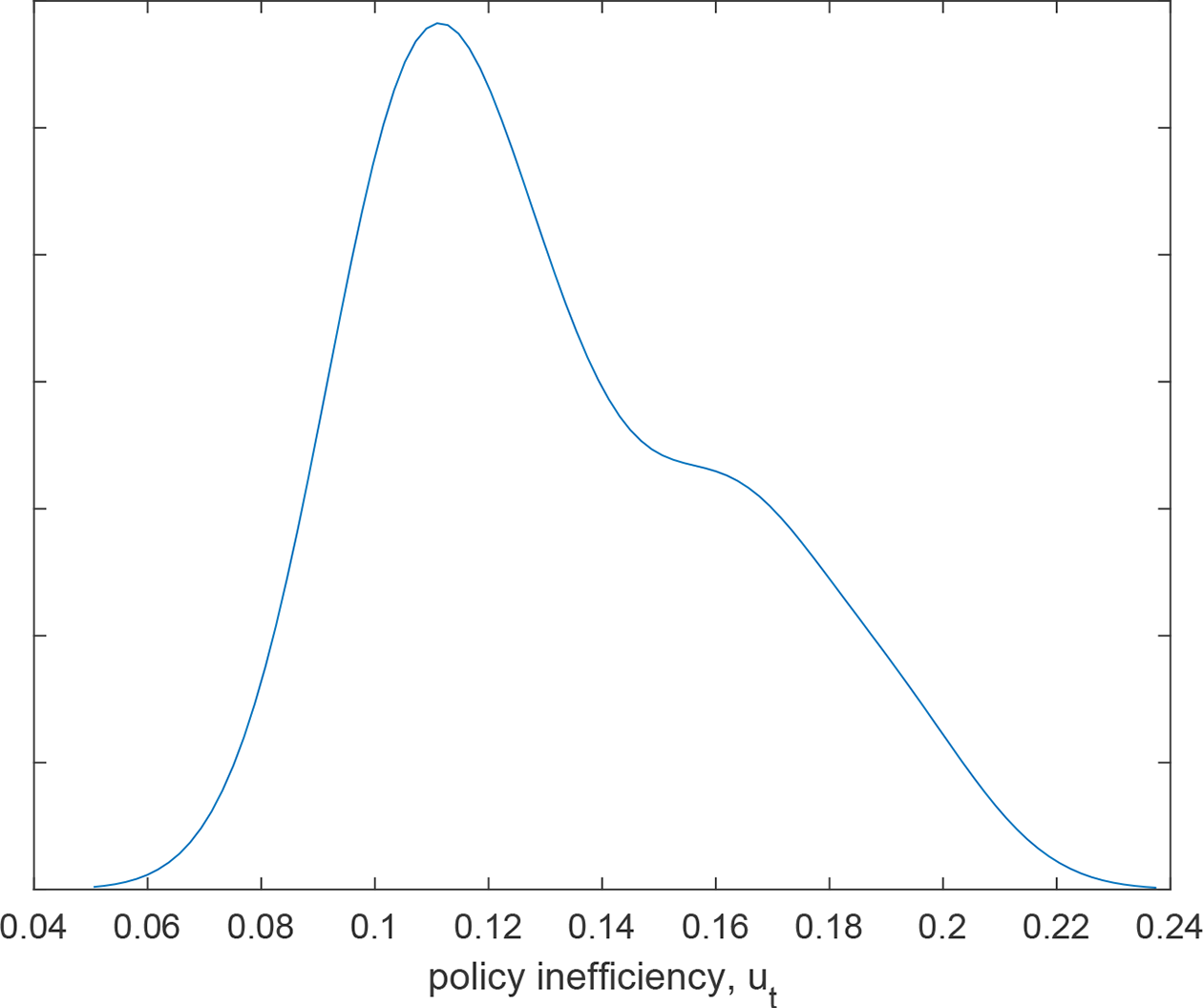

In Table E.1 of Online Appendix E, we report the results of estimating the dynamic factor model in Equation (1) using maximum likelihood state-space models. In turn, we use the new model to provide marginal posterior densities of the modified composite indicator shown in Figure 3. Figure 4 presents the sample distribution of posterior mean fits of inefficiency.

Posterior means. (a) Posterior mean fits of the modified composite indicator. (b) Risk (

Posterior mean policy inefficiency.

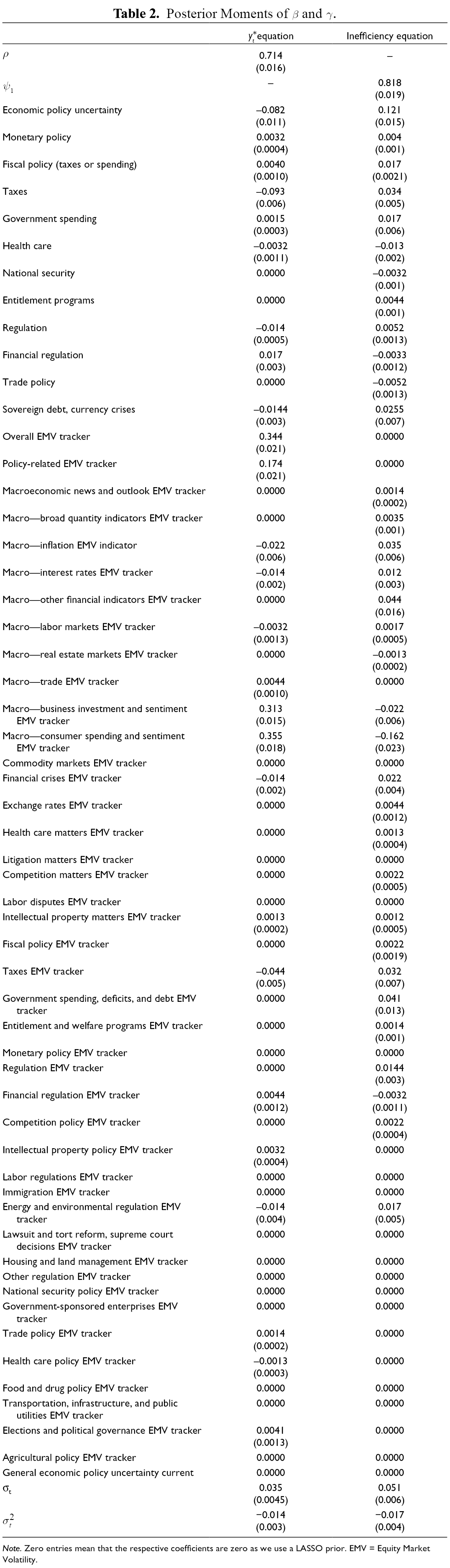

Our inferences are based on Table 2. We note that all the variables are standardized for the analysis; the optimism index is not standardized as the model forces it to be a sum of 1. Before discussing the results, we reiterate that inclusion of combined and individual dimensions is not subject to multicollinearity concerns in LASSO fits. For mean estimation,

Posterior Moments of

Note. Zero entries mean that the respective coefficients are zero as we use a LASSO prior. EMV = Equity Market Volatility.

Related to uncertainty signals, a one-tenth increase in SD in economic policy uncertainty has a negative association with optimism by −0.0082 SDs; however, there is also greater variability in how economic uncertainty is perceived (inefficiency = .0121). The effect size is meaningful in the sense that the optimism index has a posterior SD of 0.0383 (Table 1), indicating that a one-tenth SD change is feasible, and the corresponding decline of −0.0082 represents a 21.4% change in SD relative to the posterior SD.

Similarly, tax-related uncertainty has a negative association with optimism (−0.0093, or 24.89% of the change in SD relative to the posterior SD) and a much smaller variability (= .034). Surprisingly, monetary or fiscal policy is not associated with optimism and neither is health care policy uncertainty, especially given the lack of insurance for self-employed and insurance as a key consideration for small firm owners and employees. Regulation is negatively associated with optimism by a small amount; however, financial regulation is positively associated with optimism by a small amount.

Related to risk signals, policy-related EMV tracker has a positive association with optimism (= .0344 for a one-tenth SD of the predictor, or 89.81% of the change in SD relative to the posterior SD). Followed by the macro–business investment and sentiment EMV tracker also with a positive association (= .0313, with small inefficiency; 81.72% of the change in SD relative to the posterior SD). The macro–consumer spending and sentiment EMV tracker has a positive association with optimism (= .0355, and with lower inefficiency = −0.162; or 92.68% of the change in SD relative to the posterior SD). Several other trackers of volatility have a small to negligible association with optimism.

As an additional test, in Online Appendix F, we specify OLS, partialling out LASSO linear regression, cross-fit partialling out LASSO linear regression, and the post-double selection and post-regularization LASSO. The economic policy uncertainty is negative and consistent with the main inferences. Tax-related uncertainty is negative and nonsignificant in the OLS; however, for the remaining LASSO specifications (models 1–4), it is positive but nonsignificant. The policy-related EMV tracker has a nonsignificant effect, the macro–business investment and sentiment tracker has a positive effect, and the macro–consumer spending tracker has a nonsignificant effect.

Overall, based on the proposed analytical model and the general OLS and standard LASSO regression (Online Appendix F) related to uncertainty, business owners respond negatively to economic policy uncertainty and tax uncertainty. Related to risk, stock market volatility increases optimism, specifically, with macro–business investment and sentiment EMV tracker and macro– consumer spending and sentiment EMV tracker. Considering both the main specification and the additional analysis in Online Appendix F, the most consistent effect is the negative effect of economic policy uncertainty and the positive effect of the business investment and sentiment EMV tracker.

Conclusions and Future Research

For this research note, our goal was twofold—delving into drivers of optimism among small-business owners and assessing how business owner optimism is driven by risk and uncertainty. The proposed estimation approach lowers concerns for prior learning by modeling for Bayesian fits and accounts for unobserved considerations of aggregate and component-based dimensions (LASSO). The findings have the following theoretical implications.

First, the assessment of indices in entrepreneurship could consider the value of the proposed estimation approach. The decision contexts of entrepreneurship in the words of Knight (1921, p. 210–211) are an important consideration:

The ordinary decisions of life are made on the basis of ‘fits’ of a crude and superficial character. In general the future situation in relation to which we act depends upon the behavior of an indefinitely large number of objects, and is influenced by so many factors that no real effort is made to take account of them all, much less to fit and summate their separate significances. It is only in very special and crucial cases that anything like a mathematical (exhaustive and quantitative) study can be made. (as quoted in Rakow, 2010)

The quote from Knight is crucial in considering how entrepreneurs consider, report, and aggregate risk- and uncertainty-related signals. Our approach is a preliminary attempt to model some of the limitations in such aggregates to provide a nuanced view of entrepreneurial response to risk and uncertainty in developing an optimistic outlook. The aggregate mental calculus of developing optimism index could be based on collective intuitions, contagion, or herding, or any other group phenomenon. However, such mechanisms are difficult to measure and are intractable. Our estimation has its limitations; however, we focus on the collective aggregations to understand the associations among the components and we do not attempt to address the process of aggregation. Our approach complements that of Anglin et al. (2018) at the individual–industry level factors and focuses on risk and uncertainty indicators driving small business optimism index that is widely disseminated and representative of respondents from a variety of industries and regions.

Second, risk and uncertainty are studied, mostly, separately in the entrepreneurship literature (cf. Koudstaal et al., 2016). Devised as “unknown, unknown” and “known, unknown,” literature streams on uncertainty and risk have developed mostly on separate trajectories. For example, effectuation can be considered a mode of uncertainty resolution, whereas alertness could be a mode for opportunity search based on the available distribution of information in the Kirznerian framework. In our model, we relax the assumption by considering both risk- and uncertainty-related signals as they co-occur in an economy in a variety of indicators (Williamson, 1998). Our measures of uncertainty and risk are based on recently developed widely used measures. Broadly, the results demonstrate that small-business owners have lower optimism under uncertainty, but higher optimism for risky signals from the economy.

In addition to the indicators we found support for, additional discussion on the nonsignificant effects is warranted. We found that monetary and fiscal policies, government spending, health care, national security, entitlement programs, regulation, and financial regulation had negligible to no effect. Similarly, trade policy uncertainty had no effect and the sovereign debt crisis had a small effect. These nonsignificant or significant findings with negligible effects could be interpreted based on Williamson’s (1998) notions of institutions of governance. 8 Governance is a “means by which order is accomplished in a relationship in which potential conflict threatens to undo or upset opportunities to realize mutual gains” (Williamson, 1998, p. 37). Based on the classical Northian notion of institutions helping set the rules of the game, it is possible that relaxed monetary and fiscal policies over the last two decades may not be salient to small-business owners (North, 1990). Cheap debt and low inflation in the United States may have lowered the importance of these factors. Similarly, health care programs have been the focal point depending on the administrations and with limited, if any, changes in health care costs for self-employed even after Obamacare, uncertainty in health care may not influence optimism. Health care, fiscal, and monetary policy along with regulation and financial regulations are more policy-oriented and are now increasingly embedded institutionally in their reach and influence and may, therefore, be less of a factor based on uncertainty. Finally, entitlement programs and national security are perhaps far removed from small-business owner decisions. Conversely, economic policy uncertainty and the positive effect of the business investment and sentiment EMV tracker may be more transient than institutions, leading to greater sensitivity toward optimism. The notional substitution of institutionalized fiscal, monetary, and health care policies may reduce the role of these uncertainties in influencing optimism. We caution that our findings may have a limited external validity to non-U.S. contexts or additional uncertainty and volatility indicators not included in the model. Future studies can test whether our findings hold in the non-U.S. context and in alternate economic institutions (e.g., developing country or welfare economy), and may also consider additional indicators and study business optimism under extreme events (e.g., COVID-19).

Third, the findings have implications for policymakers focused on the role of multiple indicators that may calibrate small business sentiment. In addition to the significance of the effects, also of importance is the nonsignificance of the multitude of indicators in the results. Several of the indicators, including health care, labor laws, and environmental regulations, are not associated with optimism. Based on methodologies such as ours perhaps calibration of small-business owner optimism with other observable macroeconomic indicators can be useful.

Our study is not without limitations. We draw on the U.S.-based optimism index; however, due to variations in cultural and institutional dimensions, the findings may not be generalizable. We draw upon and build over a recent method on the mean-efficiency index to assess how the aggregation of composite indicators can be better modeled. Nevertheless, future studies can develop models. For example,

Finally, we used newspaper-based uncertainty and risk measures that are publicly available and used in several studies. However, future studies could also use survey-based measures or richer measures based on text analysis from alternate sources including social media. Though we rely on the measures of economic uncertainty and volatility from http://www.policyuncertainty.com/, additional measures of uncertainty based on commodity, gold, oil, and energy pricing uncertainties can be used in future studies (e.g., Balli et al., 2019; Naeem et al., 2020).

In closing, based on the monthly optimism index and uncertainty and volatility trackers over 32 years, we found that economic and tax policy uncertainty and tax uncertainty increased optimism, and surprisingly, monetary or fiscal policy, health care policy, or regulatory uncertainty did not impact optimism. Aggregate volatility, representing risk in the markets, increases optimism. For small-business owners, the findings highlight a positive response to risk but a negative response to uncertainty.

Supplemental Material

Supplementary Material 1 - Supplemental material for Macroeconomic Uncertainty and Risk: Collective Optimism of Small-Business Owners

Supplemental material, Supplementary Material 1, for Macroeconomic Uncertainty and Risk: Collective Optimism of Small-Business Owners by Pankaj C. Patel and Mike Tsionas in Entrepreneurship Theory and Practice

Footnotes

Acknowledgements

The authors thank Karl Wennberg, senior editor, and the three anonymous reviewers for their excellent comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.