Abstract

This study examines the effects of family involvement on international market entry. Bridging theories of interorganizational imitation with the notion of socioemotional wealth protection, we argue that family-managed firms are more likely to act as “intuitive statisticians,” using the internationalization outcomes of industry peers to determine when to internationalize. An event history analysis of 2427 manufacturing firms supports this position. Family-managed firms’ likelihood to internationalize increases as prior entrants’ performance mean and variance increase. Ultimately, our study demonstrates that this imitation strategy enables family-managed firms to reduce risk and endure longer in broached international markets.

Keywords

Introduction

The international strategies of family firms have received considerable attention (e.g., Alessandri et al., 2018; Bhaumik et al., 2010; Fernández & Nieto, 2005; George et al., 2005; Gómez-Mejía, Makri, & Larraza-Kintana, 2010; Hennart et al., 2017). The majority of studies in this domain adopt the behavioral agency model which suggests that family efforts to protect family socioemotional wealth (SEW) deters family firms from entering international markets (Bhaumik et al., 2010; Gómez-Mejía et al., 2007; 2010; Lahiri et al., 2020). Gómez-Mejía et al. (2010), for example, argue that the members of a controlling family are willing to sacrifice financial benefits from internationalization to avoid accessing external financing or ceding power to nonfamily professionals with the skills to grow internationally.

The behavioral agency model (BAM) suggests that family firms’ desire to protect SEW leads them to act more conservatively, avoiding decisions that would increase performance variability and thereby risk failure (Gómez-Mejía et al., 2007). However, the evidence on family firms’ internationalization is mixed (Arregle et al., 2017), and scholars now acknowledge that family firms are heterogenous, gravitating toward extreme tails of behavioral and outcome distributions (Chua et al., 2012; Miller & Le Breton-Miller, 2020). Indeed, contrary to BAM expectations, family firms are sometimes celebrated as among the most successful global companies (e.g., Casillas & Pastor, 2015; De Massis, Audretsch, et al., 2018), suggesting that their commitment to long-term value creation facilitates, not constrains, internationalization (e.g., Zahra, 2003; Arregle et al., 2012). Because of such contradictions, researchers have called for greater attention to the nuanced drivers of family firm internationalization. In a recent meta-analysis, Arregle et al. (2017) found that family firms’ likelihood to internationalize depends on a variety of situational factors. Others have highlighted the need to parse the dimensions of internationalization decisions, such as “timing, speed, pace, and resilience” (Debellis et al., 2021, p. 13).

To build a more fine-grained understanding of the drivers of international market entry decisions in family firms, we shift the focus from whether family firms are more or less likely to internationalize than others to when family-managed firms are more or less likely to do so, and with what adaptive implications. Specifically, we draw on theories of imitation and its outcomes (Lieberman & Asaba, 2006) for insights into decisions under uncertainty (Haunschild & Miner, 1997). Internationalization by industry peers provides information about its popularity and success in uncertain contexts, thereby providing cues for imitation (see Lieberman & Asaba, 2006; Naumovska et al., 2021). Two core modes of imitation are identified: frequency-based imitation (e.g., Bikhchandani et al., 1998; Fiol & O'Connor, 2003) and outcome-based imitation (e.g., Haunschild & Miner, 1997). 1 Whereas frequency-based imitation is based on prevalence or popularity and maintenance of competitive parity, outcome-based imitation is based on anticipated decision consequences, discriminant information processing, and competitive differentiation.

We argue that the goal of preserving family social and financial assets and maintaining distinctiveness causes family-managed firms, more than nonfamily firms, to rely more on outcome-based imitation and less on frequency-based imitation in international expansion. This results in more considered market entry decisions that enhance venture reliability and longevity—key indicators of success (Barkema et al., 1996, 1997). We test these arguments on international market entry decisions of 2427 Spanish manufacturing firms from 1999 to 2012. The results confirm that family-managed firm international expansion is shaped by outcome-based imitation, whereas nonfamily firms are more driven by frequency-based imitation. We also find that family-managed firms exhibit more stable performance and endure longer in broached foreign markets. Thus, our results suggest that imitation processes and targeted information processing are important drivers of international market entry and its outcomes in family firms.

Our research makes several contributions. First, we advance beyond the SEW perspective on family firm internationalization (Gómez-Mejía et al., 2010) by broaching the interorganizational imitation literature and providing a more nuanced portrait of how family-managed firms mitigate uncertainty in international market entry. In addition, we reveal important mechanisms influencing the relationship between family involvement and internationalization outcomes, thus responding to a pressing need for a more nuanced understanding of the relationship between family involvement, internationalization, and its consequences for firm performance (Arregle et al., 2017; Boellis et al., 2016; De Massis, Frattini, et al., 2018; Kano & Verbeke, 2018; Reuber, 2016). Finally, our study contributes to the literature on organizational imitation (e.g., Gaba & Terlaak, 2013; Haunschild & Miner, 1997; Henisz & Delios, 2001) by showing that imitation choices not only depend on context, but also on the priorities and motives of decision makers such as family firm owners and managers.

Theory Development and Hypotheses

International Market Entry in Family Firms

Family firm owners and managers exhibit particular priorities and risk preferences that cause significant behavioral and performance differences between family and nonfamily firms (Amore et al., 2021; Chrisman et al., 2005; Gómez-Mejía et al., 2007, 2011; Miller et al., 2010, 2013). Prior studies have found a negative relationship between family involvement and foreign sales and direct investments (e.g., Bhaumik, et al., 2010; Fernández & Nieto, 2005; Gómez-Mejía et al., 2010; Hennart et al., 2017). Gómez-Mejía et al. (2010) showed that family firms prefer domestic rather than international diversification. Similarly, others have found a negative effect of family involvement on export propensity and intensity (Fernández & Nieto, 2005, 2006) and on the scale, scope, and speed of internationalization (Cerrato & Piva, 2012; Graves & Thomas, 2006; 2008; Sciascia et al., 2012).

Much of this work builds on the behavioral agency model and the SEW perspective (Gómez-Mejía et al., 2007). According to these views, controlling family members’ accumulated affective endowments from their firms shape how they evaluate gains and losses from their strategic decisions. These socioemotional endowments stem from enduring corporate control, emotional and reputational attachment and shared identification with the firm, social ties with longstanding stakeholders, and the possibility to renew family bonds through dynastic succession (Amore et al., 2021; Chrisman & Patel, 2012; Kotlar et al., 2018; Le Breton-Miller & Miller, 2020). Family firms are argued to place greater emphasis on SEW than on purely financial considerations and thus to be reluctant to engage in decisions that may dilute family ownership and control and prevent intra-family succession, even if this risks poor performance. Yet, when facing poor performance, family members’ emotional attachment to the firm increases their sensitivity to organizational failure, inducing them to protect existing assets and avoid decisions that may increase performance variability (Gómez-Mejía et al., 2007; Lumpkin & Brigham, 2011). Extending this logic to international strategy, Gómez-Mejía et al. (2010) argue that foreign market entry entails potential SEW losses, hence family firms will internationalize less than others (see also De Massis, Frattini, et al., 2018).

However, the BAM and SEW perspectives are theories of decisions under risk (Wiseman & Gomez-Mejia, 1998), that is, decision-making where individuals can identify all potential outcomes of a choice and their probabilities (cf. Bromiley & Rau, 2019). Yet most decisions in SEW-based studies involve uncertainty rather than risk, implying that individuals cannot envision all potential outcomes of a choice (Knight, 1921). Due to their unfamiliarity with market characteristics, firms aiming to expand internationally “must successfully counter uncertainty surrounding the governance of transactions in the new markets to reap the desired benefits of higher profitability, growth, or survival” (Henisz & Delios, 2001, p. 444). Indeed, the outcomes of internationalization decisions are often hard, if not impossible, to predict.

The literature provides substantial evidence that risk and uncertainty elicit very different responses (cf. Bromiley & Rau, 2019, p.25; Ellsberg, 2001). It is important therefore to explain how family firms mitigate such uncertainty in assessing the consequences of international market entry. Thus we elucidate how family involvement in both firm ownership and management prioritizes different uncertainty mitigation strategies.

Uncertainty Mitigation and Interorganizational Imitation

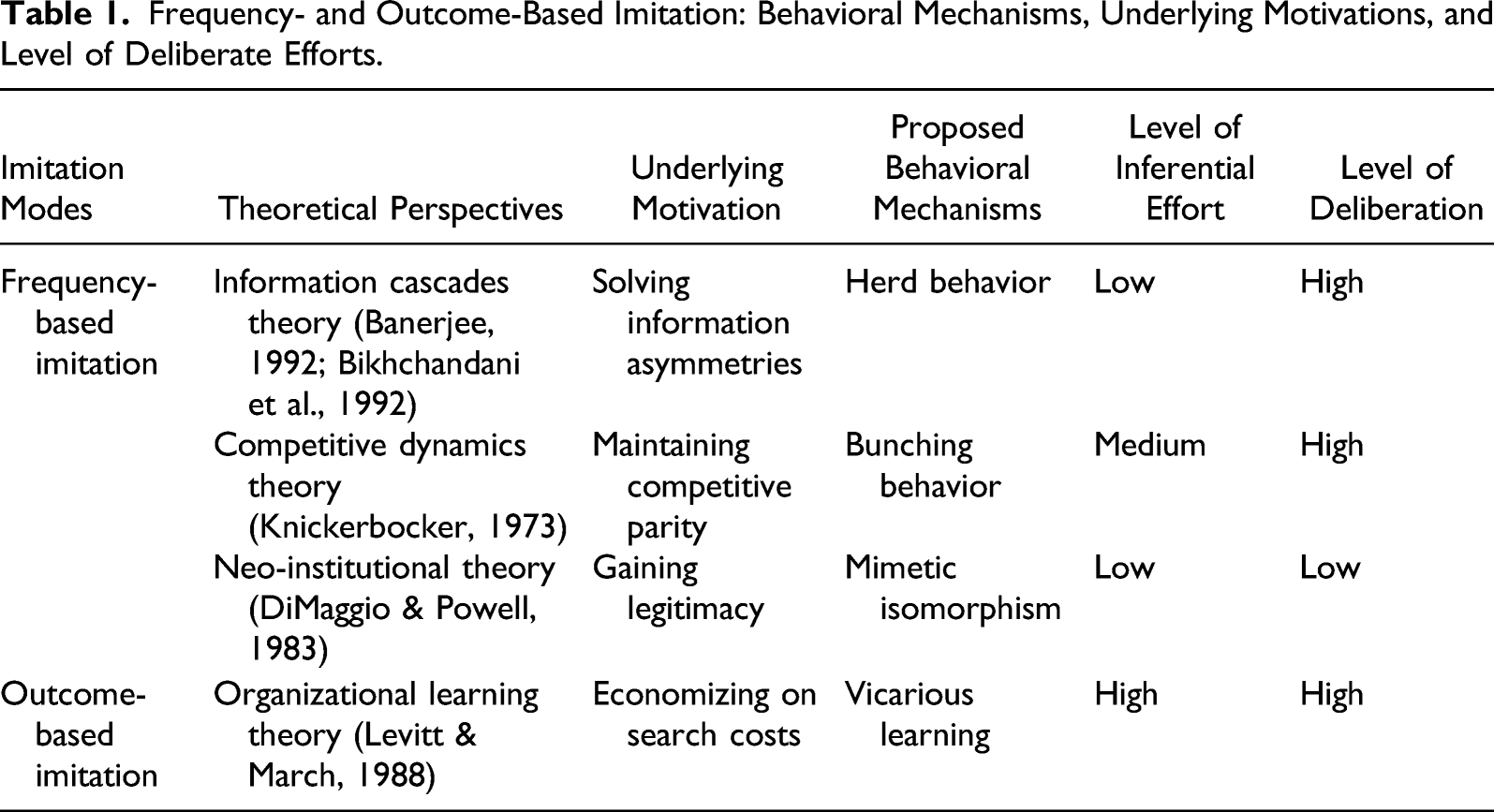

Frequency- and Outcome-Based Imitation: Behavioral Mechanisms, Underlying Motivations, and Level of Deliberate Efforts.

Frequency-Based Imitation

Under this mode, firms adopt behaviors and choices based on increasing diffusion among other players. Frequency-based imitation is featured in several literature streams. First, in the economic literature on information cascades, it is often associated with herd behavior: firms observing international market entry by other firms may assume that behavior to be valuable, update expectations accordingly, and follow suit with imitation (Banerjee, 1992; Bikhchandani et al., 1992, 1998). Not requiring substantial inferential effort or analysis, imitation is grounded on the assumption that others possess superior information, leading firms to imitate while discarding their private information (cf. Bikchandani et al., 1992; Rao et al., 2001). Second, competitive dynamics theory assumes that firms imitate to maintain competitive position: “if rivals match each other, none become better or worse relative to each other” (Lieberman & Asaba, 2006, p. 375). In the context of internationalization, rivals’ matching one another’s entries into foreign markets is referred to as “bunching” (Gimeno et al., 2005; Knickerbocker, 1973). This behavior is deliberate and involves inferential effort to assess whether a focal firm has the capabilities to match competitors (Stephan et al., 2001). Finally, neo-institutional theory views imitation as an attempt to gain legitimacy, emphasizing that the diffusion of behavior conveys legitimacy to imitators (DiMaggio & Powell, 1983). This perspective emphasizes social motivations over technical ones. Imitation here is not driven by calculative rationality but the belief that “common things are good” (Greve, 2013, p. 108).

Outcome-Based Imitation

Organizational learning theorists propose a different imitation mode that reflects more complex inferences than those involved in frequency-based imitation. They see imitation as a means to reduce the costs and risks of experimentation (Levitt & March, 1988). To do so, firms learn vicariously by observing the consequences of other firms’ actions (Levinthal & March, 1993). If adoptors do well, they are imitated, otherwise, imitation is avoided or retarded (Gaba & Bhattacharya, 2012; Haunschild & Miner, 1997). Outcome-based imitation relates more closely to technical (i.e., performance-related) than social (i.e., legitimacy-related) motivations and is often aimed at attaining a “second-mover advantage” ensuing from more thorough processing of signals from the environment to mitigate uncertainty (Fiedler & Juslin, 2006; Lieberman & Montgomery, 1988).

Imitation in Family-Managed Firms

Our main argument is that, given the level of uncertainty involved in the decision to internationalize, the foreign market entries of family and nonfamily firms are likely to be determined by different imitation modes: whereas nonfamily firms’ decisions are likely to be driven by prevalence considerations to maintain competitive parity, family-managed firms’ international market entry is driven by performance outcome competitive differentiation objectives.

Family-Managed Firms’ Susceptibility to International Market Entry Popularity

For family firm owners and managers, failures from internationalization may represent a significant financial loss (DeTienne & Chirico, 2013), as well as damages to the family reputation, limited career opportunities for family members, emotional disappointment, and other aspects eroding SEW (Gómez-Mejía et al., 2010). Families’ financial wealth is often concentrated in the company, making them especially careful in allocating funds (Miller & Le Breton-Miller, 2005). In addition, financial capital may be at a premium and have to be allocated more carefully (Carney, 2005). Hence, compared to counterparts with no family involvement, dispersed ownership, and external CEOs, family-managed firms are likely to be more concerned with the sustainability of their internationalization prospects, being more vigilant in their information search and calibrating their decisions to ensure both survival and preservation of control (cf. Fourné & Zschoche, 2020; Patel & Fiet, 2011; Reuber, 2016).

This, in turn, could induce them to interpret signals from the competition more cautiously. Given the more significant stakes involved in their international market entry decisions, family-managed firms are less likely to discount their own beliefs and private information based on the number of industry peers operating in international markets. Indeed, when international market entry is a product of unreflective imitation of rivals with short-term objectives, its costs can be steep (cf. Banerjee, 1992; Bikhchandani et al., 1998; Fiol & O'Connor, 2003).

Furthermore, compared to their nonfamily counterparts, family members’ stronger identification with the firm can make them view their resource endowments as distinctive (Habbershon & Williams, 1999; Sirmon & Hitt, 2003). So, while bunching behavior reinforces tacit collusion among rivals to maintain competitive resource parity (Lieberman & Asaba, 2006), family-managed firms are likely to be less eager to match the behavior of competitors and instead focus on leveraging their idiosyncratic resources and capabilities.

Finally, strategic distinctiveness combined with concentration of power and authority in the controlling family is likely to free family-managed firms, relative to their nonfamily counterparts, from the need to account for their actions to external constituencies, thereby giving them the discretion to act according to their particularistic goals (Carney, 2005). Although Miller, Le Breton-Miller, and Lester (2013) find US publicly listed family firms to display a stronger motivation to follow strategic behaviors exhibited by industry peers to gain legitimacy in the eyes of external evaluators, Mazzelli et al. (2018) show that the desire to be perceived as both distinctive and legitimate can lead family-managed firms to undertake more selective imitation strategies, thereby resisting isomorphic pressures at the broader industry level. In sum, due to lessened susceptibility to both competitive and institutional pressures, we expect these firms to be less responsive to increases in the number of international market entries among other industry players, relative to nonfamily firms.

When the number of industry peers operating in international markets increases, the likelihood of entering an international market increases less in family-managed firms than in nonfamily firms.

Family-Managed Firms’ Sensitivity to International Market Entry Outcomes

To expand internationally, many family firms want to understand thoroughly the conditions, rules, and strategies that will enable them to cope with uncertainty (Liesch & Knight, 1999; Mata & Portugal, 2002; Mitchell et al., 1994). If family-managed firms are less susceptible to the sheer number of prior international market entrants, they can also see the collective internationalizing behavior of peers as an opportunity to discover the fruits of competitors’ internationalization efforts, learn from their errors, and identify latent flaws (Chrisman & Patel, 2012; De Massis et al., 2016). Because these firms are concerned with the long-term future of the business, for example, to secure career opportunities for the family and accumulate financial wealth and SEW for later generations (Miller & Le Breton-Miller, 2005), they will be especially careful in scrutinizing the consequences of competitors’ market entry decisions. By acting as intuitive “statisticians” and observing outcomes that occurred after their peers internationalized, family managers will be more inclined to enter international markets only when such entry has clearly produced valuable returns for others.

It is also likely that family-managed firms will interpret between-firm performance variance amongst prior entrants differently from nonfamily firms. High variance in performance outcomes among prior entrants deters international market entry because it signals the impossibility of reaching competitive parity by matching rival moves, as well as a greater risk in international expansion. However, low performance variance reduces potential entrants’ ability to recognize events outside an expected range, making inference challenging (Denrell & March, 2001; Musaji et al., 2020; Oliver et al., 2017). Indeed, “When outcomes are invariant, knowledge about the parameters of prospective performance is absent” (Musaji et al., 2020, p.212). To the extent that family-managed firms see the performance of prior international market entrants as an opportunity to learn, we argue that they will see performance variance as an opportunity to differentiate between successful and unsuccessful internationalization strategies (cf. Henisz & Delios, 2001; Terlaak & Gong, 2008). Therefore, family-managed firms are likely to see performance variance among industry peers operating in international markets less negatively than nonfamily firms.

Finally, family firms’ long-term orientation is likely to elicit more prolonged inferential efforts regarding other players’ performance. We expect that not only will family-managed firms monitor outcomes after peers have internationalized, but also the performance of entrants over time, to differentiate merit from luck and identify harmful market conditions based on performance instability over time (i.e., within-firm performance variance). Such instability signals market volatility that is not controllable by a firm. We expect these family firms to exhibit heightened sensitivity to temporal variations in the performance of the industry players in international markets. In fact, such variability often indicates unwanted and unanticipated situations that increase the probability of failure (Hannan & Freeman, 1984) as well as instability in market conditions such as consumer tastes and prices, and institutional factors that impair economies of knowledge and experience in foreign markets (Henisz & Delios, 2001)—to which family firms are particularly averse (Gómez-Mejía et al., 2007; DeTienne & Chirico, 2013). The above arguments suggest that, compared to nonfamily firms, family-managed firms’ likelihood to internationalize will decrease more with increases in within-firm performance variance.

When the average within-firm performance variance of industry peers operating in international markets increases, the likelihood of entering an international market decreases more in family-managed firms than in nonfamily firms.

Family Firms’ Uncertainty Mitigation and Survival in International Markets

Wiedersheim-Paul, Olson, and Welch (1978) consider information gathering as fundamental to successful market entry abroad. We posit that more deliberation regarding imitation provides a more effective basis for inference, putting family-managed firms in a better position to reduce uncertainty and tailor their initiatives based on superior knowledge. It also avoids undue emphasis on popularity, preventing such family firms from faddish adoption lacking in an appreciation of potential benefits and dangers. Overall, we argue that family-managed firms’ heightened emphasis on SEW protection and uncertainty reduction will lead to a more thoughtful examination of external information and a more accurate estimation of international market entry potential consequences. By making more effortful inferences about the performance implications of competitors’ market entry decisions, these family firms will more effectively reduce uncertainty, delineating a range of potential performance outcomes from internationalization (Hutzschenreuter et al., 2014; Levinthal & March, 1981). Furthermore, the capacity to capture telling details will attune family-managed firms to environments and avoid overly volatile international markets (cf. Romme et al., 2010). This will result in better-timed foreign market entry decisions that increase performance reliability (i.e., minimize venturing risk) and decrease the likelihood of failure in the broached international markets (cf. Fiol & O'Connor, 2003).

Family-managed firms operating in international markets exhibit higher performance reliability than nonfamily firms.

Methods

Data

We tested our hypotheses on Spanish manufacturing firms in the ESEE (Encuesta Sobre Estrategias Empresariales or Survey on Business Strategies) database from 1999 to 2012. ESEE is carried out by the Fundacion Empresa Publica (SEPI Foundation) with the support of the Ministry of Industry of Spain. It was designed to ensure the representativeness of Spanish manufacturing firms through a stratified, proportional, and systematic approach to sampling, including all firms with more than 200 employees and a stratified random selection of firms employing 10 to 200 workers. Special attention was paid to minimizing attrition and incorporating new firms under the same sampling criteria as for the base year so that the sample remains representative of the Spanish manufacturing sector over time. The survey was designed to capture information about firms’ strategies and markets, and includes accounting data on performance. It has been used to investigate strategic decision-making in both family-managed firms (e.g., Greenwood et al., 2010; Mazzelli et al., 2018) and international markets (Almodóvar & Rugman, 2014; Cassiman & Veugelers, 2006). Our study examines the effect of family involvement on international market entry and survival—aspects neglected in prior studies using this dataset.

Dependent Variables and Econometric Methods

Hazard Rate of International Market Entry and Exit

Our dependent variable for hypotheses H1 to H4 is the hazard rate of international market entry. Consistent with our theoretical focus on international market entry decisions, we do not consider the scale of internationalization, but rather focus on firms’ initial decision to enter international markets.

More specifically, we used an event history analysis to estimate the probability that a firm changed the geographical scope of its main market from “local, provincial, regional, or domestic” to either “foreign” or “national and foreign” 2 (i.e., an international market entry event occurred) between t and t + Δt, given that it was operating in a “local, provincial, regional, or domestic” market at time t, calculated over Δt. As a consequence, those firms operating internationally from inception (543) or entering in 1999 (81) were excluded from the analyses. After constructing and lagging our variables (described below), our final sample included a panel of 2427 firms corresponding to 15,531 firm-year observations between 1999 and 2012. 537 of the firms in the final sample undertook international expansion, amongst which 213 were family-managed firms. The highest and lowest number of international market entries occurred in 2006 (70, 30 of which were family firms) and 2004 (24), respectively.

Similarly, to test hypothesis H6, we measured firm survival as the hazard rate of international market exit defined as the probability that a firm operating in an international market at time t changed its market scope to “local, provincial, regional, or domestic” (i.e., an international market exit event occurred) between t and t + Δt, calculated over Δt

In this case, all companies entering a foreign market between 1999 and 2012 (618 in total resulting in 3239 firm-year observations) were considered at risk of exit. 416 firms changed the scope of their markets from foreign to “local, provincial, regional, or domestic” over the study period, 40% of which (166) were family-managed firms. The most international market exits occurred in 2008 (123, among which 47 were undertaken by family-managed firms), probably under the effects of the 2007–2008 financial crisis.

Estimating hazard rates requires assumptions about the effect of time or duration on event probability. We split time into annual spells and used a semi-parametric Cox proportional hazard model, in which the underlying distribution of hazard rates is left unspecified. In general, the Cox model is viewed as conservative, which helps to avoid misspecification while allowing for time-varying covariates (Allison, 1995; Kleinbaum & Klein, 1996). Furthermore, because some firms experienced multiple international entries and exits over the study period, in addition to treating our observations as right-censored, we adopted the counting process approach of Andersen and Gill (1982) to adjust for the multi-episodic nature of entry and exit events (Ezell et al., 2003).

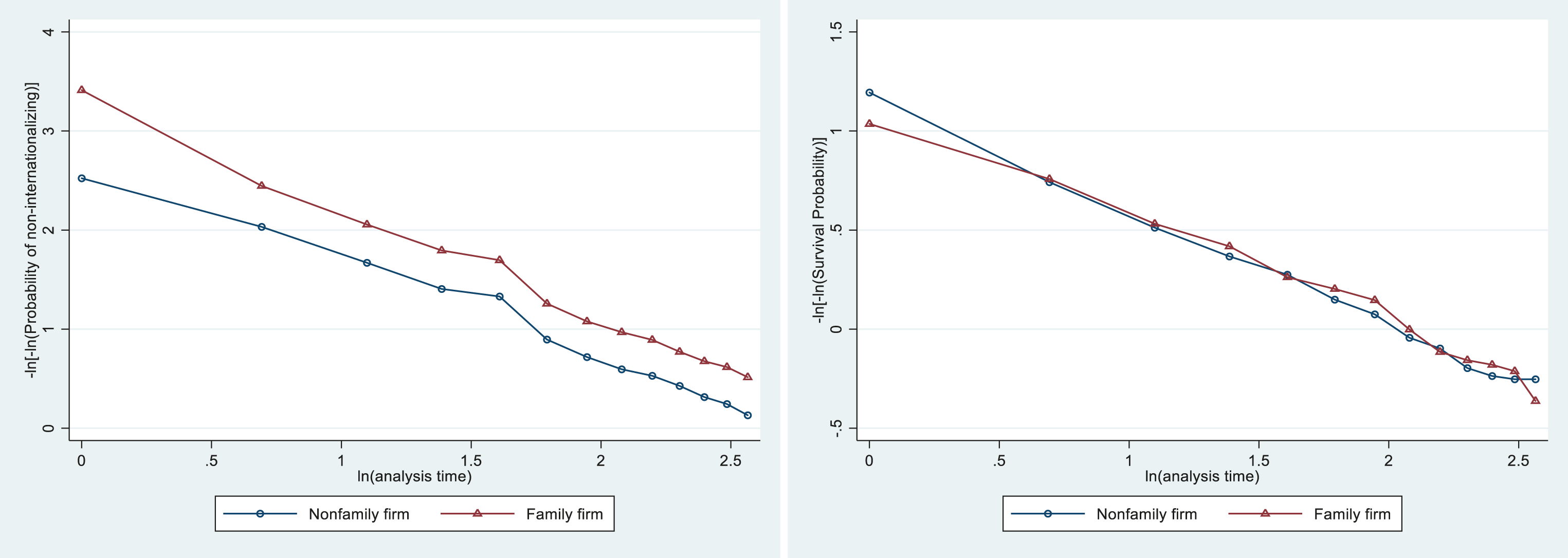

To assess the appropriateness of the Cox model, we first tested the proportional hazard assumption by comparing Kaplan–Meier curves between family and nonfamily firms in our sample. As Figure 1 illustrates, the two curves are almost parallel, thereby confirming that, at any point in time, the ratios of the entry and exit hazard functions in the group of family-managed firms to the corresponding hazard functions in the group of nonfamily firms are constant.

3

Kaplan–Meier curves and predicted survival plots for family and nonfamily firms.

The decision to enter international markets is endogenous and self-selected. However, the traditional two-step Heckman’s correction cannot be applied in survival models. Thus, to generate consistent estimators of the population parameters in the presence of a biased sample, we followed Pan and Schaubel (2008) and used an inverse probability (IP) weighted Cox model to estimate the hazard rate of international market exit. Its purpose is to weigh each firm by the reciprocal of the probability of being sampled (i.e., entering international markets). This approach corrects for selection bias by removing the association of international market entry with the covariates used in the analysis of international market exit. For example, if family-managed firms are less likely to internationalize than nonfamily firms, then family-managed firms entering a foreign market are up-weighted. We implemented this estimation strategy following a two-stage procedure. At the first stage, we ran a logistic regression to estimate international market entry probability at the firm level. In particular, we included all the control variables described below as well as the family firm variable. At the second stage, an IP-weighted Cox model was fit by weighting firms according to the inverse of their estimated probabilities from stage 1. The estimated weights had a mean of 1.02 and a SD of 0.05. Finally, to account for the potential dependence of observations of the same firm as well as for the fact that IP weights were estimated, we used robust standard errors clustered by firm.

Performance Reliability

To measure performance reliability (H5), we adopted a multiplicative heteroskedasticity approach allowing for the simultaneous estimation of the effects of covariates on the mean and variance of firm performance (cf. Chrisman & Patel, 2012; Mazzelli et al., 2019; Sorenson & Sørensen, 2001). As an indicator of firm performance, we used return on assets (ROA). ROA reflects the effective use of firm assets to generate income and is one of the most commonly used measures of profitability in the literature since it is relatively insensitive to differences in capital structure (Williamson & Cable, 2003). The multiplicative heteroskedasticity model parametrizes the error term ε

i,t

as a function of a vector of covariates Xi.t-1, which has been assumed to include the same factors used to estimate performance mean Yi,t, and a random term ui,t

The linear model for the mean of the dependent variable Yi,t (cf. Gedajlovic & Shapiro, 2002) and the log-linear model for the variance (εi,t) are estimated simultaneously using maximum likelihood methods (Greene, 1997). The Γ parameter capture the effects of Xi,t-1 on the logarithm of the variance of firm performance. Hence, factors that increase performance reliability should have Γ<0; whereas those decreasing performance reliability should have Γ>0. Following Wooldridge (2002), we extended the original cross-section specification of the multiplicative heteroscedasticity model to a panel data setting using the command xtreghet in Stata 15 (Chrisman & Patel, 2012).

To capture endogeneity effects and correct for selection bias, we adopted Heckman’s (1979) two-stage procedure: we computed the inverse Mills ratio based on the residuals of a first stage probit model predicting entry probability. This model showed a statistically significant negative association between the family variable (described below) and international market entry probability (−0.479, p = .006). Hence, we incorporated the estimated inverse Mills ratios into the performance mean equation of the multiplicative heteroskedasticity model. Our correction for endogeneity proved not to be statistically significant. 4

Independent Variables

Family Firm Measures

Consistent with prior literature, we used both a binary measure of family firm and a continuous measure of family influence. Our family firm measure distinguished family firms from nonfamily firms based on family involvement in both firm ownership and management (cf. Greenwood et al., 2010). Specifically, a firm was coded as 1 when owners and their family members were active in managing the focal firm. All firms that did not have either the owner or his/her relatives in the top management team were considered nonfamily firms and coded as 0 (Greenwood et al., 2010). For the continuous measure of family influence we counted the number of owners and owner relatives occupying top managerial positions in year t in firms where the family involvement in ownership and management criterion was met (e.g., Chrisman & Patel, 2012; Kotlar & De Massis, 2013).

Number of Prior Entrants

The number of local entrants into a foreign market was calculated as the number of other firms operating in the focal firm’s industry in year t-1, having broached a foreign market between year 1999 and t-1, and indicating the scope of their main market as “foreign” or “national and foreign” in year t-1.

Prior Entrants’ Performance Mean

To measure the performance of industry peers operating in international markets, we first calculated the return on assets (ROA) in year t-1 of each firm in our sample. Hence, we averaged the ROA of all other firms operating in the same industry as the focal firm whose main market scope was either “foreign” or “national and foreign” in year t-1.

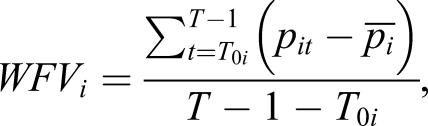

Prior Entrants’ Between-Firm Performance Variance

We measured the between-firm variance of industry peers’ international performance, by computing the variance of the ROAs of firms operating in international markets in year t-1 and belonging to the same industry as the focal firm, according to the following formula:

Prior Entrants’ Within-Firm Performance Variance

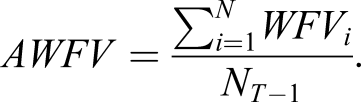

To measure the average within-firm variance of industry peers’ international performance, for each industry peer operating in international markets in year t-1, we calculated the temporal variance of performance between the year of international market entry and year t-1, according to the following formula:

Control Variables

We used a series of time-varying and time-constant controls at the firm and market levels. We also included year dummies in all the models to control for the effects of time periods on international market entry, performance reliability, and survival.

Firm-Level Controls

Since firm characteristics affecting international expansion could also influence survival in the broached international markets, we included a series of control variables. Age was the number of years since incorporation. Firm Size was measured by the log of total sales in year t-1. In addition to performance and slack at entry, we controlled for organizational performance (i.e., ROA) and slack in year t-1 measured as the standardized mean of absorbed slack (working capital to sales ratio), unabsorbed slack (current assets to current liabilities ratio) and potential slack (equity to debt ratio) (George, 2005; Mitchell et al., 1994). We also controlled for the focal firm’s strategic profile and budget allocation history. We also included R&D intensity measured as the ratio of R&D total expenditure to total sales in year t-1; Advertising intensity as the ratio of marketing and advertising expenditure to total sales in year t-1; and Capital intensity as the ratio of investment in PPE to total sales in year t-1. Since scale-efficient production capacity has been found to enhance survival (Garcia-Sanchez et al., 2014), we controlled for capacity utilization measured as the average percentage during year t-1 of standard capacity usage. We also controlled for international patents registered abroad in year t-1 and the geographical dispersion of production facilities. Geographic dispersion was computed as an entropy index,

Market-Level Controls

Market uncertainty can affect the decision to internationalize, choice of imitation mode (Henisz & Delios, 2001), and success at international market entry (Rhee & Cheng, 2002). Thus, we included market uncertainty measured as the change in the industry concentration ratio accounted for by the four largest firms between year t-2 and t-1 in the models for international market entry, and between year t-1 and t in the models predicting performance reliability and international market survival. We also controlled for market concentration in year t-1, using the four-firm concentration ratio as a proxy for sunk costs, entry barriers, and competition. This variable has been used in prior studies investigating international market entry and survival (e.g., Mitchell et al., 1994; Patel et al., 2018). Mitchell et al. (1994) stated that the concentration ratio provides a joint estimate of both the existence of significant sunk costs and entry barriers created by successful incumbents (1994, p. 561). Patel et al. (2018) used the concentration ratio as an indicator of monopoly-like conditions.

Results

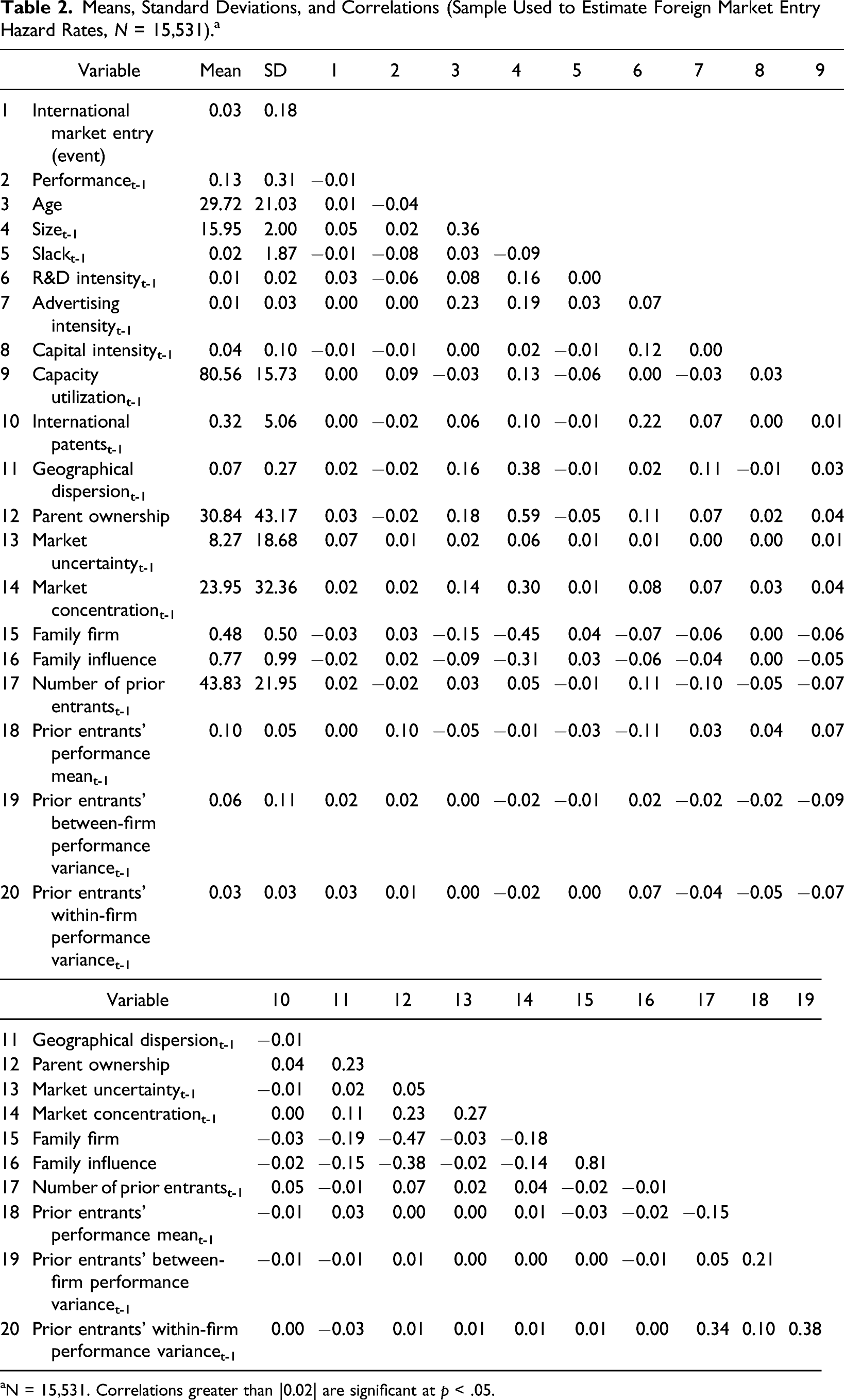

Means, Standard Deviations, and Correlations (Sample Used to Estimate Foreign Market Entry Hazard Rates, N = 15,531). a

aN = 15,531. Correlations greater than |0.02| are significant at p < .05.

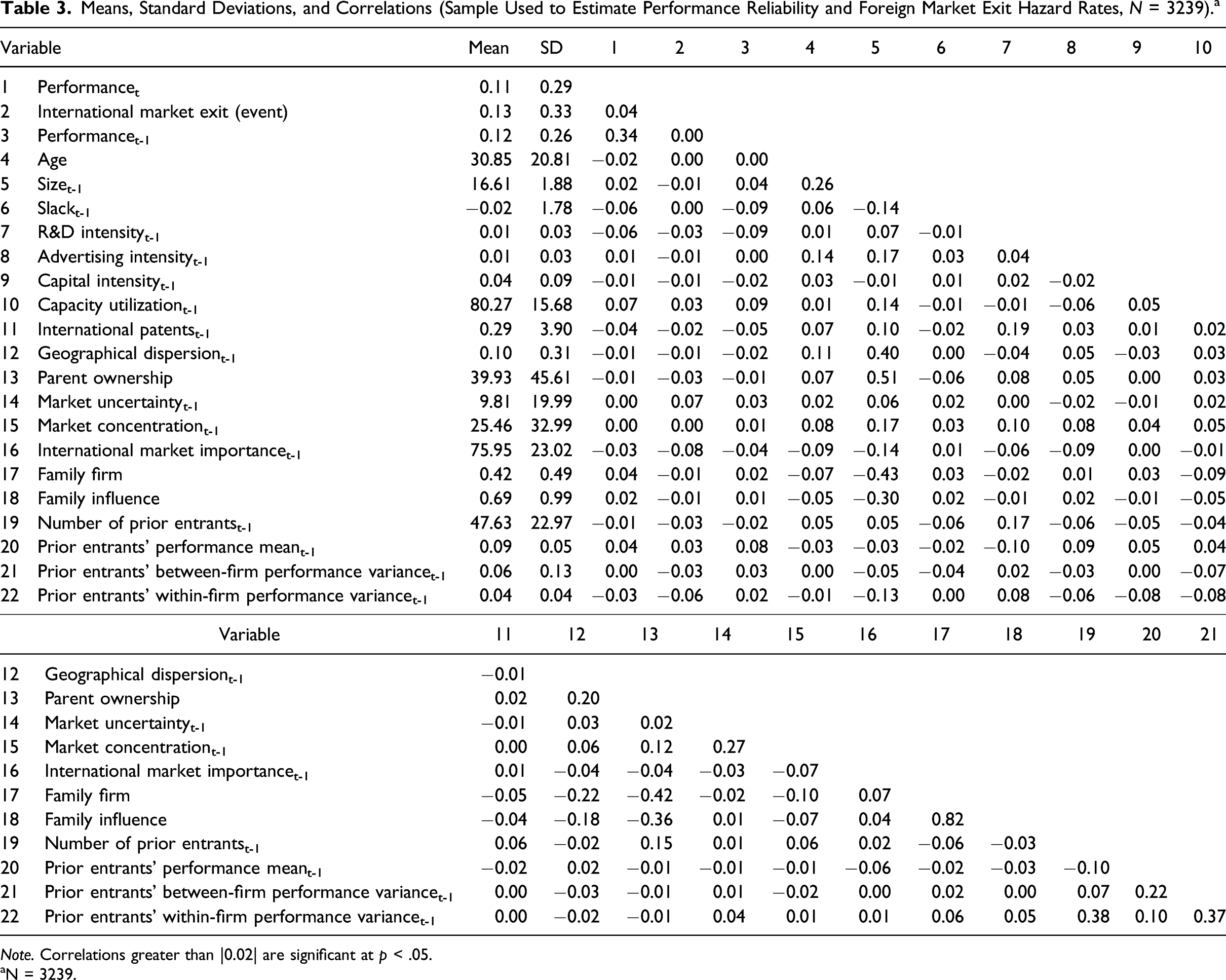

Means, Standard Deviations, and Correlations (Sample Used to Estimate Performance Reliability and Foreign Market Exit Hazard Rates, N = 3239). a

Note. Correlations greater than |0.02| are significant at p < .05.

aN = 3239.

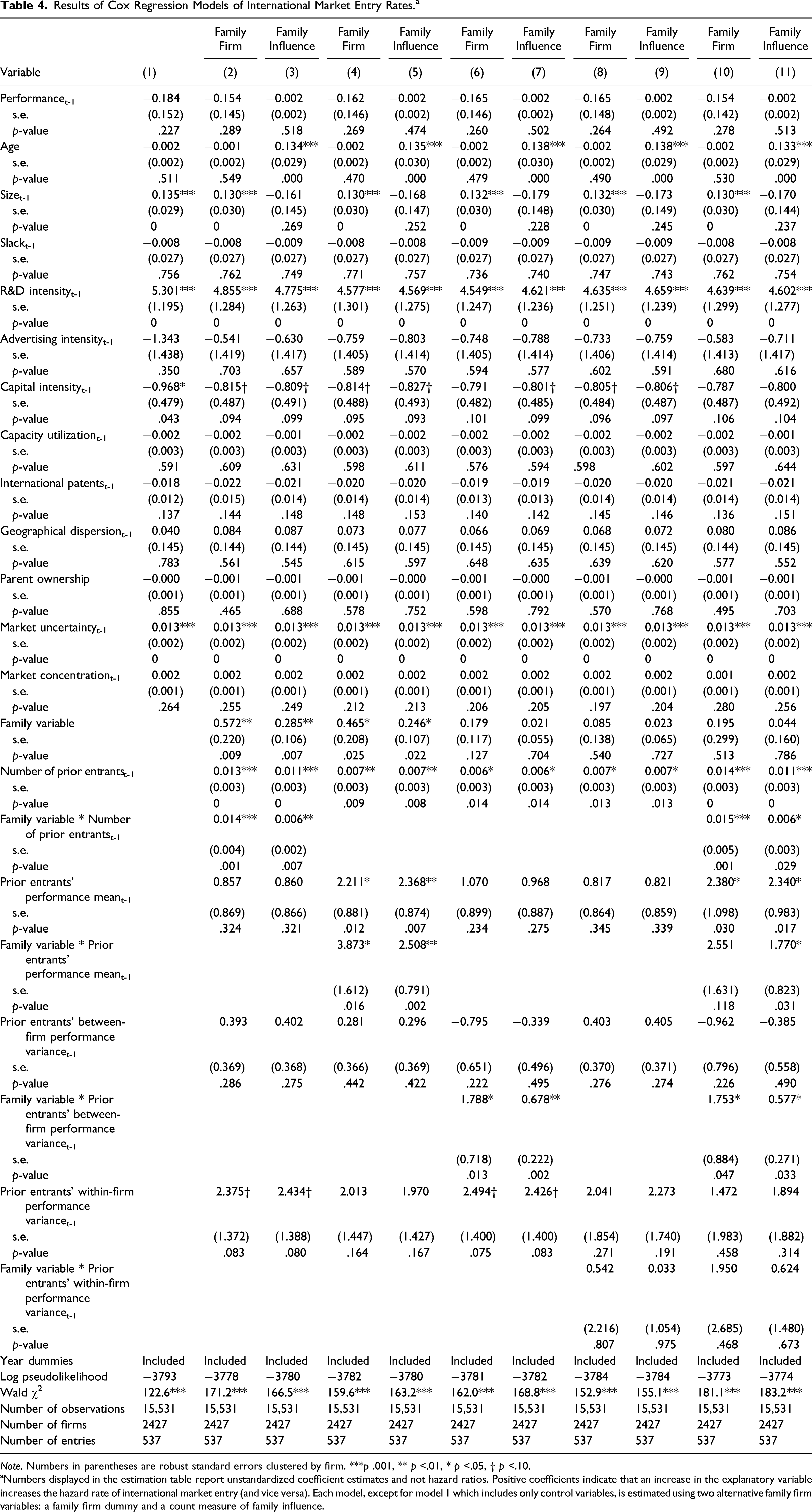

Results of Cox Regression Models of International Market Entry Rates. a

Note. Numbers in parentheses are robust standard errors clustered by firm. ***p .001, ** p <.01, * p <.05, † p <.10.

aNumbers displayed in the estimation table report unstandardized coefficient estimates and not hazard ratios. Positive coefficients indicate that an increase in the explanatory variable increases the hazard rate of international market entry (and vice versa). Each model, except for model 1 which includes only control variables, is estimated using two alternative family firm variables: a family firm dummy and a count measure of family influence.

We find support for Hypothesis 1. As shown in Model 2, the coefficient estimate for the interaction between the family firm variable and the number of prior entrants (β = −0.014, p = .001) is negative and significant. Family-managed firms are 69% ([0.54–1.77]/1.77 ≈ −69%)

5

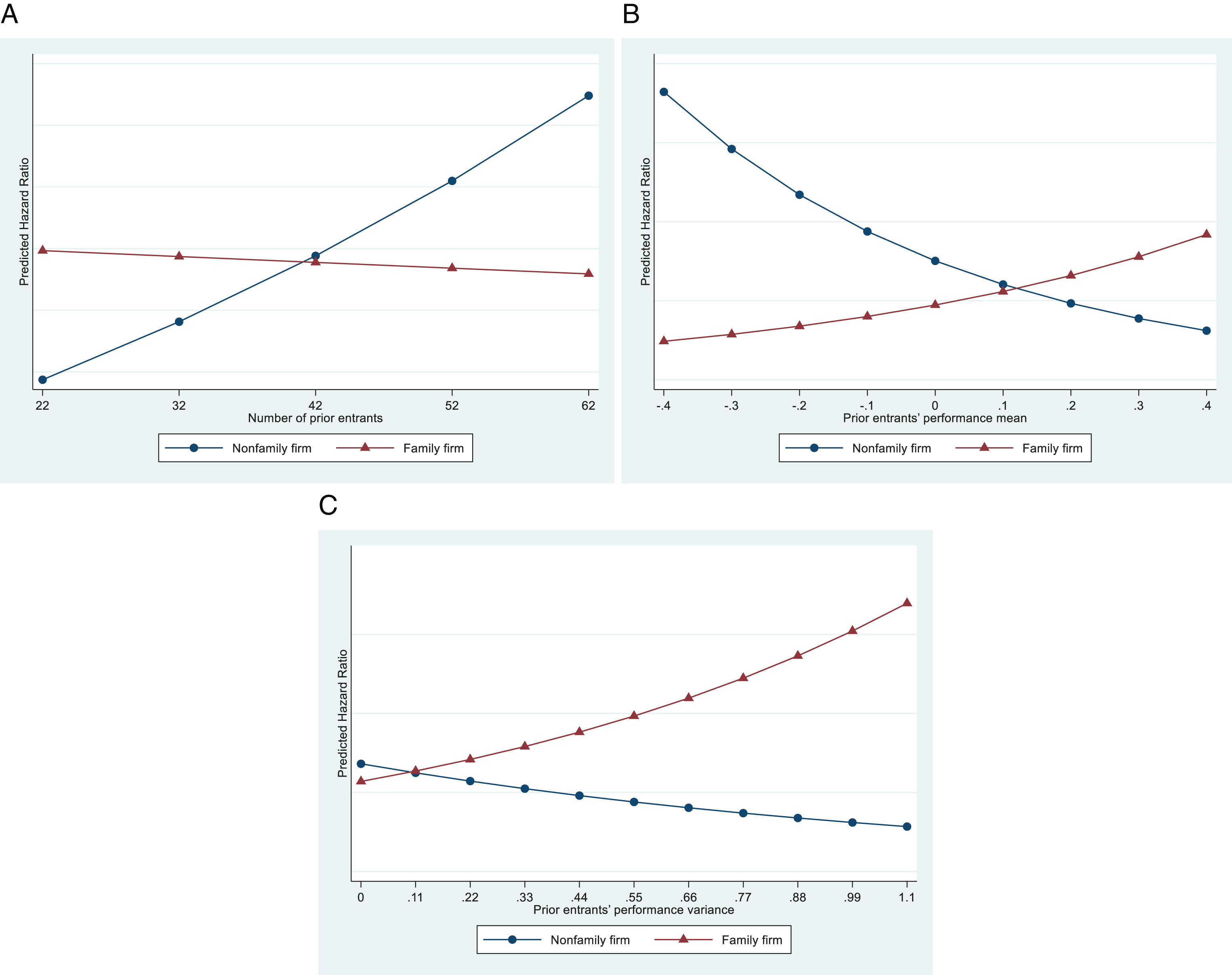

less likely than nonfamily firms to enter an international market as the number of industry peers operating in international markets increases from one SD below to one SD above the mean. Figure 2a illustrates the marginal effects of the number of prior entrants on the hazard ratios of entry in family versus nonfamily firms. Although there is no significant relationship between the number of industry players in international markets and the probability of entry among family-managed firms, the relationship is positive and significant among nonfamily firms. Hence, family-managed firms are less susceptible to pressures from the frequency of international market entries compared to their nonfamily counterparts. This finding is also supported when using the continuous measure of family influence in Model 3 (β = −0.006, p = .007). Marginal Effects of (A) Number of prior entrants, (B) Prior entrants’ Performance Mean, and (C) Prior Entrants’ Between-Firm Performance Variance on the Hazard Ratios of International Market Entry of Family versus Nonfamily Firms.

Hypothesis 2 proposes that the better the performance of industry peers that have expanded internationally, the more likely it is that family-managed firms will internationalize vis-à-vis nonfamily firms. The interaction term between the family firm variable and the prior entrants’ performance mean variable in Model 4 is positive and statistically significant (β = 3.873, p = .016). Yet, statistical significance is lost in the full model (Model 10). However, the coefficient for the interaction term remains significant in the full model when adopting a continuous measure of family influence (Model 5: β = 2.508, p = .002; Model 11: β = 1.770, p = .031). Figure 2b illustrates the marginal effects of prior entrants’ performance mean on the hazard ratios of international market entry in family versus nonfamily firms. Family firms are 88% ([1.49–0.79]/0.79 ≈ 88%) 6 more likely to internationalize as the performance of industry peers operating in an international market increases from one SD below to one SD above the mean. Surprisingly, the effect of prior entrants’ performance mean on nonfamily firms’ likelihood to enter an international market is negative.

Hypothesis 3 predicted that compared to nonfamily counterparts, family-managed firms’ market entry would be less diminished by increases in performance variance among prior entrants. Models 6 and 7 found support for the hypothesis, under the binary family firm variable (β = 1.788, p = .013) and continuous family influence variable (β = 0.678, p = .002). However, As Figure 2c illustrates, the relationship between prior entrants’ between-firm performance variability and the probability of international market entry is positive, not negative, among family-managed firms. A family-managed firm’s likelihood of international market entry increases by 20 percentage points (pp) (1.11–0.91 = 0.20) as prior entrants’ performance variance increases from one SD below the mean (hr = exp (1.79*[0.06–0.11]) = 0.91) to the mean (hr = exp (1.79*[0.06+0.11]) = 1.11), and increases by 24 pp as it increases from the mean to one SD above it (hr = exp (1.79*[0.06+0.11]) = 1.35). In contrast, nonfamily firms’ likelihood of international market entry decreases by 17 pp (0.87–1.04 = −0.17) as prior entrants’ performance variance increases from one SD below (hr = exp (-0.79*[0.06–0.11]) = 1.04) to one SD above the mean (hr = exp (-0.79*[0.06+0.11]) = 0.87). This, in turn, results in family-managed firms being 78% ([1.49–0.84]/0.84 ≈ 78%) 7 more likely to enter international markets as the variance of firm performance across industry peers operating in foreign markets in year t-1 increases from one SD below to one SD above the mean. Conversely, we did not find evidence supporting Hypothesis 4 that family-managed firms are less likely, relative to their nonfamily counterparts, to enter international markets in response to the increasing temporal instability (i.e., within-firm performance variance) of prior entrants’ performance.

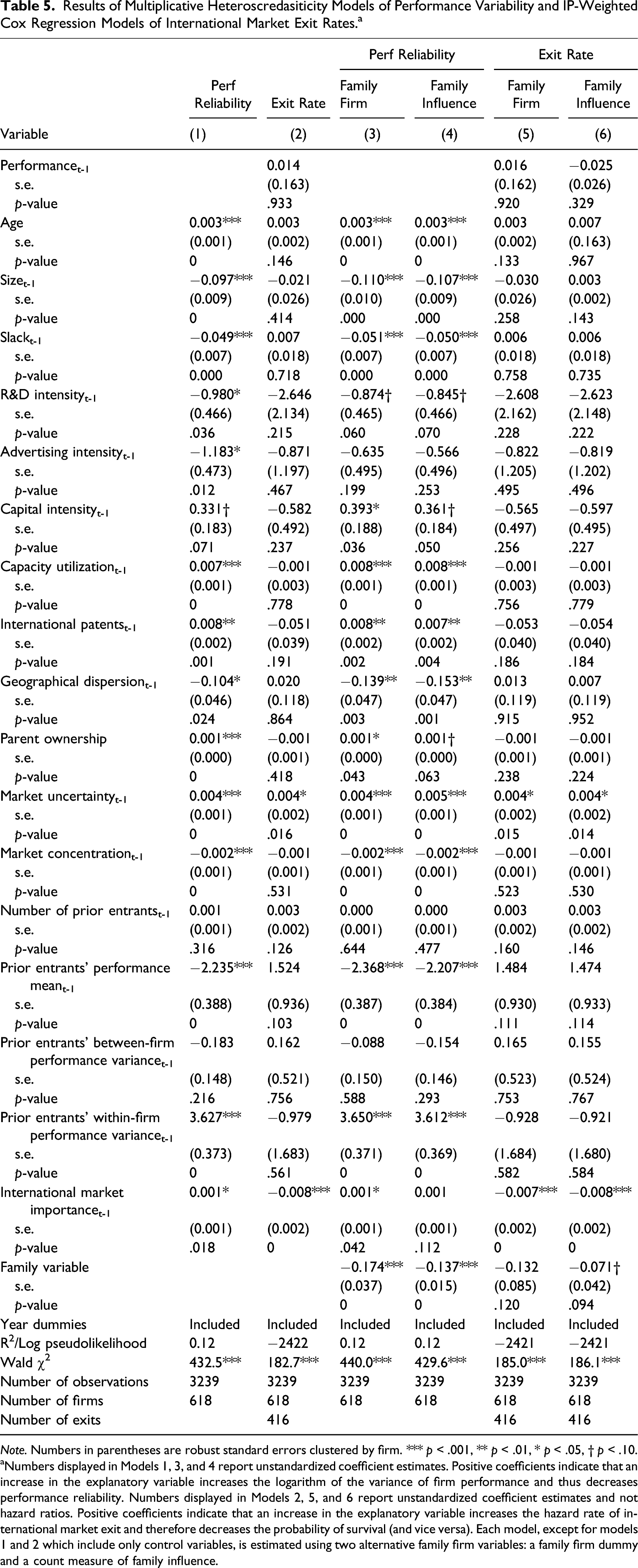

Results of Multiplicative Heteroscredasiticity Models of Performance Variability and IP-Weighted Cox Regression Models of International Market Exit Rates. a

Note. Numbers in parentheses are robust standard errors clustered by firm. *** p < .001, ** p < .01, * p < .05, † p < .10.

aNumbers displayed in Models 1, 3, and 4 report unstandardized coefficient estimates. Positive coefficients indicate that an increase in the explanatory variable increases the logarithm of the variance of firm performance and thus decreases performance reliability. Numbers displayed in Models 2, 5, and 6 report unstandardized coefficient estimates and not hazard ratios. Positive coefficients indicate that an increase in the explanatory variable increases the hazard rate of international market exit and therefore decreases the probability of survival (and vice versa). Each model, except for models 1 and 2 which include only control variables, is estimated using two alternative family firm variables: a family firm dummy and a count measure of family influence.

Hypothesis 6 predicted that family-managed firms would survive longer than nonfamily firms in their international markets—therefore, exhibiting a lower likelihood of exit. It was not supported. Although the coefficient for the family firm variable in Model 5 is in the hypothesized direction, it is not statistically significant (β = −0.132, p = .120). Marginal support for Hypothesis 6 was found when adopting a continuous measure of family influence as shown by the negative and marginally significant coefficient for family influence in Model 6 (β = −0.071, p = .094). This suggests that, as the number of family members in the top management team increases by one unit, the likelihood of foreign market exit decreases by approximately 7 pp.

Robustness Analyses

Because power imbalances within the family coalition could affect family influence on decision-making and hamper heedful interaction, we included a variable for the diversity of the positions held by family members in the models predicting post-entry outcomes. We measured family power disparity using a variation of the Gini’s index, computed as:

Discussion

Whereas much of the literature on family firms’ internationalization focuses on whether they are more or less willing to internationalize than others (Gómez-Mejía et al., 2010), we focus on when they are more likely to do so, specifically the conditions making family-managed firms more willing to internationalize. Recognizing that uncertainty is a major factor in international expansion (e.g., Gomez-Mejia et al., 2010; Henisz & Delios, 2001), our study suggests that interpretation of information from other industry players entering international markets is a key influence on how family versus nonfamily firms deal with uncertainty. Moreover, we show that family and nonfamily firms differ in the type of information they use in international entry decisions. Our results suggest that family firms are likely to rely on uncertainty-mitigation strategies that are more effortful, patient, and deliberate than those of nonfamily firms—which, in turn, lead to more effective uncertainty reduction and greater performance reliability post entry. Taken together, these findings have important implications for family firm strategic decision-making as well as broader areas of research.

Implications for Family Business Literature

Scholars often view SEW as a factor preventing the international expansion of family firms. Whereas there is evidence supporting this view, prior studies overlooked the critical role of uncertainty in family firms’ international market entry decisions. Uncertainty reduction takes place to evaluate possible outcomes of these decisions, especially when both financial and socioemotional wealth is at stake. Family-managed firms’ heightened preoccupation with SEW losses may induce them to increase the accuracy of their decisions by herding less than their nonfamily counterparts and focusing more on learning vicariously from other industry players’ international entry performance. In so doing, our results also suggest that family-managed firms’ international expansion decisions carefully monitor others’ decision consequences (Patel & Fiet, 2011), which some have implied family firms to neglect (cf. Nason et al., 2019). This, in turn, may protect them from entry bandwagons requiring reversal, making for more reliable performance and longer survival in foreign markets. Taken together, our findings suggest that a focus on information search and processing can provide a valuable addition to understand family firms’ strategic choice under uncertainty.

Accordingly, prior findings of limited international market entry in family firms - but also limited diversification (Gómez-Mejía et al., 2010) and technology adoption (Souder et al., 2017) hitherto attributed to SEW loss aversion might instead be due to more careful and deliberate inferential processes in family firms. Supporting this view, our results suggest that family-managed firms’ strategic choices are highly dependent on the level and nature of uncertainty surrounding the specific situational context: for instance, when the performance of prior entrants is strong enough to signal the promise of international market entry, these firms become even more likely to enter than nonfamily firms. Put differently, family firms might be less psychologically biased than the SEW perspective and the behavioral agency model tend to suggest. More broadly, our theory and results extend the behavioral agency model predictions of family firm behavior by introducing important and so far not considered decision rules adopted by family-managed firms to protect their SEW, which are based not only on risk but also on uncertainty.

Importantly, whereas most empirical studies in this literature focus on family firms’ willingness to internationalize (with a few exceptions, e.g., Fang et al., 2018), we advance this research by theorizing and testing the differential effects of family involvement in firm ownership and management on post-entry outcomes. Overall, our study opens up several opportunities to further explore the uncertainty mitigation strategies that family firms adopt pre-entry, versus their unique competitive positioning at entry, potential sunk cost bias, or superior adaptative strategies.

Implications for the Literature on Imitation

Our study also contributes to the literature on interorganizational imitation in economics and institutional sociology. While parallel research streams have theorized different imitation modes with distinct underlying motivations and mechanisms, they rest on the common assumption that uncertainty drives imitation (Lieberman & Asaba, 2006). Existing integrative attempts have thus focused on how different types of uncertainty differentially influence firms’ reliance on imitation and the choice of imitation mode (e.g., Gaba & Terlaak, 2013; Haunschild & Miner, 1997; Henisz & Delios, 2001). Implicit in this treatment, however, is an assumption that firms’ behaviors tend to be homogenous within uncertainty types.

Although organizational characteristics are frequently incorporated as control variables in models of imitation, their role as a potential source of heterogeneity in firms’ inferential efforts and susceptibility to social influences has received little explicit theoretical attention or empirical investigation (cf. Naumovska et al., 2021). The few available studies examining firm differences as a source of heterogeneity in imitation processes focus on structural aspects that facilitate information access—such as position in network structures (e.g., Kraatz, 1998). In contrast, save for a few exceptions (i.e., Fourné & Zschoche, 2020; Mazzelli et al., 2018), scant attention has been devoted to understanding how goals, motives, and strategic priorities specific to different owners and managers affect information search and processing processes firms use to mitigate uncertainty. Our results show that the choice of imitation mode is affected significantly by family coalitions, opening avenues for more nuanced explorations of the relationship between uncertainty and imitation across firms.

Limitations and Suggestions for Future Research

Of course, our study is subject to limitations. First, we have examined one type of decision in one nation and manufacturing industries only, thus our findings may be bound to the legal, cultural, and institutional context. Second, our international market entry dummy variable does not capture important variations across foreign markets, such as its geographic or cultural distance from the home market. Prior studies found little heterogeneity in the international markets entered by Spanish manufacturing firms, most being UE–15 member states (Observatorio de la Empresa Multinacional Español (OEME), 2008). Moreover, the sector in which Spanish firms operate is the very primary driver of their international target markets (Caldera, 2010). However, we encourage scholars to directly measure foreign market variations in future investigations. Third, our analyses capture only the activities of Spanish competitors. However, international market entry decisions may also be influenced by what key international competitors do. Fourth, like the majority of studies in both the family business literature (e.g., Chrisman & Patel, 2012; Gómez-Mejía et al., 2007, 2010) and the imitation literature (e.g., Gaba & Terlaak, 2013; Haunschild & Miner, 1997; Henisz & Delios, 2001), we inferred aspects related to information search and processing processes from behavioral outcomes. More importantly, we assumed international market entry to be a voluntary decision and imitation as involving a certain degree of deliberateness. Future research on imitation should validate this assumption using primary data to measure deliberation in information processing (e.g., using text analysis or experiments), thereby providing more direct tests of our arguments and their boundary conditions. Outcome-based imitation may be reflected in many other decision contexts such as new technology adoption, new product introductions, new market positions. We thus expect that further insights will emerge when applying our theory to these settings. Outcome-based imitation could be less advantageous in contexts where first movers gain significant competitive advantages.

Finally, our findings on the effects of power disparity on international market entry and its outcomes underscore the heterogeneity of family firms. Different ownership and governance structures, as well as the involvement of later generations, may either exacerbate or dampen some of the motivations underlying outcome-based imitation. For example, lone-founder firms have been found to undertake more farsighted and risky behaviors than traditional family firms, perhaps reflecting their tolerance of uncertainty. Unfortunately, our definition of family firms does not allow us to differentiate between family-controlled and lone-founder-controlled firms. Furthermore, it treats firms with multiple, potentially controlling family owners but without family managers as nonfamily firms, thus potentially excluding some family-owned firms. Therefore future research should replicate our study using different definitions of family firms and investigate the differential effects that uncertainty may have on the choice of imitation mode across different types of family firms.

Relatedly, we are not able to fully differentiate between exits that were voluntary—due to anticipation of future performance declines and/or the identification of more lucrative opportunities—and exits that were the result of involuntary failures—due to unfit firms succumbing to selection forces. Delving more into this issue is important to understand whether family firms’ lower exit rates reflect a weak disposition towards pursuing alternative opportunities (e.g., sunk cost bias), or simply a better fit with the broached international market.

In summary, this study provides new theory and evidence on how family-managed firms make international market entry decisions using outcome-based modes of imitation as an uncertainty mitigation strategy. We hope that the inferential processes explored by our study will guide further examinations of family firms’ decisions under uncertainty and encourage family-managed firms to make internationalization decisions that thoroughly consider and parse signals and threats from their environment.

Footnotes

Acknowledgments

We are grateful to the Editor James J. Chrisman and three anonymous reviewers for their insightful comments and suggestions throughout the review process. We would also like to acknowledge the helpful comments provided on early versions of the manuscript by Michael Frese and Jess Chua. Thanks are also due to the conference participants at the 77th Annual Meeting of the Academy of Management in Atlanta.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.