Abstract

We integrate opportunity evaluation reasoning with affordance theory to develop a nuanced theoretical model of action orientation in entrepreneurial decision-making. We test our model with a conjoint experiment of 864 decisions made by 54 corporate venture capital (CVC) managers evaluating digital ventures for investment. Our findings provide evidence that CVC managers value two sources of digital affordances: the recombinability and the reprogrammability of digital technologies. The results show that CVC managers individuate affordance-based investment opportunities based on their personal and organizational background. We contribute to a fine-grained understanding of action potentials in the evaluation of opportunities and advance affordance theory through a cognitive judgment perspective.

Keywords

Introduction

The understanding of opportunity evaluation—that is, the decision of “whether or not a specific set of circumstances represents an opportunity for me or my firm” worth pursuing (Wood & Williams, 2014, p. 576)—is central to entrepreneurship literature. In fact, the evaluation of an opportunity as attractive for its pursuit has been conceptualized as the decision that precedes entrepreneurial action (McMullen & Shepherd, 2006; Shane & Venkataraman, 2000).

The belief of actors about opportunity attractiveness depends fundamentally on the assessment of anticipated outcomes resulting from the prospective exploitation of the opportunity (Haynie et al., 2009; Tumasjan et al., 2013). Under this consideration, an important stream of research has employed the resource-based view (Barney, 1991), studying how entrepreneurial agents evaluate opportunity characteristics that potentially give rise to future resource gains (Haynie et al., 2009; Wood & Williams, 2014). However, while the resource-based view has considerably advanced our understanding about the anticipated gains in future-oriented opportunity evaluations, it does not provide sufficient explanation for concrete action potentials arising from opportunities (D’Oria et al., 2021; Kraaijenbrink et al., 2010). Thus, as Wood and McKelvie (2015, p. 271) point out, “we are in need of greater specificity about what actions entrepreneurs think about as they develop future-oriented cognitive representations of the possible effects of taking action.” Advancing the understanding about action orientation in opportunity evaluation decisions is crucial as entrepreneurial activity is ultimately an action-formation process (Autio et al., 2013; Schade & Schuhmacher, 2022).

Affordance theory offers an intriguing lens to examine action orientation in the evaluation of opportunities. Affordances refer to action potentials that arise from the relation between an object (i.e., technology) and a goal-oriented actor (i.e., individual or organization) (Gibson, 1977; Nambisan et al., 2019; Strong et al., 2014). Fundamental to affordance theory is the understanding that the action potential of an object does not arise exclusively from its technological features, but rather from its relation to an actor (Majchrzak & Markus, 2013). To achieve goal-directed outcomes, affordances have to be realized—a process that is understood as “affordance actualization” (Strong et al., 2014). While scholars have studied the emergence of affordances and processes associated with actualizing affordances (e.g., Henningsson et al., 2021; Malhotra et al., 2021), we lack an understanding of how individual actors deem affordances as worthwhile to pursue their actualization and translate them into concrete outcomes. Integrating opportunity evaluation reasoning with affordance theory, we theorize that entrepreneurial agents assess affordances as decision cues in their opportunity evaluation. Specifically, building upon the future-oriented judgment perspective (Haynie et al., 2009), we theorize that entrepreneurial agents consider outcomes of prospective affordance actualization (i.e., outcomes of acting upon affordances). That is, entrepreneurial agents envision and assess the potential benefits arising from the successful actualization of affordances after opportunity exploitation. The judgment of whether an opportunity is attractive to act upon is an interpretive process that depends on the cognitive representations of entrepreneurial agents (Gruber et al., 2015; Mitchell & Shepherd, 2010; Williams & Wood, 2015)—a phenomenon that Wood et al. (2014) refer to as opportunity individuation. Accordingly, we reason that entrepreneurial agents differ in their evaluation of affordances based on their personal and organizational background as two major influences on their cognitive judgment process (Shepherd et al., 2015).

We test our theorization by examining investment opportunity evaluations of corporate venture capital (CVC) managers. Thus far, research has extensively studied antecedent factors (e.g., Anokhin et al., 2016; Basu et al., 2011; Gaba & Meyer, 2008) and innovation benefits of CVC investments (e.g., Dushnitsky & Lenox, 2005; Smith & Shah, 2013; Wadhwa & Kotha, 2006). However, fewer studies have investigated how CVC investment decisions are made. Specifically, we lack knowledge on how CVC managers—acting as corporate entrepreneurial agents (Basu et al., 2016; Dokko & Gaba, 2012)—evaluate ventures as investment opportunities. In essence, a CVC investment opportunity represents an opportunity for the pursuit of a corporate entrepreneurial activity, allowing incumbent firms to collaborate with new ventures and thereby infuse entrepreneurial inventions and abilities into business units of the corporate parent (Sharma & Chrisman, 1999). Therefore, we theorize that CVC managers evaluate affordances arising from the relation between their corporate parent and the venture’s technology to determine the attractiveness of an investment opportunity. In light of the ever-increasing and industry-agnostic aspirations for digital transformation (Amit & Han, 2017), we examine digital affordances (Autio et al., 2018; Henningsson et al., 2021)—that is, affordances arising from the redeployment potential of digital technologies—as structural components of opportunity characteristics. In fact, affordances theory has been described as native to digital technologies (Nambisan et al., 2019), and has therefore mostly been applied to the context of digital entrepreneurship to date. We examine two specific technological characteristics as sources of digital affordances that CVC managers potentially consider in their evaluation of investment opportunities: the recombinability and the reprogrammability of ventures’ digital technologies (Kallinikos et al., 2013; Nambisan, 2017). Recombinability describes the capacity of a digital technology to be combined with other digital and physical artifacts of the CVC parent to produce synergies and new opportunities (Nambisan, 2017; Yoo, 2013). Reprogrammability refers to the potential of a digital technology to be modified and thereby repurposed to new use cases for the CVC parent (Kallinikos et al., 2013). Due to the flexible redeployability arising from these characteristics (Leonardi, 2011), we contend that how CVC managers envision the prospective outcomes of future digital technology adoption is central to their evaluation of investment opportunities. Linking affordance theory with arguments from opportunity individuation literature, we argue that CVC managers evaluate digital affordances differently as a result of their digital technology experience (Gruber et al., 2015), entrepreneurial experience (Walske & Zacharakis, 2009; Warnick et al., 2018), and CVC unit’s dependence on business units (Souitaris & Zerbinati, 2014). We test our hypotheses using a conjoint experiment of 864 evaluation decisions by 54 CVC managers from 44 CVC units and 34 industries (Shepherd & Zacharakis, 1999). To examine differences among CVC managers, we complement our insights with data from a post-experimental survey capturing information on their personal and organizational background.

Our study offers four contributions. First, we propose an affordance-based model of opportunity evaluation. Concretely, our theorization and findings suggest that entrepreneurial agents base their opportunity evaluation decisions on the consideration of affordances (i.e., relational action potentials) as structural components of opportunity characteristics. Our affordance-based theorization provides a nuanced understanding about specific action paths that entrepreneurial agents envision upon prospective opportunity exploitation. This insight is essential for the profound understanding of action orientation in entrepreneurial decision-making (Wood & McKelvie, 2015). Second, we advance affordance theory through a cognitive judgment perspective. Building upon opportunity individuation literature (Wood et al., 2014), we theorize and find that actors evaluate affordances differently depending on how they cognitively envision and assess outcomes resulting from prospective affordance actualization. This advancement is central to affordance theory, as it can explain why some affordances are actualized and produce concrete outcomes while others are never pursued (Strong et al., 2014; Volkoff & Strong, 2018). Third, we translate recombinability and reprogrammability—two affordance-enabling characteristics introduced by information systems (Kallinikos et al., 2013) and digital entrepreneurship literature (Nambisan, 2017)—into a concrete empirical setting. We find support that these digital technology characteristics indicate technological attractiveness for CVC managers. Recombinable and reprogrammable digital technologies create powerful action potentials that allow both high task specialization and scalability (Giustiziero et al., 2022), which CVC managers value positively in their evaluation decisions. Fourth, by employing the first experimental study with CVC managers, we contribute to the individual-level understanding of CVC investing. To date, extant research has largely overlooked the role of CVC managers mainly due to limited access to primary empirical data (Drover, Busenitz et al., 2017). Investigating CVC investment decisions in real time, our study sheds light on individual-level differences in the evaluation of ventures as CVC investment opportunities.

Theory and Hypotheses

Opportunity Evaluation From an Affordance Theory Perspective

The evaluation of the attractiveness of an opportunity for its pursuit has been understood as a future-oriented judgment of “what will be” after prospective opportunity exploitation (Haynie et al., 2009). Extant entrepreneurial decision-making research has investigated opportunity evaluations along two overarching themes (Williams & Wood, 2015): the environment of the opportunity (i.e., environmental decision cues) and the opportunity itself (i.e., opportunity decision cues). Considering the opportunity environment, researchers have mostly examined the importance of industry-related factors surrounding an opportunity, such as firm entry and exit rates (Wood et al., 2014). Regarding the opportunity itself, an important body of work has employed resource-based theorizing to investigate the attractiveness of characteristics such as value, rarity, and inimitability (Haynie et al., 2009), or resource efficiency and novelty (Wood & Williams, 2014). However, beyond the anticipation of resource benefits, a central theme in opportunity evaluation decisions is action orientation (Wood & McKelvie, 2015). Given the understanding of entrepreneurial activity as an action-formation process (Autio et al., 2013; Schade & Schuhmacher, 2022), we argue that the consideration of concrete action potentials arising from the future opportunity exploitation is crucial in determining its attractiveness.

We draw upon affordance theory to develop a nuanced understanding of action orientation in opportunity evaluation decisions. Originally introduced by Gibson (1977), affordance theory has entered into academic conversations on human–computer interactions (Norman, 1999), information systems (Henningsson et al., 2021; Majchrzak & Markus, 2013), and most recently digital entrepreneurship (Autio et al., 2018; Nambisan, 2017; Nambisan et al., 2019). An affordance describes the “action potential or possibilities offered by an object (e.g., digital technology) in relation to a specific user (or use context) in innovation and entrepreneurship” (Nambisan et al., 2019, p. 3). In other words, an affordance is “what an individual or organization with a particular purpose can do with a technology” (Majchrzak & Markus, 2013, p. 832). Affordances may be nested in other affordances, support other affordances, or even depend on other affordances (Strong et al., 2014). Importantly, affordances refer only to the potential, not to the actual use of action potentials (Volkoff & Strong, 2013). Thus, Strong et al. (2014) propose the distinction between affordances (potentials) and actualization processes (realization of potentials). While affordances refer to action potentials arising from an actor-technology relation, actualization describes the process through which actors translate affordances into concrete actions that produce goal-directed outcomes (Volkoff & Strong, 2018). To date, however, affordance theory does not inform us as to how actors assess affordances regarding their attractiveness for actualization. Shedding light on the decision to pursue affordances is critical because affordances might exist and be recognized by actors but not deemed as attractive for actualization. Integrating affordance theory with opportunity evaluation reasoning, we propose that affordances can serve as structural components of opportunity characteristics, which are relational and action oriented in themselves. Resultantly, we reason that entrepreneurial agents value action potentials arising from an opportunity under consideration. In other words, they assess potential actions they can perform in the realm of an entrepreneurial opportunity. Consequently, we posit that the attractiveness of affordances depends on the consideration of outcomes resulting from prospective actualization (i.e., anticipated benefits of acting upon affordances). That is, entrepreneurial agents evaluate affordances as worthwhile for actualization when they consider them to create attractive action paths (Wood & McKelvie, 2015).

CVC Managers as Corporate Entrepreneurial Agents

CVC investing is an important corporate entrepreneurial activity that allows incumbent firms to access promising technologies from new ventures and strengthen entrepreneurial abilities of their business units (Sharma & Chrisman, 1999). Incumbent firms typically organize their CVC investment activities in structurally separated units, equipped with CVC managers as corporate personnel in charge of scouting, evaluating, and selecting entrepreneurial ventures for investment (Dokko & Gaba, 2012). In their facilitating role, CVC managers have a “bird’s-eye view” on the investment relation between their corporate parent and the entrepreneurial venture (Weber, 2009). They hold responsibility for negotiating investment deals and coordinating activities among actors involved in pre- and post-investment phases (Weber et al., 2016). In other words, CVC managers serve as “entrepreneurial agents in pursuit of effective search and integration” (Basu et al., 2016, p. 149). To ensure legitimacy within their corporate parent (Souitaris & Zerbinati, 2014), CVC managers have to facilitate interactions between business units and ventures that spur innovation and value creation (Dushnitsky & Lenox, 2005; Titus & Anderson, 2018). Under this consideration, we contend that CVC investment opportunities represent opportunities for new product/service development and market entry, which reflect classical corporate entrepreneurial activities (Sharma & Chrisman, 1999). Thus, we conceptualize investment decisions as judgments by CVC managers about pursuing corporate entrepreneurial opportunities for their firm.

Digital Affordances and the Evaluation of CVC Investment Opportunities

Given their technology-accessing mandate, we argue that CVC managers value digital affordances arising from the relation between their firm and unique digital technology characteristics, such as reprogrammability, data homogenization, and self-reference (Kallinikos et al., 2013; Yoo et al., 2010), in their consideration of ventures as investment opportunities.

Reprogrammability describes the capacity to be “accessible and modifiable by (an object) other than the one governing their own behavior” (Kallinikos et al., 2013, p. 359). In this vein, reprogrammability allows the de-coupling between form and function and thus the adaptation of digital technologies for a variety of use contexts (Autio et al., 2018). For example, the company Retresco offers a natural language generation solution that uses data to automatically produce text, which has been reprogrammed to a wide range of uses, such as the automatic generation of product descriptions, insurance reports, and traffic news (Retresco GmbH, 2022). Data homogenization refers to the representation of digital data in bits and bytes, thus disentangling content from medium and enabling the transfer and combination of digital data with heterogeneous technologies (Kallinikos et al., 2013). As such, data homogenization enables the recombinability of digital technologies, that is, “the ability to associate with and build on other digital artifacts or components” (Nambisan, 2017, p. 1038). A well-known example is Google Maps, which has been coupled with digital cameras, connected cars, and other platforms to combine web mapping insights with complementary information for generating new visualizations through “mash-ups” (Yoo, 2013). Self-reference implies that the realization of digital innovation requires only the access, not necessarily the ownership, of digital technologies (Yoo et al., 2010). A prominent example of self-reference is the Internet, which serves as digital infrastructure necessary for developing online platforms. As such, self-reference creates network effects that spur the diffusion—or generativity—of digital innovations (Autio et al., 2018). While we study the importance of reprogrammability and recombinability for CVC managers’ evaluations, self-reference is inherently reflected in the inter-organizational transfer of digital technologies.

As a result of these characteristics, digital technologies may offer “uniquely powerful affordances” (Yoo, 2013, p. 231), which CVC managers will value in their evaluation of ventures. Examining investment opportunity evaluations as future-oriented judgments, we theorize that digital affordances determine CVC managers’ anticipation of outcomes along three themes: the support of business units for investment sponsoring and post-investment collaboration (Basu et al., 2016); the innovation and market-related benefits following prospective affordance actualization (Dushnitsky & Lenox, 2005; Dushnitsky & Yu, 2022); and, resultantly, the consequences for the legitimacy of CVC investing (Souitaris et al., 2012). By doing so, we conceptualize affordances as building blocks of theoretical mechanisms that explain CVC managers’ evaluation of investment opportunities (Bygstad et al., 2016).

Recombinability of Venture’s Digital Technology

Prior research has found that CVC parents are more likely to gain positive innovation outcomes from investments in ventures that are technologically related to their business units (Basu et al., 2011). Technological relatedness improves social interactions between both parties (Maula et al., 2009), and increases the likelihood for forming subsequent strategic alliances (Van de Vrande & Vanhaverbeke, 2013). Recombinability is an action-enabling capacity that builds upon technological relatedness and allows associating a digital technology with multiple complementary artifacts for the creation of synergies (Nambisan, 2017; Yoo, 2013). As such, recombinability inherently indicates an action-oriented relation between the entrepreneurial venture and business units of the CVC parent. Importantly, recombinability implies multiple action potentials with different business units of the CVC parent. Recognizing this potential, CVC managers anticipate a greater likelihood of identifying and convincing business units to support the investment and engage in a later collaboration with the venture. Furthermore, CVC managers anticipate that the actualization of affordances arising from recombinability (i.e., acting upon recombinability) enables digital innovations in core offerings or operations of business units (Lyytinen et al., 2016), which is a central objective of CVC investing today. The combination of digital and physical artifacts is necessary for realizing digital innovations (Yoo et al., 2010). Recombinability enables the initial affordance of combining the venture’s digital technology with multiple digital or physical artifacts from the CVC parent. As the “combining” affordance can be actualized in a variety of ways, CVC managers can anticipate various actualization outcomes. For example, recombination can enhance physical products and services through digital components (Wang, 2022), which ultimately helps increase demand for existing offerings of the CVC parent (Maula, 2007). Similarly, digital technologies from ventures can also be combined with operational tools of business units for optimization, for example, by incorporating automation capabilities into mainstream processes. With these envisioned outcomes, CVC managers expect to fulfill their mandate and thereby increase their legitimacy (Souitaris & Zerbinati, 2014). We hypothesize:

Reprogrammability of Venture’s Digital Technology

Extant literature suggests that CVC managers value technological usefulness when considering ventures for investment (Basu et al., 2016; Souitaris & Zerbinati, 2014). Reprogrammable digital technologies are valuable to the corporate parent of CVC units because they can be modified for various use contexts in different business units (Nambisan, 2017; Yoo, 2013). The powerful redeployment potential of reprogrammable digital technologies stems from their unique ontology, which allows modifications in their logical structure (Kallinikos et al., 2013). Concretely, reprogrammability enables the initial affordance of assimilating the venture’s digital technology into multiple use contexts of business units. Like recombinability, reprogrammability creates an action-oriented relation between the venture under consideration and business units of the CVC parent firm. In comparison to recombinability, however, this action potential is not grounded on technological complementarity but rather on the potential for assimilation by business units. Resultantly, CVC managers consider investing into ventures with reprogrammable digital technologies to be attractive for business units, both in terms of pre-deal investment support and post-deal resource commitment. With prospective affordance actualization, reprogrammability allows the generation of new digital offerings or operational tools for the corporate parent, which have the potential to substitute traditional ones (Keil et al., 2008; Maula et al., 2013; Schildt et al., 2005). For example, reprogramming digital technologies to new use contexts can enable development of new digital products, services, and business models which have the potential to represent core market offerings or capabilities of the CVC parent firm in the future (Chesbrough, 2002). Exploration is a central objective of CVC investing, which CVC managers emphasize in their evaluation of investment opportunities. In this context, reprogramming can help create pioneering inventions, which research has identified as an outcome of CVC investments (Van de Vrande et al., 2011). We posit:

Individuation of Affordance-Based Investment Opportunities by CVC Managers

Researchers have conceptualized opportunity evaluation as an individuation process, suggesting that “evaluation rules are person-centric, as individuals interpret what each cue-rule relationship means for them and for their businesses given their idiosyncratic characteristics” (Williams & Wood, 2015, p. 225). That is, the evaluation of opportunities is subject to individual interpretations of entrepreneurial agents. Accordingly, we propose that interpretive judgments of entrepreneurial agents about the worthiness of pursuing affordances for actualization through investment opportunities depend on their personal and organizational background. Concretely, we theorize on a cognitive judgment perspective on affordances, arguing that actors envision outcomes of prospective affordance actualization differently based on cognitive frames that are influenced by prior experiences and current circumstances (Wood & McKelvie, 2015). Entrepreneurial decision-making research suggests that CVC managers are influenced by two sources in their individuation process. First, extant research has found that personal experiences accumulated during prior jobs influence the decision-making of venture capital (VC) investors (Franke et al., 2006), which most likely applies to the individuation process of CVC managers as well. Second, extant research highlights that actors differ in their organizational backgrounds, which presumably influences their decision-making too (Shepherd et al., 2015). Unlike independent VCs, CVC managers serve as corporate personnel of CVC units (Dushnitsky & Shapira, 2010), which are part of corporate parents that organize them differently in terms of structure and objectives—aspects that determine the mandate of CVC managers (Souitaris & Zerbinati, 2014). Thus, heterogeneity between CVC units can explain differences in CVC managers’ individuation of investment opportunities.

Digital Technology Experience of CVC Managers

We examine the digital technology experience of CVC managers as a task-specific type of personal background experience (Marvel & Lumpkin, 2007). CVC managers serve as technology scouts who often have long-standing experience of working with newest technologies from their prior educational and professional occupations (Dokko & Gaba, 2012). Research shows that individuals with technological backgrounds emphasize functional benefits of innovations (Dougherty, 1992), which leads them toward employing a product-centric view in their evaluation of entrepreneurial opportunities (Gruber et al., 2015). We argue that this mindset, alongside their ability to perform digital technology tasks, leads CVC managers with greater digital technology experience to pay particular attention to powerful digital affordances offered by recombinability and reprogrammability in opportunity evaluation decisions. We expect that CVC managers with greater digital technology experience are well aware of the benefits that the prospective actualization of digital affordances can generate for business units and ultimately for the CVC unit itself. Their task-specific experience with digital technologies broadens the envisioning of potential use cases that arise from the recombinability and reprogrammability of digital technologies, beyond originally intended designs by the entrepreneurial venture (Garud et al., 2008). In this regard, digital technology experience increases CVC managers’ salience of technological benefits resulting from prospective affordance actualization (Dushnitsky & Lenox, 2005). Moreover, their digital literacy is expected to lead to self-selection of tasks in which CVC managers can make use of their digital technology skills (Blau, 1999; Gruber et al., 2015), such as the affordance actualization process in the post-investment phase. While CVC managers act as facilitators between business units and ventures (Weber, 2009), their digital technology skills can help them to become more actively involved in the actualization process. In this vein, CVC managers anticipate to make a stronger contribution in the integration phase, which, together with the envisioned technological benefits, increases their legitimacy within the corporate parent. We hypothesize:

Entrepreneurial Experience of CVC Managers

Similar to VC investors, some CVC managers have founded a venture prior to joining a CVC unit and can therefore draw upon their personal entrepreneurial experience (Maula et al., 2005). As founders accumulate valuable experiences while starting a new business, entrepreneurial experience has been found to influence investment decision-making (Gruber et al., 2015; Walske & Zacharakis, 2009; Warnick et al., 2018). Researchers have shown that entrepreneurs favor opportunities that are novel and allow the most efficient use of resources (Wood & Williams, 2014). As novel and action-oriented characteristics, recombinability and reprogrammability inherently reflect the potential for efficient redeployment of digital technologies over time (Helfat & Eisenhardt, 2004). The multiplicity of affordances arising from recombinability and reprogrammability creates a variety of actualization options over time, which increases entrepreneur CVC managers’ confidence for a desired pathway following the investment decision (Mitchell & Shepherd, 2010). Continuously identifying relevant use cases is particularly important for digital technologies, which are typically generative and ever evolving in their nature (Garud et al., 2008; Von Briel et al., 2018). CVC managers with entrepreneurial experience have an increased awareness that ventures typically fail when they are unable to design inventions that find applications in relevant markets (Artinger & Powell, 2016). Hence, greater entrepreneurial experience leads CVC managers to value market-related benefits resulting from the prospective actualization of digital affordances arising from a CVC investment (Dushnitsky & Yu, 2022). Specifically, entrepreneur CVC managers consider digital affordances as enabling potentials for successfully deploying and scaling inventions into existing or new markets (Huang et al., 2017). In addition, entrepreneurs typically adopt a more optimistic view on opportunities than individuals without entrepreneurial experience (Palich & Bagby, 1995). This optimism makes CVC managers more confident that the actualization of digital affordances successfully yields market-related benefits. We posit:

CVC Unit Dependence on Business Units of the Corporate Parent

Beyond the personal background, CVC managers are likely to be influenced by their organizational background—as reflected in the setting of their CVC unit—when evaluating investment opportunities (Dushnitsky & Shapira, 2010; Shepherd et al., 2015). CVC units typically exhibit differences in their structure and objectives, as opposed to independent VCs which are relatively homogeneous in these respects (Drover, Busenitz et al., 2017). CVC units differ particularly in their dependence on business units of the corporate parent, which is reflected in the extent to which approvals for final investment decisions are needed, and relatedly, the mandated involvement of business units in the post-investment phase (Hill et al., 2009).

First, while some CVC units require business unit sponsors for financing investments, others are equipped with a dedicated investment fund (Strebulaev & Wang, 2021). With a sponsoring approach, business units are already involved in the due diligence process, provide concrete referrals, and take important positions in investment committees that have to sign-off deals brought forward by CVC managers (Souitaris & Zerbinati, 2014). With investments from a dedicated fund, CVC units are largely autonomous and are usually able to realize investments without extensive involvement of business units, who then typically garner only minor roles in investment committees. Second, in the post-investment phase, CVC units may either act mostly as independent advisors to investee ventures or their key mandate may be to spur technological collaborations with business units. The dependence on business units determines the extent to which CVC managers seek legitimacy from their corporate parent (Jeon & Maula, 2022; Souitaris et al., 2012). Research suggests that with greater dependence, CVC units emphasize technology-accessing objectives more strongly (Souitaris & Zerbinati, 2014). This equips CVC managers with a clear mandate to scout and source ventures with technologies relevant to business units (Basu et al., 2016). Given this mandate, we argue that CVC managers evaluate ventures offering technologies with great redeployment potential more positively. As digital affordances indicate powerful and action-oriented redeployment potentials, CVC managers expect that business units are more willing to support investments enabling that potential. Furthermore, CVC managers regard the prospective actualization as a means of successfully nurturing business units with new digital technologies, be it for seizing market opportunities or internal operational redeployment. We hypothesize:

Method

Metric Conjoint Experiment

We employed a metric conjoint experiment to capture CVC manager evaluations of investment opportunities (Shepherd & Zacharakis, 1997, 1999). Conjoint experiments allow real-time investigations of individual decision-making processes, overcoming methodological shortcomings of post hoc methods, which are subject to biases inherent in retrospective reporting (Zacharakis & Shepherd, 2001). In the last two decades, conjoint experiments have been established as an important methodology to study entrepreneurial decision-making in different contexts (Lohrke et al., 2010; Shepherd, 2011), including, for example, opportunity evaluation (e.g., Haynie et al., 2009; Wood et al., 2014), project terminations (Behrens & Patzelt, 2016), and VC financing (Lohrke et al., 2010). In the VC context, conjoint experiments have been proven to be helpful to decompose the criteria that investors use in their evaluation of ventures (Zacharakis & Meyer, 1998). For instance, researchers used conjoint experiments to analyze how VC investors evaluate business plans (Franke et al., 2006), the probability of new venture survival (Zacharakis et al., 2007), venture teams (Franke et al., 2008), founder passion (Warnick et al., 2018), and technological quality signals (Hoenig & Henkel, 2015).

While well established in entrepreneurship and VC literature, conjoint experiments have not found application in the CVC setting as of yet. Most extant research draws upon secondary data to analyze firm- and industry-level factors present in CVC investment dynamics (Jeon & Maula, 2022), thereby overlooking the role of CVC managers as key decision-makers. Therefore, researchers have called for an individual-level examination of CVC investment decisions, albeit recognizing the difficulty in gaining access to primary empirical data in this respect (Drover, Busenitz et al., 2017). Like independent VC investors, CVC managers typically screen and evaluate a large number of ventures for each investment. In fact, the vast majority of refusals likely occurs after individual screening by CVC managers (Strebulaev & Wang, 2021). In this regard, examining CVC managers’ evaluation decisions has great potential to enrich CVC research by a fine-grained individual-level view.

Conjoint Instrument Design

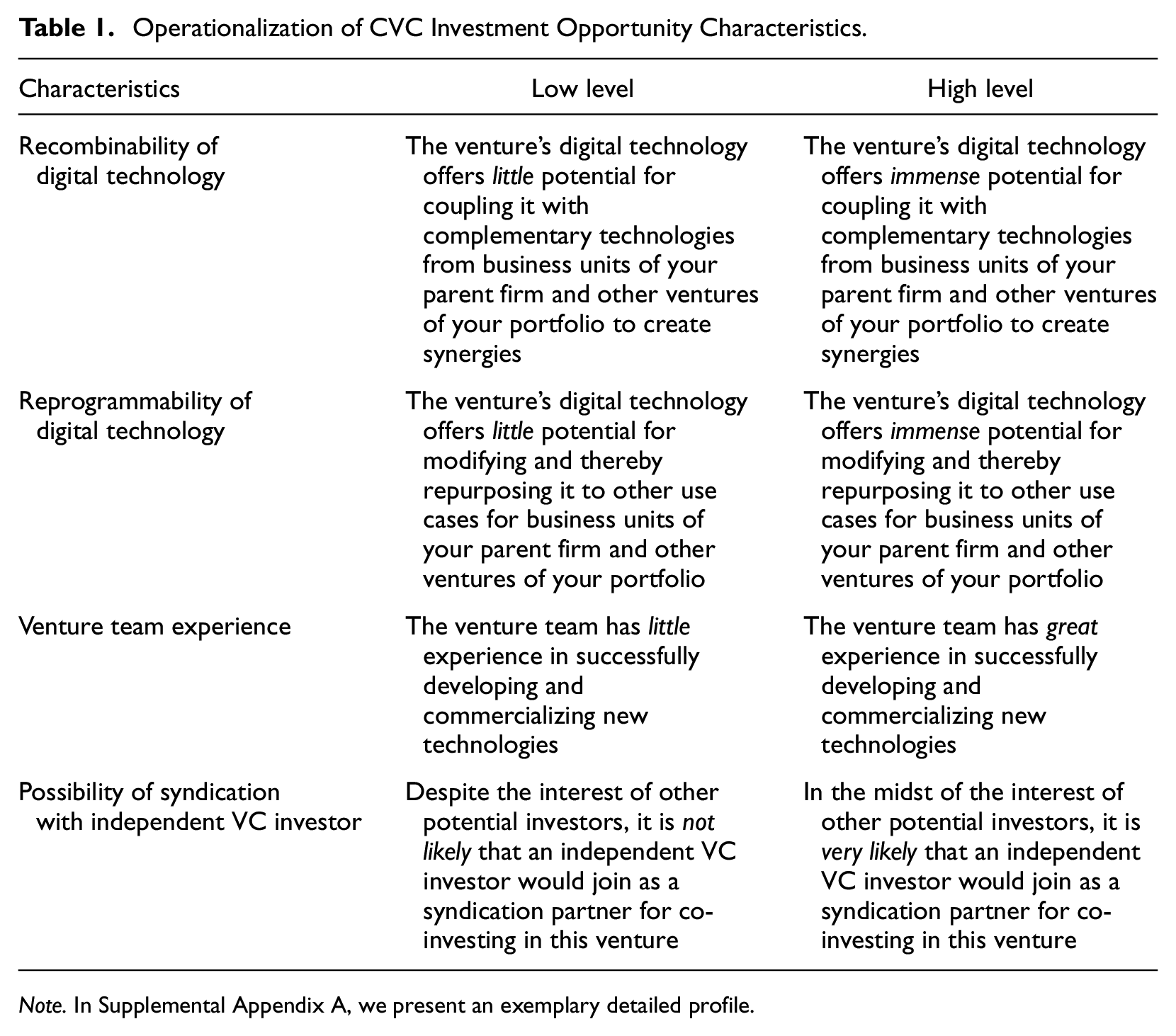

We put CVC managers into the situation where they were evaluating a digital venture for an initial investment. To control for general investment criteria, we stated that each venture under consideration owns a novel digital technology that has generated interest for an initial investment and fits with the search fields, a growing market, and the geography in which their firm invests. In addition, we noted that each evaluation decision is made contingent upon a favorable due diligence outcome (Drover, Wood et al., 2017). We highlighted that each investment opportunity is equal in all aspects other than four characteristics: recombinability, reprogrammability, venture team experience, and the possibility of syndication with an independent VC investor. While we theorized on recombinability and reprogrammability, we included venture team experience and the possibility of syndication with an independent VC investor as control variables (Basu et al., 2016; Souitaris & Zerbinati, 2014).

As our metric conjoint design encompasses four attributes varied at two levels each (Shepherd & Zacharakis, 1999), a full fractional design requires respondents to evaluate 16 (24) profiles. Prior studies have found that lengthy conjoint experiments cause respondent fatigue, which negatively affects response quality (Reibstein et al., 1988). To ensure the feasibility of our experiment, we employed an orthogonal fractional factorial design, reducing the number of conjoint profiles from 16 to 8 (Hahn & Shapiro, 1966). In line with prior studies (e.g., Warnick et al., 2018), we included two detailed profiles with comprehensive descriptions of the decision attributes to introduce respondents to the evaluation tasks in advance. We excluded answers on these two profiles in our analysis. To mitigate potential order biases (Chrzan, 1994), we created three different versions of the conjoint experiment and also randomized the order of attributes per venture profile for each respondent. Moreover, to be able to analyze test-retest reliability, we replicated all venture profiles (Aiman-Smith et al., 2002). In total, the respondents evaluated 18 venture profiles (two practice, eight summary, and eight replicated profiles). To ensure that our respondents understood the decision attributes, we asked them afterwards to classify two exemplary digital technologies as either highly recombinable or reprogrammable.

Sample

We invited 425 CVC managers to participate in our experiment. We contacted them through two channels. First, we used the professional social network LinkedIn. Second, we attended the Global Corporate Venturing (GCV) Digital Forum in January and July 2021 where we were able to connect with CVC managers. The GCV is a platform and data provider for the global CVC industry, which organizes several events for CVC practitioners every year (Global Corporate Venturing, 2021). Overall, 59 CVC managers (13.9%) participated. Our final usable sample consisted of 54 CVC managers from 44 CVC units and 34 industries. Five responses had to be dropped due to wrong answers on post-experimental understanding questions or very poor test–retest reliability (Holland & Shepherd, 2013). Our sample size is in the range of the recommendation by Shepherd and Zacharakis (1999), who propose that more than 50 respondents are typically sufficient.

Dependent Variable—Willingness to Invest

The dependent variable is the CVC manager’s willingness to invest in each investment opportunity (e.g., Murnieks et al., 2011; Warnick et al., 2018). After presenting each hypothetical investment opportunity, we asked the respondents: “What is your willingness to invest in this venture?” Respondents indicated their willingness to invest on a 7-point Likert scale, ranging from 1 (low willingness) to 7 (high willingness).

Conjoint Decision Attributes (Level 1)

We asked CVC managers to evaluate hypothetical investment opportunities based on four decision attributes: (1) recombinability of digital technology, (2) reprogrammability of digital technology, (3) venture team experience, and (4) possibility of syndication with an independent VC investor. We defined “low” and “high” levels for each characteristic based on prior definitions and consultation with experts (Table 1). Concretely, to ensure face validity of our experiment (Shepherd & Zacharakis, 1999), we conducted six semi-structured interviews with CVC experts who provided helpful insights into the formulation of the investment scenario, and the selection, labeling, and definition of our decision attributes.

Operationalization of CVC Investment Opportunity Characteristics.

Note. In Supplemental Appendix A, we present an exemplary detailed profile.

CVC Manager Variables (Level 2)

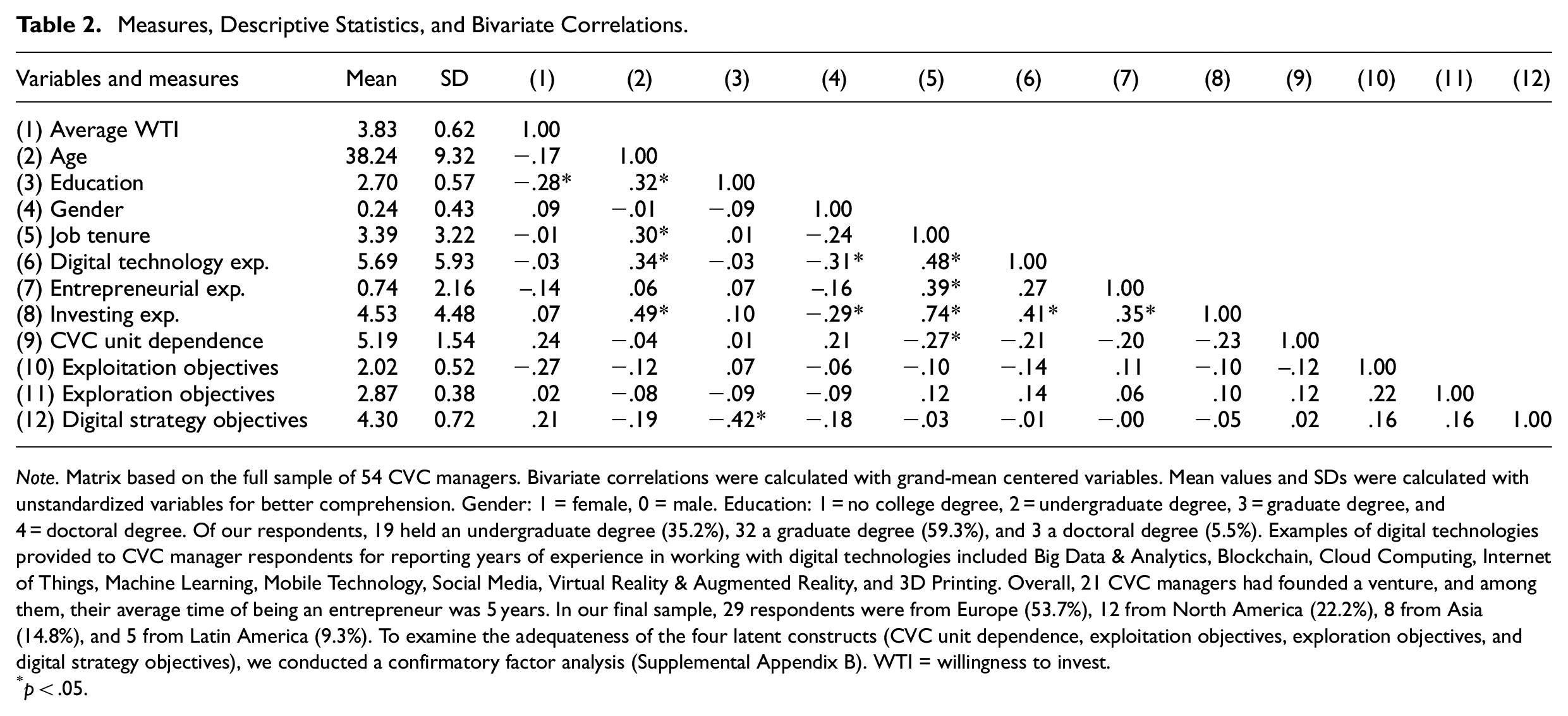

To shed light on differences among CVC managers in their evaluation decisions, we administered a post-experimental survey to gather personal and organizational background data. First, we collected personal data on general demographics (age, education, and gender) and job experiences, including tenure (years), digital technology experience (years of working with digital technologies), entrepreneurial experience (years been an entrepreneur), and investing experience (years in investing positions). Next, we obtained self-reported information on respondents’ CVC units. We gathered data on the CVC unit dependence on business units of the corporate parent using the reversed “horizontal autonomy” scale by Hill et al. (2009). Furthermore, we drew upon extant literature on CVC (Hill & Birkinshaw, 2014; Hill et al., 2009) and digitalization (Eller et al., 2020) to include three additional variables: exploration objectives, exploitation objectives, and digital strategy objectives. For all four latent constructs, we used the established scales from the originating articles. We present the exact measures, descriptive statistics, and correlation matrix of all CVC manager variables in Table 2.

Measures, Descriptive Statistics, and Bivariate Correlations.

Note. Matrix based on the full sample of 54 CVC managers. Bivariate correlations were calculated with grand-mean centered variables. Mean values and SDs were calculated with unstandardized variables for better comprehension. Gender: 1 = female, 0 = male. Education: 1 = no college degree, 2 = undergraduate degree, 3 = graduate degree, and 4 = doctoral degree. Of our respondents, 19 held an undergraduate degree (35.2%), 32 a graduate degree (59.3%), and 3 a doctoral degree (5.5%). Examples of digital technologies provided to CVC manager respondents for reporting years of experience in working with digital technologies included Big Data & Analytics, Blockchain, Cloud Computing, Internet of Things, Machine Learning, Mobile Technology, Social Media, Virtual Reality & Augmented Reality, and 3D Printing. Overall, 21 CVC managers had founded a venture, and among them, their average time of being an entrepreneur was 5 years. In our final sample, 29 respondents were from Europe (53.7%), 12 from North America (22.2%), 8 from Asia (14.8%), and 5 from Latin America (9.3%). To examine the adequateness of the four latent constructs (CVC unit dependence, exploitation objectives, exploration objectives, and digital strategy objectives), we conducted a confirmatory factor analysis (Supplemental Appendix B). WTI = willingness to invest.

p < .05.

Analysis and Results

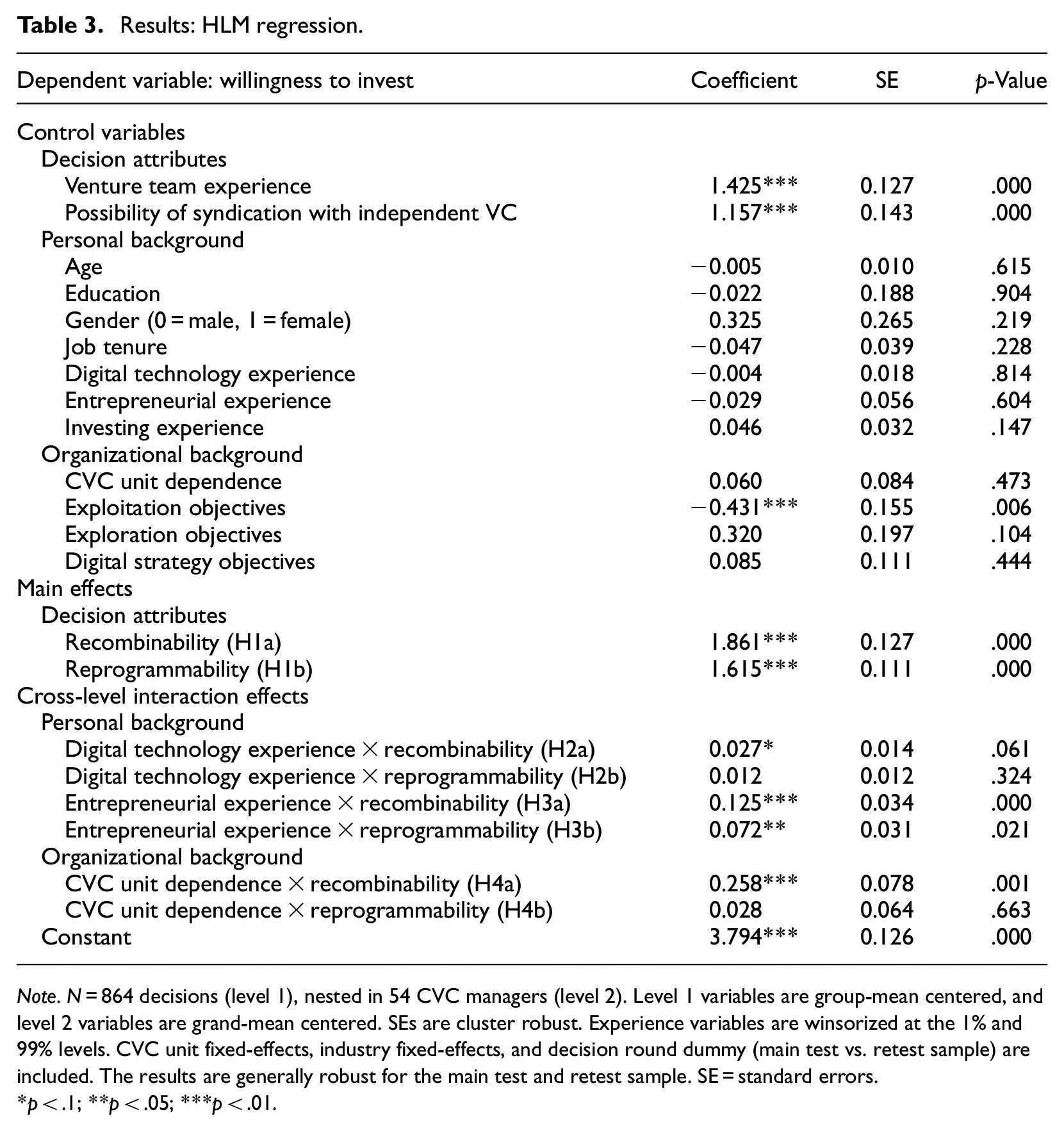

We used hierarchical linear modeling (HLM) to test our hypotheses (Aguinis et al., 2013; Raudenbush & Bryk, 2002). HLM can capture cross-level effects of (a) level 1: decision-making level and (b) level 2: CVC manager level. Thus, HLM allows not only the examination of the importance of decision attributes, but also testing individual-level differences (e.g., Murnieks et al., 2011; Shepherd, 2011). To account for potential CVC unit-level and industry-level effects, we included fixed-effects for CVC units and industries that have more than one CVC manager represented in our sample (Behrens & Patzelt, 2016). By fully replicating the decision tasks, we obtained two samples with 432 decisions each (main test and retest). We used the results from the pooled sample (864 decisions) for our analysis, as it captures all decisions by our 54 CVC manager respondents. Our sample shows a mean test–retest reliability of 0.866. Other conjoint studies have reported similar results (e.g., 0.813 [Drover, Wood et al., 2017], 0.72 [Holland & Shepherd, 2013], and 0.966 [Warnick et al., 2018]).

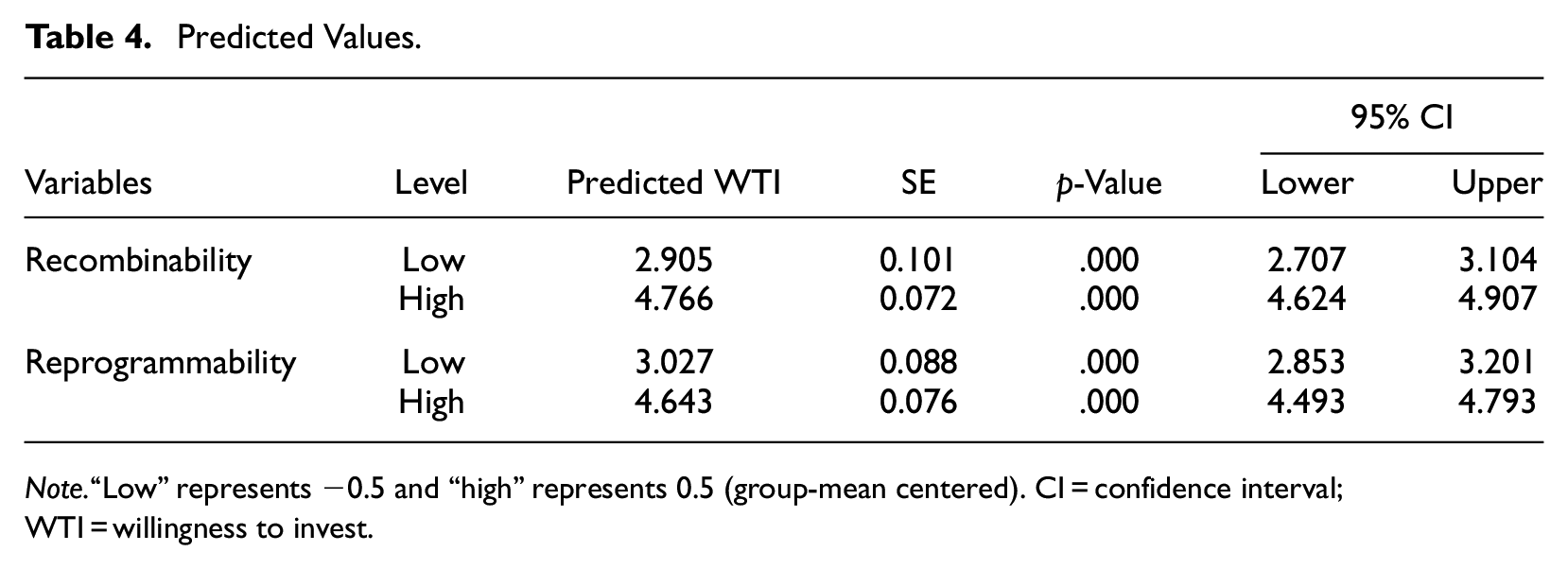

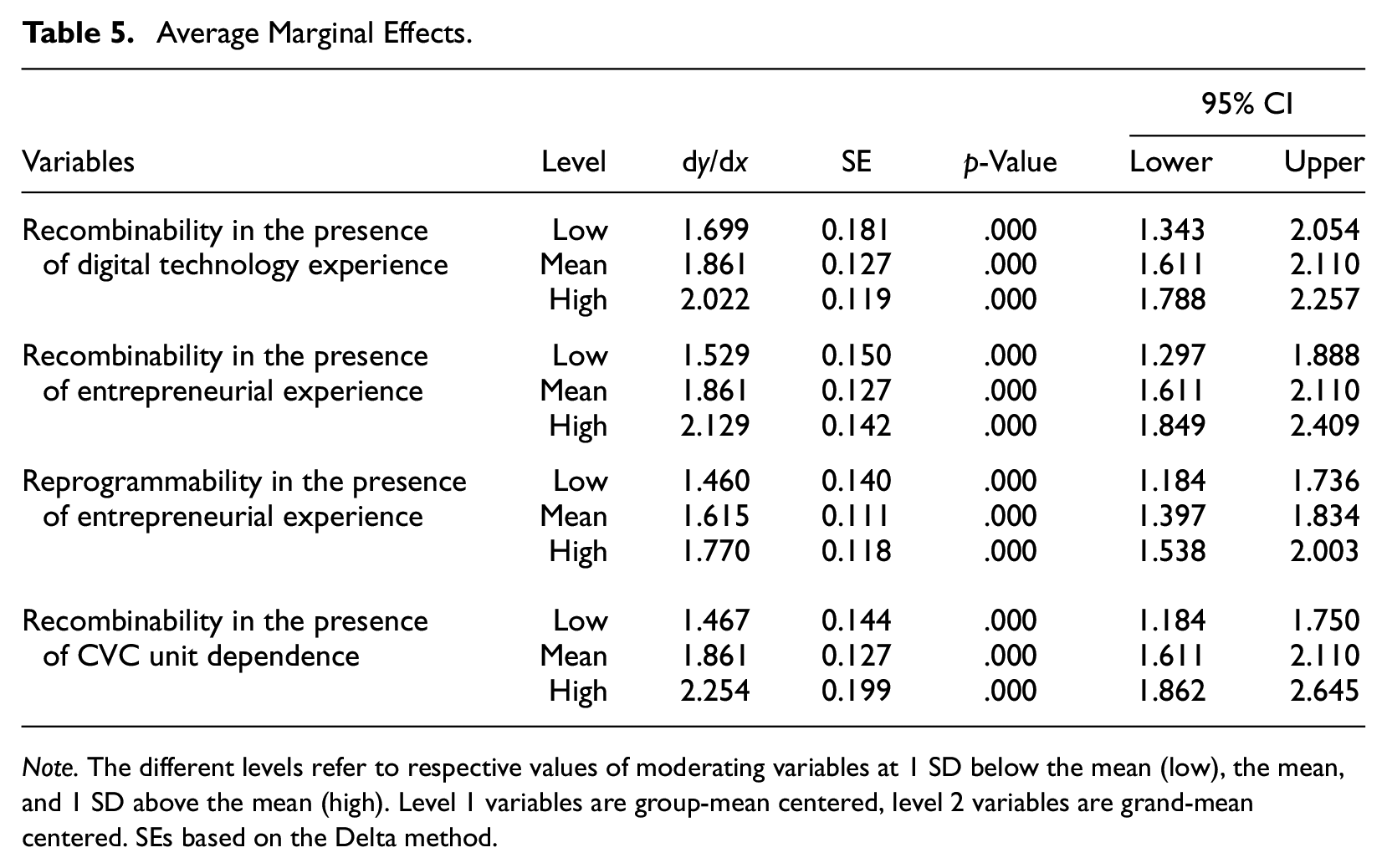

We report the results in three steps. First, we report the HLM results for all main and cross-level interaction effects (Table 3), where the coefficients reflect the shift in willingness to invest in response to a one unit increase in the respective variables. Second, we report the predicted values of willingness to invest at “low” and “high” levels of the decision attributes (Table 4). In addition, we show the predicted values for combinations of the decision attributes with low (−1 standard deviation [SD]), mean, and high (+1 SD) values of the moderators (Supplemental Appendix C). Third, next to the HLM results for the cross-level interaction effects, we follow Busenbark et al. (2022) and report the average marginal effects of the decision attributes in the presence of, again, low, mean, and high values of the moderators (Table 5).

Results: HLM regression.

Note. N = 864 decisions (level 1), nested in 54 CVC managers (level 2). Level 1 variables are group-mean centered, and level 2 variables are grand-mean centered. SEs are cluster robust. Experience variables are winsorized at the 1% and 99% levels. CVC unit fixed-effects, industry fixed-effects, and decision round dummy (main test vs. retest sample) are included. The results are generally robust for the main test and retest sample. SE = standard errors.

p < .1; **p < .05; ***p < .01.

Predicted Values.

Note.“Low” represents −0.5 and “high” represents 0.5 (group-mean centered). CI = confidence interval; WTI = willingness to invest.

Average Marginal Effects.

Note. The different levels refer to respective values of moderating variables at 1 SD below the mean (low), the mean, and 1 SD above the mean (high). Level 1 variables are group-mean centered, level 2 variables are grand-mean centered. SEs based on the Delta method.

Main Effects

Our results provide evidence for the importance of recombinability (H1a, β = 1.861, p < .001) and reprogrammability of digital technologies (H1b, β = 1.615, p < .001) for CVC managers’ willingness to invest. Results from the analysis of predicted values of willingness to invest reveal that CVC managers evaluated profiles with high recombinability most favorably (4.766 out of 7), showing an increase of 64.06% compared to venture profiles with low recombinability (2.905). Similarly, the predicted willingness to invest of venture profiles with high reprogrammability is 4.643, representing an increase of 53.38% in comparison to venture profiles with low reprogrammability (3.027). Our results also demonstrate the importance of the control decision attributes: venture team experience (β = 1.425, p < .001) and the possibility of syndication with an independent VC investor (β = 1.157, p < .001).

Differences Among CVC Managers in Investment Opportunity Evaluations

We examined cross-level interactions to test moderating effects of CVC managers’ digital technology experience and entrepreneurial experience, as well as their CVC unit’s dependence on business units of the corporate parent (Aguinis et al., 2013).

We find modest support for the moderating role of digital technology experience on the relationship between recombinability and willingness to invest (H2a, β = .027, p < 0.1). Our results show that in the presence of high digital technology experience, the average marginal effect of recombinability is by 0.161 larger than in the presence of digital technology experience at its mean value (2.022 vs. 1.861), representing an increase of 8.65%. However, we do not find support for the moderating role of digital technology experience on the reprogrammability–willingness to invest relationship (H2b, β = .012, n.s.). We conclude that digital technology experience strengthens CVC managers’ emphasis on recombinability.

Next, we find support for the moderating role of entrepreneurial experience on the relationship between recombinability and willingness to invest (H3a, β = 0.125, p < .001). The average marginal effect of recombinability is by 0.268 larger in the presence of high entrepreneurial experience than in the presence of entrepreneurial experience at its mean value (2.129 vs. 1.861), reflecting an increase of 14.4%. We also find support for the moderating role of entrepreneurial experience on the reprogrammability–willingness to invest relationship (H3b, β = .072, p < .05). The average marginal effect of reprogrammability increases by 0.155 in the presence of high entrepreneurial experience as compared to entrepreneurial experience at its mean value (1.770 vs. 1.615), showing an increase of 9.59%. In sum, our findings suggest that with greater entrepreneurial experience, CVC managers are more sensitive to both recombinability and reprogrammability when evaluating investment opportunities.

In line with our assumptions, we find support for the moderating role of CVC unit dependence on the relationship between recombinability and willingness to invest (H4a, β = 0.258, p < .001). The average marginal effect of recombinability increases by 0.393 in the presence of high CVC unit dependence as opposed to CVC unit dependence at its mean value (2.254 vs. 1.861), and thus by 21.11%. Yet, we do not find support for its moderating role on the reprogrammability–willingness to invest relationship, although the coefficient is positive (H4b, β = .028, n.s.). Overall, our results indicate that greater CVC unit dependence on business units leads CVC managers to place more emphasis on recombinability in their evaluation of investment opportunities.

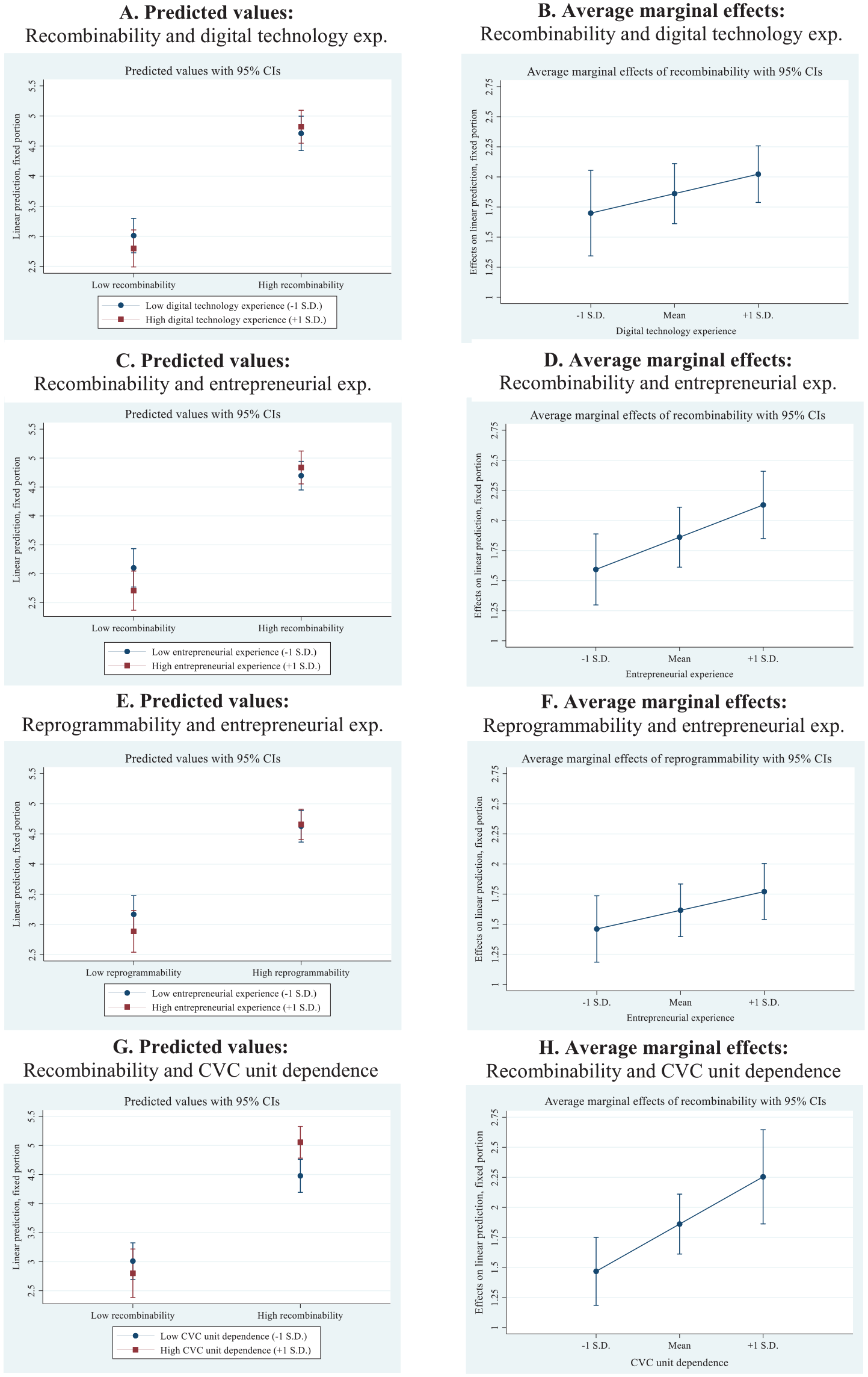

In Figure 1, we provide visualizations of the cross-level interactions, including both the predicted values of willingness to invest and the average marginal effects.

Visualizations of predicted values and average marginal effects.

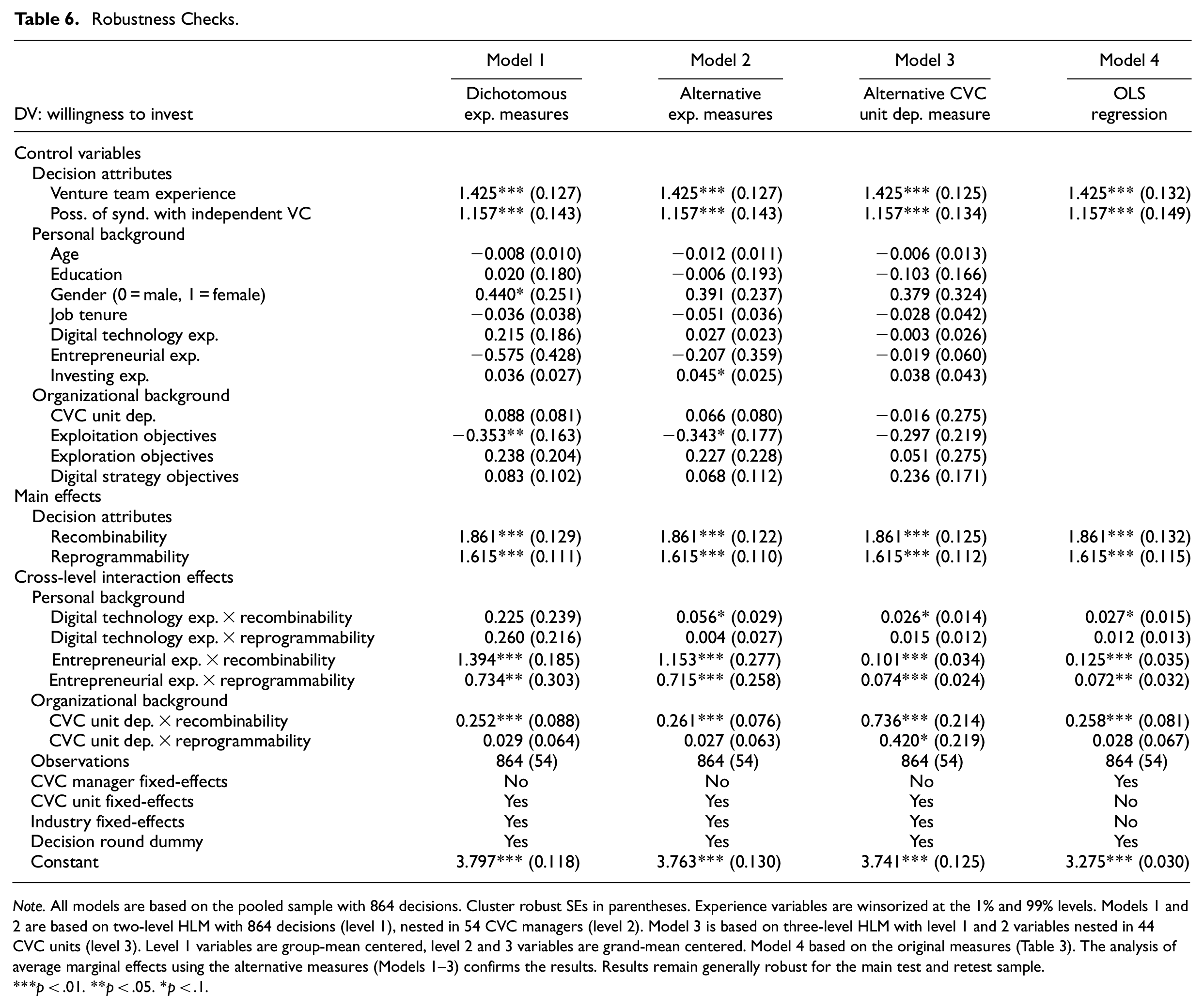

Robustness Checks

We conducted four robustness checks with alternative variables and specifications (Table 6). First, we dichotomized digital technology experience and entrepreneurial experience, assigning the value of 1 if a CVC manager had more than 5 years of experience and 0 if not (e.g., Kleinert et al., 2021). The results remain robust (Table 6, Model 1). The moderating role of entrepreneurial experience is even stronger for both the relationships of recombinability (β = 1.394, p < .001) and reprogrammability (β = 0.734, p < .05). However, the moderating role of digital technology experience on the relationship between recombinability and willingness to invest, which is already modest with the year-based measure in the main analysis (Table 3, p < .10), is statistically not significant. Nonetheless, its direction remains positive, in line with our assumption (β = 0.225).

Robustness Checks.

Note. All models are based on the pooled sample with 864 decisions. Cluster robust SEs in parentheses. Experience variables are winsorized at the 1% and 99% levels. Models 1 and 2 are based on two-level HLM with 864 decisions (level 1), nested in 54 CVC managers (level 2). Model 3 is based on three-level HLM with level 1 and 2 variables nested in 44 CVC units (level 3). Level 1 variables are group-mean centered, level 2 and 3 variables are grand-mean centered. Model 4 based on the original measures (Table 3). The analysis of average marginal effects using the alternative measures (Models 1–3) confirms the results. Results remain generally robust for the main test and retest sample.

p < .01. **p < .05. *p < .1.

Second, we applied alternative measures to the experience-based moderating variables. Specifically, we replaced digital technology experience with an equally weighted composite score of digital transformation experience, reflecting job experiences within three domains of digital transformation (Fitzgerald et al., 2014): experience with digital business models, experience with digital customer experience management, and experience with digital operations management. The results indicate a similar effect (β = .056, p < 0.1). The results are also robust for the dichotomized digital transformation experience variable, and in fact become even more pronounced. Furthermore, we replaced entrepreneurial experience with a binary variable (1 if the CVC manager had founded a venture that turned out to be successful, and 0 if not). The results remain robust (Table 6, Model 2) and are even stronger for both the effects of recombinability (β = 1.153, p < .001) and reprogrammability (β = 0.715, p < .001).

Third, we replaced the self-reported measure of CVC unit dependence with an objective measure that takes the value of 1 if the CVC unit of the CVC manager invests off the balance sheet of business units, and 0 if the CVC unit owns a dedicated investment fund. The results remain robust (Table 6, Model 3) and the interaction between recombinability and CVC unit dependence is even stronger (β = 0.736, p < .001). Notably, the hypothesized interaction effect between CVC unit dependence and reprogrammability (H4b), which is not significant with the self-reported measure, receives moderate support (β = 0.420, p = .055).

Fourth, to account for a potential omitted variable bias at the individual-level (Oster, 2019), we ran an ordinary least squares regression with fixed-effects for the 54 CVC managers (level 2 variable). The results remain robust (Table 6, Model 4).

Discussion

In this study, we develop a theoretical model proposing that entrepreneurial agents consider affordances as decision cues in their future-oriented evaluations of opportunities. We test our theorization by analyzing CVC managers’ evaluations of digital ventures as investment opportunities. The empirical results show that digital affordances—grounded in the recombinability and reprogrammability of digital technologies—determine the attractiveness of investment opportunities for CVC managers. We find that CVC managers individuate affordance-based investment opportunities differently based on their personal background (i.e., digital technology experience and entrepreneurial experience) and their organizational background (i.e., CVC unit dependence on business units).

Theoretical Implications

Our study makes four important theoretical contributions. First, we develop a theoretical model of affordance-based opportunity evaluation. Although action orientation is central to the understanding of entrepreneurial activity (McMullen & Shepherd, 2006), thus far, extant opportunity evaluation research has limited its focus on more generic opportunity characteristics that do not explicitly imply potentials for action (Wood & McKelvie, 2015). Integrating opportunity evaluation reasoning with affordance theory, we theorize and show that entrepreneurial agents develop decision rules around affordances (i.e., relational action potentials) as structural components of opportunities. Complementing the resource-based view (Haynie et al., 2009), affordance theory advances the understanding of opportunity evaluation through an explicit consideration of relationality and action orientation, which allows theorizing on concrete action paths that entrepreneurial agents anticipate with opportunity exploitation. While resources reflect capacities that build the foundation for actions (Kraaijenbrink et al., 2010), affordances are concrete action potentials arising from the relation between an object (i.e., technological resource) and an actor (i.e., individual or organization) (Majchrzak & Markus, 2013). In affordances terminology, resources provided by the opportunity under consideration represent the “object,” and therefore the functional determinant of affordances (Volkoff & Strong, 2013). Yet, for an affordance to arise, it requires not only an object or technology with certain features, but also an individual or organizational actor with specific predispositions. In this regard, while we extend the notion of opportunity evaluation to corporate entrepreneurial actions (Shepherd et al., 2015), our theorizing can help generate important insights for other entrepreneurial decision-making contexts where affordances can represent opportunity characteristics (e.g., new venture creation or internationalization).

Second, we contribute to affordance theory by adding a cognitive judgment perspective. Despite insights into the emergence (e.g., Majchrzak & Markus, 2013; Malhotra et al., 2021) and actualization of affordances (e.g., Henningsson et al., 2021; Strong et al., 2014), we lack a theoretical understanding of the process through which actors evaluate the worthiness of affordances for pursuing their actualization. Recent literature suggests that before being able to actualize an affordance, actors need to observe and perceive the affordance in the first place (Henningsson et al., 2021). However, affordance perception relates to the mere cognitive awareness of an affordance’s existence (Volkoff & Strong, 2018). Building upon opportunity individuation research (Wood et al., 2014), we advance affordance theory through a cognitive judgment perspective—that is, we theorize and show the importance of actors’ interpretive assessments about the worthiness of affordances to pursue their actualization. Opportunity individuation research suggests that personal and organizational backgrounds influence how actors cognitively view opportunity characteristics (Shepherd et al., 2015). In this regard, we hypothesize and find that actors with different personal and organizational backgrounds differ in their evaluation of affordances as structural components of opportunity characteristics. Concretely, our theorization and findings suggest that personal job experiences and organizational settings determine what outcomes actors cognitively envision from prospective affordance actualization in their future-oriented assessments. Their cognitive envisioning predisposes whether actors consider affordances as attractive for actualization. The cognitive judgment perspective is crucial for understanding the affordance-actualization process. The actual decision to pursue an affordance is an overlooked, yet critical condition of affordance actualization. Our theoretical insights into how affordances are evaluated help to understand why typically only a few affordances—out of bundles of affordances arising from actor-technology relations (Strong et al., 2014)—are pursued for actualization and produce concrete outcomes. Thus, we establish the evaluation process as an important step that precedes actualization and highlights the importance of interpretive judgments in affordance theory.

Third, we theorize upon the recombinability and reprogrammability of digital technologies (Kallinikos et al., 2013; Nambisan, 2017). Through our experimental operationalization, we were able to anchor affordances into these two observable digital technology characteristics and test their attractiveness for CVC managers. Our findings provide evidence that CVC managers value the powerful redeployment potential reflected by high recombinability and reprogrammability (Helfat & Eisenhardt, 2004). Although digital technologies can serve as “scale-free and fungible” resources (Giustiziero et al., 2022, p. 5), it is important to note that there are theoretical differences between the concepts of resource fungibility on the one hand and recombinability and reprogrammability on the other hand. While resource fungibility reflects the general capacity of resources to get redeployed, recombinability and reprogrammability are relational constructs that suggest concrete action potentials. Resource fungibility literature distinguishes between externally fungible resources, which can be redeployed between firms due to their low specificity (e.g., cash) and internally fungible resources, which are created for specific purposes and exhibit high stickiness (e.g., brands), enabling their transfer within firms (Nason & Wiklund, 2018). Due to their unique ontology (Kallinikos et al., 2013), recombinable and reprogrammable digital technologies outgo the limiting boundary conditions inherent to external and internal fungibility. On the one hand, recombinable and reprogrammable digital technologies can accomplish highly specific tasks while providing the capacity to be redeployed across firms (i.e., external fungibility). On the other hand, such digital technologies can be redeployed between business units of a firm (i.e., internal fungibility), as they are typically generative and “incomplete by design” (Garud et al., 2008). However, while technological resources serve as functional determinants of affordances, the capacity of actors (i.e., individuals or firms) for assimilation and recombination is equally important for the emergence of affordances. From a Penrosian perspective, the acquisition of novel resources by firms increases their capacity for future resource assimilation and recombination (Penrose, 1955). Accordingly, the actualization of affordances enforces the capability and resource basis of actors, which allows the emergence of powerful affordances from future actor-technology relations (Strong et al., 2014).

Fourth, by empirically examining the decision-making process of CVC managers as corporate entrepreneurial agents, we contribute to an individual-level understanding of CVC investing. Prior studies have analyzed firm- and industry-level drivers of CVC investment activity (Jeon & Maula, 2022), thus largely neglecting the role of CVC managers as important decision makers in the CVC investment process. Research on CVC managers is mostly limited to their general responsibilities (Weber, 2009), and differences to independent VCs (e.g., Dushnitsky & Shapira, 2010; Hill et al., 2009). Resultantly, researchers have increasingly called for an examination of CVC managers as corporate entrepreneurial agents in the investment decision-making context (Basu et al., 2016; Drover, Busenitz et al., 2017). Employing the first experiment with CVC managers, we analyzed their real-time evaluation decisions of investment opportunities. We provide evidence for individual-level differences in the evaluation decisions based on prior digital technology experience and entrepreneurial experience, highlighting the importance of human capital in CVC investing (Marvel et al., 2016). Moreover, we show that CVC unit dependence on business units also influences the evaluation of investment opportunities. Therewith, our results advance the understanding about implications of structural differences between CVC units, which is an underexplored theme to date. In addition, next to recombinability and reprogrammability, we provide quantitative evidence for venture team experience and VC syndication—our control decision attributes—as two investment criteria identified by prior qualitative studies (Basu et al., 2016; Souitaris & Zerbinati, 2014).

Practical Implications

Both CVC units and ventures can derive guidance from our results. Our findings can help CVC units in selecting CVC managers. Through a more detailed understanding of how CVC managers with specific personal backgrounds evaluate investment opportunities, CVC units can improve staffing decisions to hire CVC managers who fit with their investment strategy. Similarly, CVC managers can use our findings to explore their decision-making in greater detail and thereby develop tools that screen and filter investment opportunities more efficiently. Understanding how CVC managers evaluate investment opportunities is also critical for ventures that aim to attract CVC investments and thereby tap into unique resources and value-added services from CVC parents (Di Lorenzo & Van de Vrande, 2019; Uzuegbunam et al., 2019). The results suggest that ventures can increase their attractiveness for CVCs by designing digital technologies with strong redeployment potentials, hiring experienced team members, and convincing independent VCs to join as co-investors. Here, ventures have to ensure the clear communication of digital technology characteristics, particularly when negotiating with CVC managers who possess greater digital technology experience and entrepreneurial experience, or who are employed in CVC units that depend on business units of their corporate parent.

Limitations and Future Research

As with all research, our study is not without limitations. First, while our conjoint experiment serves as a powerful method to de-compose decision-making processes (Shepherd & Zacharakis, 1999), our investment profiles represent hypothetical, not real, venture profiles. Future research could employ field experiments or single case studies where CVC managers are accompanied throughout an evolving investment decision, or where archival data on prior investment decisions are made available. Importantly, although the conjoint experiment method is established in entrepreneurship research (Lohrke et al., 2010), we are the first to use it for studying CVC managers’ investment decisions. Our study opens opportunities for future CVC research using conjoint experiments combined with post-experimental surveys to provide rich insights into CVC decision-making processes that are not yet fully understood. For example, future studies could employ conjoint experiments to study how CVCs make decisions on follow-on investments, exits of portfolio ventures, or entry into syndication networks (Keil et al., 2010). Second, while we find support for most moderating hypotheses, the effect sizes of the experience-based moderations are relatively small, and the overlap of the confidence intervals is considerable. The experience-based moderators are based on numbers of years, which reflect natural values not bounded to any scales. Therefore, the results show that a one unit (i.e., 1 year) increase in experience, as reflected by the HLM interaction coefficients, does not make an extensive difference in evaluation decisions. Rather, it is the accumulation of experience that leads to greater differences in this respect. In fact, the effect sizes from the robustness checks, where we used dichotomized experience measures, indicate support for this assumption. Future research could provide helpful insights by examining how opportunity evaluation decisions change with the accumulation of experience over time, for example, by employing longitudinal study designs that capture evaluations at multiple points of time (Williams & Wood, 2015). In addition, future studies could examine the influence of other types of CVC managers’ experience (e.g., VC or acquisition experience) on their decision-making. Third, in line with extant opportunity evaluation research, we limited our theoretical scope on first-person opportunity beliefs—that is, the evaluation of opportunities for “me or my firm” (Haynie et al., 2009; Wood & McKelvie, 2015; Wood & Williams, 2014). Future studies could examine the preceding opportunity recognition phase, specifically by theorizing upon how (corporate) entrepreneurial agents identify third-person opportunity beliefs (i.e., opportunities for others), which can emerge to first-person opportunity beliefs (McMullen & Shepherd, 2006). Fourth, we theorized upon affordances as opportunity decision cues. Future research could adopt an environmental-level perspective on affordance reasoning, for instance, by studying how entrepreneurial agents consider digital and spatial affordances at the ecosystem level in the evaluation of opportunities (Autio et al., 2018). Fifth, we analyzed CVC investment decisions without examining performance implications. Based on our findings, future studies can test outcomes of CVC investments in ventures characterized by our decision attributes at the dyad level (Smith & Shah, 2013) and portfolio level (Wadhwa et al., 2016).

Supplemental Material

sj-pdf-1-etp-10.1177_10422587221134788 – Supplemental material for Evaluating Affordance-Based Opportunities

Supplemental material, sj-pdf-1-etp-10.1177_10422587221134788 for Evaluating Affordance-Based Opportunities by Petrit Ademi, Monika C. Schuhmacher and Andrew L. Zacharakis in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by an academic grant from Sawtooth Software providing access to the Lighthouse Studio platform, and a visiting scholar stipend from the German Academic Exchange Service (DAAD) for a research stay of Petrit Ademi at Babson College, USA.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.