Abstract

We integrate research on family-owned firms (FOFs) and the Behavioral Theory of the Firm (BTOF) to study wrongdoing—a specific dimension of corporate social responsibility (CSR) associated with destructive risk—in family- versus nonfamily-owned firms (NFOFs). We argue that FOFs are likely to respond differently from NFOFs to risks because in addition to concern for economic costs and benefits, FOFs are uniquely concerned with the socioemotional wealth (SEW) accruing from the noneconomic costs and benefits of their actions. Furthermore, we argue that the differences in behavior are dependent upon whether the nature of risk associated with a behavior is destructive, as in the case of wrongdoing, versus productive, as in the case of other previously examined behaviors such as research and development [R&D] investment, diversification, or internationalization. Our analyses, based on 17,022 observations from a sample of 1,900 publicly traded U.S. firms from 1999 to 2016, provide robust empirical support for these predictions, showing that FOFs commit less wrongdoing than their nonfamily counterparts and respond to performance relative to aspirations regarding wrongdoing in a way that varies from their responses regarding other behaviors examined in prior studies. We thereby advance the literatures on BTOF and FOFs by explaining how family owners’ decisions change depending on the type of risk associated with their behavior—destructive versus productive, and by integrating the additional aspiration related to SEW into BTOF predictions to tell a more complete story of organizational wrongdoing from the BTOF perspective. By focusing on wrongdoing as a specific dimension of CSR, our findings also have implications for CSR research as they show that the relative importance of social responsibilities shifts according to the type of risks (and trade-offs) associated with those responsibilities.

Keywords

Introduction

Conforming to legal responsibilities is an integral part of corporate social responsibility (CSR). However, massive corporate scandals, such as those at Wirecard and Volkswagen, have focused attention on organizational wrongdoing, defined as firm behavior that a social-control agent (e.g., the government) judges as transgressing a line separating right from wrong (Greve et al., 2010; Palmer, 2012). Research has begun to explore the behavioral motives of organizations to engage in wrongdoing (Harris & Bromiley, 2007; Mishina et al., 2010; Xu et al., 2019) based on the Behavioral Theory of the Firm (BTOF) (Cyert & March, 1963; March & Simon, 1958). This research increasingly shows that the likelihood of organizational wrongdoing depends on a firm’s performance relative to aspirations (PRA), both positive and negative. Moreover, while the family business literature has stressed the importance of behavioral aspects of family ownership (e.g., Berrone et al., 2010), the effect of ownership on BTOF predictions regarding wrongdoing remains largely unexplored.

In particular, there are strong theoretical reasons to expect that family ownership in a firm will affect the incidence of wrongdoing in firms. Family-owned firms (FOFs) differ from nonfamily-owned firms (NFOFs) because they face two utility dimensions simultaneously, namely socioemotional wealth (SEW) as well as financial wealth (Chrisman et al., 2012; Gómez-Mejía et al., 2007; Gomez-Mejia et al., 2018). SEW refers to the family’s social and emotional endowments in the firm, such as the ability to bequeath the firm to future generations, the reputational advantages of firm association, and the ability to preserve valuable ties with the family and other stakeholders (Cruz et al., 2010; Deephouse & Jaskiewicz, 2013; Zellweger et al., 2012). The desire to preserve SEW is likely to affect the incidence of wrongdoing in FOFs. When making decisions, such as those that could lead to a sanction for committing wrongdoing, family firm owners can face a dilemma whereby they must balance potential losses and gains, not only in terms of financial wealth, but also of SEW (Bromiley, 2009, 2010). Previous research has referred to this dilemma as the “mixed gamble” of family firm owners (Gomez-Mejia et al., 2014, 2018; Kotlar et al., 2018). More specifically, family firm owners must balance the likely losses and gains of decisions that could potentially lead to sanctions for wrongdoing not only in terms of financial wealth, but also in terms of SEW. Previous research has examined the direct relationship between FOFs and wrongdoing, and argued that, due to the desire to maintain SEW, family ownership can reduce organizational wrongdoing (e.g., Berrone et al., 2010; Ding et al., 2016; Yang, 2010).

However, prior BTOF research in the context of FOFs has mostly focused on behaviors associated with productive risks (e.g., Alessandri et al., 2018; Chrisman & Patel, 2012; Gomez-Mejia et al., 2010, 2018; Patel & Chrisman, 2014) overlooking those behaviors such as wrongdoing that are, instead, associated with destructive risks. While firms may take risks that provide a productive contribution to society, through innovation and creativity, they can also take destructive risks that lead to a “parasitical existence,” damaging society (Baumol, 1996). Building on this distinction, we expect that the effect of family ownership (and the preservation of SEW) will be different for some types of risk-taking behaviors as opposed to others. Specifically, FOFs are likely to respond very differently to PRA in the case of behaviors associated with destructive risks (such as wrongdoing) as compared to the case of behaviors associated with productive risks (such as research and development [R&D] investment and diversification), because the potential losses and gains to SEW are very different for each. This lack of understanding of the destructive side of risks is a limitation of current BTOF research. Specifically, we ask: How do BTOF predictions regarding wrongdoing change in FOFs?

Based on the mixed gamble approach, we predict that FOFs will respond differently from NFOFs to PRA, because in addition to concern for economic costs and benefits, FOFs are uniquely concerned with the SEW accruing from the noneconomic costs and benefits of their actions. Furthermore, these differences will depend on whether the type of risk is productive or destructive. Specifically, as our baseline hypothesis, we predict that FOFs will commit less wrongdoing than their nonfamily-owned counterparts. In addition, we theorize that while being below aspirations will lead to more wrongdoing in NFOFs, it will actually lead to less wrongdoing in FOFs. This diverges from prior research on FOFs responses to PRA regarding other behaviors such R&D investment, diversification, or internationalization. Moreover, while previous research has been ambiguous about the effect of being above aspirations on wrongdoing, with some studies finding a negative effect (Harris & Bromiley, 2007), no effect (Xu et al., 2019), and a positive effect (Mishina et al., 2010), we predict that this effect will be negative, and that this negative effect will be strengthened in FOFs.

We find strong support for our hypotheses using a comprehensive panel dataset including 17,022 observations for 1,900 publicly traded U.S. firms for the years 1999 to 2016, leading to four main contributions. First, we contribute to research on the effect of SEW on FOF decision-making under risk. While previous research has built on the mixed gamble approach to show that, when the firm is under threat, FOFs will risk SEW in pursuit of financial gains (Gómez-Mejía et al., 2007; Gomez-Mejia et al., 2018), we predict and show that FOFs will respond differently to risky destructive activities (such as wrongdoing), because the potential losses and gains to SEW are very different.

Second, and relatedly, we advance the BTOF, particularly in relation to wrongdoing behavior, by introducing SEW as an additional aspiration to provide a more complete theory of wrongdoing decisions. Specifically, diverging from previous research showing that being below aspirations leads to more wrongdoing, we predict and show that the SEW aspiration leads to FOFs actually committing less wrongdoing when below aspirations. Moreover, prior research has been ambiguous about the effect of being above aspirations on wrongdoing. By theorizing and finding that the combined effect of SEW and positive PRA makes the effect of wrongdoing more damaging to a FOF, our study clarifies why being above aspirations can have a negative effect on wrongdoing.

Third, we contribute to the study of CSR by examining a dimension of CSR with different trade-offs and risks. While the BTOF has been used to examine CSR in general (Cruz et al., 2014), wrongdoing is distinct because, in contrast to other CSR dimensions, it is specifically enforced by a social-control agent (e.g., the government). Our findings have implications for CSR research in the sense that they show that the relative importance of economic and noneconomic responsibilities and outcomes shift according to the type of risks (and trade-offs) associated with those responsibilities. Thus, our contribution is integral to the study of CSR.

Finally, we add to studies on wrongdoing by showing that family ownership (and SEW) affects wrongdoing in general, and in a very large sample of the largest, public U.S. firms. In contrast to prior research that has focused on small firms or only one type of wrongdoing (e.g., Ding et al., 2016; Ding & Wu, 2014), we use a comprehensive list of wrongdoing events consisting of the all sanctions by U.S. governmental agencies to extend the findings from previous studies to wrongdoing in general, and to a sample of the largest, most prominent firms in the world.

Theory and Hypotheses

FOFs, SEW, and Wrongdoing

Family business research has examined the effect of FOFs on numerous firm outcomes, including diversification (Gomez-Mejia et al., 2010), internationalization (Alessandri et al., 2018), executive compensation (Gomez-Mejia et al., 2003), mergers and acquisitions (M&A) (Gomez-Mejia et al., 2018; Miller et al., 2010), innovation (Chrisman & Patel, 2012; Patel & Chrisman, 2014), and CSR (Cruz et al., 2014), among many others. Most of this literature argues that the distinguishing characteristic of FOFs is the presence of SEW that plays a key role in the firm’s decision-making (e.g., Ding et al., 2016). SEW is defined as the stock of noneconomic benefits deriving from family owners’ pursuit of family-centered noneconomic goals (Gomez-Mejia et al., 2018). SEW comprises elements such as intergenerational control, preserving the family’s reputation, emotional attachment to the firm, and binding social ties (Berrone et al., 2012).

The desire to preserve SEW should affect the incidence with which FOFs commit wrongdoing. Traditionally, research on FOFs has argued that they should be more risk-averse than NFOFs (Basu et al., 2009; Fang, Chrisman, et al., 2021; McConaughy et al., 2001; Mishra & McConaughy, 1999). As the family’s financial wealth is concentrated in the (family) firm rather than diversified across firms, such wealth would be severely affected if risky decisions turn out poorly. Therefore, FOFs are thought to prefer avoiding risk due to the high economic cost of negative outcomes. However, empirical research has not definitively supported this view, suggesting that risk aversion does not accurately describe FOFs’ decision-making under risk (Gomez-Mejia et al., 2011).

A more contemporary perspective has viewed decision-making in FOFs as one in which there is a possibility of both SEW loss and gain outcomes. This mixed gamble approach has shown that decision-making in FOFs involves a trade-off between the potential losses and gains of SEW stemming from firm risk-taking (Gomez-Mejia et al., 2014, 2018; Martin et al., 2013). Executives in firms recognize that most decisions include the possibility of both losses and gains (Bromiley, 2009), and, as such, they must balance the potential for losses and gains when making decisions under risk. Based on this reasoning, prior research has shown that the trade-offs in terms of losses and gains from strategic decisions are very different for FOFs and NFOFs. Specifically, FOFs invest less in R&D (Chrisman & Patel, 2012; Gomez-Mejia et al., 2014), engage in less diversification (Gomez-Mejia et al., 2010), internationalize less (Alessandri et al., 2018), and are less likely to join industry cooperatives (Gómez-Mejía et al., 2007).

Similarly, a mixed gamble approach would predict that FOFs will commit less wrongdoing. Wrongdoing differs from other types of risk (and from other dimensions of CSR) in that it can subject the firm to sanction from a social-control agent (e.g., Greve et al., 2010; Palmer, 2012). This sanction is often direct and monetary (e.g., the average fine/settlement in our sample was approximately $11 million). However, while these direct costs are enormous, the reputational cost of wrongdoing can be just as large, running into many millions of dollars per firm (e.g., Karpoff et al., 2008). Also, wrongdoing often leads to significant turnover, loss of control, or even failure of the firm (e.g., Arthaud-Day et al., 2006; Gangloff et al., 2016; Healy & Palepu, 2003; Liou, 2008), and these dire consequences directly result from sanctions from social-control agents. For example, the Federal Deposit Insurance Corporation can take over or close banks, and the Securities and Exchange Commission can ban individuals from working in public firms, due to wrongdoing.

From a cost-benefit analysis of potential losses and gains in purely financial terms, for the typical firm it may not make sense to focus on reducing wrongdoing. The cost of investing in expensive prevention beyond compliance with regulations may not be compensated by financial gains, or the firm might be unable to calculate a reliable cost-benefit estimate for such investments (Berrone et al., 2010). Moreover, some illegal actions increase the probability of financial gain by disadvantaging competitors (Xu et al., 2019) or by providing greater leeway through covering up short-term financial losses (Harris & Bromiley, 2007). That is, firms may take destructive risks because it benefits them, or because they can shift costs to society at large. Indeed, from a purely economic standpoint, the balancing of risk and return for destructive risks (like wrongdoing) may be broadly similar for FOFs and NFOFs. For example, both types of firms should (more or less) benefit the same from disadvantaging competitors. However, because family owners hold the additional SEW utility dimension, the balancing of losses and gains when making decisions that could lead to sanctions goes beyond these purely economic considerations. Indeed, preserving SEW can occur at the expense of financial gains (Gómez-Mejía et al., 2007). Specifically, two aspects of SEW are especially likely to be affected by wrongdoing, namely family control, and family image and reputation.

Destructive risk-taking (like wrongdoing), more than other types of risk-taking behaviors, increases the possibility of loss of control of the firm. Wrongdoing often leads to changes in management (Arthaud-Day et al., 2006; Gangloff et al., 2016), and will often lead to the failure of the firm (e.g., Healy & Palepu, 2003). Indeed, wrongdoing is an excellent predictor of firm failure (Liou, 2008). FOFs have been shown to behave differently when control of the firm is at risk (Gómez-Mejía et al., 2007; Kavadis & Castañer, 2015). Family control is key for FOFs, because it provides the benefits to the family of being a FOF (Gomez-Mejia et al., 2018; Zellweger et al., 2012).

In terms of reputation, the family owner’s identity is often inextricably tied to the firm that can carry the family’s name (Berrone et al., 2012). This causes the firm to be seen by both internal and external stakeholders as an extension of the family itself. Public opprobrium for wrongdoing is more damaging to family owners because it tarnishes the family’s name (e.g., Dyer & Whetten, 2006). In contrast to NFOFs, which are not associated with any one particular group, actions that damage the firm’s reputation in FOFs also diminish the family’s reputation, potentially damaging the egos of family owners (Miller et al., 2011). Moreover, the family’s heightened identification with the business motivates family owners to pay particular attention to the firm’s favorable reputation, as it allows them to feel good about themselves, thus contributing to their SEW (Deephouse & Jaskiewicz, 2013). The firm’s reputation is also particularly important for firms with family owners due to the family’s emotional devotion and commitment to the business (Ding et al., 2016). This is especially the case for listed FOFs, which will likely be more exposed to reputational damages than non-listed firms.

From a mixed gamble approach, when compared to NFOFs, the potential losses to FOFs from destructive risk-taking (like wrongdoing) will be higher due to the importance of family control, and image and reputation. Moreover, the potential gains will be lessened. For example, FOFs are more likely to exhibit a long-term commitment and focus (Miroshnychenko et al., 2021; Sirmon & Hitt, 2003). Accordingly, the value of short-term leeway from covering up financial losses will be less valuable to them. For these reasons, from a mixed gamble approach, we expect that FOFs should commit less wrongdoing when compared to NFOFs. Consistent with prior research, we therefore formulate our baseline hypothesis:

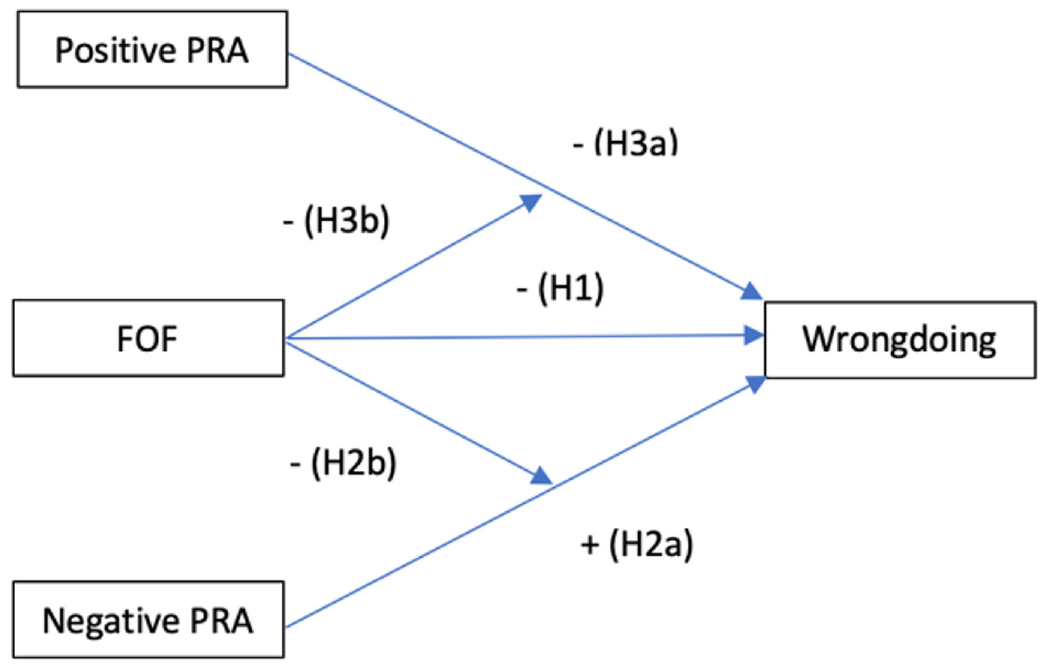

Hypothesis 1: In FOFs, the incidence of wrongdoing will be lower than in NFOFs.

Negative PRA, FOFs, and Wrongdoing

The BTOF (Cyert & March, 1963; March & Simon, 1958) is one of the most influential and important theories in management, organizational theory, and strategic management research (Argote & Greve, 2007; Gavetti et al., 2012). A significant research stream has built on the BTOF to examine organizational wrongdoing (Harris & Bromiley, 2007; Mishina et al., 2010; Xu et al., 2019), and scholars have specifically called for more research on wrongdoing to incorporate BTOF insights (Greve et al., 2010). The BTOF has also been used by family business researchers in distinguishing between FOFs and NFOFs, and distinguishing among FOFs (Fang, Memili, et al., 2021).

Research in the BTOF tradition describes numerous types of firm behaviors as responses to patterns of success or failure. PRA, both positive and negative, can affect firm behavior in numerous ways (e.g., Smulowitz et al., 2020). For example, performance below aspirations (i.e., negative PRA) triggers actions aimed at improving performance, such as increased risk-taking (Bromiley, 1991; Bromiley & Rau, 2010). Specifically, the BTOF maintains that decision-makers set goals or aspiration levels for their desired performance, and then respond to performance falling below these levels by searching for, and accepting, riskier solutions (e.g., Smulowitz et al., 2020). Such “problemistic search” involves underperforming firms engaging in risky activities with uncertain outcomes to turn around unacceptable performance or improve the firm’s position relative to other firms (Bromiley, 1991; Singh, 1986). This risk-taking can take the form of strategic decisions, such as M&A (Iyer & Miller, 2008) or new product launches (Eggers & Suh, 2019). It can also take the form of organizational wrongdoing, such as bribery (Xu et al., 2019) or financial fraud (Harris & Bromiley, 2007). Specifically, this research stream argues that negative PRA causes firms to search for ways to increase performance above aspirations, and this search may include wrongdoing.

In addition, negative PRA may cause strain for decision-makers and pressure them to adopt illicit means for meeting their goals (Greve et al., 2010). Firms may respond to strain by committing wrongdoing, as some illegal actions can increase the probability of positive financial outcomes by disadvantaging competitors (Xu et al., 2019), or covering up short-term financial losses (Harris & Bromiley, 2007). Firms with worse performance should feel greater strain, and therefore take more risks, because they can only achieve their goals with dramatic actions (Xu et al., 2019). Wrongdoing can also result from a lack of oversight by managers (Smulowitz & Almandoz, 2021; Wowak et al., 2015), and managers could be distracted from preventing wrongdoing when performance is poor. Therefore, wrongdoing could be a viable option for low-performing firms, despite its inherent legal and legitimacy risks, because it could provide a quick, short-term solution to the firms’ problems (Birhanu et al., 2016).

In sum, negative PRA can lead to firms taking more risks to turn around low performance, and it can cause strain. It can also distract managers, reducing oversight. All could lead to a higher incidence of wrongdoing. Formally stated:

Hypothesis 2a (H2a): Negative PRA will increase the incidence of wrongdoing.

However, while the BTOF predicts that firms respond to negative PRA by increasing wrongdoing, this effect may not be the same for all firms. From a mixed gamble approach, being a FOF is likely to radically alter how the firm responds to negative PRA when considering destructive risks, such as the type of risk associated with wrongdoing, because destructive risks could lead to sanctions. Specifically, from a mixed gamble approach, wrongdoing may represent a major threat to the SEW of family owners (in terms of family control, image, and reputation), with unclear financial consequences. As such, in situations of performance below aspirations, family owners may be reluctant to risk their SEW in exchange for uncertain financial gains.

Previous research from a mixed gamble approach examining how FOFs will respond to negative PRA has argued that the balance of losses and gains will militate toward increased risk-taking in FOFs. In general, this literature has argued that poor performance will make the family more economically motivated, thereby reducing the relative importance of prospective SEW losses (Gómez-Mejía et al., 2007; Gomez-Mejia et al., 2014, 2018). Put differently, negative PRA will pressure family owners to improve their firm’s financial situation, even at the cost of SEW, to reduce the risk of failure (Gomez-Mejia et al., 2018). This literature has shown that FOFs will respond to negative PRA by increasing M&A (Gomez-Mejia et al., 2018), R&D spending (Gomez-Mejia et al., 2014), and diversification (Gomez-Mejia et al., 2010).

However, wrongdoing differs from these other types of risky behavior in its destructive nature (Baumol, 1996). Specifically, the balance of losses and gains to wrongdoing is different from productive risky behavior, such as M&A or R&D spending, that have been the focus of this prior research. As we describe above, from a mixed gamble approach, the potential losses from wrongdoing are greater, and the potential gains are lessened, for FOFs. This is because family owners place greater value on not losing control and damaging the family’s image and reputation, and because they gain less from short-term leeway. However, negative PRA will increase all of these potential losses, and reduce the value of the potential gains. Specifically, negative PRA, combined with wrongdoing, makes the likelihood of failure (such as bankruptcy) much higher. FOF bankruptcy would lead to a “catastrophic” loss in SEW (Gomez-Mejia et al., 2014), depriving the family of all of the benefits of family ownership and severely damaging the family’s reputation (Gómez-Mejía et al., 2007). Moreover, even if the firm does not fail, poor performance combined with wrongdoing would have a devastating effect on the firm’s (and thereby the family’s) reputation. Indeed, there is some research showing that increased reputational concerns lead to a reduction in wrongdoing. For example, Annan (2022), using an experiment involving so-called “human ATMs” in Ghana found that increased reputation concerns for vendors reduced their misconduct. In another example, Cook et al. (2020) found that auditors with reputation concerns are less likely to deal with high misconduct clients. In addition, while wrongdoing (such as fraud) could potentially cover up short-term financial losses, allowing the firm’s decision-makers to maintain their salary and perquisites for more time, family owners are unlikely to receive these benefits, because they are likely to remain committed to the firm for the long term. Given this different calculation of losses and gains for FOFs, we expect that FOFs will actually be less likely to commit wrongdoing as negative PRA increases. Formally stated:

Hypothesis 2b (H2b): In FOFs, negative PRA will reduce the incidence of wrongdoing.

Positive PRA, FOFs, and Wrongdoing

While negative PRA is generally associated with an increase in risk-taking (and wrongdoing), the effect of positive PRA is more ambiguous (cf. Harris & Bromiley, 2007; Mishina et al., 2010). We anticipate that positive PRA will be associated with a decrease in wrongdoing, and that in FOFs this effect will be strengthened.

In general, BTOF research has shown that when performance levels rise above aspiration levels, firms prefer less risk. This derives from two related mechanisms. First, when firms are performing well in comparison to aspirations, decision-makers are not incentivized to engage in risky actions, that is, firms above aspirations do not engage in problemistic search (Sitkin & Weingart, 1995). Similarly, while wrongdoing could benefit the firm financially, the firm does not face strain when PRA is positive (Xu et al., 2019). Accordingly, decision-makers have less incentive to violate legal and moral standards when performance is above aspirations. Second, positive PRA creates an anticipation of future high performance, thus decreasing risk-taking. Wiseman and Gómez-Mejía (1998, p. 137) argue that, “when forecasts of firm performance are satisfactory (a gain situation), executives anticipate positive gains and act conservatively.” As such, firms have less incentive to engage in wrongdoing when PRA is positive.

In contrast, some scholars have argued that positive PRA should have a positive influence on outcomes, such as individual risk-taking (Boyle & Shapira, 2012) and organizational learning (Baum & Dahlin, 2007). Prominently, based on prospect theory (Kahneman & Tversky, 1979), Mishina and colleagues argued that high-performing firms engage in wrongdoing to maintain their performance relative to unsustainably high aspirations (Mishina et al., 2010). Specifically, those authors contended that increasing performance raises the aspirational reference point (Kahneman & Tversky, 1979; Tversky & Kahneman, 1981) such that firms will need to perform better and better just to maintain the status quo. This phenomenon has been referred to as the “Red Queen effect” (Derfus et al., 2008). Falling below this very high level will be interpreted as a loss, causing decision-makers to be more willing to take risky wrongful actions. Mishina and colleagues also argued that these pressures are greater for more prominent firms.

However, we still expect a negative relationship in our study. This is consistent with numerous studies finding that positive PRA leads to a reduction in various firm-level measures of risk-taking, such as R&D search intensity (Chen & Miller, 2007), exploratory R&D investments (Patel & Chrisman, 2014), organizational change (Greve, 1998), M&A (Iyer & Miller, 2008), credit risk in banks (Smulowitz et al., 2020), and capital expenditures and long-term debt (Schumacher et al., 2020). Moreover, as we state above, previous research has distinguished between productive and destructive risky behaviors (Baumol, 1996). Firms should respond differently to risky productive activities (such as organizational learning) and risky destructive activities (such as wrongdoing), because the cost to economic wealth is much higher. Moreover, the availability of slack resources has been generally regarded as one of the main reasons to predict the positive effect of positive PRA, which is why we control for it when testing our theorizing. Accordingly, we expect that positive PRA should lead to a reduction in the incidence of wrongdoing. Formally stated:

Hypothesis 3a (H3a): Positive PRA will reduce the incidence of wrongdoing.

We also expect that FOFs will respond more strongly to positive PRA, reducing the incidence of wrongdoing even further. The costs to FOFs (particularly in terms of SEW) are qualitatively different, and increase as PRA increases. This is supported by the arguments of Gomez-Mejia et al. (2014, p. 1354), where they state that “the larger the value of wealth-at-risk of loss (or risk bearing) of the agent, the more risk-averse the agent will be.” As PRA increases, the potential losses to FOFs in terms of SEW also increase. There are at least two reasons for this. First, the reputational costs of wrongdoing will not only be higher in firms with family ownership, they will be fundamentally more damaging, because the reputational damage will be to both the firm and the family (Chandler et al., 2021; Smith et al., 2021). Second, the family often relies on the firm for family-centric benefits, such as family employment and dividends, which wrongdoing can place at risk. Positive PRA will increase the value of these benefits. Moreover, avoiding wrongdoing can lead to a significant increase in the firm’s reputation.

Specifically, positive PRA increases the reputational benefits for the family. Positive PRA can buoy the firm’s reputation, and more reputable firms face greater scrutiny from stakeholders (Briscoe & Safford, 2008), and more attention when committing wrongdoing (Rhee & Haunschild, 2006). Negative events in high performing firms are associated with the greater violation of stakeholder expectations than a similar event in firms with regular performance (Zavyalova et al., 2016). Such wrongdoing can cause long-term damage to perceptions of the firm’s ethical integrity, requiring additional impression management to repair (Bansal & Clelland, 2004). Moreover, the egos and social status of family owners should be boosted by owning a highly performing firm (Zellweger et al., 2012). Accordingly, while decision-makers in NFOFs may feel greater pressure to continually increase high performance, family owners should place greater importance on the potential losses to their reputations that have been boosted by positive PRA.

In terms of family-centric benefits, positive PRA provides more of family-centered benefits to the family, thereby further raising the potential losses due to wrongdoing. For example, positive PRA allows greater community investment (O’Brien & David, 2014). Greater community investment should be especially valuable to the family because it allows the family to strengthen valuable ties with stakeholders. Positive PRA also gives decision-makers greater leeway in areas such as staffing or dividends (Smulowitz et al., 2020). This leeway should be especially valuable to the family, because it would allow greater employment for family members (e.g., Verbeke & Kano, 2012), and potentially greater dividends (e.g., Pindado et al., 2012; Schulze et al., 2003), both of which FOFs rely on more than NFOFs.

Indeed, avoiding wrongdoing may provide a substantial benefit to the FOFs in terms of reputation. For example, doing well in terms of CSR has been shown to positively affect firm reputation (Tetrault Sirsly & Lvina, 2019). As wrongdoing has greatly increased over time, preventing wrongdoing could be one way for firms to distinguish themselves from rivals and bolster their reputations. This effect could be especially large in FOFs, because the value of a positive reputation accrues not only to the FOF, but also to the family. Accordingly, avoiding wrongdoing could bolster a FOF’s reputation, increasing the family’s SEW.

Because positive PRA increases the value of reputation and family-centric benefits, it also increases the potential losses to the family from wrongdoing. Also, it does not increase the potential benefits. Accordingly, from a mixed gamble approach, the trade-off between potential losses and gains militates even more strongly against wrongdoing as positive PRA increases for FOFs. Formally stated:

Hypothesis 3b (H3b): In FOFs, the effect of positive PRA on the incidence of wrongdoing will be strengthened, reducing the incidence of wrongdoing even further.

We summarize our hypotheses in Figure 1.

Theoretical model.

Methods

Sample

We base our analyses on a unique dataset, generated by combining data from multiple sources. We derived all financial and executive pay data from Compustat and Execucomp, respectively. We derived our measures of corporate governance from the Institutional Shareholder Services (ISS). Our data cover firms in the S&P 1,500, constituting approximately 90% of the market capitalization of U.S. stocks (S&P Global, 2021). The number of firms in our sample exceeds 1,500 because of firms joining and being dropped from the S&P 1,500 index. Our results are consistent when examining only the firms in the S&P 1,500 at the beginning of our time period.

As our dependent variable, we use the number of times (i.e., the count) that the firm was sanctioned, based on Violation Tracker data, which we describe more fully below. After combining the Violation Tracker data with our other data, our analysis is based on a dataset comprised of 17,022 observations for 1,900 firms for the years 1999 to 2016. While we do not have data on the actual date of the alleged wrongdoing, we follow previous research by assuming it was 2 years immediately preceding the announcement of the sanction (Harris & Bromiley, 2007). Accordingly, all control and independent variables cover the period from 1999 to 2014, while our dependent variable covers the period from 2001 to 2016. In addition, our results are consistent when assuming that the date of the alleged wrongdoing preceded the sanction by 3 years (i.e., when our dependent variable covers the period from 2002 to 2016).

Dependent Variable

Previous research has defined wrongdoing operationally, that is, behavior that a social-control agent judges as transgressing the line separating right from wrong (Greve et al., 2010; Palmer, 2012). The critical aspect of this definition is that a social-control agent determines the extent to which a behavior is designated as wrongdoing, and how to sanction the organization for this wrongdoing.

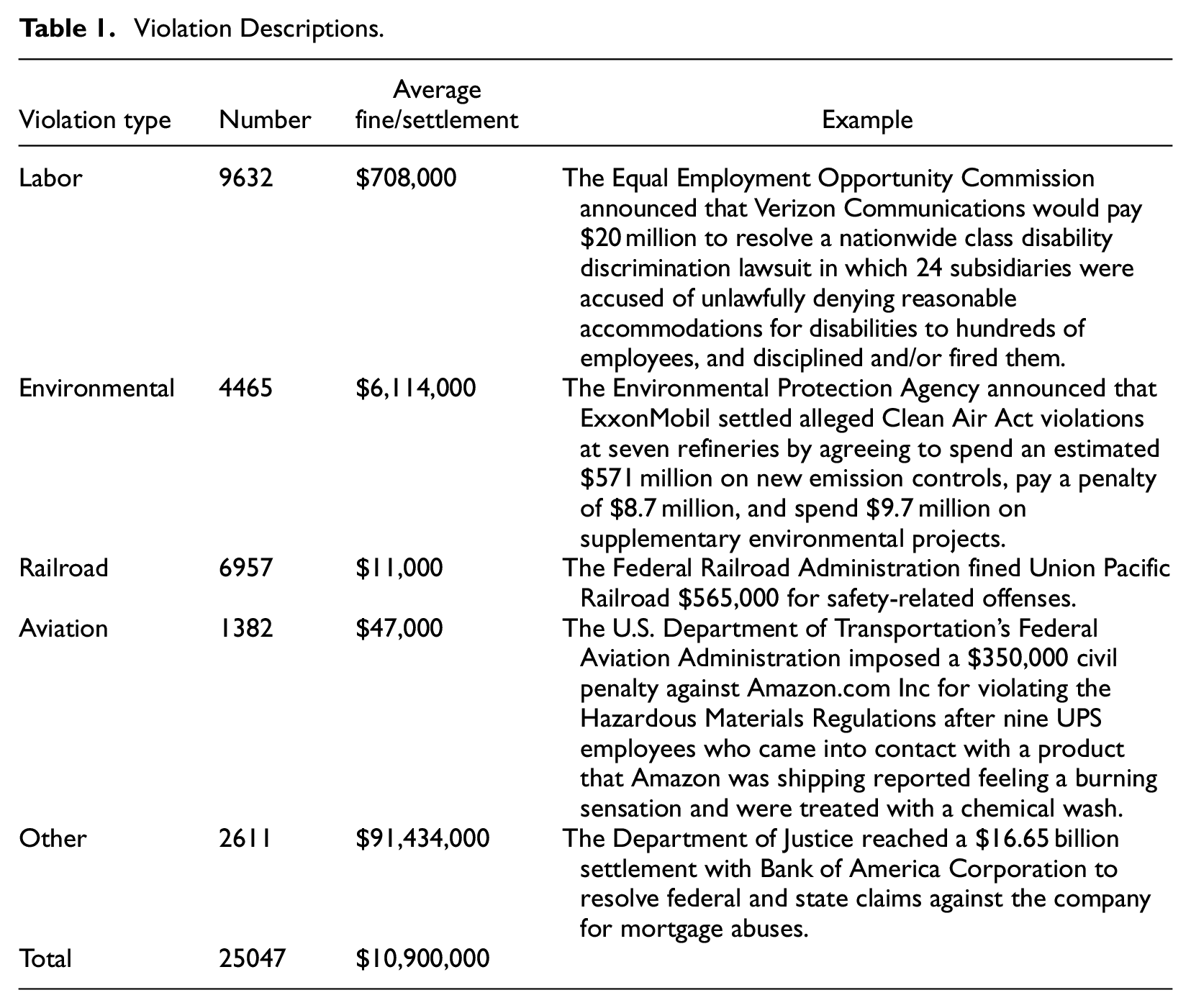

To measure organizational wrongdoing, we use data from the Violation Tracker database. Violation Tracker covers wrongdoing adjudications by more than 40 federal regulatory agencies of the U.S. government, and all parts of the U.S. Justice Department. These adjudications fall into the categories of banking, consumer protection, false claims, environmental, wage and hour, health, safety, employment discrimination, price-fixing, bribery, and other cases resolved since 2000. They also include state attorney general cases. Violation Tracker collects data directly from government regulatory websites, such that it should directly track what those social-control agents judge to be wrongdoing. Because these are sanctions imposed by government agencies, these directly track our definition of behavior that a social-control agent determines to be wrongful. In total, the firms in our sample were sanctioned 25,047 times by social-control agents (i.e., government agencies) during our time period.

We also examined whether the type of wrongdoing affected our results. The most common types of sanctions were for labor (39%) and environmental (18%) violations. Using either of these as an alternative dependent variable gave us consistent results. Our results were also robust when using only aviation sanctions as our dependent variable, which account for approximately 6% of all violations. Accordingly, our results are applicable to being sanctioned for violations in general, and not just for a specific type of violation. Table 1 provides a summary of our violation data, and an example of each type.

Violation Descriptions.

Explanatory Variables

As our baseline independent variable (FOF), we use the combined and augmented sample from Anderson et al. (2009, 2012) for the years 2001 to 2010. This data is publicly available from those researchers. For subsequent years, we followed the same procedure as those authors in measuring FOFs based on family ownership. Specifically, we define FOFs as those where the family (founders or founders’ descendants) maintains a 5% or greater ownership stake. We use a binary variable equal to one when families hold a 5% or larger ownership stake, and zero otherwise. Previous research has repeatedly used the 5% threshold as a measure of control (e.g., Hambrick & Finkelstein, 1995), including large, public FOFs, such as those in our sample (Zellweger et al., 2012). We note that our definition is aligned with many other studies of publicly traded family firms (e.g., Anderson & Reeb, 2004; Cannella et al., 2015; Faccio & Lang, 2002; Leitterstorf & Rau, 2014; Villalonga & Amit, 2006). In the Robustness section, we describe other measures of FOFs that we used, all of which provided largely consistent results.

PRA is calculated as firm performance minus aspirations, using either social aspirations (i.e., the performance of comparable organizations) or historical aspirations (i.e., the organization’s past performance) (e.g., Smulowitz et al., 2020). We follow (Greve, 2003) and combine social and historical aspirations through weighting, constructing our final measure of PRA as: PRA = (0.8 × social aspirations) + (0.2 × historical aspirations). In the Robustness section, we discuss possible alternative measures of PRA.

We measure social aspirations by the industry (two-digit Standard Industrial Classification [SIC] code) 1 median return on assets (ROA) (Mezias et al., 2002; Miller & Bromiley, 1990) and calculate PRA as the difference between firm performance and industry median ROA in the year before (time t− 1). We calculate historical aspirations as performance the year before (i.e., ROA), and calculate PRA as the difference between current year performance and previous year performance. Due to lagging, historical PRA is the difference between the firm’s performance in t − 1 and t − 2. Due to theorizing that exceeding and falling below aspiration levels have different effects, we create different variables for negative and positive PRA. We calculate negative PRA as zero if PRA is positive, and equal to PRA if it is negative. In a similar way, we calculate positive PRA as zero if the PRA is negative, and equal to the PRA if positive. As such, our variables show by how much the firm exceeds or falls below aspirational level. These measures follow previous research (e.g., Smulowitz et al., 2020). Also, to ease interpretation, we reverse code negative PRA (i.e., we multiple it by −1), such that as the difference between performance and aspired performance grows larger, this value will increase.

Control Variables

We include numerous variables that might affect the incidence of organizational wrongdoing for various reasons, controlling for these effects using our control variables.

Larger firms and those with higher debt could feel greater strain, leading to more wrongdoing. As such, we control for firm size measured as the log of total assets, and leverage calculated as the firm’s long-term debt divided by total assets. We also control for R&D expenditure (logged) as an alternative measure of risk-taking (Bromiley et al., 2017). We obtained these data from Compustat. External monitoring could also affect the firm’s level of wrongdoing (Aguilera et al., 2015). Accordingly, we control for analyst coverage measured as the number of analysts who followed the firm in a given year (Luo et al., 2015). We derived this data from Bloomberg. In addition, as large external shareholders could provide external monitoring, we control for the existence of a blockholder measured as the stock percentage owned by the largest (nonfamily) shareholder. We derived this data from Compustat.

The quality of a firm’s corporate governance could affect its likelihood of wrongdoing. Therefore, we control for board independence, measured as the number of independent directors divided by the total number of board members, board size as the total number of board members, and duality as a binary variable equal to 1 if the CEO and Chair are the same person, 0 otherwise. We obtained these data from ISS. CEO ownership and age could affect a CEO’s motivation to maximize long-term shareholder value (Fama & Jensen, 1983). As such, we include CEO ownership measured as the percent of voting shares the CEO holds, and CEO age (logged) control variables. Again, we obtained these data from ISS. Furthermore, a change in CEO could affect the incidence of wrongdoing. Accordingly, we control for CEO turnover. We derived this variable from Execucomp.

Previous research has shown that large cash balances can increase managerial discretion (Deb et al., 2017). As such, we control for available slack (logged) measured as the firm’s cash and short-term securities (Souder & Bromiley, 2012). More complex firms might have a higher incidence of wrongdoing, because they are more difficult to monitor. Accordingly, we use a firm complexity variable calculated as the Herfindahl index for firm subsidiaries and subsidiary industries (e.g., Loughran & Mcdonald, 2014). A higher score would correspond to more subsidiaries in different industries (based on SIC codes), and therefore greater complexity. We obtained these data from Compustat.

Different elements of pay could affect managers’ incentives to commit wrongdoing (e.g., Wowak et al., 2015). Accordingly, we control for CEO cash pay, the total current salary and short-term bonus, and long-term pay, the value of stock options, restricted stock, and other long-term incentives (Manner, 2010). In alternative models, we control for each of these elements of CEO pay individually and use alternative measures of long-term pay (e.g., Flammer & Bansal, 2017), with consistent results. As our controls for option pay, we use unexercisable options measured as the aggregate value of unvested stock options, and exercisable options measured as the aggregate value of positively valued vested stock options (e.g., Devers et al., 2008). To address skewness and kurtosis, and improve model fit, we take the natural log of all compensation variables.

Finally, we control for firm age, which we calculate as the difference between the year of incorporation and the data observation year. We include year dummy variables to control for the influence of specific years and other time-dependent variations, and to resolve the issue of contemporaneous correlation in panel data (Certo & Semadeni, 2006). We also control for industry using dummy variables. Our industry controls are based on the 12 Fama-French industries (Fama & French, 1997). Our results are consistent when using SIC industry dummies.

Estimation Methods

Due to the count and panel structure of our data, we use a count panel data model. Specifically, we take advantage of the panel structure of our data to perform a Poisson regression with random effects. Here, a random effects model is preferable to a fixed effects model because the latter automatically discards organizations that do not vary in the dependent variable, only modeling within-organization deviations from the firm-level mean. This would result in a very biased sample, that is, only firms that changed from FOF to NFOF or vice versa, meaning only a tiny fraction of our sample. We include both types in our analysis to maximize generalizability.

We also note that our main analyses rely on interaction terms, which are much less likely to suffer from endogeneity concerns. For example, Bun and Harrison (2019) find that for regression models including endogenous interaction terms, the estimator of the coefficient of the interaction term is consistent, and standard inference applies. Also, in all our models, we standardize all nonbinary variables with a mean of 0 and standard deviation of 1 for ease of interpretation (Combs, 2010). Our results are robust to nonstandardizing.

Results

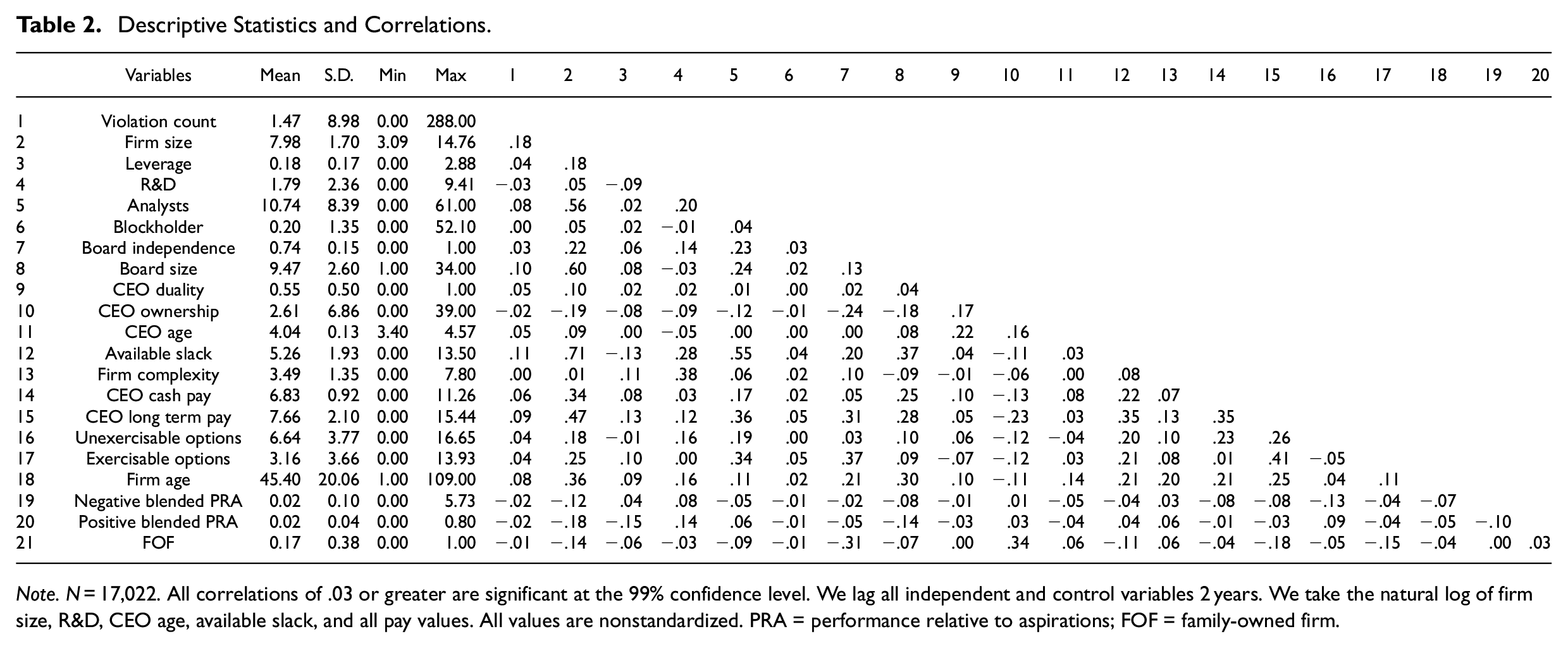

Table 2 reports the summary statistics and correlations for our dependent, explanatory, and control variables. The maximum variance inflation factor (VIF) for the variables specified in our models is 4.26, and the mean VIF is 1.53. Accordingly, multicollinearity is not a concern.

Descriptive Statistics and Correlations.

Note. N = 17,022. All correlations of .03 or greater are significant at the 99% confidence level. We lag all independent and control variables 2 years. We take the natural log of firm size, R&D, CEO age, available slack, and all pay values. All values are nonstandardized. PRA = performance relative to aspirations; FOF = family-owned firm.

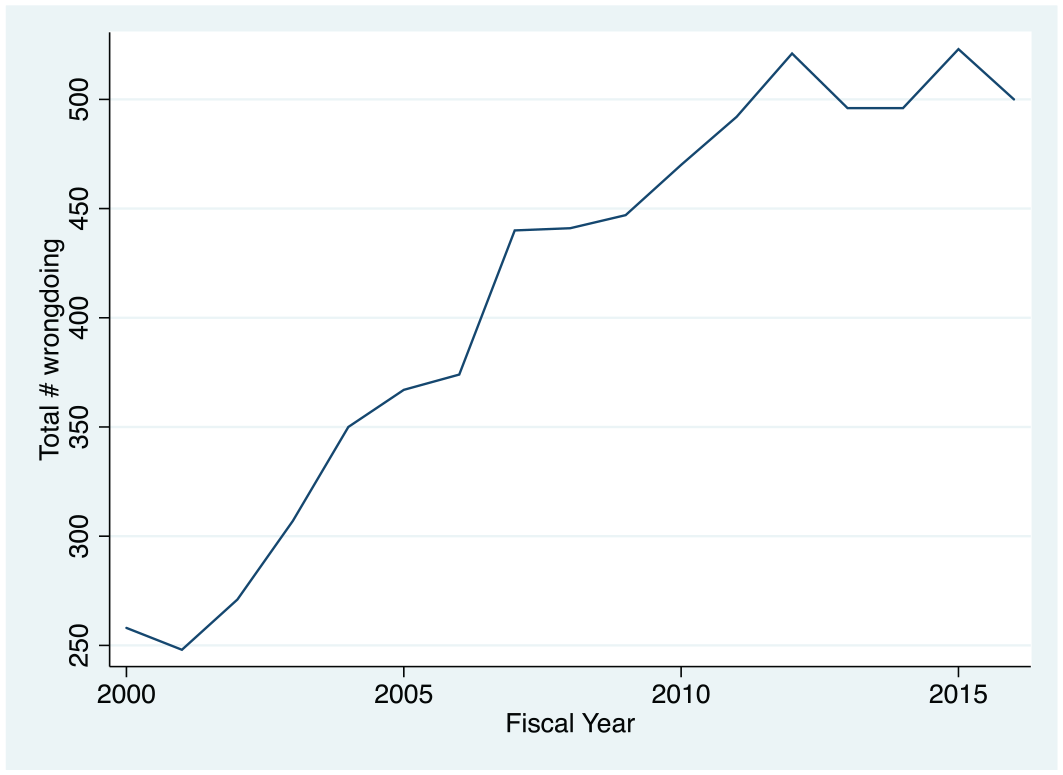

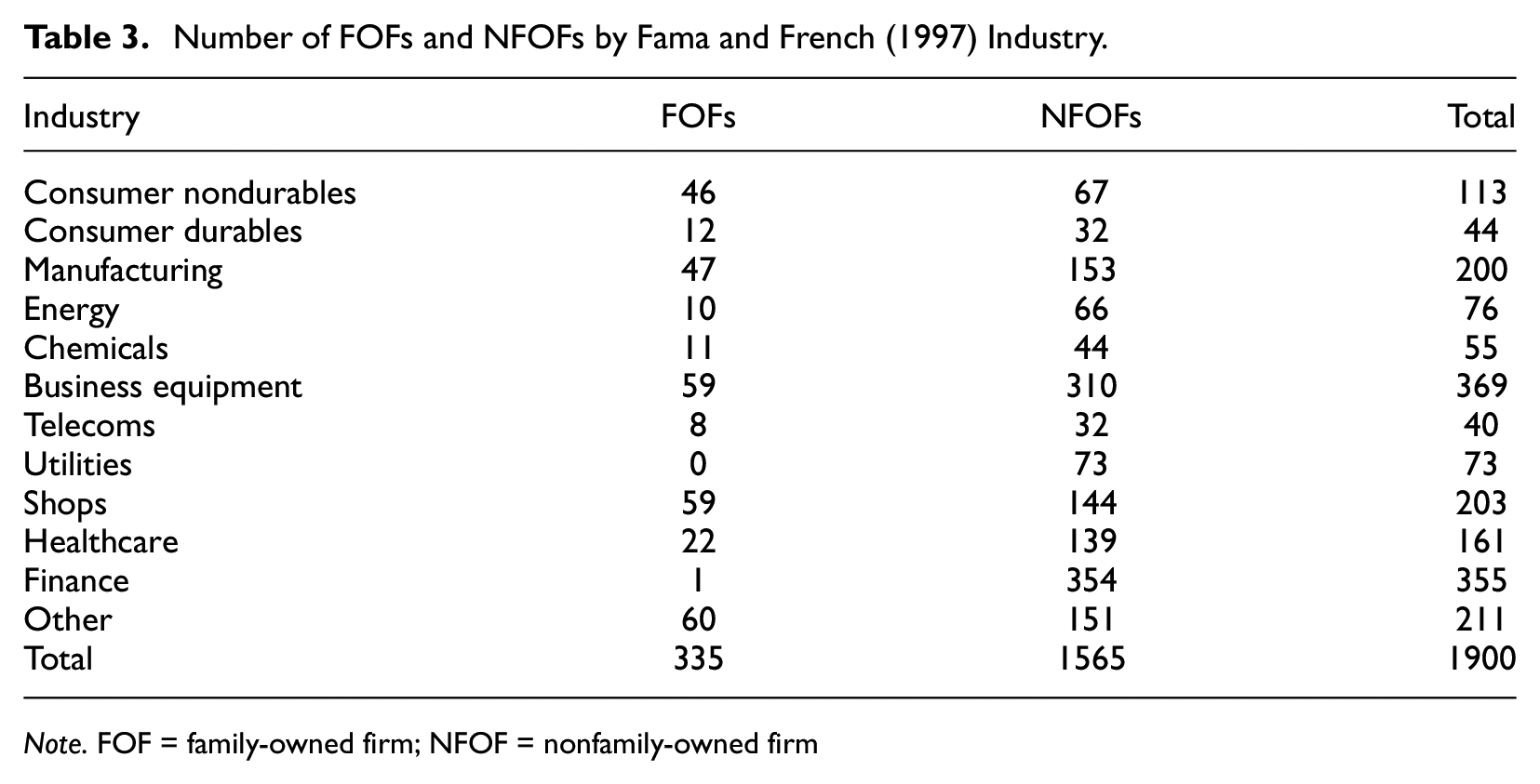

Initially, we note that there are significant time effects of wrongdoing. That is, the overall incidence of wrongdoing has been greatly increasing over time (Figure 2). We also note that there are large differences by industry as to which firms are FOFs. We report our sample by FOF and industry status in Table 3. For example, only one firm in the financial industry is a FOF, while 46 firms (approximately 41%) of firms in the consumer nondurables industry are FOFs.

Total incidences of wrongdoing in sample of firms over time.

Number of FOFs and NFOFs by Fama and French (1997) Industry.

Note. FOF = family-owned firm; NFOF = nonfamily-owned firm

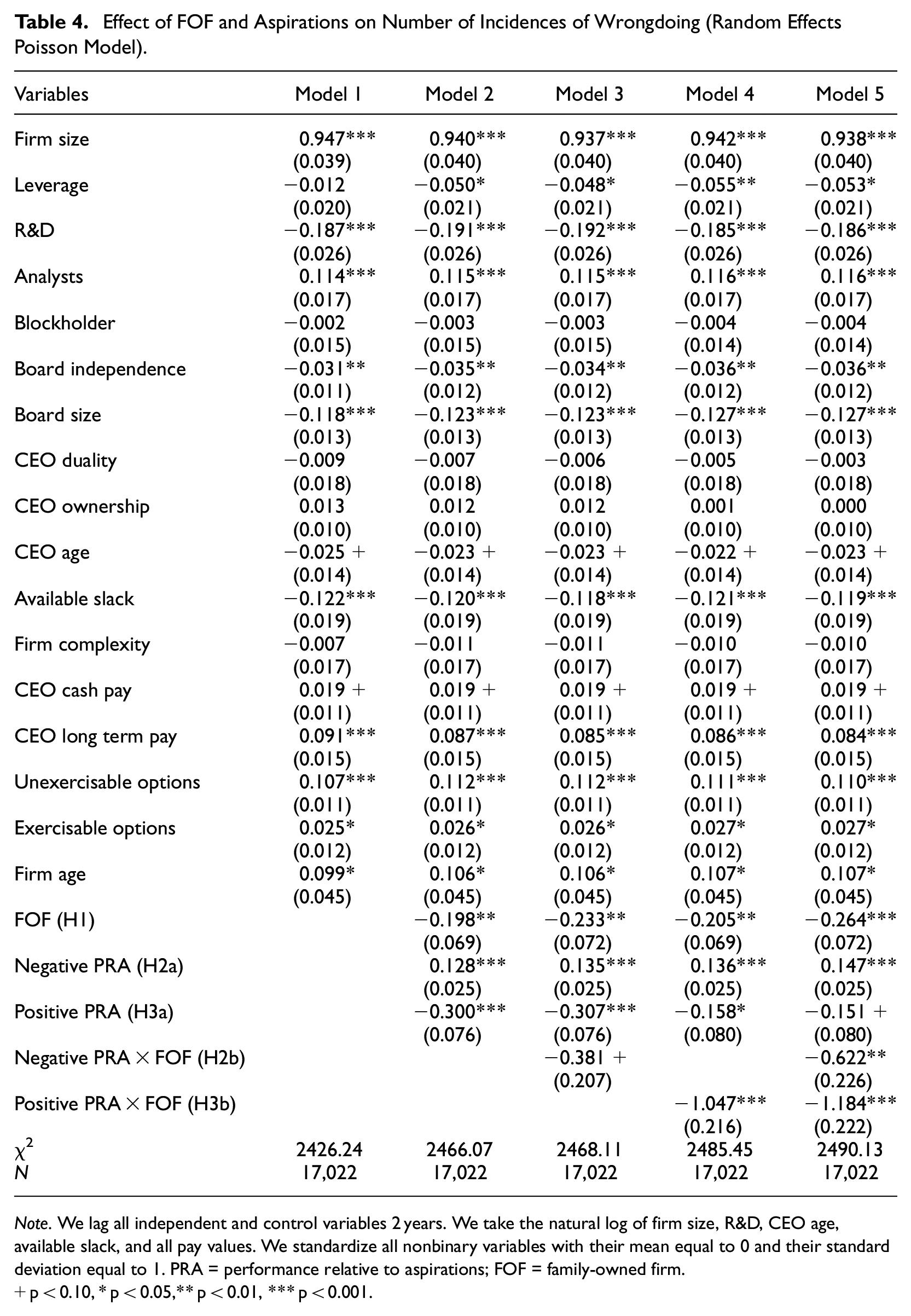

Table 4 presents the results of our Poisson regression analyses testing our hypotheses using FOF as our main independent variable. We show our results in a hierarchical fashion. Moving to our regression analyses, several control variables are significantly related to wrongdoing. Specifically, in the fully saturated model (Model 5 of Table 4), firm size has a significant and positive effect on wrongdoing, meaning that larger firms are more likely to commit wrongdoing. Leverage and R&D spending are significantly and negatively related to wrongdoing, indicating that firms with debt may be subject to greater scrutiny from debt holders and that more innovation-intensive firms may be less likely to commit wrongdoing. Analyst coverage is positively and significantly related to wrongdoing, implying that the so-called “quarterly earnings race” or “earnings pressure” (Brauer & Wiersema, 2018) could lead to more wrongdoing. Board independence and board size are negatively and significantly related to wrongdoing, implying that good corporate governance practices can reduce wrongdoing. Available slack is negatively and significantly related to wrongdoing, supporting the idea that strain can lead to more wrongdoing (i.e., slack can reduce strain). Finally, various elements of CEO pay are also positively related to wrongdoing. This supports the view that pay schemes have the negative side effect of encouraging more wrongdoing (Smulowitz & Almandoz, 2021).

Effect of FOF and Aspirations on Number of Incidences of Wrongdoing (Random Effects Poisson Model).

Note. We lag all independent and control variables 2 years. We take the natural log of firm size, R&D, CEO age, available slack, and all pay values. We standardize all nonbinary variables with their mean equal to 0 and their standard deviation equal to 1. PRA = performance relative to aspirations; FOF = family-owned firm.

p < 0.10, * p < 0.05,** p < 0.01, *** p < 0.001.

Moving to our hypotheses, H1 predicts that in FOFs, the incidence of wrongdoing will be lower than in NFOFs. Consistent with H1, in our fully saturated model (Model 5 of Table 4), the coefficient of our FOF variable is negative and highly significant (b = −0.264, p < .001). This p-value indicates that we can be confident that the observed parameter differs from 0. In terms of practical effects, the effect of FOF on wrongdoing depends on its interaction effect with various variables (see below). However, when those variables are held constant at their mean, our model suggests that FOFs commit on average 0.17 incidents of wrongdoing per year. 2 By comparison, all firms in our sample commit (on average) 1.47 incidents per year, meaning that FOFs commit 1.30 fewer incidents of wrongdoing per year than NFOFs. Thus, we find strong support for H1.

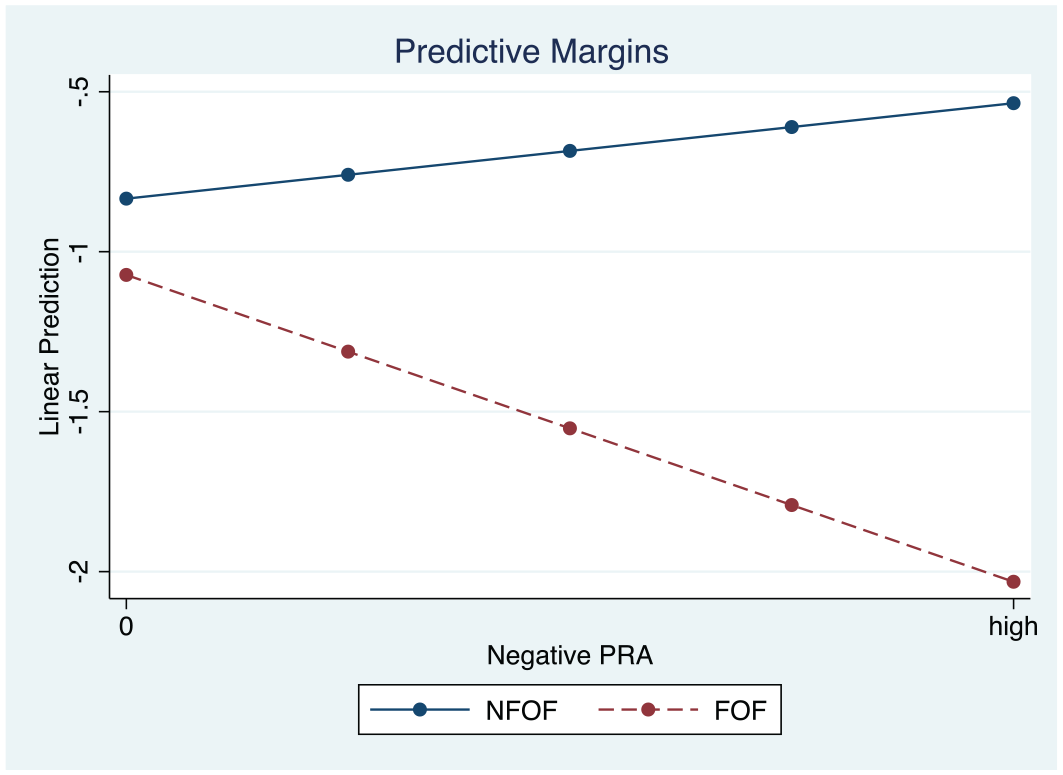

H2a predicts that negative PRA will increase the incidence of wrongdoing. Consistent with H2a, in the fully saturated model (Model 5 of Table 4), the coefficient of our negative PRA is positive and significant (b = 0.147, p < .001). H2b predicts that in the case of FOFs, negative PRA will reduce the incidence of wrongdoing. Consistent with H2b, in Model 5 of Table 4, the coefficient of the interaction term between FOF and negative PRA is negative and significant (b = −0.610, p < .01). We further examine H2b by plotting the interaction effect between FOF and negative PRA at zero and high levels. We define “high” as 2 standard deviations above the mean for this variable. 3 The graph (Figure 3) shows that negative PRA increases the incidence of wrongdoing for NFOFs. However, for FOFs, negative PRA actually decreases the incidence of wrongdoing.

Effect of FOF and negative aspirations on wrongdoing.

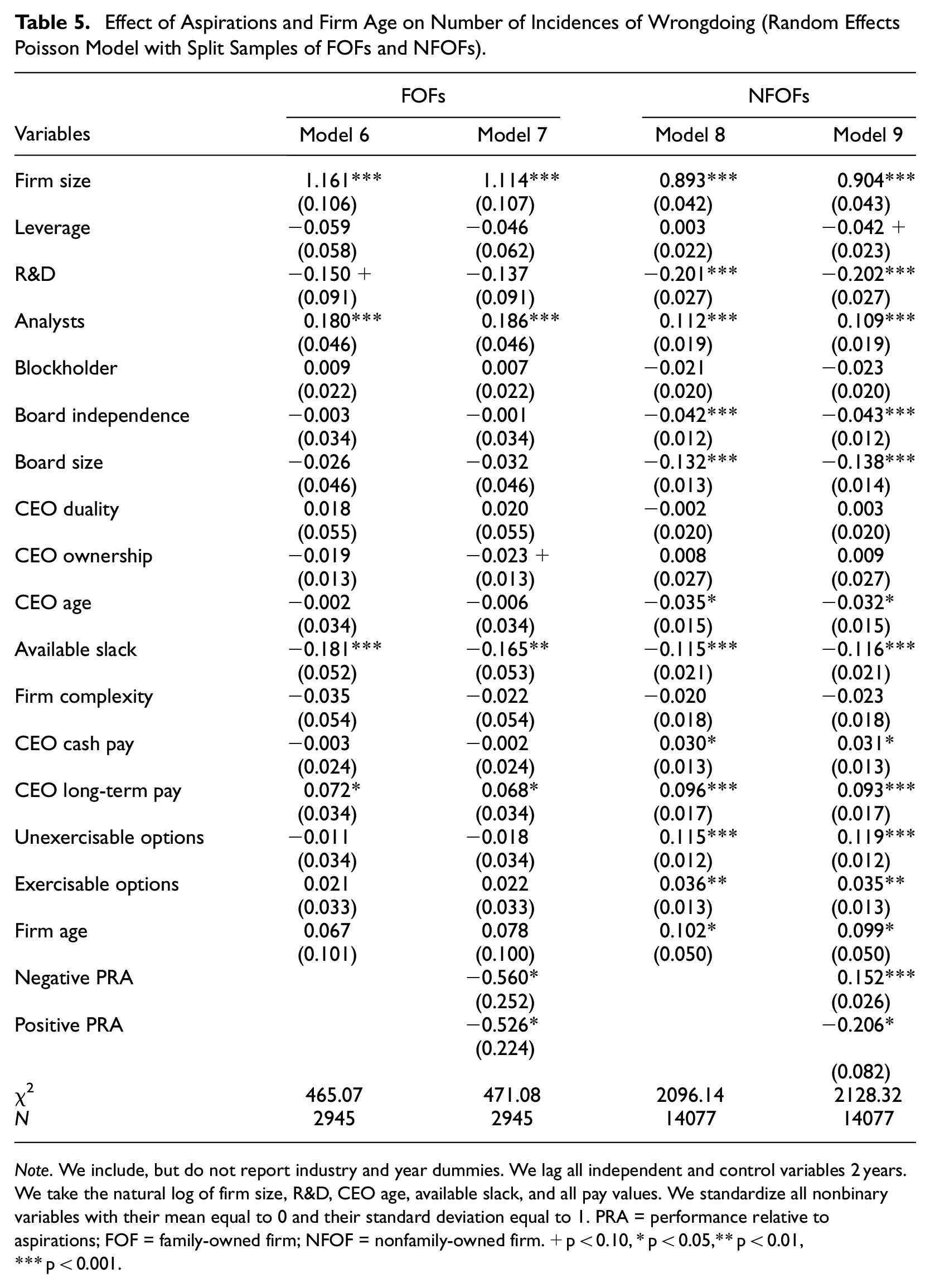

To further test H2a and H2b, we created a split sample of family and NFOFs (Table 5). Our results show that for our sample of FOFs, the coefficient of negative PRA is negative and significant (b = −0.560, p < .05), while for NFOFs, the coefficient of negative PRA is positive and significant (b = 0.152, p < .001). That is, negative PRA increases the incidence of wrongdoing for NFOFs, but decreases the incidence of wrongdoing for FOFs. Thus, we find strong support for H2a and H2b.

Effect of Aspirations and Firm Age on Number of Incidences of Wrongdoing (Random Effects Poisson Model with Split Samples of FOFs and NFOFs).

Note. We include, but do not report industry and year dummies. We lag all independent and control variables 2 years. We take the natural log of firm size, R&D, CEO age, available slack, and all pay values. We standardize all nonbinary variables with their mean equal to 0 and their standard deviation equal to 1. PRA = performance relative to aspirations; FOF = family-owned firm; NFOF = nonfamily-owned firm. +p < 0.10, * p < 0.05,** p < 0.01, *** p < 0.001.

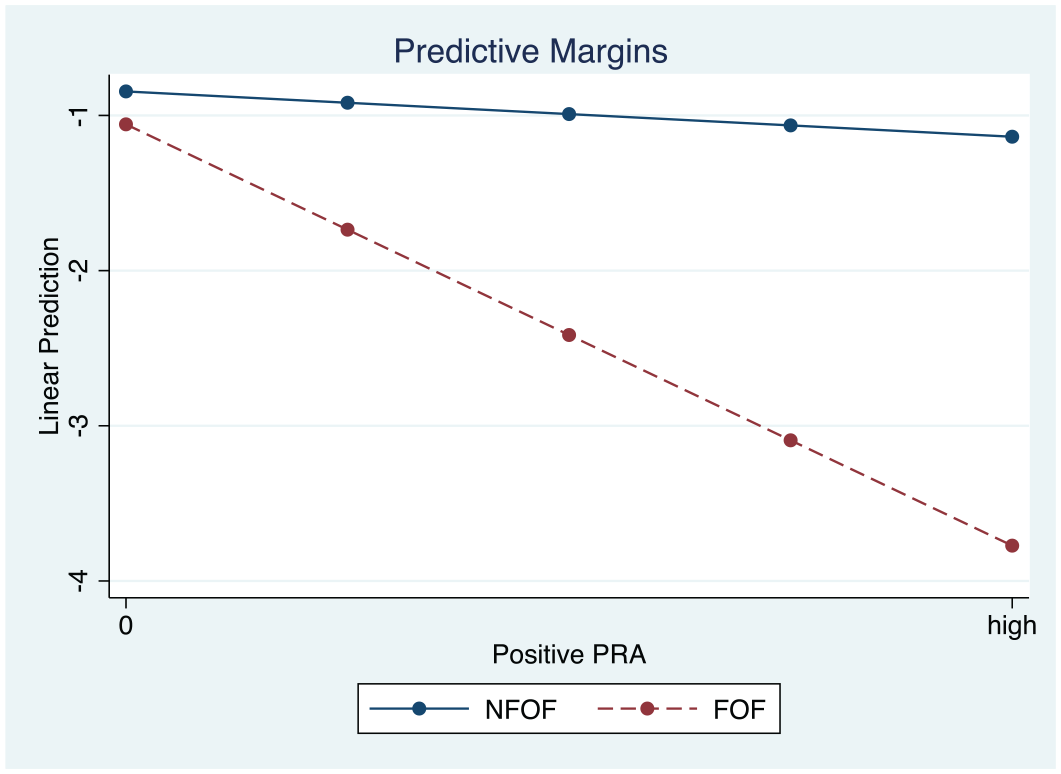

H3a predicts that positive PRA will reduce the incidence of wrongdoing. In the fully saturated model (Model 5 of Table 4), the coefficient of our positive PRA variable is negative and significant (b = −0.151, p < .10). H3b predicts that in the case of FOFs, the effect of positive PRA on the incidence of wrongdoing will be strengthened, reducing the incidence of wrongdoing even further. In the fully saturated model (Model 5 of Table 4), and the coefficient of the interaction term between FOF and positive PRA is negative and significant (b = −1.184, p < .001). Moreover, the graph of the interaction effect between FOF and positive PRA (Figure 4) shows that the incidence of wrongdoing decreases for both FOFs and NFOFs as positive PRA increases. However, this effect is much larger for FOFs (i.e., the line is much steeper). Accordingly, the reduction in wrongdoing from positive PRA is largely attributable to a reduction in wrongdoing by FOFs.

Effect of FOF and positive aspirations on wrongdoing.

To further test H3a and H3b, we again examined our split sample of FOFs and NFOFs (Table 5). Our results show that for both FOFs and NFOFs, the coefficient of negative PRA is negative and significant (b = −0.526, p < .05; b = −0.206, p <.05, respectively). However, the coefficient of our positive PRA variable in the FOF sample is more than twice that of our positive PRA variable large as in the NFOF sample, meaning that the effect in our sample of FOFs is much stronger. This is entirely consistent with the relationship we show in Figure 4. Thus, we find strong support for H3a and H3b.

Robustness Checks

First, we tested to see whether our measure of FOFs affected our results. Specifically, we replaced our binary FOF measure with a continuous variable based on the degree of family ownership. Our results remained robust. We also replaced our FOF measure with a measure based on whether the firm met a 10% and then 20% ownership threshold. Even though these thresholds greatly reduced the number of firms that we classified as FOFs, our results remained consistent. Also, prior research has shown that lone founder firms behave differently from family firms (e.g., Cannella et al., 2015). Lone founder firms are defined as those where no other person related to the founder was a significant shareholder, director, or officer (Markin et al., 2022; Miller et al., 2007). We excluded lone founder firms from our sample, and had consistent results. Finally, we also replaced our FOF measure with a measure based on whether the firm both met the 5% family ownership threshold and had at least two family managers and/or members of the board of directors. This highly restrictive definition greatly reduced the number of firms that we classified as FOFs, hence greatly reducing our variance. While using this highly restrictive definition, our results were still supported for H2a, H2b, H3a, and H3b. However, the coefficient of our variable for FOFs was no longer statistically significant. We attribute this lack of significance to our reduction in variance due to our restrictive definition of FOFs.

Second, we follow a large stream of literature that has combined social and historical aspirations (e.g., Blettner et al., 2015; Greve, 2003; Mezias et al., 2002). However, we note that our results were highly consistent when using either historical or social aspirations independently. Moreover, our results were consistent when combining historical and social aspirations with numerous different weightings.

Third, while we believe that the selection of our control variables makes sense theoretically and empirically, and is widely accepted in management literature, the use of a large number of controls raises the possibility of over-fitting. Accordingly, we also re-ran our analyses using only year and industry controls. The use of this more limited set of controls did not change our substantive results, thereby mitigating concerns of over-fitting, and providing further evidence that collinearity is not affecting our results (Kalnins, 2018).

Fourth, it is possible that an unknown, omitted variable could be affecting our results. To assess the likelihood of such an omitted variable existing, we wanted to determine how strong a correlated omitted variable would have to be to overturn our results. We did so by calculating the impact threshold of a confounding variable (ITCV) for our measure of FOF and our interaction terms (Busenbark et al., 2022; Frank, 2000; Larcker & Rusticus, 2010). Here, the ITCV indicates that, for omitted variable bias to affect our findings, an omitted variable would need to overturn the effect of the interaction of FOF and negative PRA on wrongdoing in over 4,906 of the cases (approximately 28.8% of all observations). Similarly, an omitted variable would need to overturn the relationship between the interaction of FOF and positive PRA on wrongdoing in over 10,766 of the cases (approximately 63.3% of all observations). This is extremely unlikely. Accordingly, omitted variable bias does not seem to be a concern. All these robustness tests are available upon request.

Discussion

The BTOF is one of the most important theories in organization and management studies, and an important theoretical perspective in the study of wrongdoing in organizations. At the same time, the wrongdoing behavior of FOFs has been the focus of a growing body of research (e.g., Berrone et al., 2010; Ding et al., 2016; Yang, 2010) and prior research has argued that the propensity of family owners to pursue family-centered noneconomic goals is likely to influence their aspirations and behavior (e.g., Chrisman et al., 2012; Gómez-Mejía et al., 2007; Gomez-Mejía et al., 2018). However, existing research integrating the additional SEW aspiration into BTOF predictions has failed to account for the difference between productive and destructive risks associated with firm behavior. Taking into account this important distinction, and the distinctive aspirations of family owners, we have developed and tested new theorical arguments, and shown that BTOF predictions regarding FOFs can differ markedly from those for NFOFs.

Our longitudinal study of 1,900 publicly traded U.S. firms supports our prediction that family owners’ aspirations play an important role in wrongdoing in organizations and reveals that BTOF predictions in FOFs are more complex than previously thought. First, we show that in FOFs there is a lower incidence of wrongdoing than in NFOFs. Second, we show that the increasing effect of being below aspirations on wrongdoing is positive in NFOFs, while (contrary to traditional BTOF predictions) it is negative in FOFs. Third, we show that the effect of being above aspirations on the incidence of wrongdoing is negative (i.e., positive PRA is associated with a decrease in wrongdoing), and that the effect of positive PRA in reducing wrongdoing is strengthened in FOFs (i.e., positive PRA reduces wrongdoing even more in FOFs than in NFOFs). Overall, our findings support our contention that FOFs respond differently from NFOFs to risks because in addition to concern for economic costs and benefits, FOFs are uniquely concerned with the SEW accruing from the noneconomic costs and benefits of their actions. Furthermore, our theory and evidence illustrate that the differences in the behavior are dependent upon whether the nature of risk associated with a behavior is destructive, as in the case of wrongdoing, versus productive, as in the case of other previously examined behaviors.

Contribution and Implications

Our study provides several important contributions. First, we contribute to research on the effect of SEW on FOF decision-making under risk. Previous research has built on the mixed gamble approach to show that, when the firm is under threat, FOFs will risk their SEW in pursuit of financial gains (e.g., Gómez-Mejía et al., 2007; Gomez-Mejía et al., 2018). However, we predict and show that FOFs will respond differently to PRA regarding behaviors associated with destructive risk (specifically wrongdoing) as compared to behaviors associated with productive risk (such as R&D investment, diversification, or internationalization) because the potential losses and gains to SEW are very different. We thereby advance the literatures on SEW and FOFs by explaining how family owners’ decision and behaviors change depending on the type of risk associated with behavior—destructive, as in the case of wrongdoing versus productive, as in the case of other behaviors that have been the object of investigation in prior research. Thus, our study contributes to research by underscoring the importance of considering the type of risk associated with a given behavior (Baumol, 1996). Specifically, our paper shows that FOFs respond to PRA regarding wrongdoing differently from the responses regarding other behaviors examined in prior studies. This theoretical refinement extends the mixed gamble approach to account for differing types of risk, and how family owners will engage in them, when a FOF is threatened.

Second, we develop new theorical arguments relating to the behavioral aspects of wrongdoing in firms. While BTOF predictions of the effect of aspirations on firm risk-taking are some of the most widely studied in management research, research has only begun to incorporate the idea that firms can have multiple aspirations, and that this can alter BTOF predictions. For example, Smulowitz et al. (2020) find that a community orientation causes firms to take fewer risks in response to negative PRA, but to invest more in the community in response to positive PRA. However, while “the aspirations of family-influenced or controlled firms greatly complicate the governance challenge” (Steier et al., 2015 p. 1267), prior research has not yet incorporated this additional aspiration into BTOF predictions regarding wrongdoing. Here, we advance the BTOF, particularly in relation to wrongdoing, by introducing SEW as an additional aspiration to provide a more complete theory of firms’ wrongdoing decisions.

The additional SEW aspiration challenges the assumed cost/benefit analysis in prior work (Harris & Bromiley, 2007; Xu et al., 2019), that being below aspirations should lead to more wrongdoing. Specifically, diverging from studies showing that being below aspirations leads to more wrongdoing, we predict and show that the SEW aspiration reverses this effect. We argue that this is due to a different calculation of losses and gains for FOFs, where, for instance, poor performance combined with wrongdoing would have a devastating effect on the firm’s (and thereby the family’s) reputation. Thus, our findings pave the way for a more comprehensive understanding of the effect of negative PRA on firm risk. Moreover, research is largely ambiguous about the effect of being above aspirations on wrongdoing. By theorizing that the combined effect of SEW and positive PRA makes the potential costs of wrongdoing more damaging to the family, our study clarifies and explains why being above aspirations can have a negative effect on wrongdoing.

Overall, we predict and show that the importance of SEW will increase the cost of wrongdoing as a viable response to both negative and positive PRA, thereby resulting in negative PRA reducing wrongdoing in FOFs (while it increases wrongdoing in NFOFs), and positive PRA reducing wrongdoing even more in FOFs than in in NFOFs. These theoretical refinements extend the BTOF by showing that when SEW aspirations are taken into account, its predictions regarding wrongdoing are very different.

Third, wrongdoing is a specific dimension of CSR which, different from other dimensions, is enforced by a social-control agent, and is associated with destructive rather than productive risk. As such, our study’s findings hold implications for the study of CSR by revealing that different CSR dimensions can be associated with different trade-offs and risks, and the relative importance of CSR economic and noneconomic responsibilities and outcomes swings according to the type of risks (and trade-offs) associated with those responsibilities. Thus, our study’s findings extend the CSR literature by cautioning scholars to take into account the differences in the types of risks associated with different CSR dimensions, and the effects of such differences.

Lastly, we contribute empirically to current research on wrongdoing in FOFs. On the one hand, several studies have examined the effect of family ownership on wrongdoing in small private U.S. firms (Ding & Wu, 2014) and international firms (Ding et al., 2016). On the other hand, studies have tested their predictions using only a single type of wrongdoing, such as bribery (Ding et al., 2016). We add to these studies by showing that being a FOF (and SEW) affects wrongdoing in general, and in a very large sample of the largest, publicly listed U.S. firms. Specifically, we use a comprehensive sample of wrongdoing events consisting of the full list of sanctions by U.S. governmental agencies to extend the findings of previous studies to wrongdoing in general, and to a sample of the largest, most prominent firms in the world.

In sum, our study contributes to both research in FOFs and to the BTOF by introducing important theoretical refinements. These refinements add the importance of the type of risk associated with behavior to fully understand predictions of how family owners will respond under risk. They also substantially improve the predictive power of the BTOF by highlighting the role of additional aspirations (i.e., SEW) and expanding the BTOF for a more complex understanding of wrongdoing and risk-taking decisions in organizations with family ownership.

Limitations and Opportunities for Future Research

Our study faces limitations that future research should seek to address. First, due to data limitations, we were unable to definitively distinguish in all cases between occupational crime (e.g., stealing from employers or customers) and corporate crime (e.g., committing fraud on behalf of the organization) (e.g., Mishina et al., 2010; Smulowitz & Almandoz, 2021). The distinction is that only in the latter case will the firm potentially benefit in some way from the wrongdoing committed, and the implication of the distinction is that family ownership could relate differently to the likelihood of each type of wrongdoing. To address this concern, we examined our hypothesized effects on numerous types of wrongdoing, with consistent results. For example, our results hold when examining labor, aviation, and environmental violations, which can only be viewed as corporate crimes (because the individual committing the crime does not benefit at the expense of the firm). However, a useful extension of our study would be exploring the degree to which different types of wrongdoing are affected differently by family ownership and aspirations.

Second, we use the incidence of wrongdoing actually discovered and prosecuted by government agencies as our dependent variable. Thus, we do not measure wrongdoing that is never discovered by these agencies or wrongdoing that is discovered but ignored by these agencies (Palmer, 2012). However, prior research has tied family ownership to a reduction in wrongful behavior that does not rely on being discovered and prosecuted. For example, studies show that family ownership reduces earnings management (Achleitner et al., 2014; Jiraporn & DaDalt, 2009; Siregar & Utama, 2008; Stockmans et al., 2013; Yang, 2010), and tax aggressiveness (Chen et al., 2010; Steijvers & Niskanen, 2014). Accordingly, this prior research provides evidence that our results are being driven by actual firm wrongdoing, and not the idiosyncratic choices of social-control agents.

Third, our paper is limited to publicly listed U.S. firms. Although our BTOF refinements consider differences between FOFs and NFOFs regardless of their listing status, the generalizability of our findings to private firms remains an open empirical question. Indeed, we know that findings gathered from publicly listed FOFs may not apply to privately held FOFs (e.g., Carney et al., 2015). Moreover, firms outside the U.S. may be more prone to engaging in wrongdoing as a result of more relaxed standards in their countries (Ding et al., 2016), and internationalization also increases complexity, both potentially affecting the incidence of wrongdoing. However, we note that other studies have examined the effect of family ownership on wrongdoing in the context of private U.S. firms (Ding & Wu, 2014), international firms (Ding et al., 2016), and firms in other large countries, such as China (Xu et al., 2019). Our study adds to these by showing the effect of FOFs (and SEW) on wrongdoing using a comprehensive measure of wrongdoing in a large sample of the largest U.S. firms. Nonetheless, future research using firms from diverse countries and with different listing status can extend our work in important ways by, for example, examining more nuanced differences in the effect of the institutional context on wrongdoing.

Fourth, we rely on the publication of wrongdoing by various government agencies as our measure of wrongdoing. The advantage of this measure is that we capture close to the universe of times that a firm in our sample was punished for organizational wrongdoing by these government agencies. A limitation of our measure of wrongdoing only captures the number of infractions. It does not capture the seriousness of the wrongdoing, the cost of the wrongdoing, or the visibility of the wrongdoing. This last point is the most important for family firms because it affects their reputation. For example, an incident of wrongdoing that is widely publicized in the press may do more damage to the reputation of the family than would a nonpublicized incident. Moreover, it could be that some types of wrongdoing are more likely to receive attention in the press than others. Accordingly, examining the likelihood that an incident of wrongdoing will receive press attention, and how that affects the incidence of wrongdoing in FOFs and NFOFs, would be a valuable extension of our study.

Fifth, a limitation of our study is common to most SEW literature, namely that we inferred the presence of SEW by using family firm ownership. Indeed, directly measuring an owning family’s SEW is a complex and still mostly unaddressed task (e.g., Chua et al., 2015). We have shown how our results are robust to numerous measurements of family firms. However, like most prior research, we did not directly measure SEW. Accordingly, a potential valuable extension of our study would be to measure SEW more directly through, for example, a content analysis measure of firm communication (Berrone et al., 2012) or the employment of a scale (e.g., Debicki et al., 2016).

Sixth, another potentially fruitful avenue for future research is examining the effect of other types of firm ownership on wrongdoing. Here, we examined the effect of FOFs on wrongdoing, as these effects are highly likely to manifest given that family owners have prominent family-centered non-economic goals whose pursuance leads to SEW, and typically greater discretion to influence firm behavior. However, other types of owners might have very different goals and temporal perspectives (Thomsen & Pedersen, 2000). For example, hedge fund or venture capital owners generally have much shorter time orientations, and much less affective commitment to the firms they (partially) own. Accordingly, firms may respond to PRA very differently when these types of owners have the discretion to influence firm behavior. Thus, future research should examine the effect of different types of owners besides family ones.

Finally, as our study’s findings underscore the importance of considering the type—destructive versus productive—of risk associated with a given behavior in order to predict the distinctive behavior of family firms, we welcome future scholars to draw on our findings and explicitly consider the risks behind a behavior to develop more fine-grained predictions of FOFs’ versus NFOFs’ behaviors. As the distinction between the effect of productive and destructive risk is a missing aspect in family business research, future scholars can conduct more precise investigations of the distinctive behavior of FOFs versus NFOFs. For instance, future research can examine behaviors like CSR, that have been mainly studied at aggregate level, by distinguishing among its different possible dimensions and explicitly taking into account the destructive versus productive type of risk associated with each dimension.

Implications for Practice

Our study also has important implications for practice. Most obviously, our paper informs practitioners to consider the importance of aspirations in predicting wrongdoing. Boards of directors, regulators and investors should be aware that negative PRA often leads to increases in wrongdoing. Accordingly, as firm performance suffers, these monitors should be increasingly cognizant of the increased strain and risk-taking propensity of managers, and increasingly diligent in their oversight. However, if regulators are looking to best use their limited resources in investigating firms, they might be better served in focusing more on NFOFs where there is higher likelihood of wrongdoing.

In addition, by demonstrating that being a FOF does not increase the incidence of wrongdoing, and instead can actually decrease it, our results caution policymakers to take into account the importance of SEW considerations to understand wrongdoing. As the costs associated with wrongdoing are increasing, guidance from our research may be particularly useful. Indeed, our study can constitute a background policy document for policy makers. Actions to prevent wrongdoing are increasingly the subject of attention in the public domain and mass media. FOFs, due to their ubiquity (Anderson et al., 2009; Astrachan & Shanker, 2003), play a crucial role in the development of economies across the world (La Porta et al., 1999; Villalonga & Amit, 2006). Our research favors a better understanding of how to build a system of prevention initiatives in line with the idiosyncratic characteristics of FOFs and supports policy makers in their decisions on how to prevent wrongdoing behavior in the most ubiquitous form of business organization in any world economy.

For example, while new business formation surged during the pandemic, it has more recently dropped or plateaued, and often drops during recessions (Haltiwanger, 2022). Because most family firms are born and not made (Chua et al., 2004), the vast majority of new firms in the world are family firms and (by definition) young, the results of our study suggest that increased business formation should be a boon for reducing organizational wrongdoing overall. Accordingly, policy makers should encourage more new business formation not only for the economic benefits, but also because of the potential salutary effects on overall organizational wrongdoing.

Footnotes

Acknowledgements

We would like to thank Senior Editor Jim Chrisman and three anonymous reviewers for their highly constructive and developmental reviews. We thank the participants at the Southern Management Society Annual Conference for their very helpful feedback. Also, we are extremely grateful to Phil Bromiley, Yuri Mishina and Malgorzata Smulowitz for their crucial comments, constructive suggestions and invaluable criticism on earlier drafts of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.