Abstract

Keywords

Despite social safety net programs such as Social Security and the Earned Income Tax Credit (EITC), poverty continues to be a widespread problem in the United States. According to the U.S. Census (2022), 11.1% of Americans, or 36.8 million people, have household incomes below the US poverty line. Poverty is considered a social determinant of health (i.e., a broad range of social and environmental conditions that affect health and well-being) due to its association with significant health problems (Francis et al., 2018). It affects adult and child physical health by impacting access to safe housing, healthy foods, employment and educational opportunities, healthcare services, clean air and water, and a safe neighborhood environment (HHS OASH, November 4, 2024). Poverty disproportionately impacts racial and ethnic minorities (U.S. Census Bureau, 2024)

Financial stress and strain are often experienced by those living below and just above the federal poverty level ($31,200 annually for a family of four in 2024) (U.S. Department of Health and Human Services, 2024). Financial strain is experienced when experiencing negative income shocks and/or unexpected expenses occur, such as a health bill or car repair, even for households that regularly meet daily and monthly expenses (Ridley et al., 2020). About half of the US households have fewer emergency savings than the amount needed to cover expenses for 3 months in the absence of income, as recommended by financial planners (FINRA, 2022). In 2022, only 63% of adults could cover a hypothetical unexpected $400 expense using cash, savings, or a credit card paid off at the next statement (Board of Governors of the Federal Reserve System, 2023).

Financial stress and strain negatively affect health and well-being through several pathways (Marcil et al., 2022). First, chronic financial and other types of stress lead to the acceleration of normal aging through shortening of telomeres and increases in allostatic load, together called “weathering” (Geronimus, 2023). These processes lead to premature aging and earlier onset of unfavorable physical health conditions. Second, financial stress can lead to foregone healthcare due to affordability or other poverty-related access challenges (Schickedanz et al., 2023). Preventive medical care may decrease in priority for families facing financial stress, potentially resulting in conditions becoming more acute and requiring more intervention. Racial and economic discrimination faced by people of color, people with disabilities, and other groups can compound financial stress. Children in low-income households whose parents are under financial stress may suffer harm to their cognitive and social/emotional development due to harsh, inconsistent, and/or detached parenting resulting from the stress (National Academies of Sciences, Engineering and Medicine, 2019).

Healthcare Settings as Focal Points for Poverty Interventions

Healthcare settings are well suited to deliver interventions that address poverty alongside healthcare. Clinical healthcare settings often function as the first point of contact with people who have a wide variety of needs, and social workers in these settings currently provide many services, including referrals and direct services (Rosenberg & Sude, 2024; Whitman et al., 2022). Primary and tertiary healthcare settings that target and/or serve primarily lower-income and communities of color are trusted environments that could benefit from services that lower financial stress (South et al., 2022). Primary healthcare providers are focused on the comprehensive and interrelated aspects of physical, mental, and social health, making them especially interested in addressing home environment stressors (Schickedanz et al., 2023). Health practitioners are also focused on improving health outcomes—for instance, promoting ways to promote keeping appointments focused on preventative care (Rosenberg & Sude, 2024). Primary healthcare clinics that serve low-income families have high no-show rates for appointments, with estimates ranging between 25% and 50% of all appointments (Samuels et al., 2015).

Medical–Financial Partnerships

Medical–Financial Partnerships (MFPs) are a relatively new and innovative intervention being piloted within healthcare settings that serve lower-income and Medicaid-insured patients. MFPs aim to directly address issues of patient financial stress and poverty (Liu et al., 2021), while promoting adherence to healthcare appointments (Schickedanz et al., 2023). Typically initiated by health delivery systems, such as clinics, hospitals, or broader health networks, MFPs involve collaboration with financial service organizations to offer services to integrate financial stability efforts into the healthcare provision. They attempt to create a synergistic effect on community wellness (Bell et al., 2020; Hole et al., 2017). The purpose of this service delivery model is to foster a robust connection between healthcare and financial services (Marcil et al., 2021). The goal of MFP services is to provide a platform to enhance patient financial stability for patients through a variety of offerings. MFPs serve a wide demographic, including hospital and clinic patients, their employees, and the wider community both on-site and in the broader community through formal organizational partnerships.

MFPs are pioneering approaches that operate on- and off-site of healthcare facilities through partnership arrangements (Bell et al., 2020; Hole et al., 2017). This review distinguishes on-site MFP interventions from conventional social work services in healthcare settings. The review will focus particularly on those interventions delivered on-site and through tele-consultations with financial service providers operating under a healthcare provider's service model. Whereas social workers in healthcare settings typically refer patients to external resources such as financial counseling and coaching and emergency nutrition supplements (Browne, 2019), MFPs that are colocated are distinctly different from traditional social services and provide unique features (Marcil et al., 2021). First, colocation simplifies access to services for patients to access services, whether in conjunction with their healthcare visits or as standalone services. Secondly, these services are integrated into the healthcare framework and emphasize a holistic approach to patient care. Third, on-site MFP interventions can offer a suite of financial services, including financial counseling, financial coaching, tax preparation services, credit counseling, debt consolidation and forgiveness, enrollment in savings accounts, employment assistance and workforce development, and/or assistance with applying for benefit programs (Bell et al., 2020). Patients can access these services within the physical space of healthcare settings (Dalembert et al., 2021), or via tele-consultation. Various healthcare staff members inform patients about the available financial services and encourage their utilization.

Several key factors are driving the development and offering of MFPs. The idea that financial stress is inherently a healthcare issue is gaining traction. Prominent professional and government entities, including the Academy of Pediatrics and the American Academy of Family Physicians, advocate for healthcare providers to address the social determinants of health, which includes financial stress (American Academy of Family Physicians, 2022; Gitterman et al., 2016). Additionally, the National Association of Community Health Centers and the Centers for Medicare and Medicaid Services have developed screening tools for the social determinants of health (Centers for Medicare and Medicaid Services, n.d.; National Association of Community Health Centers, Inc. & Association of Asian Pacific Community Health Organizations, 2022). Academic research further supports the significance of screening tools in recognizing the social determinants of health, including poverty (Gruß et al., 2021; LaForge et al., 2018; O'Gurek & Henke, 2018). Media coverage of MFPs is also driving interest (Huang, 2023).

Moreover, primary healthcare settings have historically incorporated nonfinancial social resources. Initiatives addressing necessities such as food security (Adams et al., 2017; Palakshappa et al., 2017), as well as behavioral health and legal services (Beck et al., 2021), have become integral components of patient care. Notably, some healthcare settings have incorporated Medical–Legal Partnerships, which embed legal services addressing legal barriers to financial wellness (Marcil et al., 2021). Furthermore, qualitative research findings suggest patients are interested in services integration, such as financial coaching and free tax preparation clinics (Liu et al., 2021). Early research findings have been promising. Individual studies suggest that the integration of financial services within healthcare settings could lead to improved financial outcomes, such as reduced debt and higher credit scores, and better health outcomes through reduced financial stress, increased adherence to healthcare appointments, and greater utilization of preventive healthcare services (Dalembert et al., 2021; Schickedanz et al., 2023).

Across the MFP models currently implemented, two services are most prominent: financial coaching and tax preparation services (Collins et al., 2021; Dalembert et al., 2021; Marcil et al., 2021). Financial coaching has evolved into a standardized, evidence-based method that empowers low-income families toward financial well-being (Hall et al., 2022; Modestino et al., 2019). Financial coaches assist clients to set and pursue their financial goals, complemented by financial education and strategies to enhance budgeting, savings, and credit. Demonstrated outcomes include increased financial knowledge and confidence, reduced stress and debt, and improvements in income, savings, and credit scores (Collins et al., 2021; Silva et al., 2022).

Free tax preparation addresses the vital need, particularly for low-income families eligible for significant refunds through credits such as the EITC and the Child Tax Credit (CTC) (Bell et al., 2020). An estimated 20% of those eligible fail to claim these benefits (Internal Revenue Service, 2022), and Black and Latinx children in families were disproportionately affected (Bruenig & Williams, 2021). MFPs may also provide diaper distribution, assistance with food insecurity, Child Development Accounts, housing assistance, savings programs, FAFSA assistance, pre-k enrollment, and medical bill negotiation (Marcil et al., 2021).

Study Purpose

As health policy increasingly acknowledges the role of social determinants of health, including financial factors, MFPs offer a promising avenue to improve health outcomes by addressing patients’ financial needs—issues that social workers often navigate in practice. Social workers are uniquely positioned to advocate for and implement these interventions, given their role in both healthcare and community settings. Whereas individual studies have reported positive outcomes from interventions like financial coaching and tax-time savings, the existing evidence is fragmented, and no systematic review has focused on the financial and health outcomes of MFPs. This review seeks to fill that gap by assessing the quality of the research and effects of MFP interventions embedded in healthcare settings, with implications for policy development and practice, particularly in healthcare settings. We examine both financial and health-related outcomes, providing critical insights for integrating financial services into health systems, an approach that social workers can help operationalize if these interventions demonstrate effectiveness. To that end, the primary objective of this review is to synthesize evidence of the effects of MFP interventions to answer the following research questions:

What is the extent and quality of MFP intervention research? What are the effects on financial outcomes of financial services embedded within healthcare settings? What are the effects on health-related outcomes of financial services embedded within healthcare settings?

Methods

The conduct and reporting of this systematic review followed the Methodological Expectations of Campbell Collaboration Intervention Reviews (MECCIR). The protocol for this review was published in Campbell Systematic Reviews (Birkenmaier et al., 2023).

Inclusion Criteria

Types of Studies

To mitigate threats to internal validity, studies must have used a prospective randomized controlled trial (RCT) or quasi-experimental (QED) research design with parallel cohorts. RCT studies minimize bias and establish strong causal relationships between an intervention and its outcome by randomly assigning participants to treatment and control groups. For similar reasons, QED studies, with treatment and comparison groups, are valuable when randomization is not feasible. Comparison groups could have included those on a waitlist, attention control, or standard care. Comparison groups could have received their needed healthcare but could not receive financial services within the healthcare setting aside from passive referral.

Types of Participants and Settings

All populations were included. All US healthcare clinical settings where primary, secondary, or tertiary healthcare services are provided were eligible to be included.

Types of Interventions

MFPs require intentional collaboration between medical facilities and/or staff and financial service providers. Studies eligible for this review had financial services embedded within the medical facility and could have been delivered in person or remotely (e.g., videoconference). Though many medical settings make referrals to local financial assistance resources, this practice alone does not qualify as a MFP and was understood as “treatment as usual” for the purposes of this review.

To meet the criteria for on-site financial services, interventions must have included at least one of the following: (a) financial education, counseling, or coaching; (b) credit counseling; (c) the provision of services that assist patients to access financial products or services, such as free tax preparation services, matched savings accounts or special child savings accounts to be used for education purposes; or (d) services to increase income, such as screening for public benefits and assistance with the application process, as well as employment services (e.g., assistance with resume writing and job interviewing skills). Interventions of any length or duration were eligible for inclusion, from single-session services such as tax preparation to multisession financial coaching offerings. Financial services could be provided by any group, organization, or agency, whether nonprofit or for-profit, whose primary role is to provide such services. The services are provided to the patients who use the healthcare setting for any duration of services. Financial services that were provided for the sole purpose of affording healthcare or services designed to help lower the cost of medication were excluded from the review.

Types of Outcome Measures

Primary Outcomes

Studies must have measured and reported a financial outcome. These outcomes could include financial knowledge and attitude, tax filing status, tax refund and receipt and amount, debt, savings, and credit scores.

Secondary Outcomes

In addition to financial outcomes, we extracted data from included studies for the following outcomes: knowledge about tax filing and tax credits (e.g., EITC and CTC); healthcare usage (e.g., feel more connected to healthcare providers); outcomes related to child patients of participating parents; outcomes related to employment services; outcomes related to income security unrelated to employment (e.g., accessing public benefits); outcomes related to microfinance and emergency finance; and adverse or unintended outcomes.

Types of Settings

All healthcare settings were eligible as long as financial services were offered on-site. Studies conducted outside the United States were excluded due to the US healthcare system being unique among high-income countries in not providing universal healthcare, and intervention effectiveness may be unique because of the healthcare system.

Other Criteria

Studies must have been published in English, which was due to being consistent with focusing on studies conducted in the United States as well as due to limitations in resources to translate studies published in other languages. Although we did not anticipate finding studies on this intervention prior to 2017, we did not restrict inclusion of studies based on the date when studies were conducted or published. We included both published and unpublished studies.

Search Methods for Identification of Studies

We conducted a comprehensive search for published and gray literature informed by Campbell's guide for searching for studies (Kugley et al., 2017), which included multiple electronic databases, gray literature sources, reference lists of reviews and relevant studies, trial registries and relevant websites, and contacting authors.

Electronic Searches

Following the procedures outlined in the protocol, we searched for and retrieved studies through a comprehensive search that included Google, Google Scholar, and 10 electronic databases (Platform): ABI/INFORM (ProQuest); Academic Search Complete (EBSCOhost); Business Source Premier (EBSCOhost); ProQuest Dissertations & Theses Global; EconLit (EBSCOhost); PubMed; APA PsychINFO (Ovid); SCOPUS (Elsevier); Social Science Research Network (Elsevier); and Social Sciences Citation Index (Clarivate). Database searches were conducted in September 2023 (see Birkenmaier et al., in press for the full search strategies used in each database).

Searching Other Resources

In addition to the database searches, we searched for studies on websites and study registries. Websites searched included the Centers for Disease Control and Prevention, the World Bank, OECD, the Global Partnership for Financial Inclusion, the Alliance for Financial Inclusion, and Social Interventions Research and Evaluation Network (SIREN) by the University of San Francisco California. We also searched Clinicaltrials.gov and the International Clinical Trials Registry Platform (WHO; https://who.int/ictrp/network/en/) for registered studies.

The reference lists from included studies were harvested for potential studies. We conducted forward citation searching using Google Scholar to search for studies citing the included studies. We contacted the first authors of the included studies and requested information about unpublished studies, studies in progress, and published studies potentially missed in the other search activities.

Data Collection and Analysis

Selection of Studies

Searches were saved in the reference management software EndNote21. Duplicates were removed using EndNote21 and then imported into Rayyan, a cloud-based application for conducting systematic reviews (Ouzzani et al., 2016). We then used the auto-resolve feature within Rayyan to conduct an initial duplicate screen of entries with 97% similarity or more. During this process, only articles that exactly matched authors, journals, and dates were eliminated, while potential secondary reports were retained. All potential duplicates remaining after auto-resolve were divided between two team members and resolved manually.

Initial title and abstract screening on the remaining unique entries were divided between four reviewers and completed in December 2023. A total of 26 were moved forward for full-text screening. Three reviewers independently conducted a full-text review of each study for eligibility. All reviewers included notes on any decisions to exclude. Discrepancies were reviewed by a fourth reviewer, who made the final eligibility decision. Protocols for included studies, when available, were retrieved for use in data extraction/risk of bias assessment.

Data Extraction and Management

The research team utilized a data extraction form to standardize data capture and coding (see Birkenmaier et al., 2023). We extracted data related to aspects of the intervention delivered, methods used, results, and outcomes. The team conducted a joint data extraction review on one study as a pilot to review and revise extraction methods. Three reviewers then independently extracted data from the studies. The full team evaluated the results of the extraction to assess for discrepancies or errors before finalizing the data. Discrepancies were reviewed and resolved through discussion. The final codes were saved in Excel. Study authors were contacted to request needed data absent in the article.

Assessment of Risk of Bias in Included Studies

Four review authors independently conducted a risk of bias assessment on each study using the Risk of Bias in Non-randomized Studies of Interventions (ROBINS-I) (Sterne et al., 2016) for studies that used QEDs and the Cochrane Collaboration's revised risk-of-bias tool for randomized trials (RoB 2) for studies that used RCT design (Higgins et al., 2019). Three of the four studies had registered protocols with the National Institute of Health, National Library of Medicine (at clinicaltrials.gov) that assisted in the risk of bias assessment (Sadigh et al., 2022 (NCT0425707); Schickedanz et al., 2023 (NCT03736590), and Marcil & Thakrar, 2022a, 2022b (NCT04135469)).

Measures of Treatment Effect

We calculated effect sizes for all outcomes of interest where study authors provided sufficient data. As anticipated, study authors reported both continuous and dichotomous outcome measures. For continuous outcomes, we calculated the magnitude of effect using the standardized mean difference effect size with Hedges’ g correction. For dichotomous outcomes, we calculated the odds ratio (OR). All effect sizes were calculated with the Practical Meta-Analysis Effect Size Calculator (Wilson, n.d.).

Unit of Analysis Issues

None of the included studies used a clustering or crossover design. For studies that reported multiple outcome measurement time points, we calculated and reported effect sizes for each time point. If there had been a sufficient number of studies reporting the same outcome at similar time points, we would have pooled similar time points together; however, we did not have a sufficient number to quantitatively synthesize, and thus, we reported effects for all reported time points in narrative and tabular format.

Criteria for Determination of Independent Findings

We assessed each of the included studies to ensure they were each reporting outcomes for unique study samples. If we found multiple reports of the same study, we used all the information from each report but counted it as only one study. Because we did not pool effects across studies, in cases where study authors reported different outcome measures for conceptually similar outcomes, we calculated effect sizes for each outcome and reported each effect size in narrative and tabular formats.

Dealing with Missing Data

All studies that met inclusion criteria were included, regardless of whether there was missing data. For studies where there was not sufficient data to calculate an effect size, we contacted study authors to request the data.

Assessment of Heterogeneity

We planned to conduct a test of homogeneity (Q test) to compare the observed variance to what would be expected from sampling error and the I2 statistic to describe the percentage of total variation across studies due to heterogeneity rather than chance. We also planned to construct a forest plot displaying study-level mean effect sizes and 95% confidence intervals (CIs) for the included studies to provide opportunity for visual analysis of the precision of the estimated effect sizes, detection of studies with extreme effects, and information regarding the heterogeneity of studies. Due to the small number of included studies and the variation across studies regarding the outcomes reported, we did not conduct meta-analysis and instead provided a narrative description of the included studies. Thus, we did not examine heterogeneity.

Assessment of Reporting Biases

Though we had originally planned to use a funnel plot to assess publication bias, the number of studies found was not sufficient for this purpose. We did assess reporting bias by comparing reported outcomes in the included studies to the studies’ protocols for three of the included studies that had published protocols and reported our findings narratively.

Data Synthesis

Due to the small number of included studies and the wide range of outcomes they measured, a meta-analysis was not feasible as we lacked a sufficient number of effect sizes for the same outcome construct. Instead, we employed a narrative synthesis approach. For each study, where data are allowed, we calculated effect sizes for individual outcomes and reported them in both narrative and tabular formats to facilitate comparison across studies. Our narrative synthesis involved a systematic description of each included study, focusing on study design, intervention characteristics, sample populations, and key findings. Additionally, we discussed the strength of evidence for each outcome, considering study quality and potential biases, to provide a comprehensive interpretation of the findings. This approach allowed us to capture the details and nuances of the varied interventions and outcomes, offering insights into both the effectiveness and limitations of financial services embedded within healthcare settings.

Results

Description of Studies

Results of the Search

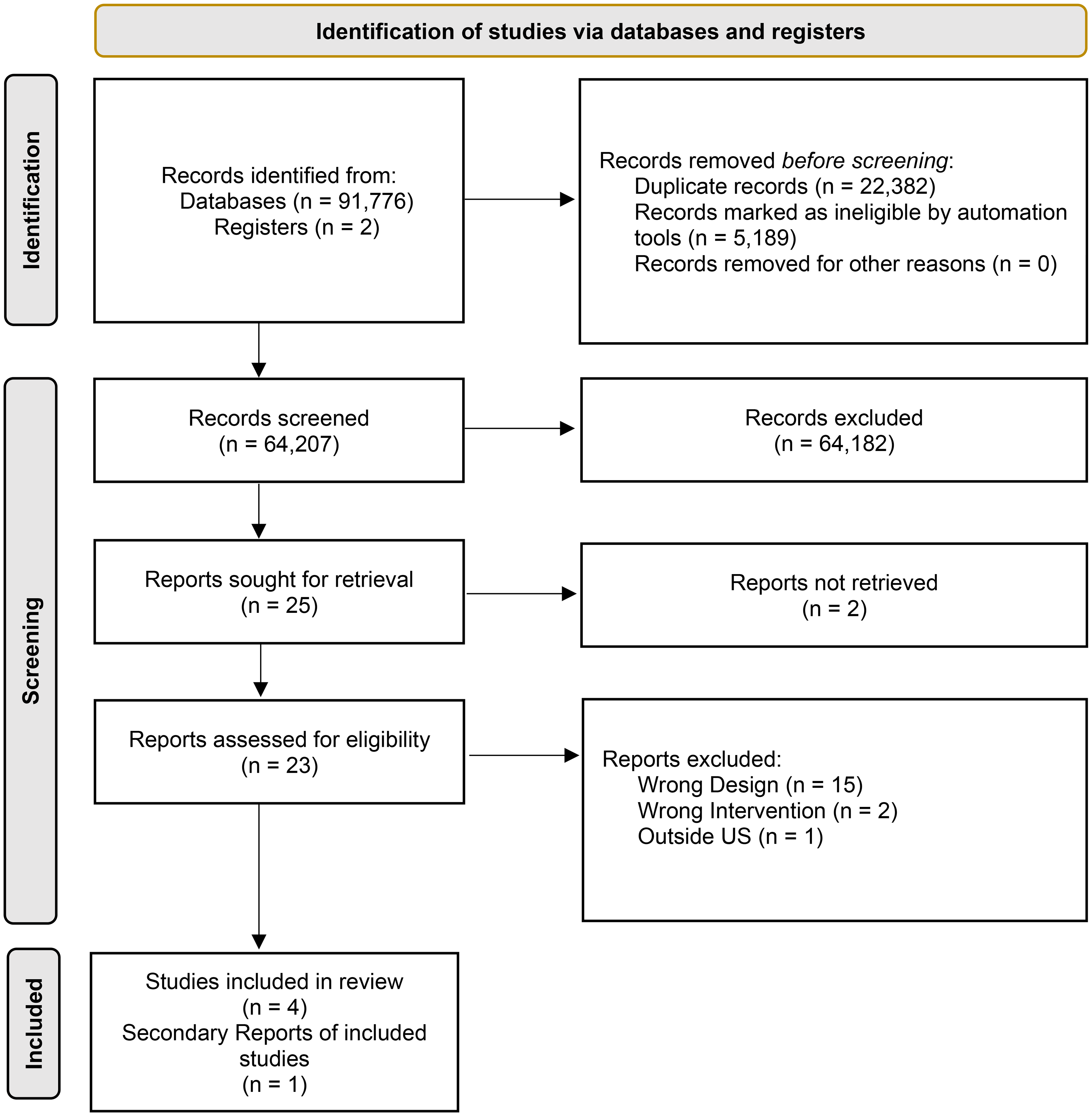

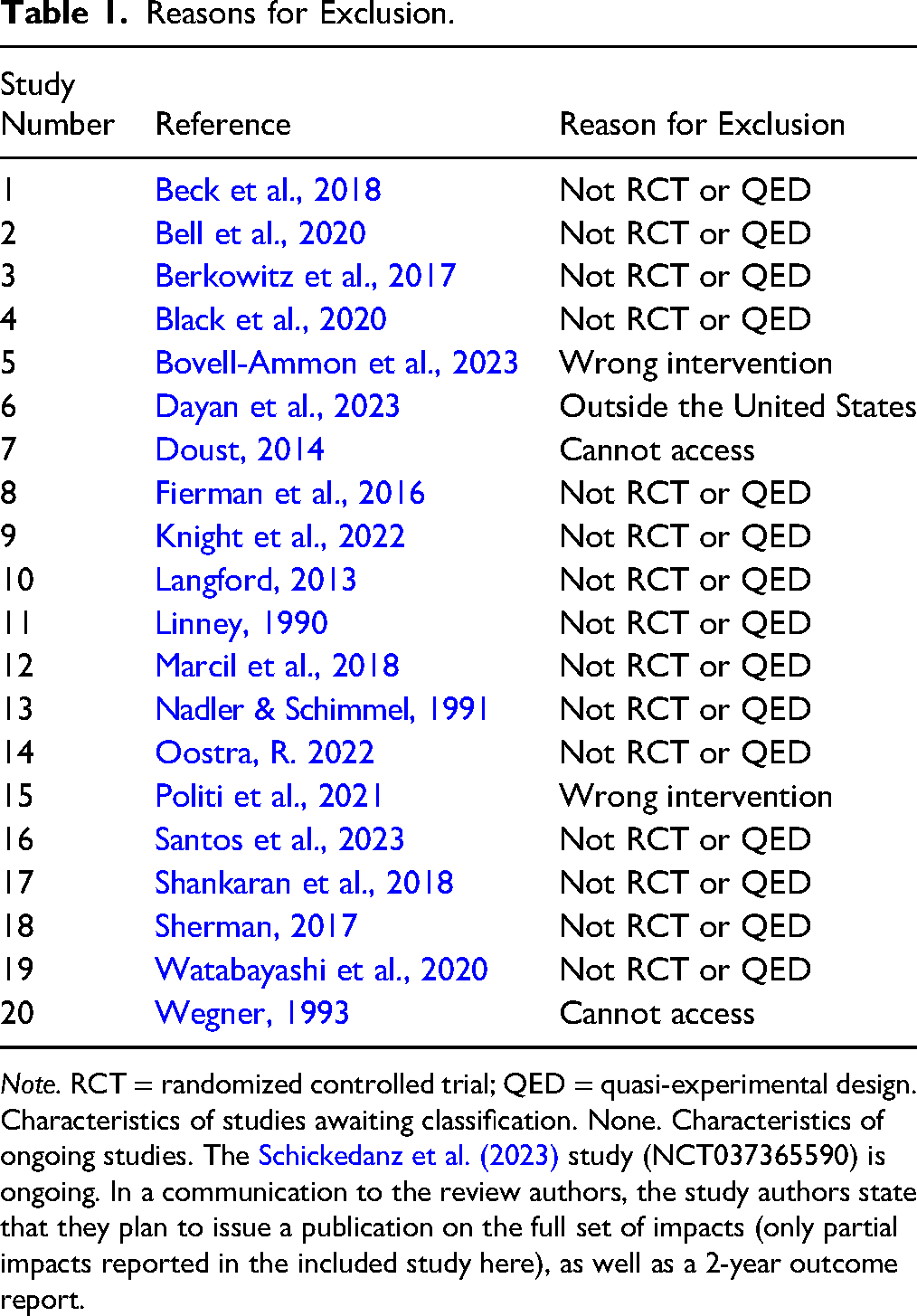

The results of the search and selection process are illustrated in Figure 1. Electronic searches of bibliographic databases and searches of other sources yielded a total of 91,778 hits. Of the 91,778 hits, 91,776 were from database searching, and 2 were registered protocols. As part of the automatic deduplication process available in Rayyan outlined above, 5,189 articles were removed as duplicates automatically. An additional 22,382 reports were manually identified as duplicates and removed. After deduplication, 64,207 titles and abstracts were screened for relevance and 64,182 were deemed inappropriate. The full text of the remaining 25 potential studies were reviewed and screened for eligibility by four independent coders. We excluded 20 reports that were deemed ineligible (see Table 1 for a list of excluded studies and reason for exclusion and included 5 reports that met the inclusion criteria). Of the five, one was a correction to an eligible report. This resulted in four unique studies (using unique samples) published in five reports that were included in this review. Published protocols were available for three of the four studies (Marcil & Thakrar, 2022a, 2022b; Sadigh et al., 2022; Schickedanz et al., 2023). We conducted forward citation searching and reference list searching on the included studies. None of the additional entries generated by these searches met the inclusion criteria for full-text review. No new studies were located from websites, from clinical trial registries, or from included authors (see the references of included studies for a list of reports that reported on the included studies).

Search and selection process.

Reasons for Exclusion.

Note. RCT = randomized controlled trial; QED = quasi-experimental design. Characteristics of studies awaiting classification. None. Characteristics of ongoing studies. The Schickedanz et al. (2023) study (NCT037365590) is ongoing. In a communication to the review authors, the study authors state that they plan to issue a publication on the full set of impacts (only partial impacts reported in the included study here), as well as a 2-year outcome report.

Included Studies

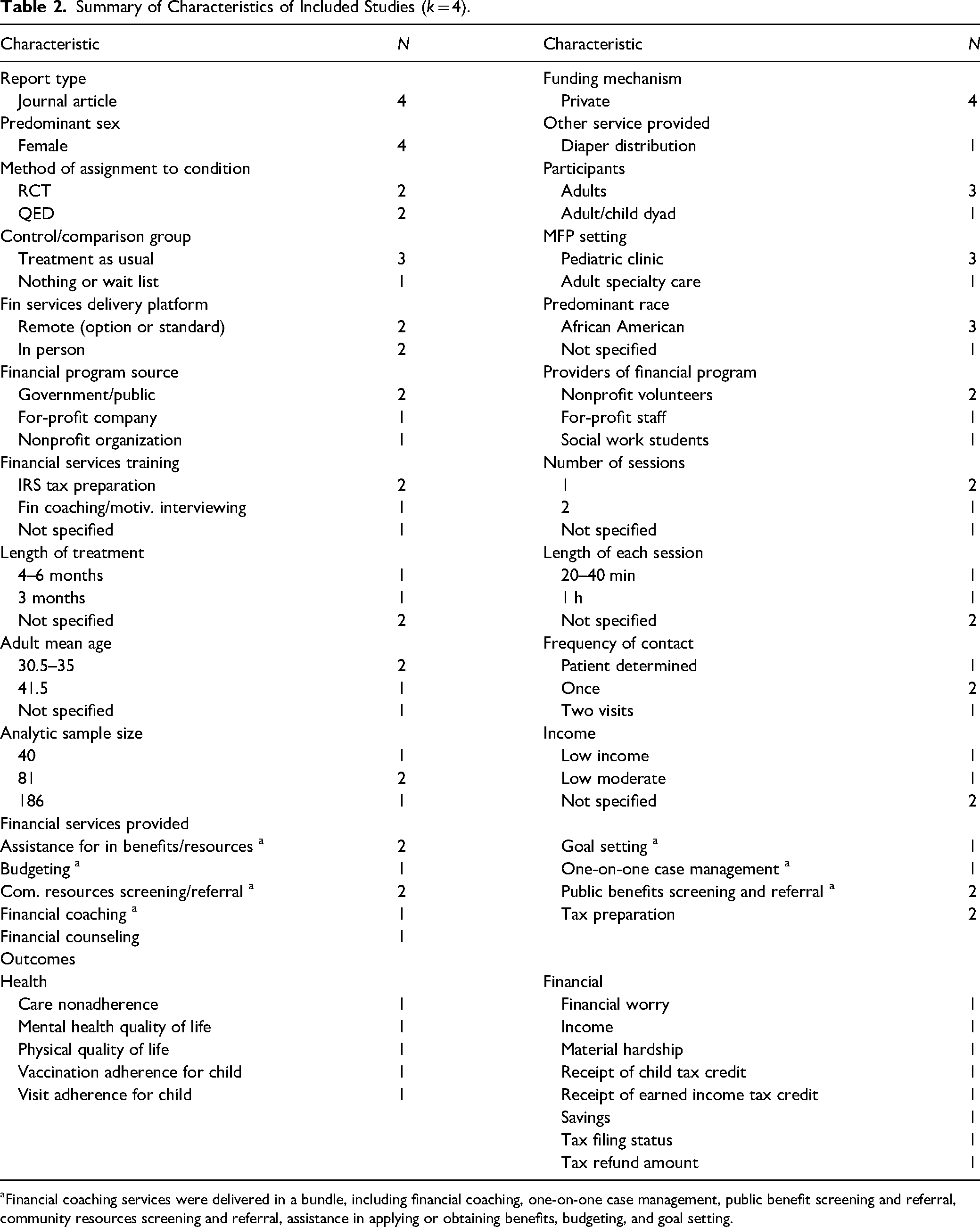

A summary of the four included studies is presented in Table 2, and study-by-study details are provided in Table 3. Two of the four included studies were RCTs (Sadigh et al., 2022; Schickedanz et al., 2023) and two were QEDs (Marcil & Thakrar, 2022a, 2022b; Markowitz et al., 2022). A total of 410 participants were included across these 4 studies, with analytic sample sizes ranging from 40 to 126 participants.

Summary of Characteristics of Included Studies (k = 4).

Financial coaching services were delivered in a bundle, including financial coaching, one-on-one case management, public benefit screening and referral, community resources screening and referral, assistance in applying or obtaining benefits, budgeting, and goal setting.

Summary of Characteristics by Study.

Study Characteristics

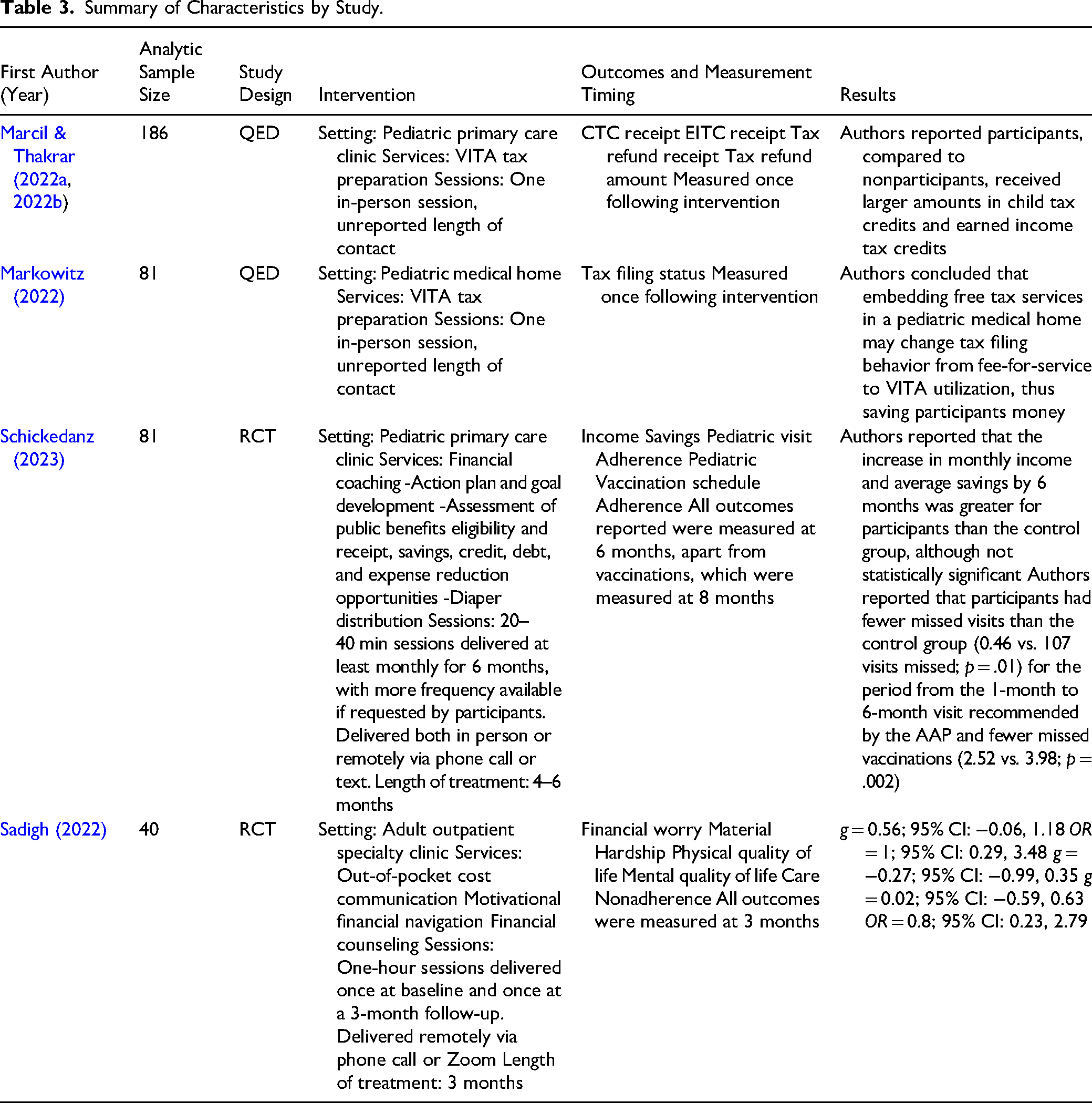

Marcil and Thakrar (2022a, 2022b) used a QED to examine the benefits of a VITA tax preparation clinic embedded in a pediatric primary care setting at Boston Medical Center (BMC), operated through the nonprofit StreetCred. The study focused on outcomes such as receipt of the CTC, EITC, tax refunds, and refund amounts. Of the 325 individuals who used the service, 186 were study participants, with 88 parents of pediatric patients in the treatment group and 98 in the control group. Markowitz et al. (2022) also employed a QED, studying a similar StreetCred program embedded in a pediatric medical home in New Haven Connecticut. The study assessed tax filing status, participants’ knowledge of StreetCred/VITA services, and attitudes about using pediatric clinics for financial services. Twenty caregivers participated in the intervention group and 61 caregivers in the control group. Schickedanz et al. (2023) conducted a RCT to evaluate the impact of financial coaching on income, savings, debt, and pediatric visit adherence. Eighty-one participants were randomized, with 35 in the intervention group and 46 in the control group. The control group received standard care, including visit reminders and screenings for social needs. Sadigh et al. (2022) also used an RCT to study the effects of a remote financial navigation program (CostCOM) for multiple sclerosis patients in a specialty clinic. The study measured financial worry, material hardship, and quality of life (QOL). Of the 62 randomized participants, 22 remained in the intervention group and 18 in the control group after attrition. The control group received usual care, including routine visits and assistance with copay or free medication resources.

Participant Characteristics

Three of the four studies focused on adult participants (Marcil & Thakrar, 2022a, 2022b; Markowitz et al., 2022; Sadigh et al., 2022), and one study focused on adult and child dyads (Schickedanz et al., 2023). Across the four studies, participants were primarily female, with female participants comprising 80% or greater of each sample. Participants in the Schickedanz et al. (2023) study were all low income, Marcil and Thakrar (2022a, 2022b) and Markowitz et al. (2022) did not report income level, and Sadigh et al. (2022) reported annual income for participants as either above or below $60,000. The three studies that reported mean ages had adult-only participants, with the average age range of participants in these studies being 30–41.5 years old. The predominant race for three of the studies was African American (Marcil & Thakrar, 2022a, 2022b; Markowitz et al., 2022; Sadigh et al., 2022). The Schickedanz et al. (2023) study did not specify the number of African American participants and only reported the percentage of White participants (50%) and those identifying as Hispanic (50%). Following African Americans, White participants made up most of the sample for each study, ranging from 10% to 50% of participants. One study (Schickedanz et al., 2023) reported a sample in which half of the participants were Hispanic, with the remaining three studies reporting Hispanic participants as being between 11% and 30% of the sample (Marcil & Thakrar, 2022a, 2022b; Markowitz et al., 2022; Sadigh et al., 2022).

Intervention Characteristics

Two of the studies (Marcil & Thakrar, 2022a, 2022b; Markowitz et al., 2022) focused on tax preparation only as their financial intervention, and both studies offered a VITA tax clinic on-site in the healthcare clinic setting. In another study (Schickedanz et al., 2023), services were labeled as financial coaching, which was further specified as one-on-one case management, public benefits screening and referral, community resource screening and referral, assistance in applying or obtaining benefits, budgeting, and goal setting. Though Sadigh et al. (2022) did not label their services as financial coaching, Schickedanz et al. (2023) and Sadigh et al. (2022) overlapped in their offering of public benefits screening and referral, community resources and referral, and assistance in applying or obtaining benefits and resources. Though there was overlap in services provided, and Schickedanz et al. (2023) had more frequent contact and placed an emphasis on fostering a longitudinal client-coach relationship, while frequency of contact between coaches and participants in the Sadigh et al. (2022) study was limited to two sessions. Schickedanz et al. (2023) also delivered services in person during clinic appointments, while Sadigh et al. (2022) delivered sessions remotely.

Markowitz et al. (2022) utilized an MFP called “Street Cred New Haven,” which offers VITA services for free tax preparation as its primary financial service. The program was advertised from September through April 2019 via flyers and written in after-visit summaries and advertised verbally through referrals from the healthcare team, financial capability organizations, and a 2-1-1 information line. From January to April 2019, 33 tax preparation sessions were held during and after clinic hours. The intervention was completed in one session, and the average time needed to complete the session was not reported.

Marcil and Thakrar (2022a, 2022b) utilized StreetCred to offer a VITA site for free tax preparation services at the BMC pediatric clinic. Additional information about recruitment, referral procedures, and services was not available for this study. The intervention was completed in one session, and the average time needed to complete the session was not reported.

Training received by those delivering the intervention for both studies (Marcil & Thakrar, 2022a, 2022b; Markowitz et al., 2022) was consistent for the identified intervention of tax preparation. All VITA tax sites are government or public-funded and are composed of nonprofit volunteers who are certified by the IRS to deliver tax preparation assistance.

Schickedanz et al. (2023) provided financial coaching to the primary caregivers of infants during their well-child visits. This intervention typically took place while caregivers were waiting for their child's appointment to begin, and the average length of visit was between 20 and 40 min. Each participant was paired with a coach at enrollment. Participants were then followed up with at least monthly, either at their child's pediatrician visit or remotely via phone calls or text messages. The bundle of services provided by Schickedanz et al. (2023) was labeled as financial coaching. This intervention included several services, beginning with the development of goals and action plans through motivational interviewing. The service also included an assessment of income, public benefits eligibility and receipt, savings, credit, debt, taxes, and potential for expense reduction opportunities. Coaches also helped participants navigate through available services such as affordable childcare, transportation and utility discounts, nutrition assistance, and free tax preparation. An additional service provided was written referral materials and diapers when they were requested by participants. The intervention in the Schickedanz et al. (2023) study was provided by social work students who received training and were supervised by a licensed clinical social worker.

Sadigh et al. (2022) collaborated with a private organization, TailorMed Medical Inc., to develop an intervention referred to as CostCOM, which included out-of-pocket cost communication, motivational financial navigation, and financial counseling. This intervention was delivered remotely via phone calls or Zoom. Out-of-pocket cost communication consisted of a review of the patient's insurance and predicted costs for their treatment, with a total estimate being offered at baseline and again at 3 months if the participant had any insurance or treatment changes. Financial navigation was defined as professional guidance to identify financial service programs, with examples provided being copay and living expenses that alleviate costs of care. Participants were also offered information about how to improve their insurance coverage. The financial counseling piece of the intervention was to address participants’ concerns about finances and to enroll them in financial assistance programs for which they were eligible. Services were provided by a remote financial counselor at TailorMed in two, 1-hour sessions, one which took place at enrollment and one taking place at a 3-month follow-up. The total length of treatment was 3 months, with a total of two contacts.

Outcomes

Financial Outcomes

All four included studies measured at least one financial outcome; however, they varied in the types of financial outcomes measured. Two studies measured tax filing status, one measured CTC and EITC amounts, one measured household income and savings, and one measured material hardship and financial worry. For Marcil and Thakrar (2022a, 2022b) and Markowitz et al. (2022), both interventions focused on tax preparation and filing and measured tax filing status, and Marcil and Thakrar (2022a, 2022b) also measured CTC and EITC amounts. Markowitz et al. (2022) did not report sufficient outcome data to calculate effect sizes, but Marcil and Thakrar (2022a, 2022b) did provide sufficient data to calculate tax filing status, but not CTC or EITC amounts. Markowitz et al. (2022) concluded that embedding free tax services in a pediatric medical home may change tax filing behavior from fee-for-service to VITA utilization, thus saving participants money. In the Marcil and Thakrar’s (2022a, 2022b) study, the effect on tax filing status was small and not statistically significant (OR = 1.08; 95% CI: 0.51, 2.26) and authors reported participants, compared to nonparticipants, received larger amounts in CTCs and EITCs. Schickedanz et al. (2023) reported household income and household savings measured via participant self-report. They reported the participants’ increase in monthly income and average savings by 6 months was greater than control participants, although not statistically significant. Sadigh et al. (2022) reported two financial-related outcomes at 3 months, material hardship measured via self-report, and financial worry measured using the Comprehensive Score for Financial Toxicity (COST) measure. The author reported sufficient data to calculate effect sizes. The effects on financial worry (Hedges’ g = 0.56; 95% CI: −0.06, 1.18) and material hardship (OR = 1; 95% CI: 0.29, 3.48) were not statistically significant.

Health-Related Outcomes

Two of the studies reported health-related outcomes (Sadigh et al., 2022; Schickedanz et al., 2023). Sadigh et al. (2022) measured care nonadherence via self-reported positive responses to delaying, foregoing, stopping, or changing prescribed medication due to cost and physical and mental health QOL using the Patient-Reported Outcomes Measurement Information System (PROMIS)-10. Effects for care nonadherence (OR = 0.8; 95% CI: 0.23, 2.79), physical health QOL (Hedges’ g = −0.27; 95% CI: −0.99, 0.35), and mental health QOL (Hedges’ g = 0.02; 95% CI: −0.59, 0.63) were small and not statistically significant. Schickedanz et al. (2023) examined missed preventive care visits and missed or delayed vaccinations. Authors reported that participants had fewer missed visits than the control group (0.46 vs. 107 visits missed; p = .01) for the period from the 1-month to 6-month visit recommended by the AAP and fewer missed vaccinations (2.52 vs. 3.98; p = .002).

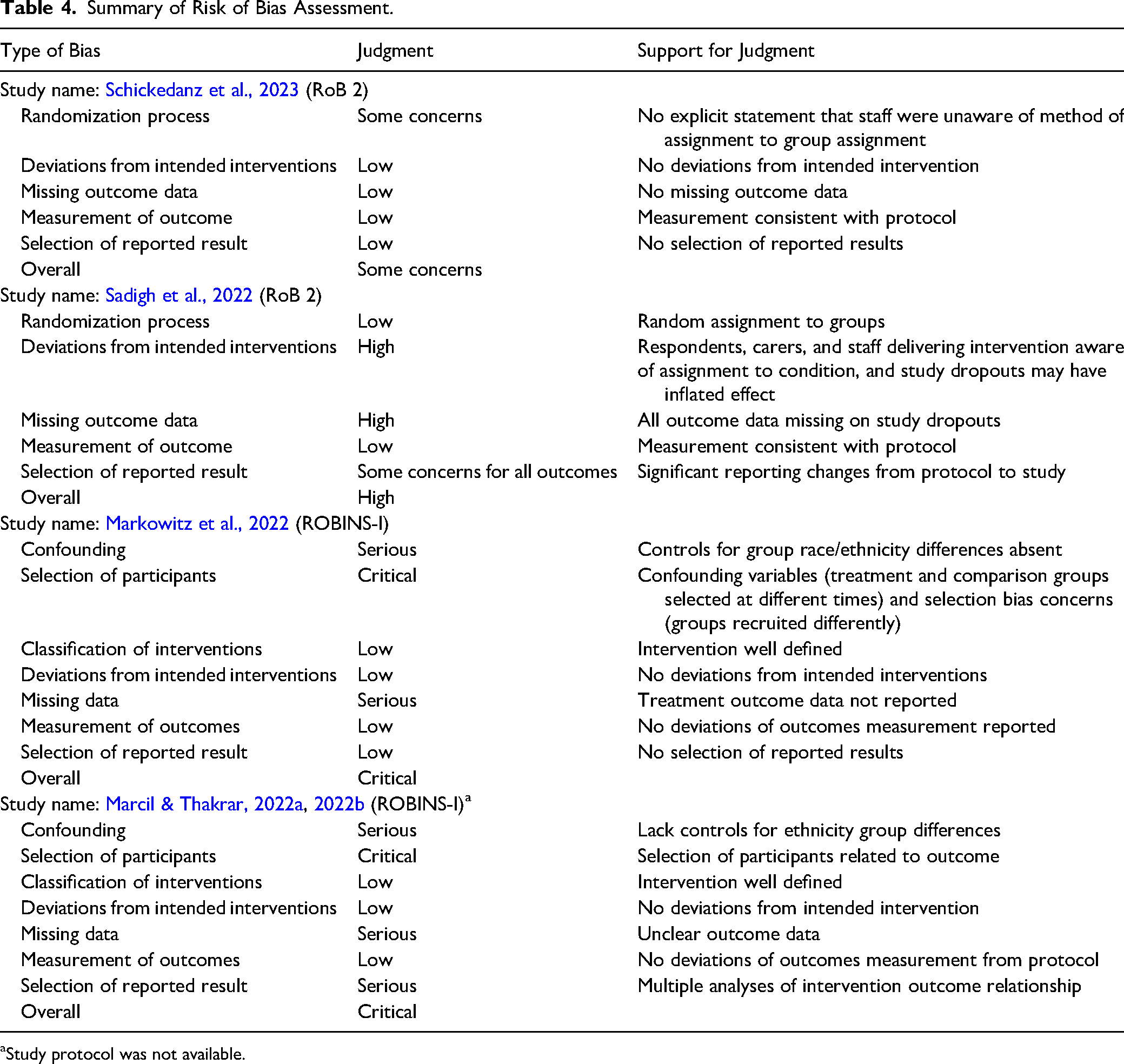

Quality of the Research

The quality of the research related to the risk of bias across the included studies ranged from “some concerns” to “critical,” with none judged to have a low risk of bias (see Table 4 risk of bias assessment for each study). Three of the four studies had preregistered protocols, which helped assess key domains such as deviations from intended interventions and reporting bias (Marcil & Thakrar, 2022a, 2022b; Sadigh et al., 2022; Schickedanz et al., 2023). The two RCTs had differing risks of bias across domains, though both had a low risk of bias for outcome measurement. Schickedanz et al. (2023) were judged to have “some concerns” due to lack of clarity around staff awareness of allocation. Sadigh et al. (2022) were judged low risk for all but three domains, including “high risk” of bias for having deviations from intended interventions (due to respondents, carers and staff delivering the intervention were aware of assignment to condition, and study dropouts may have inflated the intervention effects), and missing outcome data (outcome data missing on study dropouts). The study was also judged as having “some concern” for the selection of reported results (there are significant reporting changes from the protocol to the reported results). The overall study was assessed as having a high risk of bias. The two QED studies, Markowitz et al. (2022) and Marcil and Thakrar (2022a, 2022b), were both judged to have a “critical” risk of bias, primarily due to confounding factors, participant selection issues, and missing data. The authors of these studies acknowledged the limitations and recommended further rigorous research on MFP interventions.

Summary of Risk of Bias Assessment.

Study protocol was not available.

Discussion and Applications to Practice

The challenges of being low-income impact both the financial well-being and the health of Americans (U.S. Census, 2022; U.S. Department of Health and Human Services, 2024). Increasingly, healthcare systems are seeking to address financial stress as a social determinant of health by incorporating financial services within the healthcare delivery model (Francis et al., 2018; World Health Organization, 2023), called a MFP. The purpose of this systematic review was to determine the state of research and examine the financial and health outcomes of MFPs.

This review included a total of four unique studies reported in five reports. The studies reported on a range of services provided within MFPs in several types of healthcare settings. Two of the four included studies provided free tax preparation services, public benefits screening and referral, and/or community resources benefits and referrals. The remaining two studies provided other services: one study provided financial counseling and the other provided financial coaching, including one-on-one case management, budgeting, and goal setting.

Overall, the evidence of the health and financial effects of MFPs is sparse, given the small number of studies using randomized or QEDs. Moreover, the lack of standardization of outcomes studied, measurement of the outcomes, or timing of measurement did not allow for synthesis of outcomes across studies. None of the studies examined effects of similar types of interventions on similar outcomes, and several were missing sufficient data to calculate effect sizes; thus, we were not able to pool effects of studies to conduct a meta-analysis.

Results indicate small and nonsignificant effects of MFPs on financial outcomes reported, and some authors reported positive statistically significant effects on attending appointments and vaccination schedule adherence.

All four studies included in this review took place in outpatient clinic settings. Little research has explored whether individuals may benefit from MFPs located in other settings, such as inpatient and home settings. Due to the nature of the privatized healthcare system in the United States, financial stress may be a concern for those experiencing inpatient hospitalization (Nadarajah et al., 2024). There may be an opportunity to explore the benefit of an MFP designed to assist individuals who are hospitalized, especially for those with chronic illness and their family members. Individuals who experience chronic illness may experience frequent hospitalizations that can lead to reduced income due to the physical symptoms of a chronic illness, lost wages from employment due to absence, and medical bills from treatment (Ghazal et al., 2023).

While hospital social workers are typically knowledgeable about financial community resources and hospital financial services, they often do not have specific skills to address the full scope of patient financial needs. The availability of dedicated, trained social workers for a specific department or clinic may increase access to timely screening for financial toxicity (Zebrack et al., 2015). However, the predicted shortage of social workers in future years may impact the availability for such dedicated social workers (U.S. Bureau of Labor Statistics, 2024). In addition, social workers often have many tasks assigned to them that may take precedence including participating in discharge planning and providing counseling for coping with diagnosis and crisis intervention (Judd & Sheffield, 2010).

Hospital financial services are typically designed to address finances related to medical care and costs, but do not typically address the long-term financial health of patients or encompass financial health outside of paying for treatment. MFP providers who are specifically trained and employed to provide financial services would likely have more time to devote to each patient for addressing financial needs than a social worker who is also responsible for other priority tasks. MFP providers would have the opportunity to build long-term relationships with these patients and their caregivers, given the nature of repeated or long-term inpatient hospitalization, and therefore, MFP interventions may assist with reduced financial stress.

In addition to inpatient settings, MFP interventions may be well suited for outpatient settings focused on complex or rare diseases. In the United States, an estimated 25–30 million people are estimated to have a rare disease—defined as any disease that affects less than 200,000 Americans (National Institutes of Health, 2020). Collectively, the economic burden of rare diseases amounted to nearly $1 trillion in 2019, including direct medical care costs, productivity loss, and uncovered healthcare costs (Yang et al., 2022). Due to the nature of their illness, rare disease patients often require multiple visits across a variety of specialists’ offices, resulting in additional time off work, travel, increased healthcare costs, and enrollment in clinical trials. These requirements frequently result in financial stress, even for patients and families who were not low income at the time of diagnosis (Witt et al., 2023). Current care as usual for these patients includes referral to a variety of disease-specific nonprofits designed to provide financial and material assistance for those living with the illness (National Organization for Rare Disorders, 2022). While these organizations provide meaningful help, the onus remains on the individual patient or caregiver to navigate the complex landscape of assistance services on top of their complex landscape of assistance services in addition to their complex network of care providers, clinics, appointments, and insurance. As with the inpatient setting, MFPs with rare disease centers would have the opportunity to provide long-term relationships with these patients and caregivers, develop a specialty in assisting these patients in navigating their assistance landscape, and potentially aid in lessening the overall economic burden of rare disease.

Little research has been conducted on the use of MFPs combined with home health and visiting nurse settings. Home visits by nurses and other trained medical personnel have had positive health and social outcomes for medically and socially vulnerable populations, including low-income families and seniors (Lizano-Díez et al., 2022; Minkovitz et al., 2016). Typically, these services provide minimal material assistance such as infant or adult diapers, infant care supplies, and/or basic home health monitoring equipment. All other services, including financial assistance or coaching, are provided as referrals. MFPs made in conjunction with an established home health or visiting nurse model may achieve the desired financial benefits from the established ease of client access (due to previously established routine of home visits) and increased levels of trust and engagement afforded by associating with a client's known healthcare team.

Although MFP interventions are increasingly offered, the lack of strong evidence suggests that, while many see these as promising interventions, more evidence is needed to fully support more wide-scale implementation. The lack of strong evidence about the effectiveness of MFP interventions has implications for practice and policy in several ways. First, the diversity of components of MFP interventions results in challenges to comparing processes and outcomes across studies. The diversity of components also results in interventions being delivered by practitioners from various professional backgrounds and in different types of healthcare settings with various target audiences and goals. However, practitioners seek evidence on the effectiveness of their choice of components with MFPs so they can deliver the most effective and efficient intervention toward their clients’ healthcare and financial goals. The lack of evidence across MFPs points to the need to develop a more definitive evidence base about the components that provide the desired outcomes.

Social work practitioners in healthcare settings assume numerous roles in the design, delivery, and evaluation of care (Browne, 2019). Social workers can facilitate linkages across their organizational systems, encourage their systems to examine client financial stress and various responses and introduce the MFP intervention. They can be involved in designing, implementing, and evaluating MFPs in their systems, building on the research examined in this review. Social work practitioners can join with researchers and policy actors in their system to partner for MFP implementation and research in their settings, share their data, and contribute to the MFP knowledge base. Social work researchers can partner with MFPs to conduct outcome studies. Social workers can also work with their organizations to promote standardization of MFP component sets within specific types of settings, as well as outcome measures. Standardization of measurement time points post-intervention, as well as other aspects of the intervention, would assist in the development of an evidence base. Organizational policy work can facilitate additional research on MFPs using strong methodology, manualized MFP interventions, and common outcomes to assist in building a strong evidence base.

Despite the well-meaning intentions and perceived potential of MFP interventions, the current evidence supporting their effectiveness remains insufficient and fragmented. This lack of strong evidence highlights the urgent need for more rigorous research to identify the components that drive successful outcomes. Without this, it is difficult for practitioners to confidently apply MFPs in ways that best support clients’ financial and healthcare goals. Practitioners may instead continue to refer to other community resources, such as financial coaching and counseling and matched savings account programs that can provide financial guidance and resources (Birkenmaier et al., 2022). Moving forward, a more standardized approach to intervention design, implementation, and evaluation is essential. By aligning components and outcomes across different settings, we can build a stronger, more actionable evidence base that will empower practitioners, inform policy decisions, and ultimately improve the well-being of those served by MFPs.

The conduct and reporting of this review were guided by Campbell's standards and policies for the conduct and reporting of systematic reviews to ensure a rigorous and transparent review designed to minimize bias and error (Campbell Collaboration, n.d.). To limit bias in the review process, we conducted a thorough and transparent search for published and unpublished studies and conducted a rigorous process for screening and selecting studies and extracting data using at least two independent reviewers. We also included and reported all financial and health outcomes relevant to this review per the protocol. This review is not without its limitations, however, and the findings must be interpreted considering the study's limitations. While we made every attempt to search for published and unpublished studies, all the studies that met inclusion for this review were published journal articles. Because we limited studies to those conducted in the United States and published in English due to the uniqueness of the US healthcare and financial systems, our findings are limited to the US context.

In addition to the limitations resulting from the conduct of the review, we also note limitations resulting from the included primary studies. We were unable to calculate effect sizes for all reported outcomes due to incomplete outcome data reporting in all but one study (Sadigh et al., 2022) and for one outcome in another (Marcil & Thakrar, 2022a, 2022b). Despite requests, missing data were not provided by the authors, preventing us from conducting a meta-analysis. All studies exhibited methodological weaknesses, limiting the validity and generalizability of their findings across different settings, intervention components, regions, and household income levels. Three studies were conducted in pediatric primary care settings, while one took place in an adult specialty clinic. Two studies offered only tax preparation services: one combined financial coaching with other services and one offered a mix of financial services without coaching. This variation in intervention components and the limited geographic range (east and west coasts of the United States) further constrained generalizability. Additionally, three of the four studies had small sample sizes, reducing the statistical power to detect smaller effects. While the studies primarily focused on low-income populations, information about income levels was often limited. Three of the four studies predominantly involved African American participants, restricting applicability to other populations. The studies also exhibited considerable methodological flaws, such as inconsistent outcome reporting, high risk of bias, and unaddressed pretest differences, further limiting the strength of the evidence. Despite these limitations, the studies had notable strengths, such as two RCTs and the use of manualized interventions. Training was provided in three studies, and two RCTs and one QED had registered protocols. However, risk of bias was significant across the studies, with concerns related to randomization, missing data, and confounding.

Despite these limitations, this review provides a comprehensive summary of MFPs that combine financial services and healthcare services. This is the first systematic review examining health and financial outcomes of MFPs and therefore sheds early light on the promise and limitations of the body of evidence of MFPs on financial and health outcomes, as well as gaps to inform future MFP intervention development and research.

Footnotes

Acknowledgments

The authors are grateful for the assistance of Rebecca Hyde, MLS, Research and Instruction Services Librarian, Saint Louis University. She provided invaluable assistance with the database search strategy and implementation for this project. We also thank Hope Stratman, MSW, for her screening and editing contributions to this project.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.