Abstract

Introduction

Financial literacy is essential for managing debt, planning for retirement, and making informed money-related decisions. However, in India—especially in healthcare education—this important skill is often overlooked. For dental professionals, understanding their current financial knowledge, mindset, and habits is the first step toward addressing this gap. This study set out to assess the financial literacy of dental practitioners in Maharashtra and emphasize its importance in the current economic context.

Materials and Methods

A cross-sectional survey was carried out among 460 registered dental practitioners across five regions of Maharashtra, using a stratified sampling method. Participants completed a validated, self-administered questionnaire over a two-month period, which collected demographic details and evaluated financial awareness, attitude, and behavior. Data analysis included descriptive statistics, Chi-square tests for group comparisons, Spearman's correlation for relationships among financial domains, and logistic regression to examine links between participant characteristics and financial literacy. A p-value of less than .05 indicated statistical significance.

Results

The majority of respondents were women under 40, with fewer than 5 years of experience, holding postgraduate degrees (MDS/MBA/PhD), married, and with fewer than two financial dependents. Among them, 42.6% had good financial awareness, 99.1% demonstrated a positive financial attitude, and 36.5% showed good financial behavior.

Conclusion

Although most dental professionals exhibited a positive attitude toward financial matters, their awareness and practical financial behavior were only average. These findings point to the need for focused financial literacy initiatives tailored to dental practitioners.

Introduction

Financial literacy refers to the ability to understand and manage financial matters effectively, and it plays an important role in achieving personal financial well-being. It includes not only knowledge of financial concepts but also attitudes and behaviors related to money management, such as budgeting, saving, planning expenses, and making informed financial decisions (Howlett et al., 2008; Rai et al., 2019; Rath & Patra, 2023). Good financial literacy helps individuals maintain financial stability, while poor financial practices can contribute to debt, stress, and financial insecurity (Atkinson & Messy, 2012; Bhushan & Medury, 2014).

In recent years, financial literacy has become an important area of interest worldwide because of the increasing complexity of financial systems, investment opportunities, and credit options (Kapadia, 2019). The Global Financial Crisis of 2008 highlighted how inadequate financial understanding can lead to poor decisions with serious consequences at both individual and societal levels (Jayaraman & Jambunathan, 2018; Mulligan et al., 2020). Research has also shown that low financial literacy is associated with poor debt management, limited retirement planning, and reduced financial resilience (Ibrahim & Alqaydi, 2013; Wu et al., 2023).

In India, however, financial literacy receives limited attention in higher education, particularly in healthcare-related fields. Dental education primarily emphasizes academic knowledge and clinical skills, while practical areas such as personal finance, educational loans, investments, and financial planning for professional practice are often overlooked. As a result, many dental students and practitioners may enter the profession without sufficient financial preparedness, which can further add to the employment and economic challenges already faced in the dental profession (Awareness on Practice Management and Financial Literacy: Need of the Hour).

At present, there is limited evidence regarding financial literacy among dental practitioners in India. Understanding the financial literacy status of this group is important for identifying gaps and planning appropriate educational measures. Therefore, the present study aimed to assess financial literacy among dental practitioners in Maharashtra. The findings may help guide the inclusion of financial education in dental curricula, continuing professional development programs, and policy initiatives to better prepare dental professionals for financial decision-making and long-term career sustainability.

Materials and Methods

Study Design

It was a cross-sectional study.

Ethical Statement

The Institutional Ethical Committee approval was obtained prior to the beginning of the study (DYPDCH/IEC/33/2024).

Eligibility Criteria

Dental practitioners registered under the Maharashtra State Dental Council were included in the study. Dental practitioners residing and practicing outside Maharashtra were excluded. Participants who had not consented to be a part of the study were also excluded.

Sample Size Calculation

Dentists registered under Maharashtra State Dental Council: 46,243 (Dental Council of India, n.d.).

The sample size was calculated using the formula: n = N/(1 + Ne2).where n represents the required sample size, N is the total population size (46,243), and e is the margin of error (0.05) at a 95% confidence level. The sample size was calculated to be 382 which was increased to 480, keeping 25% as non-response rate.

Sampling and Participant Recruitment

The total sample size was 480. The list of dental practitioners registered under the Maharashtra State Dental Council was obtained from the Dental Council of India website. A stratified sampling method was used to include participants in the study. The state of Maharashtra was divided into five regions, namely: The Konkan region, Western Maharashtra region, Khandesh region, Marathwada region, and Vidarbha region (Dubey & Rishipathak, 2021). From each region, 96 registered dental practitioners were selected using simple random sampling.

Questionnaire Development

Following a review of the literature to identify the lacunae in financial literacy, a structured questionnaire was developed by the authors (RM and SM) using an online form application. The first section contained questions pertaining to demographic details, years of practice, educational qualification, marital status, and number of dependent family members. The second section consisted of 18 questions on financial awareness, the third section had nine questions on financial attitude, and the last section had ten questions on financial behavior. The questionnaire also consisted of questions on the level of satisfaction with the current financial condition, confidence in managing future financial conditions, and interest in learning about financial management. Compulsory fields were included for all the questions to ensure that no incomplete responses were accepted.

Each right response received one point, while an incorrect response received zero points, in order to determine the awareness scores. The awareness questionnaire's average score (50%) served as the benchmark for good and poor awareness. The 50% cutoff used to classify awareness, attitude, and behavior was chosen based on methods commonly used in knowledge, attitude and practice (KAP) studies when no standard cutoff values are available (Chowdhury et al., 2022). Using this threshold helped in simplifying the interpretation of responses and categorizing participants into meaningful groups. Nine was the average score (total number of questions = 18), and anything less than nine was considered poor. Positive and negative attitudes were evaluated. A cutoff point for positive and negative responses was determined by calculating the attitude questionnaire's average score. A score of less than five was considered negative, with an average of five (total number of questions = 9). The behavior was rated as either good or poor. The behavior questionnaire's average score was determined, and it served as the cutoff point for both positive and negative responses. Five was the average score (total number of questions = 10), with any number below five being labelled poor (Limbu et al., 2020). Similarly, the overall financial awareness, attitude, and behavior were calculated based on whether the overall scores were above or below average, that is, above or below 50% of the study participants.

Reliability Analysis

To ensure the questionnaire produced consistent results over time, test-retest reliability was checked by administering it to 25 individuals twice, with a one-week gap in between. The resulting score of 0.842 indicated strong reliability. Additionally, internal consistency was measured using Cronbach's alpha, which showed a value of 0.823. This suggests that the questionnaire items were well-aligned and measured the intended concepts reliably.

Validity Analysis

Five expert reviewers evaluated the content validity of the questionnaire. These experts were selected based on their experience in research and teaching, familiarity with the educational needs of the target population, and prior involvement in developing valid research instruments. Their background in scientific writing and translation also contributed to their selection (Grant & Davis, 1997).

To assess content validity, two established methods were used: the Content Validity Index (Item-Content Validity Index (I-CVI) and Scale-content validity index (S-CVI/Avg); Polit & Beck, 2006) and Lawshe's Content Validity Ratio (CVR) (Lawshe, 1975). The CVR measured how essential each item was, based on expert ratings using a 3-point scale (1 = not necessary, 2 = useful but not necessary, 3 = essential). The CVR was calculated using the formula:

For the CVI, experts rated each item's clarity and relevance using a 4-point scale (1 = not relevant to 4 = highly relevant). The Item-Level CVI (I-CVI) was determined by dividing the number of experts who rated an item as quite or highly relevant by the total number of experts. The Scale-Level CVI (S-CVI) was then calculated as the average of all I-CVI values.

I-CVI for each item was calculated using the formula:

S-CVI was used to assess the validity of the entire questionnaire. It was calculated by taking the average of all the I-CVI scores. The CVR values ranged from 0.60 to 0.95, indicating that the majority of items were seen as important by the reviewers. The I-CVI ranged from 0.80 to 1, showing strong consensus among the panel. The S-CVI was calculated to be 0.91, pointing to a high overall level of content validity for the questionnaire.

Questionnaire Administration

The questionnaire was sent online through email and WhatsApp messenger using a chain referral method. The purpose of the study, privacy protection statement and consent declaration statement were provided at the beginning of the survey. The respondents were asked to click a button of acceptance to participate in the survey. The questionnaire was open from November 2023 to January 2024.

Data Collection

Data of all the study participants were collected in Google Sheets and locked for review. All the data entries were reviewed by the principal investigator (RM) to ensure entry of correct information. The data was also reviewed and verified by the co-investigator (SM).

Statistical Analysis

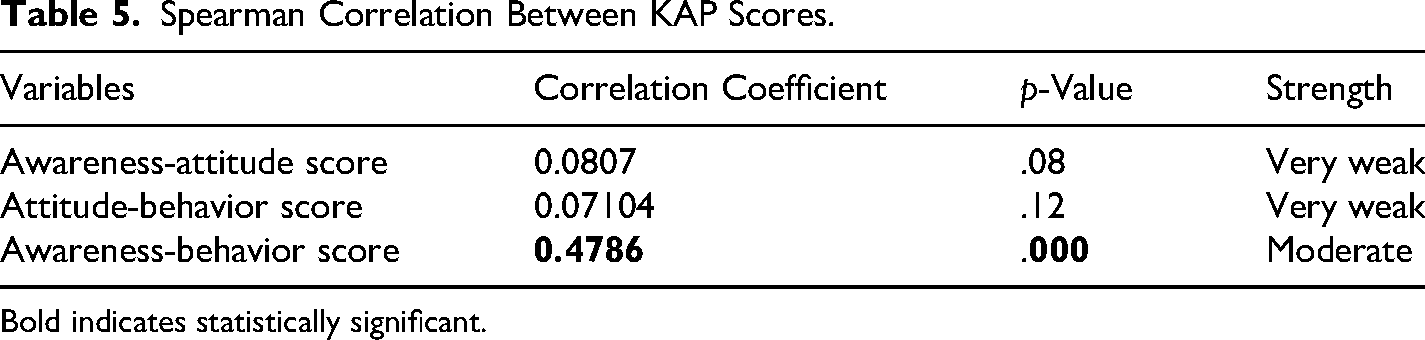

Statistical package for social studies (SPSS) version 22.0 (IBM Corporation, Chicago, IL, USA) was used for data entry and descriptive statistics. Chi-square test was used to assess the characteristics of the participants. The Spearman correlation coefficient test was used to assess the correlation between awareness, attitude, and behavior. The strength of the association between awareness, attitude, and practice was categorized as: 0.0–0.19 “very weak,” 0.20–0.39 “weak,” 0.40–0.59 “moderate,” 0.60–0.79 “strong,” and 0.80–1.0 “very strong” (Alnasser et al., 2021). Fourteen univariate and multivariate logistic regression analyses were used to assess the association between participants’ characteristics and awareness, attitude, and behavior. A p < .05 was considered statistically significant.

Results

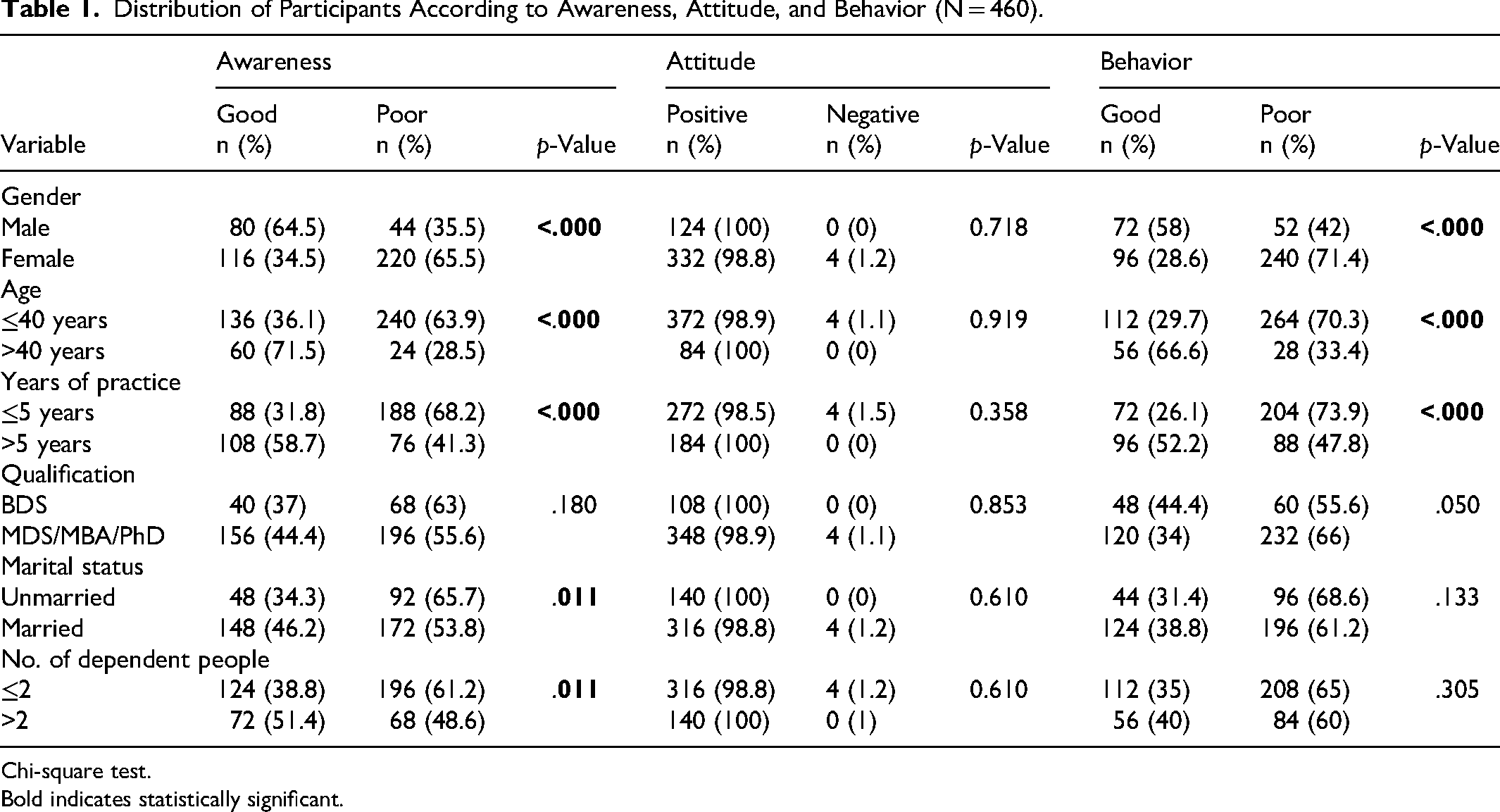

A total of 460 individuals responded to the online survey. 168 (35.5%) participants were satisfied with their current financial condition, 180 (39.1%) participants were confident about their future financial condition, and 320 (69.5%) participants were very interested in increasing their financial awareness. The majority of study participants were female, under 40 years old, had less than 5 years of experience, held an MDS, MBA, or PhD degree, were married, and had fewer than two family members who were financially dependent. Overall, only 196 (42.6%) individuals had a good financial awareness, and 168 (36.5%) people had a good financial behavior suggesting that the financial awareness and behavior among the study participants was poor. However, 456 (99.1%) participants had a positive financial attitude, suggesting that financial attitude among the study participants was good.

Awareness, Attitude, and Behavior Based on the Characteristics of the Participants

Males were found to have a better awareness and behavior as compared to females (p < .000). Participants who were above 40 years of age were found to have a better awareness and behavior as compared to participants who were below 40 years of age (p < .000). Participants with more than 5 years of practice were found to have a better awareness and behavior as compared to those with less than 5 years of practice (p < .000). Married people and those having more than two financially dependent people in the family were found to have a better awareness (p < .000) (Table 1). All other findings were statistically insignificant.

Distribution of Participants According to Awareness, Attitude, and Behavior (N = 460).

Chi-square test.

Bold indicates statistically significant.

Association Between Awareness and Characteristics of the Participants

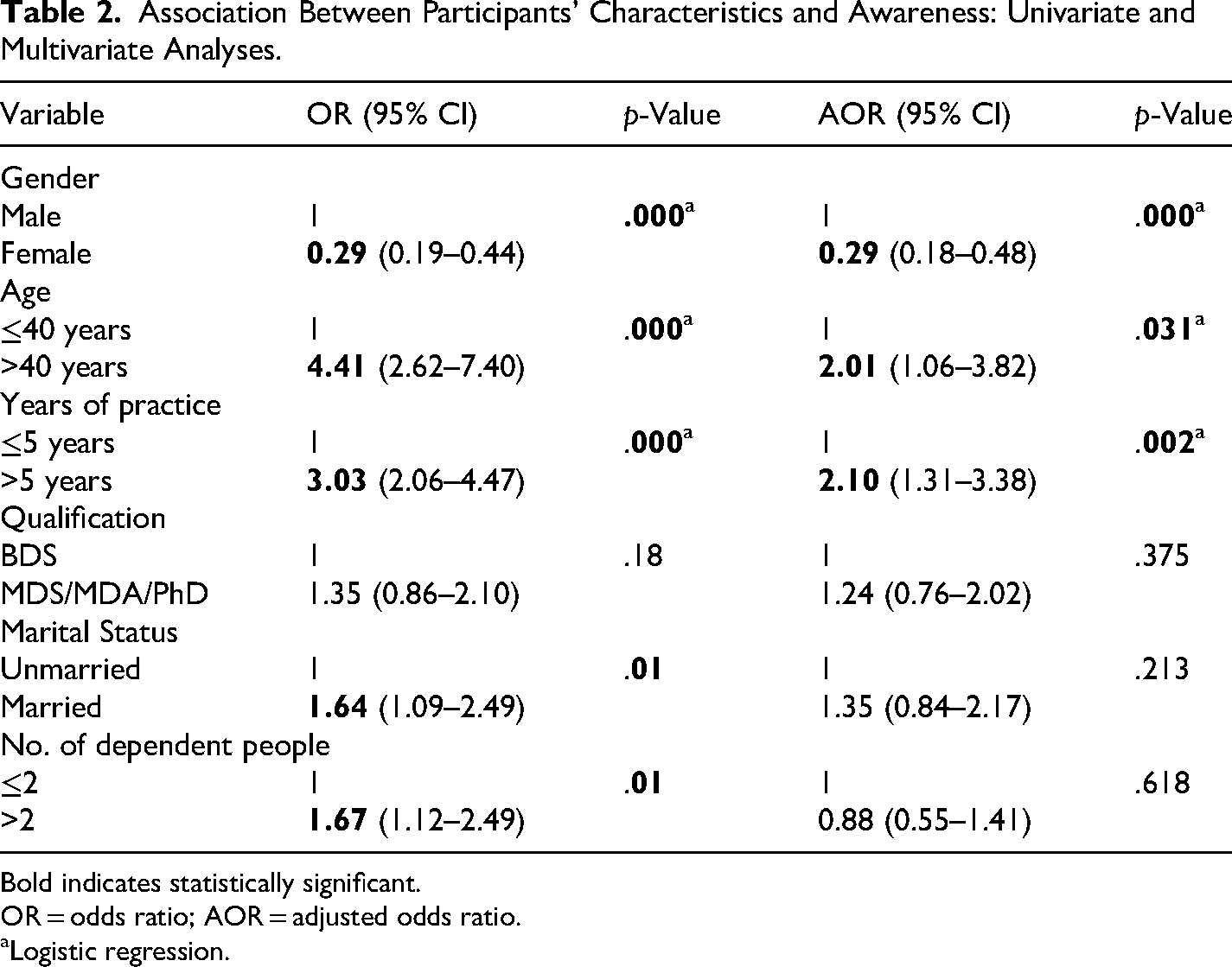

Table 2 shows the factors associated with participants’ financial awareness. In the univariate analysis, female participants were less likely to demonstrate good financial awareness compared to males. In contrast, participants aged above 40 years, those with more than 5 years of professional experience, married participants, and individuals with more than two dependents showed better financial awareness. After adjusting for potential confounding factors, gender, age, and years of practice remained significantly associated with financial awareness. Female participants continued to demonstrate lower financial awareness, whereas older participants and those with greater professional experience were more likely to exhibit good financial awareness. However, marital status and number of dependents were no longer significantly associated in the multivariate analysis.

Association Between Participants’ Characteristics and Awareness: Univariate and Multivariate Analyses.

Bold indicates statistically significant.

OR = odds ratio; AOR = adjusted odds ratio.

Logistic regression.

Association Between Attitude and Characteristics of the Participants

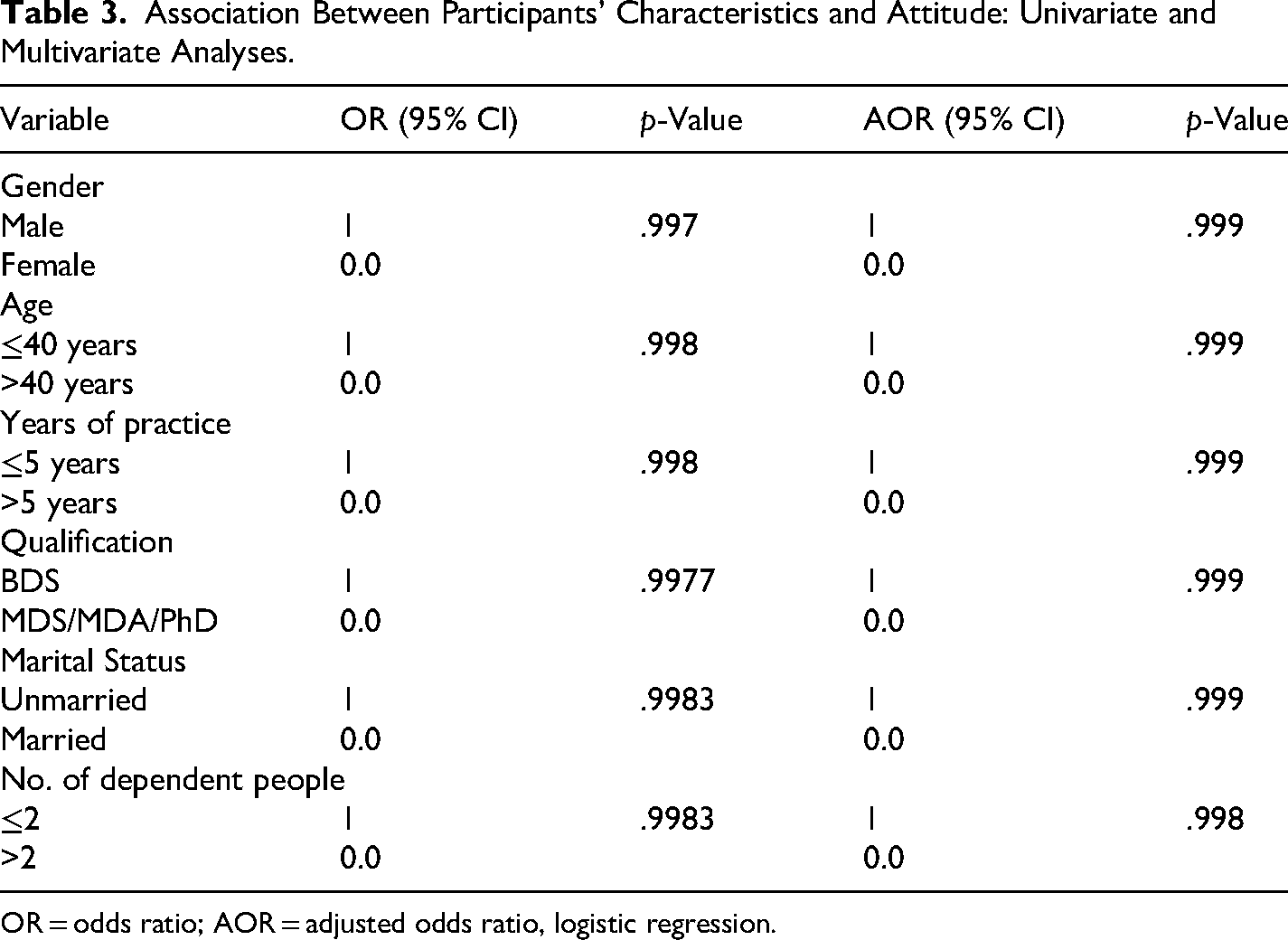

Table 3 presents the variables related to the participants’ financial attitude. Neither univariate analysis nor multivariate analysis revealed any significant correlation between the participants’ attitudes about finance and any of the following variables: gender, age, years of practice, qualification, marital status, or the number of persons who depended on them financially.

Association Between Participants’ Characteristics and Attitude: Univariate and Multivariate Analyses.

OR = odds ratio; AOR = adjusted odds ratio, logistic regression.

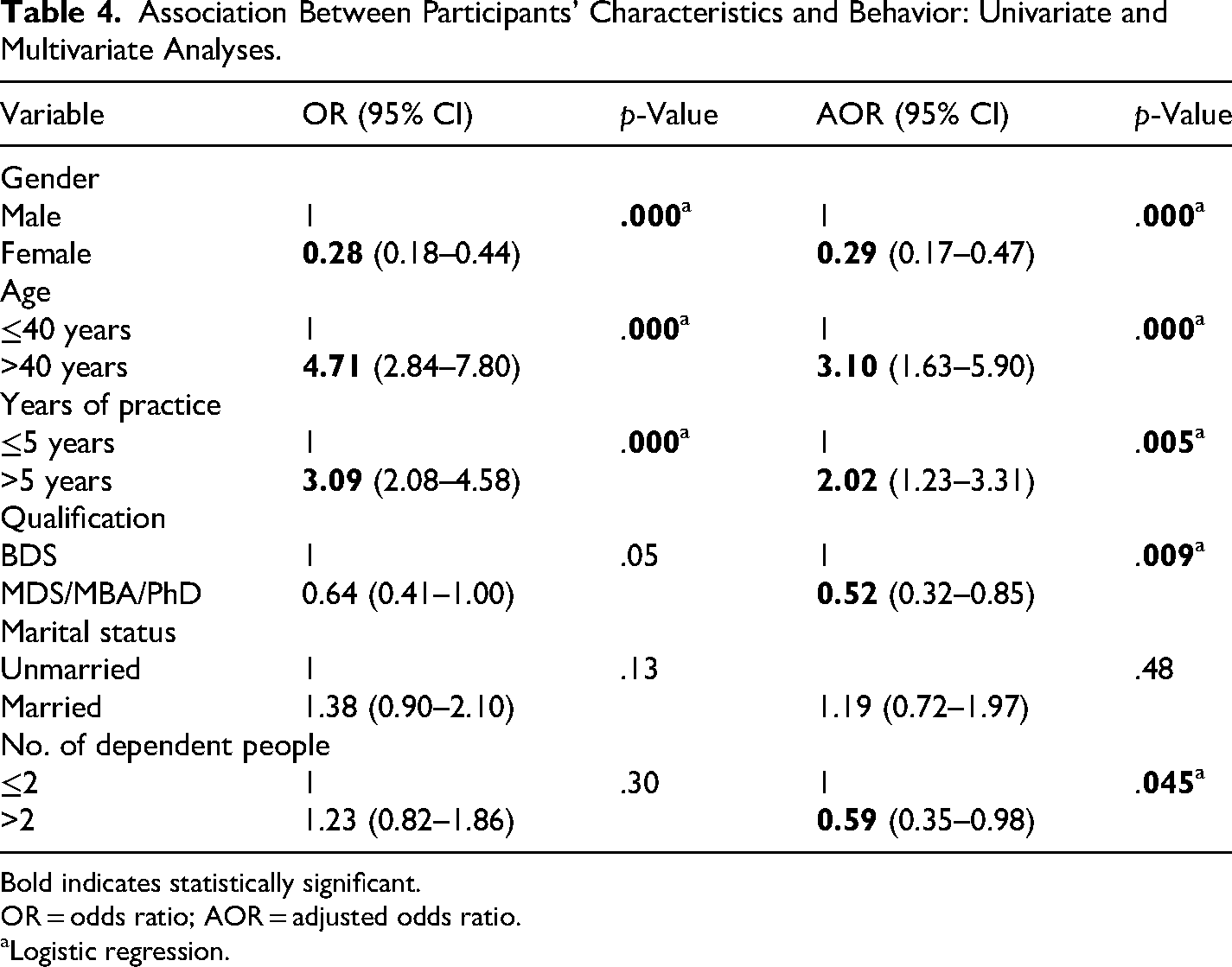

Association Between Behavior and Characteristics of the Participants

Table 4 shows the factors associated with participants’ financial behavior. In the univariate analysis, female participants demonstrated poorer financial behavior compared to males, while participants aged above 40 years and those with more than 5 years of professional experience showed more positive financial behavior. After adjusting for potential confounding variables, gender, age, years of practice, qualification, and number of dependents remained significantly associated with financial behavior. Female participants continued to exhibit lower financial behavior scores, whereas older participants and those with greater professional experience were more likely to demonstrate positive financial behavior. Participants with higher qualifications such as MDS/MBA/PhD and those with more than two dependent family members were less likely to exhibit good financial behavior. However, marital status was not found to be significantly associated with financial behavior in the multivariate analysis.

Association Between Participants’ Characteristics and Behavior: Univariate and Multivariate Analyses.

Bold indicates statistically significant.

OR = odds ratio; AOR = adjusted odds ratio.

Logistic regression.

Correlation Between Awareness, Attitude, and Practice

The findings of the Spearman's Rho test indicated a “moderate” but statistically significant positive relationship between attitude and awareness (p < .05). The strength of association between awareness-attitude, and attitude-behavior was “very weak.” However, the findings were statistically insignificant (Table 5).

Spearman Correlation Between KAP Scores.

Bold indicates statistically significant.

Discussion

There is an increasing need for financial literacy among healthcare professionals, particularly in India. Although dental practitioners generally have stable and well-paying careers, many still face difficulties in managing their finances effectively due to inadequate financial education and limited awareness regarding financial planning. Therefore, the present cross-sectional questionnaire-based study was conducted to assess the level of financial literacy among dental practitioners in Maharashtra and to highlight its growing importance in the current economic scenario.

The findings of the study revealed that while the participants demonstrated a positive attitude toward financial management, their levels of financial awareness and financial behavior were comparatively poor. This indicates that although dental professionals understand the importance of financial planning, there is still a substantial gap in practical knowledge and implementation of healthy financial practices. Encouragingly, the positive attitude observed among participants suggests that they may be receptive to financial education and willing to adopt better financial habits if appropriate learning opportunities are made available.

Multivariate regression analysis showed that gender (AOR = 0.29), age (AOR = 2.01), and years of practice (AOR = 2.10) significantly influenced financial awareness. Female participants demonstrated lower financial awareness compared to males, which is in agreement with findings from previous national and international studies (Alesina et al., 2013; Atkinson & Messy, 2012; Bucher-Koenen et al., 2014; Lusardi et al., 2014; Lusardi & Mitchell, 2008; Yu et al., 2015). This may be because men are traditionally more involved in household financial decision-making, thereby gaining greater exposure to financial matters. Participants aged above 40 years exhibited better financial awareness than younger participants, possibly due to greater professional experience, higher income levels, and improved financial decision-making skills developed over time (Satoshi & Hiroyuki, 2020; Wilson et al., 2022). Similarly, dentists with more than 5 years of professional experience showed better financial awareness than those with fewer years of practice, likely because of increased exposure to financial responsibilities and practice management (Chen & Volpe, 1998).

Most participants also demonstrated a positive attitude toward financial management, although no significant association was found between financial attitude and participant characteristics. Nevertheless, a positive financial attitude may serve as an important foundation for improving financial literacy and encouraging responsible financial behavior (Rai et al., 2019).

Financial behavior was found to be significantly associated with gender (AOR = 0.29), age (AOR = 3.10), years of practice (AOR = 2.02), qualification (AOR = 0.52), and number of dependents (AOR = 0.59). Since financial awareness and financial behavior are closely related (Khawar & Sarwar, 2021), participants aged above 40 years and those with more than 5 years of practice also demonstrated more favorable financial behavior. Female participants showed comparatively lower financial behavior scores, which may be because many relied on spouses or family members for financial decision-making, limiting their active involvement in financial management (Van Nguyen et al., 2022).

Interestingly, participants with higher qualifications such as MDS, MBA, or PhD demonstrated poorer financial behavior despite having better financial awareness. This finding differs from several previous studies that reported a positive relationship between financial awareness and financial behavior (Nave et al., 2023; Rahman et al., 2021). One possible explanation could be the financial burden associated with higher education, including educational loans and increased academic expenses, which may negatively affect savings and investment planning. In addition, participants with more than two dependents showed poorer financial behavior, possibly because increased family responsibilities and expenses reduce opportunities for saving and long-term financial planning (Lugauer et al., 2019; Van Winkle & Monden, 2022).

A positive and significant association was observed between financial awareness and financial behavior, suggesting that improving financial knowledge may help promote healthier financial practices among dental professionals. This highlights the importance of educational interventions aimed at improving financial literacy.

Only 35.5% of the participants reported satisfaction with their current financial condition, while 39.1% expressed confidence regarding their future financial status. Similar findings have been reported in previous studies (Kumar et al., 2014; Priya et al., 2014; Shyam & Dande, 2020). The low levels of financial confidence observed in the present study may reflect inadequate financial planning skills and the absence of formal financial education among dental professionals.

Implications

The findings of this study have implications beyond personal finance and extend into educational reform and institutional policy. Incorporating financial literacy into undergraduate and postgraduate dental curricula may help dental professionals develop essential life-management skills early in their careers. Topics such as budgeting, taxation, insurance, investment planning, educational loan management, retirement planning, and practice management may be particularly beneficial. In addition, dental institutions and academic leaders can play an important role by organizing workshops, mentorship programs, and continuing education initiatives focused on financial wellness. Institutional policies that support financial counselling and financial literacy training may ultimately contribute to improved professional well-being, reduced financial stress, and greater long-term career sustainability among dental practitioners.

Limitations

Since the study presents data only from one state in India (Maharashtra), the findings of this study should be utilized with caution for generalization. Furthermore, self-reported behavioral habits may not be accurate; thus, additional research is required in this direction.

Future Recommendations

Future multicentric and longitudinal studies involving dental professionals from different regions of India are needed to improve the generalizability of the findings and to better understand how financial literacy changes over the course of a professional career. Further research should also focus on assessing the effectiveness of curriculum-based financial literacy interventions, such as workshops, mentorship programs, and structured educational modules, in improving financial awareness and behavior among dental professionals. In addition, studies evaluating institutional policies and the role of educational leadership in promoting financial well-being may help identify effective and sustainable approaches for implementation within dental education. Considering the lower financial literacy observed among female participants in the present study, future research should also explore gender-specific barriers and targeted interventions to support equitable financial literacy and long-term professional well-being.

Conclusion

Our study concluded that although majority of the dental practitioners in Maharashtra had good financial attitude, their financial awareness and behavior was poor. Further, a positive and significant relationship between financial awareness and behavior was noted. Thus, targeting the financial awareness may lead to better financial behavior. To promote holistic financial development of dental practitioners, we propose the inclusion of financial literacy in the dental teaching curriculum as an elective subject.

Footnotes

Author’s Note

The manuscript has been read and approved by all the authors; the requirements for authorship as stated earlier in this document have been met, and each author believes that the manuscript represents honest work.

Authors contributions

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.