Abstract

We assess how a retailer can manage inventories and labor under an extreme condition such as a temporary negative demand shock due to a pandemic or an economic turmoil. This analysis incorporates labor market frictions whereby firms incur deadweight costs associated with hiring and firing employees, as well as the option to furlough labor. We examine the impact of these frictions on a retail firm's optimal operating policies around inventory level, furlough, and layoffs. We find that labor market frictions condition the inventory and the level of employment in two ways. First, they lead to underinvestment in inventories, which limits recovery and employment in the postshock period. Second, high labor market frictions motivate the firm to conservatively downsize workforce during the negative demand period leading to higher employment, when compared to downsizing without friction. A significant contribution of our study lies in delineating the optimal furlough decisions and quantifying the impact of the furlough option on inventory and labor decisions. We demonstrate the conditions under which it is optimal for the retailer to either (i) fully downsize labor and leverage the furlough option in the labor market, or (ii) maintain excess labor while also opting to furlough a portion of the workforce. During an extreme event such as a temporary negative demand shock, our results highlight the need for a coordinated effort when implementing governmental subsidy policies on alleviating labor and inventory reductions by accounting for labor market frictions and furlough support.

Introduction

Efficiently scaling down and then ramping up operations during and after an economic turmoil is vital for business resilience. Even temporary shocks may drive firms to bankruptcy if they are obliged to pay off their fixed costs in the short-term. Economic turbulences, such as the U.S. recession in 2001 and the global financial crisis in 2009, typically precipitate a downturn in consumer spending. This contraction in consumption predominantly affects discretionary sectors, leading to a decline in demand for nonessential items, particularly in the realms of entertainment and luxury goods. A recent driver of such demand shocks was the COVID-19 pandemic, during which retailers like car dealerships, beauty salons, and fashion stores struggled to survive as demand for their services and products vanished.

In this manuscript, we explore a retailer's optimal operations in the face of a negative demand shock, amidst labor market frictions and with the possibility of furloughing employees. We assume that the demand shock is temporary and the markets are expected to recover over time. If a demand shock results in a permanent change in supply and demand dynamics in an industry, such as changing consumption habits, then some firms may face scenarios such as voluntary liquidation, or alterations in business models, which are beyond the scope of this manuscript. That is, most retail firms hope to weather a finite and downward economic shock by temporarily downsizing and then returning to routine operations. This scenario is addressed in this paper.

Downsizing retail operations involves two crucial and interconnected decisions: (a) reducing labor through layoffs and/or furloughs, and (b) decreasing inventory levels. This dual decision strategy has been adopted during economic downturns and reported in popular press during the US recession of 2001, the global financial crisis of 2009, and more recently, the COVID-19 pandemic. Such periods often prompt retailers to simultaneously cut labor and adjust inventory. For instance, the COVID-19 pandemic led to widespread layoffs and furloughs, with a notable impact attributed to retailers (Reuters, 2020). High-profile retailers, including Ralph Lauren, Kohl's, Tailored Brands, JC Penney, PVH Corp, and Walgreens made significant inventory and labor reductions to preserve profitability (Business Insider, 2020).

While layoffs often dominate media headlines, reducing inventories is another critical aspect of retail downsizing during economic challenges. The downturns trigger a decline in consumer demand, compelling many retailers to shut stores and either postpone or completely cancel orders. This action, although less publicized, is essential for managing resources and adapting to reduced market demand.

As markets rebound from economic disruptions, restoring labor and inventory levels also pose operational challenges. Frictions in the labor market make it costly, and uncertain, to find and train new workers. The literature on labor economics has long argued that “Trade in the labor market is a nontrivial economic activity due to the existence of heterogeneities, frictions and information imperfections” (Pissarides, 2000). As explained by the Diamond-Mortensen-Pissarides (DMP) model of labor market frictions by Diamond (1982), Mortensen (1982) and Pissarides (1985), no retailer would want to lose experienced labor force, as replacing this labor later in the market will result in both indirect costs (associated with the loss of valuable tacit knowledge, reduced efficiency in meeting demand, and training costs) and direct costs of firing and hiring. Additionally, in retail, labor and inventory are complementary resources, i.e., the marginal value of each of these resources on the firms’ ability to meet customer demand increases with the availability of the other resource. Hence, scaling up and down inventory and labor are closely linked in practice.

Evidence from downturns suggests that furlough schemes play a pivotal role for firms in reorganizing operations during economic shocks, facilitating recovery without the destruction of capital and jobs (Görtz et al., 2022). This issue underscores the importance of furloughs in maintaining business resilience and aiding in postcrisis recovery. Typically, they are not part of standard business practices but are employed during significant market shocks that lead to a substantial reduction in demand. Resorting to furloughs during minor market fluctuations can negatively impact long-term labor recruitment and retention, eroding employee trust and loyalty. As such, businesses often view furloughs as a last-resort option, indicating a balance between immediate operational requirements and the long-term sustainability of the workforce (Sucher and Winterberg, 2014).

1

Thus, motivated by the observed operating decisions of retailers during the economic downturns driven by the recent pandemic or previous financial crises, we formulate the following research questions:

How do firms make integrated labor and inventory management decisions in the presence of labor market frictions? Labor management decisions include hiring, firing as well as furloughing labor in the face of an economic shock. What is the value of the furlough option for firms, and how does it affect their decisions regarding inventory and labor scaling? Additionally, how is the value of the furlough option influenced by key market conditions such as labor market frictions, labor market uncertainties and retail margins?

We set up a stylized two-period model to examine our research questions. The first period pertains to the economic downturn and the second period pertains to economic recovery. We show how a retailer would manage its inventory and labor capacity decisions in an integrated manner in the face of a negative demand shock (driven by, e.g., a pandemic or an economic downturn) and labor market frictions. Labor market frictions capture various costs such as search, training, and hiring expenses for new employees, alongside opportunity costs from potential reductions in sales efficiency during transitions. They also account for increased hiring costs amidst potential future labor shortages. Our contributions to the literature are summarized as follows:

We begin with our analysis by showcasing the benchmark scenario when there are no labor market frictions. In this context, we establish that labor and inventory decisions are separable. We show that labor market frictions call for joint consideration of labor and inventory decisions.

When labor market frictions are introduced in a downsizing scenario, these frictions are expected to attenuate labor reductions during periods of low demand due to the costs associated with rehiring in subsequent periods — a standard inference derived from stochastic control literature. However, this intuition may not hold, as shown in our analysis, due to the interplay of labor, inventory, and furlough decisions.

We demonstrate that labor market frictions only mitigate labor reduction in the first period if the level of frictions exceeds a certain threshold identified in our model. If the level of frictions is below this threshold, the presence of frictions does not affect labor downsizing. However, regardless of the friction level, it invariably results in a reduction in new inventory orders. This has a nuanced impact on operations by limiting new hires in the second period, consequently restricting the firm's ability to recover or ramp up during the time of recovery.

Our analysis highlights a key mechanism for functioning of the labor market frictions on the operations of the firm. This functioning, in our model, is characterized by two separate and complementary impacts on labor level: (a) a positive main effect on the labor amount in the first period and (b) a negative secondary effect on the labor level in the second period induced through reduced inventory levels. The net employment effect of labor market frictions is the sum of these two affects, which can be positive depending on the level of labor market frictions, profit margin and demand uncertainty.

In addition, our findings on furloughs indicate that a furlough option benefits the firm by mitigating inventory downsizing and facilitating recovery after the demand shock. However, the impact of furloughs on labor downsizing varies with the level of labor friction. With low labor friction, furloughs do not influence the extent of labor downsizing but can convert some of the terminated positions into furloughed ones. Conversely, in environments of high labor friction, the furlough option may lead to increased labor downsizing by transitioning more employees to furlough status. We also identify specific thresholds related to demand, labor friction and furlough risk, determining when a firm might opt for furloughs, retain excess labor (minimize labor downsizing), or apply both strategies—using furloughs while also maintaining excess labor.

Through detailed numerical analysis, we also explore how the impact of labor frictions and furlough options is influenced by the retail margin. We show that under a low profit margin, it is typically optimal to fully downsize labor (i.e., reducing the labor to a level that is just sufficient to meet the demand); and the main positive impact of labor market frictions on employment disappears. Hence, low profit margin firms are more likely to experience an increase in employment due to a reduction in labor market frictions (possibly driven by a governmental policy action) as compared to high profit margin firms.

In terms of the value and impact of furloughs, we observe that firms derive greater benefits from furloughs when labor market frictions and retail profits are moderate—neither too low nor too high. Although firms with low profit margins tend to initiate furloughs earlier in response to labor market frictions, firms with intermediate profit margins tend to place more labor on furlough in total.

Literature Review

Our research intersects with the literature on the operations-finance interface, the management of workforce flexibility, and labor economics. Over the last ten years, researchers have shown increasing attention to problems at the interface of operations and financial management (Babich and Birge, 2022; Babich and Kouvelis, 2018; Mutha et al., 2021). This stream focuses exclusively on frictions (and their impact on operations) associated with the acquisition of a vital resource: capital. Besides capital, labor is another vital resource, and trading in the labor market is also subject to frictions (Pissarides, 2011). However, there is limited work on the interaction of operations and labor management decisions in the presence of labor market frictions. In this study, we provide an integrated approach to coordinating labor, inventory, and furlough decisions within a retail context, amid labor market frictions.

It is well-established in the finance literature that, within imperfect capital markets, financial decisions may impact other management decisions (such as inventory levels) within the firm, and ultimately also affect the firm's ability to create value (Froot et al., 1993; Mayers and Smith, 1982; Smith and Stulz, 1985; Stulz, 1996). For example, bankruptcy cost is a prevalent form of capital market friction, and it has been shown that this cost can lead to substantially conservative operating and investment decisions by firms compared to the perfect market case (Alan and Gaur, 2018; Kouvelis and Zhao, 2012, 2016; Tanrisever et al., 2021). Similarly, the operational role of other capital market frictions such as moral hazard (Yang et al., 2021), transaction costs (Goel and Tanrisever, 2017), informational asymmetry (Lee et al., 2022; Tang et al., 2018), and financial distress cost (Birge et al., 2017) has also been explored in the operations literature. This adjacent literature has informed our models and analysis.

Regardless of the particular form of capital market frictions, they induce potentially value-destroying operating behavior within firms. A number of studies have examined how the value-destroying impact of frictions can be mitigated by (a) using innovative financial technologies such as reverse factoring (Kouvelis and Xu, 2021; Tanrisever et al., 2015), trade credit (Devalkar and Krishnan, 2019; Yang and Birge, 2018), purchase order finance (Reindorp et al., 2018), and other forms of supply chain finance applications (Tunca and Zhu, 2018); (b) adopting operational flexibility (Boyabatli and Toktay, 2011; Chod and Zhou, 2014; Iancu et al., 2017); and (c) implementing financial hedging and risk management practices (Boyabatlı et al., 2011; Devalkar et al., 2018; Ding et al., 2007; Goel and Tanrisever, 2017; Kouvelis and Li, 2019).

Within this stream of operations and finance literature, our study is most closely related to the papers exploring the role of operational flexibility and hedging in the presence of capital market frictions (Boyabatlı et al., 2016; Boyabatlı and Toktay, 2011; Chod and Zhou, 2014; Iancu et al., 2017). Boyabatli and Toktay (2011) and Boyabatlı et al. (2016) are among the first studies exploring the interaction of capital market frictions and operational flexibility on the financial performance of the firm. These authors show how the presence of capital market frictions and budget limits may motivate the firm to adopt more flexible technology. In a similar spirit, Iancu et al. (2017) examine the impact of operating flexibility in the presence of capital market frictions and debt covenants. They find that operating flexibility may not always benefit the firm under imperfect capital markets.

In a manner that is analogous to the above-mentioned flexibility papers (Boyabatli and Toktay, 2011 and Iancu et al., 2017), the ability to furlough labor provides the firm with operational flexibility when trading in the labor market via mitigating labor market frictions. In the presence of labor market frictions, this flexibility directly interacts with the operating decisions. That is, we set up a broader context for examining the interaction of market frictions and operating flexibility, which leads to novel operational insights around downsizing and furlough options.

Labor economists have long argued that trading in the labor markets is subject to deadweight costs, i.e., frictions (Diamond, 1982; Mortensen, 1982; Pissarides, 1985). These frictions include direct and indirect costs such as lost tacit knowledge due to losing a trained employee, search and training costs for a new hire, etc. Diamond–Mortensen–Pissarides (DMP) model takes labor market frictions in its core and aims to provide an explanation for the unemployment phenomena in the markets. Following the DMP model, numerous works have incorporated labor market frictions into both micro- and macro-economic models to analyze labor markets. For instance, motivated by the COVID-19 pandemic, Bernstein et al. (2020) examine the U.S. labor markets under a significant job separation shock, and Birinci et al. (2021) study the implications of labor market policies that counteract the economic fallout from containment measures during the pandemic. Birinci et al. (2021) provide an equilibrium analysis of labor markets under a standard disease spread model to examine the impact of unemployment insurance programs and payroll subsidies. They find that payroll subsidies, which preserve match capital and enable a faster economic recovery, are preferred over unemployment insurance programs. In the retail context, in a make-to-stock business model, our work provides a detailed analysis of interaction of labor, furlough and inventory decisions in the presence of labor market frictions. We highlight the mechanism through which labor frictions interact with inventory and labor decisions possibly leading to nonmonotone impact on total employment.

Furlough dynamics in our model are also linked to the literature on workforce flexibility (Kesavan et al., 2014; Pinker et al., 2009; Pinker and Larson, 2003; Qin et al., 2015). These studies focus on trade-off between employing regular versus contingent workers, emphasizing the optimization of staffing decisions to minimize costs while enhancing operational responsiveness. Related findings suggest that while flexibility in labor can significantly benefit organizations by allowing them to adapt to demand fluctuations, there exists an optimal level of such flexibility beyond which the costs may outweigh the benefits.

Model Description

We develop a two-period model where the firm, in each period, decides the volume of inventory and labor to meet random demand. The inventory decisions follow a newsvendor setup such that the firm needs to order prior to observing the demand due to long lead times that are common in many retail businesses. The firm has some flexibility in accessing the labor market, and the labor capacity can be revised after observing the demand subject to market frictions. Retail products that typically involve contingent sourcing of labor but not inventory include fashion and apparel items, tech gadgets, and custom-designed goods. These products often require specialized skills for design, production, or customization, which can be sourced on a contingent basis. However, the inventory for these products, such as raw materials or premanufactured components, may require long-term planning and purchasing agreements, making contingent sourcing less feasible.

Matching supply and demand in retail requires the simultaneous presence of labor (such as sales assistants in physical stores or packaging workers in online retailers) and customer since labor facilitates the delivery of the goods and service to the customer (Boulding et al., 1994). For expositional simplicity, we will model this “facilitation function” of labor as a linear relationship between sales and labor capacity given that there is sufficient demand and inventory, i.e., availability of labor does not affect the demand, but labor enables the firm to generate sales by exploiting demand. 2 It is also possible to model labor as an aggregation of agents who can not only generate sales but also increase demand by exerting sales effort (see e.g., Dai and Jerath, 2013). We ignore this possibility and posit that our main findings will remain the same if this possibility is considered within our model. We also assume that there is no moral hazard, and labor exerts full effort. This situation can be achieved by properly designing labor compensation packages, which is beyond the scope of our work (Dai and Jerath, 2013).

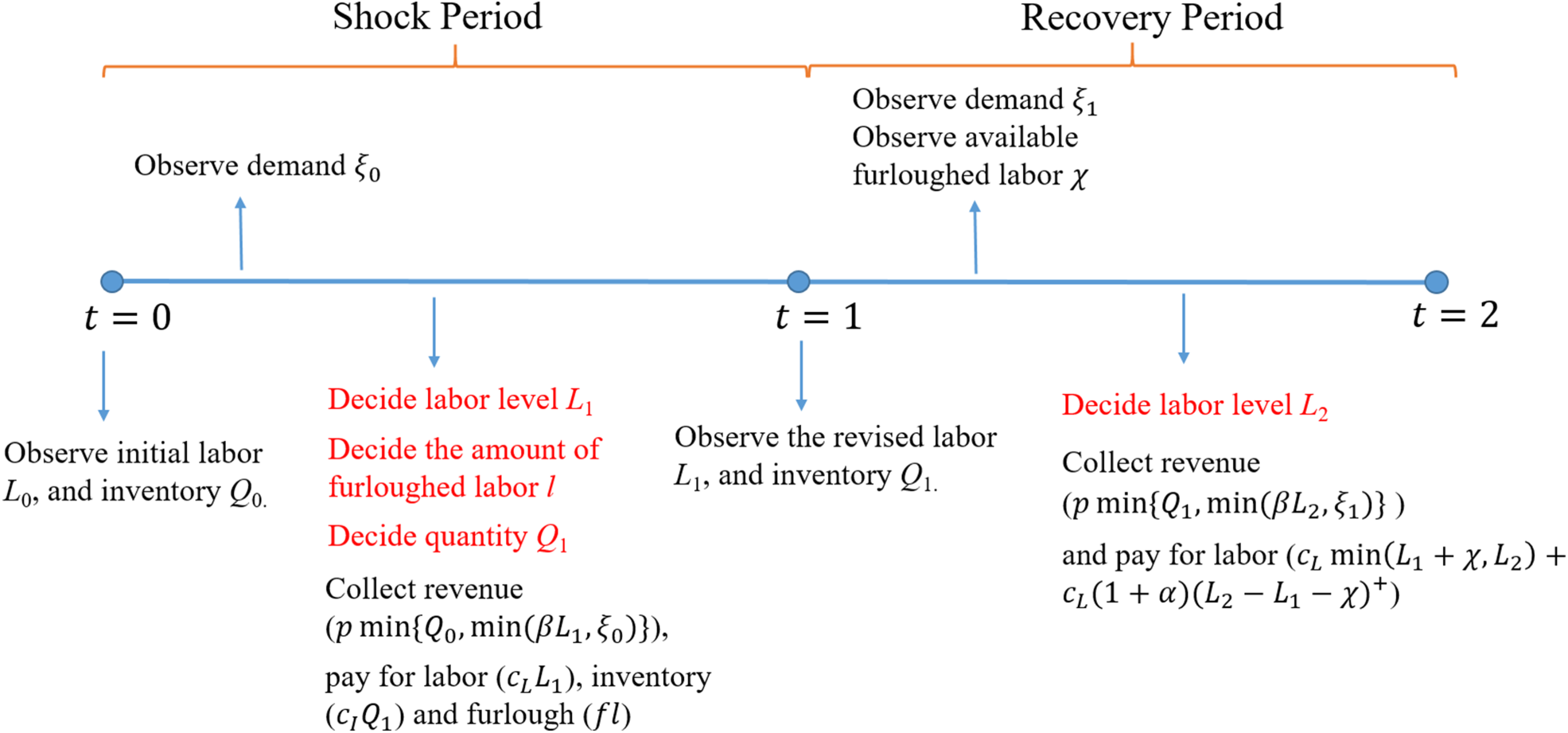

The first stage of our model denotes the shock period, where the firm is subject to a significant negative shock; and the second stage corresponds to the recovery period where the demand restores back to preshock level. For ease of exposition, we explicitly assume that the shock and recovery periods are of the same length. By properly scaling problem parameters, it is possible to capture unequal period lengths. Timeline of events and decisions are detailed below and are depicted in Figure 1.

Timeline of events and decisions.

Decisions and Events during the Shock Period: We assume that the firm embarks to the shock period with

During the shock period, the firm observes a negative demand shock significantly reducing the demand (below its usual level) down to level

The firm may also choose to put some of the laid-off workers, l, on furlough by paying a unit cost of f. In the second period, furloughed workers may be called back to increase labor capacity without being subject to labor market frictions. After the first period, the potential return of furloughed labor to work remains uncertain. In practice, the duration of this shock period greatly influences whether furloughed employees will seek alternative employment or pursue new training opportunities, potentially leading to the discovery of different job prospects. To address this uncertainty, we assume that in the recovery period, the amount of furloughed labor available to call back to work is denoted by a random variable

During the shock period, the retailer sells its existing stock

As noted above, labor is needed to exploit the observed demand and generate sales, and hence during the first period, the revenues of the firm can be stated as

Although, reduced inventory and labor levels (

Decisions and Events during the Recovery Period: During the recovery period, after observing the new inventory level

Then, the firm meets the demand, collects revenues

Given the realized profits at the end of each period and the decisions in each stage, the retailer's two-stage optimization problem can be formalized as follows:

To summarize,

Since we model a negative demand shock, both

In this section, we begin with our analysis by showcasing the benchmark scenario when there are no labor market frictions. Next, we introduce labor market frictions and examine the interaction of labor and inventory decisions. Following this, we model the option for furloughing labor, examining both its value and its influence on firm decisions.

It is convenient to analyze the model backward starting with the last decision

(Recovery stage)

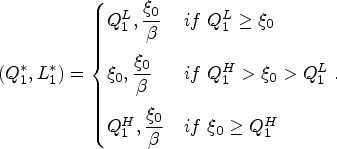

The optimal second period labor level of the firm is given by

The first scenario in Lemma 1 denotes the case when the unit sales price is sufficient to cover the marginal cost of hiring new labor, i.e.,

We begin our analysis with labor markets with no frictions in Proposition 1, i.e.,

(Labor Market with no Frictions)

When there are no labor market frictions, i.e.,

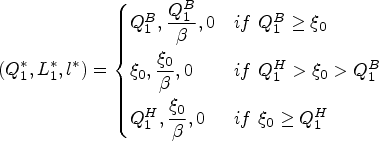

Optimal decisions without furlough.

Optimal decisions without furlough.

Modiglianni-Miller (MM) results in the finance literature establish that financial and operational decisions are separable when there are no capital market frictions. Analogously, we also find that the first stage labor (

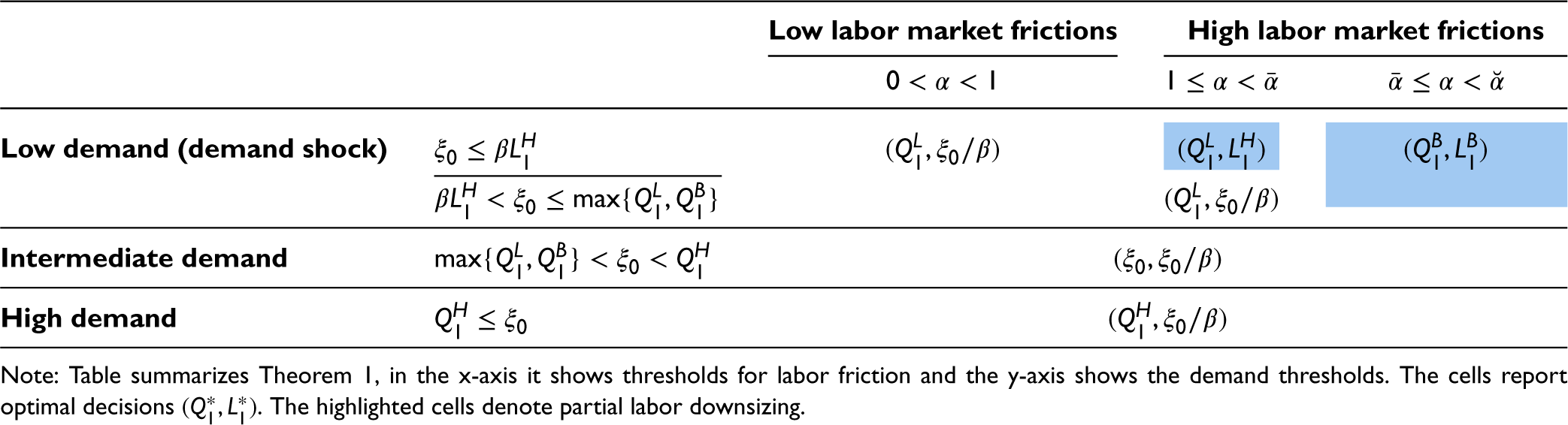

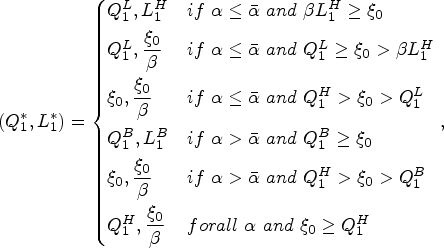

In Theorem 1, we present the results when we introduce the labor market frictions to the case discussed in Proposition 1. Theorem 1 is instrumental in explaining the impact of labor market frictions.

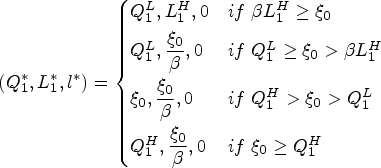

(Labor Market with Frictions and without Furlough)

Suppose there are labor market frictions (

If the level of labor market frictions is low, i.e.,

If the level of labor market frictions is high, i.e.,

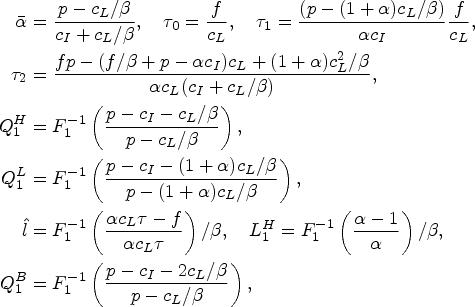

where

Under low labor market frictions (

Impact of low labor market frictions (

Recall that

Impact of high labor market frictions (

Case (i): If

Case (ii): If

Theorem 1 highlights the role of labor market frictions in shaping operating decisions. This role, in our model, is characterized by two separate and complementary impacts on labor level: (i) a positive main effect on the labor amount in the first period and (ii) a negative secondary effect on the labor level in the second period induced through reduced inventory levels. On the one hand, increased labor market frictions may lead to less aggressive downsizing of labor, i.e., partial downsizing may be possible. On the other hand, reduced orders for the second period limits firm's ability to meet the demand and hence leads to reduced hiring in the second period. The net employment effect of labor market frictions is the sum of these two affects in our model. In Section 5, we numerically illustrate the economic conditions under which the net effect of labor market frictions is positive on total employment.

So far, we have conducted our analysis in isolation of furlough possibility. In this section, we expand our examination to include furlough, assuming that furloughed employees may return to work with a probability

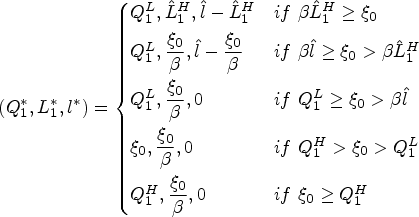

(Labor Market with Low Labor Frictions and with Furlough)

Assuming labor market frictions such that

The labor decisions in Theorem 2 align with those presented in Theorem 1-(i). That is, under low labor friction, where

When labor market frictions are relatively low (

When the labor market frictions exceed the threshold

Overall, Theorem 2 reveals that in low friction markets (

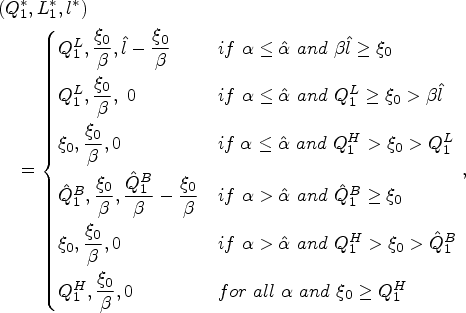

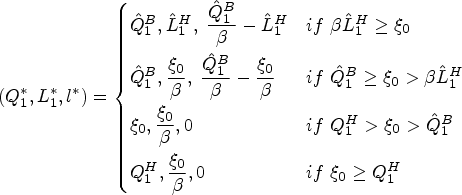

(Labor Market with High Labor Frictions and with Furlough)

Assuming labor market frictions such that

Suppose

Suppose

Suppose

Suppose

Suppose

where

Theorem 3 identifies five scenarios depending on the level of furlough risk

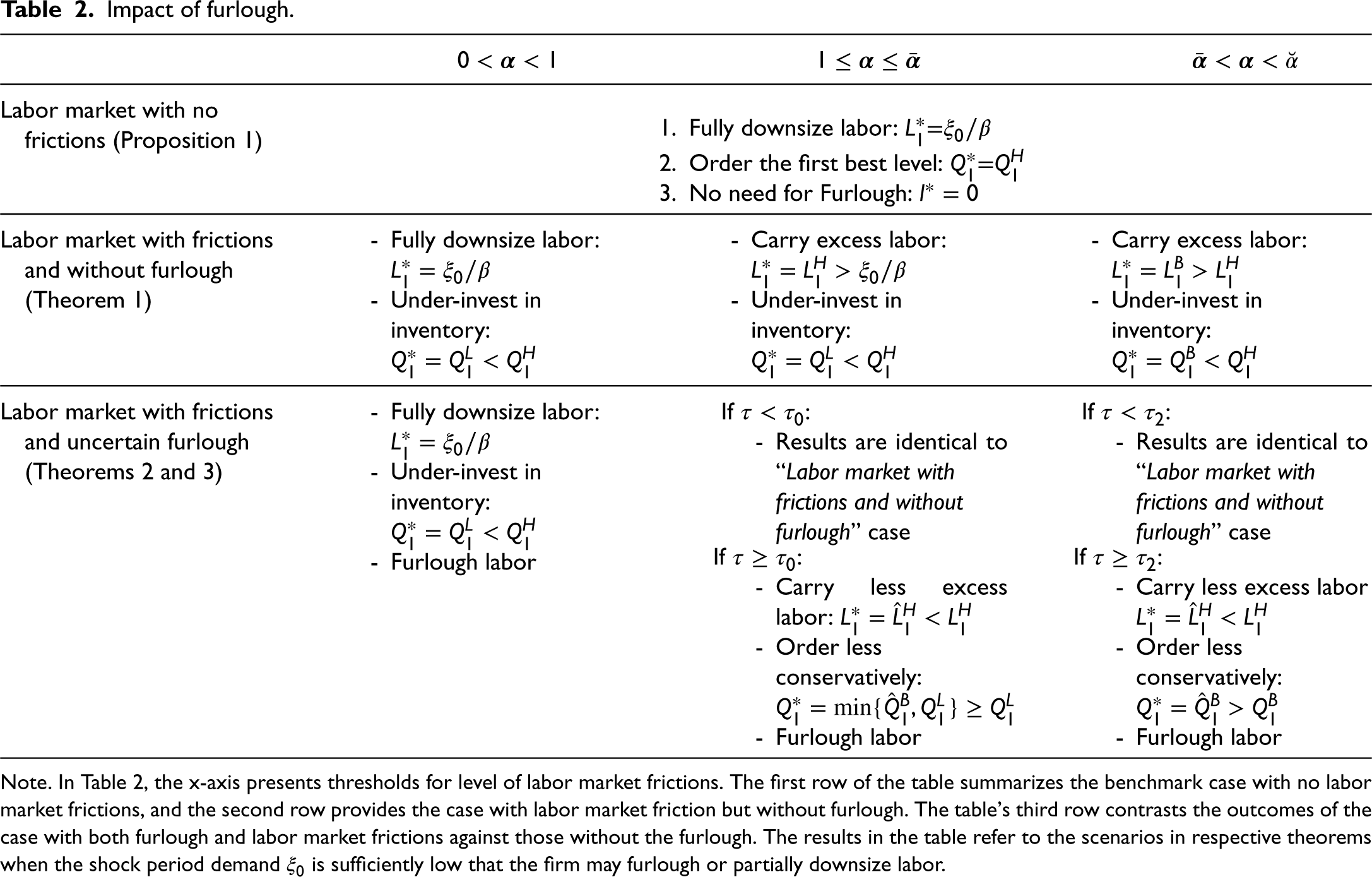

Impact of furlough.

Note. In Table 2, the x-axis presents thresholds for level of labor market frictions. The first row of the table summarizes the benchmark case with no labor market frictions, and the second row provides the case with labor market friction but without furlough. The table's third row contrasts the outcomes of the case with both furlough and labor market frictions against those without the furlough. The results in the table refer to the scenarios in respective theorems when the shock period demand

Case (i): With low labor market friction (1

Case (ii): For low friction levels (1

Case (iii): This case mirrors Case (ii) in strategy for low friction and high return probability of furloughed labor (low risk), differing in the specific quantities of labor adjustment.

Case (iv): When friction level is high (

Case (v): This case, with high friction and low furlough risk, also mimics Case (ii).

In Table 2, similar to Table 1, we provide a summary of our results illustrating the impact of market frictions and furlough option on labor and inventory decisions. The first row of the table (from Proposition 1) shows the results in the absence of labor market frictions, i.e., the firm fully downsizes labor, places the first best order quantity, and there is no need for furlough. The second row (from Theorem 1) summarizes the impact of introducing labor market frictions. It reveals that with low friction (

Finally, the last row of the table summarizes the impact of introducing the furlough option (from Theorems 2 and 3) in the presence of labor market frictions. In this case, if the friction level is low

Table 2 highlights key insights into the impact of furlough on operating decisions. When labor market frictions are low, furlough merely converts some laid-off workers to furloughed status without affecting inventory decisions, resulting in a limited effect on recovery in the second period. However, at higher levels of labor frictions, the furlough option also increases stocking levels, leading to faster recovery. Additionally, the furlough option is not effective when the probability of furloughed workers returning falls below a certain threshold, which depends on the level of labor market frictions.

In this section, we setup a numerical experiment to demonstrate the implications of the theorems in Section 4 under a wide range of conditions. This experiment is designed to not only confirm the theoretical findings but also to deepen our understanding of the interplay among critical model parameters, including profit margin, furlough risk, and labor friction. That is, through this experiment, we aim to provide a more comprehensive perspective on how these factors collectively influence the profit, labor, and inventory decisions.

Impact of Labor Frictions on Profit, Labor, and Inventory

First, we numerically illustrate the impact of frictions on optimal labor, inventory, and firm profit over the two periods. Table 3 summarizes our base-case parameters and experimental setup for our numerical analysis, which cover the entire relevant range of important model parameters.

Setup for numerical analysis.

Setup for numerical analysis.

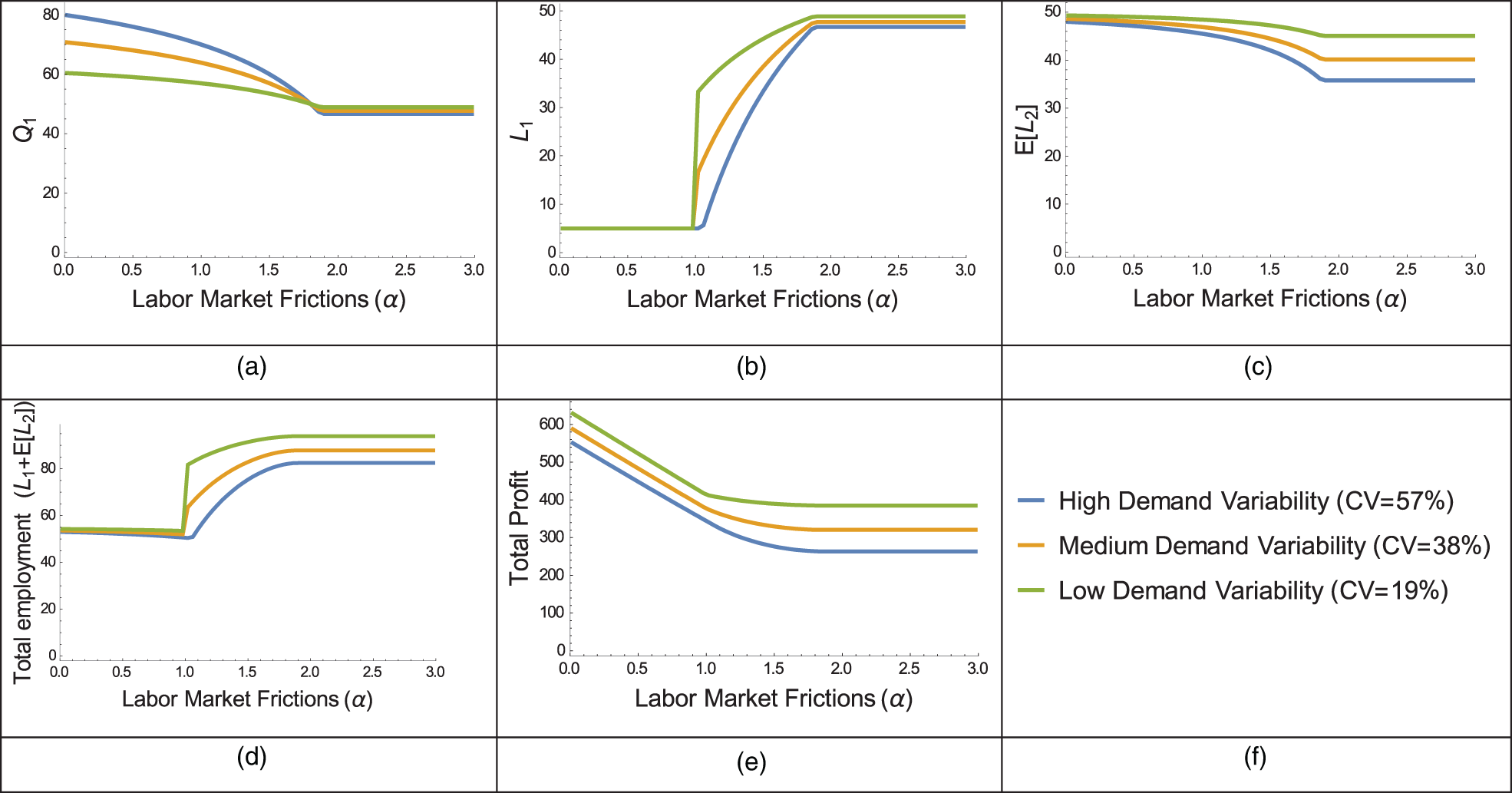

In Figure 2, we present the key performance measures—inventory, labor, and total profit—as a function of the levels of demand variability and labor market frictions. The x-axis in all figures is set to the full range of labor market frictions (

Impact of labor friction.

As we have noted in Section 4, we observe that orders for the second period (

The expected second period labor (

Figure 2(d) presents the total expected employment over the two periods (this figure can also be interpreted as the total wages or labor surplus). The total expected employment is nonmonotone in the level of labor market frictions. As explained in the previous section, labor market frictions have two distinct effects on employment: a main direct effect and a secondary lagged effect through inventory. Firstly, the presence of labor market frictions serves as a deterrence against laying off labor as it makes it costly to hire and fire labor. This effect is observed in the first period when the firm downscales labor (see Figure 2(b)), i.e., as the labor market frictions increase, firm tends to downscale less aggressively and keeps more labor during the first stage. Hence, the main effect of labor market frictions on total employment is positive and nondecreasing with friction level. The indirect secondary effect of labor market frictions on employment is generated through under-investment in inventories. Labor market frictions motivate downscaling of inventories (

Intuitively, total profit decreases with increasing labor market frictions (Figure 2(e)). Additionally, we find that the inventory decisions of firms with volatile demand are more sensitive to labor market frictions, and these firms are also more aggressive in downsizing labor in the first period (Figure 2(a) and (b)).

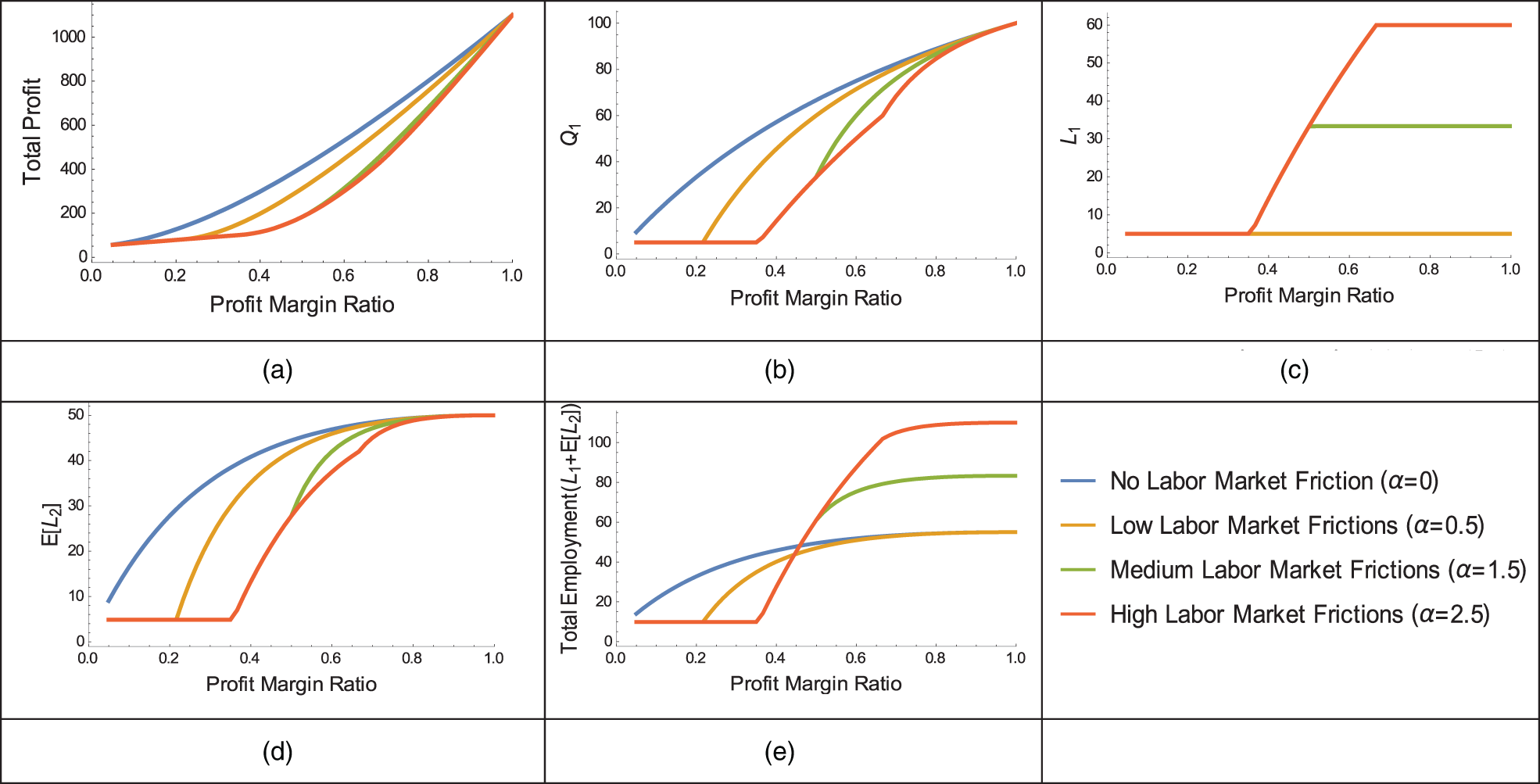

The impact of labor market frictions on the retailer depends on the firm's ability to generate profits and the composition of this profit margin, i.e., the relative dependence of the profits on unit labor and inventory costs (

Interaction of labor frictions and profit margin.

Intuitively, profits decrease when we increase labor market frictions (Figure 3(a)). However, friction's impact on profit depends on the profit margin. When the profit margin is low, labor market frictions have little impact on profits. In this case, the firm carries a low level of inventory, and it also needs a low amount of labor to sell it. Hence, the firm's expected trade volume in the labor market (firing and hiring labor) would be low limiting firm's exposure to labor market frictions.

As the profit margin increases, firm's order quantity quickly goes up in the absence of labor market frictions (Figure 3(b)). In this case, introducing labor market frictions also quickly erodes the critical fractile for inventory, making firm's total profit highly sensitive to labor market frictions, particularly when the profit margin ratio is neither too high nor too low (Figure 3(a)). If the profit margin ratio becomes very high, then the impact of labor market frictions is absorbed by the operating margin, i.e., operating margin is so high that the order quantity does not change too much when labor market frictions are introduced (Figure 3(b)).

The interaction of profit margin ratio and labor market frictions on total employment is less intuitive (Figure 3(c)–(e)). When the profit margin ratio is low, introducing labor market frictions reduces total employment. When low profit margin firms face labor market frictions, they are more likely to fully downscale labor as in the no friction case (Figure 3(c)). Hence, changes in the level of labor market frictions are less likely to impact employment in the first period for these firms. However, since the inventories are also scaled down in response to labor market frictions, the second period labor goes down with frictions (Figure 3(d)). Overall, the introduction of labor market frictions results in a reduction in total employment for low profit margin firms (Figure 3(e)). At high profit firms, however, labor market frictions motivate managers to keep excess labor in the first period via conservatively scaling down labor. These firms also act more conservatively when scaling down inventories leading to higher total employment in the presence of labor market frictions (Figure 3(e)).

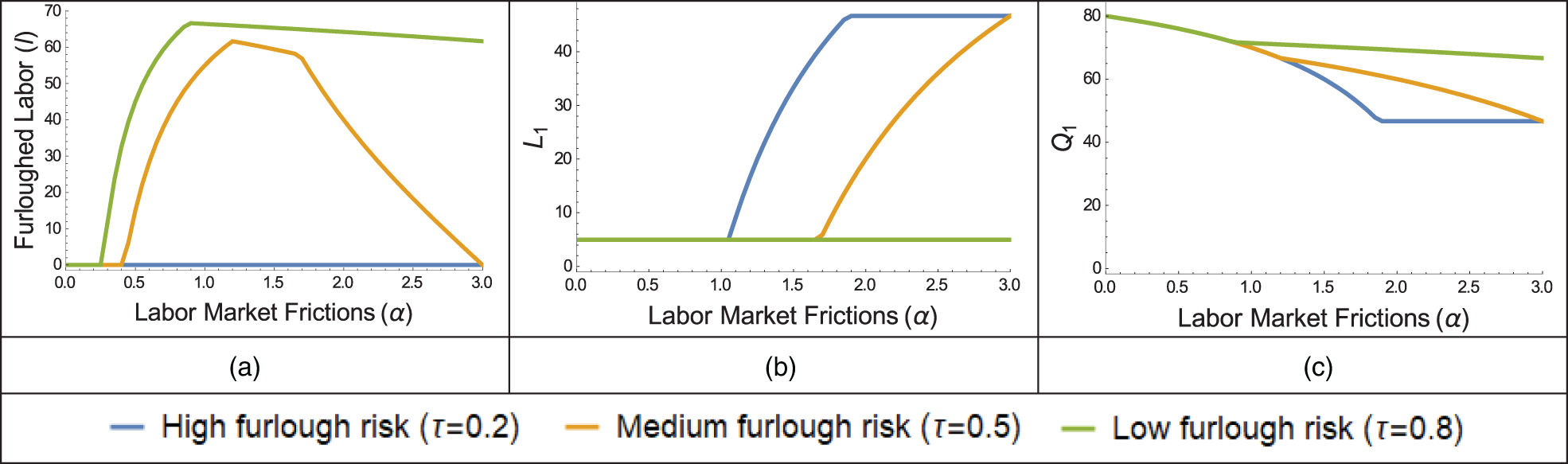

Furloughing labor provides the firm with flexibility when trading in the labor market, as furloughed employees can be called back to work – after observing the demand- without being subject to labor market frictions. That is, the firm avoids incurring search and training expenses, along with other opportunity costs, when recalling furloughed employees. However, furloughing carries a risk: employees might find alternative employment and not be available when needed later. Our model accounts for this risk through a parameter,

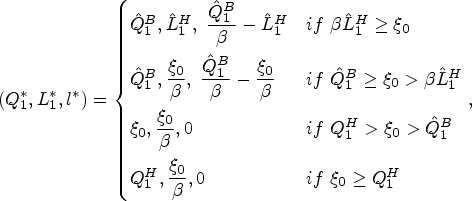

In Figure 4, we illustrate optimal decisions in the presence of furlough to highlight the impact of the furlough option on operations as a function of furlough risk and level of labor market friction. Figure 4(a)–(c) should be interpreted together. First consider the case when

Optimal decisions with furlough.

When the furlough risk is high

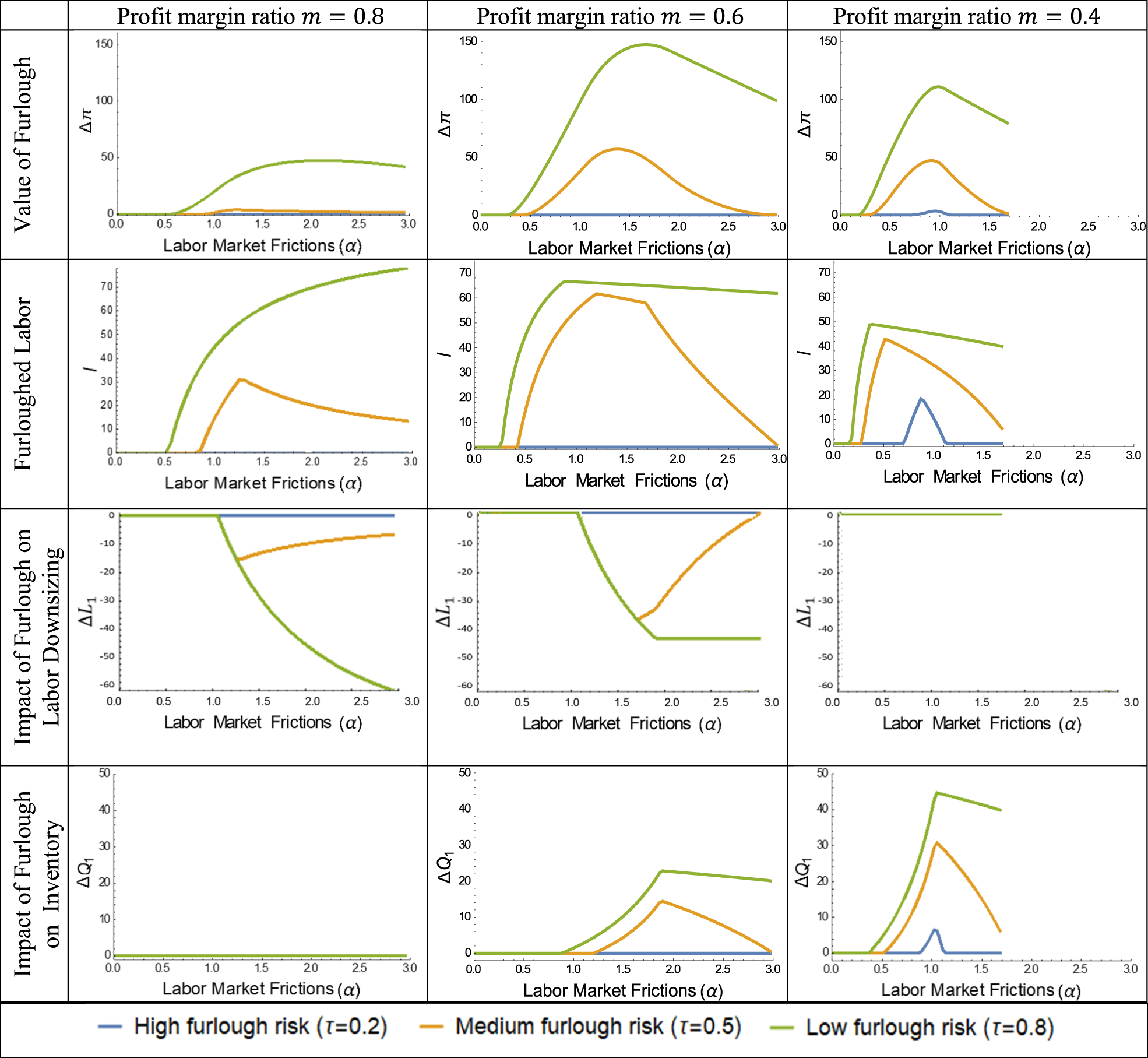

In Figure 5, we illustrate the optimal furlough amount and its impact on profits, inventory and labor decisions as we vary profit margin,

Impact of furlough.

The second row of the figure shows the optimal amount of furloughed labor. The third row shows the impact of furlough on labor downsizing decision

Impact of labor friction: One would expect that as the labor market friction increases (plotted in the x-axis in Figure 5), trading in the labor market becomes more costly increasing the value of furlough flexibility. An analysis of the first and second rows of Figure 5 reveals that this intuition, however, is not fully correct. Value of furlough, across all profit margin levels and furlough risk scenarios, initially increases and then decreases in response to labor friction. When labor friction is low, it is more cost-effective to avoid furloughs, as firing and rehiring workers is cheaper. Conversely, at high friction levels, firms tend to eschew furloughs due to the uncertainty of furloughed labor returning, opting instead to retain excess labor. Therefore, in these scenarios, furloughs have a minimal impact on operations and profits.

However, at intermediate friction levels, furloughs are employed more strategically. Here, the furlough serves as an effective tool for balancing the costs associated with market friction and labor downsizing. This leads to significant improvements in both operating decisions and overall profits.

Impact of profit margin:

For high profit margin firms (for For intermediate profit margin firms (for For low profit margin firms (for

Impact of furlough risk: Impact of furlough risk is intuitive. Higher furlough risk results in lower furloughed labor, lower impact on operations and lower value for furlough option.

We examine the interaction of inventory, labor, and furlough decisions in the presence of labor market frictions under a demand shock driven by a pandemic or an economic turmoil. A policy debate in such extreme settings is often linked with the impact of labor market frictions and furlough option on employment and firm profits (Bruhn, 2020; Eichhorst et al., 2010). We find that the net impact of labor market frictions on retail profits and employment is sizable, and it must be assessed together with the inventory and furlough decisions.

Impact of Labor Frictions on Operations

Our analysis highlights a key operational mechanism for the functioning of labor market frictions in the context of retail operations management during an economic shock (Theorem 1). It is well established in OM-finance literature that firms under-produce/order in the presence of costly external funds (a form of capital market frictions). Our findings extend this key result to the labor market friction context. That is, firms under-invest in inventories in the presence of labor market fictions since labor and inventories present complementarity in retail markets. However, the impact of labor frictions on employment is not obvious.

We show that the labor market frictions have two separate effects on labor level: (i) a positive main effect on the labor amount during the period of economic shock and (ii) a negative secondary effect on the labor level during the economic recovery period induced through reduced inventory levels. The net employment effect of labor market frictions is the sum of these two effects which can be either positive or negative depending on the severity of the economic shock, level of labor market frictions and profit margin of the firm. In particular, labor market frictions are likely to increase total employment if labor market frictions and the retail margin are high.

The Role of Profit Margin

We find that the retailer's profit margin is a key factor conditioning the impact of frictions on operating decisions and profits. In particular, when the profit margin is neither too low nor too high, labor market frictions result in a sharper reduction in critical fractile (Figure 3(b)). That is, for medium levels of profit margin, firm's total profit becomes highly sensitive to labor market frictions.

Labor market frictions are also more likely to result in a reduction in total employment for low profit margin firms (Figure 3(e)) as these firms cannot afford to keep excess labor in the first period. For high profit margin firms, however, labor market frictions motivate them to keep excess labor in the first period via conservatively scaling down labor. So, these firms also act more conservatively when scaling down inventories leading to higher total employment in the presence of labor market frictions.

Impact of Furlough Option

Our analysis shows how the strategic option to furlough, contingent upon the likelihood of furloughed employees’ return (

As labor market frictions intensify (

Furthermore, our results illustrate a significant interaction between furlough decisions, labor market frictions, and retail margins, indicating that the strategic value of furloughing is magnified under certain economic conditions. Specifically, we observe that in environments with low furlough risk and intermediate levels of labor market frictions and profit margins, firms adjust both their labor and inventory strategies to optimize profitability and operational resilience. This adjustment manifests in a more nuanced approach to furloughing—weighing the cost of potential workforce unavailability against the benefits of having a flexible, scalable labor force ready to respond to market recoveries. Through our comprehensive analysis, we shed light on the pivotal role of furloughing in retail operations management, offering insights into how firms can manage the complexities of labor dynamics to sustain profitability in the face of fluctuating market conditions.

Limitations and Future Research

In this study, we focus on understanding the impact of labor market frictions on labor, inventory, and furlough decisions of a retailer during an economic shock. Our researches can be extended in multiple ways. Firstly, our analysis does not explicitly incorporate risk aversion in the decision-making process of the retailer. Future studies could enhance our model by incorporating risk aversion, providing a more nuanced understanding of how retailer's risk aversion condition the impact of labor frictions on the operations of the firm.

Secondly, the development of a general equilibrium model represents a promising avenue for extending our findings. Such a model would allow for a comprehensive analysis of the interactions between multiple markets and the broader economic environment, capturing the dynamic effects of supply and demand across sectors. Building on this research by incorporating general equilibrium considerations could significantly deepen our understanding of the systemic impacts of retail inventory, labor, and furlough decisions on economic stability and growth. In a related manner, explicitly modelling heterogeneity among labor productivity may also lead to interesting managerial insights. Also, treating inventory and labor as substitutes would significantly alter the outcomes and insights of our model.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478241273876 - Supplemental material for Furloughing Employees with Uncertain Return? Management of Labor Frictions and Inventory Under Demand Shock

Supplemental material, sj-pdf-1-pao-10.1177_10591478241273876 for Furloughing Employees with Uncertain Return? Management of Labor Frictions and Inventory Under Demand Shock by Fehmi Tanrisever and Nitindra Joglekar in Production and Operations Management

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

How to cite this article

Tanrisever F and Joglekar N (2024) Furloughing Employees with Uncertain Return? Management of Labor Frictions and Inventory Under Demand Shock. Production and Operations Management 33(11): 2139–2157.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.