Abstract

Sustainable development demands addressing two core challenges: mobilizing financial resources and aligning stakeholder incentives. This article surveys the operations-finance interface literature through the lens of “Mobilizing Resources” and “Aligning Incentives” framework. We highlight how the literature advances our knowledge of mitigating SME financing constraints and crafting operationally-informed financial contracts to internalize externalities. We identify a critical gap: while theoretical models for incentive alignment are well-established, empirical evidence remains limited due to the difficulty of analyzing unstructured data. To bridge this gap, we present large language models (LLMs) as a rigorous methodological toolkit for empirical operations management research. We outline a four-step framework—Problem Definition, Model Selection, Prompt Engineering, and Validation—and illustrate its application via a case study that extracts novel data on supplier finance programs from corporate 10-K filings. We conclude by proposing a unified research agenda to advance future research at the intersection of operations, finance, and sustainability.

Keywords

Introduction

Businesses are increasingly integrating sustainable development in core strategies, transcending traditional shareholder value maximization to pursue a broader set of goals (Business Roundtable, 2019). To operationalize these expanded objectives, Lee and Tang (2018) propose the “triple bottom line” framework, comprising people (social sustainability), planet (environmental sustainability), and profit (economic sustainability), as an essential guide for achieving the 17 United Nations Sustainable Development Goals (SDGs). As firms strive to integrate these dimensions, they face significant operational and financial hurdles requiring novel and interdisciplinary solutions.

From an operations-finance interface perspective, sustainable development faces two primary challenges: mobilizing sufficient resources and aligning divergent incentives. This “Resource and Incentive” framework provides a powerful analytical lens for diagnosing problems and structuring solutions at the nexus of operations, finance, and sustainability.

The first challenge, mobilizing resources, arises from the substantial capital required for sustainability transition, creating an estimated $4 trillion annual SDG financing gap in developing economies (UNCTAD, 2023). This capital scarcity disproportionately affects small- and medium-sized enterprises (SMEs), which constitute the vast majority of participants within global supply chains. According to Asian Development Bank (2023), SMEs represent 45% of all trade finance rejections, driving the global trade finance gap to a record $2.5 trillion. Such a financing constraint stems primarily from market frictions, especially information asymmetry. Traditional lenders, like commercial banks, often lack visibility into granular operational data (e.g., production capabilities, order fulfillment history, quality metrics, etc.), hindering accurate credit assessments for opaque SMEs and leading to credit rationing or prohibitive interest rates. Overcoming this friction requires utilizing operations-based information and supply chain relationships to mitigate asymmetry and direct capital to sustainable initiatives.

The second challenge, aligning incentives, involves managing externalities inherent in sustainability goals—such as reducing carbon emissions, ensuring product safety, or improving labor conditions—where costs or benefits are not captured in market prices. Consequently, these objectives often exhibit the characteristics of public goods, often lacking private incentives for individual contributions. For instance, a supplier might opt for cheaper, environmentally harmful materials to cut costs, even if it damages the reputation of the entire supply chain and harms the environment. Similarly, a hospital might underinvest in post-discharge care if it is not financially penalized for patient readmissions. Resolving such market failures requires operationally grounded financial contracts and mechanisms. By structuring payments and financing terms to reward desired operational behaviors, firms can internalize these externalities, effectively aligning the goals of disparate stakeholders, including suppliers, buyers, employees, and investors, with sustainability targets.

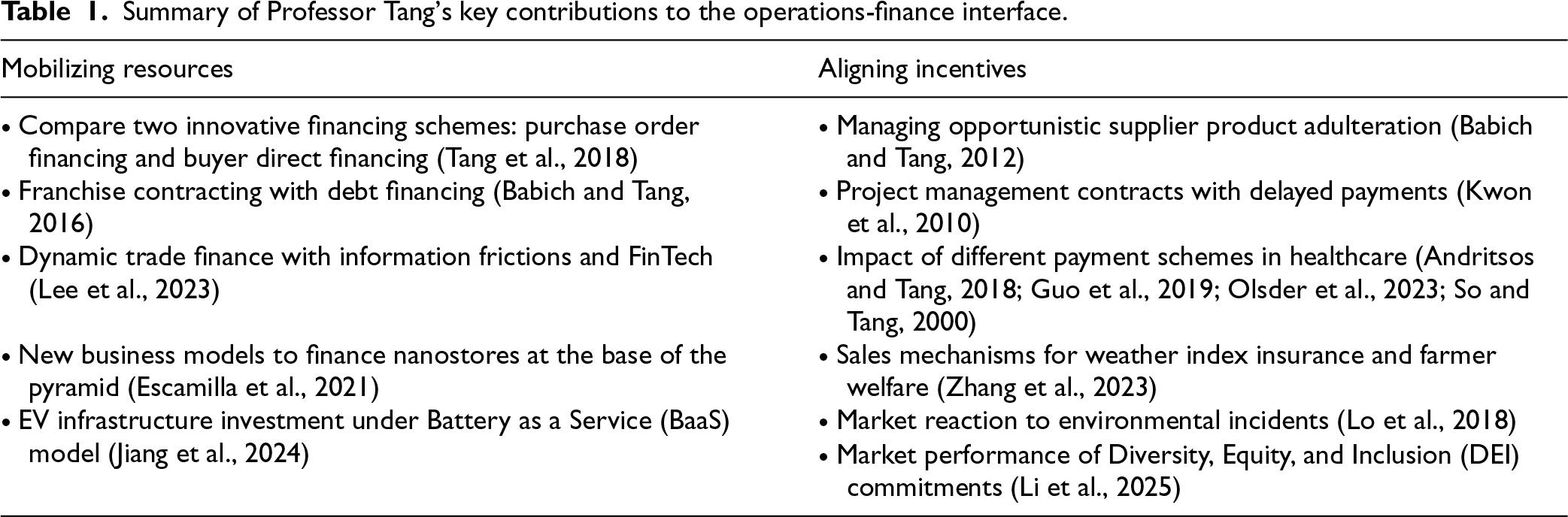

As a thought leader, Professor Christopher S. Tang has championed a broader vision where operational decisions and financial strategies converge to foster sustainable development. During his tenure as M&SOM’s Editor-in-Chief, he advanced the field through two landmark special issues: the 2018 issue on the Interface of Finance, Operations, and Risk Management (iFORM) and the 2023 issue on the Interface of Operations, Finance, and Technology (OpsFinTech). His work establishes theoretical and empirical foundations for tackling resource mobilization and incentive alignment. Table 1 summarizes these contributions, organized by the “Resource and Incentive” framework guiding this review.

Summary of Professor Tang’s key contributions to the operations-finance interface.

Summary of Professor Tang’s key contributions to the operations-finance interface.

The article is organized as follows. Section 2 and 3 review the literature on mobilizing resources and aligning incentives, emphasizing Professor Christopher S. Tang’s key contributions. Section 4 introduces large language models (LLMs) as a novel methodological tool for analyzing unstructured data to address gaps in empirical research. Section 5 concludes with a comprehensive framework for future research.

Meeting sustainable development’s financing demands requires moving beyond traditional lending models. The operations-finance interface literature offers diverse solutions using operational relationships and data to mitigate market frictions that constrain capital flow. This section surveys this body of work, beginning with the foundational role of financial frictions and trade credit (§2.1), and then progressing to more complex, structured forms of supply chain finance (SCF; §2.2) and their application in specific development contexts (§2.3).

Theoretical foundations: Financial frictions and trade credit

At its core, the operations-finance interface analyzes how financial frictions constrain a firm’s operational decisions in inventory, production, and capacity. Such frictions include agency costs (Babich et al., 2021; Chod and Zhou, 2014; de Véricourt and Gromb, 2019; Iancu et al., 2017; Ning and Babich, 2018), bankruptcy costs (Boyabatlı and Toktay, 2011; Li et al., 2013; Xu and Birge, 2004), information asymmetry (Alan and Gaur, 2018; Lai and Xiao, 2018; Schmidt et al., 2015), imperfect credit market competition (Buzacott and Zhang, 2004; Dada and Hu, 2008), and bank capital regulation (Zhang et al., 2022). By jointly analyzing a firm’s financing and operating decisions, these single-firm operations-finance models demonstrate the value of integrated decision-making and provide a foundation for future research.

In supply chains, the most commonly used form of financing is trade credit, where a supplier allows a buyer to delay payment for goods or services. This payment deferral serves dual roles: short-term financing for buyers and an operational tool influencing ordering behavior and relationship dynamics. Theoretically, trade credit enables sellers to gain competitive advantages by enhancing horizontal benefits in competition (Peura et al., 2017), facilitating risk sharing through inventory financing portfolios (Yang and Birge, 2018), and curbing retailer opportunism through transaction ties (Cai et al., 2014; Chod, 2017). Comparative analyses further clarify when trade credit outperforms or complements bank loans (Kouvelis and Zhao, 2012, 2018). Empirical studies corroborate these insights, demonstrating that trade credit smooths suppliers’ cash flows (Osadchiy et al., 2025), improves firm performance under competition (Lee et al., 2018), and provides buyer flexibility through late payments without significantly harming suppliers (Wu et al., 2020). However, these benefits entail strategic and financial trade-offs, including supplier free-riding (Chod et al., 2019) and the need of mitigating default risks through trade credit insurance (Yang et al., 2021).

Innovations in supply chain finance

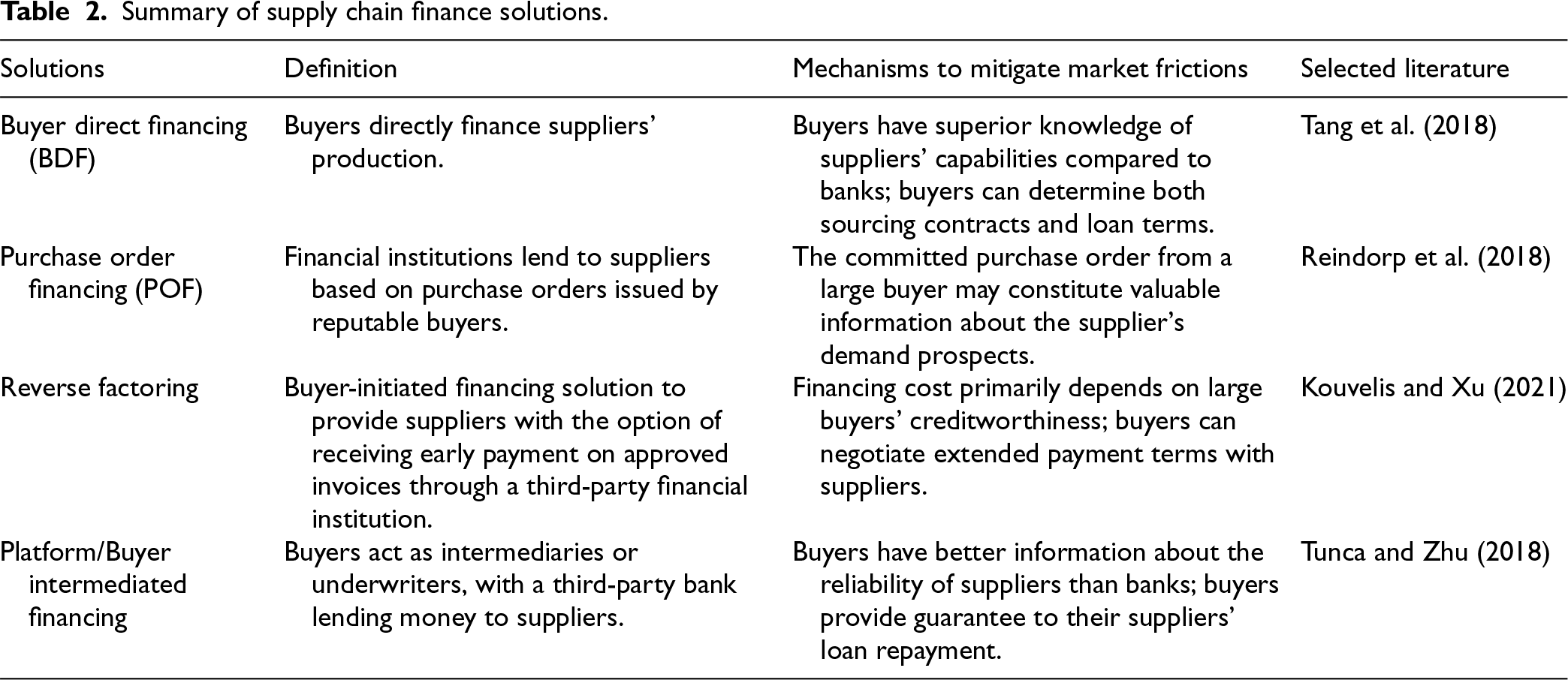

Building on the above literature, structured SCF solutions have emerged, often involving third-party institutions to infuse liquidity into the supply chain by exploiting the credit strength and operational information of a large, focal firm. Table 2 summarizes key SCF solutions.

Summary of supply chain finance solutions.

Summary of supply chain finance solutions.

This rationale for BDF persists even when the buyer’s opportunity cost of capital is high. Deng et al. (2018) demonstrate buyers may accept financing losses in order to gain operational benefits such as improved inventory support and lower purchasing prices. Thus, BDF remains attractive even when the buyer’s capital cost exceeds the bank’s risk-free rate. However, BDF is not without its challenges. A practical limitation is the potential for fund misuse by suppliers, a risk amplified in developing economies where monitoring is often infeasible or prohibitively costly. In such cases, Reindorp et al. (2018) focus on mitigating information problems under POF using purchase order commitments from large reputable buyers.

Although often portrayed as mutually beneficial (Seifert and Seifert, 2011), reverse factoring involves a critical trade-off: buyers may extend their payment terms in exchange for facilitating this financing. This can increase the supplier’s working capital requirements, potentially offsetting the benefits of the reduced financing cost. Consequently, the net value for SME suppliers is not guaranteed and depends heavily on program specifics and market conditions (Lekkakos and Serrano, 2016; Tanrisever et al., 2015; Van der Vliet et al., 2015). Specifically, Kouvelis and Xu (2021) model when factoring or reverse factoring is optimal as a function of credit ratings and recourse provisions.

Empirically, suppliers’ adoption speeds of reverse factoring vary significantly. Wuttke et al. (2019) find faster adoption among suppliers with limited access to traditional financing. However, their subsequent research confirms that the availability of reverse factoring can unintentionally motivate buyers to further delay payments (Wuttke, 2025), highlighting the need for careful program design to alleviate supplier liquidity constraints without encouraging buyer’s opportunistic behavior.

Similarly, platforms such as JD.com and Amazon use their extensive transactional data to finance their third-party sellers (Dong et al., 2019; Gupta and Chen, 2020; Huang et al., 2025; Yi et al., 2021). Beyond direct lending, platforms or buyers can also serve as intermediaries by guaranteeing supplier loan repayments, facilitating banks to extend credit with reduced risk (Li et al., 2023; Sriraman et al., 2024; Tunca and Zhu, 2018; Zhao and Huchzermeier, 2019). Empirical evidence from JD.com indicates that this supplier finance program lowers suppliers’ borrowing costs, leading to reduced wholesale prices and improved operational performance for both parties (Tunca and Zhu, 2018). Relatedly, Zhang et al. (2024) demonstrate how large sellers can orchestrate financing programs for downstream dealers to mitigate the constraints imposed by bank capital regulations.

The principles of operations-finance interface prove particularly salient for sustainable business models in emerging economies, where firms often operate beyond formal financial systems, as well as for capital-intensive green transitions.

Aligning incentives for sustainable outcomes

Beyond mobilizing capital, the operations-finance interface designs mechanisms to align the self-interest of individual actors with broader sustainability goals. This involves structuring operationally-informed financial contracts and employing market forces to incentivize desirable operational behaviors and discourage harmful ones.

Designing operationally-informed financial contracts

Financial contracts can be powerful tools for mitigating moral hazard and ensuring that supply chain partners adhere to quality, safety, and timeliness standards. The key is to appropriately link financial payoffs to verifiable operational outcomes.

Incentive alignment in critical sectors: Healthcare and agriculture

The principles of incentive alignment are especially critical in sectors with strong externalities, where the actions of providers directly impact public welfare.

Shifting to the public sector, Lu et al. (2024) model an optimal government subsidy for index-based yield protection, noting that such policies can inadvertently increase farmers’ income variability due to the index’s imperfect correlation with actual yield. Empirical research underscores the potential and challenges of these innovations. Field studies reveal low demand for index insurance hampered by high price sensitivity, basis risk, liquidity constraints, limited financial literacy, and a lack of trust (Cole et al., 2013; Karlan et al., 2014). Bundling insurance with complementary products, such as agricultural inputs (Boucher et al., 2024; Bulte et al., 2020) or credit (Mishra et al., 2021), can help boost adoption. This aligns with broader findings in microcredit, which highlight the need for product bundling and incentive alignment to achieve financial inclusion (Banerjee et al., 2015; Crépon et al., 2015).

The role of capital markets as an external incentive mechanism

Beyond inter-firm contracts, capital markets can exert external force, rewarding or penalizing corporate behavior to align incentives on sustainability. Lo et al. (2018) find negative stock reactions to Chinese firms’ environmental incidents, mitigated by government ownership or social recognition but worsened by executive political ties. Conversely, Li et al. (2025) show positive stock returns from commitments to Diversity, Equity, and Inclusion (DEI) in U.S. manufacturing, suggesting that investors view such commitments as a positive signal about a firm’s culture, risk management, and long-term financial health. Broader research confirms that financial markets interact with operational factors in various ways, such as technology adoption (Klöckner et al., 2022), operational productivity (Agrawal and Osadchiy, 2024; Jacobs et al., 2016), global sourcing strategies (Hsu and Wu, 2024; Jain and Wu, 2023), and risk propagation (Agca et al., 2022; Osadchiy et al., 2016). Together, these studies show that financial markets are increasingly pricing sustainability events, operational risks and opportunities into firm valuations.

A notable gap, however, exists in the empirical literature regarding incentive alignment. While theoretical models proposing specific contractual mechanisms are well-developed, empirical validation of their real-world effectiveness remains limited due to the data nature: specific details regarding incentive structures, contractual terms, and sustainability targets are typically embedded within vast amounts of unstructured text of supply chain contracts, ESG reports, and financial disclosures. Extracting this granular information manually is costly and inefficient, hindering researchers from testing theoretical mechanisms across broad samples.

Artificial intelligence (AI) and LLMs offer a transformative solution by enabling the efficient extraction of information from unstructured data. LLMs can parse complex documents and quantify variables such as climate risks or supply chain complexities. Converting unstructured text into structured data allows researchers to empirically validate incentive alignment theories at a scale. In the following section, we introduce LLMs as a novel methodological tool and provide a practical guide for researchers.

Methodological toolbox: LLMs for unstructured text analysis

LLMs have brought numerous opportunities for textual analysis in Operations Management. Researchers are using the LLM tools to analyze texts in financial documents (Breitung and Müller, 2025; Niu et al., 2026; Osadchiy et al., 2025; Siano, 2025), ESG reports (Rouen et al., 2024), news articles (Yoganarasimhan and Iakovetskaia, 2024), and customer reviews (Gao et al., 2025). These texts contain valuable operations-related information, such as the link-level trade credit contracts, and the manager attributions of operations performance, as shown in Appendix Table A1.

Compared to traditional text mining methods, LLMs offer the following advantages (de Kok, 2025): (i)

In this section, we provide a four-step framework for LLM textual analysis, demonstrated by an empirical application—extracting information on supplier finance programs from 10-K reports.

A framework for using LLMs in textual analysis

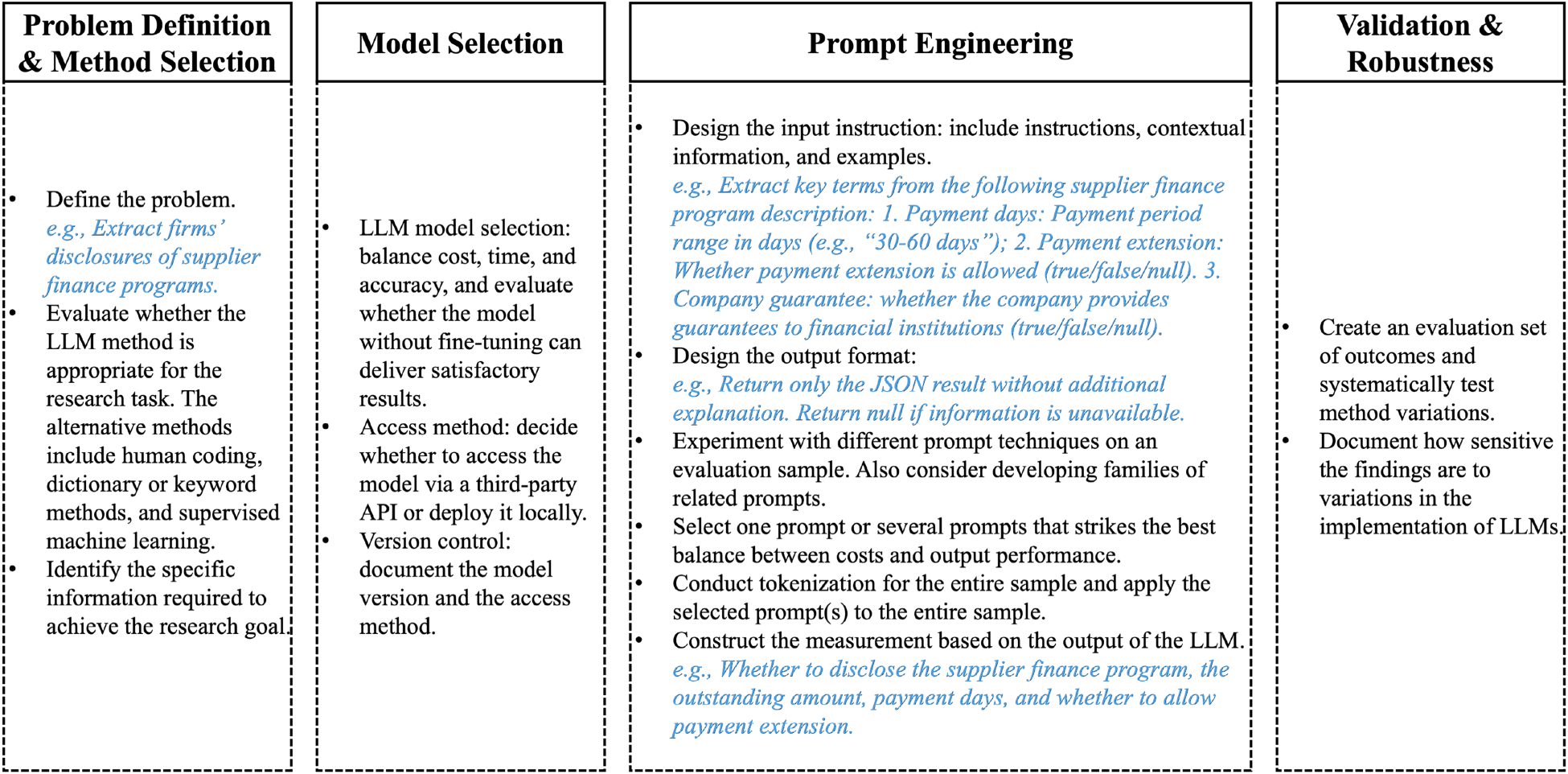

Our framework contains four steps. Figure 1 includes the steps and specific examples (highlighted in blue) from the case study in Section 4.2, which concretely demonstrate the content and execution of each step. Below, we detail each step for researcher guidance.

LLM approach roadmap.

Step 1: Problem Definition and Method Selection

The first step is to define the problem and evaluate whether LLMs are the appropriate tool. Alternatives like human coding provide a nuanced interpretation of context but lack scalability; dictionary or keyword methods are computationally efficient but struggle with semantic complexity and context; and supervised machine learning requires substantial training data (Carlson and Burbano, 2025). LLMs can solve complex semantic tasks at scale without extensive training, albeit with limitations such as textual reproducibility and output reliability. Therefore, method selection must align with specific research tasks.

Once researchers choose to use LLMs, it is essential to identify the specific information required to achieve the research goal, including background, domain knowledge, and relevant examples. We recommend manually analyzing the task on a small set of examples to understand the decision-making process and information requirements, allowing researchers to provide LLMs with sufficient information and obtain more reliable outputs.

Step 2: Model Selection

The second step is to decide which model to use. With the rapid development of LLMs, researchers must carefully evaluate the following considerations: Cost-performance balance: Each API call incurs costs based on the number of input and output tokens, and both the time and cost of using an LLM increase with the token count. Rather than defaulting to the highest-performing model, researchers should balance cost, speed, and accuracy. We recommend beginning by evaluating whether the model, without additional fine-tuning, can deliver satisfactory results. If it does not meet the construct validity needs, switch to model fine-tuning. Once the approach is determined, experiment with different model sizes using a smaller sample of the data, and choose the smallest model that provides satisfactory performance. Appendix B provides a detailed overview of LLMs. Access method: Decide whether to access the model via a third-party API or deploy it locally. While APIs offer convenience for urgent tasks or access to proprietary models, local deployment is preferable for sensitive data, open-source LLMs, or persistent workloads where investing in dedicated hardware can be more cost-effective. Version control: For reproducibility and transparency purposes, researchers need to document the model version and the access method.

Step 3: Prompt Engineering

The third step is to design and evaluate prompts that provide LLMs with natural-language input to guide their behavior and generate the desired output. The focus is on designing the input instructions and defining the output format. While fine-tuning offers a valuable extension for complex needs (Carlson and Burbano, 2025), prompt engineering remains the most accessible method for basic textual analysis. The prompts typically contain input and output parts.

Input design and iteration: Researchers can employ various prompting strategies, as shown in Carlson and Burbano (2025), such as zero-shot, few-shot, role-based, chain of thought (CoT), and tree of thought (ToT). Given that different models may vary in response quality to the same prompting strategies, it is crucial to conduct experiments on evaluation samples. Instead of relying on a single optimal prompt, we recommend developing and documenting families of related prompts to ensure robustness. Structured output: Researchers need to ensure readable and parsable output. Instead of unstructured outputs (e.g., “19.7% of accounts receivable was due from Walmart at November 2, 2012…”), researchers should instruct the LLM to return structured ones, such as a JSON object for processing simplicity (e.g.,

Finally, researchers need to construct the measurement based on the LLM’s output. Although the prompt ensures the structured output format, researchers need to transform raw extractions into quantitative variables for empirical analysis, including post-processing (e.g., standardizing units or converting percentages to decimals) and further calculation (e.g., creating a binary dummy variable indicating the disclosure of the program, or calculating a ratio based on extracted numerical values).

Step 4: Validation and Robustness

The final step is to validate the LLM outputs and robustness. Researchers should create an evaluation set of outcomes generated by human experts and systematically test method variations. When dealing with multiple outcomes, evaluate and report each outcome independently. Additionally, it is important to document how sensitive the findings are to reasonable variations in the implementation of LLMs. For instance, when using a family of prompts, researchers can test their impact on downstream analysis and produce bounded estimates that account for the methodological uncertainty (Carlson and Burbano, 2025).

We apply the above framework to a real-world setting, using the LLM to extract firms’ disclosures of supplier finance programs. In 2022, the Financial Accounting Standards Board (FASB) issued an accounting standards update that applies to all entities that use supplier finance programs in connection with the purchase of goods and services. This update requires that a buyer in a supplier finance program disclose the following information in each annual reporting period: (i) The key terms of the program, including payment days, payment term extensions, and guarantees to financial institutions. (ii) The outstanding confirmed amount. (iii) A description of where those obligations are presented in the balance sheet. (iv) Rollforward of those obligations during the annual period. Table A2 in Appendix C shows an example of Ralph Lauren’s information disclosure.

We scrape 10-K filings from January 2022 to June 2025 for 5,455 firms, extract relevant paragraphs via keywords, then employ LLMs to identify the reported supplier finance program details, including key terms and outstanding amounts. LLMs are a good fit for this extraction task, as they offer the semantic nuance needed to interpret complex disclosures at scale without the need for extensive labels required by traditional NLP models.

Balancing cost and efficiency, we use the Llama-3.1-70B-Instruct model for the task. We also use the GPT-OSS-120B model to examine whether the extracted results are consistent. Appendix D offers implementation details on the keyword list, model selection, full prompts, and validation.

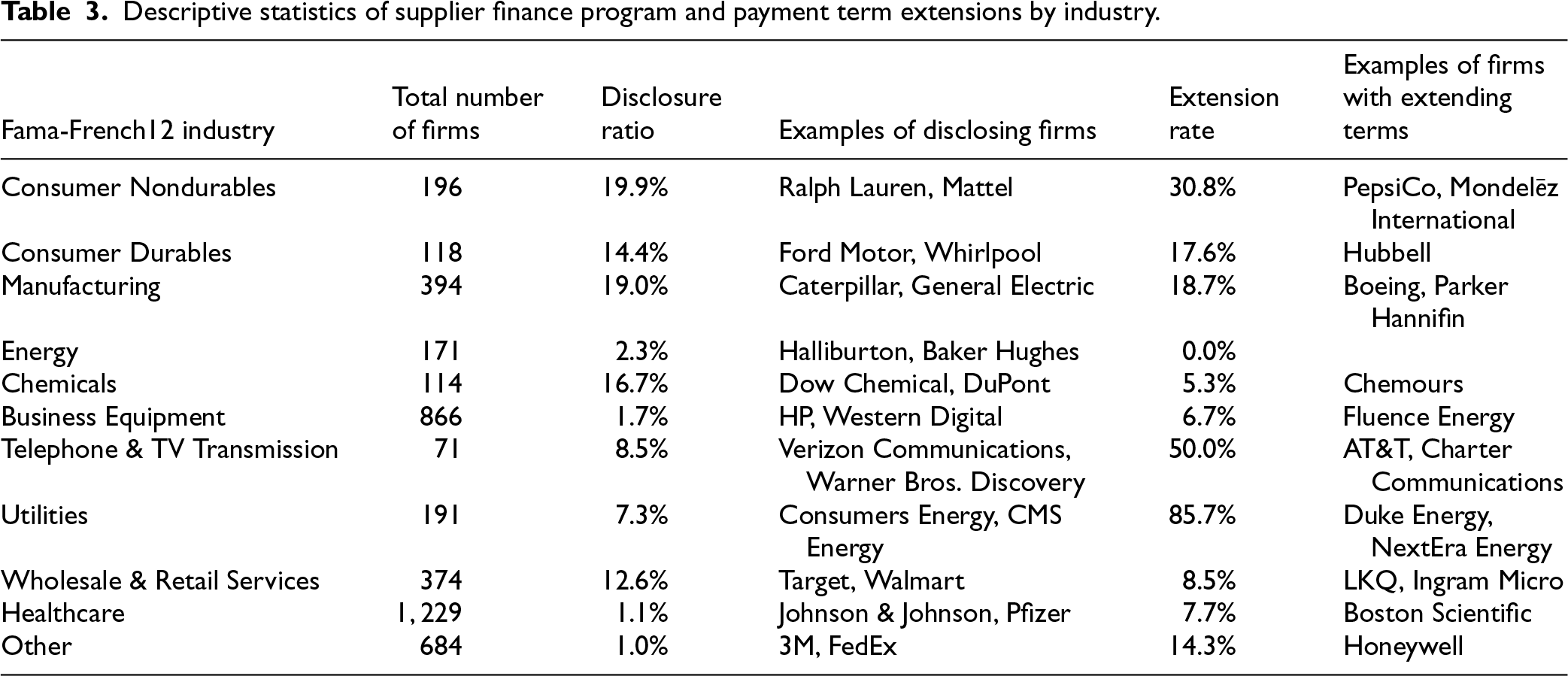

We identify 257 buyer firms that disclose supplier finance program obligations. Table 3 shows total firm counts, disclosure ratios, and example firms by Fama-French 12 industries. The consumer nondurable industry has the highest ratio of using supplier finance programs, followed by the manufacturing, chemical, consumer durable, and wholesale and retail industries.

Descriptive statistics of supplier finance program and payment term extensions by industry.

Descriptive statistics of supplier finance program and payment term extensions by industry.

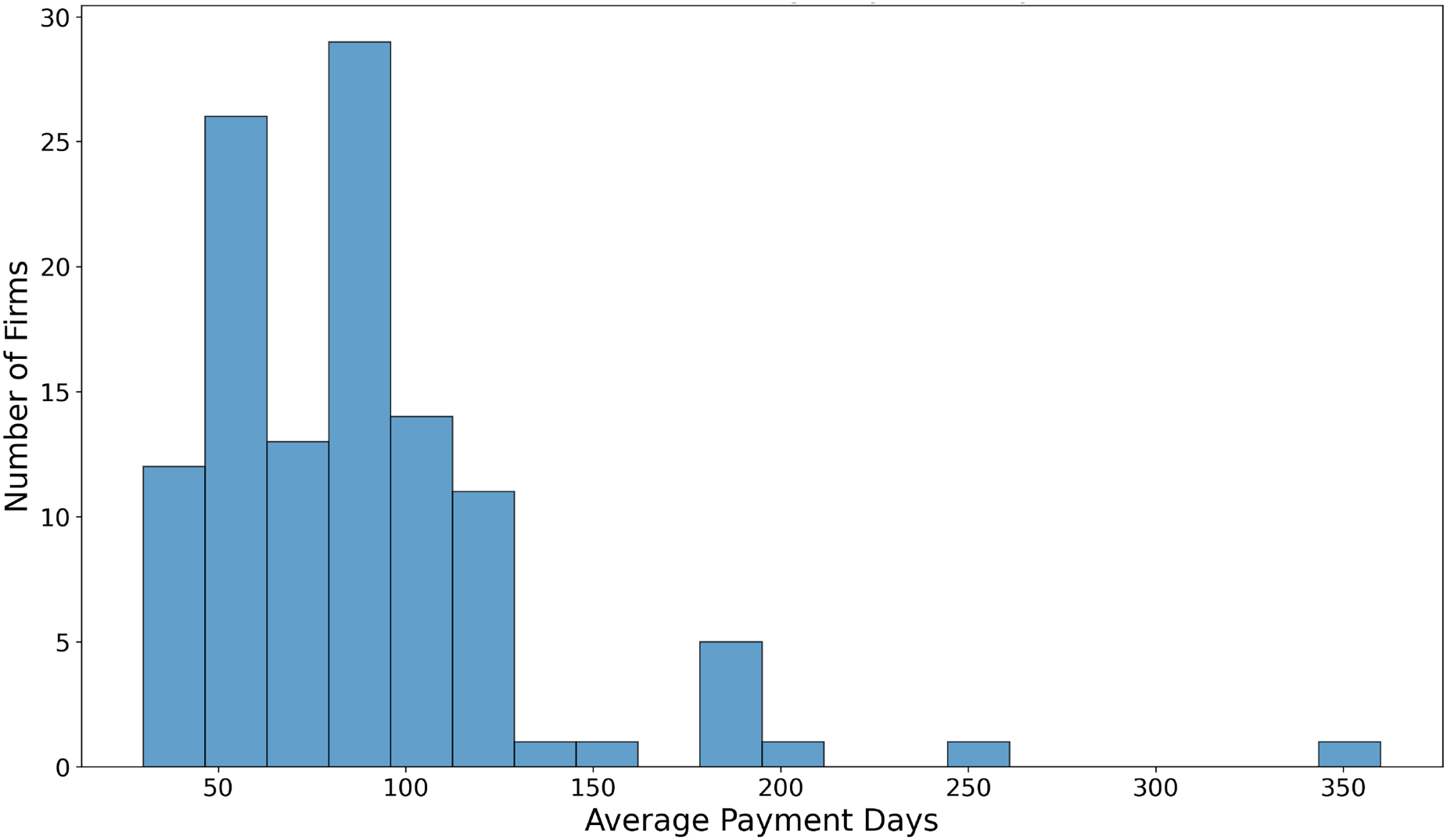

We also use LLMs to extract the key terms, including payment days, payment term extensions, and guarantees to financial institutions. There are 115 firms that provide this information, and Figure 2 presents the distribution of average payment days. 1 Most firms have average payment days of fewer than 150 days, but some firms have extremely long payment days. For example, the leading printed circuit board manufacturer, TTM Technologies, has payment days ranging from 160 days to 360 days in 2024. Monro, an automotive services company, has 360 payment days in 2024. There are 52 firms that report extending payment terms with suppliers through the supplier finance program during the sample period, including Boeing, Mondelēz International, and PepsiCo. For example, Boeing’s 10-K report in 2024 states that: “The majority of amounts payable under these programs are due within 30 to 90 days but may extend up to 12 months.”

Distribution of average payment days.

The last two columns of Table 3 show the proportion of firms with payment term extensions and example firms by industries. The utility industry has the highest proportion of payment term extensions, followed by the telephone and television transmission industries and the consumer nondurable goods industry. Such evidence demonstrates the practice of extending payment terms under supplier finance programs, potentially raising supplier working capital requirements. Building on these initial analyses, future research could use the granular data extracted by LLMs to investigate the net supplier impact of these programs. Specifically, researchers may test whether the liquidity benefits provided by SCF are sufficient to offset the costs imposed by extended payment terms, thereby validating theoretical trade-offs regarding the net value of reverse factoring. Furthermore, the significant variation in contract terms across industries warrants further investigation into how operational factors, such as inventory turnover or supply chain power dynamics, shape the strategic design of financial contracts.

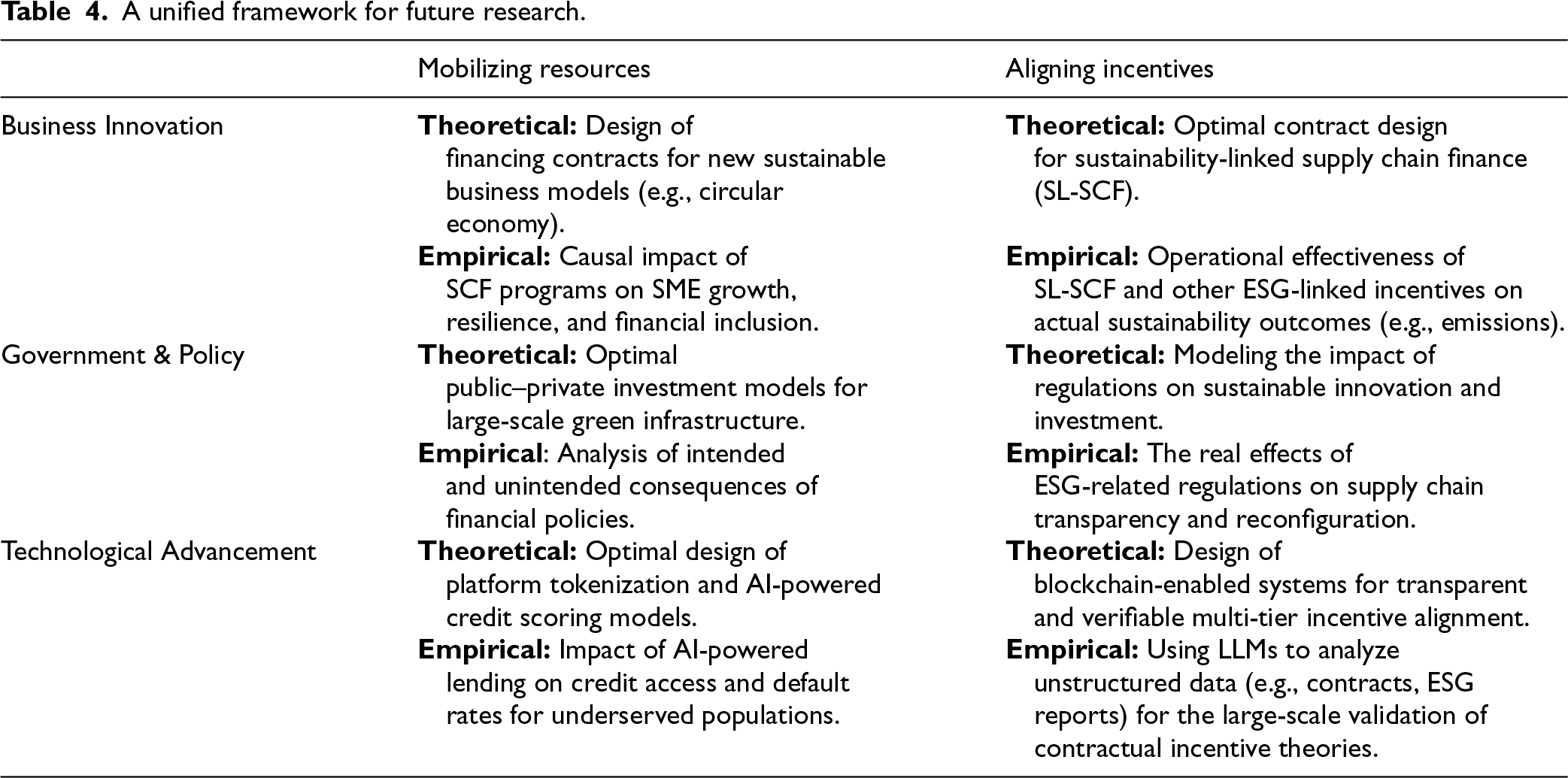

Finally, we propose a framework organizing research opportunities at the intersection of operations, finance, and sustainability. Structured by two Core Challenges (Mobilizing Resources and Aligning Incentives), two primary Methodologies (Theoretical Modeling and Empirical Investigation), and three key Levers of Change (Business Innovation, Government & Policy, and Technological Advancement), this

A unified framework for future research.

For incentive alignment, blockchain enables sustainability-linked incentives across deep-tier supply chains, which is a frontier in current theoretical research (Dong et al., 2023a, 2023b; Hou et al., 2025; Huang et al., 2022; Shibuya and Babich, 2026). Meanwhile, LLMs offer a methodological breakthrough in empirical research by extracting structured, operational data from unstructured texts (e.g., ESG reports, contracts, news).

Specifically, on one hand, LLMs can be used to test sustainability-related contractual incentive designs empirically by parsing thousands of sustainability-linked loans, SCF agreements, and ESG reports to extract granular contractual terms and identify which incentive designs are most effective at aligning supplier behavior with sustainability targets. On the other hand, LLMs enable the quantification of informal incentives, such as reputational costs, by analyzing media sentiment, analyst reports, and earnings calls to capture the real-time costs of misalignment. This facilitates rigorous examination of how market-based forces complement formal governance in promoting sustainable outcomes.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478261454786 - Supplemental material for Integrating operations and finance for sustainable development: Theory, practice, and opportunities

Supplemental material, sj-pdf-1-pao-10.1177_10591478261454786 for Integrating operations and finance for sustainable development: Theory, practice, and opportunities by Yuxuan Zhang, Boya Peng and Jing Wu in Production and Operations Management

Footnotes

Acknowledgments

The authors acknowledge the editorial team’s efforts in undertaking the review process and the anonymous reviewers’ valuable comments in improving the quality of the article.

Funding

Yuxuan Zhang acknowledges the support from the National Natural Science Foundation of China (Grant no. 72201060). Jing Wu acknowledges the support from the Research Grants Council (Grant no. 14505325).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Notes

How to cite this article

Zhang Y, Peng B and Wu J (2026) Integrating operations and finance for sustainable development: Theory, practice, and opportunities. Production and Operations Management x(x): 1–14.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.