Recent innovations have driven a steady increase in online marketplace transactions. To remain competitive, numerous marketplace platforms and independent data providers offer Competitive Intelligence Services (CIS), enabling sellers to explore not only their market potential but also that of their competitors. In this article, we employ a two-period game-theoretic approach to competitive learning to analyze the impact of CIS on participants with varying market shares in an online marketplace. In the presence of noisy demand signals, the online platform benefits from offering CIS to both sellers. This is because high demand noise makes demand exploration difficult for each seller in the first period. Consequently, price competition under poor knowledge of the price-demand relationship in the second period leads to a lower payoff for each seller as well as the platform. However, as demand uncertainty decreases, the platform prefers to induce CIS subscription exclusively for the seller with the larger market share. This scenario leads to signal-jamming behavior between the sellers, which results in a win-win-win situation for both sellers and the platform provider. Finally, we consider various model extensions and discuss the managerial implications for the design and regulation of competitive intelligence services in online marketplaces.

Online marketplaces have witnessed significant growth over the years. In 2025, these platforms accounted for more than 23% of global retail sales, and this figure is expected to reach 25% by 2030 (Statista, 2025). Online marketplaces differ considerably within the retail sector, depending on whether they facilitate business-to-business (B2B), business-to-consumer (B2C), or peer-to-peer (P2P) transactions (Anastasia, 2020); whether they exchange goods, services, or information (Pryhodko, 2020); and whether they generate revenue via advertisements, sales commission, or subscription services. Regardless, the value proposition of all online platforms is the same: facilitating transactions between independent supply and demand-side participants (Täuscher and Laudien, 2018). As such, their growth will continue in the foreseeable future, and they will continue to attract not only more consumers but also more sellers, thereby creating a win-win scenario for all stakeholders.

In order to gain a competitive advantage, many sellers on online marketplaces employ tools that gather, manage, and use information collected not only from their own customers but also from their competitors. In fact, a survey conducted by Forrester Consulting (Yakkundi, 2016) among 115 technology, marketing, and business professionals suggests that exploring the customer journey in a competitive customer-facing web environment is the highest strategic priority for sellers. However, not all online sellers have the resources to carry out competitive intelligence activities on their own. According to a 2018 survey of mostly U.S.-based Amazon sellers, 73% of them had only one to five employees (and 93% had fewer than 50 employees).1 This is why easy-to-use Competitive Intelligence2 Services (CIS), powered by artificial intelligence and machine learning, have gained popularity on platforms like Google, Amazon, and others (Mroz, 2018). For example, subscribing to Amazon Marketing Web Services (recently revised to Selling Partner API) enables sellers to understand the source of traffic for not only their own products but also for those of their competitors (Malachard, 2020). WeChat Marketing Services allow sellers to segment their own customers as well as those of their competitors based on clickstream data (TDA, 2019). The need for competitive intelligence services has given rise to a number of third-party data brokers, such as Scrapfly, Competitive Analytics, Liberty Metrics, and Jungle Scout, who provide automated data collection services to sellers in online marketplaces.

However, even though CIS are widely popular, little is known about how these services, provided by the platform to its sellers, affect seller decisions and platform actions over time. On the one hand, consider the decisions taken by the sellers after receiving business intelligence inputs. If, for instance, all the sellers on a platform are subscribed to CIS, then they will all have access to intelligence inputs. Undoubtedly, these inputs will alter their decisions compared to a situation in which only a few sellers are subscribed to CIS. In the latter case, only the sellers receiving CIS inputs will gain a competitive advantage, whereas in the former case, the effect of CIS is likely to be eroded. On the other hand, consider the decisions taken by sellers during the data collection/analysis stage, i.e., before the availability of business intelligence. In that stage, the decisions of all sellers, whether or not they have subscribed to CIS, are likely to directly affect the quality of information gathered from the data collected. Thus, sellers have an opportunity to increase or decrease the quality of intelligence available to the platform. Overall, after considering the ex-ante and ex-post impacts of CIS on all the stakeholders, we arrive at the following research questions:

How does offering CIS to both sellers affect the payoffs of the platform participants and consumer welfare?

What is the impact of offering CIS exclusively to only one seller on the decisions and payoffs of the platform, sellers, and consumers?

To address these research questions, we develop a stylized two-period model that studies two asymmetric sellers (in terms of their market potentials) who sell their products through an online marketplace, which we refer to as the platform.3 The platform charges a fixed subscription fee for CIS, and the sellers decide whether to subscribe to the CIS or not. The sellers then compete in prices in both periods. In order to capture the value and impact of CIS, we employ a demand-learning framework. Specifically, the market potential (represented by online traffic) of each seller is initially unknown to both sellers and the platform provider. In the first period, each seller sets an exploratory price with the objective of learning the true market potential during the first period. At the end of the first period, each seller observes only her own sales, whereas the platform observes sales of both sellers, and therefore has access to superior information. Based on the observed sales, both the sellers and the platform update their beliefs about the true market potential. If a seller is subscribed to CIS, then, at the end of the first period, that seller receives the updated belief of the platform. Otherwise, she relies only on her own updated belief and decides on the second-period price. Building on the above modeling framework and considering the possibility of each seller’s subscription decision for CIS information, we create four scenarios and provide a complete characterization of the equilibrium prices and payoffs in both periods.

To address the first research question, we consider two scenarios: one where both sellers subscribe to the CIS, and the other where neither seller does. Under each scenario, we characterize the subscription fees that are incentive compatible for the sellers. Finally, we compare the equilibrium payoffs from the platform’s perspective. Our analysis shows that if the observations from the first-period sales are too uncertain for the sellers to accurately identify the true market potential or when the degree of competition between the sellers is low, the platform has an incentive to induce both sellers to subscribe to the CIS. When either of these conditions is not met, the platform actually prefers not to induce any of the sellers to subscribe to the CIS. Consequently, each seller has to find her own balance between exploring the demand parameters and exploiting the available information in a competitive environment. This result is robust to various extensions under which sellers are asymmetric in marginal cost, the total parameters governing the market potential become state dependent, and the demand noise for each seller is non-uniform and partially correlated.

In order to address the second research question, we consider scenarios in which one seller subscribes to CIS while the other seller does not. Our analysis shows that the platform finds it incentive compatible to induce only the seller with the larger market to subscribe, accomplishing this by setting a subscription fee that makes it profitable for only the larger-market seller to participate. Analyzing the equilibrium, contrary to our intuition, reveals that a seller with a smaller market share may indeed benefit from not subscribing to CIS. This counterintuitive finding arises due to the nature of first-period price competition between the sellers when only one of them subscribes to CIS. Specifically, the seller who receives updated information about the market potential from the platform has an incentive to charge a price that makes it difficult for the competitor to explore. We call this signal-jamming and analyze its impact on equilibrium prices. Interestingly, signal-jamming leads to both sellers charging higher first-period prices, which turns out to be mutually beneficial for all parties involved, resulting in a win-win-win scenario for both sellers and the platform provider. However, from a consumer welfare perspective, this scenario hurts customers because of the high prices at equilibrium.

Our findings have managerial implications for platforms and regulators. First, our study identifies when and to whom marketplace providers should offer CIS: when the demand information is too uncertain for the sellers, the platform should step in and induce both sellers to subscribe to the CIS by offering this service. Our results show that this would prevent both sellers from charging suboptimal prices and increase profits for the whole platform. We expect that products with short life cycles, such as fashion items or high-tech products, are likely to have more uncertain demand; hence, in such cases, the platform should take the initiative to explore and share the demand symmetrically with all marketplace players. However, in the case of products with relatively less uncertain demand, such as commodity items or non-seasonal products, our results show that the platform should either delegate the demand exploration to each seller or, if it must interfere, induce only the seller with the larger market share to subscribe to the CIS.

That being said, from a regulator’s perspective, this asymmetric information sharing leads to lower consumer welfare. As such, a marketplace regulator should ensure that platforms do not offer a subscription policy that affects marketplace players asymmetrically. In fact, the recent data-sharing regulations designed by the European Union aim to create a level playing field for all the stakeholders in online marketplaces.4 Warnings have been issued to ensure proper regulation of platforms and guard against their powerful network effects (Sokol and Van Alstyne, 2021).

Along these lines, our findings speak directly to a sharp contrast between how the European Union (EU) and the United States (US) regulate data sharing on digital platforms. The EU adopts an ex-ante approach: the Digital Markets Act (DMA), which became applicable in May 2023 with gatekeeper compliance required from March 2024, requires designated platform “gatekeepers” (such as Amazon and Meta) to provide business users with continuous, real-time, non-discriminatory access to the data generated through their own activities on the platform, and prohibits gatekeepers from using non-public business-user data to compete against those same users (Articles 6(2) and 6(10); Cabral et al., 2021; Commission, 2025). The US, by contrast, imposes no comparable mandate and instead relies on ex-post antitrust enforcement, intervening only after specific conduct is shown to harm competition. These two philosophies embody a fundamental trade-off: the EU’s symmetric-access rule is designed to protect smaller sellers and consumers but constrains the platform’s ability to share information selectively, whereas the US’s permissive stance preserves the platform’s flexibility at the risk of asymmetric outcomes that may disadvantage smaller sellers and consumers. Our model provides an analytical lens for this debate: it identifies the specific market conditions under which the platform’s privately optimal information-sharing regime is symmetric (consistent with the DMA) versus asymmetric (permissible only under the US regime), and pinpoints exactly when each regulatory philosophy yields socially desirable outcomes.

The rest of this article is organized as follows. In § 2, we position our work in the context of other relevant literature. In § 3, we develop our modeling framework. In § 4, we analyze the impact of offering CIS to both sellers. In § 5, we analyze the impact of offering CIS exclusively to only one of the sellers. We extend our results in § 6 and conclude the article with managerial and theoretical insights in § 7.

Related literature

The design of initiatives for information exchange among members of the distribution channel has always been a crucial topic (Dukes et al., 2016; Gal-Or et al., 2008; Guo and Zhao, 2009; He et al., 2008). More recently, this has become even more critical due to the ability of online platforms to efficiently collect extensive data on consumers’ purchasing habits. Consequently, the strategies for deciding to whom and how this information is shared, often hidden from upstream manufacturers and rival sellers, have gained greater significance (Caldieraro et al., 2018; Ha et al., 2022; Long et al., 2022; Shi et al., 2023; Zha et al., 2023). Our article contributes to this research stream by examining how platforms can benefit from competitive learning through the governance of CIS among participants with varying market shares in an online marketplace.

The platform’s strategy for sharing sales information is based on how this information influences price competition among retailers and, consequently, the profit of each party, as well as the overall channel profit (Lai et al., 2022). In reality, sellers may not have precise knowledge of the relationship between price and demand. However, they can learn it through price experimentation (exploration) without completely sacrificing their revenue maximization goal (exploitation). This exploration-exploitation trade-off has been examined in prior research (Chen and Chen, 2015). With this in mind, our primary goal is to provide context for our work and highlight its value and relevance. Accordingly, we categorize existing research into three groups based on the market structures they analyze: (i) a monopolistic seller, (ii) competing sellers, and (iii) a platform and competing sellers.

Early work on the exploration-exploitation trade-off analyzed the conditions under which a monopolistic seller would eventually obtain complete information about the underlying demand environment, while it focused only on exploitation (Aghion et al., 1993; Easley and Kiefer, 1988; Harrington, 1995; McLennan, 1984; Rothschild, 1974). Later, the focus shifted to developing algorithms with provable worst-case bounds based on minimizing regret. One approach to categorizing this stream of literature is by the mechanism used to estimate the demand parameters: Bayesian updating (Araman and Caldentey, 2009; Ching et al., 2013; Gallego and Talebian, 2012; Lin, 2006; Narayan et al., 2011), realization probability (Cao and Zhang, 2021), and linear least squares (Bertsimas and Perakis, 2006; Misra et al., 2019). More recent work considers a variety of revenue management issues, such as a limited range of prices available to the seller (Perakis and Singhvi, 2024), customized pricing decisions (Chen and Gallego, 2022; Chen and Iyer, 2002; Liu and Zhang, 2006), and the impact of markdown policies for demand learning with forward-looking customers (Birge et al., 2025). Our work differs from the monopoly stream in that we study seller competition. We identify the subgame-perfect equilibrium prices, which take into account the optimum exploration-exploitation trade-off given the competitive dynamics between sellers and the platform.

Accounting for competition in a demand-learning framework not only requires a rich underlying demand model and a convoluted game-theoretic analysis, but also complicates the exploration–exploitation trade-off faced by the sellers. Each seller needs to decide on the level of exploration while being aware that their experimentation can benefit rival sellers by increasing their profits or by providing them with free demand information (Bolton and Harris, 1999). The majority of the works in this stream deploy a two-period model with two sellers. Sellers have imperfect information about the demand model when making their first-period decisions. In the second period, sellers make use of Bayesian updating based on the observed decisions and outcomes. This research focuses on identifying how the subgame-perfect equilibrium decisions compare with the myopic case (no exploration), the monopoly case, or the case of perfect demand information. Thus, the most relevant categorization of the existing work from our perspective is based on the distribution of information among the stakeholders. Specifically, it is either assumed that all sellers observe all the sales and decisions (Belleflamme and Bloch, 2001; Keller and Rady, 2003; Tsunoda and Zennyo, 2021) or that the first-period decisions (output in Cournot models and price in Bertrand models) are private information (Bernhardt and Taub, 2015; Bonatti et al., 2017; Stern and Birge, 2020). When first-period decisions are common knowledge, sellers tend to adjust their decisions to acquire more information at the end of the first period. However, when first-period decisions are private information, an opportunity arises to manipulate the information available to opponents, i.e., signal-jamming. The novelty of this work lies in its use of a platform (i.e., an online marketplace) through which all the sellers compete. As an entity that has access to the sales individually observed by each seller, the platform can also explore the true demand by itself and share this information with all or none of the sellers or even exclusively with one seller, which is a unique and novel scenario. By explicitly considering platform-mediated interactions, we explore the interaction between the platform’s exploration and sellers’ pricing decisions.

Our model is also related to Operations Management literature that explores the impact of sharing demand information in supply chains (Chen, 2003; Guo et al., 2014; Jain, 2022; Wang et al., 2022). Previous studies often examine bilevel supply chain structures and involve vertical (Cachon and Lariviere, 2001) or horizontal competition (Ha and Tong, 2008), as well as information-sharing games among competing supply chains (Ha et al., 2011; Shamir and Shin, 2016). The credibility of shared demand information is a central concern in this literature, addressed through screening (Ha and Tong, 2008) or signaling mechanisms (Gümüş, 2014). Our work differs in two main ways. First, while many studies assume one supply chain partner possesses ex-ante private information about demand, in our model, demand information is ex-ante unknown to all parties. Second, prior research often assumes that private information remains unaffected by other supply chain firms’ decisions. In contrast, our model considers how each party’s (sellers and platform) knowledge of true demand information is influenced by competing firms’ decisions (specifically pricing). These unique features allow us to analyze the exploration–exploitation trade-off in the context of platform-mediated competition.

Recent works point to a growing interest in modeling the exploration–exploitation trade-off over a duration longer than two periods (Perakis and Sood, 2006; Stern and Birge, 2020). Perakis and Sood (2006) propose a robust optimization approach that maximizes the revenue for each seller under the most adverse instances of unknown parameters of the demand function. They prove the existence of equilibrium policies and develop an iterative learning algorithm for finding them. In the work by Stern and Birge (2020), each seller estimates the underlying demand curve using least squares estimation. Interestingly, the results suggest that sellers may prefer to stay ignorant, as being informed may reduce prices (ignorance may lead to collusion). The analysis of a strategic game shows the existence of an equilibrium in which firms actively avoid learning (by avoiding experimentation) the true value of demand and attain a collusive outcome even in finite-time horizons. More recently, Yang et al. (2024) study competitive demand learning from an algorithmic perspective. They propose a nonparametric pricing algorithm that enables coordinated price experimentation among competing firms over multiple periods.

Our work differs from the literature on information sharing in retail platforms. First, unlike much of the literature (e.g., Bimpikis et al., 2019; Li et al., 2021; Liu et al., 2021; Wang et al., 2022; Zha et al., 2023), we do not assume that the platform or sellers initially hold private demand information; instead, we introduce a novel self-learning channel whereby sellers can infer demand from their own sales. Second, while most existing studies adopt a single-period or single-decision setting in which uninformed parties remain passive, we allow sellers to make two sequential pricing decisions, which creates a new intertemporal trade-off between exploration and exploitation. Finally, relative to empirical work such as Huang et al. (2022), which studies adaptive learning in real markets, our contribution lies in a game-theoretic analysis of how subscription-based and self-learning channels jointly shape equilibrium pricing, information acquisition, and welfare outcomes.

Last but not least, our model is also related to the literature on Bayesian persuasion and strategic information design (Kamenica and Gentzkow, 2011). In our model, the platform effectively commits to an information disclosure policy—implemented through its CIS subscription design—that shapes sellers’ posterior beliefs and pricing behavior. Unlike classical persuasion models, however, information in our setting is endogenously generated through sellers’ pricing decisions and sales realizations, and competing sellers can strategically manipulate the informativeness of this data. This interaction gives rise to signal-jamming incentives that are unique to platform-mediated competition and highlight new limits and possibilities of information design in competitive marketplaces.

Model framework

Consider two sellers, and , who are selling their products through an online platform, , over two periods. Both sellers are uncertain about their market sizes. To capture this uncertainty, we assume that the market size of each seller depends on the demand state , where can be high (i.e., ) or low (i.e., ) with equal probability. The true value of the demand state is set by nature and is a priori unknown to both sellers and the platform. We assume that sellers and vary in terms of their potential market sizes. Let denote the market size of seller under demand state , where . Without loss of generality, we assume that seller ’s market size is stochastically larger than that of seller , i.e., for any realization of the demand state .

Note that, at the end of the first period, each seller observes her own sales, while the platform observes the sales of both sellers. This highlights the significance of CIS benefits; the platform has a comprehensive view of total sales, resulting in a more accurate updated belief about the demand state. Consequently, the platform can share its updated belief with the seller(s) who have subscribed to the CIS. To model this, we define to represent the subscription fee, a lump-sum amount required to be paid by sellers if they desire access to CIS benefits. Let represent seller ’s decision to subscribe to CIS (i.e., ) or not (i.e., ). Consequently, four subscription regimes emerge: (i) regime under which neither of the sellers subscribe (i.e., ), (ii) regime under which both sellers subscribe (i.e., ), (iii) regime under which only the larger seller subscribes (i.e., ), and (iv) regime under which only the smaller seller subscribes (i.e., ). In order to avoid trivial cases, in which a seller can always learn the true demand state, we introduce a random shock in the demand function in a multiplicative form5 via a random variable for , where is independent and identically distributed uniformly . The sales observed by each seller in period under regime have the following linear functional form6:

where and denote the prices set by seller and the competitor , respectively, in period , given the subscription regime . Note that parameter controls the magnitude of both own- and cross-price elasticities, and as such, influences the degree of price competition between the sellers. When is set to zero, the cross-elasticity term vanishes, and therefore, the price set by the competitor firm has no effect on the demand for the firm’s product. However, as increases, a change in the competitor’s price has a progressively greater impact on the firm’s demand curve. Note also that the absolute value of the own-price elasticity of the demand function is greater than that of the cross-price elasticity in expectation, which is consistent with the findings in economics literature (e.g. Vives, 1999).

We assume that the marginal cost of the product is normalized to zero and consider the non-zero marginal cost in §6.1. Given the subscription decisions , which result in regime , the expected channel profit generated by seller can be expressed as follows:

where represents the price trajectory of seller over two periods; i.e., , the expectation is taken with respect to the a priori distribution on the demand state and the multiplicative noise for . Consequently, the payoff of seller can be written as follows:

where denotes the commission rate charged by the platform7 for each unit sold. To induce the information regime , the platform needs to solve the following optimization problem:

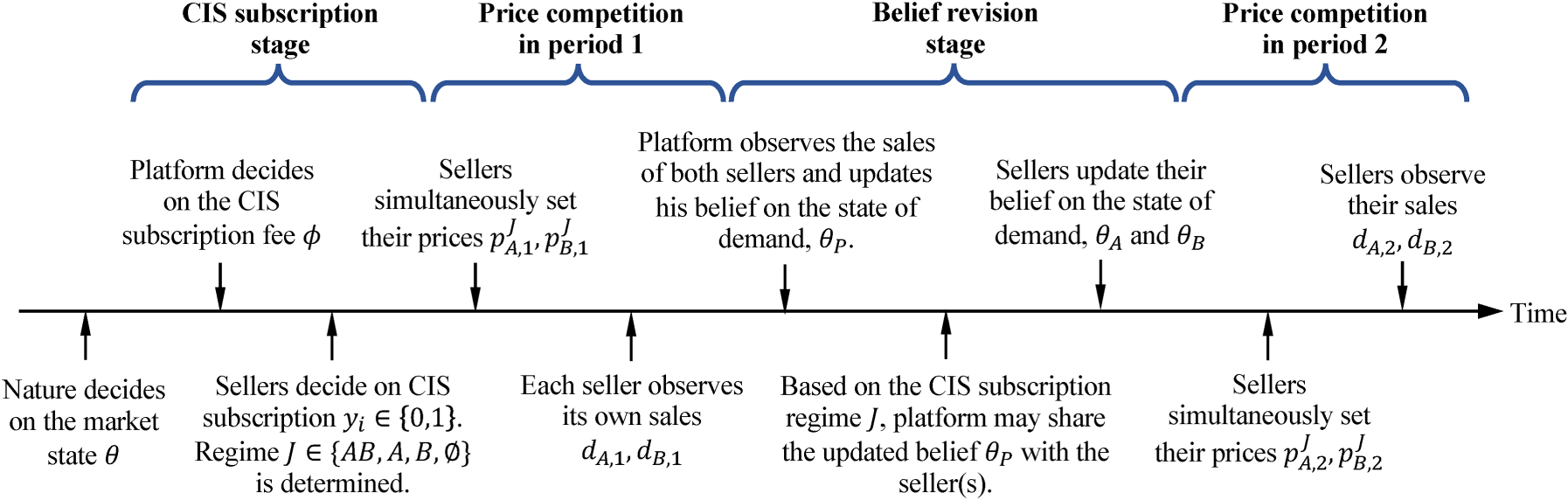

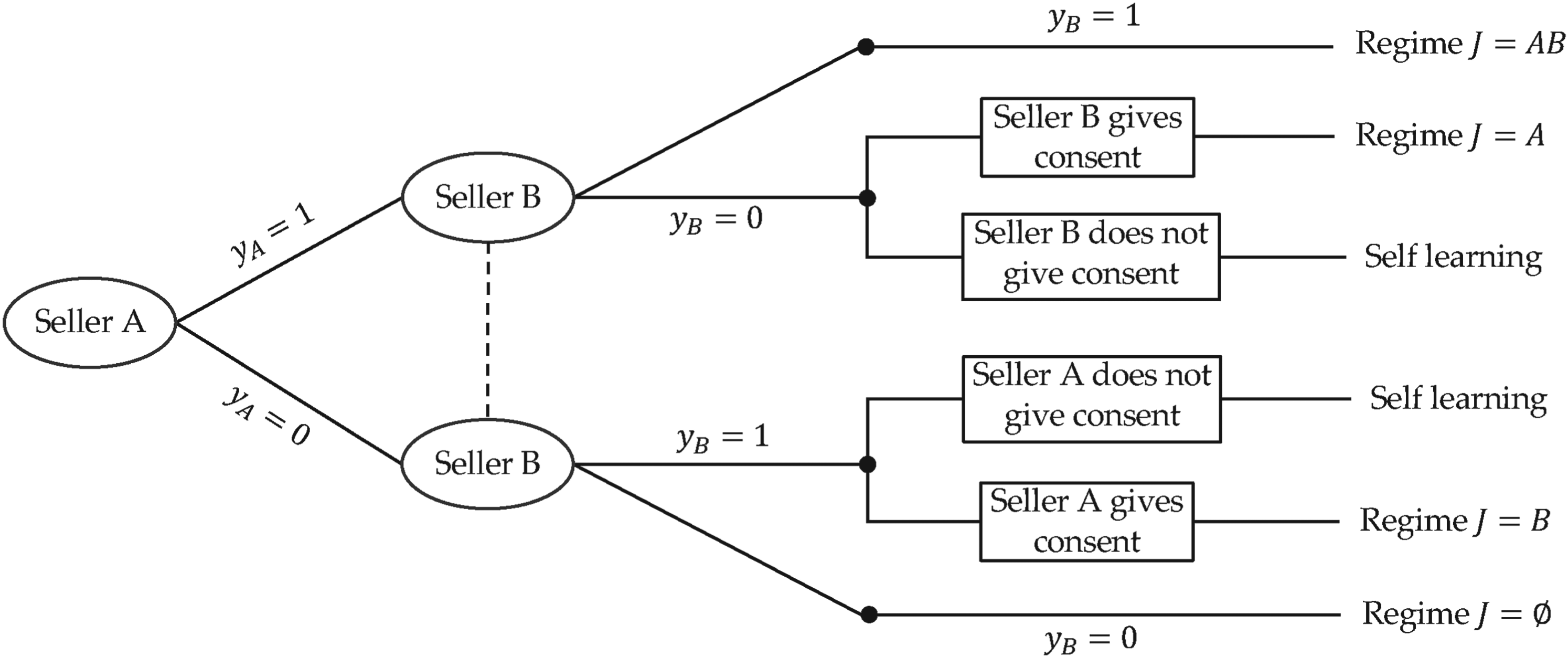

where constraint (3) represents the incentive compatibility constraint, ensuring that seller is better off by choosing a subscription decision aligned with regime . The detailed account of events is depicted in Figure 1. At the outset, nature determines the true demand state . The game is then played in the following stages:

Subscription stage: Without knowledge of the value of , the platform sets the CIS subscription fee . Sellers then rely on their prior beliefs to decide whether to subscribe to CIS (i.e., ) or not (i.e., ). Consequently, the subscription regime is established and remains valid for two periods. A key practical consideration is whether, in the presence of CIS services, a seller consents to the platform sharing her sales information with the other seller.8 In §4, we characterize the equilibrium under subscription regimes and . Under regime , the platform offers the CIS subscription to both sellers, and it is implemented only if both sellers provide their consent. In §5, we extend the analysis to subscription regimes and , where the CIS subscription is offered unilaterally to a single seller, and thus, consent from the other seller is required.

Price competition in period 1: Sellers and use their a priori beliefs about the true demand state and simultaneously set their prices and , respectively. At the end of period 1, each seller observes her own sales, , while the platform observes each seller’s sales; and .

Belief revision stage: The platform updates its belief and learns the true demand state; i.e., . It shares these updated beliefs with seller(s) if they opted for subscription to the CIS. Specifically, let denote the posterior belief of seller regarding demand at the end of the first period. Therefore, if .

Price competition in period 2: Sellers and use their posterior beliefs regarding the true demand state and simultaneously set their prices and , respectively. The sales and would be observed at the end of the second period.

To simplify the notation, in our baseline analysis, we assume that the total market size is normalized and equal to under both demand states.9 Accordingly, we use and for .

Sequence of events.

First-best solution

In this section, we analyze the first-best solution assuming that the platform controls the pricing decision of both products.10 Let denote the first-best prices charged by the platform for the product of seller and in period . Then, the platform solves the following optimization problem:

The optimal solution is fully characterized in the following proposition. Note that all proofs are provided in the e-Companion under Section EC.2. For ease of reference, each proposition has a dedicated subsection, i.e., the proof of Proposition 1 appears in EC.2.1, the proof of Proposition 2 in EC.2.2, etc.

Under the first-best scenario:

In the first period, the platform sets and where , , and ,

The learning is perfect; the platform learns the true demand state, i.e., ,

In the second period, the platform charges the state-dependent prices, i.e.,

Recall that, by assumption, seller ’s product is expected to achieve a higher market share than seller ’s product. Therefore, both first- and second-period prices for product are set higher than those for product . This price distinction is evident in the optimal price structure described in Proposition 1, where the price for product surpasses that of product . Furthermore, the price difference between the products diminishes as the degree of substitution (measured by ) increases. This is intuitive because the platform prefers to narrow the price gap to prevent demand cannibalization between the products.

Preliminaries

Before characterizing equilibrium under different CIS regimes , we first formulate the problem and define the solution concept for the equilibrium. Under a specific CIS regime, each seller sets her price in each period by solving the following price optimization problem:

given that solves the competing seller’s optimization problem:

We use the concept of perfect Bayesian equilibrium (PBE) (Fudenberg and Tirole, 1991) to solve the game above. Given the subscription regime , PBE requires the satisfaction of the following two conditions:

Subgame perfection condition: Given the updated (i.e., a posteriori) beliefs and , there is no profitable deviation for any seller from the equilibrium prices sequentially in the sense that:

In period , there is no profitable deviation for a seller given the equilibrium first-period prices and the competitor’s second-period price.

In period , there is no profitable deviation for a seller given the equilibrium subscription decisions, and given that sellers follow their best responses in period .

Bayesian updating condition: Given the first-period prices, sellers update their beliefs about the true demand state in line with the Bayesian updating rule.

Model analysis

In this section, our focus is on the competitive setting, and we analyze the impact of inducing both sellers to subscribe or not to subscribe to CIS on their equilibrium decisions and payoffs. To accomplish this, we first examine the equilibrium in the case of in §4.1, where both sellers choose to subscribe to CIS. Subsequently, in §4.2, we characterize the equilibrium prices in the case of , where neither of the sellers opts to subscribe to CIS. Next, in §4.3, we characterize the full equilibrium and evaluate the impact of the equilibrium on payoffs.

Regime : Inducing both sellers to subscribe to CIS

In this case, the platform can induce both sellers to subscribe to CIS by finding a subscription fee in Eq. (2) that satisfies the following two incentive compatibility constraints:

The above constraints collectively ensure that both sellers are better off by subscribing to CIS, thus forming the information regime . Moreover, since the platform has access to both sellers’ sales data and can always identify the true demand state at the end of the first period, both sellers are guaranteed to learn the true state of demand in the first period. This means that, unlike the no-CIS regime analyzed later in §4.2 (Proposition 4), where the first-period prices are shaped by an exploration–exploitation trade-off, in the presence of CIS, the sellers focus purely on exploitation, i.e., maximizing their first-period profit through price competition.

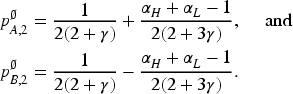

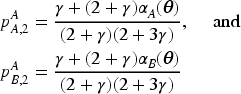

The platform can induce subscription regime only if , where is the solution of . The CIS subscription is offered at a cost ; both sellers subscribe and set the following equilibrium prices for the first period:

where , , and . After the first period, the platform learns the true demand state, i.e., , and shares the information with both sellers, i.e., . In the second period, sellers set the following equilibrium prices:

The main takeaways from Proposition 2 are as follows. First, to induce both sellers to subscribe, the platform sets the subscription fee high enough to capture the entire surplus that the smaller seller would gain from subscribing to CIS. However, the larger seller, i.e., seller , can still retain a portion of the surplus after accounting for the subscription fee. Second, inducing both sellers to subscribe to CIS is only feasible when the difference between the demand states under the a priori distribution is sufficiently low (i.e., ). Note that the first-period price of seller (and seller ) increases (decreases) with . When this difference becomes significant, i.e., , it becomes infeasible for the platform to satisfy the incentive compatibility constraint (7). This is because the price competition intensifies in the first period; as increases, seller becomes more optimistic about a favorable market state, leading her to raise her price to take advantage of the opportunity. To mitigate the price competition, seller prefers not to subscribe, opting to wait, observes her own sales, and makes decisions based on her posterior beliefs in the second period. Lastly, under regime , the average equilibrium price in the first period is lower than the first-best average price in Proposition 1 (i.e., ). However, the difference between equilibrium prices is higher than that of the first-best prices (i.e., ). These results are due to the price competition, leading to lower and more differentiated price levels compared to the first-best scenario, where the platform controls sellers’ prices.

Regime : Inducing both sellers not to subscribe

In this section, we analyze the scenario under which the platform induces both sellers not to subscribe to the CIS. To achieve this, the platform needs to satisfy the following incentive compatibility constraints:

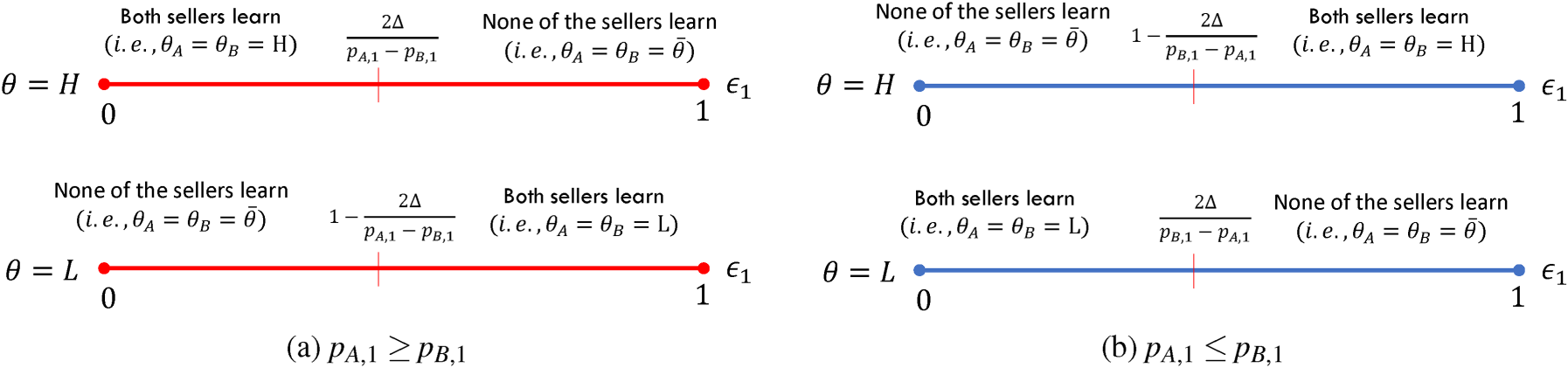

The above constraints collectively ensure that both sellers are better off by not subscribing to CIS, thus forming the information regime . Note that, without CIS, sellers only observe their own sales at the end of the first period. Using backward induction, we first establish the beliefs regarding the true demand state for each seller based on their first-period prices. Depending on the ordering of first-period prices between sellers and , two cases arise: (i) and (ii) . Throughout the article, we focus on the first case, because, as shown in the e-Companion, it is the only scenario that can be sustained on the equilibrium path. Given the price difference in the first period and realized first-period demand, one can characterize the belief revision of each seller.

Sellers’ belief updating based on first-period prices, true demand state and demand shock : (a) and (b)

Without subscribing to CIS, seller updates her beliefs about the true demand state according to Figure 2, which is illustrated as follows:

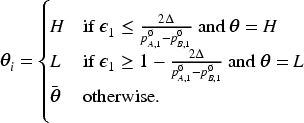

If the difference between the first-period prices is less than , where , i.e., , then, irrespective of the demand shock, both sellers and always learn the true demand state, i.e., for both .

If the price difference is larger than , i.e., , then, seller ’s learning depends on the true demand state (i.e., whether or ) and the magnitude of the first-period demand shock, i.e.,

Proposition 3 clarifies that a seller’s ability to learn the true demand state depends on the magnitude of the first-period price difference and demand shock. As shown in Figure 2, if the first-period prices are sufficiently close to each other (i.e., ), both sellers are guaranteed to learn the true demand state through individual self-exploration; i.e., they can do so on their own. The rationale behind this is that the random noise gets amplified in the price difference. Therefore, if the price difference exceeds a certain threshold, it becomes difficult (with a smaller probability) to determine whether the observed demand is driven by the true demand state or random demand noise. If the magnitude of the first-period price difference is sufficiently large, then sellers can infer the true demand state depending on the magnitude of the demand shock and true demand state. Namely, sellers can infer the true demand state only when their individual demand realization is at an extreme: either the demand shock is sufficiently low (i.e., ) or the demand shock is sufficiently high (i.e., ). This makes sense because when the price difference is large, the demand noise also becomes significant. Therefore, each seller needs to observe a signal that is sufficiently strong to differentiate between the high demand state and the low demand state.

The above observation has an important implication for the pricing policy of the sellers during the first period. On the one hand, if sellers and want to learn (i.e., explore) the true demand state by observing only their own sales, they have to converge their prices closer to each other, resulting in a smaller . On the other hand, the desire to exploit their first-period profit triggers price competition, compelling sellers to differentiate their products by widening the price gap. This creates conflicting incentives for the first-period prices and introduces an exploration–exploitation trade-off for the sellers. The following proposition fully characterizes the equilibrium first-period prices under this exploration–exploitation trade-off:

The platform can induce both sellers not to subscribe by setting subscription fee , where and .

where , and is characterized in EC.2.4. At the end of the first period, the sellers observe sales and update their own beliefs according to Proposition 3. Two scenarios may occur:

(i) If the sellers learn the demand, that is, or , then they set the following equilibrium second-period prices:

(ii) If the sellers do not learn the demand, i.e., , they set the following equilibrium second-period prices:

Characterization of equilibrium

Now, we are ready to analyze the subscription decision of the platform. By comparing Propositions 2 and 4, we can characterize the full equilibrium. Leaving the details to the e-Companion, we characterize the equilibrium subscription decision of the platform and equilibrium prices and belief-updating of the sellers in the following Proposition 5:

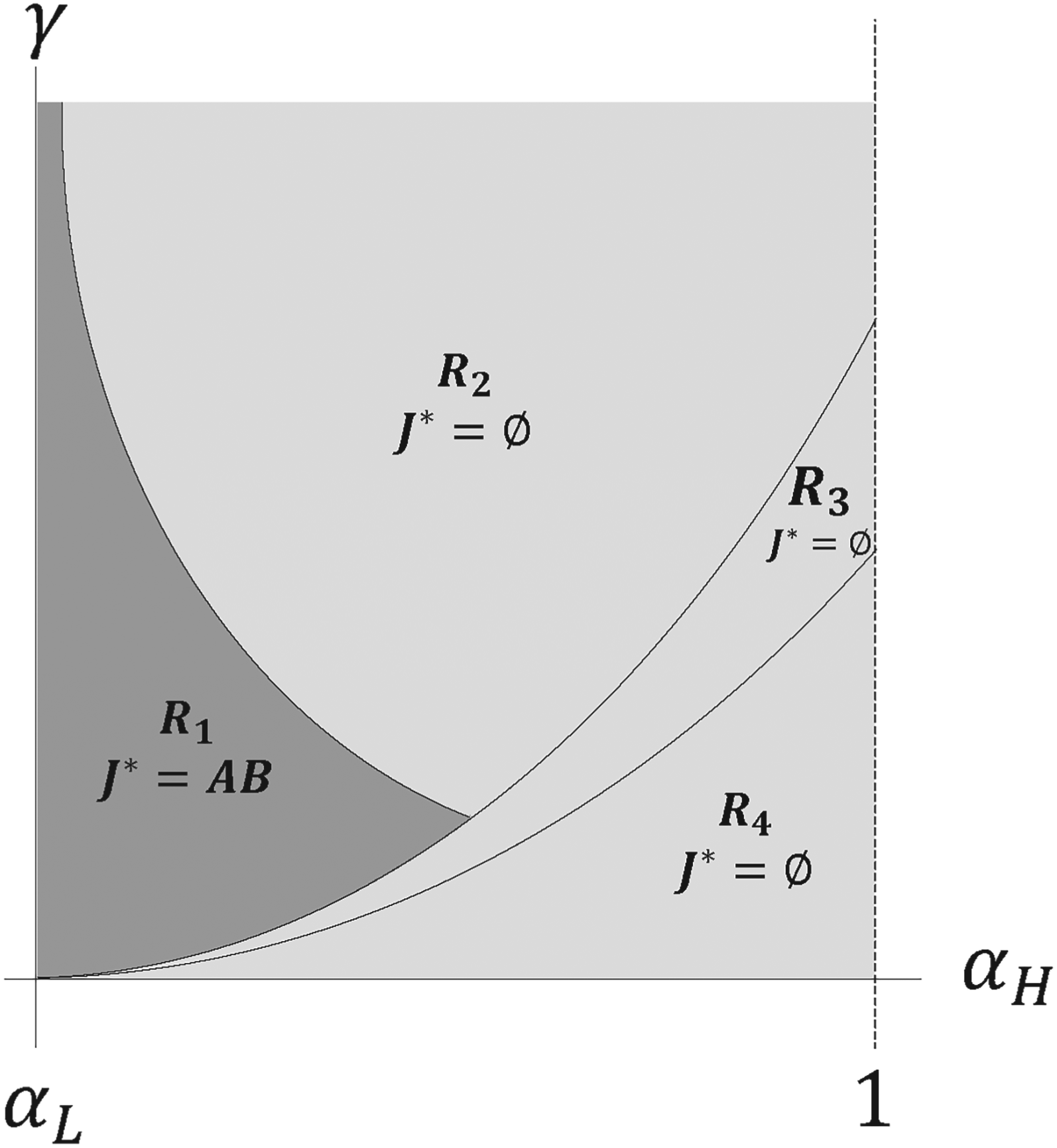

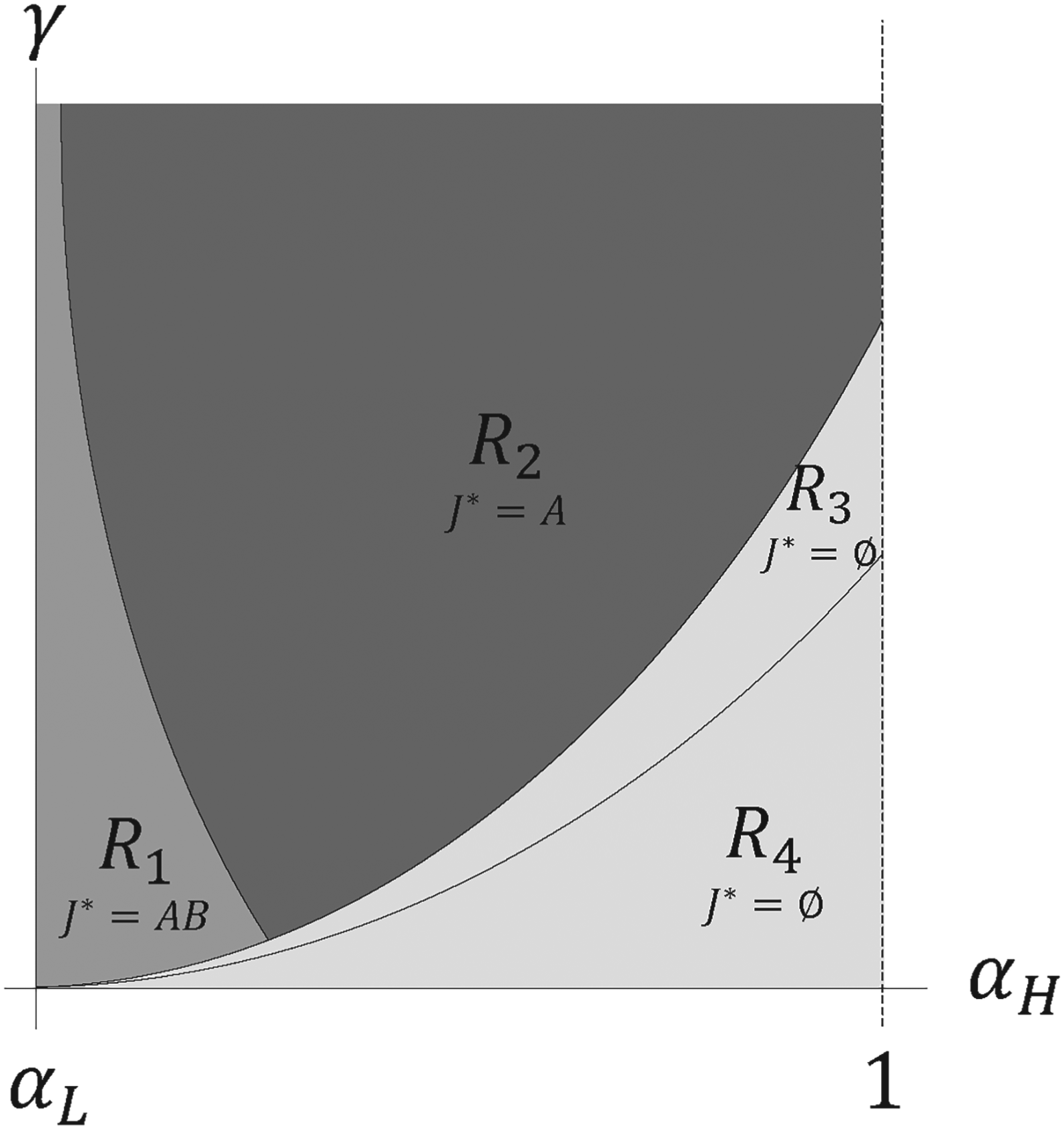

The equilibrium is divided into four regions, in each of which the platform’s equilibrium regime is characterized as follows:

Region (): Sellers are induced to subscribe to the information-sharing service and set their first-period prices accordingly. The platform observes sales, learns the true demand state, and shares this information with the sellers.

Region (): The platform sets the subscription fee high enough to discourage sellers from subscribing. Sellers set their first-period prices and update their beliefs based solely on their own demand observations.

Regions and (): Sellers do not require a subscription to learn the true demand state. They set their first-period prices and always infer the true demand by observing their own sales.

The corresponding equilibrium subscription fees, prices, and belief-updating rules are characterized in EC.2.5 and depicted in Figure 3.

Platform’s equilibrium subscription regime between and as a function of the demand spread (horizontal axis) and the substitution intensity (vertical axis).

As characterized in Proposition 5, the full equilibrium is categorized into four regions depending on the value of system parameters. To gain a deeper insight into the equilibrium analysis, we can evaluate each region by defining a ratio denoted by . Delegating the details to the e-Companion, this ratio can be shown to equal the spread between the demand states under the a priori distribution divided by the difference between the sellers’ average demands. Hence, it can be referred to as the signal-to-noise ratio (SNR).11 Since the SNR () increases in , we can rank the regions by their SNR values: region corresponds to the lowest SNR, region to a medium SNR, and regions and to the highest SNR. Using this measure, we can assess each region as follows:

Region : The SNR is extremely small, indicating only a narrow gap between the two demand states. In this setting, sellers find it difficult to identify the true demand state on their own. It is therefore up to the platform to determine whether it is beneficial to induce them to subscribe to the information-sharing service (CIS), a decision that involves a trade-off between first- and second-period outcomes. Inducing both sellers to subscribe to CIS benefits the platform in the second period: by sharing information, the platform enables sellers to fully learn the demand state at the end of the first period, allowing them to set more efficient prices and ultimately increase their second-period profits. The impact on first-period profits, however, is less straightforward. If both sellers know they will receive updated beliefs before the second-period price competition, they have no incentive to bring their prices closer together in the first period. This reduces price competition and lowers the platform’s first-period payoff. Nevertheless, the gain in the second-period payoff from more efficient pricing outweighs this loss. Accordingly, in region , the platform has an incentive to set the subscription fee low enough to encourage both sellers to subscribe to the information-sharing service.

Regions , , and : The SNR is sufficiently large for sellers to potentially learn the true demand state without subscribing. They can do so via one of two strategies: (i) bring their prices closer together (i.e., set ), which, per Proposition 3, allows both sellers to always learn the true demand state, or (ii) maintain distinct prices in the first period (i.e., set ) and infer the true demand state only probabilistically. The first strategy intensifies competition, which benefits the platform during the first period, while the second may result in suboptimal second-period prices due to the possibility that the demand state remains unidentified, which hurts the platform during the second period. Nevertheless, we can show that regardless of which strategy sellers choose, it is always optimal for the platform not to share demand information. Hence, in Regions , , and , the platform has no incentive to induce sellers to subscribe to CIS. From the sellers’ perspective, however, there is a trade-off between these two strategies, which depends on the level of , as explained below:

Region : In this region, is relatively high, which increases the degree of competition between sellers. Therefore, the sellers prefer to keep their first-period prices different (). Consequently, in some cases, the sellers cannot determine the true demand state by the end of the first period and must rely on their a priori beliefs when setting second-period prices.

Region : With sufficiently low , the cost of bringing prices closer is smaller due to weaker competitive pressure. Sellers, therefore, set their prices close enough () to fully eliminate noise and always learn the true demand state.

Region : The SNR is already very high, so sellers set , which enables them to identify the true demand state from their own demand observations without having to adjust their first-period prices.

The impact of equilibrium on sellers’ payoffs and consumer surplus

Up to this point, our analysis has focused on the platform’s perspective. Since the platform’s payoff depends on the combined profits of both sellers, it can tolerate a reduction in one seller’s profit as long as the overall change in total profit is positive. We now extend the analysis to examine how the equilibrium decisions affect the individual payoffs of sellers and seller , as formalized in the following proposition.

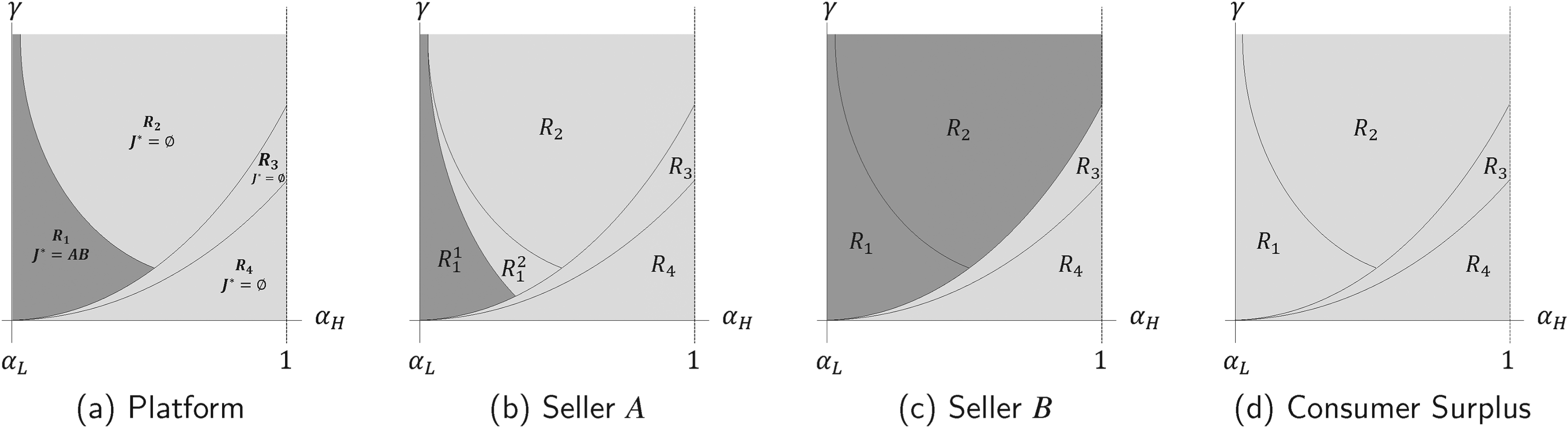

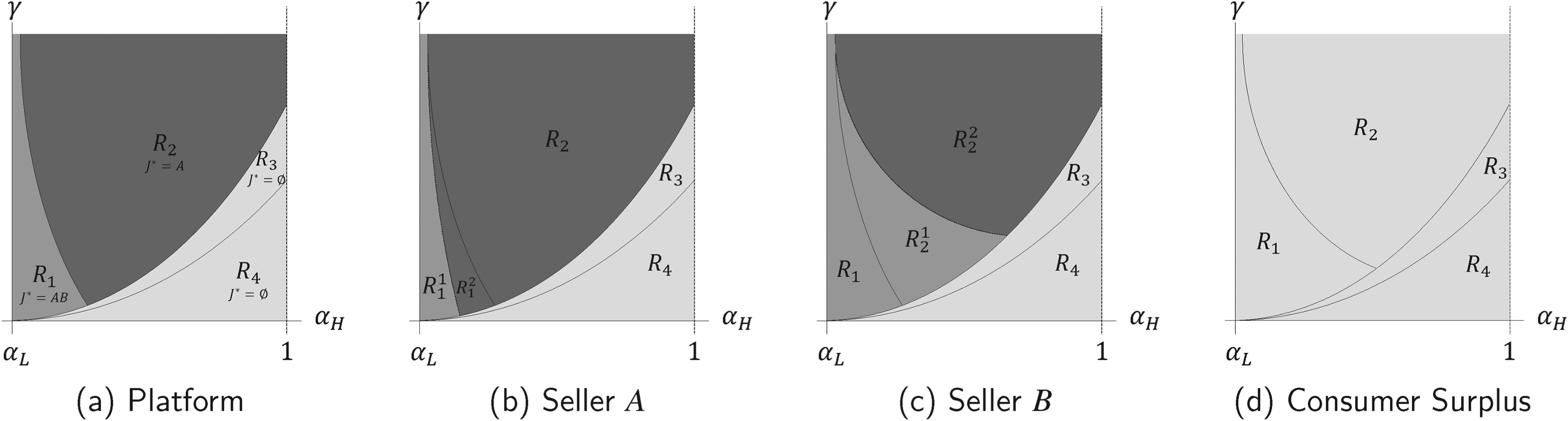

As shown in Figure 4, the comparison between each seller’s payoff under and scenarios results in the following characterizations:

Seller ’s preference is similar to that of the platform, albeit with slightly different regions, i.e., seller prefers over in region , otherwise seller prefers over .

Seller prefers over in regions and , otherwise seller prefers over .

Consumer surplus (CS) is maximized by regime in all regions.

Payoff comparison between regime (both sellers subscribe) and regime (no seller subscribes), shown for the platform, each seller, and consumer surplus, as a function of the demand spread (horizontal axis) and the substitution intensity (vertical axis) (in each panel, the dark-shaded area indicates where the corresponding party is better off under , and the light-shaded area where it is better off under ): (a) platform (b) seller (c) seller (d) consumer surplus.

Proposition 6 characterizes the preferences of sellers and consumer surplus between regime and regime . Do they prefer exploration mediated by the platform (i.e., regime ) or independent self-exploration (i.e., regime )? First, as shown in Figure 4, seller prefers CIS regime in both regions and . But seller prefers CIS regime only in a subregion inside , where the SNR is very low. Note that the smaller the SNR, the more difficult it becomes for seller to independently explore the demand state. Therefore, Proposition 6 can be interpreted as follows: If seller has to significantly reduce the price in order to self-learn, seller can benefit from CIS, while seller consistently benefits from CIS in both regions and . The rationale behind this interesting result is, again, tied to the impact of the method of demand exploration on competitive prices. When sellers need to explore demand themselves, seller ends up decreasing the price, while seller increases it. This leads to different consequences for sellers’ first- and second-period profits. For both seller and seller , self-exploration during the first period might not always reveal the true demand state in the second period. This is because they rely solely on their own observations and may not determine the true demand state if the actual sales differ only slightly from their expectations (for detailed information, refer to Proposition 4). However, if the sellers subscribe to CIS, they receive the true demand state from the platform, regardless of the sales realization. Consequently, both sellers are worse off with self-exploration from the perspective of second-period profits.

However, self-exploration, while it may harm both sellers in the second period, can actually benefit seller in the first period. To understand this difference, let us first consider the CIS scenario. When the platform provides information about the true demand state, sellers have complete knowledge in the second period, leading to intense competition between seller and seller in the first period. Seller tends to undercut seller . This benefits seller , as seller always benefits from receiving CIS, both in the short term (i.e., first period) and in the long term (i.e., second period). However, seller prefers the no-CIS scenario over CIS in the first period, primarily because it leads to reduced price competition in the form of less aggressive undercutting by seller . There is, however, a caveat. Under the no-CIS regime, seller needs to lower her price to engage in self-exploration, which results in a reduced profit margin in the first period. If the SNR is very low (i.e., subregion in ), seller needs to significantly decrease the profit margin; thus, overall, the seller benefits from CIS subscription in the first period. In summary, in subregion , seller ’s short-term loss from no-CIS is compensated by her long-term gain from receiving CIS.

The above analysis also has direct implications for the ongoing regulatory debate between the European Union (EU) and the United States on data access in digital platforms. Recent regulations in the EU increasingly emphasize improving sellers’ access to data generated through their own platform activities. Notably, the EU’s Digital Markets Act (DMA) (Commission, 2025) adopts a non-discriminatory perspective by requiring designated platform ”gatekeepers” to provide business users with continuous, high-quality access to data related to their sales and performance, without discriminatory treatment across sellers of different sizes (Cabral et al., 2021). Although our model treats the information-sharing regime as a choice variable of the platform provider, the fact that smaller sellers benefit disproportionately from information sharing relative to larger sellers yields insights that are consistent with this regulatory approach. Specifically, region (where ) corresponds precisely to the symmetric, non-discriminatory regime that the DMA mandates: when the SNR is low, the platform’s privately optimal choice happens to coincide with the symmetric-access rule, so the EU mandate is not binding. As we discuss in detail at the end of §5, the tension between the two regulatory philosophies arises only once the asymmetric regime becomes available, which is precisely the case the US framework permits but the DMA forecloses.

Figure 4(d) also shows that consumer surplus is maximized under regime . This outcome stems from how information-sharing regimes affect equilibrium prices, as described in Proposition 5. Between regimes and , the latter yields equilibrium prices that are more favorable for consumers. Intuitively, when both sellers must rely solely on their own sales to update beliefs, they bring their prices closer together to improve demand learning. This leads seller to increase her price while seller lowers hers. Although the increase in seller ’s price reduces consumer surplus, the decrease in seller ’s price has a larger positive effect, since seller serves a larger share of the market. The net result is an overall improvement in consumer welfare under regime .

The impact of inducing only one seller to subscribe to CIS

In §4, we analyzed the scenario in which the platform induces both sellers to subscribe to CIS. In this section, we extend the analysis to cases where the platform may offer the CIS subscription unilaterally to a single seller -either seller or seller - provided that the chosen seller agrees to pay the subscription fee. Since the platform derives demand information from the realized sales of both sellers, sharing this information with only one seller requires obtaining consent from the other. Consequently, as shown in Figure 5, unilateral information sharing is implemented only if the non-subscribing seller grants consent.

Sellers’ subscription and consent decisions.

Now, we analyze the equilibrium under unilateral subscription regimes. We have two cases: Regime and Regime . If the platform wants to induce CIS subscription for seller only, that is, forming the subscription regime , then the subscription fee offered by the platform should satisfy the following incentive compatibility constraints of the sellers:

where constraint (11) ensures that when seller subscribes to CIS, seller has no incentive to subscribe. Similarly, constraint (12) ensures that if seller decides not to subscribe, seller has no incentive to deviate and not subscribe. These two constraints together define subscription regime where and . Similarly, the following constraints should be met if the platform intends to induce only seller to subscribe to CIS, hence forming regime :

Before characterizing the equilibrium, we first show that inducing only seller to subscribe (i.e., the seller with the smaller market size) is not feasible. This issue stems from conflicts between the subscription incentives. On one hand, constraint (13) represents the maximum allowable value of the subscription fee to ensure that seller retains incentives to subscribe. On the other hand, constraint (14) signifies the minimum value of a subscription fee needed to prevent seller from subscribing. These two conditions together establish bounds on the subscription fee when inducing , namely: . However, the lower bound is greater than the upper bound. Therefore, as characterized below, implementing the subscription regime is not possible.

Regime is not implementable, that is, the platform cannot induce only seller to subscribe.

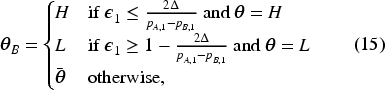

Next, we consider the case where the platform aims to induce only seller to subscribe to CIS. At the end of the first period, seller receives an updated belief from the platform, while seller relies solely on her own sales. Our analysis reveals that seller ’s belief updating follows the same process as the one characterized under the no-CIS scenario (regime ). In other words, as outlined in Proposition 4, seller updates her beliefs as follows:

where . Since is bounded between and , the updating rule implies that seller can learn the true demand state when the first-period price difference between sellers and is sufficiently small. In §4.2, we showed that both sellers have an incentive to bring their prices closer together to reduce demand noise and facilitate demand learning. However, under regime , seller is induced to subscribe to CIS and thus receives the true demand state directly from the platform, while seller must still rely on her first-period sales to update her beliefs about the true demand state. In this case, seller continues to have an incentive to align her price with seller ’s, but seller no longer benefits from doing so. In fact, as we characterize below, seller now has an incentive to increase the first-period price difference, which in turn makes demand learning more difficult for seller . We refer to this as signal-jamming and analyze its impact on equilibrium prices.

The equilibrium under regime is characterized as follows:

The platform can induce only seller to subscribe by offering .

Sellers A and B set the following prices in the first period:

where is described in EC.2.8 and .

After the first-period sales, seller receives the true demand state from the platform and seller updates her own beliefs according to Eq.(15).

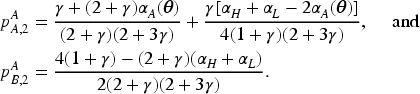

In the second period, the following equilibrium prices are set if seller learns the true demand state:

and the following equilibrium prices are set if seller does not learn:

The first part of Proposition 8 establishes that inducing subscription from seller , that is, the seller with the larger market size, is feasible provided the subscription fee is chosen appropriately. Specifically, the fee must be high enough to deter seller from subscribing to CIS, yet low enough to ensure that seller finds subscription profitable. By setting accordingly, the platform can satisfy the incentive compatibility constraints of sellers and . The second part of Proposition 8 characterizes the first-period equilibrium prices under regime . Since seller receives updated demand beliefs from the platform, she has no incentive to engage in exploration and instead focuses solely on exploitation in the first period. This behavior has two key implications. First, it increases the price gap between sellers and . As characterized in the Proposition 9 below, we compare the first-period equilibrium prices across all three regimes and demonstrate that the price difference between and is larger under regime than under regime . This wider gap between the first-period prices generates a signal-jamming effect: the greater the initial price difference, the less likely is seller to update her beliefs about the true demand state. Second, as seller raises her first-period price to hinder seller ’s learning, seller responds by increasing her own price. Consequently, the average first-period price level under regime exceeds the price levels characterized under both the full-information regime () and the no-information regime ().

The following statements hold for first-period equilibrium prices under the three regimes:

The ranking of first-period price differences between the sellers is .

Let denote the average first-period price in regime . Then, .

Note that the above proposition not only reveals the signal-jamming behavior but also has implications for the platform’s preference in implementing regime , regime or regime . By comparing the platform’s payoffs under these three regimes, we can now characterize the equilibrium as follows:

The equilibrium is divided into four regions, as summarized below:

Region : Both seller and seller are induced to subscribe to the information-sharing service.

Region : Only seller is induced to subscribe to the information-sharing service.

Regions and : Neither seller nor seller is induced to subscribe to the information-sharing service.

The corresponding equilibrium subscription fees, first- and second-period prices, and belief-updating rules are characterized in EC.2.10 for each region and depicted in Figure 6.

Platform’s equilibrium subscription regime () in the full model as a function of the demand spread (horizontal axis) and the substitution intensity (vertical axis).

The comparison between the equilibria characterized in Proposition 10 and Proposition 5 reveals both similarities and differences. First, similar to Proposition 5, the equilibria in Proposition 10 also consist of four distinct regions, although regions and differ slightly from those in Proposition 5. Second, in all regions except , the same regime is implemented in both propositions. The key distinction arises in region , where regime in Proposition 5 is replaced by regime in Proposition 10.

This difference stems from the signal-jamming behavior of seller toward seller . In region under Proposition 5, the platform benefits from not sharing demand information, as the sellers are incentivized to align their prices more closely, thereby intensifying first-period price competition. In contrast, under regime , the platform can selectively set the subscription fee to incentivize only seller to subscribe to the information-sharing service. With access to information, seller increases her price to jam seller ’s demand learning, prompting seller to increase her own price in response. As a result, both sellers charge higher prices. Even though this results in lower demand for both sellers, the increase in equilibrium prices ultimately increases the platform’s total revenue.

Although closed-form expressions for equilibrium prices in both periods can be derived, the complicated nature of these closed-form expressions makes direct comparisons of sellers’ profits and consumer surplus across regions intractable. To address this, we provide a graphical comparison of profits and consumer surplus in Figure 7 (for ).

Payoff comparison in the full equilibrium for the platform, each seller, and consumer surplus, as a function of the demand spread (horizontal axis) and the substitution intensity (vertical axis) (in each panel, dark shading marks where the corresponding party is best off under , medium shading under , and light shading under ): (a) platform (b) seller (c) seller (d) consumer surplus.

Since the platform’s preferences have already been discussed, we now restrict attention to the effects of different regions on the profits of sellers and , as well as consumer surplus:

Seller ’s preference: As shown in Figure 7(b), seller ’s preferences are generally aligned with those of the platform. This is intuitive: the platform shares demand information exclusively with seller , which benefits her in two ways. During the first period, seller can sustain higher prices, and at the start of the second period, she always has access to the true demand state, whereas seller may not. This ensures that seller maintains a competitive advantage over seller in the second period. Indeed, our numerical analysis confirms that seller prefers regime over regime in region , since under regime the true demand information is shared with both sellers, while under regime it is available only to seller . Thus, seller preserves a competitive edge in regime , making it more favorable than regime in region .

Seller ’s preference:Figure 7(c) reveals a more surprising result: within a subregion of , seller also prefers regime over regime . Although regime puts seller at a competitive disadvantage in the second period —since seller holds exclusive access to the demand state— seller nonetheless gains in the first period. The reason is that seller ’s signal-jamming behavior increases not only her own equilibrium price but also that of seller . The resulting increase in seller ’s first-period revenue can outweigh the loss from reduced learning in the second period. In summary, seller prefers regime over regime only when both the signal-to-noise ratio (SNR) and the degree of competition are very low—corresponding to region and the left portion of region (i.e., lower and lower ). In contrast, she prefers regime when competition is more intense and the SNR is relatively low - corresponding to the right portion of region . This right-hand side of region is precisely where the signal-jamming effect is strongest, leaving seller worse off in relative terms in the second period, yet still benefiting her due to higher equilibrium prices in the first period.

Consumer surplus:Figure 7(d) shows that the consumer surplus is maximized under regime even after we add regime into the consideration set. The rationale behind this is due to the effect of information-sharing regimes on equilibrium prices, as characterized in Proposition 9. Among all regimes, regime yields the most favorable prices from the consumers’ perspective. Intuitively, when both sellers must rely solely on their own sales to update beliefs, they bring their prices closer together to improve demand learning. This basically implies that seller increases her price, while seller decreases her price. Although the increase in seller ’s price reduces consumer surplus, the decrease in seller ’s price generates a larger positive effect, since seller serves a larger market. As a result, the net impact is an overall improvement in consumer surplus under regime .

We conclude this section by noting that the information-sharing regimes characterized here are also consistent with practices observed in digital markets. To illustrate how such regimes may appear in practice, consider a platform (such as Amazon.com or Google.com) that simultaneously operates as a gatekeeper and competes as a seller on its own platform. While the EU’s Digital Markets Act (DMA) (Cabral et al., 2021; Commission, 2025) takes a strict stance toward such dual-role platforms, these arrangements can readily arise under more permissive regulatory frameworks, such as those adopted in the United States. Moreover, in the United States, platforms commonly allow sellers to opt into analytics services that process seller-level data and generate insights that may be informative to competing sellers. For example, Amazon offers opt-in analytics tools (e.g., Brand Analytics (Amazon, 2025)) that use seller-level sales data to produce pricing, demand, or inventory recommendations, and platforms may also provide insights derived from aggregated activity across many sellers, such as market-basket analyses identifying products that are frequently purchased together.

The contrast between the US and EU regulatory approaches maps directly onto our equilibrium analysis, and our model helps clarify precisely what is at stake in choosing between them. The two jurisdictions embody fundamentally different philosophies. The EU relies on an ex-ante rule: under the DMA, designated gatekeepers must grant business users continuous, real-time, and non-discriminatory access to the data they generate, and are prohibited from using non-public business-user data to compete against those users (Cabral et al., 2021; Commission, 2025). In the context of our model, this rule effectively forces a symmetric information regime—either or —and forecloses the asymmetric regime , in which the platform shares demand information with the larger seller only. The US, by contrast, relies on ex-post antitrust enforcement: asymmetric data practices are permitted to emerge and are challenged only after specific conduct is shown to harm competition.

Robustness checks of analytical results

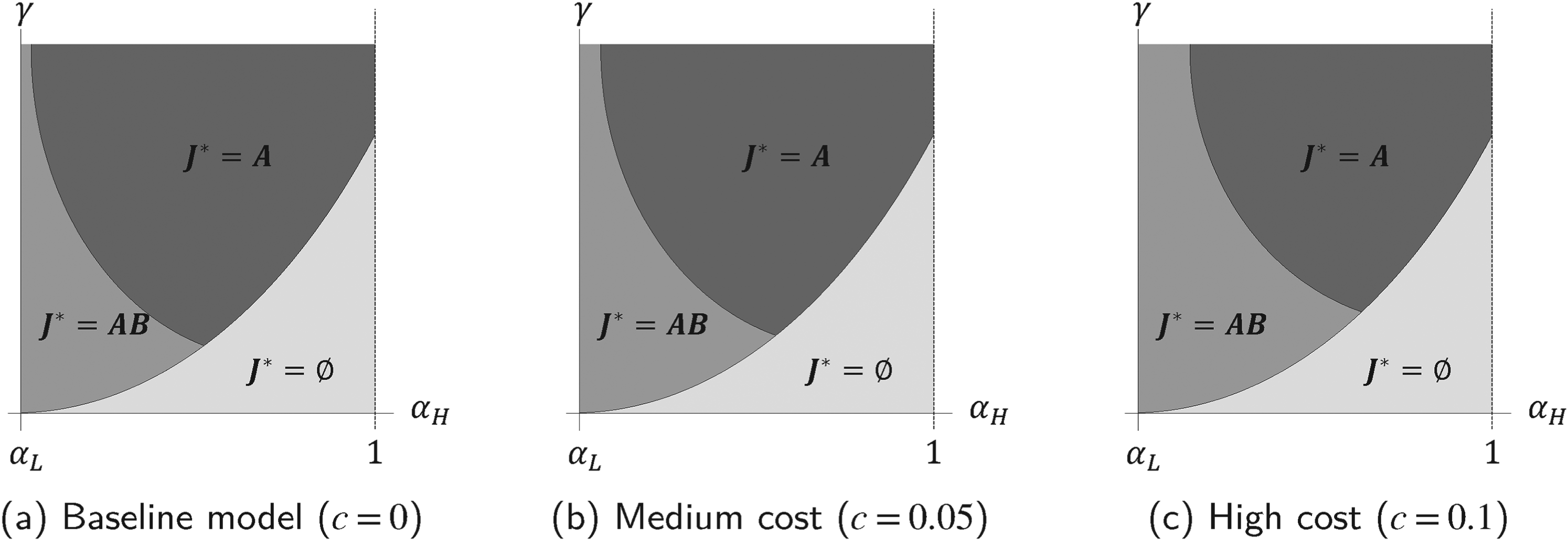

While §5 analytically established the impact of competitive demand exploration–exploitation on pricing strategies and payoffs, the results were obtained under the following assumptions required for tractability: (i) , i.e., the marginal cost is homogeneous and zero for both sellers, (ii) for , that is, the total market size under both demand states is normalized to be equal to , (iii) the noise in demand for both periods is distributed uniformly between 0 and 1, that is, , and and are independent. It turns out that relaxing any of these assumptions makes it challenging to characterize equilibrium decisions and, more importantly, to analytically establish the effects of different CIS arrangements. Leaving the details in EC.3, in this section, we numerically investigate whether or not the managerial insights presented in § 4 and § 5 remain valid if we relax the above assumptions. While our numerical study can validate the robustness of all our results, below we focus on the main insights about how heterogeneous marginal costs and state-dependent total demand affect the platform’s incentive to provide CIS.

Heterogeneous marginal costs

In this section, we use the same model framework as in § 3 and consider the case where the marginal costs for sellers are heterogeneous. It is reasonable to assume that , since seller ’s market share is larger than seller ’s market share for both demand states. For expositional brevity, we set and . By varying the value of , we focus on the impact of on the equilibrium regions. Specifically, we consider three cases: the baseline model (), a medium cost (), and a high cost (). We pick these values because when exceeds , seller finds it unprofitable to remain in the market, which leads to a monopolistic outcome for seller and thus trivial results for our model. The results are presented in Figure 8.

Comparison of the equilibrium information regimes with various values of seller ’s marginal cost (seller ’s marginal cost is normalized to 0). As increases, the region expands: (a) baseline model ()(b) medium cost ()(c) high cost ().

Recall that in §4 and §5 we show that under both regime and regime , sellers narrow the first-period price gap in order to increase the probability of learning. This implies that seller must decrease her first-period price, while seller must increase her price. However, when seller faces a positive marginal cost, her ability to reduce the price in pursuit of learning is limited. Consequently, both regimes and become more costly for the platform. As illustrated in Figure 8, our numerical results demonstrate that as marginal cost for seller increases, regime becomes relatively more advantageous for the platform compared to both regime and regime .

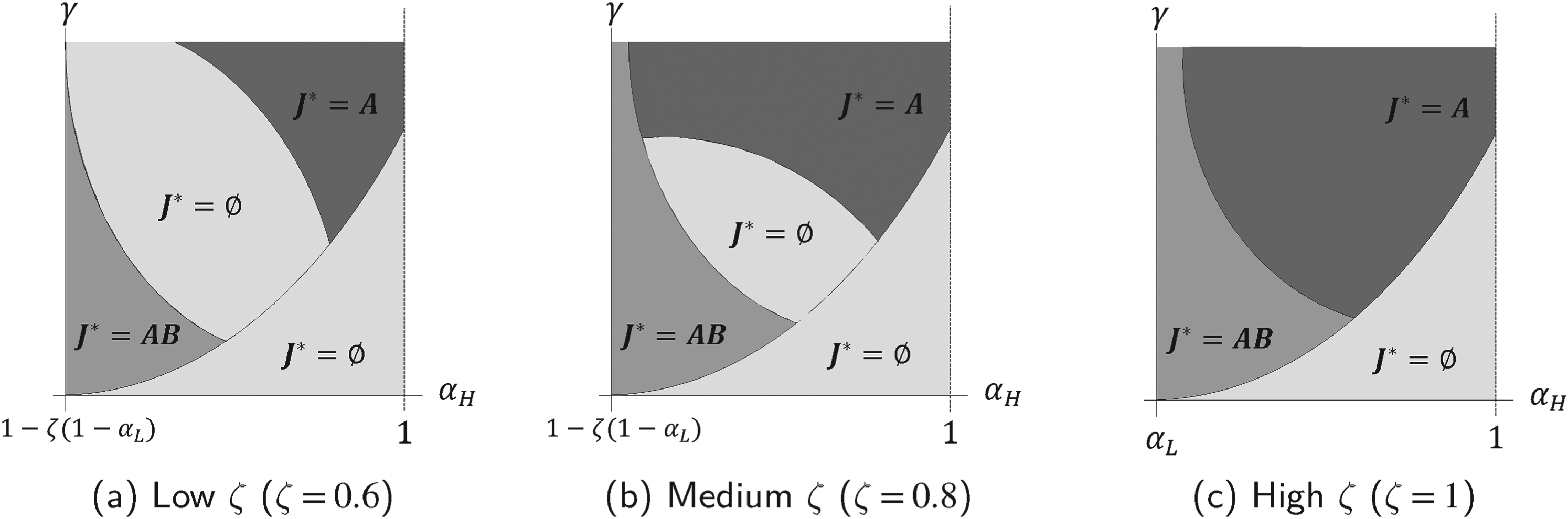

State-dependent total demand

In the baseline model, we normalized the total demand under both demand states to be equal to . In this section, we relax this assumption. That is, for the high-demand state, we still normalize the total market size to 1, but for low demand state, we normalize it to be equal to , where . Similar to § 6.1, we only focus on the impact of on the comparison between equilibrium information-sharing regimes. We consider three values for : low (i.e., ), medium (i.e., ) and high (i.e., ). The results are presented in Figure 9.

Equilibrium information regimes when low-state market size is scaled by . As decreases, variation in demand across states grows, and the region emerges due to price collusion, which enables self-exploration: (a) low ()(b) medium ()(c) high ().

Unlike in §6.1, the state-dependent aggregate demand extension changes the possible learning cases. When each seller self-explores the demand state by observing only their own sales, it is possible that seller learns the true demand state while seller does not. Moreover, by setting a price sufficiently far from the competitor’s, seller can ensure that she always learns the true demand state, regardless of demand realization, whereas seller cannot.

This new possibility has two implications. First, unlike in §4.2, seller no longer needs the platform’s demand information to engage in signal-jamming against seller in the first period. Second, this dynamic leads to price collusion, which raises the average equilibrium price in the first period. Consequently, regime emerges as the equilibrium in Figure 9, since it is preferred from the platform’s perspective. However, as increases, sustaining signal-jamming under regime becomes harder: the growing price gap between sellers and makes the signal-jamming region increasingly small. Hence, for higher values of , the platform prefers to intervene and implement regime .

Non-uniform and correlated noise distributions

In the baseline model, we assumed that the demand shocks follow independent uniform distributions on . To assess the robustness of our findings, we relax this assumption along two dimensions and summarize our key findings below.

Non-uniform noise. We first allow , which nests the uniform case () and accommodates right-skewed, left-skewed, and more concentrated symmetric shapes. The equilibrium regions remain qualitatively consistent with the baseline. When the distribution becomes more concentrated around its mean (e.g., ), demand uncertainty diminishes and the region in which both sellers share information (regime ) shrinks. Skewness shifts the mean of : a right-skewed distribution reduces effective demand noise and further contracts regime , whereas a left-skewed distribution amplifies it and expands regime . A new feature emerges in the left-skewed case: because the distribution is also more concentrated than the uniform, sellers can sometimes infer the demand state from their realized sales even absent information sharing, making regime an equilibrium when is moderate and is relatively low.

Correlated noise. We next allow and to be correlated via a truncated bivariate normal distribution with correlation . The baseline case corresponds to a benchmark of strong positive correlation (); we additionally examine . As correlation weakens, the signals observed by the two sellers diverge, producing asymmetric learning outcomes in which only one seller learns the true demand state. The resulting signal-jamming behavior cuts in opposite directions: seller ’s signal-jamming raises prices and benefits the platform, while seller ’s signal-jamming depresses prices and harms it. In the upper-right portion of the parameter space (high and ), the platform benefits on average from seller ’s signal-jamming, so regime emerges as the equilibrium. As decreases, seller ’s signal-jamming becomes too costly and the platform intervenes by sharing information with seller .

To summarize, these extensions confirm that the main qualitative insights of our baseline analysis are robust to richer distributional assumptions. We refer the reader to EC.4 for the detailed analysis and discussion.

Conclusion

Inarguably, the exponential growth in online marketplaces will attract not only more consumers but also more sellers, creating a win-win scenario for all stakeholders. In this article, we focus on the CIS that a platform can offer to its sellers. These services leverage the platform’s ability to learn about the unknown price–demand relationship faster than sellers themselves. We examine the demand exploration–exploitation trade-off faced by two sellers, competing over two periods, with varying market shares on an online platform. Each seller updates their estimate for the price-demand relationship based on individual sales observations. However, by observing the sales of both sellers, the platform excels at exploring demand, turning this demand information into valuable competitive business intelligence. As a result, the platform can mediate the demand exploration of the sellers in the first period by influencing their decision to subscribe or not to subscribe to CIS. We analytically establish the specific conditions that determine the optimal approach to demand exploration and the optimal CIS arrangement in online marketplaces. First, we characterize whether the platform should induce sellers to subscribe to CIS or not. Second, if the platform undertakes demand exploration, should it induce both sellers to subscribe to CIS, or just one of them? Finally, if the platform induces only one of the sellers to subscribe, which one should it be?

To address these research questions, we characterize closed-form expressions for the associated equilibrium prices and payoffs for the platform and the two sellers under all demand–exploration scenarios. From the platform’s perspective, our analysis suggests that by offering CIS to one or both sellers, the platform alters the nature of pricing decisions in the second period. More importantly, it also changes the nature of self-exploration and, consequently, the equilibrium pricing decisions in the first period. This transformation may have either a beneficial or a detrimental impact on the profitability of both sellers and the platform.

We also establish that the signal-to-noise ratio (SNR) of the random demand faced by the sellers is a key factor in determining the optimal CIS subscription strategy in a competitive environment. Specifically, it is optimal for the platform to offer CIS to both sellers when the SNR is low. This is because a low SNR makes self-exploration difficult for each seller in the first period. Consequently, the poor knowledge of the price–demand relationship in the second period leads to lower payoffs for both the sellers and the platform. This result appears to be rather robust and remains valid under general assumptions about the degree of demand substitution between sellers and heterogeneity in their marginal costs. In fact, as the degree of demand substitution and heterogeneity in their marginal costs increase, the provision of CIS by the platform becomes even more critical. Finally, when the SNR is high, the identity of the seller who subscribes to the CIS determines the level of price competition during the first period. Our results indicate that inducing CIS subscription solely for the smaller seller is not incentive-compatible. However, the larger seller benefits when she receives the demand information. Surprisingly, our analysis shows that the smaller seller, as well as the platform, also benefits when the demand information is shared with the opponent. This is due to price collusion triggered by the signal-jamming behavior of the larger seller. Our robustness check confirms that the larger seller engages in signal-jamming even if demand exploration is pursued independently by each seller.

Last but not least, our results highlight the inherent trade-offs faced by policymakers when regulating data sharing in digital markets. Highly restrictive regimes may limit platforms’ ability to leverage data-driven efficiencies, potentially slowing market expansion, whereas overly permissive approaches risk facilitating anti-competitive behavior and disadvantaging smaller sellers and consumers. This trade-off is precisely the one that distinguishes the EU’s ex-ante DMA mandate from the US’s ex-post antitrust approach. Our analysis shows that the two philosophies coincide when the signal-to-noise ratio of demand is either low or high, and diverge only in the intermediate range, where the asymmetric regime raises producer surplus at the expense of consumers. Our analysis suggests that carefully designed information-sharing rules are essential for the healthy development of digital markets. Along these lines, several important design issues remain open for future research. First, while many regulatory frameworks allow information to be shared in aggregated form, an open question concerns how such aggregation should be designed. Our model focuses on market size as the relevant information dimension, but in practice platforms may share more granular information, such as clickstream data capturing product views, add-to-cart actions, and purchases. Second, another important question is whether information-sharing regimes should be implemented on an opt-in or opt-out basis. Studying these design choices would help inform emerging regulatory frameworks that aim to account for the perspectives of multiple stakeholders. We leave these issues for future research.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478261460120 - Supplemental material for The impact of competitive intelligence services on online marketplaces

Supplemental material, sj-pdf-1-pao-10.1177_10591478261460120 for The impact of competitive intelligence services on online marketplaces by Mehmet Gumus, Sara Jaberi, Mohammad Nikoofal, Taner Bilgic and Arcan Nalca in Production and Operations Management

Footnotes

Acknowledgments

The authors express their gratitude to the department editor (Nitindra Joglekar), the anonymous senior editor, and the referees for their invaluable suggestions, which significantly enhanced the quality of this manuscript. Mehmet Gumus acknowledges the support from the Natural Sciences and Engineering Research Council of Canada [NSERC RGPIN-2019-06091 and NSERC RGPIN-2025-05765]; Fonds de Recherche du Québec- Nature et Technologies [FRQ-NT 331028]; and the Institute for Data Valorization [IVADO G254088 and IVADO R3AI 269015].

ORCID iDs

Mehmet Gumus

Mohammad Nikoofal

Taner Bilgic

Arcan Nalca

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online (doi: ).