Abstract

Firms engage in corporate political activity in an attempt to have a voice in the policy conversation. In recent years, CEOs have also increasingly become involved in corporate political activity. This paper investigates how CEO general ability affects the breadth of a company’s lobbying efforts, and how this relationship is moderated by the company’s performance feedback. Our findings indicate that CEO general ability is related to the breadth of lobbying efforts of a company in a curvilinear relationship, and that the gap between the company’s performance aspirations and actual performance moderates this relationship. These results have important implications for understanding the role of CEO ability in shaping corporate political activity.

Keywords

Introduction

The position of CEO in today’s business climate is multifaceted and complex. Responsibilities range from being responsible for the day-to-day operations of the organization to setting its strategic direction while at the same time being the public face of the company. While these roles are more traditional, CEOs are also increasingly called upon to lead in the corporate political activity (CPA) efforts of the firm, as businesses become more active in the political marketplace (Hadani et al., 2017; Lux et al., 2011). The diverse knowledge acquired by a CEO can significantly impact how they engage in CPA, as their multifaceted experiences can provide them with substantial human and social capital, and equipping them with the tools needed to identify and address a breadth of political issues (Custódio et al., 2019; Nahapiet & Ghoshal, 1998). By drawing on these experiences CEOs are able to apply their unique perspectives and knowledge of the diverse opportunities present in the political marketplace to confront the challenges encountered by their respective firms (Hillman et al., 2004; Rudy & Johnson, 2019).

Firms engage in CPA to proactively influence government decision-making or mitigate the negative impacts of regulatory implementation (Brown2023; Cheung et al., 2017; Hillman et al., 2004). CEO characteristics shape a firm’s CPA approach (Rudy & Johnson, 2019), but little is known about how CEO ability impacts CPA. Nonmarket strategies include a wide range of activities that extend beyond traditional market-oriented approaches and involve interactions with stakeholders such as government bodies, regulatory agencies, local communities, and advocacy groups. These strategies seek to shape the firm’s external environment, reduce risks, improve reputation, and gain a competitive advantage (Mellahi et al., 2016). CEOs with varying levels of abilities differ in the level and depth of their unique skills, experiences, and networks that allow them to navigate and influence nonmarket environments effectively. Therefore, in this study we investigate how these varying levels of abilities might influence the extent to which the CEO general ability level will determine the magnitude and the breadth of their firm’s lobbying. We examine how CEO general ability, defined as the accumulated knowledge and skills enabling strategic insights (Custódio et al., 2019), relates to CPA breadth, or the scope of government entities and issues a firm lobbies (Ridge et al., 2017). CEOs rely on performance feedback, comparing current performance to aspirations, to guide strategic decisions like CPA (Greve, 1998; Kuusela et al., 2017). Performance below aspirations spurs updates to preferences and temporal focus, requiring information search and processing skills that vary with CEO ability (Fang et al., 2014; Steinberg et al., 2022). While research shows feedback impacts strategic choices as international expansion, R&D, and communication (Jiang & Holburn, 2018; Lucas et al., 2018; Wang et al., 2022), little research currently examines its effect on CPA for CEOs with differing general ability.

We argue CEO ability has an inverted U-shaped relationship with CPA breadth. Initially, higher ability decreases CPA breadth as CEOs apply internal solutions and they do not have the knowledge, ability, or autonomy to engage broadly in CPA activities. At moderate levels, CEOs recognize CPA’s importance for managing environmental complexity and they have the knowledge, skills, and abilities to capitalize on a CPA strategy of increased breadth. However, the highest ability CEOs’ narrow their scope of CPA breadth due to their opportunity costs of other strategic opportunities. Performance feedback moderates this relationship, flattening the curvilinear effects of CEO ability on CPA breadth. We contribute to understanding CPA antecedents by applying upper echelons and human/social capital theories to CPA breadth (Hambrick & Mason, 1984; Lin et al., 2021; Nahapiet & Ghoshal, 1998). We also contribute to the literature on performance feedback’s strategic effects (Chen et al., 2022; Steinberg et al., 2022) by examining how varying aspiration levels influence CPA for CEOs with different abilities, addressing a lack of research on nonmarket strategies. Overall, a CEO’s experiences and abilities significantly impact how they engage in CPA, as they leverage their backgrounds to advance their firm’s political agenda.

Literature Review

Corporate Political Activity and Lobbying Breadth

The CEO is the primary decision-maker of the firm (Hambrick, 2007). While the bulk of the CPA research suggests that firms engage in CPA to influence public policymakers in an attempt to either proactively alter legislation being passed or mitigate the effects of regulation as it is implemented (Hillman et al., 2004). Scholars have recently investigated whether the CEO influences firms' investment in CPA (Rudy & Johnson, 2019). This research has primarily fallen into one of two camps. First, scholars have examined CEOs’ political ideology and whether firms’ CPA is an extension of their leader’s political aspirations and desires (Briscoe et al., 2014). The second path is more in line with historic CPA research, examining the CEO and their decision-making power as a factor influencing firm CPA (Brown et al., 2022).

The CEO’s political ideology has been shown to be an important factor in firms’ Corporate Political Activity (CPA). Research has found that Republican managers tend to result in higher levels of lobbying (Unsal et al., 2016). While these increased lobbying efforts may have some benefits, they also come with a cost (Unsal et al., 2016). In addition, CEOs have been found to influence PAC contributions when the interests of the firm and the CEO are aligned, and when the CEO has a high level of power and dominance within the company (Subrahmanyam et al., 2020). This suggests that the personal beliefs and values of the CEO can play a significant role in shaping the political agenda of the firm.

The relationship between a CEO’s political ideology and a firm’s political activity may be complex and multifaceted. According to Bonica (2016), corporate elites, including CEOs, tend to be more ideological and more willing to support non-incumbent candidates with higher risk profiles than firms that donate through PACs. Additionally, Bonica (2016) found that political elites, including CEOs, are less likely to donate to powerful legislators than corporate PACs. Furthermore, Fremeth et al. (2013) found that personal political activity among CEOs increased by 137% upon assuming the role. These findings suggest that not only does a CEO’s ideology influence a firm’s political activity, but assuming the role of CEO may also influence an individual’s personal political engagement.

Previous research has examined the role of the CEO as an antecedent to firm CPA in the context of Hillman et al.’s (2004) conceptual model. Ozer (2010) found that the political engagement of senior executives, including the CEO, has a strong influence on a firm’s commitment to CPA, and this influence is shaped by factors such as CEO tenure and management heterogeneity. The control and ownership structure of a firm has also been found to be important in shaping its CPA. For example, Hadani (2012) suggested that differences in views between owners and managers can impact CPA decisions, and found that institutional ownership can reduce CPA, although it may increase when institutional owners are distracted by other investments (as indicated by high levels of portfolio concentration). Hadani et al. (2015) further explored the moderating role of CEO characteristics on the relationship between CPA and firm performance, testing competing hypotheses based on agency theory and stewardship theory. In support of the agency theory, the authors found that CEO discretion negatively moderates this relationship. Despite this progress in understanding the influence of the CEO on firm CPA, further research is needed to identify the specific variables that shape CPA and the extent to which these CEO-level variables influence the effectiveness and return on CPA for firms (Brown et al., 2022).

CEO General Ability

One example of a CEO leveraging their experience and other elements of ability to invest in corporate political activity (CPA) is Ginni Rometty, who served as the chairman and CEO of IBM from 2012 to 2020, has been a prominent leader in the tech industry and a vocal advocate for social issues, drawing from her diverse professional background. Her diverse professional experience, including systems engineering, marketing, and strategy (Raval, 2023), enabled her to develop a unique perspective on the technology sector’s challenges and opportunities. This broad experience informed her political activism, as she has championed the idea of “new-collar” workers, who have relevant skills rather than formal degrees, and has supported initiatives to foster workforce development, education, and innovation (Ammerman et al., 2023; Stanford Graduate School of Business, 2018). Rometty demonstrated an unwavering commitment to driving diversity and inclusion within IBM, as well as the broader technology sector, and proactively engaged with policymakers on crucial issues, such as cybersecurity and data privacy (MIT News Office, 2021). Furthermore, she never shied away from political discourse. During a recent podcast, she stated, “you might look at the world and go, oh, the political system’s intractable. Nothing can get done. And I have just found, okay, yeah, it’s hard, but it is all changeable (Grant, 2023).” This perspective underlines her belief in the potential for change within complex systems. It is through such a strategic vision and her calculated political actions that Rometty has effectively positioned IBM as not only a thought leader but also a catalyst for positive change within the industry and society at large (Ammerman et al., 2023).

This example demonstrates how CEOs can draw on their diverse experiences and other elements of ability to effectively engage in corporate political activity. By leveraging their unique backgrounds, skills, and personal values, CEOs can shape their company’s political agenda and position on key issues, and serve as effective advocates for their business in the political sphere.

According to the upper echelons theory, CEOs are typically the most powerful individuals within an organization (Carpenter et al., 2004; Hambrick & Mason, 1984). Meta-analytic research further demonstrates that the characteristics and abilities of the CEO have a direct impact on firm-level outcomes (Quigley & Hambrick, 2015). Given the evidence that CEO general ability skills influence various firm-level strategies and outcomes (Custódio & Metzger, 2013; García-Sánchez & Martínez-Ferrero, 2019; Lin et al., 2021), it is plausible to posit that the CEO’s general ability plays a crucial role in shaping the magnitude and direction of firm-level political lobbying. Additionally, we propose that this effect may be contingent on the aspiration levels of the firm. In other words, the impact of the CEO’s general ability on firm-level political lobbying may vary depending on the goals and ambitions of the organization.

CEO ability is influenced not only by distinctive individual qualities, but also by the cumulative training and experiences that an individual accumulates over their career. CEOs often have diverse career backgrounds and education that expand their knowledge and capabilities (Hambrick & Fukutomi, 1991; Zhu & Shen, 2016). These higher quality knowledge and skill profiles may lead to better decision-making, more effective and unique strategy execution (Field & Mkrtchyan, 2017), and more effective use of firm resources in a competitive environment. Empirical evidence supports the impact of CEO general ability on firm performance (Custodio et al., 2019; Kaplan et al., 2012; Lin et al., 2021; Oh et al., 2018). However, the influence of CEO general ability or managerial ability in general has not been widely studied in the context of firm CPA. In this study, we aim to address this gap by examining the effect of CEO human capital, defined as the various skills, abilities, and knowledge that a CEO accumulates over their career through various positions (Custodio et al., 2019), on firm lobbying breadth. We anticipate that, akin to the influence of CEO demographics (Rudy & Johnson, 2019), the human capital of CEOs, particularly their general ability, will play a pivotal role in shaping a firm’s engagement in CPA.

In addition to internal factors, the expectations and goals of the CEO may also shape a firm’s engagement in political activity (CPA). Research suggests that when a CEO’s performance falls either above or below their aspiration levels, it can influence the strategic priorities and decisions they make regarding both market and non-market strategies, as well as resource allocation (Kuusela et al., 2017; Lucas et al., 2018; Ref & Shapira, 2017; Vidal & Mitchell, 2015; Ye et al., 2021). CEOs with higher general ability often possess stronger networks of relationships and a diverse range of ties and experiences that have enriched their knowledge and improved their ability to navigate the market and identify opportunities (Custódio & Metzger, 2013). These individuals may be better equipped to exploit opportunities and achieve better performance for their firms through a focus on innovation and differentiation using the diverse skills and abilities they have developed throughout their careers (Custodio et al., 2019). Cao et al. (2015) also argue that CEOs with strong social and human capital, including general ability, may have a better understanding of the external environment, which is crucial in shaping the success of a firm’s strategy.

It is not yet clear whether CEOs with better general abilities, skills, and ties will engage more or less broadly in the political process. Previous research suggests that CEO political power resulting from political connections can have an impact on firm performance (Sun & Zou, 2021), and CEOs with strong human capital may be more sensitive to negative perceptions from external audiences, as this could threaten their future opportunities (Liu et al., 2017). Given the variation in CEO general abilities and network capital, it is likely that there will also be variation in the motivations of CEOs to engage in political lobbying. In this study, we focus on the role of performance feedback, or the evaluations that firms receive based on their performance, in shaping the strategic priorities of CEOs and their decision-making in the political environment. Research on firm behavior suggests that performance feedback, particularly positive or negative discrepancies from aspiration levels, can influence the subsequent behaviors and choices of firms (Ye et al., 2021). These evaluations serve as important frames that stimulate distinct reasoning and behavioral selections (Plambeck & Weber, 2009). We propose that the magnitude of the effect of general ability on firm lobbying behavior may differ, depending on the feedback and evaluations received by the CEO. Specifically, we argue that the varying levels of CEO general ability index will have a varying effect on firm lobbying, and this effect may be moderated by performance feedback.

Hypotheses

There is an increasing awareness among management scholars that the increasing complexity of the business landscape and the pressures from diverse stakeholders, such as shareholders and governments, have fueled interest in understanding how firms balance their market and non-market strategies (Derfus et al., 2008; Gomez-Carrasco & Michelon, 2017; Jo & Harjoto, 2014). Navigating such complexity may depend on the abilities and experiences of key organizational decision-makers like the CEO (Argote & Greve, 2007; Yi et al., 2020). These organizational leaders are working in an increasingly complex environment that necessitates a broader range of abilities and skills to address constant changes and competitive pressures, as well as stakeholders’ demands, and expectations (Kaplan et al., 2012; Lin et al., 2021; Oh et al., 2018; Wei & Ling, 2015; O’Connell et al., 2005; Lin et al., 2021).

The importance of the CEO as a key decision maker has been a central focus of upper echelons theory, which posits that organizations are often seen as a reflection of their CEOs and that CEOs are the most important decision-makers in an organization (Cyert et al., 1959; Hambrick, 2007; Hambrick & Mason, 1984). Research on the role of generalist CEOs in managing the complexities faced by organizations in today’s business environment suggests that effectively addressing competitive challenges and stakeholder pressures may require the CEO to identify and manage conflicts or competing pressures that arise when the firm is proactively engaging with and reactively adapting, to varied competitive and stakeholder pressures (Chatjuthamard et al., 2021; Custódio et al., 2013; Li & Patel, 2019).

The diverse abilities and varied experiences of CEOs play a crucial role in determining organizational decisions, particularly in complex environments (Argote & Greve, 2007; Yi et al., 2020). Generalist abilities, encompassing a wide range of skills and knowledge, are particularly crucial for CEOs to handle complex challenges and competing pressures (Chatjuthamard et al., 2021; Custódio et al., 2013; Li & Patel, 2019), but we do not expect to find that the relationship between CEO general ability and their political activities to be linear. First, CEOs with low general ability are often categorized as specialists, which means they have less exposure to external resources (Custódio et al., 2013; Custodio et al., 2019). Second, due to their narrow knowledge about the external environment and the ways in which different issues and stakeholders can impact their business, low general ability CEOs may struggle to develop effective strategies for engaging with policymakers and other stakeholders, or might not have the managerial discretion to do so (Li & Tang, 2010). As the general ability of CEOs begins to increase, we expect that their lobbying breadth will also increase. When CEOs are at the lowest levels of general ability, they may not be aware of the full range of government issues that could impact their firms, and therefore, they do not engage in extensive lobbying. As they gain experience, they become more aware of these issues and start to engage in broader lobbying. But as they continue to gain experience, they learn how to manage these issues more efficiently, so they start to focus their lobbying efforts. For that reason, at the highest levels, as general ability increases, the benefits of broader lobbying efforts, such as knowledge acquisition and stakeholder influence, start to diminish, while the costs associated with managing extensive lobbying strategies and the potential for cognitive overload and limited attention span begin to escalate. Consequently, high general ability CEOs will tend to strategically narrow their lobbying focus on the most relevant and impactful issues.

CEOs with high levels of general ability may be less inclined to participate in extensive lobbying activities across a wide range of issues. Unlike low general ability CEOs, those with high levels of general ability have developed a network of external connections and possess diverse experiences, which allow them to strategically select and focus their lobbying efforts on the most relevant and impactful issues (Custodio et al., 2019). Furthermore, their wide-ranging experiences and exposure enable them to skillfully choose and concentrate their lobbying efforts more precisely and effectively. Thus, high general ability CEOs can strategically direct their lobbying resources towards targeted issues, maximizing their impact and reducing the need for broader lobbying. This selective approach to lobbying enables high general ability CEOs to efficiently utilize their resources and expertise. In line with Haans et al. (2016), we argue that the incentives or driving forces for low general ability CEOs grow proportionally, while the costs or demotivation tend to increase rapidly as general ability increases for the CEO, leading to an inverted U-shaped relationship between CEO general ability and the firm’s lobbying breadth. As CEOs gain additional skills, advantages, perspectives, and access to influence over time, they may initially increase their lobbying breadth to capitalize on these gains. However, there is a point beyond which the benefits of broader lobbying efforts no longer outweigh the costs and complexities associated with managing them.

As the CEO’s human capital increases, their ability to manage more effectively and efficiently also improves, as they have accumulated diverse experiences in various positions and capacities. As lobbying efforts expand over time, it becomes increasingly likely that the CEO may be overwhelmed by managing such extensive endeavors, which may not necessarily yield additional value for the CEO or the firm. Furthermore, the CEO may become cognitively overloaded. As a CEO’s human capital increases, they are better able to manage a wider range of tasks and responsibilities. However, there may be a point where the CEO becomes overwhelmed by the sheer number of tasks they must handle, leading to cognitive overload. When this occurs, the CEO may struggle to effectively manage the organization’s lobbying efforts, which could result in a narrower lobbying breadth. In line with the concept of limited attention span, as CEO general ability increases, they may have a wider range of interests and responsibilities. However, there may be a point where the CEO’s attention span becomes limited, and they are not able to focus on all areas of the organization equally. If the CEO becomes too focused on lobbying breadth, they may neglect other important areas of the organization, resulting in a narrower lobbying breadth.

Regarding time constraints, as CEO general ability increases, they may face more demands on their time. However, there may be a point where the CEO’s time becomes limited, and they are not able to devote sufficient time to all areas of the organization. In such a situation, if the CEO becomes too focused on lobbying breadth, they may lack enough time to manage other important areas of the organization, ultimately resulting in a narrower lobbying breadth. In other words, the CEO’s general ability, or their cumulative human capital, is derived from two main sources: the positions, capacities and firm-specific knowledge they have accumulated over the years, and the industries in which they have served over the years. These experiences have a wide variety of dynamics and situations, all of which have unique and specific elements pertaining to the development of skills, situational knowledge and analysis, and a set of networks that allow the CEO to influence their firm positioning and the environment in which it competes. We suggest that there is an inverted U shape relationship. Our reasoning is built around several theoretical arguments embedded in the literature. As the CEOs knowledge and expertise increases, they may be better equipped to navigate the complex landscape of corporate political activity and then become more focused rather than lobbying widely with extensive use of firm resources. They may be more adept at analyzing political risks and opportunities, identifying key stakeholders, and developing strategies to achieve their desired outcomes. This concept aligns with literature on CEO knowledge and experience, CEO incentives and motives, and cognitive structure of the CEO. Additionally, CEOs with strong networks and relationships in the political sphere may be able to leverage those connections to advance their corporate political agenda without spending too much on lobbying by focusing on a select few that can achieve their goals. They cannot get to that point from day one in the office, and they need to build that network. They do so through the various positions and capacities they have served in previously. Once they achieve an optimum level of general ability and a wider network of ties, they may have access to policymakers, regulators, and other influential individuals, which can facilitate their efforts to influence public policy. CEOs with greater human capital and abilities might be more effective leaders and communicators, which allows them to mobilize their employees, customers, and other stakeholders to support the firm without the need for greater involvement in political lobbying. They may be able to build coalitions and alliances to amplify their message and increase their impact.

In summary, CEOs with limited human capital and networks may not prioritize broad lobbying due to restricted access to external information. As they gain experience, their lobbying efforts expand, but with growing expertise and resources, they may narrow their focus. CEOs with moderate general ability strategically allocate resources, emphasizing core competencies and high-return areas. The CEOs highest in general ability may narrow political lobbying to ensure coherence and relevance. Recent years have shown CEOs adapting their lobbying focus in response to the organizations needs, reinforcing the importance of these points (Abdurakhmonov et al., 2022). The literature indicates, that CEOs with high general ability are better at recognizing and capitalizing on opportunities, which can lead to the expansion of their companies. As a company expands, its complexity may increase and demand more resources for maintenance, which can lead to an increase in lobbying activity. Therefore, we would expect to see a positive relationship between CEO general ability and lobbying breadth, up to an inflection point. However, as a CEO’s general ability further increases, they accumulate more experience and establish a network of close allies. Consequently, this can result in a narrowed focus and reduced interest in lobbying activities.

In strategic management, firms assess their financial performance by comparing it to aspiration levels. Feedback on CEO performance is generated by comparing the actual financial performance to the aspiration level, and this information is used to influence the CEO’s subsequent market and non-market strategies, especially in actions that involve spending and risk-taking (Schumacher et al., 2020). An increasing body of research acknowledges the significant role that performance feedback plays in shaping CEO behavior (Fang et al., 2014; Wang et al., 2022; Ye et al., 2021). Specifically, recent studies indicate that performance feedback is especially important for CEOs as they use it to decide whether to update their preferences and adjust their temporal focus, which necessitates a certain level of information search and processing in a diverse information environment (Fang et al., 2014; Steinberg et al., 2022; Ye et al., 2021). This is particularly relevant for CEOs with generalist or specialist skill sets, as generalists and specialist skill sets has been shown to influence political success in other rolls (Brown & Harris, 2022). Prior studies, drawing upon upper echelons theory, have investigated the relationship between managerial characteristics and strategic decision-making (e.g., Helfat & Martin, 2015), however, fewer studies have concentrated on how these characteristics impact the breadth of nonmarket strategic decisions. According to social learning theory (Bandura, 1977), individuals learn by observing and imitating others. Within the scope of CEO behavior, social learning theory posits that a CEO’s decision to engage in lobbying activities is influenced by the feedback they receive regarding their firm’s performance. Drawing on self-efficacy theory (Bandura, 1977; Fuchs et al., 2019), we argue that a CEO’s confidence in their abilities, which is influenced by their level of human capital, may impact their lobbying behavior. Specifically, we propose that CEOs with moderate levels of human capital may view positive performance feedback as an indication that they have built an effective network of external resources through their lobbying efforts. Consequently, these CEOs might behave like high general ability CEOs and decrease their lobbying activities, believing that further efforts may not produce considerable benefits for the firm. Conversely, CEOs possessing lower levels of human capital might perceive negative feedback as a signal that their lobbying efforts have not been sufficient in creating external impact. As a result, these CEOs might be more inclined to persist in engaging in lobbying activities in an effort to improve the firm’s standing. This proposed model adds to the literature on the behavior of CEOs by highlighting the interplay between performance feedback and human capital, and the subsequent influence on lobbying behavior. The findings of this research imply that firms seeking to enhance their lobbying strategies ought to take into account the CEO’s level of human capital and tailor their feedback accordingly to encourage targeted and efficient lobbying efforts. Moreover, organizations may support the development of CEO human capital through training and development initiatives focused on improving skills such as strategic thinking, network building, and communication. In doing so, organizations can cultivate self-efficacy, confidence, and competence among CEOs, which can lead to more effective lobbying activities and, ultimately, enhance the firm’s performance in the non-market environment. Companies employ CPA to respond to changes in their external environment, especially in response to political and regulatory shifts. Highly regulated industries are known for high levels of CPA (Hillman et al., 2004) because firms want to have a say in pertinent policy discussions when the government plays a significant role in regulating their industry (Brown et al., 2020). In addition to using CPA to respond to base levels of regulation, Brown et al. (2020) found that firms increase CPA due to annual changes in regulation. However, firms must be careful not to overspend on CPA, as this can lead to diminishing returns. Excessive spending on CPA might lead to competitors taking advantage of the situation without contributing through free-riding (Brown et al., 2019; Lenway & Rehbein, 1991; Olson, 1965) or necessitate trade-offs with other spending priorities due to limited cash on hand (Brown et al., 2020). Additionally, CEO general ability is associated with risk and innovation (Chatjuthamard et al., 2021; Lin et al., 2021), which means CEOs with such abilities prioritize market-focused actions. When performance feedback is positive, then the CEO has greater confidence in their actions and are likely to maintain their temporal focus (Custodio et al., 2019). Performance feedback is an important indicator of the CEO’s and the firm’s performance, and it is frequently utilized by analysts, shareholders, and the business media to evaluate the performance of the CEO (Chen et al., 2022; Wang et al., 2022). Empirical evidence suggests that performance feedback has a significant effect on the firm’s subsequent strategic behavior (Ertac et al., 2019; Jiang & Holburn, 2018; Schumacher et al., 2020). The impact is especially notable in market and non-market strategies involving considerable expenditure and resource allocation, such as internationalization (Jiang & Holburn, 2018), communications and marketing efforts (Wang et al., 2022), and R&D investments (Lucas et al., 2018). For CEOs depending on political lobbying as a way of compensating for their insufficient human and social capital beyond the firm’s boundaries, we expect that the more favorable the feedback received, they are less likely to allocate substantial resources to broader CPA in subsequent years. This is consistent with existing literature, which suggests that shifts in CEO and firm priorities and focus are likely to stem from either positive or negative feedback. Although we anticipate that CEO ability will have an inverted-U shaped relationship with lobbying breadth, we believe that a firm’s performance feedback will moderate this relationship such that the curve becomes flatter. This implies that favorable feedback for the CEO results in a reduced need for CPA among CEOs positioned in the middle range of managerial abilities. CEOs in this range typically invest most heavily in broad CPA efforts across various governmental bodies and legislative initiatives, but favorable performance feedback can prompt a reevaluation of their strategic priorities and diminish the firm’s reliance on extensive governmental connections and investments.

Method

Sample and Data

To collect data for our study, we began with a sample of 33,208 firm-fiscal year observations over the period 1992–2016, which we obtained from a combination of the CEO General Ability Index (GAI) database (Custodio et al., 2019) and the Standard & Poor’s Execucomp database, as well as the corporate financial information from Compustat North America Fundamental Annual. To construct our final dataset, we collected CPA data for all firms in the Compustat database and merged it with federal CPA data obtained by searching Opensecrets.org, using the fiscal year as the matching criterion. This resulted in a sample of 32,765 observations covering the same period. Next, we added governance data from GMI, using the CUSIP and calendar year starting in 2003, resulting in 15,691 firm-fiscal year observations over the period 2003–2016. Our moderator variables required information over a four-year period (current year plus previous 3 years), and we excluded any firm-year observations with missing data for our research variables. Our final unbalanced panel dataset thus comprises of 9,356 firm-fiscal year observations with 1,548 unique firms from 2006 to 2016, identified by their two-digit Standard Industrial Classification (SIC) codes.

Variables and Measurements

Dependent Variable

To capture the breadth of a firm’s lobbying efforts, we followed Ridge et al. (2017) measure of lobbying breadth by counting the number of federal agencies and legislative acts a firm lobbied each year. This measure allows us to see how far reaching the firm’s political activities are across a variety of issues and policy areas within the political landscape.

Independent Variable

CEO ability is measured following (Custodio et al., 2019; Custódio & Metzger, 2013). We use the general ability index (GAI) developed by Custódio et al. (2013). These authors provide a comprehensive index which captures a CEO’s human capital and abilities that the CEO develops over their years of experience in various capacities. The GAI of CEO i in year t is defined as

Moderator Variables

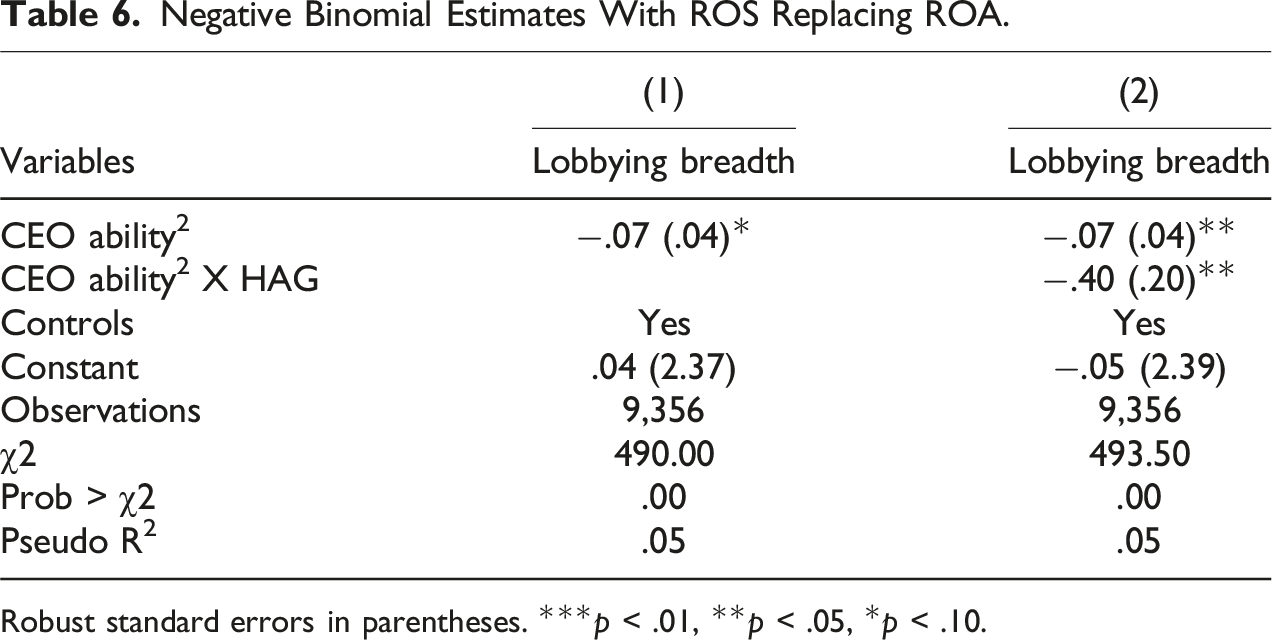

Our moderator variable is a firm’s performance relative to aspirations. According to the Behavioral Theory of the Firm (BTF), managers compare actual corporate performance with two types of aspirations: historical and social (Borgholthaus et al., 2021). Managers consider the aspiration level as the minimum satisfactory performance (Borgholthaus et al., 2021; Schneider, 1992), which shows whether the current performance is a success or failure (Borgholthaus et al., 2021). We follow a multistep process to create the moderator variables, historical aspiration gap (HAG), social aspiration gap (SAG), negative historical aspiration gap (NHAG), negative social aspiration gap (NSAG), positive historical aspiration gap (PHAG), and positive social aspiration gap (PSAG). ROA is a common corporate performance measure in the existing performance feedback literature (Borgholthaus et al., 2021; Gaba & Joseph, 2013). ROA is defined as operating income after depreciation scaled by total assets (Borgholthaus et al., 2021). Following the literature, we include two measures of aspiration levels: one with respect to a firm’s own performance, historical aspiration, and another compared to its peers in the same industry, social aspiration, while keeping historical and social aspirations separate (Gaba & Joseph, 2013; Lim & McCann, 2014; Miller & Chen, 2004). A firm’s performance feedback is the difference between its own performance and either historical or social aspiration levels (Lim & McCann, 2014). Following Vidal & Mitchell (2015), we construct the

Control Variables

We include several CEO characteristics, firm features, and industry factors that may control a firm’s lobbying breadth. CEO age and tenure are influential factors determining a firm’s strategic moves (Rudy & Johnson, 2019). Hence, we include age and tenure as natural logarithm of actual age in year and years serving as a CEO at the current company. A CEO’s political perspective may be influenced by gender, motivated by the founder status, and affected by a CEO-board chair duality (Aggarwal et al., 2012). So, we include three binary variables – one for female CEOs, another for founder CEOs, and a third for CEOs who also serve as the Chairman of the Board. Board size, natural logarithm of total number of directors, is found to act upon corporate political activities (Aggarwal et al., 2012). Following Rudy & Johnson (2016), we include firm age, calculated as the natural logarithm of the number of years since a firm first appeared in Compustat, as it is found to be related to reputation and political experience (Baron, 1995; Boddewyn & Brewer, 1994; Hillman & Hitt, 1999). Lobbying requires resources that are scarce to a firm. Due to the availability of more such resources, larger firms may be able to afford broader lobbying efforts. Hence, we control for firm size, represented by the natural logarithm of the number of employees (Brown et al., 2020). We chose this measure of firm size to avoid multicollinearity issues that might arise from using other financial measures scaled by assets or sales (Arora & Dharwadkar, 2011).

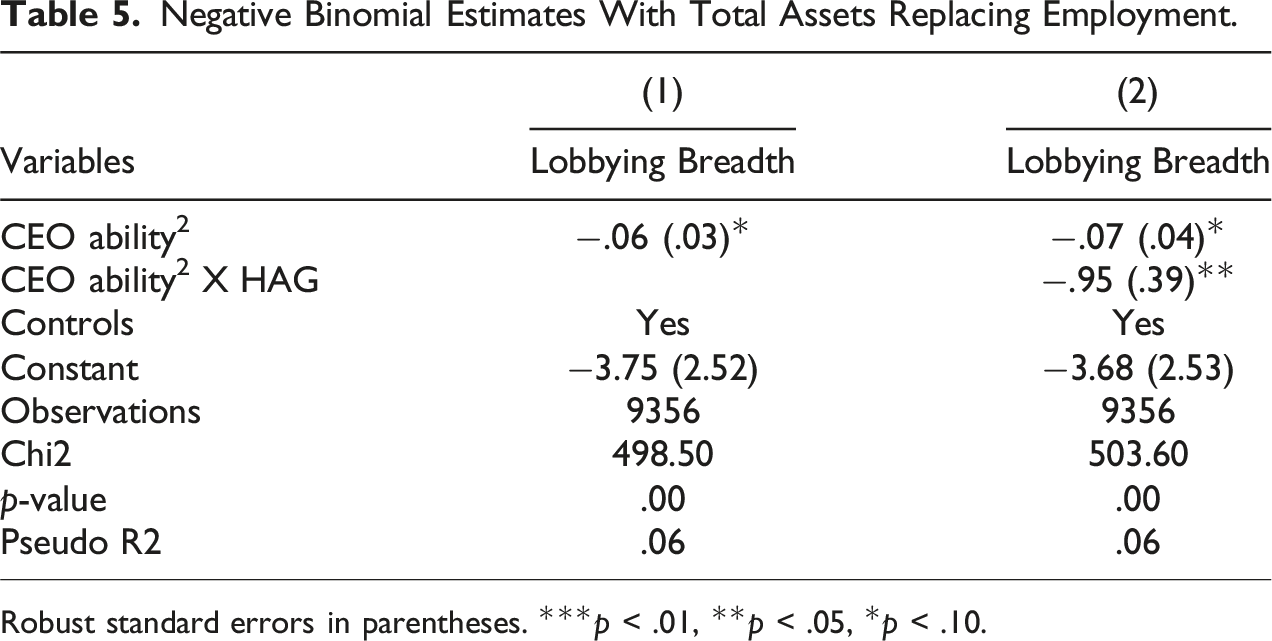

Additionally, we also test our hypotheses using the natural logarithm of total assets as an alternative proxy for firm size in robustness check section (Aggarwal et al., 2012; Rudy & Johnson, 2016; 2019). Slack is an essential resource enabling firms to engage in political actions (Brown et al., 2022; Rudy & Johnson, 2016, 2019). We create a slack index following Bourgeois and Singh (1983). The quick ratio, capital investments, and equity-to-debt ratio serve as proxies for available, recoverable, and potential slack (Daniel et al., 2004). Our slack index is the sum of these standardized proxies (Rudy & Johnson, 2016, 2019). We also include an alternative slack measure, cash and short-term investments scaled by total assets, for robustness check of our results (Brown et al., 2018). R&D spending is related to corporate political activities (Aggarwal et al., 2012; Brown et al., 2022). We control for R&D intensity, measured as R&D spending scaled by total assets, in all our regressions. An alternative measure of R&D intensity, R&D spending scaled by net sales, is used in the robustness check (Rudy & Johnson, 2016). We include industry concentration and regulations to control for industry effects (Brown et al., 2020; Brown et al., 2018). Industry concentration is calculated as the sum of squared market shares for firms in each industry, defined at the two-digit SIC level. As alternatives, we use three-digit SIC codes (Rudy & Johnson, 2016, 2019), four-digit SIC (Brown et al., 2020; Brown et al., 2018), and Fama-French SIC (Aggarwal et al., 2012) and report the results in the robustness check section. We controlled for whether or not the firm was in a regulated industry by using a binary variable which equals 1 if a firm belongs to either utility or financial sector and 0 otherwise. The trend variable captures macroeconomic impacts, set at 1 for the first year and incremented by 1 for each subsequent year (Brown et al., 2018).

Analysis

Existing literature suggests the use of count models when using a count dependent variable (Brown et al., 2018; Custódio et al., 2019; Vidal & Mitchell, 2015). We apply a negative binomial model with firm-level clustering (De Meulenaere et al., 2021; Lee et al., 2018) because the dispersion parameter alpha is found to be statistically significant along with Deviance and Pearson goodness-of-fit 124715.2 and 208686, respectively, significant at .1%, indicating the appropriateness of the negative binomial model over the Poisson model. More specifically, we estimate equation (1) to test our first hypothesis and equation (2) to test our second hypothesis —

Results

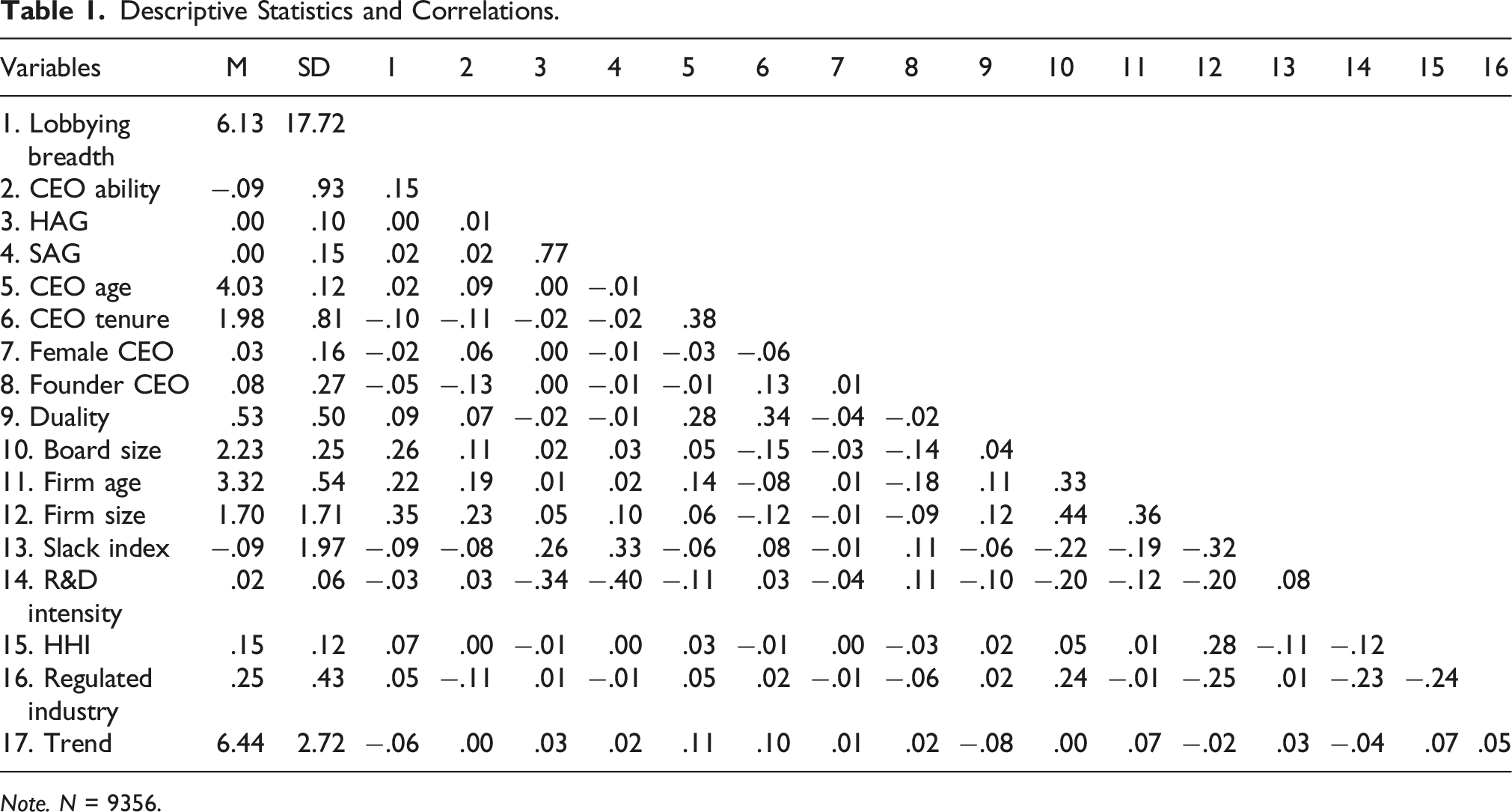

Descriptive Statistics and Correlations.

Note. N = 9356.

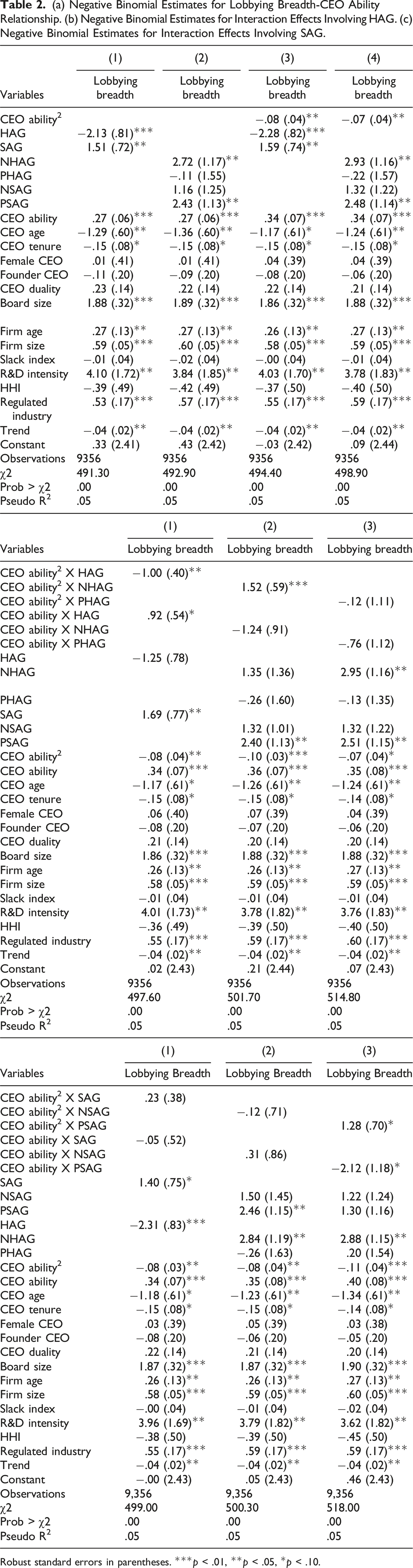

(a) Negative Binomial Estimates for Lobbying Breadth-CEO Ability Relationship. (b) Negative Binomial Estimates for Interaction Effects Involving HAG. (c) Negative Binomial Estimates for Interaction Effects Involving SAG.

Robust standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

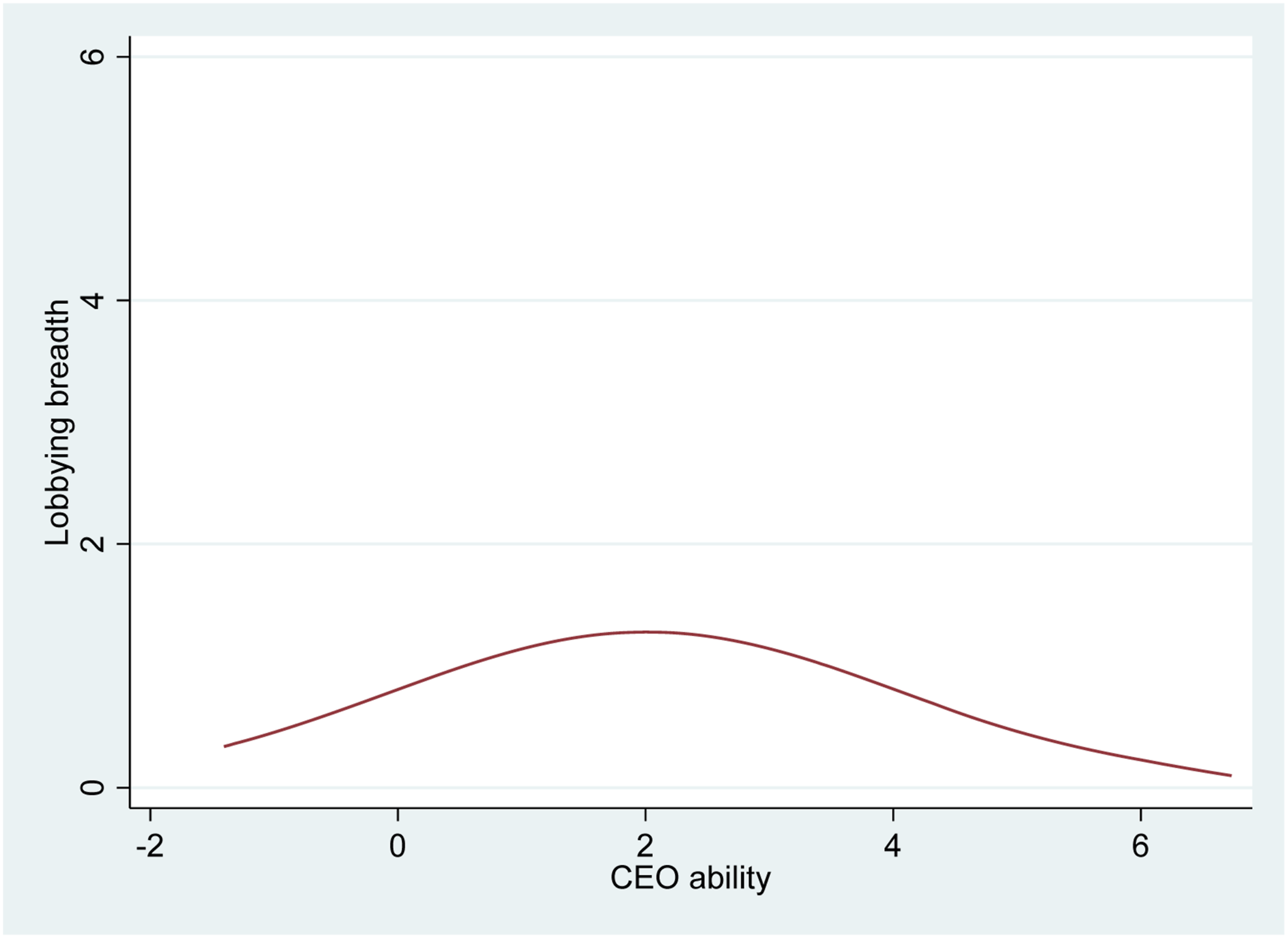

We test our main hypothesis about an inverted U-shape relationship between CEO ability and lobbying breadth in Model 3 and Model 4 by estimating equation (1). Model 3 and Model 4, similar to Model 1 and Model 2, incorporate 2 and 4 moderators, respectively. In support of this hypothesis, CEO ability yields statistically significant negative and almost identical coefficients (β = −.08, p = .04 in Model 3 and β = −.07, p = .04 in Model 4) in both models (Antonakis et al., 2017). Using Model 3, we plot the relationship (after natural logarithmic transformation of one plus lobbying breadth to enhance the prominence of the curvilinear relationship) graphically in Figure 1, which reflects initial elevation in a firm’s lobbying breadth with rising CEO ability. However, after reaching a peak, further expansion in CEO ability reduces it. The curve is flat or the slope is zero at a value of Lobbying breadth – CEO ability relationship.

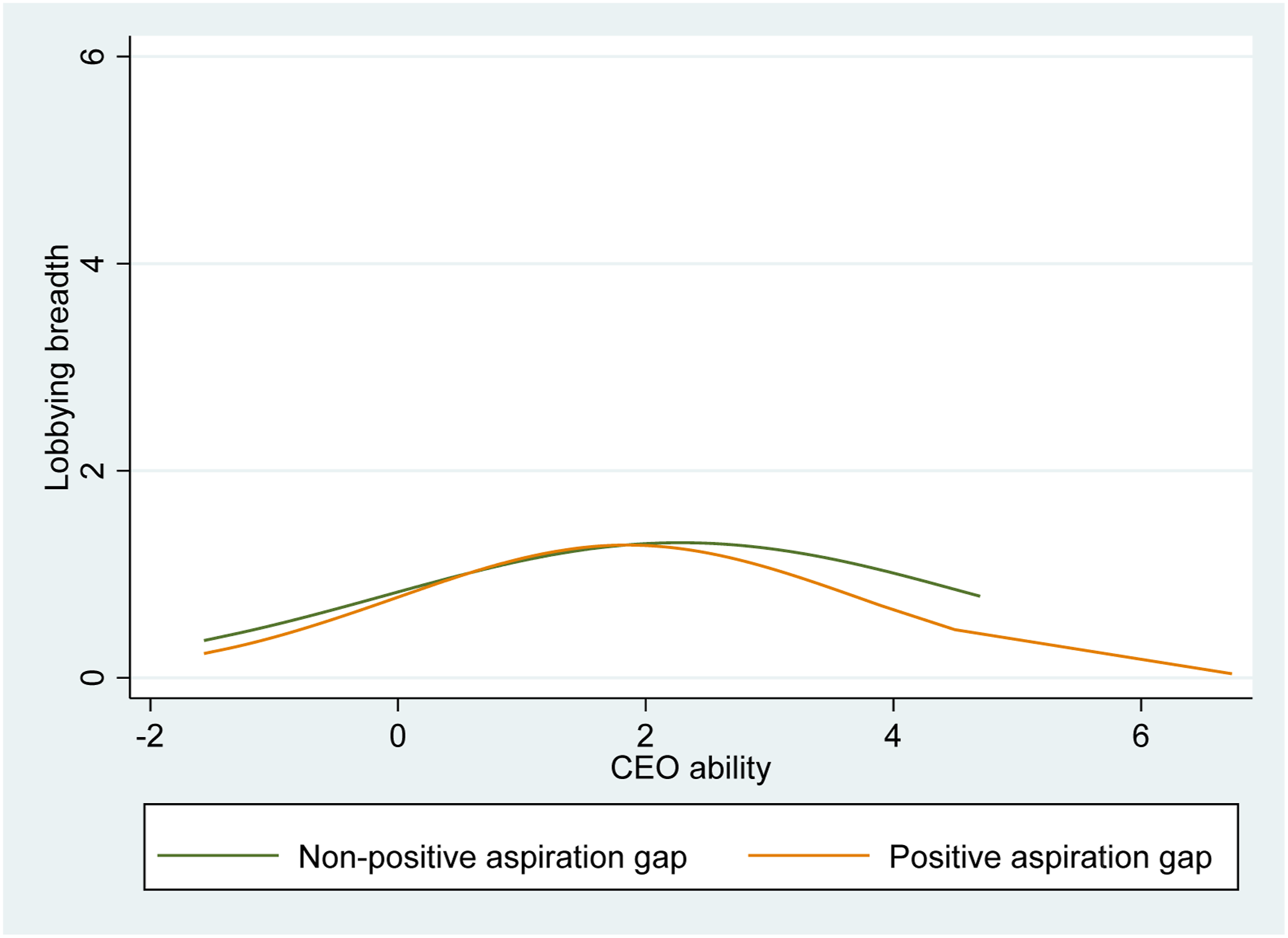

We estimate equation (2) using data in Table 2. Historical aspiration gaps are the moderators in Table 2, while social aspiration gaps serve as moderators in Table 2. Model 1, Model 2, and Model 3 test whether a firm’s HAG, NHAG and PHAG moderate the lobbying breadth-CEO ability relationship, respectively, in Table 2. The interaction terms in Model 1 reveal that HAG negatively moderates the lobbying breadth – CEO ability relationship, indicated by a statistically significant negative coefficient (β = −1.00, p = .01). Although a strong positive moderation (β = 1.52, p = .01) role is observed in case of NHAG, PHAG yields a weak negative moderation (β = −.12, p = .91). This indicates that firms with worse HAG are more inclined to engage in lobbying. Thus, similar to Figure 1, we plot Model 1 from Table 2 graphically in Figure 2. In this case, we set HAG to 1 if current performance is better than past trends and to 0 otherwise. The figure reveals that firms with HAG = 0, indicating equal or poorer current performance compared to previous periods, engage in more lobbying compared to other counterparts, especially for those with low and high CEO ability levels. The turning point of the curve is dependent on the CEO ability value calculated by Interaction effect on lobbying breadth – CEO ability relationship of historical aspiration gap.

Similarly, in Table 2, Model 1, Model 2, and Model 3 test whether a firm’s SAG, NSAG, and PSAG moderate the lobbying breadth-CEO ability relationship, respectively. Unlike HAG, SAG in Model 1 produces a statistically weak coefficient (β = .23, p = .55), indicating its non-moderating role in the lobbying breadth-CEO ability relationship. In Table 2, NSAG and PSAG, when serving as moderators, yield negative (β = −.12, p = .87) and positive (β = 1.28, p = .07) coefficients in Model 2 and Model 3, respectively. These results from Table 2 indicate that SAG plays a less significant role in moderating the lobbying breadth-CEO ability relationship compared to HAG, thereby highlighting the importance of understanding the differential effects of historical and social aspiration gaps in shaping corporate lobbying behavior.

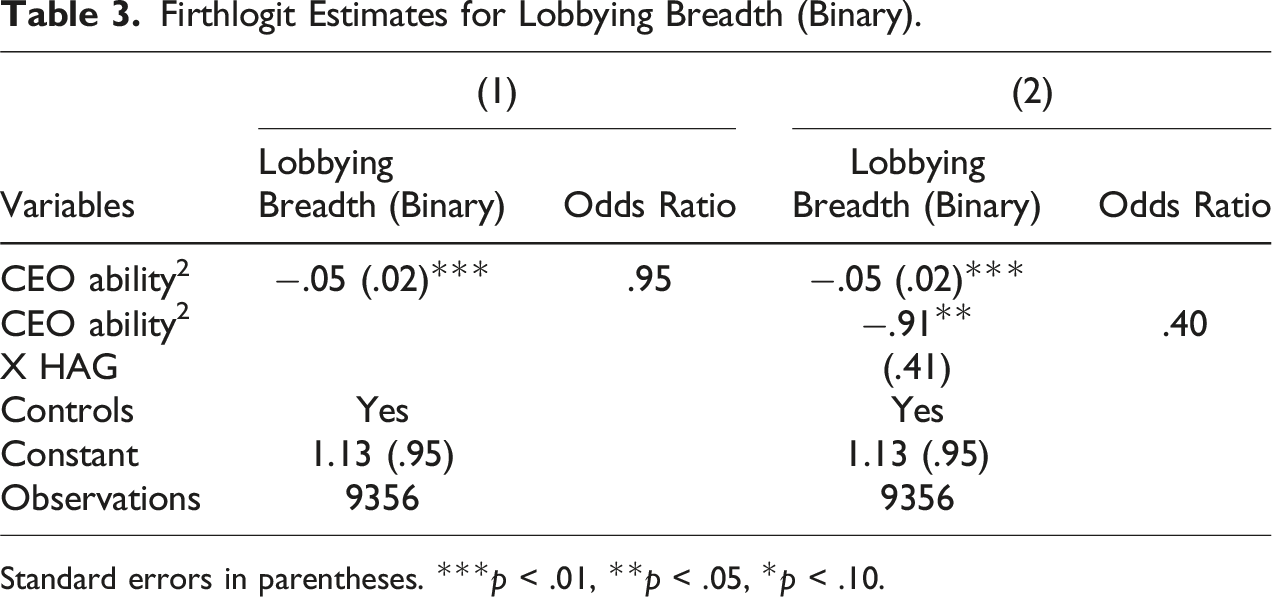

Robustness

In this section we focus on two already found statistically significant relationships in Table 2, namely the curvilinear relationship between lobbying breadth and CEO ability and HAG’s moderation in the link.

Firthlogit Estimates for Lobbying Breadth (Binary).

Standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

Residual Estimates for Lobbying Breadth.

Standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

Negative Binomial Estimates With Total Assets Replacing Employment.

Robust standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

Negative Binomial Estimates With ROS Replacing ROA.

Robust standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

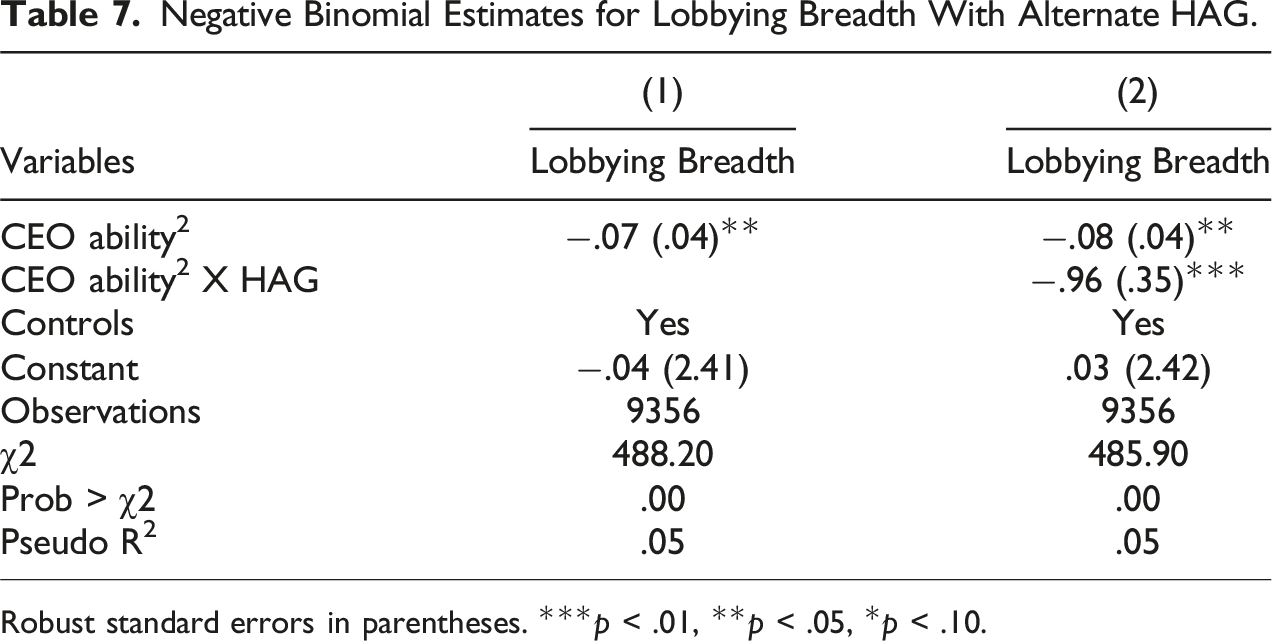

Negative Binomial Estimates for Lobbying Breadth With Alternate HAG.

Robust standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

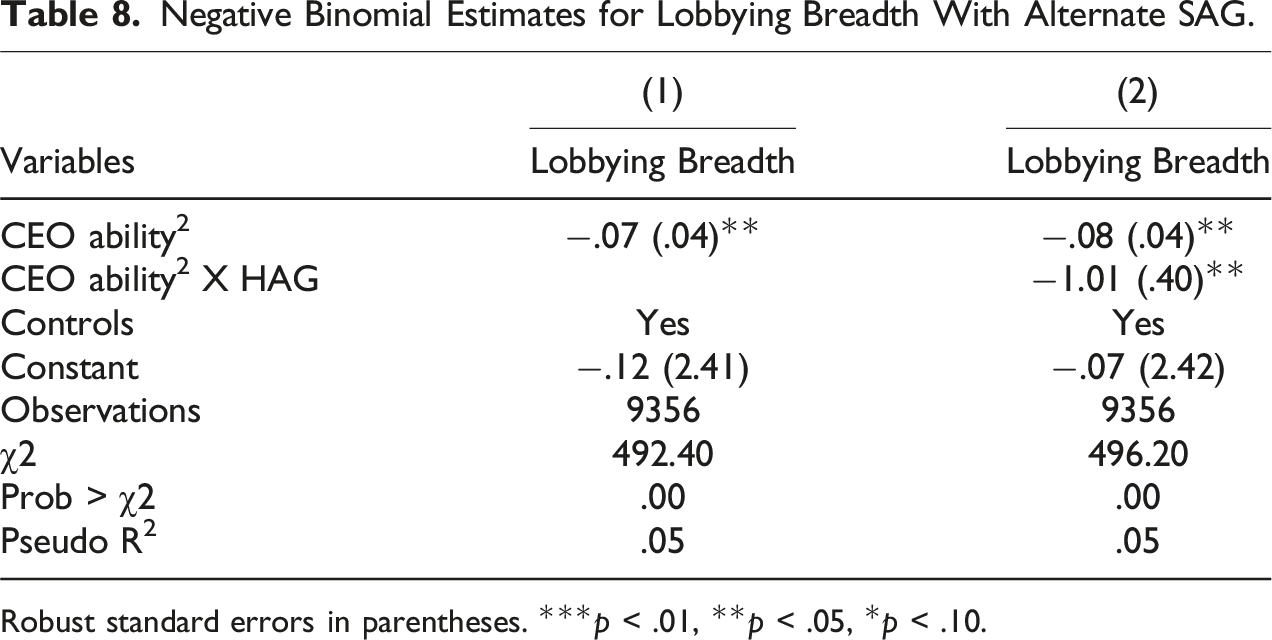

Negative Binomial Estimates for Lobbying Breadth With Alternate SAG.

Robust standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

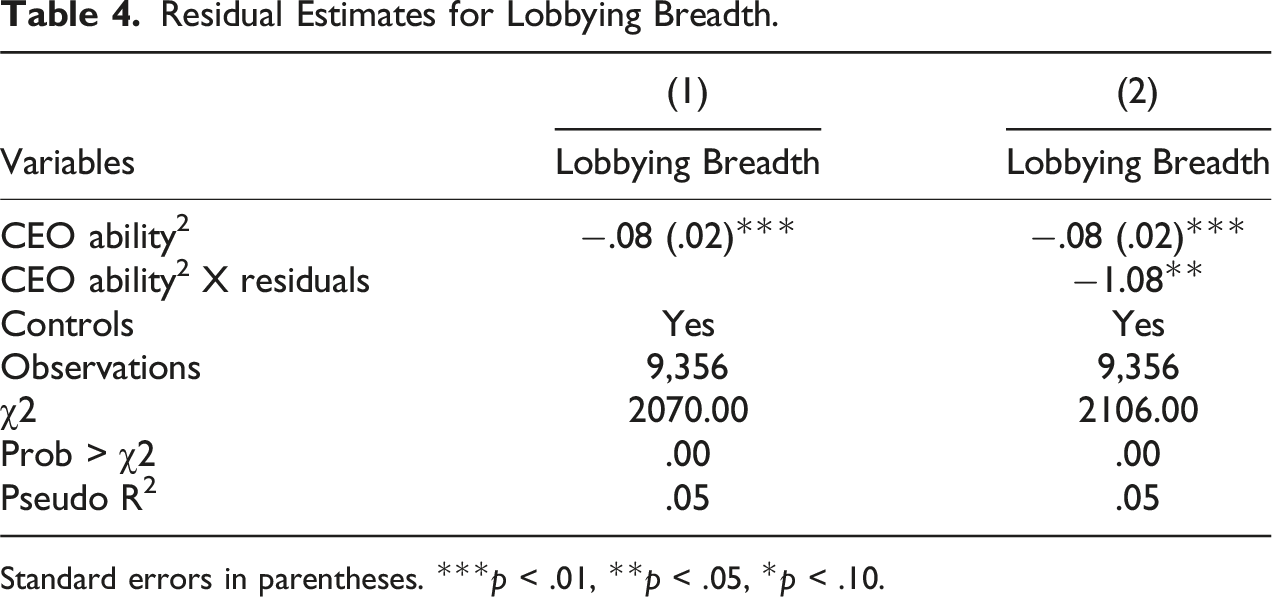

Endogeneity

We sought to ensure that endogeneity related to CEO ability, our independent variable, does not bias our results. Endogeneity issue occurs due to presence of unobserved heterogeneity, simultaneity bias, and/or sample selection bias (Liu et al., 2021). Lobbying breadth may depend on some unobserved factors like corporate culture that remains uncontrolled in a regression due to unavailability of an appropriate proxy, which makes results susceptible to omitted variable bias. Although it is difficult to establish a theoretical basis for the influence of lobbying breadth on CEO ability, we conducted robustness checks to rule out the possibility of reverse causality. Lastly, a firm’s CEO hiring decision with certain ability may drive its lobbying breadth, which may, in turn, determine whether a firm’s CEO ability is observed in the sample. In other words, we address whether our sample suffers from incidental truncation.

First, we examine the impact threshold of a confounding variable (ITCV) to evaluate potential endogeneity issues that could arise due to omitted variables (Frank, 2000) because ITCV is appropriate for any maximum likelihood estimation (Busenbark et al., 2022). As expected, given the positive correlation between dependent and independent variables, the test reveals that an omitted variable must produce a minimum correlation coefficient of .23 with the dependent and independent variables to alter the inference. Hence, observing firm size as the single factor with such a strong connection with both of the variables in Table 1 and assuming the appropriateness of our incorporated controls, we conclude that endogeneity due to omitted variables is unlikely here (Oliver et al., 2018).

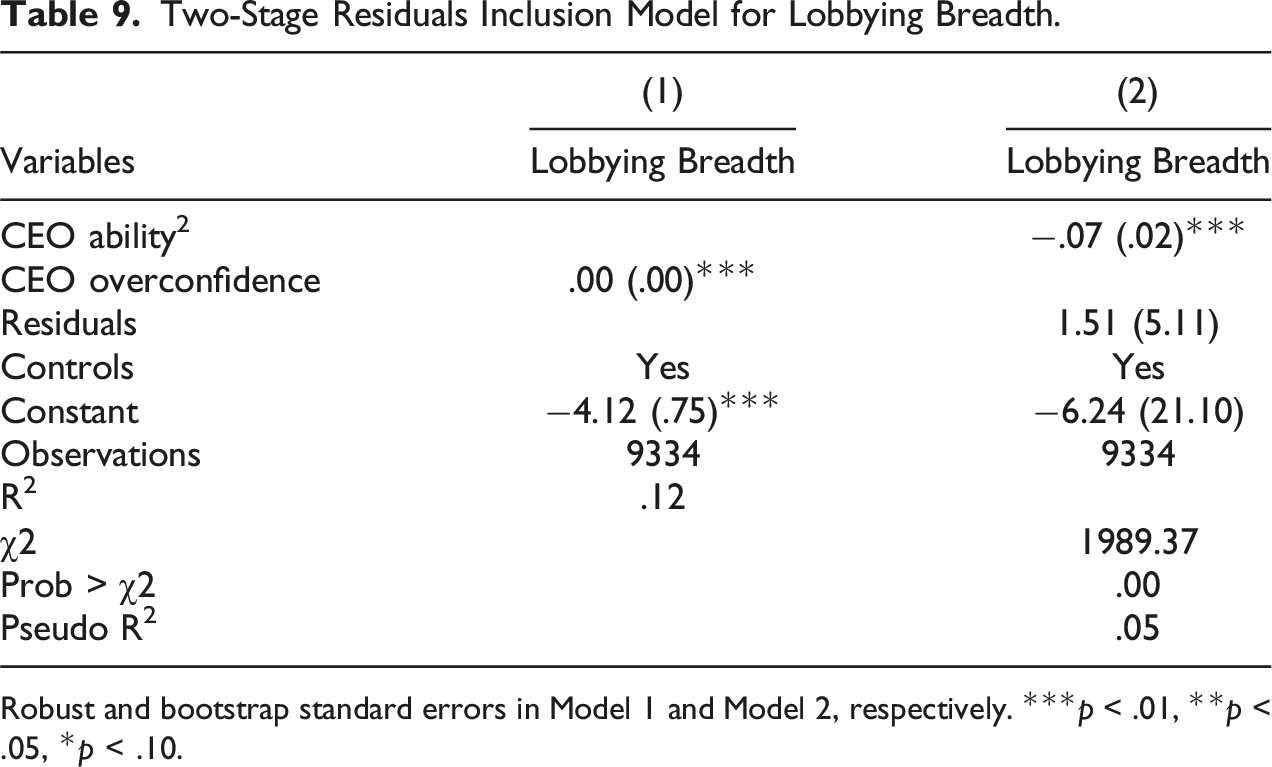

To address endogeneity concerns stemming from omitted variables or simultaneity, the instrumental variable approach can be employed, provided there is at least one valid instrument available (Hill et al., 2021). We use CEO overconfidence as an instrumental variable. Retention of more unexercised exercisable options reflects a CEO’s overconfidence in the firm’s future (Malmendier & Tate, 2005, 2008). Using data from Execucomp, we measure overconfidence as the annual value of the CEO’s holdings of vested, in-the-money options, scaled by the CEO’s total salary and bonus (Dezsö & Ross, 2012; Lee et al., 2017). A CEO’s overconfidence at a firm should not have an impact on corporate lobbying breadth due to the strategic nature of lobbying decisions.

The effective F statistic of Montiel-Pflueger robust weak instrument test is 56.127 exceeding the critical value of 37.418 at 5% confidence level, suggesting statistical strength, validity, and relevance of the instrument in this study. Our results cannot reject the nulls of Davidson-MacKinnon test of exogeneity (test statistics = .10; p = .76), reaffirming our belief in absence of concerning level of endogeneity.

Two-Stage Residuals Inclusion Model for Lobbying Breadth.

Robust and bootstrap standard errors in Model 1 and Model 2, respectively. ***p < .01, **p < .05, *p < .10.

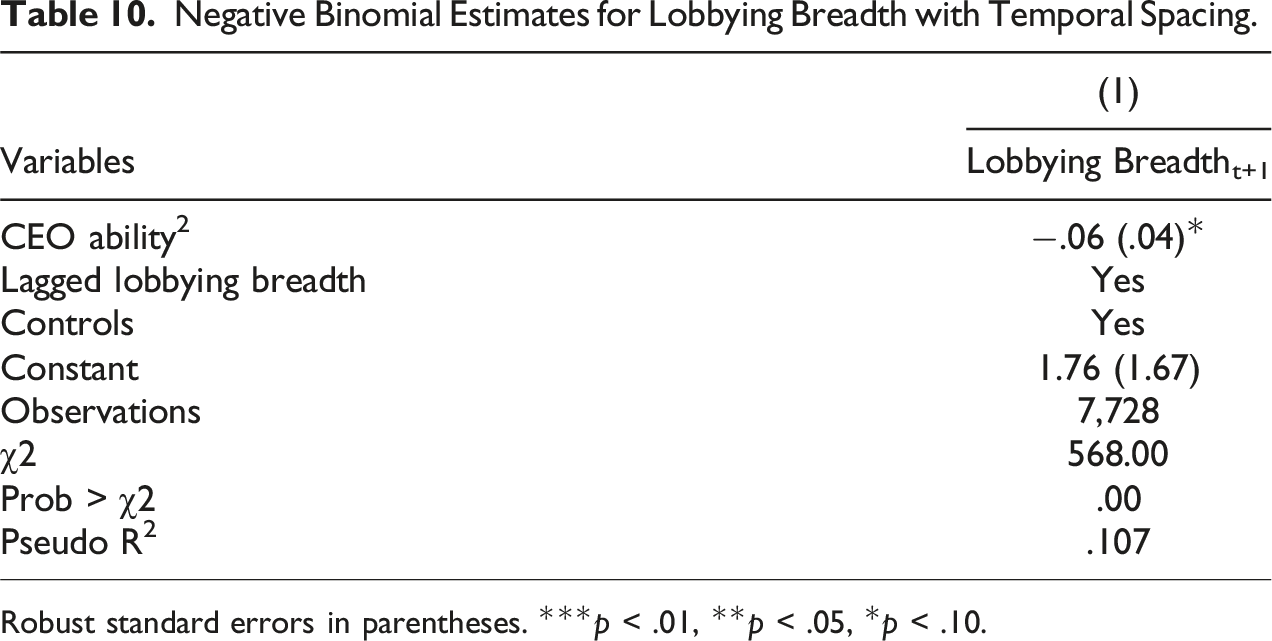

Negative Binomial Estimates for Lobbying Breadth with Temporal Spacing.

Robust standard errors in parentheses. ***p < .01, **p < .05, *p < .10.

Incidental truncation results in sample selection (Certo et al., 2016). This is probable if lobbying breadth remains unobserved for firms with CEO ability under certain threshold. However, political markets are auction markets with the largest firms dominating the giving and obtaining most of the benefits to CPA. Hence, it is safe to assume that firms without positive lobbying breadth have 0 lobbying breadth (Brown et al., 2022). In other words, our sample does not suffer from truncation because both lobbying breadth and CEO ability are observed for all firms. Therefore, our sample analyses are generalizable to the entire population.

All aforementioned endogeneity check techniques include the HAG and SAG. Even after replacing the variables with NHAG, NSAG, PHAG, and PSAG, the results remain valid.

Discussion

Our study identified an inverted U-shaped relationship between CEO ability and lobbying breadth, where lobbying breadth initially increases with rising CEO ability but decreases at higher ability levels. This suggests that CEOs with moderate levels of human capital engage in broader lobbying than those with higher levels of ability, who may be more reliant on their human capital to succeed. Conversely, CEOs with lower ability levels may engage in narrower lobbying that moderate general ability CEOs due to a lack of awareness of the political options available to them. Additionally, our findings indicate that firm performance feedback moderates this relationship, as more positive feedback leads to a flatter curve. These findings suggest that CEO ability and firm performance jointly impact a firm’s propensity to pursue broad lobbying efforts.

Corporate political activity research has mixed results in determining the effects of CPA on firm performance (Hadani et al., 2017). Some studies find a positive relationship between CPA and performance while others find negative or no relationship. While contextual variables, such as the amount of regulation in a given firm’s industry, have explained both firm’s willingness to engage in CPA (Brown et al., 2020) and the firms return on CPA (Hadani & Schuler, 2013) how a firm lobbies and heterogeneity in the firm level variables have received little attention. Our study suggests that the CEO’s general ability is highly influential in how broadly they choose to lobby, and that this relationship is curvilinear. In addition, the firm’s capacity to achieve its financial aspirations serves as a moderating factor in this relationship These results suggest that while CPA is important, both the financial context the firm finds itself in as well as the ability of the CEO will influence how firms choose to interact with government actors.

Prior research has documented that CEOs with greater ability and skills portfolios receive higher compensation (Custódio et al., 2013). This higher compensation is a result of their greater number of skills and abilities that they have developed over time and that firms can benefit from. Such a portfolio of skills and abilities comes from the various positions, capacities, experiences, and industries in which they have previously served (Custodio et al., 2019; Custódio & Metzger, 2013). Firms are willing to pay such high compensation for CEOs with a higher general ability index because they would like to benefit from their experiences for formulating and implementing effective strategies in both market and nonmarket domains. While prior studies have heavily focused on the relationship between CEO characteristics in general and the firm’s political activities, very few studies have examined whether those CEOs with greater abilities and skills will show different behavior with regard to the firm’s political activities. The present study takes this line of research a step further by examining the relationship between CEO general ability index and the firm’s political lobbying. Furthermore, we provide arguments that show that the relationship is non-linear and that different levels of the general ability index may result in different political activity orientations.

Such arguments are important for two reasons. First, prior research has mostly considered the conventional arguments regarding the effects of the CEO’s ability and firm-level behavior. These conventional beliefs may have contributed to the mixed evidence concerning the shape and form of firm’s political behavior and the consequences of such behavior. Second, CEOs with different levels of skills, experiences, and abilities have different situational circumstances they face within and outside their firms. Such differences create a window for different interpretations of the firm’s situations and different prioritization processes that will ultimately lead to different emphases. Such insights take this research a step further towards disentangling the differential effects of different CEO and firm-level characteristics on the balance between firm’s market and nonmarket strategies. We think that future research can and should look more closely at the various implications of the Upper Echelons characteristics and how they shape the firm’s optimal distinctiveness within a single policy (Taeuscher & Rothe, 2021; Zhang et al., 2020; Zhao et al., 2017) or across different policies that focus on the firm’s market and nonmarket strategies.

Furthermore, the recent literature has focused on whether and to what extent external versus internal factors can affect the firm’s optimal distinctiveness within a single policy or across policies. By bringing in two important and highly relevant variables (CEO general ability index and performance feedback), our study provides a first step for future studies to further take this important line of research. Strategic management literature has consistently been concerned with the magnitude of the effects that external and internal factors exert on the firm’s policies and prioritization processes. We believe that further research is needed to fully understand these dynamics in the context of upper echelons-market and nonmarket strategies decision-making.

Limitations and Future Research

Like much of the corporate political activity research, we have focused on federal lobbying efforts. Focusing solely on federal lobbying without also studying state lobbying may be limiting for two reasons. First, state governments often have significant power and influence, particularly in areas such as education, healthcare, and transportation. As a result, issues that are crucial to businesses may be more effectively addressed at the state level rather than the federal level. By only studying federal lobbying, researchers may overlook valuable opportunities for businesses to engage in political activity and may underestimate the potential impact of state-level policies on businesses. Second, the political landscape at the state level can be very different from that at the federal level. State governments might be more receptive to certain types of lobbying, or may have different priorities and concerns than the federal government. As a result, the strategies and tactics that are effective at the federal level may not be applicable or effective at the state level. By only studying federal lobbying, we are unable to adequately understand the nuances of the state-level political landscape and we have an incomplete picture of the breadth of a firms lobbying activities.

In addition, we acknowledge that the Generalist Ability Index (GAI) is an imperfect proxy for CEO ability. While it provides a quantifiable measure of the breadth of a CEO’s experiences, it does not capture other critical components of ability such as decision-making skills, leadership qualities, creativity, or the ability to inspire and motivate employees. There may be a discrepancy between the GAI and a CEO’s actual ability to manage complex situations and make strategic decisions, which are key aspects of CEO performance that are not directly captured by the GAI. Future research should use more direct measures of CEO general ability. Future research could benefit from using a more comprehensive or direct measure of CEO ability that takes into account both the breadth and quality of a CEO’s experiences as well as other dimensions of ability.

There are several areas for future research to further explore the complex relationships between CEO characteristics and CPA. Recent studies suggest that CEO personality traits have significant effects on the CEOs’ interpretations of the evaluations they receive and the choices they make in response to strategic issues (König et al., 2020; Schumacher et al., 2020). These include the potential impact of CEO personality and political ideology on CPA, as well as the interplay of performance feedback and responses from peer firms and CEOs on the relationship between CEO general ability and CPA. The findings of the present study indicate that the pursuit of generalist versus specialist CEOs may have some important implications for the firm’s non-market strategies, but additional research is needed to examine whether this also holds true in other non-market strategies (CSR) or in the market domain Al-Shammari et al. (2022). Additionally, the question of whether CEOs with better general abilities and certain personalities demonstrate different political behavior in response to positive/negative aspirations remains to be explored. While our study makes a modest contribution to the literature on CPA, there may be other external and internal contextual factors that influence how and why firms engage in CPA, and it would be valuable for future research to consider these factors as well. Finally, future research should examine the qualitative aspects of corporate aspirations more closely by examining the influence of 'aspirational talk’ in shaping a firm’s strategic behavior. This would enrich our understanding of how expressed corporate aspirations impact managerial decision-making and strategic planning processes, thereby providing new insights into the dynamics of performance feedback.

Conclusion

Current CPA literature lacks significant understanding of both external and internal contextual factors that influence how and why firms engage in CPA activities. Our results make a modest contribution to the literature suggesting that performance aspirations and CEO ability influence how narrow or broad a firm’s engagement in CPA can be. In addition, we find that these relationships are not linear in nature, but rather they vary between low, mid, and high levels of managerial general ability. We humbly suggest our study serves as a starting point in highlighting the nuanced nature of firm lobbying breadth.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author Biographies

Associate Editor: Curt Moore