Abstract

Diversification strategies remain a focal point in strategic management, yet conflicting findings persist regarding the relationship between diversification and performance. This paper intends to disentangle these conflicting findings by examining the role of CEO’s human capital in shaping firm strategy and performance within the context of related and unrelated diversification. Drawing on matching theory and the upper echelons literature, performance implications of diversification types depend on the alignment between CEO’s human capital and chosen strategy. Empirical analysis, based on Fortune 500 CEO appointments between 2000-2020, uses OLS regressions with random effects and Two-Stage Least Squares (2SLS) regressions. The findings reveal that outsider CEOs are negatively associated with related diversification, career variety is negatively associated with related and positively with unrelated diversification, and the fit between outsider status and diversification strategy determines firm performance. The findings contribute to the ongoing discourse on diversification, CEO characteristics, and their intricate interplay in influencing organizational outcomes.

Keywords

Introduction

Diversification strategy remains a central topic in strategic management research due to its significant implications for firm performance (Picone & Dagnino, 2016). Firms diversify through related or unrelated product expansion, each requiring distinct managerial capabilities and resource allocations (Picone & Dagnino, 2016). Despite decades of research, scholars continue to debate the impact of diversification on firm outcomes, highlighting the need to understand the underlying mechanisms that shape these strategic choices (Benito-Osorio et al., 2012; Gyan et al., 2017; Le, 2019).

Understanding the impact of diversification strategies is critical because they determine firms’ ability to leverage internal capabilities, mitigate risks, and exploit new market opportunities. Moreover, diversified firms make up more than 75% of the S&P 500 and account for over 50% of production in the United States (Mota & Santos, 2020), emphasizing their central role in the economy. Given that firms allocate substantial financial and managerial resources to diversification and that diversified firms are prevalent, identifying the factors that drive these strategic choices is essential for both academicians and practitioners.

So far, existing research on the relationship between diversification types and firm performance has produced mixed and often conflicting findings. While it is generally argued that related diversification enhances performance by enabling firms to leverage synergies (Chang et al., 2013; Garba, 2023; Tashman et al., 2023; Zheng & Tsai, 2019), this view is not universally supported, as some studies present conflicting evidence (Nigam & Gupta, 2020). Similarly, although the prevailing belief is that unrelated diversification harms performance (Benito-Osorio et al., 2012), other studies suggest it can be beneficial, particularly in reducing risk and organizational inertia (Benito-Osorio et al., 2012; Sik Cho, 2013). These inconsistencies highlight a critical gap in the literature: the need to better understand how diversifications impact firm performance, and how other factors, such as CEO human capital, may and influence the outcomes of diversification decisions.

Human capital, encompassing the knowledge, skills, and abilities of a firm’s employees, stands out as a pivotal resource influencing competitive advantage and therefore, could play a vital role in shaping the firm’s strategy (Hambrick & Mason, 1984; Perkins & Shortland, 2024). Prior studies 1 have already linked CEO characteristics to firm’s diversification decisions (Baxamusa & Jalal, 2016; Crossland et al., 2014; Gomez-Mejia et al., 2010; Kim et al., 2009; Lee et al., 2021; Li & Tang, 2010; Neyland, 2020), but have not explicitly examined how these characteristics determine the type of diversification pursued. Given that related and unrelated diversification require different managerial competencies, and that CEO knowledge is an established predictor of firm strategy, the lack of research on CEO human capital in diversification decisions represents a critical gap.

Furthermore, prior research underscores the significance of aligning CEO human capital with corporate strategies to enhance firm performance. For instance, Beal & Yasai-Ardekani (2000) found that firms achieve superior performance when there is a match between the CEO’s functional experiences and the company’s competitive strategies. Similarly, Chen et al. (2021) demonstrated that generalist CEOs create more value in diversifying acquisitions, while specialist CEOs excel in within-industry acquisitions, highlighting the importance of fit between executive human capital and strategic initiatives. These findings emphasize the need to consider CEO human capital in strategic decision-making. Therefore, this study seeks to address this gap by exploring the following research questions: “How does CEO human capital influence the type of diversification pursued by firms?” and “Does the fit between CEO human capital and the type of diversification impact firm performance?”

This paper examines the relationship between CEO’s human capital and firms’ diversification choices, distinguishing between related and unrelated diversification. We focus on two key dimensions of CEO human capital: the depth of firm-specific experience and the breadth of career variety. Additionally, we investigate whether the alignment between a CEO’s human capital and diversification strategy affects firm performance. By integrating Upper Echelons Theory (Hambrick & Mason, 1984) and Matching Theory (Ma & Pan, 2017; Weller et al., 2019), this study provides insights into how CEO’s human capital shape diversification strategies. Using a sample of CEO appointments in Fortune 500 firms between 2000 and 2020, we test whether outsider CEOs, who lack firm-specific human capital, are negatively associated with related diversification and whether the breadth of a CEO’s human capital (measured through career variety) is positively associated with unrelated diversification and negatively associated with related diversification. The findings indicate that neither type of diversification is better than the other, but firms perform better when there is a fit between the CEO’s firm-specific human capital and the type of diversification.

The study makes several contributions. First, by bridging the CEO human capital literature with diversification literature, and showing how the CEO’s role may explain conflicting findings on types of diversification and performance. Moreover, many existing studies looking at changes in diversification do not distinguish between related and unrelated diversification (Schommer et al., 2019). Second

The remainder of the paper is structured as follows. The next section reviews relevant literature and develops hypotheses regarding CEO human capital, diversification strategies, and firm performance. The third section outlines the empirical methodology, including data sources, sample selection, and variable measurement. The fourth section presents the results, followed by a discussion section of the key findings and their theoretical and managerial implications.

Theory and Hypothesis

To contextualise this study, prior work on CEO career experiences, diversification strategies, and broader CEO traits was reviewed (see Appendix I) 2 . While career variety is linked to changes in total diversification (Crossland et al., 2014), no study has examined how it influences the type of diversification pursued. This study addresses this gap, offering a more nuanced understanding of how CEO human capital determines diversification choices.

CEO’s Human Capital and Diversification Type

The Role of Firm-specific Experience on Diversification

Upper Echelons Theory posits that an organization’s outcomes reflect executive’s values, cognitive bases, and experiences. (Hambrick & Mason, 1984; Perkins & Shortland, 2024). CEOs’ backgrounds influence how they perceive opportunities and risks, thereby affecting their strategic choices (Hambrick, 2007). One key determinant of a CEO’s background is their firm-specific human capital, which captures the depth of knowledge and experience acquired within a given organization (Guizani & Larabi, 2024).

Related diversification requires firms to capitalize on existing capabilities, leveraging internal synergies across business units (Chatterjee & Singh, 1999). CEOs with firm-specific human capital are familiar with the firm’s operations, channels, and core strengths (Markides & Williamson, 1994). This in-depth knowledge allows them to integrate new ventures with the firm’s existing resources. Moreover, insiders have established internal networks that facilitate coordination across divisions, ensuring a smoother execution of related diversification strategies. By contrast, outsiders lack firm-specific knowledge, struggle to navigate internal politics and face resistance when attempting to coordinate among divisions. As a result, they may find related diversification less attractive.

While outsiders may be at a disadvantage in managing related diversification, they may be particularly suited for unrelated diversification. Unlike insiders, who are often constrained by organizational inertia and prior commitments, outsiders bring a fresh perspective, enabling them to challenge existing strategic norms and explore new opportunities (Chulkov & Barron, 2019; Hambrick et al., 1993; Liang, 2016). Since unrelated diversification involves expanding into unfamiliar markets, outsiders’ broad knowledge and networks can help identify and pursue such opportunities. They are less constrained by internal pressures and are more willing to undertake disruptive changes (Chulkov & Barron, 2019), Their impartial assessments of business units align with the fragmented structure of unrelatedly diversified firms, where units are independent and top management focuses on finances over operations (Hambrick, 1995).

From a risk perspective, unrelated diversification entails higher uncertainty due to its departure from the firm’s existing knowledge base (Chatterjee & Singh, 1999; Park, 2002; Tien & Ngoc, 2019). Outsider CEOs tend to have a higher risk tolerance, as demonstrated by their career mobility and willingness to accept roles where their existing firm-specific skills may not fully transfer (Brockman et al., 2016; Chahyadi & Wineka, 2019). In contrast, insiders often develop strong psychological commitments to past strategies (Chulkov & Barron, 2019; Hambrick et al., 1993), making them less likely to advocate for radical strategic shifts. Since unrelated diversification requires stepping beyond the firm’s core competencies, insiders, who have spent their careers within the organization, may perceive it as a riskier and less viable growth option.

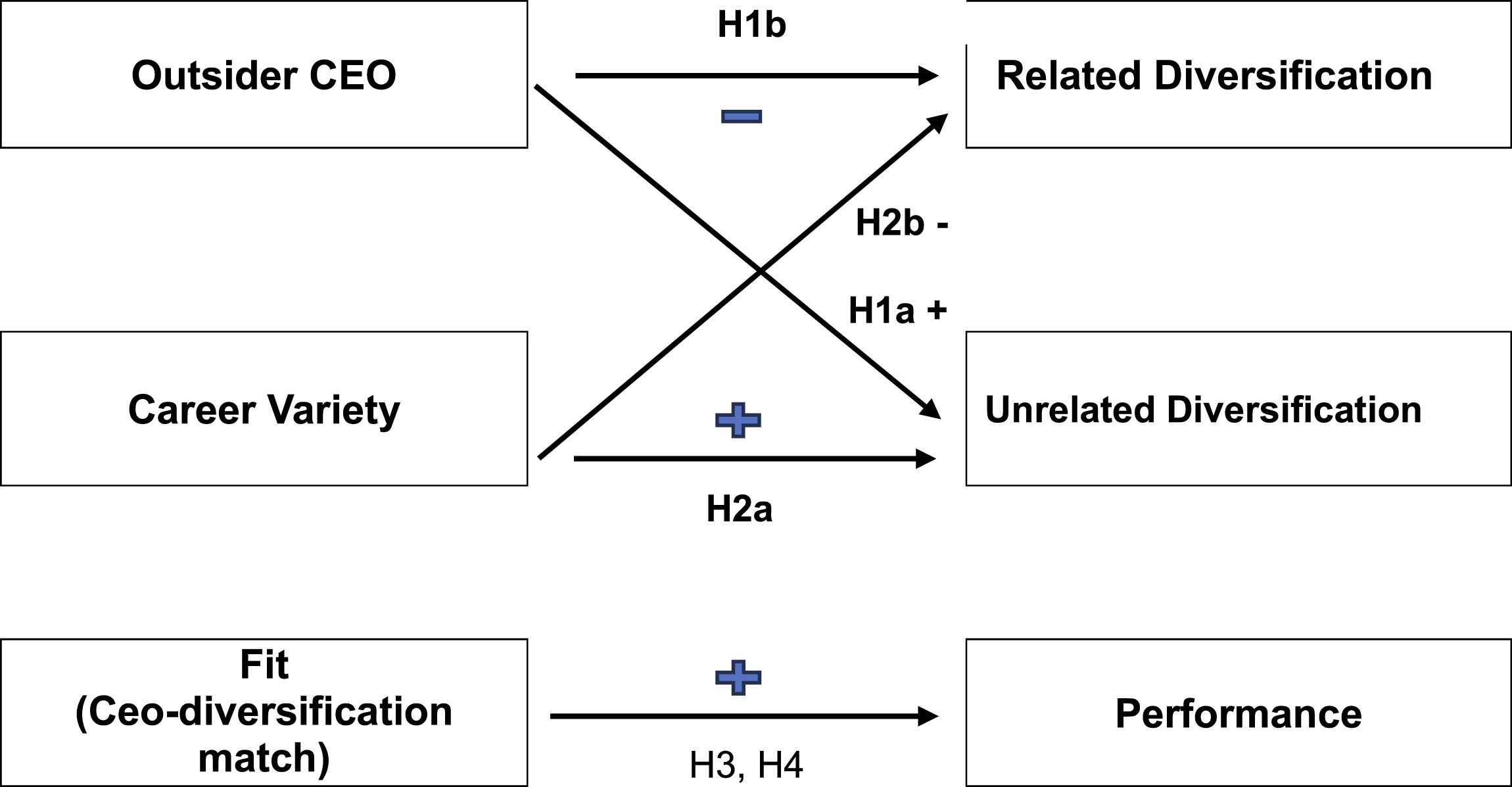

Thus, the interplay between CEO origin and diversification strategy leads to the following hypotheses:

Outsider CEO appointment is positively associated with changes in unrelated diversification

Outsider CEO appointment is negatively associated with changes in related diversification.

The Role of CEO Career Variety on Diversification

CEO career variety reflects the breadth of experience across firms, industries, and functions before reaching the current role (Crossland et al., 2014). This breadth of experience shapes their cognitive frameworks, risk preferences, and strategic choices, consequently influencing the firm’s diversification strategy. While career variety captures the overall breadth of an executive’s human capital, it is conceptually distinct from an outsider CEO status, which solely reflects the lack of firm-specific experience. A CEO could be an outsider with minimal career variety, having worked in just one other firm, or an outsider with extensive career variety, possessing a diverse set of experiences across multiple industries and functions.

The Upper Echelons Theory (Hambrick, 2007; Hambrick & Mason, 1984; Perkins & Shortland, 2024) suggests that executives’ past experiences and cognitive frameworks shape their strategic choices. CEOs with high career variety have been exposed to multiple organizational contexts, leading to greater openness to new opportunities, broader attention breadth, and a tendency to seek novelty (Crossland et al., 2014). This may facilitate entry into new markets but also limit their ability to manage industry-specific synergies.

Empirical research has shown that generalist CEOs tend to engage in a greater number of unrelated acquisitions rather than related acquisitions (Chen et al., 2021; Elia et al., 2021). Related acquisitions, similar to related diversifications, require a deep understanding of industry, and how the acquirer and target firm complement each other to facilitate integration (Chatterjee & Singh, 1999). CEOs with deep knowledge of a particular industry or firm are better equipped to recognize complementarities, manage integration challenges, and extract operational efficiencies from related expansions. However, high career variety executives who have frequently transitioned across industries or functions lack the specialized knowledge required to manage the complexities of related diversification. Moreover, career variety is associated with an exploratory mindset and a preference for novelty (Crossland et al., 2014). Given that related diversification often involves incremental expansion within an industry, it may be perceived as less appealing to CEOs who want novelty. Moreover, the dominant logic of an industry constrains decision-making, and executives with highly specialized backgrounds tend to be more attuned to industry norms and best practices (Ahn, 2022). In contrast, those with career variety may struggle to integrate deeply into a specific industry, making them less inclined to pursue related diversification.

In contrast, unrelated diversification often requires general managerial skills, broad decision-making experience, and the ability to navigate different markets. While CEOs who have specialised in an industry or function would be more likely to fail to recognize the importance of problems outside of their specialisation area (Angriawan & Abebe, 2011), those with high career variety develop a wider attention breadth, making them more likely to pursue strategies beyond industry norms (Crossland et al., 2014). Moreover, CEOs with high career variety accumulate diverse resources, including capital, talent, and knowledge, which can support broader strategic initiatives (Li et al., 2024). Their ability to leverage external social resources makes them well-positioned to lead firms into industries where they lack prior firm-specific expertise. From a risk perspective, CEOs with high career variety tend to exhibit lower risk aversion (Meyer-Doyle & Schumacher, 2019). Since their reputation and career trajectory are not tied to a single firm or industry, they may be more willing to take on the inherent risks of unrelated diversification. In short, CEOs with broad experience offer adaptability, risk tolerance, extensive networks, and strong opportunity recognition skills—key assets for managing unrelated diversifications.

CEO’s career variety is positively associated with changes in unrelated diversification.

CEO’s career variety is negatively associated with changes in related diversification.

The Effect of CEO Characteristics Alignment on Firm Performance

Matching Theory posits the importance of aligning CEOs’ human capital with a firm’s strategic needs (Abernethy et al., 2019; Greve et al., 2009; Han, 2024). For example, firms with greater R&D intensity are more likely to appoint CEOs with experience in technical functional areas (such as R&D, engineering or manufacturing) (Datta & Guthrie, 1994). Similarly, firms with greater advertising intensity will be more likely to select CEOs with output functional experience (executives with primary experience in sales, marketing or R&D) (Guthrie & Datta, 1997). Research intensive firms are shown to be a better match to executives with relevant technical knowledge, and diversified firms are a better match to executives with conglomerate experience (Pan, 2017).

Furthermore, this theory suggests that aligning CEO skills with strategy benefits both the CEO and the firm (Bidwell & Briscoe, 2009; Chen et al., 2021; Han, 2024; Jovanovic, 1979; Rosen, 1982). By matching CEO attributes to firm strategies, companies can reduce risk, optimize resource utilization, and enhance value creation (Chen et al., 2021). Consistent with this, research shows that performance is higher for firms, when the CEO’s experience is congruent with the firm’s strategy (Beal & Yasai-Ardekani, 2000).

Building on matching theory, this study extends the framework to diversification strategies. Prior research shows that CEOs whose leadership style follows the agent-model, prioritizing firm growth for personal gains, are more inclined towards unrelated diversification, as larger, more complex firms can enhance their personal rewards (Martínez-Campillo, 2016) 3 . In contrast, stewardship-oriented CEOs, who focus on long-term firm stability and shareholder interests, tend to favour related diversification strategies that consolidate the firm’s competitive advantage. The positive effect of unrelated diversifications on firm growth is stronger for firms lead by agent-model CEOs.

Based on this idea that a “fit” between CEO characteristics and firm strategies leads superior performance 4 , it is hypothesised:

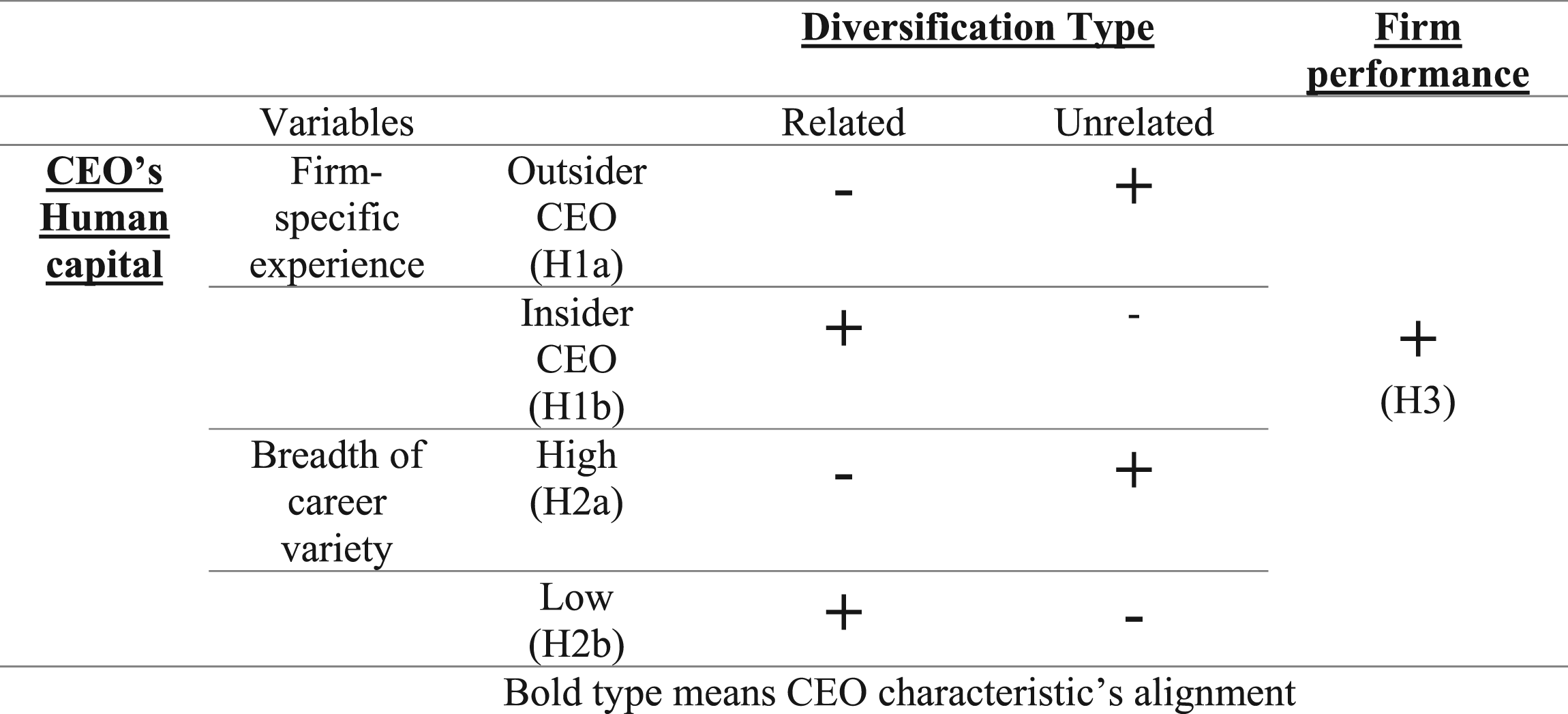

Firm performance is better when there is a fit between CEO firm-specific human capital and type of diversification (i.e. Outsider CEOs engage in unrelated diversifications and insiders engage in related diversifications) than if there is no fit.

Firm performance is better when there is a fit between CEO breadth of human capital and type of diversification (i.e. High career variety CEOs engage in unrelated diversifications and low career variety CEOs engage in related diversifications) than if there is no fit.

Below, Figure 1 illustrates the model depicting the relationships between CEO characteristics, diversification strategy type, and firm performance, based on the hypotheses developed in the previous section (Figure 2). Proposed model summary Summary of Proposed Relationships. Bold type means CEO characteristic’s alignment

Methods

Data Collection and Sample

The hypotheses were tested using data on CEO appointments at Fortune 500 firms between the years 2000 and 2020. CEO appointments were identified using data on Boardex 5 and the final sample is 1071 appointments. For each executive, employment data, including their full job history, was gathered 6 . For each job, the position title, company name, start and end dates, and industry were identified 7 .

Boardex classifies industries at the sector level. However, this sector variable was missing for many observations and provided only broad, limited industry classifications. To obtain more detailed industry identifiers, 4-digit SIC codes were gathered. First, company identifiers in Boardex were merged with Compustat, which assigns SIC codes to firms. For the remaining observations still missing SIC codes, information was manually collected from various sources, including SEC filings and Bloomberg. Through this process, more than 70% of job records for each executive were assigned a SIC code.

For each executive, demographic information, including their age, sex, and educational background, were collected. Educational information includes any degrees they have earned (such as a PhD, MBA, Bachelor’s), the name of the institution awarding the degree, and the graduation date. Additionally, ownership data was gathered from ExecuComp annual compensation database by merging records based on CEO name.

In addition to this, for the Fortune 500 firms where a CEO was appointed in the selected time frame, firm-level information was collected from Compustat. This information includes net sales, the number of employees, the number of business segments, and sales in each segment of the firm. Firm-level data was gathered for the three years preceding and five years following the CEO’s appointment.

Measures

Dependent Variable

1) Diversification

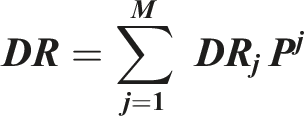

The two dependent variables are related diversification and unrelated diversification. Following prior research, related and unrelated diversification were both operationalized using the entropy measure, which is calculated based on the sales in each business segment (Palepu, 1985)

8

. Companies can do both related and unrelated diversification at the same time, or pursue a focused strategy (pursuing no diversification at all). a) Related diversification

DRj is the related diversification within the industry group j and P is the segment’s share of sales in the total sales within the industry. Firms can operate in multiple industry groups. The number of industry groups for a firm is denoted as M and the total related diversification is measured as the weighted average of related diversification within all groups (Palepu, 1985).

J, the industry group, was identified using the four-digit SIC codes. A diversification was classified as related if it was the same SIC code as the firm. Related diversification was calculated for two years post succession

9

. It could take positive or negative values. Therefore, it accounts for both increases or decreases in diversification. The final variable was the logged average of related change for the first two years of the new CEO’s tenure. b) Unrelated diversification

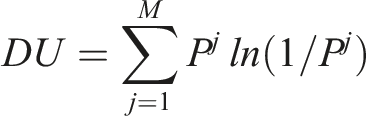

Similarly, unrelated diversification (DU) is calculated as the weighted average of group shares (Palepu, 1985), where again Pj represents the ratio of sales within the group j to the total sales of the firm.

Similar to related diversification, industry groups were identified using the four-digit SIC codes. Diversifications into different SIC codes are classified as unrelated. The unrelated diversification change was calculated for the two years post-succession 10 . The final variable was the logged average change of the two years.

Independent Variables

1) Outsider

Outsiders are strictly defined as CEOs who have 0 firm tenure at the moment of appointment. Outsider is a dummy variable. It took the value 1 if the executive was appointed from outside of the firm and 0 otherwise. 2) Career Variety

Career variety was measured as the sum of three components: the number of firms, industries, and functions an executive has worked in (Crossland et al., 2014). The number of distinct firms was determined using the company identifier in BoardEx employment data, while the number of industries was calculated using 4-digit SIC codes. To measure the number of functions, each job was manually categorised into one of eight categories: production/operations, R&D/engineering, accounting/finance, management/administration, marketing/sales, personnel/labour relations, law, and other (Carpenter & Fredrickson, 2001; Crossland et al., 2014). The total number of unique functions an executive worked in was then calculated. Finally, career variety was operationalised as the sum of these three components

11

. 3) Fit variables

To test hypotheses 3a and 3b, ‘fit’ variables were created, following a similar approach to Chen et al. (2021), which examines how CEO characteristics align with diversification strategies. Hypothesis 3 posits that a fit between CEO outsider status and diversification results in better performance. To test this, an outsider_fit variable was generated, which took the value of 1 if an outsider engaged in more unrelated diversifications, or an insider engaged in more related diversifications. Hypothesis 3b suggests that a fit between CEO career variety and the type of diversification results in better performance. In line with the methodology used by Chen et al. (2021) to create a generalist dummy, career variety was coded as a dummy variable, where a high career dummy took the value of 1 if the CEO’s career variety was above the median for all CEOs, and 0 otherwise. A ‘career_fit’ variable was then generated, which took the value of 1 if a high career variety CEO pursued more unrelated diversifications, or a low career variety CEO pursued more related diversifications, and 0 otherwise.

Control Variables

Various controls were included in the model. Demographic information, such as CEO’s age and sex, was gathered from Boardex. Female, which was a dichotomous variable that took the value 1, if the executive was a female and 0 otherwise, was included as a control in the model. Other controls at the executive level are the year of appointment to the focal CEO position, their years of experience, the number of jobs the CEO 12 has had, and the CEO’s educational capital. CEO tenure was included as a control in the career variety models to account for potential effects of the CEO’s experience within the firm. As tenure increases, the impact of prior career experience diminishes, and new experiences become more influential in shaping decision-making (Meyer-Doyle & Schumacher, 2019). Therefore, controlling for CEO tenure helps isolate the specific impact of career variety on diversification outcomes while accounting for the influence of accumulated experience within the firm.

Year of appointment was included as a control because diversification trends have changed in time (Benito-Osorio et al., 2012). CEO’s educational background may affect the relationship between new CEO appointments and subsequent firm strategies (Karaevli & Zajac, 2013a). CEO educational background was measured using a 7-point scale (Karaevli & Zajac, 2013a): (7) doctorate degree, (6) attended doctoral pro-gramme, (5) Master’s degree, (4) some graduate school, (3) undergraduate degree, (2) some college, and the remaining were coded as (1) high school. Since powerful CEOs are more likely to be able to implement the changes (Brockmann et al., 2006; Kim et al., 2009), chairman status was included as a control, as a proxy for CEO power. Chairman is a dummy variable that took the value 1, if the CEO is also a chairman. Predecessor CEO tenure was also controlled for, as it may reflect the firm’s historical trajectory and provide insight into the firm’s ongoing strategies. The tenure of the predecessor may impact the degree of change a new CEO is able to implement. Therefore, this variable helps control for any lingering effects of the predecessor’s strategic choices on the firm’s diversification decisions.

While outsider CEO appointments may lead to a change in firm’s strategies, it is also possible that outsiders are purposefully selected to firms that want to change. Therefore, the model includes several firm level controls. Prior firm performance was included as a control, since outsiders are argued to be a better match to failing firms (Karaevli, 2007; Schwartz & Menon, 1985). Prior firm performance determines the choice between related and unrelated diversification, as higher performing and profitable firms are more likely to pursue related diversifications over unrelated diversifications

13

(Park, 2002). Therefore, firm performance prior to executive appointment was included as a control. This was operationalised as the sales in the year prior to appointment (t-1). Research suggests that large companies gain more from being versatile in exploring new ideas while exploiting existing ones, thanks to their ample resources (Cao et al., 2009). On the flip side, smaller firms face limitations due to resource constraints, making it challenging to excel in both areas. For similar reasons, firm size may also play a role in determining the level of diversification. Therefore, a control for firm size was included, operationalised as the number of employees the focal firm has the year prior to appointment. Moreover, firms’ subsequent strategies depend on the firm’s previous strategies. Therefore, a control was included for the total diversification strategies prior to CEO appointment year. Total diversification was measured using the entropy measure (Palepu, 1985):

Additionally, the models with performance dependent variable include financial control variables. These models include control of previous firm ROA, industry average performance, competition, firm size, firm leverage and previous diversifications. Competition, operationalised as the number of firms in the industry, was included as a control because the enhanced performance of the firms would not be observable if the diversification strategies were designed to offset the losses from the market (Miller, 2006). Industry average performance was operationalised as the absolute change in the average industry ROA within the two years post succession. Previous diversification was operationalised as the change in total entropy measure between t and t-1. On the CEO level, CEO salary, CEO ownership, CEO tenure, sex, chairman status, and year of appointment as CEO were included as controls. All of these controls are common in previous literature, as they were shown to affect firm profitability; therefore they represent necessary controls when examining the association between fit and performance (Bhagat & Bolton, 2008; Pichler et al., 2018).

Variable Measurements

Statistical Analysis

To analyse the data, STATA was used and OLS regressions with random effects were conducted to test the hypotheses. As very few firms in the selected timeframe experienced CEO changes, there is typically few observations per firm. Consequently, firm fixed effects are not appropriate. This was further supported by Hausman test, which failed to reject the null hypothesis (p > 0.10), indicating that random effects models are appropriate for the analysis.

To address the potential endogeneity problem, arising from the possibility that executives may be selected based on unobservable factors that also influence firm strategy (e.g., the decision to hire an outsider reflecting unobservable board preferences for risk or internal politics (Quigley et al., 2019), Two-Stage Least Squares (2SLS) regression analysis with instrumental variables were employed. To ensure robustness, the instruments were tested for validity (using overidentification tests and under identification tests such as the Kleibergen-Paap rk LM statistic and the Hansen J statistic). Additionally, to mitigate concerns about reverse causality, the dependent variables were measured two years after the CEO’s appointment.

Results

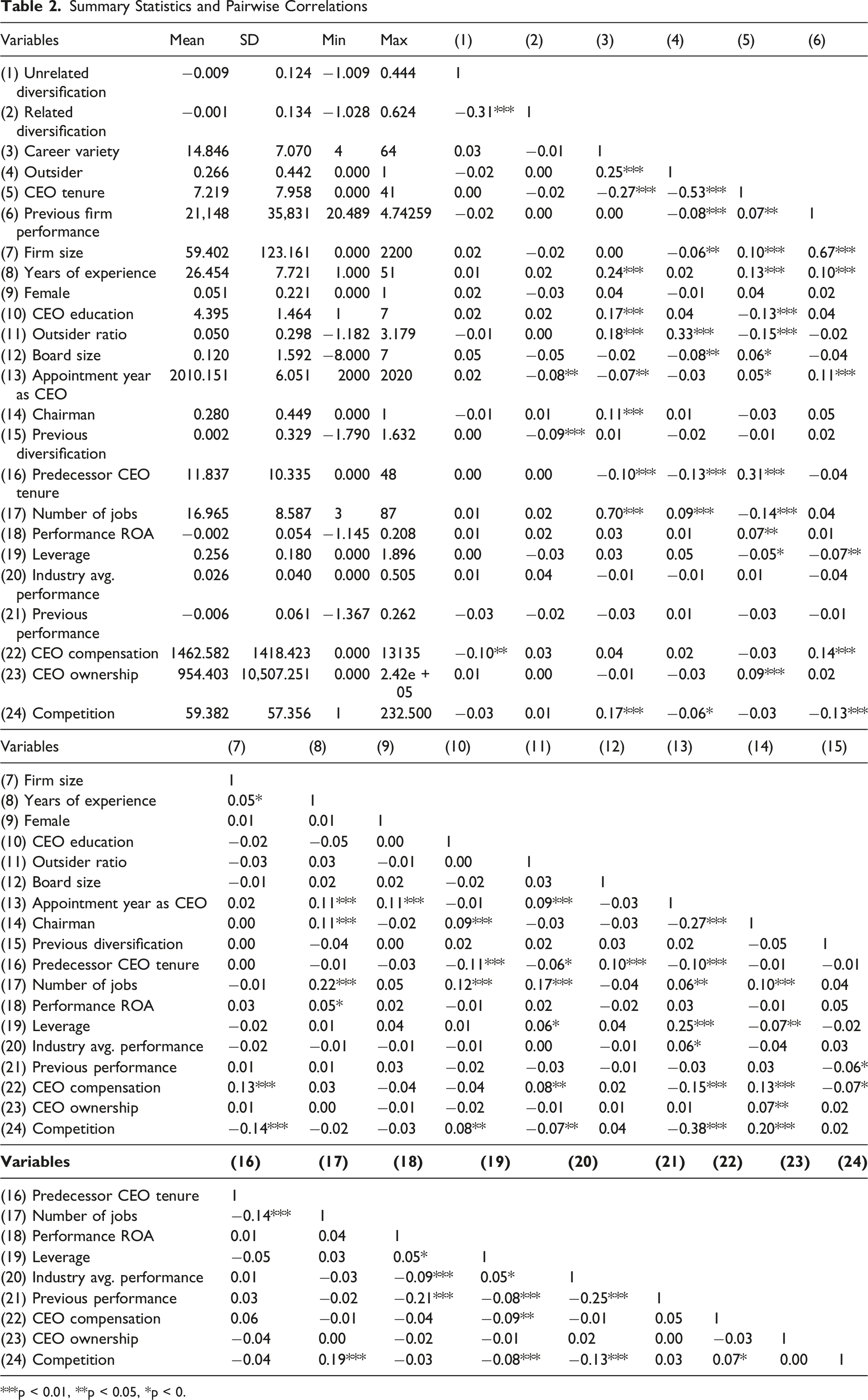

Summary Statistics and Pairwise Correlations

***p < 0.01, **p < 0.05, *p < 0.

The correlation matrix highlights several significant relationships among key variables. Related diversification is negatively correlated with unrelated diversification (correlation = −0.31, p < 0.001), indicating a trade-off between these diversification strategies. Several control variables also show significant correlations with the dependent variables, highlighting their potential influence on strategic decision-making. The appointment year of a CEO is significantly correlated with related diversification (correlation = −0.08, p < 0.05) but not with unrelated diversification (correlation = 0.02, ns.), implying that more recent CEOs are less likely to pursue related diversification strategies. Similarly, previous change in total diversification is negatively associated with related diversification (correlation = −0.09, p < 0.001) but not significantly related to unrelated diversification (correlation = 0.0, n. s.), suggesting that past diversification patterns influence future strategic choices.

Tenure in the company is negatively correlated with both outsider (correlation = −0.53, p < 0.01), and career variety (correlation = −0.27, p < 0.01). This is unsurprising, as outsiders naturally start with zero tenure, and CEOs who have been at the firm longer have had less opportunity to accumulate experience across other firms or industries, limiting their career variety. Moreover, CEO education is positively correlated with career variety (correlation = 0.17, p < 0.01), suggesting that higher educated CEOs also have a wider breadth of experience. Predecessor CEO tenure is negatively correlated with both the career variety of the focal CEO (correlation = −0.27, p < 0.01) and outsider status (correlation = −0.53, p < 0.01), suggesting that longer-serving predecessors are more likely to be succeeded by insiders with less diverse career backgrounds. Finally, outsider and career variety have low correlation (correlation = 0.25, p < 0.01), suggesting that they capture different facets of executive’s experience. Indeed, while outsider status refers to whether the CEO is appointed from outside the focal firm, career variety captures the breadth of experience across firms, industries, and functions 14 .

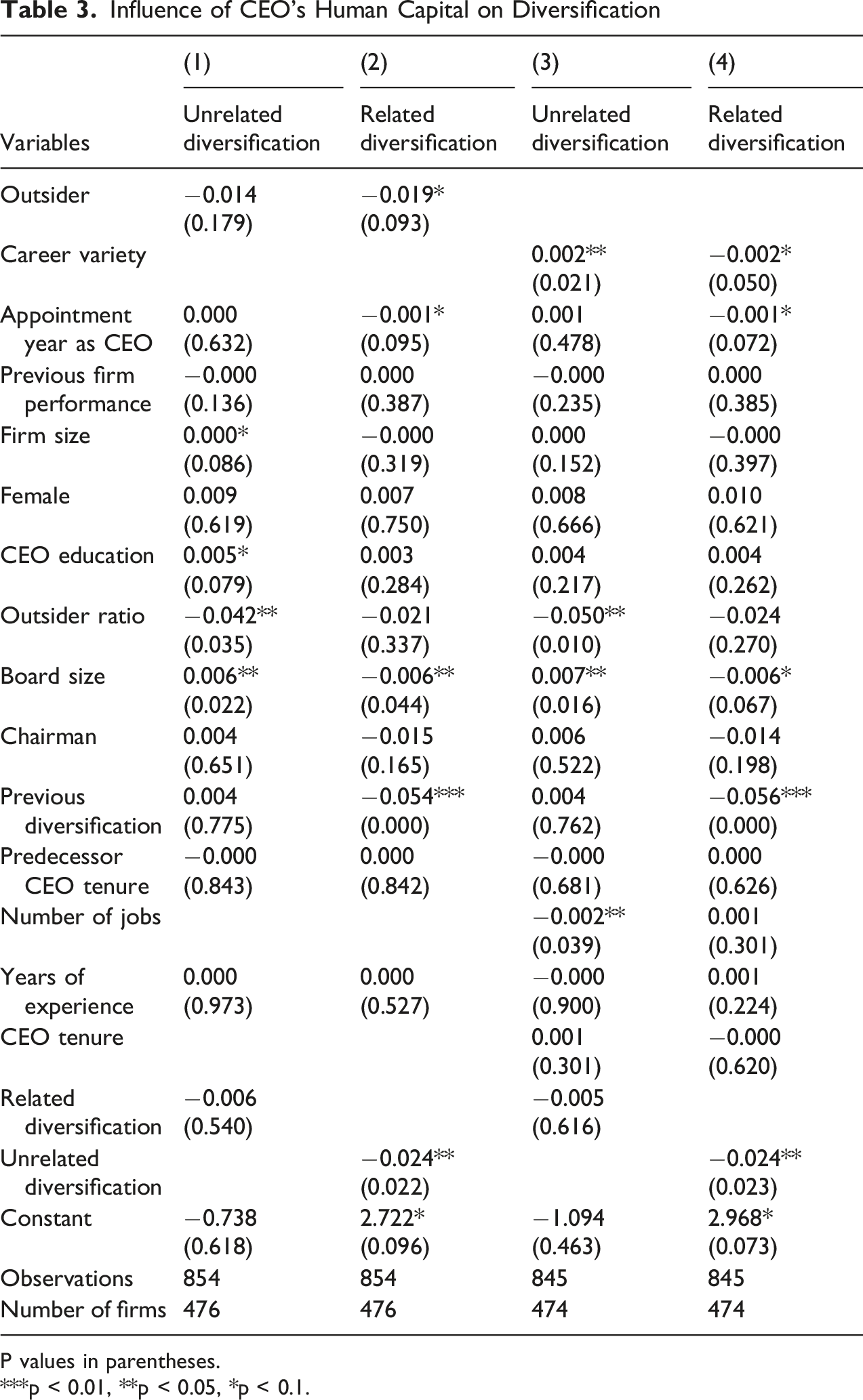

Influence of CEO’s Human Capital on Diversification

P values in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

Hypothesis 2a states that career variety is positively associated with unrelated diversification. In support of this hypothesis, column 3 shows that career variety is positive and significantly associated with unrelated diversification (β=00.002, p < 0.05). A one standard deviation increase in CEO career variety is associated with an average increase of 0.11 standard deviations in unrelated diversification 15 . Hypothesis 2b states that career variety is negatively associated with related diversification. Column 4 show the results for related diversification dependent variable. In support of hypothesis 2b, career variety is negative and weakly significant (β= −00.002, p < 0.10). A one standard deviation increase in CEO career variety is associated with a decrease of 0.10 standard deviations in related diversification.

Several control variables also yielded significant results. Board size is positively associated with unrelated diversification (Model 1: β= 0.006, p < 0.05; Model 3: β= 0.007, p < 0.05) and negatively associated with related diversification (Model 2: β= −0.006, p < 0.05; Model 4: β= −0.006, p < 0.10). The proportion of outsiders on the board is negatively associated with unrelated diversification (Model 1: β= −0.042, p < 0.05; Model 3: β= −0.05, p < 0.01). Additionally, appointment year as CEO is negatively associated with related diversification (β= −0.001, p < 0.10). Finally, unrelated diversification is negatively associated with related diversification (β= −0.024, p < 0.05), indicating that firms may prioritise one type of diversification over the other.

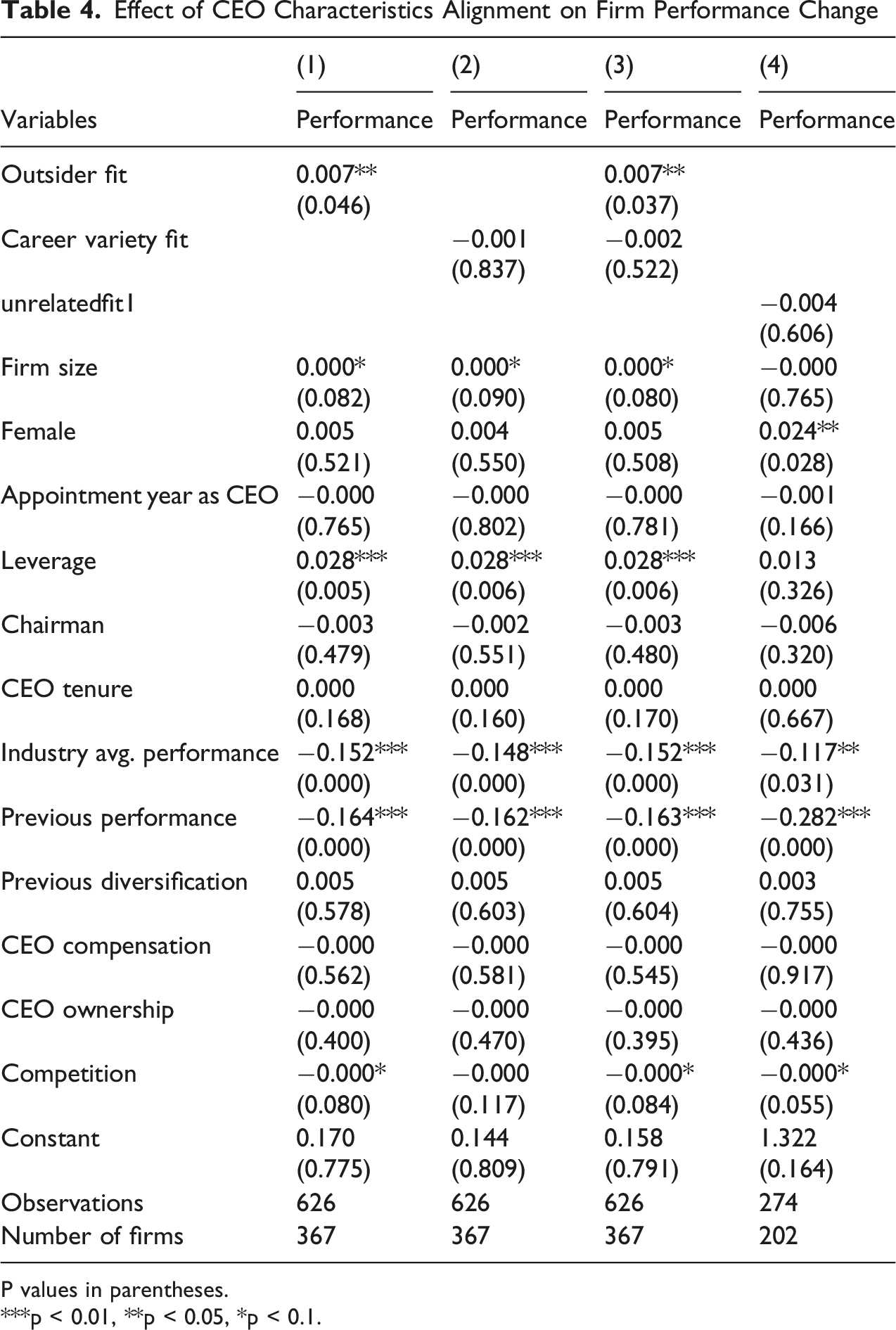

Effect of CEO Characteristics Alignment on Firm Performance Change

P values in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

To further understand this relationship, the analysis tested whether a related diversification fit (with insiders pursuing more related diversifications) or an unrelated diversification fit (with outsiders pursuing more unrelated diversifications) leads to better performance. The analysis was then repeated in a smaller sample, using only observations for CEOs whose outsider status and type of diversification were aligned. The unrelated fit variable takes the value 1 when there is an unrelated diversification fit and 0 for related diversification fit. The number of observations is reduced to 428. The results can be seen in Column 4, which shows that there is no significant difference between related fit and unrelated diversification fit (β= −00.004, n. s.) 16 .

Robustness Tests

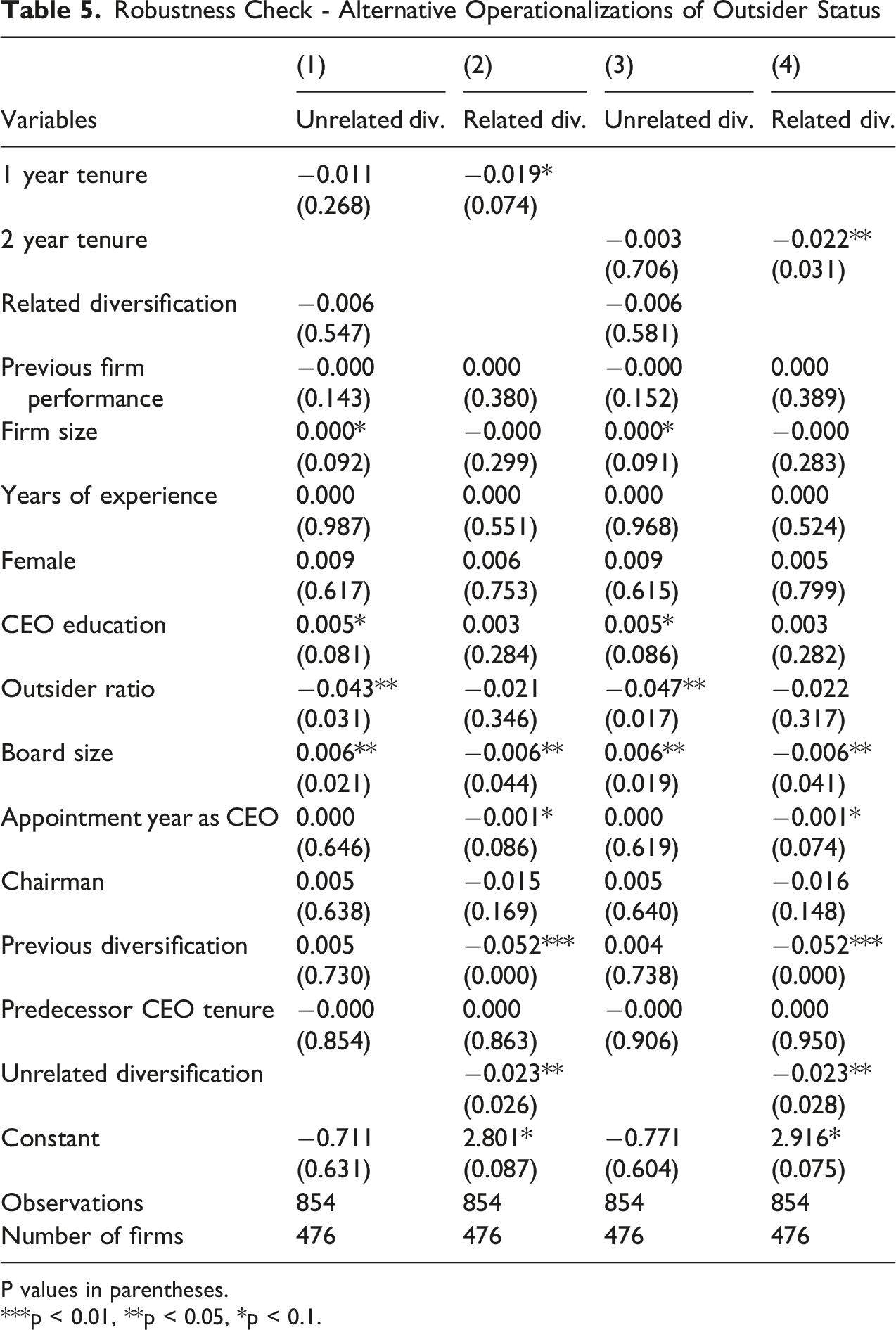

Robustness Check - Alternative Operationalizations of Outsider Status

P values in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

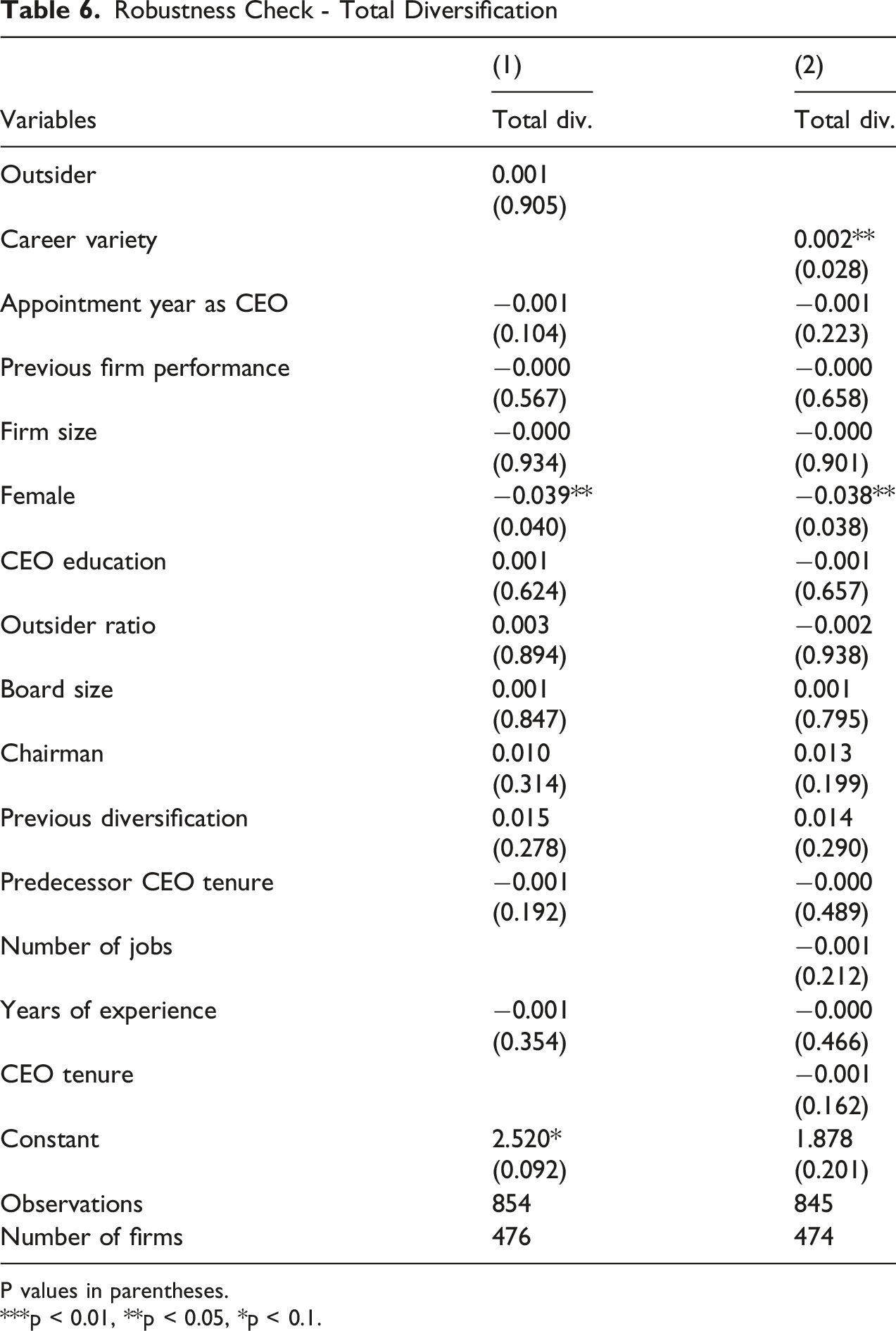

Robustness Check - Total Diversification

P values in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

Finally, we also examined if their joint effect has a significant influence on diversification decisions. Specifically, we included the interaction between outsider and career variety into the model. The results, which show that the interaction between outsider and career variety is significant and positive for related diversifications, can be seen in Appendix III.

Additional Analysis With Instrumental Variables

Executives may be selected specifically because the firms intend to pursue a specific strategy, which leads to a potential selection problem 17 . For example, the decision to hire an outsider may be driven by unobservable factors such as the boards preference for risk or the firm’s internal politics (Quigley et al., 2019). To control for this potential endogeneity, where unobservable factors may drive the selection of a CEO with certain characteristics, instrumental variables were employed. The results show that outsiders (β= −0.06, p < 0.05) and career variety (β= −0.01, p < 0.05) remains significant and negatively associated with related diversifications, and outsiders become positive and weakly significantly associated with unrelated diversification (β= 0.06, p < 0.10), while career variety is not significantly associated with unrelated diversifications (see Appendix IV). Taken together, these findings suggest that endogeneity may affect the relationship with unrelated diversification, while the results for related diversification remain robust. Either way, both career variety and outsider remain significant determinants of diversification choices.

Additional Two-Sided Matching Analysis

While instrumental variable models help address endogeneity arising from unobservable factors, we additionally employ matching methods to account for observable CEO firm selection. Following Chen et al. (2021), we first estimate a two-sided matching model using a maximum score estimator to identify complementarities between CEO and firm that determine matching. Based on the determining interactions, we then employ propensity score matching for each fit variable, using one to one nearest matching without replacement and restricting the sample to common support. The results from the matched sample (Appendix V) remain consistent with the baseline OLS findings; outsider fit remains positive and significantly associated with firm performance (β= 0.007, p < 0.05), while the effect of career variety fit remains statistically insignificant.

Discussion

The findings suggest that CEO attributes, specifically career variety and outsider status, shape preferences for types of diversification. The results are in line with prior research showing that CEO characteristics shape strategic choices, as proposed by the Upper Echelons Theory (Hambrick & Mason, 1984). Specifically, the OLS analysis supports two hypotheses related to career variety, demonstrating that CEOs with high career variety are more likely to pursue unrelated diversification and less likely to pursue related diversification. Additionally, the hypothesis regarding outsider CEOs is also supported, indicating that outsider CEOs are significantly less likely to pursue related diversification. This finding is consistent with prior work suggesting that outsiders are more inclined to implement strategic shifts that break from prior corporate strategic trajectories (Boeker, 1997).

The results contribute to the understanding of outsider CEO decision-making by reaffirming that insiders and outsiders pursue different diversification strategies. Prior studies suggest outsider CEOs often drive change, but such shifts don’t always improve performance (Karaevli, 2007; Karaevli & Zajac, 2013b). Karaevli (2007) suggests that strategic changes by outsiders may harm performance due to their limited firm-specific knowledge and lack of internal social support. However, the present findings, which show that performance does improve when outsider CEO’s pursue strategies aligned with their human capital, offer a refinement to this perspective. This suggests that outsiders can lead to successful change, if there is a fit with the strategy.

In support of Matching Theory, the results indicate that firm performance depends on the fit between a CEO’s firm-specific human capital and the type of diversification pursued. This aligns with prior studies showing that a fit between the manager and strategy can enhance organisational effectiveness and performance (Chen et al., 2021; Jovanovic, 1979; Rosen, 1982). However, in contrast to the expectations of Matching Theory, the none-significance of career variety fit suggest that that improvement also depends on the human capital in consideration.

One explanation for this pattern is that fit alone may be insufficient if the chosen strategy is poorly suited to the firm’s capabilities or competitive environment. In line with this, the effectiveness of matching managers to strategies depends on whether the selected strategy itself is suitable for the firm and its environment (Gupta, 2017). Misalignment with firm capabilities or market conditions may negate CEO-strategy fit benefits, indicating that a match alone does not guarantee performance gains. Another explanation may be the challenges high career variety CEOs face when implementing strategy. High career variety CEOs may be less effective at gathering information from the perspective of the focal industry, limiting their ability to process industry-specific knowledge or leverage firm-specific resource configurations. Supporting this view, prior research has shown that generalist CEOs, who also have broad, varied experience, often experience an initial decline in firm performance following their appointment, due to difficulties in navigating firm-specific challenges effectively (Li & Patel, 2019). Given that this study primarily captures short-term performance, it is possible that performance improves over time as these CEOs adapt and develop firm-specific expertise.

These findings suggest that assuming CEO-strategy fit always leads to superior outcomes may be overly simplistic, particularly in the short term. While Matching Theory argues that firms and managers should be optimally paired for maximum performance, this study indicates firm performance may not improve if the strategy itself is unsuitable for the firm or the market conditions. In other words, a match between CEO characteristics and strategy is a necessary but insufficient condition for superior performance.

Conclusions

The article makes several contributions. First, from a theoretical perspective, it attempts to shed light on the reasons for the conflicting findings of diversification-performance literature. By integrating human capital into diversification research, this study explains why diversification strategies may yield varying performance results. This paper also answers the call for further studies examining the fit between firm strategy and executive backgrounds (Weiss et al., 2015).

Second, many existing studies looking at changes in diversification do not distinguish between related and unrelated diversification (Schommer et al., 2019). Existing research has primarily focused on examining the relationship between CEO characteristics and total diversification, overlooking how CEO characteristics may actually influence the type of diversification they pursue. The findings show that previously documented relationships, such as the positive association between career variety and total diversification (Crossland et al., 2014), are driven primarily by unrelated diversification. Thus, this study refines the results about the strategic implications of CEO career variety.

Third, the paper extends upper echelons theory in several ways. First, by combining this theory with matching theory, the results show it is important to consider the fit between executive backgrounds and strategies. While both human capital influences diversification choices, they do not always translate into better performance. Second, it makes a theoretical contribution by demonstrating that executive characteristics should not be examined in isolation. The interaction between outsider status and career variety shows characteristics function as bundles. This moves beyond main effect explanations and shows the importance of combined executive profiles.

Fourth, this study contributes to matching theory by testing its boundary conditions. Matching theory predicts that alignment between executive background and strategy improves performance. The evidence supports this prediction for outsider status, but not for career variety. This asymmetry indicates that CEO–strategy fit improves performance only for certain types of human capital and strategic contexts. Fit, therefore, is not a general performance enhancing mechanism, but a conditional one that depends on the underlying executive attribute and the demands of the strategic change. This effect persists even after taking CEO-firm selection into account.

Finally, the findings contribute to the literature on outsider CEO appointments. This literature has the general consensus that outsiders are positively associated with change, and insiders are better for stability. The findings of this paper indicate that outsiders and insiders pursue different types of strategies and the success of these strategies depends not just on the CEO’s status as an outsider but on how well their prior experience aligns with the specific change being implemented.

From a practical perspective, diversified firms comprise over 75% of the S&P 500 and 50% of U.S. production (Mota & Santos, 2020). Therefore, furthering our understanding of the relationship between diversification and business performance has great practical importance. From a corporate perspective, these findings have implications for the management of executive talent. Firms may benefit from aligning the CEO’s background with the type of diversification they pursue, promoting executives with certain career backgrounds (for example low or high career variety). This also indicates the importance of designing internal executive career paths. The results also show the importance of managing related and unrelated diversification separately, which can help firms make more informed choices to maximise their performance. In terms of corporate governance, the role of the board of directors is particularly important, as they should consider how the professional background of the potential CEO will affect the company’s strategic direction and risk-taking. Therefore, the board must define the succession profile. In addition, the findings can guide educational institutions and business schools that design executive training and leadership programmes, for example by offering classes that mix broad perspectives with industry specific knowledge.

Despite its contributions, this study has several limitations. First, while the analysis captures short-term performance outcomes following new CEO appointments, it does not account for potential long-term effects. A key distinction between insiders and outsiders is that the latter lacks firm-specific knowledge. However, as outsiders gradually acquire this knowledge and develop a psychological commitment to existing strategies, the differences between the two groups may diminish. Similarly, high career variety CEOs may need time to adapt and fully leverage firm-specific knowledge before their strategic choices translate into performance improvements. Future research could extend this analysis by examining longer-term performance trends to determine whether the observed effects persist, diminish, or evolve over time.

Second, this study focuses on Fortune 500 firms due to data availability. These large firms typically possess the financial and operational resources necessary to implement diversification strategies. In contrast, smaller firms may face constraints that limit their ability to diversify, regardless of the CEO’s strategic preferences. As a result, the extent to which CEO characteristics influence diversification choices in smaller firms remains an open question. Future studies could explore whether resource limitations alter the relationship between CEO attributes and diversification decisions in different firm sizes and contexts.

Third, while this study examines key CEO characteristics such as career variety and outsider status, other CEO attributes, such as leadership style or risk tolerance, may also shape diversification choices and their performance implications. Future research could adopt a more comprehensive approach by incorporating additional CEO traits to better capture the complexity of executive decision-making.

Fourth, the broader governance and competitive landscape may also play a critical role in shaping how CEOs influence diversification strategies. For example, board composition may affect the extent to which CEOs are able to enact strategic change. Board size, in particular, appears to have distinct effects on diversification choices, potentially influencing whether firms pursue related or unrelated diversification. Additionally, CEO-board power dynamics could determine whether diversification strategies reflect the CEO’s vision or are constrained by board preferences. Similarly, external competitive pressures, such as industry-level competition and economic uncertainty, may moderate the relationship between CEO characteristics and diversification outcomes. Future research should explore how governance and competition interact with CEO traits to shape diversification and performance.

Supplemental Material

Supplemental material - Navigating Diversification: The CEO’s Human Capital Influence on Firm’s Diversification Strategy and Performance

Supplemental material for Navigating Diversification: The CEO’s Human Capital Influence on Firm’s Diversification Strategy and Performance by Melis Yücel, Irene Campos-García, María Asunción Sacristán-Navarro in Group & Organization Management.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper has been supported by Project PID2021-124641NB-I00 of the Ministry of Science and Innovation (Spain) and by the R&D Program of Madrid Regional Government (Grant PHS-2024/PH-HUM-294).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.