Abstract

Scholars have widely studied the impact of organizational capabilities on corporate operational performance. However, little attention has been paid to how digital and operational capabilities in resource-constrained environments shape firms’ business models and environmental performance. This study investigates how business analytics, resource bricolage, and industrial orientation capabilities relate to business model innovation (BMI) and ESG performance. To ensure sectoral and regional consistency, this research specifically focuses on Chinese companies operating within the digital economy. Furthermore, the study explores how BMI intervenes in the relationship between BAC, resource bricolage, industrial orientation, and ESG performance. A core descriptive focus of this investigation is the inclusion and role of underrepresented groups, such as women and immigrants, in driving these innovation-led sustainability outcomes. Grounded on the resource-based theory (RBT) and utilizing a sample of 223 respondents and analyzed via PLS-SEM (SmartPLS v4), the findings show that BAC, resource bricolage, and industrial orientation are strongly and positively linked to BMI and ESG performance. Furthermore, BMI is found to play a significant mediating role in the relationship between industrial orientation and ESG performance. The study contributes to the RBV theory from the context of firm capabilities and BMI and concludes by offering valuable insights for Chinese companies aiming to improve their ESG performance in the digital era.

Introduction

In today’s rapidly changing business landscape, businesses are under increasing pressure to reinvent their business models while addressing environmental, social, and governance (ESG) issues (Abbas et al., 2026). Advances in technology, societal standards, and regulatory requirements have underlined the importance of business models promoting sustainability and profitability. Business model innovation (BMI) is becoming an increasingly important aspect of firm success, particularly when balancing financial growth with environmental sustainability (Mancuso et al., 2025; Shuang et al., 2026). Businesses must reevaluate their models to incorporate social and environmental responsibilities as ESG factors become increasingly crucial in stakeholder assessments and investment decisions (Abbas et al., 2025; Saydam et al., 2024). Organizational attributes that allow organizations to adapt and thrive in this dynamic environment are essential as innovation and sustainability merge (Binesh et al., 2025). To ensure a rigorous and consistent analysis of these dynamics, this research specifically focuses on Chinese firms operating within the digital economy.

Although BMI is widely acknowledged as a critical source of competitive advantage (Feng et al., 2025; Teece, 2010), there is a lack of understanding regarding the extent to which organizational capabilities influence BMI, particularly regarding ESG outcomes. Business analytics has emerged as an indispensable instrument in this context, as organizations such as General Electric, Alibaba, and Amazon leverage data to enhance consumer experiences, optimize operations, and propel expansion. Nevertheless, research on the association between organizational capabilities such as industrial orientation, resource bricolage, business analytics, and BMI and ESG performance is scarce. In the past, research has primarily focused on the performance of BMI or ESG in isolation, neglecting the potential of these competencies to facilitate the development of innovative business models and improved ESG outcomes (Feng et al., 2025; Sklavos et al., 2025).

Furthermore, the human element within these digital transformations remains a critical yet under-researched area. A significant contribution of this study is its descriptive focus on the role of underrepresented groups, including women and immigrants, within the Chinese corporate workforce. As China transitions to a more inclusive digital economy, understanding how the diverse perspectives and unique problem-solving approaches of these marginalized groups contribute to resource bricolage and innovation becomes essential. This study argues that the creative input from these diverse human resources is a vital catalyst for driving sustainability-led business models.

This study addresses this critical lacuna by employing the resource-based theory (RBT) to examine how organizational capabilities, specifically, business analytics, resource bricolage, and industrial orientation, support BMI and ESG performance. According to RBT, businesses acquire a competitive advantage by employing resources that are valuable, rare, inimitable, and non-substitutable (VRIN) (J. Barney, 1991; Mushi, 2025). We extend this framework by conceptualizing digital capabilities and creative human capital as strategic intangible resources that form the “structural foundation” of a firm.

We argue that industrial orientation, resource bricolage, and business analytics are essential competencies that enable companies to reinvent their business models and improve their ESG performance, thereby providing them with a competitive edge in a market that is increasingly centered on sustainability.

The growing significance of ESG in corporate strategy underscores the need for businesses to adjust their models to align with sustainability and profitability objectives (Cabaleiro-Cerviño & Mendi, 2024; Sun, 2024). ESG performance, which evaluates a company’s governance, social responsibility, and environmental impact, now substantially impacts corporate success (Abbas et al., 2025; Zhang et al., 2026). Despite their increasing significance, the extent to which organizational capabilities influence ESG performance through BMI remains inadequately explored. In particular, scholars have not found a robust study that explains how BMI influences business analytics, resource bricolage, industrial orientation, and ESG consequences.

Our study addresses this gap and investigates: (1) How do diverse organizational capabilities, such as business analytics, resource bricolage, and industrial orientation, relate to BMI and ESG performance? (2) What role does BMI play in firm ESG performance? (3) Does BMI mediate between organizational capabilities and ESG performance? The investigation of these research questions contributes to the existing literature in two aspects. Initially, it enhances our understanding of how specific organizational capabilities affect BMI and ESG performance. Secondly, it contributes to the body of literature on dynamic capabilities by demonstrating the role of BMI as a mediator in the relationship between said capabilities and ESG outcomes. Finally, it describes the strategic importance of inclusive workforce diversity in achieving green outcomes.

Literature Review

Theoretical Foundation

The present analysis is based on the RBT, which holds that variations in a firm’s performance are caused by its distinct ability to recognize and utilize resources and capabilities that are valuable, rare, inimitable, and non-substitutable (VRIN) (J. B. Barney, 2001; Grant, 1996). Under this lens, organizational capabilities like business analytics and the creative potential of a diverse workforce (including women and immigrants) are viewed as strategic VRIN resources that drive long-term sustainability. These resources include the procedures, skills, data, and expertise that enable businesses to provide value and gain a competitive edge.

The RBT has drawn criticism while being a prominent strategic and operations management paradigm. Its application in dynamic and competitive markets is diminished by its assumption of a stable market environment and tautological reasoning (Priem & Butler, 2001). Despite these criticisms, RBV is still a strong and popular lens in information systems and strategic management research. Dynamic capabilities, which highlight a firm’s capacity to integrate, reorganize, and refresh its resource base to adapt to quickly changing environments, have been incorporated into the RBV in recent research (Ferreira & Ferreira, 2024; Malhotra et al., 2024; Teece, 2009).

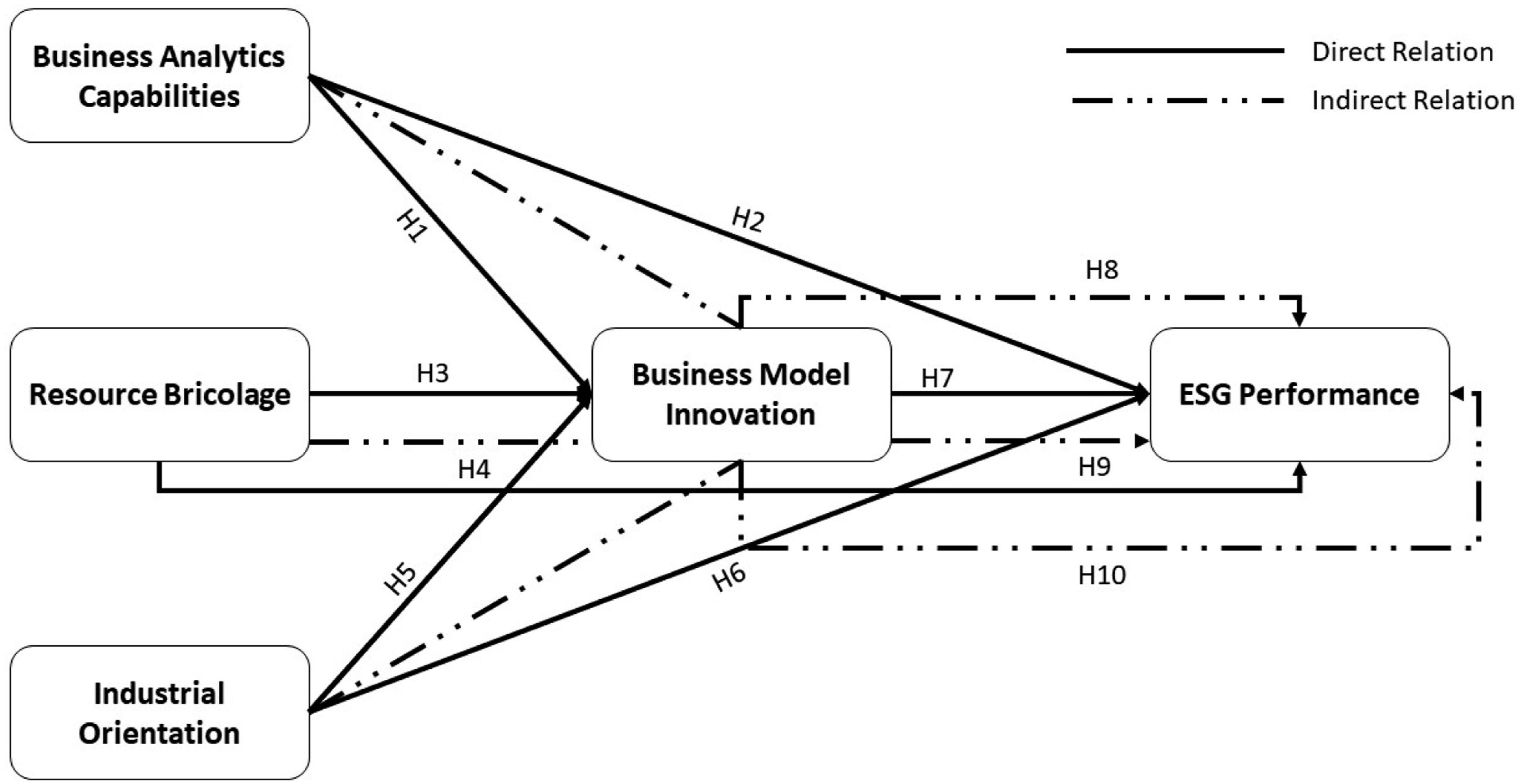

By recognizing that a firm’s ability to continuously adapt and innovate strategically using its valued resources is just as important to maintaining a competitive edge as having them, the dynamic capabilities view enhances RBT (Eisenhardt, 2000). As illustrated in Figure 1 and Figure 2 regarding global digital and AI trends, firms must leverage these dynamic capabilities to navigate the rapidly evolving digital landscape in China. The current study uses this theoretical framework to examine how resource bricolage, business analytics, and industrial orientation influence organizational ESG performance and innovation. A more thorough understanding of how businesses might utilize their distinct resources is offered by extending RBV to dynamic capabilities, particularly regarding BMI and ESG performance. Conceptual framework

Business Analytics, Business Model Innovation, and ESG Performance

The concept of BAC is multidimensional, consisting of three components: data integration, data perception and identification, and deep analysis and insight (Mikalef & Krogstie, 2020; Wamba et al., 2017). From an RBT perspective, these analytics functions serve as inimitable resources that allow firms to sense market shifts before competitors. These capabilities are essential for advancing BMI as organizations increasingly operate in dynamic and uncertain environments, particularly in the digital economy. In response to technological disruptions, market shifts, and evolving consumer demands, integrating business analytics into business strategies is critical for organizations to adapt and innovate (Teece et al., 1997). At the core of BAC, data perception and identification are the organization’s capacity to identify emergent opportunities, trends, and patterns through data analysis (Aydiner et al., 2019; Donbesuur et al., 2021; Mikalef & Krogstie, 2020). Secondly, developing data integration capabilities is essential for incorporating insights into the decision-making process and synthesizing a variety of data sources (Oesterreich et al., 2022; Osterwalder & Pigneur, 2013). This capability allows organizations to integrate and analyze internal and external data to enhance their business models. Companies proficient in comprehensive analyses can adapt to external changes, implement innovative business models, and gain a competitive advantage (Teece, 2018).

As the demand for real-time decision-making increased, business analytics evolved to incorporate increasingly sophisticated techniques such as machine learning, artificial intelligence, and predictive analytics (Nazeer et al., 2026). These techniques enable businesses to extract insights from vast volumes of data in real time, particularly when dealing with high-speed data streams and sensor data (Chen & Liao, 2011). Organizations must cultivate a dynamic competence that enables them to continually modify their business strategies and procedures to adapt to rapidly evolving business environments. Krishnan et al. (2020) argue that the capacity to strategically deploy data through business models and extract value from it is a critical distinction for businesses seeking a competitive advantage in the digital economy. Predictive analytics can identify opportunities for growth and transformation by providing insights into consumer behavior, market demands, and emerging trends (Kumar et al., 2022; Lateef & Keikhosrokiani, 2023). The relationship between business analytics skills and ESG performance is particularly relevant in the contemporary business environment, where companies are required to adopt novel approaches to address sustainability issues.

Integrating business analytics into BMI can enable organizations to enhance long-term performance, adapt their business models to novel market conditions, and continuously innovate. Organizations that implement business analytics to facilitate data-driven innovation are considerably more likely to achieve enhanced market differentiation, consumer satisfaction, and sustainable business practices (Chesbrough, 2017). This research argues that companies with strong BAC are more equipped to innovate and disrupt their business models, allowing them to quickly adapt to market conditions and technological progress shifts. In today’s market, a firm’s ability to innovate its business model is crucial for gaining a competitive edge, and BAC plays a significant role in ensuring ongoing organizational success (Teece, 2018). This study examines the twofold effect of BAC on BMI firm ESG performance, enhancing our understanding of how companies can utilize these capabilities to sustain their competitive advantage in ever-changing business landscapes. Thus, the following hypotheses are put forward;

Business analytics capabilities have a positive impact on business model innovation.

Business analytics capabilities have a positive impact on ESG performance.

Resource Bricolage, Business Model Innovation, and ESG Performance

Bricolage is the process of making use of pre-existing resources that are easily accessible or can be obtained at a low cost, such as tangible inputs, knowledge, and skills. Applying RBT, bricolage functions as a rare capability that transforms underutilized assets into valuable outputs, specifically through the creative input of diverse teams. These resources may be obtained informally or outside of conventional contractual relationships and frequently include those that are underutilized inside the company or the larger market. Bricolage’s basic tenet is that businesses can use seemingly unimportant materials to produce new goods, services, or solutions by fusing them in creative ways (Fuglsang, 2020).

This strategy is in line with the RBT, which holds that businesses can innovate by utilizing existing surroundings and internal resources frequently without having to make significant additional investments (Baker & Nelson, 2005). By empowering decentralized teams to solve problems creatively, bricolage effectively flattens rigid organizational hierarchies, making the team structure more agile and innovative Dynamic capability theory, which stresses the firm’s capacity to reorganize its resource base to attain sustainable competitive advantage in dynamic contexts, is consistent with this ability to convert limited or underutilized resources into innovative and valued products (Teece, 2010, 2018).

Bricolage becomes a crucial tool in the context of BMI for companies looking to develop their business models. It helps businesses create new value propositions by allowing them to recombine existing resources in ways that challenge conventional business paradigms. First, by repurposing existing, underutilized resources, bricolage allows businesses to create new value propositions. Second, the creative value propositions produced by Bricolage may result in broader market prospects, which may cause companies to reconsider their target markets and investigate new avenues and clientele. Lastly, by questioning accepted industry norms and standards, bricolage might increase BMI. For instance, businesses can reimagine value delivery channels and reach new consumer segments by repurposing existing resources, two crucial components of BMI (Desa & Basu, 2013). This can involve developing new service delivery models or reaching underserved customers, which eventually reorganizes the structure of the company model.

Likewise, robust bricolage capability is well-suited to the growing emphasis on sustainable practices, particularly in the context of ESG, as companies are obligated to pursue environmental objectives, encourage social change, and maintain robust governance procedures (Desa & Basu, 2013; Lateef & Keikhosrokiani, 2023). Businesses frequently incur substantial advance expenses that may limit their ability to innovate in the ESG sector as the demand for exceptional resources in sustainable operations increases (Osiyevskyy & Dewald, 2015). Resource bricolage can also facilitate the adoption of disruptive ideas that contradict established industrial standards. For example, small businesses could utilize bricolage to establish more sustainable supply chain procedures or alternative production techniques that are more adaptable to evolving regulatory contexts and require less resource consumption. This study argues that in addition to providing the company with a competitive advantage by establishing it as a pioneer in sustainability and ethical business practices, this strategy facilitates BMI and strengthens ESG performance by reducing the environmental impact. Thus, we put out the following hypothesis:

Resource bricolage capabilities have a positive impact on business model innovation.

Resource bricolage capabilities have a positive impact on ESG performance.

Industrial Orientation, Business Model Innovation, and ESG Performance

The ability of a firm to align its value propositions with the evolving realities of the market, technology, and consumer insights so that its resources are optimally utilized reflects a proactive industrial orientation in the firm (Arnold et al., 2011). Industrial orientation acts as a strategic sensor that identifies which VRIN resources should be deployed to meet digital market demands. Firm orientation grounded in market orientation—which highlights the need for malleability to changing customer appetites (Olofsson et al., 2018; Zhou & Liao, 2024)—and entrepreneurial orientation—which promotes innovative and competitive products and services (Aloulou et al., 2024)—provides firms with the agility to conform to changing settings. This is consistent with the RBV, which argues that successfully exploiting valuable, rare, and hard-to-imitate resources is the primary methodology for obtaining competitive advantage (J. Barney, 1991). Resource integration is one of the most effective mechanisms for translating industrial orientation into embedded behavior to achieve significant results. It permits firms to combine pre-existing resources in novel ways, which improves operational efficiency and unlocks BMI in response to technological disruptions and shifts in the market (Chatterjee et al., 2022). Additionally, in environments with limited resources, pursuing an industrial orientation enables resource bricolage, which allows firms to leverage existing resources into new applications to promote innovation and risk reduction (Senyard et al., 2014).

Aligning ESG practices with corporate strategy is a growing defining marker for long-term sustainability and competitive advantage (Shafait & Pan, 2025). Yet, the relationship between ESG performance and strategic orientations, like industrial orientation, has been less explored. It is crucial to address this gap, given that firms with a strong orientation toward industry are better able to align their resource strategies with the sustainability goals of the projects they aim to pursue. Dynamic capabilities, for example, market opportunity sensing, seizing, and resource reconfiguration, typically augment the relationship between industrial orientation and ESG outcomes. The most innovative firms (e.g., prospectors) will, therefore, likely be the first movers in adopting ESG practices, with positive externalities leading to enhanced environmental performance and stakeholder trust (Yuan & Cao, 2022). On the other hand, efficiency-driven companies (e.g., defenders) might be the most conservative; however, they are still able to gain in ESG by optimizing resource allocation.

By integrating ESG metrics into their strategies, industrial firms can effectuate BMI that complies with the dispositions of the new regulation while generating greater value for consumers and stakeholders (Galbreath, 2013). An example of this is highlighted by companies operating in sustainability-centric markets, like renewable energy or eco-technology (Duarte Alonso et al., 2025), that have shown the transformative impact of ESG alignment, which fosters solutions through innovation and leads to both enhanced efficiency and competitive advantages. Based on these, the following hypotheses are proposed;

Industrial orientation has a significant positive impact on business model innovation.

Industrial orientation has a significant positive impact on ESG performance.

Business Model Innovation and ESG Performance

The idea of business models has been extensively explored in the literature; however, its comprehensive integration into the business community remains limited (Birkinshaw, 2024). Within the RBT framework, BMI is the high-order capability that reconfigures firm resources to create sustainable value that competitors cannot easily duplicate. Nevertheless, it is widely recognized that a business model is a framework that outlines the allocation of resources and the operation of an organization to generate value and revenue (Zott & Amit, 2010). Despite the numerous definitions, value creation is universally acknowledged as the cornerstone of all business models (Hock-Doepgen et al., 2024). It is anticipated that businesses will integrate sustainability into their operations in response to increased scrutiny of their environmental and societal effects.

Companies are held accountable for negative externalities, which is a strategic necessity and an ethical obligation (Dunphy et al., 2017). The relationship between innovation and sustainable business models has been extensively investigated, and scholars such as Schumpeter (1976) have argued that innovation is the driving force behind development. Recent research, including those conducted by Abbas (2024), Block et al. (2025), and Chaudhuri et al. (2024), has emphasized the importance of innovation in promoting sustainable development. Zott and Amit (2010) also note that businesses can only maintain growth by integrating innovation into their business strategy.

This research focuses on the role of BMI in improving ESG performance and argues that BMI can enhance ESG performance by fostering the development of sustainable value. Companies that integrate ESG factors into their business models comply with regulatory and societal obligations and fortify their long-term competitiveness by strengthening their ability to withstand environmental and social hazards (Lüdeke-Freund, 2010). The integration of ESG factors into business models is becoming more widely acknowledged as a strategic resource rather than solely a moral obligation due to the growing emphasis on sustainability. Firms can leverage their BMI capabilities to effectively address ESG challenges and capitalize on new market opportunities from a sustainability-driven approach. Thus, the subsequent hypothesis is put forth:

Business model innovation has a positive impact on ESG performance.

The Mediating Role of Business Model Innovation (BMI)

Based on the resource-based theory and the dynamic capabilities view, this study proposes that organizational capabilities do not always influence sustainability outcomes directly; rather, they often require a strategic mechanism to reconfigure value creation processes. Business model innovation (BMI) serves as this critical bridge, allowing firms to translate analytical insights, resource improvisation, and strategic orientations into superior ESG results. Therefore, we propose the following mediation hypotheses:

Business model innovation mediates the relationship between business analytics capabilities and ESG performance.

Business model innovation mediates the relationship between resource bricolage capabilities and ESG performance.

Business model innovation mediates the relationship between industrial orientation and ESG performance.

Research Methodology

Representative provinces such as Beijing, Jiangsu, Zhejiang, Shanghai, Guangdong, and others were chosen in the sample selection process. Referring to the latest “Statistical Classification of Digital Economy and Its Core Industries (2021)” released by the National Bureau of Statistics, the research focused on approximately four hundred businesses highly committed to capitalizing on digital technology. After excluding invalid responses, including incomplete or non-compliant questionnaires, 223 valid surveys were retained. Most of the survey participants are company founders or senior executives. The questionnaires were distributed and collected between August and October 2024. The sample includes organizations 15 years or older, with 81.61% of them employing between 200 and 1,000 people. In terms of ownership, 32.74% of businesses are state-owned. To address the research focus on inclusivity, the sample deliberately accounts for diverse leadership roles, providing an empirical basis to analyze the contributions of underrepresented groups. The statistical data aligns with sample characteristics from similar studies, demonstrating the high representativeness of the research sample (Peng et al., 2022).

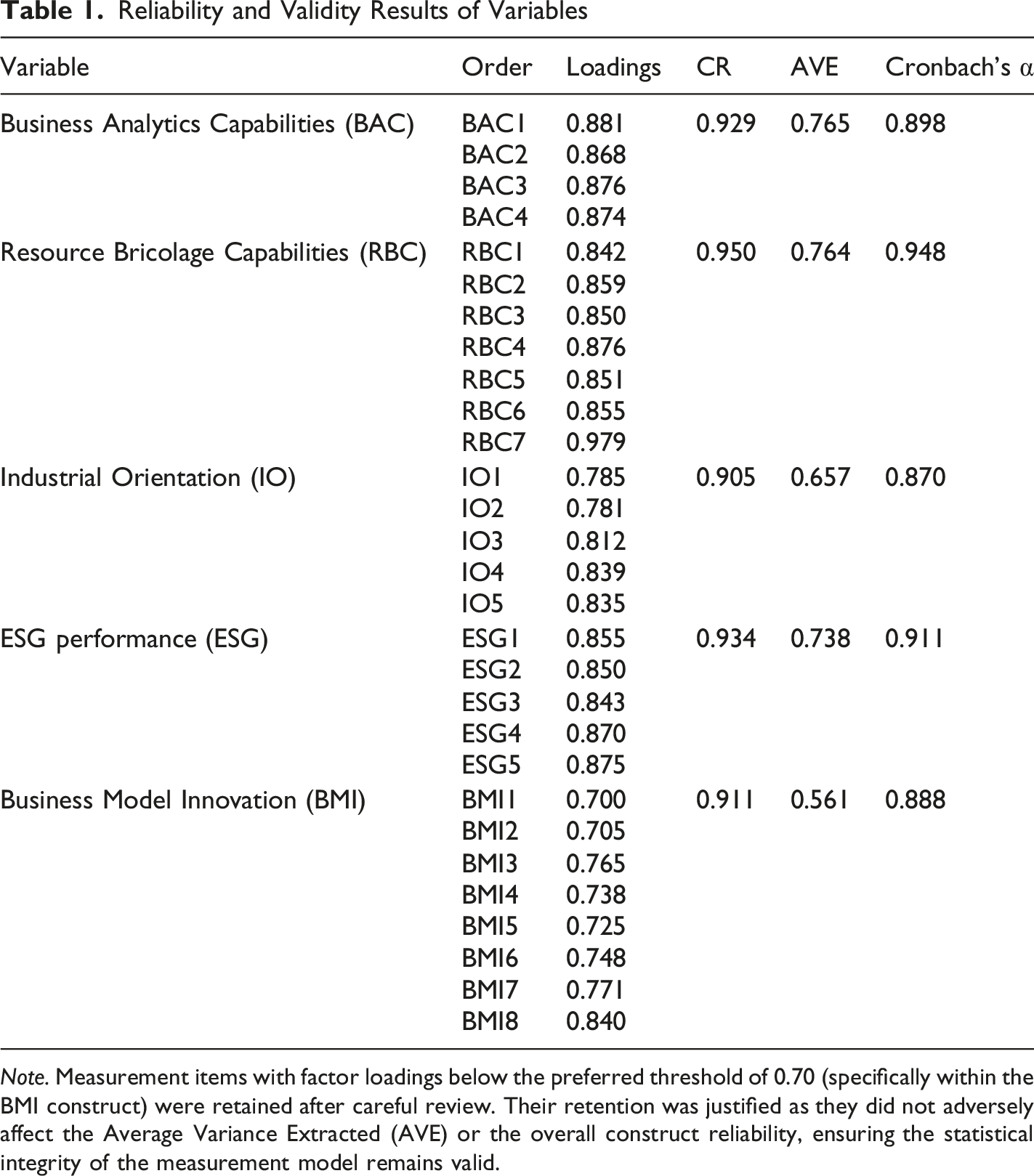

The measurement tools used in this study were sourced from established academic literature. A 5-point Likert scale was utilized for measurement, with a score of 1 indicating a very low degree and a score of 5 representing a very high degree. The survey instrument was adapted from previous research. The BAC was measured using four items Demirkan and Delen (2013). The seven-item resource bricolage scale from Senyard et al. (2014) was applied. Industrial orientation was assessed using five items from Ellis (2010). ESG performance was evaluated using five elements from Lateef and Keikhosrokiani (2023). Eight items from Zott and Amit’s (2013) and Pedroni’s studies were used to measure BMI. Following the resource-based theory (RBT), these constructs are operationalized as strategic intangible resources that facilitate competitive advantage.

Reliability and Validity Results of Variables

Note. Measurement items with factor loadings below the preferred threshold of 0.70 (specifically within the BMI construct) were retained after careful review. Their retention was justified as they did not adversely affect the Average Variance Extracted (AVE) or the overall construct reliability, ensuring the statistical integrity of the measurement model remains valid.

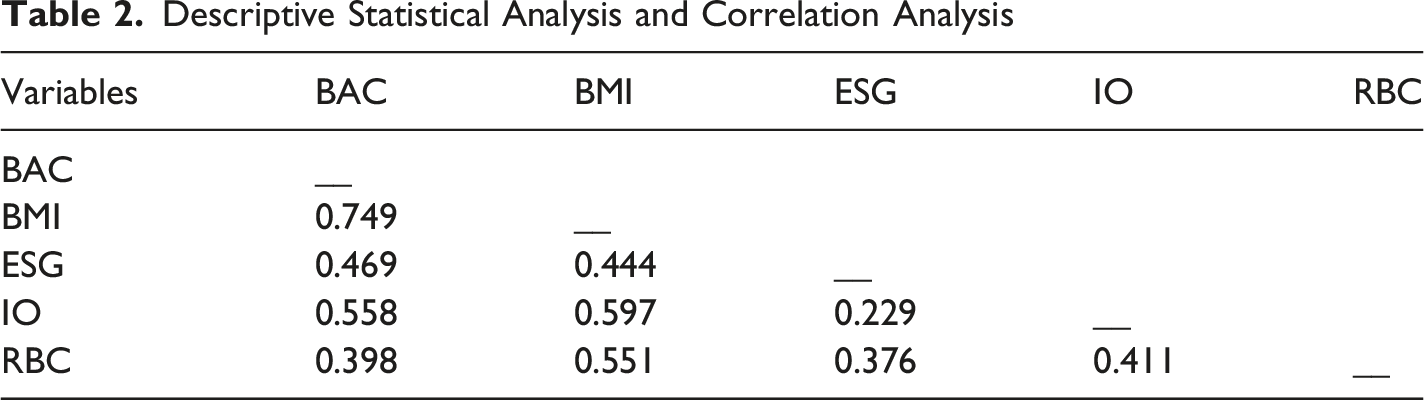

Descriptive Statistical Analysis and Correlation Analysis

Hypothesis Testing and Discussion

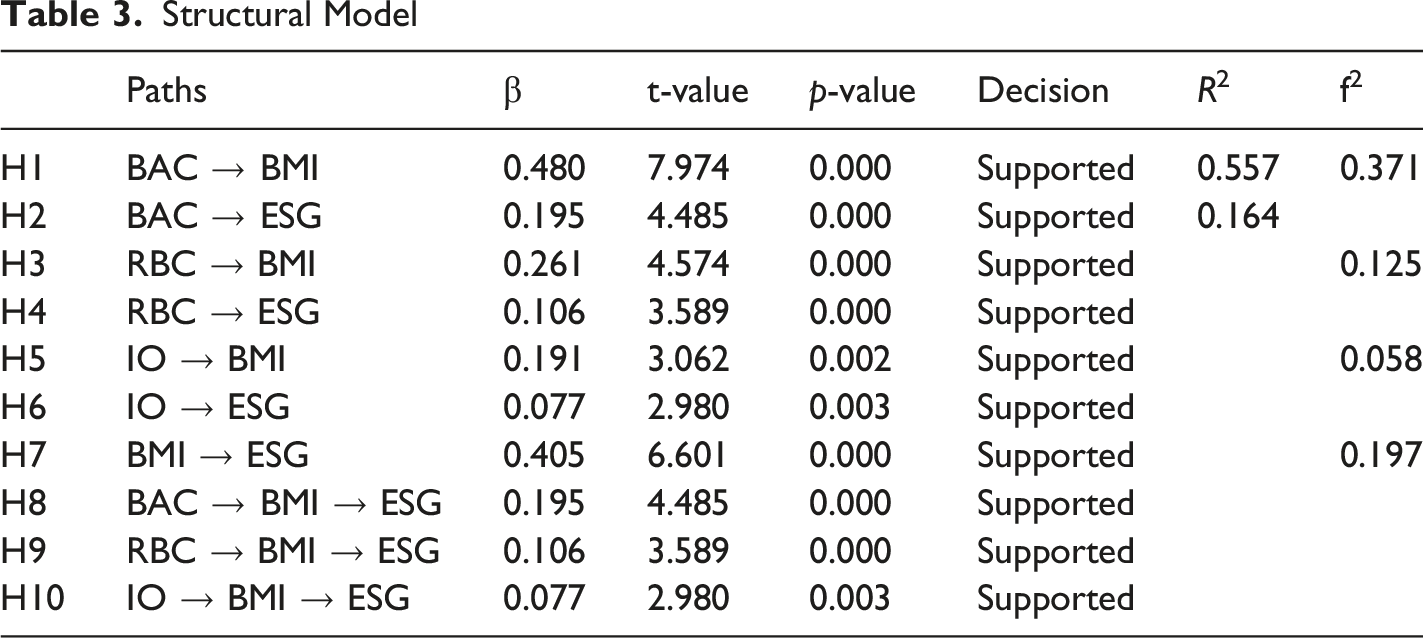

This study utilizes Partial Least Squares Structural Equation Modelling (PLS-SEM) via SmartPLS v4 to investigate how different organizational capabilities, namely, business analytics, resource bricolage, and industrial orientation, relate to BMI and ESG performance. The results help clarify the nuances through which internal capabilities lead to innovation and sustainability, drawing on the RBT and dynamic capabilities perspectives. By identifying these capabilities as strategic, value-creating resources, the study provides empirical evidence for RBT, showing how internal assets translate into competitive advantage and sustainability outcomes within the Chinese digital economy.

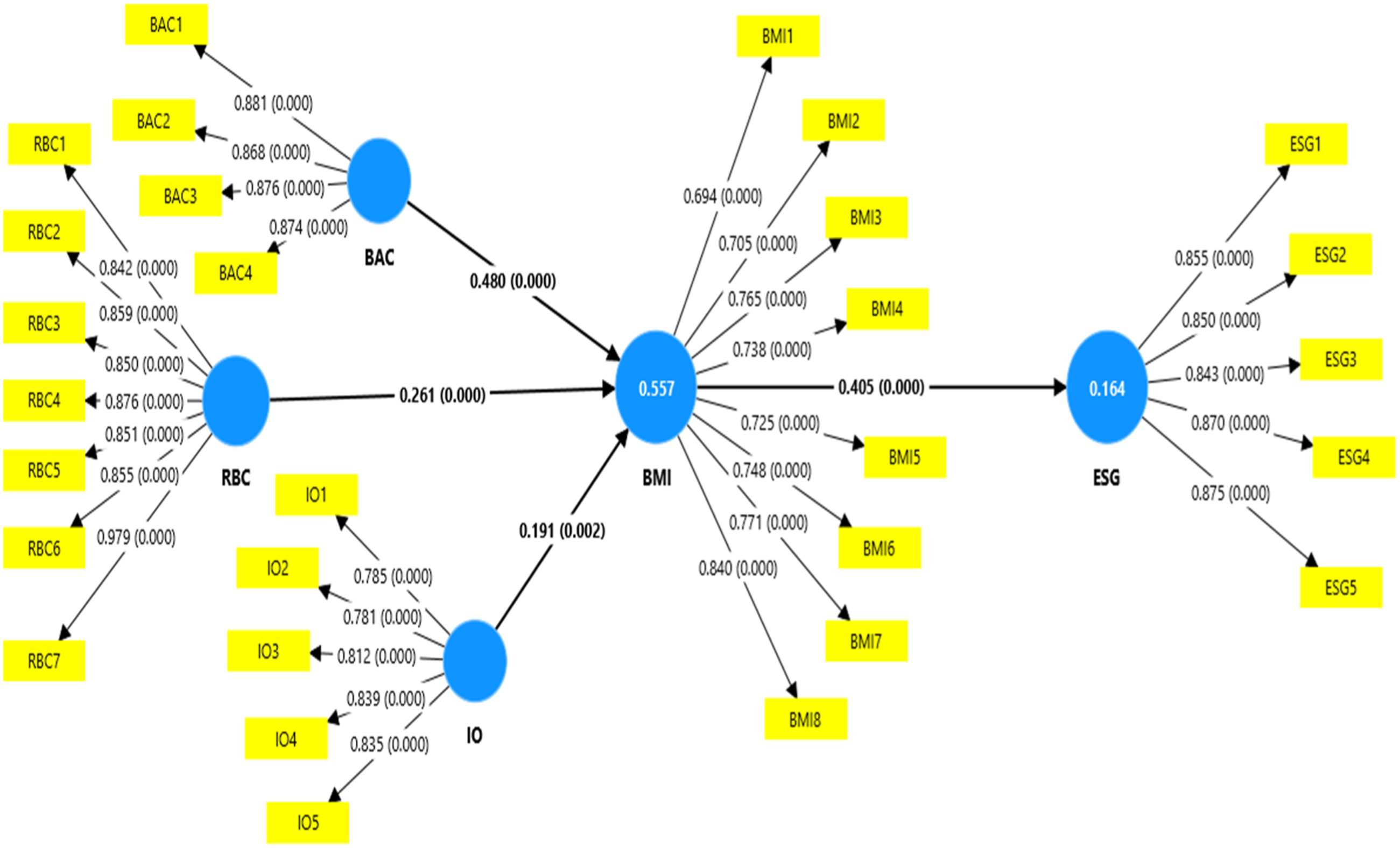

The empirical analysis indicates that BAC positively influence both BMI and ESG performance, confirming hypotheses H1 and H2. This suggests that business analytics-centric firms are best positioned to improve value propositions, segment consumers, and strengthen revenue models, thereby stimulating BMI (beta = 0.480, t = 7.974, p = 0.000) and directly improving ESG performance (beta = 0.195, t = 4.485, p = 0.000). This aligns with the perspective whereby a data-driven decision environment is foundational to driving organizational innovation and targeted sustainability initiatives.

The highly positive significance of RBC on BMI (beta = 0.261, t = 4.574, p = 0.000) and on ESG performance (beta = 0.106, t = 3.589, p = 0.000) validates hypotheses H3 and H4. These findings are consistent with literature regarding the creative reuse of resources in resource-constrained contexts. Resource bricolage gives organizations the flexibility to recombine customer relationships, channels, and operational processes in response to evolving environments. These results expand on foundational bricolage frameworks to demonstrate its relevance beyond basic entrepreneurial survival, showcasing its domain-generality in driving structured ESG-related outcomes.

In a similar vein, IO was found to be positively and significantly related to BMI (beta = 0.191, t = 3.062, p = 0.002) and ESG performance (beta = 0.077, t = 2.980, p = 0.003), supporting hypotheses H5 and H6. A strong industrial orientation allows for the early identification of key market trends and stakeholder expectations, enabling strategic alignment with sustainability requirements. This resonates with the market-facing literature suggesting that organizations oriented toward their broader industrial ecosystem are better equipped to integrate sustainability into their strategic frameworks.

Crucially, the structural model highlights the vital role of BMI as a direct driver of sustainability outcomes, as evidenced by the support for H7 (beta = 0.405, t = 6.601, p = 0.000). Beyond its direct effects, BMI’s significance as an enabler of sustainable outcomes is reflected by its supporting role in mediating the relationships between organizational capabilities and ESG performance. The indirect path mediation hypotheses for BAC (beta = 0.195, t = 4.485, p = 0.000) and RBC (beta = 0.106, t = 3.589, p = 0.000) were both supported, demonstrating that BMI enables organizations to successfully translate analytical insights and resource improvisations into stronger ESG results. These results build on dynamic capabilities literature by demonstrating that BMI itself acts as a dynamic capability that facilitates deploying core competencies toward reaching a desired future state of sustainability.

Structural Model

Conclusion and Implications

This study emphasizes the role of organizational capabilities, business analytics, resource bricolage, and industrial orientation, in enhancing BMI and ESG performance, thus contributing to the ongoing theoretical discourse surrounding RBV and dynamic capabilities. Although previous research has focused on these capabilities in isolation, we integrate them into a unified framework and explore their interrelated relationships (Figure 2). Structural model

Theoretical Contributions

This research contributes to the RBV literature by showing how resource-base functions as a complementary resource-deployment mechanism that optimizes the use of current resources in a constrained environment. Specifically, by identifying these capabilities as strategic VRIN (Valuable, Rare, Inimitable, and Non-substitutable) resources, the study provides a stronger theoretical anchor for how intangible assets drive sustainability. Previous research has examined bricolage primarily in entrepreneurial contexts (Baker & Nelson, 2005); this work extends its applicability to businesses transforming their operations with an ESG focus.

Additionally, by connecting BAC to both BMI and ESG performance, the study builds on the literature on data-driven insights leading to sustainable competitive advantages (El-Kassar & Singh, 2019), where a dichotomy exists, providing more fine-grained explanations of this phenomenon. Moreover, the findings contribute to dynamic capabilities theory through their emphasis on the mediating role of BMI. However, the non-significant mediating role of BMI in the relationship between industrial orientation and ESG (H10) offers a critical theoretical nuance. It suggests that certain strategic orientations can achieve ESG goals directly through operational compliance and stakeholder forecasting, bypassing the need for structural business model changes. This refines the argument that BMI’s role is contingent on the type of organizational capability and external market forces.

Practical Implications

The findings of this study offer several actionable insights for managers and organizational leaders, particularly those operating within the transitionary digital economy of China.

First, operationalizing broad digital strategies requires a shift from mere technology adoption to strategic integration. Managers should leverage Business Analytics Capabilities (BAC) not just for market forecasting, but as a tool for internal governance and social responsibility. For instance, broad analytical strategies can be operationalized to reduce cognitive biases in Human Resource Management (HRM). By utilizing data-driven performance metrics and algorithmic screening, firms can minimize subjective prejudices in hiring and promotion processes. This is particularly relevant for the integration of underrepresented groups, such as women and immigrants, ensuring that talent acquisition is based on objective merit and “Green Knowledge Sharing” potential rather than demographic stereotypes.

Second, managers should utilize Resource Bricolage as a mechanism for inclusive innovation. In resource-constrained environments, leaders are encouraged to empower decentralized teams to “make do” with available resources. Operationally, this involves fostering a “Creativity Mindset” where diverse team members—regardless of their background—are given the autonomy to recombine existing assets. This not only flattens rigid, bias-prone hierarchies but also facilitates a more inclusive organizational structure where diverse perspectives drive ESG-centric outcomes.

Finally, the study suggests that for Industrial Orientation to yield ESG returns, it must be integrated into the firm’s core strategic forecasting. Managers should move beyond viewing ESG as a compliance burden and instead treat it as a market-sensing tool. By operationalizing stakeholder engagement through digital platforms, firms can proactively identify environmental risks and social expectations, thereby enhancing their ESG performance without necessarily requiring a high-cost overhaul of their existing business models.

Limitations and Directions for Future Research

Although this study offers important insights, it has its limitations. BMI is a multidimensional construct, and the concept of BMI includes operational aspects, value-chain transformation, and strategic transformation. However, this study treats BMI as a one-dimensional construct. Future studies should disaggregate BMI to better appreciate the complexities of its effects. The cross-sectional nature of the data also limits causal inferences; longitudinal research design, such as time-lagged or wave studies, could reveal temporal dynamics. Moreover, extra reliance on survey data results in possible self-report bias. Mixed-method approaches would help to validate and add depth to findings, for example, using case studies or secondary data. Also, the study could show differences between industries in terms of when/why/how these capabilities work, providing a more fine-tuned understanding of their effects, enabling companies from different sectors to pursue contextual strategies.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Princess Nourah bint Abdulrahman University Researchers Supporting Project number (PNURSP2026R869), Princess Nourah bint Abdulrahman University, Riyadh, Saudi Arabia.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.