Abstract

This study examines the frequency, nature, and effects of coerced debt, defined as non-consensual, credit-related transactions that occur in intimate relationships where one partner uses coercive control to dominate the other. The sample includes 1,823 women who called the National Domestic Violence Hotline. Results suggest that coerced debt, from both coercive and fraudulent transactions, is a common problem and is significantly related to control over financial information, credit damage, and financial dependence on the abuser. This study supports the need for policy reform and victim services aimed at addressing coerced debt, thereby mitigating a potentially significant economic barrier to safety.

Introduction

Researchers estimate that between 94 and 99% of women 1 seeking services for intimate partner violence (IPV) have experienced economic abuse (Adams, Sullivan, Bybee, & Greeson, 2008; Postmus, Plummer, McMahon, Murshid, & Kim, 2011). Economic abuse involves behaviors that control a woman’s ability to acquire, use, or maintain economic resources, thus threatening her financial security (Adams et al., 2008). In an effort to exert control, batterers restrict access to economic resources by interfering with employment, dictating spending, and regulating access to financial information, among other tactics. Abusers also exert control by exploiting their partners’ resources. For instance, abusers steal their partners’ money or property, “freeload” by refusing to contribute income to expenses, and generate debt in their partners’ names through fraud or coercion (Adams et al., 2008). This last form of exploitation—generating debt through fraud or coercion—has been termed “coerced debt,” and research on this particular pernicious type of economic abuse is in its infancy. In the first study of coerced debt, Littwin (2012) interviewed lawyers and advocates, establishing its existence and showing how it operates in a variety of circumstances. The current study built on Littwin’s original research by examining the frequency, nature, and consequences of coerced debt from the perspective of survivors, using a sample of callers to the National Domestic Violence Hotline (NDVH).

“Coerced debt” is defined as all non-consensual, credit-related transactions that occur in an intimate relationship where one partner uses coercive control to dominate the other partner (Littwin, 2012). Coercive control is the defining characteristic differentiating “situational violence,” in which a couple uses violence as a problem-solving strategy, from IPV involving an underlying dynamic of dominance (M. P. Johnson, 2006; Pence & Dasgupta, 2006; Stark, 2007). In his pioneering book, Coercive Control, Evan Stark (2007) explains coercive control as the systematic, ongoing use of violence, intimidation, isolation, and control to restrict the victim’s autonomy. Dutton and Goodman (2005) explicate the mechanisms of coercive control by describing it as “a dynamic process linking a demand with a credible threatened negative consequence for noncompliance” (pp. 746-747). The theory posits that abusers make demands across diverse domains of their partners’ lives, including personal activities/appearance, social/family life, children, household management, intimate relationship, legal, immigration, and economic/resources. Consequences for noncompliance include tacit or explicit threats of physical, psychological, and/or economic harm (Dutton, Goodman, & Schmidt, 2006). Threats that are deemed credible based on past behavior compel victims to act in accordance with the demands, subordinating their own interests, desires, and values. Coercive control is a liberty crime (Stark, 2007). By coercively controlling their partners’ actions, abusers restrict women’s autonomy, freedom, or space for action (Sharp-Jeffs, Kelly, & Klein, 2017).

According to Littwin (2012), this broader context of coercive control enables abusers to generate debt in their partners’ names through discrete transactions involving coercion or fraud. Using coercive control, an abuser creates an environment in which refusing a demand or questioning behavior is dangerous. If “asked” to assume sole responsibility for a lease or utility service, sign for a loan, take out a credit card, or buy an item on credit, the victim does so or risks harm (coercive transactions). If he uses her personal information to take out credit in her name without her knowledge (fraudulent transition) and she suspects or discovers the debt, confronting him or reporting the fraud—as one might do in a non-abusive relationship—means risking harm (Littwin, 2012). This dynamic was captured in a recent qualitative study of economic abuse in which women reported that they “felt powerless over an abuser’s financial behavior due to the fear and threat of reprisal” (Sanders, 2015, p. 19).

Evidence of the existence of coerced debt has emerged in several existing studies. In a qualitative study of 187 women stalked by former intimate partners, Brewster (2003) found that 22.5% had abusive partners who exerted financial control over them, and one of the ways they did that was by opening credit cards in their partners’ names. In their research to develop the Scale of Economic Abuse (SEA), Adams and colleagues (2008) included several items that although not explicitly intended to do so, captured elements of coerced debt. For example, of the 103 women seeking services for domestic violence who were interviewed, 39% reported that their partner had built up debt under their name by doing things like putting a car, apartment/house, or credit card in their name; 53% reported that their partner had used their checkbook, ATM card, or credit card without their permission and/or knowledge; and 68% reported that their partner had forced them to give him money or let him use their checkbook, ATM card, or credit card. Sanders (2015) reported a common theme among participants of accumulating debt and damaged credit because of abuse. The connection between abuse and debt is substantiated by findings from the 2007 Consumer Bankruptcy Project (CBP) showing that 17.8% of the 258 married and cohabitating female participants experienced intimate partner abuse in the year they filed for bankruptcy, a rate much higher than the 1.5% to 9.8% annual rates of abuse reported in studies with samples of women most comparable with that of the CBP (Littwin, 2012; Tjaden & Thoennes, 2000). Finally, in the only study to date explicitly focused on coerced debt, Littwin (2012) found that of the 55 domestic violence professionals interviewed, 51 (93%) had knowledge of coerced debt based on their work with survivors. For example, participants shared stories of women whose partners forged their names on credit card offers that had arrived in the mail, forced them to sign financial documents against their will, coerced them to purchase items on credit, and required that household debts be in their names.

Littwin’s original study also surfaced key correlates of coerced debt. Participants recounted how abusers concealed the existence and extent of coerced debt by engaging in controlling behaviors such as hiding mail and prohibiting access to financial accounts. Restricting access to financial information is a tactic of economic abuse that has been reported elsewhere (Adams et al., 2008; Brewster, 2003; Postmus et al., 2011; Sanders, 2015), and Littwin characterized it as foundational to the establishment of coerced debt (Littwin, 2012). Whether by hiding the existence of coerced debt or some other form of direct or indirect prohibition, abusers kept their partners from paying on coerced debts in a timely manner or at all. When coerced debts went unpaid, damaged credit was the result. Littwin noted that a troubled credit history or score would not be as problematic if credit reports were used only by traditional lenders. However, the reality is that employers, landlords, and utility companies make extensive use of credit reports and scores in screening potential employees, tenants, and customers, which can prevent victims from obtaining jobs, housing, and basic utilities. If the victim is aware of the debt and is paying on it, this added financial obligation restricts the resources available to meet other needs. With damaged credit and limited money, starting a new life away from an abuser becomes extremely difficult. Studies consistently show that lack of financial resources is a primary reason women remain in abusive relationships (Aguirre, 1985; Anderson & Saunders, 2003; I. M. Johnson, 1992; Kim & Gray, 2008; Matlow & DePrince, 2015).

Research conducted with human service and legal professionals provided initial evidence of the problem of coerced debt, how it happens, and the effects it has on victims’ lives (Littwin, 2012). Investigations of women’s direct experiences of coerced debt are now needed to advance our understanding of this dramatically underresearched form of economic abuse. As an initial step toward filling this gap, the current study builds on Littwin’s study by using a sample of IPV survivors seeking help from the NDVH to investigate central research questions surfaced by Littwin. Specifically, the current study examines the following six foundational research questions: (1) How common is coerced debt generated via coercive and fraudulent transactions? (2) What types of consequences do survivors expect for failing to comply with abusers’ demands to take on debt? (3) How do women discover coerced debt generated via fraudulent transactions? (4) Are women with partners who control access to financial information more likely to have coerced debt? (5) Are women with coerced debt more likely than women without coerced debt to report credit damage due to an intimate relationship? and (6) Are women with coerced debt more likely to stay in an abusive relationship longer due to financial concerns than women without coerced debt? Answers to these questions will move the field forward toward understanding and addressing the extent and effects of coerced debt in women’s lives.

Method

Participants and Procedures

The study used a convenience sample of callers to the NDVH over an 8-week period in the summer of 2014. Callers were eligible to participate if they identified as female and an IPV survivor and were at least 18 years old. At the end of the call, if the caller was not in crisis and met the eligibility criteria, the trained advocate who took the call read a scripted statement explaining the survey and asking if the caller was willing to participate. The NDVH provided the researchers with a de-identified data set after data collection was complete.

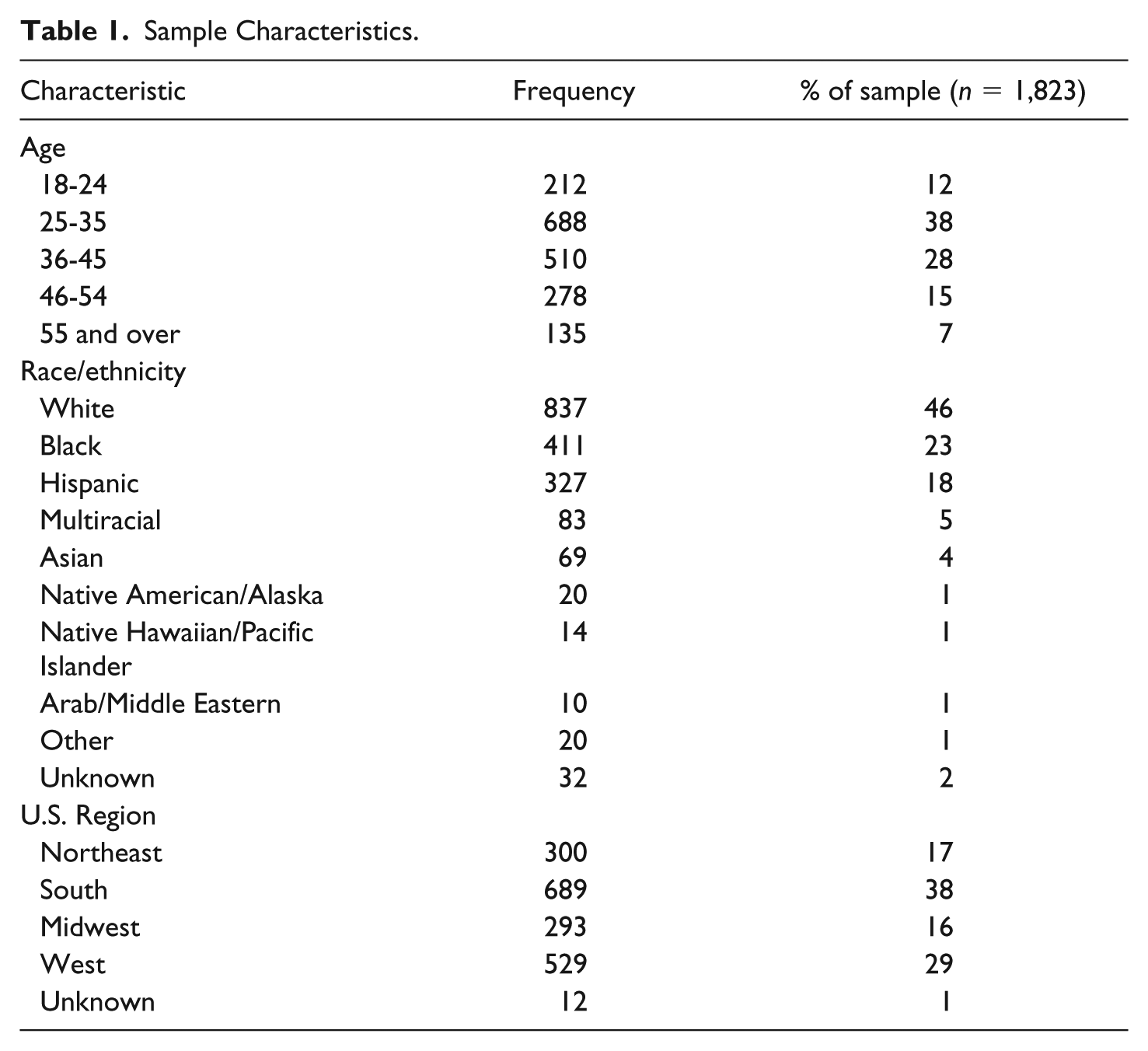

Out of 10,232 calls received during the data collection period, 8,003 callers met the eligibility criteria, and 1,863 participated in the survey. Forty of these were excluded because they lived outside of the United States, and issues of debtor–creditor law are country-specific. Our final sample consisted of 1,823 women. As shown in Table 1, most participants were between the ages of 25 and 45 (66%), and reported their race/ethnicity as non-Hispanic white (46%) or black (23%). Geographically, the majority of participants were from the South (38%) or West (29%) of the United States. The demographic characteristics of the callers who participated in the study were proportionally equivalent to those of all eligible callers during the data collection period, indicating that the sample was representative of hotline callers.

Sample Characteristics.

Measures

The instrument used in this study was developed specifically to assess coerced debt and its effects among hotline callers. Instrument length and ease of administration were prioritized to minimize the burden on the hotline advocates and callers. As such, measures were restricted to single “yes/no” items and limited open-ended questions. To maximize data quality, the advocates received training on how to administer the instrument prior to the start of the study.

Coerced debt

Coerced debt was measured with a series of three questions. Based on the conceptual work of Dutton and Goodman (2005), two questions were asked to assess for a coercive transaction. The occurrence of a demand was measured using a single, yes/no question asking, “Has an intimate partner ever convinced or pressured you to borrow money or buy something on credit when you didn’t want to?” If the caller answered “yes” to the demand question, the occurrence of a perceived consequence for non-compliance with the demand was assessed with the following question: “What did you think would happen if you said ‘no?’” Qualitative responses were coded 0 = no consequence, 1 = consequence. The occurrence of a fraudulent transaction was measured with a single, yes/no question asking, “Have you ever found out about debt or bills that an intimate partner put in your name without you knowing?” Responses were coded 0 = no, 1 = yes. The coerced debt variable was operationalized as the occurrence of either a coercive or fraudulent transaction, with 0 = no and 1 = yes.

The open-ended responses to the consequences for non-compliance question described above were thematically coded to indicate the nature of the consequence. An initial round of coding produced three broad, mutually exclusive thematic categories: physical, psychological, and economic. “Physical consequences” were defined as threats of bodily harm to the victim or the victim’s loved ones. “Psychological consequences” were defined as threats of emotionally distressing actions. “Economic consequences” were defined as threats of the loss of financial and material resources. A second round of coding was conducted to assign each response to the appropriate categories.

Discovery of a fraudulent transaction

Fraud discovery method was assessed by asking the following open-ended question to hotline callers who reported a fraudulent transaction: “How did you find out about the debt or bills?” Two coders themed the responses, and disagreements were reconciled with input from a third coder. A categorical “fraud discovery” variable was created based on the thematic analysis.

Control over financial information

Control over financial information was measured with a single, yes/no question asking, “Has an intimate partner ever kept financial information from you?” Responses were coded 0 = no, 1 = yes, indicating whether or not the hotline caller had a partner who kept financial information from her.

Credit damage

Credit damage was measured with one question: “Has your credit report or credit score been hurt by the actions of an intimate partner?” The response options included yes, no, and not sure. For the inferential analyses, “not sure” responses were coded as “no” resulting in a dichotomous variable, coded 0 = no, 1 = yes, indicating whether or not the hotline caller had her credit report or score hurt by the actions of an intimate partner.

Financial dependence

Financial dependence was measured using a single, yes/no question asking, “Have you ever stayed longer than you wanted in a relationship with someone who was controlling because of concerns about financially supporting yourself or your children?” Responses were coded 0 = no, 1 = yes, indicating whether or not the hotline caller ever stayed longer than desired in a relationship with someone who was controlling because of financial concerns.

Control variables

Age and race/ethnicity were controlled for in this study, as both characteristics could affect women’s financial well-being. Age and race/ethnicity questions did not appear on the survey; instead, the variables were generated for use in this study based on the demographic information routinely collected for all hotline callers. The age variable was ordinal, with the following categories: 18-24, 25-35, 36-45, 46-54, and 55 and over; “55 and over;” was used as the reference category. The nominal race variable had the following categories: non-Hispanic White, Black, Arab/Middle Eastern, Asian, Hispanic, Native American/Alaska Native, Native Hawaiian/Pacific Islander, multiracial, and other. For the planned inferential analyses, the categories with a low percentage were combined into the “other” category, resulting in a four-category variable: White, Black, Hispanic, and other; “White” was used as the reference category.

Data Analysis

Frequency analysis was performed to answer research questions 1-4 regarding the prevalence and nature of coerced debt. Logistic regression was conducted to answer research questions 4-6 regarding the likelihood of coerced debt for women with partners who control access to financial information; the likelihood of having damaged credit due to the actions of an intimate partner for women with coerced debt; and the likelihood of financial dependence for women with coerced debt.

In preparation for the logistic regression, missing values analysis was performed and the missing values were imputed using expectation maximization. Missing values analysis revealed 3.4% missing values on the variables of interest. Little’s Missing Completely at Random (MCAR) test was significant, indicating that the missing values were not MCAR. Further bivariate analysis showed no significant relationship among the missing values, suggesting that the data were missing at random. Expectation maximization methods were used to estimate the missing values. All analyses were conducted with SPSS version 24.

Results

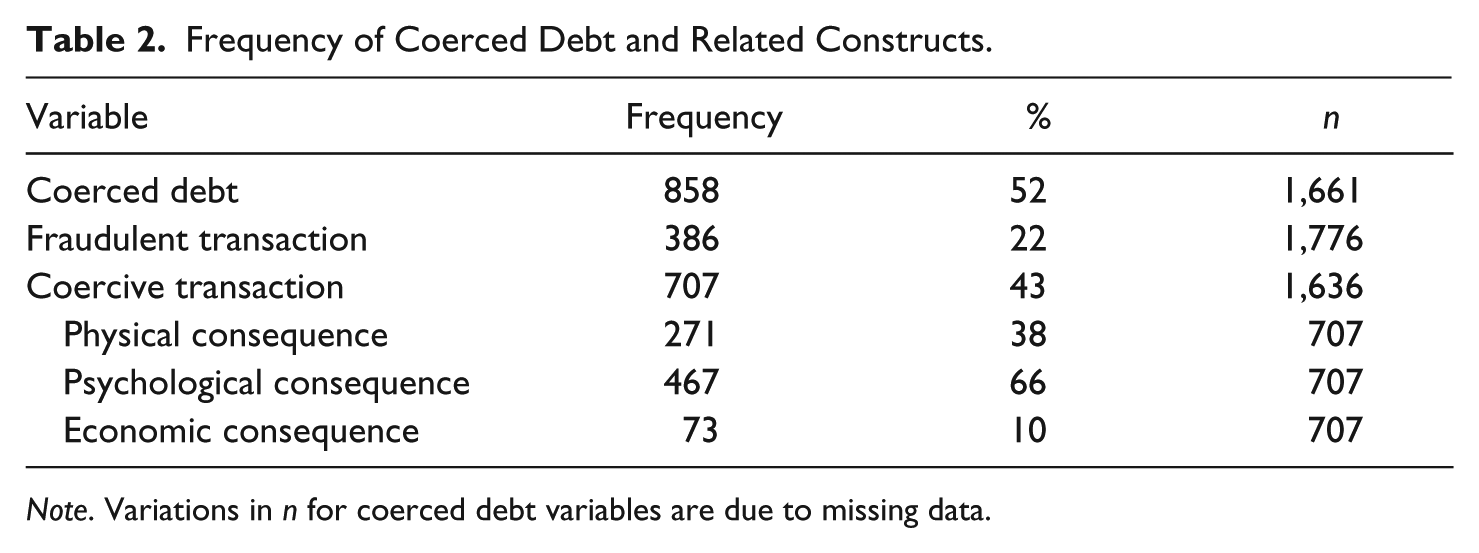

As shown in Table 2, 52% of callers to the NDVH who participated in this study reported coerced debt. In other words, half of participants had partners who generated debt in their name via a coercive and/or fraudulent transaction.

Frequency of Coerced Debt and Related Constructs.

Note. Variations in n for coerced debt variables are due to missing data.

A coercive transaction was reported by 43% of the total sample and 87% of the callers who reported either type of coerced debt. When asked what they thought would happen if they did not comply with their partner’s request to take out a loan or buy something on credit, most of the respondents (66%) who disclosed a consequence described fearing psychological consequences, such as name calling, yelling and screaming, or threatening to end the relationship. Over a third (38%) of participants who disclosed a consequence cited fear of physical consequences for saying “no,” including being beaten or killed. Ten percent (10%) explained that they feared some form of economic consequence, such as job, money, or property loss, if they did not do as their partner wished.

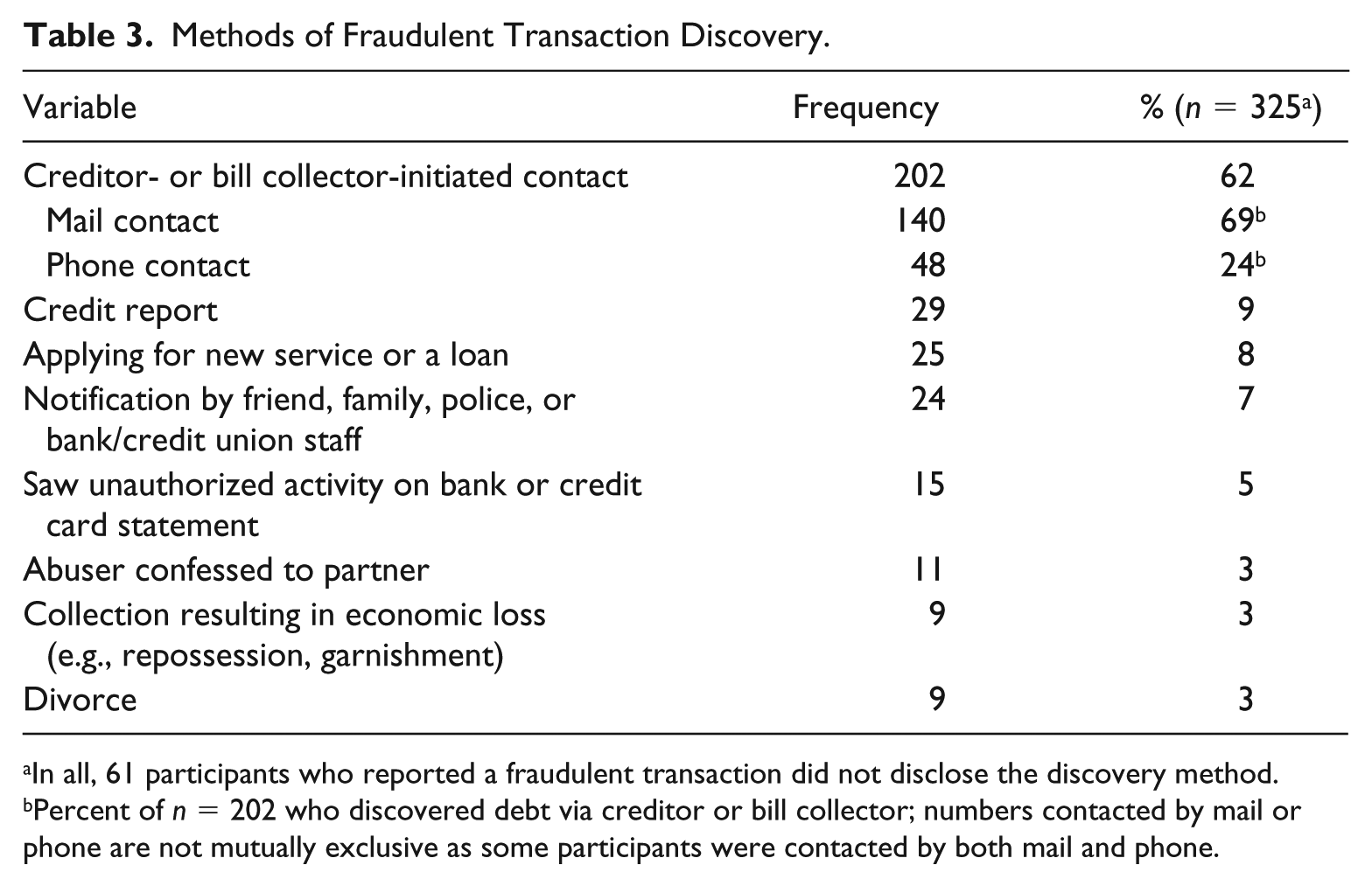

A fraudulent transaction was reported by 22% of all respondents and 46% of callers who experienced coerced debt. Of the callers who disclosed how they discovered the fraud, 62% said they learned of it through creditor- or bill collector-initiated contact. Of those, 69% reported receiving notice of the debt via mail and 24% reported receiving a call from the creditor or bill collector. A quarter of the women who reported learning of the debt via mail described finding the mail, as opposed to directly receiving it. For example, participants mentioned finding bills after a move or change of address, receiving bills sent to them by mistake, discovering bills when the abuser missed them or was away, obtaining the mail before the abuser, finding bills in the trash, and receiving bills after the relationship had ended. Other noteworthy ways callers learned of the debt were through reviewing their credit report (9%); applying for a new service or loan (8%); notification of the debt by a friend, family member, the police, bank, or credit union personnel (7%); seeing unauthorized activity on a bank or credit card statement (5%); abuser confession to the debt (3%); an economic loss such as property repossession or wage garnishment (3%); and through the divorce process (3%). The methods of fraud discovery are summarized in Table 3.

Methods of Fraudulent Transaction Discovery.

In all, 61 participants who reported a fraudulent transaction did not disclose the discovery method.

Percent of n = 202 who discovered debt via creditor or bill collector; numbers contacted by mail or phone are not mutually exclusive as some participants were contacted by both mail and phone.

Control over financial information, financial dependence, and abuse-related credit damage were also commonly reported: 71% of callers said that their partner had kept financial information from them; 46% said their credit had been damaged by the actions of an abusive partner (another 14% said they were “not sure”); and 73% stayed longer in a relationship with someone who was controlling because of concerns about financially supporting themselves or their children.

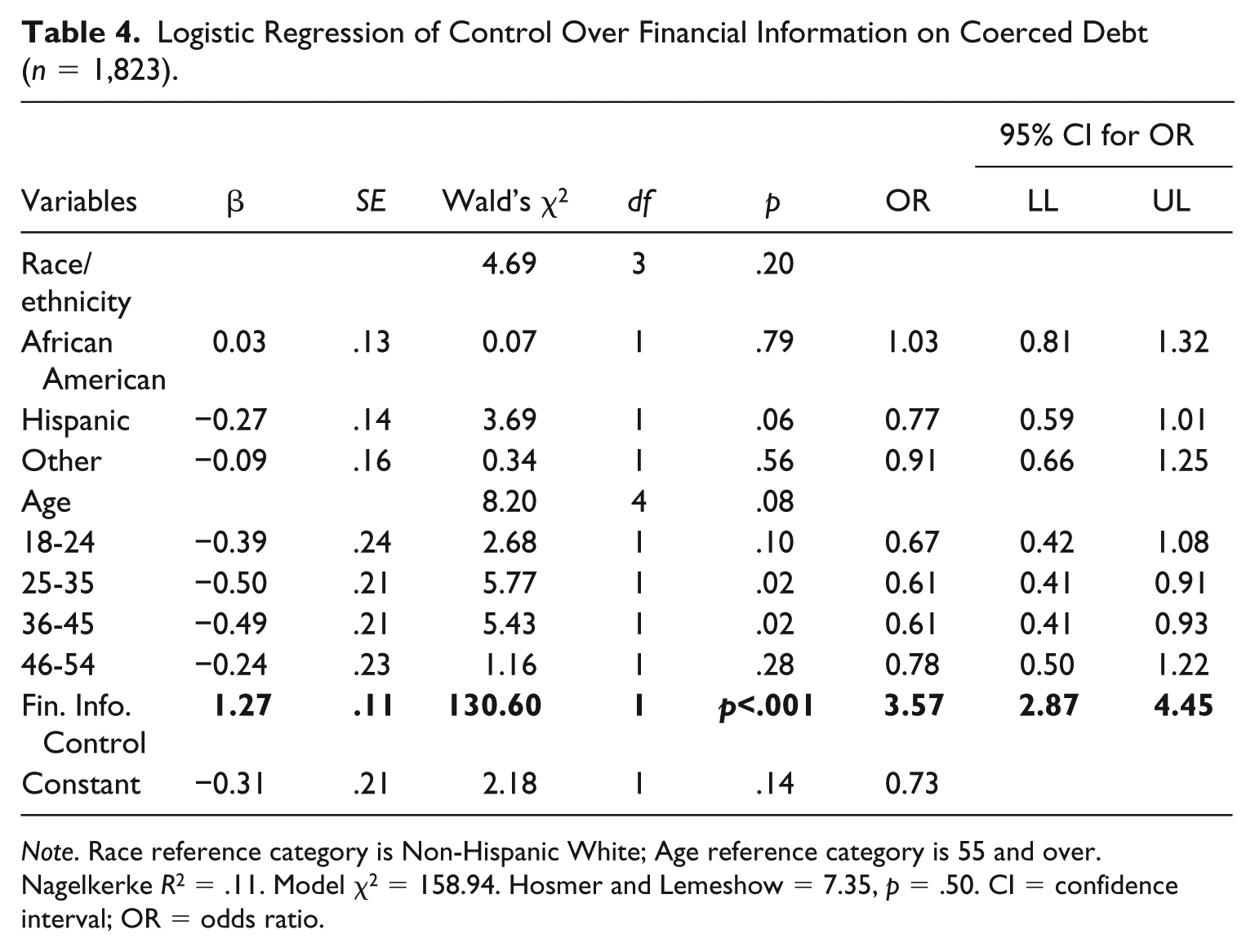

Table 4 provides the results of the logistic regression model predicting the likelihood of coerced debt based on whether abusers exerted control over financial information, controlling for race/ethnicity and age. After accounting for race/ethnicity and age, control over financial information significantly predicted the likelihood of having coerced debt (odds ratio [OR] = 3.57, p < .001). In other words, women with partners who hid financial information from them were 3.6 times more likely to have debt in their name due to a coercive or fraudulent transaction perpetrated by an intimate partner. The model predicted 11% of the variance in coerced debt (Nagelkerke R2 = .11). The Hosmer and Lemeshow test was non-significant, indicating good model fit.

Logistic Regression of Control Over Financial Information on Coerced Debt (n = 1,823).

Note. Race reference category is Non-Hispanic White; Age reference category is 55 and over. Nagelkerke R2 = .11. Model χ2 = 158.94. Hosmer and Lemeshow = 7.35, p = .50. CI = confidence interval; OR = odds ratio.

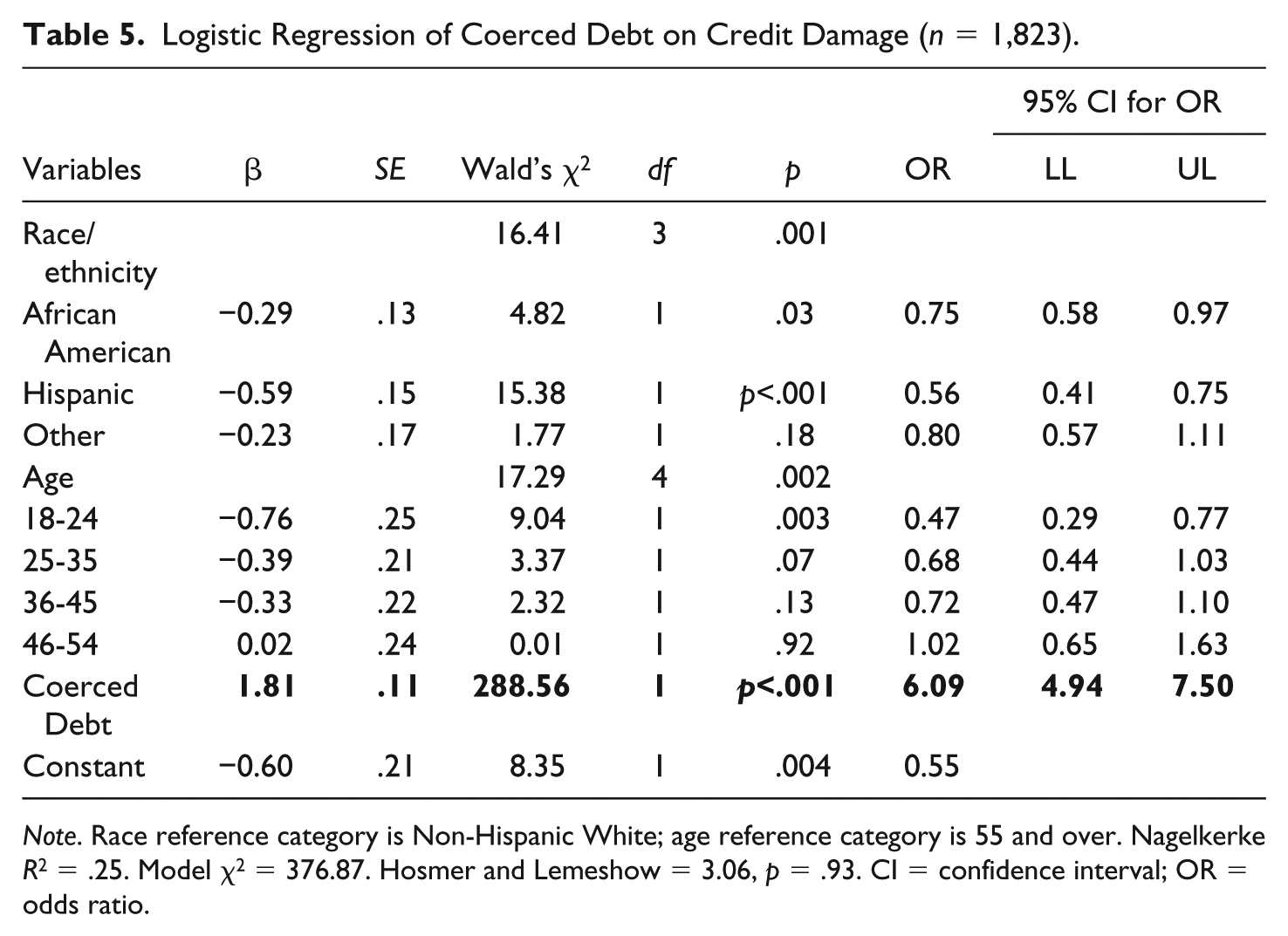

Table 5 summarizes the results of the logistic regression model predicting the likelihood of credit damage based on coerced debt. After accounting for race/ethnicity and age, coerced debt significantly predicted the likelihood of credit damage (OR = 6.09 p < .001), indicating that women with coerced debt were 6 times more likely to have their credit report or credit score hurt by the actions of an intimate partner. The model predicted 25% of the variance in credit damage (Nagelkerke R2 =.25). The Hosmer and Lemeshow test was non-significant, indicating good model fit.

Logistic Regression of Coerced Debt on Credit Damage (n = 1,823).

Note. Race reference category is Non-Hispanic White; age reference category is 55 and over. Nagelkerke R2 = .25. Model χ2 = 376.87. Hosmer and Lemeshow = 3.06, p = .93. CI = confidence interval; OR = odds ratio.

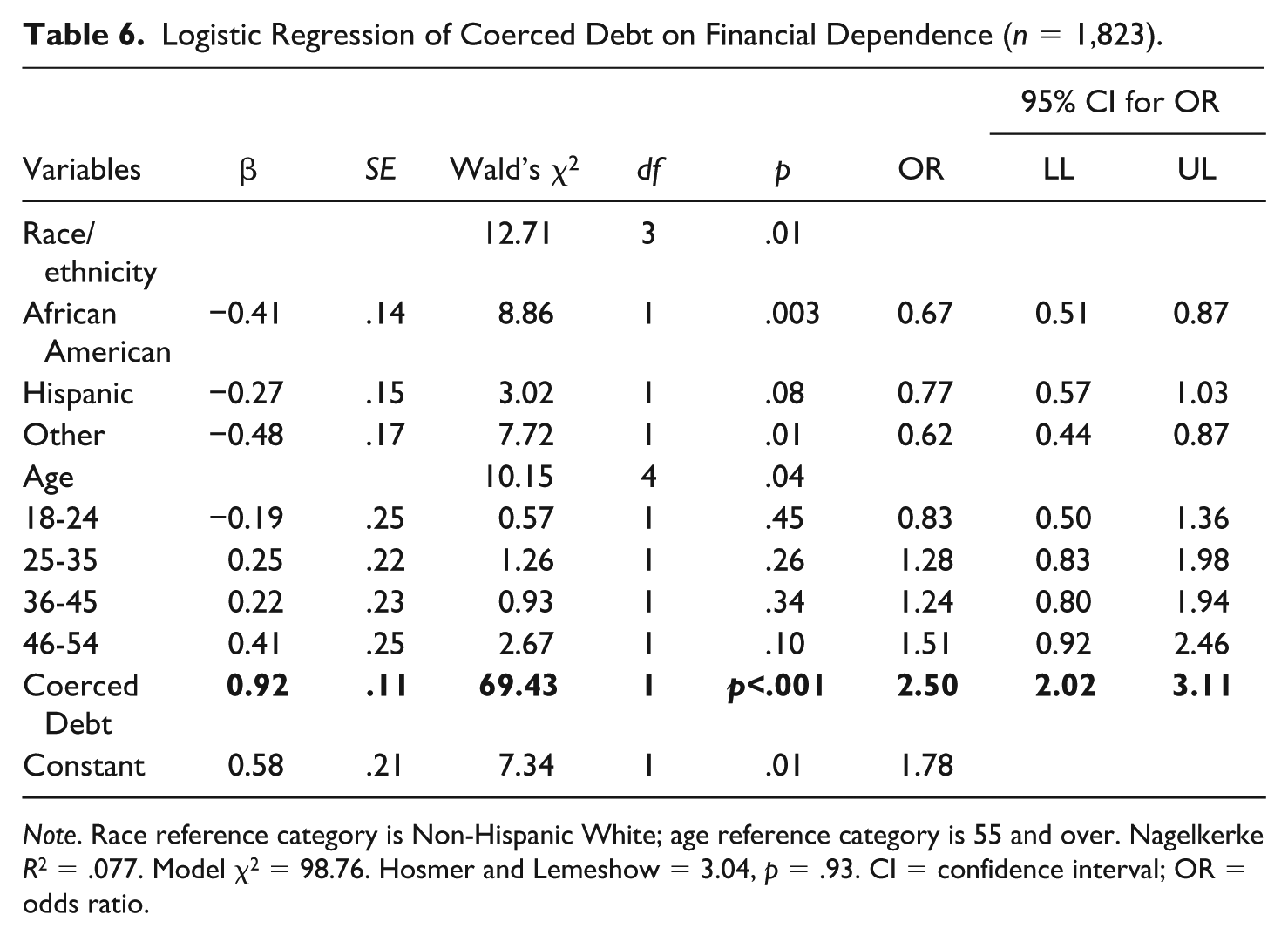

Table 6 shows the results of the logistic regression model predicting the likelihood of financial dependence based on coerced debt. After accounting for race/ethnicity and age, coerced debt significantly predicted the likelihood of financial dependence (OR = 2.50, p < .001). Women with coerced debt were 2.5 times more likely to have ever stayed longer than they wanted in a relationship with someone who was controlling because of concerns about financially supporting themselves or their children. The model predicted 7.7% of the variance in financial dependence (Nagelkerke R2 =.077). The Hosmer and Lemeshow test was non-significant, indicating good model fit.

Logistic Regression of Coerced Debt on Financial Dependence (n = 1,823).

Note. Race reference category is Non-Hispanic White; age reference category is 55 and over. Nagelkerke R2 = .077. Model χ2 = 98.76. Hosmer and Lemeshow = 3.04, p = .93. CI = confidence interval; OR = odds ratio.

Discussion

Evidence that IPV perpetrators generate debt in their partners’ names has been present in the research literature for some time (Adams et al., 2008; Brewster, 2003). Using qualitative methods, Littwin (2012) gave the phenomenon a name—coerced debt—and described its mechanisms and consequences as witnessed by professionals in the IPV field. The current study quantitatively examined research questions informed by Littwin (2012) from the perspective of IPV survivors themselves. Specifically, the current study examined the frequency, nature, and effects of coerced debt among women who sought help from the NDVH. The findings suggest that coerced debt is a common experience for women seeking help for intimate partner abuse, with about half (52%) of the sample reporting that their partner had put debt in their name either via a coercive and/or fraudulent transaction. A coercive transaction was reported by 43% of respondents, and about one in five women surveyed (22%) had discovered debt that a partner had generated in their name fraudulently. It is important to note that the fraud rate may be an undercount because women who had not yet discovered an abuser’s fraud would answer this question negatively.

Hotline callers whose partners fraudulently put debt in their names most commonly reported discovering that debt through billing or collections activity, with most of them discovering it by mail. This is interesting because the results also showed that 71% of women surveyed had partners who hid financial information from them. This potential contradiction can be partially explained by the finding that a quarter of women reported finding mail in a way that suggested that they found it despite their partners’ attempts to hide the financial information.

The results also showed that respondents with a partner who hid financial information were 3.6 times more likely to have coerced debt. Abusers might hide financial information in a deliberate attempt to perpetrate, cover up, or keep their partners from paying on coerced debt (Littwin, 2012). Alternatively, they may hide financial information as part of their control tactics, for example, to create vulnerabilities in their partners, and only later realized that they had set the stage for coerced debt (Dutton & Goodman, 2005).

This study explored two possible consequences of coerced debt: credit damage and financial dependence. Credit damage due to the actions of an abusive partner was reported by 46% of the hotline callers surveyed; this figure is likely an underreporting given that another 14% were unsure if their credit had been damaged, and women who had not yet discovered fraudulent debt would not know of any damage to their credit reports. Respondents with coerced debt were 6 times more likely to have their credit damaged by the actions of an abusive partner. A relationship between coerced debt and credit damage was also found by Littwin (2012). Based on their experiences working with IPV survivors, the professionals interviewed for that study concluded that coerced debt negatively affects survivors’ credit. Coerced debt increases victims’ overall debt burden, and the extant economic abuse literature shows that abusers engage in an array of behaviors that would make it difficult for victims to pay their debts. For instance, abusers prevent their partners from earning money; they directly forbid debt payment; they steal or spend the money needed to pay bills; and they may hide the existence of the debt (Adams et al., 2008; Brewster, 2003; Littwin, 2012; Postmus et al., 2011; Sanders, 2015).

In addition to credit damage, this study showed that coerced debt is associated with financial dependence on the abuser. Nearly three quarters (73%) of women reported that they had stayed longer than they had wanted in a relationship with someone who was controlling because of concerns about financially supporting themselves or their children. Women with coerced debt were 2.5 times more likely to report financial dependence than women without coerced debt. In other words, the odds that financial dependence will occur is greater when coerced debt is present. An association between coerced debt and financial dependence was also reported by Littwin (2012). The findings from that study indicated that coerced debt can be a significant financial barrier to leaving an abusive relationship. It may be that one’s debt burden factors into the calculation of the relative advantages and disadvantages of remaining in versus leaving an abusive relationship.

The NDVH provided an opportunity to study coerced debt among a diverse, national sample of IPV survivors; however, there were limitations of the study design that warrant attention. Brevity and ease of administration were top considerations in designing the instrument. As such, strict limits were placed on the number and type of questions asked (i.e., quantitative measurement was restricted to dichotomous items). Survey length limits imposed a number of limitations on this study. First, the length limits necessitated restricting the operationalization of coercive transactions to those involving “borrowing money or buying something on credit.” We know from prior research that coerced debt can also result from the abuser demanding that household bills including utilities, rent, or phone service are in the survivor’s name (Littwin, 2012), but we were unable to ask explicitly about coerced debt generated by these means. Future studies should expand the operationalization of coerced debt to include this tactic as well. Second, the survey design parameters prevented a more nuanced investigation into the specific types of debt abusers generated, for example, credit cards, mortgage, auto loans, and payday loans. Future research should assess for fraud and coercion around specific types of transactions. One way to do this, which the authors are piloting in another study, is to review survivors’ credit reports with them, systematically assessing for coercion and fraud in the opening and use of each account. Third, limits on survey length hindered a more comprehensive assessment of consequences for non-compliance with a partner’s request to take out a loan or buy something on credit. The consequences element of coercion was assessed with one open-ended question. Although useful for surfacing the most salient consequence or consequences and determining if coercion occurred, this approach limits the conclusions that can be drawn from the data. Future research should assess each type of threat—psychological, physical, and economic—individually to permit examination of the occurrence and co-occurrence of each type. Fourth, survey length restrictions prevented the inclusion of questions to measure potential confounding variables beyond the basic demographics collected for all hotline callers. It may be that the observed scores on coerced debt, credit damage, and financial dependence were affected by variables not controlled for in the study. Future research should control for variables, such as income or the number of dependents, which could affect these dependent variables.

It should also be noted that women were asked to report coerced debt, control over financial information, abuse-related credit damage, and financial dependence experienced in any intimate relationships. It may be that these phenomena occurred within separate intimate relationships. Although the findings show that these experiences are meaningfully related, future studies should examine these associations within and across intimate relationships.

A final limitation for consideration stems from the use of a cross-sectional design. This design prohibited conclusions regarding the directionality of the relationships among the constructs of interest. Although this study is a step forward in advancing our understanding of the nature and effects of coerced debt, longitudinal, mixed-methods research is recommended to gain a fuller picture of the types and amounts of coerced debt incurred, the mechanisms by which the debt is generated, and the consequences of that debt for victims’ immediate and long-term financial security. For example, researchers could use a prospective or retrospective longitudinal design to collect interview data from IPV survivors with and without coerced debt to examine the effects of coerced debt on survivors’ economic well-being. To aid research in this area, a comprehensive screening tool is needed to obtain a systematic understanding of coerced debt. The screening tool should reference the survivor’s credit report to simultaneously enhance recall and provide documentation of important features of each coerced debt (i.e., payment history, borrowing history).

Limitations notwithstanding, this study has important practice and policy implications. The study shows that coerced debt is a common experience among women seeking help for IPV and is associated with damaged credit and financial dependence on the abuser. As such, agencies serving IPV survivors, including crisis hotlines, shelters, advocacy programs, and legal services, must be prepared to identify and address coerced debt. Crisis hotline advocates can be trained to listen for indicators of coerced debt and, when appropriate, refer the caller to IPV and legal services for assistance. Professionals who provide more intensive services can work with survivors to assess for coerced debt and devise strategies to address it and associated issues. Specifically, providers with economic advocacy training can help survivors gain access to personal financial information that might have been hidden from them and take stock of their assets and debts. They can assist by working with survivors to safely obtain their credit reports and review them for instances of coercion and fraud. Coercion can be identified by discussing whether debts were incurred as a result of an abuser’s demands and tacit or explicit threats of consequences for noncompliance. This study suggests that consequences may include threats of physical, psychological, or economic harm. Fraud may appear on credit reports as unfamiliar accounts or transaction history, or debt that the survivor is currently aware of but that was originally incurred in her name without her knowledge.

If coerced debt is found, immediate steps that can be taken, including disputing the fraudulent charges with the three major credit bureaus (Experian, Transunion, and Equifax) and placing a fraud alert or credit freeze on the credit report, which makes it harder for the survivor’s partner to generate additional coerced debt and further damage her credit. Victims of coerced debt might also consider changing their financial security information including checking account numbers, savings account numbers, online bank passwords, credit card numbers, online shopping passwords, or information associated with any other account that their partner can access, to prevent further coerced debt. If a survivor is being turned down for jobs or housing because coerced debt has hurt her credit score, advocating directly with the potential employer or landlord may be helpful. Also, advocates can contact attorneys with expertise in consumer and family law to discuss legal options for addressing the debt. It can be useful to discuss strategies to document the circumstances around coerced debt, including hiding financial information, in case legal action is possible. Of course, with all of these strategies, safety must be considered. It is important to discuss how a victim’s partner would respond to any of these actions.

The finding that bills and debt collector activity were the most common forms of discovering fraudulent transactions suggests that financial institutions play an important role in the discovery of coerced debt. The challenge is making contact with a borrower whose partner is potentially hiding financial information from them. Although the findings suggest that some women do eventually uncover hidden mail, advocates and attorneys could work with financial institutions to develop best practices for getting this information into borrowers’ hands.

In addition to engaging in individual and systems-level economic advocacy, attorneys can help victims of coerced debt through litigation. Coerced debt implicates two areas of law: family law and consumer law. Family lawyers frequently lack training on how to use consumer law, and consumer lawyers are frequently not sensitized to IPV-specific issues. To address coerced debt effectively, cross-training and the sharing of strategies are essential. The work of the National Consumer Law Center and the Center for Survivor Agency and Justice provides a best-practices model for developing the necessary capacity. These two agencies coordinate trainings and develop resources that bridge the gap between consumer and family law. Given our finding that coerced debt appears to be common among IPV survivors, this type of coordination needs to be widespread.

This study’s finding that a coercive transaction was reported by the overwhelming majority (87%) of the women who experienced coerced debt may present problems for legal strategies to limit the impact of coerced debt on its victims because the legal remedies to address coercive transactions are limited. Although fraudulent transactions are a form of identity theft, for which federal law provides remedies (15 U.S.C. § 1643 [1980]; 15 U.S.C. § 1681c-2 [2010]), debt generated by coercion is more difficult to address because federal law provides no relief for debt generated by coercion. Attorneys are developing creative legal strategies to work within current law but the options are limited. For example, one promising approach is the argument that the Truth in Lending Act’s (TILA’s) remedies for “unauthorized use” apply to coerced transactions, but the provisions were designed for fraud, so coercion cases can be challenging to win. In addition, the TILA remedies cover only the unauthorized use of credit cards, which leaves much coerced debt ineligible for this relief [15 U.S.C. § 1643 (1980)].

State law also generally fails to address debt generated by coercive transactions. The doctrine of duress is the primary tool under contract law for voiding contracts obtained by coercion, but it currently does not apply to coerced debt. Duress law prevents victims of coercion from invaliding contracts with innocent third parties who provided value [Restatement (Second) of Contracts § 175 (1981)]. For example, if an abuser coerced a survivor into signing a contract that stated that she owed a debt to the abuser, duress law would invalidate the contract. But coerced debt involves third-party creditors such as lenders who extended credit without knowledge of the coercion and so are legally entitled to be repaid, unless one of the federal laws discussed above applies.

The 46% of callers with coerced debt who reported a fraudulent transaction have access to federal identity-theft remedies that enable victims to avoid liability and repair their credit [15 U.S.C. § 1643 (1980); U.S.C. § 1681c-2 (2010)]. These remedies also provide a process for reporting the fraud to credit reporting agencies, which in turn, must inform victims’ financial institutions [U.S.C. § 1681c-2 (2010); 12 C.F.R. 1022.3(i)]. Nevertheless, fraudulent claims can still face barriers to success. The intimate relationship between the survivor and abuser can create skepticism among decision makers about whether the fraud is legitimate and the survivor is entitled to relief (Littwin, 2013). In addition, accessing these remedies can require a police report, which can present problems because many IPV victims want to avoid police involvement (Littwin, 2013). State contract law does not fill the gaps left by the federal statutes. The doctrine of misrepresentation covers contracts induced by fraud. But like the law of duress, the law of misrepresentation generally does not allow fraud victims to avoid their contracts with innocent third parties who provide value, such as a creditor that lent money to an abuser without knowledge that the abuser fraudulently incurred the debt in the victim’s name [Restatement (Second) of Contracts § 164 (1981)].

In addition, family courts are usually unable to provide relief for victims of coerced debt (Littwin, 2012). The overwhelming majority of U.S. states have clear authority providing that family courts may not alter the divorcing parties’ contracts with creditors. 2 Thus, even if a family court in one of these states assigns a given coerced debt to the abuser, the creditor still has the right to collect the debt from the survivor and report any non-payment to the credit reporting agencies. A family court can adjust the debts between the divorcing spouses, but that is helpful only if the abuser has assets with which to compensate the victim. A small minority of states do not appear to have law addressing the rights of creditors in divorces, but do have law that permits family courts to join third parties to a divorce. These states appear to have applied this law only to third parties with property rights, not to creditors. 3 It is thus unclear whether a family court could modify a victim of coerced debt’s contract with her creditor in one of these states.

This study also has important policy implications. Our findings that coerced debt appears to be common and is associated with credit damage and financial dependence suggest a need for laws that would release victims from liability or otherwise provide them with damages as compensation for these liabilities. Federal law is the most promising place for policy reform because a state-by-state approach would likely result in a wide variety of laws that could be confusing for survivors as well as inefficient for creditors and credit reporting agencies, which operate on a national scale. The finding that coercive transactions may be quite common points to the law of duress as an area for reform, although this presents the challenge that duress doctrine is state law. Given the benefits of national uniformity, the best approach may be to encourage law-reform organizations to draft a uniform law of coerced debt for adoption by the states, a common solution in debtor–creditor law (see, for example, the Uniform Commercial Code and the Uniform Voidable Transactions Act).

In addition, the association found between coerced debt and abuse-related credit damage suggests that remedies to rehabilitate victims’ credit reports may be important. This finding provides support for Littwin’s proposal to expand laws that help victims of identity theft (Littwin, 2013). As mentioned above, federal law already has provisions that address identity theft. The Federal Trade Commission already has expertise in applying them (see, for example, https://www.identitytheft.gov/). Law reform at the federal level would need only to clarify that the existing identity-theft laws applied to coerced debt generated by fraud and to expand them to cover debt generated by coercion (Littwin, 2013). Due to concerns about the secondary nature of her data, Littwin limited the application of her proposals to married victims of coerced debt who had divorced their abusive partners (Littwin, 2013). The support for Littwin’s proposal that this study provides suggests that it may be appropriate to expand Littwin’s proposal to cover unmarried victims of coerced debt as well.

Finally, the study’s finding that participants who reported coerced debt were more likely than other participants to have stayed longer than they wanted in a relationship with a controlling partner due to financial concerns underscores the importance of the policy reforms just discussed. This finding suggests that coerced debt may be an economic barrier to leaving an abusive intimate partner. Thus, these types of policy reforms, in conjunction with efforts to enable service providers and attorneys to identify and address coerced debt, could aid in the mitigation of a potentially significant economic barrier to safety from IPV.

Supplemental Material

Online_Appendix – Supplemental material for The Frequency, Nature, and Effects of Coerced Debt Among a National Sample of Women Seeking Help for Intimate Partner Violence

Supplemental material, Online_Appendix for The Frequency, Nature, and Effects of Coerced Debt Among a National Sample of Women Seeking Help for Intimate Partner Violence by Adrienne E. Adams, Angela K. Littwin and McKenzie Javorka in Violence Against Women

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.