Abstract

The Earned Income Tax Credit (EITC) serves more than 26 million U.S. tax filers every year. The EITC is distributed annually at tax time; however, past research suggests that lump-sum disbursements leave households with a lack of funds to deal with financial emergencies throughout the year. Drawing upon the data from a pilot program conducted in 2014–2015 in Chicago, this study analyzes how advanced periodic payments help mitigate financial instability for EITC recipients. Interview participants relate that advanced periodic payments result in a reduction in perceived stress, lower levels of debt, fewer unpaid bills, and the ability to engage youth in extracurricular activities. The findings provide a unique perspective on the ways in which low-income households cope with financial instability and stress and suggest that payment frequency options can play a small but important role in the way in which the EITC operates as a support mechanism.

Introduction

The Federal Earned Income Tax Credit (EITC) represents an important safety net for low-income workers (Greene 2013). On an annual basis, the EITC raises the income of more than six million households above the poverty line (Internal Revenue Service [IRS] 2016a). While the income gap between the wealthy and the poor continues to grow (Halpern-Meekin et al. 2015; Jacobs and Myers 2014), the EITC has evolved to reduce this gap by improving the financial coping capacity of low-income households, and providing a nexus for upward social mobility (Smeeding, Phillips, and O’Connor 2000; Sykes et al. 2015).

The EITC is currently delivered as a lump-sum payment received annually as a federal tax refund. In the past, EITC recipients also had the option to receive the EITC via more frequent payments throughout the year. The periodic delivery option involved small reimbursements to qualified employee’s paychecks; however, the vast majority of EITC recipients chose the lump-sum option when taxes were filed. Analysts have characterized the periodic payment mechanism as cumbersome, poorly advertised, and as a source of workplace stigma (Bhargava and Manoli 2012; S. D. Holt 2008; D. Jones 2010). Given that many EITC recipients face financial precarity throughout the year (Mendenhall, Kramer, and Akresh 2014; Andrade et al. 2017), a reevaluation of whether a periodic payment schedule might increase households’ capacity to cope with unforeseen financial instability and emergencies is warranted (Smeeding, Phillips, and O’Connor 2000).

This study examines data from the EITC Periodic Payment Pilot which was conducted in Chicago, Illinois, in 2014–2015, and measured the effects of partial payments on EITC recipients and the mechanisms by which partial payments might impact perceptions of financial stress. 1 In this article, we draw from the experiences of Earned Income Tax Credit Periodic Payment Pilot Program (EPPP) participants to describe their perceptions of financial stress, as well as the ways in which lump-sum and periodic payments were used to alleviate financial stress. During the one-year study period, 504 past EITC recipients self-selected into two groups:

A group receiving an advanced 50% of their expected EITC, divided into four quarterly payments with the remaining 50% paid at tax refund time (n = 338), or

A group that elected to receive traditional lump-sum payments (n = 166).

Participants from these two groups participated in a baseline survey prior to their 2014 tax filing and three additional quarterly surveys until they received their final advanced payment at the end of the next tax year (four surveys in total). A subset of study participants (n = 68) were invited to participate in a series of interviews and focus groups—their accounts of financial stress over the study period are the primary focus of this article.

We find that households who elected to receive periodic payments described a reduction in their perception of financial stress over the course of the year and attributed these reductions to EITC advanced payments. While some study participants who received the traditional lump-sum payment similarly described a reduction in financial stress, most did not, and in fact, many perceived an increase in their levels of financial stress over the study period. These findings are consistent with those of Kramer et al. (2019), who examined quantitative dimensions of EPPP financial stress and instability. Participants described a range of ways in which advanced payments mitigated financial stress, including infusions of capital near the time of critical financial events within the year and access to money to repay existing debts that would otherwise go unpaid. Although the findings from these interviews are not intended to produce causal inference regarding advanced periodic payments, the accounts reveal the adaptive strategies by which study participants manage household finances and financial shocks and point to EITC periodic payments as an important option to have.

Policy Review: EITC Delivery

Initially designed to be a temporary offset to rising food and energy prices in 1975, the EITC was permanently adopted by the Revenue Act of 1978. Subsequent amendments to the EITC, including the Tax Reform Act of 1986, pegged benefits to inflation, which, coupled with increased congressional support, have made the program more generous over time (Guzman, Pirog, and Seefeldt 2013; Hungerford and Thiess 2013). In 2016, 26 million tax filers received approximately $65.6 billion in EITC (IRS 2016b). An estimated two thirds of EITC recipients spend the majority of their refunds on immediate expenses—a boon to local economies (Berube 2006; S. Holt 2015).

The EITC is a vital resource for raising the earnings of low-income households, but this increase in income is largely used to address existing budget shortfalls (Mendenhall, Kramer, and Akresh 2014). Sykes and colleagues (2015) argue, however, that unlike other means-tested social welfare programs, the EITC promotes three benefits that extend beyond filling budget shortfalls. First, the EITC allows benefits to be delivered “transparently” to beneficiaries through their tax returns. Second, its benefits focus on working parents—a group likely to face fewer stigmas than other groups receiving social welfare benefits. Finally, the lump-sum payment provides a unique form of monetary support, which constitutes “a just reward for work, and opportunity for upward social mobility, and a chance to provide recipients’ children with some of their ‘wants’ and not just their ‘needs’” (Sykes et al. 2015, pp. 243–44).

The EITC is typically delivered through a filer’s tax return, annually, as a lump-sum payment. Between 1978 and 2010, filers eligible for the EITC had the option of receiving advance EITC payments through their paychecks. Only 3% of eligible taxpayers chose to receive their EITC in this manner, and nearly 80% of recipients were found to be in some way noncompliant with program regulations (U.S. Government Accountability Office [GAO] 2007). Low uptake of the advance EITC option has been attributed to stigma associated with using the recipient’s paycheck as a refund mechanism (Sykes et al. 2015) and the administrative burden placed on the recipients and employers to set up the advance EITC (Barr and Dokko 2006). As a result of its low uptake and cumbersome administration, in 2010, the IRS eliminated the advanced EITC payment option.

Researchers have argued that more frequent payments could provide additional benefits that outweigh previously observed costs and administrative hurdles. Previous experiments with periodic payments have, for the most part, delivered small payments that had little effect on household finances (e.g., GAO 2007; Kaushal, Gao, and Waldfogel 2007; Romich and Weisner 2000) or were administratively challenging to deliver even in demonstration form (Barker and Frederick 2016). Reform proposals have included distributing advanced periodic payments directly by the IRS (S. D. Holt 2008), allowing qualified individuals to claim an “early” refund up to $500 delivered through their employer (Vallas, Boteach, and West 2014), and allowing individuals to claim a portion of their refund early so long as it is delivered into an interest-bearing savings account (Halpern-Meekin et al. 2015).

The EPPP was modeled after the proposal of distributing the advance periodic payments of the EITC directly from the IRS (S. D. Holt 2008). This model eliminates the barriers and stigma associated with claiming advance payments via one’s employer. In practice, to receive the advanced periodic payment, a taxpayer would file an additional tax form accompanied with their Schedule Earned Income Credit (EIC) when they file their federal tax return. The IRS might be able to integrate an advance payment option of the EITC into the payments system it has had to create to distribute the advance premium tax credits associated with the Affordable Care Act (S. Holt 2015). This system could include an option for recipients of the advance payment to discontinue the disbursements if they have a change of income or filing status during the year, further reducing the likelihood of overpayment and a balance due at tax time.

Participants in the EPPP were permitted to receive up to half of their estimated EITC for the following year paid in four periodic installments. Receiving only half of the next year’s estimated EITC helps to limit overpayment of the credit during the year and the financial shock of subsequent repayment when the following year’s tax return is filed. In addition, EPPP participants were only eligible to participate if they received the EITC based on their claiming dependent children on their tax refund; therefore, many were eligible to receive the Child Tax Credit as well, which can provide an additional “buffer” against overpayment.

The Theoretical Basis for Policy Intervention Around Household Financial Instability

The continued erosion of income security for the U.S. population has been felt especially acutely by low-income households (Hacker et al. 2011). For example, more than 27% of low-income families earning up to twice the poverty line experienced serious hardships such as a lack of affordable housing or a lack of childcare within a 12-month period (Boushey et al. 2001). At the same time, low-income households are resilient and use adaptive strategies on par with those of nonpoor families (Orthner, Jones-Sanpei, and Williamson 2003). Means-tested earnings supplements, such as the EITC, form an important backbone of support for low-income households (Austin et al. 2004), and are bolstered by other resources, including additional cash assistance from friends or family members (Kathryn Edin and Lein 1997).

When attempting to understand short-term consumption and long-term savings behavior, economists typically employ lifecycle theories of savings. Shefrin and Thaler (1988) modified this theory by adding three elements to further explain consumption and saving behaviors: self-control, mental accounting, and framing. Self-control deals with the conflict associated with preferences related to the long-term versus the short-term. The delay of current consumption for future savings creates the need for various self-control techniques such as rules and mental accounting. A household financial decision-maker, for instance, may place severe penalties on themselves for withdrawing money held in an account intended for savings. Households oftentimes allocate large windfalls as something to be saved, and smaller or irregular amounts of income as something to be spent (Beverly, McBride, and Schreiner 2003).

The interactions between financial stress and other forms of social stressors are well documented in the literature (Aneshensel 1992; Lazarus 1966; Pearlin 1983; Pearlin and Bierman 2013). Evidence from behavioral economics shows how financial stress may influence household financial decision making. Shah, Mullainathan and Shafir (2012) argue that scarcity forces individuals to focus on their immediate needs, and although this can be positive, it can also reduce the ability to cope with other needs, both acute and long term. The authors suggest that resources that relieve scarcity, known as slack, are a direct way to increase coping capacity. Similarly, Shah, Mullainathan, and Shafir (2012) empirically illustrate how resource deprivation alters behavior and savings strategies. Attentional neglect—being overwhelmed by an immediate need—made it difficult for poor study participants to focus on future needs. Borrowing money or other resources—often at high interest rates—was a central strategy used by study participants to alleviate acute and immediate attentional demands. The study also noted that poor individuals find ways to save for the future, but that these savings tend to be segmented and earmarked for specific household needs (such as cars) and not pooled into general savings (Shah, Mullainathan, and Shafir 2012). Research shows that often when families receive a large windfall like the EITC lump-sum payment, they view it as a mechanism for forced savings (Romich and Weisner 2000).

Sociologists have extended these behavioral economic theories to include the social meaning of money (Zelizer 1989, 1996, 1997). She describes how the ways that individuals earmark money and incorporate it into family relations have baffled market theorists. The value or meaning that individuals give to money, specifically the EITC credit, extends beyond lump-sum versus incremental payments. The context (gift or entitlement), giver (grandmother or the government), and amount (hundreds or thousands) determine the “social meaning” of the money, how it is used, and ultimately its power. Our study examines the power of the advanced periodic EITC payments to address and resolve the social conditions of urban low- and moderate-income families such as difficulty making ends meet, decreasing the stress associated with limited resources, and protecting children from violence in their communities.

The financial stress experienced by low-income EITC recipients is likely to impact both psychological and physical well-being. Aneshensel (1992) argues for a link between social and environmental factors and financial stress. Aneshensel differentiates random stressors—those that occur for all social groups (e.g., negative interactions at work, experiencing the loss of a loved one)—from systemic stressors—those that disparately influence certain social groups (e.g., inability to pay rent, a mortgage or car note, or being behind on bills). Low-income individuals experience systemic or chronic stressors at a higher rate than wealthier individuals (Wilson and Mossakowski 2009), and such chronic stress is likely to translate into other forms of instability, including family conflict, food insecurity, and physical health issues (Bickel, Carlson, and Nord 1999; Broussard 2010). These chronic vulnerabilities have a larger and more detrimental impact on low-income households when compared with occasional random stress events (Grzywacz et al. 2004; Turner and Avison 2003).

Spencer (2007, p. 852) illustrates how these forms of instability create challenges not only for individual households but also for neighborhoods and argues that the “EITC is a significant investment in poor neighborhoods because of the spatial concentration of the working poor.” Therefore, the prospect of advanced periodic payments is not only to increase the availability of material resources and extra “slack” for low-income households throughout the year, but also to increase collective coping capacity at the neighborhood and community level. As Spencer (2007) argues, this additional capacity represents a community economic benefit, but also has important ramifications for community agency and political representation.

Project Background and Research Questions

For the 2014 tax year, the maximum monetary value of the EITC was $6,143. Combined with other tax credits and refunds (for instance, the Child Tax Credit and the American Opportunity Credit), a low-income tax filer could receive a tax refund worth more than half of their annual income. Based upon past implementation strategies used to deliver EITC benefits and the theoretical relationship between income, financial stress, and well-being, the Chicago EPPP was developed to examine whether and how the advanced periodic EITC payment could positively impact household financial stability. The pilot was administered through a collaboration of public and private entities, including the Center for Economic Progress (CEP), a large public university, the City of Chicago Mayor’s Office, the Chicago Department of Family and Support Services, the Chicago Housing Authority (CHA), Advent Financial, and Santa Barbara Tax Products Group. The CEP served as the primary administrator of the project, and a team from a large public university served as the pilot evaluators. The CHA provided the necessary capital to offer the periodic EITC payments and assistance in recruiting CHA residents for the pilot. Other entities provided additional funding for the program and logistical support with processing eligibility and payments.

Recruitment activities included CHA sending direct mailings and emails to potentially eligible CHA residents announcing recruitment events as well as recruitment activities at nonprofit social service agencies. CEP also sent emails to their client-base announcing the research opportunity. CEP screened all interested individuals for eligibility which included individuals who (1) filed a tax return in which they claimed at least one qualifying child the previous year and expected to again in the following year; (2) received an EITC of at least $600 in the previous year and expectation to receive it again the following year; and (3) had no tax controversy or federal debt that would interfere with receiving a tax refund.

The EPPP specifically tested the utility of advanced quarterly payments under the assumption that advanced quarterly payments would provide greater financial stability and better conditions for savings. To ensure a smooth disbursement process and minimize the potential for stigma (Bhargava and Manoli 2012; Sykes et al. 2015), funds were delivered directly to participants.

Participants in the study were recipients of EITC in 2014 who were expected to continue receiving the benefit in 2015. Participants self-selected into an advanced periodic payment group that received half of their 2014 EITC disbursed over four payments throughout the year (henceforth, advanced payment participants). 2 To effectively observe the potential impact of advanced periodic payments, other participants selected into a “reference group” who continued to receive traditional lump-sum payments (henceforth, lump-sum participants)—a design strategy we discuss in more detail in the methodology section. Lump-sum participants agreed to complete research surveys and participate in interviews throughout the year. At the beginning of 2014, 338 EITC-qualified households were recruited to participate in the advance payment group and 166 EITC-qualified households were recruited to participate in the lump-sum group.

In this article, we report findings related to the following research questions:

Method

Data for EPPP participants were collected over four time periods: a baseline assessment (T1) occurred prior to tax time and before any EITC payments were made; three additional quarterly assessments were made (1) about two to three months later and after the first periodic payment was made (T2); (2) four to six months after the first payment (T3); and (3) after the fourth and last periodic payment was made and participants had filed their 2015 tax returns and received their EITC lump sum or remaining balance due (T4). As mentioned earlier, advanced payment recipients received up to 50% of their projected EITC refund through periodic payments. Lump-sum participants were surveyed and interviewed along the same timeline, although they received no additional funds until the normal EITC disbursement in 2015.

This article describes findings from qualitative interviews conducted with EPPP participants. One-on-one interviews were conducted with a randomly selected group of pilot participants that were asked to describe their household budgets, stress levels, and overall sense of well-being. While participant surveys were designed to measure perceived financial stress, well-being, and household budget characteristics at all four measurement periods, interviews were not designed to be longitudinal in nature. Interview questions do, however, ask participants to provide thoughts on retrospective levels of stress and well-being. We approach analysis of these data as a pooled cross-sectional data set—while we cannot look directly at within-person changes in perceived financial stress, we can explore overall changes in perceived financial stress levels for the sample.

Our analysis took an inductive approach—we focused on identifying concepts and patterns, and on highlighting key themes within the data (Creswell and Clark 2010). While some inductive approaches such as grounded theory would approach data analysis without preconceived notions or categorizations of the data (Strauss and Corbin 1998), we began with a series of reference categories related to key evaluation goals and hypothesized impacts of partial payments—social mobility, EITC spending, jobs and employment, household support, assets, finance, health and well-being, neighborhood context, intergenerational transfers, and policy. These categories are based upon past areas of empirical exploration concerning the impacts of the EITC on households, as well as questions regarding EITC payment frequency and financial stability which motivate our study (see, for instance, Bhargava and Manoli 2012; Katharine Edin, Tach, and Halpern-Meekin 2014; Mendenhall et al. 2012; Mendenhall, Kramer, and Akresh 2014; Smeeding, Phillips, and O’Connor 2000; Sykes et al. 2015; Tach and Greene 2014).

Interview audio recordings were transcribed in full and were then imported into the Atlas.ti qualitative data analysis software for coding around the 10 previously mentioned categories. To strengthen the validity of our analysis, we employed a team approach to the coding of qualitative interview data (Thomas 2006). Team members first spent time coding the same interviews and then compared codes for consistency (Armstrong et al. 1997). When differences in codes emerged during this process, coders discussed differences and also shared them with the research team. Working together, differences were reconciled to produce a consistent coding framework among multiple coders. After establishing a consistent approach to reading and identifying codes, coding was then carried out by two team members. An initial round of coding focused on the 10 preidentified categories, and then a subsequent round of coding and analysis was performed to identify themes occurring within and between each category. These initial rounds of coding helped us to define domains of financial instability for further analysis. Two additional rounds of coding focused specifically on dimensioning themes and subthemes related to financial instability and experience with either the traditional or advanced partial payment of EITC funds.

Results

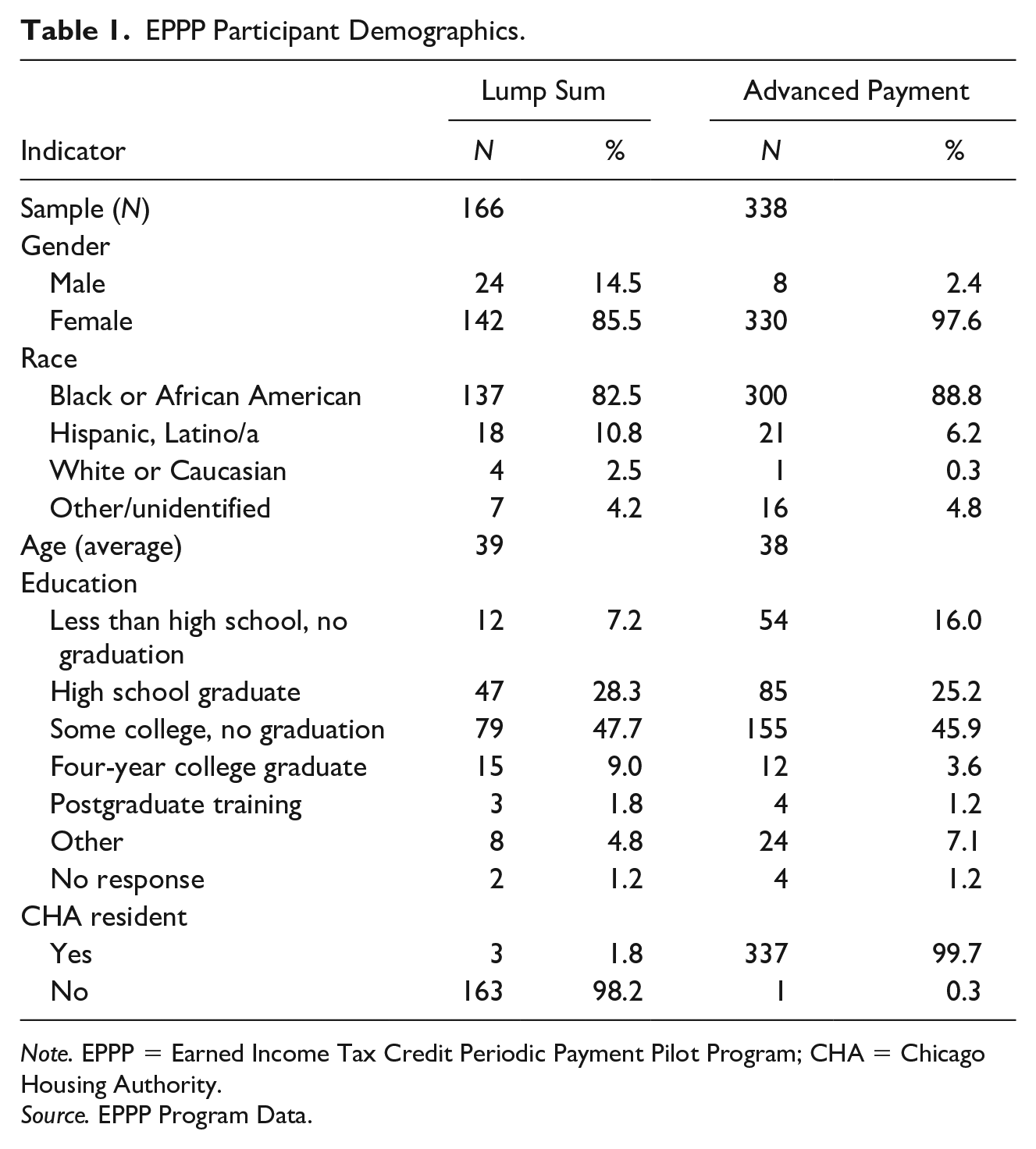

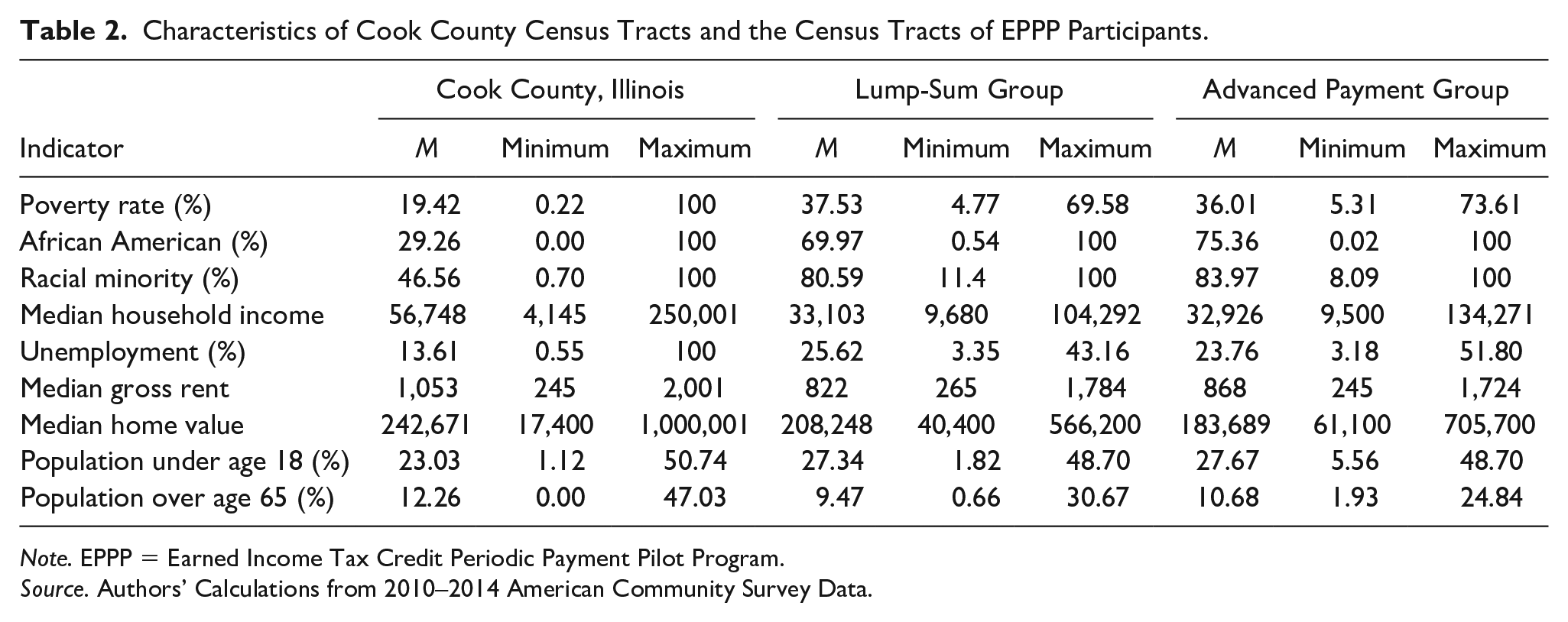

The EPPP sample included 338 participants who received periodic payments and 166 participants who received lump-sum EITC payments. The majority of participants in both programs were female and identified as being either African American or Latino/a. The majority of study participants had less than college education, with only 10.8% of lump-sum participants and 4.8% of advanced payment recipients having a college or graduate degree. The vast majority of lump-sum recipients were not residents living in CHA properties (98.2%), with the opposite (99.7%) being true for advanced payment recipients (Table 1). EPPP neighborhoods were substantially different from other neighborhoods in Cook County (where Chicago is located). When compared with Cook County, EPPP neighborhoods exhibited higher rates of poverty, minority population, lower household income, higher unemployment, and higher shares of children. However, with the exception of proportion African American residents, and median home value, lump-sum and advanced payment recipients lived in demographically similar neighborhoods (Table 2).

EPPP Participant Demographics.

Note. EPPP = Earned Income Tax Credit Periodic Payment Pilot Program; CHA = Chicago Housing Authority.

Source. EPPP Program Data.

Characteristics of Cook County Census Tracts and the Census Tracts of EPPP Participants.

Note. EPPP = Earned Income Tax Credit Periodic Payment Pilot Program.

Source. Authors’ Calculations from 2010–2014 American Community Survey Data.

We provide information on the overall sample of EPPP participants as context for thinking about the sample of participants who were interviewed. Over the course of the EPPP, we conducted 68 in-depth interviews with a randomly selected subset of study participants—30 with participants receiving advanced payments and 38 with participants receiving lump-sum payments.

Common Sources of Financial Instability

For EPPP participants, the struggle to stretch limited resources to cover basic household expenses such as housing, utility, transportation, and childcare costs, is constant. Frequently, families have to make decisions about which bills to pay on time and which bills to leave for later. When unexpected financial challenges come up, whether an emergency expense or sudden loss in income, fragile household budgets are often stretched past their limits.

Both advanced payment and lump-sum participants discussed financial challenges resulting from unexpected, one-time expenses. Unexpected expenses reduced household capacity to pay for recurring and everyday household needs. For example, one participant relies on his car to commute to work. When the car broke down, he needed to buy a new one to get to work. Without a car, he would have faced a three-hour-long commute each way to work. In this case, the participant’s car purchase coincided with receipt of his tax return, so he was able to manage this cost. However, he said that had his car broken down at another time of the year, it would have been his “biggest disaster.” The opportunity cost of vehicle ownership represents a major stressor for low-income households, further exacerbated as most low-income adults rely on automobiles, and not public transportation, for work trips (Clifton 2004; Pucher and Renne 2004). Another participant faced extra expenses that came long after tax time. She had to buy new clothes and shoes for her children as they were starting the school year. With an already stretched budget, she had to stop paying other bills to provide her children with the clothes they needed for the start of the school year. She describes,

Well actually I’ve been behind since school started. ’Cause . . . I had to buy new clothes and everything, so I’ve actually been behind since September . . . Like my rent, the phone bill, the cable bill, you know, because you have to [say] “Okay I’m not paying this cable bill ’cause my baby needs some shoes.”

This recipient resorted to overdrawing her checking account to keep up with the most important household needs, resulting in overdraft fees—an additional financial burden.

Another common financial challenge for EITC recipients is a sudden increase in the costs of utility bills. Because these bills often vary by season and may also experience price fluctuations, high-cost utility bills often came as a surprise. During the particularly cold winter of 2014, one participant described falling behind on bills because of the dramatic increase in her heating costs. She set up payment plans with utility companies to pay off those bills, but still fell behind. Cascading costs from utility bills impacted which other bills were paid immediately, and which remained unpaid until heating costs came down.

Housing instability is also a common reality for many of the EPPP participants, which brings unanticipated costs that can be detrimental to household budgets. During the study period, several participants made unexpected moves because their landlord entered foreclosure or because living conditions in their homes became intolerable. Other participants shouldered the cost of expensive maintenance or home repairs. For example, one advance payment participant paid out of pocket for costly repairs when a tree fell on her home and her landlord refused to cover the repairs. She describes the cost of this setback, which occurred after the final round of advance payments:

. . . The tree fell in on my kitchen and the roof was already bad. I’ve been telling her [the landlord] that for . . . about five years she needs to change the roof. So finally it caved in, it went too far. She did it on a day that it rained and they stopped working because it was raining real hard and everything that I worked for is gone . . . She said she’s giving me a hundred dollars. So now I have to save up money to reestablish, well, furnish the house again, which I’m gonna move because she’s gonna make me move after I sue her. Um, but I also have to get money to get an attorney to sue her! So I’m kinda hitting some hard times right now, cuz’ I still gotta continue and pay the bills until I sue her.

This participant now faces the challenge of paying legal fees to attempt to recoup costs from the landlord and keep up with regular bills. In the meantime, she risks falling behind on her household’s regular expenses. The challenge of paying for legal fees threatens to create a longer-term financial setback.

Financial instability was also driven by income instability, and frequently by the unexpected loss of regular income streams. Many EPPP participants perceived their jobs as offering extremely limited job security or unreliable work schedules. Some participants described placing spending on credit cards when hours at work were cut unexpectedly, a common coping strategy for low-income workers (Littwin 2007). Workers also faced uncertainty regarding when work schedules might change, exacerbating the challenge of budgeting with an eye toward future income and expenses (Henly and Lambert 2014; Roy, Tubbs, and Burton 2004).

As shown in these cases, financial instability for EPPP participants means that irregular expenses and incomes often result in long-term financial setbacks. We asked EPPP participants to describe what financial security might look like for them. Overwhelmingly, financial security would simply mean having the resources to pay all required expenses and to save for unexpected expenses—to have slack (Shah, Mullainathan and Shafir 2012):

. . . financially secure picture for me would just have to be just knowing you have money to the side where if it’s needed on a rainy day, you can be like, “I got this money, I could take this.” Just getting your car fixed or extra groceries in the house. Yeah, financial security, well, just saving, just putting up money enough for a rainy day, or getting a car fixed when it breaks down, or paying an extra bill.

Another says,

Where I can pay bills and still have something to lean back on where I won’t be struggling so much to pay . . . “Okay I’m gon’ pay this bill, but I ain’t got enough to pay this one, so this one got to wait ‘till the next pay period.’” I’m tired of it.

For these individuals, financial security simply means having the financial resources to weather the unexpected financial challenges all households eventually face.

The Impacts of Financial Stability

The impacts of financial instability extend beyond incapacity to pay for required expenses. EPPP participants described multiple ways financial instability affects their lives, consistent with impacts identified by other studies. One of the most common themes EPPP participants brought up regarding the impact of financial stress on their lives is its impact on mental health. Many participants related that constant worry about finances caused or worsened incidences of depression, further complicating capacity to meet goals and obligations:

I was so depressed . . . It hindered [my personal progress towards financial stability] a lot, because when you can’t pay your bills or you can’t pay your rent or your bills, your condo, anything, like you don’t know what’s gonna happen, so you’re paranoid. You don’t know if you’re gonna served with a five-day notice to move, to get out, or they’re gonna come repo your car. Or if this gone, your phone gonna cut off, or this gonna happen, or that’s gonna happen. And it’s like I was just so depressed and I didn’t want to get out the bed. I didn’t want to do nothing.

The long-term mental health impacts of financial instability also affect physical health. As one lump-sum recipient described, the stress of not being able to make ends meet influenced her ability to stay motivated to take care of her physical health:

The challenge is the lack of income and with the lack of income, of course, I can’t meet the financial goals, but also sometimes the lack of income becomes stressful enough that you’re not as motivated to stay on the health tip. Those will be the barriers is the lack of income, which may cause me to have concerns about just meeting certain financial goals and then that I may not feel as motivated as needed to do what I need to do in the health field, put it that way.

Stress over finances also impacts physical health in other ways. One advance payment participant described her experiences with severe migraines and insomnia during her worst periods of financial instability:

I’d be up all night. Like I couldn’t really sleep. I’d be trying to go to sleep and I couldn’t. I couldn’t rest ’cause I guess my mind was so stressed, headaches and when I get up I be so tired ’cause I couldn’t really sleep, but it was like I’m sleepy but I can’t go to sleep. So yeah, that’s not a good feeling.

The stress of not being able to cover basic expenses is especially difficult for parents who worry about not being able to provide for their children. Parents in the study consistently prioritized expenses for children over other needs. Still, many parents worried about disappointing their children when, for example, there was not enough money to pay for presents or provide treats from time to time. The priority given to children’s expenses may reflect physic costs that influence parents’ mental accounting and the social meaning given to money (Beverly, McBride, and Schreiner 2003; Zelizer 1997):

It’s temporary, but when you talking about finances, financial things, even when temporary, it does not feel good. It hurts not being able to do some of the things I want to do even with my daughter and I have a grandchild and she’s like one years old you know, just not being able to have . . . How would I say this . . . not liquid but have some money to you know, do other things with now . . .

As this father describes, worry about disappointing children and fear over failing at parental responsibilities can be deeply painful. For many parents, stress over finances is not merely stress over paying bills, but also stress over successfully filling their role as parents.

For EITC participants, the stress caused by financial instability has wide-ranging impacts affecting mental health, physical health, and sense of worth as a parent. The impacts of financial instability on EITC participants are extensive and often deeply damaging.

Achieving Financial Stability

Study participants in both study arms overwhelmingly indicated that they preferred to receive their EITC in periodic payments. Advanced periodic payment participants reflected on the changes periodic payments had made on their financial situations, whereas lump-sum participants reflected on how they thought periodic payments could have been helpful. Periodic payment participants found they were better able to keep up with bill payments, avoid late fees, manage unexpected expenses, and avoid financial stress. Lump-sum recipients frequently speculated that they would have experienced similar benefits had they received the periodic payments.

Improved Financial Management

Our evidence shows that periodic payments provide the resources for better financial management. Despite having savings goals, lump-sum payments were often allocated for immediate expenses (Greene 2013; Mullainathan and Shafir 2013). A lump-sum recipient describes the difficulty of saving the EITC payment when her household accumulated bills that needed to be paid off:

It’s like as soon as people get that money at the beginning or the end of the year, it’s like the next month, you broke. You broke because you think you rich because you done got this little money. That ain’t no money . . . It’s spent already because all these bills you accumulated, you’re trying to live and provide for you and your family.

While the lump-sum payment allowed her to cover important expenses during that month, it does not provide a financial resource throughout the rest of the year. For individuals who experienced financial hardship throughout the year, receiving a lump-sum payment can be insufficient. This is especially true for participants who have trouble stretching their budgets and experience financial instability after spending the lump-sum payment. For participants who previously struggled, the periodic payment plan provides a tool to better budget their financial resources.

While improved financial literacy and education are a valuable resource to help families manage their limited funds, periodic payments provide an effective infrastructure with additional funds to budget throughout the year:

It’s convenient to help people, because it, you don’t get it all at one time and then they spread it out throughout the course of a few months and that give you time to sit down and think about what you need to do because when you get your whole tax return in one lot, you run around like a chicken with your head cut off. Gotta do this, gotta do this, gotta do this, but you getting it periodic months, it gives you time to sit down, [and say] “okay, I need to do this, do this.” (Advance Payment Participant)

This participant describes the behavioral choices associated with economic and sociological theory about short-term consumption, mental accounting of large or regular income, and long-term savings (Beverly, McBride, and Schreiner 2003; Shefrin and Thaler 1988; Zelizer 1997).

Timing of Periodic Payments

Many periodic payment recipients found that the timing of periodic payments in the EPPP coincided well with regular annual expenses. Heads of households expected increased expenses most notably at the start of the school year in August and September and around the winter holidays. These expenses are a source of stress, which periodic payments helped to alleviate:

I didn’t have a problem with them splitting it up because actually like I say, the way they split it up it works fine for me. Because I looked at the fact “Well August—well, September they start school so I can do the shopping in August for them.” So I can pay the [school] fees out. This way I set it up, my fees and my bills and stuff. And then I figure, well December is a holiday, so it worked fine.

A lump-sum recipient describes how periodic payments would reduce the pressure to stretch out a lump-sum payment over the year:

Yeah, so [the EITC] spread out over a period of time, that would be ok because even when shopping for my daughter I would try to get everything that she would need for school as well as anticipate her next school event really early while I still had the money available. Now if it was spaced out, I wouldn’t be under pressure to do that and I can say while the earned income tax will be coming back a month before you go to school and take that portion and that would be the school portion so it would take some creative budgeting and I’m not gone even lie, I’m not all the time up to that.

The periodic payment plan reduces the need for “creative budgeting” to ensure participants will still have enough of the EITC payment. The periodic payment approach provides a simple mechanism to ensure households have financial resources they can tap into regularly throughout the year.

Managing Unexpected Expenses and Financial Shocks

Periodic payments assist with both expected and unexpected expenses. As our participants described, unexpected expenses are especially destabilizing. A lump-sum recipient explains why she expects periodic payments would help her manage yearly expenses:

I think for me, I don’t know about others, [the periodic payment plan] probably would be good because throughout the year, I’ll have things pop up because of the situation I’m in with my car where I’ll need that extra—that $500.00 . . . just to spend. But like recently my registration and my license plate came up, that’s $101.00 that I do not have . . .

The periodic payment approach is also helpful to participants when they experience sudden reductions in income. Periodic payments provide the resources to stay caught up with bills and other expenses during periods of time when other resources are not available. For example, an advance payment recipient describes her financial challenges when she had to take a leave from work for six months due to a pregnancy:

Well, right now the program helped me a lot, because when I was pregnant, I was put off working September 2013. I didn’t go back to work until March 14 of 2014. So I was off for six months. Within those six months, my car note fell behind. My rent fell behind—a whole lot of things. So now I’m just really getting on track. And this first payment is actually going towards my condo, because I fell behind so much, my condo [payments] went to $502.00 for the next five months. So this first payment going right towards my condo.

Another advanced payment group participant describes relying on periodic payments to make ends meet during a period of reduced income:

And it was a blessing because like during the wintertime, like after October I don’t get no hours at work. I may work like one day a month or one day a week . . . and like around the holidays, around Christmas it’s sad for me. It gets sad because I don’t have no income coming in. And it kind of hurt me and the kids. So because now that I have this it helps me to kind of like save up a little bit for the holiday, or—not just that but I get an income, I get the $500 in December. So that is fine for me so I can be able to do something nice for the kids.

Evaluation data showed that the periodic payment increases the likelihood that households will have financial resources to fall back on during especially difficult financial periods throughout the year. As the experiences of these study participants illustrate, the periodic payment plan provides a simple, effective tool to provide financial resources throughout the year, not only at tax time.

Avoiding Late Fees and Expensive Loans

An inability to keep up with bill payments can be costly. Many study participants regularly accumulate late fees because they are unable to pay their bills on time. Others accumulate credit card debt or take out high-cost loans. One of the most important benefits of the periodic payment is that it enables participants to pay more of their bills on time, thus avoiding late fees and debt accumulation. A periodic payment recipient explains the challenge of remaining current on bills:

I would always—that was always the unexpected bills. Like I wouldn’t have had that cash come in, I would have had to postpone it and [the company would’ve assessed me a late fee or a disconnection fee, things like that. So I feel like this does help you avoid certain late fees . . . So probably $20 a line disconnection fee, so that’s $60 right there. And then they prorate you if you get your services cut off and then turned back on, so that would’ve been $20 more per line to prorate the charges. So that’s $120 right there.

Another benefit of the periodic payment plan is that for many participants, it provides an alternative to taking out high-cost loans:

Sometimes you need that little extra money coming in and that’s—once I get it, it’s still considered mine, and it’s not like I have to go borrow it, get it from someone else or ask someone else for something that I need and just to know that I have something that’s coming in and I don’t have to go ask anyone and worrying about them hurting my feelings or saying no to me makes me feel good. So I most definitely would do it to prevent me from having to ask anyone, or take out loans. It didn’t have no interest on it. So that was even—I love that even more because it was no interest.

These examples show how the periodic payment supported financial stability throughout the year. Participants avoided falling behind on bills or accumulating additional expenses by relying on the periodic payments to fill the gap between their regular income and their expenses. Because EPPP recipients often struggled to make lump-sum payments stretch throughout the year, the periodic payment provides a substantial infusion of funds every three months, helping recipients to avoid costly late fees or loans that not only burden them financially, but also strain personal relationships.

Periodic Payments as a Means to Secure Financial Stability

While our study findings do not indicate that advanced payment group participants were more likely to achieve their goals (e.g., set aside more money in long-term savings accounts) for the year, they do indicate that advanced payment recipients were better able to cope with financial shocks and pay bills on time, hence avoiding further financial setbacks.

3

These findings suggest that the benefits of greater financial security accumulated over multiple years may enable participants to move closer toward their goals:

I’m glad that you all have the [periodic payment plan], because I was in a situation where I needed to pay my rent, because I had gotten behind in my rent. And it’s like the money actually came right on time. [My landlord] wanted to evict me and I was like, “Wait, hold on. I’ve got another source of income. This is about to come.” And she was like, “Okay, where you supposed to get this then? Do I need to [report] my income to say that I get another income?” And I was like, no, because it’s not really income. It comes every so often. It’s not [like] it comes monthly or whatever, or every two weeks. So she was like, okay. So she actually gave me a chance.

This case demonstrates how important it is for low-income individuals to have financial resources they can tap into throughout the year. If the participant who faced eviction had been required to wait until tax time to access her EITC funds, she would likely have lost her home. The periodic payment helps participants avoid the stress of emergency bill payments throughout the year, thereby freeing up energy and resources to allocate toward long-term goals. Some participants who received lump-sum payments expressed a desire to save it for income shocks or purchase big items.

Lump-Sum Payments and Financial Stability

Nonetheless, some participants preferred the lump-sum payment, in particular because it offers greater control over finances:

This is the reason why I have that money because every year when I get my income, my taxes I put it in the bank. I don’t spend it. I take part of it, do something that I want to do and then the other [part is saved] . . . In a worst case scenario that funds is low and something major happen . . . [I will use] advance because that will help me. That’s for instance like in the situation when my bill—I don’t want my bill to go into foreclosure because I have so many late fees and stuff like that. Let’s say, for instance, in my account I only have about I’d say $300.00 or $400.00 that advance will benefit me to make sure that I secure whatever emergency I will have . . . Because if I need $300.00 right now my account going to be going 0. You see what I’m saying? My saving will go to zero. But that advance that I’m getting I could take that whole money and put it in the bank and that will leave—you see what I’m saying? That will help me in that problem.

Another lump-sum participant preferred the lump-sum payment because she felt it encouraged more responsible spending:

Because I can do more with it [lump sum]. Meaning, if I got it periodic—it depends upon the amount—what would I really be able to accomplish with the money that would not be—how can I say this? I would be able to see the benefit, the benefit of me getting all of my money at once. It allows—gives me a greater range of what I can do as opposed to—depending upon the amount, if it was a significant amount—that I would be able pay goals or make a difference in my household and not just take it and do something frivolous with it.

As this participant describes, a lump sum feels like a serious sum of money that she should be careful to budget responsibly. She felt that periodic payments feels less substantial to her and puts limits on what she can do.

Discussion and Conclusion

As our study attests, the financial instability experienced by EITC recipients has numerous causes and consequences, many of which can unexpectedly change within a given year (Greene 2013). Our analysis and comparison of EPPP lump-sum and periodic payment recipients underscore how crucial the EITC is to household financial well-being (Center on Budget and Policy Priorities [CBPP] 2009; Marr et al. 2015; Sykes et al. 2015). Furthermore, we illustrate how advanced EITC periodic payments that deliver relatively small but consistent infusions of money reduce overall perceptions of stress for some households. While our study is designed to be largely descriptive in its nature, the narratives provided by EPPP participants provide evidence that periodic EITC payments offer tangible benefits at a minimal additional expense—further leveraging the promise of the EITC as a longstanding income support. Our findings from qualitative data are further reinforced by quantitative analysis of household finances for EPPP households (Kramer et al. 2019).

Our first research question focused on how EITC recipients characterize financial instability and frame the impact of such instability on their household and neighborhoods. Our analysis confirms previous findings regarding how low-resource households deal with both budgeted and unforeseen expenses throughout the year (Greene 2013). We examined patterns of the financial challenges which EITC recipients face over time and find that these challenges lead to decision making that satisfies immediate needs, even when these decisions come at a higher cost (Mullainathan and Shafir 2013; Shah, Mullainathan, and Shafir 2012). EPPP participants described prioritizing alleviating immediate financial stressors, the demonstration of care to children and other family members, and the management of debt to family, friends, and institutions, oftentimes to the detriment of building long-term savings. For households that selected into periodic payments, being able to anticipate an infusion of additional income represented an important circuit breaker for acute and chronic financial stress. Likewise, both lump-sum and periodic payment recipients underscored the importance of the social meaning of money as reflective of a form of caretaking, which is consistent with existing sociological theories (Beverly, McBride, and Schreiner 2003; Zelizer 1997).

While our interviews are limited in what they allow us to say regarding actual health benefits being driven by periodic payments, participants in our study reported feeling mentally and physically better when they had more resources to better deal with acute financial stress throughout the year.

These observations are important and call for improved public policy to help low-income households deal with the structural and circumstantial challenges of everyday life—from car breakdowns, to landlords facing foreclosure, to trees falling on houses, to lost hours at work. These challenges which were experienced by some of our interviewees, as well as many other unexpected events faced by low-income families, typically have policy-based antecedents which merit attention beyond the scope of this article and our discussion of the psychological impacts of financial instability.

Our second research question focused on the timing and mechanisms by which periodic payments altered perceptions of financial stress and instability. Our interviews show that advanced periodic payments are not likely to reflect a complete solution to the complex problems faced by low-income households—while periodic payment recipients perceived less financial stress at the end of the year, they still related the same types of material hardships faced by lump-sum households. At the same time, the perception of reduced financial stress experienced by advanced payment recipients is significant. These perceived changes provide support for rethinking an elective periodic payment option. Previously suggested reforms to the EITC such as Individual Development Accounts (Smeeding 2005), and other means of income smoothing (see, for instance, L. Jones and Michelmore 2016; Shaefer, Song, and Shanks 2013; Tach and Greene 2014) may be combined to encourage moderated spending as well as long-term savings.

Our study and findings come with some noteworthy limitations. Participants self-selected into lump-sum and periodic payment groups. While this has implications for the interpretation of our findings, this also reflects the likely scenario which would occur should a periodic payment option be implemented alongside the current lump-sum option. Furthermore, most of the pilot participants were recruited based upon their prior participation in support programs offered by city agencies such as the CHA. While, at the end of the study, lump-sum recipients were enthusiastic about the periodic payment option, there is likely selection bias present that is inherent to the limitations of our sampling strategy. At the same time, there are important implications to being able to observe perceptions of financial stress and stability within the “ecosystem” of means-tested support programs our interviewees participated in. Ideally, we would have tracked households for more than one tax year to be able to observe longer-term impacts of advanced payments on household financial stability. Finally, we would have ideally treated our study participants as a panel rather than a pooled sample, thereby conducting interviews with the same households over the course of the study to allow for more focused accounts of within-person changes, as opposed to cohort effects over the course of the study.

Despite these limitations, our findings support the need for continued examination of alternate means for the disbursement of EITC funds. Our findings reflect the longstanding success of the EITC program as a valuable income support for low-income Americans and provide additional evidence that a partial payment option might open up the potential for further benefits and for a more substantial impact from program dollars. Our findings also suggest that developing a better understanding of payment frequency in other income support programs is warranted, as is research that examines the timing and coordination of payments for individuals who may receive support from multiple programs.

Although the EPPP was executed through a collaboration of multiple organizations, the goal was to model what a scaled federal program would look like. Central to this model were multiple local institutional partnerships concerned with the well-being of low-income households that extend beyond prior statutory or experimental methods of program delivery. The components of the EPPP program included EITC recipients electing to receive advance periodic payments of the EITC, the actual disbursement of the advanced payments, and the reconciliation of the payments on the subsequent year’s tax return. The IRS may be able to integrate such a program into the payments systems it has had to create to distribute the advance premium tax credits associated with the Affordable Care Act. Therefore, circumventing some of the challenges experienced in the past when advance EITC payments were disbursed through employers, alternate solutions such as advance periodic payments of the EITC disbursed directly to recipients from the IRS offer useful flexibility for meeting the needs of program participants, thereby better serving low-income individuals and society as a whole.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.