Abstract

Growing concern about climate risk has intensified calls for sustainability mainstreaming. Yet firms often embed climate risk in ways that reinforce business‑as‑usual priorities rather than prompting strategic transformation. This study explains why this occurs by integrating behavioural and practice perspectives on strategy. We examine how climate‑risk management tools shape the framing of climate‑related complexity, highlight certain aspects as salient, and direct managerial attention towards pursuing business‑as‑usual rather than transformative approaches. Empirically, we analyse global food and drink firms’ open‑text CDP disclosures from 2018 to 2022. Our findings show how an overreliance on familiar, routinised tools can bias firms’ decision‑making. This bias leads many firms to incorporate climate risks into their existing strategy rather than changing it; however, in some cases, particular configurations of perceived complexity and salience enable more transformational approaches. The study advances our understanding of the process of sustainability mainstreaming and its limits in enabling strategic transformation.

Introduction

In response to growing concerns about climate change and loss of nature and biodiversity, management scholars have advocated for broadening the strategy field’s research agenda to place greater emphasis on the environmental impacts of business activities (Bansal et al., 2025; Dahlmann, Stubbs, et al., 2019; Lahneman et al., 2025). Calls for “mainstreaming” sustainability have gained momentum, especially given the urgent need to address climate change and its far-reaching consequences for nature and society (de Bakker et al., 2024; Vernay et al., 2022). This shift implies that climate risk considerations should be embedded within core business strategy rather than treated as peripheral (Pinkse et al., 2024). Yet recent research shows that such embedding often results in climate risks being incorporated in ways that continue to privilege short‑term economic interests over long‑term environmental considerations (Ferns & Amaeshi, 2021; C. Wright & Nyberg, 2017). This raises important questions about what mainstreaming climate risk actually entails for strategy-making and whether embedding alone is sufficient to align strategy with the scale and urgency of climate change. Different perspectives on mainstreaming offer contrasting expectations about how fundamentally firms need to rethink their strategic response to the climate challenge.

A first perspective sees mainstreaming as a process of framing climate risk as an issue that firms can address using their existing strategic toolkit (Porter & Reinhardt, 2007). In this perspective of mainstreaming through business-as-usual, climate risk is incorporated into current strategy-making (Hoffman, 2005). Corporate climate action becomes positioned as an extension of current business practice with a strong emphasis on the “business case” (Barnett, 2019; Busch et al., 2024; T. Hahn et al., 2015). Climate risk is treated as any other strategic issue, with the expectation that managing it effectively will enhance firm performance (Dyllick & Muff, 2016). This business‑as‑usual approach risks turning mainstreaming into a process of incorporating climate risk into existing priorities rather than questioning those priorities (Mazutis & Eckardt, 2017). However, it has been critiqued for being a form of “interpretative denial” because it “reframes the catastrophic meaning of climate change by translating it into something manageable within the dominant economic system” (Nyberg & Wright, 2022, p. 718).

A second perspective views mainstreaming as requiring firms to fundamentally rethink their approach to strategy-making so they can operate in ways that respect and remain within the limits of the socio-ecological systems on which they depend (Bansal et al., 2025; Whiteman et al., 2013). This view of mainstreaming through transformation involves reorienting strategy to enable more effective climate risk management and ensure operations remain within planetary boundaries. Climate risk is not treated as a conventional strategic issue but as a wicked problem that requires a different strategic response (Lahneman et al., 2025; Unter et al., 2024). Yet despite the urgency of this view, it remains overshadowed by the business‑as‑usual perspective (Ferns & Amaeshi, 2021). What remains unclear, though, is why firms’ strategy‑making processes lead them to fall back on business‑as‑usual responses, even when the issue clearly demands transformational change (C. Wright & Nyberg, 2017).

In this article, we draw on behavioural (Lovallo & Sibony, 2018; Powell et al., 2011) and practice (Jarzabkowski & Kaplan, 2015) perspectives on strategy to explain why firms tend to incorporate climate risk into existing strategy instead of changing their long‑term direction to operate within planetary boundaries. We argue that the tools firms rely on to manage climate risks play a key role in this process as they shape managerial attention and stabilise meaning (Jarzabkowski & Kaplan, 2015; Pollock & D’Adderio, 2012). Such tools can act as a mechanism that channels climate risk into business‑as‑usual responses by structuring how complexity is framed and by shaping which aspects of climate risk are treated as salient (Neugebauer et al., 2016). We put forward that relying on existing tools for climate risk management can introduce biases into strategic decision‑making processes which lead firms to misinterpret climate change’s urgency. Therefore, we ask: What role do tools play in shaping managerial attention and interpretation of climate risk and why do they steer firms towards business‑as‑usual rather than transformational forms of mainstreaming?

We address this question by empirically analysing how firms in the global food and drink sector assess and respond to climate risks. Drawing on open-text data from 85 firms that continuously reported to the Carbon Disclosure Project (CDP) between 2018 and 2022, our analysis uncovers why climate risk continues to fall into the trap of being oversimplified to fit “business-as-usual” (C. Wright & Nyberg, 2017), and under which conditions we can observe the emergence of more transformational approaches (Bansal et al., 2025). With our analysis, we contribute to sustainability mainstreaming research in three ways. First, we explain why business‑as‑usual mainstreaming persists by showing how using routinised risk management tools can create bias by leading firms to frame complexity and construct salience in ways that narrow their attention and interpretation of climate risk. Second, we unpack the mechanisms of salience construction and reliance on routinised risk management tools to provide a more in-depth explanation for why business-as-usual mainstreaming occurs, even under heightened pressure to address climate risk. Third, we show that mainstreaming is a dynamic process: as firms encounter rising complexity and experience more immediate climate impacts, some begin to shift towards more transformational forms of mainstreaming supported by new risk management tools, complexity framings, and external expertise.

Literature Review

Mainstreaming Corporate Climate Action

There is neither a clear definition of what it means to mainstream climate change in business strategy nor agreement on whether mainstreaming leads to the effective management of climate risk, either through absolute reductions in greenhouse gas (GHG) emissions (Slawinski et al., 2017) or improved adaptation to physical climate impacts (Linnenluecke et al., 2012). Mainstreaming is often viewed positively because it suggests that climate risk management has become a normal business practice. This interpretation aligns with the policy literature, which frames mainstreaming as integrating climate risk into existing sectoral policies and decision-making, rather than treating it as a stand-alone initiative (Kim & Shin, 2024; Runhaar et al., 2018).

Applying this interpretation to business strategy produces the first perspective: mainstreaming through business-as-usual. Here, mainstreaming refers to integrating climate risk into strategy, governance, and operations (Hoffman, 2005; Porter & Reinhardt, 2007), instead of keeping it peripheral (Pinkse et al., 2024). In practice, this includes setting net-zero targets, expanding existing risk management to include climate risks, creating reporting frameworks for non-financial value, and investing in low-carbon innovations (Berger-Schmitz et al., 2023; Pinkse & Kolk, 2009).

However, this approach has been criticised for reinforcing business-as-usual because incorporating climate risk into existing strategy does not guarantee substantive change (Nyberg & Wright, 2022). Such integration often remains instrumental or symbolic, privileging efficiency, compliance, and shareholder value (Barnett, 2019; Dahlmann, Branicki, & Brammer, 2019; Dyllick & Muff, 2016; T. Hahn et al., 2015; C. Wright & Nyberg, 2017). Firms typically act on environmental issues because they pose economic risks rather than out of ecological concern (Delgado-Ceballos et al., 2023; Dyllick & Muff, 2016). As a result, managing climate risk becomes a means to financial ends rather than an environmental goal in its own right (Barnett et al., 2020; Busch et al., 2024; R. Hahn et al., 2023).

This instrumental logic is visible in the growth of disclosure regimes such as the Task Force on Climate-related Financial Disclosures (TCFD) and the EU’s Corporate Sustainability Reporting Directive (CSRD). While these regimes help institutionalise climate risk in finance and accounting, they translate systemic ecological challenges into narrow firm-level metrics, constraining firm-level change (Callery, 2023; C. Wright & Nyberg, 2017). Institutionalisation can also drive symbolic compliance: firms meet reporting expectations without substantive internal transformation (Callery, 2023; Delmas & Burbano, 2011; Talbot & Boiral, 2015). The focus thus shifts to reporting rather than innovation in core operations, the very source of GHG emissions or climate vulnerabilities.

The second perspective – mainstreaming through transformation – calls for a deeper reconfiguration of strategy to improve resilience and avoid organisational collapse (Clément & Rivera, 2017; Linnenluecke & Griffiths, 2010). Expanding from how climate risk can affect firms, it emphasises how firms also affect socio-ecological systems and how they can operate within planetary boundaries (Bansal et al., 2025; Dentoni et al., 2021; Whiteman et al., 2013). Concepts like double materiality and Sustainable Development Goals (SDGs) reflect this broader perspective. Double materiality expands the notion of climate risk by considering firms’ societal and ecological impacts, not just financial ones (Correa-Mejía et al., 2024; Garst et al., 2022; Raith, 2022). This perspective challenges the view of firms as self-contained, profit-maximising entities and instead stresses their embeddedness within socio-ecological systems (T. Hahn & Tampe, 2021; Lahneman et al., 2025).

From this perspective, mainstreaming requires significant strategic adaptation to extreme weather events and other climate risks to enhance long-term resilience (Linnenluecke et al., 2012; Linnenluecke & Griffiths, 2010). Firms must acknowledge their dependence on and impact within socio-ecological systems for their long-term competitiveness (Bansal et al., 2025; Dentoni et al., 2021). The planetary boundaries framework, for example, identifies critical ecological thresholds such as climate change, biodiversity loss, and nitrogen cycles that must not be crossed to ensure Earth system stability (Steffen et al., 2015). Effective climate risk management involves respecting biophysical realities, contributing to socio-ecological regeneration, and developing metrics to track progress towards system-level outcomes (Howard-Grenville & Lahneman, 2021; Lahneman et al., 2025; Whiteman et al., 2013; Williams et al., 2025).

Yet this transformative form of mainstreaming remains mostly aspirational. Although firms increasingly adopt their narrative, evidence of widespread transformative practice is limited (Dyllick & Muff, 2016). For instance, Unilever’s Sustainable Living Plan tried to embed environmental and social goals into its core strategy to decouple growth from environmental harm (Lawrence et al., 2019). Its certification of tea supply chains through the Rainforest Alliance was intended to address biodiversity concerns while improving livelihoods (Winn & Pogutz, 2013). However, Unilever has struggled to maintain this strategic focus and has shifted away from its once ambitious climate targets (C. Wright & Nyberg, 2024). Despite the proliferation of frameworks like double materiality, SDGs, and climate disclosure regimes, empirical studies show little indication that they lead to transformative outcomes (Consolandi et al., 2020; Endenich et al., 2023).

In sum, mainstreaming through business‑as‑usual has gained the most traction, with firms actively engaging in numerous climate initiatives. However, the effectiveness of these initiatives in managing climate risk remains uncertain. In contrast, mainstreaming through transformation offers a more ambitious pathway by aligning strategy with planetary boundaries, but it is largely overshadowed by the dominance of business‑as‑usual and might remain rhetorical only given the scale of change required.

The Role of Tools in Managing Climate Risk

To explain why firms often stick to business-as-usual rather than pursuing transformational change, we draw on behavioural (Lovallo & Sibony, 2018; Powell et al., 2011) and practice (Jarratt & Stiles, 2010; Jarzabkowski & Kaplan, 2015) perspectives on strategy. We argue that firms’ responses to climate risk are shaped by two interrelated aspects: how they frame the complexity of climate risk and how specific aspects of climate risk become salient. From a behavioural perspective, risk management tools help firms cope with the complexity of climate risk, a level of complexity that is difficult to process due to bounded rationality (Gavetti et al., 2012). A practice perspective highlights, however, that these tools do not merely simplify complexity (Jarzabkowski & Kaplan, 2015); they are strategic artefacts that shape how climate risks are enacted by channelling managerial attention towards specific aspects of climate risk, thereby influencing which aspects become salient and which remain overlooked (Ocasio, 1997; Pinkse & Gasbarro, 2019). Tools present a double-edged sword: they support climate risk management by reducing complexity but may also hinder effective responses by introducing systemic bias through their influence on what issues are seen as salient. Next, we first examine the role of perceived complexity before turning to salience and its implications.

Managing climate risk is widely recognised as a wicked problem (Levin et al., 2012) due to continuously evolving interdependencies that make it difficult to identify and implement solutions (Neugebauer et al., 2016; Orsato et al., 2019; Rittel & Webber, 1973). While firms face increasing pressure to respond to climate risk (Unter et al., 2024), they encounter multiple layers of complexity when doing so. Managing climate risk involves both reducing emissions (Pinkse & Kolk, 2009) and adapting to physical impacts such as extreme weather to enhance resilience (Linnenluecke & Griffiths, 2010), with the former being much better understood by firms than the latter (Benischke et al., 2025; Bleda et al., 2023). Moreover, complexity is amplified because climate risks are dynamic and nonlinear, challenging conventional planning and forecasting approaches (Howard-Grenville & Lahneman, 2021), and lacking a clear endpoint or universally agreed-upon solution. As a result, firms must make long-term and often costly decisions under conditions of ambiguity, contested knowledge, or even ignorance (Goldstein et al., 2019; IPCC, 2022). This complexity places substantial demands on strategy‑making, as firms must navigate competing stakeholder expectations, shifting regulatory landscapes, and uncertain climate trajectories while sustaining operational continuity and financial performance (Pinkse & Kolk, 2009).

However, firms do not necessarily perceive all climate‑related risks as equally complex or as requiring urgent strategic action. Their interpretation often depends on whether they possess existing tools and management routines that can be applied to develop effective responses. When such tools are available, firms tend to frame climate risk as a familiar challenge that can be addressed through established risk‑management practices (Pinkse & Gasbarro, 2019). As a result, they perceive climate risks as manageable to the extent that these risks can be anticipated and quantified with existing methodologies (Weinhofer & Hoffmann, 2010). Such quantification helps transform “rich and complex realities into more abstract and thinly described representations” (Denis et al., 2006, p. 353). In this framing, climate risk becomes just one risk category among many, treated as part of a routine managerial process (Lovallo & Sibony, 2018). The danger of this approach is that it underestimates the unique and systemic nature of climate risk (Winn et al., 2011). By relying on familiar tools, firms may fall into a behavioural trap (Lovallo & Sibony, 2018): they neglect long‑term, nonlinear climate impacts that could ultimately prove more disruptive than current tools suggest. According to this line of argumentation, whether firms approach climate risk as business-as-usual or requiring transformation depends on how they frame the complexity of climate risk, either as one of many risks that existing tools can handle or as a unique challenge that exceeds the capabilities of those tools.

While the way firms frame the complexity of climate risk determines the extent to which they can rely on existing tools, how these tools are used in practice shapes the salience attached to an issue and, in turn, how much managerial attention it receives (Lovallo & Sibony, 2018). Because firms tend to rely on existing tools to make climate risk manageable, these tools shape which aspects of climate risk become salient and which issues are treated as worthy of attention or overlooked instead (Bundy et al., 2013). Strategy tools play such a central role because they form the organisational structures that amplify or attenuate what is considered strategically relevant (Ocasio, 1997). By labelling certain aspects of climate risk as strategic, such tools actively produce salience rather than simply reflecting it (Lovallo & Sibony, 2018). In this sense, tools are performative: they not only support managerial interpretation but also shape salience by determining which climate risks are noticed, prioritised, or ignored (Denis et al., 2006; Jarzabkowski & Kaplan, 2015; Pollock & D’Adderio, 2012).

In the context of climate risk, salience depends on factors creating urgency, such as the geographical proximity of climate events to a firm or its supply chain, the power and legitimacy of stakeholders who view the issue as urgent, and the level of media attention (Neugebauer et al., 2016). Different climate risks vary in their immediacy, visibility, and potential to attract attention (Mazutis & Eckardt, 2017). Acute physical risks, such as extreme weather events, droughts, and flooding, often prompt rapid responses because they threaten business continuity (Goldstein et al., 2019; Pinkse & Gasbarro, 2019; Unter et al., 2024), especially in sectors with climate-sensitive supply chains (Goldstein et al., 2019; Hennes et al., 2024). In contrast, gradual and less visible changes, such as shifting precipitation patterns, may be deprioritised unless linked to powerful and legitimate stakeholder concerns or clear financial exposure (Bleda et al., 2023; McKnight & Linnenluecke, 2019; Rivera & Clement, 2019). Firms with high levels of GHG emissions and operating in customer-facing sectors also attract greater scrutiny than those operating further upstream (Kolk & Pinkse, 2007). Given these dynamics, not all aspects of climate risk remain salient over time; instead, particular aspects periodically rise to prominence and then recede (Ocasio, 1997; Pinkse & Gasbarro, 2019). Salience is therefore not inherent to different climate risks but constructed through framing processes and fluctuates in response to physical and societal signals firms receive. Because these signals are often mediated by tools, such as risk dashboards or monitoring systems, they play a pivotal role in directing managerial attention and determining which aspects of climate risk become salient (Jarzabkowski & Kaplan, 2015).

In summary, we expect risk management tools to affect firms’ approaches to mainstreaming climate risk as they shape how firms frame the complexity of different climate risks and construct the salience of particular aspects of those risks. Yet we still know little about how tools influence complexity and salience, and their interaction, and steer firms towards business‑as‑usual rather than transformative approaches. To address this gap, we undertake an empirical study that examines the role of tools in the way firms frame complexity and construct salience in their engagement with climate risk. This enables us to observe how tool use, framing processes, and attention allocation interact and explain why transformational responses remain overshadowed by business‑as‑usual.

Data and Methods

To address our main research question, we analysed open-text responses submitted to the Carbon Disclosure Project (CDP) between 2018 and 2022, 1 5 years in total. CDP is a globally recognised platform for carbon disclosure, widely used in academic research for its structured yet open-ended data collection approach (Dahlmann & Roehrich, 2019; Kolk & Pinkse, 2004; Pinkse & Gasbarro, 2019; Weinhofer & Hoffmann, 2010). Each year, CDP requests voluntary disclosures from the world’s largest publicly traded firms through a standardised questionnaire (Callery, 2023). We focus on the food and drink sector due to its acute vulnerability to climate change, particularly regarding exposure to physical risks such as climate-sensitive agricultural productivity and supply chain disruptions due to droughts and flooding (IPCC, 2023), as well as increasing expectations around managing transition risk by reducing GHG emissions to achieve net zero. Given the sector’s substantial reliance on socio-ecological systems and its central role in global food security (Dasgupta & Robinson, 2022), it offers a critical case for studying mainstreaming of climate risk management as part of firms’ strategy. To analyse the data, we extracted them from the initial MS Excel format to MS Word documents that were uploaded to MAXQDA.

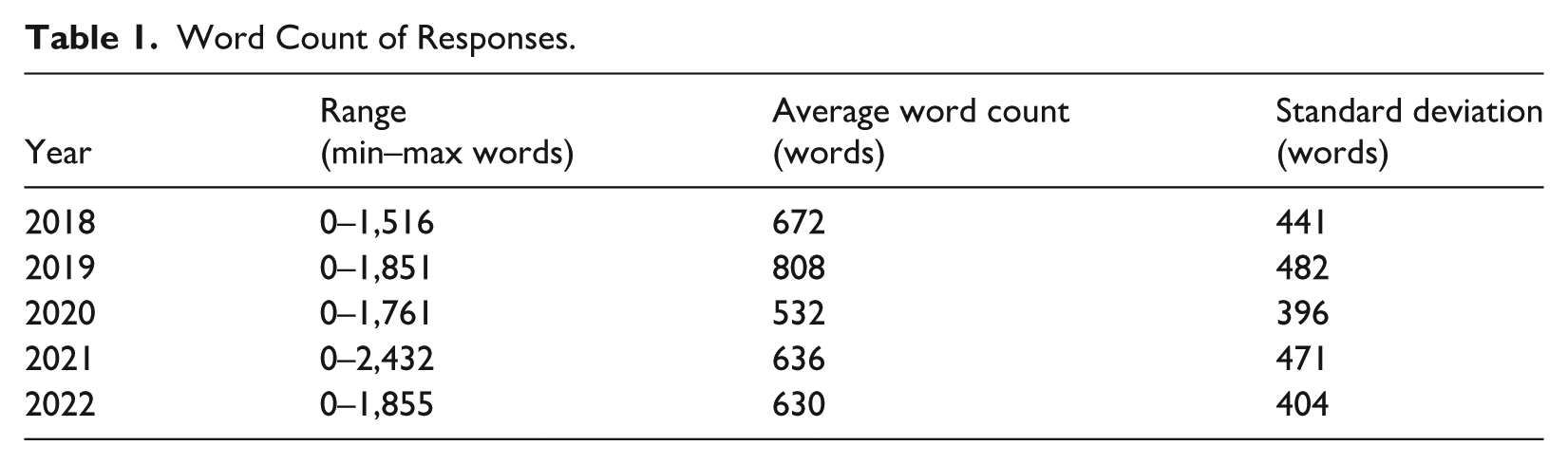

Our sample consists of 85 firms that consistently reported to CDP from 2018 to 2022. 2 The selected sample was geographically diverse, including multinational and regionally focused firms, among which 37 were headquartered in Europe, 21 in North America, 19 in Asia, 5 in Latin America, 2 in Oceania, and 1 in Africa. We analysed their open-ended responses to two key CDP questions: (1) “Describe your process(es) for identifying, assessing, and responding to climate-related risks and opportunities” and (2) “Provide further details on your organisation’s processes for managing climate-related risks.” These questions appeared with slight variations across reporting years but consistently asked firms to elaborate on their risk assessment, strategic responses, and governance structures related to managing climate risk. The open-ended nature of the responses is well-suited for qualitative analysis of how firms frame aspects of climate risk strategically and justify their actions. Table 1 summarises the word count of firms’ responses in each year of reporting.

Word Count of Responses.

Among the 85 firms, 7 consistently chose “There are no documented processes for identifying, assessing, and managing climate-related issues” as the response in all 5 years, which signals an absence of formalised climate risk management practices and relatively low level of engagement with the issue. However, as they were less relevant to our research question, which focuses on how firms framed and responded to the different aspects of climate risk, we excluded them from the subsequent analysis due to lack of information.

Data Analysis

Our analysis followed a multi-round qualitative coding process (Miles et al., 2014). We based our analysis on an abductive logic, combining inductive insights with deductive coding (Timmermans & Tavory, 2012). We started by organising the data into broad themes, capturing how firms assessed and responded to climate risk to gain a high-level understanding of salient patterns and “let the data speak.” This process identified what firms paid attention to and resulted in various themes like “climate change as part of existing risk processes,” “supply chain disruptions,” “climate change mitigation practices,” “climate risk-specific tools,” and “multi-stakeholder approach.” We then focused on the most frequent codes, including implications related to “policy and regulatory changes,” “supply chain disruptions,” or “extreme weather events.” This sensitised us to variation in how firms framed climate risk. Accordingly, we reviewed our initial codes to identify the key foci in firms’ risk assessments, which were diverse with aspects referring to “environmental hazard,” “legal/regulatory,” “reputation,” and “operational” dimensions, each linked to potential financial consequences.

Through this first round of coding, we realised that firms framed climate risks differently across the sample and responded in distinctive ways. For example, firms had diverging responses to operational risks from climate disruptions in their supply chains. Many opted to diversify supply chains to enable continuity, while some took a longer-term approach by working with suppliers to build resilience. We also found that while the majority integrated climate risk into their “enterprise risk management (ERM) systems” or “existing risk processes,” some developed “climate-specific tools” and engaged in “multi-stakeholder collaborations.” To explore this variation systematically and clarify what it reveals about the mainstreaming of climate risk management, we returned to the literature on how sustainability-related complexity is framed in strategic decision-making. In particular, we drew on Neugebauer et al. (2016), who argue that the “nature of the problem” shapes the strategies firms develop. This prompted us to ask how firms frame climate risk and what types of complexity they perceive it to involve. We then revisited the full dataset and assessed how firms articulated climate‑related complexity in their CDP disclosures.

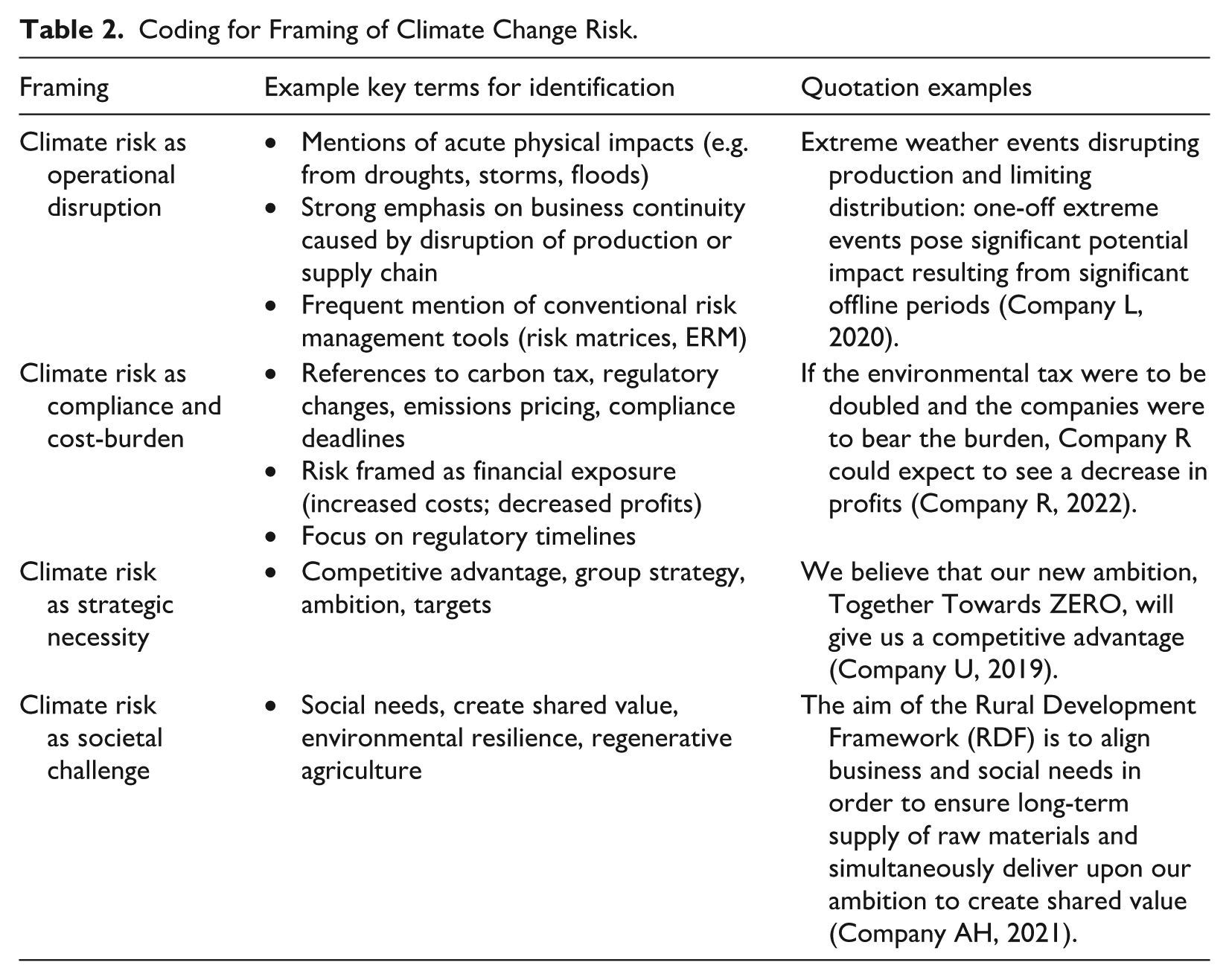

This step revealed that firms framed climate risks in four distinct ways, each highlighting different sources of complexity: (1) operational disruption, where complexity lies in the physical impacts of climate change and uncertainty about their timing; (2) compliance and cost-burden, where complexity stems from transition risks and associated financial consequences; (3) strategic necessity, where complexity relates to long-term consequences for competitiveness; and (4) societal challenge, where complexity arises from viewing climate risk as a systemic and open-ended issue. We identified these framings through an analysis of the risk identification process and associated responses. Table 2 summarises the key terms and an exemplary code informing each framing of complexity.

Coding for Framing of Climate Change Risk.

Second, our analysis showed that within each framing, firms attached salience to climate risk in distinct ways, which highlighted the need to better understand how and why certain issues become salient. We returned to the behavioural strategy literature, drawing on Lovallo and Sibony’s (2018) argument that salience is not only shaped by external conditions but can also be actively constructed. Managers can elevate an issue’s perceived importance by framing it as strategic, thereby legitimising greater attention and resource commitment. As they note, the term “strategic” is often used in managerial practice to denote importance, referring to “the actions taken, the resources committed, or the precedents set” (Mintzberg et al., 1976, p. 246). Because strategy is typically positioned as a high‑level concern, labelling an issue as strategic can itself enhance its salience and justify the allocation of managerial time and resources. These insights prompted us to examine more closely how firms constructed the salience of climate risk in their disclosures. We observed that firms framing climate risk primarily as operational disruption or compliance and cost-burden relied on traditional risk management tools to assess climate risk and justify their responses.

These tools were not only simplifying the evaluation of climate‑related risks but also actively shaped what was considered salient. This insight resonates with a practice perspective on strategy, which emphasises that tools are not neutral artefacts but direct attention, frame issues, and stabilise meanings (Jarzabkowski & Kaplan, 2015; Paroutis et al., 2015; Vuorinen et al., 2018). The calculative elements of such tools can acquire authoritative force, as attaching a high numerical value elevates an issue’s importance (Denis et al., 2006). These observations led us to consider not only how firms used tools to assess climate risk, but also how these contributed to constructing salience and shaping responses. The frequent use of conventional tools, such as risk matrices (likelihood × impact), materiality matrices, and target dashboards, prompted us to re-examine the data with a focus on how these tools influence the treatment of climate risk.

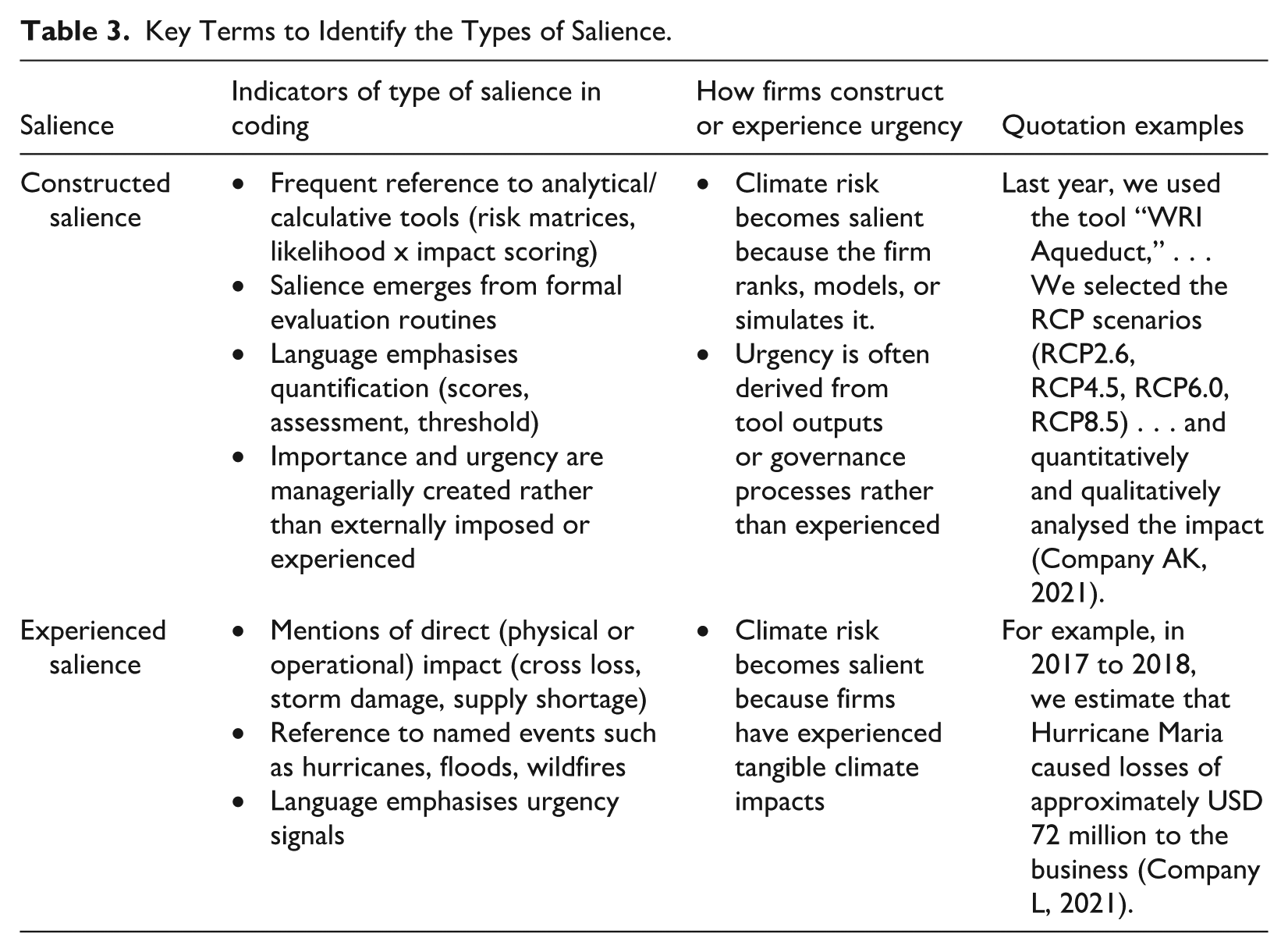

We identified two patterns in how firms assess salience: constructed and experienced salience. Constructed salience reflects a pattern in which firms actively use risk management tools to assign importance and urgency to specific aspects of climate risk. Experienced salience, by contrast, reflects a pattern in which direct exposure to climate impacts, such as extreme weather or gradual shifts in temperature and precipitation, shapes perceived importance. In our data, these processes often combined to sustain business‑as‑usual responses, even when their own experiences with climate impacts might have prompted more transformational change. Table 3 summarises the key terms informing each salience type and provides an exemplary code.

Key Terms to Identify the Types of Salience.

This abductive analysis enabled us to move from broad inductive observations to a theoretically informed understanding of how firms make sense of climate risk and act upon it. By iteratively engaging with the data and relevant literature, we traced how firms frame the complexity of climate risk, how they construct or experience salience, and how tools shape both processes. This iterative movement between emergent themes, targeted recoding, and conceptual refinement allowed us to uncover patterns in how firms identify, prioritise, and respond to climate risks. Accordingly, the findings section explains why seemingly similar climate‑related risks give rise to divergent firm responses and highlights the role of framing, salience construction, and tools in shaping the mainstreaming of climate risk management.

Findings

In our analysis, we identified four framings of the perceived complexity of climate risk: (1) operational disruption, (2) compliance and cost-burden, (3) strategic necessity, and (4) societal challenge. These framings were not mutually exclusive, as firms often drew on multiple framings simultaneously. In particular, the first two framings – operational disruption and compliance and cost-burden – frequently appeared together, as they align closely with the categories of physical risk and transition risk used by frameworks such as the TCFD (Task Force on Climate-related Financial Disclosures). While highly routinised risk management tools such as risk matrices and dashboards continued to dominate over the five years of data collection (2018–2022), we observed a gradual uptake of more climate‑specific tools, including materiality assessments and scenario planning. Firms have also increasingly developed tools to monitor specific climate risks more closely.

Climate Risk as Operational Disruption

Firms that frame climate risk as an operational disruption typically begin their reporting by detailing existing risk management processes and tools that they use to assess climate risk. Within this framing, climate risk is treated as one of several “operational and strategic risks, such as safety, leaf supply, climate change, electronic waste, or labor conditions [that] are well covered by our risk teams and management processes” (Company A, Tobacco products, 2018, 2019). Firms typically emphasise physical risks such as supply chain disruptions, production downtime, and threats to assets. For instance, Company B noted that “climate change risks assessed through the (Business Continuity Plan) include weather events, floods, and disruption of raw material supply and transportation,” and that impacts could include “a facility needing to curtail production due to lack of water or agricultural raw material availability due to climate change” (Company B, Grain & corn milling, 2018). While such risks are familiar, their timing and magnitude remain somewhat uncertain, complicating decisions about how much to invest in preventive measures.

To navigate this uncertainty, firms rely on proxies to determine which risks merit attention. They use tools such as risk matrices that embed internally predefined thresholds to construct the salience of specific climate risks. These tools simplify the issue and allow firms to manage climate-related disruptions through established practices. For example, Stratum applies explicit “likelihood” and “impact” ratings: When determining the likelihood of a risk occurring, Company C uses the following definitions: (1) Very Likely: Above 80%; (2) Likely: 50–80%; (3) Moderate: 20–50%; and Slight: 0–20%. When determining the impact, Company C uses the following parameters: (1) Material Enterprise Impact (> US $50m); (2) Major Business Impact (US $20m >< US $50m); (3) Significant Business Impact ($5m <> $20m) and Moderate (< $5m). The ERM process includes sensitivity analysis . . . then links the priority with our Long Range Planning (LRP) process to focus our resources to mitigate the most serious risks. (Company C, Alcoholic beverages, 2018)

The quote illustrates what we found prominently in our data: the internally constructed salience of a risk determines and justifies the allocation of resources and attention. Where certain thresholds are crossed (e.g., very likely to eventuate, causing material enterprise impact), the importance of managing the risk gains increased. These thresholds, therefore, take on some of the cognitive load involved in making such decisions.

When firms begin to experience climate impacts directly, risks acquire experienced salience, generating greater urgency. Company D (Alcoholic beverages, 2021) reported that “during the 2019 [. . .] wildfire, our wineries lost several tons of fruit . . .” and that 2020 fires led to “a net loss of c. $46 million due to smoke damage.” Our data suggest that such repeated events increase expectations of recurrence and can shift firms’ priorities. Company E (Other food processing) illustrates such a shift. In early reports (2018, 2019), the firm focused on low probability flood risks: [A]ccording to our insurance partner . . . the chance of a 100 year and 500 year flood . . . is 1% and 0.2% . . . This is a very low likelihood and, consequently, is not a material risk for Company E . . . [and] if a significant flood were to occur . . . a percentage of the potential loss would be covered by insurance.

By 2021, after experiencing weather-related damage to sugar beets, Company E (2021) reported that it had “to source sugar elsewhere adding an incremental cost,” prompting the firm to “advance regenerative agriculture principles on 1 million acres of farmland by 2030” to reduce climate-related risks. Across the sample, we observed similar shifts towards broader, system-oriented approaches once climate risks materialised, sometimes reframing climate change from an operational disruption to a strategic necessity, our third framing.

However, firms sometimes also internally construct salience after experiencing external disruptions, translating lived impacts back into risk matrix categories. Company F (Non-alcoholic beverages, 2021) described “poor weather impacting the availability of fruits such as lychee,” which was then rated “a 3 for likelihood . . . and as a 3 for impact,” triggering routine mitigation such as frequent supplier calls. This illustrates how experienced salience is converted back into constructed salience, making the issue more manageable within existing risk management processes.

In this framing, firms generally respond with routine activities that align with assessments of low event likelihood. As climate events become increasingly common, though, these routines seem to be increasingly mainstreamed. Company G (Aquaculture, 2021) stated that: “Global warming may lead to increased events of algae blooms . . . we need to be extra observant and monitor the environment at all times.” Supply chain diversification also functions as a routine way of hedging risk. Company H (Alcoholic beverages, 2018) noted it “has been diversifying the production areas of raw material crops since the 1980s,” now increasingly used “to avoid . . . the risk of crop shortages due to natural disasters and climate change.” Similarly, Company I (Other food processing, 2019) relies on its global tomato production network to “quickly cover procurement volumes from other production areas.” Other routine responses address symptoms, such as production downtime, without tackling the underlying vulnerabilities. After wildfire losses, Company D (2022) “implemented standard practices around Smoke Taint measurement, treatment & disposal.” Insurance remains another common approach to address climate-related risk. Company J (Tobacco products, 2019) maintains “Group-wide insurance cover . . . for ‘natural catastrophe high hazard’ locations” and worked “closely with the insurance provider” on facility improvements after a severe hurricane.

In sum, firms that rely on internally constructed salience generated and reinforced by the tools they use, frame climate risk as operational disruption and hence focus primarily on managing potential financial losses from supply chain and production interruptions. The heavy use of risk matrices, which categorise risks by likelihood and impact, tends to make physical risks appear more manageable, thereby reinforcing a business‑as‑usual approach to monitoring and mitigating these risks. Even when they experience direct impacts, firms often continue to rely on existing risk management routines, although such experiences may trigger heightened urgency or modest shifts towards more strategic thinking. Overall, this framing produces a pattern in which climate risks are translated through internally constructed salience to fit within existing risk management frameworks, enabling firms to plan for climate change while protecting the current strategic direction from significant disruption.

Climate Risk as Compliance and Cost-Burden

Firms that frame climate risk as compliance and cost-burden tend to emphasise the financial challenges linked to emerging climate policies, tightening environmental legislation, and carbon pricing or taxation. They describe these risks as “new taxes on fuel and energy use, which might be introduced in the near future in the European Union or in other regions” (Company K, Alcoholic beverages, 2018). This framing is centred on transition risks that must be managed to protect financial performance. For example, Company L (Non-alcoholic beverages) reported: GHG pricing is one of our top 8 climate-related risks. [We] estimated the combined direct and indirect costs associated with carbon pricing were $132.5 million in 2020. If global carbon pricing increases significantly to align with a 1.5°C pathway, this may increase by $2.1–4.8 billion. (Company L, 2021)

Within this framing, salience is again constructed, but now by relying on how external actors like regulators and investors construct salience which firms then emulate, rather than the result of direct climate impacts or internally through existing risk management routines. As a result, the urgency of climate risks fluctuates with regulatory developments and the expected timelines of policy implementation. Company M (Alcoholic beverages), for instance, states: “Future impacts of climate change are likely to include increases in carbon taxes both domestically and overseas, and carbon border adjustment measures in Europe and the United States, which means an increase in financial burdens” (Company M, 2021, translated by authors). Similarly, Company N (Fishing) notes that other firms “have a Carbon Tax liability in excess of R1 million” under the “South African Carbon Tax Act [which] was promulgated in June 2019.” Anticipating Phase 2 beginning in 2026, Company N developed a long-term energy plan: “It is unclear how the Carbon Tax Act will evolve. . . In order to mitigate this financial risk, Company N has set a target to be independent of third-party non-renewable electricity suppliers by 2040” (Company N, 2022).

When climate policy is understood primarily as financial exposure, firms quantify potential cost implications and treat climate action as a cost–benefit optimisation problem. Externally constructed salience steers firms towards initiatives that meet regulatory expectations or avoid financial penalties. Common responses include initiatives to reduce emissions by, for example, replacing coal-fired boilers, procuring renewable electricity, or improving energy efficiency: [T]he transition risk related to potential increases in greenhouse gas emissions pricing. To mitigate this risk, the assessment process encouraged transition to lower-emissions technologies in our facilities, such as the replacement of coal-fired boilers with natural gas boilers at three manufacturing facilities in 2014. (Company O, Tobacco products, 2021)

Such emission reduction efforts are typically framed as cost-saving opportunities that simultaneously ensure compliance. When policy timelines are uncertain, mechanisms such as internal carbon pricing are introduced to prepare for possible future regulation. These measures are quick to implement, efficient, and oriented towards financial risk management: [T]he Group Sustainability Committee decided to begin considering the introduction of internal carbon pricing in FY2020 [where] transition risks related to climate change are integrated into the company-wide management process. [We introduced] an internal carbon pricing system in fiscal 2021, setting the price per ton of CO2 at 5,000 yen. From fiscal 2022 onwards, we plan to use this system to accelerate energy-saving investments that have a high carbon reduction effect. As a result, these measures are expected to reduce the transition risk when carbon taxes and emissions trading are fully introduced. (Company P, Dairy & egg products, 2022)

Externally constructed salience can also reduce perceived urgency, especially when climate action is pursued to demonstrate compliance rather than to drive transformational change. A recurring response is target-setting, often expressed through long-term emission reduction goals. Long time horizons, such as aiming for net zero by 2050, allow firms to make incremental adjustments and revise targets over time. Target-setting is frequently paired with external frameworks such as the Science Based Targets initiative (SBTi) or TCFD

3

to signal alignment with stakeholder expectations and the Paris Agreement. For example: In 2016, Company A developed emission reduction targets. . . approved by the Science Based Targets Initiative (SBTi). . . Company A commits to climate action in line with best climate science. . . and has been able to mitigate transition risks such as reputational impacts, shifts in market preferences and policy changes related to inaction. (Company A, 2021)

Where firms do not rely on external frameworks, target-setting tends to be more modest and less formalised, reflecting a more relaxed approach: “We. . .have set a goal of reducing CO2 emissions by 12% compared to 2013 by 2030” (Company R, Alcoholic beverages, 2018). Another common response is passing responsibility to suppliers, often through supplier codes of conduct that: . . .require suppliers to comply with all applicable environmental laws and regulations. . . minimize and monitor impacts on the environment. . . through a reduction in greenhouse gas emissions, energy efficiency initiatives, [and] reduction and recycling of natural resources. (Company Q, Other food processing, 2018)

Some firms also exhibit experienced salience within this framing, particularly when referring to existing regulatory requirements rather than anticipated future ones. In such cases, climate risks are perceived as defined, predictable, and manageable through established processes. Although the consequences may be financially significant, they are viewed as straightforward compliance issues.

In summary, when firms frame climate change as compliance and cost-burden, they interpret complexity primarily in terms of transition risks related to carbon taxes, rising energy prices, and tightening regulations that threaten cost structures and financial performance. Because these risks are often anticipated rather than immediate, and they are readily quantified using financial and risk tools, firms are able to translate them into manageable priorities. This framing produces a pattern in which the salience of climate risks is largely constructed by external expectations. Rather than preparing for physical climate impacts, firms focus on transition‑risk planning by target‑setting, monitoring, and technological upgrades aimed at improving energy efficiency to limit the cost implications of noncompliance.

Climate Risk as Strategic Necessity

Firms that frame climate change as a strategic necessity treat it as a driver of a long-term strategic transition rather than a risk that can be fitted into existing risk routines. Although less common than the first two framings, some firms have shifted towards it over time. Company R (Alcoholic beverages), for instance, states that as the “damage caused by climate change is increasing year by year around the world,” the firm decided to adopt a longer‑term strategic approach, stating that “it would be difficult for us to respond unless we take medium‑term countermeasures” (Company R, 2021). Firms emphasise proactive steps to sustain competitiveness and focus on long-term transformation aligned with evolving energy systems, threats to supply chain continuity, and anticipated shifts in market demand. The emphasis is on the implications for financial performance and the explicit role of climate change in shaping strategy. Company S (Other food processing) illustrates this framing by embedding climate goals in strategic planning, engaging experts, and acting through supply programme interventions, stating: Our sustainability goals are a key way in which we manage our climate-related risks and are part of our strategic planning process . . . We had set goals for 2020 which include climate-related goals . . . and have since set a new strategy for 2025 to continue and expand our focus on these areas. . . . and we implement deforestation interventions in key agriculture supply programs, such as Cocoa Life and our Palm Oil Action Plan. . . . Since 2012, we have worked with internal and external experts to review the impact of major societal issues on our business and shape our strategic responses to them. (Company S, 2020)

Firms highlight the uncertainty and long time horizon of climate risks and the potential to reshape operational capabilities, including input availability, raw material costs, reputation, and customer-facing dynamics. Company T (Chocolate confection) notes that, due to the long-term aspect of climate-related risks, [these risks] tend to have a higher degree of uncertainty when assessing the probability of occurrence. However, the reputational risks play an important role with climate-related issues, which can make such risks become substantive strategic risks for the company. (Company T, 2022)

Similarly, Company U (Alcoholic beverages) acknowledges the inherent complexity of climate change, noting that “[w]ater scarcity is a long‑term physical risk for Company U across several locations,” while emphasising implications for business operations and financial performance: “the availability and quality of it has an impact on Company U’s production capacity and therefore our sales and financial performance” (Company U, 2021).

To navigate strategic uncertainty, firms deploy learning-oriented practices that translate ambiguous signals into actionable priorities. Salience is again constructed, but in this case, it is primarily guided by input from, or analysis of, trends and requirements articulated by external stakeholders. For example, firms use tools such as cross-functional workshops, expert consultations, continuous monitoring, and scenario analysis, often informed by frameworks such as the TCFD. These processes help firms identify evolving risks and consider them as strategically relevant. These tools further help firms coordinate responses and embed adaptive learning in decision-making. For example, Company U (2022) holds annual functional risk workshops and consults external experts; Company V (Alcoholic beverages, 2021) runs cross-functional workshops to prioritise high-impact risks and opportunities; and Company W (Aquaculture, 2021) continually monitors environmental parameters to inform siting and equipment decisions. Company X (Alcoholic beverages, 2018) integrates risk assessment into its global operations management systems and convenes regular technical meetings to update analyses.

While most firms construct salience through long-term risk analysis, some act on experienced salience as climate-related risks materialise via changing customer preferences, shifting market trends, and supply chain instability. These cases prompt firms to make concrete strategic adjustments rather than merely monitor risks. Company Y (Dairy & egg products, 2021) notes that “[p]ackaging has been identified as a main Strategic risk for Company Y as consumer pressures around plastics are moving at an unprecedented pace.” This example indicates that sustainable packaging is considered important not only because of regulatory pressures, but in this instance also gains more strategic, market-driven relevance. Company Z (Other food processing, 2021), for example, reports that “some consumer trends and interests are changing towards wanting more climate‑ and environmentally friendly foods and more plant‑based foods.” Some firms also see opportunity in climate dynamics. Company H (Alcoholic beverages, 2021) sees hotter summers increasing beverage demand, while Company AJ (Other food processing, 2020) plans to adjust product lines to align with evolving consumer preferences. These opportunity framings still depend on tools and frameworks to analyse risk and reduce uncertainty but draw attention to what is considered as strategically important to ensure long-term competitiveness.

In this framing, firms increasingly acknowledge the dynamic and evolving nature of climate risks, as well as the limitations of tools centred mainly on monitoring and assessment, prompting greater investment in more transformational forms of response. Company AA (Palm oil processing, 2020), observing severe weather effects on plantations, “has invested heavily in the Research & Development of palm seedlings which are more resilient to extreme weather patterns to ensure the sustainability of the plantations.” The firm also used the programme to adjust its business model by selling seedlings to smallholders to stabilise future supply. When salience is experienced, firms go beyond managerial planning towards strategic reconfiguration, often through R&D and product innovation, to discover new approaches to delivering their products. Company AB (Other food processing, 2021) engages in reuse-oriented packaging initiatives and product development. Company AC (Other food processing, 2022) expands plant-based offerings for food service customers, and Company Z (2021) embeds plant-based products and packaging innovations into portfolio development to capture transition opportunities.

The strategic necessity framing treats climate risk as a long-horizon, uncertain, and open-ended condition that can reshape business viability through input availability, operational capacity, reputation, and demand. When impacts are ambiguous, firms translate weak signals into manageable priorities through analytical tools and learning systems. When salience becomes experienced or more visible through market shifts or analysis, they move towards strategic reconfiguration, most commonly via transformational R&D and product innovation. The open-ended character of the risks also motivates cross-functional and inter-organisational coordination and stakeholder dialogue as ongoing learning mechanisms. Frameworks such as the TCFD and scenario analysis appear to sensitise firms to identify strategic implications and support consideration of multiple future pathways.

In supply chains, firms leaning into strategic necessity move beyond monitoring and supplier diversification to partnership-based resilience building. They invest in capacity building to improve climate resilience among producers. They recognise that heterogeneous risks require capabilities that develop over time rather than one-off solutions. Programmes like Company AD’s (Other food processing, 2021) Sustainable Farming Program support farmers in reducing climate impacts of practices, improving soil health and water efficiency, and competing in a resource-constrained future. Responsible sourcing initiatives likewise aim to secure long-term access to raw materials while enabling suppliers’ adaptation to socio-ecological change. Company AE’s (Other food processing) responsible sourcing framework anchors responsible sourcing in environmental, ethical, and social principles and uses a maturity model to transform value chain performance.

In sum, the strategic necessity framing preserves the diagnostic value of risk analysis but elevates climate risk into a strategy‑shaping agenda. Rather than relying on planning only and the tools that inform this, firms construct salience through ongoing learning and stakeholder signals, translate insights into provisional actions, and refine their approach through repeated cycles of innovation and collaboration. This produces a hybrid approach to mainstreaming climate risk: firms do make use of existing tools while at the same time building new tools and capacity to prepare, adapt, and respond as new information arises. Where firms encounter direct climate impacts or unambiguous market signals, their responses accelerate and broaden, combining R&D with portfolio adjustments and supplier development. Where impacts remain ambiguous, firms focus on turning uncertainty into strategic options and develop flexible pathways rather than fixed plans so that they can pivot quickly as conditions evolve.

Climate Risk as Societal Challenge

Firms that frame climate risk as a societal challenge emphasise its systemic nature and focus on building long‑term resilience. They highlight how climate impacts “will deeply affect the way we produce food in the future” (Company AF, Other food processing, 2018) or threaten “the sustainability of agriculture and terroirs” essential to production (Company AG, Alcoholic beverages, 2020). Within this framing, climate risk is understood not as a narrow firm‑level risk but as a challenge embedded in broader socio-ecological systems. This framing was the least common of all, though, and only a few firms seem to have shifted towards it over time, and then only partly. Company AF illustrates such a shift: Growing sustainably is Company AF’s long-term strategy and managing climate risks and opportunities is an integrated part of how Company AF does business. . . adapting to climate change and increasing resilience while, at the same time, playing a part in developing a low carbon future and providing climate friendly food to customers. (Company AF, 2021)

Here, complexity arises from long time horizons, diverse stakeholders, and uneven regional impacts. Firms explicitly acknowledge this complexity: “the risks are multi-dimensional and therefore we look at it in a holistic manner, straddling both, the external environment and the internal processes” (Company AE, 2019). Because many physical climate impacts are anticipated rather than fully realised, firms still need to construct salience to make the risk actionable. They use analytical frameworks to evaluate uncertainty across multiple dimensions.

However, firms with experienced salience, where climate impacts have already affected operations or threaten long‑term viability, tend to respond differently. As Company AG noted: Every year, climate change causes unstable meteorological conditions. . . In the longer term, the displacement of growing areas would have a critical impact on Company AG, calling into question the notion of terroir. (Company AG, 2021)

Similarly, Company AF states that “[o]ur fish are directly affected by climate risks such as rising sea water temperatures, algae blooms, ocean acidification and extreme weather events” (Company AF, 2018). Company AH (Dairy & egg products) echoes this distinction between current and future threats: “Acute risks already occur today. . . Chronic risks are more likely to manifest over the longer term, weighted to mid-century and beyond” (Company AH, 2021).

The open-endedness of these risks, where no single solution exists, prompts firms to focus on capacity building rather than one‑off fixes. They emphasise gradual development of long‑term resilience, often by extending existing efforts rather than adopting radically new strategies. For example, Company AI (Other food processing, 2021) stated: “Considering the severe impact of floods and high tides caused by climate change, we need to further improve our resilience.”

Many firms coordinate climate actions across multiple interconnected roadmaps. Company Y, for instance, reviews progress against “the overall climate roadmap – the regenerative agriculture roadmap for dairy – the packaging policy and the packaging transformation roadmap – the energy strategy, and the energy efficiency, green electricity, green thermal roadmaps” (Company Y, 2022). Higher experienced salience also leads to more concrete resilience-building interventions. These efforts are typically long-term, iterative, and oriented towards strengthening ecosystems and supply chains through various R&D and innovation initiatives: [We] launched a four-year partnership with Washington State University in 2019 . . . to identify barley varieties that flourish in regenerative agriculture and prove resilient to climate change. The Group is stepping up R&D expenses behind protective technology in case of acute weather risks (with a focus on hail and late frost) . . . The first resilient barley varieties were planted in 2021 and performed very well. The “heat dome” that the region faced in June 2021 eliminated some potential varieties, but the rest held up well despite an abnormally dry and hot summer. (Company AG, 2022)

Other firms invest in partnerships and regenerative farming to reduce suppliers’ vulnerability to climate shocks while securing more resilient raw materials. Company AD explains: Through the [Sustainable Farming Program], we are working with our farmers to reduce physical climate change impacts of farming practices, improve soil health, and improve water use efficiency. (Company AD, 2021)

These approaches are not mutually exclusive. Firms may pursue transformational interventions, such as R&D and partnerships, while also using analytical tools to manage uncertainty and allocate resources. Company Y, for example, combines long-standing commitments with practical action, as the firm states being: “strongly engaged in the implementation of regenerative agriculture (RA) practices. . . [which] aims at protecting soils and water, restoring biodiversity and sequestrating carbon in the soil,” thereby making the supply chain “more resilient to climate change” (Company Y, 2018).

In sum, firms that frame climate risk as a societal challenge view it as a systemic, long‑term issue involving many interconnected stakeholders. To handle the emerging risks, they rely on analytical tools to make uncertainty actionable and to guide decisions across the business in an iterative, adaptive way. When firms already experience climate impacts, they focus on concrete operational vulnerabilities and adopt more immediate resilience measures. Overall, firms prioritise long‑term capacity building over short‑term fixes, relying on learning and adjustment. To align these efforts, many integrate multiple roadmaps and combine data analysis, R&D, and collaborative initiatives to strengthen supply‑chain and ecosystem resilience.

Discussion and Conclusion

Towards a Framework for the Mainstreaming of Climate Risk Management

In this article, we examined how firms frame climate risk in distinct ways and explored what these differences reveal about the forms of sustainability mainstreaming that underpin their approach to climate risk. By examining strategic responses to climate risk in the global food and drink sector, we investigated the role of tools in the way complexity was framed, salience was constructed, and what the interaction between the two reveals about how firms approach climate risk management. Our core contribution lies in unpacking why firms tend to lean towards business‑as‑usual mainstreaming, even when they encounter signals that more transformative action may be required. We show how firms’ perceptions of the complexity and salience of climate risk shape the types of response they consider legitimate and feasible, and the role tools play in these processes. While our findings resonate with earlier research showing that firms often align climate risk management with existing strategic logics and routines (C. Wright & Nyberg, 2015, 2017), our analysis goes further in explaining how this occurs and under which conditions some firms begin to shift towards more transformational approaches aimed at strengthening socio-ecological systems (Lahneman et al., 2025).

Our findings show that mainstreaming through business‑as‑usual persists not only because of organisational inertia or economic self‑interest, but also because of the tools firms rely on to assess and manage climate risks. Risk matrices, ERM systems, materiality templates, and target dashboards translate the complexity of climate risk into structured categories that can be scored, ranked, and monitored. These tools stabilise particular interpretations of climate risk (Denis et al., 2006; Jarratt & Stiles, 2010; Jarzabkowski & Kaplan, 2015) and create a sense of controllability that reinforces incremental adjustments rather than systemic transformation (Pinkse & Gasbarro, 2019). This performative role of tools in constructing salience, narrowing attention, and legitimising business‑as‑usual responses helps explain why firms often revert to familiar risk management routines even when they recognise climate risk as a systemic threat. By foregrounding the role of tools in climate-related strategy-making, our study highlights an underexplored mechanism for why firms are mainstreaming sustainability through business-as-usual rather than transformation.

In the few cases where firms began adopting more transformational approaches to tackle climate risk, this shift occurred when they recognised that climate risk is a systemic problem that exceeds the capabilities of conventional tools (Burke & Wolf, 2021). These firms framed climate risk as a broader challenge requiring continuous and far‑reaching action, rather than simply stabilising operations or complying with regulators. The process of experienced salience, for example, through crop failures, extreme weather events, or supply‑chain disruptions, often provided an impetus for this reframing, which also resulted in the adoption of tools that more adequately helped address the issue (Jarratt & Stiles, 2010) or developing climate-specific tools in collaboration with other stakeholders (Burke & Wolf, 2021). Transformational responses emerged, but only when firms realised that the tools they relied on could no longer adequately capture the severity of the issue and engaged in more exploratory activities. By contrast, firms that remained within the first two framings continued to apply conventional risk management tools, which tend to be used to address other forms of risk, not climate risk in particular.

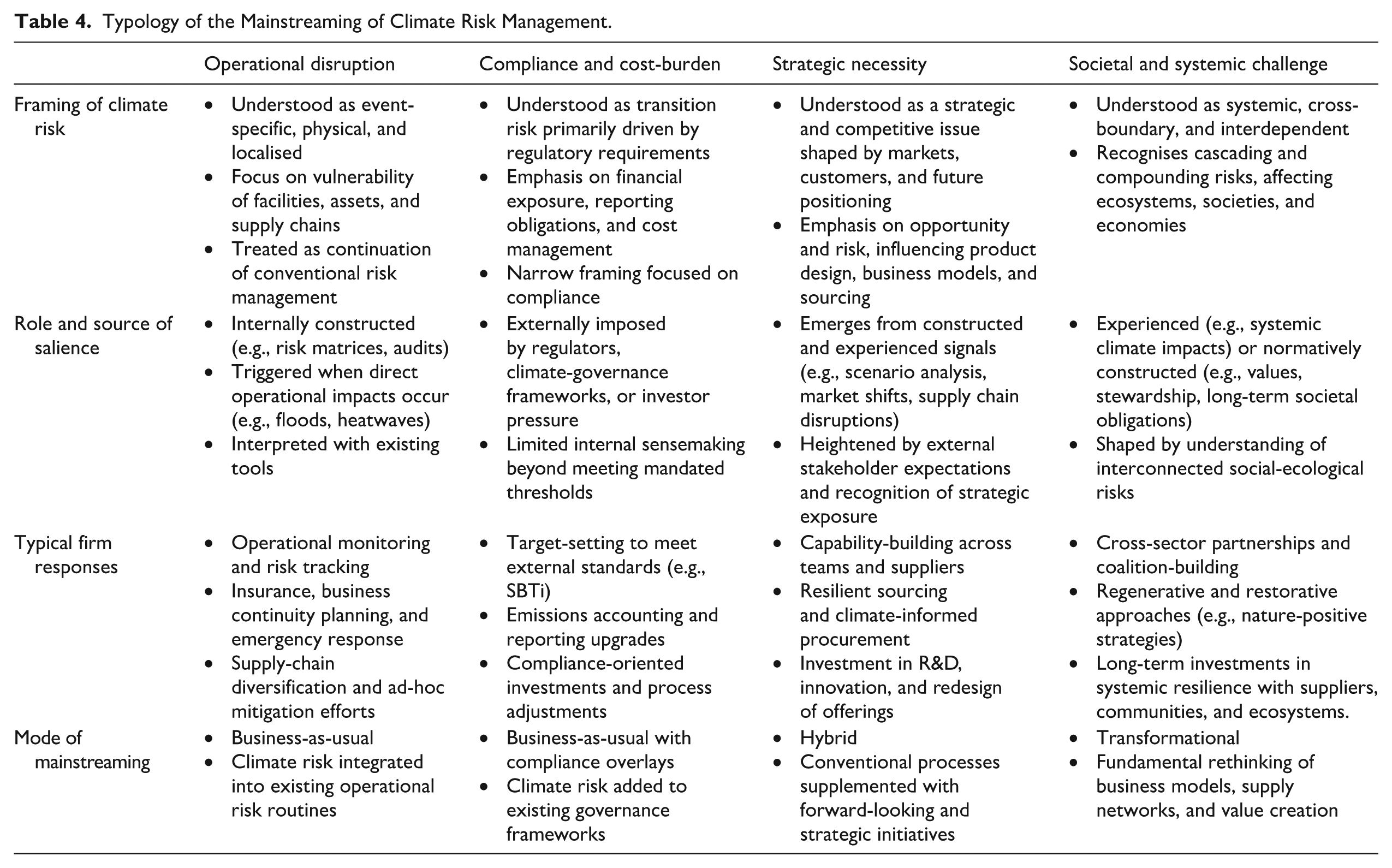

Based on our analysis, we develop a framework that clarifies how the centrality of tools shapes the mainstreaming of climate risk management (Table 4). It shows that firms’ responses depend on how they frame climate‑related complexity – whether as operational disruption, compliance burden, strategic necessity, or societal challenge – and on how salience is constructed (internally or externally) and/or experienced. These two dimensions, taken together, guide firms towards particular response patterns (Lovallo & Sibony, 2018; Neugebauer et al., 2016). A central insight is that firms perceive climate risk through distinct complexity framings and allocate attention and resources according to how they construct or experience salience. This is often mediated by the choice of tools and whether these reinforce the initial framing (Jarratt & Stiles, 2010; Pollock & D’Adderio, 2012) or prompt firms to acknowledge the systemic and interdependent nature of climate risk and consider more transformational approaches (Burke & Wolf, 2021).

Typology of the Mainstreaming of Climate Risk Management.

Our framework also shows that business‑as‑usual mainstreaming dominates across most framings of the perceived complexity of climate risk and the influence of internally constructed salience: firms tend to channel climate issues through existing risk‑management tools to make them appear manageable. Even when firms acted because they had directly experienced climate impacts, these experiences were often subsequently reframed using the same tools that underpin internally constructed salience. This pattern aligns with behavioural and practice perspectives on strategy, which highlight that bounded rationality and tool‑driven routines can introduce biases into decision‑making (Denis et al., 2006; Jarzabkowski & Kaplan, 2015; Lovallo & Sibony, 2018; Powell et al., 2011).

Contributions to Our Understanding of Sustainability Mainstreaming

With our framework and empirical insights, we make several contributions to the literature on sustainability mainstreaming (Vernay et al., 2022) and mainstreaming climate risk (Benischke et al., 2025; Bleda et al., 2023; C. Wright & Nyberg, 2017). First, our findings explain why business‑as‑usual mainstreaming of climate risk persists (C. Wright & Nyberg, 2015, 2017). We show that this persistence stems from the way firms frame climate‑related complexity and how salience – constructed or experienced – reinforces these framings. When climate risk is seen as operational disruption or a compliance‑ and cost‑burden, firms revert to conventional, routinised risk‑management tools. These tools both shape and narrow salience by filtering climate‑related information into established metrics, dashboards, and reporting cycles (Bleda et al., 2023; Pollock & D’Adderio, 2012). By drawing on highly routinised tools, firms limit their engagement with the risk to what these tools permit (Jarratt & Stiles, 2010; Pollock & D’Adderio, 2012; R. P. Wright et al., 2013). This filtering directs attention towards short‑term financial implications, creating a sense of controllability that allows firms to treat climate risks as manageable within existing processes (Galbreath, 2011; Pinkse & Gasbarro, 2019). While this constitutes a form of sustainability mainstreaming, it embeds climate risk into current routines rather than prompting transformational change, an approach ill‑suited for addressing the wicked nature of climate risk.

Second, our study shows that although firms have begun to mainstream climate risk management, they do so in largely reinforcing, non‑transformative ways, and we identify the mechanisms that produce this neutralisation. Prior research has argued that firms frequently neutralise climate risk by aligning it with prevailing commercial priorities and organisational routines (Berger-Schmitz et al., 2023; C. Wright & Nyberg, 2015, 2017). Our findings corroborate this insight but deepen it by showing how this neutralisation is produced through the interaction of complexity framings, salience construction, and the use of tools in both. In the operational disruption and compliance and cost-burden framings, firms translate climate risk through internally constructed salience (e.g., via risk dashboards) and address it with established tools (e.g., continuity planning, target-setting, monitoring, efficiency upgrades). We show that this process is not merely a choice of tools, but a tool‑enabled sensemaking process of climate risk that shapes what becomes visible, important, and actionable (Jarratt & Stiles, 2010; R. P. Wright et al., 2013). This finding demonstrates how climate risk is absorbed into existing categories of firm attention, narrowing its meaning and constraining strategic horizons. Even when direct physical impacts occur or salience is constructed through external pressures from regulators or investors, firms tend to continue relying on existing routines, with only heightened urgency or modest strategic adjustments. Firms incorporate climate risk into established strategy‑making processes so that it conforms to the current strategic direction. It is not treated as a trigger for strategic redirection (Bansal et al., 2025) but as an external factor that must be stabilised and contained (C. Wright & Nyberg, 2015, 2017), which often results in shallow or avoidant responses (Berger-Schmitz et al., 2023). Our contribution thus lies in unpacking the mechanisms of salience construction and using routinised tools for risk management that explain why neutralisation occurs, even under heightened pressure to address climate risk.

Finally, we show that business‑as‑usual mainstreaming is not a stable end-state but an evolving process. As firms experience the salience of climate risk more directly and face rising perceived complexity, some begin to shift towards more transformational forms of mainstreaming. Firms often hold multiple framings simultaneously, and in our sample, several were moving towards the strategic necessity and societal challenge framings. These shifts were reflected in a growing use of scenario planning, materiality assessments, bespoke risk‑management tools (Jarratt & Stiles, 2010), and engagement with external experts to help interpret emerging uncertainties and build resilience (Clément & Rivera, 2017). While stakeholder requests, and their underlying power and legitimacy (Eesley & Lenox, 2006; Mitchell et al., 1997; Neugebauer et al., 2016), have remained relatively stable over the past decade, firms’ increasing experience of direct physical impacts has made climate risk more tangible and urgent. These emerging framings recognise the deeper uncertainty and more open‑ended risk (Linnenluecke et al., 2012; Linnenluecke & Griffiths, 2010), consistent with the lack of agreed‑upon solutions (Pinkse et al., 2024) and the fragility of the socio‑ecological systems on which firms depend (Bansal et al., 2025; Dentoni et al., 2021). As experienced salience increases through firms’ exposure to extreme weather and more gradual physical impacts, they increasingly acknowledge that established risk management tools may no longer suffice (Linnenluecke et al., 2015). Our analysis thus explains how shifts towards more transformational forms of mainstreaming originate, not as abrupt departures from business‑as‑usual, but as emergent responses to rising complexity and increasingly experienced salience. However, these transformational responses remain tentative, characterised by adaptive learning, innovation, partnerships, and flexible strategic pathways. This underscores that mainstreaming climate risk management is a dynamic, evolving process, shaped by how firms encounter and interpret changing climate realities.

Limitations and Future Research

Our study has several limitations that future research could address. First, it relies on self-reported data from the CDP data, which may be subject to impression management (Callery, 2023). Moreover, the framing of the CDP questions that we analysed explicitly asks firms to report how they address climate risks, which may bias responses towards reporting manageable risks and away from the broader complexity and uncertainty inherent in climate change. As a result, more transformational approaches may be underrepresented in our dataset and could be more widespread in practice than the data reveals. To address these limitations, future research could complement our study’s approach with primary data, such as interviews, case studies, or ethnographic methods, to assess how climate risk management practices are enacted and embedded within organisational routines. While our findings suggest that more transformative forms of mainstreaming may be emerging, further research is needed to determine whether this shift persists and how it affects firms’ efforts to respect the limits of the socio-ecological systems (Bansal et al., 2025; Whiteman et al., 2013).

Second, while we draw on a practice perspective on strategy, further leveraging this lens would enable a closer examination of how more transformative climate responses emerge. It can illuminate how tools, routines, discourses, and interactions between actors enact climate strategy in practice (Jarzabkowski, 2004; Vaara & Whittington, 2012; Whittington, 2006). It would allow researchers to trace how compliance-oriented routines, such as reporting cycles and science-based target processes, gradually evolve into new strategic practices that reshape competitiveness. Over time, these routines may also help firms move beyond narrow self-interest and attend to the resilience of the socio-ecological systems on which they depend. A practice perspective could also shed light on how wicked problems like climate risk are framed, legitimised, and enacted or inhibited (Krull & Pinkse, 2025), offering valuable insights into how mainstreaming sustainability might become more transformational. Extending the analysis beyond the food and beverage sector would further deepen understanding, as industries differ in risk exposure, stakeholder pressure, and regulatory scrutiny. For example, firms in our sample considered regulatory risk relatively manageable because the sector is less affected by policies such as emissions trading schemes. Future research should therefore examine more carbon‑intensive sectors, such as energy and heavy industry, to assess how processes of sustainability mainstreaming may differ under stronger regulatory and transition pressures.

Finally, our analysis focused on how firms report on the way in which they address climate risks, but did not assess the effectiveness of different forms of mainstreaming. There is therefore a need for a critical examination of which forms of mainstreaming effectively address physical and transition risks and support the regeneration of socio‑ecological systems, rather than contribute to their further degradation. Future research should assess how different forms of mainstreaming translate into real outcomes, and whether transformational approaches indeed offer greater potential for meaningful and durable climate action.

Footnotes

Acknowledgements

We would like to thank Sanchari Gosh for her research assistance.

Ethical Considerations

This article does not contain any studies with human or animal participants.

Consent to Participate

Not applicable.

Consent for Publication

Not applicable.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors disclosed receipt of the following financial support for the research: This work was supported by the University of Manchester via the (1) AMBS Support Fund and the (2) MIOIR Small Grant scheme.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from CDP, but restrictions apply to the availability of these data, which were used under licence for the current study, and so are not publicly available.

Mandatory Disclosure of Use of Artificial Intelligence

Not applicable.