Abstract

Debt is a ubiquitous component of households’ financial portfolios. Yet we have scant understanding of how household debt constrains spending on needed health care. Diverse types of debt have different financial properties and recent work has shown that they may have varying implications for spending on needed health care. In this article, we explore the associations between indebtedness and medication nonadherence. First, we consider overall debt levels and then we disaggregate debt into types. We use a population-based sample of 434 residents of southeast Michigan who had been prescribed medications, collected in 2009-2010, the wake of the Great Recession. We find no association between medication nonadherence and total indebtedness. However, when we assess each type of debt separately, we find that having medical or credit card debt is positively associated with medication nonadherence, even net of household income, net worth, and other characteristics. Furthermore, patients with greater amounts of medical or credit card debt are more likely to be nonadherent than those with less. Our results suggest that credit card debt and medical debt may have serious implications for the relative affordability of prescription medications. These associations have been overlooked in past research and deserve further examination.

Concern about the cost of medications is a major cause of nonadherence to prescription medication regimens (Briesacher, Gurwitz, & Soumerai, 2007; Kurlander, Kerr, Krein, Heisler, & Piette, 2009; O’Brien, 1989; Stuart & Grana, 1998). Financially constrained patients are forced to make difficult choices about which of their needs will take priority in spending, and other financial obligations may be more immediately urgent than filling their prescriptions or using the full amount of medication that has been prescribed when other bills are due or creditors are demanding repayment. Under these circumstances, patients might become nonadherent to their prescription medication regimen, which we define in this article as “cutting doses or splitting pills in order to save money.” In the extant literature, much of the discussion of the financial side of cost-related medication nonadherence has been limited to the study of income, health insurance, and other available resources (Eaddy, Cook, O’Day, Burch, & Cantrell, 2012; Mielck, Kiess, Knesebeck, Stirbu, & Kunst, 2009; Ngo-Metzger, Sorkin, Billimek, Greenfield, & Kaplan, 2012). Our article expands this literature by conceptualizing an association between competing financial and health needs: We consider the role of debt as a restriction on available resources and as a potential predictor of medication nonadherence. Diverse types of debt have different financial properties and recent work has shown that they may have varying implications for spending on needed health care (Kalousova & Burgard, 2013). The association between debt and medication nonadherence is especially important at a time when an unprecedented number of American households reports no assets or debts greater than assets (Allegretto, 2011).

Holding some debt has been common among American families for decades. In the past 20 years, the share of U.S. households with any debt has only risen slightly, from 74% to 77% (Bricker, Kennickell, Moore, & Sabelhaus, 2012; Kennickell & Starr-McCluer, 1994). However, there has been an increase in the share of households with very high debt burdens because individuals are borrowing more and doing so with the help of a highly diverse spectrum of accessible debt products. Importantly, the percentage of individuals with a credit card rose from 16% in 1970 to 75% in 2004. Over the same period, the percentage of card holders unable to pay their credit card balance in full each month rose from 37% to 56% (Federal Reserve Board, 2006).

Debts carry a variety of complex social meanings and their potential negative or positive consequences depend on the holder’s resources and the outcome of interest. Mortgage debt or student loans have traditionally signaled creditworthiness and middle-class status, are an important means of achieving valued life goals, and are often considered to be “harmless” as long as they are being repaid on time. Other types of debt, particularly credit card debt, have been colloquially described as “bad debt.” While it can allow for consumption of important goods and services, if not repaid on time, credit card debt can lead to high interest penalties and may accumulate to unmanageable and socially stigmatized levels. Medical debt is a special type of debt because it may reflect a medical need at the same time that it limits access to medical care. Some individuals may wish to avoid the stigma of “bad debt” even at the cost of missing medications, or may already carry unmanageable “bad debt” loads and are trying to avoid exacerbating their situation by cutting back on their medication spending. Although we are limited by the cross-sectional nature of our data set, our article contributes to the understanding of the complex meanings associated with different types of debt by examining whether there are certain debt types that are more strongly associated with medication nonadherence than others.

First, we ask, is there an association between medication nonadherence and overall debt after adjusting for sociodemographic characteristics, income, and net worth? Second, we explore whether the association between medication nonadherence and debt varies across debt types. Can we distinguish “bad” from “harmless” debt in relation to medication nonadherence?

Methods

We use data from the Michigan Recession and Recovery data set, a unique population-based sample of residents in the Detroit metro area from 2009-2010 that collected extensive debt measures, as well as information about income and wealth. These data were collected through in-person interviews of a stratified random sample of English-speaking adults 19 to 64 years old living in Southeastern Michigan (Macomb, Oakland, or Wayne County). African Americans were oversampled. The interviews lasted approximately 1 hour and were administered between October 2009 and March 2010. There were 914 respondents, and the final response rate was 82.8%. For the purposes of our analysis, only respondents who reported currently being on any prescription medications (N = 434) were eligible. To address small amounts of item missing data, we conducted a multiple imputation procedure on the data set and generated five additional data sets using the IVEware software (Raghunathan, Solenberger, & Van Hoewyk, 2002). All the results presented here are based on the five multiply imputed data sets. 1

Measures

Medication nonadherence

We first determined who was prescribed medication by asking “Are you currently on any prescription medications?” and 47.6% of the sample answered yes. For those who were prescribed medications, we then assessed cost-induced medication nonadherence with a single item. Respondents were asked, “Are you skipping doses or cutting pills in order to save money?” and 13.1% answered in the affirmative.

Debt

All Michigan Recession and Recovery Study respondents were asked a battery of questions pertaining to their wealth, income, financial stability, and indebtedness, including questions about the types of debt they carry. The interviewer instructed them to consider their own debts and the debts of anyone for whom they were financially responsible at the outset of this section of the survey. If they said they had a specific type of debt, we inquired about the amount with the following question, “About how much do you owe on [specific debt type]?.” We asked separately about housing debt (held by 51.1%; conditional mean $142,151), car loans (held by 50.0%; conditional mean $11,856), student loans (held by 19.3%; conditional mean $29,935), credit card debt (held by 64%; conditional mean $8,811), medical debt (held by 30.3%; conditional mean $7,270), and “any other type of debt” that did not fit into one of the predefined categories (held by 23.4%; conditional mean $13,227). Respondents who were reluctant to give an answer were encouraged to provide their best estimate in reference to a set of categories, and values within these categories were assigned, a typical approach in collecting financial data. For the analysis, we transformed the debt values to their natural log form, as is frequently done in order to mitigate the effect of outliers, a particularly important consideration in our relatively small sample (Acock, 2010). 2

Measures of wealth, net worth, and income

To capture assets, we collected information about the value of primary residence and any cars, and checking, savings, and/or individual retirement accounts 401K. We constructed a net worth measure by subtracting respondents’ debts from their assets and generating a dichotomous indicator denoting those whose net worth was less than zero. 3 Respondents also provided their total household income from all sources before taxes in 2008, which we used in its logged continuous form.

Health

We included two measures of health that past literature linked to increased likelihood of medication nonadherence: the number of chronic conditions with which a respondent has been diagnosed and a depression symptom scale. Respondents answered a set of questions about whether they had “ever been told by a doctor or health professional” that they had a diagnosis of a specific chronic condition. These conditions included heart attack, coronary heart disease, angina, or congestive heart failure; high blood pressure or hypertension; asthma; chronic lung disease, such as bronchitis, emphysema, or chronic obstructive pulmonary disease; diabetes or high blood sugar; arthritis or rheumatism; cancer or a malignant tumor; and “any other serious, chronic condition.” To assess depression, we used the Patient Health Questionnaire, a validated 9-item scale based on the diagnostic criteria for major depressive disorder in the Diagnostic and Statistical Manual of Mental Disorders, fourth edition (Kroenke, Spitzer, & Williams, 2001).

Other variables

We considered respondents’ age, gender, race (African American vs. not), and educational attainment (bachelor’s degree or more vs. less education). We also assessed health insurance status. Because most respondents reported having some type of health insurance (93%), we created a measure that distinguishes between public (14%), private (79%), and no insurance at all (7%). Public health insurance included Medicare, Medicaid, Medi-gap, State-sponsored other type of insurance, and Indian Health Service coverage.

Statistical Analyses

We first examined bivariate associations between the variables of interest. To assess the significance of associations, we estimated separate logistic regression models predicting medication nonadherence and using each variable of interest as the sole predictor. In Table 1, we report the p values obtained from these models. We then estimated multiple regression models to examine the association between different measures of debt and medication nonadherence, examining both the dichotomous presence of debt and the amount of debt in separate models. All analyses were weighted to make the sample representative of the residents of Southeastern Michigan between the ages of 19 and 64 years. We account for complex sample survey design in Stata/SE 12 and use -mi- commands that allowed us to analyze the five multiply imputed data sets and generate one pooled estimate after the application of Rubin’s combination rules (StataCorp, 2011).

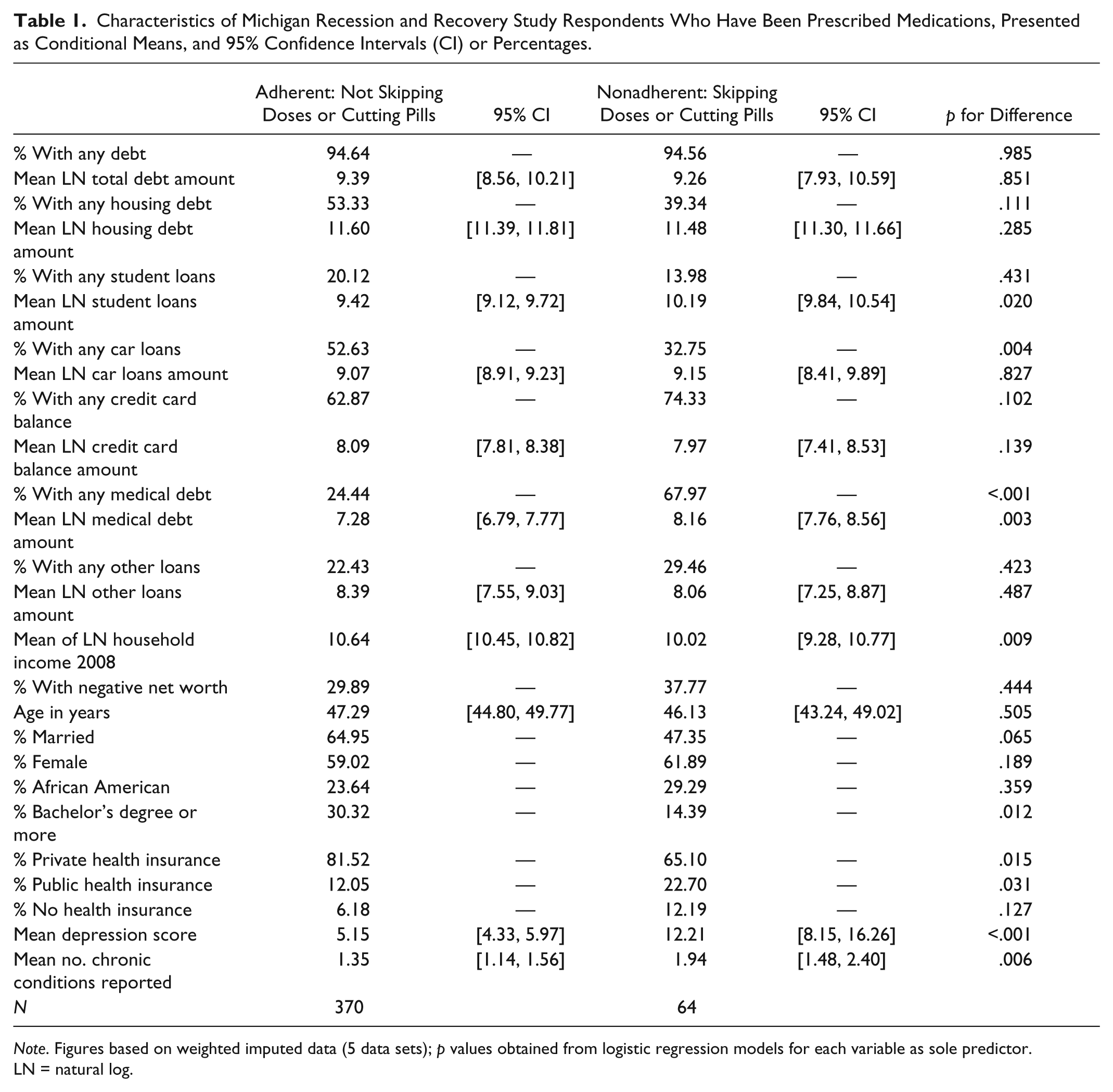

Characteristics of Michigan Recession and Recovery Study Respondents Who Have Been Prescribed Medications, Presented as Conditional Means, and 95% Confidence Intervals (CI) or Percentages.

Note. Figures based on weighted imputed data (5 data sets); p values obtained from logistic regression models for each variable as sole predictor. LN = natural log.

Results

Table 1 the shows descriptive characteristics of the analytical sample stratified by medication adherence status. About 13.1% were skipping doses or cutting pills for cost reasons in the past year. Among both adherent and nonadherent respondents, nearly 95% reported having some type of household debt. The difference across groups in the logged mean value of total debt is not significant. Adherent and nonadherent individuals also did not differ in the likelihood of holding housing debt (59% vs. 39%). We found a statistically significant difference in the logged amount of student loans held by the two groups, with the nonadherent individuals owing more (means 9.42 vs. 10.19). Adherent individuals were more likely to have car loans than nonadherent individuals (52.6% vs. 32.3%), but we found no statistically significant difference in the amounts of car loans held. We also found no significant difference in amount of credit card debt held. The nonadherent respondents were more likely to report any medical debt (68.0% vs. 24.4%) and also had significantly higher amounts of logged medical debt (8.16 vs. 7.28). For reference, we provided mean and median amounts of different types of debt without natural log transformation in the appendix.

There was no statistically significant difference across groups in the likelihood of having negative net worth, although adherent respondents have higher logged household incomes (10.6 vs. 10.0). Those skipping doses or cutting pills were marginally less likely to be married (47% vs. 65%) and significantly less likely to have a bachelor’s degree (14.4% vs. 30.3%). Nonadherent respondents also reported significantly more chronic conditions (1.9 vs. 1.4), had much higher depression scores (moderate 12.2 vs. mild 5.2), and were less likely to report private health insurance and more likely to report public health insurance.

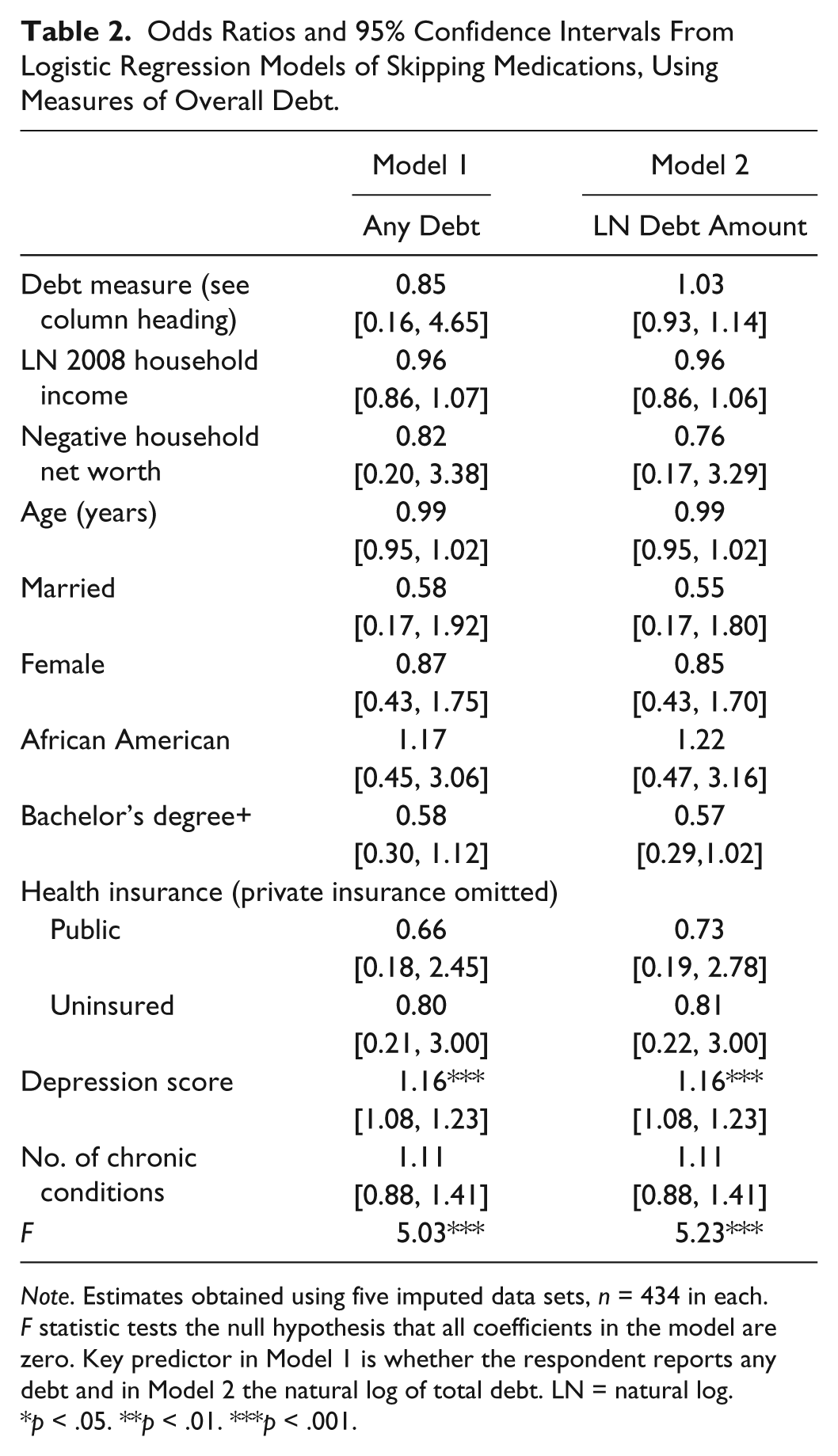

Table 2 presents the associations between medication nonadherence and the presence (Model 1) and the amount (Model 2) of total debt, adjusting for sociodemographic characteristics, financial indicators, health, and health insurance. We found no significant association between total debt and medication nonadherence in either model. The only significant predictor in these models was the measure of depression (odds ratio [OR] = 1.16 in both).

Odds Ratios and 95% Confidence Intervals From Logistic Regression Models of Skipping Medications, Using Measures of Overall Debt.

Note. Estimates obtained using five imputed data sets, n = 434 in each. F statistic tests the null hypothesis that all coefficients in the model are zero. Key predictor in Model 1 is whether the respondent reports any debt and in Model 2 the natural log of total debt. LN = natural log

p < .05. **p < .01. ***p < .001.

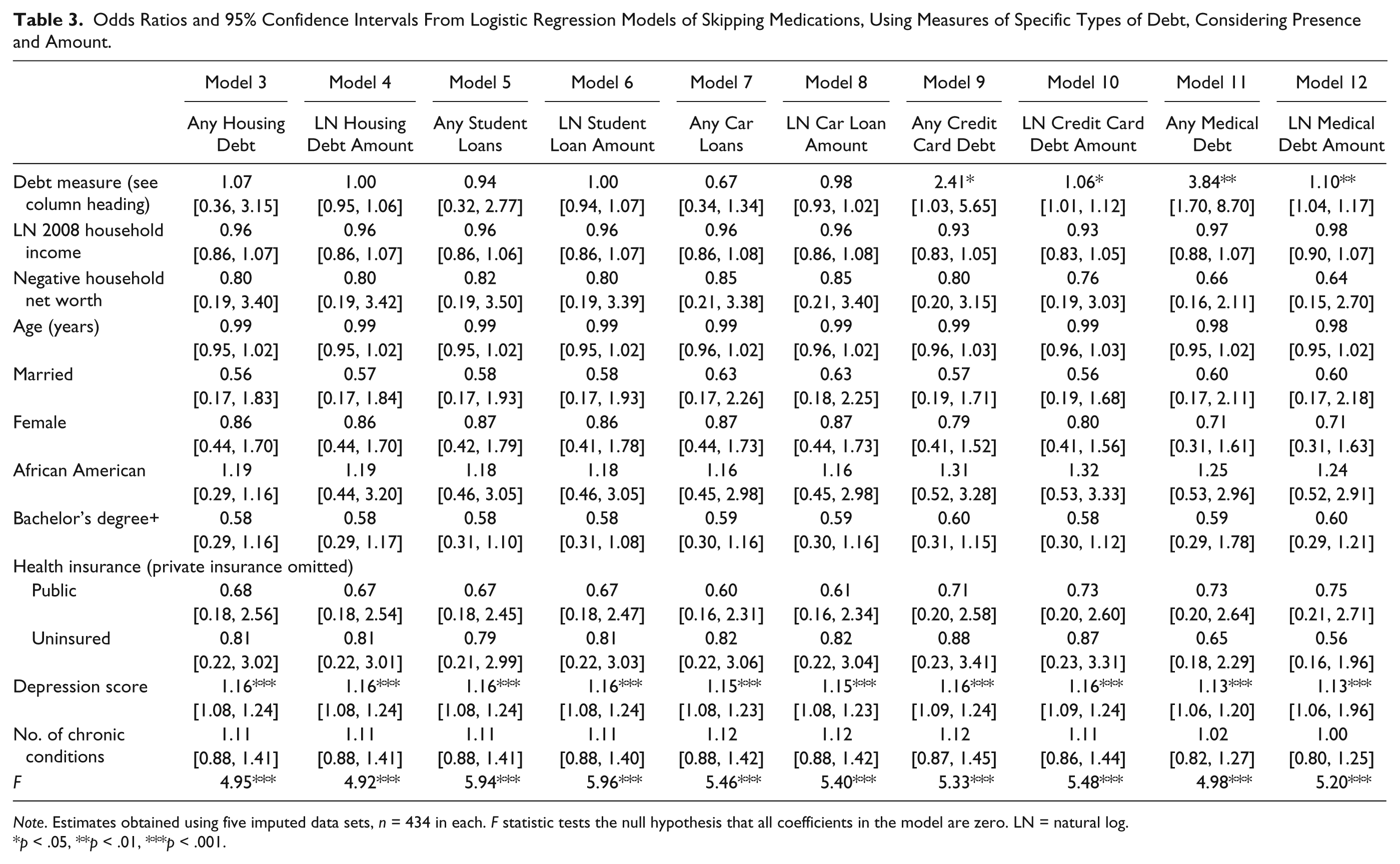

In Table 3 (Models 3 through 12), we show the associations between the presence or amount of type of debt and nonadherence. We found significant associations only with the presence and amounts of credit card debt and medical debt. Respondents with any credit card debt were more likely than those with no such debt to be skipping or cutting their medications (OR = 2.41), and odds of nonadherence increased with the logged amount of credit card debt (OR = 1.06). Similarly, having any medical debt predicted medication nonadherence (OR = 3.84), and those odds of nonadherence increased with the logged amount of medical debt (OR = 1.10) Depression was also strongly positively associated with nonadherence in these multiple regression models.

Odds Ratios and 95% Confidence Intervals From Logistic Regression Models of Skipping Medications, Using Measures of Specific Types of Debt, Considering Presence and Amount.

Note. Estimates obtained using five imputed data sets, n = 434 in each. F statistic tests the null hypothesis that all coefficients in the model are zero. LN = natural log.

p < .05, **p < .01, ***p < .001.

Discussion

Researchers have documented that the amount and type of financial resources held influence whether and what type of health care people seek when they need it (Lutfey & Freese, 2005). Existing research has emphasized certain types of resources, most often income or health insurance (Hartung et al., 2008; Kullgren et al., 2010). Our article builds on this framework by suggesting that although these available resources most certainly matter, they must be evaluated in relation to the competing demands placed on them. As other recent work on debt and foregone medical care (Kalousova & Burgard, 2013), we consider debt to be a prominent competing demand on resources and examine the associations between different types of debt and medication nonadherence, before and after adjusting for income, net worth, and health insurance.

Our descriptive results indicate that those who are nonadherent to their medication share some important similarities with their adherent counterparts, but nonadherent individuals are more disadvantaged, showing significantly lower educational attainment and household income. Moreover, we found that adherent individuals are more likely to have access to private health insurance. These results are in line with past research on nonadherence, which suggests that characteristics of health insurance—especially the amount of copay required—are an important stratifying mechanism in access to care that extends beyond the mere fact of having versus not having health insurance (Hartung et al., 2008; Sen et al., 2012). Also consistent with past research, we found that a high depression score was associated with medication nonadherence (Bautista, Vera-Cala, Colombo, & Smith, 2012; Schoenthaler, Ogedegbe, & Allegrante, 2009; Zivin, Madden, Graves, Zhang, & Soumerai, 2009). Of course, a plausible alternate explanation for this association is that patients might be cutting back on medication prescribed to them to address their depression, which could subsequently worsen their depressive symptoms, potentially accounting for the higher depression scores we find for this group. Furthermore, we found that the nonadherent population reports more chronic conditions. The presence of multiple conditions could indicate both adverse effects of earlier nonadherence on these respondents’ current health, as well as the greater cost burden that multiple prescriptions impose on them, which may propel them to privilege one medical need over another. Although a comprehensive treatment of these complex causal questions is beyond the scope of the current study, past research found support for both hypotheses (Henriques, Costa, & Cabrita, 2012; Osterberg & Blaschke, 2005).

Our analyses go beyond prior studies by considering the role of debt in nonadherence. In our multiple regression models, we first tested the association between having debt and foregoing medication, and then tested the association between the amount of debt and likelihood of foregoing medication. Our models showed that merely having debt does not lead to nonadherence, indicating that debt is a ubiquitous item in household budgets that may not cause difficulties in many cases. Similarly, having larger amounts of debt is not necessarily associated with nonadherence.

Our second research question asked whether it is possible to distinguish between “bad” and “harmless” debt, so we disaggregated the overall debt burden by the debt types composing it. We found that not all types of debt were associated with medication nonadherence, but having unpaid credit card balances and medical debt are associated with nonadherence. The likelihood of medication nonadherence also increases with greater amounts of these types of debt. Both an unpaid credit card balance and medical debt fulfill the criteria of what we understand to be “bad” debt—namely, they can accumulate quickly and unexpectedly. A substantial amount of unpaid medical debt may prevent people from seeking medical attention at their usual point of care. Unpaid credit card balances in particular might carry additional social stigmatization. Rather than facing escalating interest rates, patients may opt to cut back on their medication expenses.

Limitations

Despite these clear findings, our study has several limitations that need to be considered. Most important, we presented an analysis based on cross-sectional data. Thus, we cannot make any definite claims pertaining to the ordering of events. For example, we do not know with certainty whether medication nonadherence preceded or followed debt accumulation. By asking about nonadherence only in the past year, we were improving the likelihood that we are assuming correctly about the temporal order. However, reverse causality is a distinct possibility. Medical debt in particular could be plagued by this analytical issue. As we have argued, foregone medical care has been shown to lead to worse health outcomes, including a greater likelihood of hospital admissions for some patients. Medication nonadherence and debt could be linked together by a cyclical, self-reinforcing mechanism. Fully disentangling associations of this nature will be possible only with a larger longitudinal data set and it is therefore important to keep in mind that our study only provides initial contribution to what we hope will become a much more comprehensively explored area of research in the future.

Our study relied on self-reported data related to both debts and medication nonadherence, and measures of this type have been critiqued on the basis of reliability. Behavioral economists have argued that the amount of debt households think they have and the amount of debt they actually have may not be closely related (Keese, 2012). The conclusions we draw from our study would benefit by being verified using more objective debt data. There are no steps we could take to obtain more reliable data about medication nonadherence. Although other studies conducted in clinical settings with help of pharmaceutical dispensing data can directly measure whether their respondents have been taking their prescriptions (Greenley et al., 2012; Stegemann et al., 2012), our interviews were conducted in the homes of a representative sample of working-age residents in southeastern Michigan. Objective measures of nonadherence are not available in this setting. At the same time, because medication nonadherence was not portrayed as a core area of interest to our respondents and because it was not performed in a medical setting, it is unlikely they would have perceived any incentive to give deceptive information about this health behavior.

Conclusion

Indebtedness may influence decisions that patients make about whether they take their prescribed medications or not. Although some debts might be indicative of access to credit and middle-class status, others may put people at risk of medication nonadherence. Our study highlights the need for a more comprehensive understanding of financial profiles when studying access to medical care. Indebtedness, unlike health insurance status and sometimes income, may not be immediately apparent to a medical services provider, although debt burden has serious implications for the affordability of prescription medications. Debt—especially credit card debt and medical debt—might be an invisible hurdle keeping patients from adhering to their medication regimen that researchers have not previously considered.

The findings presented in this article have implications for both researchers and clinicians. The positive associations between medical and credit card debt and medication nonadherence implies that research concerned with examining how socioeconomic disadvantages limit access to care and influence health behaviors would be improved by a more careful consideration of varied aspects of financial portfolios, beyond the most commonly studied indicator, income. Similarly, in clinical practice, patient’s insurance status and income may not provide sufficiently nuanced understanding of why some patients find the cost of medications more burdensome than others. Even those who would not appear at risk by these measures could be in a financially precarious situation because of debts. When addressing cost-related medication nonadherence, a discussion of competing financial demands, debt among them, could lead to more successful interventions.

Footnotes

Appendix

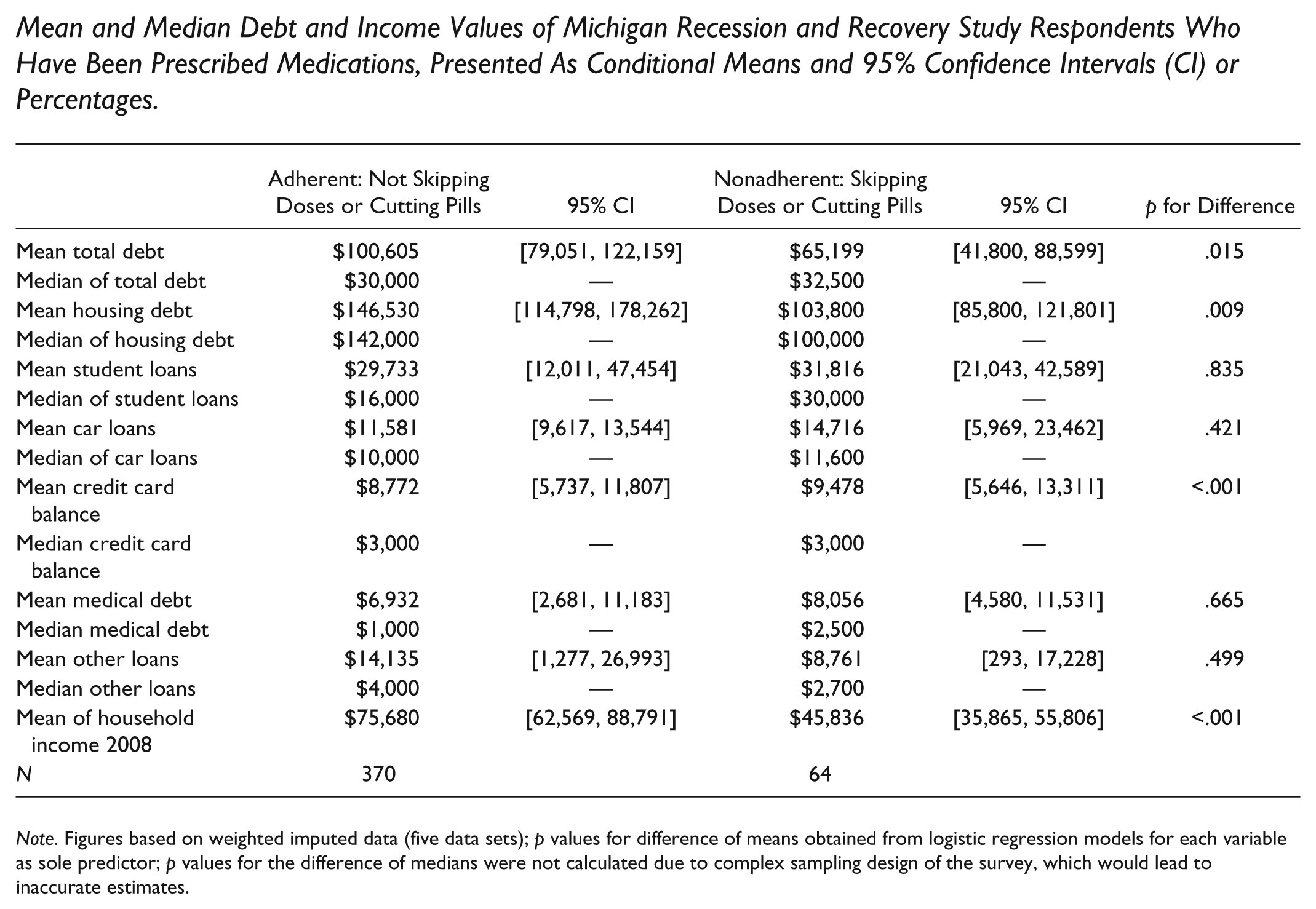

Mean and Median Debt and Income Values of Michigan Recession and Recovery Study Respondents Who Have Been Prescribed Medications, Presented As Conditional Means and 95% Confidence Intervals (CI) or Percentages.

| Adherent: Not Skipping Doses or Cutting Pills | 95% CI | Nonadherent: Skipping Doses or Cutting Pills | 95% CI | p for Difference | |

|---|---|---|---|---|---|

| Mean total debt | $100,605 | [79,051, 122,159] | $65,199 | [41,800, 88,599] | .015 |

| Median of total debt | $30,000 | — | $32,500 | — | |

| Mean housing debt | $146,530 | [114,798, 178,262] | $103,800 | [85,800, 121,801] | .009 |

| Median of housing debt | $142,000 | — | $100,000 | — | |

| Mean student loans | $29,733 | [12,011, 47,454] | $31,816 | [21,043, 42,589] | .835 |

| Median of student loans | $16,000 | — | $30,000 | — | |

| Mean car loans | $11,581 | [9,617, 13,544] | $14,716 | [5,969, 23,462] | .421 |

| Median of car loans | $10,000 | — | $11,600 | — | |

| Mean credit card balance | $8,772 | [5,737, 11,807] | $9,478 | [5,646, 13,311] | <.001 |

| Median credit card balance | $3,000 | — | $3,000 | — | |

| Mean medical debt | $6,932 | [2,681, 11,183] | $8,056 | [4,580, 11,531] | .665 |

| Median medical debt | $1,000 | — | $2,500 | — | |

| Mean other loans | $14,135 | [1,277, 26,993] | $8,761 | [293, 17,228] | .499 |

| Median other loans | $4,000 | — | $2,700 | — | |

| Mean of household income 2008 | $75,680 | [62,569, 88,791] | $45,836 | [35,865, 55,806] | <.001 |

| N | 370 | 64 |

Note. Figures based on weighted imputed data (five data sets); p values for difference of means obtained from logistic regression models for each variable as sole predictor; p values for the difference of medians were not calculated due to complex sampling design of the survey, which would lead to inaccurate estimates.

Acknowledgements

We thank Tedi Engler for assistance with coding the data, Kristin Seefeldt for thoughtful comments, Sheldon Danziger for his leadership on the project, Shawn Pelak for managing the project, staff at the Survey Research Operations unit at the Institute for Social Research for gathering the data, and our study respondents. We also thank the editor and three anonymous reviewers for their contributions to improving the quality of the final article. Any opinions expressed are solely those of the authors.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article:

Data collection for this study was supported by funds provided to the National Poverty Center (NPC) by the Office of the Assistant Secretary for Planning and Evaluation at the U.S. Department of Health and Human Services, the Office of the Vice President for Research at the University of Michigan, the John D. and Catherine T. MacArthur Foundation, and the Ford Foundation.