Abstract

We study the determinants of the maturity structure of public debt, taking as case study the regional governments of Spain. The structure of public debt is a source of vulnerability and contagion in public debt markets. Our empirical models show that regional governments reacted to increasing financing needs by leaning more toward short-term debt, instead of resorting to longer-term debt to seek the minimization of liquidity risks, a fact that is consistent with theories that predict the willingness of public financial managers to reveal to the markets their fundamental solvency and their commitment to fiscal (consolidation) plans. At the same time, we find that increased central government transfers raise the tendency of markets to hold long-term instruments, which may reflect their expectation that regional debt be bailed out/guaranteed by the center. Finally, we do not find evidence of significant differences in the maturity structure depending on the quality of the issuer.

Keywords

In most advanced economies, budget deficits, and public debt, have risen rapidly since the onset of the 2008 financial and economic crisis. As a consequence, there has been recently a significant revival in the literature dealing with the macroeconomic impact of public debt. This increase in public debt has been accompanied by a change in its structure (Hartwig-Lojsch, Rodríguez-Vives, and Slavik 2011). This is not a secondary issue, given that a recent strand of the literature has highlighted that the financing method and the resulting composition of public debt can also have sizable economic effects. For example, the structure of public debt can influence the liquidity structure of the economy, capital market stability or, more in general, sovereign credit risks, as it determines how vulnerable the balance sheet of a given government is to financial shocks, in particular those stemming from changes in interest rates and sudden changes in capital flows. 1 The exposure to vulnerabilities of this kind can be particularly acute in the case of subnational governments. Indeed, while subnational debt crises have reoccurred in both developed and developing countries over past decades (Canuto and Liu 2013; Liu and Waibel 2008), fiscal pressures for the subnational levels of government heightened during the most recent global financial crisis. In the particular case of Europe, given the existence of spillover effects among debt markets of euro area peripheral countries, these risks stemming from regions in one country could even become euro-wide risks (van Hecke 2013; Caporale and Girardi 2013). 2

Most of the studies that look at the determinants of the structure of sovereign debt tend to focus on vulnerability risks, identified with liquidity risks. Nevertheless, there is a broader, related literature 3 that stresses the existence of a trade-off between, on one hand, liquidity risk considerations of the kind discussed before, and, on the other hand, borrowers’ preference for short-term debt due to private information about future credit ratings. Thus, from the public financial management point of view, and in order to anticipate subsovereign (and national) fiscal solvency crisis, policy makers may find it instructive to explicitly know the covariates that de facto determine the observed structure of public debt. 4

We look at this issue in this article, from an empirical point of view, and take as case study subnational governments in Spain. This latter case provides a relevant case study to analyze the conceptual problem at hand from a global perspective for a number of reasons. First, subnational 5 fiscal imbalances and liquidity risks in Spain provide a recent example of negative spillovers to national public finances (Jenkner and Lu 2014; Romeu 2013; Fernández-Caballero, Pedregal, and Pérez 2012) with potential euro-wide implications (van Hecke 2013). In fact, following a swift increase in their public debt and a drastic change in their maturity structure, most Spanish regional governments had to be partially bailed out by the central government. 6 Second, from the point of view of fiscal federalism, Spain is currently one of the most decentralized countries in the European Union, after three decades of a continued and strong public revenue and expenditure devolution process, a period in which, in addition, a number of supranational and national fiscal rules were put in place in the country. Third, in terms of size, Spain is the sixth subsovereign bond issuer worldwide, after the United States, Germany, Japan, China, and Canada (Canuto and Liu 2010). 7

Our empirical application shows that public financial management decisions over the analyzed sample were not dominated by an attempt to minimize “liquidity risks.” On the contrary, regional governments reacted to increasing financing needs by leaning more toward short-term debt, a fact that may be consistent with theories that predict the willingness of public financial managers to reveal to the markets their fundamental solvency and/or their commitment to fiscal consolidation or just the operation/expectation of central government backstops—that is, central government bailout of regional governments’ debt. Finally, we do not find robust evidence that the quality of the regional debt issuer (measured, in particular, by its credit rating) significantly affects the chosen maturity structure.

The rest of the article is organized as follows: in the second section, we pose the main empirical hypotheses to be tested, against the background of existing theoretical and empirical work. In turn, in the third section, we describe the data used in our study. In particular, we exploit a newly available quarterly data set on the structure of regional government’s debt. 8 Then, in the fourth and fifth sections, we present the econometric approach and the main results of our study, respectively. Finally, in the sixth section, we provide some conclusions and policy messages.

Theoretical Background and Hypotheses to be Tested

Theoretical Background

Some empirical studies have looked at the role of the maturity structure of sovereign debt as an indicator of vulnerability to international financial crises, mainly for emerging market economies (Mehl and Reynaud 2010; Valev 2006, 2007; Lee, Xie, and Yau 2011; Borensztein et al. 2004; Rodrick and Velasco 1999; Bussiére and Mulder 1999; Baldacci, McHugh, and Petrova 2011; Jedrzejowicz and Kozinski 2012). Increased reliance on short-term debt may make a government more vulnerable in a crisis framework, because of the need to roll over increased amounts of debt. As signaled by Borensztein et al. (2004), in a case in which a debt crisis mixes elements of illiquidity and insolvency, the government would be vulnerable to a piece of bad news, whose real impact would be amplified by creditors’ unwillingness to roll over their claims (see also Jeanne 2004). In addition, short-term debt can introduce another level of vulnerability for the fiscal accounts, given that in an increasing interest rate environment interest payments may rise faster if the fraction of short- to long-term debt is higher. In this respect, the structure of public debt may become a channel or source of vulnerability to the real economy and the financial system (Das et al. 2010).

But, which are the factors that do lead public financial managers to a given debt structure? The maturity structure of government debt is to be expected to change in the face of an economic and financial crisis, even in a situation in which market access was not compromised. This might be due to a number of causes. First, because short-term instruments might be the only ones available to keep on covering financing needs. Indeed, investors might be willing to hold short-term public debt even in a situation in which they assign a nonzero probability to default, as they may expect the subcentral government to repay them before the eventual default takes place. Second, investors may expect that the central government bails out the administration under pressure, thus assigning to the default option a low probability. This is in line with the so-called soft budget constraint problem in intergovernmental fiscal relations, which arises when subnational governments’ spending and borrowing decisions are influenced by the expectation of receiving additional resources from the central government (see Vigneault 2007, for a survey on this issue). 9 As a consequence, investors might be willing to get long-term debt, given favorable interest rates and central government implicit guarantees. Third, as Missale, Giavazzi, and Benigno (1997) and Campbell (1995) argue, a government committed to fiscal consolidation and debt stabilization may reduce the cost of debt servicing by issuing short-term debt. This is the case in a framework of asymmetric information in which the government and private investors do not share the same information (or perception) and thus long-term debt instruments pay too high interest rates as a reflection of credibility problems. A government can thus issue short-term debt to signal its resolution to carry out its fiscal consolidation plans. If the implementation of the plans is successfully conducted, and fiscal targets are met, this could be taken by the markets as a signal of quality of the concerned government.

On the issue of quality signaling, asymmetric information, and the maturity structure of debt, there are valuable insights that can also be taken from a broader economic literature that looks at the determination of corporate debt maturities (see Berlin 2006, for a survey). In his traditional liquidity risk hypothesis, Diamond (1991, 1993) argues that short-term debt creates liquidity risk to the borrower because the lender may refuse to roll over the debt if a piece of bad news arrives. Nonetheless, firms with favorable private information would prefer short-term debt to benefit from refinancing on favorable terms when their true credit quality is revealed to the market at the time of refinancing, 10 while firms with unfavorable private information about future default risk will prefer long-term debt and thereby eliminate the uncertainty about the future refinancing risk. Nevertheless, even in the case of having favorable projections, a given highly rated borrower may decide to choose long-term debt if liquidity risks are perceived as high. Additionally, because of information asymmetry and extreme adverse selection cost, the firms with very poor credit rating are not able to borrow long-term debt and may have no option but to choose short-term debt. Therefore, as Diamond predicts, both very-low-risk and very-high-risk firms would use short-term debt. This theoretical prediction of a nonmonotonic relationship between debt maturity and liquidity risk has been tested and validated by a wealth of empirical research (see e.g., Barclay and Smith 1995; Guedes and Opler 1996; Stohs and Mauer 1996; Johnson 1997, 2003; Faulkender and Petersen 2006): high- and low-ranked firms tend to issue short-term debt, while medium-ranked firms tend to rely on long-term debt.

The theoretical framework on the trade-off between the choice of the maturity of debt and liquidity risks can be instrumental to analyze the problem at hand in our article. The theories discussed previously will therefore guide the selection of the variables to be included in the empirical analysis, as discussed in what follows.

Hypotheses to Be Tested

Against the background of the previous discussion, we pose in our study the following headline hypotheses to be tested:

Data and Variables for the Empirical Analysis

The Data

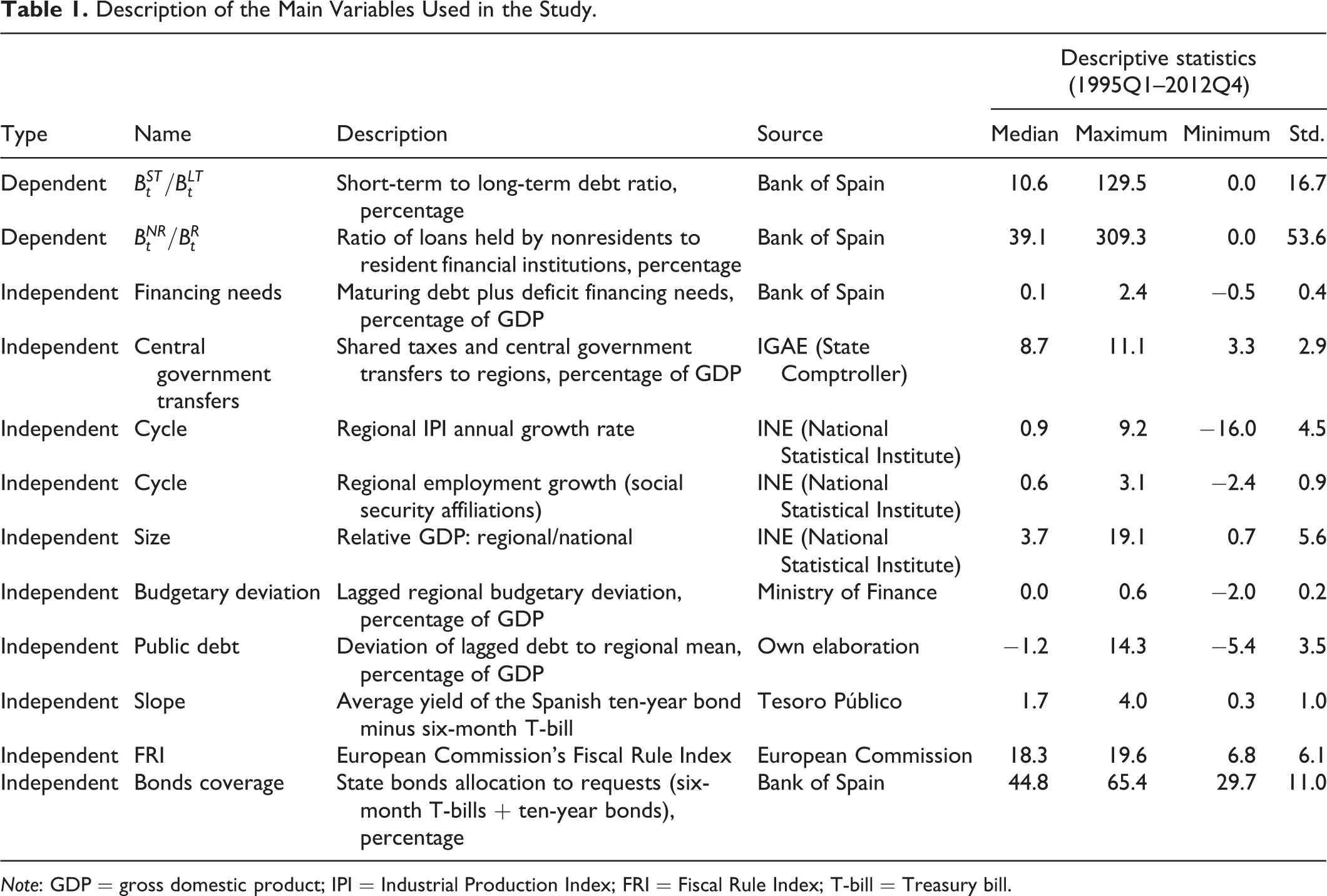

Our panel contains quarterly data for sixteen of the seventeen Spanish regional governments, 11 covering the period 1995Q1–2012Q4. The source of all the public debt data is the Bank of Spain. Table 1 describes the main variables used in our study, while table 2 and figures 1 and 2 provide some stylized facts on the maturity structure of public debt in our data.

Description of the Main Variables Used in the Study.

Note: GDP = gross domestic product; IPI = Industrial Production Index; FRI = Fiscal Rule Index; T-bill = Treasury bill.

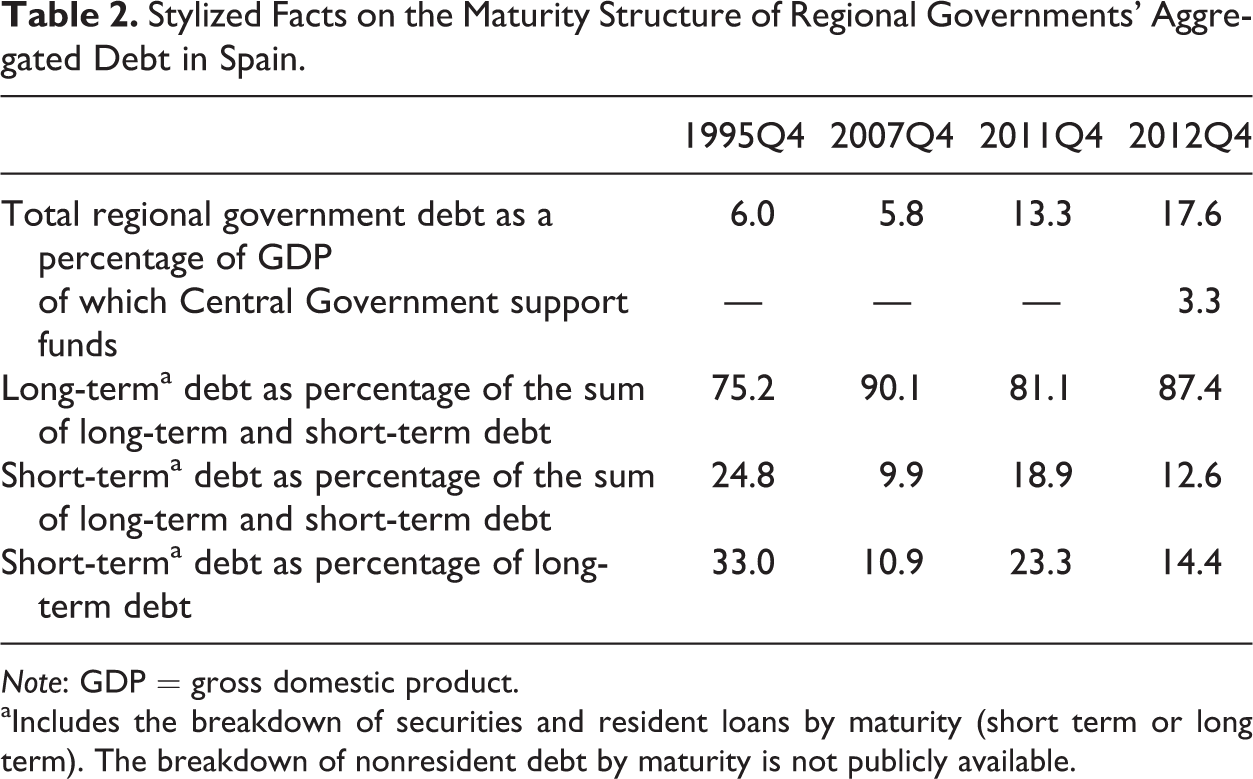

Stylized Facts on the Maturity Structure of Regional Governments’ Aggregated Debt in Spain.

Note: GDP = gross domestic product.

aIncludes the breakdown of securities and resident loans by maturity (short term or long term). The breakdown of nonresident debt by maturity is not publicly available.

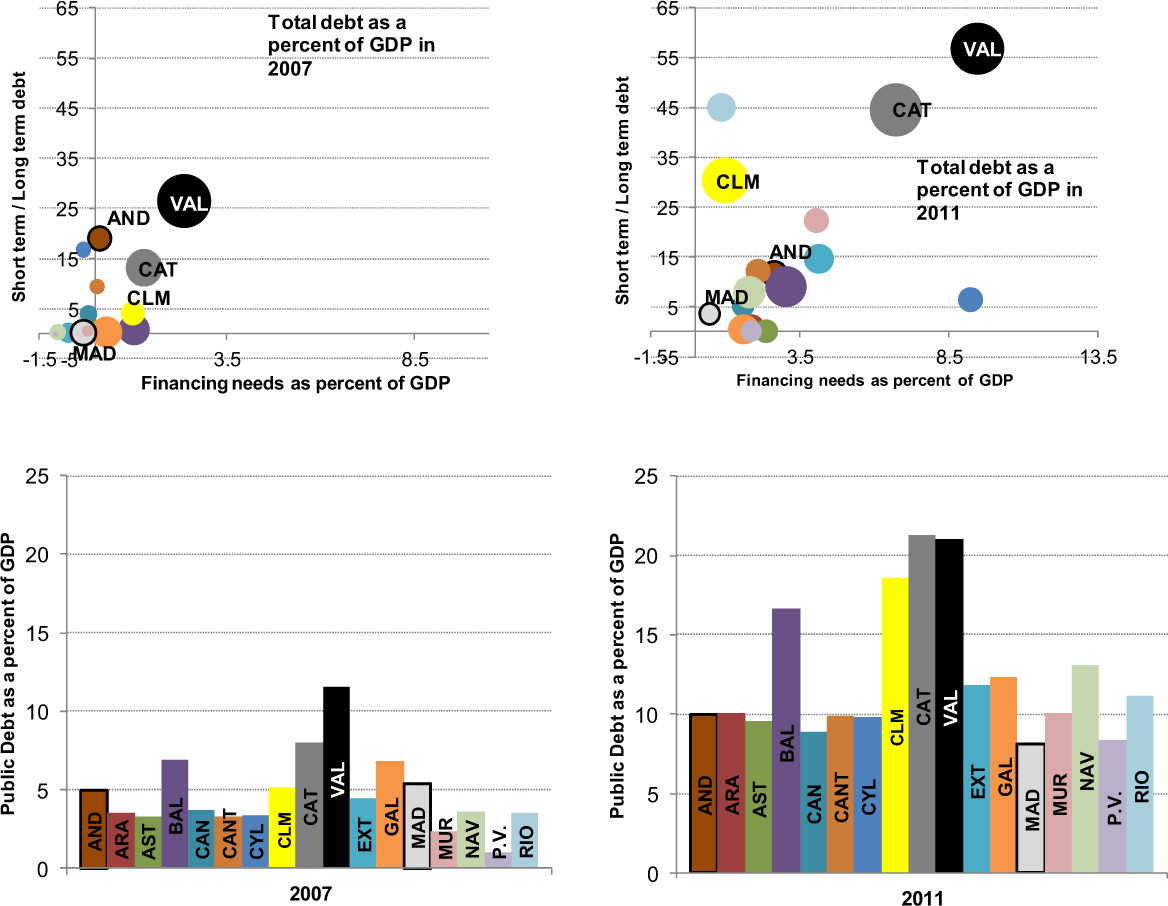

The structure of regional governments’ debt: ratio of short- to long-term debt versus the total amount of financing needs (maturing debt + public deficit financing). Short- (long)-term debt is the sum of short-(long-)term securities and loans by resident financial institutions. The breakdown by maturity of the aggregates of loans by the “rest of the world” and loans by the “central government” is not available. AND, Andalusia; ARA, Aragon; AST, Asturias; BAL, Balearic Islands; CAN, Canary Islands; CANT, Cantabria; CYL, Castille and Leon; CLM, Castille-La Mancha; CAT, Catalonia; VAL, Valencia; EXT, Extremadura; GAL, Galicia; MAD, Madrid; MUR, Murcia; NAV, Navarre; P.V., Basque Country; RIO, La Rioja.

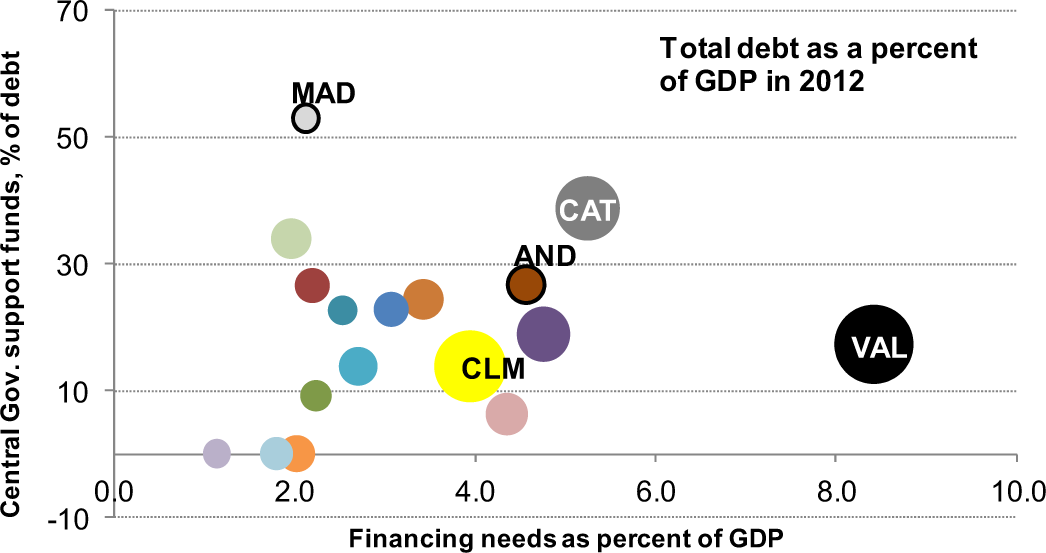

The central government support funds to ease regional governments’ liquidity troubles in 2012 versus the total amount of financing needs (maturing debt + public deficit financing). Fondo de Liquidez Autonómica (FLA, “Regional Liquidity Fund”) and Fondo para la Financiación del Pago a los Proveedores (FFPP, “Fund for the Payment of Providers”). See also notes to figure 1.

The recent crisis period has led to a substantial increase in subnational debt in Spain. In the case of regional governments, their aggregated debt level increased from about 5.8% of gross domestic product (GDP) in 2007Q4 to 13.3% in 2011Q4 and further to 17.6% at the end of 2012 (see table 2). The increase in the level of subnational debt witnessed in Spain in the crisis period occurred hand in hand with a change of its structure. In particular, as regards the maturity structure of regional debt, the ratio of short- to long-term debt 12 stood at 11% in 2007Q4, down from the 33% of the beginning of the sample (1995), but increased substantially to close to 25% by 2011Q4 at the height of the euro area sovereign crisis. The same picture can be drawn from the data by region. The change in the maturity structure of debt over the crisis occurred in parallel to an increase in the amount of maturing debt by year, as shown in figure 1 (upper panels), where we present the ratio of short- to long-term debt versus the amount of financing needs (as a percent of each region’s GDP). In 2012, the fraction of short- to long-term debt got reduced to levels similar to the ones observed at the beginning of the crisis but still stood well above the precrisis values. The increase in long-term debt in 2012, nevertheless, was affected by the fact that the Central Government put in place a program aimed at easing Regional governments’ difficulties in accessing the financial markets. The released funds amounted to some 34 billion euro (3.3% of Spanish GDP) and were accounted for as long-term loans. Excluding the latter factor, the ratio of short- to long-term debt stood at above 11% in 2012Q4. It is worth noting that support funds were aimed particularly at the more troubled regions (see figure 2), typically those with a higher amount of financing needs and/or higher levels of debt.

The Dependent Variable

As regards the dependent variable of interest, we look at the determinants of the relative stock of debt at each maturity. The ratio of interest captures the relative preference over the maturity of debt. If public financial managers were to have in mind a relative target value for each type of debt instrument, this would be, to our mind, the right type of object to study. Debt managers define an issuance policy (flow) with certain values of the stocks in mind, and departures from these target ratios only occur gradually, that is, the selected ratios display strong inertia. This is what we observe in the data. In addition, the theoretical literature would support such a view. 13

In practical terms, we construct the ratio of short- to long-term debt,

Main Explanatory Variables

We proxy liquidity risks by a variable measuring rollover risks, defined as maturing debt (securities) in the period plus regional public deficit financing needs. The source of data on maturing debt is the Bank of Spain. 14

As regards measures of the quality of the debt issuer, in the case of sovereign issuers the fulfillment of budgetary objectives can be considered as a signal of high quality, in particular in times of fiscal consolidation, which can be measured by the size of (ex post) budgetary deviations from the (ex ante) deficit target. In the same fashion, additional measures are the level of debt of the region (as percentage of GDP), the relative debt level compared to peers (deviation of debt from the regional average), the change in debt (i.e., a measure of the public deficit), and any interaction of these variables. 15 In addition, we compute a standard fiscal sustainability indicator, namely European Commission’s S1 indicator. 16

Also in order to measure the influence of the quality of the issuer, in line with the insights from Diamond’s theory outlined previously, we group regions into high-, medium-, and low-rating clusters. In order to build dummy variables for these three categories, we take as the reference the maximum and minimum ratings 17 in the period 2010Q2–2012Q4, the one in which some significant heterogeneity among regions is observed, as in the precrisis period, regions were broadly similarly rated. Regions with ratings in the vicinity of the maximum (maximum minus one standard deviation) are assigned to the high-rating group, while regions close to the minimum are included in the low-rating set. Following this procedure, and trying different measures of distance to the maximum and minimum, we grouped the regions as follows for our baseline empirical analysis: in the medium-rating group Andalucía, Baleares, Canarias, Castilla y León, Extremadura, Galicia, Murcia, and La Rioja; in the high-rating group Aragón, Asturias, Cantabria, Madrid, and the Basque Country; in the low-rating group Comunidad Valenciana, Castilla-la-Mancha, and Cataluña.

A key variable for our analysis is the total amount of Central Government transfers to the regions, as a percentage of nominal GDP. To control for changes in the form of regional financing, we construct an aggregate measure (i.e., for the aggregate of regional governments) that sums shared taxes by regions and the central government—given that taxes started to be devolved at increasing speed as of the end of the 1990s—and genuine Central Government transfers to the regions.

Other Control Variables

GDP growth is typically used as a proxy to measure current cyclical conditions and also future potential economic growth. In economic recessions, budget deficits increase and so public debt does. At the same time, the economic environment may affect the ability of a government to place its debt in the market. When the economy is in a downturn, the market becomes more restrictive and confidence levels decrease, which may entail lenders’ preference for shorter maturities and safer bonds (De Broeck and Guscina 2011; Goudswaard 1990). As a proxy to the business cycle, we take the Industrial Production Index (IPI), given the lack of quarterly GDP data. 18 IPI is a widely used measure in the literature analyzing business cycles and has been shown to be of use in the case of the Spanish regions (see Gadea, Gómez-Loscos, and Montañés 2012). We take the annual growth rate of IPI. 19

In addition to a measure of economic activity, the literature highlights the importance of price inflation (we use consumer price index annual growth data). A positive relationship between inflation and the short- to long-term debt ratio is expected: one can expect that the higher interest rates that increasing prices imply would make shorter maturities more attractive to bond takers (Goudswaard 1990; Mehl and Reynaud 2010). Higher inflation is associated with higher inflation uncertainty, leading to higher-risk premia on long-term nominal debt and thus leading governments to stop issuing long-term debt (Missale and Blanchard 1994). Hoogduin, Öztürk, and Wierts (2010) show that in an inflationary environment, investors might opt for short-term positions. In our application with regional data, though, these considerations might not be too relevant because of the different scope of the analysis (regions vs. countries) and because almost all debt issued in the past decades was debt in euro within a broad monetary union.

Another potentially relevant control is the size of the region (regional GDP as percentage of the national 20 ), a factor that is expected to be positively related to debt maturity, as wealthier/larger regions are presumed to enjoy easier access to markets and a greater ability to issue safer debt. At the same time, nevertheless, if the minimization of liquidity risks is not a major concern, wider market access may grant better and safer access to shorter debt instruments.

Turning to financial controls, a positive relation is expected between debt maturity and the term structure of interest rates (see, e.g., Brick and Ravid 1985), as investors certainly weigh the relative costs of alternative debt instruments. We use a measure of the slope of the yield curve: the average yield in a given quarter of the 10-year Spanish bond minus the equivalent measure of the 6-month Treasury bill (T-bill). On related grounds, market preferences on overall Spanish government debt instruments could influence the structure of regional public debt. Market conditions could be measured by the extent to which governments are able to issue all the debt they intend to. For this purpose, we use the ratio of central government bonds and T-bills allocations to requests (bonds coverage). The way of interpreting this ratio is as follows. As the ratio gets closer to one, the room for implementing debt issuance strategies by the government diminishes. Therefore, we expect this variable to have a positive sign on the short to long regional debt ratio. Another side of the preference equation is the presence of foreign investors in the market for regional debt. Mehl and Reynaud (2010) state that a broader domestic investor base (ratio of gross private savings to GDP) can be expected to make domestic debt composition safer by contributing to support demand for (domestic currency, unindexed) long-dated debt instruments. To avoid endogeneity problems, we include as a regressor the residual of a regression of the ratio of nonresident to resident loan providers on all the explanatory variables included in each equation.

The literature has proved that institutional and political factors need to be taken into account when fiscal performance is analyzed. Additionally, some articles study the influence of the quality of institutions on public debt management: Guscina (2008) states that better institutions decrease the share of short-term debt, as weak institutions can compromise the government’s ability to implement effective fiscal policy, to constrain policy commitments, to manage liabilities, and to control and limit fiscal risk. Nevertheless, the existence of fiscal and no bailout rules may exert some influence on moving market preference to shorter bonds. On related grounds, see also Borensztein et al. (2004) and Valev (2006). Thus, we incorporate in our analysis two control variables to measure institutional and political factors. On one hand, we consider election dates, as the well-documented government spending-induced patterns can influence public debt patterns and also debt issuance strategies. 21 On the other hand, we use the time-varying fiscal rule index constructed by the European Commission for each EU Member State (FRI). Each individual fiscal rule is weighted by the coverage of general government finances of the respective rule (i.e., public expenditure of the government subsector/subsectors concerned by the rule over total general government expenditure). 22 The assigned weights are mainly determined by the fiscal strength of the rule and its coverage.

A final set of controls has to do with the territorial organization of a country. The type of spending responsibilities assumed by the regions and the available revenue instruments for their funding are factors that influence fiscal outcomes and then public debt patterns. Following this idea, an indicator of fiscal co-responsibility has been introduced in our analysis. The index is constructed as the ratio of taxes on which regions have normative power 23 to total revenues. 24 We expect this variable to have a negative impact on the short- to long-term debt ratio, as increasing fiscal responsibility is thought to have led to reductions in systematic debt issuance and possibly disfavor short-term bonds.

Empirical Strategy

The econometric model used can be specified in general terms as

where the debt maturity ratio for each regional government i at time t,

For these reasons, the estimation is carried out by the generalized method of moments (GMM). Particularly, we perform GMM estimations instead of difference GMM since lagged levels could be poor instruments for first differences if the variables are close to a random walk. In practice, we implement the Stata routine xtabond2, which, along with the estimation of the model equation (1) in first differences (transformed equation), adds to the system the original equation in levels (untransformed equation), so additional instruments can be brought to increase efficiency. In a first step, differenced variables in (transformed) equation (1) are instrumented with their own available lagged levels. Then, level variables in (untransformed) equation (1) are instrumented with suitable lags of their own first differences (Arellano and Bover 1995; Roodman 2006).

In our framework, most of the variables included in the analysis are potentially endogenous. In fact, in our empirical models all the potential covariates discussed in the previous section are considered to be part of Ω, with the exception of the variables measuring the institutional strength of fiscal rules and electoral dates. In addition, as briefly discussed in the introductory and stylized facts sections, our dependent variables are quite persistent. Indeed, public debt managers tend to have in mind (either explicitly or implicitly) a relative target value for each type of debt instrument, a situation that to a large extent determines the issuance policy (flow), which creates a strong inertia in the observed equilibrium time series. Given the large amount of variables to be instrumented, we paid special attention to the number of lags used as instruments. We tried several specifications with one, two, and more lags. On one hand, the quarterly nature of our data advises the inclusion of more than one lag, also bearing in mind that more distant lags would qualify as better instruments. Nevertheless, on the other hand, the quality of the Hansen test of the instruments’ joint validity deteriorates significantly with more than two lags, even though the quantitative results do not vary significantly, as shown in the next section. The models with one and two lags are broadly appropriate (as it will be shown in the empirical results section) and do not differ significantly among them in qualitative and quantitative terms. Given the quarterly frequency of our data set, we show in the tables the results using two lags. 25

Finally, even though it is known that in a framework like ours, ordinary least squares (OLS) estimators may suffer from the “dynamic panel bias” (i.e., the positive correlation between a regressor and the error violates an assumption necessary for the consistency of the OLS estimator), we also provide them in all the tables of results shown in the next section. The reason is that one has to acknowledge that system GMM estimators in finite samples may be subject to instrument proliferation, and as such a simpler and more widely understood estimation alternative may be helpful for the informed reader. 26

Main Results

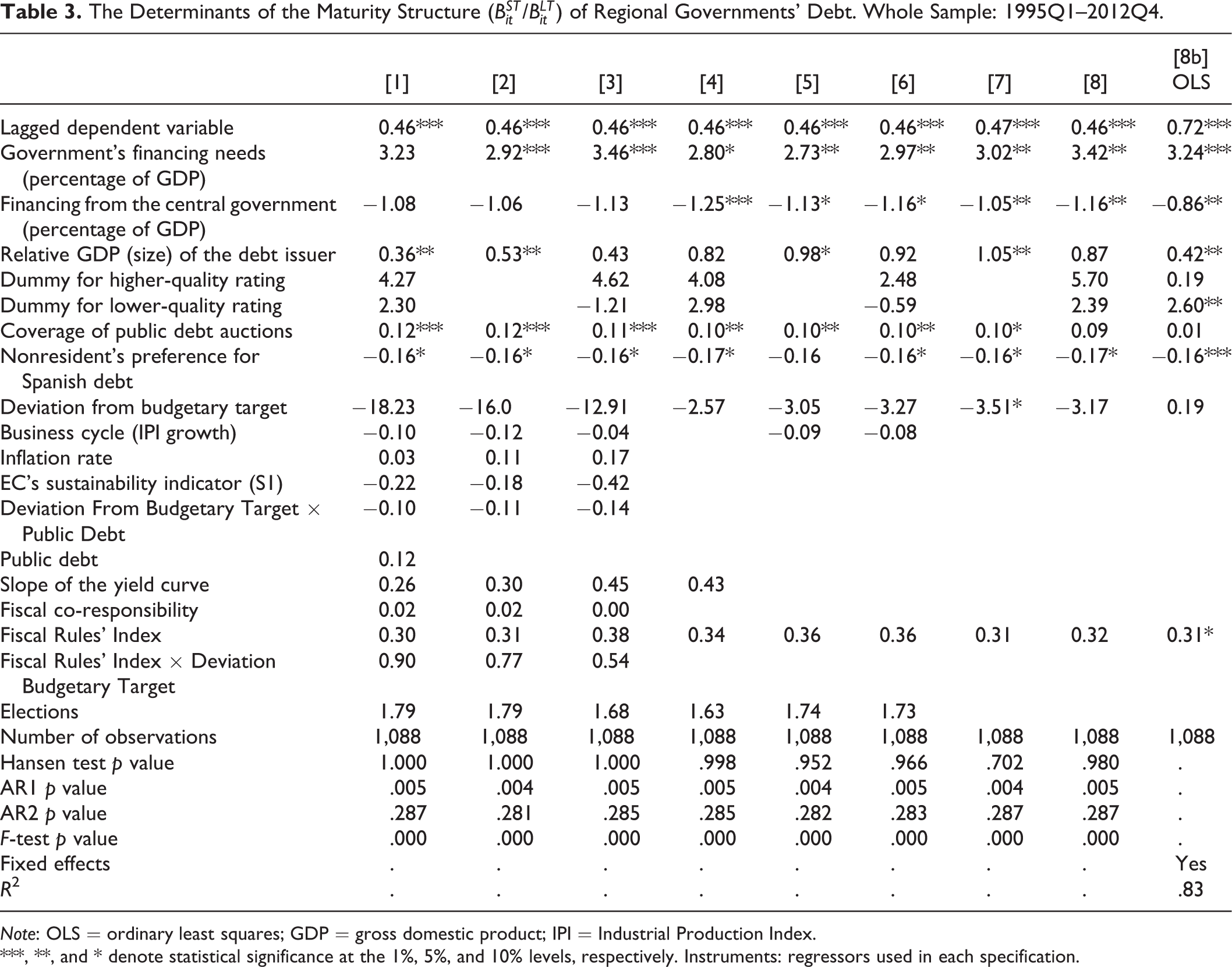

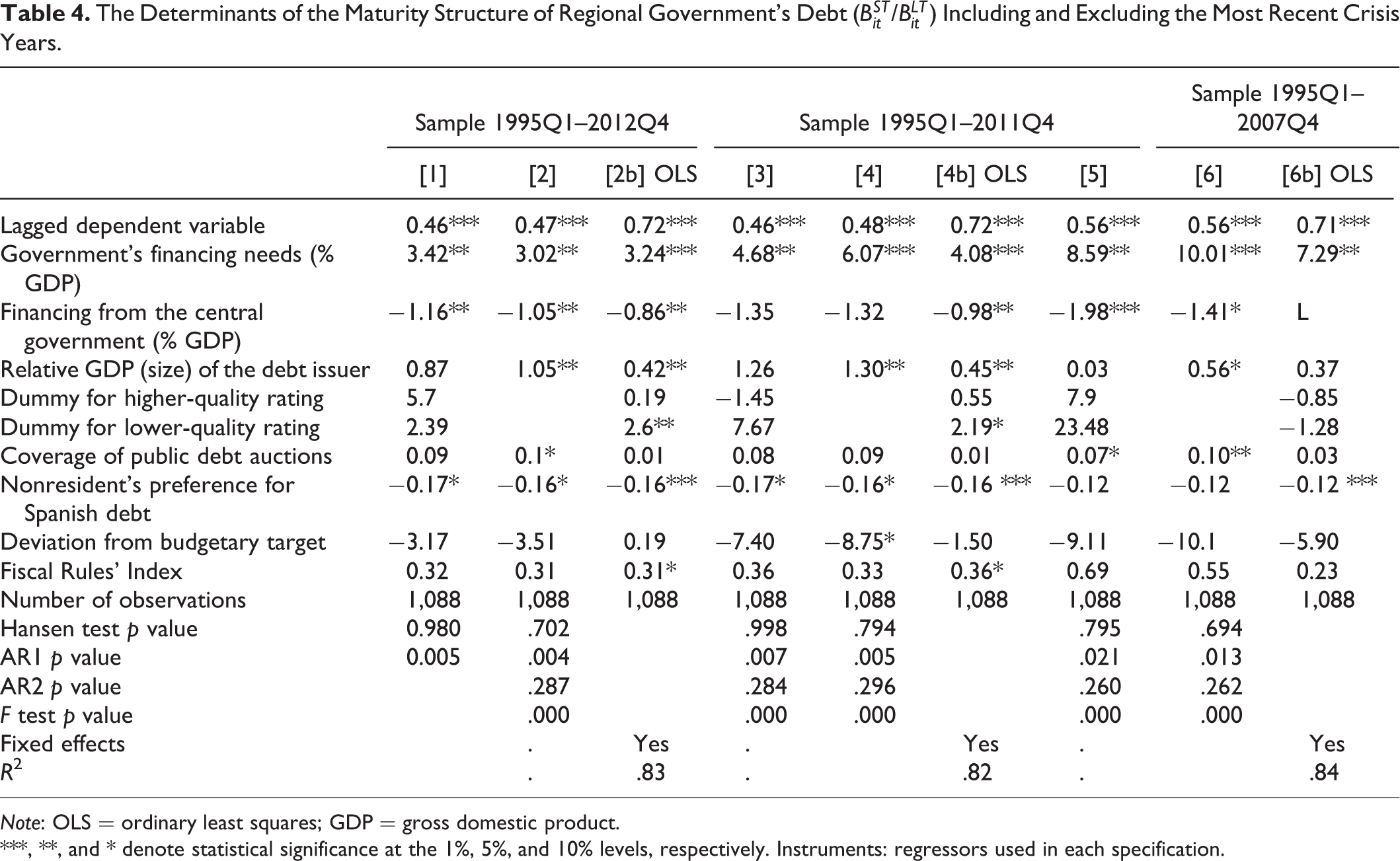

The main empirical results of the article are summarized in tables 3 and 4, where we present a subset of the results, which involved a larger number of empirical specifications that combined all the control variables described previously. In the tables, we show results for the full sample (1995Q1–2012Q4), for the precrisis sample (1995Q1–2007Q4), and for the sample excluding 2012 to control potential introduced by the launching of the central government liquidity support funds to regions discussed previously. 27

The Determinants of the Maturity Structure (

Note: OLS = ordinary least squares; GDP = gross domestic product; IPI = Industrial Production Index.

***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. Instruments: regressors used in each specification.

The Determinants of the Maturity Structure of Regional Government’s Debt (

Note: OLS = ordinary least squares; GDP = gross domestic product.

***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. Instruments: regressors used in each specification.

In table 3, the first three columns incorporate all the control variables described previously. A significant group of control variables were not found to present statistical relevance for the determination of the ratio of short- to long-term debt, 28 while at the same time they created a problem of proliferation of instruments, as reflected by the fact that we cannot reject the null hypothesis of overidentification (p value of the Hansen J statistic). Thus, in columns [3] to [8] of table 3 and in table 4 we resort to empirical specifications that focus on a more reduced set of explanatory variables. The following results are worth highlighting. 29

First, liquidity risks, measured by the financing needs of regional governments, appear as a quite robust determinant of the maturity structure of regional governments’ debt in all the specifications considered. An increase in the amount of financing needs (in the form of maturing debt and current deficit financing) leads to a maturity structure leaning more toward short-term debt, that is, the amount of short-term debt increases in relative terms with respect to the amount of long-term debt. Thus, according to these results, the liquidity risks associated with potential difficulties to roll over maturing debt (and financing new deficits) do not lead directly to a lengthening of the maturity of debt. This result holds for the whole sample and also for the precrisis sample, that is, when the post-2007 period is excluded from the estimation and also for the inclusion of different lags of the variable (not shown in the tables for the sake of brevity).

Two related explanations for this result can be drawn from the literature discussed previously. On one hand, from the point of view of lenders, under the assumption that they do not expect that a default might occur in the very short run, they are willing to lend short-term debt to the regional governments. On the other hand, from the point of view of the borrower, if governments try to reveal to the markets their fundamental solvency or their commitment to fiscal consolidation, they would tend to issue more short-term debt in relative terms, in an attempt to obtain in the near term more favorable long-term refinancing conditions when their true credit type is assessed by investors.

Second, the variable measuring the amount of resources transferred to the regions by the central government is also a robust regressor across empirical specifications and samples. The negative sign denotes that investors anticipate that the central government would increase transferred resources (be it genuine transfers or improvements in the financing arrangements) in case a given region faces financial problems, and thus they will be willing to finance longer-term debt to that particular region at favorable conditions for them. This is in line with the prescription of the “soft budget constraint” theory. The implicit bailout that increased central government transfers might imply can be seen to the light of investors as a safeguard against the potential losses of a given regional government’s default.

Third, as regards the importance of the quality of a region in the determination of its maturity structure, we do not find conclusive results, which may indicate that most Spanish regions are similar to the buyers of regional debt, that is, in general, they do not strongly discriminate among them. On one hand, stricter adherence to the previous year’s budgetary target seems to be associated with easier access to short-term debt in relative terms. This result would support the view outlined previously that quality signals would lead to issuing more short-term debt in relative terms, in order to obtain more favorable refinancing conditions in the near future. Nevertheless, even presenting the expected negative sign, the parameters are not estimated with enough precision and thus the variable does not present statistical significance. On the other hand, we do not find any statistically significant result for the dummies grouping the regions in high-, medium-, and low-quality ratings. Even though the sign of the coefficient associated with high-quality ratings is estimated to be consistently positive across models, which may indicate a major propensity to borrow short-term debt versus long-term debt compared to medium-quality regions, as dictated by Diamond’s history for corporations’ debt, we do not find statistical significance in any of the considered empirical specifications. Among controls that proxy “quality,” we find consistently significant parameter values only for the variable measuring size of the region (relative GDP). The found positive sign is consistent with the standard result in the empirical literature that the size of a debt issuer is significant for market access, possibly because it implies a deeper debt market.

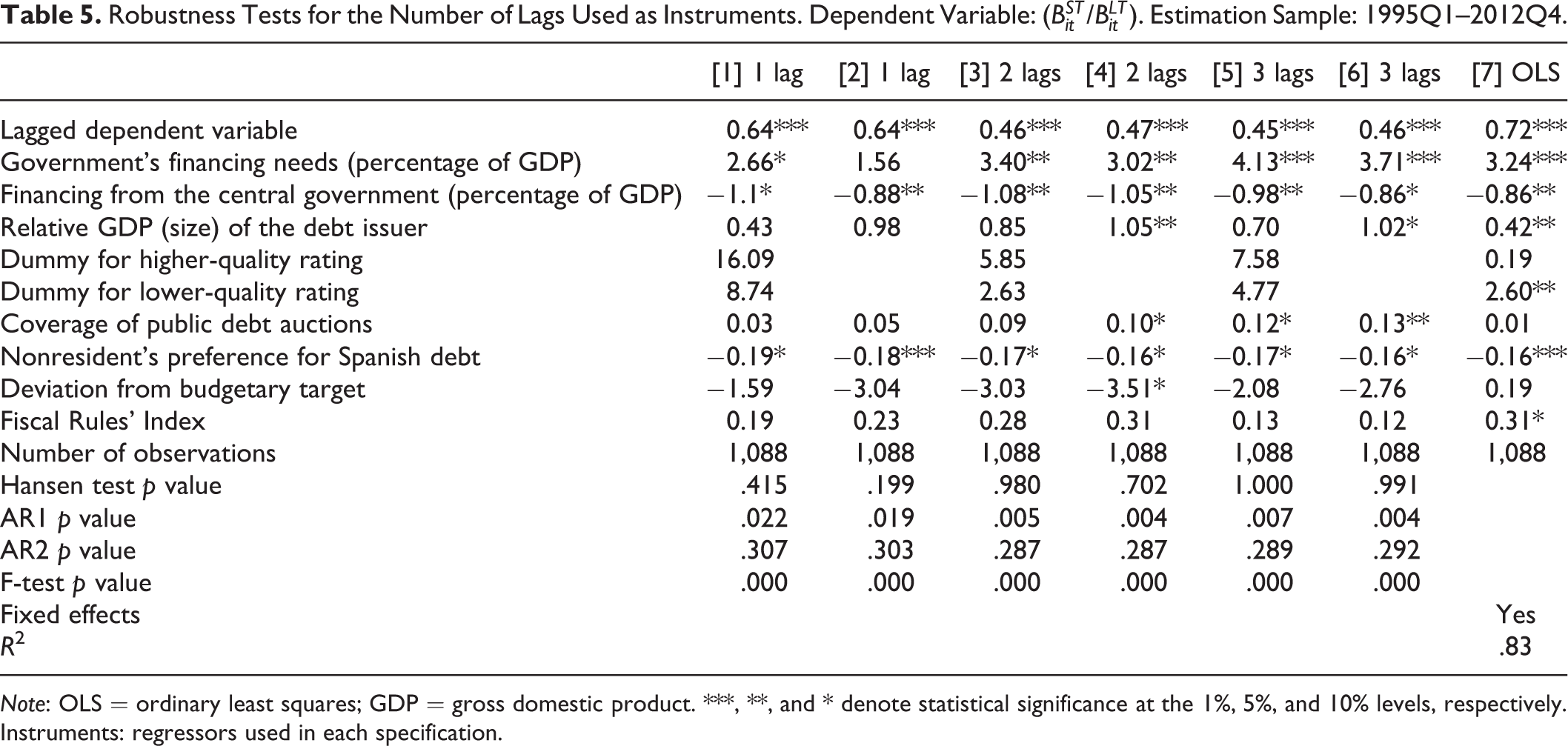

Finally, as a matter of additional robustness check for the GMM estimator, we show in table 5 the results obtained for the main empirical specifications for different number of lags used as instruments (one, two, and three lags). The figures presented show that our main results are quite robust to this critical GMM issue.

Robustness Tests for the Number of Lags Used as Instruments. Dependent Variable: (

Note: OLS = ordinary least squares; GDP = gross domestic product. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. Instruments: regressors used in each specification.

Conclusions

We analyze the determinants of the maturity structure of public debt using as a case study subnational governments in Spain, focusing on the ratios of short- to long-term debt. We incorporate a number of variables that proxy liquidity and credit risks and assess their relative merit.

According to our results, regional governments in Spain react to increasing financing needs by leaning more toward short-term debt, instead of resorting to longer-term debt to seek the minimization of liquidity risks, under normal market access. One may read this evidence in light of one strand of the literature that states that fundamentally sound governments may be willing to issue in relative terms more short-term debt, in order to obtain refinancing in the near term on favorable terms when their true credit type is assessed by investors. At the same time, we find that increased central government transfers raise the tendency of markets to hold long-term instruments, which may reflect that investors perceive that the central government would support regions in distress and thus expect that regional debt be bailed out/guaranteed by the center. In addition, we do not find robust evidence that the quality of the region issuing debt is a fundamental determinant of the maturity structure of its debt, that is, irrespective of the ability it may have to access the market, we cannot ascertain if higher-quality regions display different preferences regarding their short- to long-term debt ratio than the rest. Finally, other variables included in our analysis played a lesser role in explaining the maturity structure. In particular, institutional and political factors are not found to be of relevance in a robust manner across empirical specifications. This is also the case for the influence of the business cycle.

Footnotes

Acknowledgments

We are grateful to Prof. James Alm (Editor of PFR), two anonymous referees, participants at the National Bank of Romania-ESCB WGPF Workshop (Bucharest, June 2013), the EcoMod2013 Conference (Prague, July 2013), and the seminar at the Bank of Spain (July 2013), in particular Claudia Braz, Andre Kolodziejak, Christopher F. Baum, Amela Hubic, Angi Roesch, Harald Schmidbauer, and Ernesto Villanueva for their useful comments. We also thank Jorge Abad, Luis Gordo, José A. Jiménez, Antonio Casado, and José Pina for their help with the data.

Authors’ Note

The views expressed in this article are the authors’ and do not necessarily reflect those of the Bank of Spain or the Eurosystem.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.