Abstract

This article provides an empirical analysis of the incentive effects of equalization grants on business and personal income tax rates using panel data from Canadian provinces. We exploit the discontinuity in the equalization grant allocation formula to identify the exogenous income and incentive effects of equalization grants on tax policy. Our empirical results indicate that equalization grants provide provincial governments an incentive to raise their business and personal income tax rates. The results also suggest that if the equalization program in its current form was abandoned, then business and personal income tax rates would be lower in the grant receiving provinces.

Equalization grant systems have been the cornerstones of intergovernmental fiscal relationships in federations such as Australia, Canada, Germany, Switzerland, and others. In the literature, fiscal equity and efficiency have been put forward as major justifications for the presence of such grants (see, for instance, Boadway and Flatters 1982; Boothe and Hermanutz 1999; Kőthenbűrger 2002; Boadway 2004).

The equalization system has long been considered a vital underpinning of the Canadian federation: a means to create some purported fairness among the provinces. As enshrined in Section 36(2) of the Constitution, the equalization system is intended to enable provincial governments to provide comparable levels of public services using comparable levels of taxation. The equalization system is formula-driven and it was designed to address provincial fiscal disparities by compensating recipient provinces when their per capita fiscal capacity is below the standard per capita fiscal capacity. The grants so obtained are unconditional, and provincial governments are free to use the funds to finance any part of their public services. However, many commentators and analysts voice their concern that the elements of the grant allocation formula can be influenced by provincial governments resulting in a side effect to the noble objective of the equalization system. One of the most commonly cited side effects of the equalization system is that it provides recipient provinces the incentive to engage in potentially inefficient tax policy choices. Albouy (2012), for instance, shows that the equalization system is neither efficient nor equitable. Consequently, in public debates surrounding the equalization program, evidence-based assessment of the incentive effects of the program on recipient governments’ tax policy is of paramount importance.

Theoretical analyses of Smart (1998) and Dahlby (2002) show that in the representative tax system-based equalization programs such as the one used in Canada, equalization grant influences recipient provinces’ tax policy incentives. The reason is that when a recipient province raises its tax rate, it gets higher equalization entitlements by increasing the national standard tax rate. Further, the province can receive higher equalization grants due to a reduction in the province’s tax base associated with a rise in its tax rate. Thus, these tax rate and tax base effects of equalization grants cause a downward bias of the marginal cost of public funds (MCF; as it is perceived by provincial governments)—the loss incurred by a society when a government raises an additional dollar of tax revenue—and as a result the grant system gives recipient provinces an incentive to raise their tax rates.

An earlier empirical analysis of the Canadian equalization system by Courchene and Beavis (1973) suggests that equalization grant recipient provinces could manipulate the allocation formula to increase their equalization entitlements. Esteller-Moré and Solé-Ollé (2002) also find that equalization grant has a significant positive effect on Canadian provincial personal income tax rate. Snoddon (2003) provides indirect evidence on the effects of Canadian equalization grants on tax policy. Her empirical results show that the change in the number of standard provinces in the Canadian equalization allocation formula has a positive effect on the own-source revenue growth of those equalization grant-receiving provinces excluded from the new standard. If the equalization grant system compensates provinces for any reduction in their tax bases, it may also influence their responses to tax policy changes by other provinces. Smart (2007) investigates this issue and explores the effects of equalization grants on tax competition among Canadian provinces. His results indicate that equalization grant recipient provinces respond more positively, in terms of raising their average effective tax rates, to increases in other provinces’ average effective tax rates than nonreceiving provinces. This suggests that indeed the equalization system influences tax policy incentives.

Similar tax policy incentive effects of equalization grants were also found for other federations. Baretti, Huber, and Litchtblau (2002) find that equalization grants have a negative effect on German states’ tax revenue-to-gross domestic product (GDP) ratio, and they interpret this as a negative effect of equalization grants on tax enforcement efforts. Dahlby and Warren (2003), on the other hand, find somewhat weak evidence of the effect of equalization grants on tax policy for Australian states.

Equalization grants enable recipient subnational governments to finance their spending and hence have income effects as well. While previous studies attempt to explore the incentive effects associated with equalization grants, they ignore these income effects. Buettner (2006) introduces a novel idea to distinguish the income and tax incentive effects associated with an equalization system. He investigates the effects of equalization transfers on business tax rate for municipalities in a German state by exploiting the discontinuity in the equalization grant formula. He finds that while the income effects of equalization grants are associated with lower business tax rates, the grants also provide the local governments an incentive to raise their tax rates.

While previous theoretical studies assess the effects of the Canadian equalization program, little is known about the importance and strength of the various aspects of the incentive effects of the program on recipient provinces’ tax policy. The main objective of this article is to provide empirical evidence on the incentive effects of equalization grants on tax policy using panel data from Canadian provinces over the period 1981 to 2008. We focus on business and personal income tax rates as these taxes account for a significant part of provincial tax revenue and have been the topic of discussion in previous studies. In addition, these revenue categories have been included in the equalization grant allocation formula throughout the period under consideration. In our empirical analysis, following Buettner (2006), we differentiate the income and incentive effects of equalization grants. The incentive effects associated with the equalization system arise due to the equalization rate and base affects that cause a downward bias of the MCF. In this article, we investigate this issue by estimating both the equalization rate and base effects, and controlling for possible income effects associated with equalization grants. To the best of our knowledge, this article is the first to address this issue for Canada.

In the Canadian equalization system, a province is entitled to receive equalization grants only if its per capita fiscal capacity is below the average per capita fiscal capacity of standard provinces for the specific tax category. Provinces with per capita fiscal capacity above the standard, on the other hand, are not entitled to receive equalization grants. Thus, there is a discontinuity in the grant allocation at the point where the per capita fiscal capacity of a province is equal to the standard provinces’ fiscal capacity. As in Angrist and Lavy (1999), Buettner (2006), and Dahlberg, Mork, Rattso and Agren (2008), we rely on this discontinuity to identify the exogenous incentive effects of grants on tax rates.

Our results suggest that equalization grants provide provincial governments an incentive to raise their business and personal income tax rates. We also find that the incentive effect works mainly through the equalization base effect. That is, recipient provinces have the incentive to shrink their tax bases by raising tax rates in order to increase their equalization entitlements. These incentive effects of equalization grants clearly influence provincial tax policy. The equalization program reduces the provinces’ perceived MCF since the program compensates provinces with higher transfers when their tax bases decrease as a result of higher tax rates. Our results suggest that if the equalization program in its current form was abandoned then business and personal income tax rates would be lower in the grant receiving provinces.

The remainder of the article is organized as follows. In the second section, we provide background information on the Canadian equalization system and describe our identification strategy. We discuss the empirical specification and the data in the third section. In the fourth section, we present and discuss the empirical results. The fifth section concludes.

Background and Identification Strategy

Background

The equalization grant system has been one of the main tenets of fiscal federalism in Canada. The main objective of the equalization system is to enable provincial governments to provide comparable level of public services without resorting to excessive taxation of their residents. In the equalization grant entitlement allocation procedure, the federal government first determines the fiscal capacity—the provincial governments’ ability to raise revenue using a national standard tax rate—of the ten provinces. Then the fiscal capacity of each province so computed is compared with the fiscal capacity of the so-called standard provinces. 1 If a province’s per capita fiscal capacity is below the per capita fiscal capacity of standard provinces, then the province is entitled to receive per capita equalization grants which are equal to the per capita deficiency in fiscal capacity. Provincial governments with per capita fiscal capacity higher than that of standard provinces, on the other hand, are not entitled to receive equalization grants. The federal government finances the equalization grants from its general revenues.

In order to relate the equalization grant entitlement allocation to our investigative approach, we discuss below how the Canadian equalization grant system works in a little bit more details. Suppose Bpj

denotes the per capita tax base of province p for the tax category j,

where

That is, if the sum of equalization grant entitlements for all tax revenue categories is positive, the province will be provided per capita equalization grant which is equal to the sum. However, if the sum of equalization grants is negative or zero, the province will not be eligible to receive equalization grants. Such provinces will not be equalized down either. Accordingly, during the period under consideration, the provinces of Alberta and Ontario have not received any equalization grants. On per capita basis, Prince Edward Island received the highest equalization grants over the period under consideration. Further, during the period under investigation, real per capita grants increased for all receiving provinces except Newfoundland, which received reduced grants because of a significant increase in its offshore oil revenues. 2

Identification Strategy

In this section, we discuss how equalization grants can influence tax policy incentives of recipient provinces and describe our empirical identification strategy. A close examination of the equalization grant allocation formula of equation (1) reveals that the receiving provinces’ tax rate choices can influence the national standard tax rate (

where ypj

denotes what Buettner (2006) termed as “virtual grants” and it is the amount of equalization grant that province p would receive if its tax base j were actually zero. More specifically, the virtual equalization grant for any tax category is calculated as

Unlike in the case of Germany that Buettner (2006) examined, in the Canadian equalization grant system, ϑpj is not a fixed parameter.

4

It depends on the national standard tax rate and the relative fiscal capacity of the province both of which can be influenced by the tax policy choice of the recipient province. We obtain ϑ

pj

using the expression

Suppose the per capita total revenue for provincial government p for tax category j is given as:

where Rpj is per capita revenue, τ pj is the province’s tax rate for tax category j, Bpj is per capita tax base for the tax category j, and gpj is per capita equalization entitlement of province p for tax category j. In order to discuss the incentive effects of equalization grants on tax policy, we use the MCF framework. The MCF shows the cost to society when the government raises one dollar of tax revenue and, in the absence of grants, it can be calculated as:

where Bpj is the tax base and τ pj is the tax rate. In the presence of federal equalization grants to the provinces, using equation (3) the MCF for the recipient provincial government is given as:

Equation (6) shows that the presence of equalization grant affects the MCF of the province and hence influences the tax policy incentives of the recipient provinces. Note that if ϑ pj was based on a fixed parameter as is the case in other federations such as Germany, equation (6) would be reduced to the MCF expression used in Buettner (2006). However, in the Canadian federation, the third expression in the denominator of equation (6) is nonzero and the effect of ϑ pj on the MCF is not straightforward. To shed some light on the incentive effects of equalization grants on provincial tax policy, we further simplify the above equation. Using equation (6) and the definitions of the various variables, following Dahlby (2002) and Dahlby and Warren (2003), we can rewrite the MCF equation as:

where

For any given revenue category, when a provincial government raises its tax rate, it raises the national standard average tax rate used in the equalization allocation formula. This also increases the recipient government’s equalization grant entitlement. Dahlby and Warren (2003) termed this as the equalization rate effect. This equalization rate effect is denoted by Θ pj in equation (7). For provinces that are relatively small and have negligible effects on the national standard tax rate, Θ pj reduces to zero. For this reason, previous studies such as Smart (1998) ignore this effect from their analysis. Note also that the effect of Θ pj on the MCF depends on whether the per capita tax base of the province is higher or lower than the standard per capita tax base for the specific revenue category. If the province’s per capita tax base is less than the per capita tax base of the province (as is normally the case for equalization grant recipients), Θ pj will be positive resulting in a downward bias of the recipient government’s MCF. This provides the recipient government an incentive to raise its tax rate. Thus, equation (7) shows that equalization grants provide recipient provinces an incentive to raise their tax rates as they underestimate the true costs of higher tax rates to society.

Empirical Specification and Data

Empirical Specification

Based on the theoretical framework discussed above, our empirical analysis of the effects of equalization grants on tax rates can be specified as:

where τ pj is the tax rate, ypj is the virtual equalization grant associated with the tax category, ψ pj is the equalization base effect, Θ pj is the equalization rate effect, f(Ω pj ) denotes a nonlinear function of relative fiscal capacity, Ω pj defined as the ratio of the per capita tax base of a province to the average per capita tax base of standard provinces, and Zp denotes a vector of other variables that can influence the tax rate choices of a province. We are interested in assessing the incentive effects of equalization grants on personal and business income tax rates. These two revenue categories together account a significant source of revenue for the provincial governments and have been the focus of previous studies as well. 7

The empirical specification can formally be expressed as follows:

where τ pj,t is the average effective tax rate for tax category j in province p in year t, ψ pj,t is the equalization base effect, and Θ pj ,t is the equalization rate effect. Previous studies such as Boadway and Hayashi (2001), Esteller-Moré and Solé-Ollé (2002), and Smart (2007) also use average effective tax rates as dependent variables. D is an indicator variable that is equal to one if the province is a nonreceiving province in the year or zero otherwise. We control for this indicator variable, as our focus is on the incentive effects of grants on the recipient provinces’ tax policy. Zp contains all other relevant control variables.

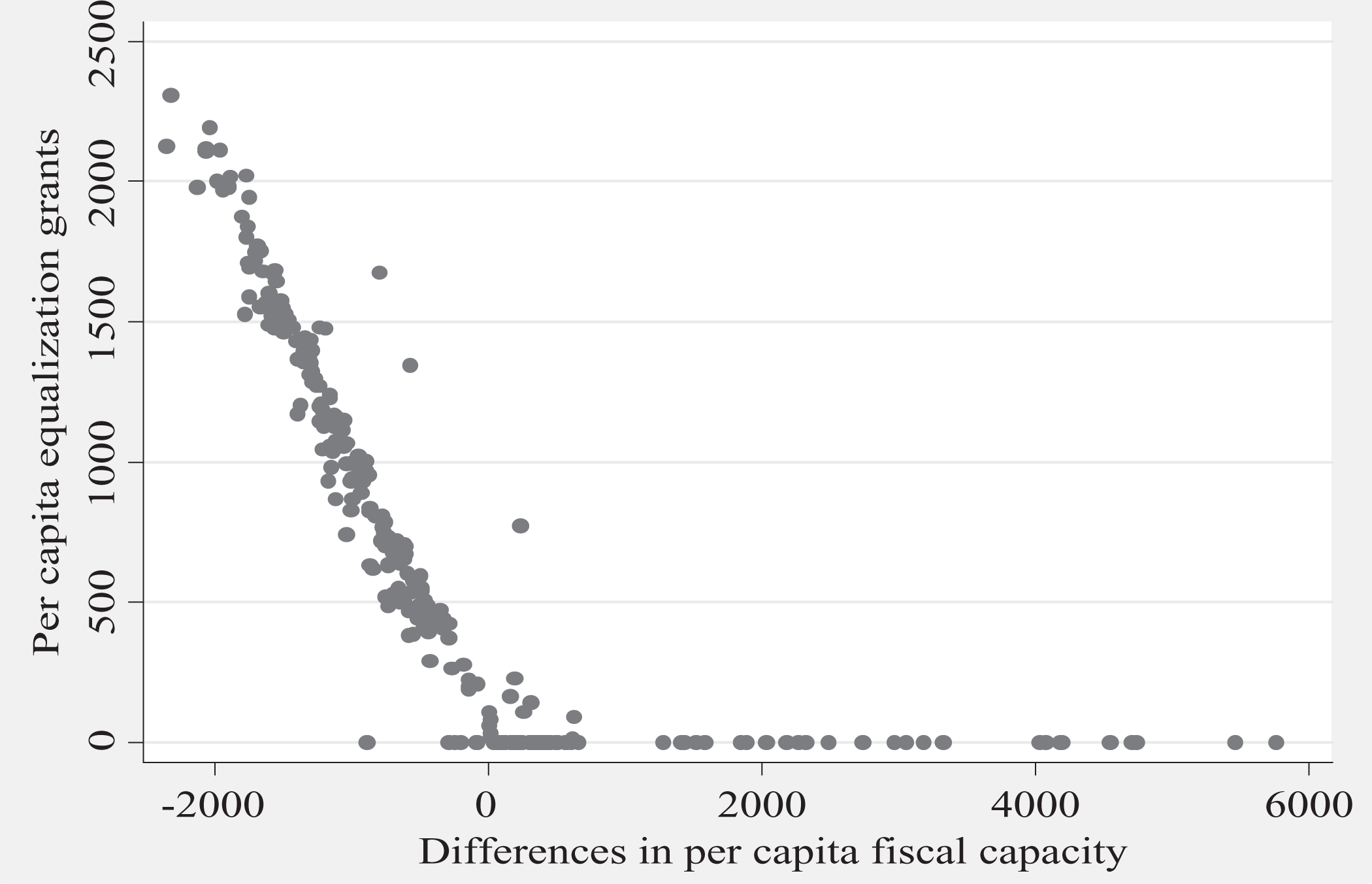

A province is entitled to receive equalization grants only if its per capita fiscal capacity is below the average per capita fiscal capacity of standard provinces for the specific tax category. Provinces with per capita fiscal capacity above the standard, on the other hand, are not entitled to receive equalization grants. Thus, there is a discontinuity in the grant allocation at the point where the per capita fiscal capacity of a province is equal to the standard provinces’ fiscal capacity. Figure 1 shows the presence of a discontinuity in the equalization system. We rely on this discontinuity to identify the effects of grants on tax rates. Provinces are entitled to receive equalization grants only when their per capita fiscal capacity is less than that of the standard provinces, that is, when the difference in fiscal capacity is negative. The figure clearly shows this.

Equalization grants and differences in fiscal capacity, 1981 to 2008.

As we discussed before, both the equalization rate and equalization base effects depend on the relative fiscal capacity of the province. Since the relative fiscal capacity of the province—the ratio of the per capita tax base of a province to the per capita tax base of standard provinces—can have a direct effect on tax rate choices, we need to control for this element of the equalization grant formula to identify the exogenous effects of our key variables of interest on tax policy. In order to achieve this, as in Buettner (2006), we need to control for a smooth nonlinear function of relative fiscal capacity related to the tax category. In equation (9), f(Ω) denotes this nonlinear function of relative fiscal capacity Ω. In the empirical analysis, we use various smooth polynomial and spline forms of relative fiscal capacity as is common in the literature.

Our empirical analysis is based on panel data from all the ten provinces. However, during the period under consideration, Alberta and Ontario did not receive any equalization grants. British Columbia, Saskatchewan, and Newfoundland also did not receive equalization grants in some years. In order to capture the incentive effects of equalization grants only for receiving provinces, we include, D, a dummy variable that is equal to one if the province does not receive equalization grants. Then we control for the interaction terms between this dummy variable and the equalization rate and base effects. Thus, in the empirical specification of equation (9), our key coefficients of interest are α2 and α3. These coefficients capture the equalization rate and base effects for recipient provinces, respectively. The theoretical model suggests that, for grant recipients, the equalization rate effect (Θ pt ) has a positive effect on tax rates, provided that the province’s fiscal capacity is lower than that of the standard provinces. Thus, we expect that α2 > 0. A positive and statistically significant coefficient estimate for α2 can be considered as evidence for the presence of the equalization rate effect. As we have indicated previously, this effect is important for large provinces such as Quebec but less so for smaller Atlantic Provinces. So in the empirical analysis, the equalization rate effect may be strongly influenced by Quebec. 8 Based on equation (7), we also expect that α3 > 0. That is, the equalization grant provides an incentive for recipient province to raise its tax rate through the equalization base effect (ψ pt ).

Regarding other control variables, as in Smart (2007), we include the weighted average (weighted by population) effective tax rate of other provinces as a control variable. This variable enters as a one period lagged since tax competition literature suggests that normally governments need some time to adjust their tax policies in response to policy changes of their neighbors. We also control for various economic, demographic, and political variables that capture the expenditure needs of the government. More specifically, as in Smart (2007), we control for the share of the population who are sixty-five years of age and above (old), the share of the population who are below twenty years of age (young), and the unemployment rate. 9 We also include nonequalization grants as additional covariates.

It is well known that tax policy decisions are often influenced by the political ideology of the governing party. Left-leaning governments generally have a tendency to raise income tax rates. Thus, we capture this ideological effect on tax policy by including a dummy variable that is equal to one if the premier of the province belongs to the Liberal Party or the New Democratic Party—which are the center-left political parties in Canada. 10 The literature on elections and fiscal policy indicates that governments may adjust their tax policy to raise their chances of reelection. As in Ferede, Dahlby, and Adjei (2015), we control for this possibility by including a dummy variable that is equal to one if there is an election in the following year in our set of control variables.

Data

In our empirical analysis, we use administrative data obtained from Finance Canada. The administrative data set includes raw data used to calculate equalization entitlements for each province and revenue category. These data are used to compute the average effective business income tax rate as the ratio of tax revenue to tax base. The average effective personal income tax rate is also calculated as the ratio of the administrative personal income tax revenue data used in equalization allocation formula to provincial taxable income. The administrative provincial data are also used to calculate the national standard average tax rate as the sum of provincial revenue divided by the sum of tax bases for business income tax. We also use the same data set to compute per capita tax base of standard provinces as the sum of the tax bases in the five standard (or ten, as the case may be) provinces by the sum of the population of the standard provinces.

The equalization base effect and the equalization rate effect variables require information on the national standard average tax rate, the population share of the standard province (relative to the total population of the standard provinces) and the own semielasticity estimates. For business income tax, data on the national standard average tax rates are obtained from Finance Canada as indicated above. For personal income tax, we compute the national standard average tax rate using administrative personal income tax revenue data used in the equalization allocation formula and provincial taxable income as the tax base. The data set on provincial taxable income was obtained from various issues of Income Statistics (formerly Tax Statistics on Individuals) published by the Canada Revenue Agency. Annual provincial data on personal income, GDP deflator, population, and the unemployment rate come from Canadian Socio-Economic Information Management database (CANSIM). The data on governing political parties and election are from the Canadian Parliamentary Guide.

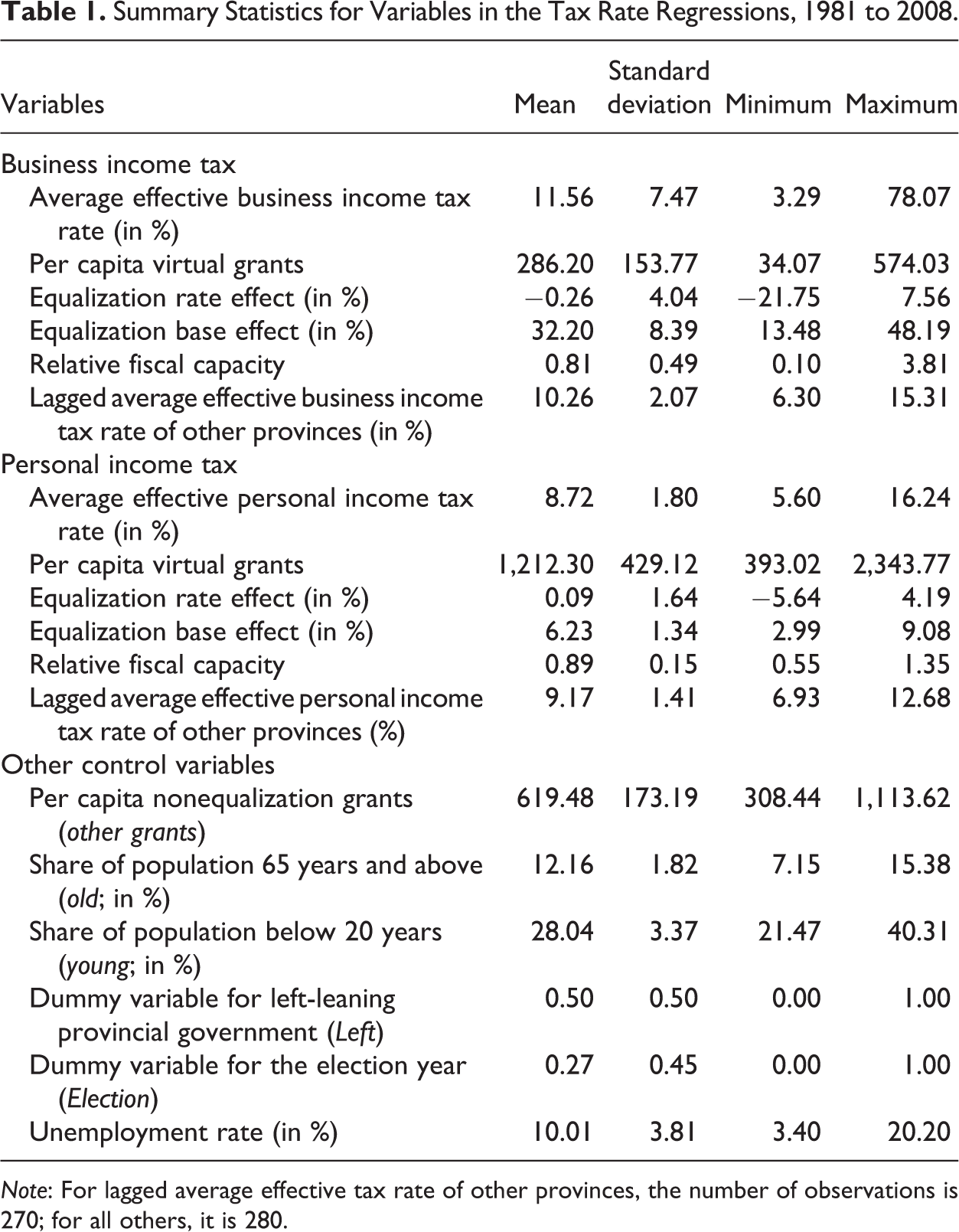

Our empirical analysis also require information on provincial own semielasticity estimates for the two taxes. Ideally, one would use province-specific own semielasticity estimates. However, such elasticity estimates are not available. In the absence of provincial specific data, we rely on the own semielasticity estimates obtained from Dahlby and Ferede (2012). These own semielasticity estimates are for all provinces and do not change across province or time. Their preferred own semielasticity estimates for the corporate income and personal income taxes are −3.671 and −0.762, respectively. We use these estimated semielasticity values to compute the equalization base effects for business income and personal income taxes, respectively. 11 The equalization rate effect variable is also computed using the tax base data obtained from Finance Canada. Table 1 provides summary statistics for the various variables used in our tax rate regressions.

Summary Statistics for Variables in the Tax Rate Regressions, 1981 to 2008.

Note: For lagged average effective tax rate of other provinces, the number of observations is 270; for all others, it is 280.

Empirical Results and Discussions

Results

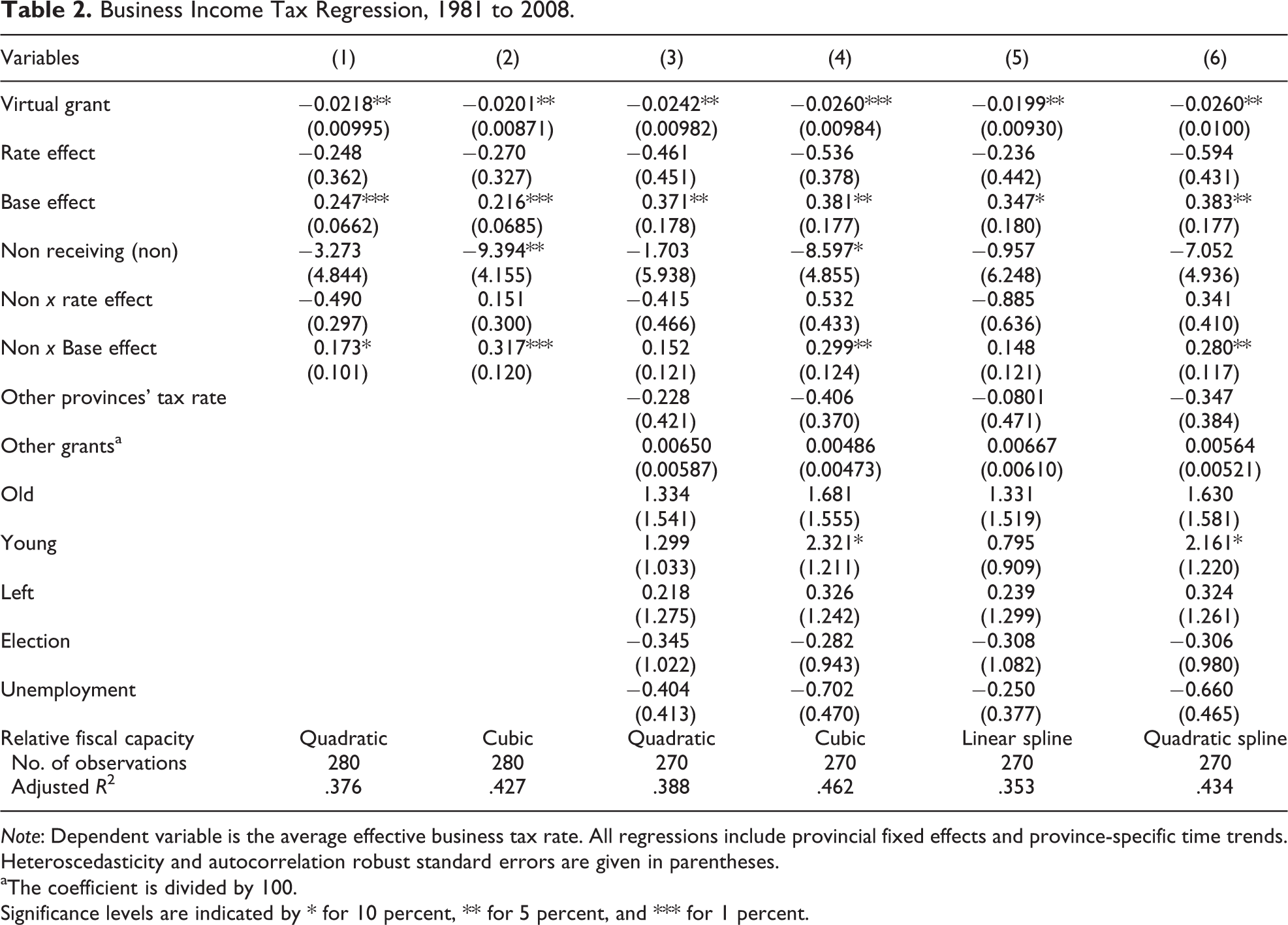

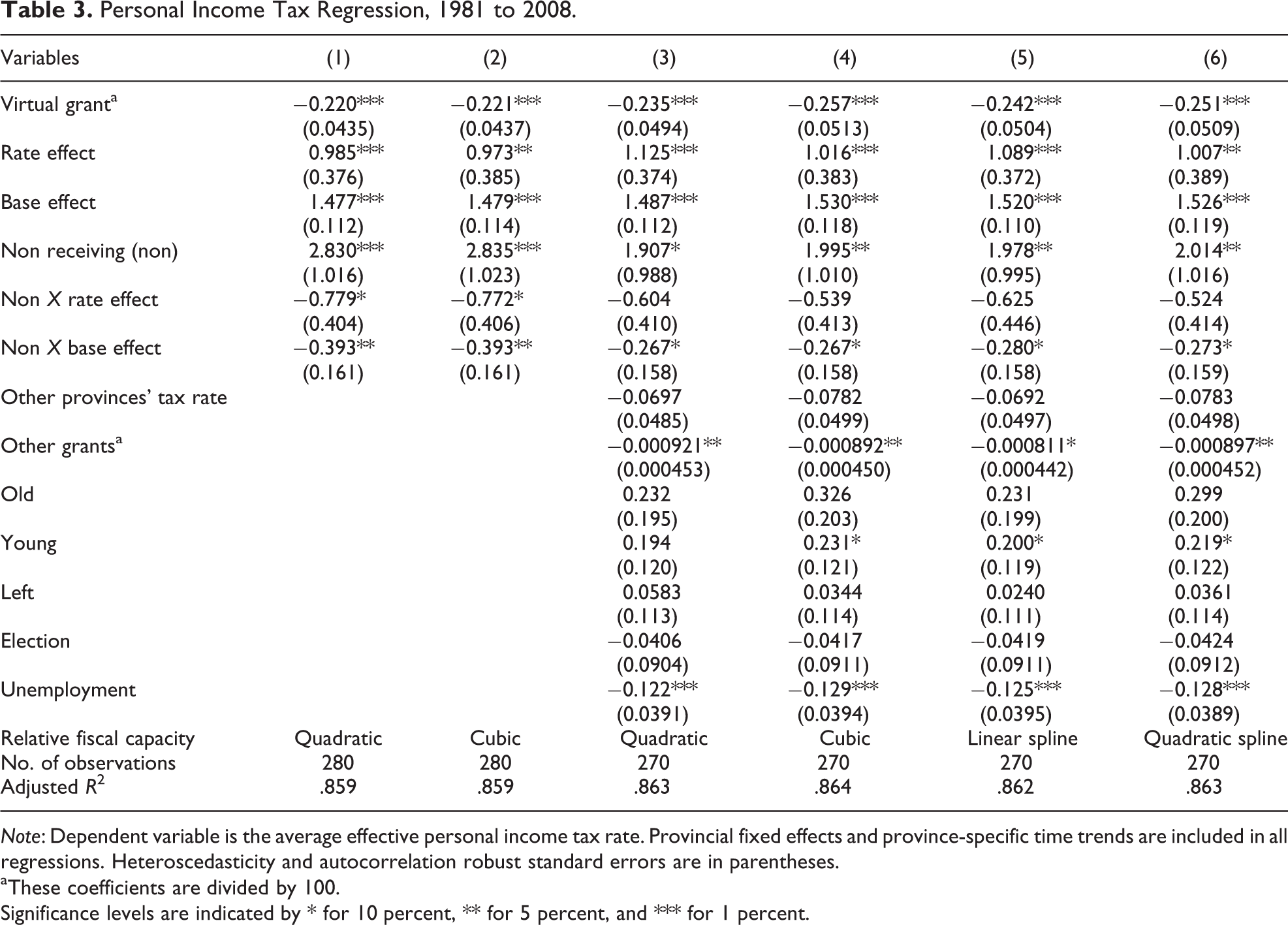

In this section, we present the empirical analysis related to the effects of equalization grants on business income and personal income tax policy incentives. While table 2 presents the regression results for business income tax, the corresponding results for personal income tax are shown in table 3. All regressions control for provincial fixed effects, province-specific time trends and nonlinear form of relative fiscal capacity as indicated but we do not report their coefficient estimates for the sake of brevity. Note also that the result tables provide standard errors which are robust to heteroscedasticity and arbitrary autocorrelation.

Business Income Tax Regression, 1981 to 2008.

Note: Dependent variable is the average effective business tax rate. All regressions include provincial fixed effects and province-specific time trends. Heteroscedasticity and autocorrelation robust standard errors are given in parentheses.

aThe coefficient is divided by 100.

Significance levels are indicated by * for 10 percent, ** for 5 percent, and *** for 1 percent.

Personal Income Tax Regression, 1981 to 2008.

Note: Dependent variable is the average effective personal income tax rate. Provincial fixed effects and province-specific time trends are included in all regressions. Heteroscedasticity and autocorrelation robust standard errors are in parentheses.

aThese coefficients are divided by 100.

Significance levels are indicated by * for 10 percent, ** for 5 percent, and *** for 1 percent.

We begin in column 1 of tables 2 and 3 by estimating our basic regression model with ordinary least squares estimation method. The dependent variables are average effective tax rates and we control for a quadratic form of relative fiscal capacity. Our results show that, as expected, the virtual grant variable is negative and statistically significant. This shows that virtual grants have a negative effect on tax rates. The reason is that virtual grant raises the financing capacity of provincial governments and as a result it enables them to finance any given amount of government spending at a lower tax rate. The virtual grant coefficient estimates show the effects of equalization grant on tax rates if the grant system were actually not based on fiscal capacity. If we consider a hypothetical situation where the equalization grants are substituted with block grants that do not depend on recipient provinces’ fiscal capacity, a $100 per capita increase in such grants is associated with a fall in business and personal income tax rates by about 2.2 and 0.22 percentage points, respectively.

The results in column 1 of tables 2 and 3 also show that, as expected, the equalization base effect is positive and statistically significant at 5 percent level or better for both regressions. However, the equalization rate effect is statistically significant only for personal income tax. Thus, the results suggest that equalization grants provide an incentive for provinces to raise the business income tax rate only thorough the equalization base effect. For personal income tax, on the other hand, our results indicate that equalization grants affect the tax policy incentives through both equalization base and rate effects. The results suggest that a one percentage point increase in the equalization base effect is associated with a 0.25 and 1.5 percentage point increase in the business and personal income tax rates, respectively. Similar results are also obtained in column 2 when we control for a cubic form of relative fiscal capacity.

In column 3, we control for a quadratic form of relative fiscal capacity and include additional covariates to capture the effects of economic, demographic, and political factors that potentially influence tax policy. Again, the equalization base effect continues to be positive and statistically significant for both business and personal income taxes while the equalization rate effect is statistically significant only in the latter.

In column 4, as in column 3, we include all the control variables and use a cubic form of relative fiscal capacity. Based on adjusted R 2, the regression with cubic specification for fiscal capacity shows the best fit for the data. Our results indicate that in a hypothetical scenario where the equalization grants are substituted with block grants, a $100 per capita increase in such grants is associated with a fall in business and personal income tax rates by about 2.6 and 0.26 percentage points, respectively.

The results also show that the equalization base effect continues to be positive and statistically significant at the 5 percent level or better in both tax rate regressions. However, the equalization rate effect is again not statistically significant for business income tax, but it is statistically significant at the 5 percent level for personal income tax. Thus, the empirical results indicate that, for business income tax, the effects of equalization grants on business income tax policy incentive work through the tax base effect. For personal income tax, however, both the equalization base and rate effects seem to be important in influencing the tax policy incentives. 12 The regression results suggest that a one percentage point increase in the equalization base effect is associated with 0.38 percentage point increase in the business income tax rate and a 1.5 percentage point increase in the personal income tax rate. Thus, our results are consistent with the widely held view that the Canadian equalization system provides the recipient provinces the incentive to raise their tax rates.

So far, we rely on using polynomial specifications for relative fiscal capacity. However, theoretically, other forms of smooth functional forms can also be employed. To check if our main result that equalization grants affect tax policy incentives is robust to other forms of specification, in columns 5 and 6, we control for linear-spline and quadratic-spline forms of relative fiscal capacity, respectively. The results are qualitatively similar to what we found before suggesting that they are robust to the form of nonlinear function of relative fiscal capacity. In general, our results suggest that equalization grants provide recipient provincial governments an incentive to raise their business and personal income tax rates. Thus, the results provide empirical support to the hypothesis that equalization grants provide an incentive to recipient governments to raise tax rates. And we find that this incentive effect works through the equalization base effect for business income tax and through both equalization base and rate effects for personal income tax. That is when provincial governments raise their income tax rates, their tax bases fall and this in turn results in an increase in the amount of their equalization entitlements.

How do our results compare to those of previous studies? Previous Canadian studies such as Esteller-Moré and Solé-Ollé (2002) and Smart (2007) find that provincial tax rates respond positively to changes in other provinces’ tax rates.

13

Our results are broadly consistent with those of Esteller-Moré and Solé-Ollé (2002) and Smart (2007). In order to make an indirect comparison of our results with those of Smart (2007), consider the case of a small equalization grant recipient province which has a negligible tax base share in the federation. In this case, the national average standard tax rate

Further, our results are related to those of Dahlby and Warren (2003) which find a somewhat weak evidence of the tax policy incentive effects of equalization grants for Australia. Using an empirical strategy very similar to ours, Buettner (2006) also shows that equalization grants have incentive effects on tax policy for Germany.

Sensitivity Analysis

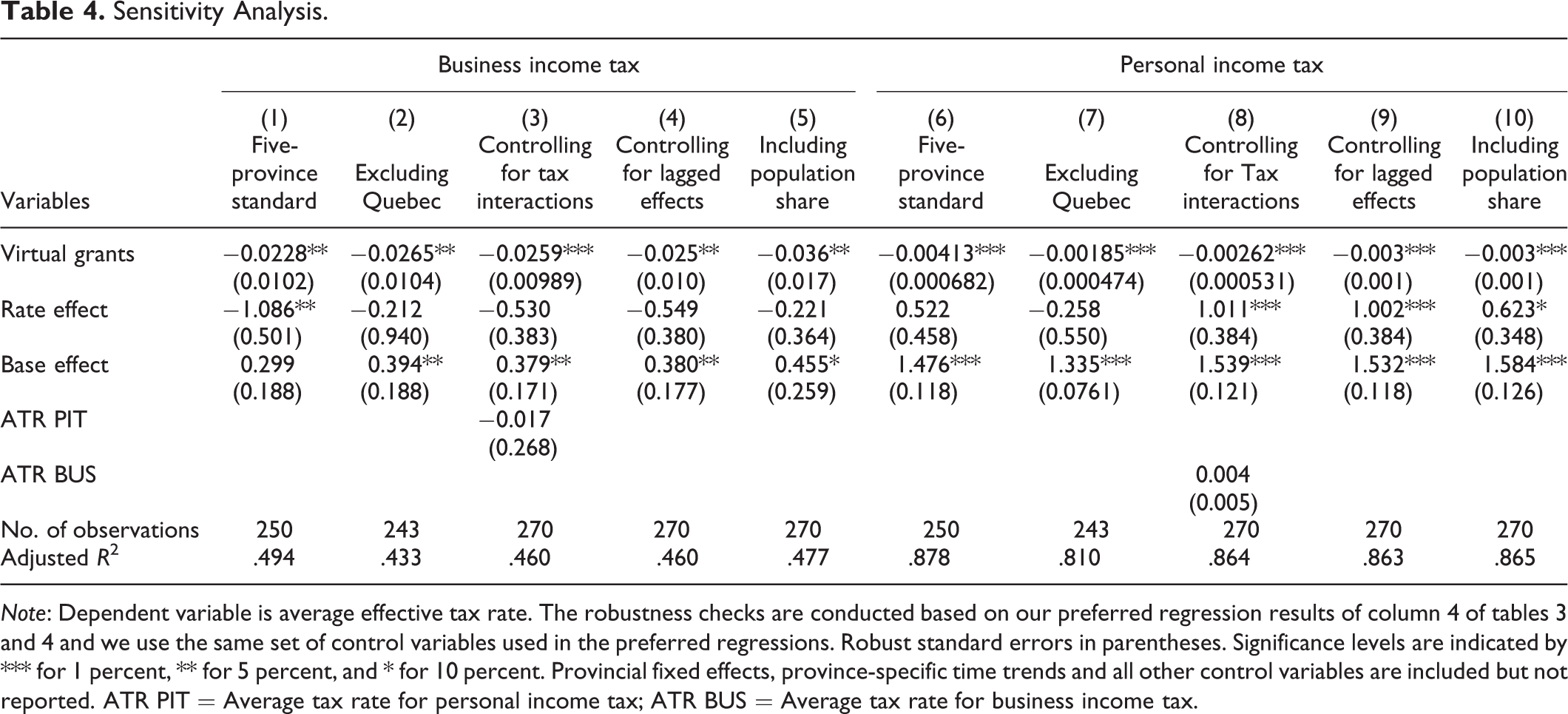

We conduct various robustness checks of our preferred regression results of tables 2 and 3. The results are shown in table 4.

Sensitivity Analysis.

Note: Dependent variable is average effective tax rate. The robustness checks are conducted based on our preferred regression results of column 4 of tables 3 and 4 and we use the same set of control variables used in the preferred regressions. Robust standard errors in parentheses. Significance levels are indicated by *** for 1 percent, ** for 5 percent, and * for 10 percent. Provincial fixed effects, province-specific time trends and all other control variables are included but not reported. ATR PIT = Average tax rate for personal income tax; ATR BUS = Average tax rate for business income tax.

During the period under consideration, the number of standard provinces change from ten provinces to five provinces and more recently back to ten provinces. 14 To check if this change in the number of standard provinces influences our results, we do the analysis only for the period where the five-province standard was in place. As results in columns 1 and 4 show, our results are robust to the change in the number of standard provinces.

As compared to other provinces, Quebec has various unique fiscal features. For example, it is the only province that receives the federal tax abatement. It is also the largest economy of all the equalization grant recipient provinces during the period under consideration. Thus, one may expect that the equalization rate effect to be more relevant and stronger for the province. To check for this, in columns 2 and 5, we exclude Quebec from our analysis. The results show that while the virtual grants and the equalization base effects continue to be statistically significant with their respective expected signs, the equalization rate effect is now insignificant in the personal income tax rate regression. This suggests that the statistical significance of the equalization rate effect in personal income tax that we find in the previous section may be driven by Quebec.

As previous studies indicate, business and personal income tax rates are related in many ways and may influence each other. Thus, one may suspect that personal income tax rate may influence the incentive effects of business income tax rate and vice versa. To capture this, we include the personal income tax rate and the business income tax rate as additional control variables in columns 3 and 8, respectively. While the estimated coefficients of these variables are not statistically significant, our main results are robust to this sensitivity check.

It may take some time for provinces to adjust to changes in equalization payments. If this is indeed the case, equalization payments may have lagged effects on tax rates. To check the robustness of our main result to this possibility, we include lagged effects of equalization payments as additional control variables in columns 4 and 9 of table 4. The lagged effects are generally found to be statistically insignificant. More importantly, our main results appear to be robust to this sensitivity check.

Smaller provinces generally have smaller tax bases and as a result they may be forced to raise tax rates regardless of the equalization program. To check the robustness of our main result for this possibility, we control for population share of provinces as an additional covariate in columns 5 and 10 of table 4. Again, our main results are robust to the inclusion of population share as a control variable.

In sum, our empirical analysis provides empirical evidence that the Canadian equalization system influences recipient provinces tax policy incentives. These incentive effects seem to work mainly through the equalization base effect. The results also show that virtual grants have statistically significant negative effects on tax rates. The policy implication of this is that if the current equalization grants are substituted with block grants that are not related to the fiscal capacity of the provinces, provincial tax rates will be lower.

Conclusions

The fiscal equalization program has been a long standing underpinning of the Canadian federation. As the program was designed to address fiscal disparities among provinces, the grant allocation formula compensates recipient provinces when their per capita tax base is below the standard per capita tax base. Thus, the key elements of the equalization formula can be influenced by the fiscal decisions of the provincial governments. This may provide recipient governments the incentive to change their tax policies in order to raise their equalization entitlements. In this article, we investigate how the Canadian equalization system influences the recipient provinces’ tax policy incentives using provincial data over the period 1981 to 2008.

Our empirical results suggest that equalization grants provide provincial governments an incentive to raise their business and personal income tax rates. We also find that this incentive effect works through the equalization base effect for business income tax. For personal income tax, on the other hand, the results indicate that equalization grants influence the tax policy incentives through both the equalization base and rate effects although the latter seems to be driven by Quebec. The equalization system reduces the provinces’ perceived MCF since the system compensates provinces with higher transfers when their tax bases shrink as a result of higher tax rates. Our results suggest that if the equalization program in its current form was abandoned, then business and personal income tax rates would be lower in the grant receiving provinces.

While this article is the first to provide empirical evidence on the incentive effects of the equalization system in a more complete setting, it does not provide answers on the net effects of the system on efficiency. Our results indicate that the equalization system provides recipient provinces the incentive to raise their tax rates and as a result creates inefficiencies. However, the incentive to raise tax rates under the equalization system may offset the competitive pressures to lower taxes to attract interprovincially mobile tax bases, and therefore counteract tax competition that reduces the ability of all provinces to raise revenues for needed public services. As the focus of this article is on just the incentive effects, the net effects of the equalization system on efficiency are not explored here. Investigating these conflicting effects of the equalization system on efficiency would be a fruitful path for future research.

Footnotes

Author’s Note

An earlier version of this article circulated as part of a technical working paper with the School of Public Policy, University of Calgary. All remaining errors are my own.

Acknowledgment

I would like to thank Thiess Buettner, Bev Dahlby, Tracy Snoddon, Jean-Francois Wen, and the anonymous referees for their valuable comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding for this project was provided by the School of Public Policy, University of Calgary.