Abstract

Because of their uncertain and destructive nature, natural disasters can pose severe shocks to societies and jurisdictions across all levels of government. Disaster-related financial risk is a critical problem in developing countries where people are highly vulnerable to the losses of natural hazards and climate change. This study empirically examines the fiscal impact of natural disasters at the provincial government level in China. Using a panel vector autoregression model, we find that natural disasters increase a province’s total governmental spending and intergovernmental revenues received from the central government while having little effect on its tax revenues. In particular, earthquakes and tropical storms cause larger impacts on spending and intergovernmental transfers. We also show that governments in higher-income Chinese provinces experience larger increases in spending and intergovernmental transfer following natural disasters than lower-income provincial governments. Our results provide important implications for the financial management of disaster risks in the developing context.

Natural disasters are low-probability incidents that can cause tremendous human and economic losses. In 2016, more than 300 large-scale natural disasters occurred worldwide, which were responsible for more than 7,000 deaths and US$100 billion direct economic damage (Centre for Research on the Epidemiology of Disasters [CRED] 2016). Because of their destructive and uncertain nature, natural disasters not only pose economic shocks to a society but also challenge the capacity of governments to protect their citizens. Disasters also place a financial burden on governments because they are often required to undertake emergency responses and provide assistance, thereby incurring more public expenses (Benson and Clay 2004). Natural disaster–induced economic shocks could further affect local tax bases and the collection of government revenues in the affected areas (Noy and Nualsri 2011). These potential consequences thus put a government’s fiscal stance at high risk of unexpected disaster shocks. Given the scientific consensus that climate change will likely worsen weather-related disasters (Intergovernmental Panel on Climate Change [IPCC] 2012), understanding the fiscal implication of natural disasters and making appropriate budgetary plans become an imperative for governments.

In this article, we examine the effects of natural disasters on provincial government finance in China. China is one of the world’s most disaster-prone countries because of its vast territory and unique geographic environment. 1 According to the statistics from CRED (2016), China has been hit by the highest number of disasters among all nations over the last decade. Its recent catastrophes include the 2008 Wenchuan earthquake, a series of severe droughts in Yunnan, Guizhou, and Sichuan provinces in 2009 and 2010, the Yushu earthquake in 2010, as well as the 2013 floods inflicting Southwest China. Given its high exposure to different types of natural hazards, China provides a compelling case to understand disaster-induced fiscal impacts and responses in the developing context.

While much of the prior research investigated the economic effects of natural disasters (e.g., on economic growth, incomes, and employment), less is known about the postdisaster fiscal dynamics. Several recent studies attempted to estimate the fiscal costs of natural disasters at the national scale (Lis and Nickel 2010; Noy and Nualsri 2011; Melecky and Raddatz 2011, 2014). However, these cross-country studies tend to neglect disaster-induced impact on intergovernmental transfers and resource reallocation within a country. As noted in Donahue and Joyce (2001), disaster management is intrinsically an intergovernmental policy issue because a disaster event often exceeds the coping capacity of local jurisdictions and calls upon the assistance from higher levels of government. Therefore, investigating how natural disasters affect subnational government finance sheds light on the local disaster burden and distribution of disaster costs between the central and subnational governments. Our research is one of the first to examine the fiscal impacts of natural disasters at the subnational level and the first one focusing on a single developing nation. Given China’s unique political regime and economic system, our research should provide useful insights into the implications of governmental institutions, intergovernmental relations, and disaster management system on local responses to natural disaster shocks.

For our empirical analysis, we compile a panel data set of thirty Chinese provinces over the period 1994 through 2014. We use the geophysical and meteorological data to measure the physical intensities for four types of disasters (earthquakes, tropical storms, floods, and droughts) and construct an aggregate disaster intensity index. Using a panel vector autoregression (VAR) method, we estimate the dynamic effects of natural disasters on fiscal behaviors including total tax revenues, governmental expenditures, and intergovernmental revenues from the central government. We find that natural disasters increase a province’s total government spending and receipt of intergovernmental transfers, although such effects gradually decay over time. Because the estimated disaster impacts on both expenditures and transfers are similar in magnitude, we infer that a large proportion of one province’s disaster cost is financed through intergovernmental aid and therefore borne by the central government. Disasters are found to have limited impacts on a province’s total tax revenues, which is consistent with the insignificant disaster effect on economic growth and outputs. Among the four types of natural disasters concerned, we show that earthquakes and tropical storms cause particularly larger impacts on a province’s expenditures and intergovernmental revenues. We also find that governments in higher-income Chinese provinces experience larger increases in spending and intergovernmental transfers following natural disasters than lower-income provincial governments.

The remainder of the article proceeds as follows. The Relevant Literature and Policy Background section reviews the prior literature on the fiscal impacts of natural disasters and provides background on disaster relief policy in China. The Data and Method section describes our data and empirical methodology. The Results section reports our primary findings and several extension tests. We conclude by discussing the implications of our results in the Conclusion section.

Relevant Literature and Policy Background

In this section, we first discuss the mechanisms through which natural disasters affect public finance and fiscal behaviors. We then provide a brief review of the recent empirical research examining the fiscal impacts of natural disasters, disaster research specifically related to China, as well as the policy background of disaster management and relief policy in China.

Understanding the Fiscal Consequence of Natural Disasters

Conceptually, natural disasters can influence a government’s financial conditions by affecting its expenditure and revenue flows (Benson and Clay 2004; Mahul et al. 2014). On the revenue side, scholars noted disasters might disrupt the robustness of tax bases depending on their influence on a local economy (Noy and Nualsri 2011; Lis and Nickel 2010). A growing body of research examined the short-run or long-run macroeconomic effects of natural disasters. 2 Many studies found natural disasters have a negative impact on economic outputs and growth (e.g., Raddatz 2007; Noy 2009; Cavallo et al. 2013; Felbermayr and Groschl 2014). Nonetheless, some researchers drew on Schumpeter’s creative destruction theory to argue that disasters provide an opportunity to upgrade physical capital and adopt new technologies, thereby leading to higher economic growth (e.g., Cuaresma, Hlouskova, and Obersteiner 2008; Skidmore and Toya 2002). In this regard, a disaster’s effect on government revenue sources through the macroeconomic dynamics could be ambiguous.

Natural disasters can also affect tax revenues depending on local tax structures (Noy and Nualsri 2011). For example, a disaster event that destroys a large number of properties could reduce local property tax revenues. At the same time, disasters may trigger more market transactions for replacing damaged physical assets, which could lead to increased sales tax revenues. It is noteworthy that a government may adjust its tax policy in the aftermath of a natural disaster (e.g., by providing tax relief for disaster victims), thereby affecting its tax revenues (Benson and Clay 2004).

Regarding public spending, large-scale disasters often require governments to undertake emergency responses such as cleaning up sites and removing debris and also provide disaster relief aid and assistance to short- and long-term recovery activities. All these responses could lead to increased public expenditures or possible reallocation of budgetary resources such as diverting funding from other sources and postponement or abandonment of planned capital projects (Benson and Clay 2004). 3 To the extent that natural disasters reduce incomes, governments may have to incur different types of expenditures such as welfare transfer payments. For example, Deryugina (2017) found hurricanes not only increased the federal disaster relief but also substantially increased US governmental spending on social safety net programs. Her research suggests that the disaster victims in developed countries are better insured than those in developing countries because of the social insurance programs.

Finally, it is essential to note that while natural disasters are mostly local incidents, their fiscal impacts may expand across all levels of government. Large-scale disasters that overwhelm local governments could trigger assistance from the national government or even from the international community. In this case, the local disaster cost is partially shifted to the rest of society through intergovernmental transfers.

Empirical Literature

Several recent studies have empirically estimated the fiscal impacts of natural disasters, mostly in a cross-country setting. For example, Lis and Nickel (2010) found large-scale extreme weather events have a negative impact on national budget balances. Their study, using a panel fixed effects model, suggested that the budgetary effect of weather shocks is around 1.4 percent of gross domestic product (GDP), and this effect is more substantial in developing countries than that in developed countries. Melecky and Raddatz (2011, 2014) examine how different types of natural disasters (geological, climatic, and others) affect government expenditures, revenues, and fiscal deficits for a sample of high- and middle-income countries during the 1975 to 2008 period. Using the panel VAR model, they find that climate hazards affect a country’s fiscal stance by increasing its budget deficits, and countries with more-developed debt markets suffer a smaller disaster disturbance. Noy and Nualsri (2011) used the quarterly data for a panel of forty-two countries between 1990 and 2005 to show different patterns of fiscal responses across countries. They found developed countries generally increase spending with decreased revenues following disasters, whereas developing countries respond in a procyclical way with decreased spending and increased revenues. Ouattara and Strobl (2013) also employed the panel VAR model to estimate the impact of hurricanes on a group of eighteen Caribbean countries over the 1970 to 2006 period. They found hurricane strikes led to a short-run increase in government spending, which worsened national budget deficits.

Our article is most similar to Miao, Hou, and Abrigo (2018) that examined the fiscal implications of natural disaster damage at the US state level. Specifically, they found natural disasters increased the total spending of state governments and also federal-to-state transfers while having little impact on states’ total own-source revenues. This finding suggests that disaster-induced additional expenditures at the state level are mainly financed through federal transfers, and therefore, the federal government bears most of the ex post fiscal costs of natural disasters. Our work further extends this line of research by examining the fiscal consequence of natural disasters in a single developing country and the distribution of disaster burdens between its central and subnational governments.

This article also draws upon another line of literature examining the economic impacts of natural disasters in China. Vu and Noy (2015) investigated the disaster impact on income and investment in China and found that natural disasters are associated with lower per capita income and higher fixed asset investment (due to the reconstruction of damaged infrastructure) in the affected provinces in the short run. Guo et al. (2015) found natural disasters have no significant effects on the provincial-level GDP growth rate, while meteorological disasters lead to higher economic growth by increasing human capital investment. Chen, Luo, and Pan (2013) investigated the relationship between economic development and disaster damage in China and showed income growth leads to a significant reduction in disaster-induced fatalities.

Disaster Aid Policy in China

In China, the State Council and particularly the Ministry of Civil Affairs (MCA) play a leading role in making and implementing disaster policy and coordinating disaster responses and relief efforts (Zheng and Mu 2006). 4 When a large-scale disaster strikes and exceeds the local capacity to respond, local governments report to and apply for financial aid from the higher levels of government. The central government has the authority to distribute disaster relief based on the application proposals by the affected local governments (Zhang et al. 2015). The MCA also classifies natural disasters into three levels based on the severity of their damages and outlines different emergency relief works and procedures for each level. 5

Once the disaster aid is approved, MCA works in conjunction with the Ministry of Finance (MOF) to distribute aid to the provincial governments and eventually to the county/township governments level by level. The central Chinese government provides disaster aid through a variety of programs including the live relief fund, sanitation relief fund, flood prevention and drought resistance fund, fund for damaged transportation infrastructure, agricultural relief fund, and reconstruction fund (Zheng and Mu 2006). The MCA and MOF have set up specific requirements for ensuring timely distribution of the disaster relief funds. 6 Because of the diverse programs that provide postdisaster assistance, it is a challenge to quantify the exact amount of disaster expenses.

The Budget Law of the People’s Republic of China of 1994 requires Chinese governments to reserve 1 percent to 3 percent of their annual budget expenditures for the contingency funds, which are now the primary source for financing postdisaster activities. When local governments’ reserve is exhausted when responding to a disaster event, the central government provides aid from its reserve funds. One problem, as noted by some researchers, is that the contingency reserves at both the central and subnational governments are often insufficient to cope with large-scale disasters (Zhang et al. 2015). For example, in 2010, the central government appropriated 40 billion Chinese yuan (5.8 billion US dollars) for its contingency funds (about 2.5 percent of the central budget expenditures), whereas the actual disaster relief spending from this account was 78 billion Chinese yuan (11.5 billion US dollars) in the same year (Zhang et al. 2015). We further discuss the implication of our findings for the Chinese disaster budgeting practices in the Conclusion section.

Data and Method

Data Sources and Variables

For our analysis, we combine natural disaster and public finance data to create a balanced panel of thirty Chinese provinces (Tibet is excluded due to data unavailability) between 1994 and 2014. To measure disaster severity, we follow Felbermayr and Gröschl (2014) and construct a multi-hazard data set of physical disaster intensities using the geophysical and meteorological information collected from various sources. This approach, as compared to previous studies (e.g., Noy and Nualsri 2011) that used disaster damage to model financial impacts, is arguably better because it captures the exogenous destructive power of a natural disaster event, whereas disaster damage is endogenous to human exposure and their socioeconomic conditions (Cavallo et al. 2013; Stroemberg 2007). Specifically, we focus on four types of natural disasters: earthquakes, storms, flooding, and droughts, all of which account for about 95 percent of total disaster fatalities and damages in China over our study period according to statistics from the Emergency Events Database (EM-DAT) maintained by the CRED. 7

For earthquakes, we use data from the Significant Earthquake Database provided by the US National Geophysical Data Center. To account for the intensity and frequency of seismic activities, we create a variable measuring the number of earthquakes measuring five and above on the Richter scale that occurred in a province in a given year.

Regarding storms, we use data from the International Best Track Archive for Climate Stewardship (IBTrACS) provided by the National Centers for Environmental Information of US National Oceanic and Atmospheric Administration. 8 We map the IBTrACS storm data to the affected regions in ArcMap and focus specifically on severe tropical cyclones that hit southeast China. For each province-year, we calculate the number of storm events with a maximum sustained wind speed of forty-eight knots or eighty-nine kilometer per hour and above (including severe tropical storms, typhoons, very strong and violent typhoons based on the Regional Specialized Meteorological Center Tokyo’s Tropical Cyclone Intensity Scale).

To measure the physical magnitude of floods and droughts, we use the monthly precipitation data from the Climatic Research Unit (CRU) Timeseries Version 401, a global gridded data set of climatic observations at 0.5° latitude/longitude resolution (Harris et al. 2014) covering the period from 1901 through 2016. We intersect the gridded precipitation data with China’s provincial boundaries in ArcMap and calculate the average monthly total precipitation using the gridded values within a province for each year. Following the approach in Felbermayr and Gröschl (2014), we create a rainfall anomaly variable by calculating the proportional deviation of a province’s monthly rainfall from its long-run average monthly rainfall for the period from 1981 through 2014. We measure the severity of flooding for a province-year observation by adding up the positive values of monthly rainfall anomalies within each year. Considering the chronic nature of droughts, we create a binary variable for droughts if a province’s monthly rainfall is below 50 percent of its long-run average for at least five months within a year.

We take a further step to create a composite disaster intensity index by aggregating all types of natural hazards discussed above. This variable is constructed as the weighted sum of different disaster intensity measures using the inverse of the standard deviation of a disaster type within a province over our study period as the weights. By doing this, we prevent a single type of natural disaster from dominating the value of the whole disaster index. We use the aggregate disaster index in our baseline estimation and then examine the fiscal impacts by disaster types as an extension.

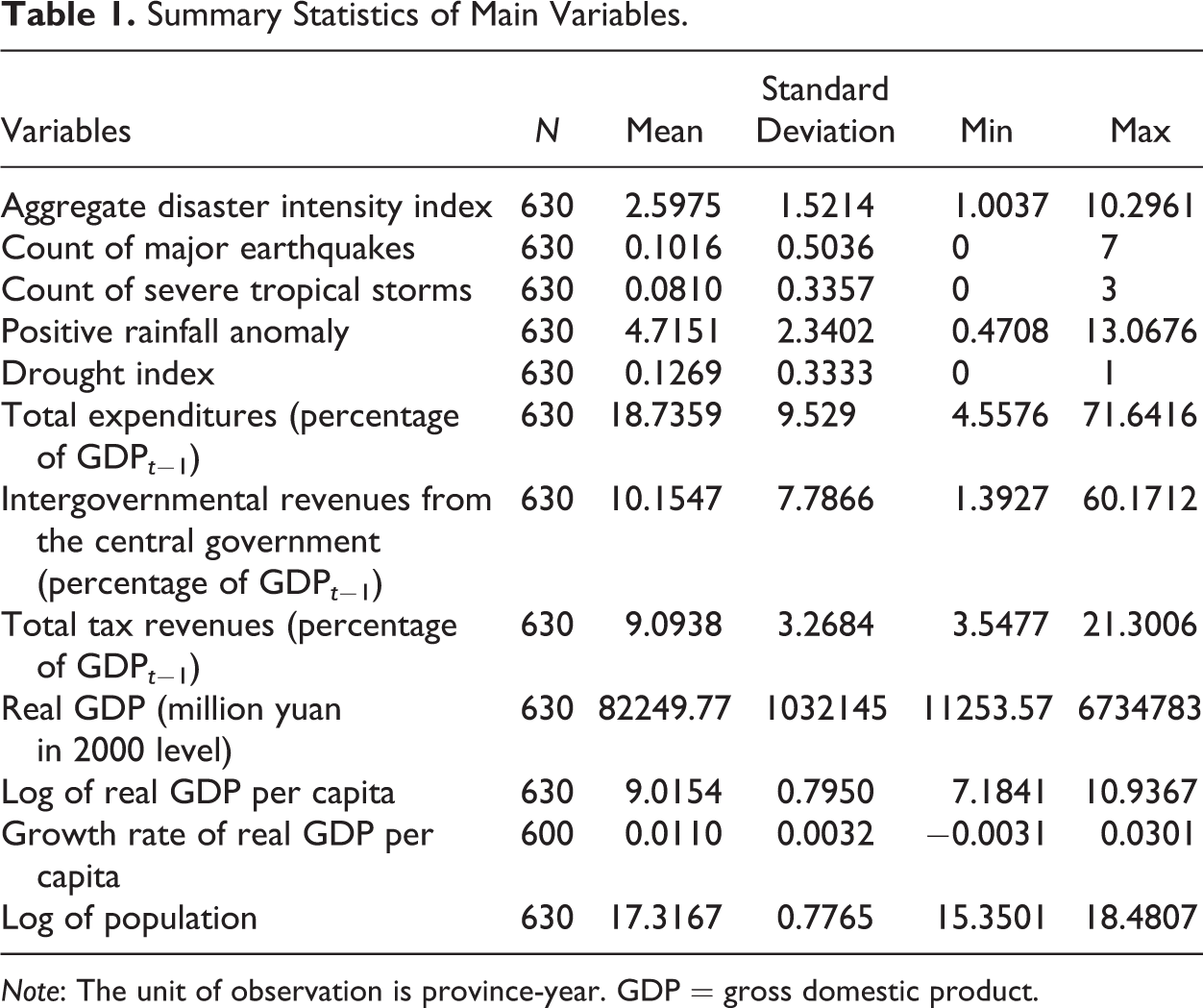

We obtain the annual data on province-level GDP, GDP per capita, and population from the China Data Online. Our public finance data come from the China Statistical Yearbook, including a province’s total tax revenue, governmental spending, and intergovernmental revenues received from the central government. 9 We do not account for debt issuance because the Chinese provincial governments were not allowed to issue debt until recently. All fiscal variables are normalized as the ratio of a province’s GDP in the previous year to address endogeneity concerns. 10 Table 1 presents the summary statistics of the variables used in our regression analyses.

Summary Statistics of Main Variables.

Note: The unit of observation is province-year. GDP = gross domestic product.

Empirical Methodology

In this study, we employ a panel VAR model, which allows for endogenous interactions among the multiple dependent variables measuring fiscal outcomes. The panel VAR framework derives from the VAR model, in which each endogenous variable is determined by its own lagged values, lagged values of other endogenous variables, and other exogenous variables. It incorporates a panel data structure that allows for controlling unobserved time-invariant cross-sectional heterogeneity (Holtz-Eakin, Newey, and Rosen 1988). Prior studies have used this method to estimate the dynamic fiscal impacts of natural disasters across countries (e.g., Ouattara and Strobl 2013; Noy and Nualsri 2011) as well as within a single country (Miao, Hou, and Abrigo 2018).

We estimate a reduced-form panel VAR model with a distributed lag of disaster variables as follows: 11

where Yit

is a vector of fiscal variables for province i in year t (Yit

Because including the individual fixed effects in a dynamic model with lagged dependent variables could cause biased estimates (Nickell 1981), we instrument for the endogenous variables with lags of Y in levels (specifically, lagged values in years t − 2 through t − 6) and estimate the model using generalized method of moments (GMM) as implemented in Abrigo and Love (2016). 14 Finally, we cluster standard errors at the province level to address potential heteroscedasticity and autocorrelation.

As discussed earlier, one unique advantage of using panel VAR in this study is allowing all fiscal variables to be treated as endogenous and interrelated, considering that fiscal decisions are often jointly or serially determined. For example, a disaster shock may immediately increase the need for government spending on disaster response, which might lead the affected jurisdiction to collect additional revenues or request more intergovernmental aid. Using this methodology, we can examine the spillovers of a disaster’s impact on one endogenous variable onto other endogenous variables in succeeding periods (Miao, Hou, and Abrigo 2018). Our identifying assumption is that natural disasters, measured by their physical intensities, are exogenous to a provincial government’s fiscal stance. 15

Based on the estimated panel VAR coefficients, we construct the dynamic multiplier functions (DMFs) by performing Monte Carlo simulations with 500 iterations to generate the 95 percent confidence interval. The DMF reports the isolated impact of a one-unit increase in disaster intensities on the concerned fiscal outcome one period at a time while holding other shocks equal to zero. Therefore, they are useful for tracing the dynamic impacts of natural disasters over different time horizons and help in identifying the duration through which a disaster shock persists.

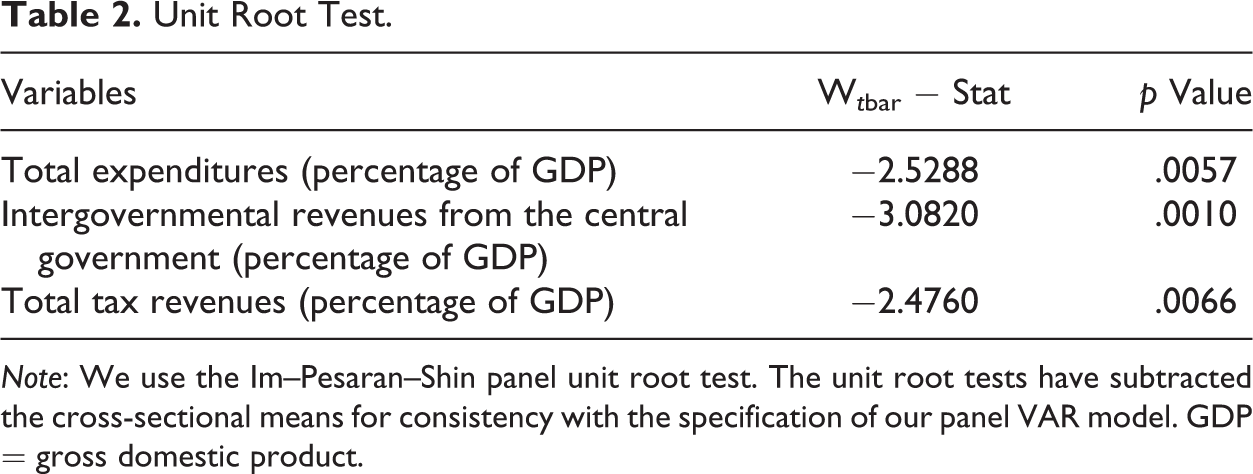

As a precondition for using the panel VAR model, we test for stationarity of the fiscal variables by performing the unit root tests. We use the test proposed by Im, Pesaran, and Shin (2003) for heterogeneous panels, given that we have moderate T and moderate N. Table 2 shows that the three variables are all stationary (i.e., the null hypothesis for the presence of panel unit root is rejected).

Unit Root Test.

Note: We use the Im–Pesaran–Shin panel unit root test. The unit root tests have subtracted the cross-sectional means for consistency with the specification of our panel VAR model. GDP = gross domestic product.

Results

Baseline Results

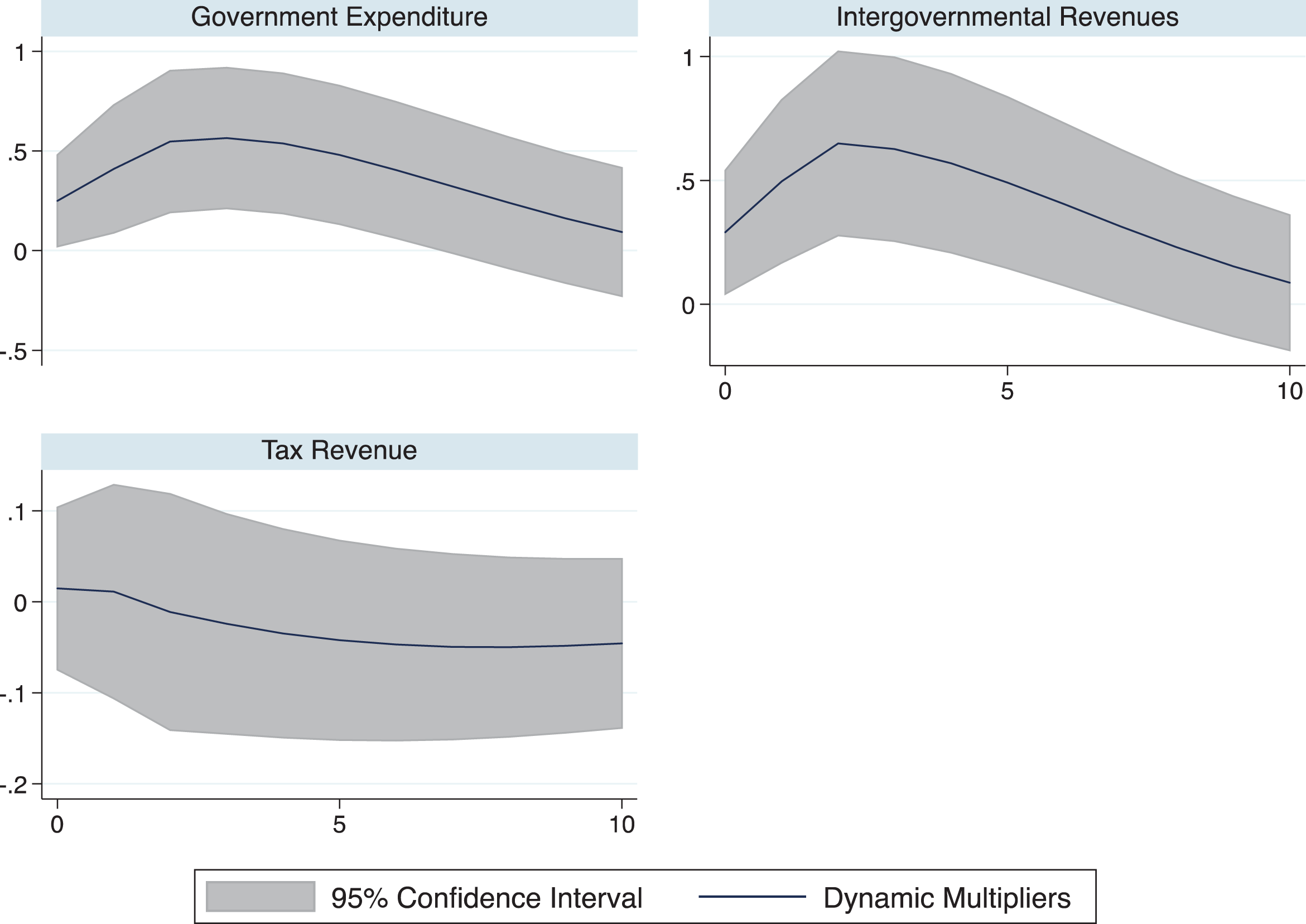

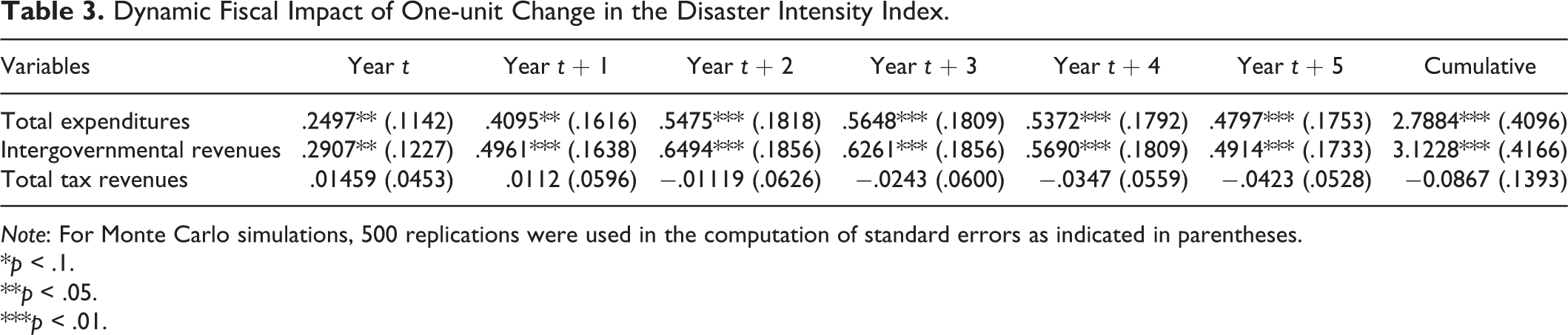

Figure 1 displays our estimated DMFs of the aggregate disaster index on each fiscal variable in year t (when a disaster shock occurs) through year t + 10, and table 3 summarizes the DMF point estimates in each year from year t through year t + 5 as well as the cumulative fiscal impact of natural disasters over this period. With an increase in the disaster index in year t, total provincial government spending and intergovernmental revenues from the central government both rise immediately, peak in year t + 3 and t + 2, respectively, and decline thereafter.

Dynamic fiscal impact of natural disasters (aggregate intensity index).

Dynamic Fiscal Impact of One-unit Change in the Disaster Intensity Index.

Note: For Monte Carlo simulations, 500 replications were used in the computation of standard errors as indicated in parentheses.

*p < .1.

**p < .05.

***p < .01.

In interpreting these estimates quantitatively, our model predicts that when the disaster index in year t increases by one standard deviation (1.5 in our sample), a province’s total spending and intergovernmental revenues increase by 0.38 and 0.44 percentage points of GDP in the same year, respectively. The five-year postdisaster effects amount to an increase of 4.2 percentage points of GDP in spending and 4.7 percentage points of GDP increase in transfers, both of which are statistically significant at the 1 percent level. This cumulative effect is equivalent to a 20-percent increase from the sample mean of annual total provincial government spending and a 46-percent increase from our sample mean of yearly intergovernmental transfers. In monetary values, the increased spending over the five years total to 33,722 million yuan (about 4,959 million US dollars), and increased transfers total to 37,012 million yuan (about 5,443 million US dollars), based on the sample mean of a province’s annual real GDP. Because disaster-induced increases in the two variables are close in magnitude, we infer that the majority of a province’s increased public expenditure is financed through transfers from the central Chinese government. By contrast, we find that changes in disaster intensity seem to have little impact on a province’s total tax revenues, either in individual years or cumulatively. Overall, these results are similar to the findings in previous studies, including Ouattara and Strobl (2013) and Miao, Hou, and Abrigo (2018) in suggesting countercyclical fiscal responses to natural disasters.

As a robustness check, we use the count of large-scale disaster incidents as an alternative disaster measure and find similar results, that is, natural disasters tend to increase total government expenditures and intergovernmental revenues while having little effect on total tax revenue (results presented in the Online Appendix). 16

Fiscal Impact by the Type of Natural Hazard

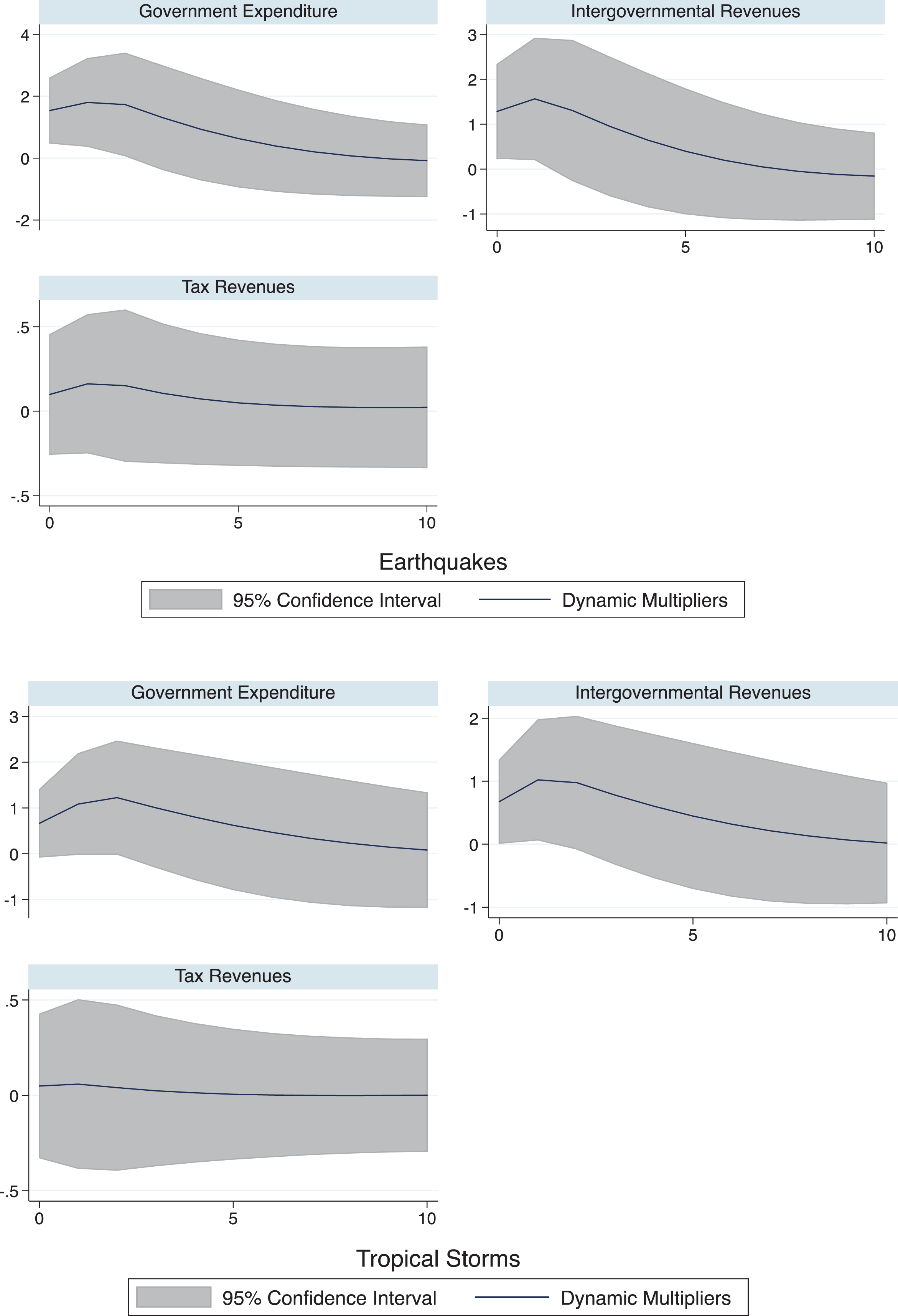

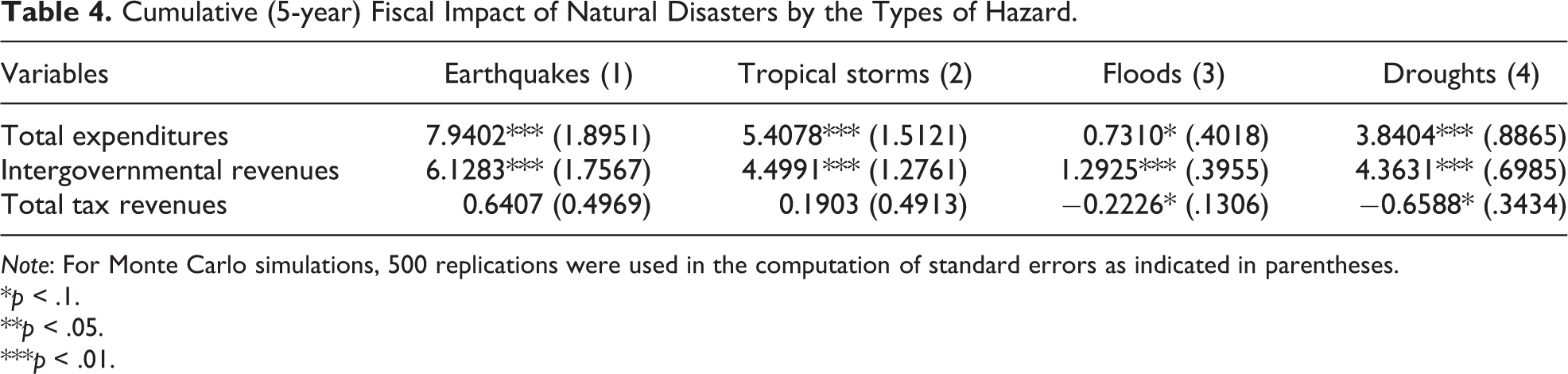

Using the baseline model, we take a further step to examine the fiscal impacts of different types of natural disasters (earthquakes, tropical storms, floods, and droughts) measured by the disaggregate hazard-specific intensity measures. Figure 2 shows the estimated DMFs for each type of disaster regarding the dynamic effects of a one-unit increase in its physical intensity from year t through year t + 10. We report our estimates of the five-year cumulative impacts by the hazard types in table 4.

Dynamic fiscal impact of natural disasters by hazard types.

Cumulative (5-year) Fiscal Impact of Natural Disasters by the Types of Hazard.

Note: For Monte Carlo simulations, 500 replications were used in the computation of standard errors as indicated in parentheses.

*p < .1.

**p < .05.

***p < .01.

We find that following a significant earthquake, a province’s total government spending and intergovernmental revenues flowing from the central government increase immediately. Both variables peak in year t + 1 with an increase of 1.8 and 1.6 percentage points of GDP. To put these numbers in perspective, a major earthquake is expected to increase a province’s total spending by 10 percent and intergovernmental revenues by 16 percent in the next year (based on the sample mean). The cumulative effect on total expenditures and transfers in the five-year postshock period amounts to 7.9 and 6.1 percentage points of GDP, respectively. 17 In monetary values, this is equivalent to 64,977 million Chinese yuan (9,555 million US dollars) increase for total government expenditure and 50,172 million Chinese yuan (or 7,378 million US dollars) increase for intergovernmental revenues, based on the sample mean of a province’s annual real GDP. We find a similar pattern for storms. A severe tropical storm (i.e., with a maximum sustained wind speed of forty-eight knots and above) is expected to increase provincial government spending and intergovernmental transfers by 5.4 and 4.5 percentage points of GDP, respectively, over the five-year poststorm period. These are equivalent to an increase of 44,415 million Chinese yuan (6,532 million US dollars) in total spending and an increase of 37,012 million Chinese yuan (5,443 million US dollars) in total transfers, based on our sample mean of real GDP.

Regarding the flooding hazard (measured by summed positive rainfall anomalies across months within a year), we find that while the impacts of floods on all three fiscal outcome variables are statistically insignificant in all individual years, their cumulative effects on total government spending and transfers are positive and significant (totaling to an increase of 0.7 and 1.3 percentage points of GDP, respectively). Similar to other types of natural disasters, droughts increase a province’s total spending and intergovernmental revenues. Such effect peaks two years later and totals to a cumulative increase of 4 percentage points of GDP (equivalent to 32,900 million Chinese yuan or 4,838 million US dollars) in both variables over the next five years following the drought.

Our results also suggest that floods and droughts cause a negative cumulative effect on a province’s total tax revenues over the five-year postshock period (statistically significant at 10 percent level). 18 By contrast, the impact of earthquakes and tropical storms on tax revenues is indistinguishable from zero, which is consistent with our main findings.

Comparing Dynamic Fiscal Responses in Higher-income versus Lower-income Provinces

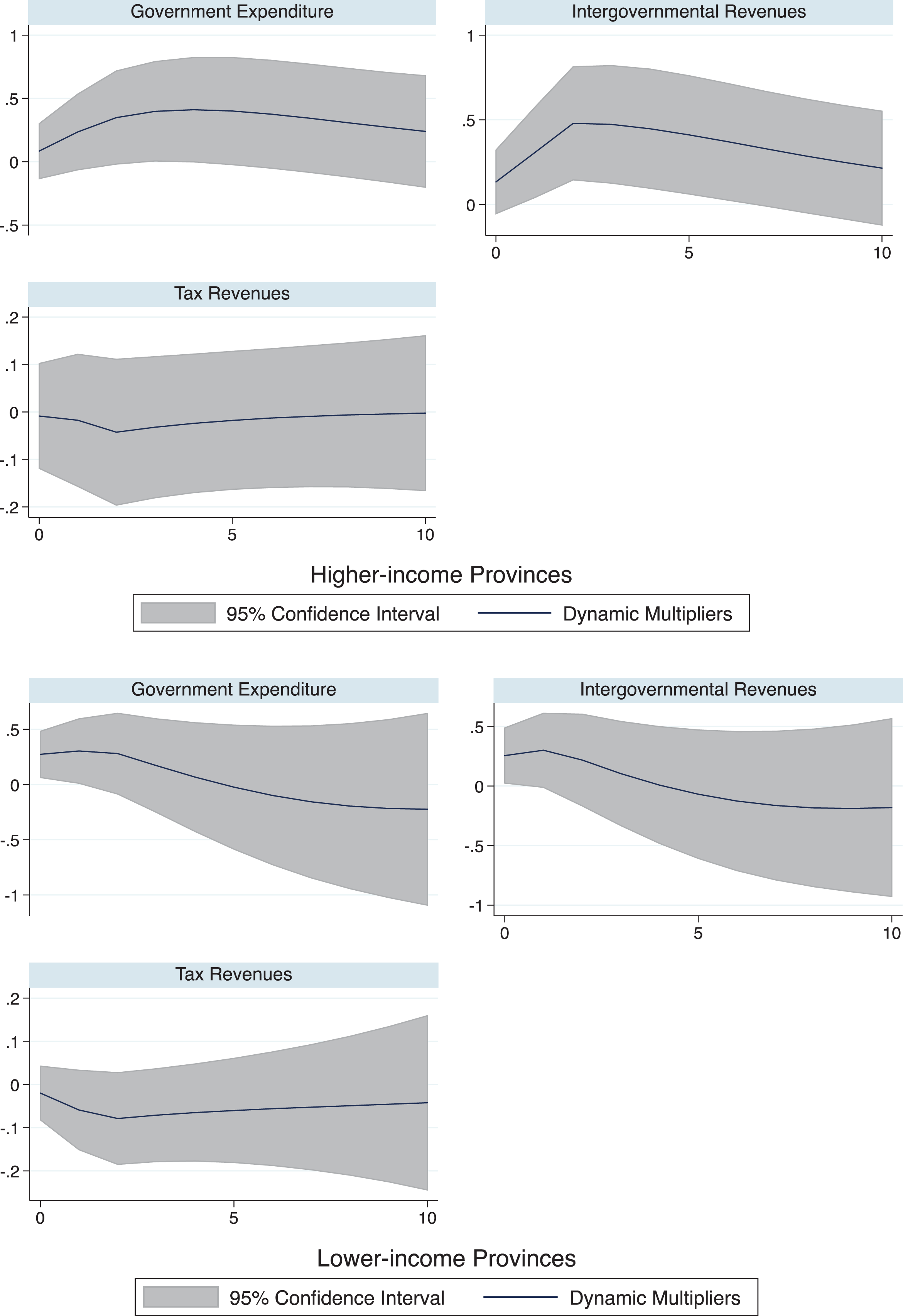

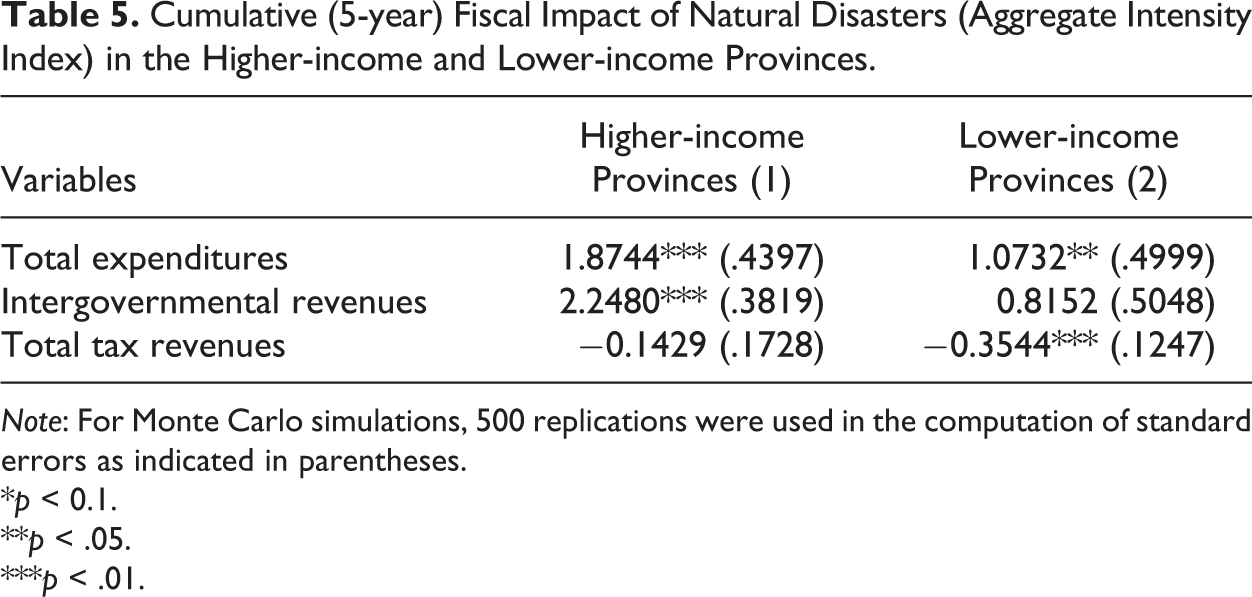

The existing literature suggests that countries at different levels of economic development may respond differently to disaster shocks. For example, Noy and Nualsri (2011) found national governments in developed countries tend to increase their spending with decreased revenues while developing countries show an opposite procyclical response. In this subsection, we examine, within a single country, whether and how subnational governments respond differently in the aftermath of natural disasters depending on their income levels. We divide our sample into two groups of provinces based on whether a province’s average real GDP per capita over our study period is above or below the national median. Then we reestimate our model separately for higher- and lower-income provinces using the aggregate disaster intensity index. We report our estimation results in figure 3 and table 5.

Dynamic fiscal impact of natural disasters (aggregate disaster intensity index) in the higher-income and lower-income provinces.

Cumulative (5-year) Fiscal Impact of Natural Disasters (Aggregate Intensity Index) in the Higher-income and Lower-income Provinces.

Note: For Monte Carlo simulations, 500 replications were used in the computation of standard errors as indicated in parentheses.

*p < 0.1.

**p < .05.

***p < .01.

Our estimates indicate that a higher disaster index generally increases government expenditures in both groups of provinces, but the cumulative effect on spending is larger in magnitude in wealthier provinces than in poorer provinces. An explanation for this finding is that higher-income provinces have a larger tax base, and therefore, their governments have more funds or slack resources that can be mobilized to finance postdisaster response and recovery. By contrast, governments in the poorer provinces are less capable of undertaking costly response and recovery activities in the postdisaster period.

We also find that the governments in wealthier provinces receive significantly more intergovernmental revenues after disasters, whereas the increase in poorer provinces is only statistically significant in the first two years (year t and year t + 1) and cumulatively insignificant over the five-year postshock period (p value = 1.6148). One possible explanation is that more affluent provinces, given their greater economic and political power in the nation, have higher chances of being offered more disaster aid by the central government. As noted in Liu, Martinez-Vazquez, and Wu (2016), the wealthier provinces in China received more resources from the central government because some of their top leaders took important positions at the Central Politburo of the Chinese Communist Party and directly influenced the aid allocation decisions made by the central government. Another explanation is that in addition to the aid from the central government, low-income regions in China could receive postdisaster assistance from other high-income provinces. For example, after the 2008 Wenchuan earthquake, the central government paired the affected counties with other unaffected, more affluent provinces and required the latter to devote at least 1 percent of their annual government revenues to assist recovery activities in their paired jurisdictions. In other words, the mandated direct assistance provided by other provincial governments may reduce the need for transfers from the central government.

Our results further suggest that more severe natural disasters decrease total tax revenues in the poorer provinces over the 5-year postdisaster shock period while having little effects on tax revenues in the wealthier provinces. As we discussed earlier, how natural disasters affect governmental revenues depends on not only the macroeconomic dynamics but also the possible adjustment in tax policy (e.g., tax relief for victims). As for the poorer provinces, since their governments did increase spending significantly following disasters, it is less likely for them to reduce the amount of tax revenues collected. The negative disaster shock to the tax revenue is more likely to result from the adverse impact of natural disasters on economic activities. This finding may suggest that the local economy and government finance in the lower-income regions are more vulnerable to natural disaster shocks.

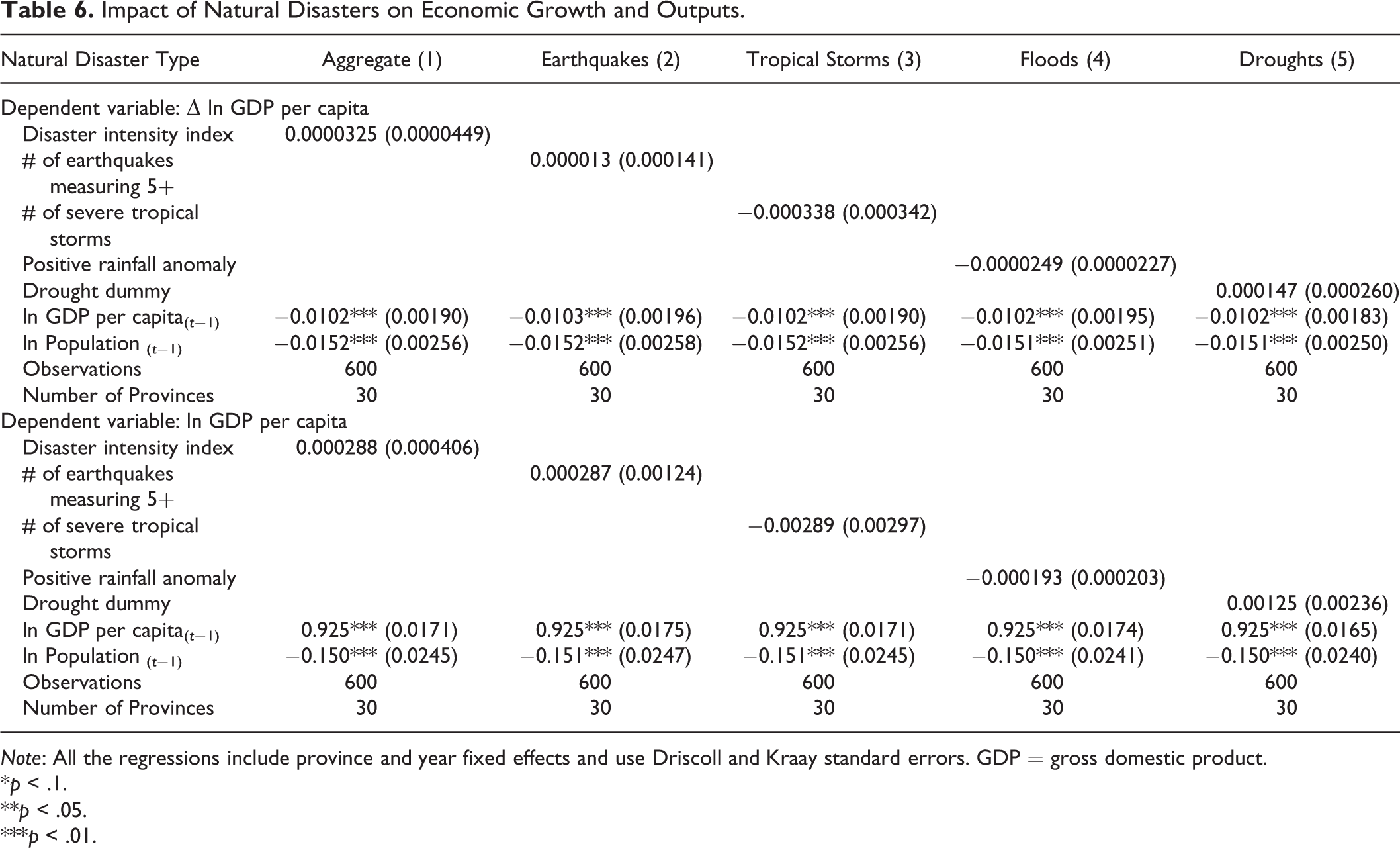

Impact of Natural Disasters on Economic Outputs and Growth

Since our baseline results suggest that disasters have little impact on total tax revenues, we further examine the macroeconomic impact of natural disasters as one plausible mechanism of a disaster’s effect on tax bases. Following the standard growth regression approach used in the prior disaster economics studies (e.g., Felbermayr and Gröschl 2014; Strobl 2011), we estimate a dynamic panel data model specified as follows:

where Growth it denotes the growth rate of real GDP per capita for province i in year t, and ln(GDPit −1) is the lagged log of GDP per capita. Dit denotes aggregate or disaggregate disaster intensity. In the specification, we also control for the lagged population, the province-specific fixed effects (θ i ), and year fixed effects (γ t ). 19 In addition to the growth rate, we use the log of real GDP per capita as an alternative dependent variable. To account for potential spatial and temporal dependence, we use the Driscoll and Kraay (1998) standard errors (Hoechle 2007).

As shown in table 6, we find that natural disasters generally have little effect on the economic growth rates or output levels at the province level. The estimated coefficients on all disaster variables are all statistically insignificant and small in magnitude. This finding resonates with our baseline finding regarding the limited disaster effect on tax revenues, which may suggest that disasters do not pose significant shocks to local tax bases.

Impact of Natural Disasters on Economic Growth and Outputs.

Note: All the regressions include province and year fixed effects and use Driscoll and Kraay standard errors. GDP = gross domestic product.

*p < .1.

**p < .05.

***p < .01.

Conclusion

Many scholars have noted that developing countries are more vulnerable to losses from natural disasters than their developed counterparts because of their lower incomes and weak institutional capacities (e.g., Kahn 2005; Kousky 2014; Escaleras and Register 2016). Large-scale natural disasters can trigger substantial fiscal ramifications for governments in developing countries and further strain their public resources. As climate change unfolds and extreme weather events (e.g., floods and hurricanes) are expected to occur more frequently, how governments should build financial resilience to external shocks is an important question for both researchers and policy makers.

In this article, we empirically estimate the dynamic fiscal impacts of natural disasters in a single developing country—China—by using a panel of thirty Chinese provinces from 1994 through 2014. We find that natural disasters increase a province’s total governmental spending and receipt of transfers from the central government while having no significant effect on total tax revenues. We also undertake a few extensions to investigate the heterogeneity in the fiscal impacts of natural disasters depending on hazard type and a province’s income level. Our results indicate that among all, earthquake and tropical storm events have particularly pronounced effects on subnational government finance. Moreover, wealthier provinces tend to spend more in the aftermath of a major disaster and also receive more transfers from the central government as compared to their lower-income counterparts. More severe natural disasters can also cause a negative shock to the tax revenues in poorer provinces. These results may raise equity concerns over the redistribution of social resources post disasters. Considering that low-income communities are often more vulnerable to external shocks due to their lack of financial resources and coping capacity, natural disasters may further worsen the wealth inequality in China.

Our research contributes to the empirical literature on natural disasters and public finance in several ways. First, by using objective meteorological and geophysical data, we can exploit the exogenous variation in disaster intensities and obtain more accurate estimates of the disaster impacts on fiscal behaviors. This approach can be useful in estimating other economic effects of natural disasters in China. Second, our article presents the first study that quantifies the fiscal costs of natural disasters across Chinese provinces and provides insights into the financial exposure to disaster risks in the developing context. It is noteworthy that our main finding on the countercyclical spending pattern is consistent with the result in the US-based studies (Miao, Hou, and Abrigo 2018) but different from the finding in Noy and Nualsri (2011) that suggest a procyclical fiscal response in developing countries. The difference in findings might be associated with different units of analysis.

Moreover, our results suggest that the central Chinese government uses intergovernmental transfers to support local disaster management and emergency responses and recovery. This finding reflects the role of the national government in pooling disaster risks across the country and also sheds light on the postdisaster welfare redistribution, that is, the intergovernmental transfer payments can alleviate the disaster impact on those directly affected regions and shift part of the disaster costs to all taxpayers within the country (Wildasin 2008). It may further raise the question of whether the subnational governments should depend solely on the assistance of the central government when a natural disaster arises (Zhang et al. 2015).

In terms of policy implications, our empirical estimates should be valuable for the Chinese governments to project future disaster costs and budget adequately for their disaster reserves. In particular, some scholars have noted that the current budget reserve for contingency funding is too low for large-scale disasters (Zhang et al. 2015). For example, the 2008 Wenchuan earthquake incurred more than 55 billion Chinese yuan (8.1 billion US dollars) in direct emergency response cost, while the total amount of central reserve in that year was 35 billion Chinese yuan (5.1 billion US dollars). In this sense, our findings could be useful in linking local budget reserves with their long-term disaster risks.

Finally, it is important to acknowledge the limitations of our study. First, this research does not account for other types of financial flows triggered by natural disasters, such as international aid or charitable donations, which could present another channel of transfers in the postdisaster dynamics. These other transfers could be a worthy aim for future research if more efforts are made to collect comprehensive data on disaster relief and transfers accruing to provinces and localities. Also, it would be ideal to collect monthly or quarterly fiscal data to study the immediate or interannual fiscal responses. Second, we should also acknowledge that a natural disaster that occurs in one jurisdiction may cause spatial spillovers to other jurisdictions, for example, through migration, and therefore influence the fiscal behaviors in its nearby regions. In our current analysis, we do not explicitly account for the possible spatial correlation of fiscal outcomes (Baicker 2005). Therefore, our estimates of the disaster effects might be biased downward in the presence of positive spatial spillovers across provinces. In this regard, more research should be performed to understand the postdisaster dynamics in migration and locational choices in China and their implications for economic outcomes and public finance. Finally, additional analyses could be done focusing on the lower levels of government (e.g., municipality or county levels) to better understand the redistribution of fiscal resources after disasters.

Supplemental Material

Supplemental Material, Online_Appendix_0630_(3) - Natural Disasters and Financial Implications for Subnational Governments: Evidence from China

Supplemental Material, Online_Appendix_0630_(3) for Natural Disasters and Financial Implications for Subnational Governments: Evidence from China by Qing Miao, Can Chen, Yi Lu and Michael Abrigo in Public Finance Review

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.