Abstract

The current study aims at investigating the relationship between private and government consumption within CFA franc zone. In fact, since the decade 2000, most of these countries have launched ambitious spending programs in order to become emergent in the 2035 horizon. For this aim, we applied the cointegration approach of Ogaki (1992) and Ogaki and Park (1997) using panel data and country level analyses for the period 1985–2019. Results from the two methodologies indicate that private consumption and public expenditure are better described as Edgeworth-Pareto substitutes. Conventionally, this means that an increase in government spending decreases the marginal utility of private consumption. Consequently, fiscal stimuli in CFA franc countries are harmful since they crowd out the private consumption. However, in case these countries have to face a fiscal consolidation, the substitutability pattern between private and public consumption is likely to moderate the contractionary impact of cuts in government consumption.

Introduction

In the wake of the financial crisis of 2008 and the subsequent fiscal responses in a number of countries, the fiscal stimulus, the size of fiscal multipliers, and the impact of discretionary fiscal spending on GDP and on unemployment have once again become central to policy debate. In fact, as a response to the Great Depression, many countries, mainly industrialized, launched fiscal stimuli such as the American Recovery and Reinvestment Act (ARRA) in the United States or the European Economic Recovery Plan in the European Union. Those fiscal stimulus packages have revived the old debate on when and why government intervention is desirable. Moreover, they have reignited academic interest in government spending multipliers to spawn a new and growing theoretical and empirical literature.

The current paper examines the magnitude of the elasticity of substitution between private and government spending in the Sub-Saharan African countries forming the CFA franc zone. 1 The Franc Zone is made up of 14 Sub-Saharan African countries, the Comoros and France with the CEMAC 2 and the WAEMU 3 being its two main currency unions. Shortly after their creation in 1994, the two main currency unions put in place a multilateral supervision inspired by the Maastricht Treaty, which was intended to clean up the macroeconomic framework of the CFA franc zone (N’Kodia and Saar 2007). Among the criteria (Four) defined in order to avoid budgetary disruptions was the necessary budgetary balance for all member countries as well as the requirement of no more than a 70% public debt/ GDP ratio. (See Avom and Colin 2007 for more details). According to Dawood and François (2018), the poor economic growth prospect in the Sub-Saharan African region for the years 2018 and 2019 and the deepening of the public debt/ GDP ratio is likely to lead to a period of fiscal consolidation in this region. Moreover, some governments in our sample have launched ambitious spending programs to attain even with different horizons the statute of emergent countries. Those spending programs have already caused a surge in public debt in most of these countries, raising concern about the sustainability of the criteria defined above. It, therefore, becomes important in such a context to investigate the effect of public spending on private consumption.

Using annual data spanning from 1985 to 2019, our results both from country-level and panel data analyses show that private and public consumption can globally be considered as Edgeworth-Pareto substitutes in the countries of the CFA franc zone.

The rest of the paper is as follows: Theoretical and Empirical Literature Review begins with a theoretical literature review on the general issue of fiscal multiplier; then provides an empirical literature review on the relationship between private and government consumption. The Econometric model and the data are presented in Econometric Model and Data while the results and their implications are discussed in Empirical Results. Conclusion concludes.

Theoretical and Empirical Literature Review

Despite an intensive professional attention, no real consensus seems to have emerged on the dynamic impacts of government spending on macroeconomic aggregates (Leeper, Traum and Walker 2017). The literature shows that fiscal multipliers, that is the effectiveness of fiscal policy in stimulating the economy; vary depending on several conditions.

Huidrom et al. (2019) for instance argue that the fiscal position- the ratio of government debt to GDP- of a country might be a key element explaining the size of fiscal multipliers. According to these authors, the fiscal position affects the size of fiscal multipliers through two specific channels namely the Ricardian channel and the interest rate channel. Huidrom et al. (2019) explain that when a government with a weak fiscal position implements a fiscal stimulus, households expect tax increases sooner than in an economy with a strong fiscal position. The perceived negative wealth effect, therefore, leads households to cut consumption and save more, thereby weakening the impact of the stimulus on output. Consequently, the net effect of fiscal policy on output may be smaller in an economy with a weaker fiscal position. Moreover, with a weak fiscal position, a fiscal stimulus can increase lenders’ concerns about sovereign credit risk. This, in turn, crowds out private investment and consumption, reducing the size of the fiscal multiplier.

In view of analyzing fiscal policy in the post-2008 great depression, some authors among who Blanchard and Leigh (2014), Christiano, Eichenbaum and Rabelo (2011), Delong et al. (2012) and Eggertsson (2009) developed New Keynesian models. Those models came to the general conclusion that when interest rates are at zero lower bound, fiscal multipliers are significantly larger than in “normal” periods. In fact, with interest rate's zero lower bound preventing the Central Bank from reducing the policy rate as a Taylor Rule would dictate in the recession, fiscal expansion raises inflation expectations. The resulting decrease in real rates stimulates aggregate investment and consumption. However, New Keynesian models have been criticized for the lack of financial sector dynamics, since recessionary conditions are often a by-product of financial sector crises. Therefore, some studies have incorporated the financial accelerator mechanism put forward by Bernanke, Gertler and Gilchrist (1999) in their models. In a dynamic stochastic general equilibrium (DSGE) framework aiming at studying the impact of fiscal expansion on output, Fernandez-Villaverde (2010) and Carillo and Poilly (2010) find that the size of the fiscal multiplier increases significantly in the presence of financial frictions, which work through the balance sheet of a representative firm. In this framework, the Fisher effect (by which the external finance premium is reduced due to the improvement of the balance sheet position of firms) and the debt deflation channel (which is activated by upward inflation expectations) play a crucial role in the efficiency of fiscal policy. Other studies, rather than including a financial accelerator in DSGE models to address firms’ financing decisions, include the analysis of financial institutions’ choices. For example, Makrelov et al. (2019) using a small general equilibrium model which is stock and flow consistent, show that the effect of fiscal policy is highly dependent on having a well-developed financial market and a sound financial sector. According to those authors, fiscal multipliers estimated from such a model in an economy like South Africa, and taking account of interactions through the financial sector, are much larger than those estimated in studies without such model's characteristics.

A particular attention in the literature dealing with the effects of fiscal policy has been given to the existence of the intratemporal substitutability between private and government consumption. Although an extensive literature predicts that increases in government consumption (expenditure) raise output in the short run, Dawood and François (2018) point out that both the short- and long-run impacts are mediated by the response of private consumption to changes in government consumption. According to Djajic (1987), it is crucial, for a thorough understanding of the fiscal policy effects of government spending to know whether the public and private consumption goods are independent, substitutes, or complements. On this issue, the size and direction of the relationship remain a source of debate in both empirical and theoretical literature (Leeper, Traum and Walker 2017).

On the one hand, neoclassical and New Keynesian models imply that the response of consumption to government spending is negative. The difficulty of generating a positive consumption multiplier in these models is in part because government spending is associated with high taxes and negative wealth effect (Hall 2009). To offset this wealth effect, the literature has offered a number of modifications to conventional models, including non-separability between consumption and leisure and deep habit formation in private and public consumption (see for example Christiano, Eichenbaum and Rabelo 2011 or Zubairy 2014).

On the other hand, some authors argue for a positive consumption multiplier based on a positive wealth effect. Assuming for wage or price rigidity and imperfect knowledge of the present value of tax liabilities, it is possible that changes in government spending positively affect private consumption. According to Murphy (2014), a positive consumption multiplier can arise from perceptions of increased permanent income in response to government spending shocks.

Many researchers have tested whether private and government consumption are complements or substitutes. Most of the studies use a partial equilibrium approach based on Euler equations while others use a general equilibrium framework. Globally the results are mixed and inconclusive due to differences in the econometric methodology. In an early work, Karras (1994) using data for 30 countries, indicates that public and private consumption are better described as complementary goods in the sense that an increase in government spending tends to raise the marginal utility of private consumption. This view is supported by Devereux, Head and Lapham (1996) who demonstrate that an increase in government expenditure, because it generates an endogenous rise in aggregate productivity and a subsequent increase in real wage, leads to an increase in private consumption. For the authors, these results imply that private consumption cannot be responsible for any crowding-out effect that government spending might have on aggregate demand. In their study, Armano and Wirjanto (1998) like many other authors, depart from a representative consumer expected lifetime utility function with a preference specification that considers a nested constant-elasticity-of-substitution (CES) utility function. A useful and testable implication arising from this type of specification is that the sign of the partial cross-derivatives is determined by the relative magnitude of the intertemporal and intratemporal elasticities of substitution. In view of examining the relationship between private and public consumption, these authors first apply cointegration methods to an intraperiod first-order condition of the model and estimate the intratemporal elasticity of substitution. They then impose this parameter in a dynamic Euler equation to estimate the intertemporal elasticity of substitution via a generalized method of moments. Their empirical results obtained using U.S. data suggest that both elasticities of substitution are equal which implies that private and public consumption are unrelated in an Edgeworth-Pareto sense. Moreover, the assumption of additive separability in private and public consumption is supported by U.S. data. Nieh and Ho (2006) develop an empirical methodology similar to Amano and Wirjanto (1997), with a preference specification which admits an addilog rather than a (CES) utility function as in Amano and Wirjanto (1998). However, the authors unfortunately use this preference specification in order to test whether private and public goods are Edgeworth complements, substitutes or unrelated, as in Amano and Wirjanto (1998). Their results are supportive of the two goods being complementary in 23 OECD countries. The evidence of complementarity is also supported by Okubo (2003) with Japanese quarterly data, though with a shorter sample than Amano and Wirjanto (1998). Using data for 54 countries, Evans and Karras (1996) provide additional evidence supporting the view that public and private consumption are complements rather than substitutes.

There are studies on the contrary that support the view that public and private consumption are best described as substitute goods rather than complementary. Examples include Aschauer (1985) for the U.S., Ahmed (1986) for UK. Likewise, Auteri and Costantini (2010) apply quite the same model specification as Nieh and Ho (2006) for 15 European countries and demonstrate that public and private consumption are Edgeworth-Pareto substitutes.

Unlike the above papers, there are some authors that rather assess the relationship between private and public consumption in a general equilibrium framework. Bouakez and Ribei (2007) were the first to exploit such a methodology. Applying maximum likelihood estimation on U.S. data, they find that private and government consumption are complementary goods within a small real business cycle (RBC) model. Therefore, government consumption exerts a crowding-in effect on private consumption. Ercolani and Azevedo (2014) on their part estimate a standard RBC model using Bayesian techniques with U.S. data in the period 1969–2008. Contrary to Bouakez and Ribei (2007), estimation of various versions of this model indicates that private and government consumption are substitute goods. Moreover, substitutability makes labor supply to react little to a government consumption shock, all that lowers the estimated output multiplier.

The above literature on the relationship between private and government consumption has predominantly focused on non-African countries, an exception being the recent study by Dawood and François (2018). In this research, the authors estimate the intratemporal elasticity of substitution between private and government consumption in 24 African countries accounting for general fungibility. Their results support the view that the two variables are Edgeworth substitutes in African countries. In such a case, they also show that fungibility that is high enough to undermine the growth impact of investment-earmarked aid will for the same reason substantially soften the growth impact of a decline in aid. If the study of Dawood and François (2018) has the merit of being the first one to be devoted to African countries, it exhibits however an important limit due to the heterogeneity of the countries considered in their sample. Studies employing the cointegration-based strategy of Ogaki (1992) and Ogaki and Park (1997) to estimate the elasticity of substitution between government and private consumption in a sample of countries usually assume for the presence of common features among different countries (see for e.g., Auteri and Costantini 2010; Nieh and Ho 2006). According to Auteri and Costantini (2010), these common features or cross-sectional dependence are likely to exist in the context of a monetary union like the European Union. It is in this light that we chose to assess the relationship between private and government consumption within the CFA Franc zone, a currency area made of 14 sub-Saharan African countries.

Econometric Model and Data

The Empirical Model

As in Amano and Wirjanto (1998) and Dawood and François (2018), the intratemporal elasticity of substitution between private and public consumption is obtained by estimating the following cointegrating regression:

Recall that as equation (1) is a reduced form specification, it does not have any structural interpretation.

4

Substitutability or complementarity between private and government consumption correspond to the estimated values of

Data

In this study, we use annual data from 1985 to 2019 for eight countries belonging to the CFA franc zone. The starting and ending years are governed by data availability. Data are sourced from the World Development Indicators (WDI) of the World Bank (2022). In essence, 1985 is set as our starting period in order to avoid losing one more country (Mali) in the sample of eight that were finally retained for the estimation. Indeed, data on the variable “general government final consumption expenditures” (in 2015 constant dollars), which is crucial for the estimation of our model, are available in Mali only as from 1985. The choice of the ending year for its part is justified by the fact that at the time of study, the most current date in the World Development Indicators database, which has data for all eight countries in our sample, is 2019. Initially, all the 14 CFA franc zone countries were included in the dataset but 6 of them had to be dropped because of data availability. The consumption ratio

Empirical Results

Prior to our results on the relationship between private and public consumption, it is important to perform some useful preliminary tests. We begin with the cross-sectional dependence test which is a necessary step before panel unit root tests.

Cross-sectional Dependence Test

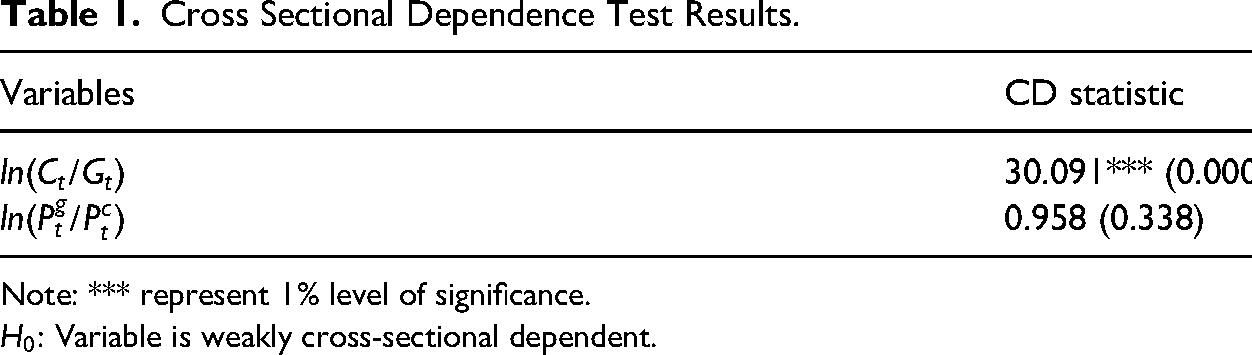

According to Banerjee, Marcellino and Osbat (2000), panel unit root tests which do not take into account the presence of cross-sectional dependence are likely to always reject the null hypothesis of non-stationarity. It is therefore necessary to test for the presence of cross-sectional dependence on our variables before testing for the presence of unit root. The results of weak cross-sectional dependence tests for our two variables are presented in Table 1. This table gives the cross-sectional dependence (CD) statistics and their p-values for each variable. The results indicate that the null hypothesis of the test is accepted for the log price ratio and rejected for the log consumption ratio. These results suggest that all countries of our sample have highly integrated economies in terms of log consumption ratio so that, a shock occurring in one country's consumption ratio is likely to affect the others.

Cross Sectional Dependence Test Results.

Note: *** represent 1% level of significance.

Panel Unit Root Test Allowing for Cross-sectional Dependence

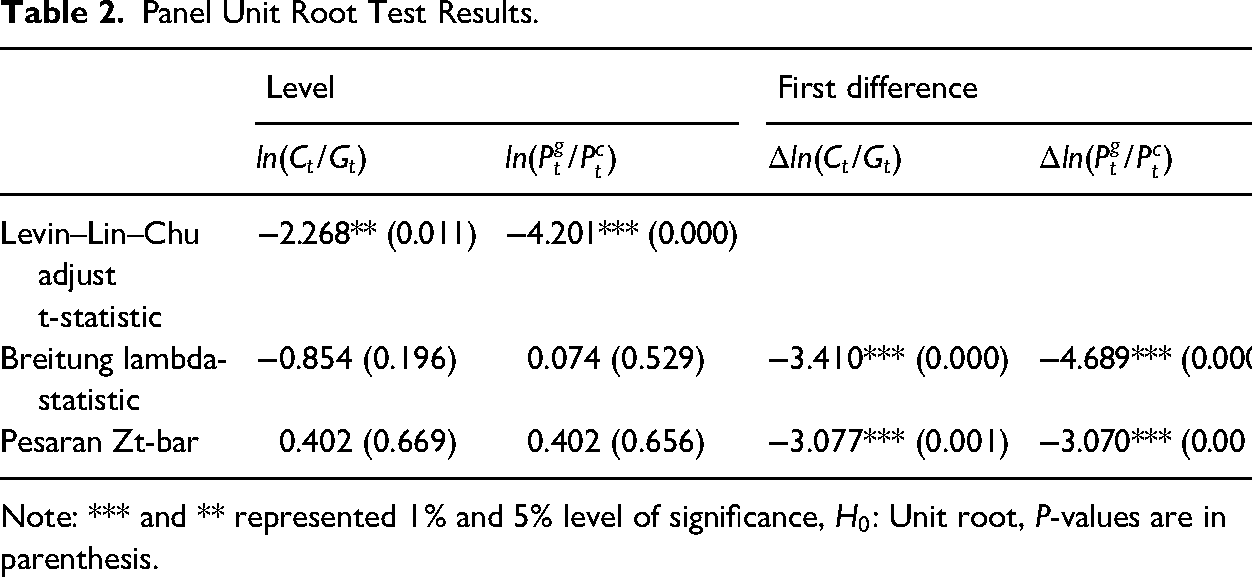

Since the previous sub-section establishes that one of the variables included in our model is not weakly cross-sectional dependent, second generation panel unit root tests suggested by Breitung and Das (2005) and Pesaran (2007), which control for cross-sectional dependence, are performed and compared with Levin, Lin and Chu (2002) first generation panel unit root test results. Since the lag length frequently influences the tests results, we carefully determine the number of lags using Newey and West's (1994) plug-in procedure at

Panel Unit Root Test Results.

Note: *** and ** represented 1% and 5% level of significance,

Panel Cointegration Test Allowing for Cross-sectional Dependence

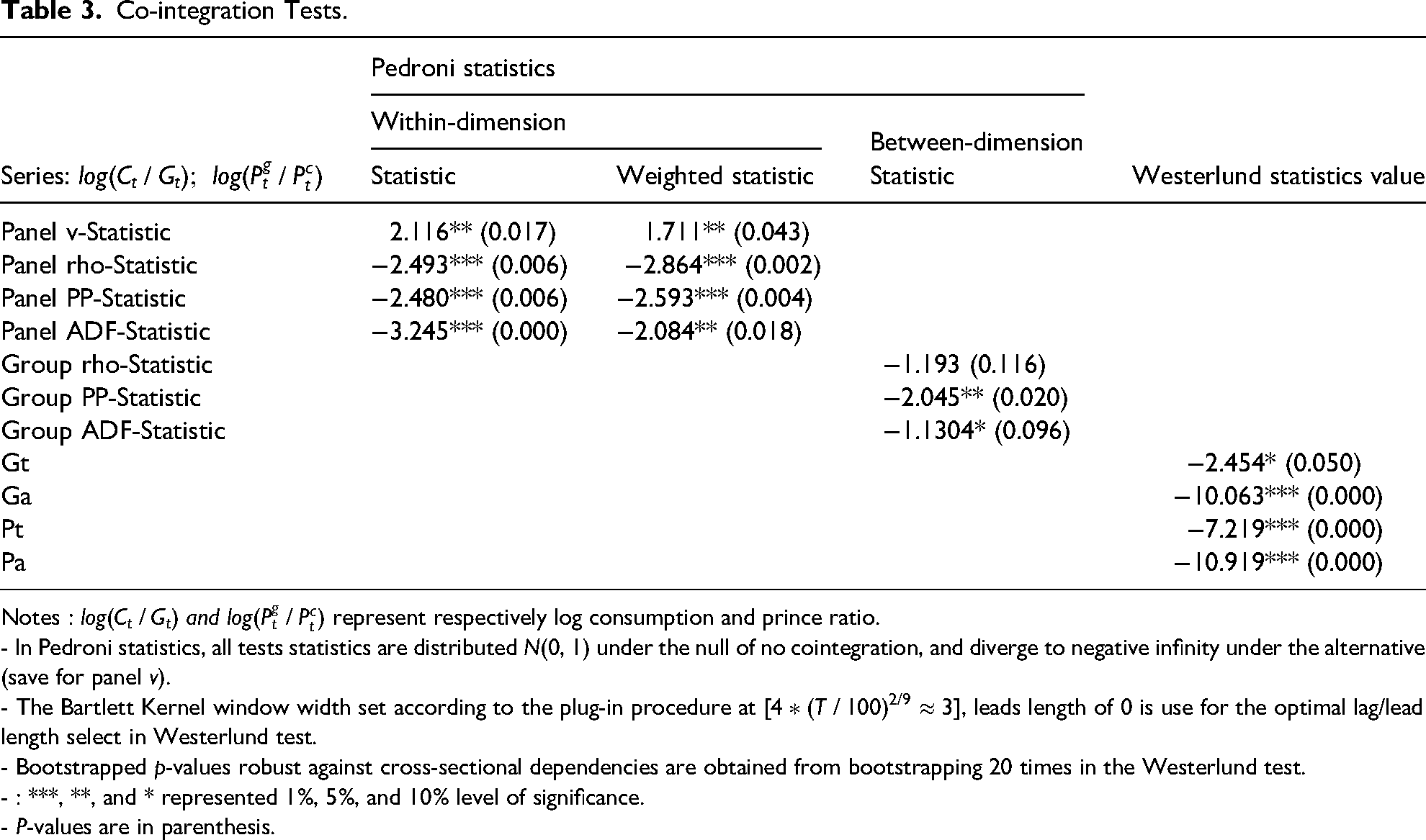

The previous subsections show that there is typically cross-sectional dependence based on Pesaran (2015) test and the variables are non-stationary in levels based on Breitung and Das (2005) and Pesaran (2007) tests. Therefore, the next step is to check for the existence of cointegration among our variables. For this purpose, the results from both the Pedroni (1999) and Westerlund (2007) tests, that is, the first and the second generation panel cointegration tests, respectively, are presented in Table 3.

Co-integration Tests.

Notes :

- In Pedroni statistics, all tests statistics are distributed N(0, 1) under the null of no cointegration, and diverge to negative infinity under the alternative (save for panel v).

- The Bartlett Kernel window width set according to the plug-in procedure at

- Bootstrapped p-values robust against cross-sectional dependencies are obtained from bootstrapping 20 times in the Westerlund test.

- : ***, **, and * represented 1%, 5%, and 10% level of significance.

- P-values are in parenthesis.

The results suggest that ten out of the eleven Pedroni tests (Panel and Group) reject the null hypothesis of no cointegration, indicating that log price ratio has a long run relationship with log consumption ratio. On the other hand, considering the presence of potential cross-sectional dependence across the countries of our sample, it is more robust to apply Westerlund (2007) panel cointegration tests. According to this author, under the presence of cross-sectional dependence, the asymptotic p-values without bootstrapping are inefficient and inconsistent as compared to the robust p-values with bootstrapping. As a matter of fact, this second generation panel cointegration test comes along with an optional bootstrap procedure that allows for multiple repetitions of the cointegration tests which is meaningful since we have indications for cointegration in the panel (Burret, Feld and Köhler 2014). The Westerlund test has the null hypothesis of no cointegration. As it can be seen in Table 3, all the four statistics of the Westerlund tests (Gt, Ga, Pt, and Pa) clearly reject the null of no cointegration. Consequently, the results indicate the presence of a strong cointegration relationship between log consumption and log price ratios in our sample of countries.

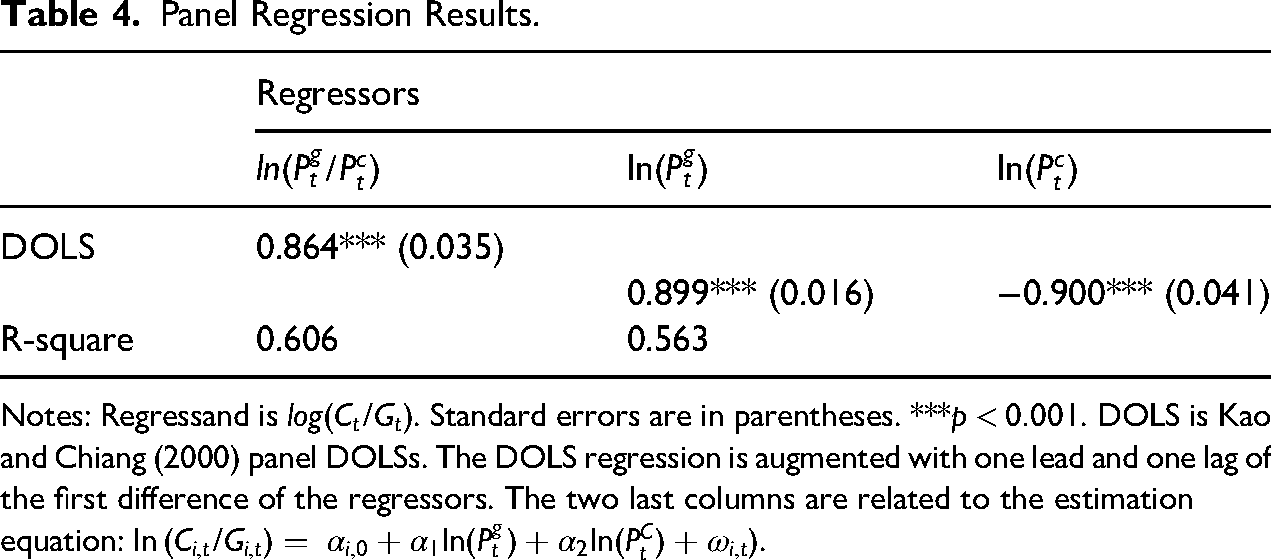

Results of Cointegration Model

Table 4 reports the panel cointegrating regression results of dynamic ordinary least squares (DOLS) estimation method which takes in account country-specific fixed effects. The parameter of interest is the coefficient on log price ratio (

Panel Regression Results.

Notes: Regressand is

For robustness purposes and specification check, we also estimate as suggested by Dawood and François (2018), the following unrestricted version of the baseline equation:

In order to better appreciate the policy implications of our results, it is essential to consider whether the uncovered intratemporal elasticity of substitution implies Edgeworth substitutability or complementarity between private and government consumption. From the expected lifetime utility function defined in equation (1) of their work, Amano and Wirjanto (1998) show that the sign of the cross-partial derivative

According to Ogaki et al. (1996), plausible values of the intertemporal elasticity of substitution for African countries are found to be small and less than 0.5. For these authors, the baseline intertemporal elasticity is 0.34. We also use in our study this value as our baseline intertemporal elasticity of substitution, as was the case by Dawood and François (2018). We combine this value of the intertemporal elasticity of substitution with our pooled DOLS estimate of the intratemporal elasticity to determine the estimated direction of Edgeworth substitutability. The sign of cross-partial derivative implied by the pooled estimate is negative (

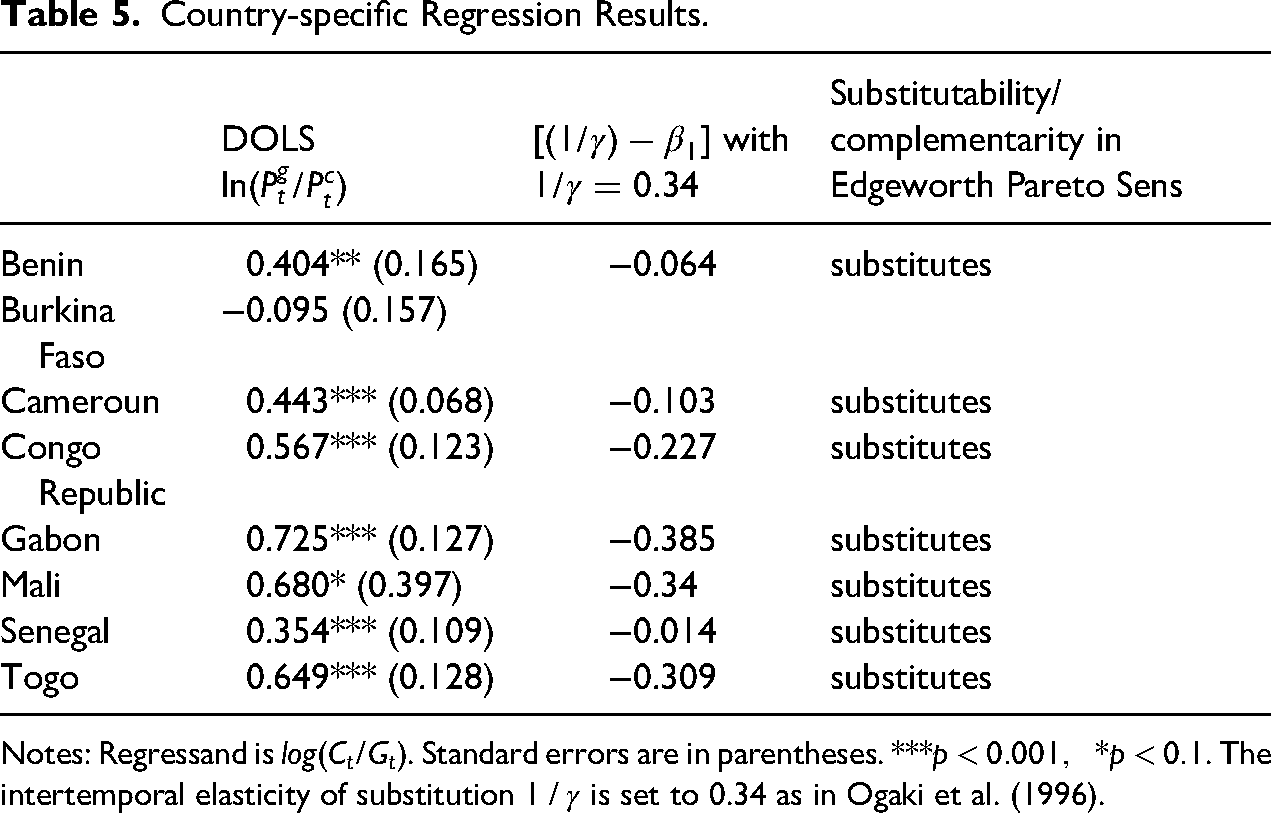

For a policy perspective, the panel estimate may not be of much practical relevance, as it tells us little about any individual country. To address this concern, we estimate the intratemporal elasticity of substitution between private and government consumption for each individual country in the panel. For this purpose, we still employ DOLSs. Recall that this method is an asymptotically efficient procedure used in estimating cointegrating regressions. The results from Table 5 can be grouped into two categories: (1) insignificant estimates of

Country-specific Regression Results.

Notes: Regressand is

The insignificant estimate of

Similar to the panel analysis, we determine whether the country-by-country estimates imply Edgeworth substitutability or complementarity in individual countries. Columns 3 and 4 of Table 5 report respectively the sign of the cross-partial derivatives and the implication in terms of Edgeworth substitutability/complementarity, stemming from the country level estimates of the intratemporal elasticity of substitution. Notice that according to our theoretical condition (a negative value of intratemporal elasticity is implausible), we have calculated the cross-partial derivative only for the countries that have a significant positive estimate of

Conclusion

The main objective of this study was to assess the relationship between public and private consumption in the countries of the CFA franc zone. Since the decade 2000, most of the countries of this currency area have launched ambitious spending programs in view of becoming emergent countries in the 2035 horizon. In order to better understand the effects of government spending programs on the overall economic activity within such a currency area, it is crucial to assess the relationship between public and private consumption. For this aim, we applied the cointegration approach of Ogaki (1992) and Ogaki and Park (1997) using both time series analyses and panel data analyses for the period spanning from 1980 to 2019. The panel data analysis was conducted under the assumption of cross-sectional dependence. Results from the two methodologies indicate that private consumption and public expenditure are better described as Edgeworth–Pareto substitutes. Conventionally, this means that for our countries, an increase in government spending decreases the marginal utility of private consumption meaning that fiscal stimuli in CFA franc countries are harmful since they crowd out the private sector. However, in case our sample countries have to face a fiscal consolidation, the substitutability pattern between private and public consumption is likely to moderate the contractionary impact of cuts in government consumption.

Although this paper is the first to provide systematic evidence of the intratemporal elasticity of substitution between private and public consumption in CFA franc zone countries, there is scope for further research. A possible extension would be to address the sizable fraction of government consumption that is diverted by state agents. In fact, one of the main characteristics that is common to all developing countries is public funds embezzlement. Future research can therefore investigate how public fund embezzlement influence the relationship between private and government consumption in CFA franc zone countries.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.